Embed Size (px)

Citation preview

Annual Report 2018

1521 Lake Pointe Parkway, Sugar Land, Texas 77478Phone: 281-566-8000 Fax: 281-566-8001

www.pioneeronline.org

8801 Research Blvd, Suite 105, Austin, TX 78758Phone: (512) 467-PMCU (7628) Fax: (512) 467-PFAX (7329)

SUGAR LAND OFFICE

AUSTIN BRANCH

8643 W Rayford Road, Spring TX 77389Phone: 281-566-8071 Fax: 281-566-8072

NORTH HOUSTON BRANCH

Members Helping Members

Board of Directors 2018

Faheem N PraslaSecretary

Altaf A PraslaChairman,

Supervisory Committee

Shaheen N MominTreasurer

Moiz N Dhuka Convenor,

Collection Committee

Mustakali R MominMember,

Credit Committee

Mahendi K PraslaConvenor,

BSA Committee

Salman S KadiwalMember,

Credit Committee

Saddiq M SunesraChairman,

Credit & Business Loan Committee

Shaukat AliPresident/CEO

Naushad Ali DhukkaChairman

Riyaz R SunesaraVice Chairman

2018 Annual Report |

Chairman's Message 1

Supervisory Committee's Report 2

Credit & Business Loan Committee’s Report 2

Statement of Financial Position 3

Statement of Operations 4

Statement of Cash Flows 5

Statement of Equity / Key Financial Ratios 6

Notes to Financial Statements:

Nature of Business 7

ClassificationsofLoans 8

SignificantAccountingPolicies 9

Bar Charts & Key Indicators 10

Products and Services 11

CONTENTS

DESCRIPTION PAGE #

| 2018 Annual Report

Dear Members,

Year after year, Pioneer Mutual Federal Credit Union (PMFCU) has made tremendous progress and so have its members. The community that PMFCU serves has advanced a great deal as well. In the most recent 7 years of its 37-year life, PMFCU’s assets have increased by 200% from $56.45 Million in 2011 to $169.29 Million in 2018. Over that same time period, PMFCU’s loan portfolio has grown from $44.97 Million to $100.41 Million. Such outstanding growth could not have been achieved without our members’ trust, confidence and unconditional loyalty. Additionally, these achievements were made possible through the remarkable contribution of time and resources from our hard working, caring, committed and intelligent staff and management team. And behind all these successes has been a single driving force – the Board of Directors of PMFCU. The board, current and past, has always made it a top priority to ensure that the credit union not only remains healthy, stable and progressive, but also to reassure that its directors are fully cognizant of their duties and fiduciary responsibilities at all times. The board is always eager to help members by all means possible and by being fair to each and every member. This would not be possible if the board was not to create, maintain and periodically review policies and procedures that can aid the staff and management team in delivering quality work product.

Whether it is a $500 unsecured loan as in the early days of the credit union or $100K unsecured loans and $2.5M+ commercial loans from more recent days, Pioneer has undoubtedly come a long way. 26% of all loans issued since inception were in just last 3 years alone i.e. $120 Million out of $465 Million in loans since the inception. Pioneer also recorded the lowest delinquency rate of 0.14% in 2018. All of this growth and activity has come responsibly and methodically. Members now seem to be more organized and more efficient in preparing loan applications and supporting documents. While all operating departments work smoothly and seamlessly, the compliance department has its iron grip

on all methods and areas of operation. It is these checks and balances between the operations and compliance teams that help Pioneer pass all the audits and rigorous examinations by the NCUA (at both the District and the Federal levels) with flying colors. For that, the examiners have always commended Pioneer’s staff, management and the board.

Additionally, now that our North Houston location is open, MSB and other services to member businesses are in full effect. Pioneer is grateful to all members and member businesses in North Houston for welcoming our newest branch there and benefiting from all the products and services offered. Of course, MSB and other similar products are subject to a higher level of scrutiny and more stringent regulatory requirements. In response, Pioneer has been holding educational seminars/town-hall meetings for MSB accounts. We thank the members for their full support and cooperation in helping Pioneer stay compliant in all areas including member privacy, BSA, AML, lending, saving, ACH and other transactional activity.

Lastly, I must acknowledge all the volunteers, staff members and the management team for their hard work and commitment to serve with a smile, the founders of PMFCU for their remarkably ambitious vision, all the past directors who paved the way for PMFCU and all the current directors with whom I had the pleasure and honor of serving alongside for past 7 years. I am absolutely convinced that tomorrow’s leadership and board will bring more success to this fine institution and will put PMFCU in an even better position to serve the community.

With best wishes to Pioneer and to its members,

Naushad Dhukka

Chairman

1

CHAIRMAN’S MESSAGE

2018 Annual Report | 2

The Supervisory Committee of Pioneer Mutual Federal Credit Union (PMFCU) is responsible for assessing the activities of the credit union. The committee ensures that the credit union operations are effective in safeguarding credit union assets and maintaining accurate member records. It verifies that the adequate policies and procedures are established and regularly reviewed by the Board as per the NCUA rules and regulations; and are followed by the staff of the credit union. It also oversees the financial statements to confirm that they represent a fair and reasonably accurate picture of the financial condition of the credit union. The committee is appointed by the Board annually which include Supervisory Chairman from the Board and two committee members from general membership. During 2018, the committee was comprised of the following individuals:Altaf A. Prasla – Chairman; Irfan K. Ali – Member; and Altaf A. Dholasaniya – MemberThe committee meets regularly to discuss and perform internal audit. The audit findings are reported to the Board and communicated to the management and staff. The committee ensures that the external audits for NCUA Annual Examination, Money Service Business (MSB), Bank Secrecy Act (BSA), Automatic Clearing House (ACH), Customer Identification Program (CIP), Office of Foreign Assets Control (OFAC), and Supervisory Committee Annual Review are performed regularly and reports are reviewed by the Board. The management has also engaged with third-party consulting firm to seek advice during the year 2018 for the operations and compliance of Money Services Business (MSB) portfolio.Based on the various internal and external audits, the committee is pleased to report that the credit union maintains firm internal control to protect member assets and information. The credit union is operating with strict adherence to NCUA rules and regulations; and in compliance with the policies and procedures set by the Board. The committee would like to extend its appreciation to NCUA examiners for their continues guidance during the year and to the staff for assisting in the audit process. We are grateful to the members and Board of Directors for the continuous support and confidence in the committee.Altaf A. Prasla,Chairman, Supervisory Committee

The Credit & Business Loan Committee of Pioneer Mutual Federal Credit Union plays an important role in maintaining the loan portfolio as per policies and procedures and as required by regulatory requirement of the NCUA. The Credit & Business Loan Committee is elected by the Board of Directors and consists of five members. The Committee meets regularly on a weekly basis to review and approve the loan applications.

I take this privilege in informing our members that our Credit Union offers the best competitive interest rates across our league while maintaining a safe and secure capital base.

In the year 2018, the committee received and reviewed 769 loan applications, of which 760 loans totaling $37,975,050 were approved. Overall loan portfolio stood at $100,410,707 in the year 2018 as compared to $85,790,912 for the year 2017 with an increase of 17.04%. During the last 3 years, our Credit Union has loaned out loans as follows: Year 2016: $41.02M. Year 2017: $40.76M and in the Year 2018: $37.97M.

The increase in the Loan portfolio reveals our continued ability to meet financial needs of our members. Special promotions were offered to the members to gain benefits on availing the lower and competitive interest rates on various loan products and also providing cash back incentives on Home Mortgage loans. We will continue to focus on meeting the financial needs of our members by offering various financial loan products and services.

On behalf of the Credit & Business Loan Committee Members, I would like to express my appreciation to the Board of Directors and the Staff members for their continuous support and also to all our members, without you it would have not been possible to achieve our objectives and goals. We look forward in providing our excellent service and serve you better in the years ahead.

Saddiq SunesraChairman, Credit & Business Loan Committee

SUPERVISORY COMMITTEE’S REPORT

CREDIT & BUSINESS LOAN COMMITTEE’S REPORT

| 2018 Annual Report

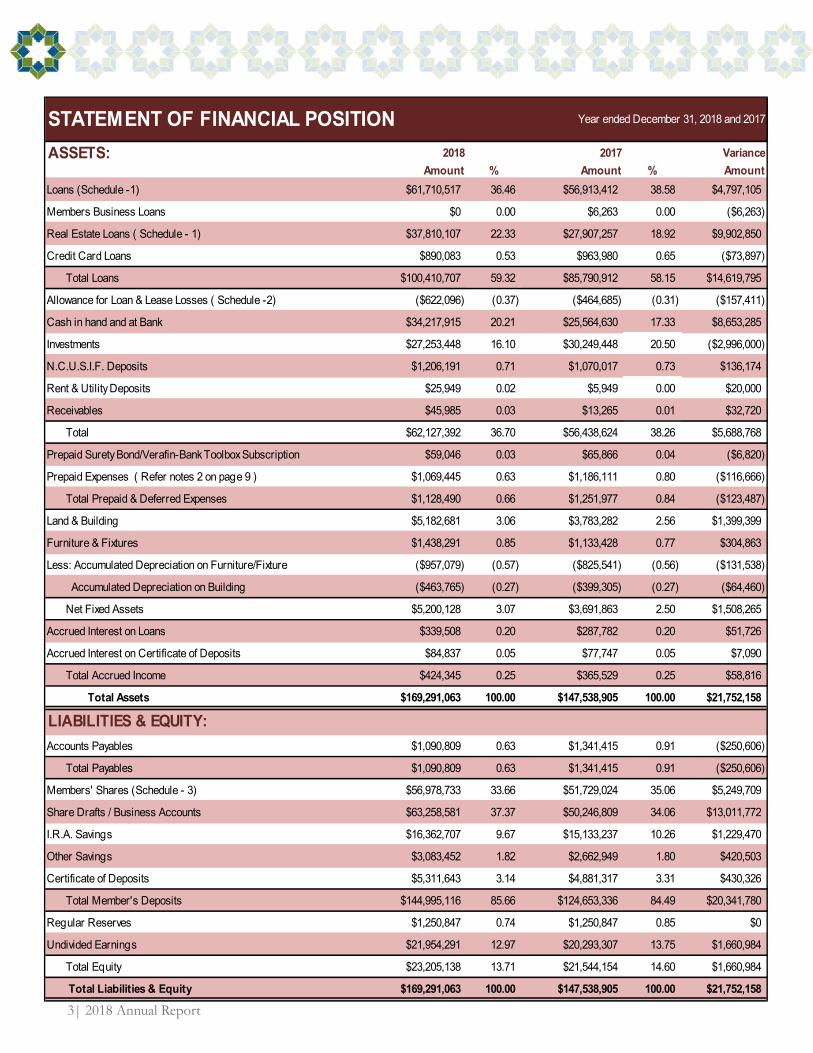

STATEMENT OF FINANCIAL POSITIONASSETS: 2018 2017 Variance Amount % Amount % AmountLoans (Schedule -1) $61,710,517 36.46 $56,913,412 38.58 $4,797,105

Members Business Loans $0 0.00 $6,263 0.00 ($6,263)

Real Estate Loans ( Schedule - 1) $37,810,107 22.33 $27,907,257 18.92 $9,902,850

Credit Card Loans $890,083 0.53 $963,980 0.65 ($73,897)

Total Loans $100,410,707 59.32 $85,790,912 58.15 $14,619,795

Allowance for Loan & Lease Losses ( Schedule -2) ($622,096) (0.37) ($464,685) (0.31) ($157,411)

Cash in hand and at Bank $34,217,915 20.21 $25,564,630 17.33 $8,653,285

Investments $27,253,448 16.10 $30,249,448 20.50 ($2,996,000)

N.C.U.S.I.F. Deposits $1,206,191 0.71 $1,070,017 0.73 $136,174

Rent & Utility Deposits $25,949 0.02 $5,949 0.00 $20,000

Receivables $45,985 0.03 $13,265 0.01 $32,720

Total $62,127,392 36.70 $56,438,624 38.26 $5,688,768

Prepaid Surety Bond/Verafin-Bank Toolbox Subscription $59,046 0.03 $65,866 0.04 ($6,820)

Prepaid Expenses ( Refer notes 2 on page 9 ) $1,069,445 0.63 $1,186,111 0.80 ($116,666)

Total Prepaid & Deferred Expenses $1,128,490 0.66 $1,251,977 0.84 ($123,487)

Land & Building $5,182,681 3.06 $3,783,282 2.56 $1,399,399

Furniture & Fixtures $1,438,291 0.85 $1,133,428 0.77 $304,863

Less: Accumulated Depreciation on Furniture/Fixture ($957,079) (0.57) ($825,541) (0.56) ($131,538)

Accumulated Depreciation on Building ($463,765) (0.27) ($399,305) (0.27) ($64,460)

Net Fixed Assets $5,200,128 3.07 $3,691,863 2.50 $1,508,265

Accrued Interest on Loans $339,508 0.20 $287,782 0.20 $51,726

Accrued Interest on Certificate of Deposits $84,837 0.05 $77,747 0.05 $7,090

Total Accrued Income $424,345 0.25 $365,529 0.25 $58,816

Total Assets $169,291,063 100.00 $147,538,905 100.00 $21,752,158

LIABILITIES & EQUITY:Accounts Payables $1,090,809 0.63 $1,341,415 0.91 ($250,606)

Total Payables $1,090,809 0.63 $1,341,415 0.91 ($250,606)

Members' Shares (Schedule - 3) $56,978,733 33.66 $51,729,024 35.06 $5,249,709

Share Drafts / Business Accounts $63,258,581 37.37 $50,246,809 34.06 $13,011,772

I.R.A. Savings $16,362,707 9.67 $15,133,237 10.26 $1,229,470

Other Savings $3,083,452 1.82 $2,662,949 1.80 $420,503

Certificate of Deposits $5,311,643 3.14 $4,881,317 3.31 $430,326

Total Member's Deposits $144,995,116 85.66 $124,653,336 84.49 $20,341,780

Regular Reserves $1,250,847 0.74 $1,250,847 0.85 $0

Undivided Earnings $21,954,291 12.97 $20,293,307 13.75 $1,660,984

Total Equity $23,205,138 13.71 $21,544,154 14.60 $1,660,984

Total Liabilities & Equity $169,291,063 100.00 $147,538,905 100.00 $21,752,158

Year ended December 31, 2018 and 2017

3

2018 Annual Report |

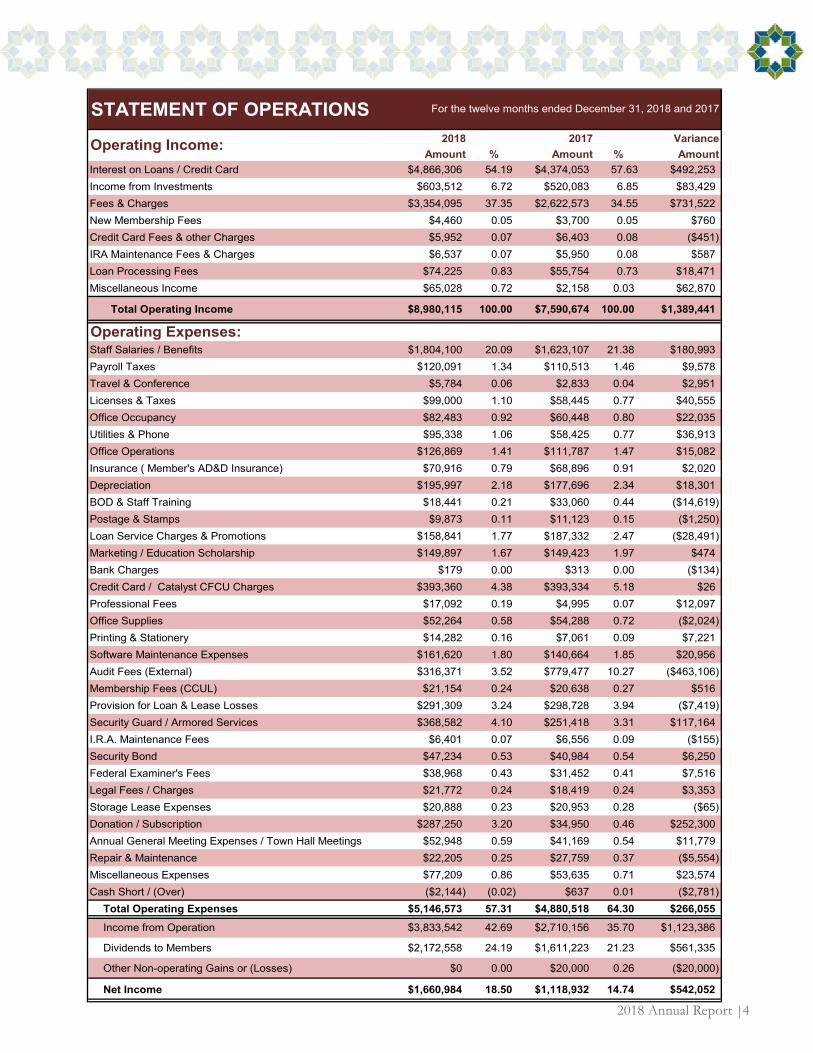

STATEMENT OF OPERATIONS2018 2017 Variance

Amount % Amount % AmountInterest on Loans / Credit Card $4,866,306 54.19 $4,374,053 57.63 $492,253Income from Investments $603,512 6.72 $520,083 6.85 $83,429Fees & Charges $3,354,095 37.35 $2,622,573 34.55 $731,522New Membership Fees $4,460 0.05 $3,700 0.05 $760Credit Card Fees & other Charges $5,952 0.07 $6,403 0.08 ($451)IRA Maintenance Fees & Charges $6,537 0.07 $5,950 0.08 $587Loan Processing Fees $74,225 0.83 $55,754 0.73 $18,471Miscellaneous Income $65,028 0.72 $2,158 0.03 $62,870

Total Operating Income $8,980,115 100.00 $7,590,674 100.00 $1,389,441

Operating Expenses:Staff Salaries / Benefits $1,804,100 20.09 $1,623,107 21.38 $180,993Payroll Taxes $120,091 1.34 $110,513 1.46 $9,578Travel & Conference $5,784 0.06 $2,833 0.04 $2,951Licenses & Taxes $99,000 1.10 $58,445 0.77 $40,555Office Occupancy $82,483 0.92 $60,448 0.80 $22,035Utilities & Phone $95,338 1.06 $58,425 0.77 $36,913Office Operations $126,869 1.41 $111,787 1.47 $15,082Insurance ( Member's AD&D Insurance) $70,916 0.79 $68,896 0.91 $2,020Depreciation $195,997 2.18 $177,696 2.34 $18,301BOD & Staff Training $18,441 0.21 $33,060 0.44 ($14,619)Postage & Stamps $9,873 0.11 $11,123 0.15 ($1,250)Loan Service Charges & Promotions $158,841 1.77 $187,332 2.47 ($28,491)Marketing / Education Scholarship $149,897 1.67 $149,423 1.97 $474Bank Charges $179 0.00 $313 0.00 ($134)Credit Card / Catalyst CFCU Charges $393,360 4.38 $393,334 5.18 $26Professional Fees $17,092 0.19 $4,995 0.07 $12,097Office Supplies $52,264 0.58 $54,288 0.72 ($2,024)Printing & Stationery $14,282 0.16 $7,061 0.09 $7,221Software Maintenance Expenses $161,620 1.80 $140,664 1.85 $20,956Audit Fees (External) $316,371 3.52 $779,477 10.27 ($463,106)Membership Fees (CCUL) $21,154 0.24 $20,638 0.27 $516Provision for Loan & Lease Losses $291,309 3.24 $298,728 3.94 ($7,419)Security Guard / Armored Services $368,582 4.10 $251,418 3.31 $117,164I.R.A. Maintenance Fees $6,401 0.07 $6,556 0.09 ($155)Security Bond $47,234 0.53 $40,984 0.54 $6,250Federal Examiner's Fees $38,968 0.43 $31,452 0.41 $7,516Legal Fees / Charges $21,772 0.24 $18,419 0.24 $3,353Storage Lease Expenses $20,888 0.23 $20,953 0.28 ($65)Donation / Subscription $287,250 3.20 $34,950 0.46 $252,300Annual General Meeting Expenses / Town Hall Meetings $52,948 0.59 $41,169 0.54 $11,779Repair & Maintenance $22,205 0.25 $27,759 0.37 ($5,554)Miscellaneous Expenses $77,209 0.86 $53,635 0.71 $23,574Cash Short / (Over) ($2,144) (0.02) $637 0.01 ($2,781)

Total Operating Expenses $5,146,573 57.31 $4,880,518 64.30 $266,055Income from Operation $3,833,542 42.69 $2,710,156 35.70 $1,123,386

Dividends to Members $2,172,558 24.19 $1,611,223 21.23 $561,335

Other Non-operating Gains or (Losses) $0 0.00 $20,000 0.26 ($20,000)

Net Income $1,660,984 18.50 $1,118,932 14.74 $542,052

Operating Income:

For the twelve months ended December 31, 2018 and 2017

4

| 2018 Annual Report 5

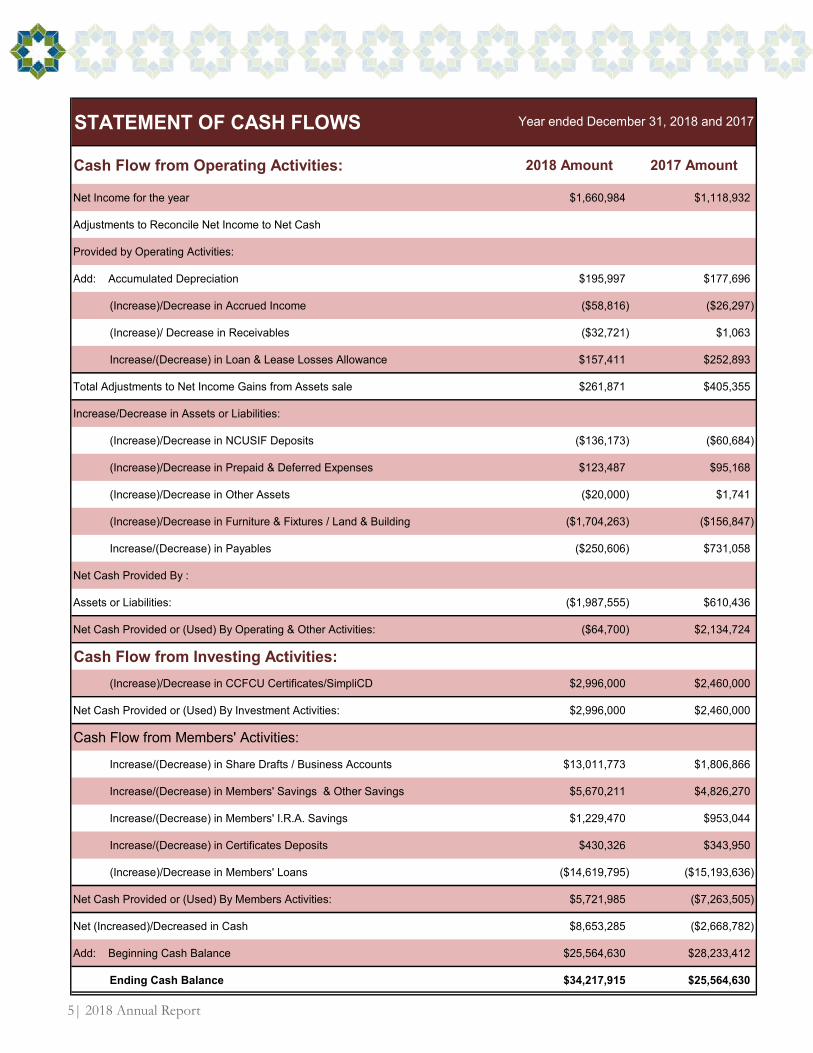

STATEMENT OF CASH FLOWS

Cash Flow from Operating Activities: 2018 Amount 2017 Amount

Net Income for the year $1,660,984 $1,118,932

Adjustments to Reconcile Net Income to Net Cash

Provided by Operating Activities:

Add: Accumulated Depreciation $195,997 $177,696

(Increase)/Decrease in Accrued Income ($58,816) ($26,297)

(Increase)/ Decrease in Receivables ($32,721) $1,063

Increase/(Decrease) in Loan & Lease Losses Allowance $157,411 $252,893

Total Adjustments to Net Income Gains from Assets sale $261,871 $405,355

Increase/Decrease in Assets or Liabilities:

(Increase)/Decrease in NCUSIF Deposits ($136,173) ($60,684)

(Increase)/Decrease in Prepaid & Deferred Expenses $123,487 $95,168

(Increase)/Decrease in Other Assets ($20,000) $1,741

(Increase)/Decrease in Furniture & Fixtures / Land & Building ($1,704,263) ($156,847)

Increase/(Decrease) in Payables ($250,606) $731,058

Net Cash Provided By :

Assets or Liabilities: ($1,987,555) $610,436

Net Cash Provided or (Used) By Operating & Other Activities: ($64,700) $2,134,724

Cash Flow from Investing Activities: (Increase)/Decrease in CCFCU Certificates/SimpliCD $2,996,000 $2,460,000

Net Cash Provided or (Used) By Investment Activities: $2,996,000 $2,460,000

Cash Flow from Members' Activities:

Increase/(Decrease) in Share Drafts / Business Accounts $13,011,773 $1,806,866

Increase/(Decrease) in Members' Savings & Other Savings $5,670,211 $4,826,270

Increase/(Decrease) in Members' I.R.A. Savings $1,229,470 $953,044

Increase/(Decrease) in Certificates Deposits $430,326 $343,950

(Increase)/Decrease in Members' Loans ($14,619,795) ($15,193,636)

Net Cash Provided or (Used) By Members Activities: $5,721,985 ($7,263,505)

Net (Increased)/Decreased in Cash $8,653,285 ($2,668,782)

Add: Beginning Cash Balance $25,564,630 $28,233,412

Ending Cash Balance $34,217,915 $25,564,630

Year ended December 31, 2018 and 2017

2018 Annual Report |

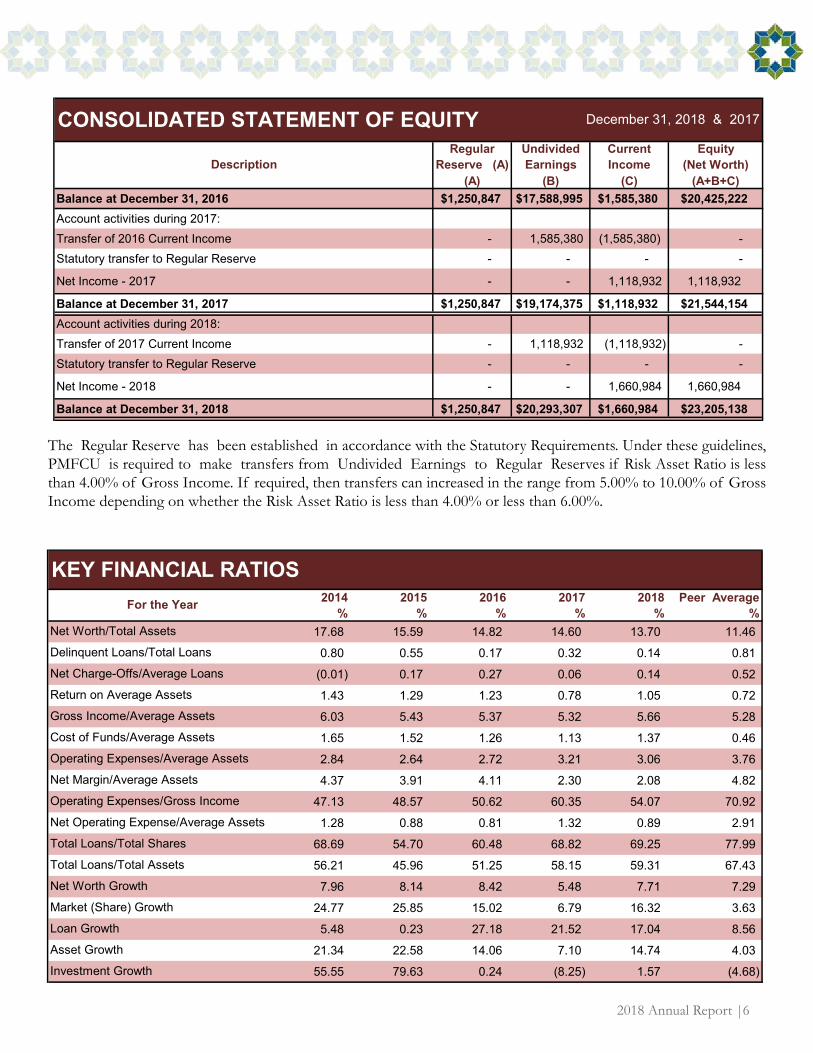

(A) (B) (C) (A+B+C)Balance at December 31, 2016 $1,250,847 $17,588,995 $1,585,380 $20,425,222Account activities during 2017:Transfer of 2016 Current Income - 1,585,380 (1,585,380) - Statutory transfer to Regular Reserve - - - -

Net Income - 2017 - - 1,118,932 1,118,932

Balance at December 31, 2017 $1,250,847 $19,174,375 $1,118,932 $21,544,154Account activities during 2018:Transfer of 2017 Current Income - 1,118,932 (1,118,932) - Statutory transfer to Regular Reserve - - - -

Net Income - 2018 - - 1,660,984 1,660,984

Balance at December 31, 2018 $1,250,847 $20,293,307 $1,660,984 $23,205,138

Equity(Net Worth)Description

CONSOLIDATED STATEMENT OF EQUITY December 31, 2018 & 2017

RegularReserve (A)

UndividedEarnings

CurrentIncome

6

2014 2015 2016 2017 2018 Peer Average% % % % % %

17.68 15.59 14.82 14.60 13.70 11.46

0.80 0.55 0.17 0.32 0.14 0.81

(0.01) 0.17 0.27 0.06 0.14 0.52

1.43 1.29 1.23 0.78 1.05 0.72

6.03 5.43 5.37 5.32 5.66 5.28

1.65 1.52 1.26 1.13 1.37 0.46

2.84 2.64 2.72 3.21 3.06 3.76

4.37 3.91 4.11 2.30 2.08 4.82

47.13 48.57 50.62 60.35 54.07 70.92

1.28 0.88 0.81 1.32 0.89 2.91

68.69 54.70 60.48 68.82 69.25 77.99

56.21 45.96 51.25 58.15 59.31 67.43

7.96 8.14 8.42 5.48 7.71 7.29

24.77 25.85 15.02 6.79 16.32 3.63

5.48 0.23 27.18 21.52 17.04 8.56

21.34 22.58 14.06 7.10 14.74 4.03

55.55 79.63 0.24 (8.25) 1.57 (4.68)

Asset Growth

Net Operating Expense/Average Assets

Total Loans/Total Shares

Net Worth Growth

Market (Share) Growth

Loan Growth

Total Loans/Total Assets

Net Worth/Total Assets

Delinquent Loans/Total Loans

Net Charge-Offs/Average Loans

Return on Average Assets

Net Margin/Average Assets

Operating Expenses/Gross Income

Gross Income/Average Assets

Cost of Funds/Average Assets

Investment Growth

Operating Expenses/Average Assets

For the Year

KEY FINANCIAL RATIOS

The Regular Reserve has been established in accordance with the Statutory Requirements. Under these guidelines, PMFCU is required to make transfers from Undivided Earnings to Regular Reserves if Risk Asset Ratio is less than 4.00% of Gross Income. If required, then transfers can increased in the range from 5.00% to 10.00% of Gross Income depending on whether the Risk Asset Ratio is less than 4.00% or less than 6.00%.

| 2018 Annual Report

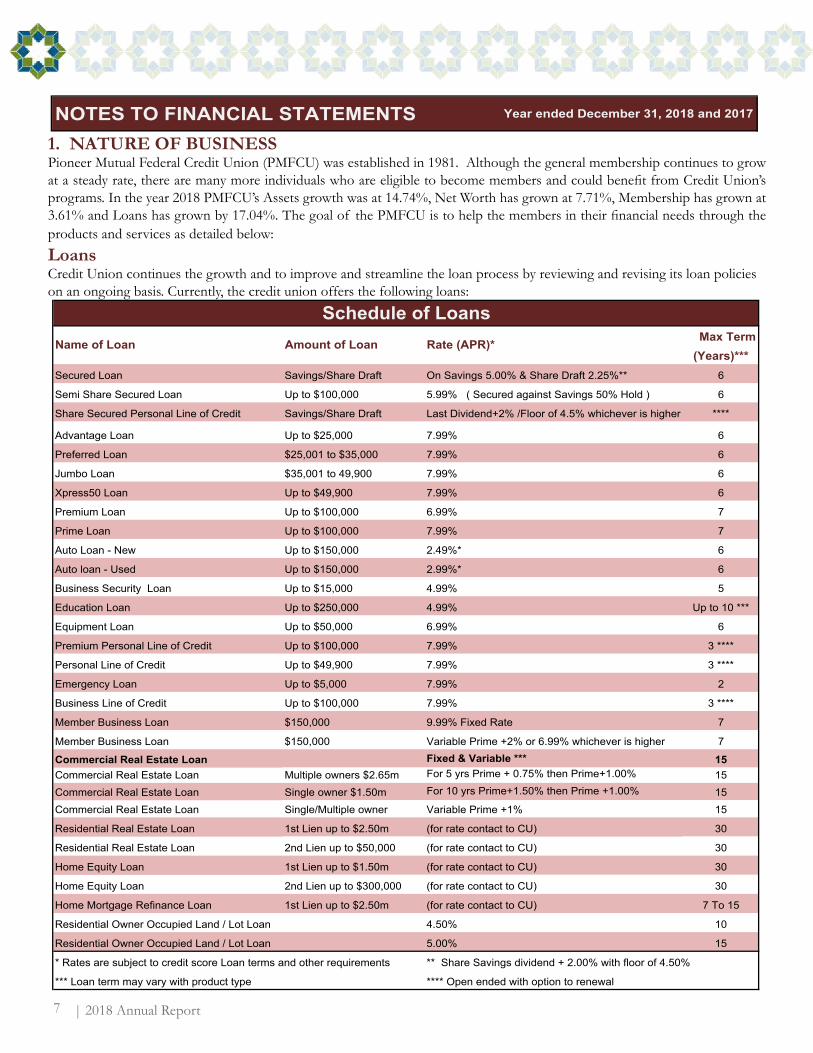

Max Term(Years)***

Secured Loan Savings/Share Draft On Savings 5.00% & Share Draft 2.25%** 6

Semi Share Secured Loan Up to $100,000 5.99% ( Secured against Savings 50% Hold ) 6

Share Secured Personal Line of Credit Savings/Share Draft Last Dividend+2% /Floor of 4.5% whichever is higher ****

Advantage Loan Up to $25,000 7.99% 6

Preferred Loan $25,001 to $35,000 7.99% 6

Jumbo Loan $35,001 to 49,900 7.99% 6

Xpress50 Loan Up to $49,900 7.99% 6

Premium Loan Up to $100,000 6.99% 7

Prime Loan Up to $100,000 7.99% 7

Auto Loan - New Up to $150,000 2.49%* 6

Auto loan - Used Up to $150,000 2.99%* 6

Business Security Loan Up to $15,000 4.99% 5

Education Loan Up to $250,000 4.99% Up to 10 ***

Equipment Loan Up to $50,000 6.99% 6

Premium Personal Line of Credit Up to $100,000 7.99% 3 ****

Personal Line of Credit Up to $49,900 7.99% 3 ****

Emergency Loan Up to $5,000 7.99% 2

Business Line of Credit Up to $100,000 7.99% 3 ****

Member Business Loan $150,000 9.99% Fixed Rate 7

Member Business Loan $150,000 Variable Prime +2% or 6.99% whichever is higher 7

Commercial Real Estate Loan Fixed & Variable *** 15Commercial Real Estate Loan Multiple owners $2.65m For 5 yrs Prime + 0.75% then Prime+1.00% 15Commercial Real Estate Loan Single owner $1.50m For 10 yrs Prime+1.50% then Prime +1.00% 15Commercial Real Estate Loan Single/Multiple owner Variable Prime +1% 15

Residential Real Estate Loan 1st Lien up to $2.50m (for rate contact to CU) 30

Residential Real Estate Loan 2nd Lien up to $50,000 (for rate contact to CU) 30

Home Equity Loan 1st Lien up to $1.50m (for rate contact to CU) 30

Home Equity Loan 2nd Lien up to $300,000 (for rate contact to CU) 30

Home Mortgage Refinance Loan 1st Lien up to $2.50m (for rate contact to CU) 7 To 15

Residential Owner Occupied Land / Lot Loan 4.50% 10

Residential Owner Occupied Land / Lot Loan 5.00% 15

**** Open ended with option to renewal *** Loan term may vary with product type

* Rates are subject to credit score Loan terms and other requirements ** Share Savings dividend + 2.00% with floor of 4.50%

Schedule of LoansName of Loan Amount of Loan Rate (APR)*

1. NATURE OF BUSINESSPioneer Mutual Federal Credit Union (PMFCU) was established in 1981. Although the general membership continues to grow at a steady rate, there are many more individuals who are eligible to become members and could benefit from Credit Union’s programs. In the year 2018 PMFCU’s Assets growth was at 14.74%, Net Worth has grown at 7.71%, Membership has grown at 3.61% and Loans has grown by 17.04%. The goal of the PMFCU is to help the members in their financial needs through the products and services as detailed below:LoansCredit Union continues the growth and to improve and streamline the loan process by reviewing and revising its loan policies on an ongoing basis. Currently, the credit union offers the following loans:

7

NOTES TO FINANCIAL STATEMENTS Year ended December 31, 2018 and 2017

2018 Annual Report |

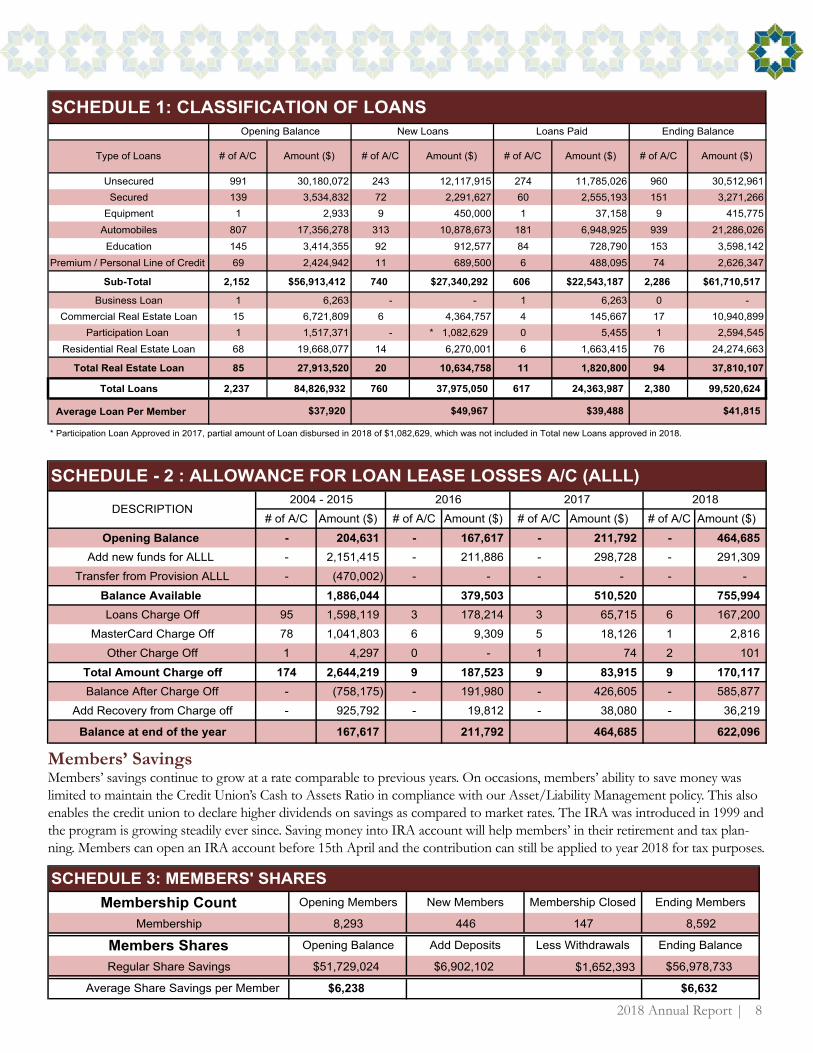

Unsecured 991 30,180,072 243 12,117,915 274 11,785,026 960 30,512,961Secured 139 3,534,832 72 2,291,627 60 2,555,193 151 3,271,266

Equipment 1 2,933 9 450,000 1 37,158 9 415,775Automobiles 807 17,356,278 313 10,878,673 181 6,948,925 939 21,286,026Education 145 3,414,355 92 912,577 84 728,790 153 3,598,142

Premium / Personal Line of Credit 69 2,424,942 11 689,500 6 488,095 74 2,626,347

Sub-Total 2,152 $56,913,412 740 $27,340,292 606 $22,543,187 2,286 $61,710,517

Business Loan 1 6,263 - - 1 6,263 0 - Commercial Real Estate Loan 15 6,721,809 6 4,364,757 4 145,667 17 10,940,899

Participation Loan 1 1,517,371 - * 1,082,629 0 5,455 1 2,594,545Residential Real Estate Loan 68 19,668,077 14 6,270,001 6 1,663,415 76 24,274,663

Total Real Estate Loan 85 27,913,520 20 10,634,758 11 1,820,800 94 37,810,107

Total Loans 2,237 84,826,932 760 37,975,050 617 24,363,987 2,380 99,520,624

Average Loan Per Member

* Participation Loan Approved in 2017, partial amount of Loan disbursed in 2018 of $1,082,629, which was not included in Total new Loans approved in 2018.

$37,920 $49,967 $39,488

# of A/C # of A/C# of A/C

$41,815

Amount ($)Amount ($) Amount ($)

SCHEDULE 1: CLASSIFICATION OF LOANSOpening Balance New Loans Loans Paid

Type of Loans Amount ($)# of A/C

Ending Balance

# of A/C Amount ($) # of A/C Amount ($) # of A/C Amount ($) # of A/C Amount ($)Opening Balance - 204,631 - 167,617 - 211,792 - 464,685

Add new funds for ALLL - 2,151,415 - 211,886 - 298,728 - 291,309 Transfer from Provision ALLL - (470,002) - - - - - -

Balance Available 1,886,044 379,503 510,520 755,994 Loans Charge Off 95 1,598,119 3 178,214 3 65,715 6 167,200

MasterCard Charge Off 78 1,041,803 6 9,309 5 18,126 1 2,816 Other Charge Off 1 4,297 0 - 1 74 2 101

Total Amount Charge off 174 2,644,219 9 187,523 9 83,915 9 170,117 Balance After Charge Off - (758,175) - 191,980 - 426,605 - 585,877

Add Recovery from Charge off - 925,792 - 19,812 - 38,080 - 36,219

Balance at end of the year 167,617 211,792 464,685 622,096

SCHEDULE - 2 : ALLOWANCE FOR LOAN LEASE LOSSES A/C (ALLL)

DESCRIPTION20182004 - 2015 2016 2017

Members’ SavingsMembers’ savings continue to grow at a rate comparable to previous years. On occasions, members’ ability to save money was limited to maintain the Credit Union’s Cash to Assets Ratio in compliance with our Asset/Liability Management policy. This also enables the credit union to declare higher dividends on savings as compared to market rates. The IRA was introduced in 1999 and the program is growing steadily ever since. Saving money into IRA account will help members’ in their retirement and tax plan-ning. Members can open an IRA account before 15th April and the contribution can still be applied to year 2018 for tax purposes.

8

Membership Count Opening Members New Members Membership Closed Ending Members

Membership 8,293 446 147 8,592

Members Shares Opening Balance Add Deposits Less Withdrawals Ending Balance

Regular Share Savings $51,729,024 $6,902,102 $1,652,393 $56,978,733

Average Share Savings per Member $6,238 $6,632

SCHEDULE 3: MEMBERS' SHARES

| 2018 Annual Report 9

2. SIGNIFICANT ACCOUNTING POLICESThe accounting policies of PMFCU are in conformity with Generally Accepted Accounting Principles (GAAP) in the United States of America. A description of the more significant of these policies is as follows:

Use of EstimatesThe preparation of financial statements in conformity with GAAP in the United States of America requires management to make estimates and assumptions that affect certain reported amounts of assets, liabilities, the reported amount revenues and expenses for the period.

Cash EquivalentsFor purposes of reporting cash flows, the Credit Union considers all investments in overnight to be cash equivalents and all investments purchased with original maturities of three month or less to be cash equivalents.

InvestmentsIn order to get better investment return on excess liquidity of $27.134 million, up to $248K each has been invested in ‘laddered’ form of certificate of deposits (SimpliCD with various banks) through Catalyst Corporate Federal Credit Union. These CDs mature in below 3 months interval up to 60 months. Currently we have invested $27.134 millions on an average rate at 2.19% as of December 31, 2018.

Prepaid ExpensesPioneer Mutual Federal Credit Union contributed $1.75 million to Community Focus Foundation for “Pioneer Community Center” for name branding as a Marketing Expenses, which is amortized for 15 years. Outstanding balance as of December 31, 2018 is $1,069,445.

3. LINE OF CREDITPMFCU has $15,000,000 line of credit facility at 3.5% interest rate with Catalyst Corporate Federal Credit Union (CCFCU) as of December 31, 2018. Interest is payable monthly based on the daily balance. There was no balance outstanding on the line of Credit as of December 31, 2018.

4. CONCENTRATIONS OF CREDIT RISKPMFCU maintains an account with Catalyst Corporate Federal Credit Union a balance $2,163,131 of as of December 31, 2018. This account is insured by the National Credit Union Share Insurance Fund (NCUSIF) up to $250,000. The Credit Union also maintains other account with Wallis Bank (WB). The total balances in the WB Checking Account was $1,877,042.51 as of December 31, 2018. The Checking account is insured up to $250,000.00 by the Federal Deposit Insurance Corporation (FDIC). Under the Personal Line of Credit and Credit Card Program members have different credit limits. At the year ended on December 31, 2018, approximately $2,525,663 and $4,765,705 respectively remained unused credit card limits.

Loans to membersLoans to members are stated at the current principal amount outstanding. Interest on loans is accrued on monthly basis on the amount of principal outstanding.

Premises and EquipmentsThe Credit Union occupies Austin premises of approximately 1,850 square feet for $3,700 and Compliance Department premises of approximately 1,768 square feet. for $3,173.56 monthly rent. The equipment is carried at cost less accumulated depreciation. Provisions for depreciation are computed using the straight-line method. Average useful lives used for depreciation with respect to major classifications of property are as follows:Furniture and Equipment 3 to10 years and Computer and Software 2 to 5 years.Expenses for maintenance and repairs are charged against operations. Assets and related amounts are removed from the accounts upon retirement or other disposition and any resulting gains or losses are recorded in the statement of activities.

Income TaxesPMFCU is exempted from Federal Income Taxes under Internal Revenue Code sections 501(c) (1) and are also exempted from State Sales Taxes.

2018 Annual Report |

0

20

40

60

80

100

120

140

160

180

2014 2015 2016 2017 2018

17.42 18.84 20.43 21.54 23.21

55.38 55.49

70.60

85.79

100.41

80.64

101.46

116.72124.65

144.99

98.53

120.76

137.76147.54

169.29

Amou

nt in M

illions ($

)

Years

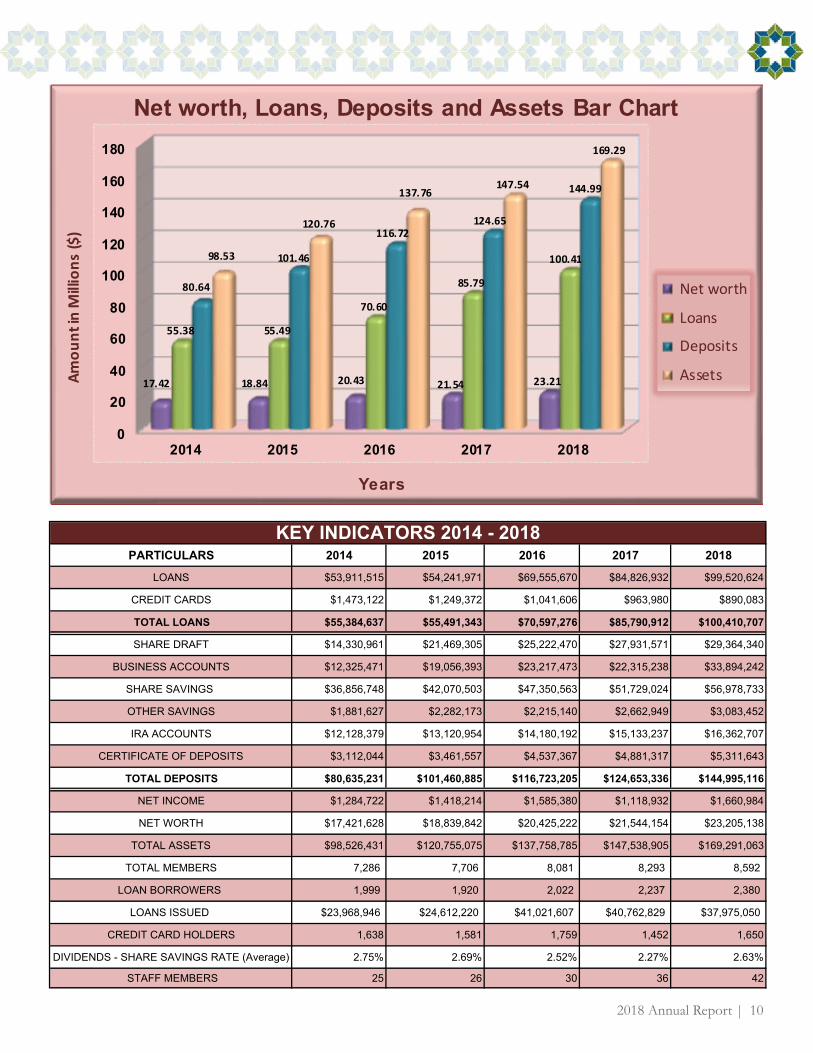

Net worth, Loans, Deposits and Assets Bar Chart

Net worth

Loans

Deposits

Assets

PARTICULARS 2014 2015 2016 2017 2018

LOANS $53,911,515 $54,241,971 $69,555,670 $84,826,932 $99,520,624

CREDIT CARDS $1,473,122 $1,249,372 $1,041,606 $963,980 $890,083

TOTAL LOANS $55,384,637 $55,491,343 $70,597,276 $85,790,912 $100,410,707

SHARE DRAFT $14,330,961 $21,469,305 $25,222,470 $27,931,571 $29,364,340

BUSINESS ACCOUNTS $12,325,471 $19,056,393 $23,217,473 $22,315,238 $33,894,242

SHARE SAVINGS $36,856,748 $42,070,503 $47,350,563 $51,729,024 $56,978,733

OTHER SAVINGS $1,881,627 $2,282,173 $2,215,140 $2,662,949 $3,083,452

IRA ACCOUNTS $12,128,379 $13,120,954 $14,180,192 $15,133,237 $16,362,707

CERTIFICATE OF DEPOSITS $3,112,044 $3,461,557 $4,537,367 $4,881,317 $5,311,643

TOTAL DEPOSITS $80,635,231 $101,460,885 $116,723,205 $124,653,336 $144,995,116

NET INCOME $1,284,722 $1,418,214 $1,585,380 $1,118,932 $1,660,984

NET WORTH $17,421,628 $18,839,842 $20,425,222 $21,544,154 $23,205,138

TOTAL ASSETS $98,526,431 $120,755,075 $137,758,785 $147,538,905 $169,291,063

TOTAL MEMBERS 7,286 7,706 8,081 8,293 8,592

LOAN BORROWERS 1,999 1,920 2,022 2,237 2,380

LOANS ISSUED $23,968,946 $24,612,220 $41,021,607 $40,762,829 $37,975,050

CREDIT CARD HOLDERS 1,638 1,581 1,759 1,452 1,650

DIVIDENDS - SHARE SAVINGS RATE (Average) 2.75% 2.69% 2.52% 2.27% 2.63%

STAFF MEMBERS 25 26 30 36 42

KEY INDICATORS 2014 - 2018

10

| 2018 Annual Report 11

LOANS :• Share Secured Loan• Semi Share Secured Loan• Auto Loan (New & Used)• Business Security Loan• Equipment Loan• Member Business Loan• Commercial Real Estate Loan• Home Mortgage Loan• Home Equity Loan• Home Mortgage Refinance Loan• Home Mortgage Jumbo Loan• Residential Owner Occupied Land

/ Lot Loan• Business Line of Credit• Personal Line of Credit• Premium Personal Line of Credit• Share Secured Personal Line Of

Credit (against Savings)• Advantage Loan• Preferred Loan• Jumbo Loan• Xpress50 Loan• Prime Loan• Premium Loan• Emergency Loan• Education Loan

ACCOUNTS:• Share Savings Account• Share Draft (Checking Account)• Pioneer Education Savings Account• IRA Account• Small Business Checking Account• Commercial Business Checking

Account• Commercial MSB Account• Check Cashing Account

MASTERCARD: • Gold

SERVICES:• Online Banking• ACH Services• Auto Transfer Services• Cashier’s Check Facility• Safe Deposit Boxes• Drive Thru Facility• Night Depository• Remote Deposit Services• Wire Transfer Services• E-Statement• AD&D Insurance Coverage• Notary Public Service

PRODUCTS AND SERVICES

| 2018 Annual Report

Nooruddin MominAccounting Manager

Sanif KarowaliyaFinancial Compliance

Officer

Swati PatelOperations Manager

Faiza AliBusiness & Mortgage

Loan Manager

Afrojaben DhukaCredit Analyst

Shama MominHead Teller & Supervisor

Alvin MominOperationsOfficer

Austin Branch

Naeema AliBranch Manager

Austin Branch

Shabira MominOperations Manager North Houston Branch

Farhana MominComplianceOfficer

OfficeStaff

Zahra MaknojiaLoanOfficer

Wafee AliBSAComplianceOfficer

Sonia MominHR & Administrative

Officer

Nimrusha AliTeller I

Austin Branch

Alvina AliMember ServiceRepresentative II

Huma MominCollection Assistant

Aroshna SherwaOperations Assistant II

Noreen MarediaTeller II

Austin Branch

Firuza BuribekovaOperations Assistant I

Shahina ManknojiaTeller I

Akhtar NoorwaniAudit Manager

Anum K AliAccountingOfficer

KamarinBahen Maknojiya

Teller Supervisor

Munija KadiwalaCompliance Assistant

Aqeel AliOperations Assistant

Munisha PraslaMember ServiceRepresentativeAustin Branch

Sonika MaknojiaOperations Assistant

Nabil MaknojiyaLoanOfficer

Sajjad AliCompliance Associate II

Alzaib MaknojiaTeller

Mahera MominSenior BSA Compliance

Officer

Shamina DholasaniyaTeller I

North Houston Branch

Rashmin AliTeller

North Houston Branch

Rifaa DhukaAdministrative Assistant

Sobia AliTeller

Austin Branch

Sanam AliTeller

Mubarak AliManager

Nayeem ParasalaITOfficer

Suman KarovadiyaMember ServiceRepresentative

North Houston Branch

Anum JafferTeller

Austin Branch

Annual Report 2018

1521 Lake Pointe Parkway, Sugar Land, Texas 77478Phone: 281-566-8000 Fax: 281-566-8001

www.pioneeronline.org

8801 Research Blvd, Suite 105, Austin, TX 78758Phone: (512) 467-PMCU (7628) Fax: (512) 467-PFAX (7329)

SUGAR LAND OFFICE

AUSTIN BRANCH

8643 W Rayford Road, Spring TX 77389Phone: 281-566-8071 Fax: 281-566-8072

NORTH HOUSTON BRANCH

Members Helping Members

![[WMD 2015] Branch Metrics, Alex Austin >> "Mobile-izing The Masses: Case Studies On How To Build, Release & Grow B2C Apps"](https://img.pdfslide.us/doc/110x75/55a56f421a28ab00388b4626/wmd-2015-branch-metrics-alex-austin-mobile-izing-the-masses-case-studies-on-how-to-build-release-grow-b2c-apps.jpg)