Embed Size (px)

Citation preview

www.moodys.com

Banking Moody’s Global

Credit Analysis

Table of Contents: Summary Rating Rationale 1

Group Structure 3 Crédit Mutuel Group 4 Business Activities 6 Distribution Capacity and Market Shares 13 Company History 15 Ownership and Structure 17

Key Issues 18 Analysis of Rating Considerations 19

Discussion of Qualitative Rating Drivers 19 Discussion of Quantitative Rating Drivers 22 Discussion of Support Considerations 26

Company Annual Statistics 29 Moody’s Related Research 33

Analyst Contacts:

Paris 33.1.70.70.22.29

Stéphane Le Priol Vice President - Senior Credit Officer

Virginie Merlin Vice President - Senior Analyst

Stéphane Herndl Associate Analyst

Frankfurt 49.69.70730.700

Carola Schuler Team Managing Director

August 2009

Banque Fédérative du Crédit Mutuel Strasbourg, France

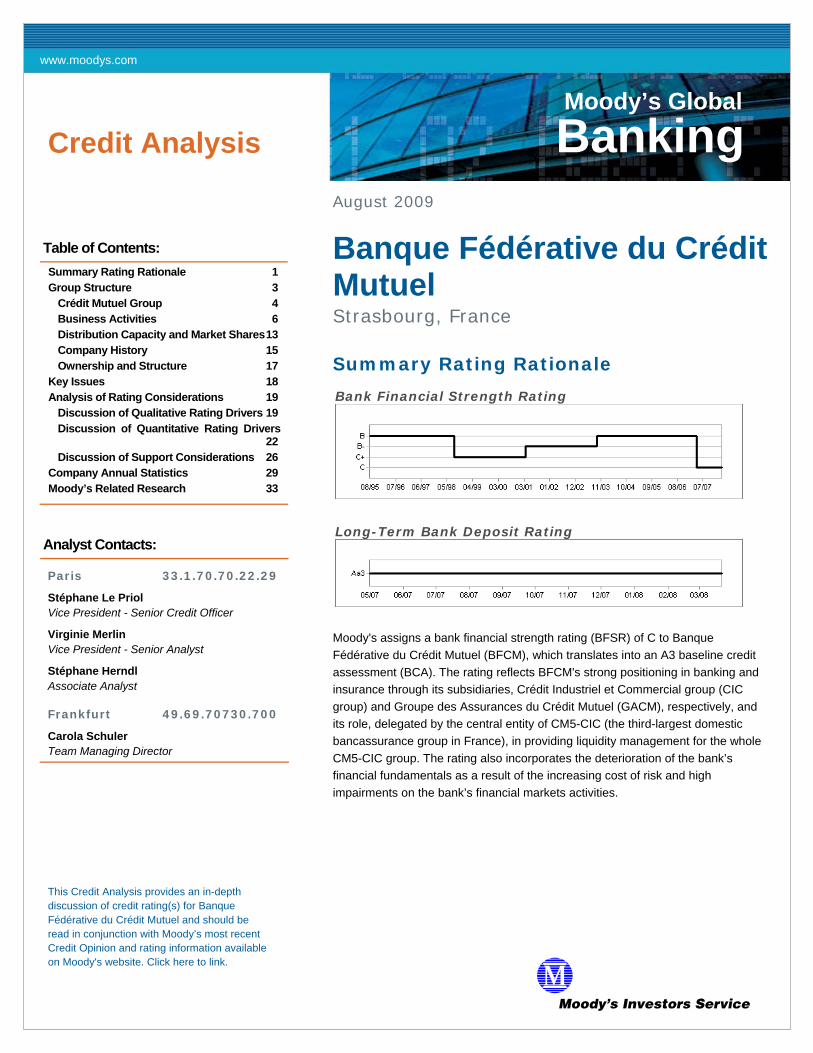

Summary Rating Rationale

Bank Financial Strength Rating

Long-Term Bank Deposit Rating

Moody's assigns a bank financial strength rating (BFSR) of C to Banque Fédérative du Crédit Mutuel (BFCM), which translates into an A3 baseline credit assessment (BCA). The rating reflects BFCM's strong positioning in banking and insurance through its subsidiaries, Crédit Industriel et Commercial group (CIC group) and Groupe des Assurances du Crédit Mutuel (GACM), respectively, and its role, delegated by the central entity of CM5-CIC (the third-largest domestic bancassurance group in France), in providing liquidity management for the whole CM5-CIC group. The rating also incorporates the deterioration of the bank’s financial fundamentals as a result of the increasing cost of risk and high impairments on the bank’s financial markets activities.

This Credit Analysis provides an in-depth discussion of credit rating(s) for Banque Fédérative du Crédit Mutuel and should be read in conjunction with Moody’s most recent Credit Opinion and rating information available on Moody's website. Click here to link.

2 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

BFCM's long-term global local currency (GLC) deposit rating is Aa3 – under Moody's joint default analysis (JDA) methodology – based on its BCA of A3 and on a very high probability of support in the event of need from CM5-CIC group. Although BFCM is not part of the group's cross-guarantee and solidarity mechanisms, the role which is to specifically cover the mutualist part of the group, it is fully integrated within CM5-CIC both strategically and operationally and it is core to the group. BFCM's GLC deposit rating also incorporates a very high probability of systemic support in the event of a crisis, through CM5-CIC.

The outlook on the BFSR is negative and reflects Moody's view that BFCM’s financial markets activities and assets lead to high volatility in its P&L. It also reflects the likely further deterioration of the French retail activities given the challenging macro environment, as well as the addition of potentially more volatile consumer finance activities into BFCM's business mix, following the acquisitions of Citibank Deutschland and Cofidis (both unrated). BFCM's Aa3 long-term debt and deposit ratings carry a stable outlook.

Moody's cautions that, given the group's structure and BFCM's specific role within the group, BFCM's BFSR – which expresses its financial strength as if it were a standalone entity – conveys only part of the information. We do not rate the CM5-CIC group or its central institution, CFCMCEE.

The BFSR is unlikely to be upgraded in the foreseeable future as it currently carries a negative outlook. Likewise, the deposit and debt ratings are unlikely to be upgraded in the foreseeable future given the negative outlook on the bank’s BFSR and the likelihood that Moody’s assessment of the probability of group and systemic support will remain unchanged.

Conversely, any further deterioration of the bank’s financial fundamentals beyond Moody’s expectations, resulting notably from an increase in the cost of risk or higher-than-expected volatility in the bank’s earnings, could exert negative pressure on the BFSR. Other factors that could exert downward pressure on the BFSR include any lapse in controls and risk management or our assessment of a higher risk appetite; for instance, if the group were to stop short of de-risking its remaining financial markets activities.

The deposit and debt ratings could be downgraded in the event of a severe deterioration of the bank’s intrinsic creditworthiness. They could also be downgraded if we were to perceive a decrease in the probability of support from CM5-CIC, which we do not expect given the strategic roles of BFCM as a liquidity provider for the whole of CM5-CIC group and as a holding company for CIC group and GACM.

3 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

Group Structure

Local cooperative banks(Paris area)

CM IdF FederationLocal cooperative banks

(Lyon area)

CM SE Federation

Local cooperative banks(French Alps)

CM SMB Federation

CFCMCEE

(Central body)

Funding and treasury operations for CM5-CIC group

(and some other CM federations)

BFCM

and subsidiaries(retail banking)

CIC Group

and subsidiaries(insurance)

GACM Other subsidiaries

Local cooperative banks(North-Eastern France)

CM CEE Federation

Local cooperative banks(Toulouse area)

CM MA Federation

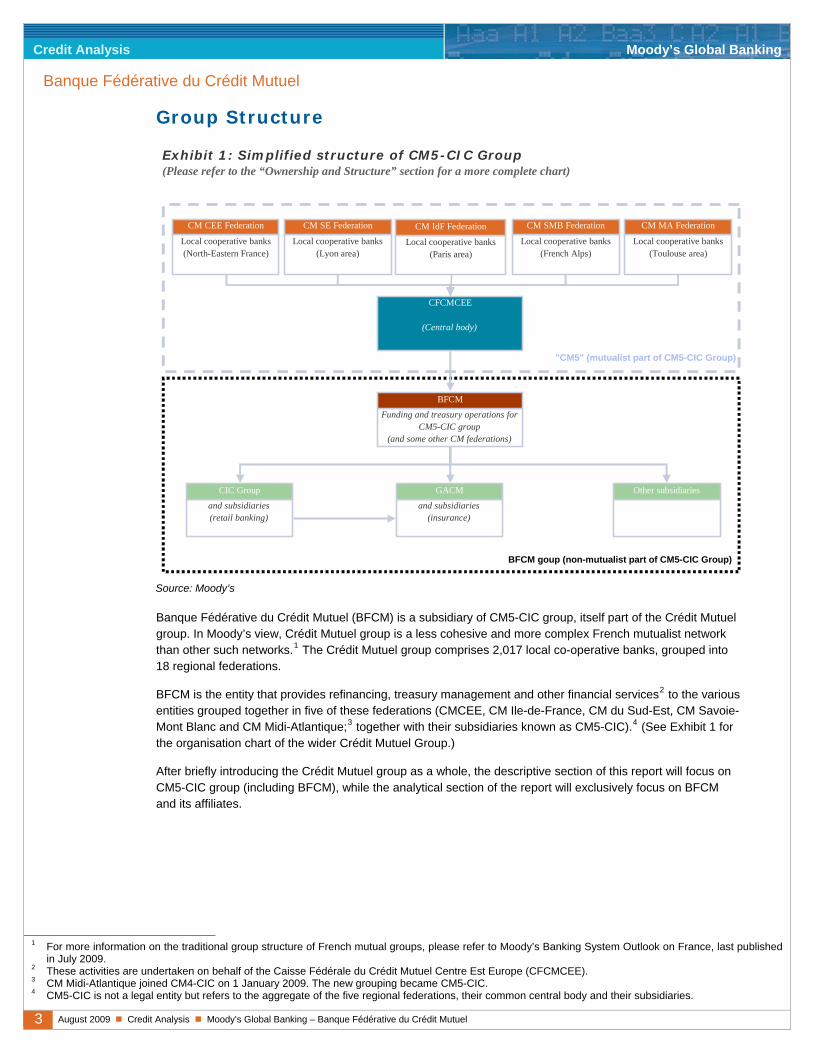

Exhibit 1: Simplified structure of CM5-CIC Group(Please refer to the “Ownership and Structure” section for a more complete chart)

"CM5" (mutualist part of CM5-CIC Group)

BFCM goup (non-mutualist part of CM5-CIC Group)

Source: Moody’s Banque Fédérative du Crédit Mutuel (BFCM) is a subsidiary of CM5-CIC group, itself part of the Crédit Mutuel group. In Moody’s view, Crédit Mutuel group is a less cohesive and more complex French mutualist network than other such networks.1 The Crédit Mutuel group comprises 2,017 local co-operative banks, grouped into 18 regional federations.

BFCM is the entity that provides refinancing, treasury management and other financial services2 to the various entities grouped together in five of these federations (CMCEE, CM Ile-de-France, CM du Sud-Est, CM Savoie-Mont Blanc and CM Midi-Atlantique;3 together with their subsidiaries known as CM5-CIC).4 (See Exhibit 1 for the organisation chart of the wider Crédit Mutuel Group.)

After briefly introducing the Crédit Mutuel group as a whole, the descriptive section of this report will focus on CM5-CIC group (including BFCM), while the analytical section of the report will exclusively focus on BFCM and its affiliates.

1 For more information on the traditional group structure of French mutual groups, please refer to Moody’s Banking System Outlook on France, last published

in July 2009. 2 These activities are undertaken on behalf of the Caisse Fédérale du Crédit Mutuel Centre Est Europe (CFCMCEE). 3 CM Midi-Atlantique joined CM4-CIC on 1 January 2009. The new grouping became CM5-CIC. 4 CM5-CIC is not a legal entity but refers to the aggregate of the five regional federations, their common central body and their subsidiaries.

4 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

Crédit Mutuel Group

The organisational structure of the Crédit Mutuel Group5 is less cohesive and more complex than other mutualist networks. At year-end 2008, the group comprised:

2,017 local co-operative banks or Caisses locales. These are at the root of the organisation, and are regulated as credit institutions. They collect deposits, make loans and provide a wide range of financial services to retail customers, professionals and small corporates. These local banks are owned by 7.2 million bank customers or sociétaires, from a pool of around 11.2 million customers.

18 regional groups or federations, each of which has its own central body or Caisse fédérale. Each Caisse locale and its joint subsidiary, the Caisse fédérale, are members of the regional federation. Federations are not financial institutions. They are entrusted by French banking law with responsibility for controlling the Caisses locales, ensuring their solvency, defining the strategy at regional level, designing products and services, and optimising asset and liability management. They are the strategic and control entities representing Crédit Mutuel group at regional level. The Caisses fédérales provide refinancing, treasury management and other financial services to their Caisses locales. Some federations have decided to join forces into “super-regional” groupings and merge their Caisses fédérales. Five of them are grouped together into “CM5” (CMCEE, CM Ile-de-France, CM du Sud-Est, CM Savoie-Mont Blanc and CM Midi-Atlantique), three others into Arkéa (CM de Bretagne, CM du Sud-Ouest and CM Massif Central) and two into Crédit Mutuel Sud Europe Méditerranéen (CM Méditerranéen and CM Dauphiné-Vivarais). Banque Fédérale du Crédit Mutuel (BFCM) and CIC are subsidiaries of CM5’s central body, CFCMCEE. In addition to the 18 regional groups, the Fédération du Crédit Mutuel Agricole et Rural (CMAR) has competence over the domestic agricultural sector nationwide.

The National Federation (Confédération Nationale du Crédit Mutuel or CNCM) is the central regulatory body according to French banking law. It represents Crédit Mutuel at the national level and oversees the regional federations. At each level – local, regional and national – representatives are elected by the sociétaires to supervise the various entities of the network.

The central bank of the group, Caisse Centrale du Crédit Mutuel (CCCM), is owned by the Caisses fédérales. It manages their treasury but plays a very limited role in the network.

Altogether, Crédit Mutuel group had 18.7 million customers (of which 17.1 million individuals) and approximately 5,600 branches at year-end 2008 (figures including the branches of the Caisses locales of Crédit Mutuel as well as branches of Crédit Industriel et Commercial –CIC– network.

5 Crédit Mutuel Group is not a legal entity but refers to the aggregate of all 2,017 local cooperative banks and their subsidiaries.

5 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

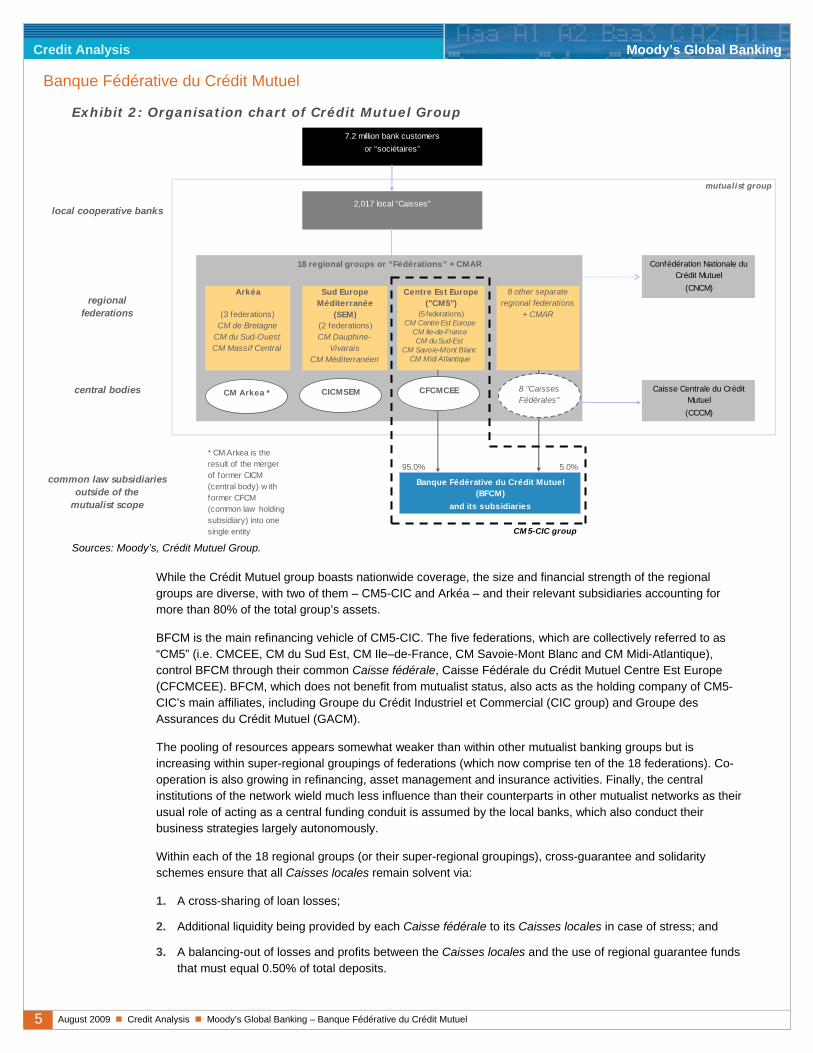

Exhibit 2: Organisation chart of Crédit Mutuel Group

mutualist group

local cooperative banks

regionalfederations

central bodies

95.0% 5.0%common law subsidiaries

outside of themutualist scope

CM 5-CIC group

* CM Arkea is the result of the merger of former CICM (central body) w ith former CFCM (common law holding subsidiary) into one single entity

18 regional groups or “Fédérations” + CMAR Confédération Nationale du Crédit Mutuel

(CNCM)

2,017 local "Caisses"

Banque Fédérative du Crédit Mutuel(BFCM)

and its subsidiaries

7.2 million bank customers or “sociétaires”

Caisse Centrale du Crédit Mutuel(CCCM)

CICMSEM

Arkéa

(3 federations)CM de Bretagne

CM du Sud-OuestCM Massif Central

Sud Europe Méditerranée

(SEM)(2 federations)CM Dauphine-

Vivarais CM Méditerranéen

Centre Est Europe ("CM5")

(5 federations)CM Centre Est Europe

CM Ile-de-FranceCM du Sud-Est

CM Savoie-Mont BlancCM Midi Atlantique

8 other separate regional federations

+ CMAR

CM Arkea * CFCMCEE 8 "Caisses Fédérales"

Sources: Moody’s, Crédit Mutuel Group. While the Crédit Mutuel group boasts nationwide coverage, the size and financial strength of the regional groups are diverse, with two of them – CM5-CIC and Arkéa – and their relevant subsidiaries accounting for more than 80% of the total group’s assets.

BFCM is the main refinancing vehicle of CM5-CIC. The five federations, which are collectively referred to as “CM5” (i.e. CMCEE, CM du Sud Est, CM Ile–de-France, CM Savoie-Mont Blanc and CM Midi-Atlantique), control BFCM through their common Caisse fédérale, Caisse Fédérale du Crédit Mutuel Centre Est Europe (CFCMCEE). BFCM, which does not benefit from mutualist status, also acts as the holding company of CM5-CIC’s main affiliates, including Groupe du Crédit Industriel et Commercial (CIC group) and Groupe des Assurances du Crédit Mutuel (GACM).

The pooling of resources appears somewhat weaker than within other mutualist banking groups but is increasing within super-regional groupings of federations (which now comprise ten of the 18 federations). Co-operation is also growing in refinancing, asset management and insurance activities. Finally, the central institutions of the network wield much less influence than their counterparts in other mutualist networks as their usual role of acting as a central funding conduit is assumed by the local banks, which also conduct their business strategies largely autonomously.

Within each of the 18 regional groups (or their super-regional groupings), cross-guarantee and solidarity schemes ensure that all Caisses locales remain solvent via:

1. A cross-sharing of loan losses;

2. Additional liquidity being provided by each Caisse fédérale to its Caisses locales in case of stress; and

3. A balancing-out of losses and profits between the Caisses locales and the use of regional guarantee funds that must equal 0.50% of total deposits.

6 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

Furthermore, the solidarity between all Caisses locales and Caisses fédérales is formalised by CNCM at the national level:

1. Under the 1984 Banking Law, CNCM is endowed with supervisory powers to monitor the solvency of the members of the network;

2. Regional groups must satisfy internal liquidity ratios;

3. Regional groups must deposit 2% of their customers’ deposits at the CCCM; these funds can be used to provide support to an ailing member; and

4. As a last resort, the CNCM is empowered to take decisions allowing it to make advances, grants or provide additional financing in order to rescue a troubled member.

For a more detailed discussion on CM5-CIC’s structure and the position of BFCM in the CM5-CIC group, please refer to the Ownership and Structure sub-section.

Sources: Moody’s, Credit Mutuel Group and CM5-CIC.

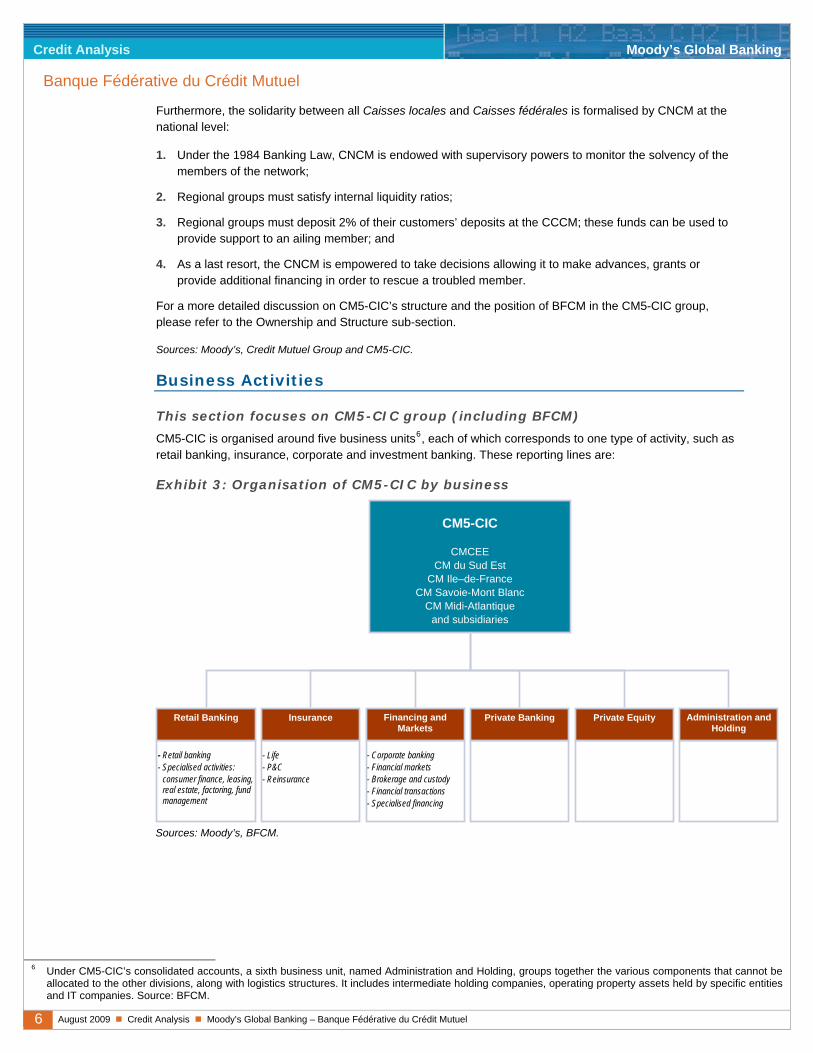

Business Activities

This section focuses on CM5-CIC group (including BFCM)

CM5-CIC is organised around five business units6, each of which corresponds to one type of activity, such as retail banking, insurance, corporate and investment banking. These reporting lines are:

Exhibit 3: Organisation of CM5-CIC by business

Sources: Moody’s, BFCM.

6 Under CM5-CIC’s consolidated accounts, a sixth business unit, named Administration and Holding, groups together the various components that cannot be

allocated to the other divisions, along with logistics structures. It includes intermediate holding companies, operating property assets held by specific entities and IT companies. Source: BFCM.

CM5-CIC

CMCEE CM du Sud Est

CM Ile–de-France CM Savoie-Mont Blanc

CM Midi-Atlantique and subsidiaries

- Life - P&C - Reinsurance

Insurance

Private Banking

Private Equity

- Retail banking - Specialised activities:

consumer finance, leasing, real estate, factoring, fund management

Retail Banking

Administration and Holding

- Corporate banking - Financial markets - Brokerage and custody - Financial transactions - Specialised financing

Financing and Markets

7 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

Retail Bank

This business unit comprises the retail banking activities undertaken essentially in France7 as well as all of the specialised activities whose products are marketed through the branch network (including consumer finance, the leasing of goods and property, real estate, fund management, employee savings plans and factoring). Retail banking activities are undertaken by CM5 networks and BFCM Group (mainly through CIC) while all other retail finance activities are undertaken by BFCM Group, i.e. BFCM and its subsidiaries.

Activities undertaken under the umbrella of BFCM group

Retail activities undertaken within the scope of BFCM are purely those of its subsidiaries as BFCM does not undertake itself any retail activity. BFCM’s subsidiaries active in the retail business are CIC group, Banque de l’Economie, du Commerce et de la Monétique (BECM) and CIC Iberbanco, which are described in more detail below:

CIC group is composed of Crédit Industriel et Commercial (CIC) and its subsidiaries. The group’s retail activities are undertaken by CIC in the Paris area, and by its five regional banks, which together offer retail coverage nationwide.8

In 1998, CIC was privatised and BFCM acquired a 67% stake. CIC was previously owned by GAN, a then state-owned insurance company.

CIC group’s activities are carried out under the CIC brand.9 While CIC and its regional banks share the same brand and graphic charter, no reference on the linkage with Crédit Mutuel group is made to the customers.

In terms of segmentation with private banking, clients serviced by the retail network of CIC are those with a net worth of less than €1 million. Insurance products of the Groupe des Assurances du Crédit Mutuel (GACM) are also cross-sold to retail customers of the retail banking segment (for more details on insurance products and services, please refer to the Insurance sub-section below).

BECM is 98.5% owned by BFCM and focuses on three main business activities:

Services to large corporates and medium enterprises such as treasury operations, medium-to-long term loans, real estate leases, cash management and payment systems, but also LBOs. For these activities, BECM is largely integrated with CIC Ile-de-France (CIC’s subsidiary in the Paris area) for commercial developments, processes and credit risk;

Financing real estate companies mainly for real estate promotion. For real estate-related business, BECM acts as a centre of expertise for all CM5-CIC networks; and

Wealth management for entrepreneurs, in close co-operation with CIC and CM5 networks.

BECM is a niche player with a relatively small size (at year-end 2008, its total assets amounted to €12.5 billion). It benefits from national coverage in France with dedicated branches for each of the activities and relies largely on the CM5 and CIC networks. In addition, BECM also has a local bank in Frankfurt.

The activities of BECM are undertaken under its own brand, but the graphic charter and information provided on its Internet site refer to Crédit Mutuel group.

CIC Iberbanco was acquired in June 2008 by BFCM from Banco Popular Español. It has a network of 18 branches in France, four businesses centres and a retail promotion branch. Although Banco Popular France was re-branded as CIC Iberbanco in April 2009, it is directly held by BFCM and CIC holds no stake in it.

7 The Retail Bank business unit also comprises the foreign activities of Banque de l’Economie, du Commerce et de la Monétique in Frankfurt as well as the

retail activities of Banque de Tunisie (Tunisia) and Banque Marocaine du Commerce Extérieur (Morocco). 8 Each regional bank is responsible for retail activities for a specific region and there is no overlap between CIC’s regional banks. 9 Previously, CIC’s regional banks’ branches used their own brand, which was called CIC followed by the name of the regional bank. The regional banks also

used CIC’s graphic charter. In 2008, all regional banks switched to the CIC brand.

8 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

BFCM also consolidates activities10 undertaken in Tunisia by Banque de Tunisie and in Morocco by Banque Marocaine pour le Commerce Extérieur (BMCE Bank). The stakes in both banks were previously held by CIC Group, which transferred the ownership to BFCM on 5 January 2009. BFCM group holds 20% in Banque du Tunisie and in February 2009 it increased its stake in BMCE Bank to 19.94% from 15% previously. In addition, BFCM holds 5% of Banca Popolare de Milano (BPM).

Activities undertaken by the rest of the CM5-CIC group

Retail activities within the scope of BFCM are complemented by retail banking activities undertaken by the local co-operative banks (Caisses locales) of the five federations of the CM5-CIC group, which conduct operations in separate regions:11

Caisses locales of the CM Centre Est Europe federation are active in north-eastern France;

Caisses locales of the CM du Sud Est federation are active in Lyon area;

Caisses locales of the CM Ile-de-France federation are active in the Paris area;

Caisses locales of the CM Savoie-Mont Blanc federation are active in the French Alps; and

Caisses locales of the CM Midi-Atlantique federation are active in Toulouse area.

The retail banking activities serve individuals with a net worth of less than €1 million as well as SMEs.12 They provide them with a wide variety of products and services, from current accounts to assets under management, savings products (including Livret Bleu,13 the equivalent of Livret A offered to retail customers of the Crédit Mutuel group’s co-operative network).14

Specialised Activities

Activities undertaken under the umbrella of BFCM group

This business line comprises the specialised activities of CM5-CIC. All the specialised activities are undertaken by BFCM’s subsidiaries and as such appear in BFCM’s reporting.

Consumer Finance Consumer credit activities are undertaken by Sofémo group (Société Fédérative Européenne de Monétique et de Financement), Citibank Germany and by Cofidis SA, which are described in more detail below:

Sofémo is held 66.7% by BFCM and 33.3% by CIC. It provides individuals with consumer loans marketed through four dedicated centres and payment facilities to customers of more than 50,000 stores that have entered into co-operation with Sofémo. This service is also available in the retail networks of CM5-CIC (i.e. of both the Caisses locales of CM5 and of CIC group) and in the retail networks of other CM federations, with the exceptions of Arkéa and CM Nord Europe.

Citibank Deutschland was acquired by BFCM in December 2008 from Citibank. Citibank Deutschland is a specialist in consumer finance with more than 3.25 million customers, 6,800 employees and 340 branches at year-end 2008. Unlike traditional consumer finance companies, Citibank Germany also collects deposits from its customers and had a deposit base of €9.4 billion at year-end 2008 (versus a total loan portfolio of €10.4 billion at the same point in time). The final agreement valued BFCM’s 100% stake in Citibank Deutschland at €4.9 billion. Citibank Deutschland was consolidated on 5 December 2008.

10 In accordance with IFRS, the results of Banque de Tunisie are accounted using the equity method (mise en équivalence), as BFCM can exercise significant

influence. The results of BMCE are not consolidated in CIC group’s results as the group holds less than 20% of the voting rights. 11 The size and the boundaries of each federation are based on the historical consolidation of Caisses locales. For more details, please refer to the Company

History section of this report. 12 Corporates not considered to be SMEs are served by CM5-CIC’s Financing and Capital Markets business unit. 13 For more details on Livret Bleu and Livret A, please refer to Moody’s Banking System Outlook on France, last published in July 2009. 14 Until year-end 2008, Livret Bleu savings products could only be sold under the Crédit Mutuel brand. In the case of CM5-CIC group, it could only be provided

to retail customers of the Caisses locales of the five Federations of CM5 (CMCEE, CM du Sud Est, CM Ile-de-France, CM Savoie-Mont Blanc and Midi-Atlantique) and not to CIC’s customers. From this year, all French banks have been authorised to sell Livrets A. CIC will sell the product as Livret A while the Livret Bleu name will be kept for products sold through the five federations’ networks.

9 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

Cofidis SA provides consumer credit services, such as revolving credit, loans repayable in instalments, and credit cards. It has 11.5 million customers in France, Belgium, Spain, Italy, Portugal, Greece, the Czech Republic and Hungary. In March 2009, BFCM and 3 Suisses International (3SI, a French retailer which previously owned 100% of Cofidis SA through Cofidis Participations), reached a final agreement whereby BFCM took 51% control and a 34.17% economic interest in Cofidis. More specifically, BFCM and 3SI created a joint holding company (held 67% by BFCM and 33% by 3SI), which owns 51% of Cofidis Participations, while the remaining 49% in Cofidis Participations is owned directly by 3SI. Cofidis Participations owns 100% of Cofidis SA, the operating entity.

Under the final terms of the acquisition, BFCM will potentially increase its ownership in Cofidis Participations to 67% from 51%, should BFCM and 3SI decide on this by 2016. Under the final terms, Cofidis Participations also has the exclusive right to potentially acquire 3SI’s 66% stake in Monabanq, an online retail bank with 250,000 individual customers.

Leasing In leasing, CM5-CIC operates under CM-CIC Lease for real-estate leasing and under CM-CIC Bail for equipment-leasing activities (e.g. car leasing, industrial equipment leasing). CIC group owns15 54% of CM-CIC Lease and 99% of CM-CIC Bail.

At year-end 2008, CM-CIC Lease’s portfolio mainly consisted of warehouses, commercial premises and industrial premises (26% of total portfolio each), retail premises (10%) and offices (12%).

Equipment-leasing contracts are generated by the banking networks and specialised financing entities of the CM5-CIC group and also by the networks of other CM federations (except Arkéa and CM Nord Europe).

Real Estate Real estate-related activities are undertaken by subsidiaries of CIC group. The activities include:

The investment in real-estate development projects in France through CM-CIC Participations Immobilières SA;

Real estate investments for the group through CM-CIC Soparim; and

Realtor business through CM-CIC Agence Immobilière (AFEDIM), which sells new residential properties on behalf of the Crédit Mutuel and CIC networks (including CIC Banque Privée).

Fund Management CM-CIC Asset Management SA (CM-CIC AM) is the entity responsible for asset management for the whole CM5-CIC group, including BFCM.16 It manages a large number of mutual funds invested in four categories: equity and diversified funds, money market funds, bond funds and formula funds.17

CM-CIC AM’s products are marketed in the two branch networks of CM5’s Caisses locales and of CIC group, but also in the networks of other CM federations (except Arkéa and CM Nord Europe). That said, some products are exclusively marketed in one of the two networks. In addition, CM-CIC AM resorts to external funds for funds invested in international equities.

In addition to the mutual funds for the group’s customers, CM-CIC AM manages a number of employees’ mutual investment funds schemes for corporates (referred to as OPCVM). These activities are undertaken by CM-CIC Epargne Salariale,18 a 100%-owned subsidiary of CIC group.

15 Aggregate shareholding through CIC (main shareholder) and its regional banks. BFCM also owns 45.9% of CM-CIC Lease. Source: BFCM. 16 CM-CIC AM was created in 2004 via the merger of Crédit Mutuel Finance and CIC AM. It is now jointly owned by BFCM (51%) and by CIC (23.5%). 17 Source: BFCM. 18 CM-CIC Epargne Salariale was created via the merger of CIC group’s subsidiary CIC Epargne Salariale and BFCM’s subsidiary Crédit Mutuel Participation in 2007.

10 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

Factoring Factoring activities are undertaken by Factocic and CM-CIC Laviolette Financement.

Factocic was created in 1992 as a partnership between CIC, Crédit Mutuel Group and GE FactoFrance, which, respectively, own 51%, 15% and 34% of the voting rights.

CM-CIC Laviolette Financement is 100%-owned by CIC group.

Both subsidiaries offer factoring services to SME and large corporate customers of the branch networks of the 18 federations of the Crédit Mutuel Group and of CIC. The factoring services include cash advances and the settlement of customers’ accounts as well as the purchase of assigned business receivables.

In 2007, three new partners (CIC Société Bordelaise, a regional bank of CIC group, Crédit Mutuel Nord Europe and Crédit Mutuel de Normandie) entered into business with CM-CIC Laviolette Financement.

CM-CIC Covered Bonds CM-CIC Covered Bonds is a subsidiary of BFCM created in June 2007 to issue covered bonds backed with French real-estate mortgage loans and prêts cautionnés19 originated by the retail networks of CM5-CIC and other CM federations. The entity, which is supervised by the Banque de France, issued covered bonds for the first time in July 2007.20

Insurance

Activities undertaken under the umbrella of BFCM group

The insurance activities of BFCM are undertaken by GACM, which is ultimately owned 73.3%21 by BFCM. GACM is the holding company of a number of subsidiaries specialising in specific insurance products and services.

Life insurance activities are undertaken by ACM Vie SA, Sérénis Vie, ACM Vie SAM and International Crédit Mutuel Life (ICM LIFE), all 100% subsidiaries of the GACM;

Personal and P&C insurance activities are undertaken by ACM IARD SA (owned 96.4% by GACM), Sérénis Assurances SA (owned 99.13% by GACM) and S.A. Partners Assurances. S.A. Partners Assurance was fully acquired by GACM in 2006;

Reinsurance activities are undertaken by Crédit Mutuel Reinsurance (ICM RE), a 100% owned subsidiary of GACM.

GACM’s life insurance, personal risk and P&C policies are provided to the customers of the branch networks of CIC group (including private banking clients), CM5 and to those of other federations of Crédit Mutuel group, with the exception of Arkéa and CM Nord Europe. In addition to selling its own insurance products, GACM is also active in insurance brokerage through its subsidiary Procourtage and in a number of specialised niche insurance services.

GACM also owns minority stakes in several foreign insurance companies, including three Canadian non-life insurance companies that are part of Mouvement Desjardins (a 10% stake in each), the Tunisian insurance company Astree (30%), the Moroccan company Royale Marocaine d’Assurance-Watanya (20.25%) and the Spanish firms SA Nostra and Serbrok (5% and 10%, respectively). More recently, in October 2008, the Group created a joint venture with the Royal Automobile Club of Catalonia (RACC). The joint company, RACC Seguros, is 51% held by RACC and 49% by GACM. The company offers insurance policies, spanning from car insurance to other P&C products, as well as to life insurance products. Through its 240 branches, the RACC has more than 1 million members, is the fifth-largest insurance broker in Spain with more than 850,000

19 Prêts cautionnés are residential housing loans guaranteed by credit institutions such as Crédit Logement or Saccef. For more details on prêts cautionnés,

please refer to Crédit Logement on moodys.com. 20 CM-CIC Covered Bonds has established a €15 billion EMTN programme under which it issues its covered bonds. 21 BFCM directly owns 55.96% of the shares of GACM, while 20.52% are owned by ADEPI, a 100%-owned subsidiary of CIC group; 23.52% are owned by the

central bodies of Crédit Mutuel federations other than CM5 federations.

11 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

insurance contracts (all insurance contract types included), but is also the leading car insurance broker in Spain (with 400,000 contracts).

Financing and Markets

Activities undertaken under the umbrella of BFCM group

In addition to providing large corporate customers with banking services and products, the financing and markets business unit groups together all of the group’s financial market activities, the financial transactions on the primary market (such as M&A, IPO) as well as project finance.

The activities are organised into the two divisions that follow.

General banking activities service large corporates as well as customers of the retail and private banking business units who require the expertise of the proprietary trading desks for specific products/services.

The products marketed are interest and FX hedges, as well as investment propositions.

Financial market activities are undertaken by CM-CIC Marchés, a division within CIC created in 2006 as a merger of BFCM’s, CIC’s and CIC Banque CIAL’s22 formerly separate trading activities. CM-CIC Marchés’ activities are twofold:

Proprietary trading activities of the CIC group (and thus consolidated in CIC group’s accounts). These activities were previously organised into four trading groups (equity trading, hybrids trading, trading of fixed-income securities issued by corporates and financial institutions and trading of sovereign fixed-income securities).

In 2009, the group decided to scale down its proprietary trading activities. In addition to reducing the equity allocation to this business segment, it decided to focus on trading activities with potential cross-sale opportunities with corporate or private banking customers.

In addition, the group also reorganised the proprietary trading activities as follows:

Equity and hybrids:

On equity trading, the main focus is on cash equity. This business involves taking arbitrage positions on M&A deals, event-driven positions and long/short equity positions (including quantitative trading). In addition to trading cash equity products, this group has also recently started to trade volatility products;

Hybrids trading focuses on convertibles and structured products, mostly on convertible bonds;

Trading of fixed-income securities issued by financial institutions, mostly from Europe and of correlation;

Trading of fixed-income securities issued by corporates, mostly from Europe and of asset-backed securities (ABS).

Trading of sovereign fixed-income securities, mostly arbitrage between sovereign securities and the equivalent swap.

Treasury, refinancing and ALM for CM5-CIC group, as well as the other federations of Credit Mutuel group, with the exception of Arkéa and CM Nord Europe. These positions are booked directly in BFCM’s accounts and do not appear in CIC group’s reporting.

All activities are undertaken by the same trading floors but are booked either in CIC group’s accounts23 or directly in BFCM’s own accounts.

22 CIC Banque CIAL, a regional bank of CIC Group headquartered in Strasbourg, France, had its own investment banking department until 2006. This

department was combined with its parent, CIC, in order to create a single entity, CM-CIC Marchés. 23 Activities booked in CIC group’s accounts are also fully accounted for in BFCM’s accounts as BFCM ultimately owns 91% of CIC group.

12 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

Brokerage and custody: CM-CIC Securities, a 100% subsidiary of CIC group, acts as a broker-dealer, clearing agent and custodian. In brokerage, CM-CIC Securities is a member of ESN LLP, a “multi-local” network of ten brokers in European equity markets and covering 15 European countries. Custodian activities are undertaken by its subsidiary, CM-CIC Titres.

Financial transaction activities comprise all businesses involved in the primary market.

Specialised financing comprises the services extended to Crédit Mutuel group’s clients for the funding of acquisitions, assets or projects.

Private Bank

Activities undertaken under the umbrella of BFCM group

This business unit comprises all of the private banking activities of CM5-CIC. These activities are exclusively undertaken under the umbrella of CIC group by its private banking business unit, CIC Banque Privée24, both in France and abroad. Private banking customers are defined as customers with a net worth of €1 million and more.

The main private banking subsidiaries in France are:

CIC Banque Transatlantique (100% owned by CIC); and

Dubly-Douilhet (61.9% owned by CIC);

The private banking arm of BFCM has established itself in a number of foreign countries with strong private banking markets. Private banking operations are carried out through a number of entities. The major ones are:

Banque de Luxembourg and Banque Transatlantique Luxembourg (71.1% and 60% owned by CIC, respectively) in Luxembourg;

Banque CIC Suisse and CIC Private Banking-Banque Pasche in Switzerland (both 100% owned by CIC group); and

CIC Singapour and CIC Private Limited Hong Kong (both 100% owned by CIC group).

Private Equity

Activities undertaken under the umbrella of BFCM group

This business unit mainly comprises three entities of CIC group, each responsible for private equity activities in a specific region of France. These subsidiaries of CIC group are:

CIC Finance (100%-owned), which is active in the Paris region and in north-eastern France. It engages in proprietary transactions and provides M&A advisory services;

IPO, which is 76.6%-owned by CIC group, is active in western France; and

CIC Banque de Vizille (93.9%-owned) in southern France

Administration and Holding

Activities undertaken under the umbrella of BFCM group

The administration and holding unit comprises the various components that cannot be allocated to the other divisions, along with logistics structures. These components are intermediate holding companies, operating property assets held by specific entities and IT companies of BFCM.

24 CIC Banque Privée is a business unit of CIC group and is not a legal entity.

13 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

Exhibit 4: Breakdown of net banking income (NBI) by BFCM’s business units

NBI by activity (in %) (1)

71.2%

16.6%0.6%

9.2%2.4% Retail banking

Insurance

Financing and Markets

Private Bank

Venture Capital

Segment Net Banking Income (NBI)

(EUR million)

H1 2009 (2) YE 2008 (3)

Retail banking 1,636 3,289

Insurance 491 765

Financing and Markets -88 26

Private Bank 225 427

Venture Capital 94 112

Structure and Holding -195 -671

Intra-Group -19 -46

GROUP 2,144 3,902

(1) Excluding Structured and Holding and Intra-Group. (2) Including full contribution of CIC Iberbanco, Citibank Deutschland and Cofidis. (3) Including contribution of CIC Iberbanco and Citibank Deutschland since the date of acquisitions. Source: Moody's, BFCM.

Distribution Capacity and Market Shares

Retail Banking

Activities undertaken under the umbrella of BFCM group

As regards the distribution capacity and the market shares of the business activities carried out solely under the umbrella of BFCM:

The CIC retail network comprises five CIC regional commercial banks with more than 2,122 branches (of which 1,702 are retail oriented, 59 geared toward private banking activities and 294 cater services to corporate customers). It has approximately 22,600 employees, catering services and products offered to 3.45 million individual customers (including customers of the private banking business unit) and approximately 691,300 corporates and self-employed professionals;25

BECM has 26 corporate branches in France, nine real estate branches and three private banking branches. BECM’s own distribution capacity is supplemented by that of the CM5 federations and of CIC group. The bank has 330 employees and approximately 15,400 customers; and

Banco Popular, rebranded CIC Iberbanco, has 18 branches in France.

25 As disclosed by CIC group, without breakdown between customers of the retail banking business line and those of financing and capital markets.

14 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

Activities undertaken by the rest of the CM5-CIC group

At year-end 2008, the retail network of the Caisses locales of the CM5-CIC group comprised 1,309 branches and boasted more than 4 million customers.

More specifically:

The CMCEE federation has 900 branches and reports market shares of more than 45% in deposits and loans in the Alsace region, approximately 20% in the Lorraine region and over 15% in the Franche Comté region. Its market shares in the Bourgogne region are lower, at 7.5% for deposits and 13.1% for loans;26

CM du Sud-Est federation has 134 branches with market shares of 6.0% of deposits and 13.3% of loans in the Rhône-Alpes region;27

CM Ile-de-France federation has 171 branches and market shares of 1.7% in deposits and 3.2% of loans in the Paris area;28

CM Savoie-Mont Blanc federation has 64 branches and market shares of 7.1% of deposits and 8.6% of loans in the Savoie-Mont Blanc region;29 and

CM Midi- Atlantique federation has 84 branches and 260.000 customers and market shares of 4.5% of deposits and 3.5% of loans in the Toulouse area.

Specialised Activities

In Consumer Finance, Sofémo has four dedicated centres and more than 50,000 points of sale that have entered into partnership with it. The services and products of Sofémo are also available through the retail networks of CM5-CIC.

Citibank Deutschland has more than 3.25 million customers serviced through 340 branches.

Cofidis SA has 11.5 million customers in France, Belgium, Spain, Italy, Portugal, Greece, the Czech Republic and Hungary.

During 2008, CM-CIC Lease SA increased its real estate portfolio by €474 million, with 279 new leasing operations. As regards equipment leasing activities, CM-CIC Bail had 170,000 leasing transactions at year-end 2008 and its equipment portfolio stood at €4.7 billion, up by 12% from YE 2007.

The real estate investments of CM-CIC Participations Immobilières SA generated €95 million of revenues in 2008 and represented nine new projects (corresponding to approximately 471 housing units).

As regards real estate activities in 2008, 2,750 homes worth €480 million were sold by CM-CIC Agence Immobilière AFEDIM, which generated €17.4 million of fees before tax.

CM CIC Asset Management has €54.7 of funds under management. CM-CIC Epargne Salariale offered 231 OPCVM30 to approximately 44,332 corporates and 1.6 million employees at year-end 2008. Assets under management stood at approximately €3.8 billion at year-end 2008.

In factoring, Factocic works with one in ten companies in factoring services in France. In 2008, it reached a market share of 7.5% in receivables purchased; it had 2.849 active contracts and 214 employees at year-end 2008.

As regards receivables purchasing, in 2008 CM-CIC Laviolette Financement processed approximately 255,000 invoices, representing inflows of approximately €1.5 billion.

26 Source: CM5-CIC. 27 Source: CM5-CIC. 28 Source: CM5-CIC. 29 Source: CM5-CIC. 30 For a definition of OPCVM, Please refer to the description of the fund management business unit in the Business Activities section of this report.

15 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

Insurance

The consolidated income of GACM in 2008 stood at €6.71 billion, down by 13.9% from 2007. The IFRS net result stood at €395 million, down by 29% from 2007. GACM had 6.5 million customers (in P&C and life insurance together) at year-end, up by 4.8% from 6.2 million customers at year-end 2007, while the number of contracts was up by 9% to 19.331 million from 8.2 million at year-end 2007.

GACM distributes its products through the retail banking networks of CM5, CIC and the other federations of Credit Mutuel group, with the exception of Arkéa and CM Nord Europe. GACM is the second-largest bancassurer in France, after Crédit Agricole Assurances. Overall, it is the fourth-largest life insurer in France and one of the leaders in P&C insurance.

Financing and Capital Markets

As regards financial markets activities, three sales teams cater services and products to the retail networks (including SMEs), the large corporates and the regional and local governments (RLGs) and sovereign investors.

Brokerage activities at CM-CIC Securities are undertaken by a team of 50 salespersons, which is supported by a research team of 30 analysts and strategists.

Private Bank

In France, CIC Banque Privée offers its products through 59 dedicated branches. Abroad, this network is complemented by the group’s foreign private banking entities.

Private Equity

CIC Finance has a team of 55 employees in Paris and in the rest of France and managed a portfolio of €1.3 billion at year-end 2008, of which €629 million was funds managed for third parties (consolidated figures including portfolios held by CIC Finance’s subsidiaries).

IPO comprised a team of 15 employees and managed €345 million invested in 156 regional corporates at year-end 2008, in which year IPO took part in 27 new deals, managing €82.9 million.

CIC Banque de Vizille comprised 42 employees and managed 153 investment portfolio lines and a €465 million invested portfolio at year-end 2008.

The new investments of the three private equity subsidiaries of CIC group totalled €341 million in2008 and the investment portfolio stood at over €2.1 billion at year-end 2008.32

Company History

BFCM was created in 1919 as a member of the Fédération d’Alsace-Lorraine (federation of the Alsace-Lorraine region) of the Caisses Locales of Crédit Mutuel. In 1958, Crédit Mutuel was granted legal status as a mutualist group and the Fédération d’Alsace-Lorraine was renamed Fédération du Crédit Mutuel d’Alsace et de Lorraine. In 1971, the group started its insurance activities under its subsidiary, GACM. In 1972, the Caisses locales of the Franche Comté region joined the federation and were followed by the Caisses Locales of Fédération du Crédit Mutuel Centre-Est in 1992. The federation was then renamed Fédération du Crédit Mutuel Centre-Est-Europe (CMCEE).

In 1998, Crédit Industriel et Commercial (CIC) was privatised by the state and CMCEE, one of the bidders, was allowed to acquire a 67% stake in CIC. This stake was increased to 90% in 2001.

CMCEE established a partnership with Fédération du Crédit Mutuel du Sud-Est (CM Sud-Est) in 1993 and with Fédération du Crédit Mutuel Ile-de-France in 2002. Fédération du Crédit Mutuel Savoie Mont Blanc joined in 2006.The last partner to join was the Fédération Midi-Atlantique, in January 2009. Together, the five

31 Excluding ACM Vie Mutuelle 32 Source: CM5-CIC.

16 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

federations and their subsidiaries are now known as “CM5” (when referring only to the mutualist part of the group) or “CM5-CIC” (when referring to the overall group, including common law subsidiaries).

In 2004, CIC acquired a 10% minority stake in Banque Marocaine du Commerce Extérieur (BMCE).

In December 2008, BFCM acquired 100% of Citibank Germany, Citigroup’s German retail banking operation and, in March 2009, BFCM acquired 51% ownership (34.17% economic interest) of Cofidis Participations, the parent company of the French consumer finance provider Cofidis SA.33

33 For more details on the ownership structure of Cofidis S.A., please refer to the Business Activities section of this report.

17 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

Ownership and Structure

BFCM is the entity that provides refinancing, treasury management and other financial services34 to the entities comprising the five federations (CMCEE, CM Ile-de-France, CM du Sud-Est, CM Savoie-Mont Blanc and CM Midi–Atlantique) together referred to as CM5-CIC35 (see Exhibit 1 for the organisation chart of the wider Crédit Mutuel group), but also to most of the other federations of the Crédit Mutuel group, with the usual exceptions of Arkéa and Crédit Mutuel Nord Europe.

Exhibit 5: Structure of CM5-CIC Group

BFCM group (non-mutualist part of CM5-CIC group)

" CM5" (muatualist part of CM5-CIC Group)

Caisse Fédérale du CM CEE, CM SE, CMIdF, CM SMB et CM MA

(CFCMCEE)central body

Local cooperative banks

CM CEE Federation

Local cooperative banks

CM SE Federation

Local cooperative banks

CM IdF Federation

Local cooperative banks

CM SMB Federation

Funding and liquidity management for CM5-CIC group

Banque Fédérative du Crédit Mutuel (BFCM)

Specialised entities

Technologies

Asset Management

CM-CIC AM

Retail & commercial banking in Paris area,

CIB

CIC

Insurance

GACM

Commercial Banking

BECM

Consumer Finance in Crédit Mutuel network

Sofémo

CICBanque BSD-CIN

Retail banking in North France

CICBanque CIO-BRO

Retail banking in West France

CICSociété Bordelaise

Retail banking in South West France

CIC Lyonnaisede Banque

Retail banking in South East France

CIC EST

Retail banking in East France

CIC BanqueTransatlanique

Private banking

Dubly-Douilhet

Private banking

Banque Transatlantique Luxembourg

Private banking

CIC Private Banking Banque Pasche

Private banking

Banque de Luxembourg

Private Banking

CIC Suisse

Private Banking

72%

94.56%

78.08%

Ventadour Investissement

100%

20.34%

CIC Finance

Private equity

IPO &CIC Banque de Vizille

Private equity

CM-CICSecurities

Brokerage and custody

CM-CIC Bail *

Leasing

CM-CIC Lease *

Real-estate leasing

Factocic *

Factoring

ADEPI ACM Vie S.A. ACM IARD S.A.

CM5-CIC Group

56% 98.5% 66.7% 51%

18.98%

29%

45.9

100%

20.52%

33.3% 23%

100% 100% 100% 100% 100%

100% 61.90% 60% 100% 100% 71.1%

100% 76.6% / 93.9% 100% 98.9% 54.1% 51%

Local cooperative banks

CM MA Federation

Retail banking in France

CIC Iberbanco

Consumer finance in Germany

Citibank Germany

100%100%

Internationel consumer finance

Cofidis SA

Joint holding with 3SI *

Cofidis Participations *

67% 51%

100%

NRJ Mobile

90%

* The remainder is held by 3SI (3 Suisse International). For more details, please refer to the Business Activities section of this report. Sources: Moody’s, BFCM.

34 These activities are undertaken on behalf of Caisse Fédérale du Crédit Mutuel Centre Est Europe (CFCMCEE). 35 CM5-CIC is not a legal entity but relates to the consolidation of the five regional groups and their subsidiaries since they merged their central bodies.

18 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

Key Issues

CM5-CIC: a pole of consolidation within a loose mutualist group

In comparison with other French mutualist groups, Crédit Mutuel group appears to be less cohesive, with much looser co-operation at the group level and more independence for the regional federations. The co-operative support mechanisms of Credit Mutuel group are somewhat weaker than those of other French mutualist groups. Each federation also has its own central body, responsible for treasury operations and funding, although those central bodies can –and do– delegate their operations to designated entities, mainly to BFCM.

However, over the past decade, some of the federations within the group have started to develop partnerships in specific businesses to improve efficiency and rationalise their activities. Some have gone further and merged their central bodies while extending their partnerships to all activities, as is the case for CM5-CIC.36 In Moody’s view, the cohesiveness and centralisation within CM5-CIC is at least as strong –and in many instances stronger– than in the other French mutualist groups.

In summary, Credit Mutuel group is probably the least cohesive of the French mutualist groups, but it consists of sub-groups that are, in some cases, among the most cohesive of the French mutualist groups.

Moody’s notes that most of the federations’ central bodies have delegated their treasury and funding to CM5-CIC’s subsidiary – BFCM – with the exception of Arkéa and Crédit Mutuel Nord Europe. In addition, the insurance arm of CM5-CIC services its products for the customers of the entire Crédit Mutuel group (with the same exceptions: Arkéa and CM Nord Europe), as do other “factories” within CM5-CIC (factoring, leasing, etc.]).

In the context of high competition and the need for Caisses locales to provide retail and commercial customers with more complex or tailor-made products, it appears likely, in Moody’s view, that other federations of the Crédit Mutuel group will decide to join CM5-CIC, as was the case for the Midi-Atlantique federation, which joined CM4-CIC on 1 January 2009, thus forming CM5-CIC. This process is facilitated by the gradual migration of most federations to CM5-CIC’s IT platform. Moody’s expects the trend of the “concentration” of Credit Mutuel group around CM5-CIC to continue.

Franchise developments under the scope of BFCM

BFCM’s strong presence throughout France through CIC group and BECM in retail and commercial banking as well as in insurance through GACM is an important rating driver. Alongside the integration of CIC group, BFCM has managed to develop cross-selling opportunities with its insurance arm, GACM. Moody’s expects the cross-sales to continue to deliver improved profitability in the medium term. In Moody’s view, CM5-CIC –and BFCM within CM5-CIC – has developed a complete universal banking model in France, which has helped the group to maintain its growth in the past few years.

Given the stiff competition in France and the deterioration of the macroeconomic environment, we believe it will be difficult for CM5-CIC to organically improve its market shares. We understand that some of BFCM’s businesses activities could, however, benefit in the event that other federations of the Crédit Mutuel group decide to join CM5-CIC. Indeed, although the Caisses locales of CM5-CIC are outside the scope of BFCM, a significant proportion of the services and products they offer to their clients stem from BFCM and its subsidiaries.37

We note also that BFCM has recently been acquisitive, with the purchase of controlling stakes in CIC Iberbanco (previously Banco Popular France) in June 2008, Citibank Deutschland, a German consumer finance company previously controlled by Citibank, in December 2008, and Cofidis Participations, the parent of the French consumer-lending arm of 3 Suisses retailer (Cofidis SA), in March 2009.

36 CM5-CIC group is not a legal structure. For more details of this partnership between the five federations, please refer to the Group Structure of the Crédit

Mutuel Group and to the Company History sections of this report. 37 This includes the consumer finance products of Sofémo, the funds from CM-CIC AM and the insurance products from GACM.

19 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

In addition to bringing some earnings diversification, the acquisition of significant franchises in the consumer-lending field has also brought geographic diversification, particularly given that Citibank Deutschland’s operations are concentrated in Germany, where BFCM previously had only one branch (through BECM).

We note that the group had viewed consumer finance as a strategic development focus for some time, but caution about the timing of the acquisition given the deterioration of the macro-economic environment in France and Germany and our expectation of an increase of the cost of risk, especially in consumer-lending activities, which are more vulnerable to an increase in unemployment rates and individual insolvencies.

Analysis of Rating Considerations

Discussion of Qualitative Rating Drivers

Franchise Value

Strong national bancassurance franchise

BFCM’s franchise is characterised by a strong foothold in retail and commercial banking and insurance in France, resulting in a resilient earnings mix. Its franchise is also growing in the field of consumer finance, although we caution that this activity results in higher earnings volatility, especially in the current macroeconomic environment.

Market Share and Sustainability

Strong bancassurance franchise and increasing integration within CM5-CIC group

BFCM has built strong domestic franchises in banking and insurance. While the banking activities have significantly increased as a result of the acquisition of CIC group, the GACM’s insurance activities were developed internally by the group.

CM5-CIC group as a whole (i.e. including CM5’s mutualist network and BFCM’s networks, but excluding the 13 other Crédit Mutuel federations’ networks) ranks as the third-largest domestic bank in France, ahead of Société Générale and BNP Paribas. CIC group on its own has attained good national coverage in retail and commercial banking. GACM ranks second in France in bancassurance, fourth overall in life insurance and among the market leaders in P&C insurance.

Moody’s views positively BFCM’s cross-selling opportunities with the mutualist network (Caisses locales) of CM5’s federations. Indeed, although CM5’s retail banking activities are carried out outside the scope of BFCM, the strong and increasing integration within CM5-CIC group enables retail coverage and penetration to be carried out and promoted on a group basis. As such, CIC group’s network, like the mutualist network of CM5, has adopted a model of cross-selling products and promotes GACM’s insurance policies and CM-CIC Asset Management’s products.

Moody’s also notes that BFCM’s franchise extends beyond CM5-CIC group. BFCM, through its subsidiaries, acts as the product factory for most of Crédit Mutuel group’s other federations. BFCM’s subsidiaries’ products and services are distributed throughout these federations’ networks under common brand names.

The bank has also recently acquired significant existing franchises in consumer finance in France, through Cofidis, and in Germany, through Citibank Deutschland. While Citibank Deutschland’s customer base does not overlap with that of BFCM and while Cofidis’s customer base may differ from that of BFCM’s retail arm, we believe the group may benefit from the technology and know-how of both firms in the fields of consumer lending in terms of streamlining its own consumer-lending activities and those of CM5-CIC’s network (and, more widely, those of the rest of Crédit Mutuel’s network).

Overall, Moody's views BFCM's franchise as strong and we expect it to improve in the medium term thanks to the increasing cross-selling opportunities within CM5-CIC’s networks and those of the other

20 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

federations. However, we view the successful operational and risk management integration of the new consumer-lending activities as the key to maintaining BFCM’s risk profile and earnings volatility level.

Geographic Diversification

Growing presence abroad, albeit in relatively risky markets

BFCM’s retail activities remain predominantly focused on the French banking and insurance markets; following the acquisition of Citibank Deutschland, the German consumer-lending market represents BFCM’s first significant non-domestic foothold. BFCM’s insurance activities have also developed a life and P&C insurance partnership in Spain with the Royal Automobile Club of Catalonia.

While the acquisition of consumer-lending activities is a positive driver for the bank’s earnings and customer diversification over the medium-to-long term, we caution that the weakening macroeconomic environment in France and in Germany may prove challenging, especially given the rising unemployment rate and greater levels of individual insolvency.

Earnings Stability and Earnings Diversification

Increasing diversification mitigated by high volatility in financial markets activities

BFCM’s strong reliance on retail activities –including banking and insurance– results in a high proportion of relatively stable earnings. Moody’s also considers the liquidity management activities undertaken by BFCM for both CIC and CM5 to be stable.38

In addition to these activities, BFCM also has riskier and more volatile businesses, including proprietary trading activities. Moody’s understands that BFCM has decided to scale down some of its financial markets activities, but notes that such activities had a significant adverse effect on the bank’s earnings in 2008. What is more, BFCM’s net result would have been negative had the group not reclassified its assets as permitted under the IAS 39 amendments.

We further note that the consumer-lending activities will also bring some extra volatility, at least in the short-to-medium term, given the deteriorating macroeconomic environments in France and Germany.

Risk Positioning

Controls and Risk Management

Improving, yet not sufficiently integrated, controls and risk management

Following the losses linked to CIC’s structured equity derivatives portfolio in 2005, the group decided to restructure its market activities and beef-up its risk management capacity. A number of projects started after the 2005 losses, including a group-wide effort to put in place a historical VaR and stress-testing models covering the bulk of market-related activities. The models were established in late 2007 and provided a much-needed improvement.

Moody’s understands that the group has decided to scale down its financial markets activities after losses incurred in the financial turmoil since 2007. For more details, please refer to the Market Risk Appetite sub-section, below.

Another development has been the establishment at group level of an independent risk department with oversight over credit, market and operational risk. However, this department has not been empowered with decision-making or sanction capacities. The risk department's main attributes are to measure and control risks and to validate processes. For all practical and operational purposes, the various business lines have retained control over their various risk departments.

38 CFCMCEE, the central body of CM5’s five federations, delegated its liquidity management activities to BFCM. Moody’s does not expect any change in that

respect in the foreseeable future.

21 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

Overall, Moody's believes that, given CIC's size and broad market activities, its risk management teams are probably not sufficiently integrated and remain primarily linked to the operational business lines. That said, the group has developed or is developing tools that will allow for effective management of risks. For instance, the credit department has developed its own state-of-the-art IT tool to fully identify, follow and consolidate all credit risks within CM5-CIC, including BFCM and its subsidiaries (including CIC) but also including all credit activities carried out by the local banks of the co-operative network.

Financial Reporting Transparency

Weak financial transparency

The quality of information publicly available on BFCM is weak and, in our view, does not provide market participants and counterparties with all the necessary information to fully assess the risks undertaken at the level of BFCM. More specifically, the information on market risk appears to be poor in comparison to the still sizeable market activities undertaken at the CIC level and the importance of BFCM to the whole CM5-CIC group for treasury and funding activities. Moody’s is aware that the French regulator does not require specific capital adequacy measures at BFCM’s level. Thus, we note that the risk-weighted assets and capital adequacy ratios, such as the Tier 1 ratio, are publicly available at the levels of CIC group and CM5-CIC, but are not disclosed at the level of BFCM.

The bank’s annual reports are complemented by semi-annual summarised reports and a Reference Document (Document de Référence). Despite being richer in terms of information, the latter is published only later in the year and does not provide market participants and counterparties with timely information.

The information disclosed at the level of BFCM’s subsidiary CIC group is slightly richer and is a direct consequence of the listing of CIC group’s shares. As such, CIC group publishes semi-annual press releases but containing only selected items of the profit & loss account and balance sheet.39

Credit Risk Concentration

Higher granularity provided by the proportion of retail activities

As is the case for other important banks and financial institutions in France, BFCM has a high borrower concentration to other financial institutions and to sovereigns. However, Moody’s notes that the bulk of these exposures are highly rated (A3 and above) and, when adjusted for this, the credit risk concentration is average.

We view positively the high proportion of “retail activities” stemming from CIC group and GACM, as they result in a higher granularity of the bank’s overall exposure.

Excluding the exposures to individuals and to financial institutions, insurance and sovereigns, the biggest industry exposure is to real estate,40 encompassing all real estate-related sectors and representing 14.13% of total commitments, followed by manufacturing (12.5%).

Liquidity Management

A reflection of BFCM’s role in managing CM5-CIC group’s liquidity

Although CM5-CIC has a strong retail base and solid retail-deposit-gathering capacity, which is helping it through the present crisis, BFCM and its subsidiaries are slightly more reliant on market funding. The group took steps, however, to alleviate and manage the situation and it has adequate liquidity management, in our view. Notably:

BFCM monitors its liquidity risk through various crisis scenarios;

The share of medium-term refinancing has been growing over the past few years;

39 Itemised accounts are available only in the annual report. 40 As reported in BFCM’s Reference Document for 2008. These figures are based on loan exposures and exclude other exposures encompassed by Moody’s

definition of credit risk concentration. For more details of Moody’s definition of credit risk concentrations, please refer to Moody’s ‘Bank Financial Strength Ratings: Global Methodology’, published in February 2007.

22 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

The group set up a covered bonds issuer (CM-CIC Covered Bonds) in 2007;

The group maintains at all times 30% cover of its deposits by available liquid assets;

The net one-day borrowing position is closely monitored and strictly limited to a maximum of €10 billion; and

The total cash inflows and outflows over a month must be balanced at all times for all entities within the group.

Market Risk Appetite

Scaled down, yet still sizeable proprietary trading activities

Following the losses linked to CIC’s equity structured derivatives business in 2005, the group decided to restructure its market activities. As such, CIC’s market activities were largely discontinued and merged into those of CIAL (then one of CIC’s regional subsidiaries) and re-grouped directly at CIC level. However, although CIC is no longer active in some of the riskier businesses, its market activities remain somewhat similar to those of a hedge fund and they are not dominated by client-driven flows.

Earlier in 2009, the group took the decision to downsize its proprietary activities and to focus on trading activities, which lead to cross-selling opportunities with corporate and private banking customers. Although the trading desks have been maintained, we understand that the group has decided to reduce the capital allocation for proprietary trading activities as a whole.

We will closely monitor developments in CIC’s financial markets activities and notably its proprietary trading activities to ensure they remain within the risk appetite of the bank and of the group. Moody’s views the large losses generated by those activities as an indicator of a larger risk appetite than we had previously anticipated.

Regulatory Environment

In common with other banks incorporated in France, BFCM is first and foremost subject to the French regulatory environment.

For a detailed discussion of the French regulatory environment, please refer to Moody's latest Banking System Outlook on France, published in July 2009.

Operating Environment

This factor is common to all French banks. For detailed discussion of the French operating environment, please refer to Moody's latest Banking System Outlook on France, published in July 2009.

We note that the proportion of earnings stemming from and the ratio of assets located in foreign countries increased in late 2008/early 2009, following the acquisition of Citibank Deutschland and Cofidis, and the increased stake in BMCE.

Moody's expectation of deteriorating operating environments in BFCM’s main markets, namely France and Germany, leads to a weakening perspective for the bank's overall operating environment.

Discussion of Quantitative Rating Drivers

Profitability

Satisfactory commercial performance hampered by impairments and increasing cost of risk

Thanks to the stable income generated by retail banking activities and insurance (which accounted for 56.3% and 17.2% of NBI in 2007, respectively), BFCM’s profitability steadily improved from the 2005 trough until 2007.

23 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

In light of the impairments the bank had to book on its structured credit and securities portfolios, the contribution of the financing and markets activities wiped out its net income, which stood at €138 million in 2008 (2007: €1.703 billion). We note that net income would have been negative without the reclassification of assets as permitted under IAS 39 and effective from 1 July 2008 for CIC and BFCM. Following the reclassification, we expect the bank’s earnings to be less severely affected by the mark-to-market fluctuations on its securities and structured credit portfolio going forward.

We expect BFCM’s net interest income (NII) to benefit from the re-pricing of loans and deposits in France and, more marginally, from the consolidation of Citibank Deutschland and Cofidis, both of which charge high interest rates to their customers. However, we do not expect the bank’s pre-provision profit to be restored to pre-crisis levels given the lower appetite for life insurance and mutual funds products, the lower demand for complex products and the strong competition between banks.

Furthermore, we expect the bank’s bottom-line profitability to be hampered by the increased cost of risk, stemming from the deterioration of the macroeconomic environment in the markets where BFCM operates. In addition, the cost of risk will mechanically remain higher because of the higher proportion of consumer-lending activities since the consolidation of Citibank Deutschland and Cofidis.

Liquidity

A reflection of BFCM’s role in managing CM5-CIC group’s liquidity

Although the bulk of BFCM’s activities are geared towards retail banking and insurance, the bank is heavily reliant on market funding. This is mainly explained by BFCM’s role as the liquidity manager for the whole CM5-CIC group on behalf of the central body of the group (CFCMCEE), as well as for some of the other Crédit Mutuel federations. BFCM bears the weight of the re-financing of the whole CM5-CIC group on its balance sheet, while it does not consolidate the co-operative networks’ retail deposits. Hence, BFCM’s strong asset growth has only been partly compensated for by on-balance-sheet retail deposits and has resulted in an increasing recourse to market funding.

Unlike Cofidis, which was historically a wholesale funding institution, Citibank Deutschland collects deposits in addition to servicing consumer loans. We estimate that the consolidation of Citibank Deutschland, unlike that of Cofidis, has been overall neutral for the bank’s liquidity position.

Exhibit 6

Market Funds - Liquid Assets Ratio (%)

-3.43

0.34

2.36

-1.06-2.05

-4.00

-3.00

-2.00

-1.00

0.00

1.00

2.00

3.00

2005 2006 2007 2008 H1-2009

Source: Moody's

At end-June 2009, BFCM’s main sources of funding were:

Customer deposits (30.4% of total funding);

Interbank (28.5%);

24 August 2009 Credit Analysis Moody’s Global Banking – Banque Fédérative du Crédit Mutuel

Credit Analysis Moody’s Global Banking

Banque Fédérative du Crédit Mutuel

Market funding (39.7%); and

Subordinated debt (1.4%).

These are balance-sheet figures at end-June 2009, relative to the sum of all four items (source: Moody's Investors Service).

BFCM benefits from a high proportion of marketable securities and pledgeable assets (at end-June 2009, liquid assets41 accounted for 55% of total assets).

Capital Adequacy

We estimate capitalisation to be satisfactory, although it is not publicly disclosed

Moody's views BFCM's capital adequacy as satisfactory. However, the lack of disclosure at the level of BFCM does not provide us with a fair and complete picture of the bank's solvency. The French regulator focuses on CM5-CIC's consolidated capital adequacy levels rather than on BFCM's own consolidated capital adequacy figures.

At the CIC level, which accounted for around 56% of BFCM's total assets at end-June 2009 and which undertakes market activities,42 the Tier 1 ratio was 9.1% at end-March 2009.43

BFCM issued a titre super subordonné à durée indéterminée (TSSDI – French deeply subordinated debt) in late 2008 in order to finance the acquisition of Cofidis Participations. This TSSDI was subscribed by GACM.

We also note that the Crédit Mutuel group, like other French banking groups, benefited from a capital injection from the French government through its Société de Prises de Participations de l’Etat (SPPE), a vehicle established in October 2008.

Out of the total €1.2 billion allocated to Crédit Mutuel group for the first issuance of SPPE,44 the bulk was streamlined to CM5-CIC. CM5-CIC announced that it would not tap the second tranche of SPPE. In our analysis of BFCM, we take the whole amount into account as it is our understanding that CM5 (i.e. the retail part of CM5-CIC not consolidated under BFCM) has high capital adequacy when looked at on a stand-alone basis.

Efficiency

Will not be restored to pre-crisis levels in the short-to-medium term

After several years of relative stability, BFCM’s efficiency deteriorated in 2008 when the cost-to-income ratio stood at 80.9%. Admittedly, this indicator was hampered by the mark-to-market impairments on the bank’s structured credit and securities portfolios.

The bank’s cost-to-income ratio was of 60.65% in H1 2009, on the back of satisfactory commercial performance, improved NII and the positive contribution of the financing and markets activities. Moody’s views this level as a better reflection of the bank’s recurring efficiency. We understand that the consolidation of Citibank Deutschland and Cofidis might also have a positive impact on the bank’s overall cost-to-income ratio, since they do not have to bear the same level of costs on their network as does the rest of BFCM.

We expect the bank’s efficiency to remain under pressure in the short-to-medium term because of the strong competition in the French banking market and the costs linked to the integration of Citibank Deutschland and Cofidis.