Embed Size (px)

Citation preview

Supplementary Notes for

Corporate Financial Management

in

Southern Africa

2nd edition

by

Pieter van der Merwe (FCIS)

Version 1/2017

Chartered Secretaries Southern Africa

Riviera Office Park (Block C), 6 – 10 Riviera Road, Killarney, Johannesburg, 2193

Copyright © Chartered Secretaries Southern Africa 2015

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system,

or transmitted, in any form, or by any means, electronic, mechanical, photocopying, recording

or otherwise, without prior permission, in writing, from the publisher.

Corporate Financial Management Page 2

INTRODUCTION

Please note that this is ESSENTIAL ADDITIONAL READING and is examinable.

These notes supplement Corporate Financial Management in Southern Africa, 2nd Edition.

The objective of these supplementary notes is to provide the reader with additional support

through:

- Additional examples in order to enhance the practical understanding of some concepts;

- Further explanatory notes aimed at clarifying certain theoretical principles;

- Corrections to some of the mistakes in the text;

- Revised formulae sheet incorporating updates and amendments.

The instructions have been colour coded as follows:

Add: - this means that additional information has been supplied

Replace: this means that a correction has been made

They follow the page numbers in the text book consecutively.

We hope that this supplement will enhance and clarify the related topics in the textbook.

Corporate Financial Management Page 3

1. Replace the word “SA” in the first line under heading 1.8 on page 42 with the word

“international”.

2. Add to the top of page 71:

“Consequently, ordinary shareholders expect a higher return than debenture holders do,

as debenture interest will be paid each year whatever the financial results, whereas

payment of dividends is not guaranteed.”

3. Replace the word “standing” in the second line of the first paragraph on page 72 with the

word “trading”.

4. Add at the end of the example on top of page 77 (after 8.97%):

“The realised compound yield is based on the same principal as the modified internal rate

of return (MIRR) in Part 5, Chapter 1.”

5. Replace the Growth rate (g) formula at the bottom of page 97 with the following formula:

𝑔 = √𝐿𝑎𝑡𝑒𝑠𝑡 𝑑𝑖𝑣𝑖𝑑𝑒𝑛𝑑

𝐸𝑎𝑟𝑙𝑖𝑒𝑠𝑡 𝑑𝑖𝑣𝑖𝑑𝑒𝑛𝑑

𝑛

− 1

6. At the bottom of page 106, after the question box, add the following:

Interest rate conversions

Interest rates are quoted by the banks and in the financial markets based on compounding conventions. The compounding conventions most frequently used are as follows:

- nacm nominal annual compounded monthly

- nacq nominal annual compounded quarterly

- nacs nominal annual compounded semi-annually

- naca nominal annual compounded annually (the effective rate)

In order to make accurate comparisons between interest rates, whether it is for investment or

borrowing purposes, the rates must be on the same compounding basis. Should the rates not

be on the same compounding basis, they must first be converted as such in order for them to

be comparable. Care should be taken when comparing interest rates at face value as it may

result in wrong decision making. There are a few methods by which such conversions can be

done, following is one such method or formula:

o

M

M

iio

M

MRR i

o

12x }1]))

12 x(1{[(

where: Ro = Rate of interest required (output)

Ri = Rate of interest to be converted (input) Mo = Number of months required (output) Mi = Number of months corresponding with Ri above (input)

Corporate Financial Management Page 4

PRACTICAL EXAMPLES

1. ABC Ltd has bought factory premises at prime less 1%. Given that prime is at 9.25%,

what is the effective rate of interest that the company pays per year. Answer:

Prime is an interest rate compounded monthly (nacm) while the effective rate is the annual rate (naca). Ri = 9.25% - 1.00% = 8.25% nacm Mo = 12 months Mi = 1 month

12

12x }1]))

12

1 x%25.8(1{[( 1

12

oR

naca %87.8oR

2. Green Bank is offering investors the following fixed deposit rates:

6 months: 6.50% 12 months: 6.60%

Which rate is the more attractive investment rate? Answer:

The rates cannot be compared as stated above, as they are not quoted on a comparable basis i.e. the 6 months rate is nacs and the 12-month rate is naca. The one rate must first be converted into the other rate’s compounding convention for them to be comparable. Converting the nacs rate to naca as follows: Ri = 6.50% Mo = 12 months Mi = 6 months

12

12x }1]))

12

6 x%50.6(1{[( 6

12

oR

naca %61.6oR

Thus, the 6 months rate quoted at 6.50% provides a higher annual effective rate of 6.61% compared to the 12 months quoted rate at 6.60%. Rather invest in the 6 month fixed deposit offering (though it is very marginal). To convert the 6.61% naca back to a semi-annual rate (nacs), the formula would be: Ri = 6.61% Mo = 6 months

o

M

M

iio

M

MRR i

o

12x }1]))

12 x(1{[(

o

M

M

iio

M

MRR i

o

12x }1]))

12 x(1{[(

Corporate Financial Management Page 5

Mi = 12 months

6

12x }1]))

12

12 x%61.6(1{[( 12

6

oR

nacs %50.6oR

7. Replace the formula and its workings at the bottom of page 113 with the following:

13.75

1.70) (y 0.72

10

)60.2(72.0 =

shares of no.

Interest) - t)(EBIT-(1 = EPS

y

13.75

12.24 y 7.21.8720.72y

13.75(0.72y −1.872) = 7.2y −12.24

9.90y − 25.74 = 7.2y −12.24

9.90y − 7.2y = 25.74 −12.24

2.70y = 13.50

2.70

13.50 =y

y = 5

8. Replace the Figure: Head and shoulders at the bottom of page 136 with the following figure

and commentary:

What is important with this pattern (and other patterns) is to establish the target that the share

price is expected to reach after the fall below the neckline. In this instance, the target from

where the share price breaks the neckline downwards is equal to the distance between the

5

7

9

11

13

15

17

19

21

1/J

an/1

0

1/M

ar/1

0

1/M

ay/1

0

1/J

ul/

10

1/S

ep/1

0

1/N

ov/

10

1/J

an/1

1

1/M

ar/1

1

1/M

ay/1

1

1/J

ul/

11

1/S

ep/1

1

1/N

ov/

11

1/J

an/1

2

1/M

ar/1

2

1/M

ay/1

2

1/J

ul/

12

1/S

ep/1

2

1/N

ov/

12

1/J

an/1

3

1/M

ar/1

3

1/M

ay/1

3

1/J

ul/

13

1/S

ep/1

3

1/N

ov/

13

Share Price

Left Shoulder

HeadRight Shoulder

NecklineTarget

Corporate Financial Management Page 6

neckline and the head (indicated by the two straight arrows). Note that this is not an exact

science but only a calculated estimate.

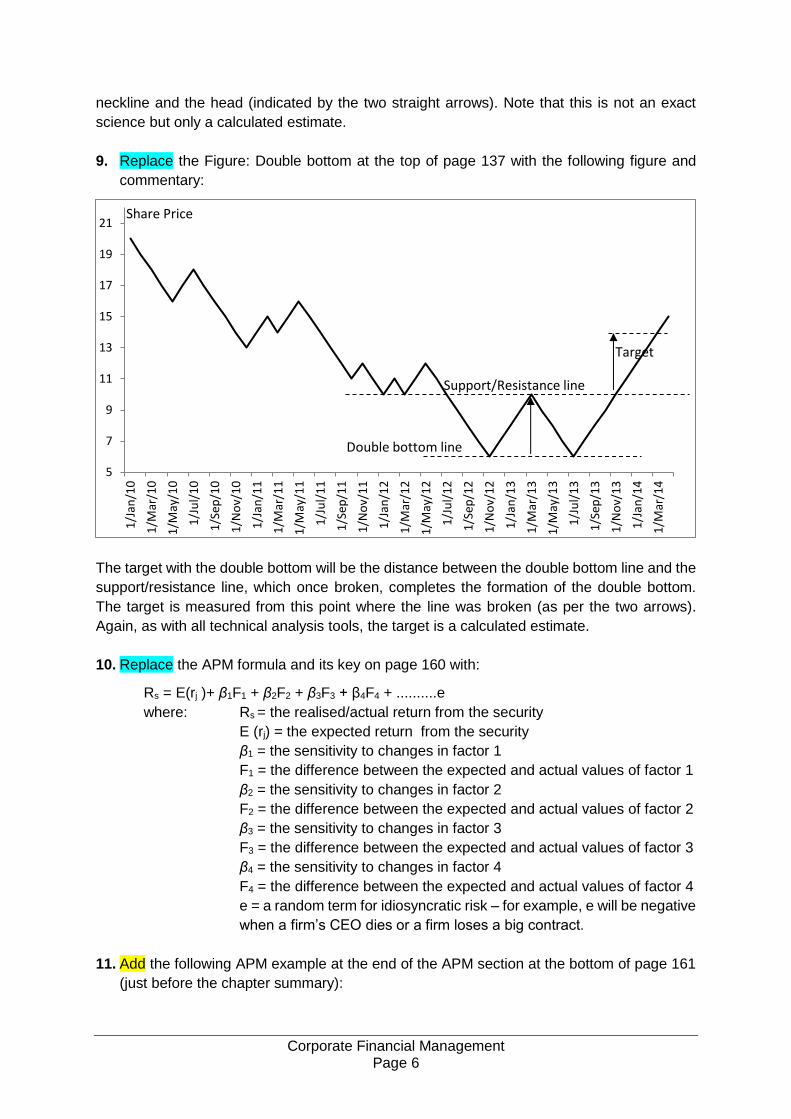

9. Replace the Figure: Double bottom at the top of page 137 with the following figure and

commentary:

The target with the double bottom will be the distance between the double bottom line and the

support/resistance line, which once broken, completes the formation of the double bottom.

The target is measured from this point where the line was broken (as per the two arrows).

Again, as with all technical analysis tools, the target is a calculated estimate.

10. Replace the APM formula and its key on page 160 with:

Rs = E(rj )+ β1F1 + β2F2 + β3F3 + β4F4 + ..........e

where: Rs = the realised/actual return from the security

E (rj) = the expected return from the security

β1 = the sensitivity to changes in factor 1

F1 = the difference between the expected and actual values of factor 1

β2 = the sensitivity to changes in factor 2

F2 = the difference between the expected and actual values of factor 2

β3 = the sensitivity to changes in factor 3

F3 = the difference between the expected and actual values of factor 3

β4 = the sensitivity to changes in factor 4

F4 = the difference between the expected and actual values of factor 4

e = a random term for idiosyncratic risk – for example, e will be negative

when a firm’s CEO dies or a firm loses a big contract.

11. Add the following APM example at the end of the APM section at the bottom of page 161

(just before the chapter summary):

5

7

9

11

13

15

17

19

21

1/J

an/1

0

1/M

ar/1

0

1/M

ay/1

0

1/J

ul/

10

1/S

ep/1

0

1/N

ov/

10

1/J

an/1

1

1/M

ar/1

1

1/M

ay/1

1

1/J

ul/

11

1/S

ep/1

1

1/N

ov/

11

1/J

an/1

2

1/M

ar/1

2

1/M

ay/1

2

1/J

ul/

12

1/S

ep/1

2

1/N

ov/

12

1/J

an/1

3

1/M

ar/1

3

1/M

ay/1

3

1/J

ul/

13

1/S

ep/1

3

1/N

ov/

13

1/J

an/1

4

1/M

ar/1

4

Share Price

Support/Resistance line

Double bottom line

Target

Corporate Financial Management Page 7

PRACTICAL EXAMPLE

An investor is considering investing in Vusi Ltd (“Vusi”). Two macro-economic factors in the

South African economy have been identified as having a major influence on Vusi namely

the growth rate of gross domestic product (GDP) and the domestic rate of inflation (CPI).

GDP is expected to be 3% and CPI at 5% with the risk-free rate currently at 8%. Vusi has a

current beta of 1.25 on GDP and 0.5 on CPI. The investor requires a return on GDP risk of

11.20% (1.4 times risk-free) and a return of 14% on CPI risk (1.75 times risk free). Should

GDP actually grow by 2% and CPI end up at 7% with no idiosyncratic adjustments, there

could be a difference between the expected and actual returns on Vusi shares.

Required:

Calculate the expected and realised returns on Vusi shares.

Answer:

From the above, E(GDP) = 3% with βGDP = 1.25, E(CPI) = 5% with βCPI = 0.5, FGDP = (0.02

– 0.03) = -0.01, FCPI = (0.07 – 0.05) = 0.02, rf = 8%, rGDP = 11.20%, rCPI = 14%.

E(rj ) = rf + β1(r1 − rf)+ β2(r2 − rf)

E(rVUSI) = rf + βGDP(rGDP − rf)+ βCPI(rCPI − rf)

= 0.08 + 1.25 (0.1120 – 0.08) + 0.5 (0.14 – 0.08)

= 15.00%

Rs = E(rj )+ β1F1 + β2F2 + e

RVUSI = E(rVUSI) + βGDPFGDP + βCPIFCPI + e

= 0.15 + 1.25(-0.01) + 0.5(0.02) + 0

= 0.15 – 0.0125 + 0.01 + 0

= 14.75%

Thus, even though the drop in GDP was less than the increase in CPI, the bigger beta of

GDP relative to CPI caused a drop in the realised/actual return on the Vusi shares compared

to the expected return.

12. Add the following to the opening sentence under “Operating gearing” on page 168:

“The higher the degree of operating leverage, the more volatile the EBIT figure will be

relative to a given change in sales, all other things remaining unchanged.”

13. Replace the whole Miller-Orr model section on pages 195 and 196 with the following:

• Miller-Orr model

The Miller-Orr model was developed to produce a more useful model than the Baumol model.

It sets upper and lower limits to the level of cash a firm should hold. When these levels are

reached the firm either buys or sells short-term marketable securities to audit the cash levels.

To set these levels, the variability of cash flows needs to be determined along with the costs

of buying and selling securities and the interest rate.

Corporate Financial Management Page 8

The steps in using the model are:

• Determine the lower level of cash the firm is happy to have. This is generally set at a

minimum safety level, which in theory could be zero.

• Determine the variance of the firm’s cash flows (perhaps over a three or six month period).

• Calculate the spread between the minimum (lower) and maximum (upper) cash balance

limits, using the following formula:

Spread=3×√0.75 × variance of cash flow × transaction cost

interest rate

3

• Calculate the upper limit – this is the lower limit plus the spread.

• However, to minimise the cost of holding excess cash and to avoid the danger of

insufficient cash, a pre-calculated target level of cash holdings (the return point) is

determined. The return point is the lower limit plus ⅓ of the spread.

PRACTICAL EXAMPLE

Pull Ltd faces an interest rate of 0.5% per day and its brokers charge R75 for each

transaction in short-term securities. The managing director of Pull Ltd has stated that the

minimum cash balance that is acceptable is R2 000 and that the variance of cash flows on

a daily basis is R16 000 (standard deviation of daily cash flows is thus R126.49 (rounded)).

Required:

What is the maximum level of cash the firm should hold and at what point should it start to

purchase or sell securities?

Following the above procedure:

• Determine the lower level of cash the firm is happy to have – this has been set at R2 000.

• Determine the variation in cash flows of the firm – this has been found to be R16 000.

• Calculate the spread of transactions.

• Calculate the upper limit.

Answer:

Spread=3×√(0.75×16000×75)

0.005

3

= R1 694

• Calculate the upper limit – this is the sum of the lower limit and the spread:

Upper limit = R2 000 + R1 694 = R3 694

• Securities should be sold when the lower level is reached. The amount of securities to

be sold is equal to the difference between the lower level and the return point. The return

point is the sum of the lower limit and ⅓ of the spread: return point = R2 000 + ⅓ (R1

694) = R2 565

Corporate Financial Management Page 9

Thus the firm is aiming for a cash holding of R2 565 (the return point). Therefore, if the

balance of cash reaches R3 694 the firm should buy R3 694 - R2 565 = R1 129 of

marketable securities and if it falls to R2 000 then R565 of securities should be sold.

The Miller-Orr model is useful in that it considers:

• the level of interest rates (higher rates give a narrower spread, so less cash needs to be

held before the return point and the upper limit is reached);

• transaction costs (higher transaction costs increase the spread and therefore reduce the

number of transactions);

• variability of cash flows (more variable cash flows means more unpredictability, requiring

a higher spread to absorb the variability).

A drawback of the model is that it assumes that cash flows vary randomly and does not take

account of the fact that some cash flows (for example, dividend payments) can be predicted

accurately.

14. Replace the EOQ formula on page 217 with:

EOQ=√2 (Cost per order)(Annual usage in units)

Annual holding cost per unit

15. Add the following after the “Conclusion” in the first example on page 225:

Note: The reduction in working capital above can be broken down further. Total sales are

made up of 80% cost of sales (COS) and 20% gross profit (GP). The logic goes that the

only item that is actually been financed is the COS that had to be incurred to generate the

sales. The GP does not need to be financed but is rather caught up in the debtors figure

representing an amount that could have been banked on day one of the sale (if it was a

cash sale) and could have earned interest i.e. the interest not earned on the GP is an

opportunity cost.

Present: 2 month’s COS = 2/12 x R1.2mil x 80% = R160 000

2 month’s GP = 2/12 x R1.2mil x 20% = R40 000

New: ½ month’s COS = 30% x 0.5/12 x 0.85 x R1.2mil x 80% = R10 200

½ month’s GP = 30% x 0.5/12 x 0.85 x R1.2mil x 20% = R2 550

1 month’s COS = 70% x 1/12 x 0.85 x R1.2mil x 80% = R47 600

1 month’s GP = 70% x 1/12 x 0.85 x R1.2mil x 20% = R11 900

Working capital tied up in COS have dropped from R160 000 to R57 800 (R10 200 +

R47 600) = R102 200 at an annual saving in financing cost of R16 352.

Gross Profit tied up in working capital dropped from R40 000 to R14 450 (R2 550 +

R11 900) = R25 550 on which interest can now be earned of R4 088.

Thus, the total annual finance cost saving is R20 440 (R16 352 + R4 088).

Add the following at the end of the example on page 227:

Corporate Financial Management Page 10

As with the example on pg.225, the reduction in working capital above can be broken down

further. Total sales are made up of 95% cost of sales (COS) and 5% gross profit (GP).

Present: 1 month’s COS = 1/12 x R1.25mil x 95% = R98 958

1 month’s GP = 1/12 x R1.25mil x 5% = R5 208

New: 2 month’s COS = 2/12 x R1.75mil x 95% = R277 083

Increased Working Capital (ex. Debtors) = R50 000

2 month’s GP = 2/12 x R1.75mil x 5% = R14 583

Working capital tied up in COS have increased from R98 958 to R327 083 (R277 083 +

R50 000) = R228 125 at an annual increase in financing cost of R34 219.

Gross Profit tied up in working capital increased from R5 208 to R14 583 = R9 375 on which

interest could have been earned of R1 406.

Thus, the total annual increase in financing cost is R35 625 (R34 219 + R1 406).

16. Replace: The second sentence after the practical example time line on page 243 should

read:

“However the last seven do represent such an annuity.” (not last six as per the text)

17. Remove the third sentence of the first paragraph under the heading “The second way of

calculating” on page 246 i.e. remove the wording:

“See Guidance Note 2: Annuities”. (There are no more guidance notes)

18. Replace the formula on page 249 and page 253 with the following formula:

IRR = low rate +

rate) low - ratehigh (

rate)high NPV - rate low (NPV

rate low NPV

19. Replace the whole of paragraphs 1.7.1 and 1.7.2 from pages 253 to 255 with the following:

1.7.1 Multiple solutions: a possible further drawback of IRR

Most capital investment projects involve an initial investment – with cash outflows – followed

by a series of cash inflows in later years. This is called a conventional cash flow pattern.

Sometimes the cash flows change direction again in later years.

Typically, this happens when there are closure costs that cause cash outflows at the end of

the project. An example of this could be a nuclear power station, where decommissioning

costs at the end of the station’s life are very high. Another example could be a chemical

production facility, where decontamination has to be done when the facility is closed down, at

a cash cost greater than any operating cash inflow in the final year. If the cash flows change

direction more than once, the cash flows are said to be ‘non-conventional’. With non-

conventional cash flows, the internal rate of return can take more than one value. The following

example shows what can happen:

PRACTICAL EXAMPLE

Corporate Financial Management Page 11

Enzo Ltd is considering investing in a project i.e. Project C: the project will last for two years

and has the following details:

Cash flow Cash flow Cash flow IRR

Yr. 0 Yr. 1 Yr. 2

Project C (R907 325) R8m (R8m) 15% and

667%*

*The exact percentages are 14.999% and 666.71% (used in the table below)

Using the IRR, Project C end up with two IRR’s as the cash flows change direction at least

twice. This also assumes that that the cash flows are reinvested at the particular IRR being

used. The present values (PV’s) of the cash flows will be as follows:

Yr. 0 Yr. 1 Yr. 2 NPV

Cash Flows (R907 325) R8m (R8m)

PV’s @ 15%* (R907 325) R 6 956 586 (R6 049 261) 0

PV’s @ 667%* (R907 325) R 1 043 414 (R136 089) 0

Thus, both IRR’s provide a zero NPV result.

The net present value is zero with a discount rate of about 15% and also with a discount rate

of 667%. Between 15% and 667%, the NPV is positive. Below 15%, or above 667%, the NPV

is negative. What does this mean? Not much to practical people. A slightly different approach

is required.

1.7.2 Modified IRR (MIRR)

The problem with using the IRR is that it assumes that all cash flows from a project are

reinvested at the IRR of that particular project. By changing this assumption and applying a

more realistic reinvestment rate e.g. a money market deposit rate, this problem with IRR is

solved. The IRR arrived at by using this alternative reinvestment rate is referred to as the

modified IRR (MIRR). The same principle is applied in calculating the “realised compound

yield” of a bond in Part 2, Chapter 3.

PRACTICAL EXAMPLE

Using the same data as in the Enzo Ltd example above.

The cash flows from the project are deposited into Enzo’s money market account, earning

interest at a rate of 13.00% p.a. Thus, we need to calculate the MIRR of the project,

reinvesting the cash flows at 13.00%.

This is done by taking each cash in-flow and reinvesting it until the end of the project (end

of year 2) at 13.00% p.a. (see the table below). By adding these respective reinvested cash

flows for each project, we arrive at the Terminal Value (Future Value) of these reinvested

cash flows as at the end of the project. There are then only two cash flows used in

calculating the MIRR namely the initial investment and the accumulated Terminal Value.

Corporate Financial Management Page 12

The MIRR can then be found by trial and error (as with the IRR) i.e. the rate of interest that

will make the NPV of the two cash flows equal to zero (last column in the table below).

PROJECT C:

Year Cash Flows

Years to end

of Project

FV Factor

at 13.00%

Terminal

Value

Cash Flows

and MIRR

0 (R907 325) (R907 325)

1 R8 000 000 1 1.1300 R9 040 000

2 (R8 000 000) 0 1.0000 (R8 000 000) R1 040 000*

MIRR = 7.06%

*R1 040 000 is the sum total of the individual Terminal Values from the second last column.

Thus the real IRR (MIRR) of this project is 7.06%, which is significantly lower than the 15%

and 667% IRR’s arrived at earlier.

If a company embarks on numerous projects, this then translates into multiple but different

reinvestment rates of the respective cash flows from each project. This is not a valid

assumption as all cash flows from the different projects are most probably deposited into a

single bank account or money market account, earning the same rate of interest. This rate of

interest will most probably be different to the IRRs of the respective projects. The MIRR solves

this problem by calculating each project’s IRR by reinvesting all cash flows, regardless from

which project, at the same rate of interest i.e. the rate earned on the money market account.

PRACTICAL EXAMPLE

Benso Ltd is investing in two projects i.e. Project A and Project B; both projects last three

years and have the following details:

Cash flow Cash flow Cash flow Cash flow IRR

Yr. 0 Yr. 1 Yr. 2 Yr. 3

Project A (R100 000) R15 000 R15 000 R115 000 15.00%

Project B (R100 000) R90 000 R20 000 R15 000 17.79%

Using the IRR, Project B is doing better than Project A. This assumes of course that the

cash flows from each project are reinvested at the IRR of that particular project. All cash

flows from both projects are however deposited into the Benso’s money market account,

earning interest at a rate of 11.00% p.a. Thus, we need to calculate the MIRR of each

project, reinvesting the cash flows of each project at 11.00%.

This is done by taking each cash in-flow and reinvesting it until the end of the project (end

of year 3) at 11.00% p.a. (see the table below). By adding these respective reinvested cash

flows for each project, we arrive at the Terminal Value (Future Value) of these reinvested

cash flows as at the end of each project. There are only two cash flows used in calculating

the MIRR namely the initial investment and the accumulated Terminal Value. The MIRR can

then be found by trial and error (as with the IRR) i.e. the rate of interest that will make the

NPV of the two cash flows equal to zero (last column in the tables below).

PROJECT A:

Corporate Financial Management Page 13

Year Cash Flows

and IRR

Years to end

of Project

FV Factor

at 11.00%

Terminal

Value

Cash Flows

and MIRR

0 -R100 000 -R100 000.00

1 R15 000 2 1.2321 R18 481.50

2 R15 000 1 1.1100 R16 650.00

3 R115 000 0 1.0000 R115 000.00 R150 131.50*

IRR = 15.00% MIRR = 14.50%

*R150 131.50 is the sum total of the individual Terminal Values from the second last column.

PROJECT B:

Year Cash Flows

and IRR

Years to end

of Project

FV Factor

at 11.00%

Terminal

Value

Cash Flows

and MIRR

0 -R100 000 -R100 000.00

1 R90 000 2 1.2321 R110 889.00

2 R20 000 1 1.1100 R22 200.00

3 R15 000 0 1.0000 R15 000.00 R148 089.00*

IRR = 17.79% MIRR = 13.98%

*R148 089.00 is the sum total of the individual Terminal Values from the second last column.

Based on the MIRR, Project A at 14.50% is now more lucrative than Project B at 13.98%

(opposite to the IRR result). This illustrates the importance of the effect that the reinvestment

rate has on the projects above and on investments in general. The reinvestment rate used

determines the degree and power of the compounding effect. Instead of using the money

market deposit rate as in this example, companies can also use their cost of capital as the

reinvestment rate for the cash flows from their various projects.

20. Replace the wording as indicated below in the second sentence of the first paragraph

under “Earnings per share” on page 287:

“An example is given is section 8 below”. (there is no section 8)

21. Replace the whole of paragraph 1.5 from pages 293 to 296 with the following:

1.5 SYNERGIES

The object of a merger may be to obtain operating benefits that exceed the scope of operations

of the individual companies involved in the merger. The “excess benefit” is often referred to

as the benefit of synergies. Note that these benefits can be expressed either as a single value

(representing “P” in the P/E formula) or as annual synergy earnings (representing “E” in the

P/E formula), which can be converted into “P” by multiplying “E” with the P/E ratio.

These benefits may be dealt with as follows:

• The benefit may be apportioned pro-rata between the acquiring company and the target

company.

• The benefit may be allocated entirely to the target company’s shareholders in arriving at

the share offer price.

Corporate Financial Management Page 14

• The benefit may be allocated entirely to the acquiring company in arriving at the share

offer price.

Where the benefits of synergies are experienced this may lead to the acquiring company

calculating a maximum offer price (all synergistic benefits allocated to the target company) or

a minimum offer price (all synergistic benefits retained by the acquiring company).

Should a merger or acquisition be financed through an exchange of shares (as in paragraph

1.9.1 of this chapter), an exchange ratio (ER) of shares needs to be calculated in order to

determine the number of shares that needs to be issued by the predator company in exchange

for each share in the target company. The ER is determined by two important factors namely

market values and earnings per share, as set out in the discussion to follow.

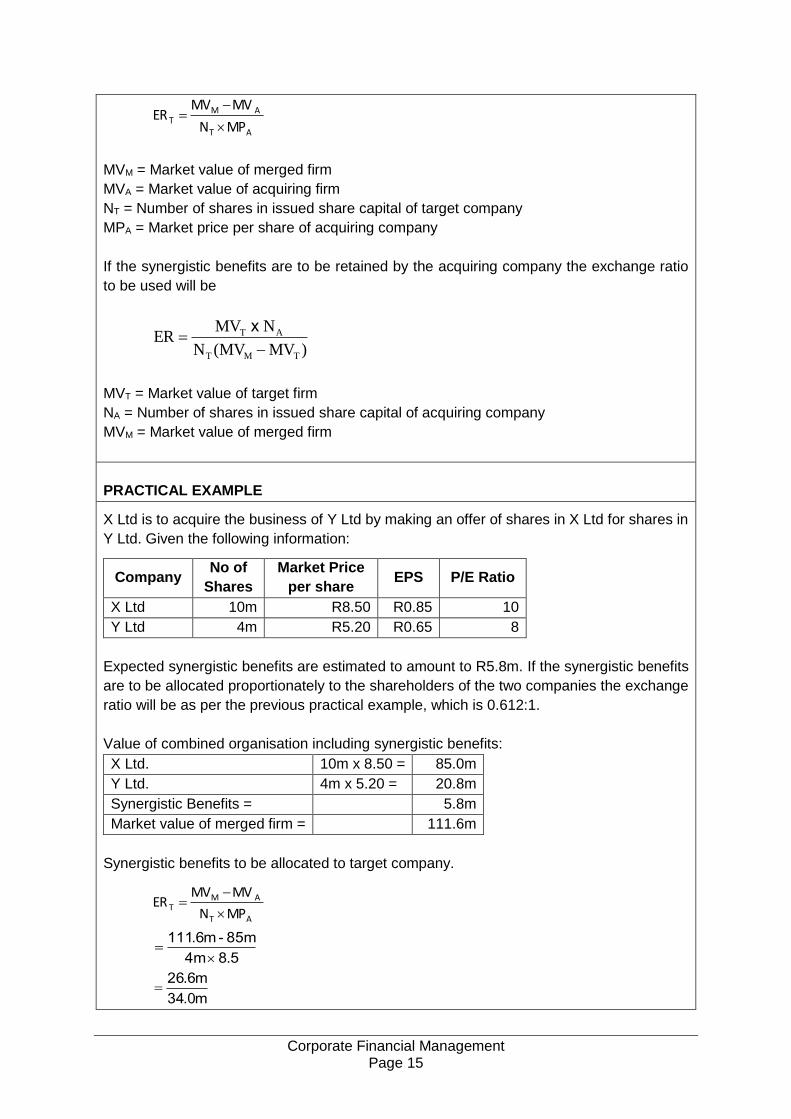

1.5.1 Exchange ratios based upon market value

ERT = Market Value per Target Company Share/Market Value per Acquiring Company Share

A

TT

MP

MPER

An exchange ratio based upon this formula assumes that there are no synergistic benefits. If

there are synergistic benefits the takeover price will be at a premium to the market value of

the target company’s shares.

1premium Market

T

TA

MP

ER MP

PRACTICAL EXAMPLE

X Ltd to acquire Y Ltd.

Market price per share of X = R8.50

Market price per share of Y = R5.20

Exchange ratio = 5.20 / 8.50 = 0.612:1

If exchange ratio offered by X Ltd to Y Ltd shareholders was 0.8:1 the market premium

would be:

(0.8 / 0.612) - 1

= 1.307 – 1.00

=0.307

= 30.7%

X Ltd would be paying Y Ltd’s shareholders a premium of 31% for their shares.

If all the synergistic benefits are to be allocated to the target company’s shareholders the

following formula must be used:

Corporate Financial Management Page 15

AT

AMT

MP N

MVMVER

MVM = Market value of merged firm

MVA = Market value of acquiring firm

NT = Number of shares in issued share capital of target company

MPA = Market price per share of acquiring company

If the synergistic benefits are to be retained by the acquiring company the exchange ratio

to be used will be

)MV (MVN

N MVER

TMT

AT

x

MVT = Market value of target firm

NA = Number of shares in issued share capital of acquiring company

MVM = Market value of merged firm

PRACTICAL EXAMPLE

X Ltd is to acquire the business of Y Ltd by making an offer of shares in X Ltd for shares in

Y Ltd. Given the following information:

Company No of

Shares

Market Price

per share EPS P/E Ratio

X Ltd 10m R8.50 R0.85 10

Y Ltd 4m R5.20 R0.65 8

Expected synergistic benefits are estimated to amount to R5.8m. If the synergistic benefits

are to be allocated proportionately to the shareholders of the two companies the exchange

ratio will be as per the previous practical example, which is 0.612:1.

Value of combined organisation including synergistic benefits:

X Ltd. 10m x 8.50 = 85.0m

Y Ltd. 4m x 5.20 = 20.8m

Synergistic Benefits = 5.8m

Market value of merged firm = 111.6m

Synergistic benefits to be allocated to target company.

584m

85m-m6111

.

.

m034

m626

.

.

AT

AMT

MP N

MVMVER

Corporate Financial Management Page 16

= 0.78235

Number of shares in X Ltd to be issued to the shareholders of Y Ltd = 0.78235 x 4m =

3 129 400 shares.

Synergistic benefits to be retained by the acquiring company:

)TMT

AT

MV (MVN

N x MVER

)20.8m 4m(111.6m

10m20.8m

363.2m

208m

= 0.57269

57.27 shares in X Ltd for every 100 shares in Y Ltd

Number of shares to be issued to the shareholders of Y Ltd = 4m x 0.5727 =

2 290 800 shares.

1.5.2 Exchange ratios based upon earnings per share (EPS)

ERT = EPS of Target Company/EPS of Acquiring Company

A

T

TEPS

EPSER

The ratio above assumes no dilution in EPS for the acquiring company. If the synergistic

benefits are expected to result in an increase in earnings, there may be a range of possible

ER’s that will not result in a dilution in EPS as a result of the merger.

The formula for the maximum exchange ratio that the acquiring company can offer before it

incurs a decline in EPS is:

TAA

Tmax

Nx EPS

SE

EPS

EPSER

The formula for the minimum exchange ratio that the target company can accept before it

incurs a decline in EPS is:

AA

AT

minN x EPS SE

N x EPSER

where: EPST = EPS of the target company

EPSA = EPS of the acquiring company

SE = Synergistic Earnings (annual earnings)

NT = Number of target company’s shares

NA = Number of acquiring company’s shares

PRACTICAL EXAMPLE

Corporate Financial Management Page 17

The same information as in the previous example applies.

Note that the expected synergistic benefits of R5.8m is the value of these benefits (“P” in

the P/E ratio) and must be converted to its annual earnings equivalent (“E”) through the P/E

ratio. In order to do that it is assumed that the new merged company will have the same P/E

ratio as the weighted average P/E ratio (weighted according to earnings) of the two

companies combined:

Company No of

Shares EPS Earnings Weighting

Current

P/E Ratio

Weighted

P/E Ratio

X Ltd 10m R0.85 R8 500 000 0.7658 10 7.658

Y Ltd 4m R0.65 R2 600 000 0.2342 8 1.8736

R 11 100 000 1.0000 9.5316

The R5.8m synergistic value (“P”) is divided by the weighted P/E ratio of 9.5316 to arrive at

the annual synergistic earnings (“E”) of R608 507 (rounding).

The maximum exchange ratio that the acquiring company can offer before it suffers a

decline in EPS is:

TAA

T

maxNx EPS

SE

EPS

EPSER

4m x 0.85

507 608

0.85

0.65

1790.07647.0

9437.0

Maximum number of shares in X Ltd to be issued to the shareholders of Y Ltd = 0.9437 x

4m = 3 774 800 shares.

Check: Annual total earnings + annual synergy earnings = R11 708 507 (R11 100 000 +

R608 507) divided by X Ltd’s shares of 10m + newly issued 3 774 800 (13 774 800) = EPS

of R0.85. This is the same as per the table above for X Ltd before the acquisition.

The minimum exchange ratio that the target company can accept before it incurs a decline

in EPS is:

AA

AT

minN x EPS SE

N x EPSER

10m x 0.85 507 608

10m x 0.65

507 108 9

000 500 6

7136.0

71.36 shares in X Ltd for every 100 shares in Y Ltd

Corporate Financial Management Page 18

Number of shares to be issued to the shareholders of Y Ltd = 4m x 0.7136 = 2 854

400 shares.

Check: Annual total earnings + annual synergy earnings = R11 708 507 (R11 100 000 +

R608 507). Y Ltd shareholder’s proportion of this income will be 2 854 400/(2 854 400 +

10m) = 22.21% x R11 708 507 = R2 599 947. The EPS will then be R2 599 947 divided by

Y Ltd’s original share issue of 4m = R0.65 per share. This is the same as per the table

above for Y Ltd before the acquisition.

Should the decision be to base the acquisition on market value, there might still be a

requirement to prevent a dilution in EPS. The acquiring company might then structure an offer

through convertible debentures with conversion to ordinary shares at a later stage, when

earnings are of an adequate size so that the EPS after conversion is the same as at the time

of the merger. Another alternative is the issue of convertible preferred ordinary shares with a

fixed preferred ordinary dividend. These shares will be convertible into ordinary shares when

the ordinary dividend reaches a level that will equate to the fixed preferred ordinary dividend.

This should coincide with an EPS that is the same as at the time of the merger.

22. Replace the sentence in the “Answer:” section at the bottom of page 303 that reads

“Shares in Modali received = 10m x 2 = R10m shares” with “Shares in Modali received =

10m x 2 = 20m shares”

23. Replace the whole of paragraph 1.7 from pages 345 to 346 with the following:

1.7 BUYING AND SELLING FOREIGN CURRENCY

Many firms and individuals buy any foreign currency they need from their bank and sell the

bank any foreign currency they want converted into Rands. In these transactions the bank is

selling and then buying, the currency respectively. The rates that banks charge are quoted

typically as such (exchange rates are also shown in a similar fashion in the financial press):

Value of the Rand against other currencies (spot rates)

US Dollar 11.3700 - 11.7200

Euro 13.1812 - 13.6784

Pound Sterling 17.2233 - 17.8261

(Note that these rates vary on a daily basis and the figures given here are for illustration only.)

• In the quotations above, the US Dollar, Euro and Pound Sterling are referred to as the

base currencies while the Rand is the variable currency.

• A spot rate is the rate used for immediate transactions and quotations for which no

previous arrangements have been made. Delivery to the buyer is made two days later.

• A forward rate is the rate quoted for a transaction at a defined date in the future, e.g. one

month forward and three months forward being for one month and three months in the

future respectively.

The first point to note is that there is a spread in each rate. This represents the dealer’s (the

bank’s) turn or profit. So company A selling US dollars to the bank would receive a smaller

amount in Rand than company B would have to pay the bank to buy the same amount of

Corporate Financial Management Page 19

US dollars from the bank. For example, if a SA exporter has sold goods for $1 million, he will

probably sell the US$ to the bank and will receive R11 370 000 from which the bank will

generally deduct commission. An SA importer buying $1 million from the bank will pay R11 720

000, plus the bank’s commission.

The financial papers quote spot exchange rates and also quote the forward spreads for one,

three, or more months in advance:

Currency Spot rates One month forward Three months forward

US Dollar 11.37 – 11.72 0.0439 – 0.0445 0.1362 – 0.1388

Euro 13.1812 – 13.6784 0.0583 – 0.0633 0.1857 – 0.1927

Pound Sterling 17.2233 – 17.8261 0.0630 – 0.0690 0.1980 – 0.2070

1.7.1 Premiums and Discounts

Premiums and discounts are quoted in fractions of a currency: cents for US dollars and euro,

pence for £. When calculating the forward rates, adding or deducting a premium or a discount

is a function of which currency is being referenced as the base currency and which the variable

currency. For example, if the US dollar is quoted at a premium one month forward and three

months forward against the Rand, this means that the value of the dollar is expected to rise

against the Rand, so a greater number of Rand will buy $1 in one month or three months than

today. Thus, the forward premium is added to the spot rate with the US dollar being the base

currency and the Rand the variable currency. Using interest rate parity, if the base currency

interest rate is lower than the variable currency rate, the forward exchange rate will be greater

than the spot rate. In this case, the base currency is said to be at a premium i.e. the US Dollar.

Conversely, the currency with the higher interest rate is worth fewer units of the other currency

forward than spot and is said to be at a forward discount i.e. the Rand in this example. Using

the spot rates and the forward rates shown above, the same information could alternatively

be set out as below:

Currency Spot rates One month forward Three months forward

US Dollar 11.37 – 11.72 11.4139 – 11.7645 11.5062 – 11.8588

Euro 13.1812 – 13.6784 13.2395 – 13.7417 13.3669 – 13.8711

Pound Sterling 17.2233 – 17.8261 17.2863 – 17.8951 17.4213 – 18.0331

Note: Exchange rates are provided by several South African and international financial newspapers including The Business Day, The Business Report and the Financial Times.

All printed rates should be taken as guide lines only. The Foreign Exchange market is very big and very active. Rates need to be ascertained from a bank to get an exact value in order to make financial decisions. The newspapers typically note that “These are indications rates only.”

24. Replace the Practical Example on page 347 with the following reworked example:

PRACTICAL EXAMPLE

Corporate Financial Management Page 20

The US dollar is quoted in South Africa at the following rate ($ to R):

Spot rates One month forward Three months forward

US dollar 11.57 – 11.92 0.0439 – 0.0445 0.1362 – 0.1388

Required:

• What does this mean the actual exchange rates will be for transactions one month and

three months forward?

• What is the R equivalent of a purchase of $1 million (selling Rand) one month forward?

• What is the R equivalent of a sale of $4 million (buying Rand) three months forward?

Answer:

Spot rates One month forward Three months forward

US dollar 11.57 – 11.92 11.6139 – 11.9645 11.7062 – 12.0588

• $1 million x 11.9645 = R11 964 500

• $4 million x 11.7062 = R46 824 800

25. Replace the typical exam question 2. on page 351 with the following:

Using the following table, show the exchange rates after one and three months:

Currency Spot rates One month forward Three months forward

US Dollar 11.37 – 11.72 0.0409 – 0.0415 0.1302 – 0.1328

Euro 13.1812 – 13.6784 0.0553 – 0.0603 0.1837 – 0.1907

and convert the following into Rand:

• Receive $100 000 in one month.

• Pay Euro 250 000 in one month.

• Receive Euro 40 000 in three months.

• Pay $600 000 in one month.

26. Replace: The US Dollar Exchange Rates next to Germany in the table on page 352 is

“Dollar/Euro” (not Euro/Dollar).

27. Expand the sentence to the International Fisher Effect formula on page 360 as follows:

“where nd is the domestic money rate of interest, nf is the foreign money rate of interest,

id is the domestic rate of inflation and if is the foreign rate of inflation.”

28. Add the following at the bottom of page 361:

Investors often have appetite to invest in foreign jurisdictions for various reasons. In South

Africa, some investors find it attractive to have “Rand hedges” in their investment portfolios

i.e. investments that benefit from a depreciation of the Rand against the US Dollar for

example. The questions is that given the forward exchange rate, what is the rate of interest

a local investor must earn in a foreign jurisdiction in order for it to be comparable to a

similar investment (and risk rating) locally? The following example illustrates this issue.

The Interest Rate Parity Model is being applied but instead of solving for a rate of

exchange, a rate of interest is being solved for.

PRACTICAL EXAMPLE

The exchange rate of the Rand against the US dollar is currently R12.00 to $1. An RSA

investor can make a one year local money market investment at 6.50% p.a. The $Rand

exchange rate one year from now is quoted at R12.5899.

Corporate Financial Management Page 21

Required:

Use the Interest Rate Parity Model to calculate the rate of interest the investor should earn

on a similar one year money market investment in the US that will equate to the 6.50%

available locally.

Answer:

The Interest Rate Parity Model gives nf, the foreign money rate of interest, in terms of So

(the current spot rate of the domestic currency), nd (the domestic money rate of interest)

and St (the spot rate of the domestic currency at time t) by the equation:

o

t

f

d

S

S

n

n

1

1

Which can be re-written as:

t

o

d

f

S

S

n

n

1

1

Solving for fn (the rate to be earned in the US):

1)]1(x [ d

t

of n

S

Sn

Substituting the values:

So = 12.00; nd = 0.065; St = 12.5899

in the equation above gives:

%51.11-(1.065)]x 5899.12

00.12[ fn

Assuming the investments are of similar risk, a return of less than 1.51% in the USA will not

be worthwhile for the RSA investor.

29. Replace the formula in paragraph 2.4.5 on page 366 (cost of forward exchange cover) with

the following:

“The annualised percentage cost will be determined by using the formula:”

Premium (or discount) x 12 x 100

Number of months forward cover required x Spot rate

30. Below is an additional Practical Example to be added at the bottom of page 372 (in addition

to the existing example on that page).

PRACTICAL EXAMPLE

A South African company needs to pay its US supplier $1 million in 3 months’ time. You

have been asked by the company to consider five possible choices:

Corporate Financial Management Page 22

a. No hedging

b. Hedge through Forwards

c. Hedge using the Money Markets

d. Arrange a Futures hedge.

e. Arrange an Option hedge.

You are also given the following information:

Date Today: 20 June 20.5

US$/ZAR Spot: 11.37/11.72

US$/ZAR in 3 months can be: 11.50 or 12.00 (do calculations for both)

Forwards: 1 month 11.4145/11.7639

3 months 11.5088/11.8562

Interest Rates (naca): USA 2.00%/2.40%

RSA 6.00%/6.50%

Futures (via JSE): US$ Contract Size $1000.00

Initial Margin R310.00 per contract

Futures Prices (per $1.00):

September 20.5 R11.84

December 20.5 R11.95

March 20.5 R12.07

Options (via JSE): US$ Contract Size $1000.00

Premiums (ZAR cents per $1.00):

Exercise Price: Call Options: Put Options:

(US$/ZAR) Sep Dec Sep Dec

11.75 20 40 5 10

12.00 10 20 11 25

12.25 5 10 35 50

Answer:

Before answering the question, let us consider which side of the bid/offers above we should

use. The rule of thumb is that the banks always make money through the bid/offer prices

and the bank’s customer always loses money in this process. Thus, calculate both sides

and see which side is more detrimental to the customer, which will be the figure used in the

calculation.

Considering each alternative in turn:

a. No hedge, i.e. purchase $1m at the spot rate in 90 days’ time. The forecast cost at

R11.50 is $1m x R11.50 = R11 500 000 and at R12.00 is $1m x R12.00 = R12 000 000.

b. Forward hedge i.e. purchase $1m 3 months forward: R cost = $1m x forward rate of

R11.8562 = R11 856 200. These hedges are typically done OTC. It does not matter

where the exchange rate is in 3 months’ time i.e. the cost has effectively been locked

in at the Forward Rate.

c. Money Market hedge consists of 3 steps:

Corporate Financial Management Page 23

i) How much US$ is required today in order to pay $1m in 3 months’ time? This is a

simple PV calculation by investing the required US$ at 2.00% naca (from the table

above) for 3 months. Enter the following into a financial calculator: FV = $1m, i = 2%,

n = 1/4 years, then calculate the PV as $995 062. (Can convert 2.00% naca to nacq

of 1.985% then FV = $1m, i = 1.985%/4, n = 1 quarter, then PV = $995 062.

ii) Buy the $995 062 needed today through the spot exchange rate i.e. $995 062 x

R11.72 = R11 662 127.

iii) The ZAR needs to be borrowed for 3 months to buy the $, thus borrow R11 662 127

x 6.50% = R189 510 in interest. This interest combined with the amount borrowed

equals to a total cost of R11 851 637 (R11 662 127 + R189 510)

d. Do a 3 month Futures hedge at R11.84 x $1 000 000 = R11 840 000. Again, as with

Forwards, this amount is locked in regardless of where the exchange rate is in 3

months. Note however that with Forwards, it can be tailored to the exact date of hedging

required in the OTC market while Futures can only be traded at the fixed standardised

dates. Thus, if the required hedge date and Futures date do not coincide, there remains

a risk of loss due to the maturity mismatch. Futures also require initial and variation

margin. 1000 Futures contracts will be required ($1 000 000/$1 000) x R310 initial

margin = R310 000. Thus, borrow R310 000 at 6.50% for 3 months = R5038 and pay

the initial margin to the exchange, on which interest will be earned at 6% for 3 months

= R4650. The net finance cost is R388 (R5038 - R4650). Total cost of the Futures

contract is R11 840 388 (R11 840 000 + R388).

e. With the option hedge, US$ needs to be purchased i.e. purchase a call option on US$.

The option contract size is $1 000, thus 1000 option contracts are required ($ 1000 000/

$1 000). Call options expiring in 3 months are required so September 20.5 calls need to

be purchased (these are European style options that can only be exercised on the expiry

date). The question then is at what exercise price should the options be done? There

are three alternatives (the effective cost is the exercise price + the option premium):

- R11.75 + R0.20 = R11.95

- R12.00 + R0.10 = R12.10

- R12.25 + R0.05 = R12.30

From the above, the cheaper option is at an exercise price of R11.75 with an option

price of R0.20 per $1 000 000. The option premium per contract is R0.20 x $ 1000 =

R200. The total option premium is then 1000 contracts x R200 = R200 000. The cost of

exercising the option at the exercise price of R11.75 will be $1 000 000 x R11.75 =

R11 750 000. The total cost of buying and exercising the option will be R11.95 x

$1 000 000 = R11 950 000. Note again that if the required hedge date and options

expiry date do not coincide, there remains a risk of loss due to the maturity mismatch.

Alternatively, purchase OTC options from a reputable counterparty that will match the

European option expiry date with the required hedging date.

If the US$/ZAR exchange rate is R11.50, then the comparisons would be:

a) R11 500 000 – cheapest but with open risk

b) R11 856 200 – hedged to the exact date

c) R11 851 637 – also hedged to the exact date

d) R11 840 388 – cheaper than the forward but with basis risk

e) R11 700 000 i.e. no need to exercise (R11 500 000 + R200 000 premium) –

cheapest of the 4 hedging methods

Corporate Financial Management Page 24

If the US$/ZAR exchange rate is R12.00, then the comparisons would be:

a) R12 000 000 – most expensive

b) R11 856 200 – hedged to the exact date

c) R11 851 637 – also hedged to the exact date

d) R11 840 388 – cheapest but with basis risk

e) R11 950 000 (Exercised at R11.75 = R11 750 000 + R200 000 premium) – most

expensive of the 4 hedging methods but with upside potential

Comparing the five alternatives above the cheapest and the most expensive is not to hedge

at all but it is the riskiest – (a). The forward hedge (b) removes all uncertainty by fixing the

Exchange Rate now to the exact required hedging date. The Money Market hedge (c) is a

very close approximation of (b) as it should be, given that both are hedges to the exact date

and dependent on the same pricing drivers. Always calculate both and choose the cheapest

one. Futures (d) can be very attractive due to their standardised nature, tradability and

attractive pricing but they are not tailored for bespoke hedging dates and can leave the

hedger with basis risk. Options provide the hedger with “insurance” protection through the

payment of the premium while enjoying the upside, should the exchange rate move in a

favourable direction. In summary, (a) is too risky, (b to d) are used if the hedger is fairly

convinced or concerned that the exchange rate will deteriorate and (e) is used if the hedger

requires protection against a deterioration of the exchange rate but would also like to benefit

from a favourable move in the exchange rate.

Note that if the option premium above was quoted per ZAR1.00, then the $1m must first be

converted to its ZAR equivalent at the current spot rate (re: the premium is payable now)

and then multiplied by the ZAR option premium.

31. Replace the formula for Standard Deviation on page 400 with the formula below: Standard deviation is

N

X)(Xs

2

i

And the variance is s2

FORMULAE Note: these formulae are supplied in the examination paper (without the

keys). You are not expected to know them by heart, but you must be able to use and

apply them where necessary.

Corporate Financial Management Page 25

Sources of Finance

Equity:

Cost of Equity = (Ke)

There are 3 ways to

calculate Ke namely:

i) DDM (if given level of

dividend & rate of

growth derived from

Gordons’s Growth

Model – see below)

ii) CAPM (if given the

risk-free rate and

market return)

iii) Dividend Yield method

Ke = (Do (1+g)/Po) + g Do (1+g) = future dividend Po = current share price (ex-div) Do = current dividend g = rate of growth Ke = rf + (rm - rf)ß where: rf = risk free rate (return on government security) rm = expected return on market (rm - rf) = equity risk premium (maybe given as a whole in exam) ß = beta factor (level of systematic risk faced by an investor)

OR

E(ri) = Rf + ßi (E(rm) – Rf) where: E(ri) = the return from the investment Rf = the risk free rate of return ßi = the beta value of the investment, a measure of the systematic risk of the investment E(rm) = the return from the market

o

oe

P

dK

Where:

Ke = cost of equity

do = current dividend payable

Po = current ex dividend share price

Preference shares:

Cost of Preference shares

= (Kp)

p

p

pS

dK

Corporate Financial Management Page 26

Where:

Kp = cost of preference shares

dp = fixed dividend based on the nominal value of the shares

Sp = market price of preference shares

Debt:

Cost of Debt = (Kd)

There are 3 ways to calculate Kd namely: i)Perpetual (Irredeemable)

ii) Redeemable

iii) Non-tradable debt,

such as bank loans

d

dS

t1IK

)(

Where:

Kd = cost of debt capital

I = annual interest payment

Sd = current market price of debt capital

t = the rate of company tax applicable

Kd = IRR (1-T) Where: IRR = Internal Rate of Return T = Rate of tax Kd = %I (1-T) Where: %I = Interest paid in percentage T = Rate of tax

Breakeven EBIT

(solve for EBIT)

shares ofNumber

Interest) - t)(EBIT-(1 = EPS

shares ofNumber

Interest) - t)(EBIT-(1 =

Gordon's Growth Model

(DDM) P0= d0

1 + g

Ke g

Where:

Po = the current ex-dividend market price

do = current dividend

g = growth rate

Ke (or R in some texts) = expected return

Growth rate

𝑔 = √𝐿𝑎𝑡𝑒𝑠𝑡 𝑑𝑖𝑣𝑖𝑑𝑒𝑛𝑑

𝐸𝑎𝑟𝑙𝑖𝑒𝑠𝑡 𝑑𝑖𝑣𝑖𝑑𝑒𝑛𝑑

𝑛

− 1

Corporate Financial Management Page 27

Weighted Average Cost

of Capital (WACC)

DE

Dt1K

DE

EK deg )(

where:

Keg = the cost of equity in the geared company

Kd = the cost of debt before tax relief

E = the market value of the company’s equity

D = the market value of the company’s debt

t = the rate of company tax applicable to the company

Gearing

Basic financial gearing

formula Gearing % =

Long term liabilities

Capital employed x 100

= ( Debt

Debt + Equity)

Degree of operational

leverage/gearing (DOL)

DOL = Contribution

EBIT

where: Contribution = Sales minus Variable Costs EBIT = Earnings before Interest and Tax

Discounts

Discount factor 1/(1 + i)n

Effective discount rate

annualised (Cost of early

payment discount

foregone)

td

d 365

100

where d = the percentage discount offered for early payment t = the reduction in days in the payment period required to earn the discount

Interpolation of Internal

Rate of Return (IRR)

low rate +

rate) low - ratehigh (

rate)high NPV - rate low (NPV

rate low NPV

Profitability index

(Cost/benefit ratio)

PV of future inflows (discounted at the cost of capital)

PV of initial investment outflows

Inventory

Economic Ordering Quantity EOQ =√

2 (Cost per order)(Annual usage in units)

Annual holding cost per unit

Corporate Financial Management Page 28

=h

Cd2

Combined cost of inventory holding and inventory ordering over one year

Q

dCh

2

Q or hxdxcx2

where:

h= cost of holding one unit of inventory for one year

C = cost of ordering a consignment from a supplier

d = annual demand in units

Q = reorder quantity

Inventory days

Inventory holding at end of period x no. of days in period

Cost of materials purchased in the period = no of days

Shares

Earnings per share Market value per share ÷ P/E ratio

Share Issue costs g

I P

g1dK

o

oe

)(

Where:

Ke = cost of equity

do = current dividend payable

Po = current share price (ex div)

I = issue cost per share

Capital Market Line

(CML) p

m

fmfm σ

σ

RRRR

Where:

m

p

σ

σ= beta factor β

Rf = the risk-free rate of return

Rm = the market rate of return (the return on the all share index)

Ơp = standard deviation of portfolio returns

Ơm = standard deviation of market returns

The relationship

between the nominal

cost of capital and the

real cost of capital

(1 + nominal interest rate) = (1 + real interest rate) x (1+ inflation

rate)

(1 + n)=(1 + r)*(1 + i)

where:

n = the nominal or money cost of capital

r = the real cost of capital

i = the rate of inflation

Corporate Financial Management Page 29

The equation above can be arranged in the form:

i1

n1r1

This can be re-arranged to give:

i1

i - nr

ARR method (Share

Value)

Value = estimated future profits/required return on capital

employed

Capital Asset Pricing Model (see also above)

(Rs – Rf) = β(Rm - Rf)

or

(Rs) = Rf + β(Rm - Rf)

where:

Rs = expected return from an individual investment

Rf = the risk-free rate of return

Rm = the market rate of return (the return on the all share index)

β = the beta factor of the investment

Beta factor β

m

p

σ

σ = β in Rp = Rf + β(Rm − Rf)

where:

Rp = the return required on a portfolio by an investor

β = the beta factor

Rm = the return required for holding the market portfolio

Rf = risk-free rate

Ơp = standard deviation of portfolio returns

Ơm = standard deviation of market returns

m

sms p

(with correlation)

Ơs = standard deviation of the share’s returns

Ơm = standard deviation of market returns

Ƿsm = correlation between the share’s returns and market returns

The beta value of a

geared company

calculated from the

ungeared beta and the

gearing ratio (as per

Modigliani and Miller)

βg = βug [1 + Vd(1 - t)/Veg]

where:

βg = β of geared firm

βug = β of ungeared firm

Vd =Value of debt Veg =Value of equity in the geared firm

t = Tax rate

MM’s first proposition Vd +Veg =Veug = earnings before interest/WACC

Corporate Financial Management Page 30

where: Vd =Value of debt Veg =Value of equity in the geared firm Veug =Value of equity in the ungeared firm

Arbitrage Pricing Model

(APM)

Rs = E(rj )+ β1F1 + β2F2 + β3F3 + β4F4 + ..........e

where:

Rs = the realised/actual return from the security

E (rj) = the expected return from the security

β1 = the sensitivity to changes in factor 1

F1 = the difference between expected and actual values of factor

1

β2 = the sensitivity to changes in factor 2

F2 = the difference between expected and actual values of factor

2

β3 = the sensitivity to changes in factor 3

F3 = the difference between expected and actual values of factor

3

β4 = the sensitivity to changes in factor 4

F4 = the difference between expected and actual values of factor

4

e = a random term for idiosyncratic risk

APM (no arbitrage

remain)

E(rj )= rf + β1(r1 − rf)+ β2(r2 − rf)+ β3(r3 − rf)+ β4(r4 − rf)+ ...........

where: rf = the risk-free rate

r1 = the expected return on a portfolio which has unit sensitivity

to factor 1 and zero sensitivity to any other factor

r2 = the expected return on a portfolio which has unit sensitivity

to factor 2 and zero sensitivity to any other factor

r3 = the expected return on a portfolio which has unit sensitivity

to factor 3 and zero sensitivity to any other factor

r4 = the expected return on a portfolio which has unit sensitivity

to factor 4 and zero sensitivity to any other factor

Miller-Orr model

Spread = 3 × √0.75 × variance of cash flow × transaction cost

interest rate

3

Cost of convertible

debentures n

n

n32or1

CRV

r1

t1I

r1

t1I

r1

t1I

r1

t1IP

)()()()(

where:

P0 = current market price of the convertible ex interest (i.e. after

paying the current year’s interest)

I = annual interest payment

t = rate of company tax

r = cost of capital

Corporate Financial Management Page 31

Vn = projected market value of the shares at year n, when

conversion

can take place

CR = conversion ratio

Mergers and Acquisitions

Exchange Ratio (ER)

based upon Market Value

ERT = Market Value per Target Company Share/Market Value

per Acquiring Company Share:

A

TT

MP

MPER

Exchange ratio with

synergistic benefits 1MP

ER MP premiumMarket

T

TA

Synergistic benefits are to

be allocated to the target

company’s shareholders AT

AMT

MP N

MVMVER

Where:

MVM = Market value of merged firm

MVA = Market value of acquiring firm

NT = Number of shares in issued share capital of target

company

MPA = Market price per share of acquiring company

Synergistic benefits are to

be retained by the

acquiring company )MV (MVN

N x MVER

TMT

AT

Where:

MVT = Market value of target firm

NA =Number of shares in issued share capital of acquiring

company

MVM = Market value of merged firm

Maximum exchange ratio

to be offered by the

acquiring company

ERmax=EPS𝑇

EPSA

+SE

EPSAN𝑇

Where: EPST = EPS of the target company

EPSA = EPS of the acquiring company

SE = Synergistic Earnings (annual earnings)

NT = Number of target company’s shares

NA = Number of acquiring company’s shares

Minimum exchange ratio

the target company can

accept

ERmin=EPS𝑇NA

SE + EPSANA

Sustainable Growth Rate

SGR =D

E (R − i)p + Rp

Corporate Financial Management Page 32

Where: R = % return on assets after tax p = proportion of earnings retained D = debt E = equity i = % interest rate on debt after tax

Exchange Rates

Purchasing Power Parity St

So

=I+id

I+if

Where: So = the spot (current) rate of the domestic currency against the

foreign currency

St = the spot rate at time t

if = the expected rate of inflation in the foreign country to time t

id = the expected domestic rate of inflation to time t. Cost of forward exchange cover

Premium (or discount) x 12 x 100

Number of months forward cover required x Spot rate

The Fisher equation (1 + money or nominal rate of return) = (1 + real rate of return)

x (1 + expected rate of inflation)

The International Fisher Effect can be expressed as:

d

f

d

f

i

i

n

n

1

1

1

1

Where:

nd is the domestic money rate of interest

nf is the foreign money rate of interest

id is the domestic rate of inflation

if is the foreign rate of inflation

Interest Rate Parity

of

d

S

St

n

n

1

1

Where:

nd is the domestic money rate of interest and

nf is the foreign money rate of interest

St, the spot rate at time t, in terms of:

So the spot (current) rate of the domestic currency against the

foreign currency

Z score

Z = 1.2 X1 + 1.4 X2 + 3.3 X3 + 0.6 X4 + 1.0 X5

where:

X1 = Working capital/total assets

X2 = earnings/total assets

Corporate Financial Management Page 33

X3 = earnings before tax and interest/total assets

X4 = market value of equity/book value of total debt

X5 = sales/total assets

Interest Rate Conversions

where: Ro = Rate of interest required (output) Ri = Rate of interest to be converted (input) Mo = Number of months required (output) Mi = Number of months corresponding with Ri above (input)

Beaver’s Ratio

(Default prediction)

Cash Flow from Operations

Total Debt

Financial Ratios

Current ratio = Current assets

Current liabilities

Quick ratio = Current assets – inventory

Current liabilities

Inventory turnover = Cost of sales/Purchases

Inventory

Inventory days =

Inventory x 365 Cost of sales/Purchases

Average collection = Accounts receivable x 365

Sales

Fixed asset turnover = Sales

Fixed assets

Asset turnover = Sales

Operating assets

Debt ratio = Debt

Total assets

Debt to equity = Total debt

Total equity

Times interest earned = EBIT

Interest

EBITDA coverage = EBIT + depreciation + amortisation

Interest

Fixed charge coverage = EBIT + depreciation + amortisation + lease payments

Interest + lease payments

o

M

M

iio

M

MRR i

o

12x }1]))

12 x(1{[(

Corporate Financial Management Page 34

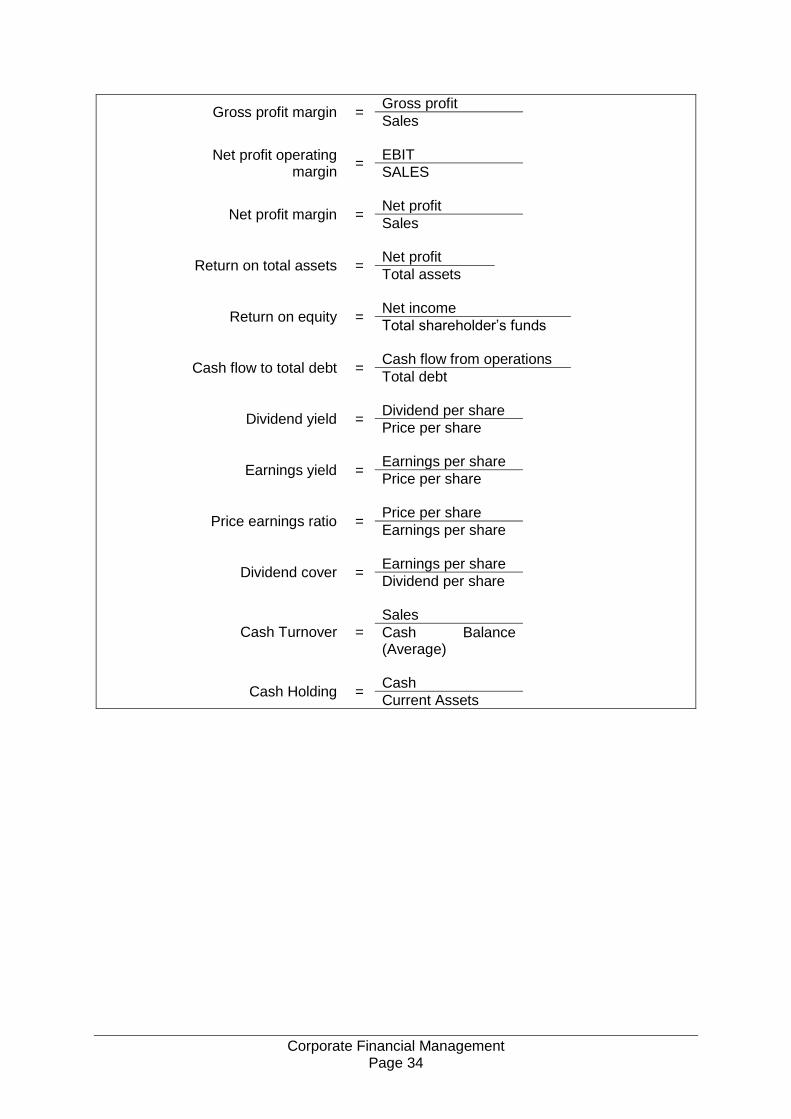

Gross profit margin = Gross profit

Sales

Net profit operating margin

= EBIT

SALES

Net profit margin = Net profit

Sales

Return on total assets = Net profit

Total assets

Return on equity = Net income

Total shareholder’s funds

Cash flow to total debt = Cash flow from operations

Total debt

Dividend yield = Dividend per share

Price per share

Earnings yield = Earnings per share

Price per share

Price earnings ratio = Price per share

Earnings per share

Dividend cover = Earnings per share

Dividend per share

Cash Turnover =

Sales

Cash Balance (Average)

Cash Holding = Cash

Current Assets