Embed Size (px)

Citation preview

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 1/26

What’s News

Maryam Ishaq* and Muhammad Atiq Ur Rehman

Surmounting the Individual: Establishing a Common Currency in Asia – A Case Study of East Asian Economies

Abstract: In the Ministerial meeting of ASEAN held in 1998, the devastation caused

by Asian financial crisis remained the point of contemplation. The participants

enthusiastically discussed the need to establish common currency and exchange

rate system in order to counter any financial crisis anticipated. The ever-growingfinancial crisis threatening every region in the world has compelled the economists

to acknowledge the elevating need of financial cooperation in their respective

territories. This is certainly meant to ensure economic stability at both economic

and political level. The authors, in the course of this paper, have focused the need

to materialize the ideal of promoting monetary integration in the major economies

of South, South East, and North East Asia. Calculating Optimum Currency Area

(OCA) Index, the authors in a way present costs and benefits associated with the

adoption of this currency union. Demand and supply sides of each economy aretested as a pre requisite of OCA in order to provide a good rationale in favor of

selection of regions. For this purpose, Structural VAR Analysis (SVAR) method was

employed and innovation accounting is done through variance decomposition of

forecast errors, impulse response function and correlation matrix. The theory of

OCA has been tested by (i) calculating the OCA index estimated by simple OLS

method and (ii) following Bayoumi and Eichengreen extrapolating the variability

of exchange rate data. The common consensus drawn from the two approaches

adopted implies that there is a good potential in the region excluding China to

construct a currency union particularly amongst South and North East Asianeconomies. It is worth mentioning, however, that some of these will have to

work harder to join and become an effective member of this currency merger.

Keywords: intraregional trade, macroeconomic shocks, variance decomposition,

impulse response function, optimum currency area

*Corresponding author: Maryam Ishaq, Hajvery University, Lahore 54660, Pakistan,

E-mail: [email protected]

Muhammad Atiq Ur Rehman, Punjab University, Lahore 54890, Pakistan,

E-mail: [email protected]

doi 10.1515/gej-2012-0018 Global Economy Journal 2013; 13(1): 63–88

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 2/26

1 Introduction

Asian financial crisis was such a shock for the South Asian countries which

certainly compelled them to adopt a cautious attitude towards both short andlong term exchange rate volatility. At this point, the names of those five coun-

tries are worth mentioning which confronted a sharp devaluation in their

nominal and real exchange rate immediately after this crisis. These names

include Thailand, Malaysia, Indonesia, and Philippines from South East Asia

and Korea from North East Asia. This was an intensely horrifying experience for

all of them since it made these to revise their strategy regarding exchange rate

regime, capital convertibility, directive of financial institutions and macroeco-

nomic policy options.

All these issues are far greater than that of economic integration. In this

connection, one can easily trace out the deep and direct relationship existing

between exchange rate market movements and Regional Trade Agreements

(RTAs). The idea of monetary union strikes one’s mind which can be of good

and help in confronting the macroeconomic problems, reserving the transaction

costs and minimizing the exchange risks associated with RTA member econo-

mies. Besides, if one closely looks at the most obvious rationale of Optimal

Currency Area (OCA), one realizes that abrupt response extended by national

economies towards the foreign ones in terms of macroeconomic shocks thatacted as the strongest explanation for a monetary integration.

Defining monetary union or common currency, it can be taken as a common

legal tender to be used in multiple countries. This legal tender can either be the

currency of any of union member countries or the one which has achieved a

certain level of permanence and acceptance at global level. In a way, the

establishment of monetary union can be taken as the establishment of a pact

among a group of countries according to which all the participants submit to a

single currency and a common Central Bank. The bank must be autonomous

enough to issue currency and frame monetary policy for all the member econo-

mies. Such monetary unions are found rare. European Monetary Union (EMU),

the monetary union between Switzerland and Lichtenstein, CFA Franc Zone and

Eastern Caribbean Currency Union (ECCU) which comprises of two groups: West

African’ Economic and Monetary Union and Central African Economic and

Monetary Union.

At present, a number of economic policy makers from South East Asia have

emphasized the profitability of monetary integration for the region. These

include Kurdo (2004) and Chino (2004) remarkably. Both are of the view that on account of invariably and elevating economic interdependence of

major East Asian economies, intraregional exchange rate stability has become

64 Maryam Ishaq and Muhammad Atiq Ur Rehman

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 3/26

indispensable. This ideal can be materialized only through the adoption of

shared currency only.

2 Key channels of economic integration in

East Asia

The economic linkages between East Asian Economies are growing stronger with

every passing day. Through the market-driven channels of cross border trade,

Foreign Direct Investment (FDI) and finance, we are indebted to multilateral and

unilateral trade liberalization by the virtue of which, there has been a rapid

growth in FDI activities and exchange of goods and services during last 20 years.

Owing to the removal of various cross border trade barriers and geographical

closeness, there occurred spontaneous economic linkages among East Asian

countries.

2.1 Integration through trade and FDI

The expansion of intraregional trade has been remarkable for last three decades.East Asia’s share in intraregional trade grown from 37% in 1980 to reach 54% in

2007.This clearly indicates the reduced dependence of region on United States

and European markets for its final goods. The dependence is expected to

decrease even more in the years to come. The basic motivation for this economic

integration channelized through trade and FDI is those intraregional business

activities of multinational manufacturing companies which initially came from

United States, Japan, and Europe. This initiative promoted such an encouraging

business environment in the region that following these countries many East

Asian countries also came into the field. All over the East Asia, these multi-

national companies developed such closely organized production networks and

supply chains which are linked up with international goods market in a very

broad manner. Here the role of China is worth mentioning who is one of the

leading market recipients of FDI inflows in the region. Today China is playing a

highly effective role in developing regional production networks. Besides, the

country is continuously striving to prove itself as a responsible and reliable

platform for regional and global manufacturers. China is importing capital

equipments, industrial material and intermediate inputs from its neighbor coun-tries and in return exports finished manufactured goods. Hence, China on one

side is establishing complementary linkages with its East Asian trading partners

Establishing a Common Currency in Asia 65

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 4/26

and on the other hand is promoting very healthy competition in the region

through the aggressive exchange of goods and services. Thus, it may be con-

fidently claimed that the exchange rate movement of Yuan against other East

Asian currencies is of growing importance in the context of regional and globaltrade and FDI activities.

2.2 Financial integration and capital mobility

Like goods markets, East Asian financial markets are also getting integrated with

each other at a very fast pace. Basic reasons include deregulation of domestic

financial institutions, opening up of financial services and continuous relaxation

of capital and exchange controls. Besides, establishment of various commercialand investment banks into East Asia by developed countries and portfolio

investments made by institutional investors are some of the other major reasons

for integrating domestic financial markets of the region. Here the role of com-

mercial banks is of vital importance as they are increasingly aggressively

extending their banking services to neighbor countries. As a result, world

witnessed an unusually growing cross-country correlations of regional interest

rates and stock market returns.

From a closed analysis of data, it is evident that during the Asian financialcrisis of 1997–1998 cross-market differentials in the interest rates and bond yield

in the region grew very rapidly but started dropping during 1999. However, the

integration through regional financial systems and capital mobility is less pro-

minent as compared to that by which came through trade and FDI. According to

a report published by IMF on the region, for the entire decade of 2000, the

volumes of cross border equity investment flows grew very speedily in the region

but the volumes of intraregional portfolio investment flows are still quite low

and are approximated around 8% only. On the other hand, the counter parts like

European Union and North American Free Trade Agreement are standing at 62%

and 16%, respectively. For these limited levels of intraregional investments, one

of the probable reasons can be besides Japan, Korea and Hong Kong there are

still some of the East Asian countries who are affectively practicing capital and

exchange controls and other kinds of financial restriction in their economies.

The practice is proving to be one of the biggest obstacles in the way of free

movement of financial capital. Particularly, China from North East Asia and

some of the low-income AEAN economies are still insistent to employ heavy

financial controls and regulations. Besides, relatively weak and instable finan-cial market structures of many of the East Asian countries can also be one of the

core causes which keep the local investors away from thinking on the idea of

66 Maryam Ishaq and Muhammad Atiq Ur Rehman

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 5/26

investing their assets within the region. Rather, they are found more inclined

towards directing their international portfolios towards European and North

American financial markets.

2.3 Labor market integration

In East Asia, labor market linkages are relatively less evident, even lesser that

through trade, FDI, and financial markets. Here the names of Japan and Korea

from North East Asia are noteworthy who are imposing tight restrictions on labor

market integration as compared to rest of the countries of this region. However,

in South East Asia labor mobility is considerably liberal specifically in Malaysia,

Thailand and Singapore. Bayoumi and Eichengreen (1988) and Hamad and Gota(2000) found that during the 1980s and 1990s, the intraregional labor mobility in

South East Asia was much free than that in Europe. Such a moderate policy may

indicate towards the unusually pleasant and unique nature of macroeconomic

environment of the region that is high capability of making good adjustments

towards and economic shock. As a result, it can be anticipated that possibly the

region would not have to pay much huge cost for its initiative towards perma-

nently fixing the exchange rate and foregoing monetary policy autonomy by

each country.

3 Review of the literature

In 1961, Robert Mundell was the first one to present the theory of OCA. In actual,

it was his attempt to examine how the economies engaged in cross border trade

may be benefited from the establishment of a monetary union amongst them.

Nevertheless, the establishment of a single currency area is the other name of

exterminating the option of combating asymmetric shocks with the help of

exchange rate and monetary policies. The countries will, however, remain in a

position to take help from structural policies, so that they may cope their short

term and long term macroeconomic disturbances.

On presenting all the things in a very ideal setting, Mundell claimed that the

economies joining a monetary union will be benefited by two types of compe-

titive efficiencies: (a) labor mobility (b) wage flexibility. These efficiencies pro-

vide participant countries with an opportunity to re-equilibrate about

automatically to counterbalance the effects of asymmetric shocks.For instance, the growth in exports of Country A will boost up its aggregate

demand but at the cost of exports of Country B. This will make the aggregate

Establishing a Common Currency in Asia 67

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 6/26

demand curves of both the countries to shift in the opposite directions. However,

equilibrium can be restored if the labor of depressed economy brings down their

wage rates. This will make the aggregate supply curve to shift downwards;

hence, equilibrium employment level of the economy will be reinstated onceagain. Besides, the resultant fall in price levels will make the exports of Country

B more competitive in comparison to Country A, thus, pushing the aggregate

demand curve of Country A to shift downwards. In this way, the actual equili-

brium position will be restored. Besides, due to perfect labor mobility, the

unemployed man-power of Country B would get an opportunity to find employ-

ment in Country A. This will once again help both the countries to re-equilibrate

their current accounts. The current account surplus which was created in boom-

ing country as its citizen were more in a position to save, will be counter-

balanced by the inflow of migrants from Country B. On the contrary, for the

country with relatively smaller export base, the reduction in spending levels will

be not as much as fall in exports. Reason is, due to social security benefits

extended to unemployed will help to maintain almost similar levels of consump-

tion as before, thus, making the country to face current account deficits in

long run.

As it is quite obvious that the above stated conditions may be imagined for

developing countries but for developed economies these are least probable.

Hence, it may be concluded that the establishment of a monetary union willnot be of much worth for the region where member states are faced with

asymmetric macroeconomic shocks.

In contrast, European Commission is of the view that single currency area

may serve as a high way to contest the future macroeconomic shocks. On

constitution of a common currency and monetary union, with lowered trade

barriers and sequential stepping towards a single market would indeed take the

members countries to increased convergence in terms of economic activity, thus,

paving the path for combating anticipated future shocks.

Researching the same arguments, Kenen (1969) proposed that the lessened

significance of national borders in a free trade area has an obvious implication

that symmetric shocks must be felt in same industry of each member country. As

they would be selling their product in a single market, so it distinctively a

common issue which has always been presented in the form of multiple con-

cerns. So this must be deal with an only toll, that is, formation of a monetary

union.

By presenting an opposing view, Krugman (1993) said that monetary union

can hardly work for eliminating the asymmetric nature of systematic shocks. Thebasic reason behind this is the consolidation of various industries which will

emerge as a consequence of faster economic linkages between member

68 Maryam Ishaq and Muhammad Atiq Ur Rehman

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 7/26

countries. In order to get benefited from economies of scale, countries will opt

for the practice of geographically concentrated sectors. This means that country

hitting up of a demand shocks to a specific sector of some specific country; this

would indeed be an absolutely disproportionate attitude towards that country where she will be the only sufferer amongst all the union member states.

3.1 Are macroeconomic disturbances symmetrical in East Asia

In the context of evaluation of OCA, the work done by Bayoumi and Eichengreen

(1992, 1994) is commendable. By using aggregate demand aggregate supply

(AD-AS) model they developed Structural VAR (SVAR) model for the sake of

identification of demand and supply shocks. Following Blanchard and Quah

(1989) they regarded supply shocks of greater importance as compared to

demand shocks. In their view, the supply side of the economy is less affected

by the stabilization policies. Secondly, supply side is more likely to be invariant

with respect to various international monetary regimes. Hence, in order to

inspect the economic organization of any region, supply shocks are more con-

sistent measure as compared to demand shocks. Keeping this in view, Bayoumi

and Eichengreen found that if the region is experiencing systematic supply shocks, then the region would be a plausible nominee for OCA.

Zhang et al. (2004) empirically attempted to evaluate the aptness of East

Asian economies for a probable monetary integration using various macroeco-

nomic data. Using a model consisting of demand shocks (represented by domes-

tic output), monetary shocks (represented by real effective exchange rate) and

supply shocks (represented by domestic price levels), Structural VAR (SVAR)

model was applied in order to make out the underlying shocks in each economy.

The authors came up with quite a strange finding that as a whole East Asian

region is not a good nominee for monetary integration. Although some small sub

regions may be potential candidates for sharing a single currency as their

macroeconomic disturbances, they are somewhat correlated with mild severity.

Due to these reasons, these groups of countries are displaying a good tendency

to adjust rapidly to macroeconomic shocks, showing their hidden propensity to

establish a single currency.

On criticizing Bayoumi and Eichengreen, Chow and Kim (2003) commented

that the most difficult thing proposed in their model is the non-specification of

the nature of supply shocks; whether they global, regional or domestic. As dueto the hasty adoption of export-oriented growth policies by East Asian countries,

the intraregional trade in the region has progressed promptly. So the

Establishing a Common Currency in Asia 69

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 8/26

fluctuations occurring in the domestic output in the region may be transmitted

through the business cycles taking place in the economies of trading partners.

So, Chow and Kim applied three-variable model in their study. By employing the

series of global, regional, and domestic outputs, the authors tried to highlightthe possible channel from which the economy is being shaken. The study

presented that the East Asian economies are strongly stroked by country specific

shocks during the period 1970–1999. However, here, the point raised by Frankle

and Rose (1998) is noteworthy that as the intraregional trade gets deeper, it is

more likely that the countries will suffer from the shocks of similar nature. So,

most probably, the countries of the region would be hit by common systematic

shocks, as with the every passing day from 1980s, the intraregional trade and

economic linkages are growing amongst member states.

Kawai and Motonishi (2004) observed East Asian macroeconomic variables,

so they may assess the degree of macroeconomic interdependence in the region.

They checked for the cross-country correlation against the various financial and

price variables for various economies. Employing a sample period of 1980–2002

they experimented on ASEAN+3. Besides, they included Australia, India, New

Zealand, United States, and European Union in their study. Their results suggest

that in comparison to other region the cross-country correlation among macro-

economic variables is considerably significant excluding China and low income

ASEAN states. Afterwards, the authors tested the magnitude of convergence of macroeconomic variables for East Asian vis-à-vis non East Asian economies with

the help of Principal Component Analysis. Both the cross-country correlations

and convergence results proved that there exist strong real and financial macro-

economic linkages amongst East Asian economies except some of the countries

mentioned above. In the last, the study attempted to highlight those underlying

shocks which are significant in impacting macroeconomic environment of the

region. Employing Structural VAR (SVAR) model the results positively speak in

favor of existence of strong correlation amongst supply shocks which explain

the profound factual macroeconomic interdependence present between East

Asian states.

Achsani and Partiswi (2010) tested for the feasibility of establishing a single

currency area in ASEAN+3. Working on some selected economies of North and

South East Asia, the authors tried to judge the viability of a currency union in

the region. The analysis was carried by employing two different techniques;

exchange rate variability based on OCA index and hierarchical clustering ana-

lysis. Using quarterly data from 1997 to 2003, authors tried to find some good

evidence in the favor of this notion that the currency with lowest value of OCAindex, most stable its currency would be. Results suggested that Singapore

dollar is the most secure currency in the entire region. Both the above mentioned

70 Maryam Ishaq and Muhammad Atiq Ur Rehman

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 9/26

techniques suggest that by starting with Singapore and Malaysia, the region is

quite a suitable candidate for currency union, excluding Indonesia whose cur-

rency characteristics are quite far removed from those of other currencies of the

region.Taguchi (2010) examined the economic achievability of developing a regio-

nal currency block in Asia. By employing Generalized Purchasing Power Parity

(GPPP) approach, author tried to map out those common macroeconomic trends

which were experienced by each specific group of countries. Taking up a sample

of 17 Asian economies the author came up with a conclusion that China, Japan

and Korea are least capable of making an currency block in the region. As on

employing bi-lateral Co-integration the fact was revealed that countries are

sharing a negligible Co-integration amongst their macroeconomic variables.

Nevertheless, the author found good evidence for the presence of multilateral

Co-integration among the member state of SAARC and high income ASEAN

countries. Finally, the author recommended that the direct and comprehensive

formation of currency union in Asia appears to be untimely and impulsive in the

sense of deficiency of likeness amongst the primary macroeconomic variables of

member countries. This inference supports the implication of smaller local sub

groups along with multi speed policy towards a long-term goal of regional

currency block in Asia.

4 Macroeconomic and structural convergence:

exploring underlying shocks

The theoretical framework for optimum currency area (OCA) advocates that there

are three different criterions to gauge the suitability of a country to be a

candidate for optimum currency area. These factors include the patterns of

trade, the size and correlations of macroeconomic shocks, and the similarity of

economic development and financial systems, in the countries under considera-

tion (Bayoumi and Mauro 2001).

Precisely, macroeconomic and structural convergence has never been

amongst the criterion of OCA. It is certainly not inevitable for the establishment

of a single currency area. But once a common currency union is established it

becomes obligatory for member countries to guarantee macro economic conver-

gence and symmetric patterns of macroeconomic variables. The basic need

behind the fulfillment of this condition is that without achieving this propor-tionality, countries with differential inflation rates and fiscal deficits, it would be

very hard for them to agree upon a mutual non-inflationary monetary policy.

Establishing a Common Currency in Asia 71

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 10/26

For the purpose of preliminary evaluation, the demand and supply shocks

are taken into account. Following Bayoumi and Eichengreen (1998) and

Gyeongsang et al. (2006), demand shocks are represented by real GDP growth

rates and the supply shocks are given through the growth rates of GDP deflatorreflecting the general price level of the economy, respectively. For the purpose of

study the Nine East Asian economies are taken into consideration. These include

Singapore, Thailand, Malaysia, Indonesia, and Philippines for South East Asia

and China, Japan, Korea, and Taiwan from North East Asia. The study period

employed here is from 1992 to 2010. According to Johan Taylor, the demand

shocks lead to the expansion and contraction of the economic activity or output.

The countries with similar demand shocks can be good candidates for the

common currency area. A group of countries facing symmetric economic shocks

will be better candidates for a common currency area.

4.1 Measures of innovation accounting

4.1.1 Variance decomposition of forecast errors

In order to account for the short run innovation accounting and for supplemen-

tary conclusions, variance decomposition test (VDC) and impulse responsefunction (IRF) are the most suggested tools.VDC and IRF serve the purpose of

assessing the dynamic connections and magnitude of causal relations among

system variables. The forecast errors of VDC will reveal the percentage of

demand and supply series forecast error variance credited to their own shocks

versus the shocks from other competitor states. Thus, VDC is a short run tool to

calculate the comparative significance of global cyclical conditions in explaining

fluctuations in domestic macroeconomic variables.

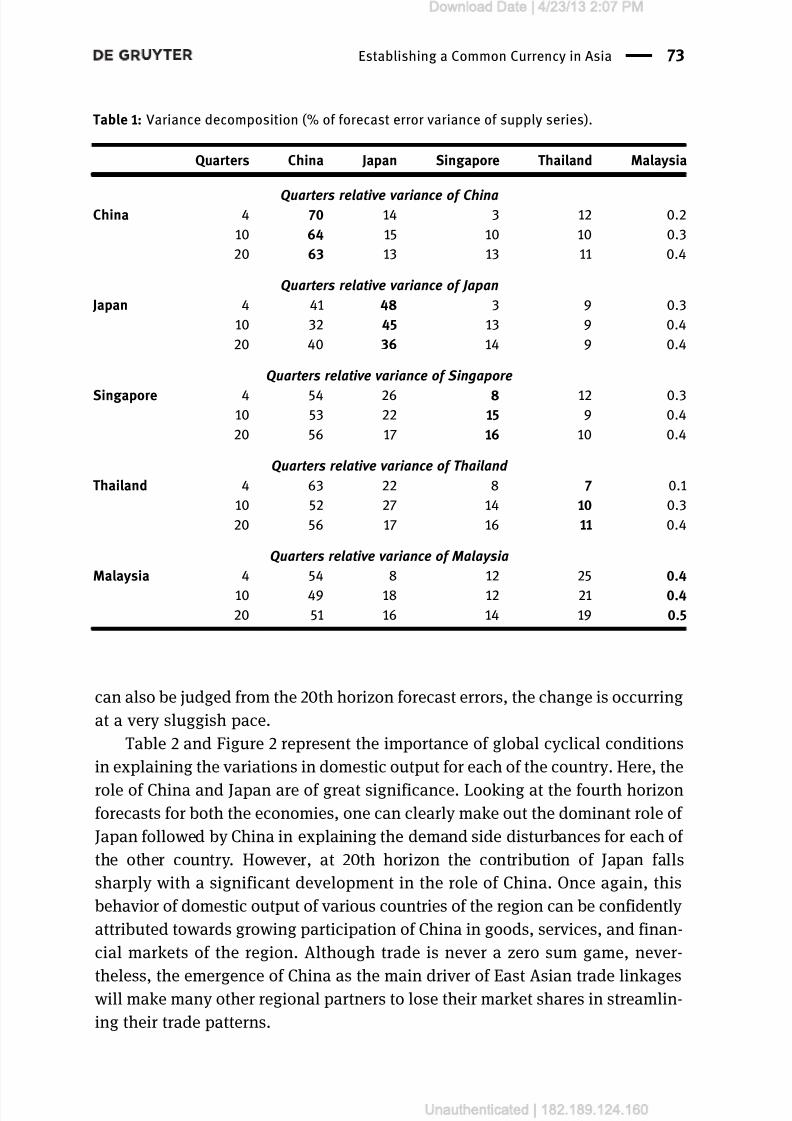

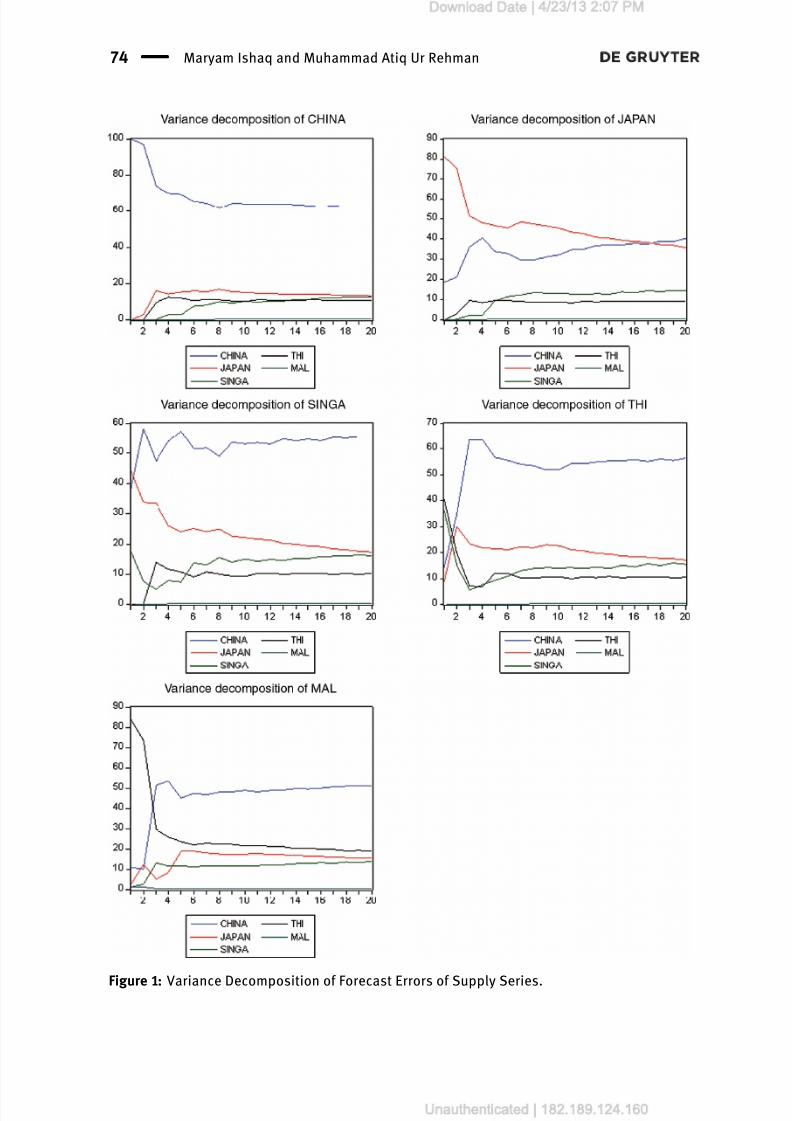

Table 1 and Figure 1 states the variance decomposition of forecast errors of

supply series in percentage form at four and twenty quarters forecast horizon for

some of the selected high income North and South East Asian economies. It is

clearly evident from the statistics that China is noticeably dominant and is

accounting for 56% for Singapore, 56% for Thailand and, 51% for Malaysia

and 40% of Japan’s total variations. Hence, it may be deduced that China’s

economic conditions are most influential amongst all the other members. The

fact also points towards the deepening trade linkages of China with rest of the

region exhibiting her as the most prominent economy of the region. This finding

is in line with that of Frankle and Rose (1998) who pointed the importance of intraregional trade linkages in the context of symmetric shocks region wide.

Although the growing importance of domestic shocks for each of the economy

72 Maryam Ishaq and Muhammad Atiq Ur Rehman

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 11/26

can also be judged from the 20th horizon forecast errors, the change is occurring

at a very sluggish pace.

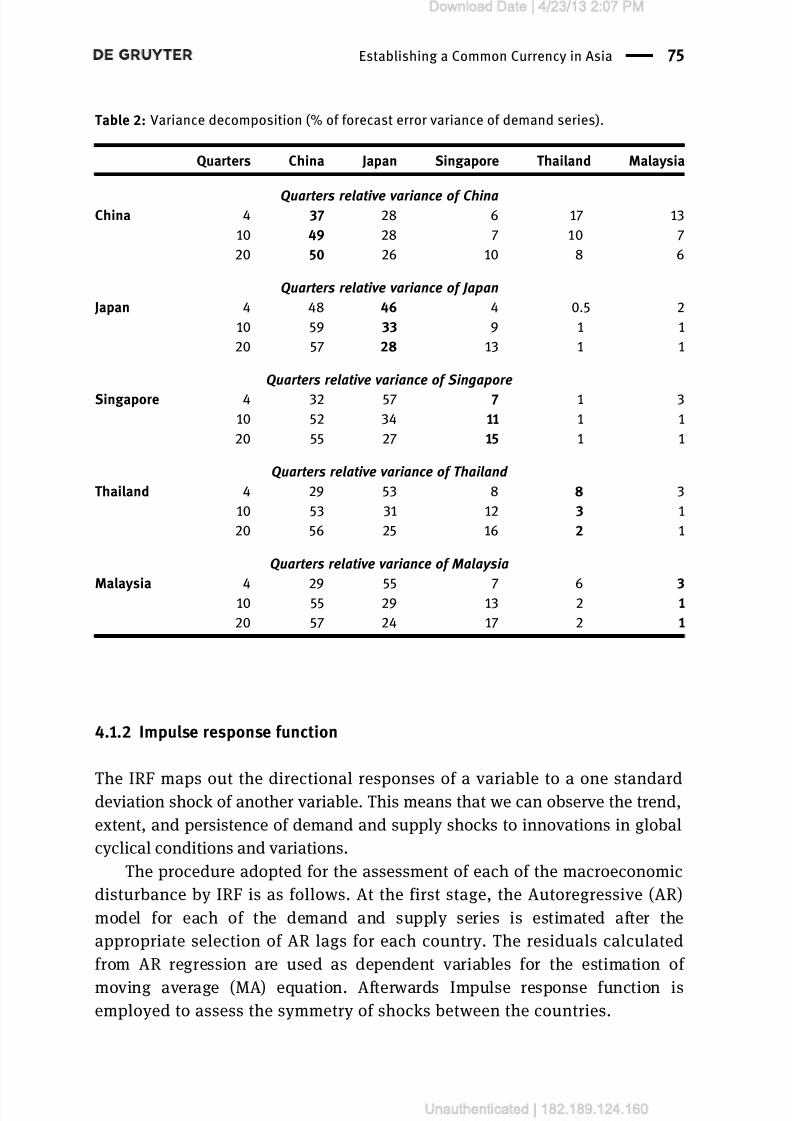

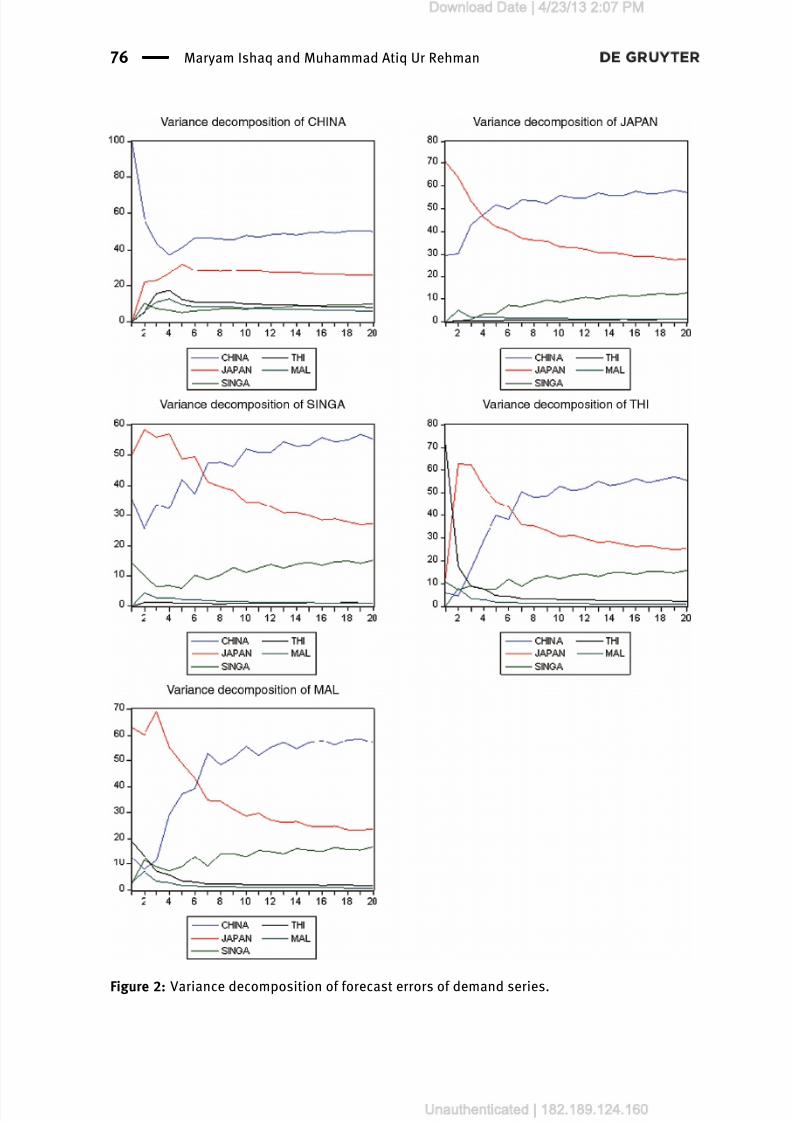

Table 2 and Figure 2 represent the importance of global cyclical conditions

in explaining the variations in domestic output for each of the country. Here, the

role of China and Japan are of great significance. Looking at the fourth horizonforecasts for both the economies, one can clearly make out the dominant role of

Japan followed by China in explaining the demand side disturbances for each of

the other country. However, at 20th horizon the contribution of Japan falls

sharply with a significant development in the role of China. Once again, this

behavior of domestic output of various countries of the region can be confidently

attributed towards growing participation of China in goods, services, and finan-

cial markets of the region. Although trade is never a zero sum game, never-

theless, the emergence of China as the main driver of East Asian trade linkageswill make many other regional partners to lose their market shares in streamlin-

ing their trade patterns.

Table 1: Variance decomposition (% of forecast error variance of supply series).

Quarters China Japan Singapore Thailand Malaysia

Quarters relative variance of ChinaChina 4 70 14 3 12 0.2

10 64 15 10 10 0.3

20 63 13 13 11 0.4

Quarters relative variance of Japan

Japan 4 41 48 3 9 0.3

10 32 45 13 9 0.4

20 40 36 14 9 0.4

Quarters relative variance of Singapore

Singapore 4 54 26 8 12 0.310 53 22 15 9 0.4

20 56 17 16 10 0.4

Quarters relative variance of Thailand

Thailand 4 63 22 8 7 0.1

10 52 27 14 10 0.3

20 56 17 16 11 0.4

Quarters relative variance of Malaysia

Malaysia 4 54 8 12 25 0.4

10 49 18 12 21 0.4

20 51 16 14 19 0.5

Establishing a Common Currency in Asia 73

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 12/26

Figure 1: Variance Decomposition of Forecast Errors of Supply Series.

74 Maryam Ishaq and Muhammad Atiq Ur Rehman

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 13/26

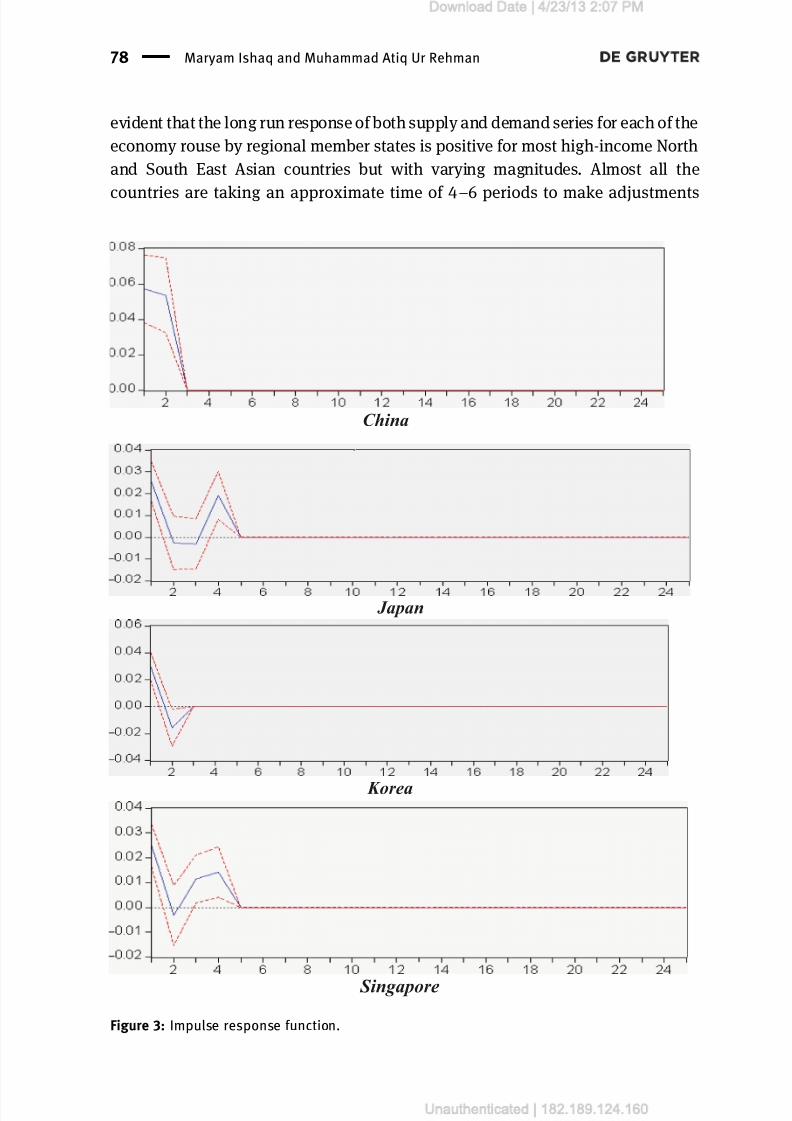

4.1.2 Impulse response function

The IRF maps out the directional responses of a variable to a one standarddeviation shock of another variable. This means that we can observe the trend,

extent, and persistence of demand and supply shocks to innovations in global

cyclical conditions and variations.

The procedure adopted for the assessment of each of the macroeconomic

disturbance by IRF is as follows. At the first stage, the Autoregressive (AR)

model for each of the demand and supply series is estimated after the

appropriate selection of AR lags for each country. The residuals calculated

from AR regression are used as dependent variables for the estimation of

moving average (MA) equation. Afterwards Impulse response function isemployed to assess the symmetry of shocks between the countries.

Table 2: Variance decomposition (% of forecast error variance of demand series).

Quarters China Japan Singapore Thailand Malaysia

Quarters relative variance of ChinaChina 4 37 28 6 17 13

10 49 28 7 10 7

20 50 26 10 8 6

Quarters relative variance of Japan

Japan 4 48 46 4 0.5 2

10 59 33 9 1 1

20 57 28 13 1 1

Quarters relative variance of Singapore

Singapore 4 32 57 7 1 3

10 52 34 11 1 1

20 55 27 15 1 1

Quarters relative variance of Thailand

Thailand 4 29 53 8 8 3

10 53 31 12 3 1

20 56 25 16 2 1

Quarters relative variance of Malaysia

Malaysia 4 29 55 7 6 310 55 29 13 2 1

20 57 24 17 2 1

Establishing a Common Currency in Asia 75

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 14/26

Figure 2: Variance decomposition of forecast errors of demand series.

76 Maryam Ishaq and Muhammad Atiq Ur Rehman

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 15/26

If Z t is the structural shocks to an economy, the AR process in which each element

of Z t is regressed on lagged values of all the elements of Z t can be written as

Z t ¼ 1Z tÀ1 þ 2Z tÀ2 þ Á Á Á þ nZ tÀn þ "t

where "t represents the residuals from the AR equation for the demand and

supply shocks each. We can denote the residuals individually as "t d for demand

and "t s for supply equation. Following Bayoumi and Eichengreen (1994), we

consider a system in which the true model can be represented by an infinite

moving average of and an equal number of shocks "t . The error from AR process

can be shown as a linear combination of current and past structural shocks by

the following moving average process:

"t ¼ 0t þ 1tÀ1 þ 2tÀ2 þ Á Á Á ¼X

Liit

The matrix i represents impulse response functions of the shocks to the elements

of Z t .

Precisely, macroeconomic and structural convergence has never been

amongst the criterion of OCA. It is certainly not inevitable for the establishment

of a single currency area. But once a common currency union is established it

becomes obligatory for member countries to guarantee macro economic conver-

gence and symmetric patterns of macroeconomic variables. The basic needbehind the fulfillment of this condition is that without achieving this propor-

tionality, countries with differential inflation rates and fiscal deficits, it would be

very hard for them to agree upon a mutual non-inflationary monetary policy.

Supply shocks are “generally more relevant” than demand shocks, since supply

shocks are “more related to underlying private sector behavior” (Bayoumi and

Mauro 2001, 943) and “unaffected by changes in demand-management policies

and are more likely to be invariant with respect to alternative international

monetary arrangements” (Bayoumi and Eichengreen 1994, 23).

Countries experiencing symmetric macroeconomic shocks are likely to favorsimilar policy responses and make themselves good candidates for a common

currency area. The Structural Var approach allows us to identify the underlying

shocks affecting the observed macroeconomic variables. It is assumed that if the

correlation of structural shocks is positive, the shocks will be considered to be

symmetric and if negative or insignificant they are asymmetric. A group of

economies – if identified to have higher correlations of macroeconomic shocks

with each other – may well qualify for an OCA.

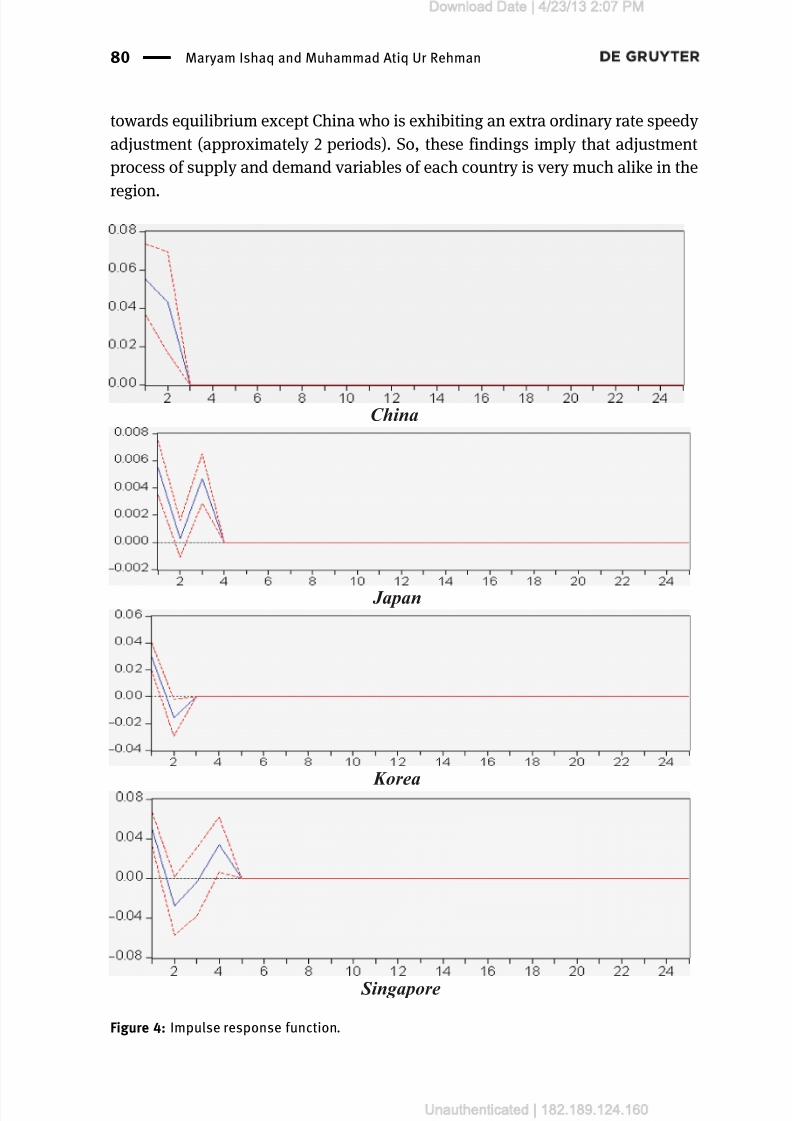

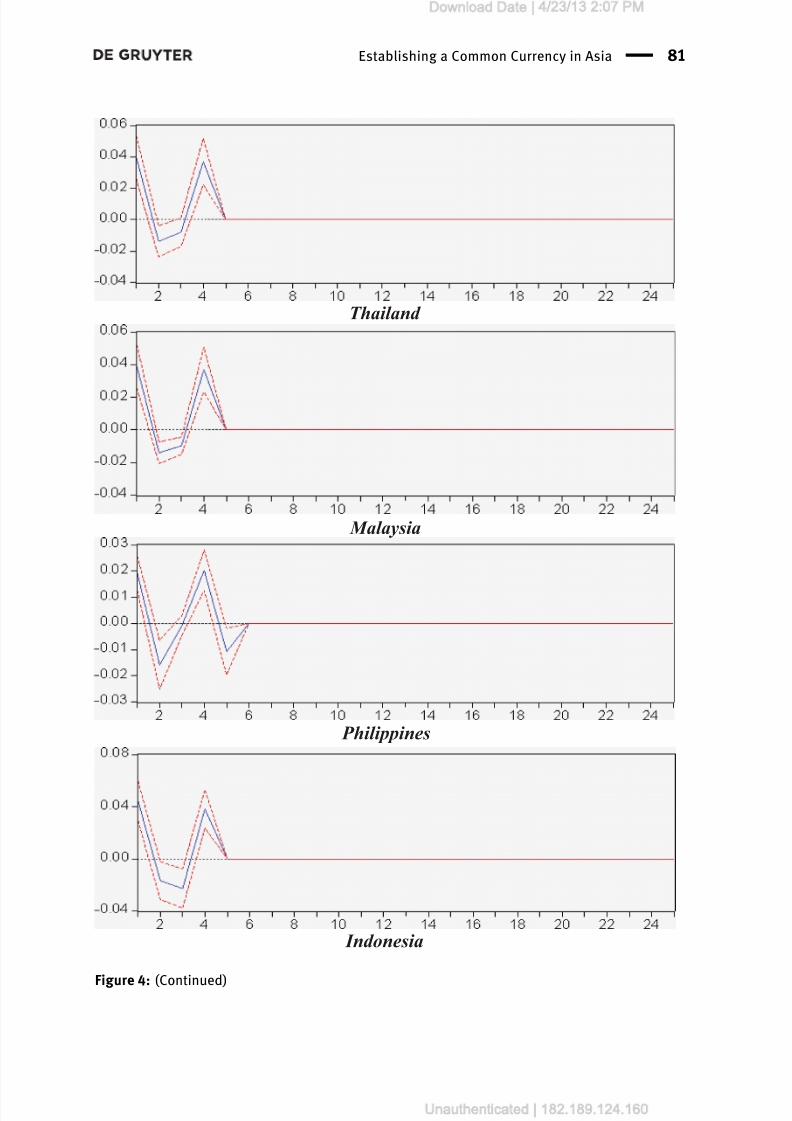

Figures 3 and 4 are representing the dynamic effect of one standard deviationstructural shock on domestic output over a 24-quarter period for all of the states

under study. One may observe that the path of response is much parallel. Hence, it is

Establishing a Common Currency in Asia 77

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 16/26

evident that the long run response of both supply and demand series for each of the

economy rouse by regional member states is positive for most high-income North

and South East Asian countries but with varying magnitudes. Almost all the

countries are taking an approximate time of 4–

6 periods to make adjustments

Singapore

Figure 3: Impulse response function.

China

Japan

Korea

78 Maryam Ishaq and Muhammad Atiq Ur Rehman

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 17/26

Indonesia

Figure 3: (Continued)

Thailand

Malaysia

Philippines

Establishing a Common Currency in Asia 79

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 18/26

towards equilibrium except China who is exhibiting an extra ordinary rate speedy

adjustment (approximately 2 periods). So, these findings imply that adjustment

process of supply and demand variables of each country is very much alike in the

region.

Korea

China

Japan

Singapore

Figure 4: Impulse response function.

80 Maryam Ishaq and Muhammad Atiq Ur Rehman

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 19/26

Indonesia

Figure 4: (Continued)

Thailand

Malaysia

Philippines

Establishing a Common Currency in Asia 81

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 20/26

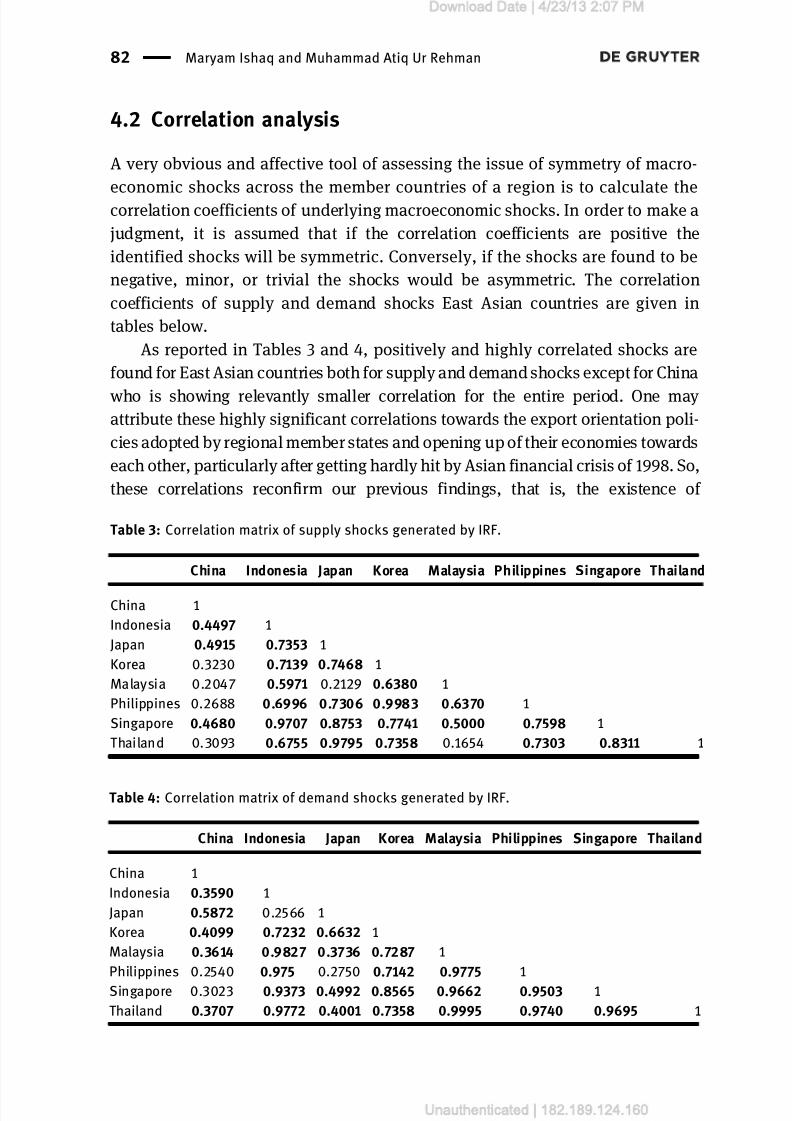

4.2 Correlation analysis

A very obvious and affective tool of assessing the issue of symmetry of macro-

economic shocks across the member countries of a region is to calculate the

correlation coefficients of underlying macroeconomic shocks. In order to make a

judgment, it is assumed that if the correlation coefficients are positive the

identified shocks will be symmetric. Conversely, if the shocks are found to be

negative, minor, or trivial the shocks would be asymmetric. The correlation

coefficients of supply and demand shocks East Asian countries are given in

tables below.

As reported in Tables 3 and 4, positively and highly correlated shocks are

found for East Asian countries both for supply and demand shocks except for China

who is showing relevantly smaller correlation for the entire period. One may attribute these highly significant correlations towards the export orientation poli-

cies adopted by regional member states and opening up of their economies towards

each other, particularly after getting hardly hit by Asian financial crisis of 1998. So,

these correlations reconfirm our previous findings, that is, the existence of

Table 3: Correlation matrix of supply shocks generated by IRF.

China Indonesia Japan Korea Malaysia Philippines Singapore Thailand

China 1

Indonesia 0.4497 1

Japan 0.4915 0.7353 1

Korea 0.3230 0.7139 0.7468 1

Malaysia 0.2047 0.5971 0.2129 0.6380 1

Philippines 0.2688 0.6996 0.7306 0.9983 0.6370 1

Singapore 0.4680 0.9707 0.8753 0.7741 0.5000 0.7598 1

Thailand 0.3093 0.6755 0.9795 0.7358 0.1654 0.7303 0.8311 1

Table 4: Correlation matrix of demand shocks generated by IRF.

China Indonesia Japan Korea Malaysia Philippines Singapore Thailand

China 1

Indonesia 0.3590 1

Japan 0.5872 0.2566 1

Korea 0.4099 0.7232 0.6632 1

Malaysia 0.3614 0.9827 0.3736 0.7287 1

Philippines 0.2540 0.975 0.2750 0.7142 0.9775 1

Singapore 0.3023 0.9373 0.4992 0.8565 0.9662 0.9503 1

Thailand 0.3707 0.9772 0.4001 0.7358 0.9995 0.9740 0.9695 1

82 Maryam Ishaq and Muhammad Atiq Ur Rehman

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 21/26

symmetry in macroeconomic environment amongst the economies of the region

excluding China who is showing somewhat secluded behavior in this respect. So,

one may take this conclusion as the costs associated with opting for a common

currency for the region are relatively small as were anticipated before. This willpositively cut down the probable commotions caused by global business cycles

under bilateral fixed exchange rates amongst the member economies.

5 Computation of optimum currency area

(OCA) index

This part of paper aims at estimating the variability of exchange rate behaviors

of East Asian economies by formulating OCA index. The index is formed by the

ordinary least square (OLS) method. All the currencies are taken against US

dollar. It is hypothesized that smaller the value of OCA index will be for a

country more stable its currency would be and vice versa.

Originally, the model of exchange rate variability was proposed by Vaubel

(1977). He employed the model for the sake of estimating OCA index for various

economies of European region. The magnitude of variability was then calculated

by measuring the standard deviation of exchange rate fluctuation between twocountries. The index is also very functional in the sense that it gives a very

comprehensive picture of costs and benefits associated with the establishment of

a single currency area.

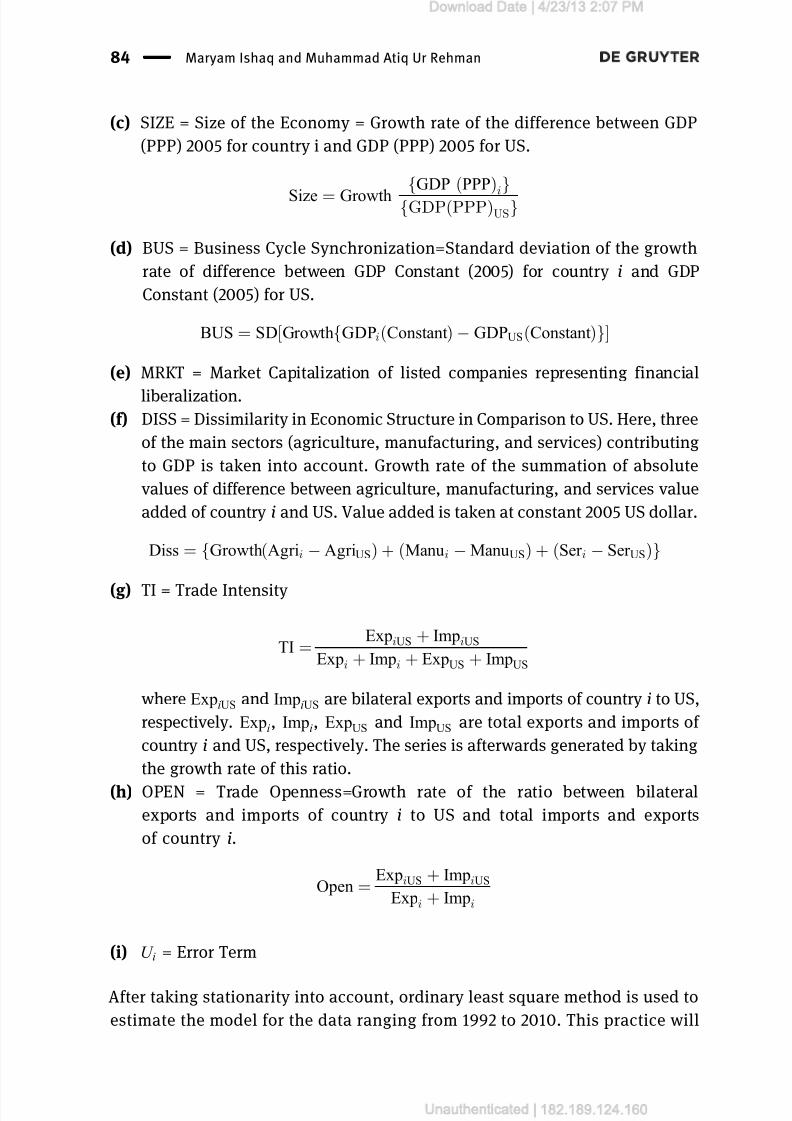

5.1 Defining variables

Using the improved version of Bayoumi and Eichengreen model devised by

Hovert (2003) and further used by Achsani and Partiswi (2010), for each of theparticipant country, following linear equation will be estimated.

LEXR ij ¼ INFij þ SIZEij þ BUSij þ MRKTij þ DISSij þ TIij þ OPENij þ U t

(a) LEXR = Logarithm of bilateral exchange rate volatility between countries i

and US, that is, the OCA index. Volatility is calculated by taking the standard

deviation of projected values of exchange rate. The variable is calculated at

market rate and the period averages are taken.

(b) INF = Inflation = Growth rate of Consumer Price Index (CPI) calculated with

the base year 2005.

Establishing a Common Currency in Asia 83

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 22/26

(c) SIZE = Size of the Economy = Growth rate of the difference between GDP

(PPP) 2005 for country i and GDP (PPP) 2005 for US.

Size ¼ GrowthfGDP ðPPPÞ

i

g

fGDPðPPPÞUS

g

(d) BUS = Business Cycle Synchronization=Standard deviation of the growth

rate of difference between GDP Constant (2005) for country i and GDP

Constant (2005) for US.

BUS ¼ SD Growth GDPi Constant ð Þ À GDPUS Constant ð Þf g½

(e) MRKT = Market Capitalization of listed companies representing financial

liberalization.(f) DISS = Dissimilarity in Economic Structure in Comparison to US. Here, three

of the main sectors (agriculture, manufacturing, and services) contributing

to GDP is taken into account. Growth rate of the summation of absolute

values of difference between agriculture, manufacturing, and services value

added of country i and US. Value added is taken at constant 2005 US dollar.

Diss ¼ Growth Agrii À AgriUSð Þ þ Manui À ManuUSð Þ þ Ser i À Ser USð Þf g

(g) TI = Trade Intensity

TI ¼ExpiUS þ ImpiUS

Expi þ Impi þ ExpUS þ ImpUS

where ExpiUS and Imp

iUS are bilateral exports and imports of country i to US,

respectively. Expi, Imp

i, ExpUS and ImpUS are total exports and imports of

country i and US, respectively. The series is afterwards generated by taking

the growth rate of this ratio.

(h) OPEN = Trade Openness=Growth rate of the ratio between bilateralexports and imports of country i to US and total imports and exports

of country i.

Open ¼ExpiUS þ ImpiUS

Expi þ Impi

(i) U i = Error Term

After taking stationarity into account, ordinary least square method is used to

estimate the model for the data ranging from 1992 to 2010. This practice will

84 Maryam Ishaq and Muhammad Atiq Ur Rehman

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 23/26

provide with the general behavior of all the explanatory variables for the

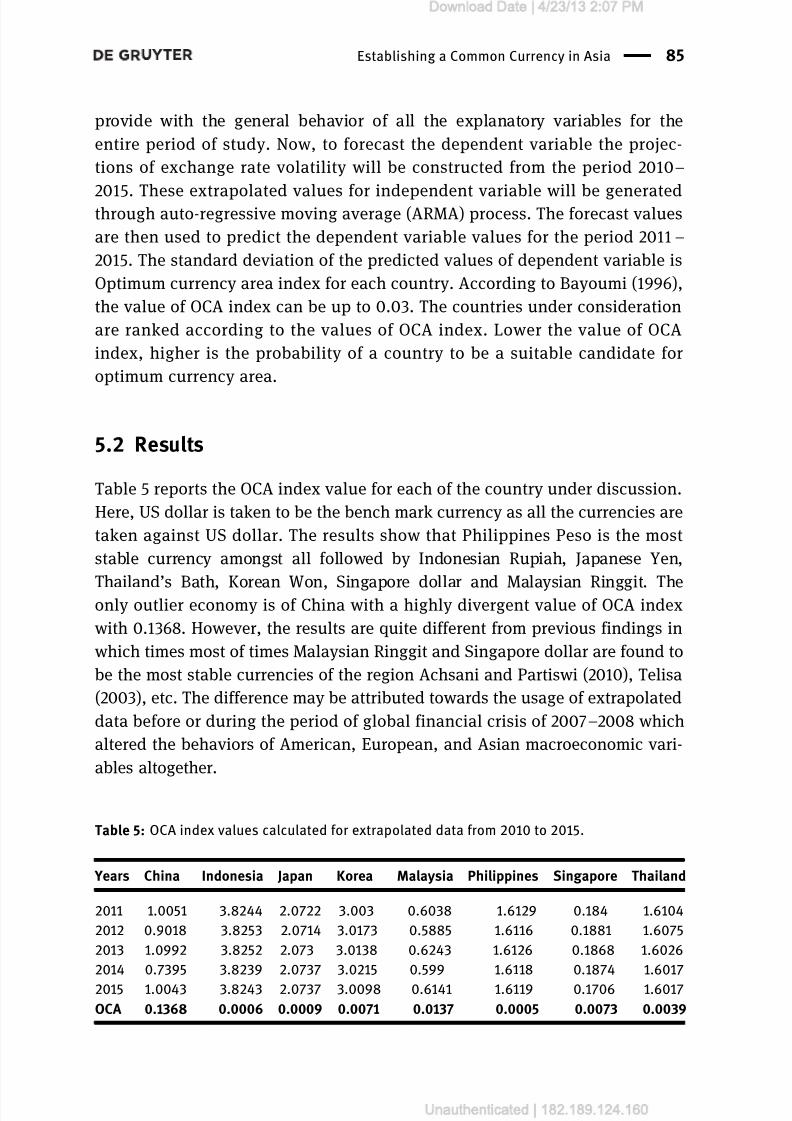

entire period of study. Now, to forecast the dependent variable the projec-

tions of exchange rate volatility will be constructed from the period 2010–

2015. These extrapolated values for independent variable will be generatedthrough auto-regressive moving average (ARMA) process. The forecast values

are then used to predict the dependent variable values for the period 2011–

2015. The standard deviation of the predicted values of dependent variable is

Optimum currency area index for each country. According to Bayoumi (1996),

the value of OCA index can be up to 0.03. The countries under consideration

are ranked according to the values of OCA index. Lower the value of OCA

index, higher is the probability of a country to be a suitable candidate for

optimum currency area.

5.2 Results

Table 5 reports the OCA index value for each of the country under discussion.

Here, US dollar is taken to be the bench mark currency as all the currencies are

taken against US dollar. The results show that Philippines Peso is the most

stable currency amongst all followed by Indonesian Rupiah, Japanese Yen,

Thailand’

s Bath, Korean Won, Singapore dollar and Malaysian Ringgit. Theonly outlier economy is of China with a highly divergent value of OCA index

with 0.1368. However, the results are quite different from previous findings in

which times most of times Malaysian Ringgit and Singapore dollar are found to

be the most stable currencies of the region Achsani and Partiswi (2010), Telisa

(2003), etc. The difference may be attributed towards the usage of extrapolated

data before or during the period of global financial crisis of 2007–2008 which

altered the behaviors of American, European, and Asian macroeconomic vari-

ables altogether.

Table 5: OCA index values calculated for extrapolated data from 2010 to 2015.

Years China Indonesia Japan Korea Malaysia Philippines Singapore Thailand

2011 1.0051 3.8244 2.0722 3.003 0.6038 1.6129 0.184 1.6104

2012 0.9018 3.8253 2.0714 3.0173 0.5885 1.6116 0.1881 1.6075

2013 1.0992 3.8252 2.073 3.0138 0.6243 1.6126 0.1868 1.6026

2014 0.7395 3.8239 2.0737 3.0215 0.599 1.6118 0.1874 1.6017

2015 1.0043 3.8243 2.0737 3.0098 0.6141 1.6119 0.1706 1.6017

OCA 0.1368 0.0006 0.0009 0.0071 0.0137 0.0005 0.0073 0.0039

Establishing a Common Currency in Asia 85

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 24/26

6 Concluding remarks

The study was basically aimed at two major objectives (i) identification of

underlying macroeconomic shocks using a two-variable VAR model by employ-ing almost two decades of annual data (ii) testing the possibility of establishing

a single currency area among East Asian high income countries.

The results suggest that exchange rate of East Asian economies are relatively

stable. Most of them are exhibiting a consistent pattern of GDP growth proven by

highly significant values of correlation analysis. Supply shocks are also signifi-

cantly correlated particular amongst those economies which are most directly hit

by Asian financial crisis of 1998. But except for China who is displaying quite a

contrary attitude in comparison to its neighbor economies. So it may be con-cluded that, on the average, structural shocks are remarkably symmetric with

high magnitudes. The speed of adjustment towards these shocks is quite

encouraging in the sense that on the whole all the economies are displaying a

good tendency of reverting back to their equilibriums after a short period of

time, probably due to relatively flexible labor market and less rigid wage rate,

providing them with a good potential of adjusting themselves towards macro-

economic and structural disturbances, thus, proving them to be capable of

making a good currency union amongst each other.

The empirical results drawn from the calculation of OCA index display strong support in favor of establishing an optimum currency area in the region

excluding China. Taking start with Philippines, Indonesia and Japan the region

proves itself to b a potential candidate for currency union. As the macroeco-

nomic disturbances are highly correlated and countries are exhibiting good

adjustments towards equilibrium, we may expect to see relatively mild cost of

this single currency adoption. However, this all must be done in a sequential

and cautious manner.

References

Achsani, N.A., and T. Partisiwi. 2010. “Testing the Feasibility of Asean+3 Single Currency

Comparing Optimum Currency Area and Clusturing Approach.” International Research

Journal of Finance and Economics 6(37):69–75.

Ahn, et al. 2006. “Is East Asia Fit for an Optimum Currency Area? An Assessment of the

Economic Feasibility of a Higher Degree of Monetary Cooperation in East Asia.” The

developing Economies 3(53):288–

305.Baffes, J., and I. Alison. 1997. “Single-Equation Estimation of Equilibrium Real Exchange Rate.”

Policy Research Working Paper Series 1800, 378–396.

86 Maryam Ishaq and Muhammad Atiq Ur Rehman

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 25/26

Bayoumi, T., and B. Eichengreen. 1988. One Money or Many? Analyzing the Prospects for

Monetary Unification in Various Parts of the World . Princeton, NJ: International Finance

Section, Department of Economics, Princeton University.

Bayoumi, T. 1996. “Operationalizing the Theory of Optimum Currency Areas.” CEPR Discussion

Papers 1484, C.E.P.R. Discussion Papers.Bayoumi, T., and B. Eichengreen 1998 “Exchange Rate Volatility and Intervention: Implications

of the Theory of Optimum Currency Areas,” CEPR Discussion Papers 1982, C.E.P.R.

Discussion Papers.

Bayoumi, T., and B. Eichengreen (1998).“One Money or Many? Analyzing the Prospects of

Monetary Unification in Various Parts of the World.” Princeton Studies in International

Finance No 76.

Bayoumi, T., and P. Mauro. 2001. “The Suitability of ASEAN for a Regional Currency Agreement.”

World Economy 7(24):933–954.

Blanchard, O.J., and D. Quah. 1989. “The Dynamic Effects of Aggregate Demand and Supply

Disturbances.” The American Economic Review 4(79):655–673.Chow, H.K., and Y. Kim. 2003. “A common currency peg in East Asia? Perspectives from Western

Europe,” Journal of Macroeconomics 25, 331–356.

Clark, P.B., and R. McMillan. 1998. “Exchange Rate and Economic Fundamentals:

A Methodological Comparison between BEERs and FEERs.” IMF Working Paper Series,

Paper No. 67 , 1–34.

Enders, W., and S. Hurn. 1994. “Theory and Tests of Generalized Purchasing-Power Parity:

Common Trends and Real Exchange Rates in the Pacific Rim.” Review of International

Economics 2(2):179–190.

Francois, J.F., and G. Wignaraja. 2008. “Economic Implications of Asian Integration.” Global

Economy Journal 8(3):334–361.Frankel, A.J., and A.K. Rose. 1998. “The Endogeneity of the Optimum Currency Area Criteria.”

Economic Journal, Royal Economic Society 108(449):1009–25.

Gregorio, J.D., and H.C. Wolf. 1994. “Terms of Trade, Productivity and the Real Exchange Rate.”

NBER Working Paper Series No. 4807 , 448–467.

Hamanaka, S. 2012. “Trends of Trade Interdependence and Proliferation of FTAs in Asia.” Global

Economy Journal 12(2):211–237.

Horvath, J., and R. Grabowski. 1997. “Prospects of African Integration in Light of the Theory of

Optimum Currency Areas.” Journal of Economic Integration 1(12):1–25.

Hovert. 2003. “Does Monetary Policy Matter? A new Test in the Spirit of Friedman and

Schwartz.” NBER Macroeconomic Annual 22(7):121–170.Kawai, M., and T. Motonishi. 2004. “International Macroeconomic Interdependence in East

Asia: Empirical Evidence and Issues.” A revised version (December) of a paper presented

to the High-Level Conference on “Asia’s Economic Cooperation and Integration” (July 1–2)

organized by the Asian Development Bank, Manila.

Kenen, P., 1969. “The Theory of Optimum Currency Areas and Exchange-Rate Flexibility.”

Special Papers in International Economics No. 11, Princeton: International Finance Section,

Department of Economics, Princeton University.

Krugman, Paul. 1993 “Lessons from Massachusetts for EMU” in F. Torres and F. Giavazzi

(eds.), Adjustment and Growth in the European Monetary Union, Cambridge University

Press.Kwack, S. Yeung. 2004. “An Optimum Currency Area in East Asia: Feasibility, Coordination, and

Leadership Role.” Journal of Asian Economics 1(15):153–169.

Establishing a Common Currency in Asia 87

Unauthenticated | 182.189.124.160

Download Date | 4/23/13 2:07 PM

7/28/2019 Surmounting the Individual: possibility of common currency area in Asia, A case study of East Asian Economies

http://slidepdf.com/reader/full/surmounting-the-individual-possibility-of-common-currency-area-in-asia-a 26/26

Ling, P., and H. Yuen. 2001. “Optimum Currency Areas in East Asia: A Structural VAR Approach.”

ASEAN Economic Bulletin 2(18):206–217.

McDonalald, S., and S. Robinson. 2008. “Asian Growth and Trade Poles: India, China and East

and South East Asia.” World Development 36(2):210–234.

Oskooee, M.B., S.W. Hegerty, and Xu, J. 2012. “Exchange-Rate Volatility and Industry Tradebetween Japan and China.” Global Economy Journal 12(3):677–689.

Taguchi, H. 2010. “Feasibility of Currency Unions in Asia – An Assessment Using Generalized

Purchasing Power Parity.” Policy Research Institute, Ministry of Finance, Japan Public

Policy Review 6(5):859–872.

Telisa, A.F. 2003. “Feasibility of Forming Currency Union in ASEAN-5 Countries.” Research

Laboratory of Economics, Department of Economics, University of Indonesia.

Vaubel, R. 1976. “Real exchange-rate changes in the European community: The empirical

evidence and its implications for European currency unification.” Review of World

Economics (Weltwirtschaftliches Archiv), Springer 112(3): 429–470.

Yousoff, M.B. 2010. “Bilateral Trade Balance, Exchange Rate and Incomes: Evidence fromMalaysia.” Global Economy Journal 9(4):1323–1337.

Zhang et al. (2004). “Is a Monetary Union Feasible for East Asia.” Applied Economics

10(36):1031–1043.

88 Maryam Ishaq and Muhammad Atiq Ur Rehman