Embed Size (px)

Citation preview

Where Math Gets Real

from

Sup

ple

men

t to

Sch

olas

tic M

agaz

ines

. SC

HO

LAS

TIC

and

ass

ocia

ted

logo

s ar

e tr

adem

arks

and

/or

regi

ster

ed t

rad

emar

ks o

f Sch

olas

tic In

c.

All

right

s re

serv

ed. 0

-545

-849

18-7

MO

NE

Y C

ON

FID

EN

T K

IDS

is a

reg

iste

red

tra

dem

ark

of T

. Row

e P

rice

Gro

up, I

nc.,

2014

-US

-669

5 P

hoto

: © M

ikeg

ol/D

ream

stim

e.

A supplement to

With tons of spending opportunities, do

you feel equipped to make smart money choices?

®

Check out Star Banks Adventure, an all-new financial education game at www.scholastic.com/MCK.

2

You have goals. Big ones, most likely! But an overwhelming number of young people—83%—admit they don’t know much about managing money.1 And only 38% of young people say they are currently putting money aside to spend later.2 If you’re like most teens, your goals are a combination of short-term wants, like having some cash for a movie, and long-term desires, like saving for college or buying a car.

So here’s the real question: What do you want and what’s your plan for getting there?

First, stop thinking of money in two buckets—spending and saving. It’s really all spending. The difference is whether you’re planning to spend now or spend later.

Use this magazine and your own research to create a spending plan that will help you meet your goals. Keep track of your progress and don’t be afraid to make changes if something isn’t working.

What’s Financial Path?

What’s your goal?

How much do you think your goal will cost?

When do you want to reach your goal?

Look at how much money you receive each year from jobs or gifts. How much do you need to put aside each month or week to achieve your goal? What spending choices do you need to make to reach your goal on time?

Every year $258 billion is spent on and by young people like you.3 But do you really know what you’re spending your money on? The average 12- to 14-year-old receives $2,767 per year from a combination of jobs and gifts.4 Imagine that you really want a new tablet (cost: $750) to build a new app you’re thinking about developing. That seems like a reasonable amount to spend based on an annual income of $2,767, right? You just need to tuck some money aside each month until you have enough to buy your dream tablet.

Here’s the problem:Retailers use a variety of marketing

strategies to get people to spend their money now instead of later.

Impulse buys are purchases that are made for immediate enjoyment, like a candy bar at the checkout, a T-shirt at a concert, or an extra snack at the movie theater. They are

not planned purchases like the tablet we mentioned above.

Check the impulse! Approximately 40% of all purchases are impulse buys5, so think carefully about your long-term goals before spending:

• Did I want this before I came into the store?

• Is there a sale sign, a coupon, or other advertising that is tempting me to buy this item?

• Is the price reasonable?

• How much longer will it take me to make my larger purchase if I spend now?

SPENDING

What

How Much

When

Calculate

Think About It

Check out Star Banks Adventure, a financial education game at www.scholastic.com/MCK.This magazine contains commentary from third-party sources unaffiliated with T. Rowe Price. Use of this content does not imply endorsement from T. Rowe Price. T. Rowe Price makes no guarantees that information supplied is accurate, complete, or timely. 2016-US-24620

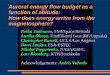

1 2 3 4 5 6 7 8 9 10

Poun

d

Number of Years

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Lauren

Carly

3

Twin Tales of SpendingLauren and Cassidy are twins. When they were 12, they opened their first bank accounts. Lauren decided that she wanted to buy a car after college and put $100 a month into an investment account for the next 10 years with the allocation of 60% stocks, 30% bonds, and 10% money market funds. Cassidy decided to spend $100 a month for a gym membership. She kept her membership for seven years and then started putting $100 a month into a savings account to pay for a graduation trip to Paris. When they were 22 years old they looked at their accounts and were happy. Lauren had $17,202 and Cassidy had $3,628—goals met!

SPENDING

Getting ready to make a big purchase like a used car, concert tickets, or a racing bike feels great! You can see

your money grow, and anticipating your purchase gives you time to make sure

you’re getting the best deal.

of teens said they were saving for clothes6

of teens said they were saving for a car 7

PLANNING AHEAD

What the Average Teen Buys

Food 20%

Accessories/Personal Care

10%

Other 3%

Furniture 1%Books/

Magazines 2%

Events 6%

Music/ Movies

6%

Video Games

7%

Electronics 7%

Shoes 8%

Car 9%

Clothing 21%

57% 36%What about you?

Sou

rces

: 1. I

NG

DIR

EC

T U

SA

Sur

vey

(htt

p:/

/prn

.to/

1A4s

dG

w);

2, 3

, 4, 6

, 7.

Mar

ketin

gvox

, Ran

d Y

outh

Pol

l, S

even

teen

mag

azin

e, P

acka

ged

Fac

ts (h

ttp

://w

ww

.sta

tistic

bra

in.c

om/t

eena

ge-c

onsu

mer

-sp

end

ing-

stat

istic

s/);

5. T

he C

heck

out

cond

ucte

d b

y Th

e In

tege

r G

roup

® a

nd M

/A/R

/C R

esea

rch

(htt

p:/

/ww

w.p

rnew

swire

.com

/new

s-re

leas

es/s

tud

y-sh

ows-

nine

-out

-of-

ten-

shop

per

s-m

ake-

imp

ulse

-pur

chas

es-1

4773

3845

.htm

l).

NOTE: This example assumes an annual rate of return of 7% for equity funds, 5% for bond funds, .8% for Money Market funds and 0.5% for a savings account.

Check out Star Banks Adventure, a financial education game at www.scholastic.com/MCK.This magazine contains commentary from third-party sources unaffiliated with T. Rowe Price. Use of this content does not imply endorsement from T. Rowe Price. T. Rowe Price makes no guarantees that information supplied is accurate, complete, or timely. 2016-US-24620

The Value of

Goals come in all shapes and sizes. But to create a solid financial plan, you need to know how quickly you want to reach them.

LOOKING AHEAD

Source: www.usinflationcalculator.com/inflation/current-inflation-rates/

4

3.3%3.4%

4.1%

2.5%

0.1%

2.7%

1.5%

3.0%

1.7%

1.5%

0.8%

4%

3%

2%

1%

Inflation Rates (2004–2014)

Short-Term(within 2 years)

Medium-Term(within 2–15 years)

Long-Term(more than 15 years)

20042005

20062007

20082009

20102011

20122013

2014

In 1908, Milton Hershey began selling one of the first mass-produced chocolates in the United States—the Hershey bar! The price was 2 cents, and the average American earned $574 a year.8 Today, that same candy bar costs more than $1—a 4,900% rise in price.9 This increase over time is called inflation. But what causes it?

Inflation happens for a variety of reasons, including market power, demand, and supply. Market power occurs when a company or group controls most (or all) of one particular resource. They can then set the price that they want, as long as people are still willing to pay it. When a lot of people want something, the increased demand raises prices. We see supply-related price increases when a product people want becomes less available. This inflation in prices causes money to lose value over time.

Check out Star Banks Adventure, a financial education game at www.scholastic.com/MCK. This magazine contains commentary from third-party sources unaffiliated with T. Rowe Price. Use of this content does not imply endorsement from T. Rowe Price. T. Rowe Price makes no guarantees that information supplied is accurate, complete, or timely. 2016-US-24620

5

Sou

rces

: 8, 9

. Foo

d T

imel

ine

(htt

p:/

/ww

w.fo

odtim

elin

e.or

g/fo

odfa

q5.

htm

l#ca

ndyb

ar);

10. T

he 1

0 B

est

Sav

ings

Acc

ount

s in

201

5 (h

ttp

://m

oney

.usn

ews.

com

/mon

ey/b

logs

/my-

mon

ey/2

015/

01/1

6/th

e-10

-bes

t-sa

ving

s-ac

coun

ts-i

n-20

15)

If you put money into a savings account, you will earn .17% in interest (on average10) each year. This means if you put $100 in a savings account when you’re 10 (and don’t spend any of it), you will have $101.70 in your account when you are 20 years old.

Now let’s say you wanted to buy a bike with your savings. Today a great bike could cost you about $100. However, in 10 years an equally amazing bike would cost $134.39.

Due to inflation, your $100 might actually buy you less in 10 years! But you can keep that from happening.

Asset allocation is all about finding ways to make your money work hard for you before you need to spend it. First, decide whether your goals are short term, long term, or somewhere in the middle. If you need to buy a new soccer uniform next week, that’s a short-term goal. Inflation won’t increase the cost of your uniform that quickly, so it makes sense to put your money into a savings account (so it’s out of your pocket and you’re not tempted to spend it).

Starting a college fund when you’re 10, however, is a longer term goal. You should consider strategies that will grow your college fund, such as investing in a combination of stocks and bonds. If you put in $200, you could have more than $200 once you’re ready to start sending in applications!

MAKING MONEYHistory shows that bonds and stocks can earn more money over time. In the short term, however, they are riskier than a simple savings account. Based on the time horizon of your goal, select a good mix of investments. You will need to make sure that you own a blend of different kinds of stocks and bonds. This mix is important because if you were to buy all the same kind of stock (such as fast-food or video-game companies) and people suddenly stopped purchasing those products, you’d be in trouble. However, a blend of stocks (which can be easy to get with a mutual fund) provides better protection. As your goal gets closer, you may want to move your money into a combination of bonds and a savings account.

An asset is something useful or valuable.

YOU CAN DO IT!

Check out Star Banks Adventure, a financial education game at www.scholastic.com/MCK.This magazine contains commentary from third-party sources unaffiliated with T. Rowe Price. Use of this content does not imply endorsement from T. Rowe Price. T. Rowe Price makes no guarantees that information supplied is accurate, complete, or timely. 2016-US-24620

AC

TIV

ITY

• G

oal:

Vaca

tion

to P

aris

• T

ime

Hor

izon

: 3 y

ears

• F

lip a

coi

n to

dec

ide

whi

ch

actio

n to

take

WH

AT

YO

U’L

L N

EE

D

• O

ne c

oin

• 1

5 m

inut

es

You

earn

ed

$1,0

00 m

owin

g la

wns

this

su

mm

er

Dec

isio

n P

oint

: Flip

a c

oin

Hea

ds

Hea

dsH

eads

Tails

Tails

Tails

Yea

r 1

:

Goal

:Di

d y

ou

mee

t

your

goal

of

a

Paris

vaca

tion?

Out

com

e:

How m

uch

is lef

t in

th

e ba

nk?

Sor

ry! Y

ou d

idn’

t sav

e

enou

gh m

oney

to g

o to

P

aris

. You

spe

nd a

wee

k

at h

ome

inst

ead.

Sor

ry! Y

ou d

idn’

t sav

e

enou

gh m

oney

to g

o to

Par

is,

but y

ou s

till h

ave

enou

gh to

go

on

vaca

tion.

You

dec

ide

on a

road

trip

to th

e be

ach.

Sor

ry! Y

ou d

idn’

t sav

e

enou

gh m

oney

to g

o to

Par

is,

but y

ou s

till h

ave

enou

gh to

go

on

vaca

tion.

You

dec

ide

to

vis

it ne

arby

rela

tives

.

GO

AL

ME

T!

You

earn

ed e

noug

h

to ta

ke y

our d

ream

va

catio

n to

Par

is!

You

have

$1,

000

afte

r sav

ing

your

mon

ey e

arne

d fro

m s

umm

er c

hore

s! It

’s p

erfe

ct ti

min

g be

caus

e yo

u’re

sav

ing

up fo

r a h

igh

scho

ol g

radu

atio

n tri

p to

Par

is. Y

ou k

now

that

you

nee

d at

leas

t $2,

700

to p

ay fo

r flig

hts,

hot

els,

and

sou

veni

rs. U

se a

coi

n to

pla

y th

e ga

me

belo

w a

nd s

ee h

ow a

ddin

g m

oney

to y

our s

avin

gs a

ccou

nt c

an h

elp

your

mon

ey g

row

fast

er a

nd h

elp

you

mee

t you

r goa

l!

Out

com

e:

$1,

01

5 in

acc

oun

tO

utco

me:

$

1,6

23

in a

ccou

nt

Out

com

e:

$2

,27

1 in

acc

oun

tO

utco

me:

$

2,8

28

in a

ccou

nt

Hea

ds o

r Ta

ils S

avin

gs

You

put $

1,00

0

into

a s

avin

gsac

coun

t ear

ning

0.

5% in

tere

st

You

put $

1,00

0

into

a s

avin

gs

acco

unt e

arni

ng

0.5%

inte

rest

+

adde

d $5

0/m

onth

to

the

acco

unt

You

leav

e yo

ur m

oney

w

here

it is

You

stop

addi

ng$5

0/m

onth

You

star

t add

ing

$50/

mon

th m

ore

to

you

r acc

ount

You

keep

ad

ding

$50/

mon

th

Yea

r 3

:

Out

com

e:

$1,

60

6 in

acc

oun

tO

utco

me:

$

1,0

05

in a

ccou

nt

Dec

isio

n P

oint

Dec

isio

n P

oint

6

4% R

etur

nB

alan

ce: $

6,5

68

6% R

etur

nB

alan

ce: $

9,6

18

6.5%

Ret

urn

Bal

ance

: $1

0,5

71

Rol

l: 5–

8R

oll:

2–4

Rol

l: 9–

12

AC

TIV

ITY

• G

oal:

O

wn

a ca

r

• T

ime

Hor

izon

: 20

yea

rs

• R

oll t

he d

ice

to d

eter

min

e yo

ur c

ours

e of

act

ion

WH

AT

YO

U’L

L N

EE

D

• T

wo

dice

• 1

5 m

inut

es

AV

ER

AG

E

PE

RC

EN

TAG

E

EA

RN

ED

Y

EA

RLY

IN

RE

TU

RN

S

• S

tock

s: 8

%•

Bon

ds: 5

%

You’

ve in

herit

ed $

3,00

0! N

ow it

’s ti

me

to s

ee th

e di

ffere

nt w

ays

that

mon

ey c

an g

row

ove

r tim

e to

hel

p yo

u ac

hiev

e yo

ur lo

ng-te

rm g

oals

, su

ch a

s bu

ying

a c

ar. R

oll y

our w

ay th

roug

h th

ree

diffe

rent

inve

stm

ent o

ptio

ns a

nd te

st th

e re

sults

! A p

ositi

ve r

etur

n m

eans

that

the

stoc

k

or b

ond

you

inve

sted

in g

ener

ated

mor

e m

oney

than

you

put

into

it. A

neg

ativ

e re

turn

mea

ns th

at y

ou lo

st s

ome

mon

ey y

ou in

vest

ed.

Ris

k M

anag

emen

t Dec

isio

n

Yea

r 20

Out

com

e:

Yea

r 10

Out

com

e:

You

inve

st$3

,000

eve

nly

betw

een

2bo

nd fu

nds

You

have

posi

tive

retu

rns

on y

our f

unds

!

5% R

etur

nB

alan

ce:

$4

,88

7

You

have

a

nega

tive

retu

rn

on o

ne o

f yo

ur fu

nds

3% R

etur

nB

alan

ce:

$4

,03

2

You

have

a

10-y

ear

perio

d w

ith a

ne

gativ

e re

turn

and

a

10-y

ear p

erio

d w

ith n

o ne

gativ

e re

turn

s

You

have

a

nega

tive

retu

rn

on o

ne o

f yo

ur fu

nds

3% R

etur

nB

alan

ce:

$5

,41

8

You

have

posi

tive

retu

rns

on y

our f

unds

!

5% R

etur

nB

alan

ce:

$7,

96

0

You

inve

st$3

,000

eve

nly

in

2 b

ond

fund

san

d 2

stoc

kfu

nds

You

have

posi

tive

retu

rns

on y

our f

unds

!

6.5%

Ret

urn

Bal

ance

: $

5,6

31

Loss

. But

be

caus

e yo

u in

vest

ed in

sev

eral

fu

nds,

you

did

n’t

lose

muc

h ov

eral

l!

5.5%

Ret

urn

Bal

ance

: $

5,1

24

You

have

a

10-y

ear

perio

d w

ith a

ne

gativ

e re

turn

and

a

10-y

ear p

erio

d w

ith n

o ne

gativ

e re

turn

s

Loss

. But

be

caus

e yo

u in

vest

ed in

sev

eral

fu

nds,

you

did

n’t

lose

muc

h!

5.5%

Ret

urn

Bal

ance

: $

8,3

47

You

have

posi

tive

retu

rns

on y

our f

unds

!

6.5%

Ret

urn

Bal

ance

: $

10

,57

1

You

inve

st$3

,000

eve

nly

betw

een

2st

ock

fund

s

You

have

posi

tive

retu

rns

on y

our f

unds

!

8% R

etur

nB

alan

ce:

$6

,47

7

You

have

a

nega

tive

retu

rn

on o

ne o

f yo

ur fu

nds

5% R

etur

nB

alan

ce:

$4

,88

7

You

have

a

10-y

ear

perio

d w

ith a

ne

gativ

e re

turn

and

a

10-y

ear p

erio

d w

ith n

o ne

gativ

e re

turn

s

You

have

a

nega

tive

retu

rn

on o

ne o

f yo

ur fu

nds

5% R

etur

nB

alan

ce:

$7,

96

0

You

have

posi

tive

retu

rns

on y

our f

unds

!

8% R

etur

nB

alan

ce:

$1

3,9

83

You

in

herit

ed

$3,0

00 fr

om y

our

gran

dpar

ents

.W

hat w

ill

you

do?

Rol

l: 2–

4

Roll: 1

0–12

Roll: 11

–12

Roll: 11

–12

Rol

l: 7–

9

Rol

l: 8

–10

Rol

l: 8

–10

Roll: 2–

6

Roll: 2–7

Roll: 2–7

Rol

l: 2–

3R

oll:

2–5

Rol

l: 5

–12

Rol

l: 4–

12R

oll:

6–12

*Not

e: A

ll in

vest

ing

invo

lves

risk

, inc

ludi

ng th

e lo

ss o

f mon

ey y

ou in

vest

. Pro

babi

litie

s in

this

less

on d

o no

t refl

ect r

eal r

etur

ns a

nd a

re u

sed

for t

each

ing

purp

oses

onl

y.

LE

AS

ED

CA

RL

EA

SE

D C

AR

LE

AS

ED

CA

RL

EA

SE

D C

AR

US

ED

CA

RU

SE

D C

AR

U

ND

ER

WA

RR

AN

TY

BA

SE

MO

DE

L

NE

W C

AR

BA

SE

MO

DE

L

NE

W C

AR

NE

W C

AR

WIT

H

UP

GR

AD

ES

7

Getting to Your Steps you can take to identify and reach your dream goal now, five years from now, or 10 years from now!

1 DARE TO DREAM...

2 DECLARE YOUR DREAM Write it down (yes, on paper!). Put it in places that you’ll see often.

3 DRILL DOWN ON THE DOUGHWhat do you think it will cost you? Write this down too and put it somewhere noticeable.

4 SET A DEADLINEKnowing when you want to achieve your goal is important (this is called a time horizon). You’ll want to know how long you’ll have to wait!

6 DIVIDE AND CONQUERFigure out how much you need to set aside each week or month to reach your goal and know you can spend the rest on other things.

5 CONSIDER YOUR INCOMEFor many teens, more than 60% of their spending money comes from their parents.

7ACHIEVE

YOUR DREAM!

8

Check out Star Banks Adventure, a financial education game at www.scholastic.com/MCK.This magazine contains commentary from third-party sources unaffiliated with T. Rowe Price. Use of this content does not imply endorsement from T. Rowe Price. T. Rowe Price makes no guarantees that information supplied is accurate, complete, or timely. 2016-US-24620