Embed Size (px)

Citation preview

Supply

Chapter 5

A family buys a half-gallon of orange juice at the supermarket. An author hires a graduate student to translate a book. A store sells a bicycle to a woman over the Internet.

Each of these exchanges involves a buyer and a seller. In this chapter, we will look at the “supply side” of the marketplace.

Section 1: Understanding Supply

Imagine you own a factory that produces sunglasses and that

the price of sunglasses begins to rise rapidly. Will you produce

more pairs of sunglasses, fewer pairs of sunglasses, or the same

number as before?

In this section, you will learn what the law of supply says about this

situation.

How do producers decide how much to supply?

• Supply – is the amount of goods available.

• According to the Law of Supply, the higher the price, the larger the quantity produced.

• Quantity supplied – the amount a supplier is willing and able to supply at a certain price.

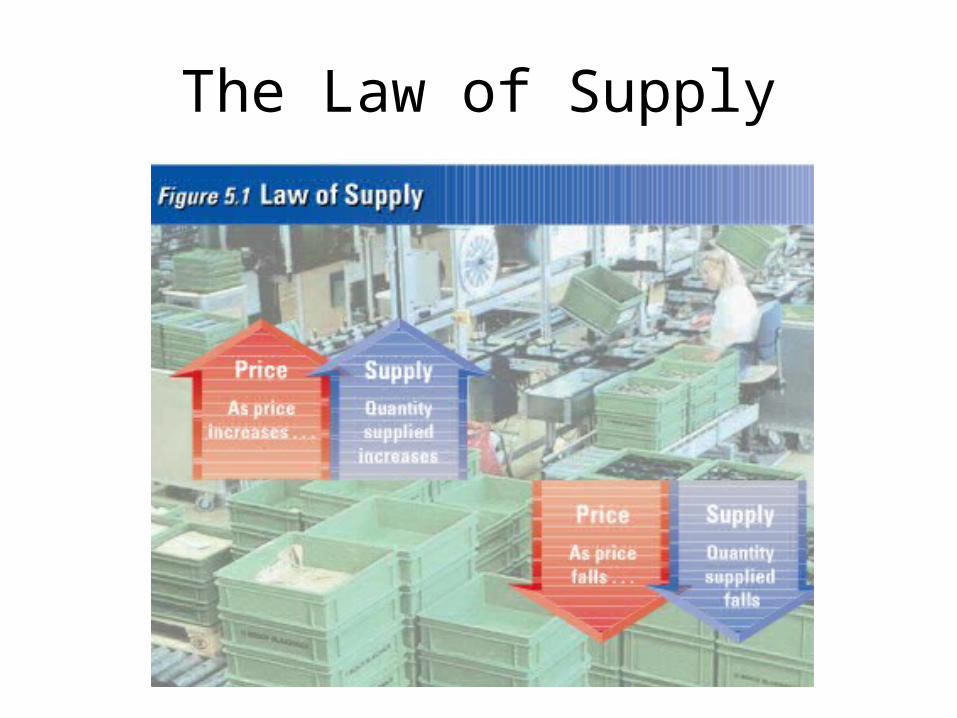

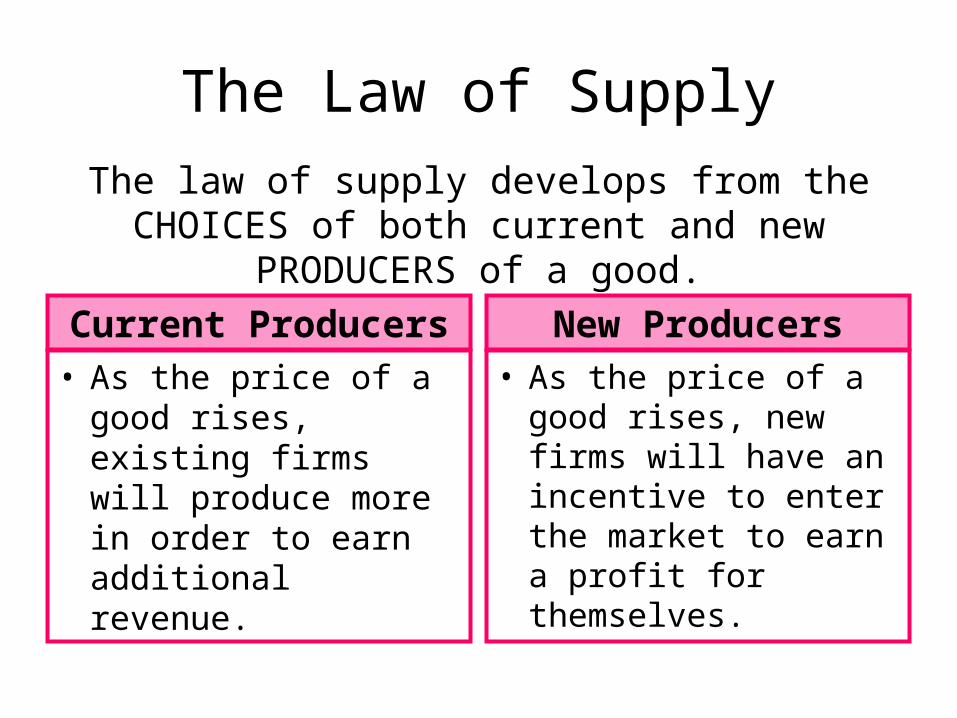

The Law of Supply

The Law of Supply

• As the price of a good rises, existing firms will produce more in order to earn additional revenue.

• As the price of a good rises, new firms will have an incentive to enter the market to earn a profit for themselves.

The law of supply develops from the CHOICES of both current and new PRODUCERS of a good.

Current Producers New Producers

Current Producers: Higher Production

• If a firm is already earning a profit by selling a good, then an increase in the price will increase the firm’s profit.

• The promise of higher revenues for each sale also encourages the firm to produce more.

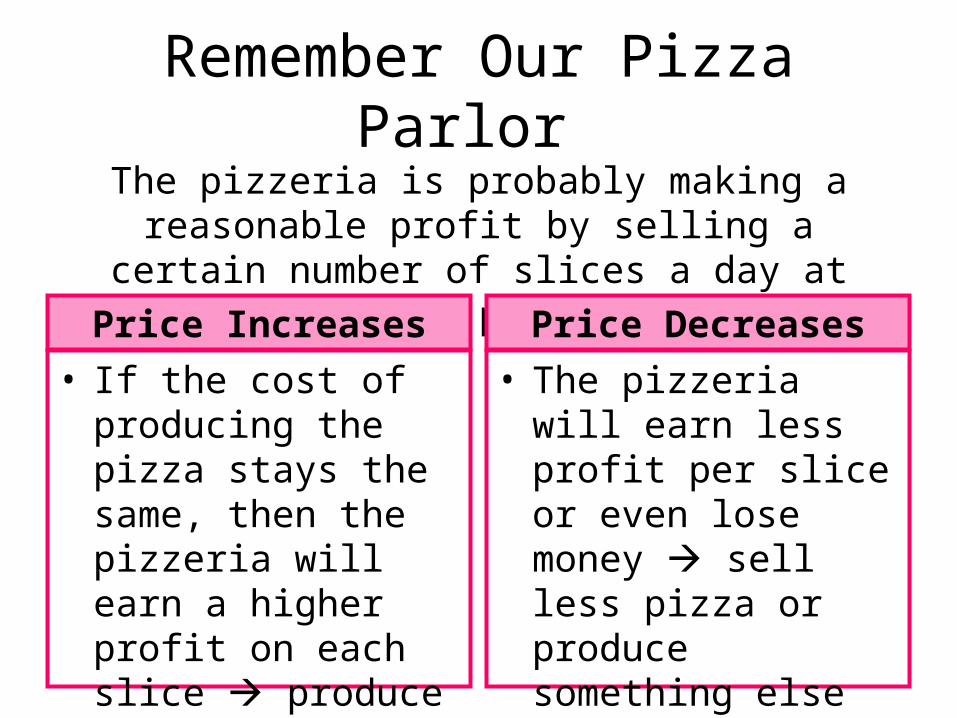

Remember Our Pizza Parlor

• If the cost of producing the pizza stays the same, then the pizzeria will earn a higher profit on each slice produce more pizza

• The pizzeria will earn less profit per slice or even lose money sell less pizza or produce something else to yield more profit.

The pizzeria is probably making a reasonable profit by selling a certain number of slices a day at

market price.

Price Increases Price Decreases

New Producers: Market Entry

• If the price of a good rises, a firms has a good opportunity to make money. This encourages others to make a “safe-bet” and enter the market.

• In this way, rising prices draw new firms into a market and add to the quantity supplied of the good.

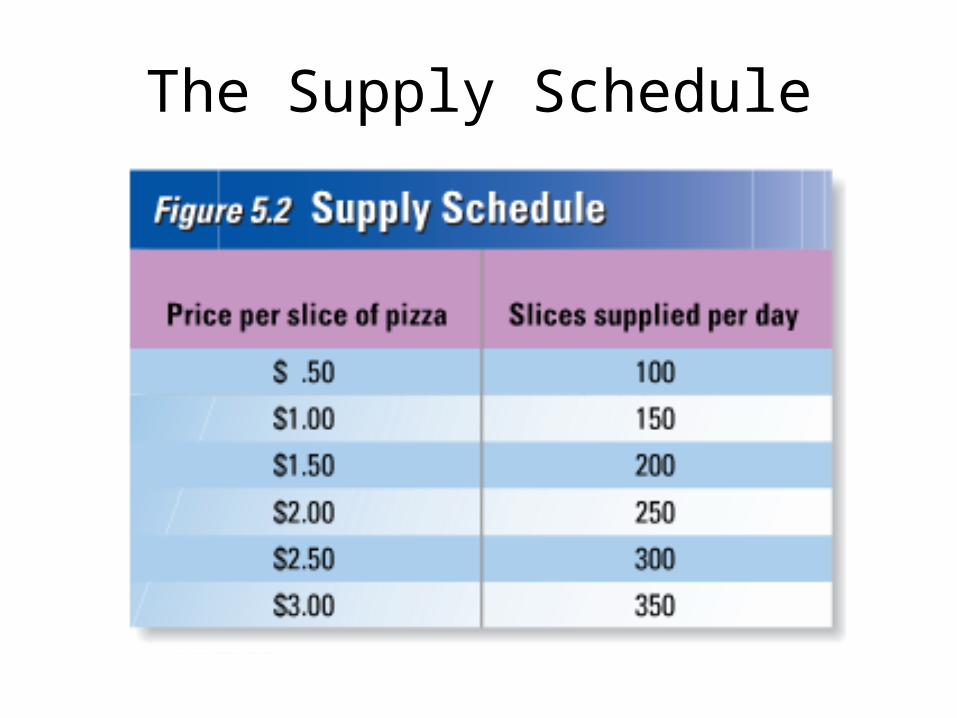

The Supply Schedule

• A supply schedule shows the relationship between price and quantity supplied for a specific good.

The Supply Schedule

The Supply Schedule

• Similar to a demand schedule, a supply schedule lists supply for a specific set of conditions. The schedule shows how the PRICE of good and ONLY THE PRICE of the good affects output. All other factors that could change output are held constant.

A Change in the Quantity Supplied

• The number of goods supplied at a specific price is the quantity supplied at that price.

• A rise or fall in the price of a good will cause the quantity supplied to change, but not the supply schedule. The change is reflected on the SAME supply schedule.

• When a factor other than price affects output, we build a NEW supply schedule to show the NEW market conditions.

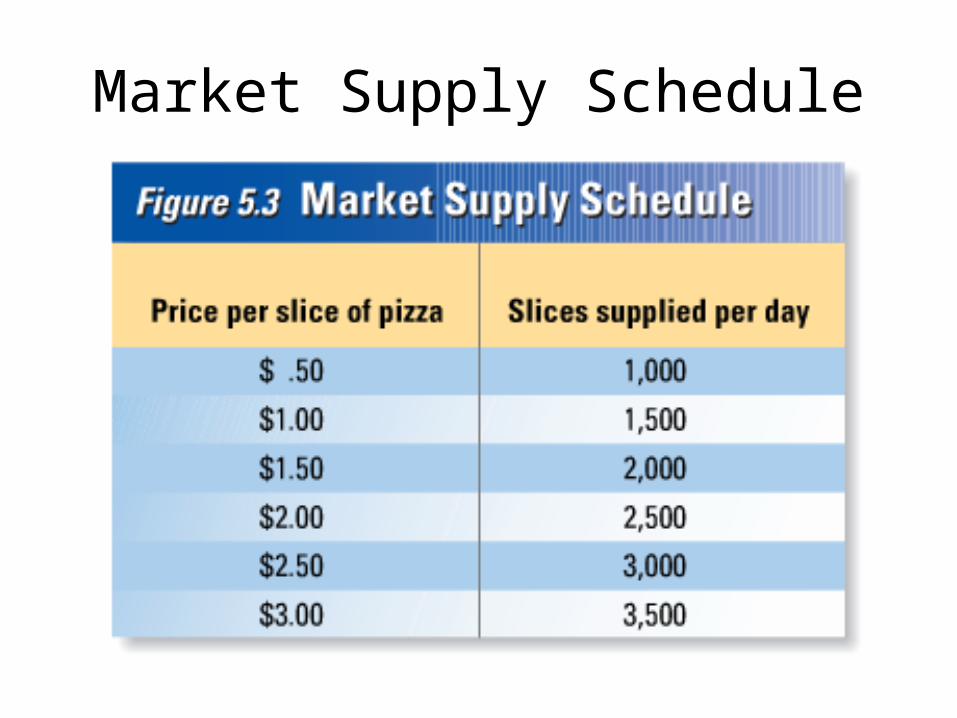

Market Supply Schedule

• All of the supply schedules of individual firms in a market can be added to create a market supply schedule.

• The market supply schedule lists how much of a good all suppliers will offer at different prices.

Market Supply Schedule

The Supply Graph

• When all data points in the supply schedule are graphed, they create a supply curve.

• A supply curve is very similar to a demand curve, expect that the horizontal axis now measures the quantity of the good supplied, not the quantity demanded.

• A supply curve for all firms creates a market supply curve.

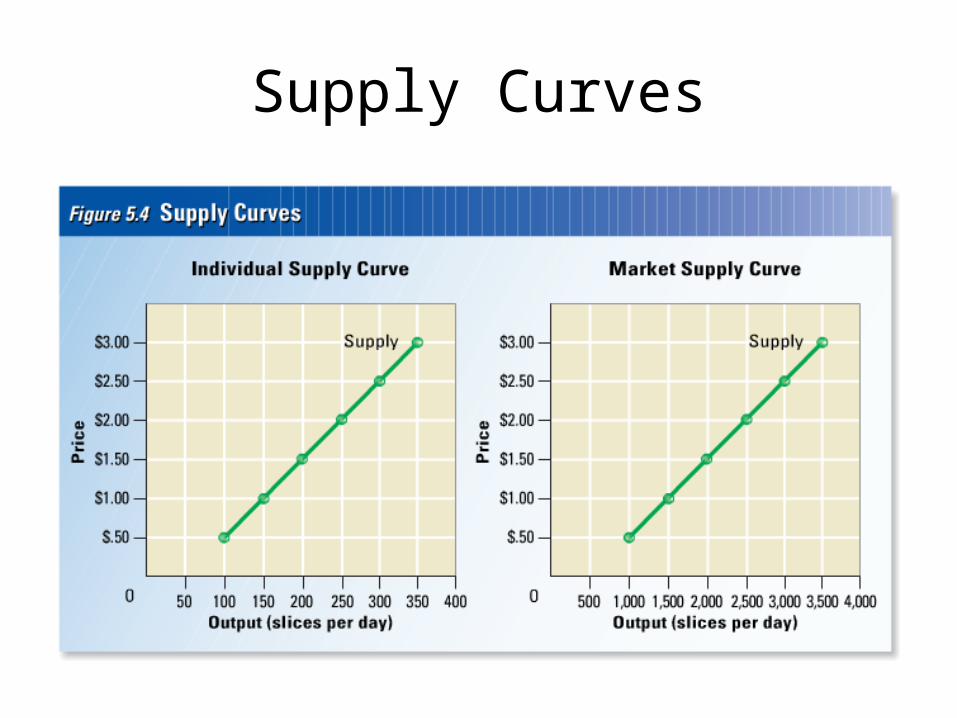

Supply Curves

Supply and Elasticity

• Elasticity of supply is based on the same concept of elasticity of demand. Rather than measuring how consumers would react to a change in price as with the elasticity of demand, elasticity of supply tells how firms will respond to changes in the price of a good.

• The values inelastic, elastic, and unitary elastic represent the same values of elasticity of supply.

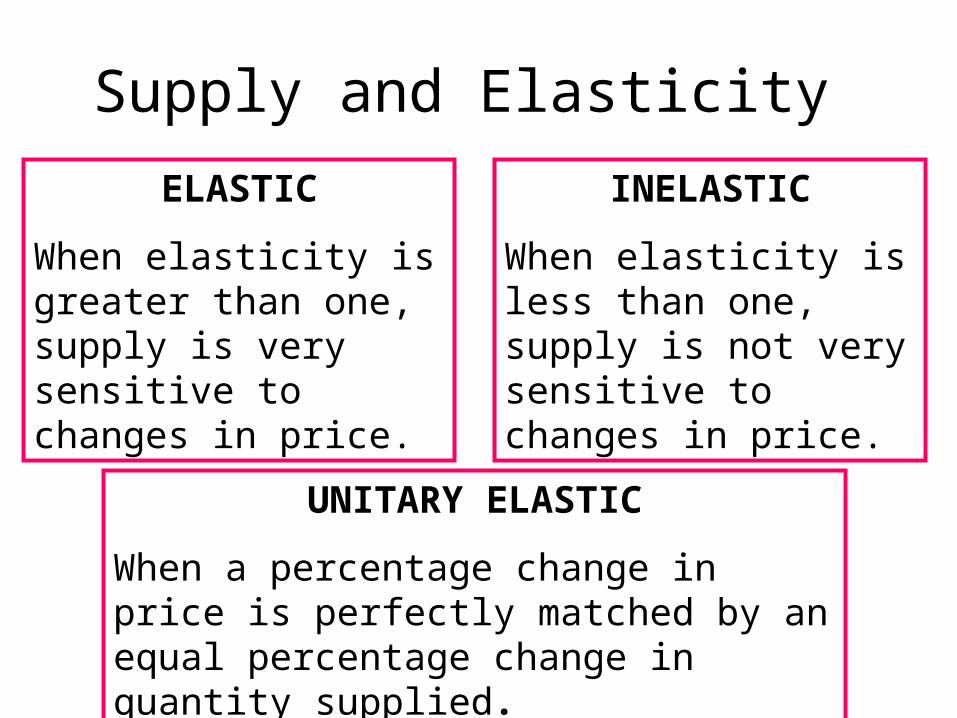

Supply and Elasticity

ELASTIC

When elasticity is greater than one, supply is very sensitive to changes in price.

INELASTIC

When elasticity is less than one, supply is not very sensitive to changes in price.

UNITARY ELASTIC

When a percentage change in price is perfectly matched by an equal percentage change in quantity supplied.

Elasticity of Supply

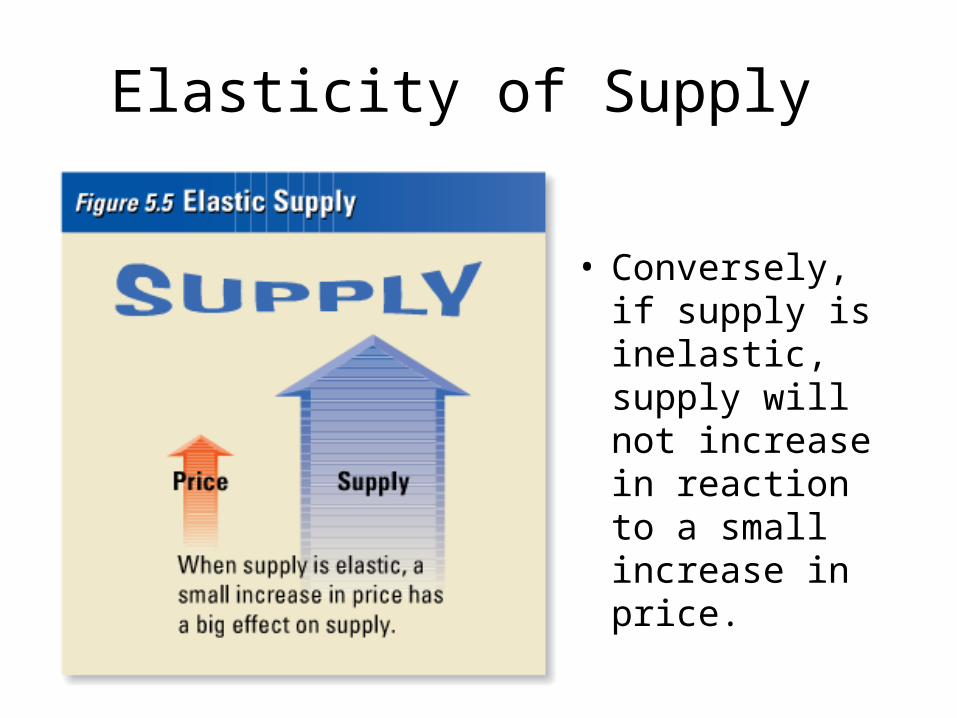

• Conversely, if supply is inelastic, supply will not increase in reaction to a small increase in price.

What determines whether the supply of a good will be elastic or

inelastic?

TIME

Elasticity of Supply and Time

• In the short run, a firm cannot easily change its output level, so supply is inelastic.

• In the long run, firms are more flexible, so supply is more elastic.

Elasticity of Supply in the Short Run

• An orange grove is one example of a business that has difficulty adjusting to a change in price in the short term.

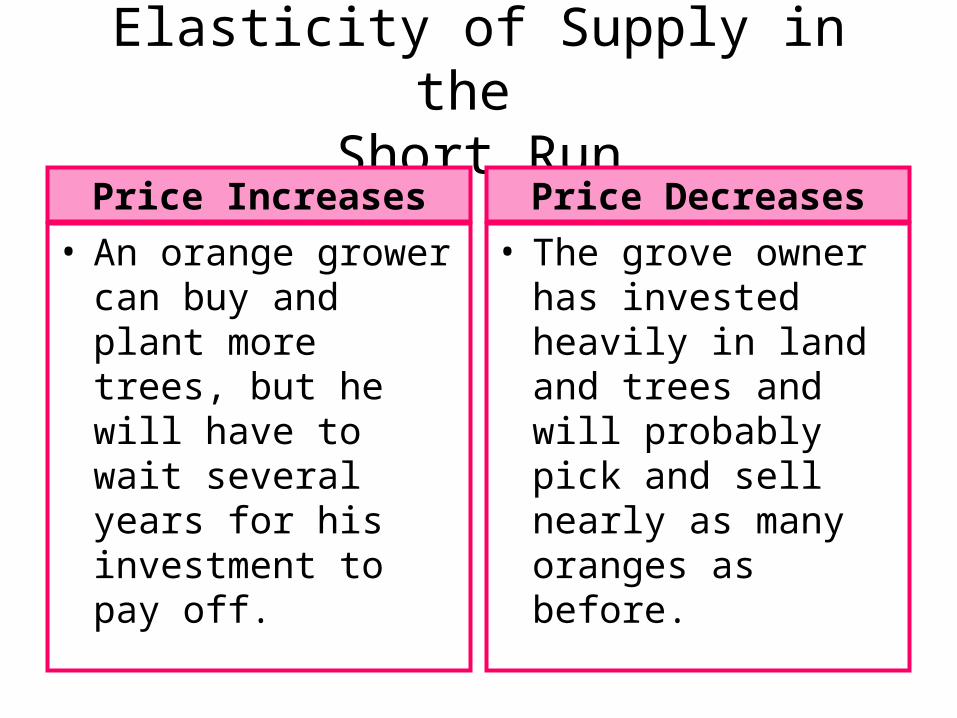

Elasticity of Supply in the Short Run

• An orange grower can buy and plant more trees, but he will have to wait several years for his investment to pay off.

• The grove owner has invested heavily in land and trees and will probably pick and sell nearly as many oranges as before.

Price Increases Price Decreases

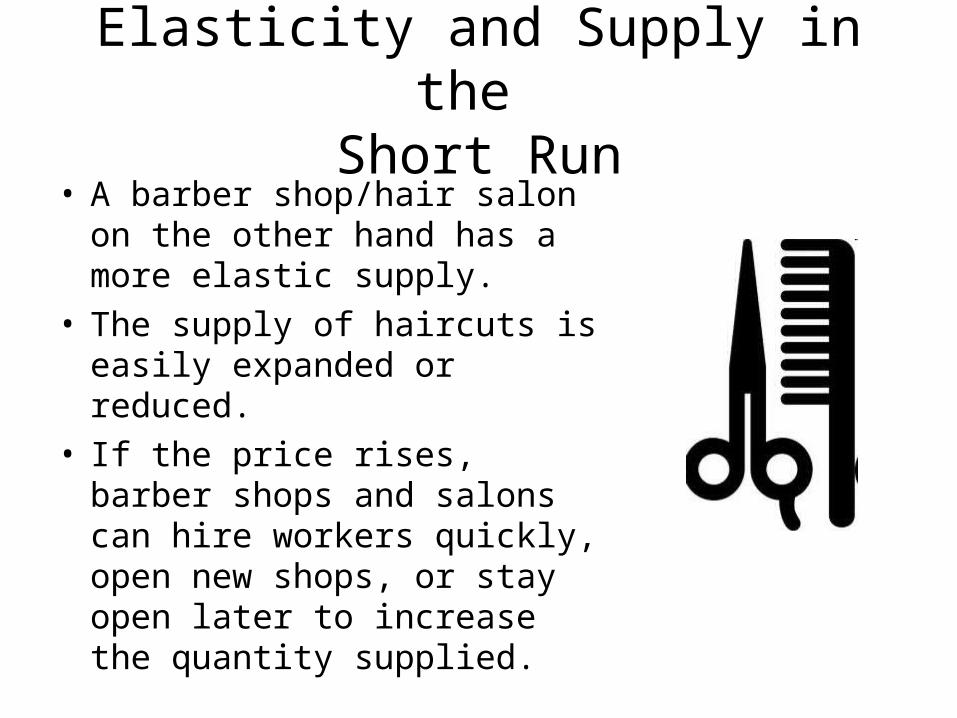

Elasticity and Supply in the Short Run

• A barber shop/hair salon on the other hand has a more elastic supply.

• The supply of haircuts is easily expanded or reduced.

• If the price rises, barber shops and salons can hire workers quickly, open new shops, or stay open later to increase the quantity supplied.

Elasticity in the Long Run

• Supply becomes more elastic if the supplier has a long time to respond to a price change.

• Consider our orange grower… after a few years he/she will be able to increase the supply of oranges as the tree begin to bear fruit and therefore be able to sell many more oranges at the high market price.

Explain whether you think the supply of the following goods

is elastic or inelastic, and why.

Hotel Rooms

Hotel Rooms

Inelastic – the number of hotel rooms can be increased, but not

quickly or easily.

Taxi Rides

Taxi Rides

Elastic – taxi drivers could work more or fewer hours, or taxi

companies can put more taxis into use

Painting by Vincent Van Gogh

Painting by Vincent Van Gogh

Inelastic – supply remains constant... A dead artist cannot

paint!

Photographs

Photographs

Elastic – more or fewer photographs could be produced if

the price changes

Economic Cartoon

Section 2: Cost of Production

Think about fast-food restaurants… How do the owners

of these restaurants know how much food to produce each day?

What would happen to the owner’s profits if the restaurant produced too much or too little

food?

How much to produce?

Consider a firm that produces beanbags. The firm’s factory has

one sewing machine and one pair of scissors. The firm’s inputs are

workers and materials (cloth, thread, beans). As the number of workers

increases, what happens to the quantity of beanbags produced?

Labor and Output

• One of the basic questions any business owner has to answer is how many workers to hire.

• To answer this question, owners have to consider how the number of workers they hire will affect their total production.

Beanbag Factory

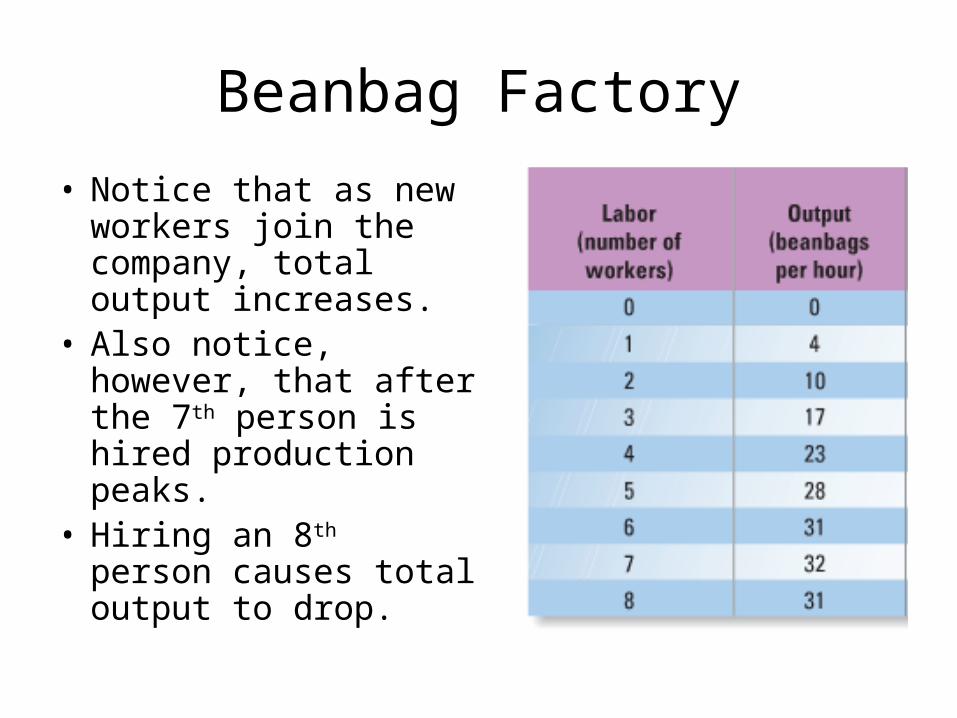

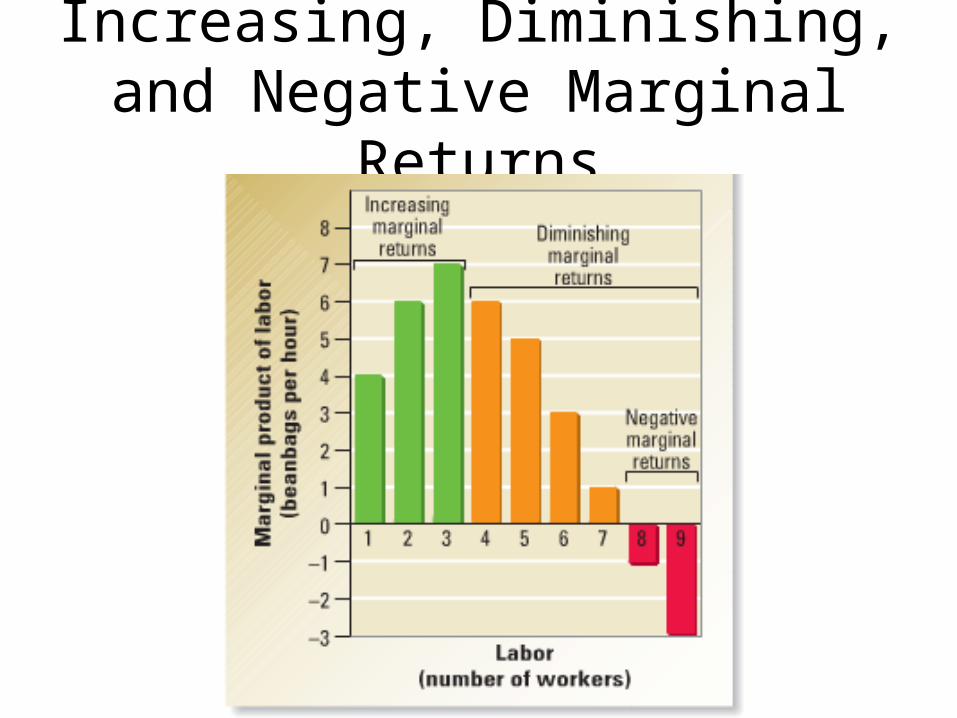

• Notice that as new workers join the company, total output increases.

• Also notice, however, that after the 7th person is hired production peaks.

• Hiring an 8th person causes total output to drop.

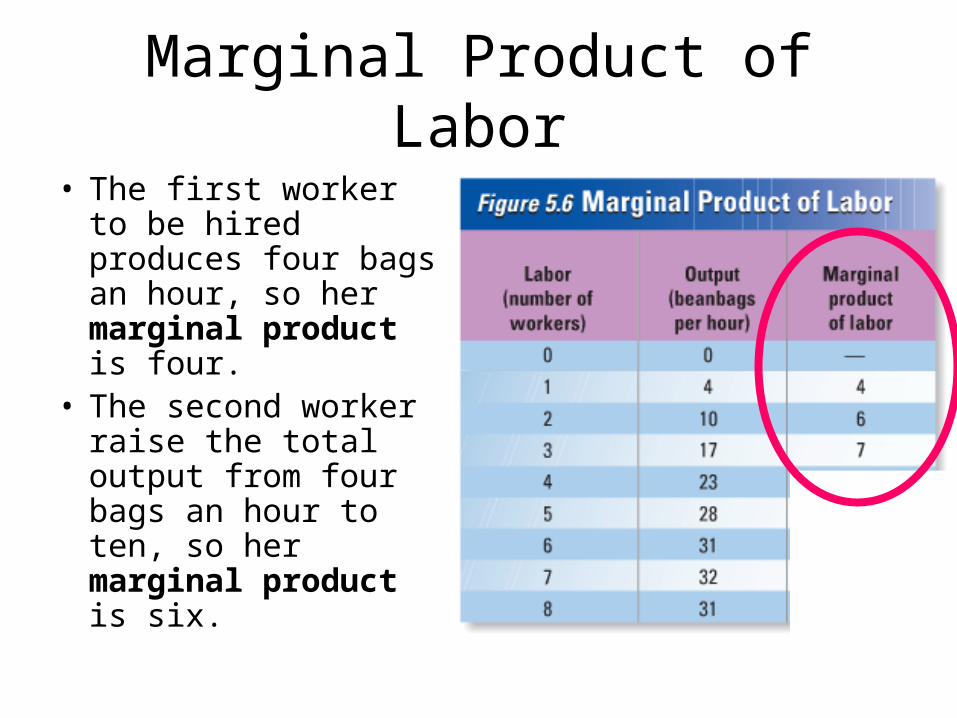

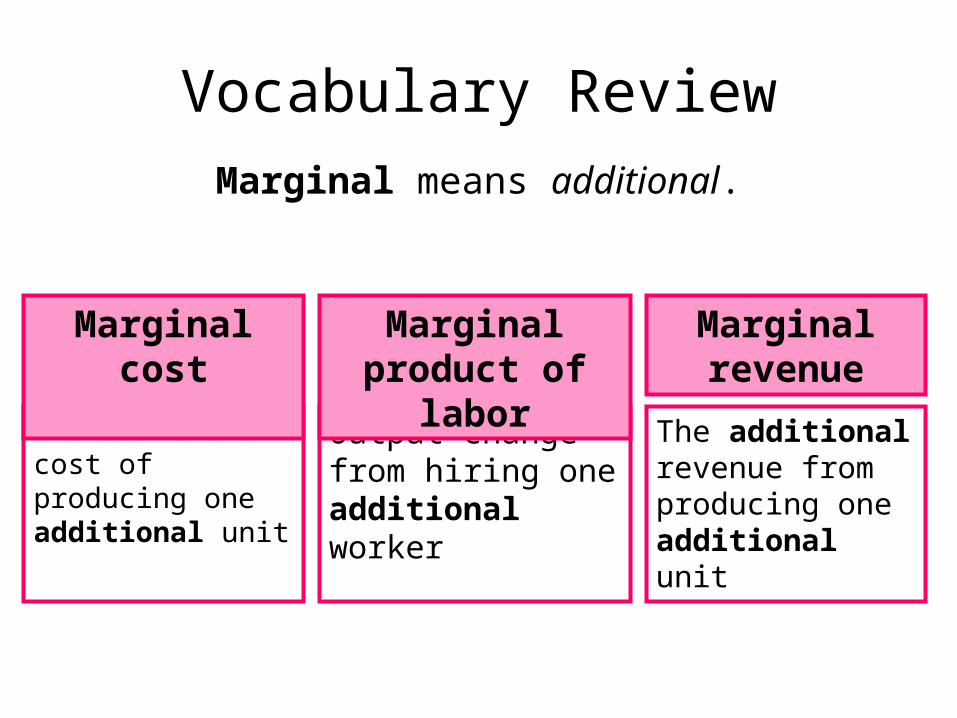

Marginal Product of Labor

• Marginal Product of Labor is the change in output from hiring one more worker.

• This is called the marginal product because it measures the change in output at the margin, where the last worker has been hired or fired.

Marginal Product of Labor

• The first worker to be hired produces four bags an hour, so her marginal product is four.

• The second worker raise the total output from four bags an hour to ten, so her marginal product is six.

Increasing Marginal Returns

• The marginal product of labor increases for the first three workers because there are three tasks involved in making a beanbag: cut and sew cloth into the correct shape, stuff with beans, and sew closed.

• Adding more workers allows for specialization of tasks, thereby increasing output per worker.

Increasing Marginal Returns

• This is known as increasing marginal returns - - a level of production in which the marginal product of labor increases as the number of workers increase.

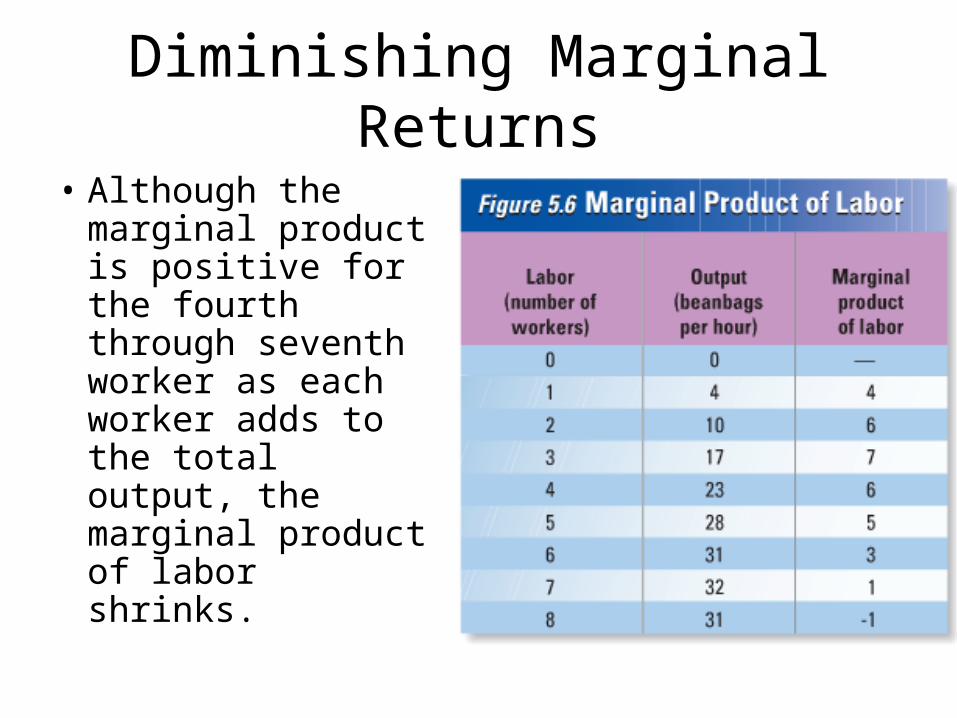

Diminishing Marginal Returns

• Although the marginal product is positive for the fourth through seventh worker as each worker adds to the total output, the marginal product of labor shrinks.

Why???

After the beanbag firm hires its first three workers, one for each task, the

benefits of specialization end.

Diminishing Marginal Returns

• After the benefits of specialization ends, adding more workers increases total output, but at a decreasing rate.

• This is known as diminishing marginal returns, a level of production in which the marginal product of labor decreases as the number of workers increases.

Diminishing Marginal Returns

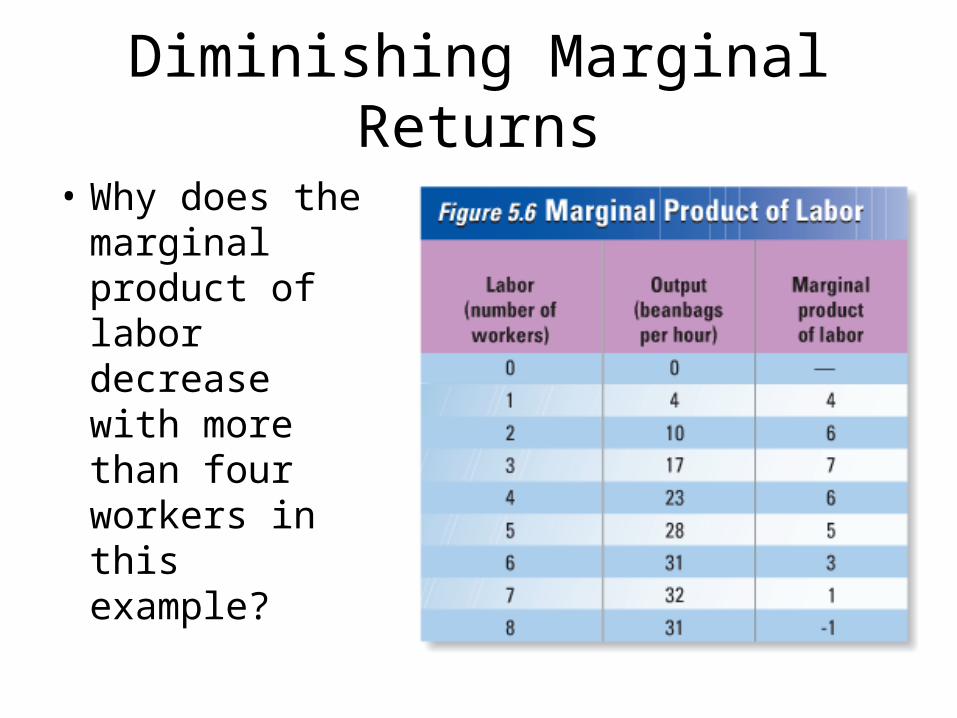

• Why does the marginal product of labor decrease with more than four workers in this example?

Diminishing Marginal Returns

• It decreases because the workers are working with a limited amount of capital.

• Remember, capital is any human-made resource that is used to produce other goods.

• In this example, capital is represented by the factory’s single sewing machine. When there are more than three workers, workers have to share the machine, thus slowing production.

Negative Marginal Returns

• The problem gets worse as more workers are hired and the amount of capital remains constant.

• Wasted time waiting at a machine means that additional workers will add less and less to total output at the factory.

• Hence, adding the eighth worker can actually decrease output.

Increasing, Diminishing, and Negative Marginal Returns

Production Costs

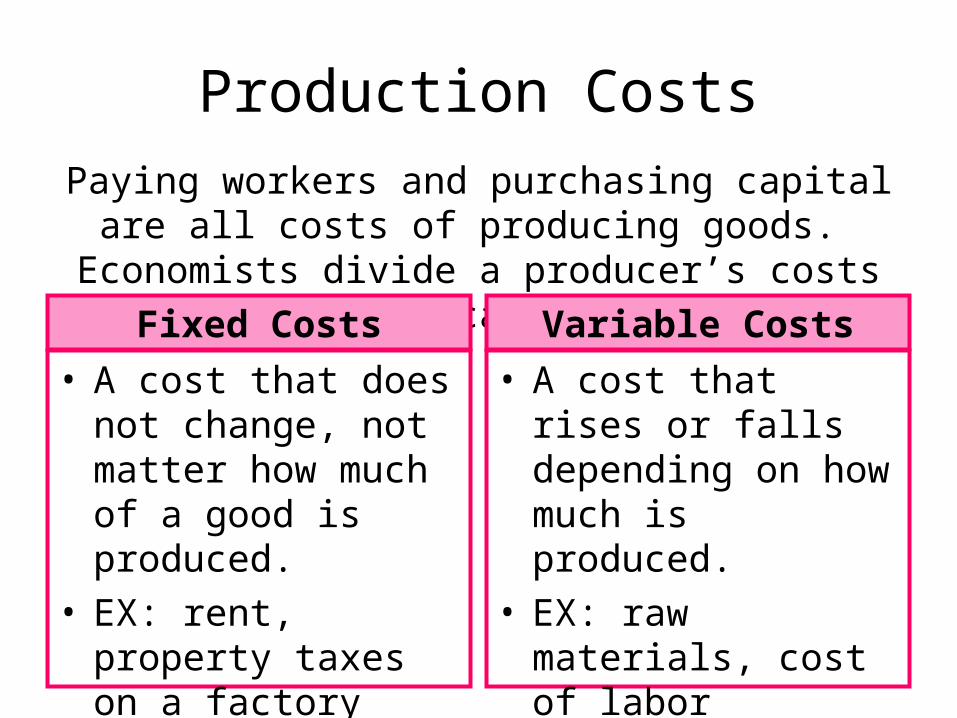

• A cost that does not change, not matter how much of a good is produced.

• EX: rent, property taxes on a factory

• A cost that rises or falls depending on how much is produced.

• EX: raw materials, cost of labor

Paying workers and purchasing capital are all costs of producing goods. Economists divide a

producer’s costs into two categories.

Fixed Costs Variable Costs

Production Costs

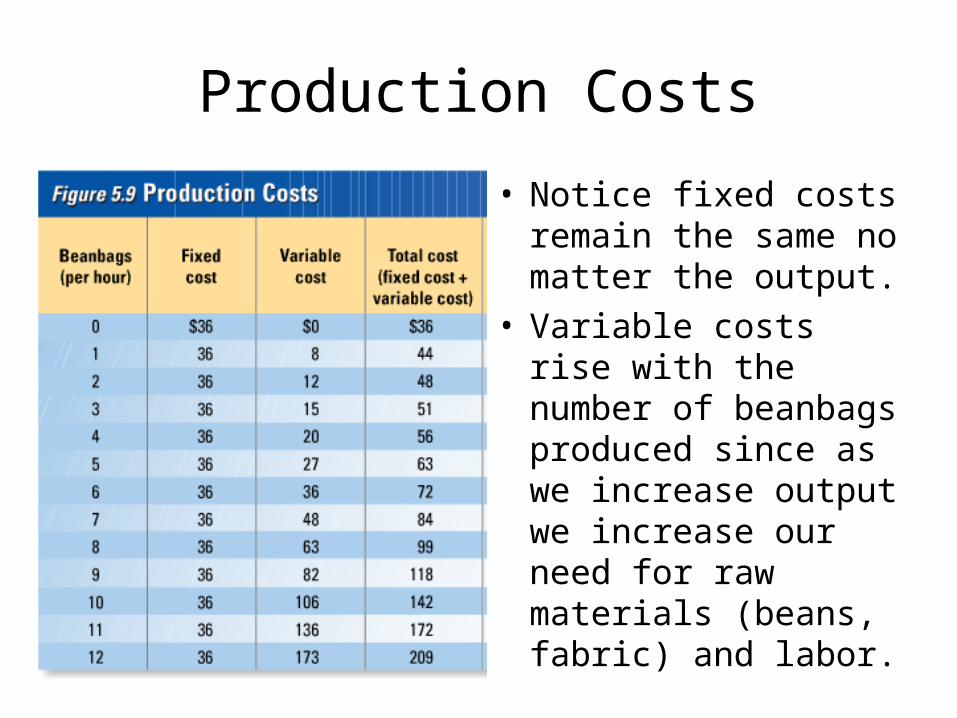

• Notice fixed costs remain the same no matter the output.

• Variable costs rise with the number of beanbags produced since as we increase output we increase our need for raw materials (beans, fabric) and labor.

Marginal Costs

• Marginal Cost is the additional cost of producing one more unit.

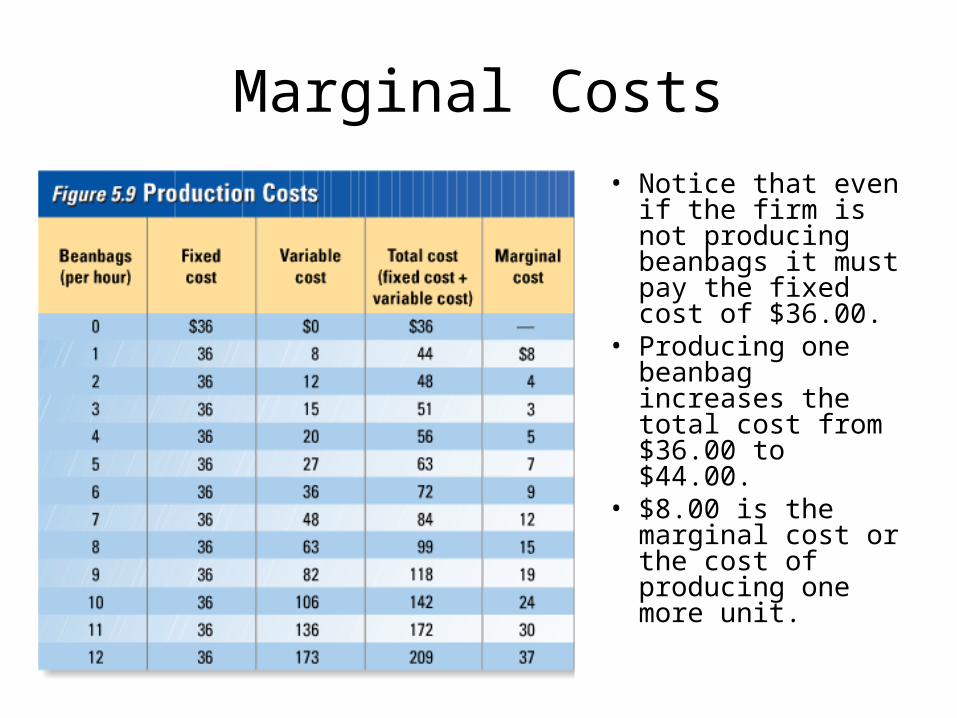

Marginal Costs

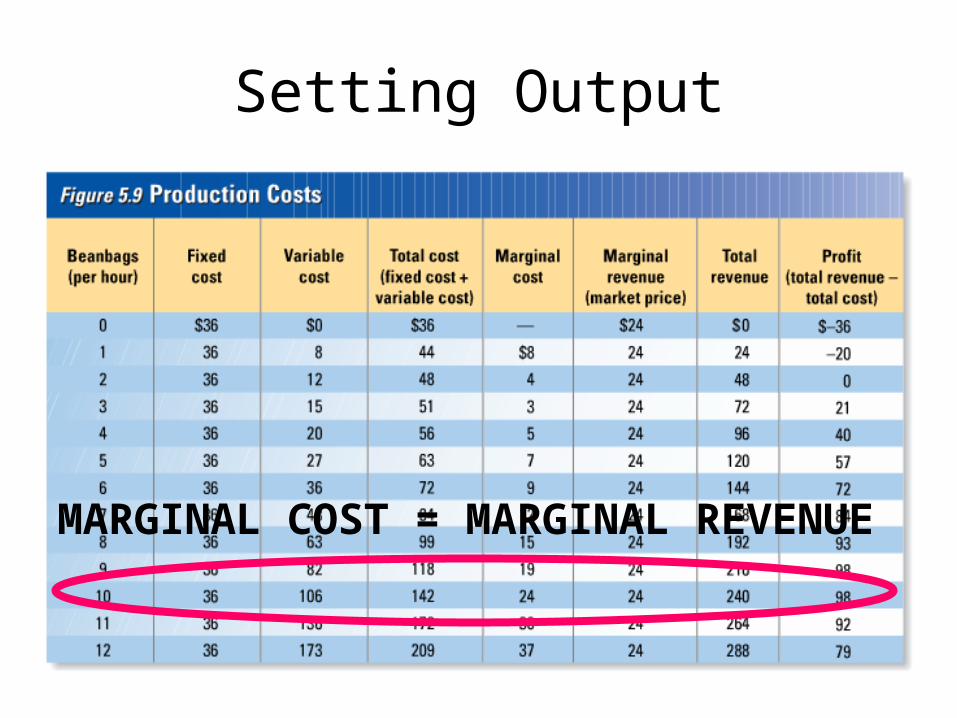

• Notice that even if the firm is not producing beanbags it must pay the fixed cost of $36.00.

• Producing one beanbag increases the total cost from $36.00 to $44.00.

• $8.00 is the marginal cost or the cost of producing one more unit.

Marginal Costs

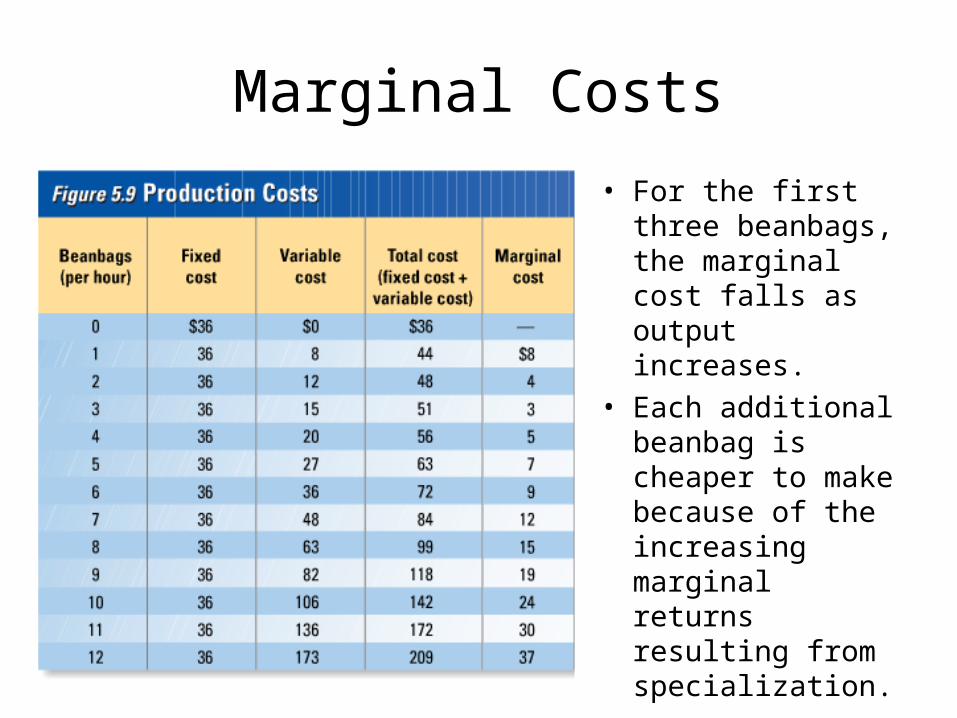

• For the first three beanbags, the marginal cost falls as output increases.

• Each additional beanbag is cheaper to make because of the increasing marginal returns resulting from specialization.

Marginal Costs

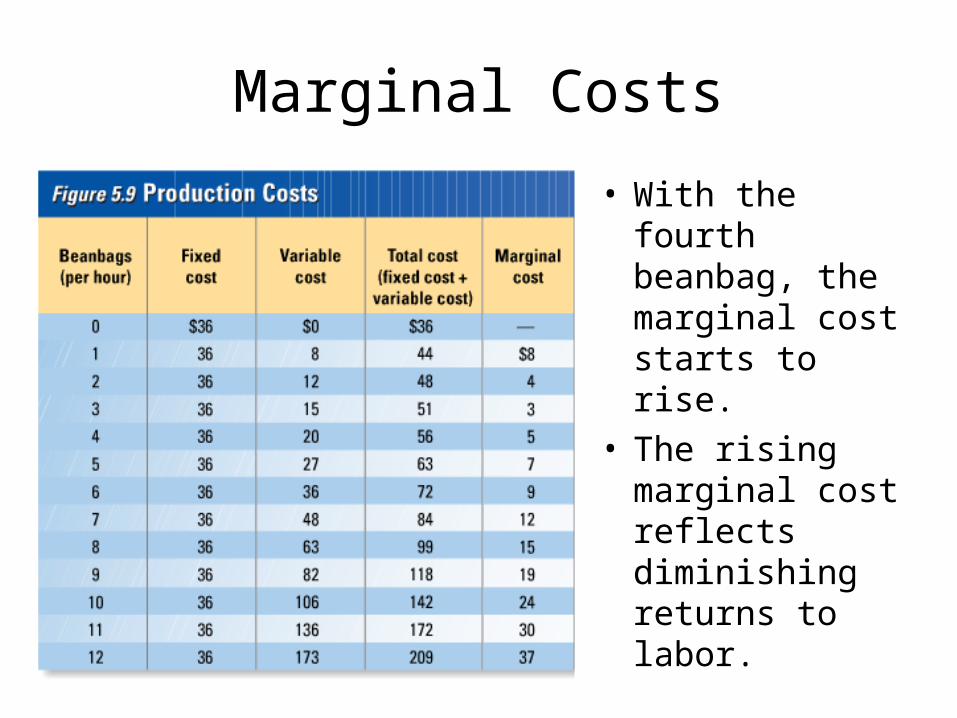

• With the fourth beanbag, the marginal cost starts to rise.

• The rising marginal cost reflects diminishing returns to labor.

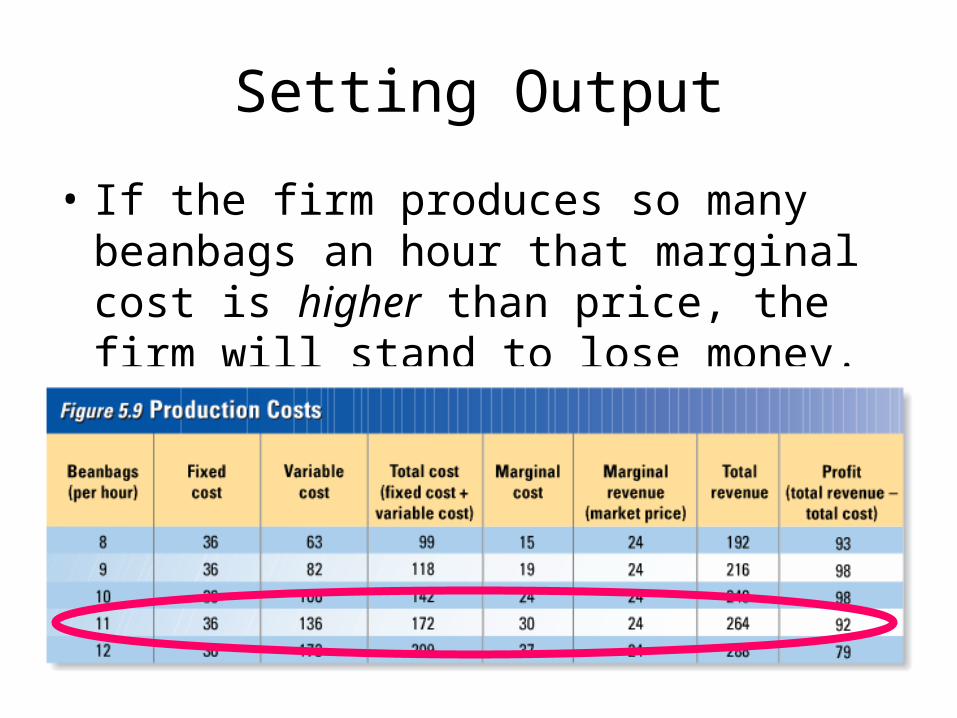

Setting Output

Remember… our goal is to make a PROFIT!

Setting Output

• To make the highest profit possible we have to find the level of output that has the biggest gap between total revenue and total cost.

• To do this, we have to find the level of output where the marginal revenue is equal to marginal cost.

Marginal Revenue

• Marginal revenue is the additional income from selling one more unit of a good.

• If the firm has no control over the market price, the marginal revenue equals the market price.

Setting Output

MARGINAL COST = MARGINAL REVENUE

Setting Output

• If the firm produces so many beanbags an hour that marginal cost is higher than price, the firm will stand to lose money.

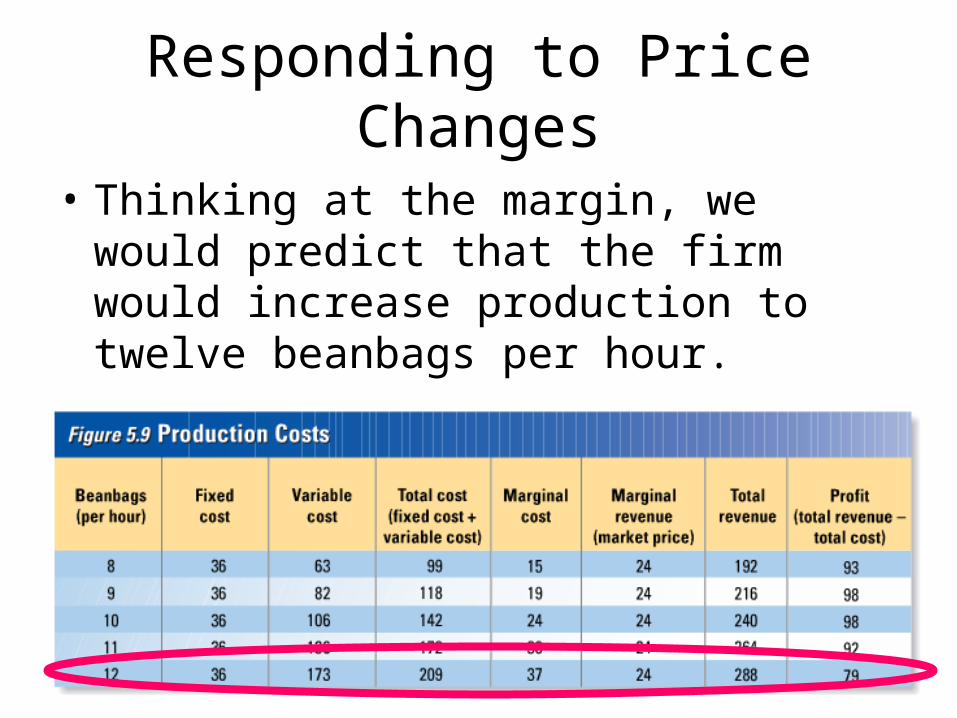

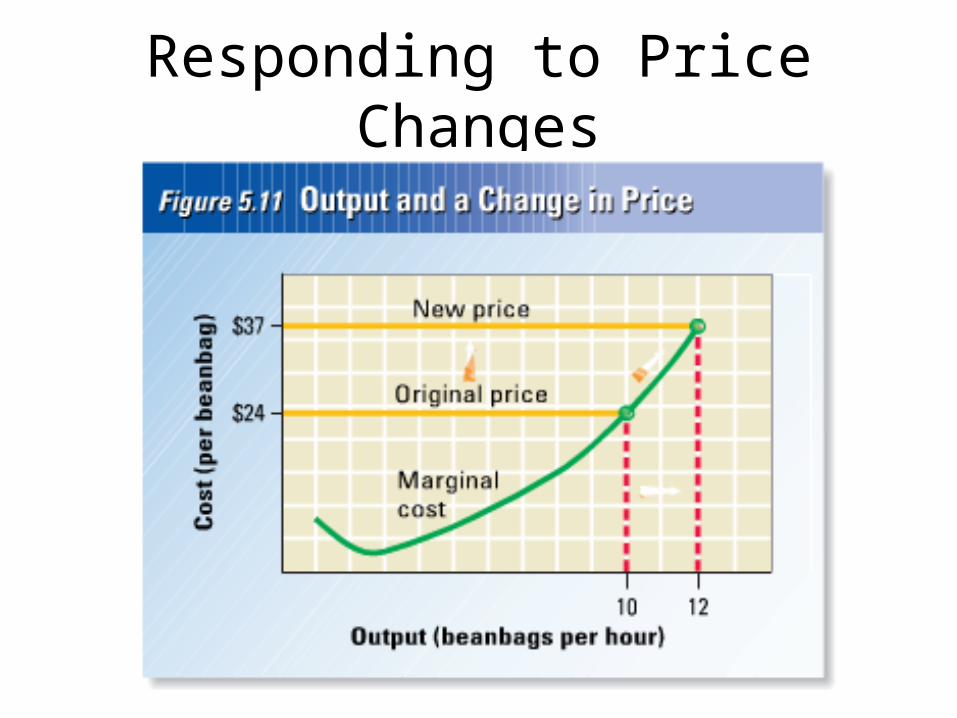

What would happen if the price of a beanbag rose from$24.00 to

$37.00?

Responding to Price Changes

• Thinking at the margin, we would predict that the firm would increase production to twelve beanbags per hour.

• This is the LAW OF SUPPLY!

Responding to Price Changes

The Shutdown Decision

• A firm should remain open if the total revenue from the goods and services is greater than the cost of keeping it open (operating costs).

Vocabulary Review

Output change from hiring one additional worker

The additional cost of producing one additional unit

Marginal means additional.

Marginal product of labor

Marginal cost

The additional revenue from producing one additional unit

Marginal revenue

Maximizing Profit Worksheet

Activity: Production and Costs

Section 3: Changes in Supply

As with demand, the entire supply curve can shift to the right

or left because of factors other than price. What might these

factors be?

Input Costs

• Any change in the cost of an input used to produce a good – raw materials, machinery, labor – will affect supply.

• A rise in the cost of an input will cause a fall in supply at all price levels because the good has become more expensive to produce.

• A fall in the cost of an input will cause an increase in supply at all price levels.

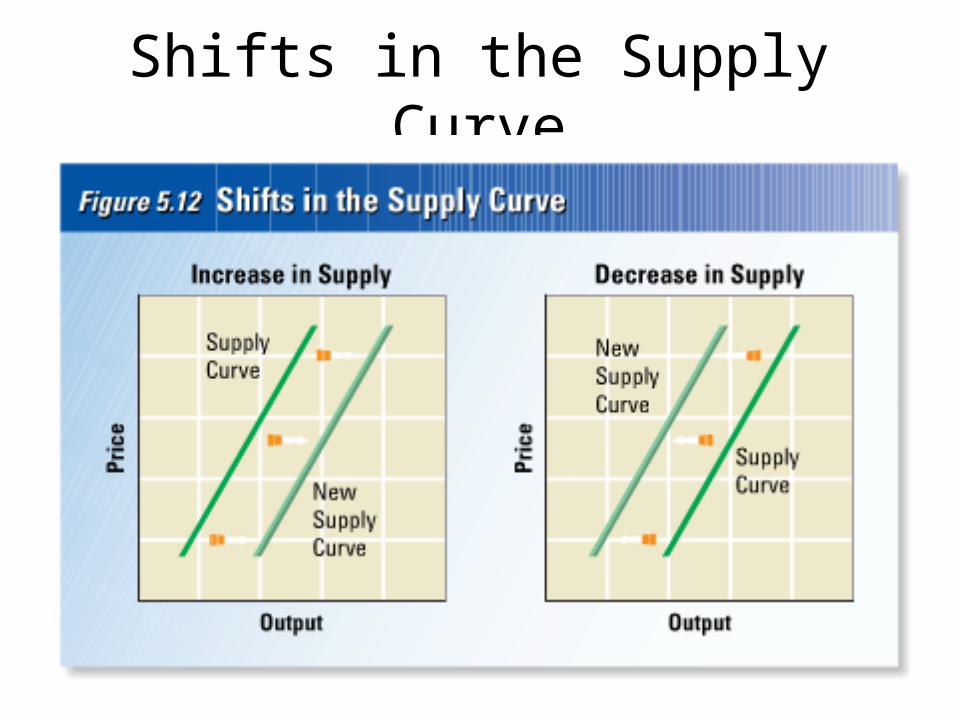

Shifts in the Supply Curve

Government’s Influence on Supply

• Use of subsidies (government payment that supports a business or market)– Government of France subsidizes small farms

because French citizens want to protect the lifestyle and character of the French countryside.

• Excise Tax (a tax on the production or sale of a good)– Increases production costs, thereby reducing supply

at all price levels– Placed on goods such as cigarettes, alcohol, high-

pollutant gasoline

In other words...

• Support production• Usually increase

supply

• Increases production costs

• Decrease supply of good

Subsidies Excise Tax

Government’s Influence on Supply

• Regulations (government intervention in a market that affects the price, quantity, or quality of a good). – 1970s car manufacturers are required to

install technology to reduce pollution from auto exhaust = increase cost of production = decrease supply at all price levels

Supply in the Global Economy

• Changes in other countries that supply goods to the United States could also affect the supply of products imported by the United States.

• Import restrictions (quotas) could also affect the supply curves of restricted goods.

Other Influences on Supply

• Future Expectation of Prices– If a seller expects the price of a good to rise in

the future, the seller will store the goods now in order to sell more in the future (PEANUTS).

– If a seller expects the price of a good to drop in the future, the seller will earn more money by placing goods on the market now before the price falls.

– Expectations of higher prices will reduce supply now and increase supply later, and expectations of lower prices will increase supply now and decrease supply later.

Other Influences on Supply

• Inflation– A condition of rising prices that makes the

value of cash decrease– A good can hold its value, provided that it can

be stored for a long period of time suppliers might prefer to hold onto their goods (higher value) than sell for cash (lower value) supply decreases

Other Influences on Supply

• Number of Suppliers– If more suppliers enter a market to produce a

certain good, the market supply of the good will rise, and the supply curve will shift to the right.

– If suppliers stop producing the good and leave the market, the supply will decline.

Where do Firms Produce?

• Key determining factor: transportation costs– If it is more expensive to transport raw

materials, producers locate close to the source of the raw material needed.

– If it is more expensive to transport to consumers, producers locate close to the consumer market.

• Other factors: concentration of specialized workers, areas of low energy costs

In each of the following cases, decide if the event will cause

any change in the current market supply of new cars

sold in the US.

Auto workers agree to wage and fringe cuts

Supply increases

New Technology Increase Efficiency in Detroit Factories

Supply increases

Steel Prices Rise 100%

Supply decreases

Quotas Eliminated: Foreign Car Imports Rise

Supply increases

Large Auto Producers Goes Bankrupt, Closes Factory

Supply decreases

Buyers Reject New Car Models: Sellers Lower Prices

No change in supply; change in quantity supplied

Shortages Abound in Consumer Electronics –

Consumers Can’t Buy Enough Gadgets

Supply decreases