Embed Size (px)

Citation preview

There are tentative signs of recovery in London’s super prime (£10 million-plus) residential property market after a series of tax changes have slowed activity.

Leading indicators of demand are rising as vendors are increasingly prepared to adjust asking prices to reflect an increased tax burden on purchasers.

While the result of the EU referendum has added a degree of longer-term political uncertainty, in the short-term it has served as a catalyst for overdue price reductions. Demand has been further boosted by a favourable currency movement, which has made London property more than 15% cheaper for buyers denominated in US dollars.

The number of new prospective buyers above £10 million in the 14 weeks following the EU referendum increased 18.8% year-on-year, while the number of viewings rose by half.

“Buyers initially took stock following the referendum but there has been a notable uptick in activity in recent weeks,” said Tim Wright. “More realistic asking prices and a favourable currency movement mean many buyers have benefited from a twin boost.”

However, in what can be slower-moving and more discretionary market than the rest of prime central London, sales volumes remain lower than 2015. The number of transactions above £10 million between January and September declined -17.8% to 83 from 101 in the same period in 2015. The total value of transactions fell -18% over the same period.

“There is still a portion of the market that remains circumspect about the short-term prospects for pricing, which has been amplified by the political uncertainty surrounding Brexit,”

said Richard Cutt. “However, the reality on the ground is that demand is strengthening and the risk is that you miss the moment when the market starts to bottom out.”

In a sign that demand for high-value London property remains resilient, the number of transactions above £30 million increased to 14 from 10 year-on-year between January and September 2016, while the total value of transactions in that price-bracket rose by 28%.

“What this underlines is how there has been no diminution of London’s standing as a place to live for many of the world’s wealthiest families since the referendum” said Tim.

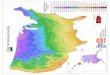

Kensington retained the largest share of super-prime market sales over the period, with 19% of transactions in 2016. Alongside Belgravia and Knightsbridge, it is an area where demand is strengthening as a result of price reductions that make it look better value, combined with growing demand for well-established prime central London neighbourhoods against a more uncertain backdrop.

“Buyers have a higher appetite for risk when the market is buoyant” said Daniel Daggers. “When activity is more constrained, the focus intensifies for best-in-class properties in the best locations.”

However, as a result of higher levels of stamp duty, there is also growing interest in large un-modernised houses to avoid higher upfront tax costs. “People are prepared to do more work than they were in the past,” said Richard. “The saving on stamp duty can represent a large chunk of any build costs.”

Leading indicators of activity point to an improvement in demand in the super prime market, as Tim Wright, Richard Cutt and Daniel Daggers tell Tom Bill

London Super Prime Team The London Super Prime Team draws upon Knight Frank’s network of London, national and global offices to provide ultra-high-net-worth buyers with a bespoke and confidential service. Their focus on building excellent long-term relationships provides buyers with continued and direct access to Knight Frank’s full range of services.

Top: Left to right

Tim Wright: [email protected] +44 7786 312408

Richard Cutt: [email protected] +44 7765 220529

Daniel Daggers: [email protected] +44 7879 848374

Penthouse, 21 Chesham Place, SW1X

3 Fitzroy Square, W1T

SUPER PRIME LONDON INSIGHT AUTUMN 2016

Maximum price by output areaJan-Sep 2016

St John's Wood

Marylebone

Mayfair

Chelsea

Belgravia

Knightsbridge

Kensington

Notting Hill

St John's Wood

Marylebone

Mayfair

Chelsea

Belgravia

Knightsbridge

Kensington

Notting Hill

Source: Knight Frank Research, Land Registry, LonRes

£5,000,000 - £7,500,000

Sub £5,000,000

£7,500,000 - £10,000,000

£10,000,000 - £20,000,000

£20,000,000 +

Hampstead Heath

Regent's Park

Hyde ParkHolland Park

SUPER PRIME LONDON INSIGHT AUTUMN 2016

RESIDENTIAL RESEARCH

FIGURE 1 Super prime map of London

FIGURE 2 Super prime price growth slows £10 million-plus price growth

FIGURE 4 The super prime London market in numbers

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

Sep-

14N

ov-1

4Ja

n-15

Mar

-15

May

-15

Jul-1

5Se

p-15

Nov

-15

Jan-

16M

ar-1

6M

ay-1

6Ju

l-16

Sep-

16

-1%

-2.8%

Annual Quarterly

0%

5%

10%

15%

20%

25%

30%

Belg

ravi

a

Che

lsea

Ham

pste

ad

Kens

ingt

on

Knig

htsb

ridge

Mar

yleb

one

May

fair

Not

ting

hill

St J

ohn’

s W

ood

FIGURE 3 Super prime market share by area

2014 2015 2016 (Jan-Sept)

Source: Knight Frank Research

Source: Knight Frank ResearchSource: Knight Frank Research

Change in total value of super prime transactions by postcode area Biggest increases and decreases, January-September 2016 versus January-September 2015

SW7 +257% SW1W +57% W11 +52%

W2 -77% W14 -85% NW3 -87%

28%Year-on-year increase in the value of £30 million-plus sales between January and September 2016

19%Percentage of £10 million-plus sales in Kensington between January and September 2016

18.8%Year-on-year increase in the number of new prospective buyers registering in the 14 weeks following the EU referendum

49.7%Year-on-year increase in the number of viewings in the 14 weeks following the EU referendum

RESIDENTIAL RESEARCH Tom Bill Head of London Residential Research +44 20 7861 1492 [email protected]

PRESS OFFICE Harry Turner +44 20 3861 6974 [email protected]

Jamie Obertelli+44 20 7861 [email protected]

Important Notice © Knight Frank LLP 2016 - This report is published for general information only and not to be relied upon in any way. Although high standards have been used in the preparation of the information, analysis, views and projections presented in this report, no responsibility or liability whatsoever can be accepted by Knight Frank LLP for any loss or damage resultant from any use of, reliance on or reference to the contents of this document. As a general report, this material does not necessarily represent the view of Knight Frank LLP in relation to particular properties or projects. Reproduction of this report in whole or in part is not allowed without prior written approval of Knight Frank LLP to the form and content within which it appears. Knight Frank LLP is a limited liability partnership registered in England with registered number OC305934. Our registered office is 55 Baker Street, London, W1U 8AN, where you may look at a list of members’ names.