-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

1/34

ETHANOL,

,Finally regaining its sweetness SPA Securities Ltd.

October 03, 2013

Rohit Agarwal

Minimum Tariff

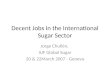

Controls on sector prior to reforms Controls after partial

decontrol

[email protected]. No. 91 33 40114800/ 839

GOVT.POLICIES

Distance Criteria between mills

Cane AreaReservation

rates on trade

40% sugarto be packed in jute bags only

GOVT.POLICIES

Minimum Distance Criteria

between mills

Cane AreaReservation

Levy SugarObligation on

mills

RegulatedRelease

Mechanism

Dual CanePricing:

Centre/State

State Govt. Controls Central Govt. Con

Dual CanePricing:

Centre/StateCompulsory

sugar packingin jute only

Import andExport

State Govt. Controls Central Govt. Controls

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

2/34

SUGAR SECTOR Structurally poised for sweet time

Sensex: 19517 Nifty: 5780

SECTOR INITIATION REPORT

Sharp correction witnessed in sugar stocks have thrown up

significant value buying opportunities for long term investors.

Weinitiate coverage on Balrampur Chini Mills and Shree Renuka

Sugars with an Outperformer rating, our preferred exposure in

theindustry, as they remain best proxies to ride out of the current

sugar cycle. We have selected the companies based on their

competitive positioning on long-term structural factors such as

size, geographical presence, operating efficiencies and we

stronglybelieve that both these companies are geared to capture

emerging opportunities with their integrated business models.

Domestic production to decline by 5% in 2013-14India's sugar

production is expected to decline by 5% to 23.7 mt in 2013-14 after

production of + 24 mt for 3 consecutiveyears (production of +20 mt

for 3 consecutive years has not happened over the past many years).

Sugarcane area is set to fallto the lowest in 4 years to ~4.85

million hectares, 3% lower than last year's 5.0 mh. Moreover rupee

depreciation in additionto squeezing imports has turned exports

viable, thereby further improving the overall demand supply

scenario.

Ethanol Blending Program gains momentum - To completely

transform the industryEBP in India has the potential to transform

the sugar industry given significant visible demand for ethanol

(~1.05 bn litresfor mere 5% blending). Sugar industry has

contracted to supply 0.55 bn litre of ethanol to OMCs @ INR

35/litre by Mar 2014and bidded for supplying further 1.34 bn litre

by Dec 2014. Realisations can increase further given a) the scope

of enhancingethanol prices by ~INR 12/litre at the current petrol

prices and b) lowest price quoted by foreign suppliers are ~INR

75/litre.Assured realisation coupled with the commitment of lifting

of full potential can lead to significant improvement in

profitabilityof sugar producers.

Partial decontrol of sugar - Will lead to rerating of the

sectorWe expect the sector to get rerated over medium to longer

term following the partial decontrol of sector. The GoI has

removedthe levy obligations on sugar and abolished the regulated

release mechanism in April 2013. While removal of levy

obligationwould lead to ~INR 1.3/kg increase in blended realisation

of sugar manufacturers, abolition of regulated release

mechanismwill allow mills to capitalize on better sugar

realizations and better manage their working capital

requirements.

Ray of hope emerging for adoption of cane pricing

formulaKarnataka government has recently enacted an Act prescribing

that the sugarcane price will be based on the revenuesharing model

in line with Rangarajan Committee report (70% of total revenue/75%

of sugar revenue). Maharashtra is alsoreadying to consider a

similar move. We view these policy changes as a game changer for

the entire industry and expect thisto have a positive influence on

UP government. Otherwise these two states, which account for ~49%

of the country's sugaroutput, would out-price UP sugar mills due to

their lower cost of production.

World sugar surplus to decline significantly to 3.5 mt in

2014The global sugar surplus is expected to narrow significantly to

3.5 mt in 2013-14 due to less supply emulating from Brazil,thereby

supporting prices. Total sucrose content diverted for sugar is

expected to decline from 50% in 2013 to 45% in 2014.Given the

ethanol price parity coupled with several encouraging measures

introduced by Brazilian Government, ethanoldemand can significantly

increase in Brazil. This holds importance as 20% increase in

Brazil's ethanol consumption has thepotential to completely

eliminate the world sugar surplus. By 2022, OECD is expecting

ethanol production in developingcountries to increase by 30 bnl to

72 bnl, with Brazil accounting for 80% of this supply increase.

Sugar prices to remain steadyWe expect global prices to bottom

out and find a floor around USD 16 cents/lb, as slump in prices

below these levels will spurBrazilian millers to produce more of

ethanol and less of sugar. Prices are expected to edge up higher

gradually in 2014-15 due tosignificant expected decline in global

sugar surplus. Domestically prices are expected to remain stable

and marginally improvein the short term following abatement of

supply pressure with end of crushing season and an increase in

import duty from 10% to15%. Depreciating Rupee has also made export

realization marginally competitive thereby partly relieving

pressure on stocks.

CompanyCMP MCAP APAT (INR mn) EPS P/E (x) P/BV (x) EV/EBIDTAINR

INR bn FY14E FY15E FY14E FY15E FY14E FY15E FY14E FY15E FY14E

FY1

Balrampur Chini 43 10 1876 1820 7.68 7.45 5.58 5.75 0.73 0.67

5.13 5.25

Shree Renuka Sugars 20 13 922 1943 1.37 2.90 14.56 6.91 0.68

0.63 5.37 4.25

Valuation Summary

Source: SPA Research

World SugarStatistics

Indian SugarIndustry Global Scenario

Sugar PricingOutlookSugar Sector Balrampur Chini

Shree RenukaSugarsContents

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

3/34

TABLE OF CONTENTSWorld Sugar Statistics

...............................................................................................................................................

4

Indian Sugar Industry

...............................................................................................................................................

5-18

Background

...............................................................................................................................................

5

Indian sugar cycle

...............................................................................................................................................

6Domestic demand supply situation

.....................................................................................................................

7-9

Production to remain +24 mt for third consecutive year

..............................................................................

7

Production to decline by 5% in 2013-14

........................................................................................................

8Acreage under Sugarcane to touch four-year low on drought

.......................................................................

8

Export & Import - Ceteris paribus, currency playing an

important role

.............................................................

10

Sugar Manufacturing & Its By-products

..............................................................................................................

11Ethanol Blending Program gains momentum - To completely transform

the industry ....................................... 12

Regulatory

Framework..........................................................................................................................................

14

Partial decontrol of sugar - Leading to rerating of

sector...................................................................................

16Trend in domestic sugar prices

............................................................................................................................

17

Global scenario

...............................................................................................................................................

18-25World sugar dynamics

.........................................................................................................................................

18-19

Main producing countries

..............................................................................................................................

18Main exporting countries

...............................................................................................................................

19

Main importing countries

..............................................................................................................................

19World Ethanol Dynamics

......................................................................................................................................

19-21

Ethanol & Its advantages

................................................................................................................................

19Demand drivers & Growth potential

..............................................................................................................

19Crude oil has little direct impact on ethanol prices

......................................................................................

20So with all of these benefits, is ethanol the fix-all solution?

........................................................................

21

Ethanol from sugarcane stands out

.....................................................................................................................

22

Global demand supply situation - Sugar

.............................................................................................................

23-27Global surplus to decline significantly in 2014

............................................................................................

23

Brazil - The Potential game changer

...............................................................................................................

23

Thailand - Continues to remain 2nd largest

exporter....................................................................................

25Australia: Output to decline by

6.5%..............................................................................................................

26

Mexico - Largest exporter to the United States

...............................................................................................

26China becoming the 'buyer of last resort' for the world sugar

market .........................................................

26Indonesia - Imports expected to more than double

.......................................................................................

26

Russia - Rare setback for world output prospects

.........................................................................................

27

International sugar prices at 3 years low

...........................................................................................................

27

Sugar Pricing Outlook

...............................................................................................................................................

28

Companies Section

...............................................................................................................................................

29-33

Balrampur Chini Mills

..........................................................................................................................................

30-31Shree Renuka Sugars Ltd.

......................................................................................................................................

32-33

Contents World SugarStatistics

Indian SugarIndustry Global Scenario

Sugar PricingOutlook

Balrampur Chini Shree RenukaSugarsSugar Sector

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

4/34

World Sugar Statistics

Sugar is one of the most valuable agricultural commodities. In

2011 its global export trade wasworth $47bn, up from $10bn in 2000.

Of the total $47bn, $33.5bn of sugar exports were fromdeveloping

countries and $12.2bn from developed countries.

About 80% of global production comes from sugar cane (which is

grown in the tropics) and 20%comes from sugar beet (grown in

temperate climates, including Europe).

More than 123 countries produce sugar worldwide, with 70% of the

world's sugar consumed inproducer countries and only 30% traded on

the international market.

Brazil plays an important role in the global sugar market, as

the world's largest sugar producerwith 12-14% recovery rate, the

world's major exporter (contributes 45% of world exports) andone of

the highest per capita consumers, at around 55 kg a year.

Top 5 sugar producers in the world, namely Brazil, India, the

EU, China and Thailand, accountfor over 60% of total

production.

Top 10 sugar producing countries between 2011-13E

Source: USDA FAS Sugar: World Markets & Trade, SPA

Research

The top five consumers of sugar use 51% of the world's sugar.

They include India, the EU-27,China, Brazil and the US.

Asia consumes 45% of world sugar production and produces approx.

36% of world production. World consumption of sugar has grown at an

average annual rate of 2.7% over the past 50

years. It is driven by rising incomes and populations in

developing countries.

Sugar cane cultivation is labour intensive and an important

source of rural employment. TheBrazilian sugar cane industry

employs over 1 million people, or nearly a quarter of the

country'stotal rural workforce. In South Africa - Africa's largest

producer - around half a million peopledepend on sugar for a

living. Sugar mills employ around 15 per cent of workers in

Switzerlandand two-thirds of rural workers in Mauritius.

US 4.42%

Thailand 6.10%

China 7.22%

EU 9.65%

India 16.79%

Brazil 22.15%

Mexico 3.18%

Russia 2.67%

Australia 2.39%

Pakistan 2.44%

India is the second largest producer & largest consumer of

sugar in the world

World sugar consumption growing at CAGR of 2.7% over the past 50

years

World SugarStatistics

Indian SugarIndustry Global Scenario

Sugar PricingOutlookSugar Sector Balrampur Chini

Shree RenuSugarsContents

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

5/34

World Per Capita Consumption of Sugar (kg)

0

1020304050607080

B r a z i l

A u s t r a l i a

T h a i

l a n d

R u s s i a

S o u t h U

S A

P a k i s t a n

I n d i a

C h i n a

W o r

l d

Source: ISMA

Indian Sugar Industry

Background India is the second largest producer and the world's

largest sugar consumer, consuming one-

third more sugar than the EU combined and 60% more than China.

Bulk consumers (soft drink manufacturer, bakeries, confectionary,

hotel and restaurant

consumer) account for 60% of India's mill sugar demand. Low per

capita consumption at 19 kgs against 33 kgs in USA, 40 kgs in

Thailand and Russia and

70 kgs in Brazil. The industry plays a pivotal role in rural

economic development, supporting over about 50

million sugarcane farmer, dependents and agricultural labourer.

About 2.4% of cultivable land is under sugar cane. Sugarcane was

cultivated in over 5 million

hectares in 2011/12, with Uttar Pradesh and Maharashtra

accounting for a combined 65% of the total acreage.

Percentage Share of Indian States in Indias Sugarcane Production

(SY2012)

Source: ISMA, SPA Research

Over 664 sugar factories in India widely dispersed with an

average crushing capacity of roughly3,800 Tonnes Crushed per day

(TCD). Maharashtra, the country's largest sugar producer produced9

MT sugar in 2011-12, followed by UP at 7 mt and Karnataka at 3.8

mt.

Ownership of sugar sector - 55% private sector and 45% in

co-operative & Govt. Sector.

Domestically, six major states namely Uttar Pradesh,

Maharashtra, Karnataka, Tamil Nadu,Gujarat and Andhra Pradesh

contribute to over 85% of the sugar production in the country,

withUP & Maharashtra alone contributing ~62%.

Statewise sugar production as a % of total sugar production

2 6 . 9

% 3 4

. 6 %

1 4 . 6

%

8 . 7 %

7 . 5 %

3 0 . 8 %

3 1 . 6

%

1 2 . 4

%

8 . 8 %

4 . 0 %

4 . 0 %

8 . 4 % 3

. 8 %

3 . 8 %

0%5%

10%15%20%

25%30%

35%40%

UP Maharashtra Karnataka TN Gujarat AP Others

SY201 2 SY20 13 E

Source: ISMA, SPA Research

Other states 1.7%

Haryana 1.3%

Bihar 1.4%

Uttarakhand 1.5%

AP 2.7%

Gujarat 6.3%

Tamil Nadu 6.8%

Karnataka 13.5%

UP 27.4%

Maharashtra 37.4%

World SugarStatistics

Indian SugarIndustry Global Scenario

Sugar PricingOutlook

Balrampur Chini Shree RenukaSugarsSugar Sector Contents

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

6/34

Cane price arrears directly impact the sugar production. Cane

arrears are higher in case of UPbecause of a political SAP and no

relationship with returns on sugar sales.

Cane price arrears during last 5 years

0102030405060708090

SY2007 SY2008 SY2009 SY2010 SY2011 SY2012

I N R

b n

Ut ta r P ra de sh Ma ha ra shtra Indus try

Source: ISMA

The domestic sugar industry is estimated at INR 800 bn in size,

supporting over 5 crore sugarcanefarmers.

Size of Indian Sugar Industry

Area under sugar cane cultivation 5 million hectares

Sugar cane production 340 million tons

Number of sugar mills 664

Average capacity of mills 3800 tons cane per day

Production of sugar 25 mt estimated for season 2012-13

Average per capita 21 kgs of sugar and 6 kgs consumption of

other sweeteners

RefineryRefineries have been set up to process raw sugar subject

to govt

of India's policy for import & exports. Capacity : 4.5

million tons [

season, off-season and stand alone combined ]Source: SPA

Research

Indian Sugar CycleA typical feature of the sugar market in India

is the cyclical nature of production, where 2-3 yearsof surplus are

followed by 2-3 years of deficit. Against this backdrop of

recurrent large swings inproduction, consumption growth has been

linear, growing steadily at about 4% per year over thepast 10

years. This results in huge swings in overall sugar

equilibrium.

The year-wise swings: Since 2000-01

Period No. of seasons Production Range (mt) Swing from previous

high/low (mt) Swing %

00-01 to 02-03 3 18.5 to 20.1

03-04 to 04-05 2 12.7 to 13.5 (-) 6.6 (-)32.8%

05-06 to 07-08 3 19.3 to 28.4 (+) 14.9 (+)110.4%

08-09 to 09-10 2 14.5 to 18.9 (-) 9.5 (-) 33.5%

10-11 to 12-13 3 24.0 to 26.2 (+) 7.3 (+) 38.6%

Source: SPA Research

Monsoon plays a key role in sugar production as sugarcane yields

are greatly affected by the levelof rainfall, notably during the

critical monsoon season. The other most important factor is

thedomestic sugar policy that amplifies the cycle through its

impact on incentives along the sugarvalue chain, including for

farmers and sugar factories.

Source: SPA Research

Maharashtra

Orissa

Gujarat

K a r n

a t a k

a Andhara

T a m i l N

a d u

K e r

a l a

West Bengal

Bihar

UttarpradeshRajasthan

Punjab

Haryana

Jamu & Kashmir

Himachal

Uttaranchal

Sikkim

Madhya Pradesh

J h a r k h a n d

C h h a

t t i s g a r

h

Assam Nagaland

ArunachalPradesh

MeghalayaManipur

TripuraMizoram

Sugar Producing States of India

High

Medium

Low

Cane price in UP has gone up by 70% in the last 3 years, but

sugar prices have increased by just 11% in the same period

While consumption is growing @ 4% over last 10 years, production

is cyclical

Contents World SugarStatistics

Indian SugarIndustry

Global Scenario Sugar Pricing

OutlookSugar Sector Balrampur Chini

Shree RenuSugars

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

7/34

The cyclicality of sugarcane production causes large swings in

the area under cultivation of sugarcane and hence its availability

to the sugar industry. During the stage of high

sugarcaneproduction, profitability of sugar manufacturers decline

due to lower realisations, resulting inuntimely payments to the

farmers and increasing cane arrears. As a result, farmers reduce

theirsugarcane acreage and opt for other crops, which can give them

higher returns. Consequently, itleads to lower sugarcane production

and supply deficit of sugar in the market, leading to declinein

sugar prices. This again improves their profitability and enables

them to clear the arrears. Asthe incidence of default declines,

sugarcane cultivation becomes attractive once more, shifting

thedomestic sugar balance into the upside phase of the cycle. Over

a period of time there isoverproduction and the prices fall again.

Thus, the infamous 'Indian Sugar Cycle' is set in motionagain. For

instance, after an increase in 2006/07 to 28.4 mt, 41% over the

record 2002/03 crop,sugar output declined to 14.5 mt in 2008/09 and

is currently estimated at 24 mt for 2012/13.

Higher production leading to accumulation of cane arrears

18.5 18.5 20.1

13.5 12.7

19.3

14.5

18.9

24.4 26.0 25.028.4 26.4

16.728.2

51.9

12.327.2

43.2

85.7

127.0

23.29.78.8

20.830.5

0

5

10

15

20

25

30

S Y 2 0 0 1

S Y 2 0 0 2

S Y 2 0 0 3

S Y 2 0 0 4

S Y 2 0 0 5

S Y 2 0 0 6

S Y 2 0 0 7

S Y 2 0 0 8

S Y 2 0 0 9

S Y 2 0 1 0

S Y 2 0 1 1

S Y 2 0 1 2

S Y 2 0 1 3 E

020406080101214

Produc ti on (mt) Cane Ar rea rs (INR bn ) RHS

Source: ISMA, Directorate of Economics & Statistics, SPA

Research

Domestic demand supply situation

Production to remain +24 mt for third consecutive yearIndia's

sugar production has increased by 6.6% in 2011-12 (Oct-Sep) to 26.0

mt from 24.4 mt in theprevious year. Drought in Maharashtra,

India's biggest sugar producing state, in the last year islikely to

pull down India's overall sugar production by 3.8% to 25.0 mt in

2012-13. This will be thethird consecutive year that sugar

production will remain more than 24 mt due to remunerativecane

prices vis a vis other crops. Production of more than 20 mt for 3

consecutive years has nothappened over the past many years and only

cumulative exports of 7.3 mt in 2011 and 2012 havehelped lower

domestic inventory.

Domestic Sugar Balance

(Million Tones) F2006 F2007 F2008 F2009 F2010 F2011 F2012

F2013E

Opening Stock 5.7 5.4 12.2 12.7 7.7 7.7 5.0 4.5

Production 19.3 28.4 26.4 14.5 18.9 24.4 26.0 25.0Growth YoY

51.8% 47.2% -7.0% -45.1% 30.3% 29.1% 6.6% -3.8%

Internal Consumption 18.5 19.9 20.9 21.7 22.8 23.3 23.0

23.5Growth YoY 3.2% 7.6% 5.0% 3.8% 5.1% 2.2% -1.3% 2.2%Exports 1.1

1.7 5.0 0.2 0.2 3.8 3.5 0.5

Imports 0 0 0 2.4 4.1 0 0 1Closing Stock 5.4 12.2 12.7 7.7 7.7

5.0 4.5 6.5

Stock to use ratio 29.2% 61.3% 60.8% 35.5% 33.8% 21.5% 19.6%

27.7%

Source: ISMA

U p c y

c l e

( 2 3 y

e a r s )

D o w n

c y c l e

( 2 3 y

e a r s )

Low canearrears/High

canecultivation

High caneproduction

High sugarproduction

Decline insugar prices

Lowerprofitability

High canearrears

Decline in areaunder

Cultivation

Lower caneproduction

Lower sugarproduction

High sugarprice/

Improvedprofitability

We are here

Higher production leads to depressed sugar prices, resulting in

higher cane arrears

Indian Sugar Cycle

Source: SPA Research

Contents World SugarStatistics

Indian SugarIndustry Global Scenario

Sugar PricingOutlook

Balrampur Chini Shree RenukaSugarsSugar Sector

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

8/34

Production in two sugarcane growing states of Maharashtra and

Karnataka (which togetheraccounted for 49% of India's sugar

output), is expected to decline by 12.2% and 18.4% to 7.9 mt and3.1

mt respectively in 2012-13. Un-favourable climatic conditions have

negatively impactedsugarcane acreage and sugar production in

Karnataka and Maharashtra, where sugar recoveriesat 10.9% and

11.3%, respectively, are among the highest in the country. The loss

in these two Statesis expected to be made up by India's top sugar

producing state, Uttar Pradesh, where farmersbuoyed by higher

returns last year have planted cane on an additional area of 2.2

lakh hectares(lh). Production in UP is expected to increase around

10.0% to 7.7 mt in the current season.

State wise sugar production (mt)

7.09.0

3.8 2.3 2.07.7 7.9

3.1 2.2 2.11.01.0 1.01.0

28.8% 33.1%

13.5%8.7%

3.9% 3.9% 7.9%

0

24

68

10

U P

M a h a r a s h t r a

K a r n a t a k a T N

G u

j a r a t

A P

O t h e r s

0%5%10%15%20%25%30%35%

SY2012 SY2013E % of total production (Avg.)

Source: ISMA, SPA Research

Production to decline by 5% in 2013-14Early and above normal

rains have curtailed damages to some extent and now sugar

production isexpected to decline by 5% to 23.7 mt in 2013-14.

Importantly some of the farmers have alreadyswitched to other crops

inspite of higher cane prices due to water unavailability as unlike

othercrops sugarcane production requires abundant water. Production

is expected to decline by 25.3%and 12.9% to 5.9 mt and 2.7 mt in

Maharashtra and Karnataka respectively in SY2014.

Acreage under Sugarcane to touch four-year low on

droughtSugarcane is the India's third largest crop, next to rice

and wheat. The sugar yield is not onlyrelated to the industry's

manufacturing capacity but also to the availability of sugarcane.

Acreageunder Sugarcane has not increased much in the last 10 years.

In fact there is a huge fluctuation inarea under cultivation

because of the uncertainty over payments from the millers and

erraticmonsoon, which prompts farmers to shift to other crops. Area

under cane cultivation was the

highest ever (5151 thousand hectares) in the year 2006-07. The

yield per hectare was also thehighest that year.

Contents World SugarStatistics

Indian SugarIndustry Global Scenario

Sugar PricingOutlookSugar Sector Balrampur Chini

Shree RenuSugars

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

9/34

Area under sugarcane production & Recovery trend

Source: ISMA, Directorate of Economics & Statistics, SPA

Research

The total cane area across the country is set to fall to the

lowest in four years to ~4.85 millionhectares (mh), 3% lower than

last years 5.0 mh. That's the lowest since the 2009-2010 seasonand

below the government' s target of 5.3 mh for this year. However,

early monsoon and properdistribution of rains have eased some

concerns over sugar cane acreage for sugar season2013-14.

Though India is among the largest producer of sugarcane, yield

from the crop and sugar recoveryis ~66 tonne per hectare and 10.2%,

respectively, which is much lower than the world average.

Also,there is a high variation in the yield within the country

across different regions. This is mainlybecause of variation in the

climatic conditions prevailing in the country. The average cane

yield intropical region is about 85.1 tonnes while in the

subtropical region, it is only about 60.7 tonnes perhectare.

Despite Maharashtra and Uttar Pradesh being the top two Indian

states in terms of thearea under cultivation as well as their

contribution to sugar production in India, Tamil Nadu hasthe

highest yield of 103 tonnes per hectare in 2011-12. The second

place in productivity is taken byWest Bengal, followed by

Karnataka. Uttar Pradesh, with the largest area under cultivation,

ranks14th in productivity.

Percentage Share of Indian States in Area under Sugarcane

Cultivation

Other states 2.1%Punjab 1.4%MP 1.4%Haryana 1.8%Uttarakhand

2.3%Bihar 2.8%

AP 3.8%

Gujarat 4.6%

Tamil Nadu 7.5%

Karnataka 7.8%

Maharashtra 17.5%

UP 47.1%

Source: ISMA, SPA Research

010203040506070

80

SY02 SY03 SY04 SY05 SY06 SY07 SY08 SY09 SY10 SY11 SY12 SY13E

Sugar Production (In mt) Sugarcane Area (In lac ha) Sugarcane

Production (in 10 mt)

Sugarcane Yield (In mt/ha) % Sugar Recovery

Cane plantation set to fall to the lowest in four

years to ~4.85 mh, 3% lower than last years 5.0mh and below the

government's target of 5.3mh for this year

Cane Yield & Sugar Recovery (2011-12)Regions Area Cane

Sugar

('000 ha) Yield (t/ha) Rec.(%)TropicalMaharashtra 9 40 80.1

11.3Karnataka 410 90.3 10.9Gujarat 203 70.2 10.5TN 333 102.8 9.1AP

200 82.0 9.8Sub-tropicalUP 2277 59.6 9.1

Bihar 235 51.5 9.3Punjab 84 58.4 8.8Haryana 107 73.3 9.0

Source : Cooperative Sugar Journal, November, 2012 SPA

Research

Contents World SugarStatistics

Indian SugarIndustry Global Scenario

Sugar PricingOutlook

Balrampur Chini Shree RenukaSugarsSugar Sector

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

10/34

Export & Import - Ceteris paribus, currency playing an

important roleIndia's status as a net importer or exporter

frequently changes as a result of imbalances causeddue to cyclical

nature of production, with imports exceeding 2 mt during the

deficit phase of thecycle, replaced by large exports during the

surplus phase.

Import & Exports across cycles

-2.00

-0.20-0.94 -1.00

-0.40 -0.12 -0.33

-2.14 -2.40

-4.08

0.000.360.41

0.01 0.061.02

0.42 0.07 0.02 0.070.99 1.08

1.77

0.27 0.00

1.111.73

4.90

0.17 0.24

2.603.

-5

-4-3-2-10123456

1 9 9 1

- 9 2

1 9 9 2

- 9 3

1 9 9 3

- 9 4

1 9 9 4

- 9 5

1 9 9 5

- 9 6

1 9 9 6

- 9 7

1 9 9 7

- 9 8

1 9 9 8

- 9 9

1 9 9 9

- 0 0

2 0 0 0

- 0 1

2 0 0 1

- 0 2

2 0 0 1

- 0 3

2 0 0 3

- 0 4

2 0 0 4

- 0 5

2 0 0 5

- 0 6

2 0 0 6

- 0 7

2 0 0 7

- 0 8

2 0 0 8

- 0 9

2 0 0 9

- 1 0

2 0 1 0

- 1 1

Import (mn tn) Exports (mn tn)

Source: ISMA, SPA Research

In addition to the infamous Indian Sugar Cycle, currency factor

and global fundamentals alsoinfluences the Indian trade scenario.

After exporting ~3.5 mt of sugar last year, Indian exports

havesuffered drastically this season on the back of weak

international prices which has made overseasshipments unviable.

Importing sugar has mostly been unviable for the domestic

players as the landed cost (import dutyof 15% + freight charges+

handling charges) of sugar is largely higher that domestic prices.

However

given the sharp decline in global sugar prices to three years

low, Indian players has alreadyimported ~0.7 mt of sugar till date

in this season despite holding comfortable stocks which hasresulted

in a downward pressure on domestic sugar prices. However with the

increase in importduty from 10% to 15% coupled with sharp

depreciation of rupee, the prospects of further importsseems

limited at the moment.

Moreover rupee depreciation in addition to squeezing imports has

turned exports viable. Givenlow international prices at this point

in time, it is extremely favorable for export from costalmillers.

In fact, Indian traders have signed deals at $ 500-501 per tonne

(FOB) to export 75,000tonnes of white sugar in July, on the back of

strong demand in Gulf and African states due to theIslamic fasting

month of Ramadan. This in addition to already lower sugar

production forecast forSY14, will lead to further tightening in

domestic sugar availability, thereby presenting a bullish

scenario from overall demand supply perspective.

Despite weak international prices, rupeedepreciation in turning

exports viable

Contents World SugarStatistics

Indian SugarIndustry Global Scenario

Sugar PricingOutlookSugar Sector Balrampur Chini

Shree RenuSugars

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

11/34

Sugar Manufacturing & Its By-products

By-products - An integral part of industryIn sugar manufacture,

the major byproducts comprise of bagasse, molasses and press-mud,

whichare utilized to generate power and produce industrial

alcohol/ethanol and fertilizers. The byproducts

account for about ~40% of crushed sugar cane by weight. India

has achieved considerable progressutilising these by-products.

A) BagasseThe fiber (30-33% per tonne of sugarcane crushed)

derived from crushing sugarcane is known asbagasse. Bagasse is used

as a combustible in furnaces to produce steam which is used

togenerate power. The power generated is used in processing

sugarcane and surplus power issupplied to the grids.B)

MolassesMolasses is used primarily for production of rectified

spirit and extra neutral alcohol. It accountsfor ~5% per tonne of

sugarcane crushed. Alcohol serves as raw material for industrial

manufactureof potable alcohol and fuel ethanol. Sugarcane is

generally regarded as one of the most efficientsources of biomass

for bio fuel (ethanol) production. The demand of ethanol is

generated due to itscompulsory blending with petrol.

C) Organic manureOrganic manures accounts for around 3%-5% of

the sugar cane crushed. Sulphitation press mud ismainly used as

manure. The press mud organic manure is free of inorganic elements

present in thetraditional form of organic manures, commonly used by

the farming community. Crops yield goodresults when applied during

early land preparation. It increases soil porosity and helps the

cropin the uptake of chemical fertilisers (NPK).

Cane Milling / Crushing

Juice Defecation & Clarification

Juice Sulphitation

Syrup Boiling

Centrifuging

Factory Raw SugarDistillery

Alcohol Fermentation

MolassesSpent Wash

Bio-Composting

Press Mud

Cogeneration

To Factory

To Grid

Power Steam BagasseTurbines Boilers

Weighed & Prepared Cane

Sugar Plant

Source: SPA Research

Production of Molasses (mt)

SY07 13.1

SY08 11.3

SY09 6.5

SY10 8.4

SY11 10.7

SY12 11.5

Source: SPA Research

Source: SPA Research

Sugarcane By-products

Press mud4%

Molasses5%

Sugar10%

Water51%

Bagasse30%

Manufacturing ProcessThe process of manufacturing sugar starts

with pressingof sugarcane to extract the juice. It is followed by

boilingthe juice resulting in thickening of the juice and

sugarbegins to crystallize. The crystals are spun in acentrifuge to

remove the syrup, thereby producing rawsugar.

The raw sugar is then transported to a refinery where itis

washed and filtered to remove remaining non-sugaringredients and

colour. It is then followed bycrystallization, drying and resultant

packaging of therefined sugar.

Contents World SugarStatistics

Indian SugarIndustry Global Scenario

Sugar PricingOutlook

Balrampur Chini Shree RenukaSugarsSugar Sector

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

12/34

A significant part of the total revenue and profits of sugar

mills comes from by-products, especiallyin the case of forward

integrated entities. In down-cycle these products act as a savior

to bottomlinede-risking the business model. Greater the level of

integration, better is the ability to wither thedownturn and

de-risk the business model from cyclicality.

Most of the sugar mills are integrated having power generation

and facility for alcohol production.The forward integrated model

aids in generating enhanced realisations and optimum

resourceutilisation.

We feel by-products will remain important part of the industry

due to improving macro scenariofor these products. Prices of

by-products such as bagasse and molasses continue to

remainremunerative driven by healthy demand from consuming sectors

such as power, paper and alcohol.Higher realizations for fuel

ethanol in the current financial year will further result in

improvedreturns from by-products.

Ethanol Blending Program gains momentum To completely transform

the industryIn November 2012, the Cabinet Committee on Economic

Affairs (CCEA) has made it mandatory forthree major oil marketing

companies (OMCs) - Bharat Petroleum, Hindustan Petroleum and

IndianOil Corporation to blend 5% ethanol with petrol. Although

this mandate has been there since last twoyears, it was partially

implemented due to the absence of any clear directive and largely

due to lowprocurement price of INR 27/litre fixed by the CCEA in

August 2010. To remove this bottleneck, thecommittee has approved

market-based pricing of ethanol (to be implemented from June 2013)

as aresult of which sugar producers will willingly supply ENA at

market determined price. This hasresulted in Ethanol Blending

Program (EBP) gaining momentum and it can potentially transform

theindustry given significant visible demand for ethanol (~1.05 bn

litres for 5% blending with petrol).

OMCs have floated first tender for 1.1 bn litres of ethanol in

Jan 13, out of which they could finaliseprocurement of only 0.55 bn

litres at an average price of INR 35/litre from domestic sugar

companies(to be supplied in the current sugar year ending

September), as most the sugar mills have alreadycontracted for the

supply of molasses and rectified spirits for producing potable

achohol. Importantlyto meet the gap OMCs floated a global tender to

import 0.50 bn litres, but the lowest price quoted byforeign

suppliers of ethanol was about ~INR 75 a litre, double the

preferred domestic quote. Thisresulted in OMCS floating second

domestic tender to procure 1.34 bn litres of ethanol between

theperiod 1st Dec 2013 to 30th Nov 2014, which was fully met by

sugar companies. Moreover in thesecond tender prices offered might

be higher because of high imported cost and 5% increase insugarcane

price by central government in FRP regime. Assured realisations

coupled with thecommitment of lifting of full potential will

positively impact the profitability of sugar producers.

Out of the world's total ethanol production, around 80% is used

for fuel purpose. However Ethanolmarket in India is driven more by

beverage alcohol market rather than fuel alcohol market unlike

restof the world. Newer players especially global alcohol majors

are entering Indian market seeing thegrowth opportunities and the

beverage alcohol investment is not showing any slow down.

Taking clues from the way the sugar industry has diversified in

Brazil, it is high time that Indiastarts planning for radical

shifts in the sugar alcohol production combinations, so that we

meetat least a part of the domestic requirements of petrol. This

would help in saving valuable foreignexchange outgoes and in

reduction of current account deficits, which have been of concern

in thecountry. As indicated in table given below, there is scope

for enhancement of ethanol prices by amargin of INR 11-12 per unit

at the current petrol prices and more than that there is a sound

casefor premium pricing on ethanol due to its renewable/green

status.

By products de-risk the business model & actsas savior to

the bottomline during the down

cycle

Free pricing will help to implement the ethanol blending

programme

Overseas players offering ethanol at INR 75/ litre, double the

domestic offer price

Need to change the sugar - alcohol productioncombination

Contents World SugarStatistics

Indian SugarIndustry Global Scenario

Sugar PricingOutlookSugar Sector Balrampur Chini

Shree RenuSugars

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

13/34

Price Comparison @ Rs 59 per USD as on 24th June'13 for imported

Petrol and domestic Ethanol

Sr.No Particulars Unit Petrol Ethanol Remarks

1 FOB Gasoline Price at Arab Gulf $/bbl 111.79 - Calculated2

Add: Ocean Freight from AG to Indian Ports $/bbl 2.06 -

Assumed for Petrol as takenfor Diesel

3 C&F (Cost & Freight) Gasoline Price $/bbl 113.85

-Taken from IOCL website ason 16th June'13

C&F (Cost & Freight) Gasoline Price Rs/Lit 41.98 - At Rs

59 per USD

4 Import Charges Rs/Lit 0.40 -Assumed for Petrol as takenfor

Diesel

5 Bas ic Customs Duty @ 2.575% (2 .50% +Rs/Lit 1.11 -

Assumed for Petrol as taken3% Education cess) for Diesel

6 Import Parity Price (at 29.5 C)Rs/Lit 43.49 -(Sum of 3 to

5)

7 Export Parity Price (at 29.5 C) Rs/Lit 42.31 - Calculated8

Trade Parity Price (80% of (6)+20% of (7)) Rs/Lit 43.26 -

9Refinery Transfer Price (RTP)

Rs/Lit 43.26 35.00 Calculated(Price Paid by the Oil

MarketingCompanies to Refineries)

10 Add: Excise Duty & Cess @ 12.36% Rs/Lit - 4.33

11 Add: Freight Rs/Lit - 2.76Freight may vary from Depotto

Depot

12Add: Premium recovered for BS-IV Grade

Rs/Lit - -over BS-III Grade

13 Add: Inland Freight, Delivery Charges etc. Rs/Lit 0.95

-Assumed for Petrol as takenfor Diesel

14 Add: Marketing Cost of OMCs Rs/Lit 0.69 0.69 Calculated15

Add: Marketing Margin of OMCs Rs/Lit 0.67 0.67 Calculated

16Total Desired Price (Sum of 9 to 15)-Before Excise Duty, VAT

and DealerCommission

Rs/Lit 45.57 - Calculated

17Price Charged to Dealers (17-18)-

Rs/Lit 45.57 - CalculatedExcluding Excise Duty & VAT

18 Add: Specific Excise Duty & Cess Rs/Lit 9.48 -@ Rs 9.48

per Lit- Petrol

19 Sub-Total Rs/Lit 55.05 43.45Difference b/w Petrol

&Ethanol- Rs 11.60 per Lit

20 Add: Dealer Commission Rs/Lit 1.79 1.79It may vary from state

tostate

21 Add: VAT Rs/Lit 11.37 11.37Tax remains same as ethanolwill be

sold as petrol

22 Add: Cess & Service Tax- Ethanol Rs/Lit 1.01 1.01As per

invoice taken fromHPCL petrol pump

23Retail Selling Price at Delhi -

Rs/Lit 69.21 57.62Rounded off (Sum of 18 to 24)

Source: Report of the Working Group on Sugarcane Productivity

and Sugar Recovery in the Country, SPA Research

Crushing of 1 ton of sugarcane yields either a) 100kg Sugar

along with 11 litres Ethanol, or only 76

litres of Ethanol. This results in a price parity of 1:1.53

between Ethanol and Sugar. Hence dependingupon the prevailing

prices, sugar manufacturers will enjoy the flexibility to divert

sugar capacity toethanol production.

Scope for enhancement of ethanol prices by amargin of INR

11-12/Lit remains

Contents World SugarStatistics

Indian SugarIndustry Global Scenario

Sugar PricingOutlook

Balrampur Chini Shree RenukaSugarsSugar Sector

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

14/34

Regulatory Framework

The Indian sugar industry is one of the most regulated

industries. Till few months back, its entiregamut of activities

starting from procurement of sugarcane and ending with the sale of

sugar weregoverned by Indian government. However after years of

deliberation, Indian government has finallydecontrolled the sugar

sector albeit partially, in April 2013. The major pertinent

regulations andpolicies still adopted by the Government are given

below:

Source: SPA ResearchDual sugarcane pricing (FRP/SAP)The industry

is subject to fair and remunerative price (FRP) for sugarcane fixed

by the CentralGovernment from year to year, taking into account

cost of production of sugarcane, return togrowers from alternative

crops, fair consumer price of sugar, etc.

In addition to the FRP, 5 States in the country viz. UP,

Haryana, Punjab, Uttarakhand and Tamil Nadu(together accounting for

~38% of total sugar production), fixes a price (generally higher

then FRP)known as the State Advised Price/SAP (on political

considerations, without any transparent laiddown criteria and no

relation to sugar price). Dual cane pricing distorts cane and sugar

economyand is contributing majorly to cane price arrears and

cyclicality. This is very unlike than all themajor sugar producing

nations in the world like Brazil, Australia and Thailand, where

there is adirect linkage between sugarcane and the sugar prices.

Sugarcane growers revenue share in thetotal industry revenue is

62-67% in Australia; 56-61% in Brazil and 70% plus in Thailand.

A look at the sugar economy and growth of sugar sector,

including investments in the farm and factory,will clearly

distinguish states following SAP from the others like Maharashtra,

Karnataka, Gujarat etc,which have never followed the system of SAP.

The sugar sector therein has grown in leaps and boundsin comparison

to the SAP States, where either the growth is flat or negative. A

higher price for cane issustainable only if the sugar recoveries

compensate for the high costs, like for Maharashtra or

Karnataka,but not if the recoveries are the lowest in the country,

as for example in UP.

Share of cane price as perce ntage of ex mill sugar price

48.5

66.5 64.857.1

81.4

81.277.3

64.7

75.968.8

86.496.4

83.7 79.1

70.9 73.0

40

50

60

70

8090

100

SS05 SS06 SS07 SS08 SS09 SS10 SS11 SS12

%

UP MAHARASTRA

Source: Committee report on sugar deregulation, SPA Research

Controls on sector prior to reforms Controls after partial

decontrol

GOVT.POLICIES

MinimumDistance Criteria

between mills

Cane AreaReservation

Dual CanePricing:

Centre/StateCompulsory

sugar packingin jute only

Levy SugarObligation on

mills

RegulatedRelease

Mechanism

Import andExport

State Govt. Controls Central Govt. Controls

GOVT.POLICIES

MinimumDistance Criteria

between mills

Cane AreaReservation

Dual CanePricing:

Centre/State

Tariffrates on

trade

40% sugarto be packed in jut e bags on ly

State Govt. Controls Central Govt. Controls

Dual pricing contributing largely to cane arrears&

cyclicality in sugar industry

Contents World SugarStatistics

Indian SugarIndustry

Global Scenario Sugar Pricing

OutlookSugar Sector Balrampur ChiniShree Renu

Sugars

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

15/34

The SAP in UP has been increased from INR 165 per quintal of

cane in 2009-10 sugar season to INR280 per quintal in 2012-13,

which has meant:

An increase of INR 115 per quintal in just 3 years (@ INR 40 per

quintal yearly).

It has increased the average cost of production of sugar in UP

from INR 24 per kg in 2009-10 toINR 35 per kg in 2012-13

season.

As compared to these very high costs, the sugar prices which

were INR 28 per kg in 2009-10increased to only INR 31 per kg in

2012-13.

Cane price in UP has gone up by 70% in the last 3 years, but

sugar prices have increased by just11% in the same period.

Sugarcane Production & Price trend

050

100150200

250300350

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

UP Su ga rc an e P ro d. (m t) TN Suga rc ane P ro d. (mt) Su ga

rca ne FRP (INR)

TN SAP (INR) UP SAP (INR)

Source: ISMA, SPA Research

Import-export of sugarDepending on mill-wise monthly production

and stocks, local production levels and world marketconditions, the

Government regulates the import (through import duty) and export

[through opengeneral license (OGL) and advance license scheme

(ALS)].

Minimum distance criteria and Cane area reservationEach sugar

mill is allocated a command area in its vicinity (which usually

varies from 15 km to 25km radius, depending on the state). The mill

is obligated to purchase sugarcane from cane farmerswithin the cane

reservation area, and conversely, farmers are bound to sell to the

mill. This isintended to serve the twin purposes of giving a

minimum assured supply of the highly-perishableraw material to a

mill, while committing the mill to procure at a minimum price

(FRP/SAP).

Jute Packaging mandate for sugarJute Packaging Materials Act

mandates that sugar be packed only in jute bags. It is estimated by

thesugar industry that this leads to an increase in cost by about

~40 paise per kg of sugar besides

adversely impacting quality on account of ingress of jute fibers

of jute bags. Further there is oftena shortage of jute bags.

However this has now been relaxed for 60% of production.

Controls on sale of by-productsThere are several regulatory

hurdles in respect of the by-products of sugar industry. In respect

of molasses, these are at the state level, in terms of state

government decisions relating to fixation of quotas for different

end uses of molasses, restrictions on movement (particularly across

stateboundaries), etc.

Political Agenda destroying UP's sugar economy

Contents World SugarStatistics

Indian SugarIndustry

Global Scenario Sugar PricingOutlook

Balrampur Chini Shree RenukaSugars

Sugar Sector

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

16/34

Partial decontrol of sugar - Leading to rerating of sector

The expert committee headed by Dr. Rangarajan submitted its

recommendations on the deregulation of the sugar sector to the

government in Oct 2012. The key proposals suggested were a)

abolition of levysugar, b) doing away with monthly/quarterly

release mechanism of non-levy sugar, c) sugarcane price tobe linked

to 70% of realized value from sugar, molasses and bagasse with FRP

forming a floor and nostate-wise SAPs, d) removal on quantitative

restriction on sugar exports and imports, e) removal of controls on

sale of by-products, and f) gradual phasing away of cane area

reservation and minimumdistance criteria for mills.

The GoI accepted the Rangarajan Committee report on April 4,

2013 and announced a partial decontrol of the sugar industry

by:-

a) Removing the levy obligation to supply part of the sugar

production at subsidized prices - Earlier,central government used

to procure 10% of the sugar production at subsidised price of INR

19.7/kg,

which resulted in financial burden to the tune of ~INR 30 bn on

the sugar industry. The removal of levyobligation will have a

substantial impact on profitability as it would lead to ~ 1.3/kg

increase inblended realisation of sugar manufacturers.

b) Abolishing the regulated release mechanism to sell non-levy

sugar in the market - The abolition of themonthly release mechanism

will facilitate the free play of market forces for the commodity.

It will benefitsugar mills in the medium to long-term by enabling

them to manage their working capital requirementsbetter while also

enabling financially stronger sugar mills to capitalize on better

sugar realizations.

Importantly other key recommendations of Rangarajan Committee

namely, the revenue sharing formulafor sugar cane pricing, the

minimum distance between factories and the reservation of area for

factoriesetc, have been delegated to the State Governments to take

a considered view.

The revenue sharing formula for sugar cane pricing entails that

70% of revenues (sugar, molasses andbagasse)/75% of revenues for

non-integrated mill, should be shared with farmers and payment

would bemade in 2 stages; FRP within 14 days of cane purchase and

balance on half yearly basis on ex-mill pricedeclared by respective

states. It has been gathered that the Government of Karnataka has

already enactedan Act in May 2013 deciding to form a sugar board

and prescribing that the sugarcane price will be basedon the

revenue sharing model. Maharashtra is also readying to consider a

similar move prior to the startof the next season. This is a

remarkable initiative taken by these two State Governments and we

hope thatthis will have a positive influence on the Government of

UP. Otherwise these two states, which account for~49% of the

country's sugar output, would out-price UP sugar due to their lower

cost of production. Weview these policy changes as a step in the

right direction and expect the sugar industry to get transformedand

re-rated in the coming years.

ncial burden before decontroluction for 2012-13 25.0 mt

share 2.4 mtncial burden on company

Price INR 19.7ket price of sugar INR 32.0

on levy quota INR 12.3 Burden INR 29.52 mn

: SPA Research

taka & Maharashtra finally showingst for adopting revenue

sharing formulane pricing

Contents World SugarStatistics

Indian SugarIndustry

Global Scenario Sugar Pricing

OutlookSugar Sector Balrampur ChiniShree Renu

Sugars

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

17/34

Significantly beneficial for sugar mills, particularly UP

based

Units Uttar Pradesh Maharashtra

Cane crushed mt 8.0 8.0

Sugar

Recovery rate 9.5% 11.0%

sugar prodn/sales mt 0.76 0.88

sugar realisation (Ex-mill) INR/tn 32000 32000

Sugar revenue INR mn 24320 28160

Molasses

Recovery rate % 5.0% 5.0%

Production mt 0.40 0.40

Realisation (assumed) `/t 3200 3200

Molasses Revenue INR mn 1280 1280

BagasseRecovery rate 30.0% 30.0%

Production mt 2.40 2.40

Captive cons 30% 0.72 0.72

Exportable surplus mt 1.68 1.68

Realisation (assumed) INR/tn 800 800

Bagasse Revenue INR mn 1920 1920

Cane price estimation

Total revenue (sugar+molasses+bagasse) INR mn 27520 31360

Cane cost (% of total revenue) % 70% 70%

Total Cane cost INR mn 19264 21952

Cane crushed mt 8.0 8.0

Cane cost per tonne INR/tn 2408 2744

as % of sugar realisation % 75.3% 85.8%

Trend in domestic sugar pricesIndia has been witnessing higher

sugarcane price over the last few years, however sugar priceshave

not risen in direct proportion leading to severe margin pressure on

the industry. Sugar pricesduring 2011-12 did not increase sharply

and ranged between INR 29 to INR 31 per kg, due to anexpected rise

in sugar production and more than sufficient availability of

stocks.

Prices have inched northward in early 2012-13 between May 2012

to November 2012 (peaking ataround INR 36/kg, due to expectation of

lower sugarcane production in Maharashtra and Karnatakain current

sugar year. However with consumption remaining at ~23.5 mt in

addition to higher global

production and subdued global prices (restricting export

attractiveness), sugar prices has remainedunder pressure since

H2FY13.

There were several other factors also that led to decline in

prices. While the initial decline in the periodJanuary- March 2013

was driven mainly by seasonal supply pressure from new production

and sale of sugar in the domestic market by shore based refiners

having access to cheap raw sugar, the continueddecline since April

2013 has been driven mainly by the announcement of partial

decontrol in April2013, which resulted in large scale releases of

sugar by financially weak mills with large cane dues. Inaddition,

competition from sugar produced by processing raw sugar (whose

prices remained weakglobally because of supply pressures) also

continued to prevent any rally in sugar prices.

Sugar prices at NCEDX declined around 18% and touched a low of

INR 29.8/kg in the month of April2013 and has finally stabilized at

~INR 31/kg on concerns over lower cane acreage.

Contents World SugarStatistics

Indian SugarIndustry

Global Scenario Sugar PricingOutlook

Balrampur Chini Shree RenukaSugars

Sugar Sector

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

18/34

Prices stabilising

Source: Bloomberg, SPA Research

Global Scenario

World sugar dynamicsWorld consumption of sugar has grown at an

average annual rate of 2.7% over the past 50 years.Sugar

consumption has been declining in developed countries - partly due

to the availability of substitutes and concerns about obesity and

health. At the same time, it has been increasing indeveloping

countries, which now account for around 70% of world sugar

consumption, driven byrising incomes, population growth and changes

in diet.

Sugar crops in many parts of the world are projected to expand

in response to rising demand forsugar and other uses. World sugar

production is expected to increase by 30 mt to reach over 210mt in

2020-21. The bulk of the additional sugar production will come from

the developing countriesand the main burden of growth will continue

to fall on Brazil. Brazil has expanded productionrapidly in the

past two decades, but a slowdown in investment in new mills

occurred after thefinancial crisis of 2008, slowing the overall

growth in the following years.

The use of sugar in the development of ethanol as an alternative

fuel is also an important factor inthe sugar supply-and-demand

equation. Brazil is both the largest exporter of sugar and the

largestproducer and consumer of ethanol. Any decision that Brazil

takes to expand ethanol production -for example, when a large sugar

crop is forecast - can affect the balance of supply and demand

inthe global sugar market.

Main producing countriesRaw sugar is derived from both sugar

cane and sugar beet. Brazil and India are the world's twolargest

sugar producers. Together, they have accounted for over half the

world's sugar caneproduction for the past 40 years. The EU is the

third-largest producer and accounts for around half the world's

sugar-beet production. World production of raw sugar has increased

by 2% YoY to174.5 mt in 2011-12. By 2018, production is projected

to reach 202 mt - slightly higher than theprojected consumption of

198 mt.

Source: USDA, SPA Research

AGR in sugar consumption to 2021

0.00.51.01.52.02.53.03.54.0

A f r i c a

A s i a

S o u t

h A m e r i c a

O c e a n i a

N & C A m e r i c a

E u r o p e

W o r l

d

urce: Rabobank 2013

Major sugar producing countries contri bution (%) in total world

sugar production

22.66

14.49

10.428.23

4.532.74

4.59 3.31 2.39 2.20

24.44

0.00

5.00

10.00

15.00

20.00

25.00

30.00

B r a z i l

I n d i a E U

C h i n a

U S A

A u s t r a

l i a

T h a i

l a n d

M e x i c o

P a k i s t a n

R u s s i a

R e s t o f

w o r

l d

Contents World SugarStatistics

Indian SugarIndustry

Global Scenario Sugar Pricing

OutlookSugar Sector Balrampur Chini

Shree RenuSugars

0

500

1000

1500

2000

2500

3000

35004000

4500

A u g 0 7

J a n 0 8

J u n 0 8

N o v 0 8

A p r 0 9

S e p 0 9

F e b 1 0

J u l 1 0

D e c 1 0

M a y

1 1

O c t

1 1

M a r

1 2

A u g 1 2

J a n 1 3

I N R p e r t o n n e

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

19/34

Main exporting countriesWorld exports of raw sugar increased by

1% YoY to 58 mt in 2011-12 led by Brazil (24.6 mt) and

Thailand (9 mt).Largest exporters of Raw sugar as a % of total

exports by volume, 2007-12

EU 4%

UAE 3%

Guatemala 3%

Mexico 2%

Columbia 1%

Cuba 1%

Others 19%

India 5%

Australia 6%

Thailand 12%

Brazil 44%

Source: USDA FAS Sugar: World Markets & Trade, SPA

Research

Main importing countriesImport of raw sugar stood at 49 mt in

2011-12. The EU, US and Indonesia are the leading importers,at

around 3 mt each per year.

World Ethanol DynamicsEthanol & Its advantagesWith

ever-rising cost of petrol, global warming, peak oil and so on,

there has been a growing needfor sourcing alternative sources of

energy and ethanol seems to be a product that many economiesare

putting much of their hopes into.

The use of ethanol as a blended fuel component in gasoline is

steadily increasing. Ethanol's mainattraction comes from the fact

that it burns cleaner than petroleum oil, and that it is more cost

andfuel-efficient. Ethanol is also a renewable energy resource, an

important factor considering ourhigh dependence on petroleum, being

non-renewable, which is entering into a stage of scarcity,

orpeak-oil, driving the price of petrol up. Furthermore, the

production of ethanol may have a role ineasing the global economic

crisis. The financial worth of ethanol producing crops will drive

up theprices of vegetation such as corn, so farmers can enjoy a

significant profit. These same crops needto processed, meaning

there will be an increased need for factories and workforces.

Demand drivers & Growth potentialThe US, Brazil and to a

smaller extent, the European Union, together dominates global

productionof fuel ethanol producing ~89% of the world's output. The

US product is largely distilled from corn,while Brazil makes

ethanol from its sugar cane crop. Production and use in the United

States andthe European Union are mainly driven by the policies in

place (i.e. Renewable Fuels Standard(RFS2) and the Renewable Energy

Directive (RED), respectively). The growing use of ethanol in

Brazilis linked to the development of the flex-fuel industry (FFVs)

and the import demand of the UnitedStates to fill the advanced

biofuel mandate as well as to their increase in blending

minimums.

Global ethanol production has fallen in CY12 for the first time

since 2000, due to declines in theUnited States and in Brazil. With

lower prices of maize and sugar anticipated in 2013-14, a

largeincrease in production is anticipated in both countries. In

addition to the pivotal 3 markets - the

USA59.22%

China2.39%

Canada1.93%

Other Countries9.94%

India2.53%

Brazil23.99%

Global Ethanol Production in 2012

Source: USDA, SPA Research

Contents World SugarStatistics

Indian SugarIndustry

Global Scenario Sugar PricingOutlook

Balrampur Chini Shree RenukaSugars

Sugar Sector

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

20/34

US, Brazil and the EU -rising transport fuel demand in other

countries, together with additionalgovernments expressing mandates

and targets for ethanol inclusion in gasoline, point to

considerable potential for fuel ethanol demand over the

remainder of this decade.

Renewable Energy & Nuclear Power are fastest growing sources

of energy consumption

Source: EIA, International Energy Outlook 2013, SPA Research

By 2022, OECD is expecting world ethanol production to increase

by almost 70% compared to theaverage of 2010-12 and reach some 168

bnl. Out of this, production in developing countries isprojected to

increase from 42 bnl in 2012 to 72 bnl. in 2022, with Brazil

accounting for 80% of thissupply increase and a large part of the

rest coming from China, where less than half of theirethanol

production is consumed in the fuel market, the rest is consumed as

alcohol in many foodand nonfood preparations.

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

250

200

150

100

50

0

7%

15%

23%

27%28%

5%

11%

22%

28%

34%

History Projections2010

Liquid fuels(including biofuels) Coal

Natural gas

Renewables(excluding biofuels)

Nuclear

Production to grow at 6% CAGR

0

50

100

150

200

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

2 0 1 1

2 0 1 2

2 0 1 3

2 0 1 4

2 0 1 5

2 0 1 6

2 0 1 7

2 0 1 8

2 0 1 9

2 0 2 0

2 0 2 1

2 0 2 2

World ethanol production (bnl) World ethanol trade (bnl)

Production

Brazil28%

EU7%

China6%

Thailand1%

India2%

USA48%

Consumption

China6%

India2%

Thailand1%

Other8%

EU10%

U52

Brazil21%

w o r l d e n e r g y c o n s u m p t i o n

b y

f u e

l q u a d r i

l l i o n

b t u

S h a r e o

f w o r l

d t o t a

l

Regional distribution of world ethanol production and use in

2022

Source: OECD-FAO Agriculture Outlook 2013, SPA Research

Crude oil has little direct impact on ethanol pricesIncreasing

gasoline prices lead to surge in demand of ethanol because it makes

ethanol morecompetitive. Ceteris paribus, blending ethanol is cost

effective as long as ethanol price is at 30%discount to the price

of gasoline due to its lower energy content. Demand for crude oil

has a minimalimpact on the price of ethanol. In the world market

for crude oil, an individual country's supply anddemand decisions

are small relative to the market as a whole-even for a country the

size of the US. Toput this into perspective, the US consumes

roughly 20% of world oil. Roughly half of the US oilconsumption

goes toward gasoline and ethanol comprises roughly 10% of

gasoline-blend fuel. Thus,on a volumetric basis, US ethanol

constitutes about 2% of world oil use. Crude-oil supply anddemand

would need to be very inelastic before such a quantity had a

noticeable effect on price.

Contents World SugarStatistics

Indian SugarIndustry

Global Scenario Sugar Pricing

OutlookSugar Sector Balrampur Chini

Shree RenuSugars

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

21/34

CBOT Ethanol Nearest-Futures versus NYMEX RBOB Gasoline

Nearest-Futures

Source: SPA ResearchOECD is expecting the world gasoline price

to increase in real terms by 7% between 2012 and 2022,as a result

of which ethanol will become increasingly competitive with petrol.

This will lead to anincrease in demand and consumption of ethanol

by owners of flex-fuel cars thereby putting upwardpressure on the

world price of ethanol in the medium-term. As a result OECD is

expecting anincrease of 8% in the world price of ethanol in real

terms between 2012 and 2022.

So with all of these benefits, is ethanol the fix-all

solution?Unfortunately, it is not as production of ethanol has many

negative points working against it in itspotential role as the next

major source of fuel. The most important is the fact that creating

ethanolis thought to consume more energy than its overall output.

The amount of crops needed to fuel a carfor only one day could go a

long way towards feeding a person for considerably longer.

Also,although ethanol is being advocated as environmentally

friendly, the amount of farmland neededto satisfy the global thirst

for fuel is staggering. This need for fuel means that more

farmlands mustbe created, resulting in considerable deforestation.

There would also be less of an incentive forfarmers to grow other

crops, when ethanol-producing harvest would fetch more of a price,

or evenusing vegetation, such as corn, for food products instead of

as fuel. The result would be over-inflated prices on all food

products, an expense that could further damage populations

alreadydealing economic distress. Earlier this year the USDA

reported the largest corn planting in history.Yet record

temperatures and drought throughout the country means this year's

crop could be farlower than originally expected. Weather is

uncontrollable, but we can influence demand for cornsupplies.

Government incentives for corn ethanol increase demand at a time

when corn is expectedto be in short supply and that has made global

hunger advocates worried.

CBOT Ethanol Nearest-Futures versus CBOT Corn

Nearest-Futures

Source: SPA Research

Hence instead of relying entirely on ethanol as alternate fuel,

it can be used to take strain off of theenvironment by being

implemented in ethanol-gasoline, or ethanol-electric cars.

7% CAGR in world gasoline prices to result in 8%CAGR in world

ethanol prices

Contents World SugarStatistics

Indian SugarIndustry

Global Scenario Sugar PricingOutlook

Balrampur Chini Shree RenukaSugars

Sugar Sector

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

22/34

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

23/34

Global demand supply situation - SugarGlobal surplus to decline

significantly in 2014Production deficits in 2008-09 and 2009-10

were followed by surpluses in 2010-11 and 2011-12as sugar crop

areas expanded on the back of higher prices. The International

Sugar Organisationhas forecast a 10.1 mt global supply surplus in

2012-13 on account of more supplies from majorexporting countries

like Brazil (+6.8%), Australia (+9.0%), Thailand (although -2.9% on

YoY butsubstantially higher than previous estimates) and high

production in major importing countrieslike China (+17%). Global

production is projected to rise to a record high of 184.2 mt in

2012-13,while consumption is expected at 174.1 mt, leading to a

surplus of 10.1 mt, more than 8.5 mtanticipated earlier.

Importantly the global sugar surplus is expected to decline

significantly in 2014 with ISO estimatesindicating 3.5 mt of

surplus for the period 2013-14. Sugar price declines in recent

years havecreated incentives for a new equilibrium in the sector.

On the demand side, cheaper prices boostconsumption. On the supply

side, lower prices squeeze profit margins, causing farmers to opt

forother crops and to invest less in the remaining sugarcane

plantations. World sugar output isexpected to decline by 2.8% to

178.5 mt while consumption is expected to grow by around 0.8%

to175.5 mt in 2013-14.

The expected global sugar surplus for the fourth consecutive

year can totally be eliminated alsodepending on the amount of cane

that is used in Brazil for ethanol. A 20% increase in

Brazilsethanol consumption has the potential to completely

eliminate the world sugar surplus.

Demand Supply Dynamics10.4 8.2

(14.0)(10.6)

(0.1)

7.810.1

3.5

0

50

100

150

200

FY07 FY08 FY09 FY10 FY11 FY12 FY13E FY14E(20

(15

(10

(5)

0

5

10

15

Production Consumption Surplus/Deficit

Source: USDA, SPA Research

Brazil - The Potential game changer

Brazil - Sugar production to cross 40 mt in 2013-14Brazilian

cane production increased by 5.4% to 591.1 mt in 2012-13 season

while sugar productionsurged by 6.8% to 38.6 mt YoY, showing a

strong upturn of the cane crop from a sharp drop in yieldsin

2010-11 & 2011-12 resulting from adverse weather

conditions.

In 2013-14, Brazilian sugarcane production is expected to

increase by 8.3% to 640 mt, while sugarproduction is expected to

surge by 4.7% to 40.4 mt. The center-south (CS) region is expected

toharvest 585 mt of sugarcane (+9.8% YoY) and crush 36.4 mt sugar

(+6.6% YoY) in 2013-14, due toexpected higher agricultural yields

as a result of good weather conditions and adequate renewalof

sugarcane stocks.

Brazilian sugar exports are expected to increase by 6.0% to 29.3

mt in 2013-14 to meet projectedinternational demand. Raw sugar

should account for 23.0 mt, whereas the remainder representsexports

of refined sugar.

Most important factor for the world sugar & ethanol

market

Positioned in the world as (2012):

- No. 1: sugarcane producer (35% of world)

- No. 1: sugar producer (23% of world)

- No. 2: ethanol producer (28% of world)

- No. 1: sugar exporter (49% of world)

- No. 1: ethanol exporter (55% of wo rld)

World sugar surplus to decline significantly to3.5 mt in

2013-14

20% increase in Brazils ethanol consumptioncan completely

eliminate the world sugar surplus.

Contents World SugarStatistics

Indian SugarIndustry

Global Scenario Sugar PricingOutlook

Balrampur Chini Shree RenukaSugars

Sugar Sector

-

8/13/2019 Sugar Sector - Sector Initiation Report - SPA Sec

24/34

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0

0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1

0

2 0 1 1

2 0 1 2

2 0 1 3

2 0 1 4

2 0 1 5

2 0

1 6

2 0

1 7

2 0 1 8

2 0 1 9

2 0 2 0

2 0 2

1

2 0 2 2

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

Brazil Ethanol & Sugar Production

27.0 26.0 25.0 23.0 23.426.8

26.031.0 31.0

36.2 38.640.4

0

10

20

30

40

50

2009 2010 2011 2012 2013 2014E

Ethanol (bn lt) Sugar (mt)

Source: USDA, SPA Research

Mills are seen to be allocating much more of the cane they

harvested to ethanol production thanthey did last year. Total

ethanol production is forecast to increase by 14.9% to 26.8 bn

liters (12.6bn liters of anhydrous ethanol and 14.2 bn liters of

hydrated ethanol).