Embed Size (px)

Citation preview

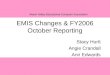

16 pwc

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

• Definition ofimpracticableintroduced(FRS1.11).

• Definition of materialincluded (FRS 1.11).

FRS 1Presentationof FinancialStatements

• Application of FRS is presumed toresult in fair presentation (FRS1.13).

• Use of true and fair override restrictedto extremely rare circumstances wherecompliance will be misleading anddeparture is not prohibited by therelevant regulatory framework(FRS1.17).

• Reclassification of comparatives requiredunless impracticable (FRS 1.40).

• Tightening of requirement for classificationand disclosure of current and non-currentitems on the balance sheet– Current and non-current classification on

the balance sheet except when the liquiditypresentation of assets and liabilitiesprovides information that is reliable andmore relevant than a current/non-currentpresentation (FRS 1.51).

– The following to be classified as currentliability:- liability held primarily for trading

(FRS1.57);- financial liability for which an entity has

no unconditional right to defer settlementfor at least 12 months after the balancesheet date (FRS 1.60); and

- long-term financial liability payable ondemand due to breach(es) on loanagreement on or before the balancesheet date, even if the lender has agreed,after the balance sheet date and beforethe authorisation of the financialstatements for issue, not to demandpayment as a consequence of the breach(FRS 1.65). However, the liability isclassified as non-current if the lenderagreed by the balance sheet date toprovide a period of grace ending at leasttwelve months after the balance sheetdate, within which the entity can rectifythe breach and during which the lendercannot demand immediate repayment(FRS 1.66).

• Investment properties, biological assets andassets held for sale required to be disclosedon the face of the balance sheet (FRS 1.68).

• Deferred tax not included under currentasset/liabilities on the balance sheet (FRS1.70).

• Requires disclosure of results of discontinuedoperations on income statements (FRS 1.81)

• Prohibits disclosure of ‘extraordinary items’on income statement (FRS 1.85).

• Removes the disclosure requirement ofresults of operating activities on the face ofthe income statement and number ofemployees (FRS IN13).

• Requires disclosure of judgements made bymanagement in applying accounting policiesand key assumptions or uncertaintiesaffecting their estimation (FRS 1.113 to 124).

• Minority interest:– allocation of amount between ‘profit or loss

attributable to minority interest’ and ‘profitor loss attributable to equity holders of theparent’ to be shown on the face of incomestatement. The allocated amounts are notto be presented as items of income orexpenses (FRS 1.82).

– total income and expense recogniseddirectly in equity in statement of changes inequity with amounts allocated to minorityinterest and shareholders of parentseparately disclosed (FRS 1.96).

Significant changes on

17Illustrative Annual Report 2005

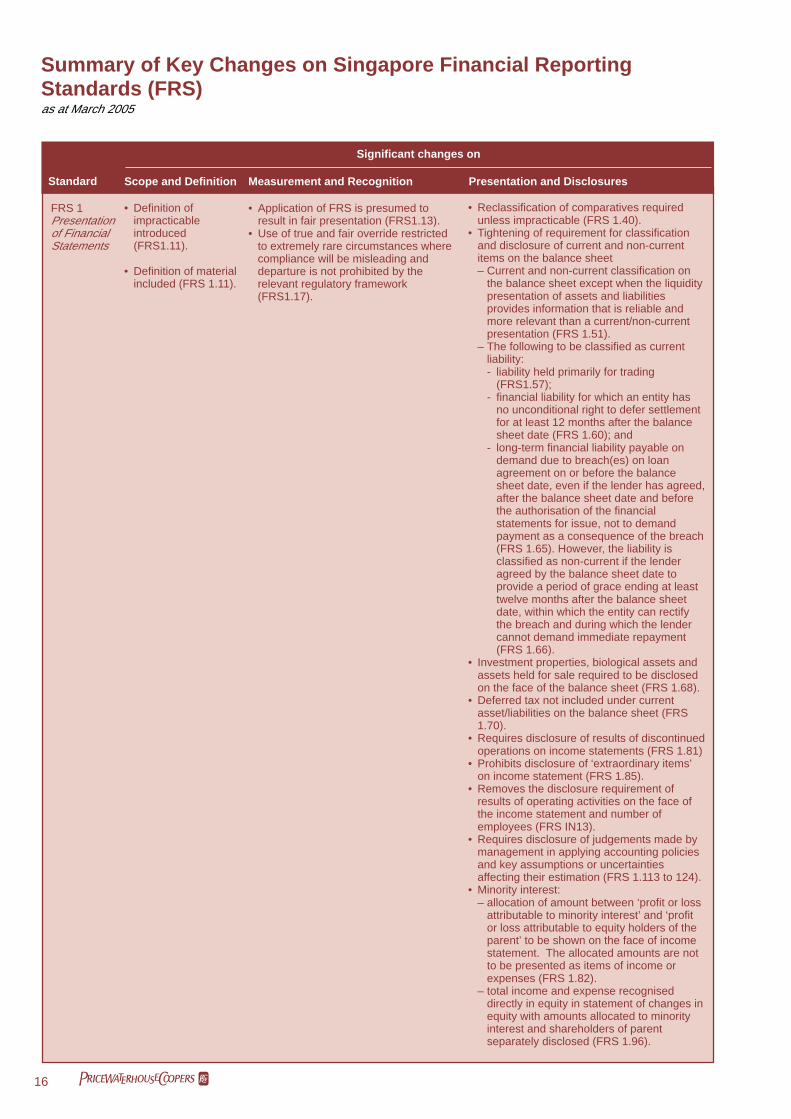

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

• In the objective andscope paragraphs,reference toinventories “heldunder historical costsystem” was deletedto clarify that theStandard applies toall inventories thatare not specificallyexcluded from itsscope (FRS 2.IN5).

• Scope exclusion forcertain inventories(work-in-progressfrom constructioncontracts, financialinstruments andbiological assetsrelated toagricultural activityand produce) areoutside the scope ofthe standard(FRS 2.3).

• FRS 2 measurementrequirements neednot be complied withfor (FRS 2.3):– producers of

agricultural andforest products,agriculturalproduce, andmineral andmineral products ifthey measure theirinventories at netrealisable value;and

– commodity broker-traders if theymeasure theirinventories at fairvalue less coststo sell.

• Incorporates andsupersedes INTFRS 1 requirementto use same costformula forinventories of similarnature and use(FRS 2.25).

FRS 2Inventories

• Difference between net realisable valueand fair value less costs to sell clarified(FRS 2.6).

• Does not permit exchange differencesfrom being included in the costs ofpurchase of inventories (previousversion of FRS 2 allowed inclusion ofcertain foreign exchange differencesarising directly on the acquisition ofinventories.) (FRS 2.IN10).

• Clarifies that when inventories arepurchased with deferred settlementterms, the difference between thepurchase price for normal credit termsand the amount paid shall berecognised as interest expense overthe period of financing (FRS 2.18).

• Describes circumstances that wouldtrigger a reversal of a write-down ofinventories recognised in a prior period(FRS 2.33).

• Matching principle eliminated(FRS 2.IN14).

• Requires disclosure of carrying amounts ofinventories carried at fair value less costs tosell (FRS 2.36).

• Requires disclosure of amount of write-downof inventories included as an expense(FRS 2.36).

• Eliminates the requirement to disclose theamount of inventories carried at netrealisable value (FRS 2.IN17).

Significant changes on

18 pwc

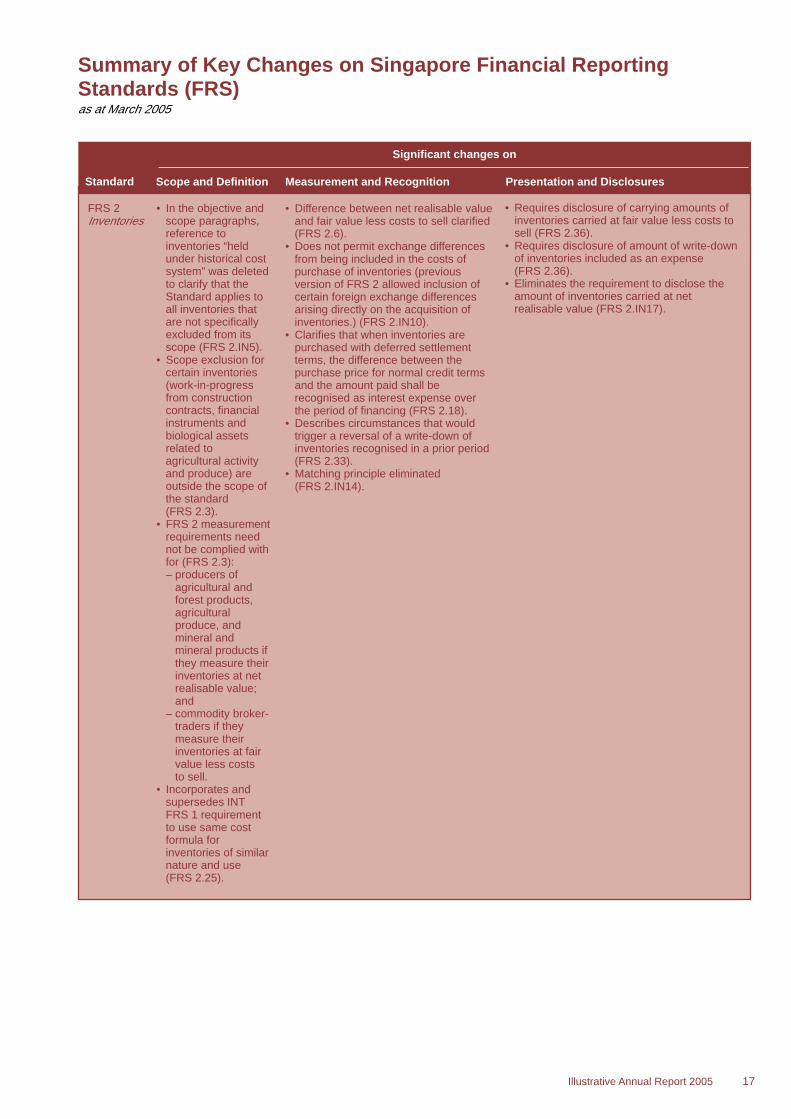

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

Significant changes on

• Updates the hierarchy of guidance forselecting accounting policies in theabsence of standards andinterpretations that specifically apply(FRS 8.7 to 12, 21). In such situations,management should use its judgementto develop relevant and reliableaccounting policies, considering thefollowing sources in descending order:1. Standards and Interpretations

dealing with similar and relatedissues;

2. definitions, recognition criteria andmeasurement concepts for assets,liabilities, income and expenses inthe Framework; and

3. the most recent pronouncements ofother standard-setting bodies thatuse a similar conceptual framework,other accounting literature, acceptedindustry practices.

• Eliminates the concept of fundamentalerror and thus, the distinction betweenfundamental errors and other materialprior period errors (FRS 8.IN12).

• Removes alternative to include, in thecurrent period income statement, thecumulative effect of a voluntary changein accounting policy or a correction oferror; retrospective application isrequired (FRS 8.41 to 48). However,when it is impracticable to determinethe effect of applying a new accountingpolicy to all prior periods, the standardallows the policy to be appliedprospectively from the earliest datepracticable (FRS 8.24 to 27).

• Clarifies that dividends declared afterthe balance sheet date shall not berecognised as a liability at the balancesheet date (FRS 10.12).

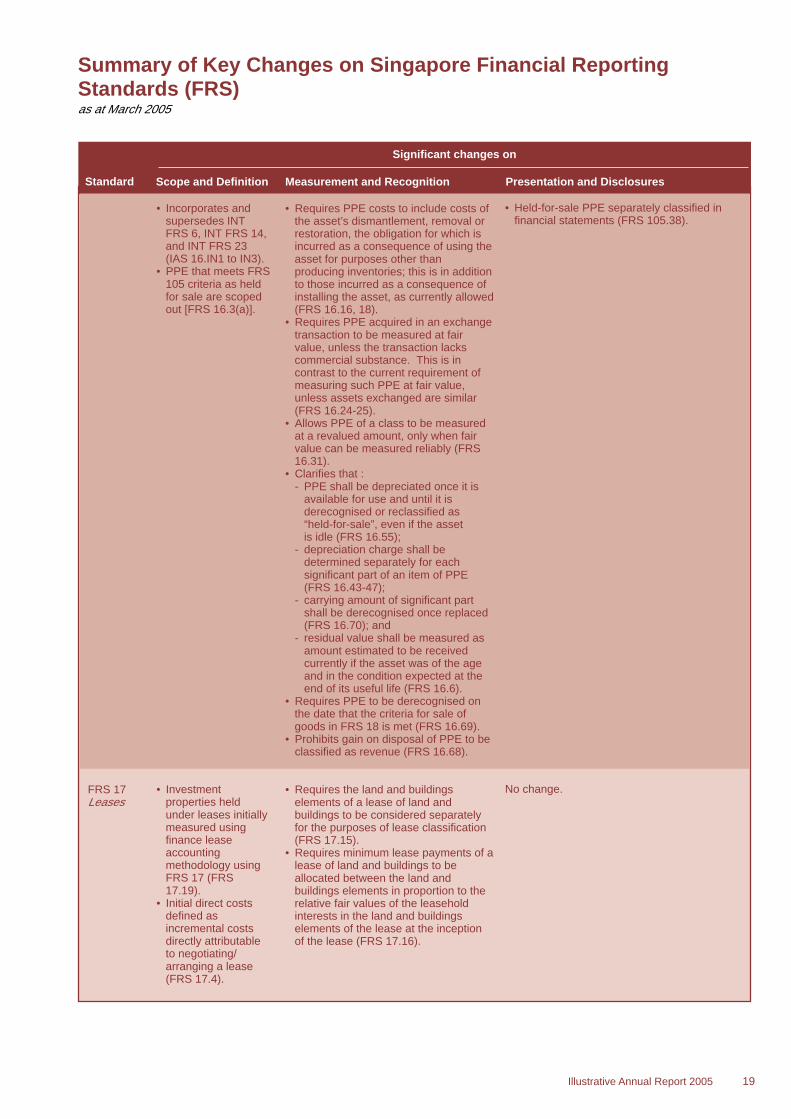

• Removes separate recognition principlefor subsequent expenditure; all PPEcosts (whether incurred initially toacquire or construct the asset, orincurred subsequently to add to,replace part of or service the asset)shall be capitalised when it is probablethat future economic benefitsassociated with the item will flow to theentity and the cost of the item can bemeasured reliably (FRS 16.IN6,FRS 16.7)

• Requires the disclosure of impending changein accounting policy from a new standard orinterpretation that has been issued but notyet effective, and its possible impact(FRS 8.30 to 31).

• More detailed disclosures of effect ofchanges of policies and errors required(including the effect on each line item and onbasic and diluted earnings per share)(FRS 8.28 to 31, 49).

• The disclosure requirements regardingextraordinary items in the old FRS 8 hasbeen removed. Extraordinary items are nolonger allowed in the income statement(FRS 1.85).

No change.

• Prior-year comparatives for PPE mandatory[FRS 16.73(e)].

• Additional disclosures for revalued assets(FRS 16.77):- the methods and significant assumptions

applied in estimating the items’ fair values;- the extent to which the items’ fair values

were determined directly by reference toobservable prices in an active market orrecent market transactions on arm’s lengthterms or were estimated using othervaluation techniques.

• Name of standardchanged from “Profitor Loss for thePeriod, FundamentalErrors and Changesin AccountingPolicies”.

• Defines (FRS 8.5):- material omissions

or misstatements;- impracticable;- prior period errors;- change in

accountingestimates.

• Changes toaccounting policiesfrom adopting FRSscoped out of FRS 8(FRS 101.42).

• Incorporates andsupersedesINT FRS 2 andINT FRS 18.

• Selection ofaccounting policiestransferred fromFRS 1 (FRS 8.7to 12).

No change.

• FRS 15, iswithdrawn from1 January 2005.

• Clarifies that thestandard applies toProperty, Plant andEquipment (“PPE”)used to develop ormaintain biologicalassets, mineral rightsand mineral reserves(FRS 16.3).

FRS 8AccountingPolicies,Changes inAccountingEstimatesand Errors

FRS 10Events afterthe BalanceSheet Date

FRS 15InformationReflecting theEffects ofChangingPrices

FRS 16Property,Plant andEquipment

19Illustrative Annual Report 2005

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

• Incorporates andsupersedes INTFRS 6, INT FRS 14,and INT FRS 23(IAS 16.IN1 to IN3).

• PPE that meets FRS105 criteria as heldfor sale are scopedout [FRS 16.3(a)].

• Investmentproperties heldunder leases initiallymeasured usingfinance leaseaccountingmethodology usingFRS 17 (FRS17.19).

• Initial direct costsdefined asincremental costsdirectly attributableto negotiating/arranging a lease(FRS 17.4).

FRS 17Leases

• Requires PPE costs to include costs ofthe asset’s dismantlement, removal orrestoration, the obligation for which isincurred as a consequence of using theasset for purposes other thanproducing inventories; this is in additionto those incurred as a consequence ofinstalling the asset, as currently allowed(FRS 16.16, 18).

• Requires PPE acquired in an exchangetransaction to be measured at fairvalue, unless the transaction lackscommercial substance. This is incontrast to the current requirement ofmeasuring such PPE at fair value,unless assets exchanged are similar(FRS 16.24-25).

• Allows PPE of a class to be measuredat a revalued amount, only when fairvalue can be measured reliably (FRS16.31).

• Clarifies that :- PPE shall be depreciated once it is

available for use and until it isderecognised or reclassified as“held-for-sale”, even if the assetis idle (FRS 16.55);

- depreciation charge shall bedetermined separately for eachsignificant part of an item of PPE(FRS 16.43-47);

- carrying amount of significant partshall be derecognised once replaced(FRS 16.70); and

- residual value shall be measured asamount estimated to be receivedcurrently if the asset was of the ageand in the condition expected at theend of its useful life (FRS 16.6).

• Requires PPE to be derecognised onthe date that the criteria for sale ofgoods in FRS 18 is met (FRS 16.69).

• Prohibits gain on disposal of PPE to beclassified as revenue (FRS 16.68).

• Requires the land and buildingselements of a lease of land andbuildings to be considered separatelyfor the purposes of lease classification(FRS 17.15).

• Requires minimum lease payments of alease of land and buildings to beallocated between the land andbuildings elements in proportion to therelative fair values of the leaseholdinterests in the land and buildingselements of the lease at the inceptionof the lease (FRS 17.16).

• Held-for-sale PPE separately classified infinancial statements (FRS 105.38).

No change.

Significant changes on

20 pwc

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

Significant changes on

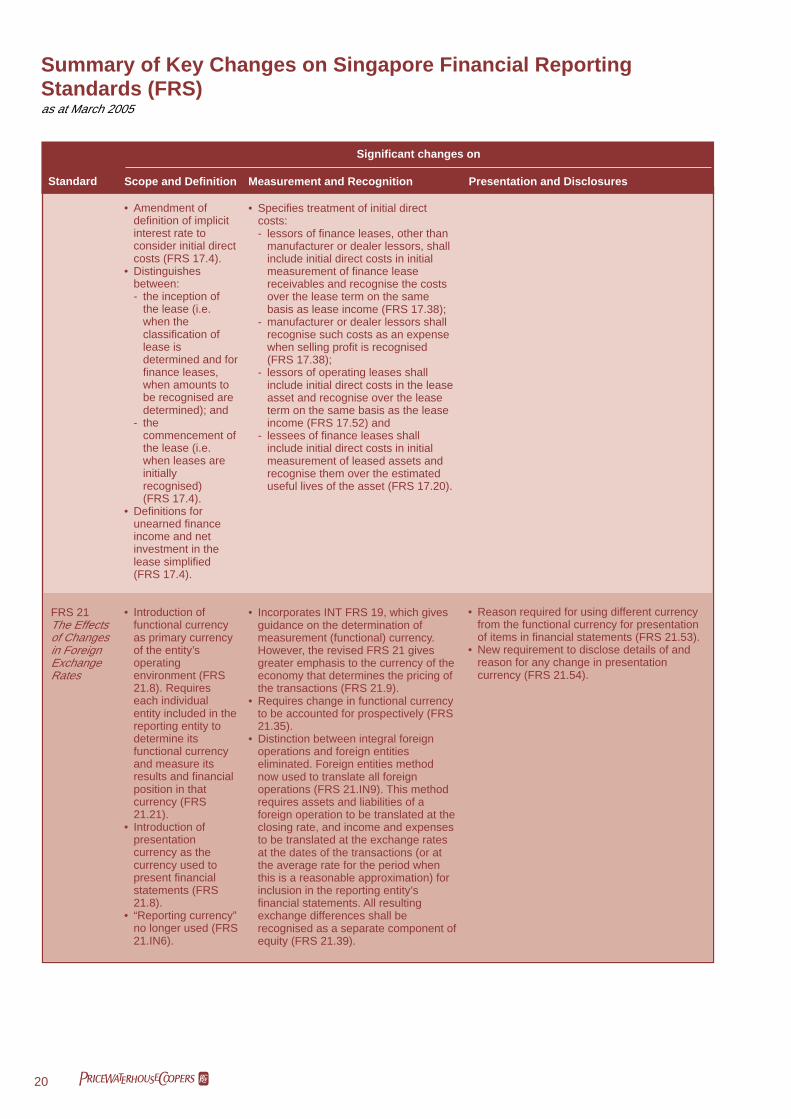

• Specifies treatment of initial directcosts:- lessors of finance leases, other than

manufacturer or dealer lessors, shallinclude initial direct costs in initialmeasurement of finance leasereceivables and recognise the costsover the lease term on the samebasis as lease income (FRS 17.38);

- manufacturer or dealer lessors shallrecognise such costs as an expensewhen selling profit is recognised(FRS 17.38);

- lessors of operating leases shallinclude initial direct costs in the leaseasset and recognise over the leaseterm on the same basis as the leaseincome (FRS 17.52) and

- lessees of finance leases shallinclude initial direct costs in initialmeasurement of leased assets andrecognise them over the estimateduseful lives of the asset (FRS 17.20).

• Incorporates INT FRS 19, which givesguidance on the determination ofmeasurement (functional) currency.However, the revised FRS 21 givesgreater emphasis to the currency of theeconomy that determines the pricing ofthe transactions (FRS 21.9).

• Requires change in functional currencyto be accounted for prospectively (FRS21.35).

• Distinction between integral foreignoperations and foreign entitieseliminated. Foreign entities methodnow used to translate all foreignoperations (FRS 21.IN9). This methodrequires assets and liabilities of aforeign operation to be translated at theclosing rate, and income and expensesto be translated at the exchange ratesat the dates of the transactions (or atthe average rate for the period whenthis is a reasonable approximation) forinclusion in the reporting entity’sfinancial statements. All resultingexchange differences shall berecognised as a separate component ofequity (FRS 21.39).

• Reason required for using different currencyfrom the functional currency for presentationof items in financial statements (FRS 21.53).

• New requirement to disclose details of andreason for any change in presentationcurrency (FRS 21.54).

• Amendment ofdefinition of implicitinterest rate toconsider initial directcosts (FRS 17.4).

• Distinguishesbetween:- the inception of

the lease (i.e.when theclassification oflease isdetermined and forfinance leases,when amounts tobe recognised aredetermined); and

- thecommencement ofthe lease (i.e.when leases areinitiallyrecognised)(FRS 17.4).

• Definitions forunearned financeincome and netinvestment in thelease simplified(FRS 17.4).

• Introduction offunctional currencyas primary currencyof the entity’soperatingenvironment (FRS21.8). Requireseach individualentity included in thereporting entity todetermine itsfunctional currencyand measure itsresults and financialposition in thatcurrency (FRS21.21).

• Introduction ofpresentationcurrency as thecurrency used topresent financialstatements (FRS21.8).

• “Reporting currency”no longer used (FRS21.IN6).

FRS 21The Effectsof Changesin ForeignExchangeRates

21Illustrative Annual Report 2005

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

• Requirements forhedge accountingand foreign currencyderivatives moved toFRS 39 (FRS21.IN5).

• Incorporates andsupersedes INTFRS 11, INT FRS 19and INT FRS 30(FRS 21.IN1).

• Does not permit limited option in theprevious version to capitalise exchangedifferences resulting from a severe devaluationor depreciation of a currency against whichthere is no means of hedging; such exchangedifferences shall be recognised in profit or loss(FRS 21.IN10).

• Presentation of financial statementspermitted in any currency (FRS 21.38).

• Requires an entity to translate its resultsand financial position from its functionalcurrency into a presentation currency using themethod required for translating a foreignoperation for inclusion in the reporting entity’sfinancial statements (FRS 21.39).

• For an entity whose functional currency isthe currency of a hyperinflationary economy:- If the results and financial position are

translated into the currency of a differenthyperinflationary economy, all amounts (e.g.balance sheet and income statementamounts, including comparatives) aretranslated at the closing rate of the mostrecent balance sheet presented [(FRS21.42(a)].

- If the results and financial position aretranslated into the currency of a non-hyperinflationary economy, comparativeamounts are those presented in the relevantprior year financial statements [FRS 21.42(b)].

• Requires goodwill and fair valueadjustments to assets and liabilities arising fromthe acquisition of foreign entity to be expressedin acquiree’s currency and translated usingclosing rates (FRS 21.47).

• Requires exchange differences arising ona monetary item that forms part of a reportingentity’s net investment in a foreign operation tobe recognised in profit and loss (FRS 21.32).However, such exchange differences arerequired to be recognised as a separatecomponent of equity in the consolidatedaccounts only, provided the following conditionsare met:- settlement is neither planned nor likely

to occur in the foreseeable future(FRS 21.15);

- the monetary item is not a tradereceivable or payable (FRS 21.15);

- the monetary item is denominated ineither the functional currency of the reportingentity or the foreign operation (FRS 21.33);

- the monetary item must be areceivable/payable between the reportingentity and the foreign operation that is thesubsidiary/associate/joint venture/branch ofthe reporting entity (FRS 21.8, 21.15). E.g.exchange differences arising on a loan from asubsidiary to a fellow subsidiary that is aforeign operation cannot be taken to equity.

Significant changes on

22 pwc

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

Significant changes on

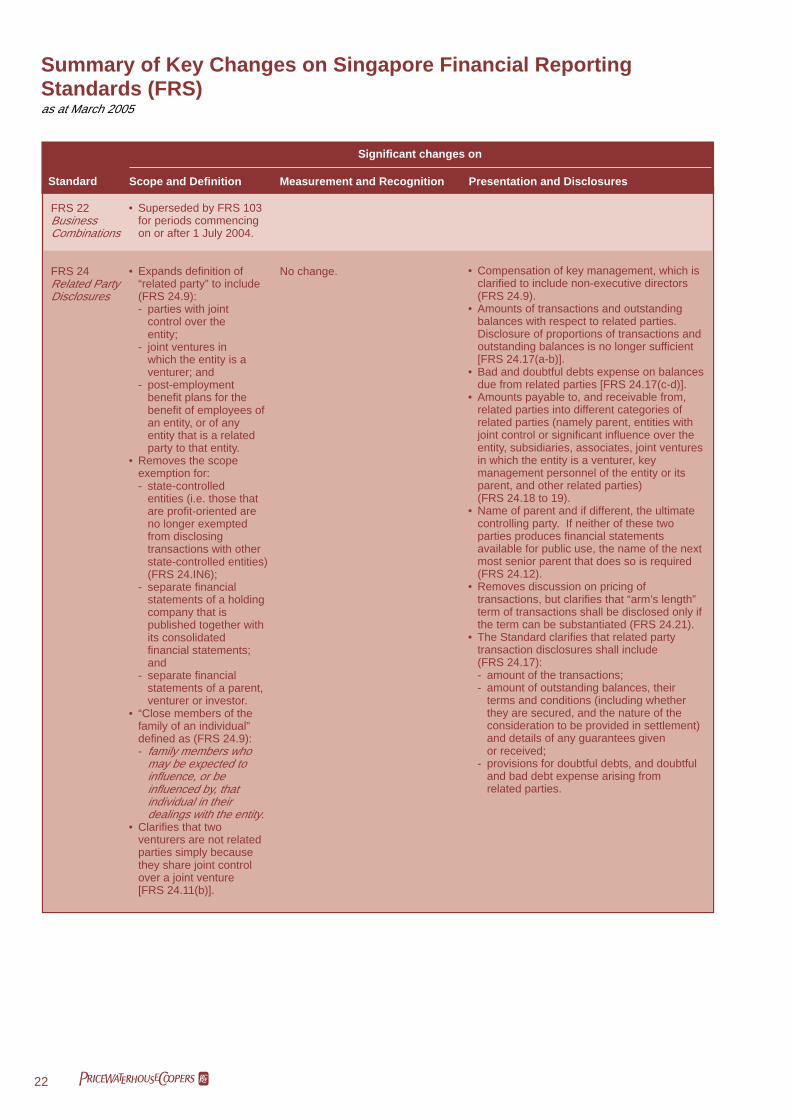

No change. • Compensation of key management, which isclarified to include non-executive directors(FRS 24.9).

• Amounts of transactions and outstandingbalances with respect to related parties.Disclosure of proportions of transactions andoutstanding balances is no longer sufficient[FRS 24.17(a-b)].

• Bad and doubtful debts expense on balancesdue from related parties [FRS 24.17(c-d)].

• Amounts payable to, and receivable from,related parties into different categories ofrelated parties (namely parent, entities withjoint control or significant influence over theentity, subsidiaries, associates, joint venturesin which the entity is a venturer, keymanagement personnel of the entity or itsparent, and other related parties)(FRS 24.18 to 19).

• Name of parent and if different, the ultimatecontrolling party. If neither of these twoparties produces financial statementsavailable for public use, the name of the nextmost senior parent that does so is required(FRS 24.12).

• Removes discussion on pricing oftransactions, but clarifies that “arm’s length”term of transactions shall be disclosed only ifthe term can be substantiated (FRS 24.21).

• The Standard clarifies that related partytransaction disclosures shall include(FRS 24.17):- amount of the transactions;- amount of outstanding balances, their

terms and conditions (including whetherthey are secured, and the nature of theconsideration to be provided in settlement)and details of any guarantees givenor received;

- provisions for doubtful debts, and doubtfuland bad debt expense arising fromrelated parties.

• Superseded by FRS 103for periods commencingon or after 1 July 2004.

• Expands definition of“related party” to include(FRS 24.9):- parties with joint

control over theentity;

- joint ventures inwhich the entity is aventurer; and

- post-employmentbenefit plans for thebenefit of employees ofan entity, or of anyentity that is a relatedparty to that entity.

• Removes the scopeexemption for:- state-controlled

entities (i.e. those thatare profit-oriented areno longer exemptedfrom disclosingtransactions with otherstate-controlled entities)(FRS 24.IN6);

- separate financialstatements of a holdingcompany that ispublished together withits consolidatedfinancial statements;and

- separate financialstatements of a parent,venturer or investor.

• “Close members of thefamily of an individual”defined as (FRS 24.9):- family members who

may be expected toinfluence, or beinfluenced by, thatindividual in theirdealings with the entity.

• Clarifies that twoventurers are not relatedparties simply becausethey share joint controlover a joint venture[FRS 24.11(b)].

FRS 22BusinessCombinations

FRS 24Related PartyDisclosures

23Illustrative Annual Report 2005

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

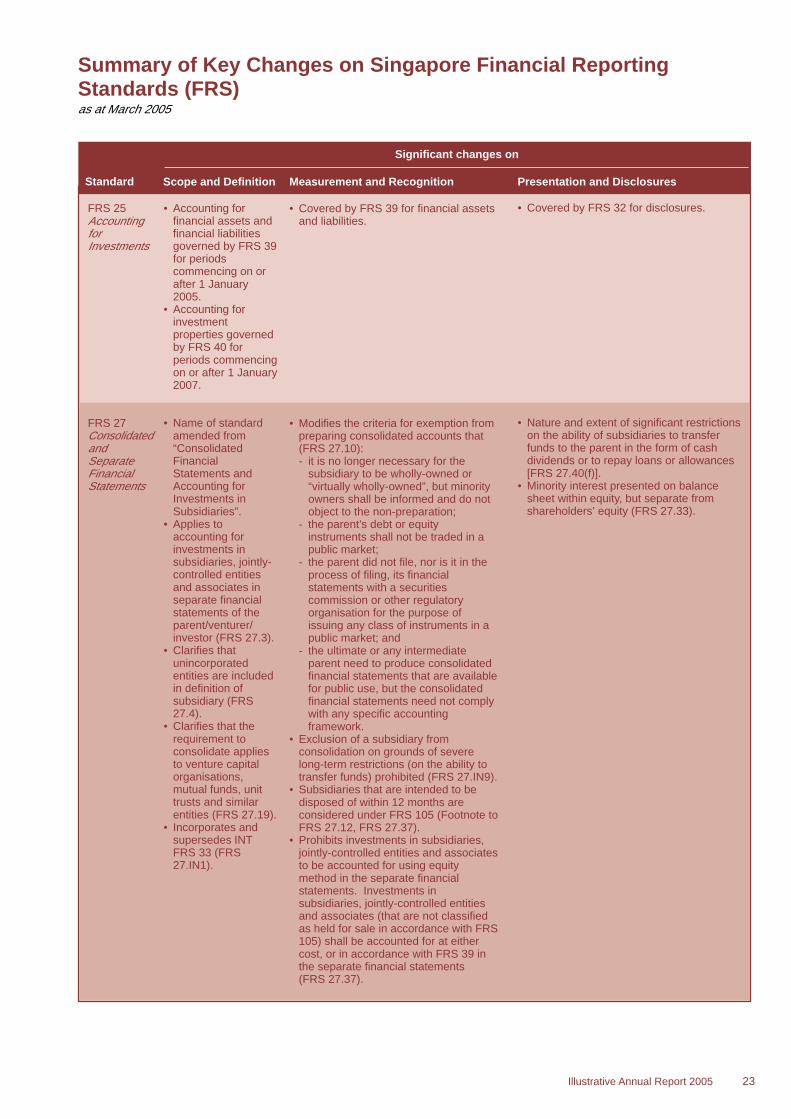

• Accounting forfinancial assets andfinancial liabilitiesgoverned by FRS 39for periodscommencing on orafter 1 January2005.

• Accounting forinvestmentproperties governedby FRS 40 forperiods commencingon or after 1 January2007.

• Name of standardamended from“ConsolidatedFinancialStatements andAccounting forInvestments inSubsidiaries”.

• Applies toaccounting forinvestments insubsidiaries, jointly-controlled entitiesand associates inseparate financialstatements of theparent/venturer/investor (FRS 27.3).

• Clarifies thatunincorporatedentities are includedin definition ofsubsidiary (FRS27.4).

• Clarifies that therequirement toconsolidate appliesto venture capitalorganisations,mutual funds, unittrusts and similarentities (FRS 27.19).

• Incorporates andsupersedes INTFRS 33 (FRS27.IN1).

FRS 25AccountingforInvestments

FRS 27ConsolidatedandSeparateFinancialStatements

• Covered by FRS 39 for financial assetsand liabilities.

• Modifies the criteria for exemption frompreparing consolidated accounts that(FRS 27.10):- it is no longer necessary for the

subsidiary to be wholly-owned or“virtually wholly-owned”, but minorityowners shall be informed and do notobject to the non-preparation;

- the parent’s debt or equityinstruments shall not be traded in apublic market;

- the parent did not file, nor is it in theprocess of filing, its financialstatements with a securitiescommission or other regulatoryorganisation for the purpose ofissuing any class of instruments in apublic market; and

- the ultimate or any intermediateparent need to produce consolidatedfinancial statements that are availablefor public use, but the consolidatedfinancial statements need not complywith any specific accountingframework.

• Exclusion of a subsidiary fromconsolidation on grounds of severelong-term restrictions (on the ability totransfer funds) prohibited (FRS 27.IN9).

• Subsidiaries that are intended to bedisposed of within 12 months areconsidered under FRS 105 (Footnote toFRS 27.12, FRS 27.37).

• Prohibits investments in subsidiaries,jointly-controlled entities and associatesto be accounted for using equitymethod in the separate financialstatements. Investments insubsidiaries, jointly-controlled entitiesand associates (that are not classifiedas held for sale in accordance with FRS105) shall be accounted for at eithercost, or in accordance with FRS 39 inthe separate financial statements(FRS 27.37).

• Covered by FRS 32 for disclosures.

• Nature and extent of significant restrictionson the ability of subsidiaries to transferfunds to the parent in the form of cashdividends or to repay loans or allowances[FRS 27.40(f)].

• Minority interest presented on balancesheet within equity, but separate fromshareholders’ equity (FRS 27.33).

Significant changes on

24 pwc

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

Significant changes on

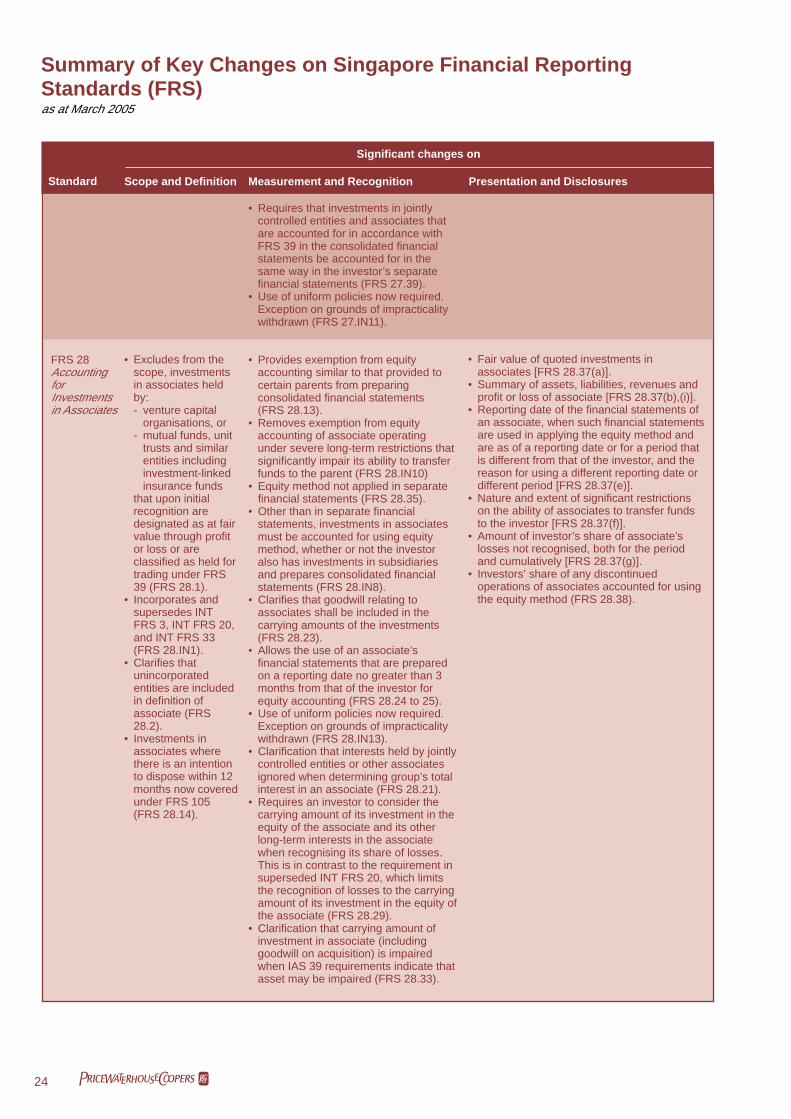

• Requires that investments in jointlycontrolled entities and associates thatare accounted for in accordance withFRS 39 in the consolidated financialstatements be accounted for in thesame way in the investor’s separatefinancial statements (FRS 27.39).

• Use of uniform policies now required.Exception on grounds of impracticalitywithdrawn (FRS 27.IN11).

• Provides exemption from equityaccounting similar to that provided tocertain parents from preparingconsolidated financial statements(FRS 28.13).

• Removes exemption from equityaccounting of associate operatingunder severe long-term restrictions thatsignificantly impair its ability to transferfunds to the parent (FRS 28.IN10)

• Equity method not applied in separatefinancial statements (FRS 28.35).

• Other than in separate financialstatements, investments in associatesmust be accounted for using equitymethod, whether or not the investoralso has investments in subsidiariesand prepares consolidated financialstatements (FRS 28.IN8).

• Clarifies that goodwill relating toassociates shall be included in thecarrying amounts of the investments(FRS 28.23).

• Allows the use of an associate’sfinancial statements that are preparedon a reporting date no greater than 3months from that of the investor forequity accounting (FRS 28.24 to 25).

• Use of uniform policies now required.Exception on grounds of impracticalitywithdrawn (FRS 28.IN13).

• Clarification that interests held by jointlycontrolled entities or other associatesignored when determining group’s totalinterest in an associate (FRS 28.21).

• Requires an investor to consider thecarrying amount of its investment in theequity of the associate and its otherlong-term interests in the associatewhen recognising its share of losses.This is in contrast to the requirement insuperseded INT FRS 20, which limitsthe recognition of losses to the carryingamount of its investment in the equity ofthe associate (FRS 28.29).

• Clarification that carrying amount ofinvestment in associate (includinggoodwill on acquisition) is impairedwhen IAS 39 requirements indicate thatasset may be impaired (FRS 28.33).

• Fair value of quoted investments inassociates [FRS 28.37(a)].

• Summary of assets, liabilities, revenues andprofit or loss of associate [FRS 28.37(b),(i)].

• Reporting date of the financial statements ofan associate, when such financial statementsare used in applying the equity method andare as of a reporting date or for a period thatis different from that of the investor, and thereason for using a different reporting date ordifferent period [FRS 28.37(e)].

• Nature and extent of significant restrictionson the ability of associates to transfer fundsto the investor [FRS 28.37(f)].

• Amount of investor’s share of associate’slosses not recognised, both for the periodand cumulatively [FRS 28.37(g)].

• Investors’ share of any discontinuedoperations of associates accounted for usingthe equity method (FRS 28.38).

• Excludes from thescope, investmentsin associates heldby:- venture capital

organisations, or- mutual funds, unit

trusts and similarentities includinginvestment-linkedinsurance funds

that upon initialrecognition aredesignated as at fairvalue through profitor loss or areclassified as held fortrading under FRS39 (FRS 28.1).

• Incorporates andsupersedes INTFRS 3, INT FRS 20,and INT FRS 33(FRS 28.IN1).

• Clarifies thatunincorporatedentities are includedin definition ofassociate (FRS28.2).

• Investments inassociates wherethere is an intentionto dispose within 12months now coveredunder FRS 105(FRS 28.14).

FRS 28AccountingforInvestmentsin Associates

25Illustrative Annual Report 2005

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

Significant changes on

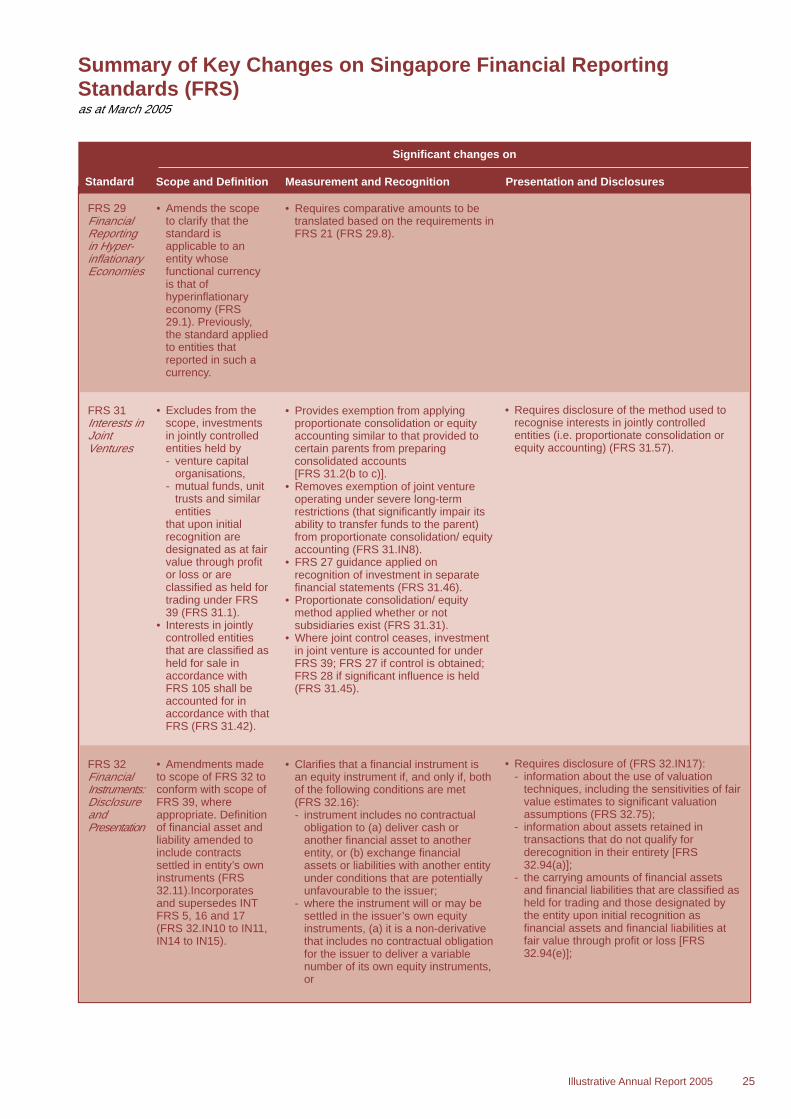

• Amends the scopeto clarify that thestandard isapplicable to anentity whosefunctional currencyis that ofhyperinflationaryeconomy (FRS29.1). Previously,the standard appliedto entities thatreported in such acurrency.

• Excludes from thescope, investmentsin jointly controlledentities held by- venture capital

organisations,- mutual funds, unit

trusts and similarentities

that upon initialrecognition aredesignated as at fairvalue through profitor loss or areclassified as held fortrading under FRS39 (FRS 31.1).

• Interests in jointlycontrolled entitiesthat are classified asheld for sale inaccordance withFRS 105 shall beaccounted for inaccordance with thatFRS (FRS 31.42).

• Amendments madeto scope of FRS 32 toconform with scope ofFRS 39, whereappropriate. Definitionof financial asset andliability amended toinclude contractssettled in entity’s owninstruments (FRS32.11).Incorporatesand supersedes INTFRS 5, 16 and 17(FRS 32.IN10 to IN11,IN14 to IN15).

FRS 29FinancialReportingin Hyper-inflationaryEconomies

FRS 31Interests inJointVentures

FRS 32FinancialInstruments:DisclosureandPresentation

• Requires comparative amounts to betranslated based on the requirements inFRS 21 (FRS 29.8).

• Provides exemption from applyingproportionate consolidation or equityaccounting similar to that provided tocertain parents from preparingconsolidated accounts[FRS 31.2(b to c)].

• Removes exemption of joint ventureoperating under severe long-termrestrictions (that significantly impair itsability to transfer funds to the parent)from proportionate consolidation/ equityaccounting (FRS 31.IN8).

• FRS 27 guidance applied onrecognition of investment in separatefinancial statements (FRS 31.46).

• Proportionate consolidation/ equitymethod applied whether or notsubsidiaries exist (FRS 31.31).

• Where joint control ceases, investmentin joint venture is accounted for underFRS 39; FRS 27 if control is obtained;FRS 28 if significant influence is held(FRS 31.45).

• Clarifies that a financial instrument isan equity instrument if, and only if, bothof the following conditions are met(FRS 32.16):- instrument includes no contractual

obligation to (a) deliver cash oranother financial asset to anotherentity, or (b) exchange financialassets or liabilities with another entityunder conditions that are potentiallyunfavourable to the issuer;

- where the instrument will or may besettled in the issuer’s own equityinstruments, (a) it is a non-derivativethat includes no contractual obligationfor the issuer to deliver a variablenumber of its own equity instruments,or

• Requires disclosure of the method used torecognise interests in jointly controlledentities (i.e. proportionate consolidation orequity accounting) (FRS 31.57).

• Requires disclosure of (FRS 32.IN17):- information about the use of valuation

techniques, including the sensitivities of fairvalue estimates to significant valuationassumptions (FRS 32.75);

- information about assets retained intransactions that do not qualify forderecognition in their entirety [FRS32.94(a)];

- the carrying amounts of financial assetsand financial liabilities that are classified asheld for trading and those designated bythe entity upon initial recognition asfinancial assets and financial liabilities atfair value through profit or loss [FRS32.94(e)];

26 pwc

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

Significant changes on

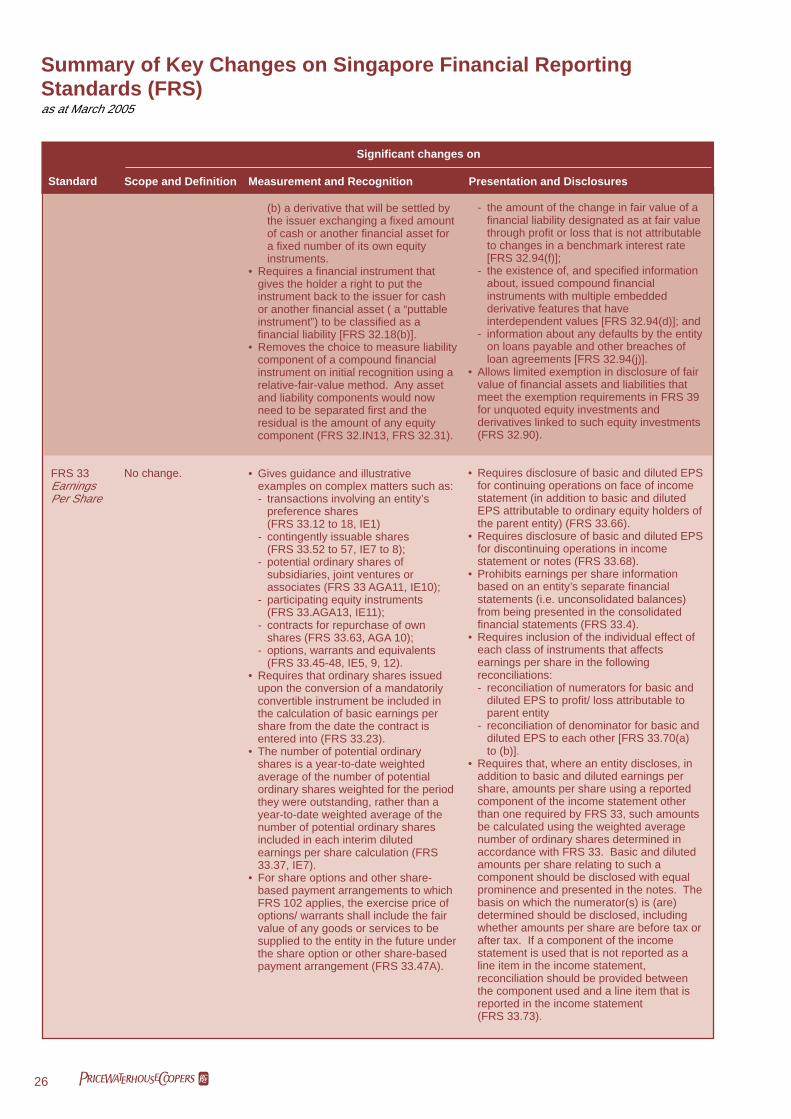

(b) a derivative that will be settled bythe issuer exchanging a fixed amountof cash or another financial asset fora fixed number of its own equityinstruments.

• Requires a financial instrument thatgives the holder a right to put theinstrument back to the issuer for cashor another financial asset ( a “puttableinstrument”) to be classified as afinancial liability [FRS 32.18(b)].

• Removes the choice to measure liabilitycomponent of a compound financialinstrument on initial recognition using arelative-fair-value method. Any assetand liability components would nowneed to be separated first and theresidual is the amount of any equitycomponent (FRS 32.IN13, FRS 32.31).

• Gives guidance and illustrativeexamples on complex matters such as:- transactions involving an entity’s

preference shares(FRS 33.12 to 18, IE1)

- contingently issuable shares(FRS 33.52 to 57, IE7 to 8);

- potential ordinary shares ofsubsidiaries, joint ventures orassociates (FRS 33 AGA11, IE10);

- participating equity instruments(FRS 33.AGA13, IE11);

- contracts for repurchase of ownshares (FRS 33.63, AGA 10);

- options, warrants and equivalents(FRS 33.45-48, IE5, 9, 12).

• Requires that ordinary shares issuedupon the conversion of a mandatorilyconvertible instrument be included inthe calculation of basic earnings pershare from the date the contract isentered into (FRS 33.23).

• The number of potential ordinaryshares is a year-to-date weightedaverage of the number of potentialordinary shares weighted for the periodthey were outstanding, rather than ayear-to-date weighted average of thenumber of potential ordinary sharesincluded in each interim dilutedearnings per share calculation (FRS33.37, IE7).

• For share options and other share-based payment arrangements to whichFRS 102 applies, the exercise price ofoptions/ warrants shall include the fairvalue of any goods or services to besupplied to the entity in the future underthe share option or other share-basedpayment arrangement (FRS 33.47A).

- the amount of the change in fair value of afinancial liability designated as at fair valuethrough profit or loss that is not attributableto changes in a benchmark interest rate[FRS 32.94(f)];

- the existence of, and specified informationabout, issued compound financialinstruments with multiple embeddedderivative features that haveinterdependent values [FRS 32.94(d)]; and

- information about any defaults by the entityon loans payable and other breaches ofloan agreements [FRS 32.94(j)].

• Allows limited exemption in disclosure of fairvalue of financial assets and liabilities thatmeet the exemption requirements in FRS 39for unquoted equity investments andderivatives linked to such equity investments(FRS 32.90).

• Requires disclosure of basic and diluted EPSfor continuing operations on face of incomestatement (in addition to basic and dilutedEPS attributable to ordinary equity holders ofthe parent entity) (FRS 33.66).

• Requires disclosure of basic and diluted EPSfor discontinuing operations in incomestatement or notes (FRS 33.68).

• Prohibits earnings per share informationbased on an entity’s separate financialstatements (i.e. unconsolidated balances)from being presented in the consolidatedfinancial statements (FRS 33.4).

• Requires inclusion of the individual effect ofeach class of instruments that affectsearnings per share in the followingreconciliations:- reconciliation of numerators for basic and

diluted EPS to profit/ loss attributable toparent entity

- reconciliation of denominator for basic anddiluted EPS to each other [FRS 33.70(a)to (b)].

• Requires that, where an entity discloses, inaddition to basic and diluted earnings pershare, amounts per share using a reportedcomponent of the income statement otherthan one required by FRS 33, such amountsbe calculated using the weighted averagenumber of ordinary shares determined inaccordance with FRS 33. Basic and dilutedamounts per share relating to such acomponent should be disclosed with equalprominence and presented in the notes. Thebasis on which the numerator(s) is (are)determined should be disclosed, includingwhether amounts per share are before tax orafter tax. If a component of the incomestatement is used that is not reported as aline item in the income statement,reconciliation should be provided betweenthe component used and a line item that isreported in the income statement(FRS 33.73).

No change.FRS 33EarningsPer Share

27Illustrative Annual Report 2005

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

• Superseded byFRS 105 forperiodscommencing on orafter 1 January2005.

• New term “fairvalue less costs tosell” introduced toreplace “net sellingprice” (FRS 36.6).

• Assets held for saleand disposalgroups arescoped out(FRS 36.2(i), 3).

FRS 35DiscontinuingOperations

FRS 36Impairmentof Assets

• Requires the recoverable amounts ofthe following assets to be measured atleast annually and whenever there is anindication of impairment, rather thanonly when there is an indication ofimpairment (FRS 36.10):- intangible asset with an indefinite

useful life;- intangible asset not yet available for

use; and- goodwill acquired in a business

combination.• Clarifies that the following elements

should be reflected in the calculation ofan asset’s value-in-use (FRS 36.30):- an estimate of the future cash flows

the entity expects to derive fromthe asset;

- expectations about possiblevariations in the amount or timing ofthose future cash flows;

- the time value of money, representedby the current market risk-free rate ofinterest;

- the price for bearing the uncertaintyinherent in the asset; and

• Requires disclosure of instruments (includingcontingently issuable shares) that couldpotentially dilute basic earnings per share inthe future, but were not included in thecalculation of diluted earnings per sharebecause they are anti-dilutive for theperiod(s) presented [FRS 33.70(c)].

• Requires a description of ordinary sharetransactions or potential ordinary sharetransactions occurring after the balancesheet date, other than those accounted for inaccordance with para. 64*, that would havechanged significantly the number of ordinaryshares or potential ordinary sharesoutstanding at the end of the period if thosetransactions had occurred before the end ofthe reporting period [FRS 33.70(d)].

* Mainly bonus issue, share split, reservecapitalisation, reverse share split, or othercapital transactions that require EPS for allperiods presented to be adjustedretrospectively. The accounting anddisclosure requirements for thesetransactions are separately dealt with inpara.64.

• Requires disclosure of amount of goodwillthat has not been allocated to a CGU, andthe reasons why that amount remainsunallocated (FRS 36.133).

• Additional disclosures required ofassumptions used in estimating recoverableamount for CGUs containing goodwill orintangibles with indefinite useful lives(FRS 36.134 to 135).

• Additional disclosures of amount of goodwillallocated to each CGU and, whereappropriate, a declaration that no individualCGU holds a substantial portion(FRS 36.135).

Significant changes on

28 pwc

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

Significant changes on

- other factors, such as illiquidity, thatmarket participants would reflect inpricing the future cash flows the entityexpects to derive from the asset.

• Clarifies that cash flow projections usedto measure value-in-use should excludecash flows that are expected to arisefrom- a future restructuring to which an

entity is not yet committed, or- improving/ enhancing the asset’s

performance (FRS 36.44).• Provides guidance on present value

techniques (FRS 36.A1 to A21).• If output from a cash-generating unit is

consumed internally, the standardrequires value-in-use of all CGUsaffected by the internal transfer pricing tobe based on cash flows determined frommanagement’s best estimate of futurearm’s-length price(s) (instead of theinternal transfer prices)(FRS 36.70).

• Requires that in projecting cash flowsto determine value-in-use, managementshould examine and take into accountcauses of differences between past cashflow projections and actual cash flows,and should ensure that, whereappropriate, current assumptions shouldbe consistent with actual past outcomes(FRS 36.IN7, FRS36.34).

• Requires that goodwill should, from theacquisition date, be allocated to each ofthe acquirer’s cash-generating units(CGUs), or groups of CGUs, that areexpected to benefit from the synergies ofthe business combination, irrespective ofwhether other assets or liabilities of theacquiree are assigned to those units orgroups of units (FRS 36.80).

• Each unit or group of units to which thegoodwill is so allocated should (1)represent the lowest level within theentity at which the goodwill is monitoredfor internal management purposes; and(2) not be larger than a segment basedon either the entity’s primary or entity’ssecondary reporting format determined inaccordance with FRS 14(FRS 36.80).

• Requires that goodwill allocation shouldbe completed before end of the firstannual period beginning after theacquisition date (FRS 36.IN12, 36.84).

• Requires that when an entity disposesof an operation within a cash-generatingunit (group of units) to which goodwillhas been allocated, the goodwillassociated with that operation should be:

29Illustrative Annual Report 2005

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

(i) included in the carrying amount ofthe operation when determining thegain or loss on disposal; and

(ii)measured on the basis of the relativevalues of the operation disposed ofand the portion of the cash-generatingunit (group of units) retained, unlessthe entity can demonstrate that someother method better reflects thegoodwill associated with the operationdisposed of (FRS 36.86).

• Requires that when an entityreorganises its reporting structure in amanner that changes the composition ofcash-generating units (groups of units) towhich goodwill has been allocated, thegoodwill should be reallocated to theunits (groups of units) affected. Thisreallocation should be performed using arelative value approach similar to thatused when an entity disposes of anoperation within a cash-generating unit(group of units), unless the entity candemonstrate that some other methodbetter reflects the goodwill associatedwith the reorganised units (groups ofunits) (FRS 36.87).

• Allows annual impairment test for aCGU (groups of units) to which goodwillhas been allocated to be performed atany time during an annual reportingperiod, provided the test is performed atthe same time every year (FRS 36.96).

• Allows different CGUs (groups of units)to be tested for impairment at differenttimes (FRS 36.96).

• The Standard permits the most recentdetailed calculation made in a precedingperiod of the recoverable amount of acash-generating unit (group of units) towhich goodwill has been allocated to beused in the impairment test for that unit(group of units) in the current period,provided specified criteria are met (FRS36.99).

• Prohibits reversal of impairment lossesfor goodwill recognised in previousperiod(s) (FRS 36.124).

Significant changes on

30 pwc

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

Significant changes on

• Clarifies that an asset meets theidentifiability criterion in the definition of anintangible asset when it is separable orarises from contractual or other legal rights(FRS 38.12).

• Clarifies that the probability recognitioncriterion is always considered to besatisfied for intangible assets that areacquired separately or in a businesscombination (FRS 38.33).

• Introduction of rebuttable presumptionthat the fair value of an intangible assetwith a finite life can be measured reliably ifacquired in a business combination(FRS 38.35 to 41).

• Requires subsequent expenditure onan in-process research and developmentproject acquired in a business combinationto be recognised as:- an expense when incurred if it is

research expenditure or developmentexpenditure that does not satisfy therecognition criteria in FRS 38.

- an intangible asset when incurred if itis development expenditure that satisfiesrecognition criteria in FRS 38(FRS 38.42 to 43)

• Removes the rebuttable assumptionthat the useful life of an intangible assetcannot exceed 20 years from the date theasset is available for use (FRS 38.IN12).

• Regards an intangible asset to haveindefinite useful life when, based on ananalysis of all the relevant factors, there isno foreseeable limit to the period overwhich the asset is expected to generate netcash inflows for the entity (FRS 38.88).

• For contractual/ legal rights that have alimited term but can be renewed, the usefullife should include the renewal period(s)only if there is evidence to support renewalby the entity without significant cost(FRS 38.94).

• An intangible asset with an indefiniteuseful life is not amortised but tested forimpairment annually or whenever there isindicator of impairment(FRS 38.107 to 108).

• The useful life of an intangible assetwith an indefinite life to be reviewed eachreporting period to determine whetherevents and circumstances continue tosupport an indefinite useful life assessmentfor that asset. A change in the useful lifeassessment from indefinite to finite shouldbe accounted for as a change inaccounting estimate under FRS 8(FRS 38.109).

• Reassessing the useful life of anintangible asset as finite rather thanindefinite is an indicator that the asset maybe impaired (FRS 38.110).

• Carrying amount of intangible assetswith indefinite useful lives[FRS 38.122(a)].

• Reasons supporting the indefiniteuseful life assessment, including adescription of the factor(s) that played asignificant role in determining that theasset has an indefinite useful life [FRS38.122(a)].

• Comparative information for thereconciliation of opening and closingbalances for each class of intangibleassets is now required [FRS 38.118(e)].

• Within the reconciliation of opening andclosing balances for each class ofintangible assets, disclosure is requiredof any movements in intangibles arisingfrom classifying the assets as held forsale or including the assets in adisposal group classified as held forsale in accordance with FRS 105 [FRS38.118e(ii)].

• Methods and significant assumptionsapplied in estimating the fair values ofintangible assets accounted for usingthe revaluation model [FRS 124(c)].

FRS 38IntangibleAssets

• Removes therequirement forasset to be held foruse in theproduction or supplyof goods or services,for rental to others,or for administrativepurposes from thedefinition ofintangible asset(FRS 38.IN5,FRS 38.7).

• Intangible thatmeets FRS 105criteria as held forsale scoped out[FRS 38.3(h)].

• Deferred acquisitioncosts andintangibles arisingfrom insurer’scontractual rightsunder an insurancecontract withinscope of FRS 104[FRS 38.3(g)].

31Illustrative Annual Report 2005

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

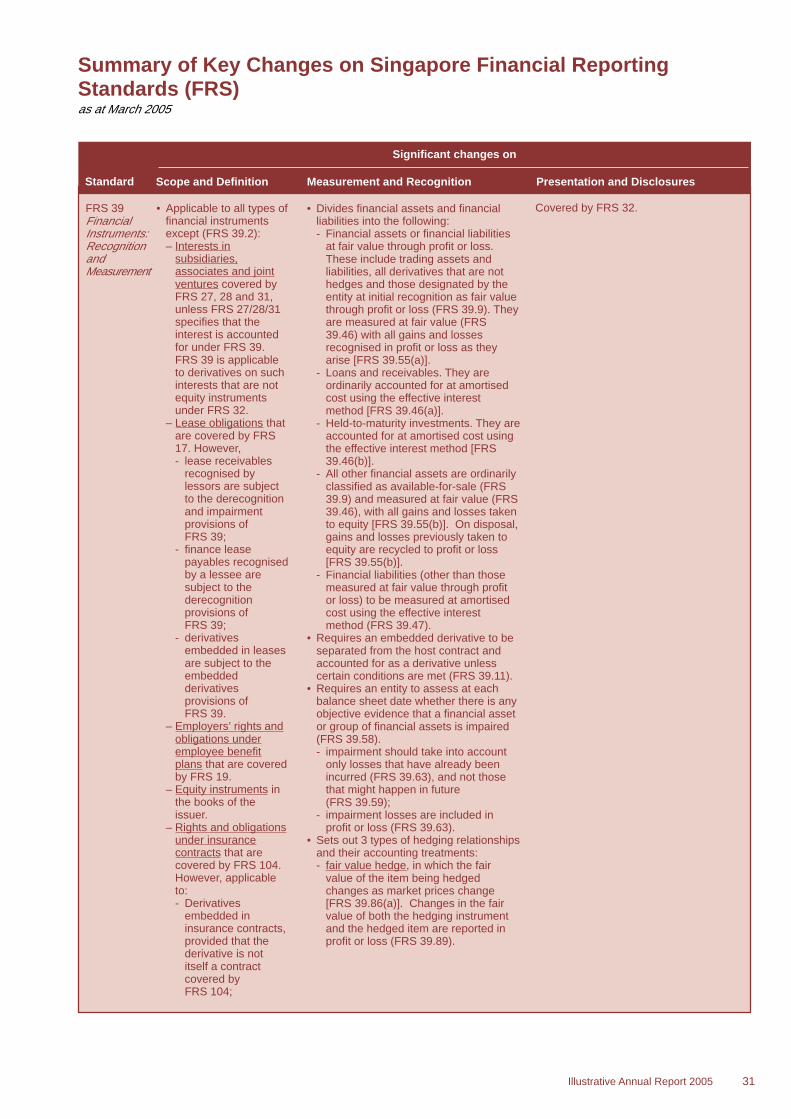

• Applicable to all types offinancial instrumentsexcept (FRS 39.2):– Interests in

subsidiaries,associates and jointventures covered byFRS 27, 28 and 31,unless FRS 27/28/31specifies that theinterest is accountedfor under FRS 39.FRS 39 is applicableto derivatives on suchinterests that are notequity instrumentsunder FRS 32.

– Lease obligations thatare covered by FRS17. However,- lease receivables

recognised bylessors are subjectto the derecognitionand impairmentprovisions ofFRS 39;

- finance leasepayables recognisedby a lessee aresubject to thederecognitionprovisions ofFRS 39;

- derivativesembedded in leasesare subject to theembeddedderivativesprovisions ofFRS 39.

– Employers’ rights andobligations underemployee benefitplans that are coveredby FRS 19.

– Equity instruments inthe books of theissuer.

– Rights and obligationsunder insurancecontracts that arecovered by FRS 104.However, applicableto:- Derivatives

embedded ininsurance contracts,provided that thederivative is notitself a contractcovered byFRS 104;

FRS 39FinancialInstruments:RecognitionandMeasurement

• Divides financial assets and financialliabilities into the following:- Financial assets or financial liabilities

at fair value through profit or loss.These include trading assets andliabilities, all derivatives that are nothedges and those designated by theentity at initial recognition as fair valuethrough profit or loss (FRS 39.9). Theyare measured at fair value (FRS39.46) with all gains and lossesrecognised in profit or loss as theyarise [FRS 39.55(a)].

- Loans and receivables. They areordinarily accounted for at amortisedcost using the effective interestmethod [FRS 39.46(a)].

- Held-to-maturity investments. They areaccounted for at amortised cost usingthe effective interest method [FRS39.46(b)].

- All other financial assets are ordinarilyclassified as available-for-sale (FRS39.9) and measured at fair value (FRS39.46), with all gains and losses takento equity [FRS 39.55(b)]. On disposal,gains and losses previously taken toequity are recycled to profit or loss[FRS 39.55(b)].

- Financial liabilities (other than thosemeasured at fair value through profitor loss) to be measured at amortisedcost using the effective interestmethod (FRS 39.47).

• Requires an embedded derivative to beseparated from the host contract andaccounted for as a derivative unlesscertain conditions are met (FRS 39.11).

• Requires an entity to assess at eachbalance sheet date whether there is anyobjective evidence that a financial assetor group of financial assets is impaired(FRS 39.58).- impairment should take into account

only losses that have already beenincurred (FRS 39.63), and not thosethat might happen in future(FRS 39.59);

- impairment losses are included inprofit or loss (FRS 39.63).

• Sets out 3 types of hedging relationshipsand their accounting treatments:- fair value hedge, in which the fair

value of the item being hedgedchanges as market prices change[FRS 39.86(a)]. Changes in the fairvalue of both the hedging instrumentand the hedged item are reported inprofit or loss (FRS 39.89).

Covered by FRS 32.

Significant changes on

32 pwc

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

Significant changes on

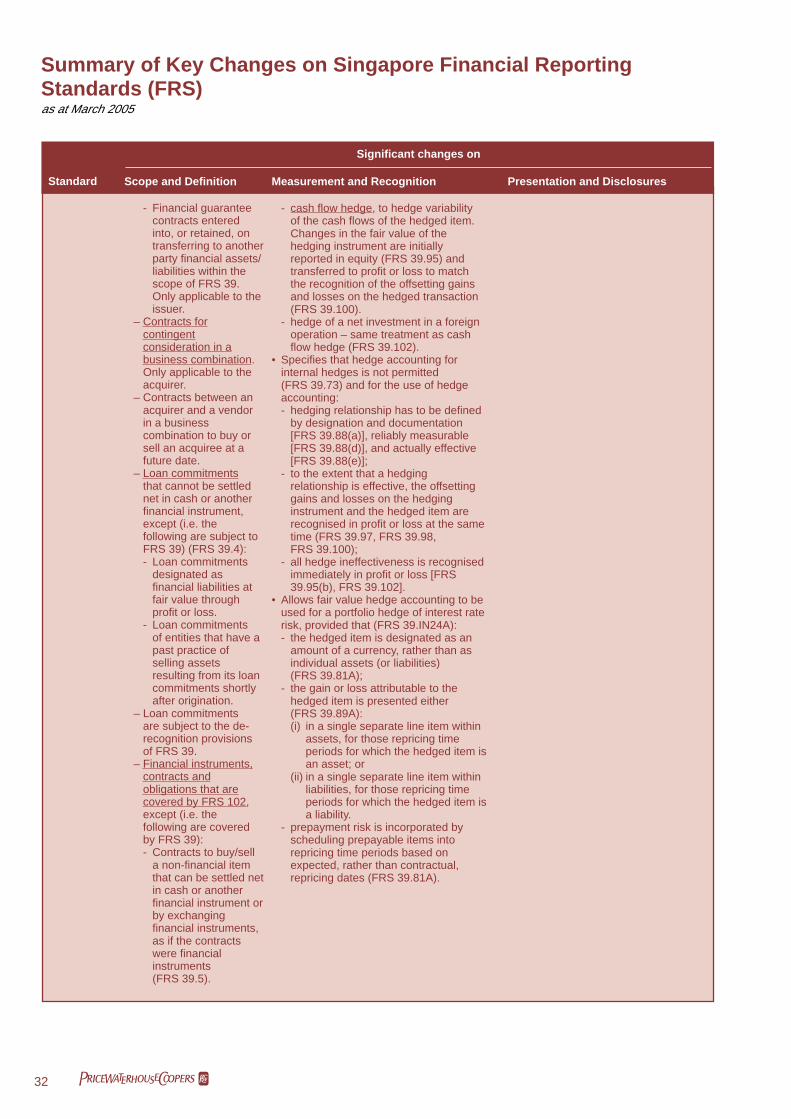

- cash flow hedge, to hedge variabilityof the cash flows of the hedged item.Changes in the fair value of thehedging instrument are initiallyreported in equity (FRS 39.95) andtransferred to profit or loss to matchthe recognition of the offsetting gainsand losses on the hedged transaction(FRS 39.100).

- hedge of a net investment in a foreignoperation – same treatment as cashflow hedge (FRS 39.102).

• Specifies that hedge accounting forinternal hedges is not permitted(FRS 39.73) and for the use of hedgeaccounting:- hedging relationship has to be defined

by designation and documentation[FRS 39.88(a)], reliably measurable[FRS 39.88(d)], and actually effective[FRS 39.88(e)];

- to the extent that a hedgingrelationship is effective, the offsettinggains and losses on the hedginginstrument and the hedged item arerecognised in profit or loss at the sametime (FRS 39.97, FRS 39.98,FRS 39.100);

- all hedge ineffectiveness is recognisedimmediately in profit or loss [FRS39.95(b), FRS 39.102].

• Allows fair value hedge accounting to beused for a portfolio hedge of interest raterisk, provided that (FRS 39.IN24A):- the hedged item is designated as an

amount of a currency, rather than asindividual assets (or liabilities)(FRS 39.81A);

- the gain or loss attributable to thehedged item is presented either(FRS 39.89A):(i) in a single separate line item within

assets, for those repricing timeperiods for which the hedged item isan asset; or

(ii) in a single separate line item withinliabilities, for those repricing timeperiods for which the hedged item isa liability.

- prepayment risk is incorporated byscheduling prepayable items intorepricing time periods based onexpected, rather than contractual,repricing dates (FRS 39.81A).

- Financial guaranteecontracts enteredinto, or retained, ontransferring to anotherparty financial assets/liabilities within thescope of FRS 39.Only applicable to theissuer.

– Contracts forcontingentconsideration in abusiness combination.Only applicable to theacquirer.

– Contracts between anacquirer and a vendorin a businesscombination to buy orsell an acquiree at afuture date.

– Loan commitmentsthat cannot be settlednet in cash or anotherfinancial instrument,except (i.e. thefollowing are subject toFRS 39) (FRS 39.4):- Loan commitments

designated asfinancial liabilities atfair value throughprofit or loss.

- Loan commitmentsof entities that have apast practice ofselling assetsresulting from its loancommitments shortlyafter origination.

– Loan commitmentsare subject to the de-recognition provisionsof FRS 39.

– Financial instruments,contracts andobligations that arecovered by FRS 102,except (i.e. thefollowing are coveredby FRS 39):- Contracts to buy/sell

a non-financial itemthat can be settled netin cash or anotherfinancial instrument orby exchangingfinancial instruments,as if the contractswere financialinstruments(FRS 39.5).

33Illustrative Annual Report 2005

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

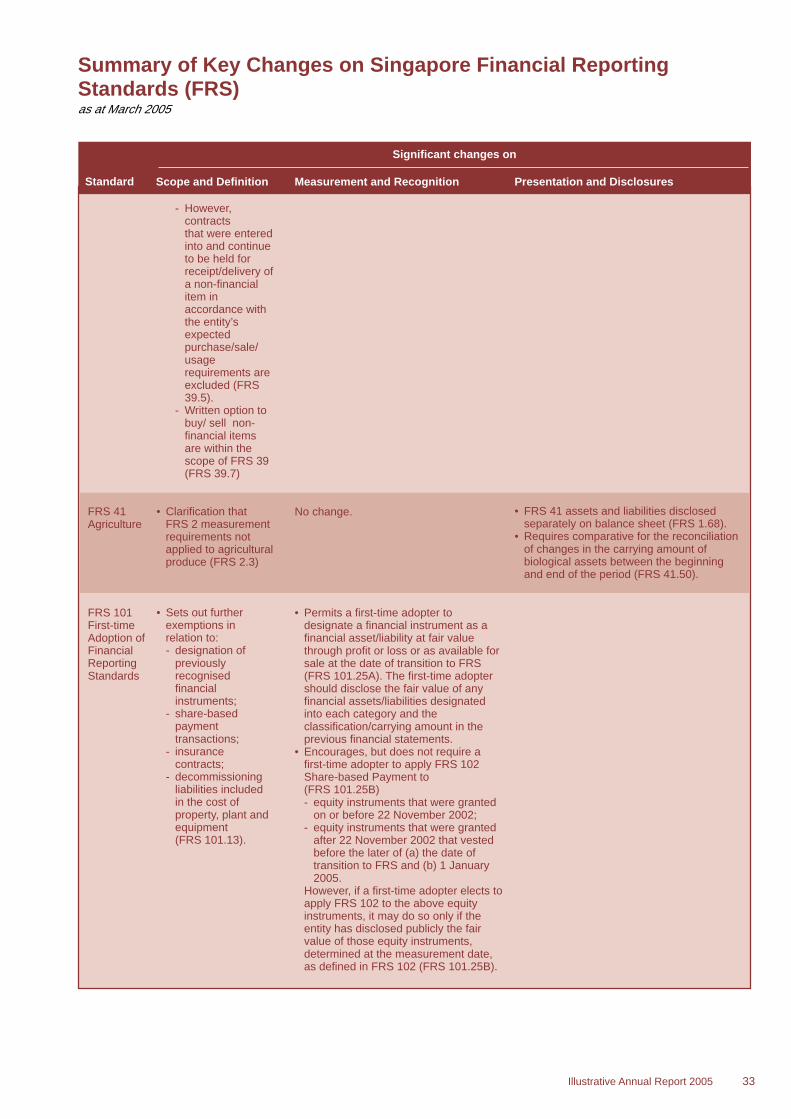

- However,contractsthat were enteredinto and continueto be held forreceipt/delivery ofa non-financialitem inaccordance withthe entity’sexpectedpurchase/sale/usagerequirements areexcluded (FRS39.5).

- Written option tobuy/ sell non-financial itemsare within thescope of FRS 39(FRS 39.7)

• Clarification thatFRS 2 measurementrequirements notapplied to agriculturalproduce (FRS 2.3)

• Sets out furtherexemptions inrelation to:- designation of

previouslyrecognisedfinancialinstruments;

- share-basedpaymenttransactions;

- insurancecontracts;

- decommissioningliabilities includedin the cost ofproperty, plant andequipment(FRS 101.13).

FRS 41Agriculture

FRS 101First-timeAdoption ofFinancialReportingStandards

No change.

• Permits a first-time adopter todesignate a financial instrument as afinancial asset/liability at fair valuethrough profit or loss or as available forsale at the date of transition to FRS(FRS 101.25A). The first-time adoptershould disclose the fair value of anyfinancial assets/liabilities designatedinto each category and theclassification/carrying amount in theprevious financial statements.

• Encourages, but does not require afirst-time adopter to apply FRS 102Share-based Payment to(FRS 101.25B)- equity instruments that were granted

on or before 22 November 2002;- equity instruments that were granted

after 22 November 2002 that vestedbefore the later of (a) the date oftransition to FRS and (b) 1 January2005.

However, if a first-time adopter elects toapply FRS 102 to the above equityinstruments, it may do so only if theentity has disclosed publicly the fairvalue of those equity instruments,determined at the measurement date,as defined in FRS 102 (FRS 101.25B).

• FRS 41 assets and liabilities disclosedseparately on balance sheet (FRS 1.68).

• Requires comparative for the reconciliationof changes in the carrying amount ofbiological assets between the beginningand end of the period (FRS 41.50).

Significant changes on

34 pwc

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

Significant changes on

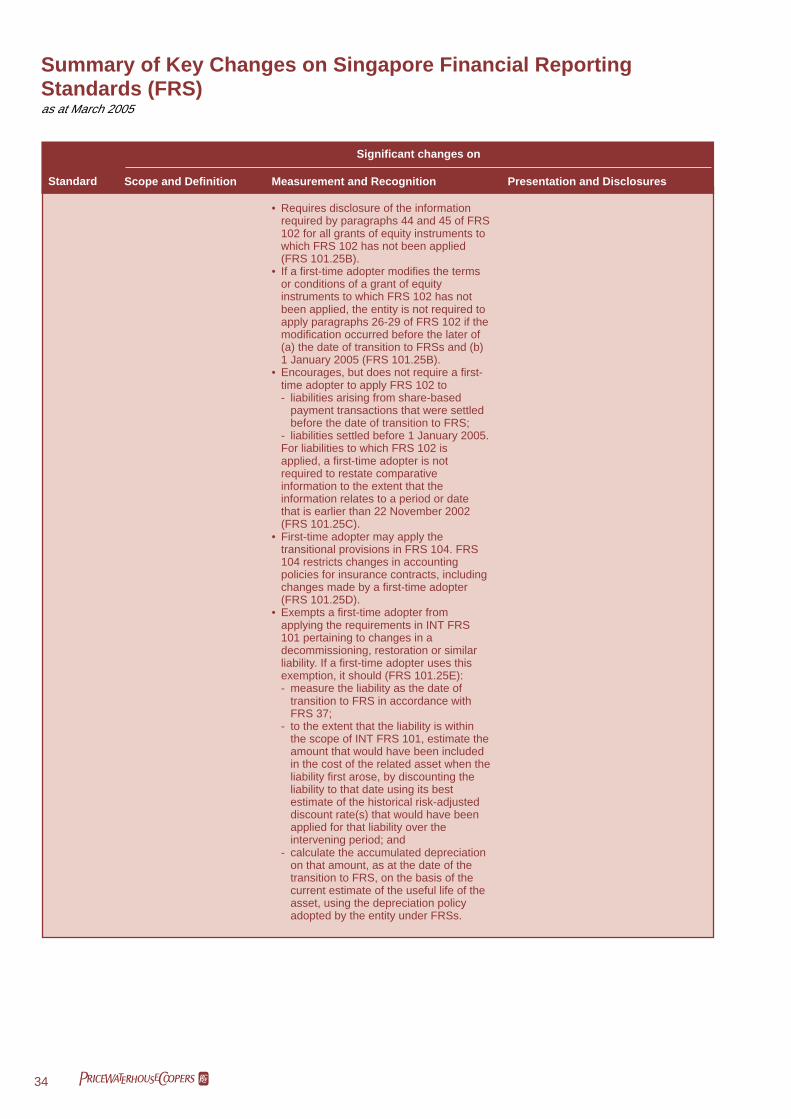

• Requires disclosure of the informationrequired by paragraphs 44 and 45 of FRS102 for all grants of equity instruments towhich FRS 102 has not been applied(FRS 101.25B).

• If a first-time adopter modifies the termsor conditions of a grant of equityinstruments to which FRS 102 has notbeen applied, the entity is not required toapply paragraphs 26-29 of FRS 102 if themodification occurred before the later of(a) the date of transition to FRSs and (b)1 January 2005 (FRS 101.25B).

• Encourages, but does not require a first-time adopter to apply FRS 102 to- liabilities arising from share-based

payment transactions that were settledbefore the date of transition to FRS;

- liabilities settled before 1 January 2005.For liabilities to which FRS 102 isapplied, a first-time adopter is notrequired to restate comparativeinformation to the extent that theinformation relates to a period or datethat is earlier than 22 November 2002(FRS 101.25C).

• First-time adopter may apply thetransitional provisions in FRS 104. FRS104 restricts changes in accountingpolicies for insurance contracts, includingchanges made by a first-time adopter(FRS 101.25D).

• Exempts a first-time adopter fromapplying the requirements in INT FRS101 pertaining to changes in adecommissioning, restoration or similarliability. If a first-time adopter uses thisexemption, it should (FRS 101.25E):- measure the liability as the date of

transition to FRS in accordance withFRS 37;

- to the extent that the liability is withinthe scope of INT FRS 101, estimate theamount that would have been includedin the cost of the related asset when theliability first arose, by discounting theliability to that date using its bestestimate of the historical risk-adjusteddiscount rate(s) that would have beenapplied for that liability over theintervening period; and

- calculate the accumulated depreciationon that amount, as at the date of thetransition to FRS, on the basis of thecurrent estimate of the useful life of theasset, using the depreciation policyadopted by the entity under FRSs.

35Illustrative Annual Report 2005

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

• Allows an entity to apply thederecognition requirements in FRS 39retrospectively from a date of theentity’s own choosing, provided that theinformation needed to apply FRS 39 tofinancial assets and financial liabilitiesderecognised as a result of pasttransactions was obtained at the time ofinitially accounting for thesetransactions (FRS 101.27A).

• Requires an entity with a date oftransition to FRS before 1 January2005 to make the transition to FRS 105in accordance with the transitionalprovisions of FRS 105 (i.e. prospectiveapplication). However, an entity with adate of transition to FRS on or after 1January 2005 should apply FRS 105retrospectively (FRS 101.34A,101.34B).

• Requires the first FRS financialstatements of an entity that adopts FRSbefore 1 January 2006 to present atleast one year of comparativeinformation. However, the comparativeinformation need not comply with FRS32, 39 and 104, provided that the entity(FRS 101.36A):- apply its previous GAAP in the

comparative information to financialinstruments within the scope of FRS32 and FRS 39 and to insurancecontracts within the scope ofFRS 104;

- disclose this fact, together with thebasis used to prepare thisinformation; and

- disclose the nature of the mainadjustments that would make theinformation comply with FRS 32, FRS39 and FRS 104. The entity need notquantify those adjustments.However, the entity shall treat anyadjustment between the balancesheet at the comparative period’sreporting date (i.e. the balance sheetthat includes comparative informationunder previous GAAP) and thebalance sheet at the start of the firstFRS reporting period (i.e. the firstperiod that includes information thatcomplies with FRS 32, FRS 39 andFRS 104) as arising from a change inaccounting policy and give thedisclosures required by paragraph28(a)-(e) and (f)(i) of FRS 8.Paragraph 28(f)(i) applies only toamounts presented in the balancesheet at the comparative period’sreporting date.

Significant changes on

36 pwc

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

• Sets outrequirements for 3types of share-based paymenttransactions(FRS 102.2):- equity-settled

share-basedpaymenttransactions, inwhich the entityreceives goods orservices asconsideration forequity instrumentsof the entity(including sharesor share options);

- cash-settledshare-basedpaymenttransactions, inwhich the entityacquires goods orservices byincurring liabilitiesto the supplier ofthose goods orservices foramounts that arebased on the price(or value) of theentity’s shares orother equityinstruments of theentity;

- transactions inwhich the entityreceives oracquires goods orservices and theterms of thearrangementprovide either theentity or thesupplier of thosegoods or serviceswith a choice ofwhether the entitysettles thetransaction in cashor by issuingequity instruments.

FRS 102Share-basedPayments

• Requires an entity to recognise share-based payment transactions, includingtransactions with employees or otherparties to be settled in cash, otherassets or equity instruments of the entity(FRS 102.IN3, 102.1).

• Equity-settled share-based paymenttransactions- Requires an entity to measure the

goods or services received fromparties other than employees, and thecorresponding increase in equity,directly, at the fair value of the goodsor services received, unless that fairvalue cannot be estimated reliably(FRS 102.10). For transactions withemployees and others providingsimilar services, the entity is requiredto measure the fair value of the equityinstruments granted (FRS 102.11).

- Requires the fair value of equityinstruments granted to be based onmarket prices, if available, and to takeinto account the terms and conditionsupon which those equity instrumentswere granted (FRS 102.16). In theabsence of market prices, fair value isestimated, using a valuation techniqueto estimate what the price of thoseequity instruments would have beenon the measurement date in an arm’slength transaction betweenknowledgeable, willing parties(FRS 102.17).

- For goods and services measured byreference to the fair value of the equityinstruments granted, FRS 102specifies that vesting conditions, otherthan market conditions, are not takeninto account when estimating the fairvalue of the shares or options at therelevant measurement date. Instead,vesting conditions are taken intoaccount by adjusting the number ofequity instruments included in themeasurement of the transactionamount so that, ultimately, the amountrecognised for goods or servicesreceived as consideration for theequity instruments granted is based onthe number of equity instruments thateventually vest. Hence, on acumulative basis, no amount isrecognised for goods or servicesreceived if the equity instrumentsgranted do not vest because of failureto satisfy a vesting condition (otherthan a market condition)(FRS 102.19).

• Nature and extent of share-based paymentarrangements that existed during theperiod (FRS 102.44). Para.45 lists downthe minimum disclosure requirements thatare required to comply with thisrequirement.

• How the fair value of the goods or servicesreceived, or the fair value of the equityinstruments granted, was determined (FRS102.46). Para.47 to 49 lists down theminimum disclosure requirements that arerequired to comply with this requirement.

• Effect of share-based paymenttransactions on the entity’s profit or lossand on its financial position (FRS 102.50).Para. 51 to 52 lists down the minimumdisclosure requirements that are requiredto comply with this requirement.

Significant changes on

37Illustrative Annual Report 2005

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

• Replaces FRS 22for annual periodsbeginning on or after1 July 2004.

• Not applicable to(FRS 103.3):- business

combinations inwhich separateentities orbusinesses arebrought togetherto form a jointventure;

- businesscombinationsinvolving entitiesor businessesunder commoncontrol;

- businesscombinationsinvolving two ormore mutualentities;

FRS 103BusinessCombina-tions

- Sets out requirements if the termsand conditions of an option or sharegrant are modified (e.g. an option isre-priced) or if a grant is cancelled,repurchased or replaced with anothergrant of equity instruments(FRS 102.26 to 29).

• Cash-settled share-based paymenttransactions- Requires an entity to measure the

goods or services acquired and theliability incurred at the fair value of theliability. Until the liability is settled, theentity is required to re-measure thefair value of the liability at eachreporting date and at the date ofsettlement, with any changes in valuerecognised in profit or loss for theperiod (FRS 102.30).

• Share-based payment transactions inwhich the terms of the arrangementprovide the entity with a choice ofsettlement- Requires the entity to account for the

transaction, or the components of thattransaction, as a cash-settled share-based payment transaction if, and tothe extent that, the entity has incurreda liability to settle in cash (or assets),or as an equity-settled share-basedpayment transaction if, and to theextent that, no such liability has beenincurred (FRS 102.34).

• Prohibits the use of pooling-of-interestsmethod. All business combinationswithin its scope should be accountedfor using the purchase method (FRS103.IN9).

• Requires an acquirer to be identified forevery business combination within itsscope (FRS 103.17).

• Requires an acquirer to recogniseliabilities for terminating or reducing theactivities of the acquiree as part ofallocating the cost of the combinationonly when the acquiree has, at theacquisition date, an existing liability forrestructuring recognised in accordancewith FRS 37 (FRS 103.41).

• Requires that an intangible asset (asdefined in FRS 38) or a contingentliability (as defined in FRS 37) acquiredin a business combination should onlybe recognised separately if its fair valuecan be measured reliably(FRS 103.37).

• Amounts recognised at the acquisition datefor each class of the acquiree’s assets,liabilities and contingent liabilities, and,unless disclosure would be impracticable,the carrying amounts of each of thoseclasses, determined in accordance withFRSs, immediately before the combination.[FRS 103.67(f)].

• Either:- Description of the factors that contributed

to a cost that results in the recognition ofgoodwill – a description of each intangibleasset that was not recognised separatelyfrom goodwill and an explanation of whythe intangible asset’s fair value could notbe measured reliably; or

- Description of the nature of any excessrecognised in profit or loss as a result ofthe acquirer’s interest in the net fair valueof the acquiree’s identifiable assets,liabilities and contingent liabilities being inexcess of the cost of the combination[FRS 103.67(h)].

Significant changes on

38 pwc

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

Significant changes on

• Removes FRS 22 benchmark treatmentof measuring acquirees’ identifiableassets and liabilities recognised as theaggregate of (1) the fair value ofidentifiable assets and liabilities as atthe date of the exchange to the extentof the acquirer’s interest obtained in theexchange transaction; and (2) theminority’s proportion of the pre-acquisition carrying amounts of theidentifiable assets and liabilities of thesubsidiary. FRS 103 requires theacquiree’s identifiable assets, liabilitiesand contingent liabilities recognised tobe measured initially by the acquirer attheir fair values at the acquisition date.Therefore, any minority interest in theacquiree is stated at the minority’sproportion of the net fair values of thoseitems (FRS 103.IN14, 103.36).

• Requires goodwill acquired in abusiness combination to be measuredafter initial recognition at cost less anyaccumulated impairment losses.Therefore, the goodwill is not amortisedand instead must be tested forimpairment annually, or more frequentlyif events or changes in circumstancesindicate that it might be impaired(FRS 103.54 to 55).

• Revises treatment of negative goodwill.If, at the acquisition date, the acquirer’sinterest in the net fair value of theacquiree’s identifiable assets, liabilitiesand contingent liabilities exceeds thecost of the combination, the standardrequires the acquirer to reassess theidentification and measurement ofthose items acquired and themeasurement of the cost of thecombination. Any excess remainingafter that reassessment must berecognised by the acquirer immediatelyin profit or loss (FRS 103.56).

• Detailed guidelines provided for reversetakeover (FRS 103.B1 to B17).

• Amount of the acquiree’s profit or loss sincethe acquisition date included in the acquirer’sprofit or loss for the period, unless disclosurewould be impracticable. [FRS 103.67(i)].

• The disclosures required by paragraph 67(see above) are only required in aggregatefor business combinations effected during thereporting period that are individuallyimmaterial (FRS 103.68).

• The disclosures required by paragraph 67(see above) are also required for eachbusiness combination effected after thebalance sheet date but before the financialstatements are authorised for issue, unlesssuch disclosure would be impracticable(FRS 103.71).

• Revenue of the combined entity for theperiod as though the acquisition date for allbusiness combinations effected during theperiod had been the beginning of that period[FRS 103.70(a)].

• Profit or loss of the combined entity for theperiod as though the acquisition date for allbusiness combinations effected during theperiod had been the beginning of the period[FRS 103.70(b)].

• Amount and explanation of any gain or lossrecognised in the current period that:- relates to the identifiable assets acquired or

liabilities or contingent liabilities assumed ina business combination that was effectedin the current or a previous period; and

- is of such size, nature or incidence thatdisclosure is relevant to an understandingof the combined entity’s financialperformance [FRS 103.73(a)].

• Where information is not disclosed on thebasis of impracticability, this fact shall bedisclosed, together with an explanation ofwhy this is the case [FRS 103.67(f),103.67(i), 103.68 to 71].

• The standard specifies that the reconciliationof carrying amount of goodwill at beginningand end of the period should showseparately:- adjustments resulting from the subsequent

recognition of deferred tax assets duringthe period [FRS 103.75(c)];

- goodwill included in a disposal groupclassified as held for sale in accordancewith FRS 105 and goodwill derecognisedduring the period without having previouslybeen included in a disposal group classifiedas held for sale [FRS 103.75(d)];

- net exchange differences arising during theperiod in accordance with FRS 21 [FRS103.75(f)].

• Comparative information is now required forgoodwill reconciliation (Para.75).

- businesscombinations inwhich separateentities orbusinesses arebrought togetherto form a reportingentity by contractalone without theobtaining of anownership interest(for example,combinations inwhich separateentities arebrought togetherby contract aloneto form a duallisted corporation).

• Incorporates andsupersedes INTFRS 9, INT FRS 22and INT FRS 28(FRS 103.IN1).

39Illustrative Annual Report 2005

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

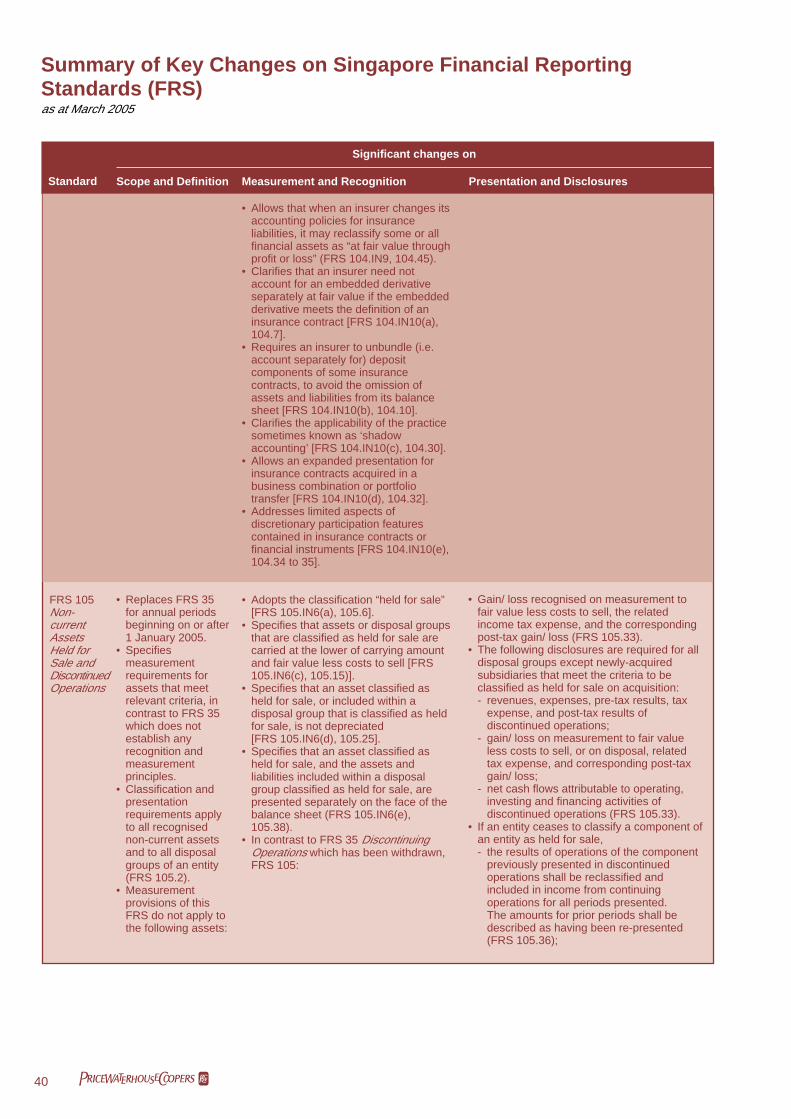

• Applies to allinsurance contracts(includingreinsurancecontracts) that anentity issues and toreinsurancecontracts that itholds, except forspecified contractscovered by otherFRSs (FRS 104.IN3, 104.2 to 104.6).

• Derivativesembedded ininsurance contractsare still within scopeof FRS 39. Someexceptions coveredin FRS 104.

FRS 104InsuranceContracts

• Exempts an insurer temporarily (i.e.during phase I of the project) fromsome requirements of other FRSs,including the requirement to considerthe Framework in selecting accountingpolicies for insurance contracts (FRS104.IN4). However, the FRS:- prohibits provisions for possible

claims under contracts that are not inexistence at the reporting date (suchas catastrophe and equalisationprovisions) (FRS 104.IN4),

- requires a test for the adequacy ofrecognised insurance liabilities andan impairment test for reinsuranceassets (FRS 104.IN4),

- requires an insurer to keep insuranceliabilities in its balance sheet untilthey are discharged or cancelled, orexpire (FRS 104.IN4),

- requires an insurer to presentinsurance liabilities without offsettingthem against related reinsuranceassets (FRS 104.IN4).

• Permits an insurer to change itsaccounting policies for insurancecontracts only if, as a result, its financialstatements present information that ismore relevant and no less reliable, ormore reliable and no less relevant (FRS104.22). In particular, an insurer cannotintroduce any of the following practices,although it may continue usingaccounting policies that involve them(FRS 104.IN5, 104.25):- measuring insurance liabilities on an

undiscounted basis;- measuring contractual rights to future

investment management fees at anamount that exceeds their fair valueas implied by a comparison withcurrent fees charged by other marketparticipants for similar services;

- using non-uniform accounting policiesfor the insurance liabilities ofsubsidiaries.

• Allows introduction of an accountingpolicy that involves remeasuringdesignated insurance liabilitiesconsistently in each period to reflectcurrent market interest rates (and, if theinsurer so elects, other currentestimates and assumptions)(FRS 104.IN6, 104.24).

• Added rebuttable presumption that aninsurer’s financial statements willbecome less relevant and reliable if itintroduces an accounting policy thatreflects future investment margins inthe measurement of insurancecontracts (FRS 104.IN8, 104.27).

• Requires disclosure to help usersunderstand:- Amounts in the insurer’s financial

statements that arise from insurancecontracts [FRS 104.IN11(a), 104.36]. A listof minimum disclosures required to complywith this requirement is provided(FRS 104.37).

- Amount, timing and uncertainty of futurecash flows from insurance contracts (FRS104.IN11(b), 104.38). A list of minimumdisclosures required to comply with thisrequirement is provided (FRS 104.39).

- Disclosures required where FRS 104participatory features cannot be measuredreliably (FRS 32.91A).

Significant changes on

40 pwc

Summary of Key Changes on Singapore Financial ReportingStandards (FRS)as at March 2005

Scope and Definition Measurement and Recognition Presentation and DisclosuresStandard

Significant changes on

• Gain/ loss recognised on measurement tofair value less costs to sell, the relatedincome tax expense, and the correspondingpost-tax gain/ loss (FRS 105.33).

• The following disclosures are required for alldisposal groups except newly-acquiredsubsidiaries that meet the criteria to beclassified as held for sale on acquisition:- revenues, expenses, pre-tax results, tax

expense, and post-tax results ofdiscontinued operations;

- gain/ loss on measurement to fair valueless costs to sell, or on disposal, relatedtax expense, and corresponding post-taxgain/ loss;

- net cash flows attributable to operating,investing and financing activities ofdiscontinued operations (FRS 105.33).

• If an entity ceases to classify a component ofan entity as held for sale,- the results of operations of the component

previously presented in discontinuedoperations shall be reclassified andincluded in income from continuingoperations for all periods presented.The amounts for prior periods shall bedescribed as having been re-presented(FRS 105.36);

• Allows that when an insurer changes itsaccounting policies for insuranceliabilities, it may reclassify some or allfinancial assets as “at fair value throughprofit or loss” (FRS 104.IN9, 104.45).

• Clarifies that an insurer need notaccount for an embedded derivativeseparately at fair value if the embeddedderivative meets the definition of aninsurance contract [FRS 104.IN10(a),104.7].

• Requires an insurer to unbundle (i.e.account separately for) depositcomponents of some insurancecontracts, to avoid the omission ofassets and liabilities from its balancesheet [FRS 104.IN10(b), 104.10].

• Clarifies the applicability of the practicesometimes known as ‘shadowaccounting’ [FRS 104.IN10(c), 104.30].

• Allows an expanded presentation forinsurance contracts acquired in abusiness combination or portfoliotransfer [FRS 104.IN10(d), 104.32].

• Addresses limited aspects ofdiscretionary participation featurescontained in insurance contracts orfinancial instruments [FRS 104.IN10(e),104.34 to 35].

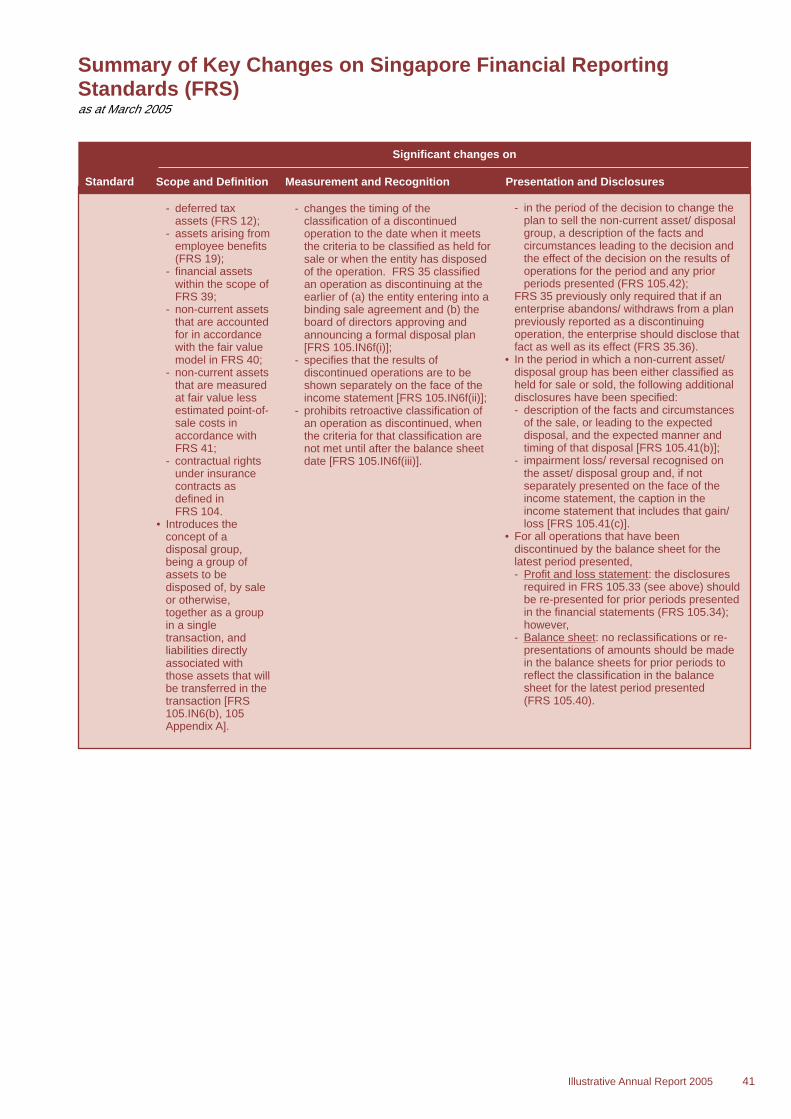

• Adopts the classification “held for sale”[FRS 105.IN6(a), 105.6].

• Specifies that assets or disposal groupsthat are classified as held for sale arecarried at the lower of carrying amountand fair value less costs to sell [FRS105.IN6(c), 105.15)].

• Specifies that an asset classified asheld for sale, or included within adisposal group that is classified as heldfor sale, is not depreciated[FRS 105.IN6(d), 105.25].