Embed Size (px)

DESCRIPTION

Surety Association of Canada 2012 Future Projects Summit Presentation

Citation preview

Fort McMurray Future Projects SummitMarch 29, 2012

Surety Bonds &Construction Risk

PresentersDave Bentley, Senior Surety Broker, Hub

Insurance Services Edmonton; Past ChairInsurance Services, Edmonton; Past Chair, SAC-Prairies Regional CommitteeJason Smith, Managing Director, Surety,Jason Smith, Managing Director, Surety,

Construction Services, Foster Park Baskett Insurance Ltd.; Vice Chair, SAC-Prairies Regional CommitteeDonna Anderson, Vice President, Trisura

Guarantee Insurance Company

Introduction: Surety Association of Canada“Your Bonding Resource”Your Bonding Resource

National & Regional PresenceThe Voice of the IndustryThe Voice of the IndustryWork with Public/Private Owners

Membership:Surety Companiesy pBrokers Related professionals (e.g.) lawyers, p ( g ) y ,

claims managers

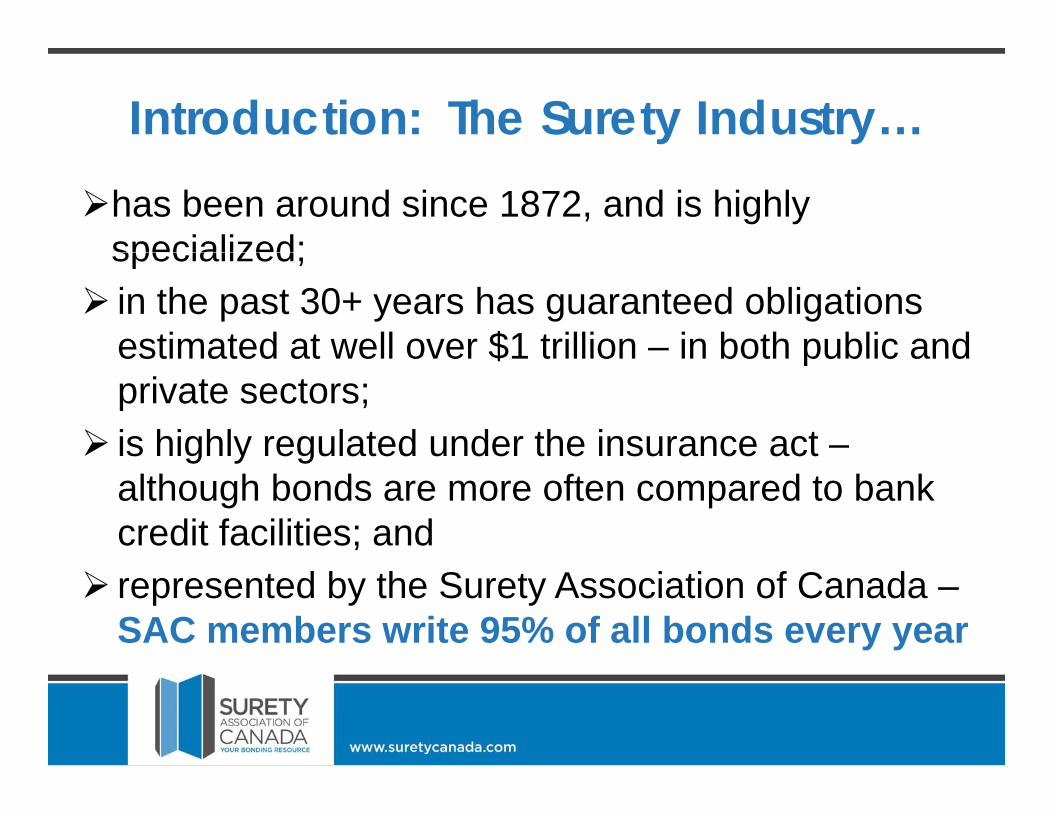

Introduction: The Surety Industry…has been around since 1872, and is highly

specialized;specialized; in the past 30+ years has guaranteed obligations

estimated at well over $1 trillion – in both public andestimated at well over $1 trillion in both public and private sectors;

is highly regulated under the insurance act –g y galthough bonds are more often compared to bank credit facilities; and

Surety Association of Canaa represented by the Surety Association of Canada –

SAC members write 95% of all bonds every year

Construction 2012 Increase in GC/Prime Contractor Defaults Increase in Sub/Specialty Contractor Defaultsp yNumber of local Contractors “Creeping Death”Total CDN surety premium in 2010 - $520 mTotal CDN surety premium in 2010 $520 mTotal CDN loss ratio in 2010 – 30% ($110 m)Total loss ratio in 2010 for AB 81% ($51 m)Total loss ratio in 2010 for AB – 81% ($51 m)Total surety premium in AB 2010 - $64 mJan 2011 to July 2011 – multiple defaults in AB 2011 year-end results will be interesting

Why Contractors FailUnqualified Contractors: the lowest “irresponsible”

bidderInsolvency of ContractorContractor default for non-financial reasons:Contractor default for non-financial reasons:

Over Extension (cash flow problems)Inability to complete/lack of continuityy p yIncapacity of Key people/losing key people

Unpaid subs and suppliers resulting in liensp pp gWarranty problems from past jobs

Surety BondsSurety BondsWhat are They?What are They?

How do they Work?

Surety is not InsuranceyINSURANCE

2 party agreement;SURETY

3 party agreement; 2 party agreement; Insured & Insurer

Premiums actuarially

3 party agreement; Owner, Contractor & SuretyPremiums actuarially

determined Losses anticipated

SuretyPremiums (multiple

factors) Losses anticipatedNo recourse against

insured in the event of

acto s)No losses anticipatedAccountability of Principalinsured in the event of

lossAccountability of Principal

via indemnity agreement

Surety Bonds: Three Essential Services1. Prequalification:

Assurance that the bonded contractor is qualified for the job for which they are contracted

2. Ongoing monitoring (and “hidden services”): S ti it ll f th b d d t t ’ Sureties monitor all of the bonded contractor’s

work and can supply technical, management and even financial assistance to prevent a defaulteven financial assistance to prevent a default

3. Security: Financial protection in the event that the

bonded contractor should default on its obligation.

PrequalificationO i Th h & V l Add dOngoing, Thorough & Value Added

IntensiveIntensive

OngoingOngoing

Comprehensive

Value Added

Standard Construction BondsPrequalification & Financial Security

(throughout the procurement process)(throughout the procurement process) Prequalification Letter Bid B d Bid Bond Consent of Surety P f B d Performance Bond Labour & Material Payment Bond R bl M lti Y B d ( i Renewable Multi-Year Bonds (service

contracts)

Prequalification LetterqNot a bond but a letter from a surety to the project

owner confirming “bondability”owner confirming bondability

Used during the pre-tender phase; i.e. before contract terms scope or pricing details are knowncontract terms, scope or pricing details are known

Non-binding – surety and principal reserve the i ht t i th d t il b f fi it tright to review the details before firm commitment

Typically refer to the project at handyp y p j

SAC standard form available on SAC website

Bid Bondsprotection from the “lowest irresponsible bidder”provide assurance that contractor will:enter into contractprovide the required security

Typically required in the amount of 10% of tenderif contractor defaults, surety pays the difference

between successful bid and second bidderTender must be accepted within time frame set out in

tender documentsseven months to file suit

Consent of SuretyNot a bond at all; a letter of commitment from the

Surety to the Obligee to execute performance y gand/or payment bonds

N l t t t t tiNo penal sum set out; payment not an option

Typically bonds must be required within 30 daysTypically, bonds must be required within 30 days following award

No standard (CCDC) form in existence, many variations in wording

Performance BondsGuarantees Contractor will perform contract inGuarantees Contractor will perform contract in

accordance with its terms & conditions.Contractor must be in default and the default mustContractor must be in default and the default must

be declaredOwner must perform their obligationsOwner must perform their obligations 4 options available to Surety:Remedy the defaultRemedy the defaultComplete the ContractArrange for new contractor to completeg pTender Payment

Two years to file suitTwo years to file suit

Labour &Material Payment BondsGuarantee that the contractor will pay all directGuarantee that the contractor will pay all direct

subcontractors, suppliers for materials and services provided to bonded project.provided to bonded project.Obligee is trustee on behalf of the claimantsClaimant must have a direct contract with theClaimant must have a direct contract with the

PrincipalClaimants may only claim for goods and services y y g

supplied to the bonded jobClaim must be filed within 120 days of the last day

worked or the date material shippedOne year to file suit

S t B dSurety BondsHow are they Obtained?

Who Obtains the Bond? Project Owner is not responsible for obtaining

the required bonding or other contract security.Owner only has to include bonding

requirement in tender documents or contract specificationsThe contractor obtains the bondingSelects a professional surety bond broker orSelects a professional surety bond broker or

agent who assists in submitting case to a surety underwriting company

How is a Bond Obtained?How is a Bond Obtained?Contractor Submits Financial

Statements and other background information to Surety

Participates in prequalification process: an in depth look at contractor’san in-depth look at contractor s business operations and financial structurestructure.

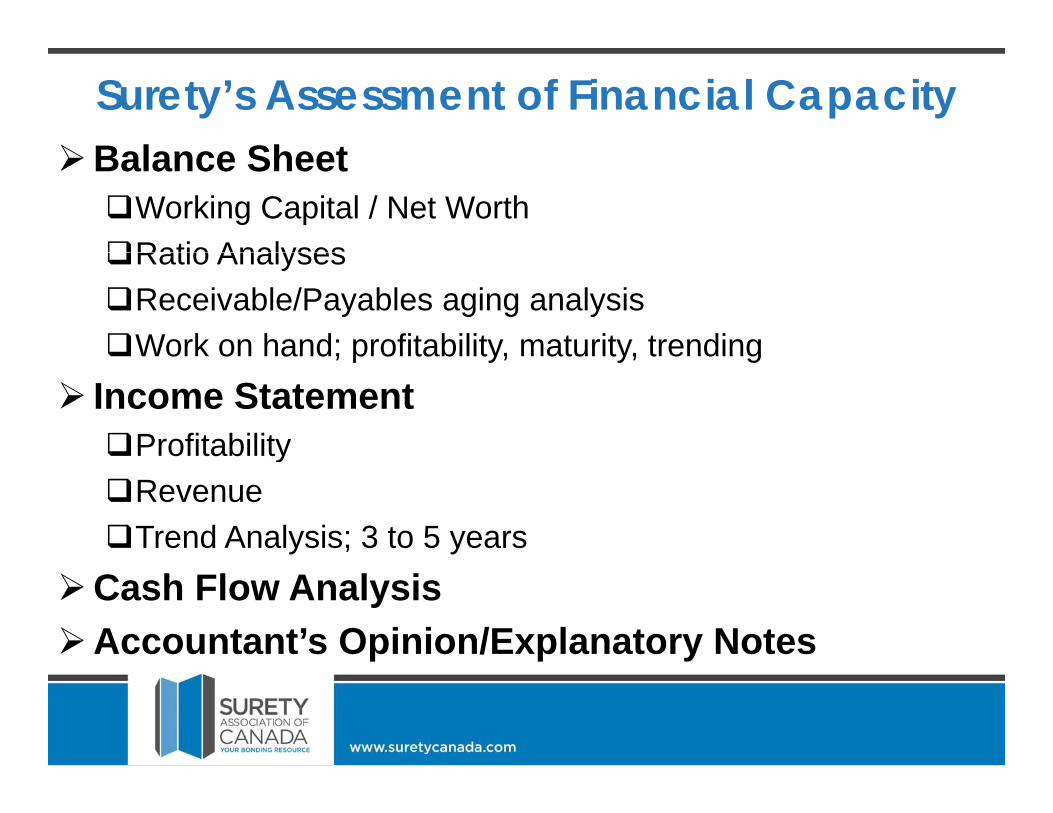

Surety’s Assessment of Financial CapacityB l Sh tBalance SheetWorking Capital / Net WorthRatio AnalysesRatio AnalysesReceivable/Payables aging analysisWork on hand; profitability, maturity, trendingWork on hand; profitability, maturity, trending

Income StatementProfitabilityyRevenueTrend Analysis; 3 to 5 years

Cash Flow AnalysisAccountant’s Opinion/Explanatory Notes

What Else does a Surety Need?Complete details – Affiliated/Related Companiesownership financial information etcownership, financial information, etc.

Detailed Work on Hand SchedulesA d Li ti f R i bl d P blAged Listing of Receivables and PayablesOrganization Chart of Key EmployeesDetailed Resumes of Principal & EmployeesBusiness Plan & Contingency PlansSubcontractor & Supplier References

What Else does a Surety Need?Details of construction operations; areas of

expertise, list of key projects, key people, etc.Letters of Recommendations from OwnersEvidence and details of a Line of Credit from a

Financial InstitutionDetails of business continuity plans in the event of

death or incapacity of owners/key peopleReports on Similar Completed Projectsp p jOwner, contract price, date completed, profit

earned

Surety BondsSurety BondsWhat Happens when a Contractor Defaults?

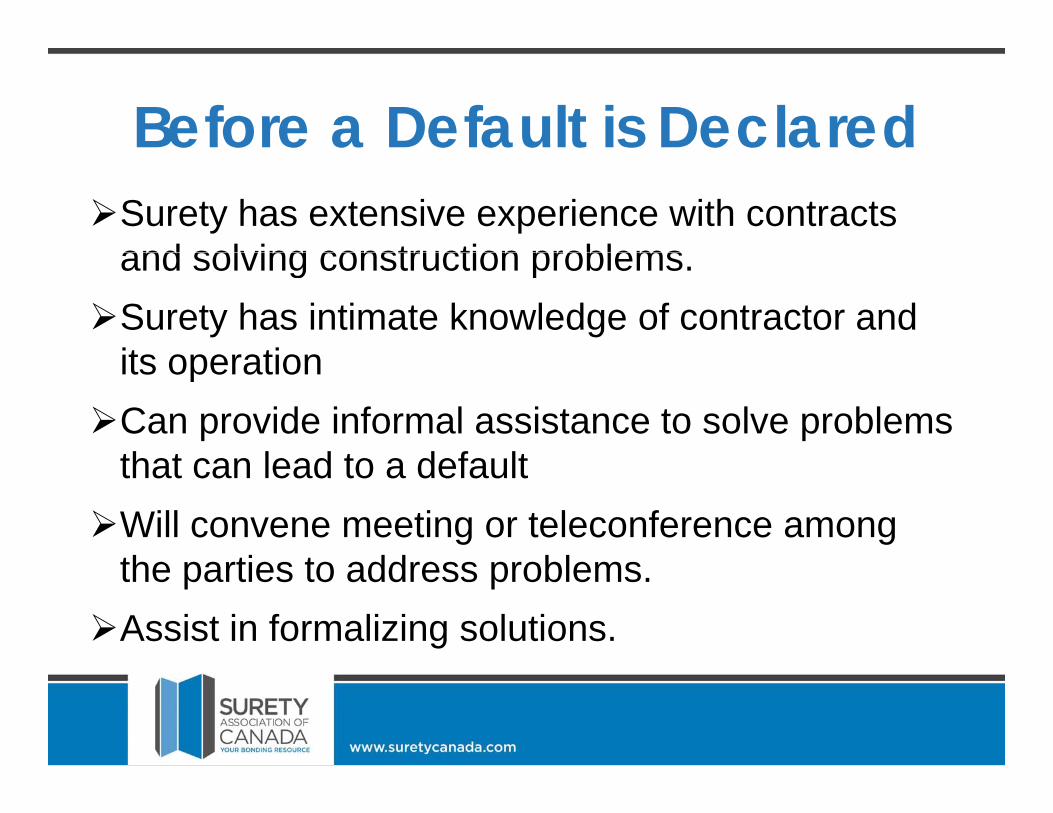

Before a Default is DeclaredSurety has extensive experience with contracts

and solving construction problemsand solving construction problems.Surety has intimate knowledge of contractor and

its operationits operationCan provide informal assistance to solve problems

th t l d t d f ltthat can lead to a defaultWill convene meeting or teleconference among

th ti t dd blthe parties to address problems.Assist in formalizing solutions.

ClaimsWh A C D f lWhen A Contractor Defaults:Surety will promptly acknowledge notice of default

and begin to gather information. Surety will begin an investigation as soon as

possible.Surety will conclude the investigation as soon as

possible.If requested by owner, surety will provide periodic

written updates on investigation status and best estimates as to completion date.

ClaimsDuring and After the Investigation:

Surety will cooperate with the owner to protect y p pwork from damage or deterioration.Surety will work with the owner to:yIdentify and implement a solution.Minimize delays, keep the job going and

protect the rights of all parties.Pay valid labour and material payment

bond claims as promptly as possible tobond claims as promptly as possible to ensure continuity of subs and suppliers.

How can the Project Owner Help?j pComply with bond & contract terms! (e.g. proper

notifications, payments and certifications)

Communicate: keep surety apprised of problems p y pp pand provide default notice promptly.

Cooperate: Ensure surety has access toCooperate: Ensure surety has access to knowledgeable staff and relevant documents.

K t ti li tiKeep expectations realistic.

Surety BondsSurety BondsUnseen Services to Owners & Lenders

Unseen Services of Surety BondsA surety can provide assistance and default preventionA surety can provide assistance and default prevention services to owners & lenders by: F ilit ti th l ti f t ti Facilitating the resolution of construction

performance issues that could lead to default P idi t d b i i t Providing management and business assistance

to assist contractors with administrative issues. P idi fi i l i fi i ll Providing financial assistance to financially

distressed contractors Providing technical/engineering expertise if

required

Letters of Credit (LOC)( )Yield cash; not performanceP id lifi tiProvide no prequalification assuranceAvailable in smaller; usually insufficient

amounts (5% to 20% of contract value)Deplete a contractor’s borrowing power - can p g p

bring on the very problem they seek to avoidProvide no dedicated protection for subs orProvide no dedicated protection for subs or

suppliers (only payment bonds do this)

Contractor Default Insurance (CDI or ‘Subguard’)(CDI, or Subguard )

Insurance product – designed to protect General Contractors – not owners compensates for loss incurred by the GC

Only one insurance company sells Subguard in Western Canada – about 8 large GCs have access to itInsured GCs are required to do their own underwritingNo independent third party surety involved (sureties

have 100 years of experience)have 100 years of experience)Very large deductibles and co-payment requirements

Contractor Default Insurance (CDI)Single event and aggregate policy limits (coverage

limits could be exceeded in a worst case scenario)Subguard GCs have a very strong financial

incentive (big profits) to sell this insuranceSummaryCDI protects General Contractors not ownersCDI protects General Contractors not ownersWithout bonding, there is no owner protection from

risks associated with default of prime contractorrisks associated with default of prime contractorCDI provides no protection for subs and suppliers

Another side to CDISubtrade and Supplier resistance is a growing issue,

as construction economy has tightenedNo payment assurance for subtrades & suppliers Without a L&MP bond, there is no payment protection

for themfor themThis will be reflected in their pricing, as there is

obviously more riskyTrades may object to being forced into CDI programIt requires that they surrender sensitive financial

i f ti t th GC th biddi tinformation to the GCs they are bidding toLess protection against unilateral action by the GCs

New & Improved pWhat’s the Latest in the World of Surety Bonds?World of Surety Bonds?

SAC Performance Bond 2012Designed to respond to owners’ concernsSAC consultations with Owners & Contractors: M “ t i t ” i th l iMore “certainty” in the claims process.More responsiveness to a claimMore frequent and effective communicationMore frequent and effective communication

between sureties and owners.In 2008 SAC Task Force appointed to respond toIn 2008 SAC Task Force appointed to respond to

needs of stakeholders.December 2011 – SAC Board of Directors approves ece be 0 S C oa d o ecto s app o es

new process enhanced performance bond; introduced in January 2012.

SAC Performance Bond 2012New “enhanced” performance bond provides construction buyers with more timely &responsive y y pclaim service.

SAC to work with CCDC to include new provisions inSAC to work with CCDC to include new provisions in the updated industry standard.Includes many features of the standard CCDC 221Includes many features of the standard CCDC 221

Performance Bond but with service improvements and clarifications.Provides more responsive services to owners by…..

SAC Performance Bond 2012Pre Demand Conference to allo s ret and o nerPre-Demand Conference to allow surety and owner

to prevent problems from turning into a default Timelines for Surety’s Response:Timelines for Surety s Response:5 days to acknowledge a response & request info.21 days (from receipt of information) for surety to

respond to owner with their response.Emergency Remedial Work: Allows Owner to

address urgent issues (e g safety) under the bondaddress urgent issues (e.g. safety) under the bondPost-Demand Conference: Mechanism to minimize

or eliminate work stoppages while surety investigates.or eliminate work stoppages while surety investigates.Contact Coordinates: Contact information for all

parties to facilitate notices and communication.

Surety Bonds & P3 ProjectsComprehensive and adequate performance securityComprehensive and adequate performance security

against construction default on mega-P3 projects.Sufficient capacity for mega-projects.Sufficient capacity for mega projects.Broad and flexible protection packages which include:Professional surety prequalficationSpecialty P3 bonds designed by member sureties: Provide liquid / cash on demand protection. Built in “fast track” dispute resolution Built-in “fast-track” dispute resolution Early Response; surety involved pre-default.

Protection for trades & suppliers via the payment bondProtection for trades & suppliers via the payment bond.Renewable Multi-year bonds provide protection during

long term operation/maintenance phase.g

E-Bidding & E-BondingSAC supports the broadening move across CanadaSAC supports the broadening move across Canada

toward e-biddingGreater efficiencyyMore accuracy (fewer mistakes)

Three years ago, SAC researched the state of the law respecting electronic commerce across CanadaProduced the SAC “E-Bonding Guidelines &

Checklist”ChecklistVendors (system software developers) are making use

of the guidelines and checklistof the guidelines and checklistMore info: go to www.suretycanada.com and click on

E-Bonding

Last Word…SAC is “your bonding resource”SAC is your bonding resourceWe are available to consult with you and your

organization on matters of risk managementg gSAC can tailor a presentation for your organization

– don’t hesitate to ask More info: go to www.suretycanada.comLots of information and resources available

including on line tutorials that can be completed byincluding on-line tutorials that can be completed by you or others in your organizationClick on Resource – then Educate – then SuretyClick on Resource then Educate then Surety

Learning Centre for the tutorials

Contact UsContact UsPhone: 403-612-4-70

email: [email protected] @ y

or visit our www.suretycanada.comywebsite: