Embed Size (px)

Citation preview

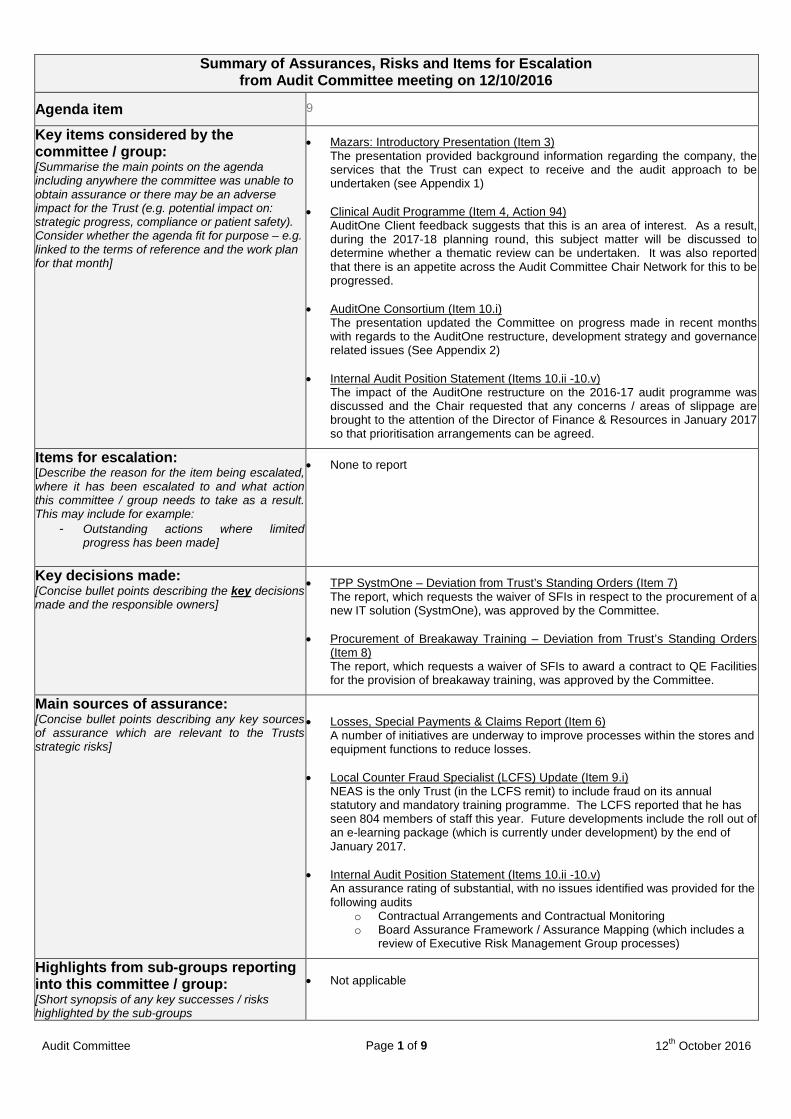

Summary of Assurances, Risks and Items for Escalation from Audit Committee meeting on 12/10/2016

Agenda item 9

Key items considered by the committee / group: [Summarise the main points on the agenda including anywhere the committee was unable to obtain assurance or there may be an adverse impact for the Trust (e.g. potential impact on: strategic progress, compliance or patient safety). Consider whether the agenda fit for purpose – e.g. linked to the terms of reference and the work plan for that month]

• Mazars: Introductory Presentation (Item 3)The presentation provided background information regarding the company, the services that the Trust can expect to receive and the audit approach to be undertaken (see Appendix 1)

• Clinical Audit Programme (Item 4, Action 94)AuditOne Client feedback suggests that this is an area of interest. As a result, during the 2017-18 planning round, this subject matter will be discussed to determine whether a thematic review can be undertaken. It was also reported that there is an appetite across the Audit Committee Chair Network for this to be progressed.

• AuditOne Consortium (Item 10.i)The presentation updated the Committee on progress made in recent months with regards to the AuditOne restructure, development strategy and governance related issues (See Appendix 2)

• Internal Audit Position Statement (Items 10.ii -10.v)The impact of the AuditOne restructure on the 2016-17 audit programme was discussed and the Chair requested that any concerns / areas of slippage are brought to the attention of the Director of Finance & Resources in January 2017 so that prioritisation arrangements can be agreed.

Items for escalation: [Describe the reason for the item being escalated, where it has been escalated to and what action this committee / group needs to take as a result. This may include for example:

- Outstanding actions where limited progress has been made]

• None to report

Key decisions made: [Concise bullet points describing the key decisions made and the responsible owners]

• TPP SystmOne – Deviation from Trust’s Standing Orders (Item 7)The report, which requests the waiver of SFIs in respect to the procurement of a new IT solution (SystmOne), was approved by the Committee.

• Procurement of Breakaway Training – Deviation from Trust’s Standing Orders (Item 8) The report, which requests a waiver of SFIs to award a contract to QE Facilities for the provision of breakaway training, was approved by the Committee.

Main sources of assurance: [Concise bullet points describing any key sources of assurance which are relevant to the Trusts strategic risks]

• Losses, Special Payments & Claims Report (Item 6)A number of initiatives are underway to improve processes within the stores andequipment functions to reduce losses.

• Local Counter Fraud Specialist (LCFS) Update (Item 9.i)NEAS is the only Trust (in the LCFS remit) to include fraud on its annualstatutory and mandatory training programme. The LCFS reported that he hasseen 804 members of staff this year. Future developments include the roll out ofan e-learning package (which is currently under development) by the end ofJanuary 2017.

• Internal Audit Position Statement (Items 10.ii -10.v)An assurance rating of substantial, with no issues identified was provided for thefollowing audits

o Contractual Arrangements and Contractual Monitoringo Board Assurance Framework / Assurance Mapping (which includes a

review of Executive Risk Management Group processes)

Highlights from sub-groups reporting into this committee / group: [Short synopsis of any key successes / risks highlighted by the sub-groups

• Not applicable

Audit Committee Page 1 of 9 12th October 2016

The Trust corporate objectives are: 1. To continuously improve the quality and safety of our services, ensuring the CQC fundamental standards are achieved and patient outcomes

are improved. 2. To achieve financial break-even position in 2017/18. 3. To improve organisational culture, aligned to Trust mission, vision and values to achieve delivery of our strategy. 4. Develop a future workforce with the correct staffing levels and skill mix across both clinical and non-clinical functions to support safe, effective

and compassionate care and employee well-being. 5. To deliver the agreed Transformational and Vanguard programmes. 6. To plan, agree and implement a front line operational delivery model aligned to current and future need and planned performance

improvement. Document Information

Author Name: Gemma Wong

Author Title: PA to Director of Finance & Resources

Sponsor Name: Douglas Taylor

Sponsor Title: Non Executive Director

Last Saved: 2016-10-19 10:00:00

Save Location: N:\Public\Chief Executive Directorate\Meetings\Audit\2016\10 October 2016\Audit Committee Minutes 12.10.16.docx

Word Count: 4018

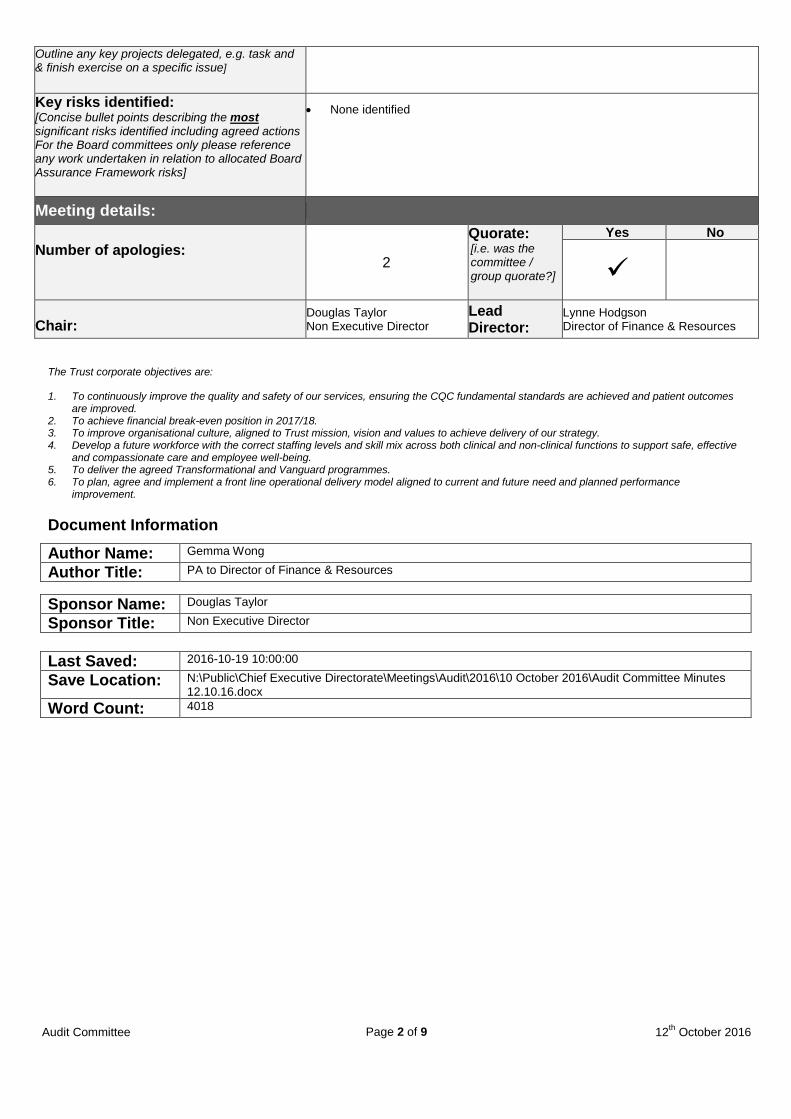

Outline any key projects delegated, e.g. task and & finish exercise on a specific issue] Key risks identified: [Concise bullet points describing the most significant risks identified including agreed actions For the Board committees only please reference any work undertaken in relation to allocated Board Assurance Framework risks]

• None identified

Meeting details: Number of apologies:

2

Quorate: [i.e. was the committee / group quorate?]

Yes No

Chair:

Douglas Taylor Non Executive Director

Lead Director:

Lynne Hodgson Director of Finance & Resources

Audit Committee Page 2 of 9 12th October 2016

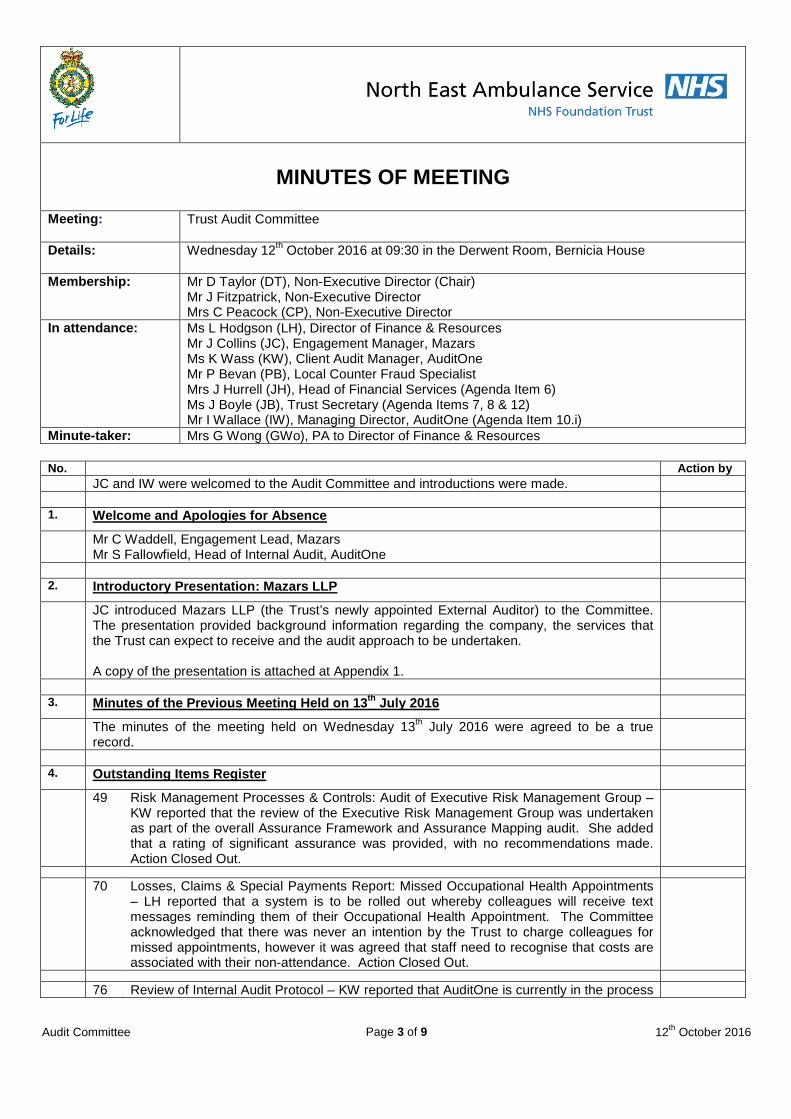

MINUTES OF MEETING

Meeting: Trust Audit Committee

Details: Wednesday 12th October 2016 at 09:30 in the Derwent Room, Bernicia House

Membership:

Mr D Taylor (DT), Non-Executive Director (Chair) Mr J Fitzpatrick, Non-Executive Director Mrs C Peacock (CP), Non-Executive Director

In attendance:

Ms L Hodgson (LH), Director of Finance & Resources Mr J Collins (JC), Engagement Manager, Mazars Ms K Wass (KW), Client Audit Manager, AuditOne Mr P Bevan (PB), Local Counter Fraud Specialist Mrs J Hurrell (JH), Head of Financial Services (Agenda Item 6) Ms J Boyle (JB), Trust Secretary (Agenda Items 7, 8 & 12) Mr I Wallace (IW), Managing Director, AuditOne (Agenda Item 10.i)

Minute-taker: Mrs G Wong (GWo), PA to Director of Finance & Resources No. Action by JC and IW were welcomed to the Audit Committee and introductions were made. 1. Welcome and Apologies for Absence

Mr C Waddell, Engagement Lead, Mazars Mr S Fallowfield, Head of Internal Audit, AuditOne

2. Introductory Presentation: Mazars LLP

JC introduced Mazars LLP (the Trust’s newly appointed External Auditor) to the Committee. The presentation provided background information regarding the company, the services that the Trust can expect to receive and the audit approach to be undertaken. A copy of the presentation is attached at Appendix 1.

3. Minutes of the Previous Meeting Held on 13th July 2016

The minutes of the meeting held on Wednesday 13th July 2016 were agreed to be a true record.

4. Outstanding Items Register

49 Risk Management Processes & Controls: Audit of Executive Risk Management Group – KW reported that the review of the Executive Risk Management Group was undertaken as part of the overall Assurance Framework and Assurance Mapping audit. She added that a rating of significant assurance was provided, with no recommendations made. Action Closed Out.

70 Losses, Claims & Special Payments Report: Missed Occupational Health Appointments

– LH reported that a system is to be rolled out whereby colleagues will receive text messages reminding them of their Occupational Health Appointment. The Committee acknowledged that there was never an intention by the Trust to charge colleagues for missed appointments, however it was agreed that staff need to recognise that costs are associated with their non-attendance. Action Closed Out.

76 Review of Internal Audit Protocol – KW reported that AuditOne is currently in the process

Audit Committee Page 3 of 9 12th October 2016

of drafting a standardised protocol which will be applicable to all AuditOne clients. She explained that is it anticipated that the protocol will be issued in January 2017 with a view to implementing it immediately. An update will be provided at the January 2017 Audit Committee.

84 Losses, Claims & Special Payments Report: Missing Scoops – JH reported that she

continues to share information regarding missing equipment (including scoops) with Service Line Managers. In addition, a routine report is submitted to the Patient Safety Group which includes details of un-located / missing equipment. JH explained that there is limited further action that can be taken by the Audit Committee, however an update on new initiatives (which will assist in addressing the issue) will be provided under agenda item 6. Action Closed Out.

87 Losses, Claims & Special Payments Report: Serial Claimants – JH Reported that the

Risk and Regulatory Services team produce a monthly report for the ECLIPs Group which shows the trends for litigation cases received by the Trust. Litigation data is also included within the monthly Governance Report to the Board of Directors and the Strategic Health and Safety Committee receive details of the litigation cases received during the reporting period. In addition, a report is under development for the Executive Team which will be presented on a monthly basis and will provide further information with regards to trends and suspected serial claimants. PB advised that he is confident that the Trust’s Claims Manager would report any suspicious activity. Action Closed Out.

88 Internal Audit / External Audit Protocol – KW confirmed that the current protocol has

been updated to include references to AuditOne. Action Closed Out.

89 Internal Audit Update: DBS Risk Assessment Process: Small Sample Review - It was

noted that findings will be presented at the January 2017 Committee meeting.

90 Requirement for Ambulance presence at County Fayres – LH advised that the subject

has been reviewed from a financial perspective to gain assurance that sufficient processes are in place to cover the cost of the services. She confirmed that standard costing is in place and standard prices have been agreed for events to ensure that a contribution to overheads is achieved and compliance is audited annually by Internal Audit. Action Closed Out.

91 Annual Review of the Effectiveness of the Internal Audit Function: Format of future

AuditOne update reports – DT explained that a general point was made at the July Committee whereby incorporating comparative data (where available) in future reports would be beneficial. IW confirmed that the request has been noted. Action Closed Out.

92 Annual Review of the Effectiveness of the Internal Audit Function: Feedback – DT

reported that LH, IW and himself met to discuss changes to the structure of AuditOne (see presentation under agenda item 10.i). Feedback from the effectiveness review was provided to IW for him to take on board moving forward. Action Closed Out.

93 Audit Committee Bespoke Training Programme – DT reminded the Committee that CP

would be attending an external training event at the end of October and would be attending the next Local Audit Chairs meeting as part of her induction programme. He added that CP, JB and himself would then meet to agree a bespoke training package for new Audit Committee members. An update will be provided at the January 2017 Committee.

94 Clinical Audit Programme – DT advised that he would be meeting with the Consultant

Paramedic on the 21st October to discuss the programme. IW reported that he has received feedback from Clients which suggests that this is an area of interest for future audits. As a result, during the 2017-18 planning round, this subject matter will be discussed to determine whether a thematic review can be undertaken. DT added that there is an appetite across the Audit Committee Chair Network for this to be progressed. An update will be provided at the January 2017 Committee.

D Taylor

5. Matters Arising

None to report.

Audit Committee Page 4 of 9 12th October 2016

Governance, Risk Management & Internal Controls 6. Losses, Special Payments & Claims Report

JH presented the Q1 update report, highlighting the following key areas:

• Appendix Aii contains details regarding lost radios. Managers have been tasked with being more effective in tracing this equipment, however the Audit Committee were assured that data can be disabled remotely therefore removing any risk of sensitive data being accessed. Information has also been made available regarding missing mobile phones (vehicle based) at a cost of £25 per phone. JH advised that the IM&T Department is progressing a project to look at personal issue phones in the future.

• Three initiatives are underway with regards to stores / equipment as follows: o Electronic VDI solution o Information is being made available on each vehicle regarding the equipment

on board together with the cost of this. o Scan4Safety – a longer term barcoding project which will enable the

traceability of an individual (patient and staff), equipment and consumables. For example data will be available to pin point where a piece of equipment was last used and by whom. Representatives from the DH will be visiting the Trust on the 18th & 19th October to determine whether the organisation is ‘ready’ to progress with this initiative, following which a Business Case will need to be developed.

• The report contains information regarding out of date consumables (information which has been captured for the first time this quarter). It has been identified that consumables that don’t have a 6 month+ shelf life are donated to charity. Work is therefore underway to instigate a methodology for recording medical consumables – this will be linked with Scan4Safety in the future, however in the short term will assist with stock control so that the volume of out of date stock can be reduced.

PB referred to the compensation payments made in respect of a needle stick injury (£6,487.00). He suggested that this is excessive compared to other Trusts for which the compensation payment is normally circa £1,200. JH explained that the compensation claim was based on the information provided and will also include litigation costs. She added that she would look into this claim further and provide further information / discuss with PB out with the meeting.

7. TPP SystmOne – Deviation from Trust’s Standing Orders

JB presented the above report which requests the waiver of SFIs in respect to the procurement of a new IT solution (SystmOne). It was explained that the request has been deemed ‘business critical’ because a significant number of local Urgent Care Services use SystmOne - which enables the transfer of patient information across healthcare organisations. In addition, the operating model for the Trust’s planned clinical hub requires a clinical patient management system, the functionality for which is not currently available in Cleric. It is therefore essential that the Trust can demonstrate to Commissioners its readiness to implement the Clinical Hub. DT queried what the consequences would be if the request was declined. JB explained that the Trust is looking to increase the number of Clinicians within the Clinical Hub. In the specification there is a requirement for the Trust to prescribe – which SystmOne would provide. The process involved in progressing through a formal tender would add an additional 3 months onto the project. JF queried the lead time associated with receiving the solution. JB advised that it is a National system which would be available to download immediately. Training would be provided to staff. CP queried whether this requirement was considered as part of the initial planning for the Clinical Hub. LH explained that at that stage in the process the Trust may well have been unaware of the requirement to prescribe. Following further discussion Committee Members agreed to approve the request.

Audit Committee Page 5 of 9 12th October 2016

8. Procurement of Breakaway Training – Deviation from Trust’s Standing Orders

JB presented the above report which requests a waiver of SFIs to award a contract to QE Facilities for the provision of breakaway training. The training will provide front line staff with the skills required to breakaway from threatening, or potentially threatening situations where their physical and emotional well-being is at risk from patients who are holding or restraining them in an aggressive way. The requirement has been deemed urgent because training needs to be done as soon as possible in order to support the delivery of the agreed and scheduled training plan. Specialist expertise will be required in providing the training to staff, and training of this nature has been requested by staff. The contract is initially for 3 months, when it is then planned that a reciprocal training arrangement with Northumbria Police will commence where Northumbria Police will become the training provider. This reciprocal arrangement with Northumbria Police is a “no-cost” arrangement as the cost of the training will be off-set by income NEAS will earn from the sales of First Aid training to the officers of Northumbria Police. JB noted that in the run up to the CQC inspection this aspect was identified as a significant gap. She added that the provision of training is also a response to staff feedback via the staff survey regarding violence and aggression. Following further discussion Committee Members agreed to approve the request.

Internal Audit 9. Countering Fraud 9.i Local Counter Fraud Specialist Update

PB presented the above report, highlighting the following key points:

• Good progress is being made against the plan.

• One investigation is on-going and advice is awaited from NHS Protect with regards to this. Feedback will be provided to the Director of Finance & Resources once this advice has been received.

• NEAS is the only Trust (in PB’s remit) to include fraud on its annual statutory and mandatory training programme. PB reported that he has seen 804 members of staff this year. Future developments include the roll out of an e-learning package (which is currently under development) by the end of January 2017.

• Fraud awareness visits to stations will commence in November 2016.

• The national Fraud Initiative Fair Processing Notice has been uploaded to the Intranet and staff have received the required notices via their payslip.

10. Internal Audit

10.i AuditOne Consortium IW provided an update of progress made in recent months with regards to the AuditOne restructure, development strategy and governance related issues. A copy of the presentation is attached at Appendix 2.

10.ii

10.iii 10.iv

Internal Audit Position Statement Follow-up of Internal Audit Recommendations Interim Review re: adherence against the requirements of the Internal Audit Protocol

Audit Committee Page 6 of 9 12th October 2016

10.v Review of Executive Risk Management Group Processes and Controls KW advised that two audit reports have been issued since the July Audit Committee – Contractual Arrangements and Contractual Monitoring and Board Assurance Framework / Assurance Mapping. An assurance rating of substantial was provided for both reviews and no issues were identified during the course of the audits. A draft report has been developed with regards to the Management of Health & Safety follow up audit. Management responses have been received and the report is awaiting internal sign-off. Section 4 of the report outlines changes to the 2016-17 Plan. KW reminded the Committee that agreement was reached at the July 2016 Committee to defer the audit of first responders to Quarter 4. In addition it has also been proposed, by the Director of Strategy, Transformation and Workforce that the audit of Staff Engagement, Surveys and Feedback is deferred until Q1 2017-18 (this was originally planned for Q4 2016-17). KW explained that this is because the 2016-17 staff survey has very recently been circulated to staff and the results will be collated during Q4. Deferring the audit would allow Internal Audit to review the outcome of this survey. Committee Members agreed with this proposal. Section 5 of the report provides a summary of agreed actions. KW advised that the new process relating to revised implementation dates has been rolled out. The new process requires Director authorisation before any action implementation date can be revised. This appears to have had an impact with only 3 actions having been assigned revised implementation dates since the process was rolled out. The status of 8 actions is to be confirmed – these relate to the HR and Operations Directorates. LH advised that she will escalate information such as this to the Executive Team. DT referred to Appendix 1 which details the status of all Audits included in the 2016-17 plan. He referred to the AuditOne presentation (Item 10.i), in particular the restructure, and asked that the Committee is provided with assurance that the programme will not slip. IW explained that in the case of the 2015-16 audit programme, all work was completed by early June 2016. For the 2016-17 programme the target for the completion of all fieldwork is early April 2017 with reports being finalised by early May. Resourcing considerations are underway. IW added that the AuditOne management team have been asked to take a view on the status of the programme and what is needed to reach the April and May target dates. DT requested that any concerns regarding the achievement of the programme are reported to LH in January 2017. He explained that LH and himself would then discuss and prioritise. LH suggested that if there is any slippage, audits which are required for the Trust’s assurance statement at the year end are prioritised.

I Wallace

External Audit 11. External Audit 11.i Handover with PwC

JC reported PwC will be contacted in accordance with internal processes and auditing standards. He added that Mazars have written to the Trust (and received a response) for permission to contact the previous auditors. A handover meeting will be arranged with PwC to discuss the Trust’s audit and issues encountered and their working papers will be reviewed to give assurance over the opening balance of the next financial statements.

11.ii Engagement Pack – Charitable Funds 2016-17

JC presented the above paper which sets out the terms and conditions of the 2016-17 Charitable Fund audit. LH confirmed that the engagement pack has been reviewed and signed off.

11.iii Engagement Pack – FT Audit

Audit Committee Page 7 of 9 12th October 2016

JC presented the above paper which sets out the terms and conditions of the 2016-17 FT Audit. He explained that the audit includes additional responsibilities for the auditor with regards to value for money arrangements. LH confirmed that the engagement pack has been reviewed and signed off.

11.iv Independent Examination of 2015-16 Charitable Fund

JC explained that Mazars have been asked to undertake an independent review of the 2015-16 Charitable Fund. The engagement pack has been signed off and the work will commence within the near future. It is anticipated that the audit will take no longer than 4 days to complete.

Other Assurance Functions 12. External Assurances

None to report. 13. Audit Committee Business

13.i Audit Committee Cycle of Business (for Members to note the items of business for the next meeting) It was suggested that there may be issues/actions in response to the forthcoming issue of the CQC report for the Audit Committee to consider. It was therefore agreed to add the CQC report onto the January 2017 agenda. IW noted that the AuditOne progress report will outline any changes to the 2016-17 audit plan (as per discussions under agenda items 10.ii-10.v).

G Wong

13.ii Items for Escalation to the Board of Directors and Council of Governors

Assurance gained with regards to the Contractual Arrangements & Contractual Monitoring and Board Assurance Framework / Assurance Mapping audits – both of which were provided with an assurance rating of substantial (with no issues identified.)

14. Any Other Business

JF reported that the September Finance Committee received a report from the Operations Centre, a section of which provided information regarding chairs. It was stated that chairs used by call operators cost the Trust £700 per chair (they are ergonomically sound etc.) JF suggested that this appears expensive and is further compounded by the fact that a number of colleagues have reported that they require a more specialist chair which is at further expense to the Trust. He requested assurance that a robust process is in place with regards to the monitoring and approval of these requests. DT suggested that this is a health and safety issue which requires an independent work station assessment. He queried whether the Committee can be confident that such a process is in place. LH reported that Task and Finish Group has been established to assess the process, determine whether the best value for money contractor is being used etc. CP queried whether any benchmarking has been undertaken with other Trusts, or whether any data is available regarding back related sickness levels. LH advised that she would feed both suggestions into the Task & Finish Group. Committee members were assured that an assessment is underway and that progress /feedback would be provided to the Finance Committee. DT requested that the issue is referred back to the Audit Committee should there be any concerns regarding the outcome of the review.

L Hodgson

15. Date and time of next meeting

Monday 16th January 2017 at 09:30 in Room 14. 16. Monitor – Potential Exceptions and Reporting

Audit Committee Page 8 of 9 12th October 2016

None to report. 17. Meeting Review

No comments received.

Audit Committee Page 9 of 9 12th October 2016

An introduction to Mazars October 2016

Appendix 1

1

Who we are

Added value Latest UK fee

income £150m

Top Ten Partnership by

Audit fee

19 Offices in UK

138 Partners

Over 1,750

Employees

Appendix 1

2

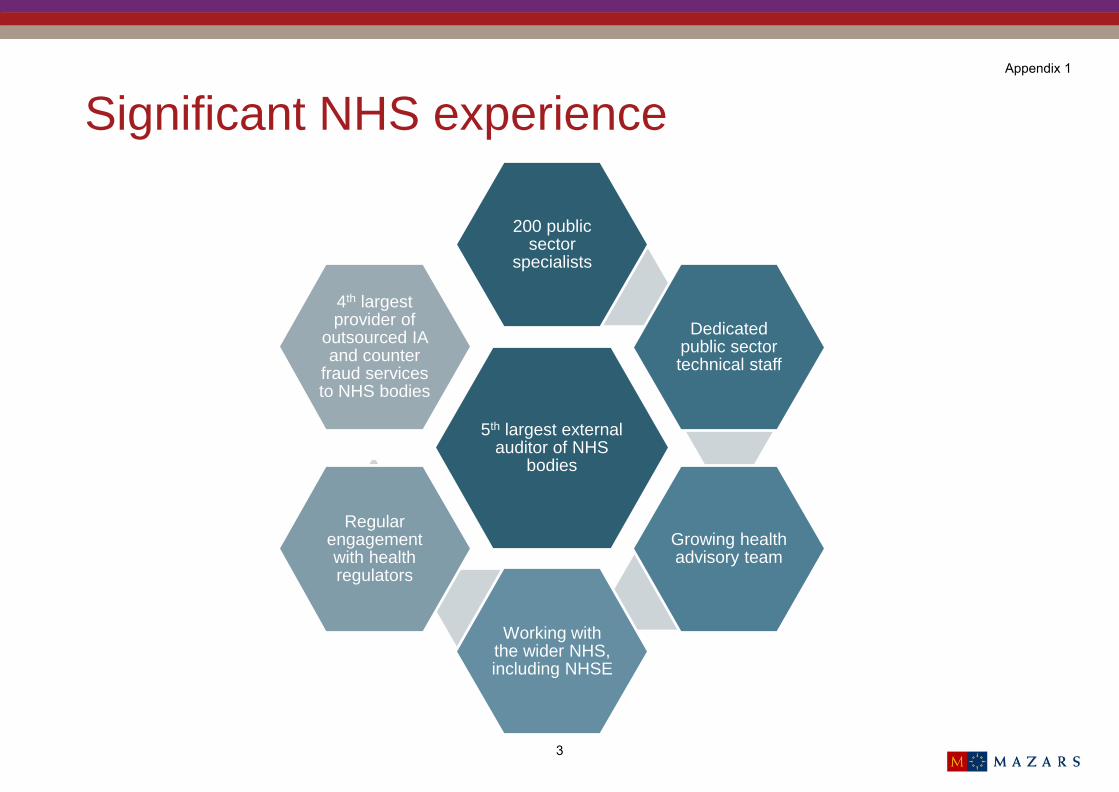

Significant NHS experience

5th largest external auditor of NHS

bodies

200 public sector

specialists

Dedicated public sector technical staff

Growing health advisory team

Working with the wider NHS, including NHSE

Regular engagement with health regulators

4th largest provider of

outsourced IA and counter

fraud services to NHS bodies

Appendix 1

3

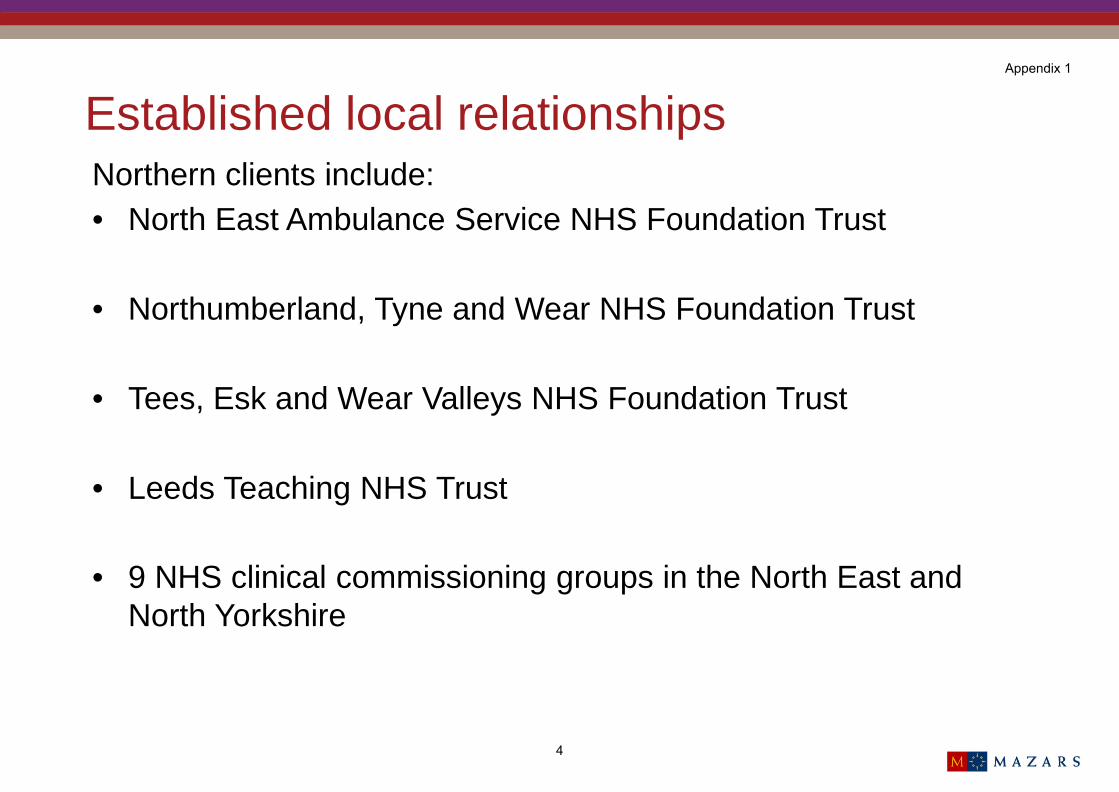

Established local relationships Northern clients include: • North East Ambulance Service NHS Foundation Trust

• Northumberland, Tyne and Wear NHS Foundation Trust

• Tees, Esk and Wear Valleys NHS Foundation Trust

• Leeds Teaching NHS Trust

• 9 NHS clinical commissioning groups in the North East andNorth Yorkshire

Appendix 1

4

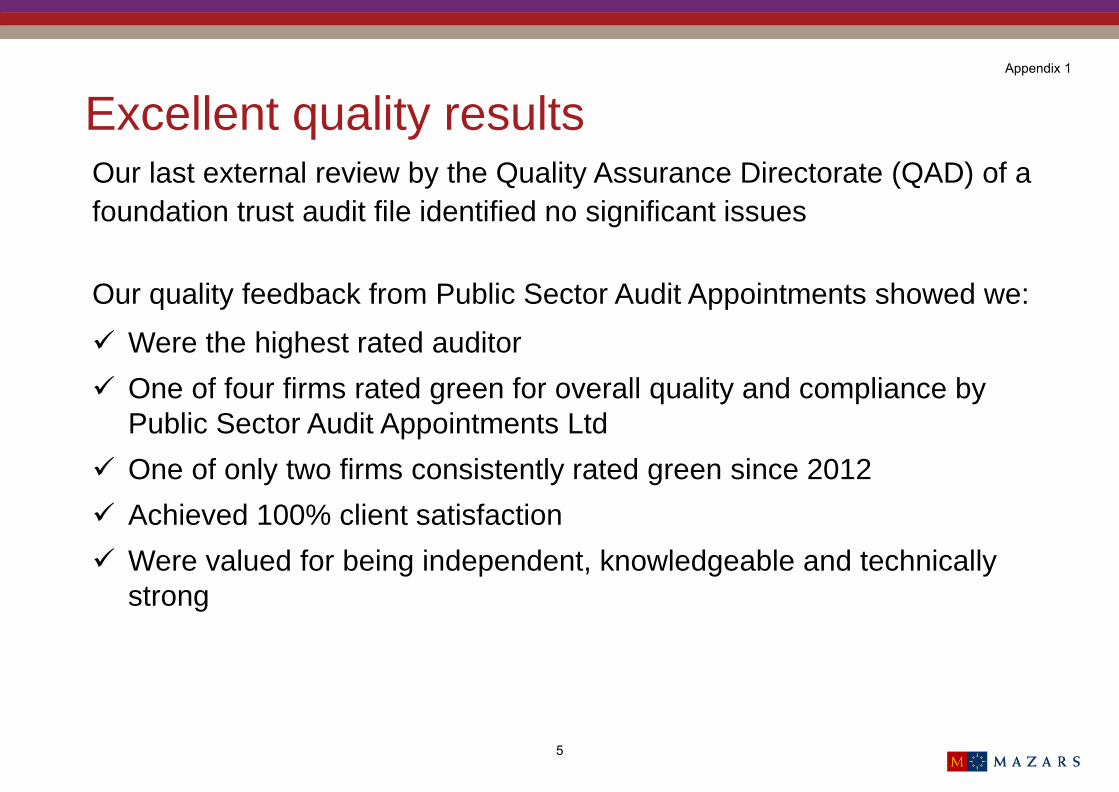

Excellent quality results Our last external review by the Quality Assurance Directorate (QAD) of a foundation trust audit file identified no significant issues

Our quality feedback from Public Sector Audit Appointments showed we:

Were the highest rated auditor One of four firms rated green for overall quality and compliance by

Public Sector Audit Appointments Ltd One of only two firms consistently rated green since 2012 Achieved 100% client satisfaction Were valued for being independent, knowledgeable and technically

strong

Appendix 1

5

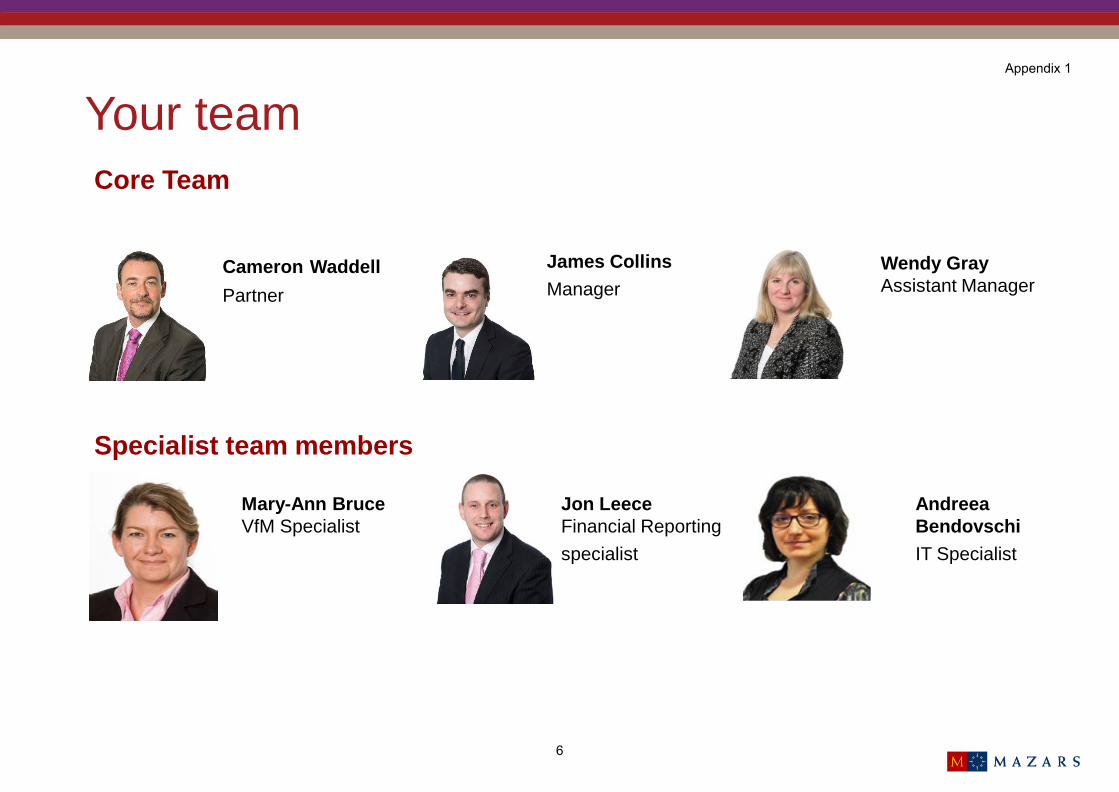

Your team Core Team

Cameron Waddell Partner

James Collins Manager

Wendy Gray Assistant Manager

Specialist team members

Mary-Ann Bruce VfM Specialist

Jon Leece Financial Reporting specialist

Andreea Bendovschi IT Specialist

Appendix 1

6

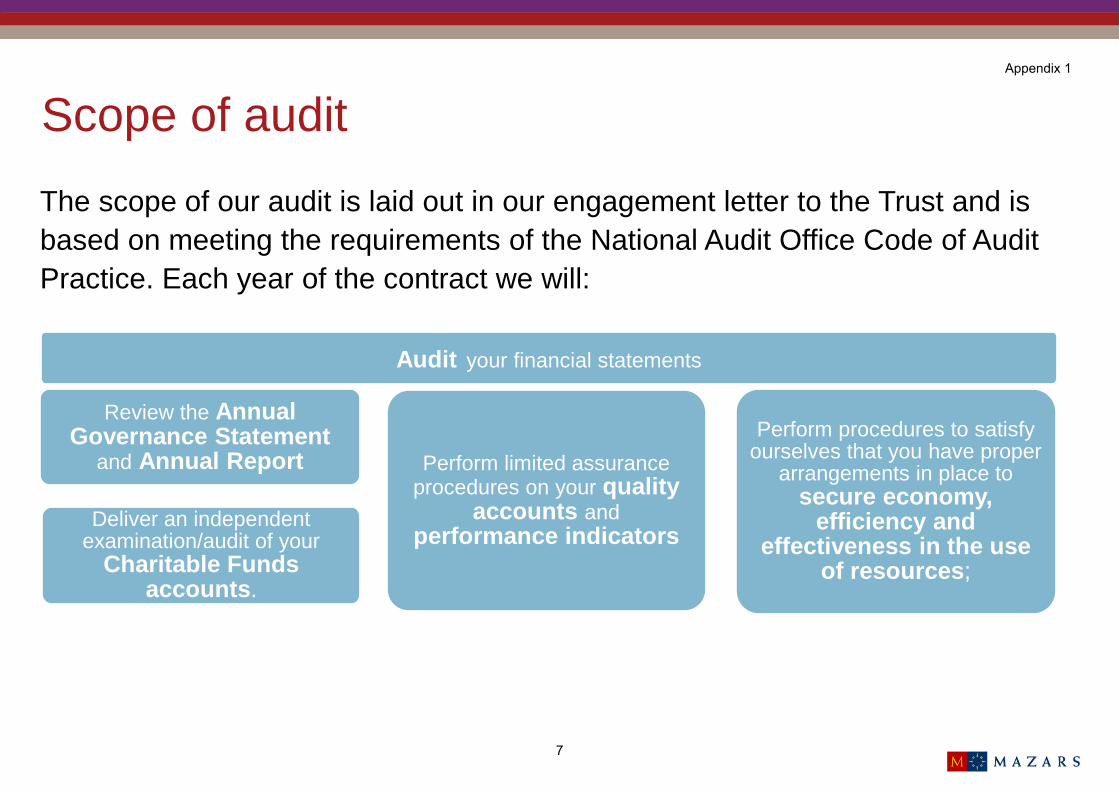

Scope of audit

The scope of our audit is laid out in our engagement letter to the Trust and is based on meeting the requirements of the National Audit Office Code of Audit Practice. Each year of the contract we will:

Audit your financial statements

Perform limited assurance procedures on your quality

accounts and performance indicators

Deliver an independent examination/audit of your

Charitable Funds accounts.

Review the Annual Governance Statement

and Annual Report Perform procedures to satisfy

ourselves that you have proper arrangements in place to

secure economy, efficiency and

effectiveness in the use of resources;

Appendix 1

7

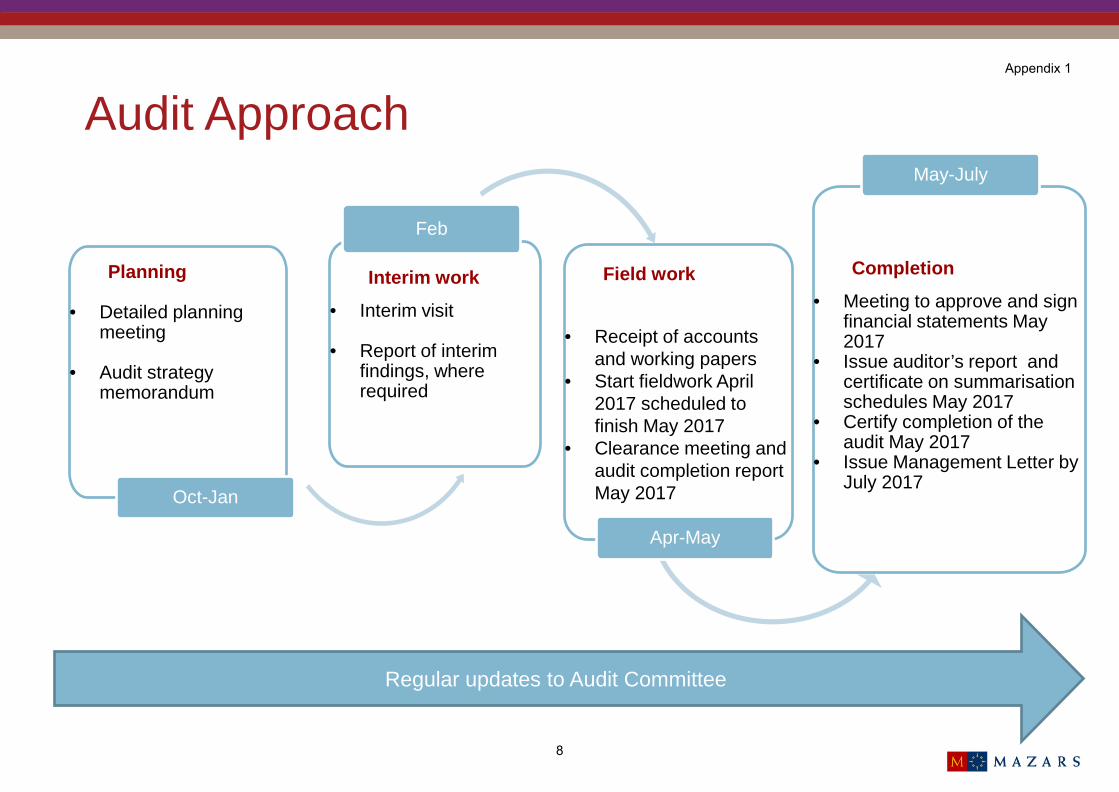

Planning

• Detailed planningmeeting

• Audit strategymemorandum

Oct-Jan

Interim work

• Interim visit

• Report of interimfindings, whererequired

Feb

Field work

• Receipt of accountsand working papers

• Start fieldwork April2017 scheduled tofinish May 2017

• Clearance meeting andaudit completion reportMay 2017

Apr-May

Completion

• Meeting to approve and signfinancial statements May2017

• Issue auditor’s report andcertificate on summarisation schedules May 2017

• Certify completion of theaudit May 2017

• Issue Management Letter byJuly 2017

May-July

Audit Approach

Regular updates to Audit Committee

Appendix 1

8

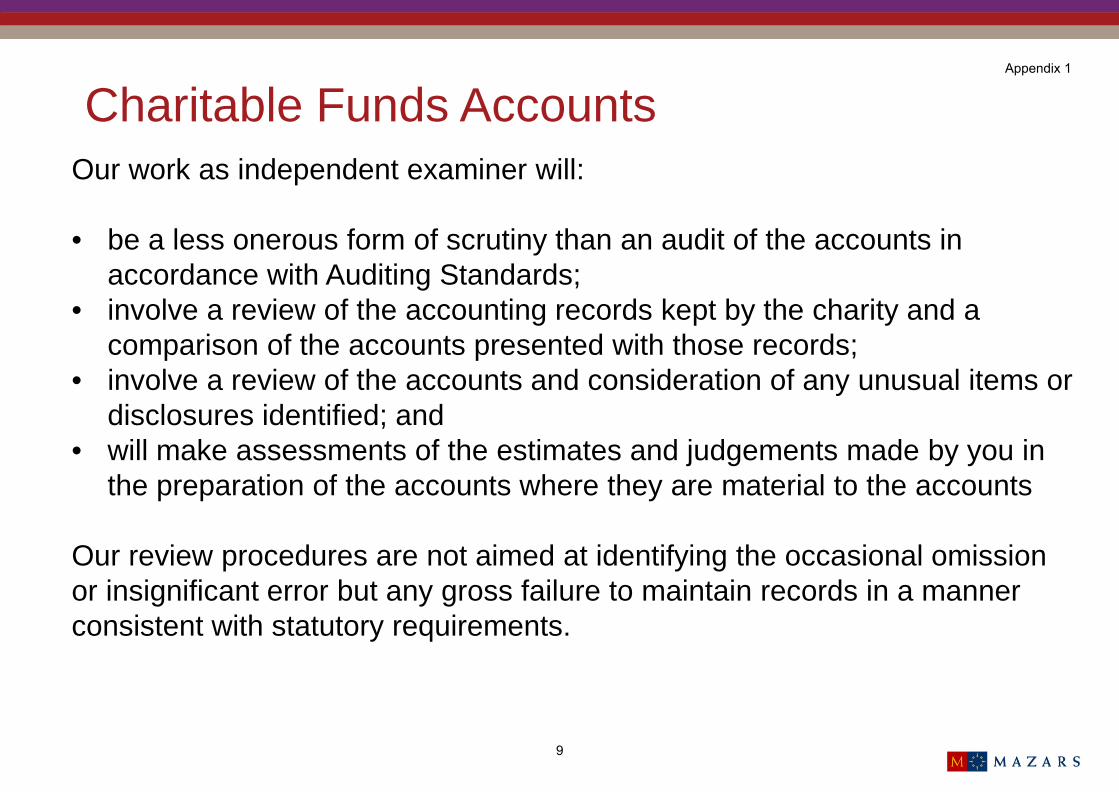

Charitable Funds Accounts Our work as independent examiner will:

• be a less onerous form of scrutiny than an audit of the accounts inaccordance with Auditing Standards;

• involve a review of the accounting records kept by the charity and acomparison of the accounts presented with those records;

• involve a review of the accounts and consideration of any unusual items ordisclosures identified; and

• will make assessments of the estimates and judgements made by you inthe preparation of the accounts where they are material to the accounts

Our review procedures are not aimed at identifying the occasional omission or insignificant error but any gross failure to maintain records in a manner consistent with statutory requirements.

Appendix 1

9

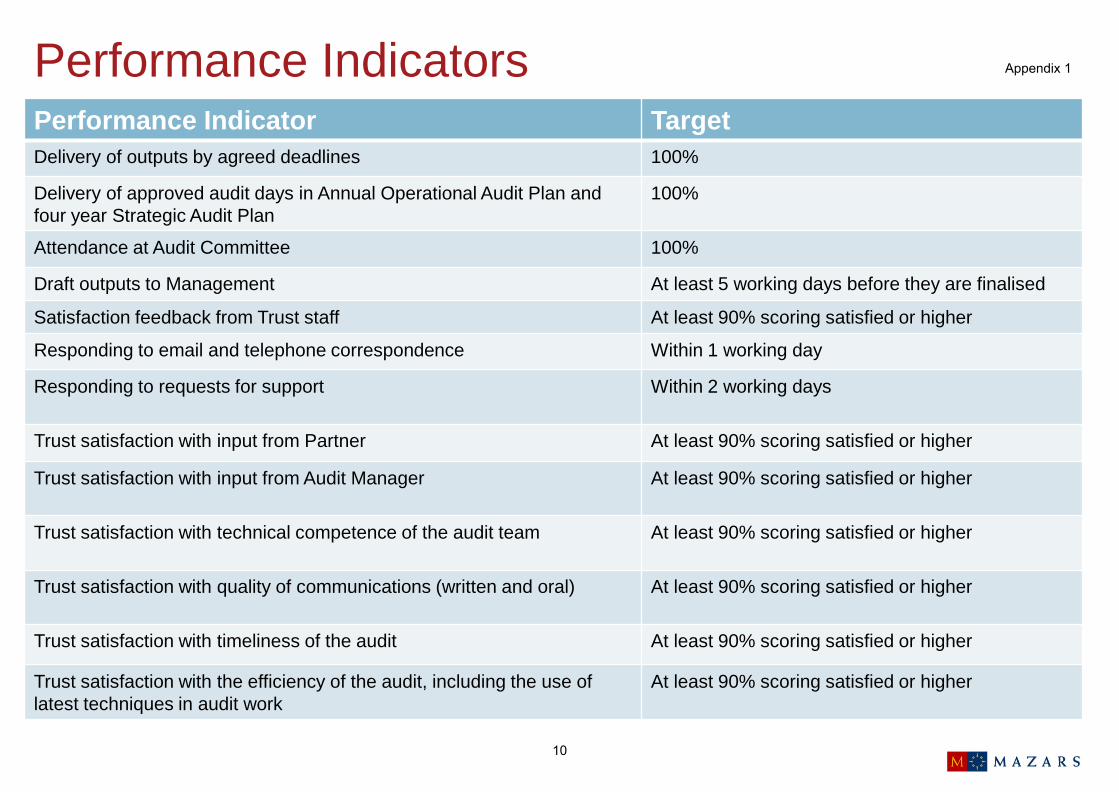

Performance Indicators Performance Indicator Target Delivery of outputs by agreed deadlines 100%

Delivery of approved audit days in Annual Operational Audit Plan and four year Strategic Audit Plan

100%

Attendance at Audit Committee 100%

Draft outputs to Management At least 5 working days before they are finalised

Satisfaction feedback from Trust staff At least 90% scoring satisfied or higher

Responding to email and telephone correspondence Within 1 working day

Responding to requests for support Within 2 working days

Trust satisfaction with input from Partner At least 90% scoring satisfied or higher

Trust satisfaction with input from Audit Manager At least 90% scoring satisfied or higher

Trust satisfaction with technical competence of the audit team At least 90% scoring satisfied or higher

Trust satisfaction with quality of communications (written and oral) At least 90% scoring satisfied or higher

Trust satisfaction with timeliness of the audit At least 90% scoring satisfied or higher

Trust satisfaction with the efficiency of the audit, including the use of latest techniques in audit work

At least 90% scoring satisfied or higher

Appendix 1

10

The contents of this presentation are confidential and not for distribution to anyone other than North East Ambulance Service NHS Foundation Trust. Disclosure to third parties cannot be made without the prior written consent of Mazars LLP.

Mazars LLP is the UK firm of Mazars, an international advisory and accountancy organisation, and is a limited liability partnership registered in England with registered number OC308299. A list of partners’ names is available for inspection at the firm’s registered office, Tower Bridge House, St Katharine’s Way, London E1W 1DD. We are registered to carry on audit work in the UK and Ireland by the Institute of Chartered Accountants in England and Wales. Details about our audit registration can be viewed at www.auditregister.org.uk under reference number C001139861.

© Mazars 2016

Should you require any further information, please do not hesitate to contact:

T:

A:

0191 383 6314

The Rivergreen Centre, Aykley Heads, Durham DH1 5TS

Cameron Waddell, Partner

Appendix 1

11

AuditOne Update

NEAS Audit Committee Meeting 12 October 2016

Appendix 2

1

Agenda

• General update • Restructure • Development strategy • Governance issues

Appendix 2

2

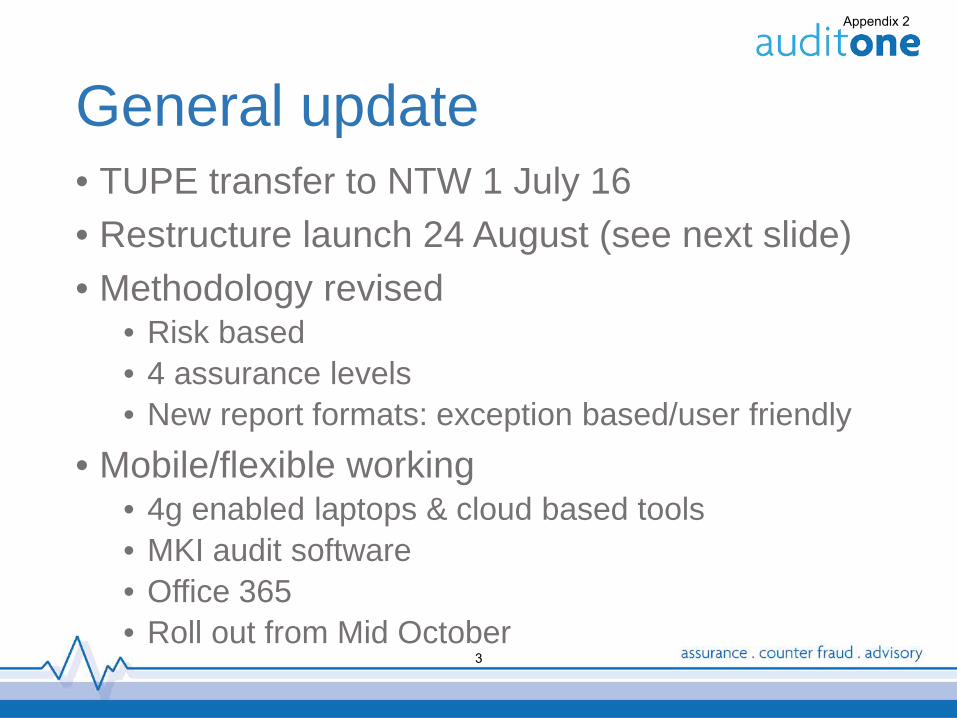

General update • TUPE transfer to NTW 1 July 16 • Restructure launch 24 August (see next slide) • Methodology revised

• Risk based • 4 assurance levels • New report formats: exception based/user friendly

• Mobile/flexible working • 4g enabled laptops & cloud based tools • MKI audit software • Office 365 • Roll out from Mid October

Appendix 2

3

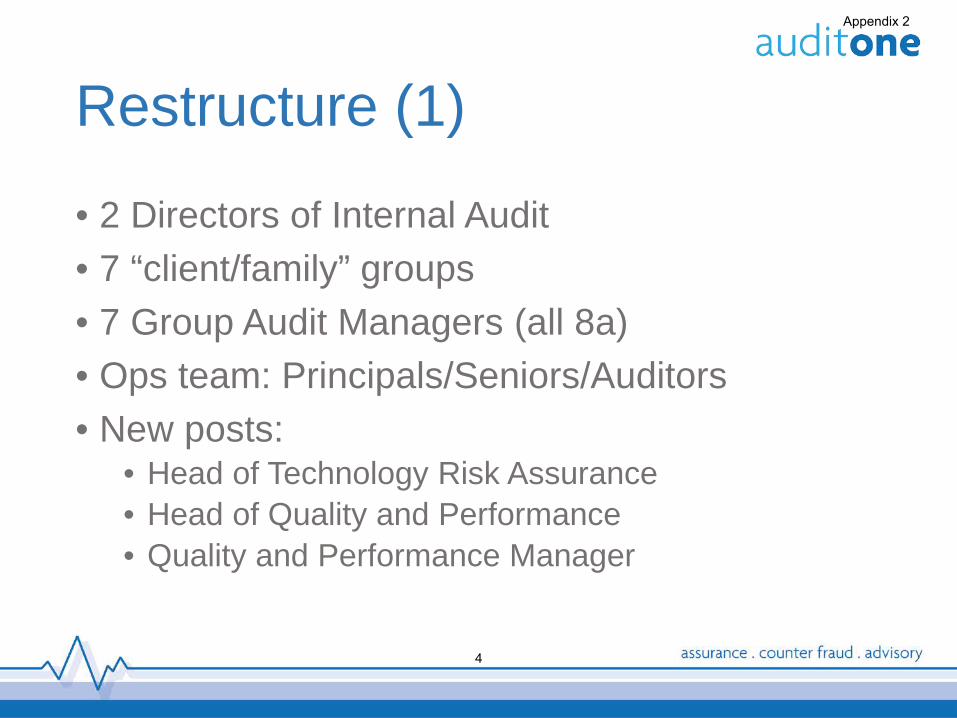

Restructure (1)

• 2 Directors of Internal Audit • 7 “client/family” groups • 7 Group Audit Managers (all 8a) • Ops team: Principals/Seniors/Auditors • New posts:

• Head of Technology Risk Assurance • Head of Quality and Performance • Quality and Performance Manager

Appendix 2

4

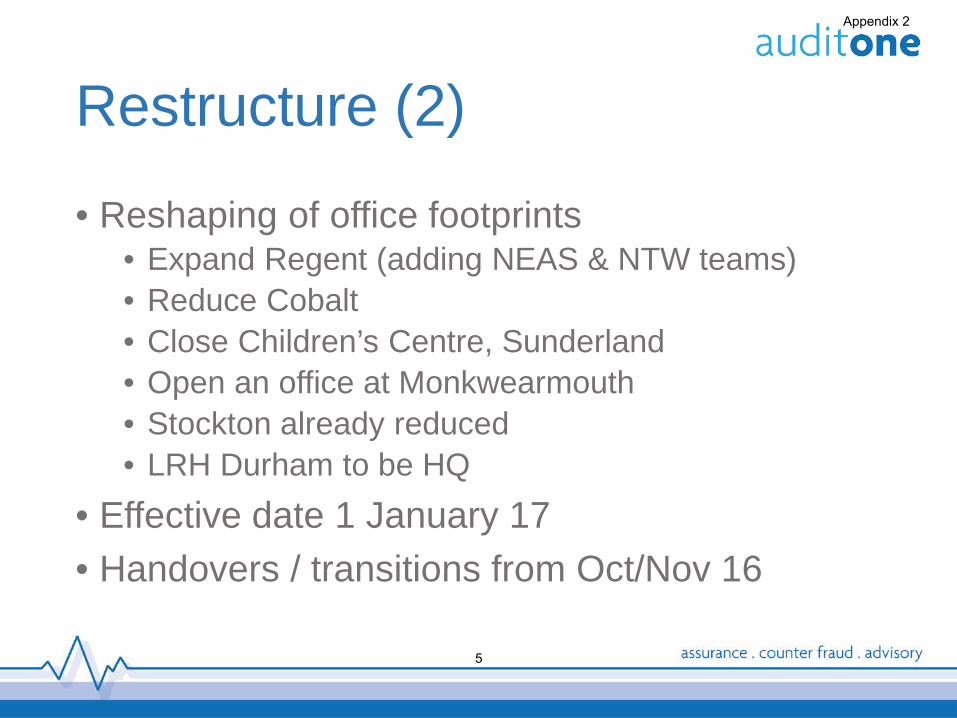

Restructure (2)

• Reshaping of office footprints • Expand Regent (adding NEAS & NTW teams) • Reduce Cobalt • Close Children’s Centre, Sunderland • Open an office at Monkwearmouth • Stockton already reduced • LRH Durham to be HQ

• Effective date 1 January 17 • Handovers / transitions from Oct/Nov 16

Appendix 2

5

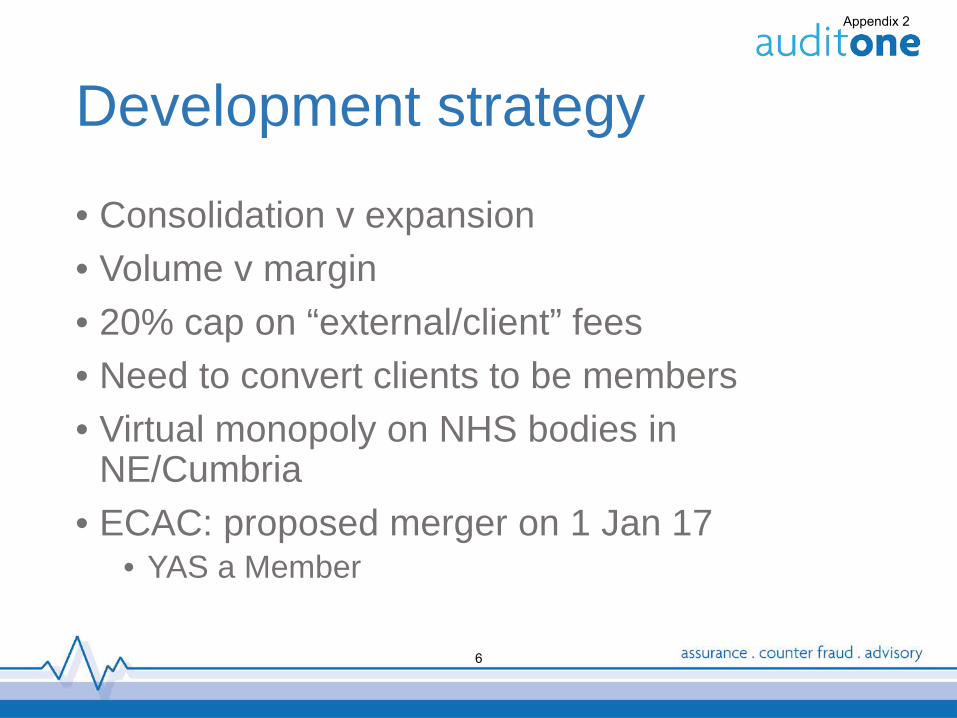

Development strategy

• Consolidation v expansion • Volume v margin • 20% cap on “external/client” fees • Need to convert clients to be members • Virtual monopoly on NHS bodies in

NE/Cumbria • ECAC: proposed merger on 1 Jan 17

• YAS a Member

Appendix 2

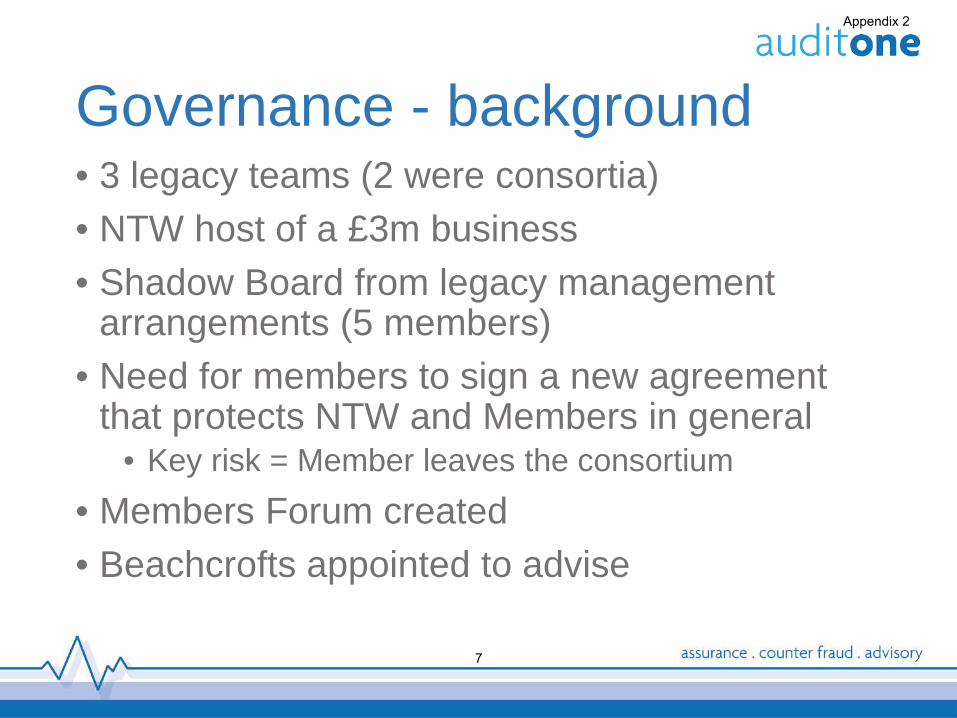

6

Governance - background • 3 legacy teams (2 were consortia) • NTW host of a £3m business • Shadow Board from legacy management

arrangements (5 members) • Need for members to sign a new agreement

that protects NTW and Members in general • Key risk = Member leaves the consortium

• Members Forum created • Beachcrofts appointed to advise

Appendix 2

7

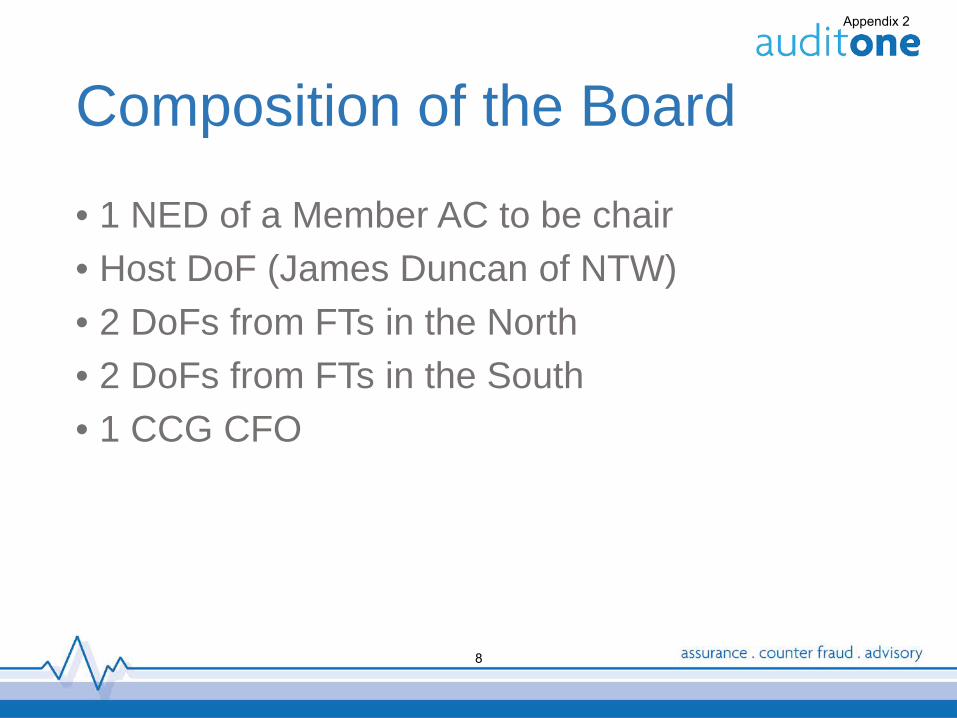

Composition of the Board

• 1 NED of a Member AC to be chair • Host DoF (James Duncan of NTW) • 2 DoFs from FTs in the North • 2 DoFs from FTs in the South • 1 CCG CFO

Appendix 2

8

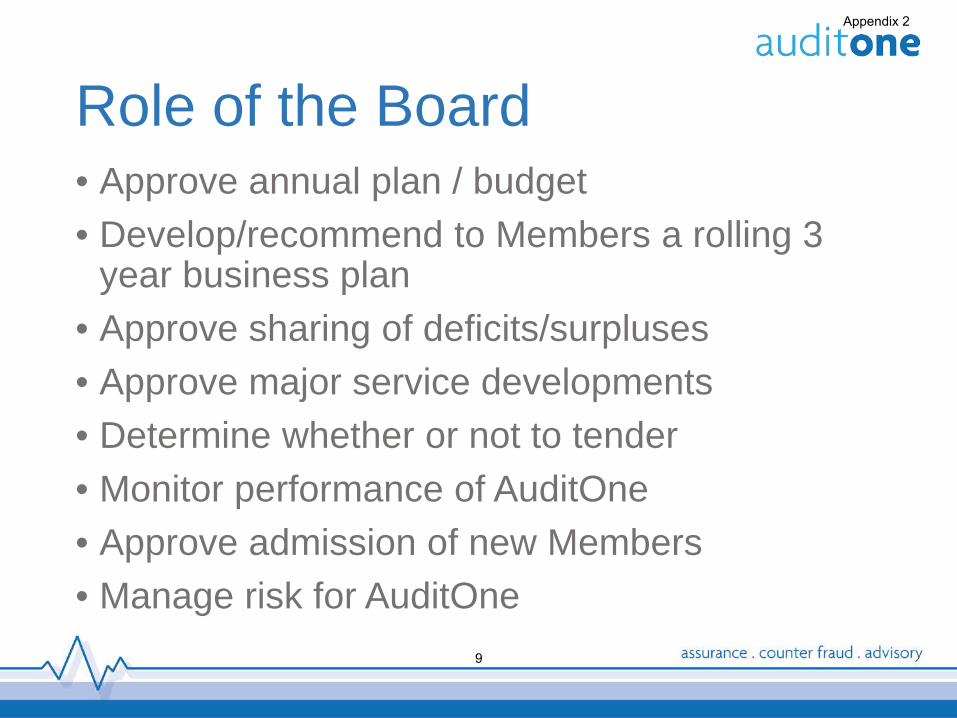

Role of the Board • Approve annual plan / budget • Develop/recommend to Members a rolling 3

year business plan • Approve sharing of deficits/surpluses • Approve major service developments • Determine whether or not to tender • Monitor performance of AuditOne • Approve admission of new Members • Manage risk for AuditOne

Appendix 2

9

Questions

Ian Wallace. Managing Director. [email protected] 07890 525776 www.audit-one.co.uk

Appendix 2

10