Embed Size (px)

Citation preview

Sun Corridor Projections 1

Sun Corridor Projections

Base and Alternative Scenarios

Prepared for

Central Arizona Association of GovernmentsJanuary 8, 2009

Sun Corridor Projections 2

Study Outline• Joint effort

– ASU’s WP Carey School of Business– UA’s Eller College of Management

• Review economic & demographic research• Development of Sun Corridor (3-county) model• Base forecast highlights

– Population and demographic outlook– Employment outlook– Earnings, income and sales outlook

• High & low scenario results

Sun Corridor Projections 3

Economic & Demographic Research

Sun Corridor Projections 4

Introduction

• The Economic and Demographic Research portion examines/identifies long-term economic and demographic forces that could affect economic development in 3-county “megapolitan” area (Pinal, Maricopa and Pima counties combined)

Sun Corridor Projections 5

Economic & Demographic Topics

• Population, demographics and net migration analysis

• Industry mix and basic industries in the region

• Target industry recommendations• Interviews with “experts”• Case study: Riverside vs. Pinal County

Sun Corridor Projections 6

Population, Demographics and

Net Migration Analysis• Historical population growth

– Natural increase– Domestic migration– Immigration

• Comparison of long-term forecasts• Expert interview summary

Sun Corridor Projections 7

Population, Demographics and

Net Migration Analysis• Use Census Bureau estimates of population

– By age, sex, ethnicity

• Domestic migration to AZ is much larger than immigration– Undocumented immigration surged in mid-90s,

peaked in 2000, and has declined since

• Largest migration flows from Los Angeles– And other So. California metros (55% of total)– Chicago (during the 1980s, 6% in 2006)

Sun Corridor Projections 8

Industry Mix and Basic Industries, 2004

• Manufacturing is a key driver of the megapolitan economy (33,000 excess jobs)– Electronic components (11,000)– Instruments (4,300)– Aerospace (17,700)– 2 Wholesale trade industries tied to high tech mfg. (6,000)

• Tourism (30,000 excess jobs) – low wage • Administrative support and finance (16,000 excess

jobs)• Copper mining and smelting (2,000 excess jobs)

Sun Corridor Projections 9

TARGET INDUSTRY SECTORS• Aerospace/Avionics/Defense/Homeland Security• Healthcare and Health Industries• Bioscience/Bioindustries/Biotechnology/Biomedical• Transportation and Logistics• Agriculture/Food Processing/Agricultural Technology • Sustainability/Environmental Technology/Renewable Energy

– Solar Energy – Environmental Technologies – Water Management – Waste Treatment – Other Renewable Energy (Wind, Biofuels)

• General Manufacturing – Industrial Machinery

• Business and Professional Services

– Communication Services – Engineering Services Research and Testing – Financial Services – Information Tech./Computer Software & Systems

• High Tech Industry

– High-tech Instruments – Medical Devices – Electronics/Semiconductor– Nanotechnologies – Analytical Instruments

Sun Corridor Projections 10

Economic Interview Summary• Global competitiveness Issues

– Workforce and education– Infrastructure– Labor costs– Geographic location

• Constraints to economic development– K-12 education quality– Transportation system– Water and waste water systems– Availability of high skilled workforce– Access to local employment opportunities– Funding is the key to avoiding constraints

• Water issues– With proper management there will be enough water in Arizona in the long-run– AZ will have to develop incremental water supplies to extend life of resources– There could be temporary localized water shortages– Water will become more expensive

Sun Corridor Projections 11

Case Study: Riverside vs. Pinal County• Population Growth

– Population growth in Riverside County has remained rapid over extended period of time, indicating Pinal County population growth could remain rapid for many years

• Employment Growth– The strong economies in Phoenix and Tucson are providing jobs for Pinal

County residents and are likely retarding the job creation in Pinal County– Pinal County’s ability to create high wage jobs is limited by its relatively

low skilled workforce, and lack of arterial transportation infrastructure within the County

• Payroll per employee (PPE)– If the example of Riverside County is any indication, the PPE in Pinal

County will stay below the U.S. average and below Maricopa and Pima Counties average PPE

• Employment to Population Ratio (E/P)– Pinal County needs to increase the number of jobs. Over time the E/P will

improve, but not to Pima or Maricopa County levels

Sun Corridor Projections 12

Sun Corridor Model

Sun Corridor Projections 13

The Sun Corridor Model

• The Sun Corridor model was developed using data for the 3-county megapolitan area that includes Pinal, Maricopa and Pima Counties

• The model consists of an econometric general equilibrium structural model with an embedded cohort survival model

Sun Corridor Projections 14

Personal Income

Population& Migration

Employment

Output/Demand

Wage Rates

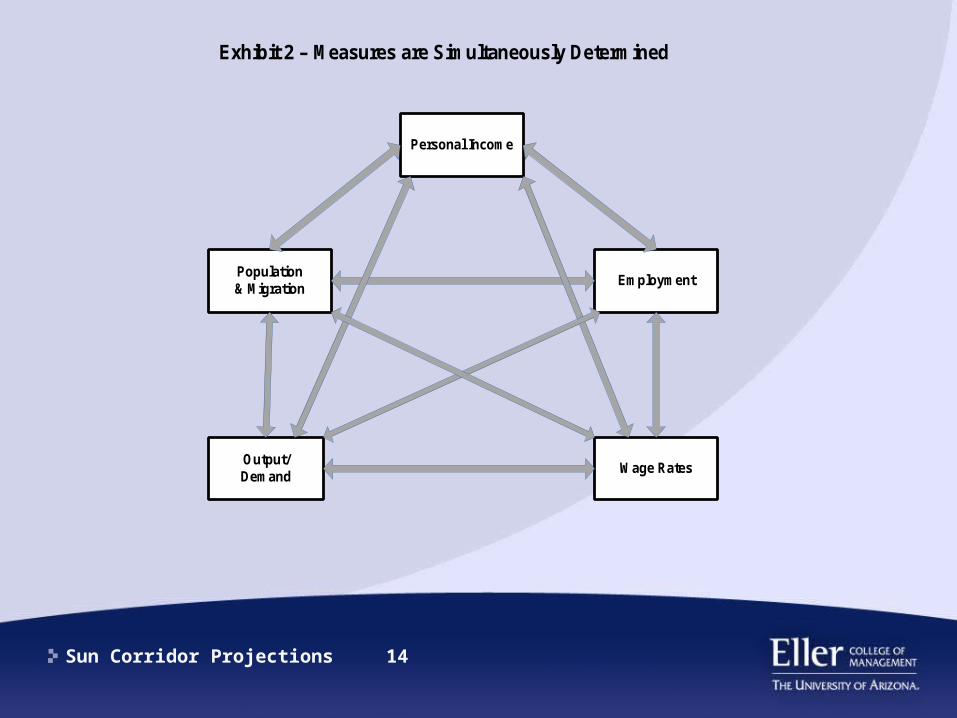

Exhibit 2 – Measures are Simultaneously Determined

Sun Corridor Projections 15

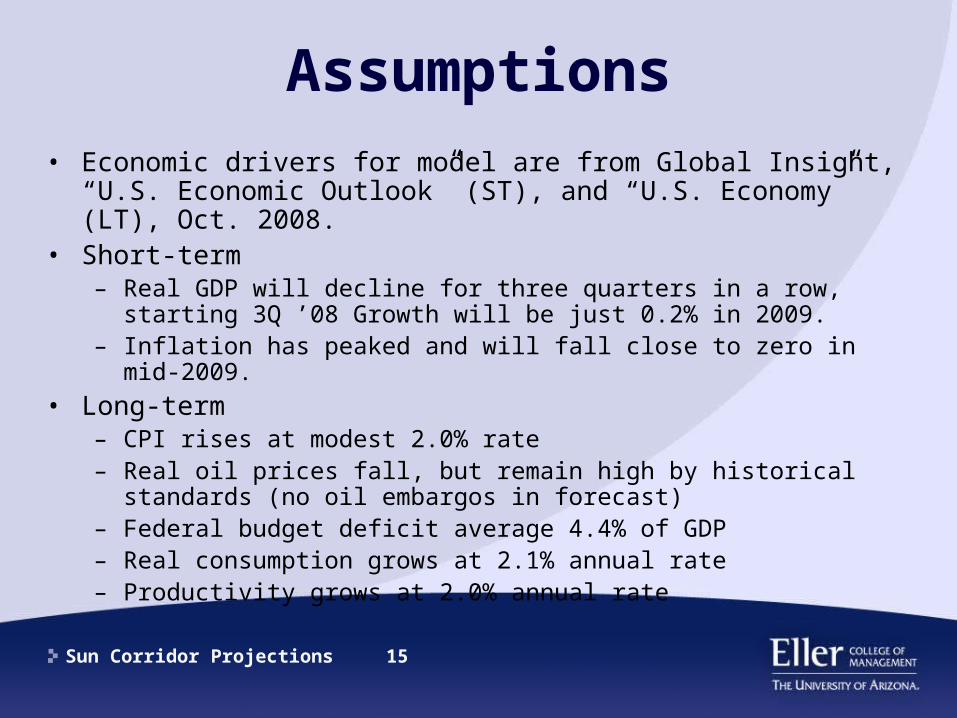

Assumptions• Economic drivers for model are from Global Insight, “U.S.

Economic Outlook” (ST), and “U.S. Economy” (LT), Oct. 2008.• Short-term

– Real GDP will decline for three quarters in a row, starting 3Q ’08 Growth will be just 0.2% in 2009.

– Inflation has peaked and will fall close to zero in mid-2009.• Long-term

– CPI rises at modest 2.0% rate– Real oil prices fall, but remain high by historical standards (no oil

embargos in forecast)– Federal budget deficit average 4.4% of GDP– Real consumption grows at 2.1% annual rate– Productivity grows at 2.0% annual rate

Sun Corridor Projections 16

Assumptions

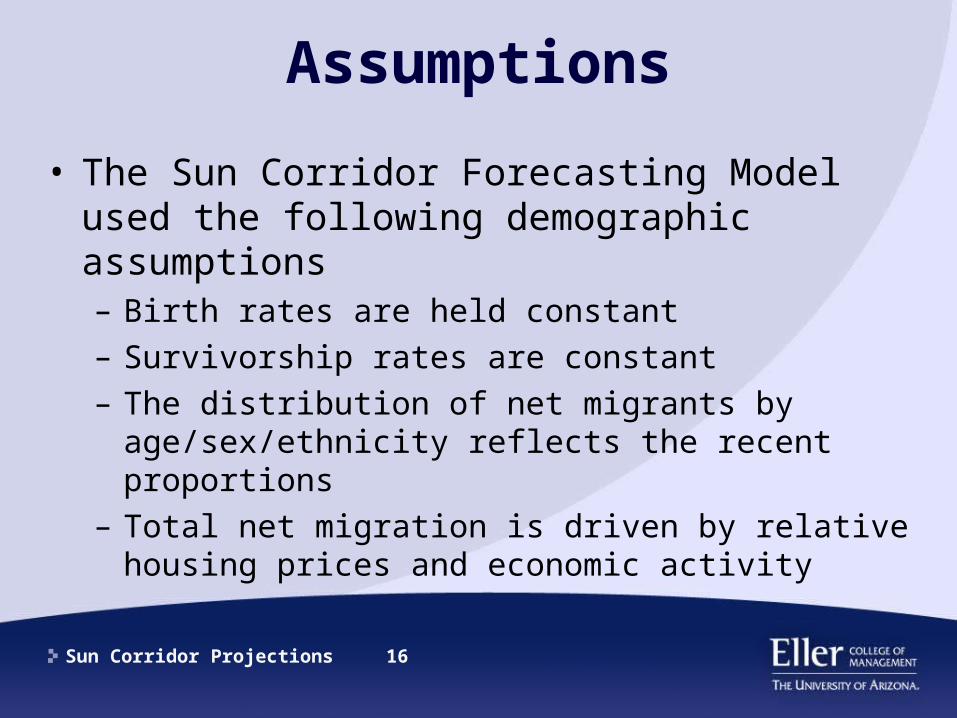

• The Sun Corridor Forecasting Model used the following demographic assumptions– Birth rates are held constant– Survivorship rates are constant– The distribution of net migrants by

age/sex/ethnicity reflects the recent proportions– Total net migration is driven by relative housing

prices and economic activity

Sun Corridor Projections 17

Assumptions

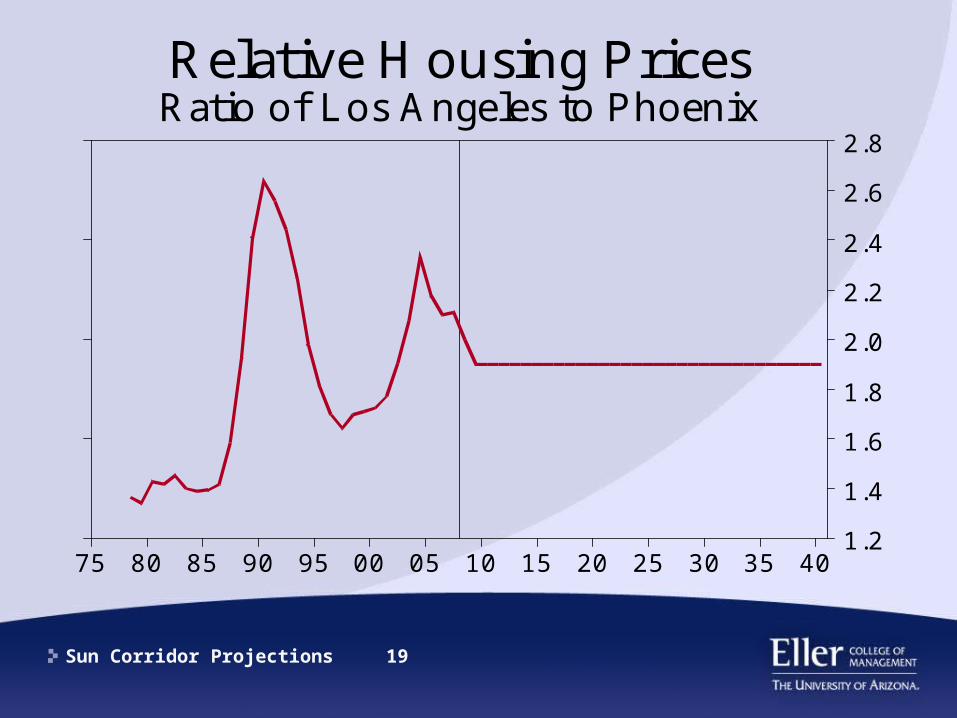

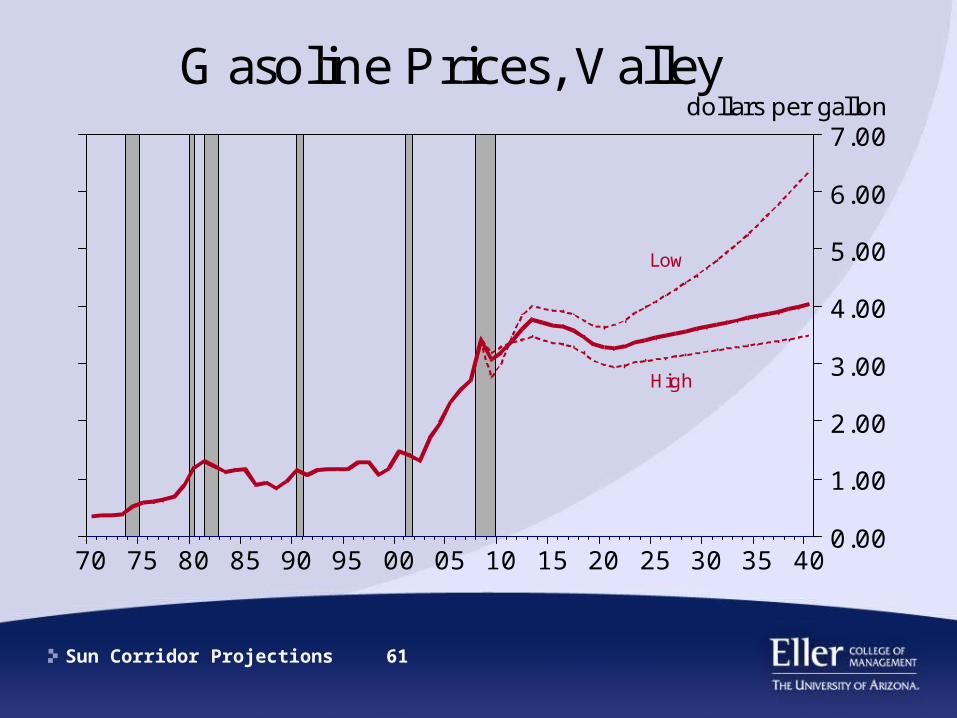

• Gasoline prices in the Phoenix area remain high and drift upward from current levels to near $4.00 per gallon in 2015

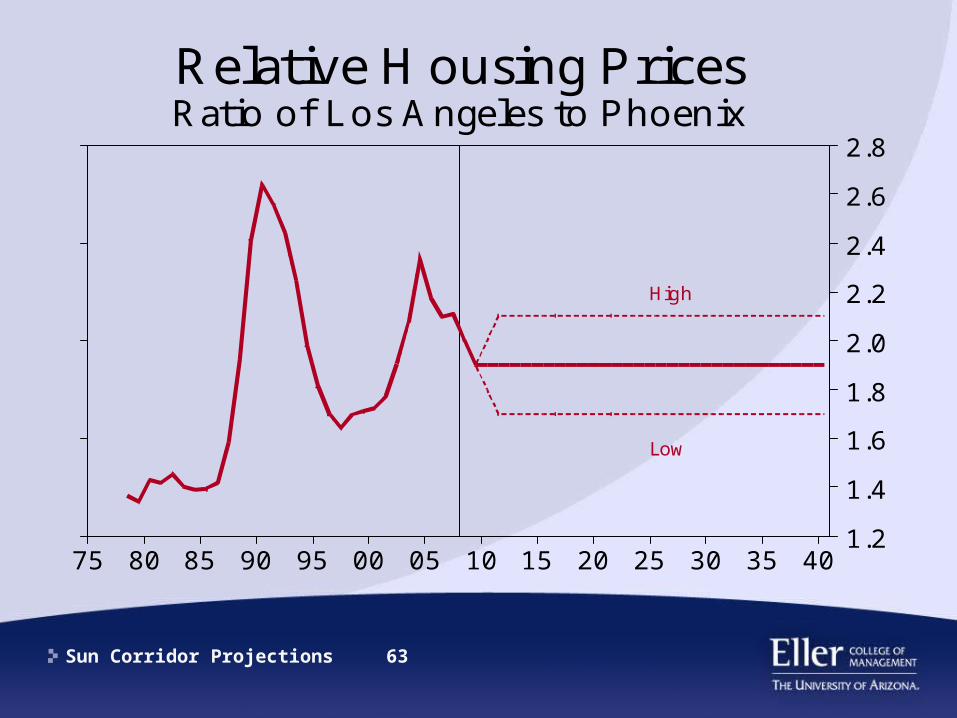

• Housing prices in the Sun Corridor have fallen significantly– Relative to prices in Los Angeles, the Sun

Corridor remains “cheap”– Prices in LA will remain nearly twice those in the

Sun Corridor

Sun Corridor Projections 18

403530252015100500959085807570

5.00

4.00

3.00

2.00

1.00

0.00

dollars per gallonGasoline Prices, Valley

inflationadjusted2007 dollars

Sun Corridor Projections 19

4035302520151005009590858075

2.8

2.6

2.4

2.2

2.0

1.8

1.6

1.4

1.2

Relative Housing PricesRatio of Los Angeles to Phoenix

Sun Corridor Projections 20

Determinants of Growth

• In the long term, supply factors matter– Labor force– Capital stock (infrastructure AND human)– Technological progress

• For the 3-county area, population growth is the most important– Migration flows– Natural increase

Sun Corridor Projections 21

Base Scenario Results

Sun Corridor Projections 22

Highlights: Year 2040

• 10.1 million people will live in the Sun Corridor

• The Sun Corridor will grow into one of the nation’s 10 “megapolitan” areas

• Growth rates for both population and jobs moderate to near 2% annually

Sun Corridor Projections 23

Forecasts to 2040, Sun Corridor2000 2010 2020 2030 2040

Population (000s) 4,122 5,323 6,740 8,370 10,100

Nonfarm Jobs (000s) 1,925 2,180 3,020 3,830 4,760

Personal Income ($bil)

113 188 380 670 1,150

Retail Sales ($ bil) 46 67 129 215 353

Sun Corridor Projections 24

403530252015100500959085807570

12

10

8

6

4

2

0

-2

-4

% chg

Annual Growth Rates, Valley

nonfarm jobspopulation

Sun Corridor Projections 25

403530252015100500959085807570

13000

10000

7500

5000

2500

1250

000s

Population, Valley

2040 population: 10.1 mil

Sun Corridor Projections 26

Population Dynamics

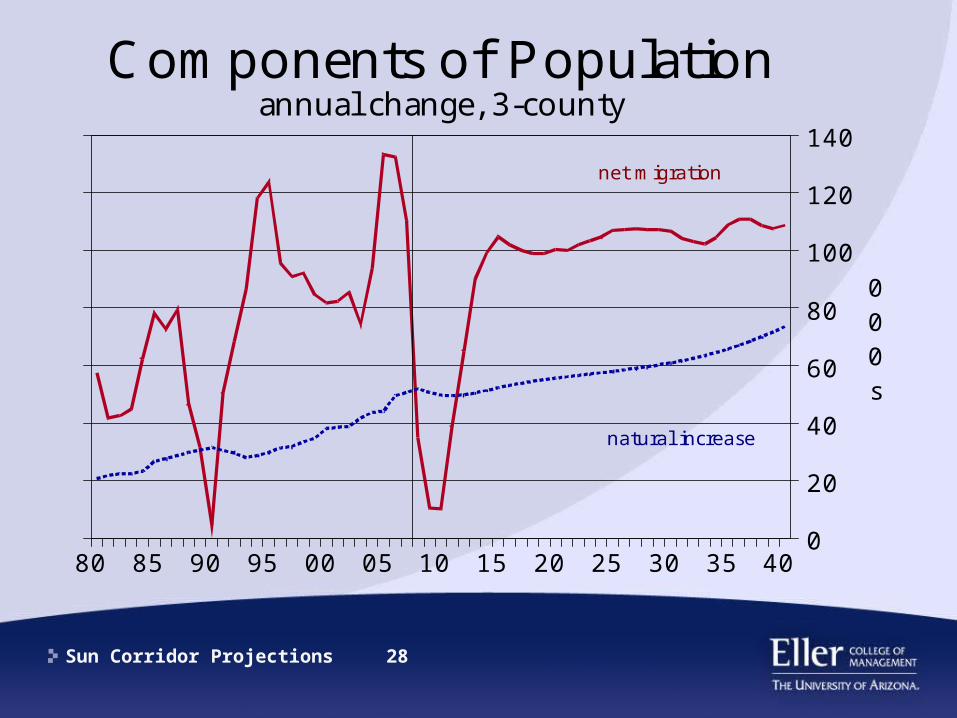

• Natural increase (births – deaths)– Birth rates remain relatively constant– Death rates trend upward as population ages– Calculated relative to total population

• Migration (net)– On average, provides twice the number of

natural increase– As a percent of population, continues on

downward trend

Sun Corridor Projections 27

40353025201510050095908580

20

15

10

5

0

Birth and Death Ratesper 1000 Persons, 3-county

Births

Deaths

Sun Corridor Projections 28

40353025201510050095908580

140

120

100

80

60

40

20

0

000s

Components of Populationannual change, 3-county

net migration

natural increase

Sun Corridor Projections 29

40353025201510050095908580757065

140

120

100

80

60

40

20

0

-20

5

4

3

2

1

0

-1

000s

%

Annual Net Migration3-county

as a % of population(right)

number (left)

Sun Corridor Projections 30

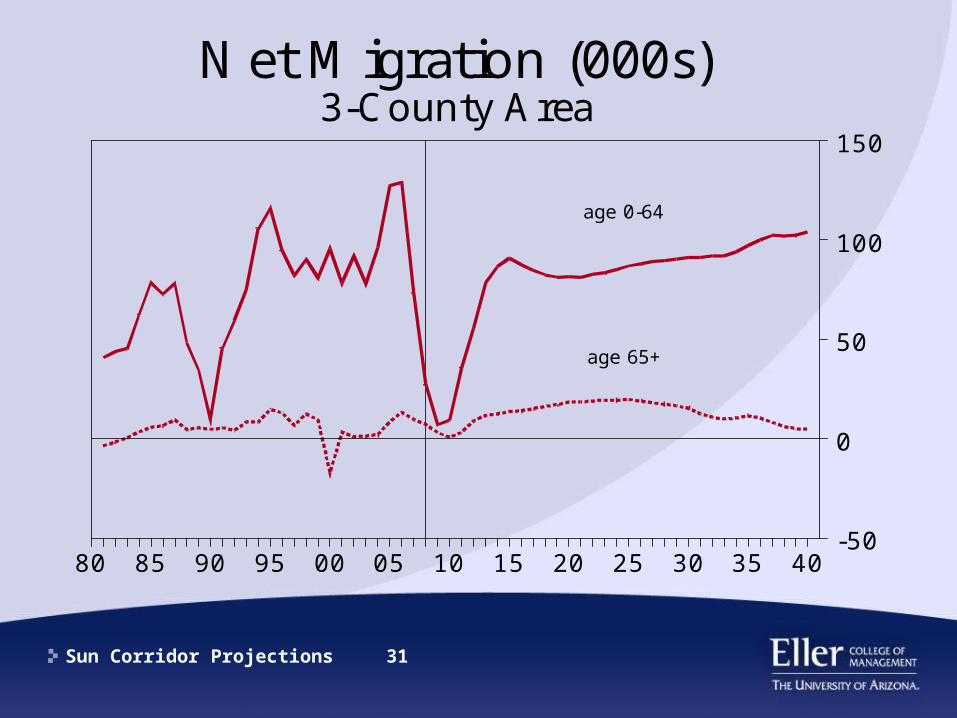

Population Dynamics

• Retirement-related migration will double as boomers retire– but the numbers are small compared 0-64 age

group

• Work-related migration returns to “average” (90-100 thousand per year) by 2015

Sun Corridor Projections 31

40353025201510050095908580

150

100

50

0

-50

Net Migration (000s)3-County Area

age 0-64

age 65+

Sun Corridor Projections 32

Population Dynamics

• Once the economy recovers from current downturn, annual population growth returns to roughly 160,000 per year in 2015– Then drifts slowly upward

Sun Corridor Projections 33

40353025201510050095908580757065

200

150

100

50

0

000s

Annual Changes in Population3-county

Sun Corridor Projections 34

Highlights: Year 2040

• The proportion of the population age 65+ – will increase significantly, but remain less than

nationwide – AZ will remain one of the youngest states

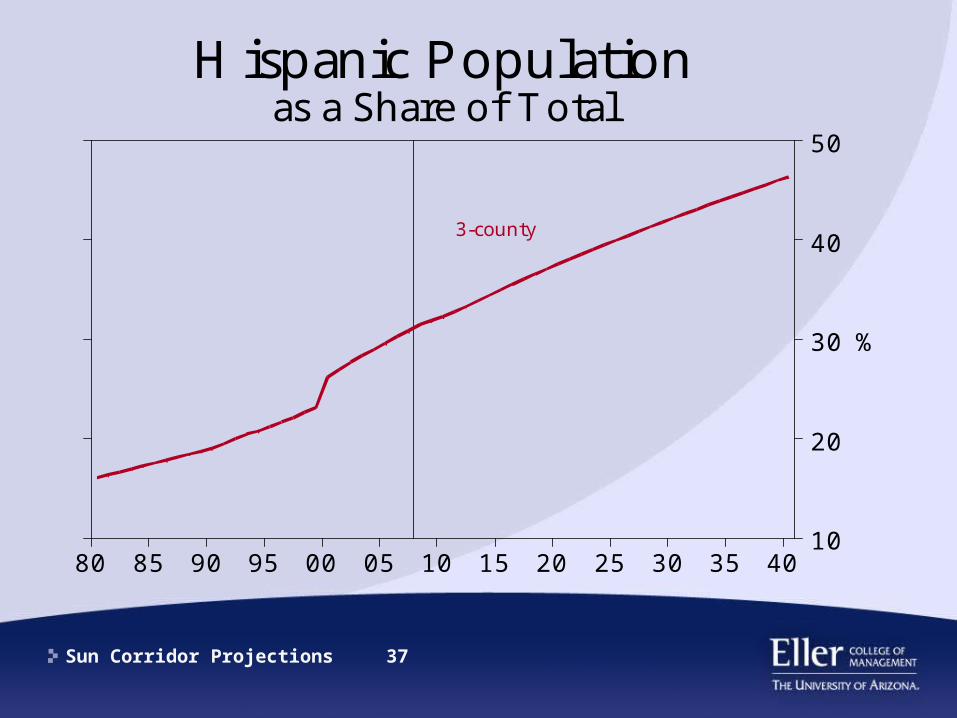

• School age population remains flat at 21%• Hispanics share of the total population rises

from 33% to 48%– Hispanic share of school age population

increases from 42% to 58%

Sun Corridor Projections 35

4035302520151005009590858075706560

22

20

18

16

14

12

10

8

%

Shares of Total PopulationAge 65 and over

3-county

US

Sun Corridor Projections 36

40353025201510050095908580

25

24

23

22

21

20

%

School-Age Population (5-19)as a Share of Total

3-county

Sun Corridor Projections 37

40353025201510050095908580

50

40

30

20

10

%

Hispanic Populationas a Share of Total

3-county

Sun Corridor Projections 38

40353025201510050095908580

60

50

40

30

20

%

Hispanic Share of School-AgePopulation (5-19)

3-county

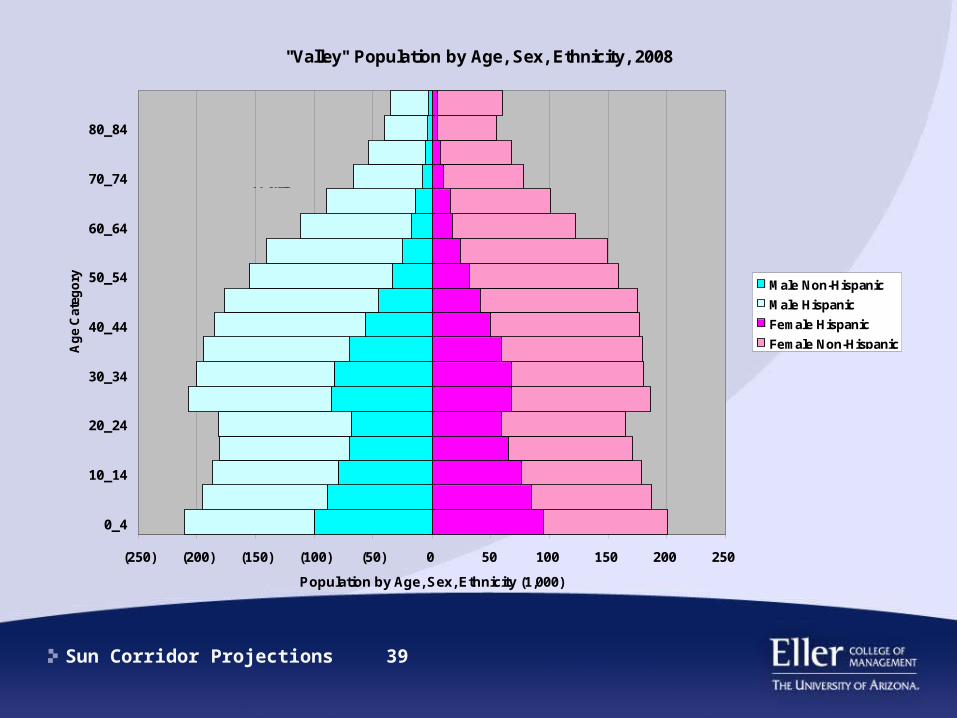

Sun Corridor Projections 39

"Valley" Population by Age, Sex, Ethnicity, 2008

(250) (200) (150) (100) (50) 0 50 100 150 200 250

0_4

10_14

20_24

30_34

40_44

50_54

60_64

70_74

80_84

Ag

e C

ateg

ory

Population by Age, Sex, Ethnicity (1,000)

Male Non-Hispanic

Male Hispanic

Female Hispanic

Female Non-Hispanic

Male Female

Sun Corridor Projections 40

"Valley" Population by Age, Sex, Ethnicity, 2040

(500) (400) (300) (200) (100) 0 100 200 300 400 500

0_4

10_14

20_24

30_34

40_44

50_54

60_64

70_74

80_84

Ag

e C

ate

go

ry

Population by Age, Sex, Ethnicity (1,000)

Male Hispanic

Male Non-Hispanic

Female Hispanic

Female Non-Hispanic

Male Female

Sun Corridor Projections 41

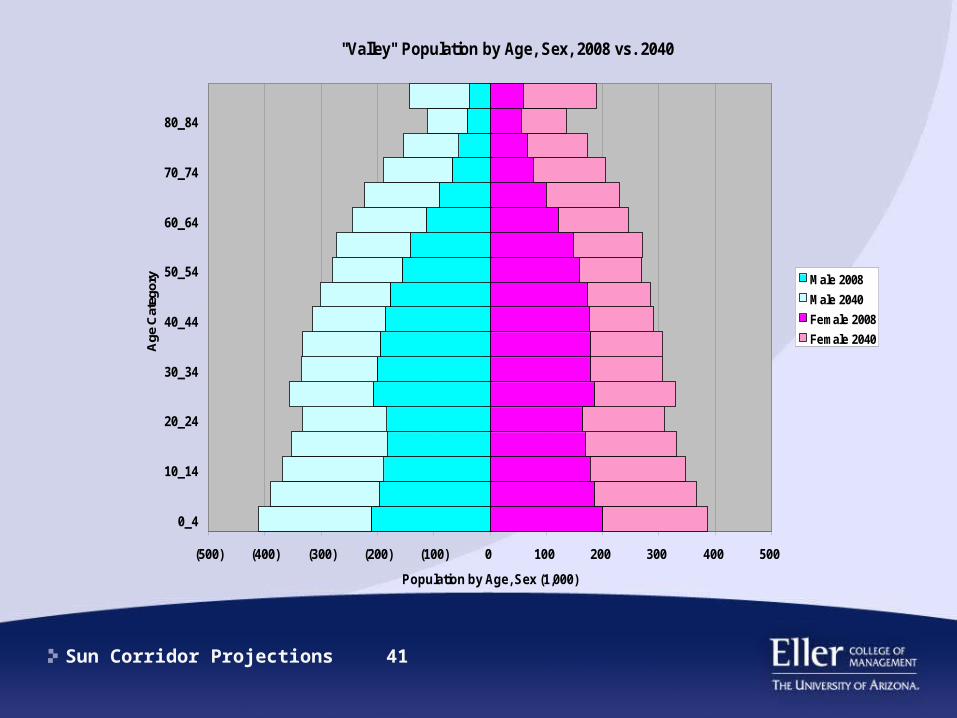

"Valley" Population by Age, Sex, 2008 vs. 2040

(500) (400) (300) (200) (100) 0 100 200 300 400 500

0_4

10_14

20_24

30_34

40_44

50_54

60_64

70_74

80_84

Age

Cat

egor

y

Population by Age, Sex (1,000)

Male 2008

Male 2040

Female 2008

Female 2040

Male Female

Sun Corridor Projections 42

Highlights: Year 2040

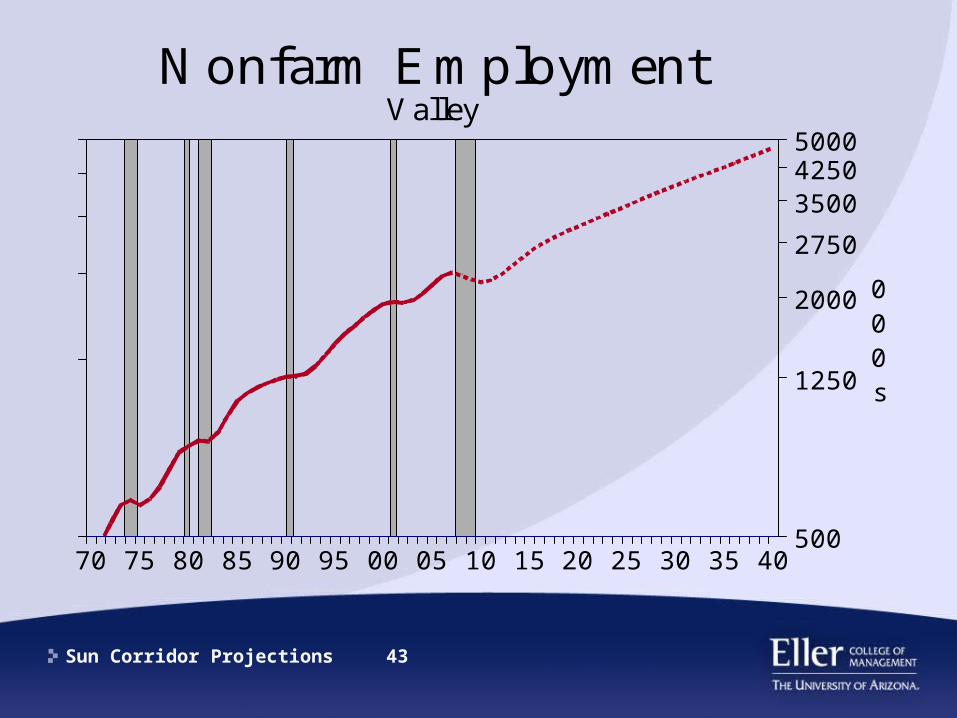

• 2.25 mil new nonfarm jobs will be created during the next 32 years– 4.75 mil total– Most will be in services sectors

Sun Corridor Projections 43

403530252015100500959085807570

5000425035002750

2000

1250

500

000s

Nonfarm EmploymentValley

Sun Corridor Projections 44

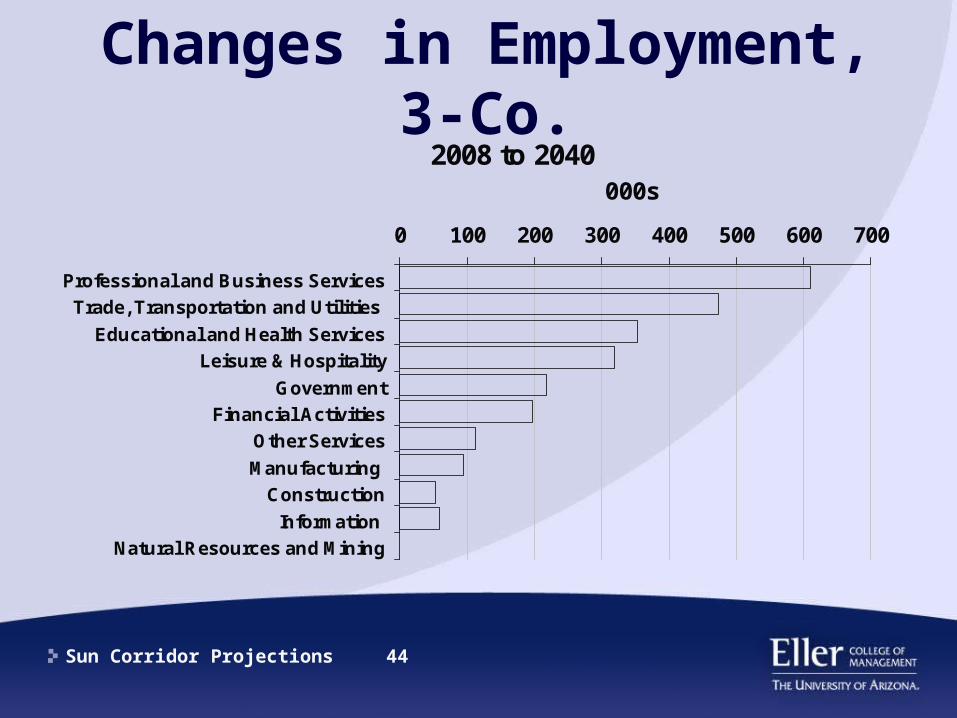

Changes in Employment, 3-Co.

2008 to 2040

0 100 200 300 400 500 600 700

Professional and Business Services

Trade, Transportation and Utilities

Educational and Health Services

Leisure &Hospitality

Government

Financial Activities

Other Services

Manufacturing

Construction

Information

Natural Resources and Mining

000s

Sun Corridor Projections 45

Employment Sector Growth

Growth Leaders• Professional & Business

Services• Leisure & Hospitality• Financial Activities• Information• Other services • Health Care & Social

Assistance

Growth Laggards• Government• Construction• Manufacturing• Mining

Sun Corridor Projections 46

40353025201510050095908580757065

22

20

18

16

14

12

10

%

Government Employmentas a Percent of Total Nonfarm

3-county

Sun Corridor Projections 47

40353025201510050095908580757065

20

18

16

14

12

10

8

6

4

%

Manufacturing Jobsas a Percent of Total Nonfarm

3-county

Sun Corridor Projections 48

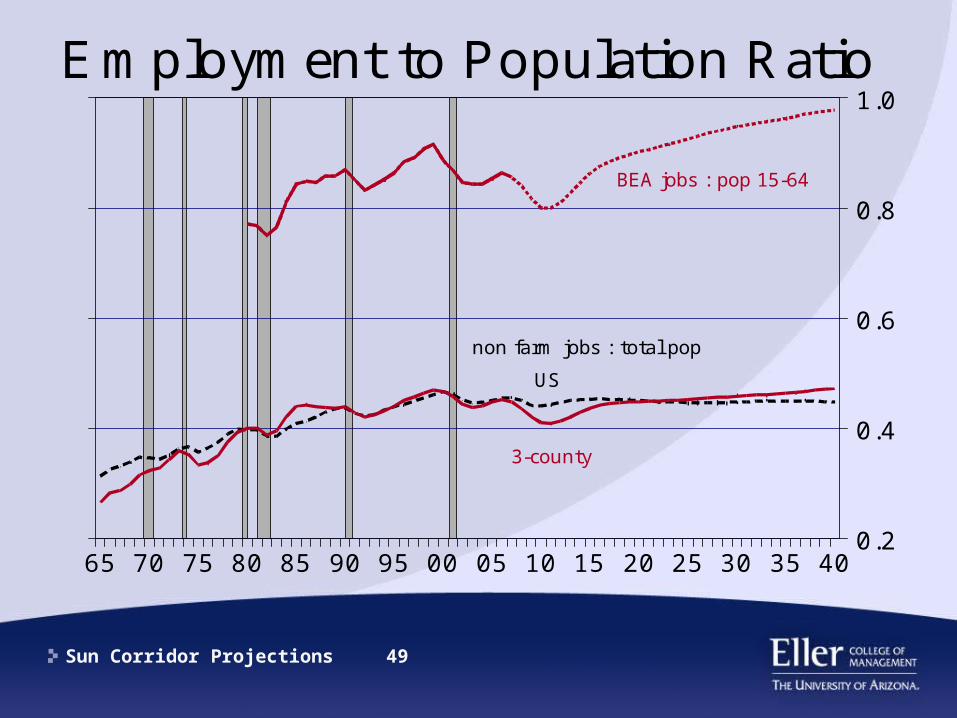

Highlights: Year 2040

• Employment to population ratio recovers after the recession and drifts slowly upward– Nationwide, the ratio remains flat at 0.46

• An alternative measure using BEA employment relative to working-age population (15-64) is significantly higher and moves upward more quickly over the forecast period

Sun Corridor Projections 49

40353025201510050095908580757065

1.0

0.8

0.6

0.4

0.2

Employment to Population Ratio

US

3-county

BEA jobs : pop 15-64

non farm jobs : total pop

Sun Corridor Projections 50

Highlights: Year 2040

• PCPI relative to US stabilizes at 88% after ratcheting down during the current recession

Sun Corridor Projections 51

403530252015100500959085807570

105

100

95

90

85

80

%

Per Capita Personal Incomeas a percent of US

3-county

Sun Corridor Projections 52

Long Term Outlook - BASE

• 10.1 million people in the Valley by 2040– Population growth rate moderates from 3.7%

annually in decade of 1990s to 1.9% in 2030s

• Hispanic population’s share grows from 31.5% today to 46.4% in 2040

• Net migration flows stabilize at 100,000 per year rather than trending ever upward– An increasing share is age 65 and over

• Proportion of 65+ rises from 12% to 18%

Sun Corridor Projections 53

Long Term Outlook

• 2.3 mil new jobs will be created by 2040– Service-related industries play larger role

• Employment:population steadies at 46%• Per capita personal income relative to US

stabilizes near 88%• A larger portion of our income will come

from transfer payments– Less from “property” income

Sun Corridor Projections 54

Alternative Scenarios

Sun Corridor Projections 55

Scenario Forecast Development

• Forecast scenarios were developed on the basis of the work done on the Demographic & Economic White Papers, and expert interviews

• National economic forecasts from Global Insight (GI) were used to incorporate alternative economic assumptions of business conditions

• Future investments in education, workforce development and infrastructure are necessary for Arizona to attract high tech industry, raise income levels, and improve the overall quality of life

• The level of investment in education and infrastructure, along with national economic conditions were key factors in developing the three forecast scenarios

Sun Corridor Projections 56

Base Scenario• Assumes that the national economy will grow according to

the GI base (trend) economic forecast • Investment in education and infrastructure remains on a

business-as-usual basis

Sun Corridor Projections 57

High Scenario Assumptions• The GI high economic scenario boosts regional economic

growth• Relatively higher housing prices in other regions sustains a

high rate of in-migration • The state makes a commitment to increase expenditures for

education and infrastructure on a sustained basis• That investment results, with a lag, in better education,

improved workforce skills, increased attraction of higher waged industries, higher average wage levels and a better quality of life

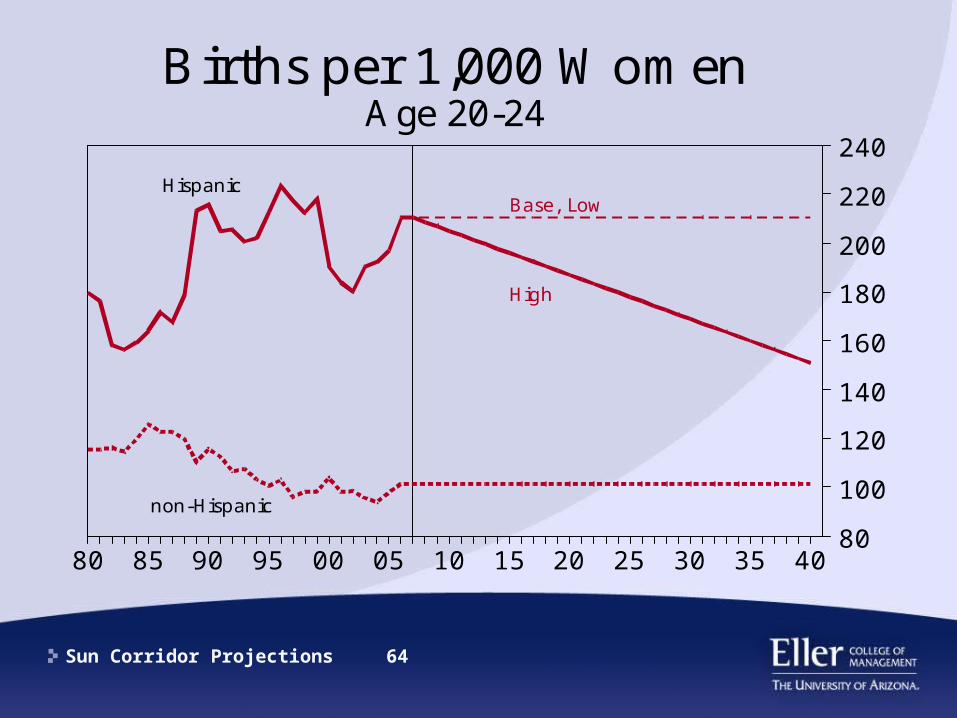

• Increased economic opportunities result in lower birth rates for working aged Hispanic females, but their birth rates remain above those for non-Hispanic females

Sun Corridor Projections 58

High Scenario (Cont.)• Increased spending for education and infrastructure raise

wages for educators, improves the quality of the workforce and results in greater success attracting, retaining and expanding higher wage industries, including high tech industries

• Construction employment benefits from increased expenditures for infrastructure development

• Employment increases in utilities as solar power generation capacity is added

• Employment also rises in other manufacturing industries due to increased activity in high tech industries such as biotechnology, pharmaceuticals, etc

• Healthcare industry employment expands due to increased research and development activity and higher incomes

• Transportation and warehousing employment expand to take advantage of better rail, highway and airport infrastructure

Sun Corridor Projections 59

Low Scenario Assumptions• The national economy grows at the GI low scenario • Homes in other parts of the country become relatively less

expensive than those in the megapolitan region, resulting in slower in-migration rates

• Expenditures for education and infrastructure are inadequate to support population growth, resulting in deteriorating workforce quality, slower income growth, and a lower overall quality of life in the region

• The poor quality workforce and weaker infrastructure cause employment to suffer in manufacturing, information technology industries, and those with higher wages and higher workforce skill requirements

• Transportation and warehousing employment drops due to poorer transportation infrastructure

• Finally, the diminished quality of life in the region discourages employment in the leisure and hospitality industry as tourism activity declines

Sun Corridor Projections 60

40353025201510050095908580

240

215

190

165

140

115

90

mil

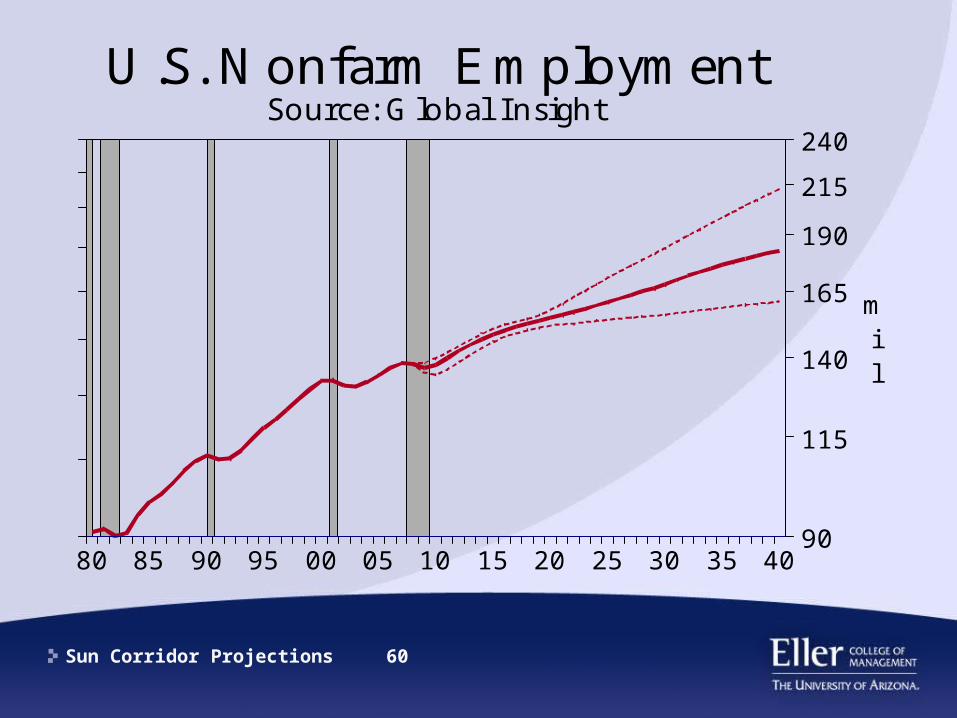

U.S. Nonfarm EmploymentSource: Global Insight

Sun Corridor Projections 61

403530252015100500959085807570

7.00

6.00

5.00

4.00

3.00

2.00

1.00

0.00

dollars per gallonGasoline Prices, Valley

Low

High

Sun Corridor Projections 62

40353025201510050095908580

6.0

5.0

4.0

3.0

2.0

1.0

0.0

1982-84=1.00

U.S. Consumer Price IndexSource: Global Insight

High

Low

Sun Corridor Projections 63

4035302520151005009590858075

2.8

2.6

2.4

2.2

2.0

1.8

1.6

1.4

1.2

Relative Housing PricesRatio of Los Angeles to Phoenix

High

Low

Sun Corridor Projections 64

40353025201510050095908580

240

220

200

180

160

140

120

100

80

Births per 1,000 WomenAge 20-24

Hispanic

non-Hispanic

Base, Low

High

Sun Corridor Projections 65

403530252015100500959085807570

13000

10000

7500

5000

2500

1250

000s

Population, Valley

2040 population:11.5 mil

10.1 8.9

highlowbaseactual

Sun Corridor Projections 66

40353025201510050095908580757065

250

200

150

100

50

0

000s

Annual Changes in Population3-county

High

Low

Sun Corridor Projections 67

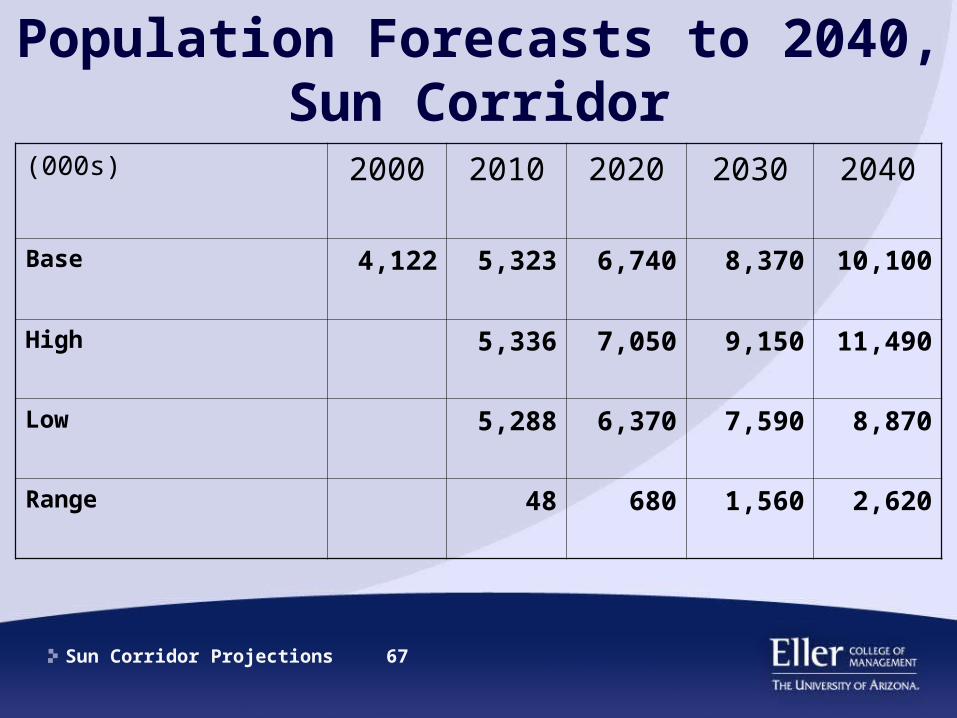

Population Forecasts to 2040, Sun Corridor

(000s) 2000 2010 2020 2030 2040

Base 4,122 5,323 6,740 8,370 10,100

High 5,336 7,050 9,150 11,490

Low 5,288 6,370 7,590 8,870

Range 48 680 1,560 2,620

Sun Corridor Projections 68

Report Available At:

http://appliedeconomics.net/caag/ThreeCountyProjections.html