Embed Size (px)

Citation preview

SUPPLY, DEMAND, ENERGY AND LOCATION: THE FOUR PILLARS TO SUCCESS

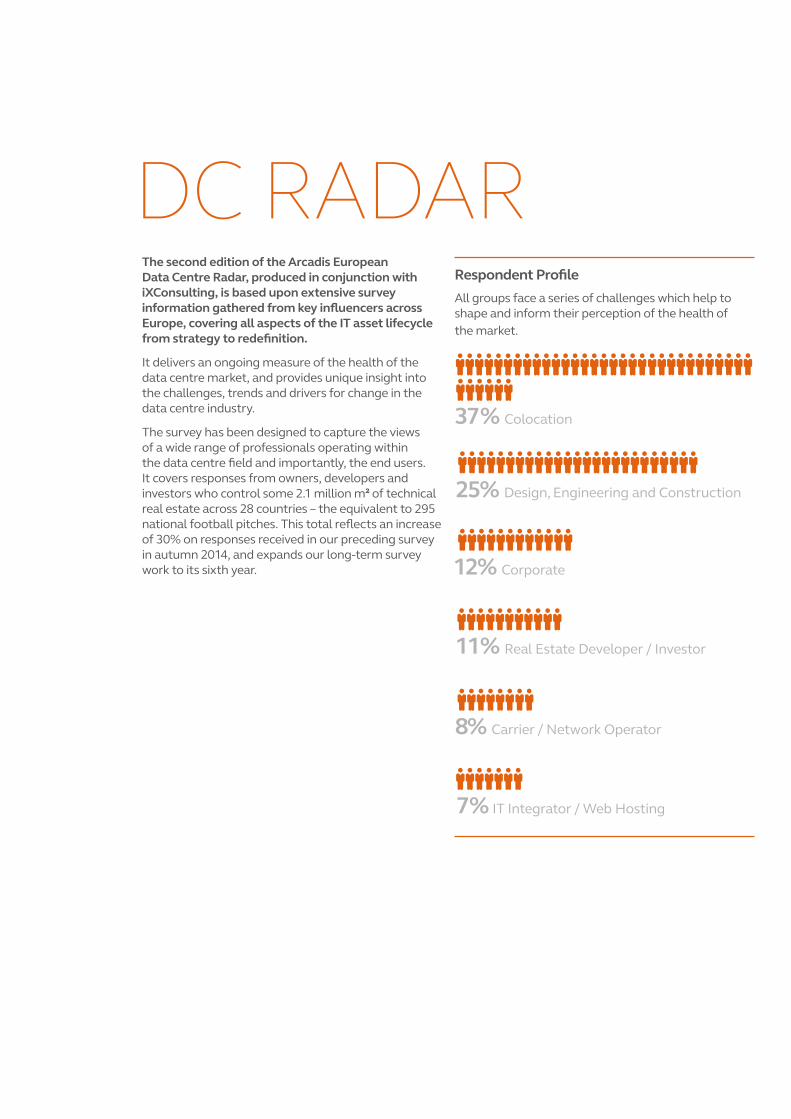

The second edition of the Arcadis European Data Centre Radar, produced in conjunction with iXConsulting, is based upon extensive survey information gathered from key influencers across Europe, covering all aspects of the IT asset lifecycle from strategy to redefinition.

It delivers an ongoing measure of the health of the data centre market, and provides unique insight into the challenges, trends and drivers for change in the data centre industry.

The survey has been designed to capture the views of a wide range of professionals operating within the data centre field and importantly, the end users. It covers responses from owners, developers and investors who control some 2.1 million m² of technical real estate across 28 countries – the equivalent to 295 national football pitches. This total reflects an increase of 30% on responses received in our preceding survey in autumn 2014, and expands our long-term survey work to its sixth year.

37% Colocation

25% Design, Engineering and Construction

8% Carrier / Network Operator

7% IT Integrator / Web Hosting

11% Real Estate Developer / Investor

12% Corporate

Respondent Profile All groups face a series of challenges which help to shape and inform their perception of the health of the market.

DC RADAR

Hungary

Serbia

Russia

Finland

Sweden

Norway

Iceland

UKIreland

PortugalSpain

FranceItaly

Germany

LuxembourgBelgium

Poland

Romania

Bulgaria

TurkeyGreece

Czech

AustriaSwitzerland

Slovakia

LatviaLithuania

Denmark

Netherlands

For this edition of DC Radar, we will be examining the responses and distilling the key trends emerging from the survey.

Following this, we will deliver a series of focussed insight garnered from the survey results that will have significant impact on our sector. These insights will be released later this year and will give you an in depth assessment of trends that will shape the future of how our industry develops.

The three major themes that will be developed are those of supply and demand, location and energy. Whilst these should come as no surprise as they have dominated the discussion points in data centre development over the past five years, we have discerned a subtle shift in emphasis and approach.

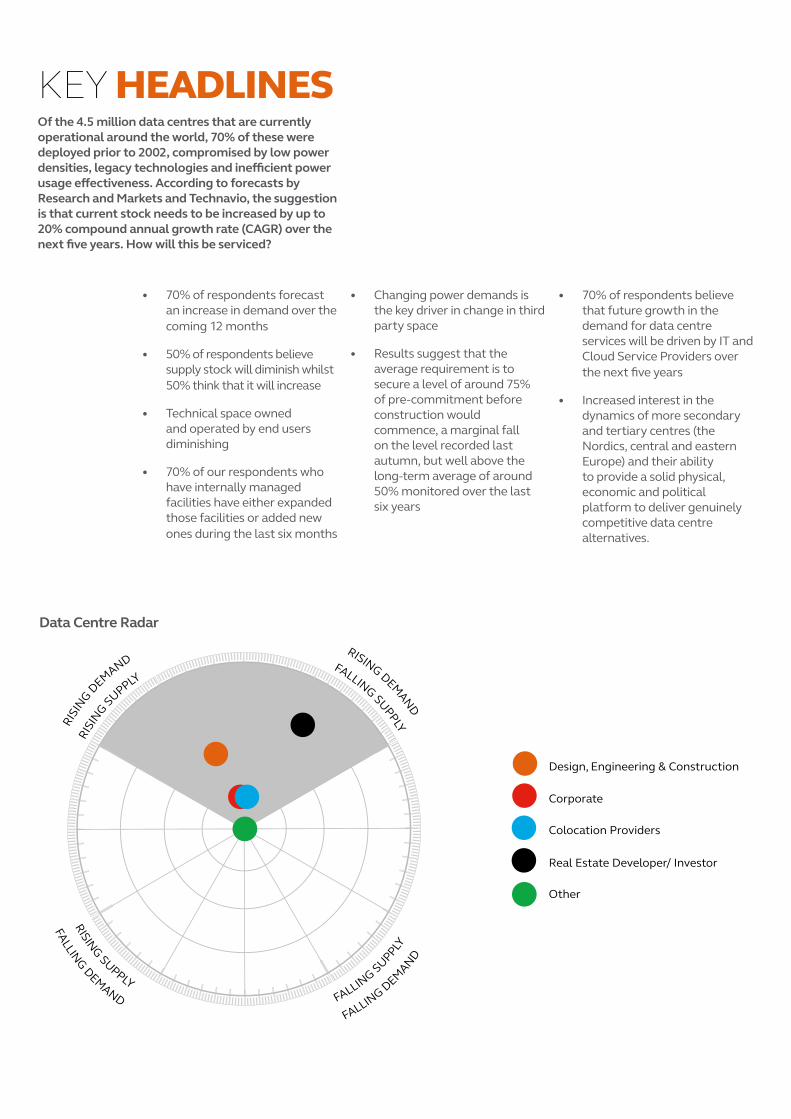

KEY HEADLINES

Of the 4.5 million data centres that are currently operational around the world, 70% of these were deployed prior to 2002, compromised by low power densities, legacy technologies and inefficient power usage effectiveness. According to forecasts by Research and Markets and Technavio, the suggestion is that current stock needs to be increased by up to 20% compound annual growth rate (CAGR) over the next five years. How will this be serviced?

• 70% of respondents forecast an increase in demand over the coming 12 months

• 50% of respondents believe supply stock will diminish whilst 50% think that it will increase

• Technical space owned and operated by end users diminishing

• 70% of our respondents who have internally managed facilities have either expanded those facilities or added new ones during the last six months

• Changing power demands is the key driver in change in third party space

• Results suggest that the average requirement is to secure a level of around 75% of pre-commitment before construction would commence, a marginal fall on the level recorded last autumn, but well above the long-term average of around 50% monitored over the last six years

• 70% of respondents believe that future growth in the demand for data centre services will be driven by IT and Cloud Service Providers over the next five years

• Increased interest in the dynamics of more secondary and tertiary centres (the Nordics, central and eastern Europe) and their ability to provide a solid physical, economic and political platform to deliver genuinely competitive data centre alternatives.

RISING DEMAND

FALLING SUPPLY RISI

NG D

EMAND

RISI

NG SUPPLY

FALLING DEMAND

RISING SUPPLY

FALLING DEMAND

FALLING SUPPLY

Other

Design, Engineering & Construction

Corporate

Colocation Providers

Real Estate Developer/ Investor

Data Centre Radar

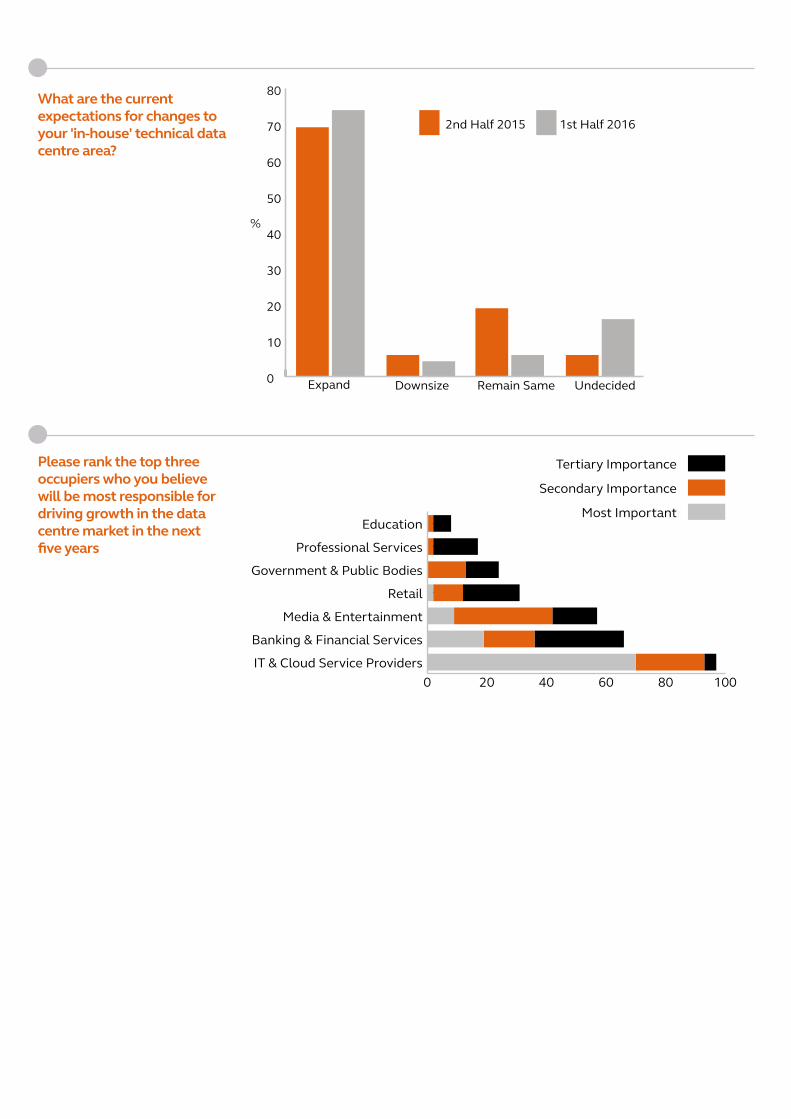

What are the current expectations for changes to your 'in-house' technical data centre area?

0

10

20

30

40

50

60

70

80

%

UndecidedRemain SameDownsizeExpand

1st Half 20162nd Half 2015

Please rank the top three occupiers who you believe will be most responsible for driving growth in the data centre market in the next five years

0 20 40 60 80 100

Tertiary Importance

Secondary Importance

Most Important

IT & Cloud Service Providers

Banking & Financial Services

Media & Entertainment

Retail

Government & Public Bodies

Professional Services

Education

THE FOUR PILLARS TO SUCCESS

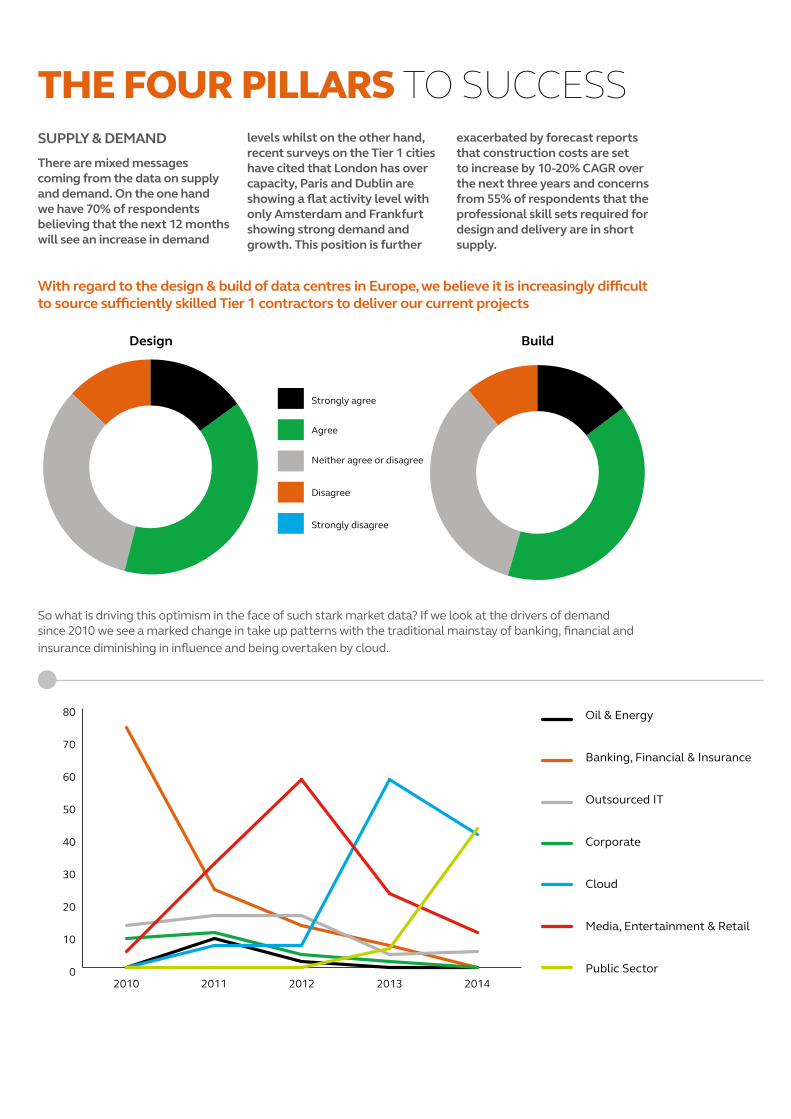

So what is driving this optimism in the face of such stark market data? If we look at the drivers of demand since 2010 we see a marked change in take up patterns with the traditional mainstay of banking, financial and insurance diminishing in influence and being overtaken by cloud.

0

10

20

30

40

50

60

70

80 Oil & Energy

Banking, Financial & Insurance

Outsourced IT

Corporate

Cloud

Media, Entertainment & Retail

Public Sector20142013201220112010

With regard to the design & build of data centres in Europe, we believe it is increasingly difficult to source sufficiently skilled Tier 1 contractors to deliver our current projects

Strongly disagree

Disagree

Neither agree or disagree

Agree

Strongly agree

Design Build

SUPPLY & DEMAND There are mixed messages coming from the data on supply and demand. On the one hand we have 70% of respondents believing that the next 12 months will see an increase in demand

levels whilst on the other hand, recent surveys on the Tier 1 cities have cited that London has over capacity, Paris and Dublin are showing a flat activity level with only Amsterdam and Frankfurt showing strong demand and growth. This position is further

exacerbated by forecast reports that construction costs are set to increase by 10-20% CAGR over the next three years and concerns from 55% of respondents that the professional skill sets required for design and delivery are in short supply.

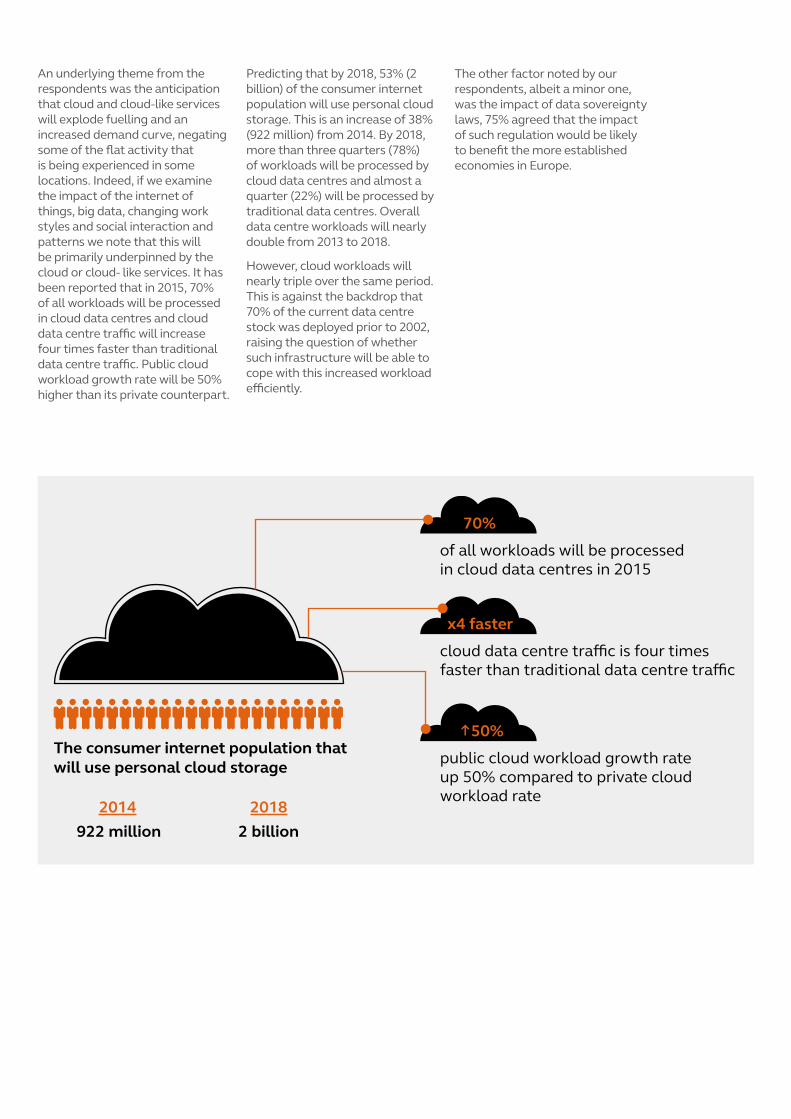

An underlying theme from the respondents was the anticipation that cloud and cloud-like services will explode fuelling and an increased demand curve, negating some of the flat activity that is being experienced in some locations. Indeed, if we examine the impact of the internet of things, big data, changing work styles and social interaction and patterns we note that this will be primarily underpinned by the cloud or cloud- like services. It has been reported that in 2015, 70% of all workloads will be processed in cloud data centres and cloud data centre traffic will increase four times faster than traditional data centre traffic. Public cloud workload growth rate will be 50% higher than its private counterpart.

Predicting that by 2018, 53% (2 billion) of the consumer internet population will use personal cloud storage. This is an increase of 38% (922 million) from 2014. By 2018, more than three quarters (78%) of workloads will be processed by cloud data centres and almost a quarter (22%) will be processed by traditional data centres. Overall data centre workloads will nearly double from 2013 to 2018.

However, cloud workloads will nearly triple over the same period. This is against the backdrop that 70% of the current data centre stock was deployed prior to 2002, raising the question of whether such infrastructure will be able to cope with this increased workload efficiently.

The other factor noted by our respondents, albeit a minor one, was the impact of data sovereignty laws, 75% agreed that the impact of such regulation would be likely to benefit the more established economies in Europe.

70%

of all workloads will be processed in cloud data centres in 2015

x4 faster

cloud data centre trac is four times faster than traditional data centre trac

↑50%

public cloud workload growth rateup 50% compared to private cloudworkload rate

2014 2018

The consumer internet population that will use personal cloud storage

922 million 2 billion

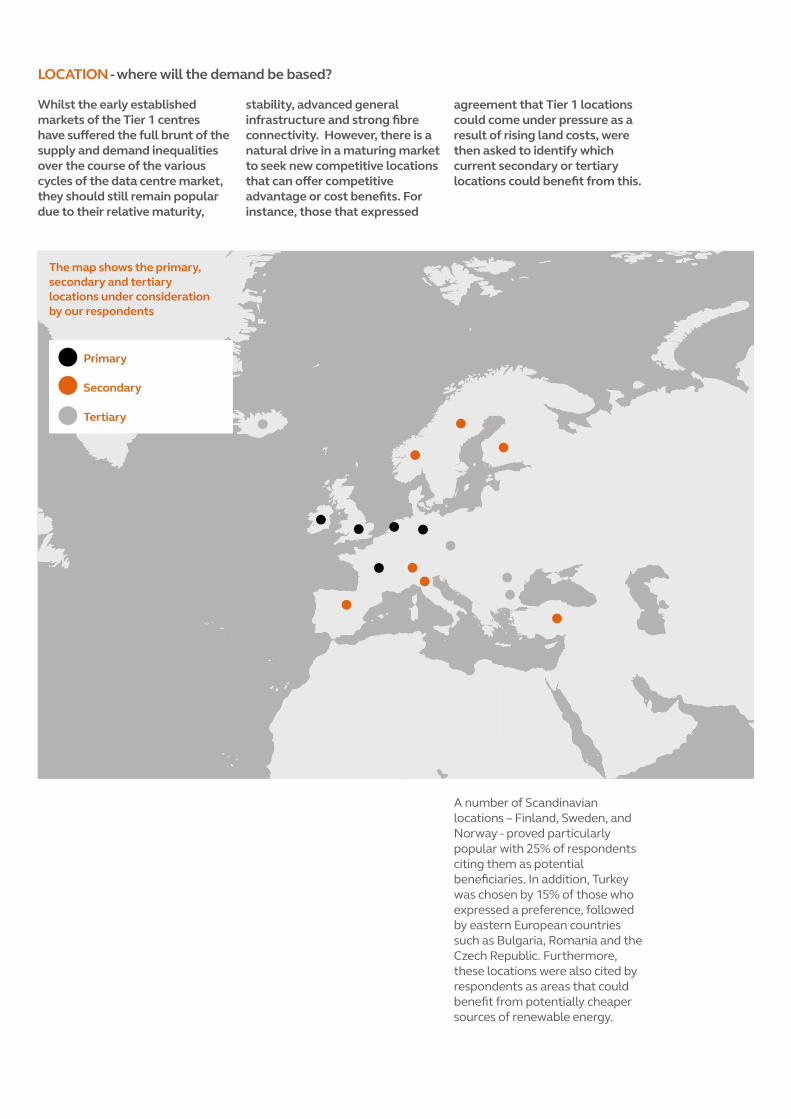

LOCATION - where will the demand be based?

The map shows the primary, secondary and tertiary locations under consideration by our respondents

Primary

Secondary

Tertiary

Whilst the early established markets of the Tier 1 centres have suffered the full brunt of the supply and demand inequalities over the course of the various cycles of the data centre market, they should still remain popular due to their relative maturity,

stability, advanced general infrastructure and strong fibre connectivity. However, there is a natural drive in a maturing market to seek new competitive locations that can offer competitive advantage or cost benefits. For instance, those that expressed

agreement that Tier 1 locations could come under pressure as a result of rising land costs, were then asked to identify which current secondary or tertiary locations could benefit from this.

A number of Scandinavian locations – Finland, Sweden, and Norway - proved particularly popular with 25% of respondents citing them as potential beneficiaries. In addition, Turkey was chosen by 15% of those who expressed a preference, followed by eastern European countries such as Bulgaria, Romania and the Czech Republic. Furthermore, these locations were also cited by respondents as areas that could benefit from potentially cheaper sources of renewable energy.

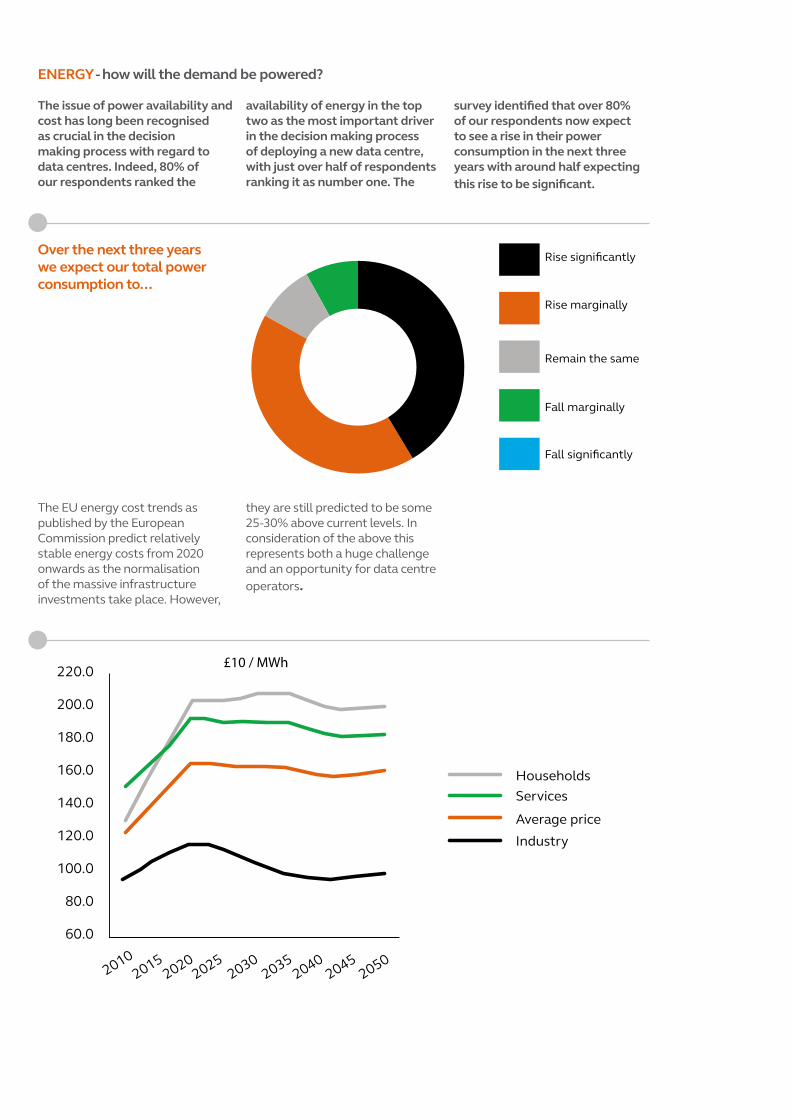

ENERGY - how will the demand be powered?

Over the next three years we expect our total power consumption to...

Fall significantly

Fall marginally

Remain the same

Rise marginally

Rise significantly

The EU energy cost trends as published by the European Commission predict relatively stable energy costs from 2020 onwards as the normalisation of the massive infrastructure investments take place. However,

they are still predicted to be some 25-30% above current levels. In consideration of the above this represents both a huge challenge and an opportunity for data centre operators.

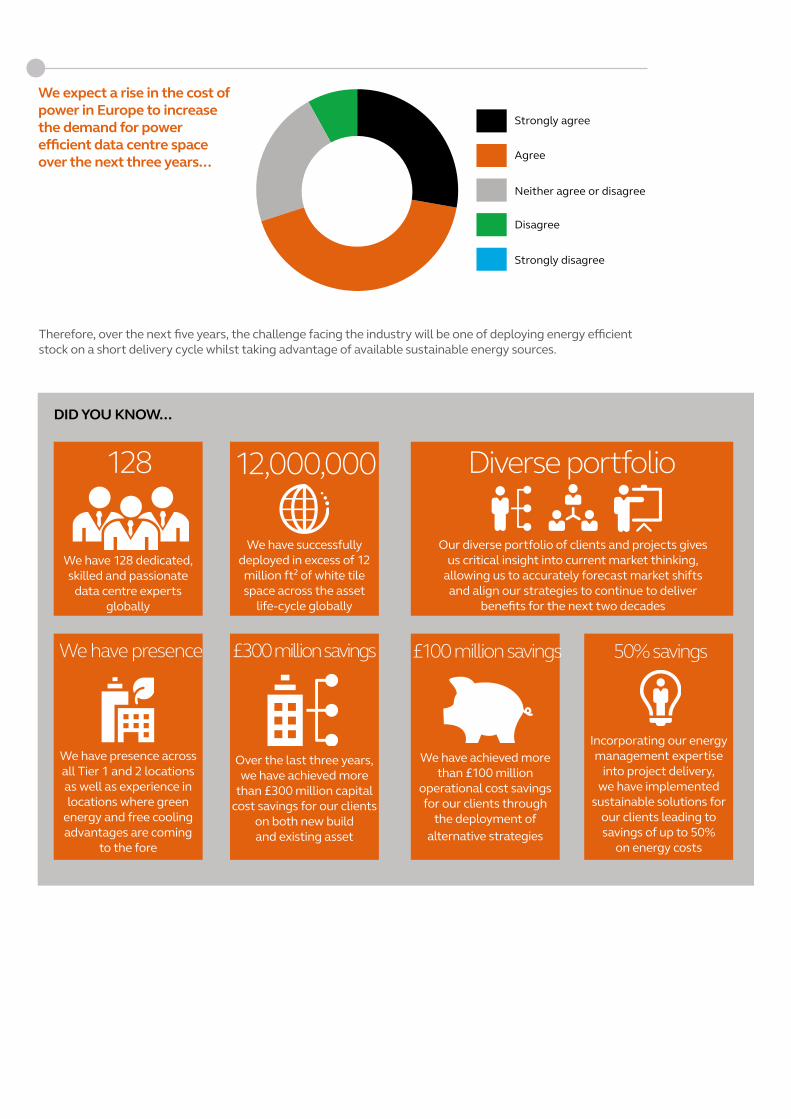

The issue of power availability and cost has long been recognised as crucial in the decision making process with regard to data centres. Indeed, 80% of our respondents ranked the

availability of energy in the top two as the most important driver in the decision making process of deploying a new data centre, with just over half of respondents ranking it as number one. The

survey identified that over 80% of our respondents now expect to see a rise in their power consumption in the next three years with around half expecting this rise to be significant.

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

Industry

Banking, Financial & Insurance

20102015

20202025

20302035

20402045

2050

Average price

ServicesHouseholds

£10 / MWh

Therefore, over the next five years, the challenge facing the industry will be one of deploying energy efficient stock on a short delivery cycle whilst taking advantage of available sustainable energy sources.

We expect a rise in the cost of power in Europe to increase the demand for power efficient data centre space over the next three years...

We have 128 dedicated, skilled and passionate

data centre experts globally

128

We have presence across all Tier 1 and 2 locations as well as experience in locations where green

energy and free cooling advantages are coming

to the fore

We have presence

Over the last three years, we have achieved more

than £300 million capital cost savings for our clients

on both new build and existing asset

£300 million savings

We have successfully deployed in excess of 12 million ft² of white tile space across the asset

life-cycle globally

12,000,000

We have achieved more than £100 million

operational cost savings for our clients through

the deployment of alternative strategies

£100 million savings

Incorporating our energy management expertise

into project delivery, we have implemented

sustainable solutions for our clients leading to savings of up to 50%

on energy costs

50% savings

Our diverse portfolio of clients and projects gives us critical insight into current market thinking,

allowing us to accurately forecast market shifts and align our strategies to continue to deliver

benefits for the next two decades

Diverse portfolio

Disagree

Neither agree or disagree

Agree

Strongly agree

Strongly disagree

DID YOU KNOW...

ABOUT ARCADIS Arcadis is the leading global Design & Consultancy firm for natural and built assets. Applying our deep market sector insights and collective design, consultancy, engineering, project and management services we work in partnership with our clients to finance, plan and execute strategies that optimise the construction, operation and ownership of mission critical facilities to improve business.

ARCADIS differentiates through its talented and passionate people and its unique combination of capabilities covering the whole asset life cycle, its deep market sector insights and its ability to integrate health & safety and sustainability into the design and delivery of solutions across the globe.

MEET THE EXPERTS If you would like to hear more, please get in touch.

Jim HartHead of Business Critical Systems M +44 (0)7909 682 452E [email protected]

Scott ShearerHead of Service M +44 (0)7810 850 027E [email protected]

David WillcocksSenior ConsultantM +44 (0)7841 618 512 E [email protected]

Paul RyanSenior Consultant, iX ConsultingM +44 (0)7971 551 335E [email protected]

ABOUT IX CONSULTING iXConsulting are a real estate consulting company with a specialist focus on the global data centre industry. Formed in 2001, iXConsulting offer expert, independent, customised research in response to the increasingly sophisticated needs of their clients. Whether a developer, investor or occupier of real estate, iXConsulting provides timely and insightful analysis tailored to your specific business strategy.

www.arcadis.com

@Arcadisglobal

ARCADIS

9361

ARC