Embed Size (px)

Citation preview

Supporting Older

People Conference

SP6: Private Rented Sector –

an opportunity or a risk too far?

Speakers: Dominic Martin

PRS Taskforce, Communities and Local Government

Jack Stephen

Finance Director and Deputy Chief Executive, Thames Valley Housing Association Chair: Robert Kerse

Executive Director of Finance, Circle Housing

The New Investor / Institutional

Private Rented Sector

Dominic Martin MRICS

PRS Taskforce

81

PRS Context: Understand the growing role of

PRS in the housing market and hear first-hand

how a housing association has successfully

diversified into the market

Location/Property Strategies: Discover

strategies for market, location, customer and

property type and design

Schemes: Hear about schemes that have been

developed and their typical characteristics

Identify how to protect your social housing

assets

Funding Initiatives & Op Costs: Find out

about funding initiatives and how to keep

operating costs down

Corporate Structures: Learn how to structure

the commercial corporate structure to make it

attractive to investors

To Cover

PRS / B2R

From a private

sector market

perspective

But

Relevance for

the HA

audience

Agenda

1. Market Activity / Context

2. Government Overview / Initiatives

3. Why Now

4. Investment Considerations

5. Management & Tenant Considerations

Appendices: Government Funding Initiatives

NPPF Planning Guidance

Valuation

Rental Premiums

Amenities – Importance vs Pay More Rent

Development Considerations

82

Market Context /

Activity

83

84

Market Context / Activity

Excluding Private Placement & Bond Issues

Transaction Type Example Location

Frwd Commitment to Purchase Macquarie: Fizzy Living / Thames Valley London/M25

Frwd Commitment to Purchase Notting Hill Group London

Frwd Commitment to Purchase APG: Delancey London

Frwd Commitment to Purchase L&Q & Bellway London

Joint Venture Grainger & Bouygues Barking

Joint Venture Sigma Barking Riverside

Joint Venture Amcorp Properties: Native Land, Grosvenor London

Joint Venture L&Q & Barratts London

Long-dated Income M&G: Popula HARCA & Be:Here Now London

Long-dated Income Aviva: Derwent Living Regions

Site Acquisition Qatari Diar: Delancey (East Village) London

Site Acquisition ADIA: Fizzy Living / Thames Valley tbc

Site Acquisition Gatehouse: Sigma Manchester / Liverpool

Site Acquisition Washington State Pension Board: Essential Living London

BTR1 R1 & R2 London,South East, Manc'ster

Not primarily the volume housebuilders

Developers: Dev Sec, Lend Lease, Grosvenor, Quintain, Delancey

Investors: Direct let; international investors!

Structures: Joint ventures, partnerships & corporate vehicles

85

The New PRS: What Does it Look Like

Wholesale not Retail: preferably c.£20m say

Commercial Product : Income driven; like a shopping centre or a

multi tenanted office. Valued as Investment (ie NOI * cap rate).

Professionally Managed

85

BUT

Physically can be low rise, medium rise or high rise

Urban or suburban

Pools / Concierge Not Obligatory

Low Rise Suburbia Low Rise Urban High Rise - Urban

Business Centre Roof Terrace ATM Cinema Room Concierge Shared Space Pool/Gym

86

NEW / RECENT HISTORIC

Skyline Central (130 units)

Manchester

Dolphin Square (1,200 units)

Pimlico, London

East Village (1,500 units)

Stratford, London

Hamlet Gardens (150 units)

Hammersmith, London

Halo (400 units)

Stratford, London

Genesis & M&G

Sales & Leaseback

Waverley Court (90 units )

Horsham

Fizzy Living (120 units)

Canning Town, London

Off-Plan Purchase

Viney Court (16 units)

Clapham, London

Market Context / Activity

Exists Already

Not ‘specifically designed’ as rental

HA

HA

Construction Costs (Height / Region - ECH)

Rents (Annual / Region - Hometrack)

Development Viability – National Context

End Value vs

Delivery Costs

GDV: £20m + GDV: £10m

Invest Unit

ValUnits

Unit Area

(sqft)£psf

Invest Unit

ValUnits

Unit Area

(sqft)£psf

£100,000 200 700 £143 £100,000 100 700 £143

£125,000 160 700 £179 £125,000 80 700 £179

£150,000 133 700 £214 £150,000 67 700 £214

£175,000 114 700 £250 £175,000 57 700 £250

£200,000 100 700 £286 £200,000 50 700 £286

£225,000 89 700 £321 £225,000 44 700 £321

88

Market Context / Activity

Investors: Min Lot Size vs Units??

Why Now

89

Barriers vs Favourable Conditions

Favourable Conditions: conditions for institutional investment in large scale developments more favourable than they have been in the past:

• Strong rental demand and good long term prospects

• Returns vs commercial property / low volatility (IPD)

• Tax changes (SDLT)

• Emerging models helping establish the concept & developing expertise

• Government support

Remaining barriers/concerns?: these include:

• Scale

• Management platforms & quality of teams to

underpin returns

• Rental returns / rental growth prospects (lack of

data)

• Planning system

• Government regulation “We are at a tipping point [in the PRS]. The journey from niche to mainstream is

just beginning.”

Martin Moore, Chairman PRUPIM – 16th April 2013

“It depends on the planning environment…but…it’s our…intention to have a much bigger role in the private

rented accommodation market”

Nigel Wilson – Chief Executive – Legal and General – 14th August 2013

91

Demand is Growing: PRS houses

3.8 million households in England,

compared to 2 million in the early

‘80s. Greater than AH housing stock

Small Landlords: Much of the

growth in the rented sector has

been driven by individual landlords.

Where 10% all stock, LL’s with 4 or

less properties

Institutional Ownership – Other

Countries: Contrast to international

comparators where institutional

ownership is more prevalent

(US@13%, Dutch @ 37%.

Germany @ 17%) .

Context

92

Favourable Conditions: Construction &

Returns of UK Resi Property

...versus other asset classes

6.6

3.2

6.6

10.1

0

2

4

6

8

10

12

All property

index

Equities Gilts Residential

Market Lets

Annualised total return

0

50

100

150

200

250

300

350

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

2023

Permanent dwellings completed (thousands)

Projected new household formation (thousands)

Source: IPD Residential Index 2012 (last 12yrs)

Source: Hometrack Source: DCLG

Government

93

94

Government Initiatives: Overview

Recognition of Tenure: x 4 Housing Tenures: Private

ownership, shared ownership, social/affordable rents and

market rent (PRS)

Sir Adrian Montague review (summer 2012): Taskforce

and two Government funding schemes: Build to Rent Fund

and Long Term Debt Guarantees

National Planning Policy - Specific Recognition: PRS to

taken account of within the assessment of Housing Need,

and LPAs to understand that viability drivers are different

than housing for sale

Developers / Land

Owners

&

Investors / Banks

95

Government Initiatives: PRS Taskforce

Stakeholders

Government

Land Owners/Developers

Investors/Funders (inc Banks)

Local Authorities

Contractors

Consultants / Agents

Taskforce Role

Support Government Initiatives: Build to Rent & Debt Guarantee

Supply & Demand: Land & Investors

Standards: Management / Valuation

Legacy: Research & Design

Valuation

Design

Planning Data /

Research

Management / Lettings

Investment

Considerations

96

97

Investment Considerations

GVA Data – Top 10 (Gross Value Added) 1997 to 2011 2008 to 2011

Rank Location Growth Region Rank Location Growth Region

1 Inner London - East 160% London 1 Bedford 26% East

2 Inner London - West 110% London 2 West Cumbria 22% North West

3 Bath and North East Somerset, North Somerset and South Gloucestershire108% South West 3 Oxfordshire 18% South East

4 Oxfordshire 106% South East 4 East Derbyshire 17% East Midlands

5 Milton Keynes 105% South East 5 Inner London - East 16% London

6 Cambridgeshire CC 103% East 6 Bath and North East Somerset, North Somerset and South Gloucestershire16% South West

7 Berkshire 99% South East 7 Sandwell 15% West Midlands

8 Surrey 96% South East 8 Central Bedfordshire 14% East

9 Cornwall and Isles of Scilly 95% South West 9 Cambridgeshire CC 13% East

10 Hampshire CC 93% South East 10 Berkshire 13% South East

Region Count Region Count

East 1 East 3

East Midlands 0 East Midlands 1

London 2 London 1

North East 0 North East 0

North West 0 North West 1

South East 5 South East 2

South West 2 South West 1

West Midlands 0 West Midlands 1

Yorkshire & The Humber 0 Yorkshire & The Humber 0

East / Midlands

Income certainty…

Job market / Where is the Growth

98

Demographic Trends (8 ‘Core Cities’)

Pop

%

change

since Living in PRS

Location 2011 % 2001 2001 2011 % in 2011

%

change Location 16-24 25-34 16-24 25-34

Manchester 503,127 28.1 26,885 58,170 28.4 116 Manchester 65 114 6,598 19,757

Birmingham 1,073,045 9.8 34,508 73,405 17.9 113 Liverpool 71 90 4,065 13,006

Bristol 428,234 12.5 21,711 43,028 23.5 98 Birmingham 42 64 9,800 30,994

Liverpool 466,415 6.1 24,604 48,290 23.4 96 Bristol 40 64 5,829 21,823

Sheffield 552,698 7.7 18,544 35,760 15.6 93 Sheffield 50 62 5,206 17,133

Leeds 751,485 5.0 30,599 57,456 17.9 88 Leeds 35 61 9,318 28,749

Nottingham UA 305,680 14.5 16,307 29,098 23.1 78 Newcastle 54 47 3,525 10,862

Newcastle 280,177 7.9 13,466 22,318 19.1 66 Nottingham UA 10 44 3,979 10,470

% Change in

employed with

high level

qualifications

2001 Employed

with

high level

qualifications

98

Manchester: PRS up by 116% + High Level Qual up by 114%

Liverpool: PRS up by 96% + High Level Qual up by 90%

Living In PRS Employed with High Level Qual

CLG / ONS CLG / ONS

Investment Considerations

99

Investment Considerations

Affordability

Savills – Jacqui Daly (020 7016 3779 / [email protected])

Affordability & Culture of Sharing:

- Particular to cities / local markets

- Will influence mix of units

- Eye on:

- Initial Let-up

- Long term: limiting void

turnaround

- Long term; matching long-term

demographic changes

Management &

Tenants

100

Management & Tenants

101

Front of house:

gross rents

Back office

operation efficiency:

net rent

Do it yourself Buy in some

services X 2 Options:

X 2 Perspectives:

102

Estate Management

(Freeholder) Property / Unit

Management function

Unit Letting

Function

Estate Manager

Estate Management teams

(common parts repair &

maintenance; full time or

shared teams across

buildings)

Front of house/concierge

Data analysis and asset

management reporting

Property management team

Arrangement and scheduling of

emergency and routine repairs

and maintenance from initial

instruction to final payment

Voids repairs/refurbishment

Rent collection/credit control

General customer liaison

Emergency helpline service

Record keeping and reporting

Marketing / Tenant find

Viewing / Offer

Negotiating and agreeing

terms of AST

Reference / Credit check

Check in / check out

Inventories

Tenancy deposit liaison

Handover/intro to Property

Manager

Management & Tenants

UK Current – Property Functions: x 3

UK Future – Property Functions: x 1

103

Management & Tenants

Gross to Net Rental Attrition

With Sinking Fund

Void 2.50% 2.50% 5.00%

Bad Debt 2.50% 2.50% 5.00%

Management & Letting Costs 7.00% 10.00% 13.00%

Repairs and Maitenance 8.00% 10.00% 12.00%

Sinking Fund 2.50% 2.50% 5.00%

Sub-total 22.50% 27.50% 40.00%

Running Cost Range: 22.5% to 40.0%

Functions:Types: Strategy:

Estate Management Internal

Property Management Externalise

or

Lettings Combination

MFH Operation

What Tenants Want

Savills Tenant Survey (Oct 2013)

104

Savills – Susan Emmett (0203 107 5460/ [email protected])

105

QUESTIONS

106

• Up to £1bn commercial development finance at rates lower than would normally be available in the market

• Large-scale, professionally managed institutional quality rental homes

• Round 1. 2 deals contracted. Further 19 in pipeline.

•c£300m. Nearly 4000 units. Across England.

• Round 2. c£700m available. £2.7bn of bids. 36,000 units. Weighted to London, South East and Manchester

•Shortlisting by end February/DD commencing March 2014.

• Up to £6.5bn of direct debt guarantees to support long term ownership – 30 years

• Enable owners to borrow at a lower rate than might otherwise be possible • Min project size £10m (can be more than one site)

• Maximum loan/equity: 80:20

• Maximum rent/interest cover net – 1.2:1

• Probable dual approach – direct and indirect • First direct proposal received

Build to Rent Fund PRS Debt Guarantee Scheme

Government Initiatives: B2R Fund & Debt

Guarantee

107

PRS & Local Housing Strategies:

“Plan makers should look at the household types, tenure and size in the

current stock and in recent supply, and assess whether continuation of

these trends would meet future needs.”

Text thereafter follows in respect of PRS.

PRS & Viability:

“The viability of individual development types, both commercial and

residential, should be considered. Relevant factors will vary from one land

use type to another. For residential schemes, viability will vary with

housing type. For example, in respect of developments of multiple units

held in single ownership as private rented sector housing intended for long

term rental, viability considerations in decision-taking should take account

of the economics of such schemes, which will differ from build for sale.

This may require a different approach to planning obligations or an

adjustment of policy requirements.”

NPPF Planning Guidance

Planning Viability

108

Viability Negotiations / Local Requirements

Birmingham City Council & Evenbrook (2010)

RBKC & Grainger (2013)

City of Westminster & Mercers (2014)

LB Brent & Wembley City (2014)

Manchester City Council (ongoing)

LB Ealing (ongoing)

LLDC & Sweetwater & Eastwick (ongoing)

Planning Viability

- Every LA / Needs Are Different

- Negotiation therefore specific to those needs (no right or

wrong approach)

Examples

109

- Scale: 20 units vs 50 vs 100 vs 200 vs 300+

- Housing Type: apartments vs houses

- Local Market: Break up potential, tbc on demand for units for

sale and stock in question vs local market competition

Considerations:

- Net Operating Income

- Discount Vacant Possession Value (Open Market)

Approach:

Development Viability

Valuation

Development Viability

Notes:

Analysis of selected new build schemes in

mid-market inner London locations

Evidence of a new build rental premium but

driven by a variety of factors. 110

10%-15%

Premium Therefore:

1.New build proven @ c.10% to 15%

2.Service @ c.?

Target Rent But New Build Rental Premium?

Hometrack – Richard Donnell (0845 013 2360 / [email protected])

What Tenants Want

Savills Tenant Survey (Oct 2013)

111

Savills – Susan Emmett (0203 107 5460/ [email protected])

Development Considerations

I) Development Viability:

- Construction Costs

- Floor Areas & Efficiency*

- Rent Premiums

II) Investment Viability:

- Job Market / Growing Local Economy

- Running Costs / Gross 2 Net Attrition (front and back of house)

III) Planning & Local Authorities:

- Local Authorities – What are the Benefits / Concerns

- Flexible Negotiation (S106 / CIL / AH) & Covenant / Clawback

IV) What Tenants Want (Savills)*:

- Longer Leases Or Not

- Amenities or Not

V) Local Market Dynamics:

- Demographic trends / sharers or not

- Competition (amenities / quality / specification)

- Rental Growth Projections*

- Unit mix (local agents – shortage of stock) 112

PRIVATE RENTED SECTOR: AN OPPORTUNITY OR A RISK TOO FAR?

19 March 2014 Jack Stephen

Finance Director Thames Valley Housing

▸ Thames Valley Housing (TVH) is a Registered Provider.

▸ TVH owns and manages a portfolio of 14,500 properties valued at over £1.3bn across the rented, shared ownership, student and key worker sectors.

▸ Portfolio predominantly located in London, Berkshire, Surrey, Hampshire and Oxfordshire.

▸ Company has grown organically, developing its own stock using in-house development capabilities.

TVH Housing Stock Growth (No. of Dwellings) TVH Housing Tenure By Type

Overview

WHO ARE TVH?

7,646

10,415 10,521 11,057 13,037

14,077 14,663 14,639

2005 2006 2007 2008 2009 2010 2011 2012

36.0%

27.0%

16.0%

11.0%

7.0% 3.0% Social rented

SharedownershipKey worker loans

Key worker NHS

Leaseholder

Studentaccommodation

TVH INVOLVEMENT IN FIZZY LIVING

▸ TVH is a housing business with a social purpose.

▸ A longstanding element of its strategy is to invest in commercial and market based ventures to generate surpluses to invest back into its affordable housing.

▸ In 2009, it was becoming increasingly apparent to TVH that there was a need for a form of housing to bridge the gap between the owner-occupied and social housing sectors.

▸ With social housing grants declining and deposit requirements increasing, the number of tenants looking for an alternative accommodation model was rapidly increasing.

▸ TVH saw an opportunity to leverage its existing expertise and in-house capabilities through the establishment of Fizzy Living, and generate profits that could be repatriated to the group.

Background

FIZZY LIVING BACKGROUND

▸ Strategy is to capitalise on increasing demand for high quality, well managed private rented residential accommodation and create market leading platform of institutional scale.

▸ Target market is “Rentysomethings”, an increasingly large section of the population either priced out of home ownership or with no desire to own.

▸ Tenant service offering in the UK is notoriously poor, providing significant opportunity for specialist platform.

▸ Assets will be newly built, offering at least 40 units per scheme.

▸ Located in key Greater London and South East commuter locations.

THE INVESTMENT TO DATE

▸ The business of Fizzy Living is the acquisition, management and eventual disposal of a portfolio of branded, new build apartment blocks for private rental.

▸ TVH has invested its own equity into Fizzy to commit to the acquisition of four assets with a gross asset value of £64.8m. The acquisitions have been supported by debt financing from Macquarie Capital.

▸ TVH recently sold down a portion of its interest in Fizzy to a subsidiary of Abu Dhabi Investment Authority, Silver Arrow. ADIA has committed a significant amount of capital to grow the Fizzy platform and the venture is currently reviewing numerous pipeline acquisitions in and around Greater London.

▸ As at the end of February 2014, four buildings have been acquired, the two earliest acquisitions are now fully let.

▸ 3 sites in East London:

▸ Canning Town (75 flats) – completed September 2012.

▸ Poplar (45 flats) – completed February 2014.

▸ Stepney Green (63 flats) – completed February 2014.

▸ One South West of Central London:

▸ Epsom (63 flats) – completed March 2013.

Epsom Stepney Green Canning Town Poplar

FIZZY LIVING – EXISTING PORTFOLIO

Site and Building Criteria

▸ Freehold / Leasehold (> 99 years).

▸ No more than 25% by value outside M25.

▸ Maximum 40 minutes commute to City of London, West End or Canary Wharf and commuter hotspots outside the M25.

▸ Within 10 minutes’ walk from rail and/or tube stations.

▸ Minimum average space requirements of:

▸ 1 bed 500 sq ft / 2 bed 800 sq ft / 3 bed 1,000 sq ft

Stepney Green Canning Town Canning Town

FUTURE ACQUISITIONS – SITE AND BUILDING CRITERIA

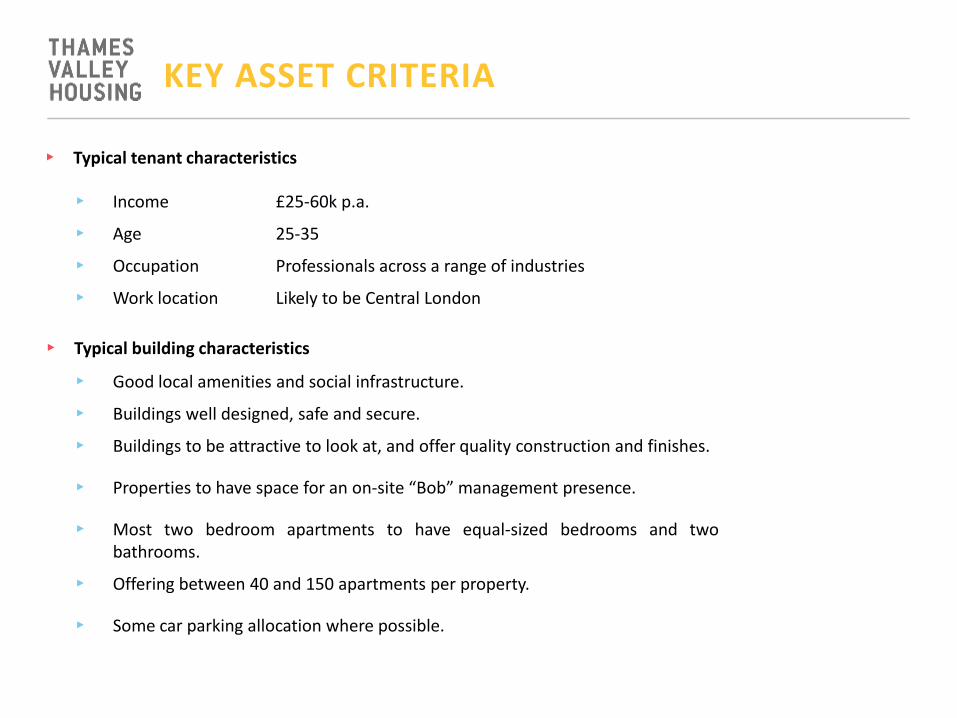

▸ Income £25-60k p.a.

▸ Age 25-35

▸ Occupation Professionals across a range of industries

▸ Work location Likely to be Central London

▸ Good local amenities and social infrastructure.

▸ Buildings well designed, safe and secure.

▸ Buildings to be attractive to look at, and offer quality construction and finishes.

▸ Properties to have space for an on-site “Bob” management presence.

▸ Most two bedroom apartments to have equal-sized bedrooms and two bathrooms.

▸ Offering between 40 and 150 apartments per property.

▸ Some car parking allocation where possible.

▸ Typical tenant characteristics

▸ Typical building characteristics

KEY ASSET CRITERIA

FUTURE FUNDING

▸ Fizzy believes it offers a unique product in the market, thinking about renting in a fresh and exciting way:

▸ Fizzy was voted “Newcomer of the Year” in the RESI Awards 2013.

▸ As a well funded and energetic company, Fizzy has ambitions in the Greater London PRS market.

▸ With an exciting pipeline of schemes, Fizzy is looking to create strong relationships with lenders who will help fund the expansion of the portfolio.

▸ £200+m of equity to be invested over the next three years.

▸ £200m of external debt is being sourced.

▸ Total investment in four years to be £500m.

VALUE GENERATED BY FIZZY LIVING MODEL

▸ Source: MacCap estimates. Assumes gross yield of 6%.

▸ 1. Assumes Fizzy benefits from 15% developer’s profit above typical forward-purchase price.

Advantage Benefit Indicative impact on NOI

yield

Direct tenant sourcing Agents typically charge 5-7.5% of year 1 rent as a fee for sourcing tenants.

Economies of scale Fizzy leverages TVH scale economies.

Identifiable brand and service offering

Aids retention of tenants and reduces churn, refurbishment spend and void costs. Reduces new building lease-up period.

Development capabilities Benefit from developers’ margin and also design buildings offering maximum operational efficiency.

50-100bps

75-100bps1

▸ Target gross to net rent loss of less than 25%.

0

10,000

20,000

30,000

40,000

50,000

60,000

1991 1994 1997 2000 2003 2006 2009 2012 2015 2018

Strong demand: GOV.UK forecasts an additional 265,000 households over next 5 years in London

2,900

3,100

3,300

3,500

3,700

3,900

2011 2016 2021

'00

0s

Household Projections, London

8.1% 5yr growth

7.3% 5yr growth

The government figures also showed a widening gap between demand and supply in London

▸ Between 2011 and 2021, GOV.UK forecasts that there will be demand for an extra 52,579 units each year in London.

▸ Over the same period, only 27,240 units are forecasted to be completed per year.

▸ This housing shortage relative to household growth will continue to increase the upward pressure on house prices in the capital.

▸ The younger generations therefore find it harder and harder to purchase in London.

▸ First time buyer deposit requirement averages 170% of annual earnings.

▸ Average age of first time buyer now 38 years old1.

LONDON RESIDENTIAL RENTAL MARKET

1. Money Supermarket survey.

Source: Macquarie Capital, GOV.UK, NHCB, GLA.

Household growth

Dwellings completed

Oversupply

Undersupply

GOV.UK (f)

An

nu

al in

crea

se

0%

10%

20%

30%

40%

50%

60%

70%

1991 1994 1997 2000 2003 2006 2009 2012

▸ There is an established trend away from owner occupation and towards private renting:

▸ Home ownership increasingly unaffordable.

▸ Constrained mortgage availability and high deposit requirements expected to continue in medium term.

▸ Social and economic mobility trends causing home ownership to be less attractive for younger generations.

▸ PRS is therefore becoming increasingly popular, with the UK sector now housing 3.6m households compared to just 2m in early-1980s.

Over past 10 years in London, PRS grown 6.6% annually, while % owner occupied and social housing has declined

Owner Occupied

Social Housing

PRS

PRS – 6.6% 10yr CAGR

LONDON PRS MARKET

▸ The UK PRS sector now houses 3.6m h/holds compared to 2m in early-1980s.

▸ In London, % of owner-occupier stock has declined swiftly to 50%.

PRS EXPANDING, BUT NEW SUPPLY STILL SUBDUED

▸ Source: Macquarie Capital, ONS, Bloomberg, NAHB.

45%

50%

55%

60%

1991 1994 1997 2000 2003 2006 2009 2012

London: Owner-occupied As % Total Housing Stock

50%

59%

▸ 20 years ago, 30% of London tenants rented from PRS.

▸ Now increased to 53% and expected to rise further.

PRS EXPANDING, BUT NEW SUPPLY STILL SUBDUED

▸ Source: Macquarie Capital, ONS, Bloomberg, NAHB.

20%

30%

40%

50%

60%

70%

1991 1994 1997 2000 2003 2006 2009 2012

London Rented Housing Stock: Landlord

Public: Local Authorities, Housing Associations

Rented Privately

53%

30%

▸ High Gen Y population numbers support continued rental demand – a similar pattern to the US with multifamily the strongest investment sector.

GROWTH AND DEMOGRAPHIC DRIVERS

▸ Source: Macquarie Capital, IMF, ONS, UK Census.

250

500

750

1000

01020304050607080

'00

0s

Age (years)

UK Population By Age (2012)

Baby Boomers

Gen X Upgraders Gen Y Renter demographic

GROWTH AND DEMOGRAPHIC DRIVERS

▸ Source: Macquarie Capital, IMF, ONS, UK Census.

0%

2%

4%

6%

8%

10%

12%

0-4

5-9

10

-14

15

-19

20

-24

25

-29

30

-34

35

-39

40

-44

45

-49

50

-59

55

-59

60

-64

65

-69

70

-74

75

-79

80

+

Renter demographic

London

UK ex. London

% of Persons By 5 Year Age Group: 2011 Census

Years

▸ Recently released Census data shows the strong renter demographic profile is particularly pronounced in London.

▸ Source: Macquarie Capital, IMF, ONS, UK Census.

0%

10%

20%

30%

40%

1 person 2 person 3 person 4 person 5 person

London Households At 2011 Census, % Of Total

GROWTH AND DEMOGRAPHIC DRIVERS

▸ In line with demographic trends, 60% of London households comprise 1 or 2 persons – the smaller household size trend is expected to continue.

560

600

640

680

720

760

30%

35%

40%

45%

50%

2004 2005 2006 2007 2008 2009 2010 2011 2012

%16-64yrs with NVQ4+ education: London

£pw

Av. weekly earnings London (RHS)

PRIVATE RENTED SECTOR DEMAND DRIVERS

▸ Source: Macquarie Capital, ONS, BoE.

▸ Increase in persons higher education qualification underpins wages growth (+4.3% in 2012) and demand for modern rental housing in London.

▸ Source: Macquarie Capital, ONS, BoE.

5%

10%

15%

20%

25%

30%

1990 1993 1996 1999 2002 2005 2008 2011

UK first time buyers deposit as % of house price

28%

10%

PRIVATE RENTED SECTOR DEMAND DRIVERS

▸ Gen Y’s are finding it difficult to purchase in London where the first time buyer deposit requirement averages 170% of annual earnings.

▸ London residential has outperformed commercial real estate, equities and gilts over 10, 20 and 30 year time horizons (source: Knight Frank).

POTENTIAL FOR INSTITUTIONAL AND REIT INVESTMENT

▸ Source: Macquarie Capital, IPD, BoE, Knight Frank, RCA.

11.4%

10.0%

14.4%

7.3% 7.0%

9.9%

0.9%

8.0%

9.1%

5.7%

8.5%

10.7%

0%

5%

10%

15%

10 years 20 years 30 years

London Residential IPD Commercial Equities Gilts

Total Returns % p.a.

Commercial Real Estate

▸ UK residential property has outperformed other major asset classes.

▸ Delivered more attractive and less volatile returns over a long term.

POTENTIAL FOR INSTITUTIONAL AND REIT INVESTMENT

▸ Source: Macquarie Capital, IPD, BoE, Knight Frank, RCA.

Office

Industrial

Equities Gilts

Residential

7.0%

9.0%

11.0%

13.0%

15.0%

6.0% 8.0% 10.0% 12.0% 14.0% 16.0% 18.0%

Annualis

ed t

ota

l re

turn

Standard deviation

Annual Total Returns & Volatility (1991 to 2011)

2014 2015 2016 2017 2018 5 years to end 2018

Savills1 – London Mainstream 3.5% 3.5% 4.5% 6.0% 6.0% 25.8%

JLL2 – Greater London 2.0% 3.5% 3.5% 4.0% 3.0% 17.0%

Knight Frank3 – Prime Outer London

2.0% 3.0% 3.5% 3.8% 3.8% 17.2%

Hamptons4 – Greater London 3.5% 4.0% 4.0% 4.5% 5.0% 22.8%

▸ The high demand for PRS relative to the scarcity of supply is forecasted to result in high and stable levels of rental growth for Greater London’s private residential market.

PROJECTED RENTAL GROWTH - LONDON PRS

Source: Macquarie Capital, GOV.UK, ONS.

1. Savills Spotlight Prime Rental markets January 2014. 2. JLL Residential Eye, November 2013. 3. Knight Frank Residential Research Q4 2013. 4. Hamptons Housing Market

Forecasts Autumn 2013

— Tenancy agreements range from 6 months to 24 months, with the added peace of mind that the apartment will continue to be available for as long as they choose to stay.

— Each building has a dedicated on-site manager available to conduct viewings, and responsible for operations, security, and responsive repairs.

— Manager arranges and coordinates any specialist building/plumbing work and is a presence on site to sign for deliveries while tenants are away at work.

THE FIZZY LIVING EXPERIENCE

Superior service

Flexible lease terms

— Buildings are located within 10 minutes walk of public transport and provide on-site parking and bicycle storage.

— Focus on locations within 45 minutes work commute.

Excellent connectivity

— Upon moving in tenants can select from furniture package ranges, which they can pay for in monthly instalments to help spread out the costs of setting up home.

— All apartments come with high speed wireless broadband included in the rent.

— Tenants can communicate with building manager online at a time that suits them.

Stress free living

▸ By bringing an institutional approach to the private rental market we offer to our target market a considerably higher standard of management than they are accustomed to in this sector.

▸ The key features of the service offer to tenants is accessibility:

▸ Property managers (called “Bob”s) are accessible over the ‘phone and face-to-face 5 days a week. Bob’s days and hours of work vary to accommodate viewings and new lettings, so some days he/she may start late and finish late, and some weeks he/she may work Saturdays.

▸ Outside normal working hours, Fizzy provides an emergency response service. Non-emergency response will not necessarily be instant, but responding and providing a timescale for action within the following working day is a priority performance standard.

▸ The responsive repairs contractor will respond to emergency, out of hours repair phone calls. Again, follow-up action will be taken and communicated to the tenant within the following working day.

Epsom’s “Bob”

Poplar’s “Bob”

SERVICE OFFERING

▸ Innovative operational model

THE FIZZY LIVING ADVANTAGE

▸ Direct tenant sourcing model

▸ Media-led direct tenant acquisition strategy including web, facebook and twitter.

▸ Reduces ongoing operating costs by circumventing need for traditional letting agents.

▸ Builds direct tenant relationship.

▸ Marketing and branding strategy raises awareness and encourages loyalty.

▸ Quality and reliability of service offering encourages people to move within the buildings.

▸ Promotes word-of-mouth and online endorsement.

Fizzy targets the “Rentysomethings”! This demographic is professionals in the 25 - 35 age range, who would be first-time buyers if they were able to access mortgage finance or chose not to own their own home for simplicity and flexibility.

Strongly branded on to new tenants via website (www.fizzyliving.com) and social media (facebook and twitter).

The brand tone of voice is flexible and understanding. For example, Fizzy waives tenancy extension / renewal charges, and offers tenants the option to align annual rent review dates with their salary review dates.

BRANDING

FIZZY LIVING DEVELOPMENT CONCEPT

▸ Fizzy Living has been working with HTA Architects and EC Harris to design attractive and cost efficient schemes specifically for occupation by private renters.

▸ Although the initial portfolio comprises blocks that were built for owner occupation, these were carefully selected because they offer the characteristics that FizzyLiving considers important for a PRS building:

▸ Equal sized bedrooms, each with adequate storage.

▸ Versatile common areas, with sufficient space for entertaining friends.

▸ One bathroom per bedroom (not necessarily ensuite).

▸ Outside space, likely a balcony.

▸ Designs provide for optimal efficiency through innovative use of space, and are cost effective to reproduce given their modular nature.

▸ This cost efficiency translates to improved investment returns for Fizzy Living’s investors.

1 BEDROOM FLAT

LIVING SPACE

Living and dining space

separated just by

furniture, giving a flexible

and large open space.

KITCHEN

Easy to keep clean and

tidy with a place for

every gadget.

TERRACE

A substantial outdoor

terrace for entertaining or

relaxing with the papers.

BEDROOM

Enough space for a

home office or study,

fitted storage for all

your stuff and a big

bed. Sliding doors

separate bedroom

from living space for

privacy when your

friends stay over.

2 BEDROOM FLAT

BEDROOM

Enough space for a big

bed, a table to work at,

fitted storage, and an

exercise mat on the

floor.

LIVING SPACE

Separate dining,

cooking and

seating zones.

BATHROOM

Every bedroom has

a bathroom, for rest

and recuperation

TERRACE

A terrace, to catch

the sun and enjoy

the sound of the city

on an early summer

morning

LIVING ROOM

Sliding walls pull back to open up

the front of the flat to the city view,

and

to make a great flat for socialising.

TVH Silver Arrow

Fizzy Enterprises LLP

Fizzy One LLP

Fizzy

Canning

Town LLP

Fizzy

Epsom

LLP

Fizzy

Poplar LLP

Fizzy

Stepney

Green LLP

New

PropCos

Fizzy Services

Management LLP

Management Agreement

Se

cu

rity

Po

ol

FIZZY GROUP STRUCTURE

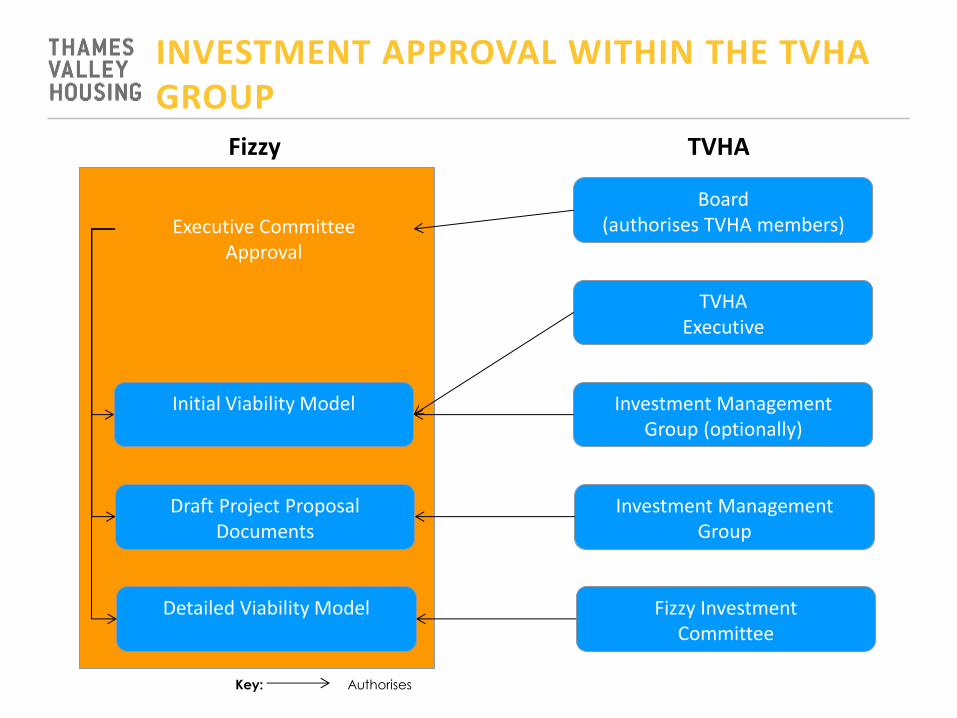

GOVERNANCE FOR FIZZY WITHIN THE TVHA GROUP

Fizzy Investment Committee (FIC)

Fizzy Enterprises LLP

Operational Management

TVHA Fizzy Holdings Limited

TVHA Board

Appoints Directors

Appoints its representative on Fizzy Enterprises LLP and provides representative with scheme of delegation for certain decisions. Other decisions will need to be referred back to FIC or to TVHA board.

Scheme of Delegation for day-today decisions.

Delegates authority to approve decisions in accordance with Fizzy Enterprises LLP’s Business Plan.

Delegates authority to approve decisions in accordance with TVHA Holdings Business Plan.

INVESTMENT APPROVAL WITHIN THE TVHA GROUP

Board (authorises TVHA members)

TVHA Executive

Investment Management Group (optionally)

Investment Management Group

Fizzy Investment Committee

TVHA

Executive Committee

Approval

Initial Viability Model

Draft Project Proposal Documents

Detailed Viability Model

Fizzy

Key: Authorises

Supporting Older

People Conference

SP6: Private Rented Sector –

an opportunity or a risk too far?

Speakers: Dominic Martin

PRS Taskforce, Communities and Local Government

Jack Stephen

Finance Director and Deputy Chief Executive, Thames Valley Housing Association Chair: Robert Kerse

Executive Director of Finance, Circle Housing

![WELCOME [leedsplayhouse.org.uk] · supporting creativity in schools PLAYHOUSE OLDER PEOPLE dynamic and pioneering projects with older adults and people living with dementia PLAYHOUSE](https://img.pdfslide.us/doc/110x75/5f031e5b7e708231d407a0e1/welcome-supporting-creativity-in-schools-playhouse-older-people-dynamic-and.jpg)