Embed Size (px)

Citation preview

Supply, Demand and the Value of GreenBuildings

Andrea Chegut, Piet Eichholtz and Nils Kok

[Paper first received, March 2012; in final form, January 2013]

Abstract

Attention to ‘sustainability’ and energy efficiency rating schemes in the commercialproperty sector has increased rapidly during the past decade. In the UK, commercialproperties have been certified under the BREEAM rating scheme since 1999, offeringfertile ground to investigate the economic dynamics of ‘green’ certification in thecommercial property market. This paper documents that, over the 2000–09 period,the expanding supply of green buildings within a given London neighbourhood hada positive impact on average rents and prices, but reduced rents and prices for envir-onmentally certified real estate. The results suggest that there is a gentrificationeffect from green buildings. However, each additional ‘‘green’’ building decreases themarginal effect of certification in the rental and transaction markets by 2 per centand 5 per cent respectively. In addition, controlling for lease contract features, likecontract length and the rent-free period, modifies the impact of environmental certi-fication on rental prices.

1. Introduction

In the current debate on global climatechange, buildings are increasingly consid-ered by policy-makers, corporations andinstitutional investors to represent vehiclesfor achieving energy efficiency, carbonabatement and corporate social responsibil-ity. This shift in the perception and use of

buildings is gradually moving commercialproperty markets towards increased levelsof energy efficiency and ‘sustainability’.

Anecdotally, London’s 2015 skyline pro-vides testimony to this development. Forexample, The Shard, towering 72 storeys and306 metres into the London sky, is expected

Andrea Chegut and Piet Eichholtz are in the Department of Finance, Maastricht University,Maastricht, The Netherlands. Email: [email protected] and [email protected].

Nils Kok (corresponding author) is a visiting scholar at the Goldman School of Public Policy,University of California at Berkeley, 2607 Hearst Avenue, Berkeley, California, 94720, USA. Email:[email protected].

Article1–22, 2013

0042-0980 Print/1360-063X Online� 2013 Urban Studies Journal Limited

DOI: 10.1177/0042098013484526 at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

to consume 30 per cent less energy than anotherwise similar building; BishopsgateTower generates electricity through 2000square metres of photovoltaic cells; andBroadgate Tower, through its extensive heatrecovery system and efficient cooling plant,aims to reduce carbon emissions by 40 percent. In general, for most of the new or reno-vated commercial real estate coming tomarket in London, energy efficiency andsustainability features are primary buildingcharacteristics.

Part of the focus on energy efficiency isdriven by the UK’s regulatory frameworkregarding the carbon abatement and energyefficiency potential of the built environ-ment. This framework is embedded in EUlegislation, where buildings represent astrategic cornerstone of the recently recastEnergy Performance and BuildingsDirective and the Energy Efficiency Plan of2011. To comply, the UK has enforcedbuilding energy efficiency regulationsthrough two initiatives. First, it has imple-mented the mandatory display of EnergyPerformance Certificates, Declaration ofEnergy Certificates and zero-carbon build-ing initiatives. Secondly, the UK has insti-tuted a carbon market, solely aimed atbuilding energy consumption, with theCarbon Reduction Commitment of 2010.This legislation is among the first to pricethe negative externalities from energy con-sumption in buildings and ranks landlordsthrough carbon performance league tables.

Besides regulation, private-sector invol-vement in the energy efficiency of buildingsis growing. In 1990, the UK commercial realestate market was the first to introduce aprivate third-party assessment tool to mea-sure a building’s environmental impact—the BRE Environmental Assessment Method(BREEAM). Moreover, London’s largestcommercial landlords, including BritishLand, Grosvenor, Hammerson, Hermes andLand Securities, have taken action through

the formation of the Better BuildingsPartnership, with the aim to cut carbonemissions and to improve the ‘sustainabil-ity’ of London’s commercial buildings.

Despite these initiatives, the financialimplications of the transition to a more effi-cient building stock are not yet clear. Thisinformation becomes more important asthe supply of commercial buildings certifiedto be ‘green’ increases, as demand for suchbuildings is affected by more private-sectorattention to energy-efficient buildings andas the regulations surrounding the energyefficiency and carbon abatement potentialof buildings are tightened. Importantly,there is a notable degree of uncertainty andscepticism surrounding the economics ofgreen building in the UK.

Prior published literature on the finan-cial implications of green certificationmostly focuses on the US and results gener-ally indicate a positive relationship betweenenvironmental certification and financialoutcomes in the marketplace. Eichholtzet al. (2010) document significant and posi-tive effects on market rents and sellingprices following environmental certificationof office buildings. Relative to a controlsample of conventional office buildings,LEED or Energy Star labelled office build-ings achieve rents that are about 2 per centhigher, effective rents that are about 6 percent higher and premiums to selling pricesas high as 16 per cent. Other studies con-firm these findings (Fuerst and McAllister,2011a; Miller et al., 2008) and, importantly,these results appear robust over the courseof the financial crisis—the effect is notdented by the recent downturn in propertymarkets (Eichholtz et al., 2013).

For investors, it is important to under-stand the value and risk implications of theincreased focus on green building in thecommercial real estate sector. In the UK,green buildings have expanded over the pastdecade, accounting for about 10 per cent of

2 ANDREA CHEGUT ET AL.

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

the current commercial stock. However,market performance analysis of green certi-fied commercial real estate is scant withinthe UK.1 This is surprising, as London rep-resents one of the largest commercial realestate markets in the world.2 Moreover,London is a dominant player in the globalfinancial system, hosting a myriad of inter-national financial and service-sector firms(Clark, 2002). Building off this existinginfrastructure, London is capitalising on thenascent green economy, creating ‘comple-mentary’ legal and financial instruments tosupport new markets—for example, carbonmarkets and energy efficiency policy reforms(Knox-Hayes, 2009).

This paper investigates the dynamicsbehind the financial performance ofLondon’s environmentally certified com-mercial building stock within the context ofa changing supply and demand framework,measured ex post by sales transactions andachieved rents over the 2000–09 period.Addressing the economic fundamentalsdriving the value of green (i.e. supply anddemand), this paper makes two contribu-tions to the nascent literature on commer-cial building energy efficiency. First, weinvestigate the role of green building supplyon market dynamics by assessing the impactof growing competition of environmentallycertified real estate on the prices of ‘certi-fied’ and ‘non-certified’ office buildings.Secondly, we analyse in more detail thedemand for environmentally certified realestate, by including rental contract featuresand identifying the buyers of commercialproperties, exploring their impact on realestate rents and prices respectively.

To identify London’s stock of certifiedbuildings, we utilise BRE’s database on greenbuilding certification—BREEAM. We matchBREEAM-labelled buildings to a rental data-base over the 2005–10 period. We then con-struct a database using information fromfour data sources and complement these with

manual collection of information on buildingquality. This results in a final sample of 1149rental transactions, of which 64 rental trans-actions are in commercial properties certifiedby BREEAM. In addition, we match theBREEAM address files to sales transactionsover the period 2000–09. Following the samedata collection procedure, we obtain a sampleof 2103 observations, including 68 BREEAM-certified transactions.

At the point of means, we documentpremiums for certified buildings of 19.7 percent for rental transactions and 14.7 percent for sales transactions, relative to non-certified buildings in the same locationalcluster. A comparable analysis for Chicago,New York and Washington, DC, depicts asimilar premium for transactions of certi-fied buildings in the US. Importantly, wedocument that growth and concentrationin the green building supply have a negativeeffect on the marginal rents and prices paidfor green buildings as compared with non-certified buildings in the same neighbour-hood, but a positive impact on the averagelevel of rents and prices of all commercialbuildings in that neighbourhood—‘greengentrification’. The diffusion of certifiedreal estate over the past decade has contrib-uted to the gentrification of London’s com-mercial districts. However, the growth inenvironmentally certified buildings has ledthese properties to become the standardrather than the exception, which has animpact on their pricing in the marketplace.Finally, investor type and contract featureshave a modifying impact on prices of certi-fied buildings and it is therefore imperativefor these factors to be included in futureresearch on this topic.

The remainder of this paper is organisedas follows. Section 2 introduces and dis-cusses the UK market for green real estate. Insection 3, we discuss BREEAM and financialdata obtained for commercial buildings inLondon. In section 4, we outline the

THE VALUE OF GREEN BUILDINGS 3

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

methodology for our analysis. In section 5,we present the results of the formal analysis.Section 6 provides a discussion and someconclusions.

2. The UK Market for Green OfficeSpace

2.1 Environmental Certification forCommercial Buildings

Building certification facilitates the inter-mediation process between building develo-pers, investors and tenants in the context ofwhat constitutes ‘quality’ or ‘efficiency’ in abuilding. This intermediation process mayreduce investment in ‘lemons’ (Akerlof,1970). For ‘green’ real estate, rating agenciesmay reduce adverse selection by acting asaccredited and recognised assessors of envi-ronmental information. Thus, building per-formance disclosure may lead to reducedinvestment in environmentally underper-forming buildings.

Within the UK, there are two privateintermediaries of environmental informa-tion on buildings, BREEAM and LEED. In1990, the UK’s Building ResearchEstablishment (BRE) began the indepen-dent certification of the environmental per-formance of buildings in the UK. The firstcommercial office space was certified in1999. Under the 2008 scheme, a commer-cial office can receive BREEAM certifica-tion if it meets the minimum standards setby BRE in eight core dimensions: buildingmanagement, health and wellbeing, energyefficiency, transport efficiency, water effi-ciency, material usage, pollution and landuse ecology.

Competition for third-party environ-mental certification in the UK market ismainly with LEED, the Leadership in Energyand Environmental Design rating systemdesigned by the US Green Building Council.

The purpose of LEED is similar to that ofBREEAM: increasing the energy efficiencyand sustainability of the built environmentthrough the certification of exemplarybuildings.3

2.2 Supply of Green Office Space

Green buildings are considered differentfrom conventional buildings because theycommand a different set of technologicaland human capital requirements. Greenbuilding supply is most likely to be drivenby construction costs, other certified build-ings’ price signals, the prices and availabilityof raw materials and human capital to con-struct green buildings, advances in greentechnology and government policies man-dating energy efficiency (see Kok, McGrawand Quigley, 2011). Thus, growth in thegreen building supply may have a dynamicimpact on equilibrium prices over the 2000–09 period.

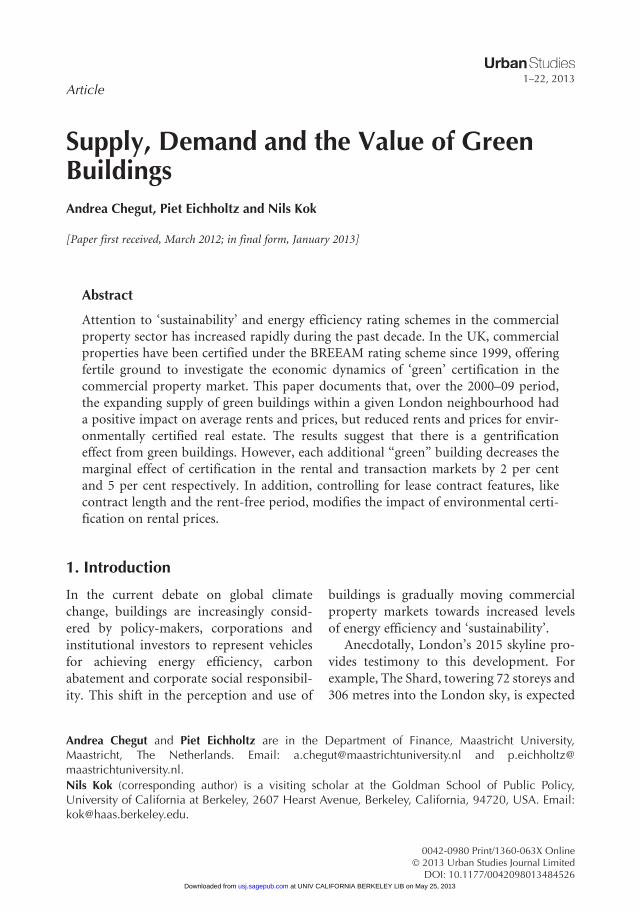

Figure 1 displays the geography of UKoffice buildings labelled by BREEAM bylevel of certification, which corresponds to alabel ranging from ‘‘Pass’’ to ‘‘Outstanding’’.The map displays the dispersion of greenoffice buildings across the UK, with a signif-icant cluster of buildings located in London(368 buildings, or 23 per cent of theBREEAM office population). Bristol,Manchester, Newcastle Upon Tyne andGlasgow are other cities with relatively highconcentrations of green buildings (a total of171 buildings, or 10 per cent of theBREEAM office population). Highly ratedbuildings are mainly in London, with thenumber of ‘‘Excellent’’ and ‘‘Very Good’’rated buildings far surpassing other markets(181 buildings).

2.3 Demand for Green Office Space

Improving the bottom line through buildingenergy efficiency is often reported as one of

4 ANDREA CHEGUT ET AL.

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

Figure 1. Geography of green buildings in the UK and London by BREEAM rating.

THE VALUE OF GREEN BUILDINGS 5

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

the direct economic benefits for real estateinvestors when considering the energy effi-ciency and sustainability of a portfolio. Forexample, Jones Lang LaSalle (2009) reportsfor 115 office properties in their portfolio forwhich the energy efficiency was improved,the average realised savings for 2007 and2008 were £1.4 million and £1.9 millionrespectively. British Land (2010) reported a12 per cent decrease in energy use in 2009(some 11.1 GW of electricity), amounting to£700 000 in annual energy savings.

In addition, institutional investors mayhave different investment beliefs whenintroducing corporate social responsibilitycriteria into their real estate investmentstrategy. A recent sustainability benchmark,commissioned by 35 of the largest institu-tional investors around the globe, docu-ments institutional investor engagement inthe building sector’s sustainability. Theproperty sector, by being mindful of man-agement and implementation of energyefficiency and sustainability within theirown portfolios, reduced carbon emissionsby 1.8 per cent and achieved $1 billion inenergy savings in 2010–11 period (Kok,Bauer and Eichholtz, 2011).

The most important factor determiningdemand for rental space is employment in thelegal and financial service sectors (Wheatonet al., 1997). In the US, the financial servicesector (i.e. legal services, national commercialbanks, executive legislative and general office)began occupying LEED and Energy Star certi-fied space over the 2004–09 period (Eichholtzet al., 2011). Data from London are indicatinga similar trend, where financial services firms,advertising and insurance sectors are domi-nant users of green space. For example, CBREreports that 58 per cent of tenants find energyefficiency ‘essential’ and 50 per cent find othergreen attributes ‘essential’ (CBRE, 2010).

Anecdotally, the move of tenants towardsgreen real estate is due to enhanced reputa-tion benefits, corporate social responsibility

mandates and employee productivity(Nelson and Rakau, 2010). Shifting tenantpreferences suggest that tenants are usingthe buildings they occupy to communicatetheir corporate vision to shareholders andemployees. The literature on corporatesocial responsibility (CSR) has investigatedthis link between corporate social perfor-mance, reputation benefits and employerattractiveness (Turban and Greening, 1997;Margolis and Walsh, 2003), although claimsare mostly based on case studies.

3. UK Property Market Data

The UK’s primary commercial real estatemarket is the London metropolitan market.London is currently the most active com-mercial real estate market in the world(Chegut et al., forthcoming). Any UK studywill be biased towards London, leading tothe following concerns: first, in hedonicmodels at the national level, the ‘Londoneffect’ creates inconsistent estimates in pric-ing common building characteristics, suchas age, storey, renovations and amenities, asthese features are specific to London and itshistory. Secondly, a sample combining thecommercial property markets of London,Manchester, Bristol and Leeds is geographi-cally clustered in London, which is a con-cern when location is a principal factor inmodelling rental and transaction prices.Thirdly, UK databases overwhelminglyreport rental and transaction observationsin London, as transaction and buildingcharacteristic knowledge is more abundantfor the London area than for any otherregion in the country. Given these threeconcerns, we focus on the London metro-politan area in this paper.

To analyse the economic implications ofenvironmentally certified commercial realestate in London, we match BREEAMaddress files to a combined dataset of rents

6 ANDREA CHEGUT ET AL.

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

and property transactions maintained byCoStar FOCUS4 and Estates GazetteInteractive5 (EGi) over the periods 2005–09and 1999–2009 respectively. Over these peri-ods, CoStar covered a sample of some 5028commercial leasing transactions and EGi andCoStar covered 4500 sales transactionsacross London. However, CoStar data do notinclude basic building characteristics, such asage, storeys, amenities, third-party assess-ment of building quality, etc. To collect thesemissing hedonic features, we consulted threedatabases: Emporis, a global building designdatabase, EGi and Real Capital Analytics. Inaddition, we hand-collected building fea-tures from building prospectuses and adver-tisements, and went on physical site visits inLondon. Approximately 2500 rental transac-tions were collected for London utilising thismanual effort. For sales data, a similar datacollection procedure was conducted. Thisextensive data collection procedure, coupledwith removal of erroneous data and portfoliosales, resulted in a sample of 1149 lease trans-actions, including 64 BREEAM-certifiedleases, and a sales transaction sample of 2103observations, including 68 BREEAM-certi-fied transactions.

Our dataset contains information on abuilding’s environmental characteristics(i.e. the BREEAM-rating), quality charac-teristics, address, distance to local transportnetworks, transaction date, investor typesand contract features. Ex ante, we have thefollowing expectations concerning qualitycharacteristics, contract features, marketcompetition, investor types and location.

(1) Quality characteristics: rental unit sizewill play a significant and positive rolein price determination. In addition,standard hedonic features, like age,storeys, amenities and renovation areexpected to have a significant and posi-tive impact, where younger, taller andrenovated buildings with amenities will

have higher rental prices. Moreover,differences between the green and con-trol sample may manifest from differ-ences in building quality variables. Inthe UK, building quality is rated on aper floor basis. Thus, a building repre-sents a collection of different buildingqualities. We expect that building qual-ity will have a positive impact on pricesand modifying impact on the value ofcertification.

(2) Contract features: longer lease lengthssignal longer durations in cash flows,which implies less fluctuation intenants and more rental stability, con-ditional upon tenants’ credit quality.This suggests a positive impact onprice. However, longer rent-free peri-ods6 can signal larger discounts inrental cash flows, thus reducing prices.Moreover, contract features potentiallyhave a moderating effect on certifica-tion. Furthermore, prices may also bediscounted when buildings are on themarket for a longer period.

(3) Market competition and gentrification:market competition may substantiallyinfluence rental prices in certifiedbuildings. Literature on developmentsuggests that competition plays a role indevelopment decisions (see Grenadier,2002; and Bulan et al., 2009, for the roleof competition in influencing commer-cial real estate investments). We createa ‘certified building supply’ variable,which is a numerical measure of allBREEAM-certified buildings within a500-metre radius at the time of rentingor sale. The value of this variable is sim-ilar for the green building and all non-green buildings in a given cluster.Ex ante, as the number of certifiedbuildings in a micro location increases,we anticipate moderating effects on themarginal rents and prices commandedby certified buildings. However, the

THE VALUE OF GREEN BUILDINGS 7

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

literature on neighbourhood gentrifica-tion suggests that potential increases insocial and middle-class environmentalimprovements can lead to positive new-build ‘gentrification’ for neighbour-hoods or ‘super-gentrification’ (Butlerand Lees, 2006). Thus, we suspect thatincreasing the number of renovated ornew certified buildings in centralLondon will add to the average loca-tional value of a neighbourhood.

(4) Investor types: theoretically, there shouldbe no anticipated price difference fordifferent investor types. However, prin-cipals and agents of financial capital mayhave different investment criteria andmandates. Principals, like private devel-opers and investors, manage their ownfinancial capital, whereas agents, such asreal estate investment managers (forexample, REITs),7 institutional investorsand municipal government investorsmanage financial capital on behalf ofshareholders, trustees and communities.Thus, the type of investor may have animpact on prices.

(5) Location: following standard methodol-ogy, we control for building locationusing post-codes and transport net-works in London. London is brokendown into London sub post-code units,the 1-3 letter prefix, which correspondsto its compass location. Transport sta-tions (i.e. the UK’s national rail system,London tube stations and DocklandsLight Rail) are geocoded using latitudeand longitude, and station distances(within 500 m) to buildings are then cal-culated. To control for accessibility fordrivers and cyclists, we use OrdnanceSurvey road networks to calculatemetric unit distances to the buildings.The physical distances for tube stations,local roads and motorways have in thepast had inconsistent impacts on com-mercial rents and prices (Debrezion

et al., 2007), but may have an economi-cally significant impact on prices forLondon.

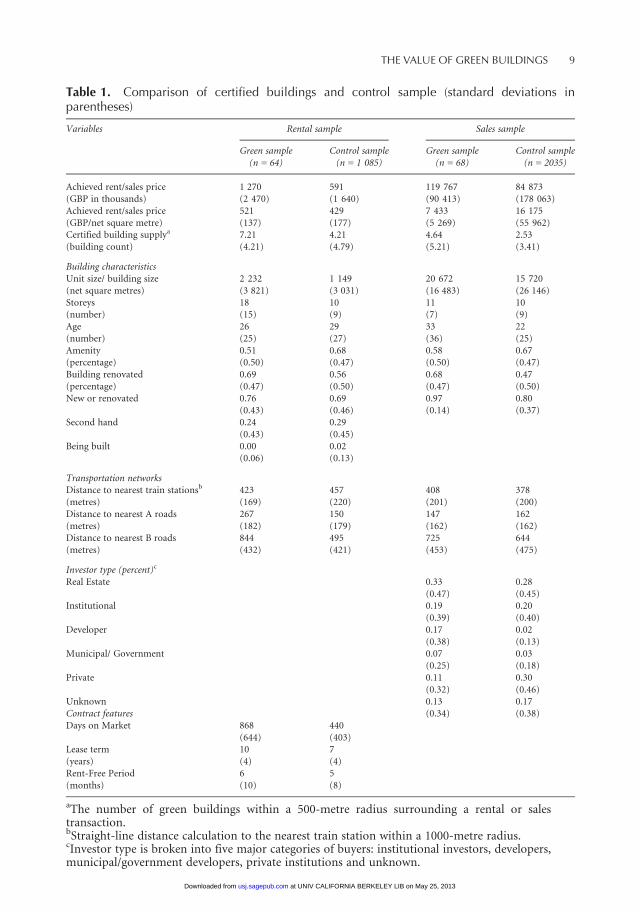

Table 1 shows the dependent and indepen-dent variables used in the analysis, compar-ing the average characteristics of greenbuildings in the sample with buildings inthe control sample. Certified buildings havehigher achieved rents, on average, than con-trol buildings, but the variability of rents ishigher in green buildings. The size of leasesin green buildings is larger, on average,than rental transactions in the controlsample, by about 1100 square metres. Morethan half the certified sample is renovated,about double compared with the controlsample. Amenities are available in 51 percent of certified rentals and 68 per cent ofcontrol rentals.8 Building quality variablessuggest that over 75 per cent of the certifiedsample is new or renovated, which is com-parable with the control sample. The dis-tance to the nearest train stations within500 metres from certified rentals is greaterby 50 metres. It is interesting to note thatgreen buildings are further from A roadsand B roads on average, with comparablevariability.

The average lease length in green proper-ties is longer by almost three years and withvariability comparable with that of the con-trol sample, but the rent-free period islonger by about three months, with greatervariation than control rentals. The averagenumber of days that certified buildings areon the market is longer. The ‘certifiedbuilding supply’ variable shows that, onaverage, certified properties have sevenother certified buildings in their immediatearea at the time of the rental transaction,whereas control rentals have, on average,four green buildings in their immediateneighbourhood.

In our sample, 52 per cent of certifiedbuildings are owned by a real estate or

8 ANDREA CHEGUT ET AL.

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

Table 1. Comparison of certified buildings and control sample (standard deviations inparentheses)

Variables Rental sample Sales sample

Green sample(n = 64)

Control sample(n = 1 085)

Green sample(n = 68)

Control sample(n = 2035)

Achieved rent/sales price 1 270 591 119 767 84 873(GBP in thousands) (2 470) (1 640) (90 413) (178 063)Achieved rent/sales price 521 429 7 433 16 175(GBP/net square metre) (137) (177) (5 269) (55 962)Certified building supplya 7.21 4.21 4.64 2.53(building count) (4.21) (4.79) (5.21) (3.41)

Building characteristicsUnit size/ building size 2 232 1 149 20 672 15 720(net square metres) (3 821) (3 031) (16 483) (26 146)Storeys 18 10 11 10(number) (15) (9) (7) (9)Age 26 29 33 22(number) (25) (27) (36) (25)Amenity 0.51 0.68 0.58 0.67(percentage) (0.50) (0.47) (0.50) (0.47)Building renovated 0.69 0.56 0.68 0.47(percentage) (0.47) (0.50) (0.47) (0.50)New or renovated 0.76 0.69 0.97 0.80

(0.43) (0.46) (0.14) (0.37)Second hand 0.24 0.29

(0.43) (0.45)Being built 0.00 0.02

(0.06) (0.13)

Transportation networksDistance to nearest train stationsb 423 457 408 378(metres) (169) (220) (201) (200)Distance to nearest A roads 267 150 147 162(metres) (182) (179) (162) (162)Distance to nearest B roads 844 495 725 644(metres) (432) (421) (453) (475)

Investor type (percent)c

Real Estate 0.33 0.28(0.47) (0.45)

Institutional 0.19 0.20(0.39) (0.40)

Developer 0.17 0.02(0.38) (0.13)

Municipal/ Government 0.07 0.03(0.25) (0.18)

Private 0.11 0.30(0.32) (0.46)

Unknown 0.13 0.17Contract features (0.34) (0.38)Days on Market 868 440

(644) (403)Lease term 10 7(years) (4) (4)Rent-Free Period 6 5(months) (10) (8)

aThe number of green buildings within a 500-metre radius surrounding a rental or salestransaction.bStraight-line distance calculation to the nearest train station within a 1000-metre radius.cInvestor type is broken into five major categories of buyers: institutional investors, developers,municipal/government developers, private institutions and unknown.

THE VALUE OF GREEN BUILDINGS 9

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

institutional investor, as compared with 48per cent of control buildings. Moreover, themunicipal and government sector owns just7 per cent of the buildings in the sample.

Non-parametric comparisons betweenthe sample of certified transactions and thesample of non-certified transactions yieldsimilar results. The variable approximatingcompetition in the sales transaction marketis noteworthy. For certified buildings, thereare on average five green buildings in agiven 500-square-metre radius at the timeof transaction, while the control sample hasonly three such buildings, on average.

4. Method

We investigate the economic implicationsof environmental certification for Londoncommercial office buildings through anex post transaction-based hedonic model(Rosen, 1974). We use the sample ofBREEAM-rated office buildings and a con-trol sample of conventional office buildingsto estimate a semi-log equation relating theoffice rents per net square metre (or theselling price per net square metre) to thehedonic characteristics of a building

log Pi = a + bXi + dgi + ei ð1Þ

where, the dependent variable is the loga-rithm of the rental price (selling price) pernet square metre Pi in commercial officebuilding i; Xi is a vector of hedonic charac-teristics (for example, age, storeys, size,public transport accessibility), rental con-tract features (for example, lease length andrent-free period), market signals (days onmarket), investor types and macroeconomicconditions (for example, quarterly timedummies) of building i; and gi is a dummyvariable with a value of 1 if building i israted by BREEAM and zero otherwise; a, b

and d are estimated coefficients and ei is anerror term.

We estimate equation (1) using OLS cor-rected for heteroscedasticity with clusteredstandard errors (White, 1980), but employpropensity score weighting techniques tominimise bias between the BREEAM-certified and control buildings. In ourapplication, propensity score weightingaims to minimise the selection bias betweencertified and non-certified buildings by dif-ferentiating based on individual buildingcharacteristics. Conditional upon observa-ble characteristics, we eliminate differencesbetween ‘treated’ green buildings and ‘non-treated’ control buildings by estimating thepropensity of receiving a BREEAM ratingfor all buildings in the sales and rental sam-ples, using a logit model (Black and Smith,2004). The propensity score specificationincludes all hedonic characteristics availablefor each sample and the resulting propen-sity score is subsequently applied as aweight in the regression of equation (1)(see also Eichholtz et al., 2013).

In the second part of our analysis, wedocument the impact of the supply ofBREEAM-rated buildings on transactionsprices. We investigate how local certifiedbuilding competition acts as a moderatorto rental and transaction prices in general,and how this may moderate BREEAM-cer-tified rented and transacted properties inparticular. Following Brambor et al. (2006),we examine the interaction effects betweencertification and the market competitionfor certified buildings

log Pi = a + bXi + dgi + uCi + sgiCi + ei ð2Þ

where, equation (2) introduces Ci, a ‘certi-fied building supply’ variable, into equation(1) to allow the average price or rent in aneighbourhood to be moderated by thelevel of green building competition in themarketplace. In addition, we interact certi-fication status, gi, with the ‘certified build-ing supply’, Ci, to isolate the moderating

10 ANDREA CHEGUT ET AL.

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

effect of geographical clustering of certifiedbuildings on the marginal effect of certifica-tion on the price or rent of individual greenbuildings.

To assess the impact of a larger existingsupply of green buildings on the effect ofcertified prices, we calculate

∂ log Pi

∂gi= d + sCi ð3Þ

where, equation (3) is the marginal effect ofcertified rents or prices conditional upon theexisting green building supply. To supportthe robustness of the conditional marginaleffect analysis, we introduce confidenceinterval bands for statistical significance anduse kernel density estimators to show thedensity of the green building supply.

5. Results

5.1 Green Buildings and Rental Rates

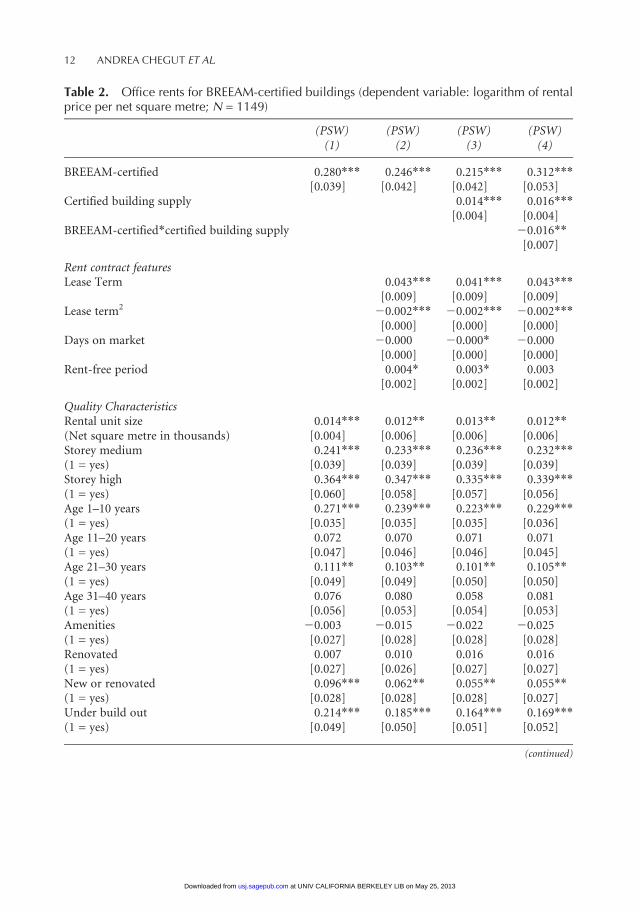

Table 2 presents the regression results forthe rental sample, relating the logarithm ofrent per net square metre of commercialoffice space to a set of hedonic characteris-tics, neighbourhood controls and contractfeatures. These specifications explain almost60 per cent of the variation in the logarithmof rents per net square metre with anadjusted R2 ranging from 59 to 62 per cent.

Column (1) reports the propensity-weighted results for the hedonic specifica-tion relating office rents to the hedoniccharacteristics—i.e. rental size, age, storeys,amenities, renovation, unit quality, trans-port networks, time-fixed effects andpostcode fixed effects. The coefficient onrental size is positive and significant: largerspaces command higher rental rates per netsquare metre. Buildings greater than 10storeys or 20 storeys transact for 24–36 percent more than those less than 10 storeys,

respectively. For buildings less than 10 yearsold, rents are 27 per cent higher relative tobuildings more than 40 years old. The ame-nities dummy is negative, but insignificant.Regarding building quality, there is a 9.6 percent premium for new or refurbished unitscompared with second-hand units.

Importantly, keeping constant the obser-vable characteristics, the green certificationdummy is positive and significant.BREEAM-certified properties command a28 per cent premium over non-certifiedproperties.

In column (2), we add control variablesfor rental contract features to the hedonicspecification. The term structure of leaseshas an impact on rent levels: the rent pernet square metre increases at a rate of 4.3per cent per additional year of lease, but theterm structure is non-linear. Thus, the max-imum achieved rent is realised at lease dura-tion of about 12 years and the marginalincrease in rent becomes zero once leaselengths surpass 11.5 years. The number ofdays that a unit is on the market has no sig-nificant impact on achieved rents, whereasrent-free periods have a statistically signifi-cant and positive impact on rents. Rentalcontract features have a moderating effecton the certification coefficient, decreasingthe green rental premium by almost fourpercentage points.

In column (3), the specification isreported with further controls for the localsupply of certified buildings. The variablesfor ‘BREEAM-certified’ and ‘certifiedbuilding supply’ are jointly significant atthe 1 per cent level. The ‘certified buildingsupply’ does not have a substantial impacton the hedonic parametres. However, asthe number of observed certified buildingswithin the transacted building’s micro loca-tion increases, average rents per net squaremetre increase by 1.4 per cent in the neigh-bourhood, which provides some evidenceon a ‘green gentrification’ effect.

THE VALUE OF GREEN BUILDINGS 11

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

Table 2. Office rents for BREEAM-certified buildings (dependent variable: logarithm of rentalprice per net square metre; N = 1149)

(PSW) (PSW) (PSW) (PSW)(1) (2) (3) (4)

BREEAM-certified 0.280*** 0.246*** 0.215*** 0.312***[0.039] [0.042] [0.042] [0.053]

Certified building supply 0.014*** 0.016***[0.004] [0.004]

BREEAM-certified*certified building supply 20.016**[0.007]

Rent contract featuresLease Term 0.043*** 0.041*** 0.043***

[0.009] [0.009] [0.009]Lease term2 20.002*** 20.002*** 20.002***

[0.000] [0.000] [0.000]Days on market 20.000 20.000* 20.000

[0.000] [0.000] [0.000]Rent-free period 0.004* 0.003* 0.003

[0.002] [0.002] [0.002]

Quality CharacteristicsRental unit size 0.014*** 0.012** 0.013** 0.012**(Net square metre in thousands) [0.004] [0.006] [0.006] [0.006]Storey medium 0.241*** 0.233*** 0.236*** 0.232***(1 = yes) [0.039] [0.039] [0.039] [0.039]Storey high 0.364*** 0.347*** 0.335*** 0.339***(1 = yes) [0.060] [0.058] [0.057] [0.056]Age 1–10 years 0.271*** 0.239*** 0.223*** 0.229***(1 = yes) [0.035] [0.035] [0.035] [0.036]Age 11–20 years 0.072 0.070 0.071 0.071(1 = yes) [0.047] [0.046] [0.046] [0.045]Age 21–30 years 0.111** 0.103** 0.101** 0.105**(1 = yes) [0.049] [0.049] [0.050] [0.050]Age 31–40 years 0.076 0.080 0.058 0.081(1 = yes) [0.056] [0.053] [0.054] [0.053]Amenities 20.003 20.015 20.022 20.025(1 = yes) [0.027] [0.028] [0.028] [0.028]Renovated 0.007 0.010 0.016 0.016(1 = yes) [0.027] [0.026] [0.027] [0.027]New or renovated 0.096*** 0.062** 0.055** 0.055**(1 = yes) [0.028] [0.028] [0.028] [0.027]Under build out 0.214*** 0.185*** 0.164*** 0.169***(1 = yes) [0.049] [0.050] [0.051] [0.052]

(continued)

12 ANDREA CHEGUT ET AL.

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

In column (4), the specification isreported with an interaction term for‘BREEAM-certified’ and ‘certified buildingsupply’. Isolating the effect of green build-ing competition in the specification showsthat each additional green building in acluster decreases the marginal effect of cer-tification by some 1.6 per cent, ceteris pari-bus. At the average number of certifiedbuildings (7.21), the marginal rent com-manded by a green building, relative tonon-green buildings in the same neigh-bourhood, is 19.7 per cent.

Figure 2 shows the results of the condi-tional marginal effects analysis. There arethree axes: the left vertical axis depicts thebeta coefficient of the conditional marginaleffect; the horizontal axis is the ‘certifiedbuilding supply’ (the number of BREEAM-certified buildings within 500 metres at thetime of renting); and the right vertical axisrepresents the ‘certified building supply’s’

univariate kernel density estimate. Thekernel density estimate is a non-parametricestimation of the probability densityfunction.

In the figure, the dotted line depicts thekernel density of the certified buildingsupply. From left to right, about 15 per centof units have at least two certified buildingswithin 500 metres and less than 5 per cent ofthe sample has more than six certified build-ings surrounding them. The solid line showsthe change in rents per net square metre forcertified units when the ‘certified buildingsupply’ increases. Thus, when the numberof certified buildings in a cluster increases,the green premium decreases by 1.6 percent, on average.9 From confidence intervalbounds, the interaction term (BREEAM-certified*certified building supply) is statis-tically significant until approximately 9buildings, where the premium is still posi-tive, but substantially lower.

Table 2. (Continued)

(PSW) (PSW) (PSW) (PSW)(1) (2) (3) (4)

Transportation networksTrain distance 25.219 25.800 27.506 27.794(1/metric distance) [5.433] [5.485] [6.196] [6.271]A road distance 20.073 20.052 20.042 20.042(1/metric distance) [0.052] [0.052] [0.054] [0.054]B road distance 20.002 0.013 20.028 20.033(1/metric distance) [0.074] [0.073] [0.076] [0.075]Constant 4.809*** 4.731*** 4.784*** 4.780***

[0.083] [0.091] [0.090] [0.091]

R2 0.596 0.615 0.626 0.628Adjusted R2 0.57 0.59 0.60 0.61

Notes: All models include post-code fixed effects to control for location and time-fixed effects tocontrol for time variation in rental prices. Storeys medium and high are relative to low-storeybuildings and the age factors are relative to buildings older than 40 years in age. New or renovatedand under build out units are relative to second-hand units. Lastly, BREEAM-certified*certifiedbuilding supply remarks the number of certified buildings within 500 metres of the BREEAM-certified rental unit. *, ** and *** denote significance at the 10, 5 and 1 per cent levels,respectively.

THE VALUE OF GREEN BUILDINGS 13

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

5.2 Green Buildings and Transaction Prices

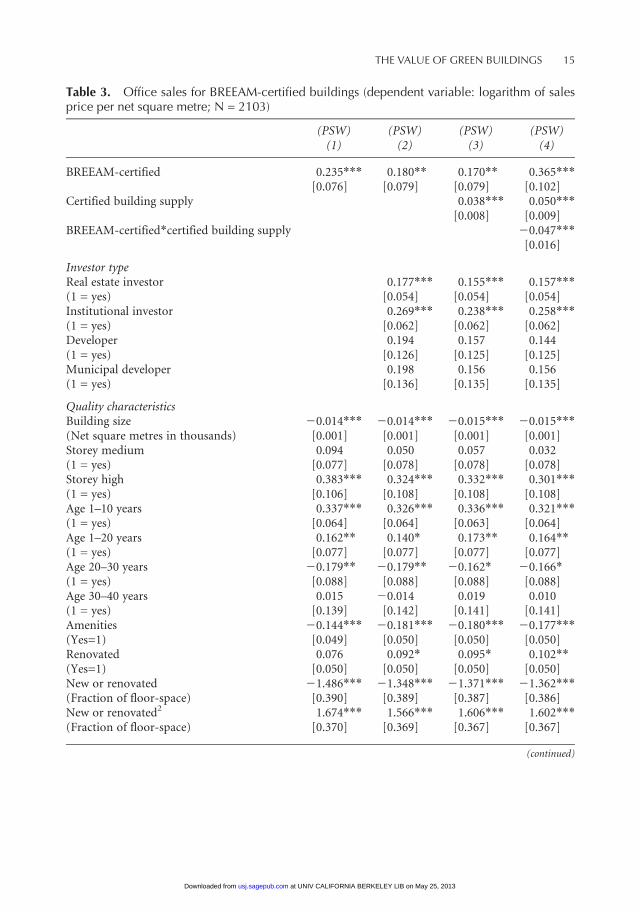

Table 3 presents the results for the salessample, relating the logarithm of sales priceper net square metre of office buildings to aset of hedonic characteristics, investor typesand neighbourhood controls. These specifi-cations explain about 22 per cent of thevariation in the sales price per net squaremetre.

Column (1) reports the propensity-weighted hedonic specification relatingsales prices to hedonic qualities—i.e. size,age, storeys, amenities, renovation, buildingquality, transport networks, post-code fixedeffects and time-fixed effects.

Building size has a negative and signifi-cant impact on transaction price, withtransaction prices decreasing by 1.4 percent as building size increases by 1000square metres. Relative to buildings morethan 40 years old, buildings constructedafter 2000 transact at a premium and build-ings from the 1980s transact at a discount.The variable for new and renovated build-ings (as a percentage of floor space) is

significantly negative, suggesting that, asnew and renovated floor space increases,there is a negative relationship with price,but other (unreported) specifications indi-cate that this is mostly due to second-handspace. Lastly, transport networks (i.e. theproximity of buildings to a station) have apositive impact on prices, but road net-works, while modifying other parametres,are insignificant. In central London, publictransport matters more than accessibilityby car. Comparable results have been docu-mented for the Dutch office market (Kokand Jennen, 2012).

Most importantly, the ‘BREEAM-certi-fied’ coefficient is positive and significant,suggesting that BREEAM-certified build-ings transacted at a 24 per cent premiumduring the sample period, after controllingfor observable differences in building qual-ity and location.

In column (2), investor types are addedto the specification. Relative to privateinvestors, real estate investors and institu-tional investors paid more for commercialreal estate during the sample period. Inaddition, when adding investor types, thepremium for certified real estate decreasesto 18 per cent. Controlling for the identityof the buyer is an important moderatingfactor in determining the economic valueof green buildings in the marketplace.

In column (3), the ‘certified buildingsupply’ measure is added to the specifica-tion. Controlling for ‘certified buildingsupply’ has a positive and significant impacton the average transaction price in the clus-ter, resulting in a 3.8 per cent increase intransaction price per net square metre. Thisreinforces the gentrification effect of greenbuildings previously documented for therental results. Including ‘certified buildingsupply’ has a moderating effect on the greenpremium, decreasing the coefficient by onepercentage point. The ‘BREEAM certified’

Con

ditio

nal m

argi

nal e

ffect

Ker

nel d

ensi

ty g

reen

bui

ldin

g su

pply

Kernel density green building supply95% confidence interval

Green building supply

Effect of certification on price, conditional on green building supply

Figure 2. Marginal effects of certified build-ing supply (number of green buildings withina 500-metre radius): rental sample (2005–09Period).Notes: The dotted line depicts the kernel den-sity of the certified building supply. The solidline is the marginal effect of rents per netsquare metre, given that the unit is certified,with the certified building supply. The twodashed lines denote confidence intervals.

14 ANDREA CHEGUT ET AL.

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

Table 3. Office sales for BREEAM-certified buildings (dependent variable: logarithm of salesprice per net square metre; N = 2103)

(PSW) (PSW) (PSW) (PSW)(1) (2) (3) (4)

BREEAM-certified 0.235*** 0.180** 0.170** 0.365***[0.076] [0.079] [0.079] [0.102]

Certified building supply 0.038*** 0.050***[0.008] [0.009]

BREEAM-certified*certified building supply 20.047***[0.016]

Investor typeReal estate investor 0.177*** 0.155*** 0.157***(1 = yes) [0.054] [0.054] [0.054]Institutional investor 0.269*** 0.238*** 0.258***(1 = yes) [0.062] [0.062] [0.062]Developer 0.194 0.157 0.144(1 = yes) [0.126] [0.125] [0.125]Municipal developer 0.198 0.156 0.156(1 = yes) [0.136] [0.135] [0.135]

Quality characteristicsBuilding size 20.014*** 20.014*** 20.015*** 20.015***(Net square metres in thousands) [0.001] [0.001] [0.001] [0.001]Storey medium 0.094 0.050 0.057 0.032(1 = yes) [0.077] [0.078] [0.078] [0.078]Storey high 0.383*** 0.324*** 0.332*** 0.301***(1 = yes) [0.106] [0.108] [0.108] [0.108]Age 1–10 years 0.337*** 0.326*** 0.336*** 0.321***(1 = yes) [0.064] [0.064] [0.063] [0.064]Age 1–20 years 0.162** 0.140* 0.173** 0.164**(1 = yes) [0.077] [0.077] [0.077] [0.077]Age 20–30 years 20.179** 20.179** 20.162* 20.166*(1 = yes) [0.088] [0.088] [0.088] [0.088]Age 30–40 years 0.015 20.014 0.019 0.010(1 = yes) [0.139] [0.142] [0.141] [0.141]Amenities 20.144*** 20.181*** 20.180*** 20.177***(Yes=1) [0.049] [0.050] [0.050] [0.050]Renovated 0.076 0.092* 0.095* 0.102**(Yes=1) [0.050] [0.050] [0.050] [0.050]New or renovated 21.486*** 21.348*** 21.371*** 21.362***(Fraction of floor-space) [0.390] [0.389] [0.387] [0.386]New or renovated2 1.674*** 1.566*** 1.606*** 1.602***(Fraction of floor-space) [0.370] [0.369] [0.367] [0.367]

(continued)

THE VALUE OF GREEN BUILDINGS 15

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

and ‘certified building supply’ parametresare jointly significant at the 1 per cent level.

In column (4), the interaction term isadded to the transaction price specification.The green gentrification effects remain, butthe results show that the marginal effect ofgreen building certification decreases whenmore green buildings come on the marketat a given location. At the average numberof certified buildings (4.64), the marginaleffect of green building certification is 14.7per cent, relative to non-green buildings inthe same neighbourhood.

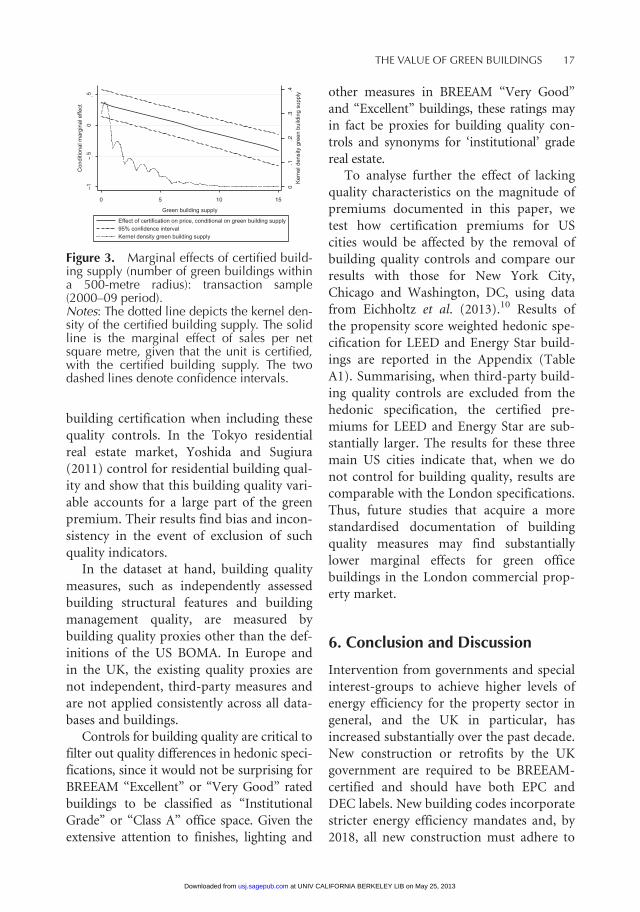

Figure 3 presents the results of the condi-tional marginal effects analysis. In the figure,the marginal effect of the sales price per netsquare metre and the ‘certified buildingsupply’ are shown. In the figure, the dottedline depicts the kernel density of the ‘certi-fied building supply’. From left to right,about 30 per cent of observations have atleast two certified buildings within 500metres and less than 5 per cent of the samplehas more than six certified buildings

surrounding them. The solid line shows themarginal effect of the sales price per netsquare metre, given that the building is cer-tified, with the certified building supply. Ascertified buildings in a cluster increase, thegreen premium decreases, by 4.7 per cent onaverage. The certified green building supplyresult is statistically significant until approx-imately eight buildings, where the premiumis still positive, but reduced substantially.

5.3 Additional Analysis

The marginal effects documented for envir-onmentally certified real estate in the UKare generally in line with the literatureinvestigating the economic outcomes ofLEED and Energy Star certification in UScommercial markets. However, Eichholtzet al. (2010) specifically control for buildingquality using the Building Owners andManagers Association (BOMA) buildingclass definitions and document significantreductions in the marginal effects of green

Table 3. (Continued)

(PSW) (PSW) (PSW) (PSW)(1) (2) (3) (4)

Transportation networksTrain distance 33.592*** 31.678*** 31.228*** 31.876***(1/metric distance) [8.805] [8.786] [8.744] [8.730]A road distance 20.109 20.146 20.126 20.121(1/metric distance) [0.102] [0.103] [0.102] [0.102]B road distance 20.081 20.043 20.045 20.094(1/metric distance) [0.270] [0.270] [0.269] [0.269]Constant 8.906*** 8.785*** 8.890*** 8.918***

[2.458] [2.448] [2.436] [2.431]

R2 0.226 0.234 0.242 0.245Adjusted R2 0.21 0.21 0.22 0.22

Notes: All models include post-code fixed effects to control for location and time fixed effects to controlfor time variation in transaction prices. Investor types are relative to private investors; storeys mediumand high are relative to low-storey buildings and the age factors are relative to buildings older than 40years in age. Lastly, certified supply demarks the number of certified buildings within 500 metres of thetransacted building and certified competition is the same measure, but for BREEAM-certified variables.*, ** and *** denotes significance at the 10, 5 and 1 per cent levels respectively.

16 ANDREA CHEGUT ET AL.

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

building certification when including thesequality controls. In the Tokyo residentialreal estate market, Yoshida and Sugiura(2011) control for residential building qual-ity and show that this building quality vari-able accounts for a large part of the greenpremium. Their results find bias and incon-sistency in the event of exclusion of suchquality indicators.

In the dataset at hand, building qualitymeasures, such as independently assessedbuilding structural features and buildingmanagement quality, are measured bybuilding quality proxies other than the def-initions of the US BOMA. In Europe andin the UK, the existing quality proxies arenot independent, third-party measures andare not applied consistently across all data-bases and buildings.

Controls for building quality are critical tofilter out quality differences in hedonic speci-fications, since it would not be surprising forBREEAM ‘‘Excellent’’ or ‘‘Very Good’’ ratedbuildings to be classified as ‘‘InstitutionalGrade’’ or ‘‘Class A’’ office space. Given theextensive attention to finishes, lighting and

other measures in BREEAM ‘‘Very Good’’and ‘‘Excellent’’ buildings, these ratings mayin fact be proxies for building quality con-trols and synonyms for ‘institutional’ gradereal estate.

To analyse further the effect of lackingquality characteristics on the magnitude ofpremiums documented in this paper, wetest how certification premiums for UScities would be affected by the removal ofbuilding quality controls and compare ourresults with those for New York City,Chicago and Washington, DC, using datafrom Eichholtz et al. (2013).10 Results ofthe propensity score weighted hedonic spe-cification for LEED and Energy Star build-ings are reported in the Appendix (TableA1). Summarising, when third-party build-ing quality controls are excluded from thehedonic specification, the certified pre-miums for LEED and Energy Star are sub-stantially larger. The results for these threemain US cities indicate that, when we donot control for building quality, results arecomparable with the London specifications.Thus, future studies that acquire a morestandardised documentation of buildingquality measures may find substantiallylower marginal effects for green officebuildings in the London commercial prop-erty market.

6. Conclusion and Discussion

Intervention from governments and specialinterest-groups to achieve higher levels ofenergy efficiency for the property sector ingeneral, and the UK in particular, hasincreased substantially over the past decade.New construction or retrofits by the UKgovernment are required to be BREEAM-certified and should have both EPC andDEC labels. New building codes incorporatestricter energy efficiency mandates and, by2018, all new construction must adhere to

Ker

nel d

ensi

ty g

reen

bui

ldin

g su

pply

Con

ditio

nal m

argi

nal e

ffect

Green building supply

Kernel density green building supply95% confidence intervalEffect of certification on price, conditional on green building supply

Figure 3. Marginal effects of certified build-ing supply (number of green buildings withina 500-metre radius): transaction sample(2000–09 period).Notes: The dotted line depicts the kernel den-sity of the certified building supply. The solidline is the marginal effect of sales per netsquare metre, given that the unit is certified,with the certified building supply. The twodashed lines denote confidence intervals.

THE VALUE OF GREEN BUILDINGS 17

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

zero-carbon standards. Ultimately, this willhave a substantial impact on the supply ofgreen buildings and the competition withinthat market. The advent of the CarbonReduction Commitment in 2012, in whichcapital market investors and tenants areresponsible for buildings’ CO2 emissions,represents another nudge towards increaseddemand for energy efficient real estate, andcan only increase the salience of sustainabil-ity for the commercial property sector.

This paper investigates the financial per-formance of London’s rapidly evolvingenvironmentally certified commercial build-ing stock, within the context of a dynamicsupply and demand framework as measuredby ex post sales transactions and achievedrents over the 2000–09 period. We docu-ment that, at the point of means, BREEAMcertification in the London office marketresults in a premium of 19.7 per cent forrents and 14.7 per cent for sales transac-tions, relative to non-certified buildings inthe same neighbourhood. Importantly, thismarginal effect is conditional upon the leaseconditions and the identity of the acquirer.We show that growth in green buildingsupply has an economically significantimpact on London’s commercial real estateprices in general and on certified real estatein particular. From 2000 to 2009, stand-alone green building rents and transactionprices were higher relative to non-greenbuildings in the same neighbourhood.However, non-green buildings that were apart of those neighbourhoods were able tocapture some of the gentrification benefits,through higher average location rents andprices. Importantly, buildings increasinglyfeature green credentials, but late entrantsdo not realise the same rental and price pre-miums as early adopters, as the marginaleffect of certification relative to non-greenbuildings in the neighbourhood decreases asthe number of certified buildings increases.

Over the sample period, the supply ofgreen buildings expanded by 1.8 per cent,resulting in some 1600 green office buildingsin 2010. Within the UK, London had thehighest growth in certified real estate wherethe supply expanded to 368 buildings as of2010, with an average of seven (five) certi-fied buildings for a given neighbourhood, atthe time of a certified rental (sales) transac-tion. Within the context of London, wherebuildings transact with an increasing supplyof green buildings surrounding them, it isthus important to take into considerationthe diffusion of environmentally certifiedreal estate. However, real estate supply inthe UK is highly regulated, with British reg-ulatory policies that limit development cre-ating considerable supply-side restrictions inthe commercial real estate market (Cheshireand Hilber, 2008). The geographical spreadof green building in the UK confirms thetheory of slow diffusion and, in the absenceof market equilibrium, there may still beprofitable investment opportunities forgreen buildings in local UK markets.

Of course, green premiums may reflectincreased construction or renovation costs—i.e. demand-side responses to changes insupply. To date, there is limited systematicevidence reporting on the marginal con-struction costs of environmentally certifiedreal estate in the UK and US commercial realestate sector.11 Furthermore, the transactioncosts associated with certification, consult-ing, design fees, contingencies and develop-ment are largely unavailable (Fisher andBradshaw, 2011). Unfortunately, currenttransaction cost data are insufficient formeaningful statistical inferences. Thus,future research incorporating constructionand redevelopment cost may provide a betterunderstanding of the ROI related to invest-ments in green building.

The results of this paper provide the firstevidence on the economic outcomes from

18 ANDREA CHEGUT ET AL.

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

investments in energy efficiency and sus-tainability in the UK marketplace. There iscurrently a measurable premium for devel-opers and investors that take their greenbuildings to market, but future outcomesare contingent upon new development,existing building regulations and the drivefor energy efficiency by the UK govern-ment. Importantly, communities are gain-ing from the advance of green buildings intheir surroundings on three fronts. First,green buildings in London are designed forreduced energy consumption, carbon emis-sions and waste. Secondly, green buildingshave a positive price impact (i.e. gentrifica-tion) on their peers, which can increasinglyimprove neighbourhoods. Finally, as greenbuildings increasingly diffuse and cluster,more and more buildings will need to com-pete on energy efficiency and sustainabilitymetrics, where premiums for green willbecome discounts for non-green, ‘brown’buildings. In combination, these positiveeconomic externalities from green buildingsin the commercial property sector can helpto mitigate the substantial negative extern-alities that buildings impose on theenvironment.

Acknowledgements

We would like to thank Thomas Saunders,Martin Townsend and Scott Steedman of BREGlobal for their assistance in collecting andinterpreting BREEAM data used in this analysis.In addition, we are grateful for the comments ofthree anonymous referees, Jaap Bos, JohnQuigley, Andy Naranjo and William Strange,participants at the 2012 ASSA Meetings andat seminars at the Centre for European EconomicResearch (ZEW) and the University of Groningen.Valentin Voigt and Ignas Gostautas also providedexcellent research assistance.

Funding

Financial support for this research has been pro-vided by the European Centre for Corporate

Engagement (ECCE) and the Royal Institutionof Chartered Surveyors (RICS). Nils Kok is sup-ported by a VENI grant from the Dutch ScienceFoundation.

Notes

1. Fuerst and McAllister (2011b) documentfor 24 BREEAM-rated properties in asample of UK office buildings that there isno significant impact on appraised capitalvalues and rental values. Estimated equiva-lent yields have a very small and negativecoefficient. In addition, there is onemarket-based initiative on this topic: theInvestment Property Databank (IPD) andHermes publish quarterly their IPD/IPFSustainable Property Index for UK ‘sustain-able’ properties. The ‘sustainable’ commer-cial properties are retrieved from the IPDdatabase, using a questionnaire coveringbuilding quality, energy efficiency, wastemanagement, building accessibility, waterefficiency and flood risk.

2. Using the Real Capital AnalyticsTransaction tool, the ranking for London’stransaction turnover remains consistentlyin the global top five.

3. LEED also operates using a point systemwith the main focus on the following ele-ments: sustainable sites, water efficiency,energy and atmosphere, materials andresources and indoor environmental quality.

4. CoStar FOCUS is a commercial propertyinformation platform covering deals, build-ing reports, town reports and values. Forthis analysis, we used the CoStar FOCUSDeals database.

5. EGi is a comprehensive commercial prop-erty database covering news, buildingreports, deals, auction, availability andoccupier data and values analysis. For thisanalysis, we utilised the Building Reportsdatabase to collect detailed buildinginformation.

6. A rent-free period is a time frame of onemonth or greater in a rental contract, duringwhich no rental payments are required. It isgenerally a concession to tenants signinglease contracts in commercial real estate.

THE VALUE OF GREEN BUILDINGS 19

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

7. Real estate investment trusts are tax-exemptreal estate companies whose tax designationrequires a 90 per cent redistribution of tax-able income to their investors.

8. One or more of the following amenities arein the transacted building or rented space:24-hour access, 24-hour security, air condi-tioning, atrium, bicycle facilities, buildingreception, central heating, commissionaire,concierge, dockside, double glazing, electricheating, entry phone, gas central heating,gym, information point, lift(s), loadingbay(s), marble ceilings, metal ceilings, naturallight, parking spaces, raised floors, roof ter-race, separate entrance, suspended ceilings.

9. Green building supply and competitionhave a linear relationship with price, theestimations of non-linear parametres arevery small and insignificant.

10. Holly et al. (2011) document that there ishigh correlation between the real estatemarkets of London and New York City.

11. For a specific case study focusing onBREEAM, BRE Centre for SustainableConstruction, BRE Trust and Cyril Sweett(2005) estimated the incremental construc-tion costs for a single building in the case itwould have been rated by BREEAM as‘‘Good’, ‘‘Very Good’’ and ‘‘Excellent’’, dis-tinguishing between natural ventilation airconditioning. For the naturally ventilatedspace (493 square metres), a ‘‘Good’’ ratingcost a maximum of 0.4 per cent more andan ‘‘Excellent’’ rating about 3.4 per cent.For an air-conditioned space (10 098square metres), maximum additional costsfor a ‘‘Good’’ rating were 0.2 per cent andfor an ‘‘Excellent’’ rating 7.0 per cent.

References

Akerlof, G. A. (1970) The market for ‘lemons’:quality uncertainty and the market mechan-ism, Quarterly Journal of Economics, 84, pp.488–500

Black, D. A. and Smith, J. A. (2004) How robustis the evidence on the effects of college qual-ity? Evidence from matching, Journal ofEconometrics, 121, pp. 99–124.

Brambor, T., Clark, W. R. and Gold, M. (2006)Understanding interaction models: improv-ing empirical analysis, Political Analysis, 14,pp. 63–82.

BRE Centre for Sustainable Construction, BRETrust and Cyril Sweett (2005) Putting a priceon sustainability. BREPress, London.

British Land (2010) Achieving more together:corporate responsibility summary report2010.

Bulan, L., Mayer, C. and Somerville, C. T. (2009)Irreversible investment, real options, andcompetition: evidence from real estate devel-opment, Journal of Urban Economics, 65, pp.237–251.

Butler, T. and Lees, L. (2006) Super-gentrifica-tion in Barnsbury, London: globalization andgentrifying global elites at the neighbourhoodlevel, Transactions of The Institute of BritishGeographers, 31, pp. 467–487.

CBRE (2010) Locational preferences of centralLondon occupiers. CBRE Research.

Chegut, A., Eichholtz, P. M. A. and Rodrigues, P.(forthcoming) The London commercialproperty price index. The Journal of RealEstate Finance and Economics.

Cheshire, P. C. and Hilber, C. A. L. (2008) Officespace supply restrictions in Britain: the politi-cal economy of market revenge, The EconomicJournal, 118, pp. F185–F221.

Clark, G. L. (2002) London in the Europeanfinancial services industry: locational advan-tage and product complementarities, Journalof Economic Geography, 2, pp. 433–453.

Debrezion, G., Pels, E. and Rietveld, P. (2007)The impact of railway stations on residentialand commercial property value: a meta-anal-ysis, The Journal of Real Estate Finance andEconomics, 35, pp. 161–180.

Eichholtz, P. M. A., Kok, N. and Quigley, J. M.(2010) Doing well by doing good: green officebuildings, American Economic Review, 100,pp. 2494–2511.

Eichholtz, P. M. A., Kok, N. and Quigley, J. M.(2011) Who rents green? Ecological responsive-ness and corporate real estate. Working paper,University of California at Berkeley.

Eichholtz, P. M. A., Kok, N. and Quigley, J. M.(2013) The economics of green building,Review of Economics and Statistics, 95 (1), pp.50–63

20 ANDREA CHEGUT ET AL.

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

Fisher, L. and Bradshaw, W. (2011) Green build-ing and the organization of development. Paperpresented at the 46th AREUEA Conference,Denver, January.

Fuerst, F. and McAllister, P. (2011a) Green noiseor green value? Measuring the effects of envi-ronmental certification on office values, RealEstate Economics, 39, pp. 45–69.

Fuerst, F. and McAllister, P. (2011b) The impactof energy performance certificates on therental and capital values of commercial prop-erty assets, Energy Policy, 39, pp. 6608–6614.

Grenadier, S. R. (2002) Option exercise games:an application to the equilibrium investmentstrategies of firms, Review of Financial Stud-ies, 15(3), pp. 691–721.

Holly, S., Pesaran, M. H. and Yamagata, T.(2011) The spatial and temporal diffusion ofhouse prices in the UK, Journal of UrbanEconomics, 69, pp. 2–23.

Jones Lang Lasalle (2009) The performance mea-surement challenge. Jones Lang Lasalle, Chi-cago, IL.

Knox-Hayes, J. (2009) The developing carbonfinancial service industry: expertise, adapta-tion and complementarity in London andNew York, Journal of Economic Geography, 9,pp. 749–777.

Kok, N. and Jennen, M. G. J. (2012) The impactof energy labels and accessibility on officerents, Energy Policy, 46, pp. 489–497.

Kok, N., Bauer, R. and Eichholtz, P. M. (2011)GRESB research report. GRESB, Maastricht.

Kok, N., McGraw, M. and Quigley, J. M.(2011) The diffusion of energy efficiency in

building, American Economic Review, 101,pp. 77–82.

Margolis, J. D. and Walsh, J. P. (2003) Miseryloves company: rethinking social initiativesby business, Administrative Science Quarterly,48, pp. 268–305.

Miller, N., Spivey, J. and Florance, A. (2008)Does green pay off?, Journal of Real EstatePortfolio Management, 14, pp. 385–400.

Nelson, A. and Rakau, A. J. (2010) Green build-ings: a niche becomes mainstream. DeutscheBank Research, Frankfurt am Main.

Rosen, S. (1974) Hedonic prices and implicitmarkets: product differentiation in pure com-petition, Journal of Political Economy, 82, pp.34–55.

Turban, D. B. and Greening, D. W. (1997) Cor-porate social performance and organizationalattractiveness to prospective employees,Academy of Management Journal, 40, pp.658–672.

Wheaton, W., Torto, R. and Evans, P. (1997)The cyclic behaviour in the greater Londonoffice market, Journal of Real Estate Financeand Economics, 15, pp. 77–92.

White, H. (1980) A heteroskedasticity-consistentcovariance matrix estimator and a direct testfor heteroskedasticity, Econometrica, 48, pp.817–838.

Yoshida, J. and Sugiura, A. (2011) Which green-ness is valued? Evidence from green condomi-niums in Tokyo. Paper presented at the 46thAnnual AREUEA Conference, Denver,January.

THE VALUE OF GREEN BUILDINGS 21

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

Appendix

Table A1. The value of green certification in US cities (dependent variable: logarithm of salesprice per square foot)

(1) (2) (3) (4)Full sample Chicago Washington New York

Green certification 0.133*** 0.324*** 0.334*** 0.245[0.0167] [0.0591] [0.0594] [0.153]

Quality characteristicsClass A 0.213***(1 = yes) [0.0409]Class B 20.0377(1 = yes) [0.0336]Building size 20.0487*** 20.123*** 20.170*** 0.0155(log) [0.00989] [0.0415] [0.0215] [0.0647]Age 0–5 years 20.0242 0.110 0.0403 21.911(1 = yes) [0.0445] [0.122] [0.0768] [1.178]Age 5–10 years 0.353*** 0.427*** 0.655*** 20.317(1 = yes) [0.0344] [0.0945] [0.0827] [0.222]Age 10–20 years 0.115*** 0.0630 0.230*** 0.555***(1 = yes) [0.0330] [0.110] [0.0770] [0.189]Age 20–30 years 0.0870*** 20.275*** 0.224*** 0.308**(1 = yes) [0.0262] [0.0866] [0.0609] [0.129]Age 30–40 years 0.0449 20.124* 0.149** 0.162(1 = yes) [0.0290] [0.0728] [0.0644] [0.162]Renovated 0.0154 0.0675 0.0231 0.405***(1 = yes) [0.0191] [0.0443] [0.0364] [0.123]Storey medium 0.167*** 0.474*** 0.345*** 20.901***(1 = yes) [0.0232] [0.109] [0.0441] [0.215]Storey high 0.338*** 1.170*** 0 20.611***(1 = yes) [0.0285] [0.124] [0] [0.231]Amenities 0.0324* 20.337*** 20.146*** 0.132(1 = yes) [0.0189] [0.0586] [0.0389] [0.103]

Transportation networksPublic transport 20.124*** 20.471*** 20.259*** 20.198(1 = yes) [0.0263] [0.0733] [0.0680] [0.129]

Constant 5.078*** 5.332*** 7.221*** 6.251***[1.952] [0.511] [0.282] [0.751]

Year fixed effects Yes Yes Yes Yes

Observations 5993 615 597 363Green 686 34 22 16R2 0.662 0.731 0.442 0.386Adjusted R2 0.616 0.705 0.404 0.327

Notes: Specifications are based on propensity score weighted hedonic regressions: Green certifica-tion corresponds to LEED or energy star labelled properties. Full sample results correspond tothose reported in Eichholtz et al. (2013). Sub-sample rental and sales results are presented forChicago, Washington, DC, and New York City. *, ** and *** denotes significance at the 10, 5 and1 per cent levels respectively.Source: Eichholtz et al. (2013).

22 ANDREA CHEGUT ET AL.

at UNIV CALIFORNIA BERKELEY LIB on May 25, 2013usj.sagepub.comDownloaded from

![Lift Passenger Demand in Office Buildings - ELE-LIFElab.ele-life.com/pdf/traffic_demand.pdf · Lift Passenger Demand in Office Buildings ... Transportation Handbook.[1] ... sengers](https://img.pdfslide.us/doc/110x75/5ad4454a7f8b9a075a8b7482/lift-passenger-demand-in-office-buildings-ele-passenger-demand-in-office-buildings.jpg)