Embed Size (px)

Citation preview

Sustainability

• “meeting the needs of the present without compromising the ability of future generations to meet their own needs.” – 1987 World Commission on Environment and

Development “Our Common Future”

• Can development be sustainable ?

– many resources we depend upon are finite– the current pattern of world growth follows the

pattern set by the “western world” which involved increased use of resources and increased production of waste

– Development, even theoretically environmentally friendly development, can have devastating effects

– Answer depends large on the “model” you use

Models of Development/Growth

1. Classical Economics

2. Neoclassical Economics

3. “Ecological Economics”

Classical Economics developed in the 1700s – Resources are considered finite – as population grows resources become scarce– scarcity reduces the quality of life & leads to

conflict– competition increases– ultimately population falls

“Boom - Bust Cycle”

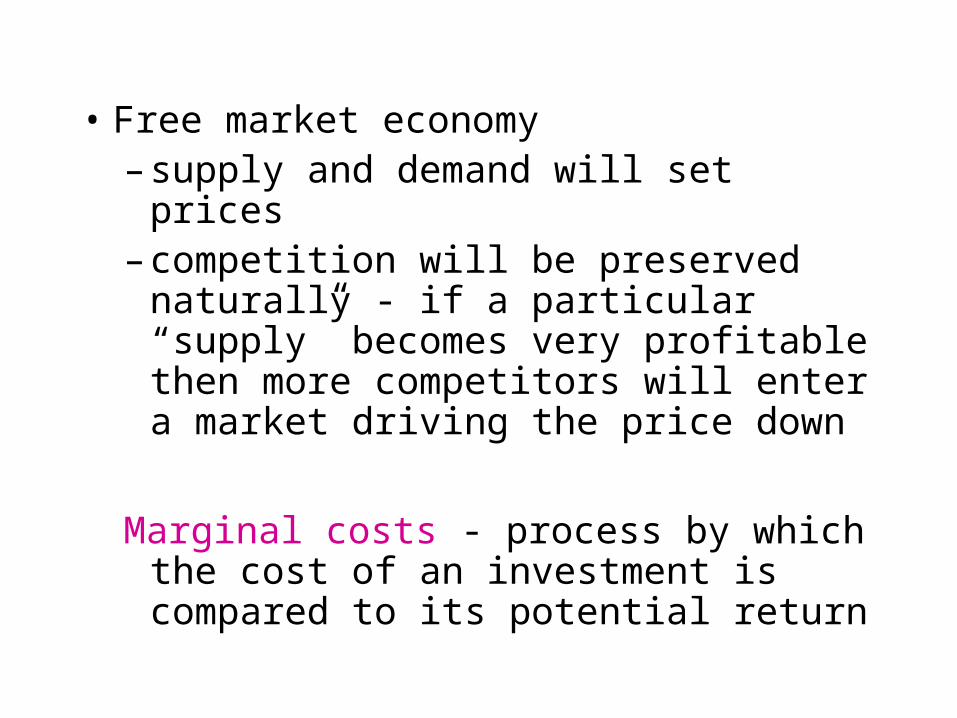

• Free market economy – supply and demand will set prices– competition will be preserved naturally -

if a particular “supply” becomes very profitable then more competitors will enter a market driving the price down

Marginal costs - process by which the cost of an investment is compared to its potential return

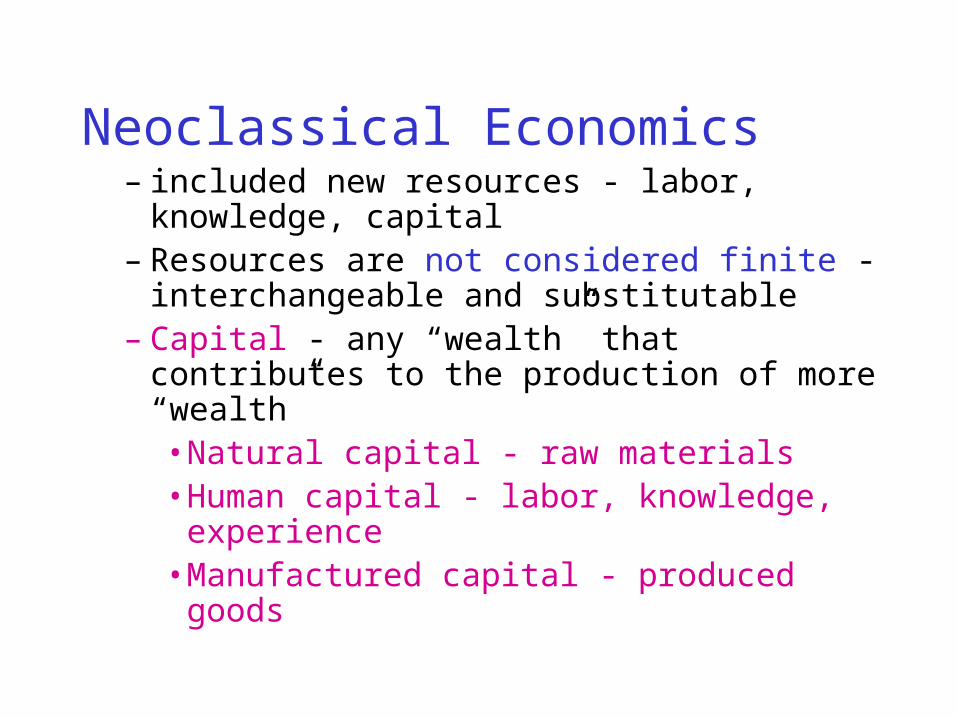

Neoclassical Economics – included new resources - labor, knowledge,

capital – Resources are not considered finite -

interchangeable and substitutable – Capital - any “wealth” that contributes to the

production of more “wealth” • Natural capital - raw materials• Human capital - labor, knowledge,

experience• Manufactured capital - produced goods

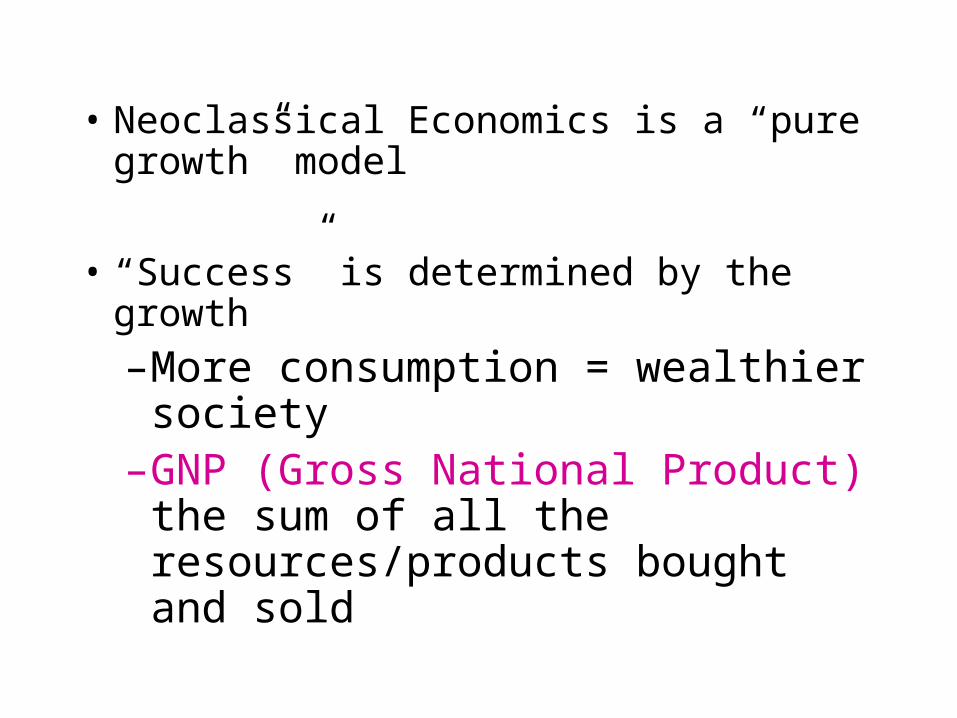

• Neoclassical Economics is a “pure growth” model

• “Success” is determined by the growth

– More consumption = wealthier society

– GNP (Gross National Product) the sum of all the resources/products bought and sold

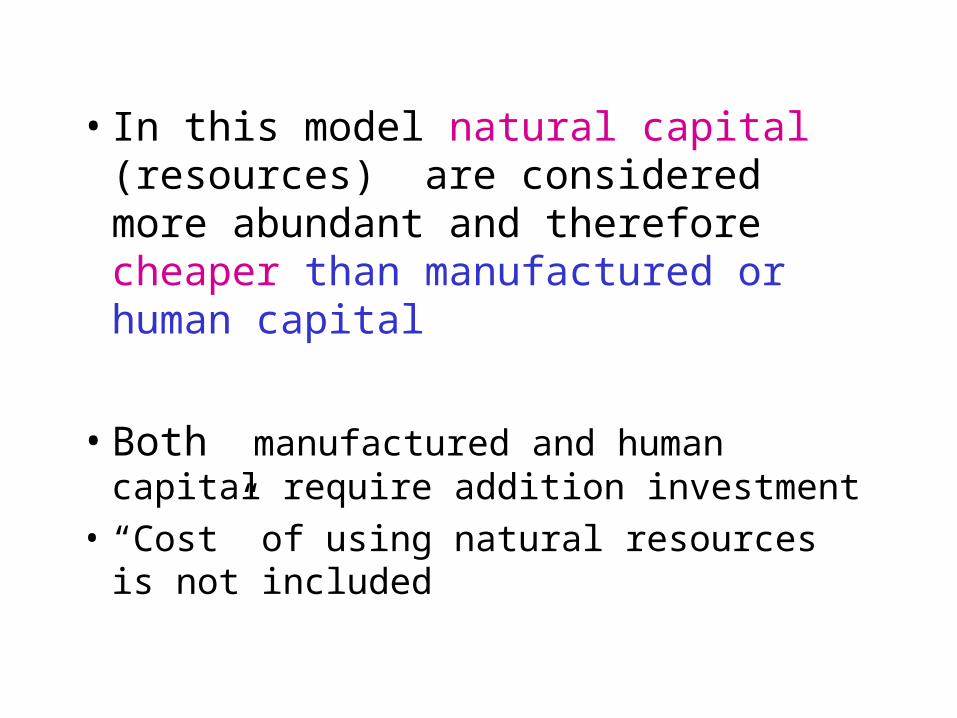

• In this model natural capital (resources) are considered more abundant and therefore cheaper than manufactured or human capital

• Both manufactured and human capital require addition investment

• “Cost” of using natural resources is not included

Ecological Economics– Recent development– proposes an “ecological pattern of use” is

maintains and recycles resources– treats natural environment as part of the

economy • ecological services

– Steady-state economy - equilibrium – Scarcity of resources can provide incentive for

innovation

• Scarcity or Limits to Growth

– if there is a finite supply of nonrenewable resources, at some point they will run out

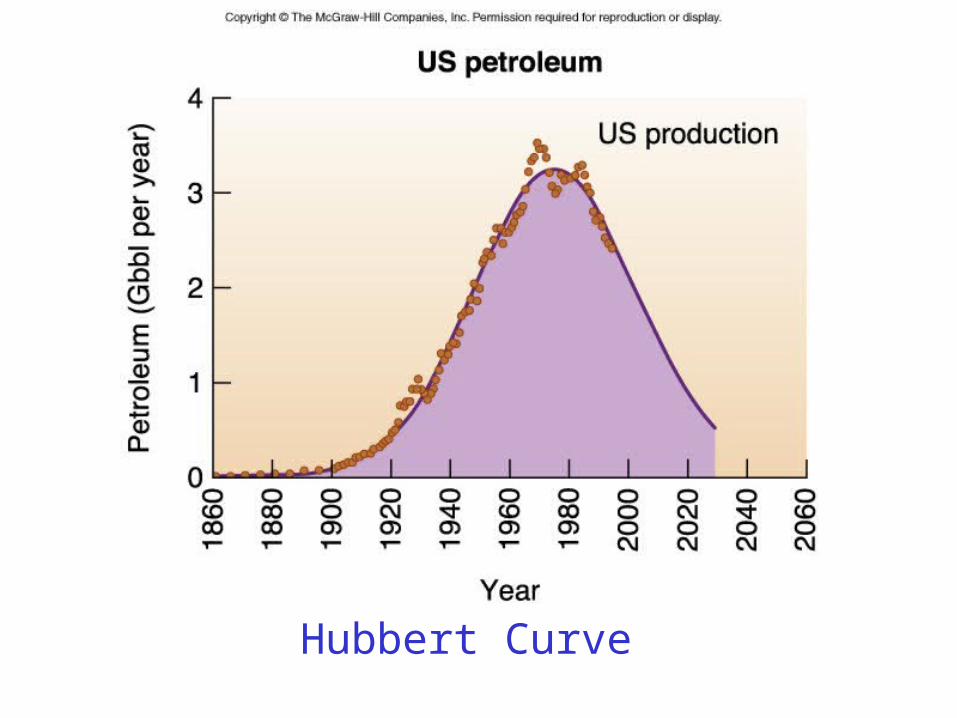

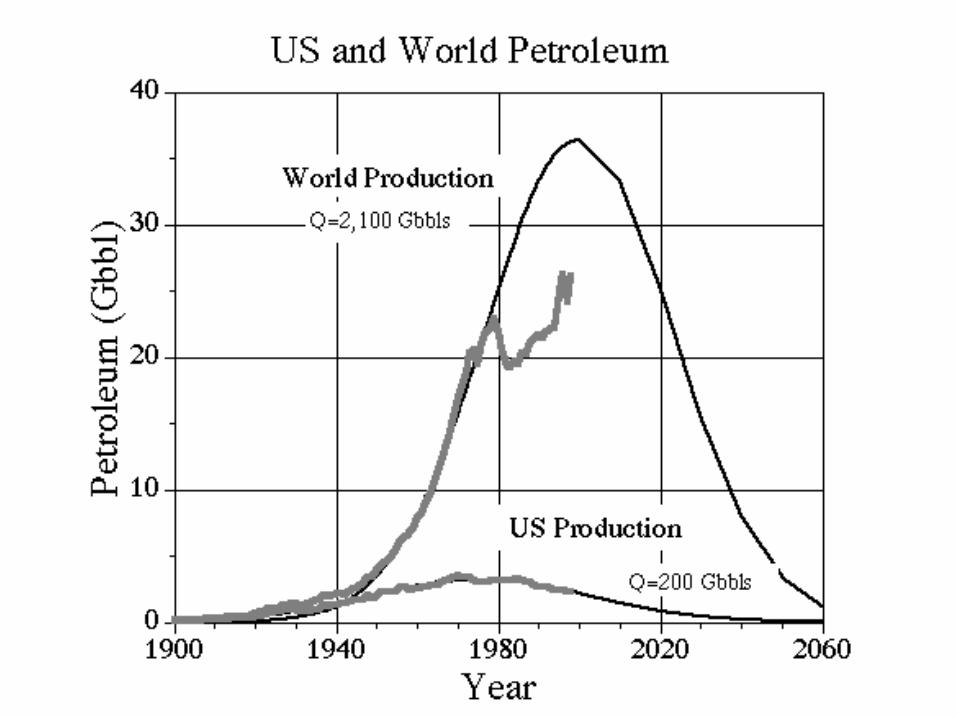

– Basic model for exploitation rate of nonrenewable resources was developed by Hubbert - Hubbert Curves

Hubbert Curve

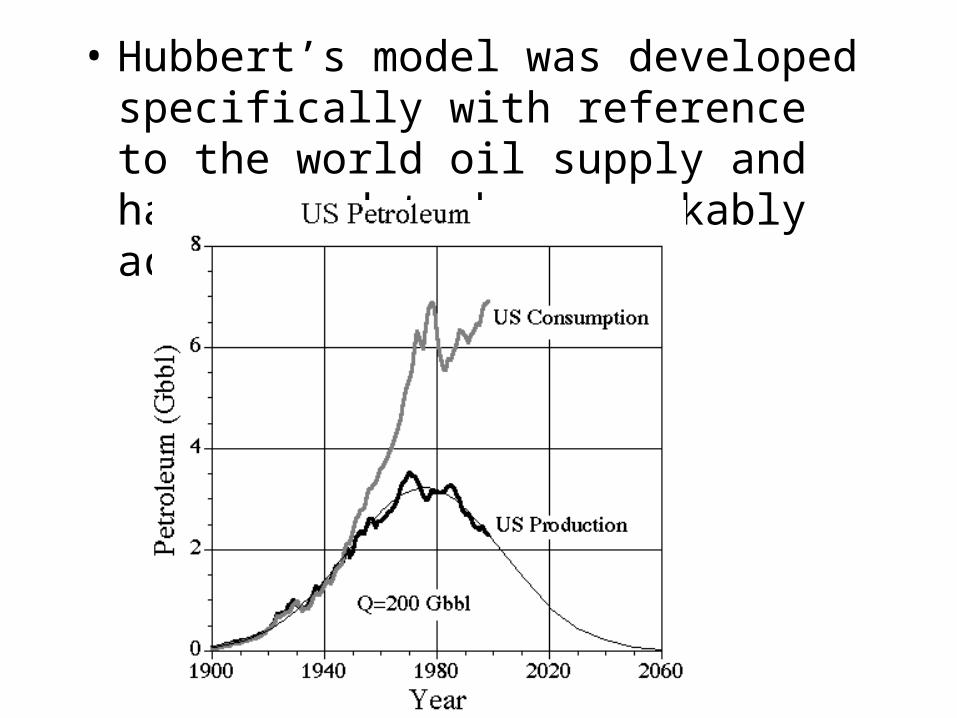

• Hubbert’s model was developed specifically with reference to the world oil supply and has proved to be remarkably accurate.

• Enhanced oil recovery techniques, new seismic methods of finding oil, and new types of drilling and fracturing as examples of ongoing technological changes have not been able to displace this curve very much.

• Due to its success the Hubbert model has been applied to other nonrenewable resources (coal …)

• The current world model of growth is basically a version of the Neoclassical Model

• Developing countries are forced into following this model because the world economic powers follow this model – it is cheaper to follow already established

patterns than to develop new ones – Do as we say, don’t do as we do

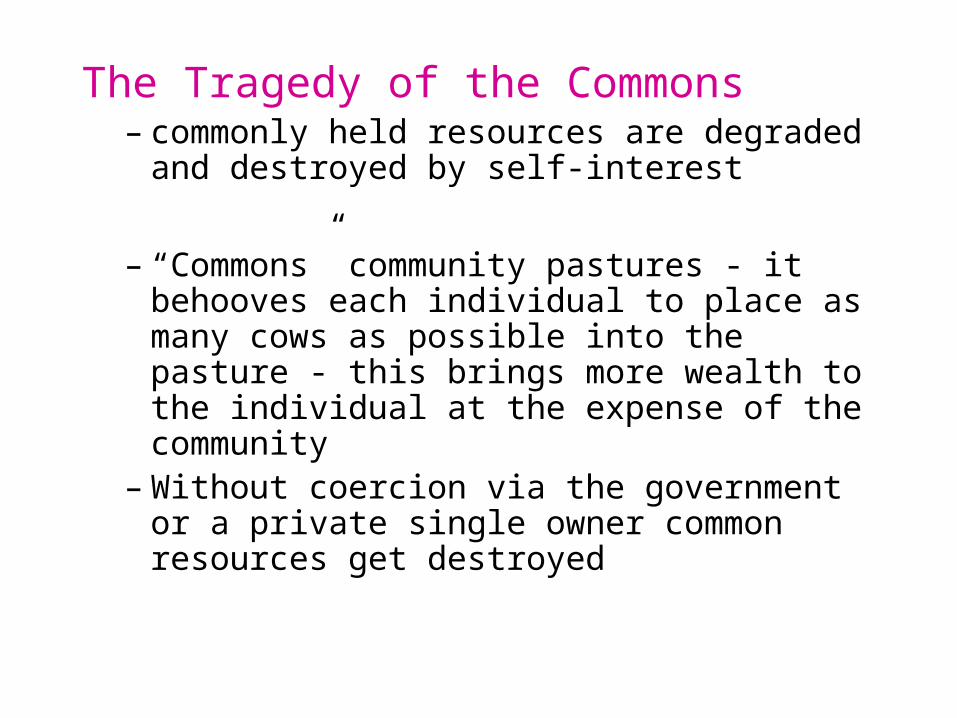

The Tragedy of the Commons– commonly held resources are degraded and

destroyed by self-interest

– “Commons” community pastures - it behooves each individual to place as many cows as possible into the pasture - this brings more wealth to the individual at the expense of the community

– Without coercion via the government or a private single owner common resources get destroyed

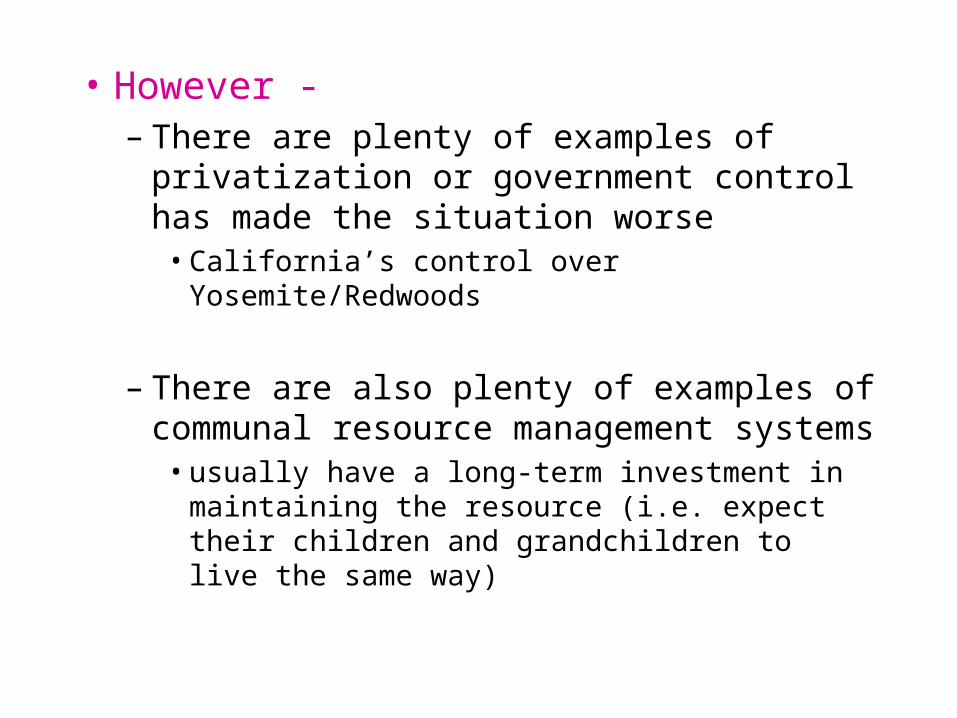

• However - – There are plenty of examples of privatization or

government control has made the situation worse

• California’s control over Yosemite/Redwoods

– There are also plenty of examples of communal resource management systems

• usually have a long-term investment in maintaining the resource (i.e. expect their children and grandchildren to live the same way)

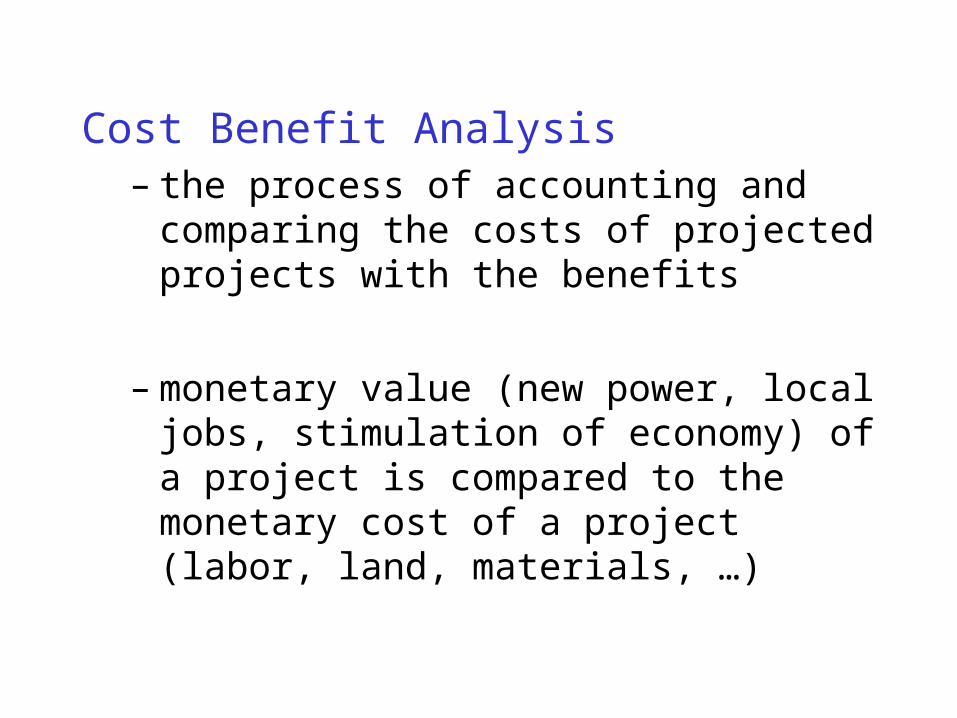

Cost Benefit Analysis – the process of accounting and comparing the

costs of projected projects with the benefits

– monetary value (new power, local jobs, stimulation of economy) of a project is compared to the monetary cost of a project (labor, land, materials, …)

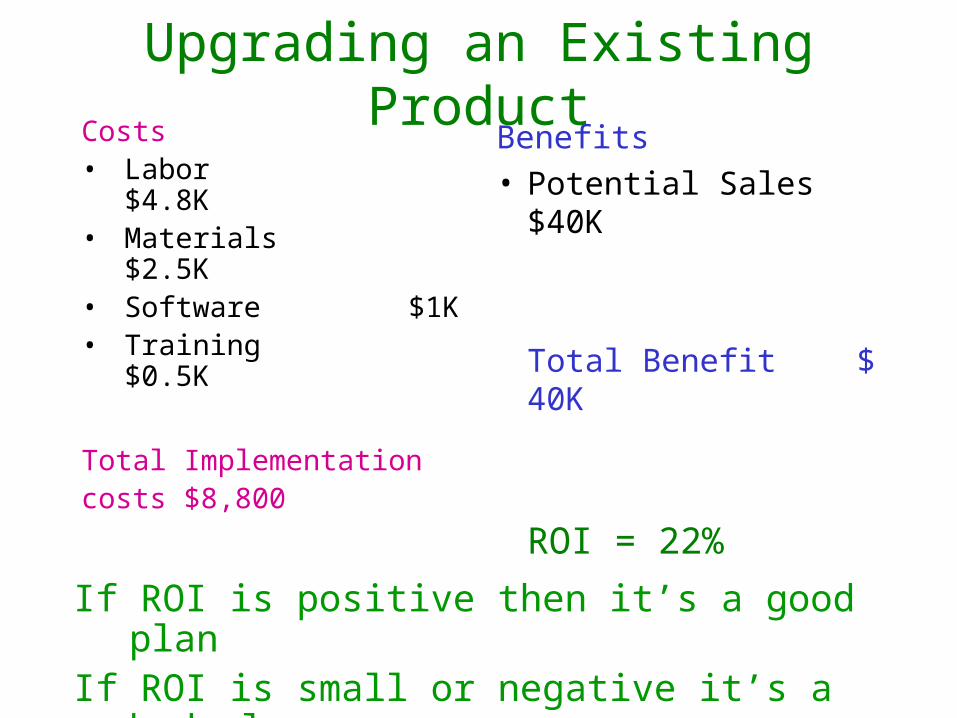

Upgrading an Existing ProductCosts• Labor

$4.8K• Materials $2.5K• Software $1K• Training $0.5K

Total Implementationcosts $8,800

Benefits• Potential Sales $40K

Total Benefit $ 40K

ROI = 22% If ROI is positive then it’s a good plan If ROI is small or negative it’s a bad plan

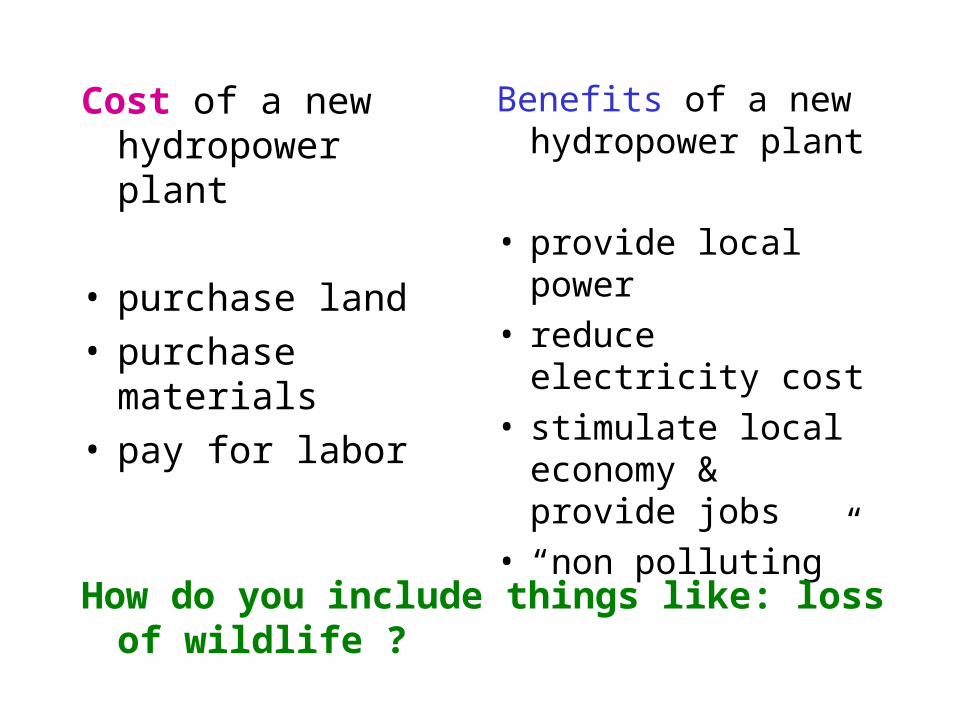

Cost of a new hydropower plant

• purchase land• purchase materials• pay for labor

Benefits of a new hydropower plant

• provide local power• reduce electricity cost• stimulate local

economy & provide jobs

• “non polluting”

How do you include things like: loss of wildlife ?

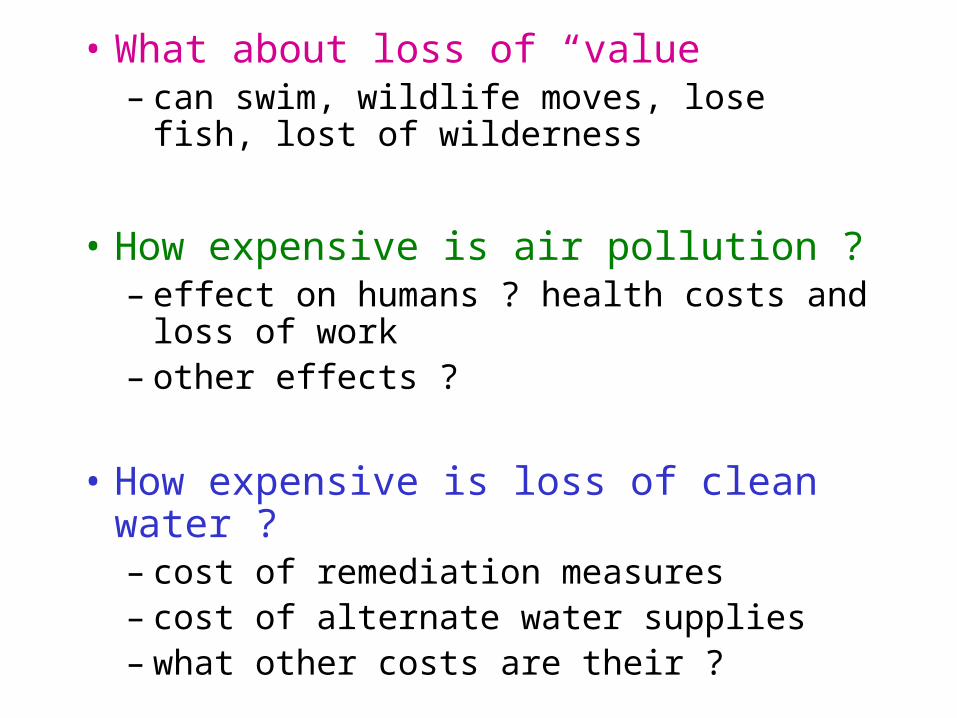

• What about loss of “value” – can swim, wildlife moves, lose fish, lost of

wilderness

• How expensive is air pollution ? – effect on humans ? health costs and loss of

work– other effects ?

• How expensive is loss of clean water ? – cost of remediation measures– cost of alternate water supplies – what other costs are their ?

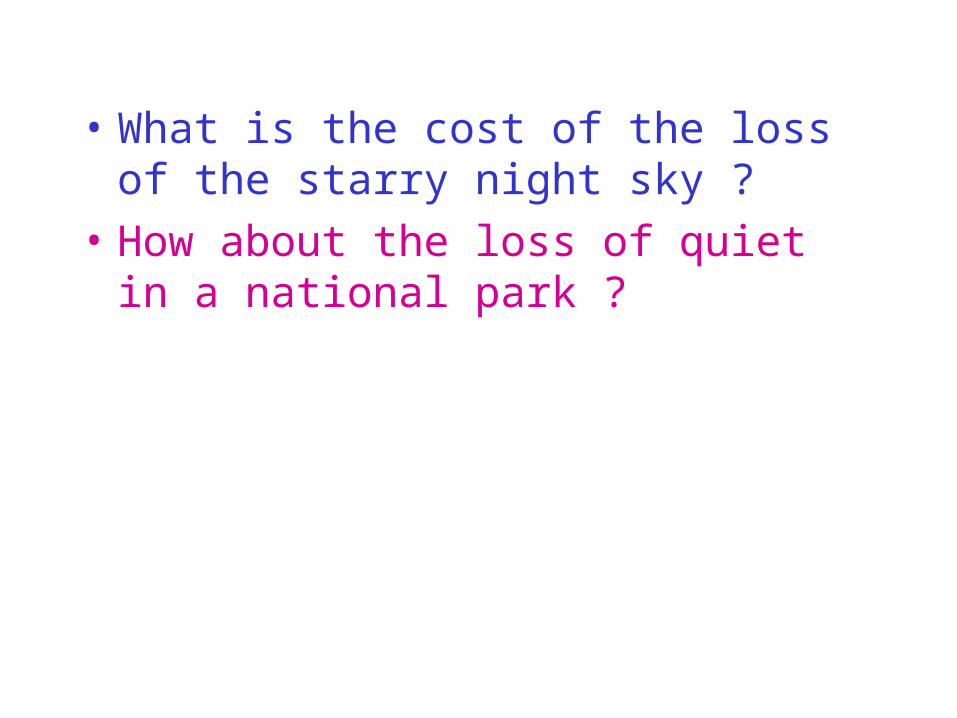

• What is the cost of the loss of the starry night sky ?

• How about the loss of quiet in a national park ?

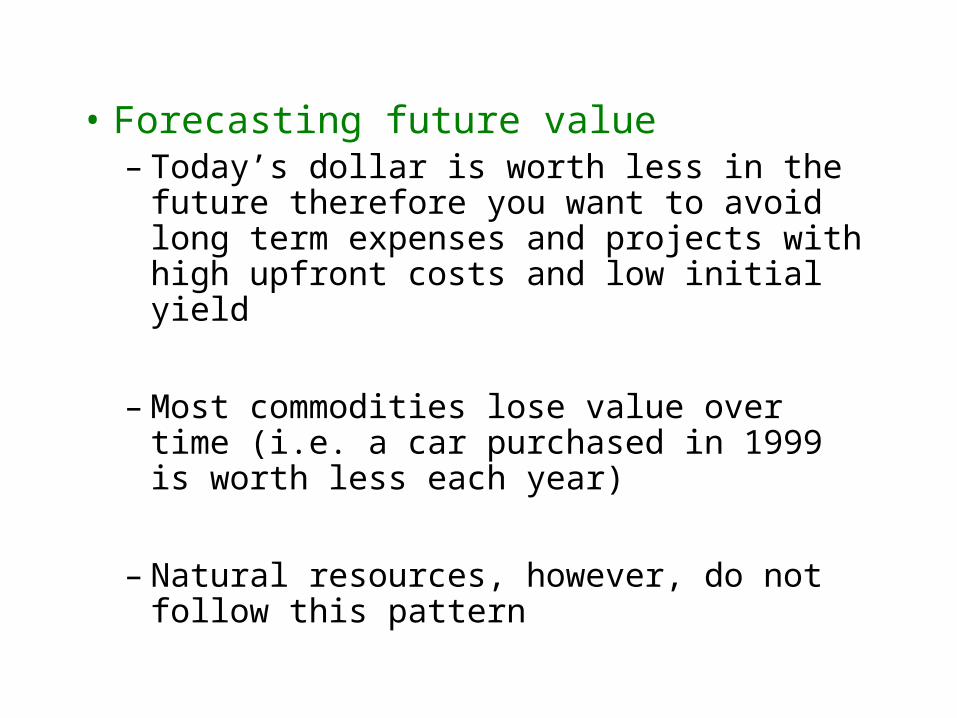

• Forecasting future value – Today’s dollar is worth less in the future

therefore you want to avoid long term expenses and projects with high upfront costs and low initial yield

– Most commodities lose value over time (i.e. a car purchased in 1999 is worth less each year)

– Natural resources, however, do not follow this pattern

![Development of Sustainable Performance …ieomsociety.org/ieom_2016/pdfs/311.pdfpresent generation without compromising the ability of future generations to meet economy needs [1],](https://img.pdfslide.us/doc/110x75/5b0334b47f8b9a3c378be27b/development-of-sustainable-performance-generation-without-compromising-the-ability.jpg)

![Liubov Zharova, D.Sc. in Economics, University of ... · the present without compromising the ability of future generations to meet their own needs [Our common future, 1987]. Concept](https://img.pdfslide.us/doc/110x75/5ec767b76ad72d1a6d1d66f6/liubov-zharova-dsc-in-economics-university-of-the-present-without-compromising.jpg)