Embed Size (px)

Citation preview

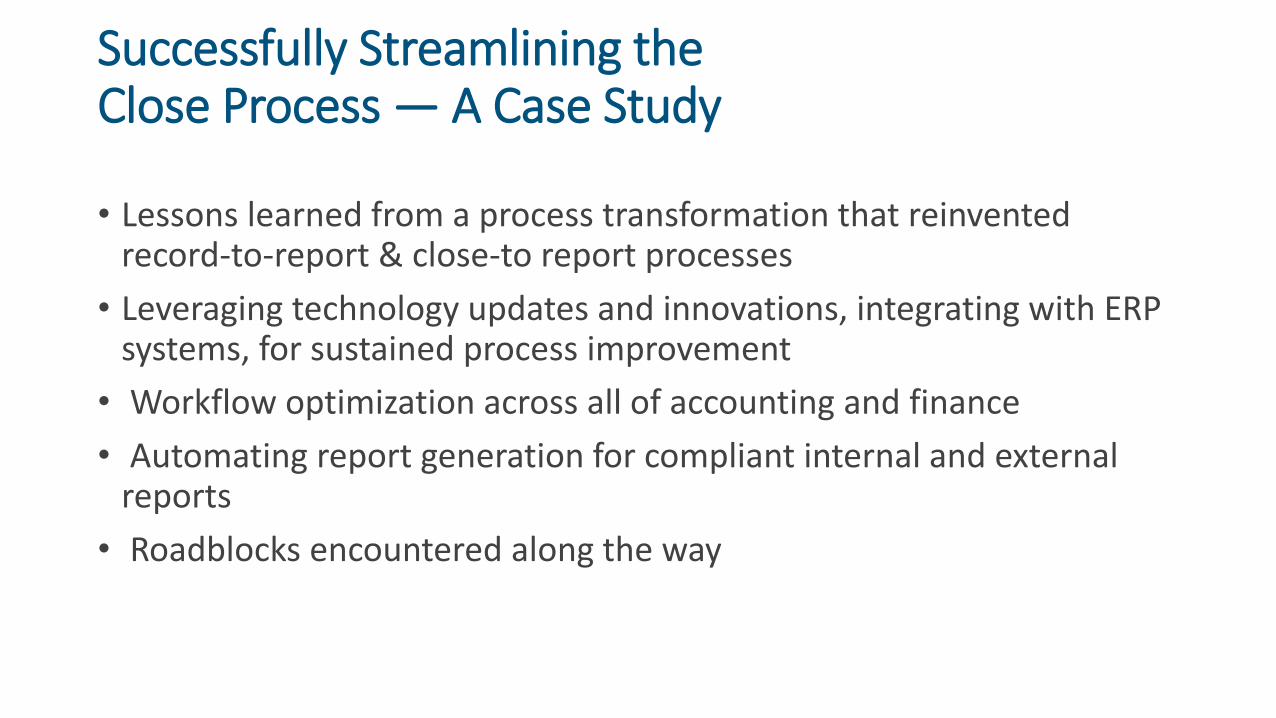

Successfully Streamlining theClose Process — A Case Study

• Lessons learned from a process transformation that reinvented record-to-report & close-to report processes

• Leveraging technology updates and innovations, integrating with ERP systems, for sustained process improvement

• Workflow optimization across all of accounting and finance

• Automating report generation for compliant internal and external reports

• Roadblocks encountered along the way

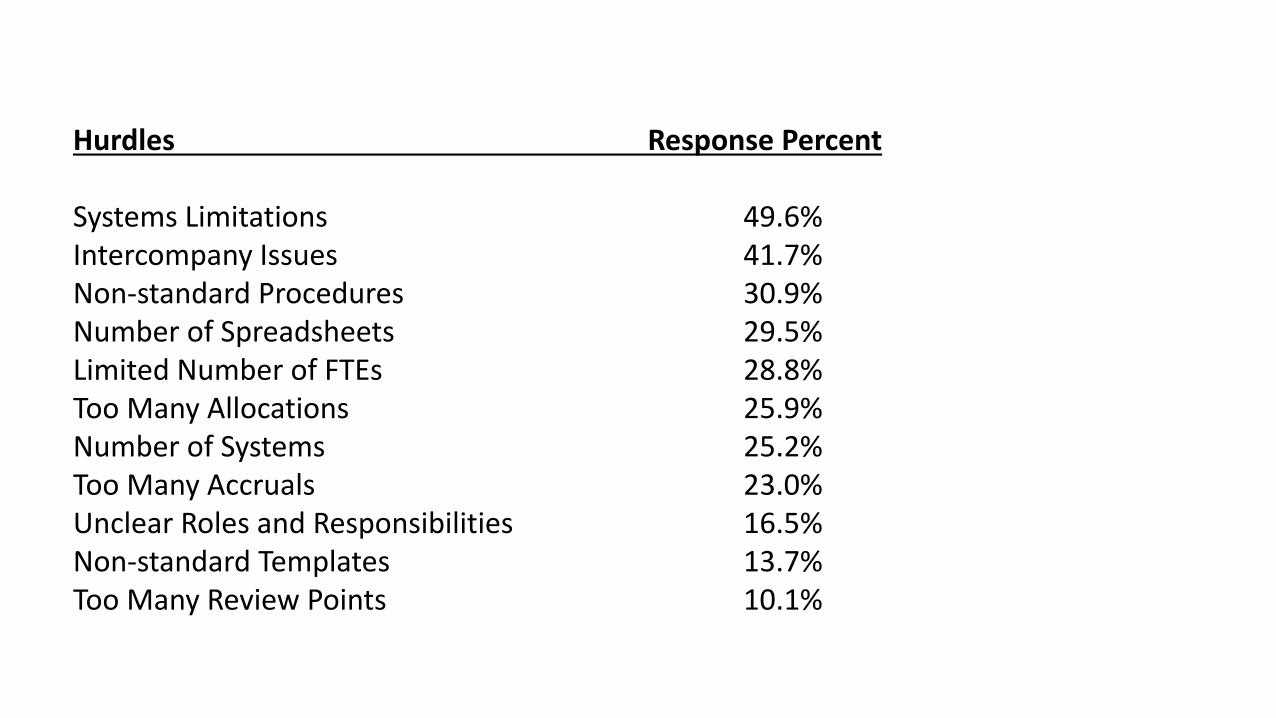

Hurdles Response Percent

Systems Limitations 49.6%Intercompany Issues 41.7%Non-standard Procedures 30.9%Number of Spreadsheets 29.5% Limited Number of FTEs 28.8%Too Many Allocations 25.9%Number of Systems 25.2%Too Many Accruals 23.0%Unclear Roles and Responsibilities 16.5%Non-standard Templates 13.7%Too Many Review Points 10.1%

Common Pain Points

•Close process exceeding 5 day benchmark•Finance resembles a fire-drill during the monthly close process•All other finance activity shuts down during month-end close•Reports are too late, too difficult to understand, overly complex, suspect or often revised•Differences between internal and external financial reports; conflicting internal reports•Reports are usually created in spreadsheets•Limited capacity or ability to report operational metrics or KPIs•Disparate and disconnected business and financial systems•Multiple, nonstandard or overly complex charts of accounts (the basic ‘bones’ of the accounting system)

Financial Closing Strategies

Getting Started

• Two overlapping strategies are often at work when organizations have fast monthly, quarterly, and annual accounting closes.

• These strategies are: 1. Leveraging Technology -Invest in robust information technology systems 2. Work Flow Optimization - Implement best practices

• Managers reorganize processes or tweak procedures inside the accounting and finance function so that their staffs produce accounting information in ways that are faster, smarter, better, and cheaper.

• With this approach, the operative dynamic is continuous improvement, with managers regularly monitoring and adjusting each component of a close so that efficiency and value rise.

Leverage Technology

• Start small and work up

• ADP • Current version? Fewer hours on payroll can free up time for the close

• Import payroll to GL using templates.

• Depreciation – automate

• FAS 123r – automate

• GL software

• Train, Train, Train – Excel etc.

• Recent college grad program

Financial Closing Best Practices

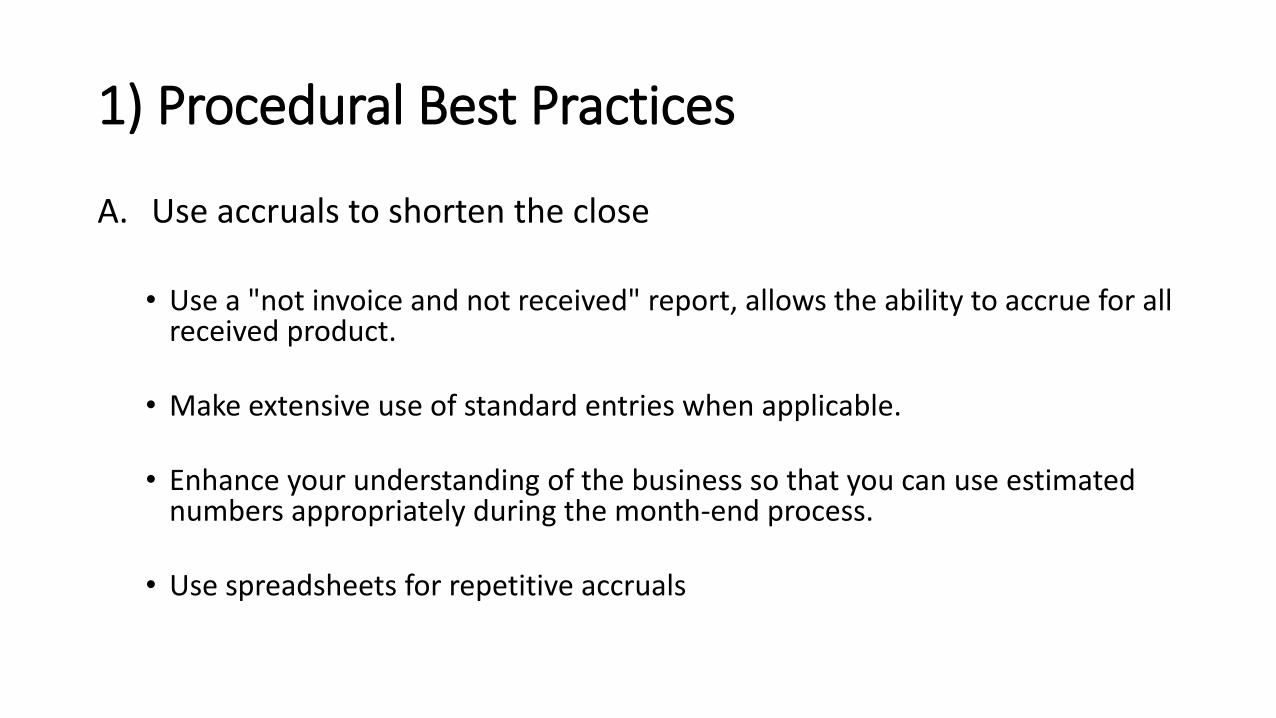

1) Procedural Best Practices

A. Use accruals to shorten the close

• Use a "not invoice and not received" report, allows the ability to accrue for all received product.

• Make extensive use of standard entries when applicable.

• Enhance your understanding of the business so that you can use estimated numbers appropriately during the month-end process.

• Use spreadsheets for repetitive accruals

1) Procedural Best Practices (cont.)

• Examples of accruals used to shorten the close

• Annual bonus – Q1 to Q3 accrue 1/12 each month. True up in Q4

• Audit, tax and other services – level load

• Conferences and other marketing costs – based on budget

• Focus on accruals for the January close – invoices post in February.• Travel

2) Cross-train Staff • Cross-training and documentation of the close processes have proven very

beneficial, especially when there is an unexpected absence of a critical associate

• This approach allows validates procedures, checklists, and controls

• Included on Month end close checklist

• Incorporated into annual review and merit increase process

• New college graduation/Front desk position

3) Document each process

• Document all steps of the closing process and ensure all those impacted by the close are trained

• Communicate the importance of the close and the critical nature of financial reporting

• Hold controller review meetings during the close • (ABCDE)

• Hold a post close review

• Continuously improve your process! NCAA – UNC – Getting better everyday!

4) Create templates for recurring reports

• Implement standardized closing packages. The subsidiaries use standard templates to reconcile material accounts

• Use templates for recurring reports. This makes month-end closing much faster

• Use a standardized management reporting process, which can result in greater efficiencies in reporting

• Streamline the use of recurring journal entries through the use of templates.

5) Reduce Investigation Levels

• Document a “soft close” versus “hard close” rules and guidelines.• Accounts payable

• After doing so, transition from a monthly “hard close” to “soft monthly closes” and “quarterly hard closes”.

• This approach has forces the organization to reduce investigation levels and rely on accruals and estimates during “soft closes,” in order to reduce our average number of days to close.

• Free up time for larger projects

6) Minimize journal entries during the close process• Make greater use of importing tools to upload information into the

accounting package. This minimizes duplicate data entry.

• Minimize manual data entry during the close, and urge staff to have accounts payable invoices entered in a more timely and accurate manner.

• Upload entries as opposed to manual entries.

• Automate the journal entry process!

7) Move Routine Work Out of the Closing Crunch

• Move routine work out of the closing crunch.

• Move recurring allocations and accruals back from the close. As a result, this can shorten the number of days used for posting journal entries during the close.

Financial Close Process Metrics

• Time to close the processing of period-end cash

• Time to finish processing accounts payable

• Time to issue billings to customers

• Time to close payroll and record accrued wages

• Time to count and value ending inventory

• Time to issue related management reports

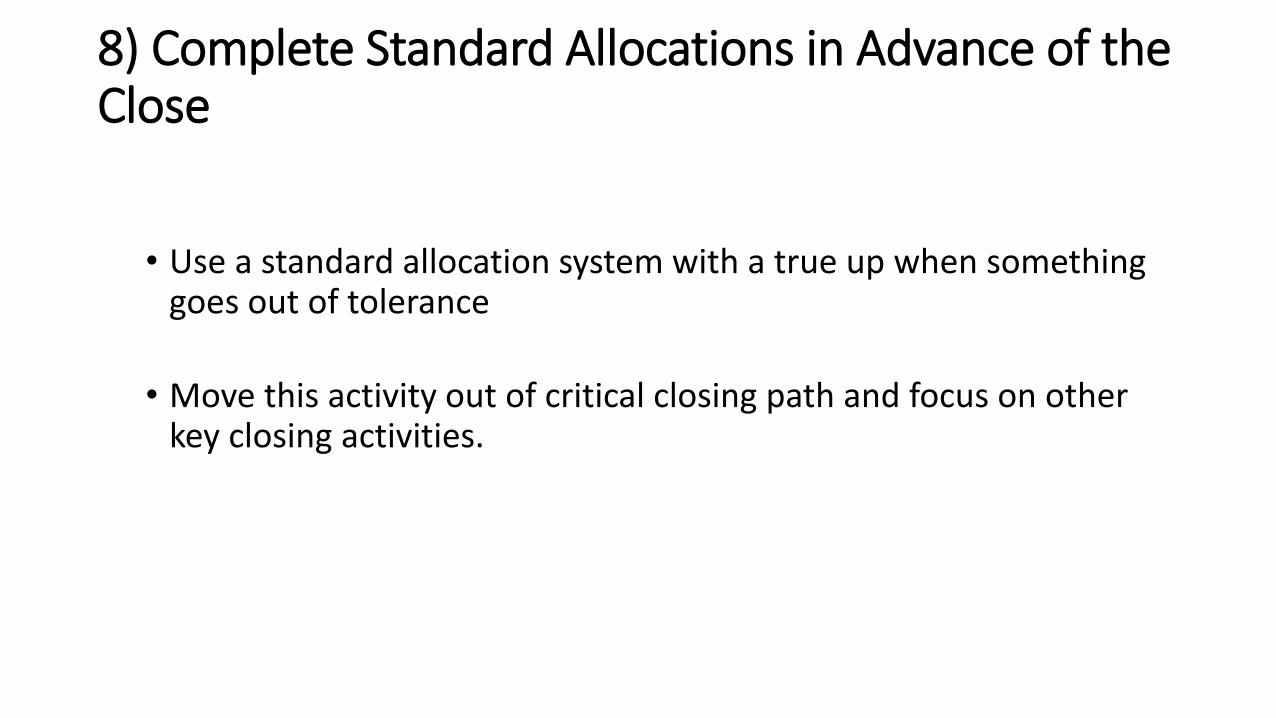

8) Complete Standard Allocations in Advance of the Close

• Use a standard allocation system with a true up when something goes out of tolerance

• Move this activity out of critical closing path and focus on other key closing activities.

2) General Ledger Best Practices

• Eliminate unused accounts and in the general ledger.

• Implement a chart of accounts structure and policy – Minimize # of accts

Use Expense account reconciliations

• Alleviate unused or inactive cost centers.

• While these accounts do not necessarily slow the close, they can create the opportunity for fraud, as well as endow financial reports with needless precision.

• At the same time, a graveyard of unused accounts can be aggravating to senior executives, who often prefer flash reports or quick summaries of business drivers or key developments for their monthly closing sign-offs.

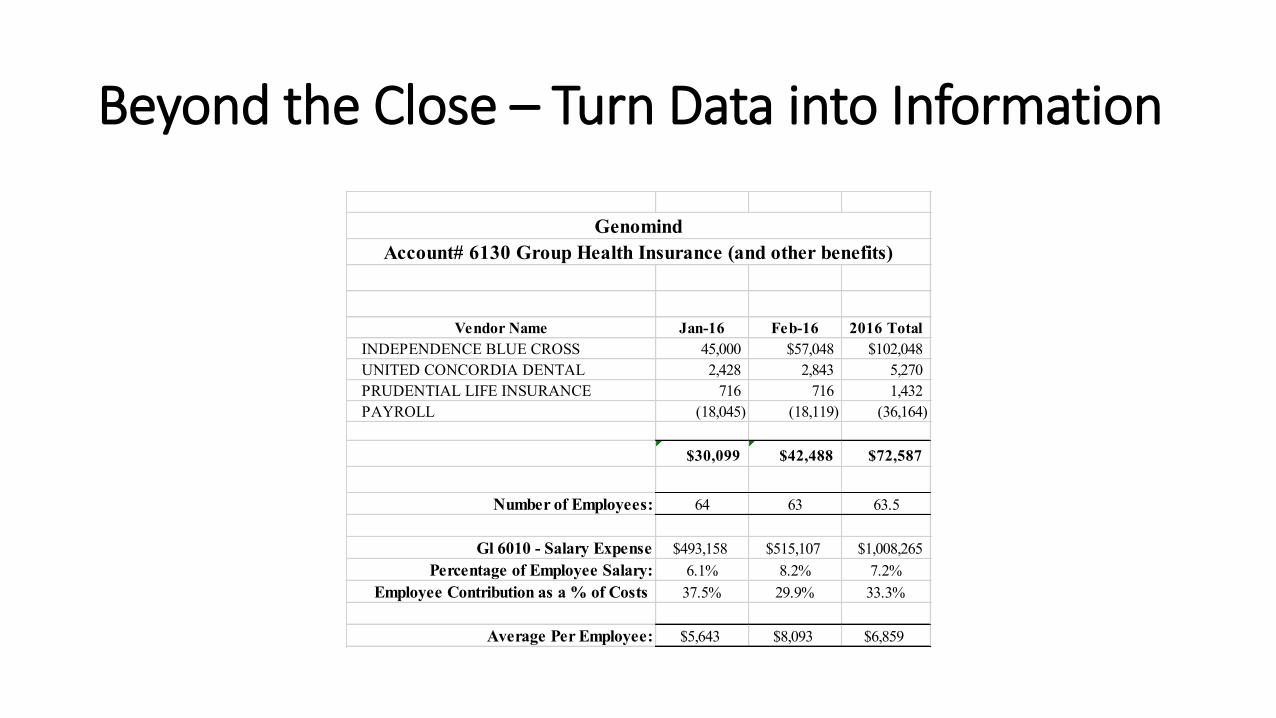

Beyond the Close – Turn Data into Information

Genomind

Account# 6130 Group Health Insurance (and other benefits)

Vendor Name Jan-16 Feb-16 2016 Total

INDEPENDENCE BLUE CROSS 45,000 $57,048 $102,048

UNITED CONCORDIA DENTAL 2,428 2,843 5,270

PRUDENTIAL LIFE INSURANCE 716 716 1,432

PAYROLL (18,045) (18,119) (36,164)

$30,099 $42,488 $72,587

Number of Employees: 64 63 63.5

Gl 6010 - Salary Expense $493,158 $515,107 $1,008,265

Percentage of Employee Salary: 6.1% 8.2% 7.2%

Employee Contribution as a % of Costs 37.5% 29.9% 33.3%

Average Per Employee: $5,643 $8,093 $6,859

3) General Ledger Best Practices (Continued)

• Minimize accounting data in the core general ledger by limiting code segments to sub-ledgers.

• This is a somewhat overlooked opportunity to improve the close process, since keeping the general ledger relatively simple accelerates data roll-ups, as well as pushes problem resolution into payables, receivables, and other departments that are closer to transactions.

• Companies can increase their use of the best practice “simplify transaction and accounting codes.”

• Such simplification is a small but important change, since it does accelerate data input and consolidation.

3) Managerial Best Practices • Implement a closing checklist indicating + or – days from the period

end to complete tasks.

• Have clear schedules and everyone understands what is expected.

• Establish clear accountability for closing tasks and a closing schedule and have frequent communication throughout the closing process.

• The closing process is a large portion of an accounting manager’s annual performance objectives, which puts a focus on the process at all times.

Close Schedule Format Task No. Day Activity Date Time Taken Primary Cross Training

1 -13 Post payroll bank transaction (SB 2 days prior to pay) 2/13 TH 0.50 Amy Alicea

2 -11 Record Payroll entry - period 1 Break out wages by department for G/L 60000-00. Post to accrued payroll and do bank transaction for cash account. 2/14 F 1.00 Amy Alicea

3 -13 Receive reporting revenue from Maureen & create invoices for review - Ck EIN# 2/13 TH 4.00 Minh Melissa

4 -11 Make sure Computershare Invoice has been received for prior month. Invoice is sent to Kevin Hartman 2/14 F 0.50 Nicole Amy

5 -11 Send Flexible Spending Account File to Vantagen - employee deductions for medical, dependent care & transit 2/14 F 0.50 Amy Nicole/Casey

6 -11 Send Healthcare Savings Acct. File to Wells Fargo - employee deductions and employer contribution 2/14 F 0.50 Amy Nicole/Casey

7 -11 Post Reporting Revenue from Maureen after invs are reviewed/credit Postage Exp - EIN number= 26-3855734 2/14 F 1.00 Minh Melissa

8 -9 Forward emails of new client request form to Tom, Alicea, Melisa to verify if sign contract existed before assiging GP ID 2/18 T 0.50 Minh Melissa

9 -9 Record $160,767 Management bonus accrual Dr. 63000 Bonus Exp. Cr. 20230 Accrued Bonus - Mgmt. 2/18 T 0.50 Nicole Alicea

10 -9 Post entry to amortize debt discount over the term of the debt agmt. $10,400/month Dr. 80400 Cr. 25114 2/18 T 0.50 Nicole Alicea

11 -9 Accrue $10K for Client holiday party Dr. 70100-00 Event & Conference. Cr. 20100-00 Accrued Expenses 2/18 T 0.50 Nicole Alicea

12 -9 Record $6,820 accrual for Annual Maranon Credit Facility fees Dr. 80200 Cr. 20100 (75K/11mo=$6,820) - No rec 2/18 T 0.50 Nicole Alicea

13 -9 Record Deferred Rent $416 for PA facility Credit Rent Expense 71000 and Debit Deferred rent 23600 The amount changes in August 2014 2/18 T 1.00 Nicole Alicea

14 -8 Reconcile Gl 16990 - Goodwill - annual impairment test 2/19 W 0.50 Lori Alicea

15 -8 Reconcile Gl 16991/17991 - Customer Relationships Record monthly entry: Dr. 74350 Cr. 17991 2/19 W 0.50 Lori Al

16 -8 Reconcile Gl 16992/17992 - Covenant Not to Compete Record monthly entry: Dr. 74350 Cr. 17992 2/19 W 0.50 Lori Al

17 -8 Accrue Outside sales people commissions $58,333 Dr. 65000-00 Cr. 20220-00 2/19 W 0.50 Nicole Alicea

18 -8 Accrue $2,500/month (Jan to Feb for Broadhaven travel expenses) Dr. 80500-00 Cr. 20100-00 2/19 W 0.50 Nicole Alicea

19 -8 Post Current Month UNUM Invoice for ST disability, LT disability, & grp Life insur - receive invoice around 20th of month 2/19 W 1.00 Nicole Amy

20 -7 Accrue CEO Club $23,750.00 Dr 75200-00 CR 20100-00 2/20 TH 0.50 Nicole Alicea

21 -7 Set up meetings with Kevin Hartman, Bill Berger, Jarrett Roth & Dennis Hughes for AR file reviews 2/20 TH 0.50 Alicea Melissa

22 -7 Send DST $1.5k inv, Fidelity $3K, JP Morgan Chase $3K, Plains All Amer $3k, Parago $1.5k Qtrly(Mar, Jun, Sep, Dec), BFDS Semi-Annual-Rpt (Aug, Feb), Schwab $8K (annual) 2/20 TH 1.00 Minh Melissa

Financial Close Process Metrics“You can only manage what you can measure”

• Gross number of adjusting entries. Transaction errors must be corrected, and their correction delays the closing process. Thus, investigating the gross number of adjusting entries can be used to track down issues that are delaying the close.

• Review errors. Note the types of errors found during the initial review of the financial statements. This information can be used to track down and correct underlying problems that can be prevented during future closing processes.

• Completion times. Further refine the duration of the closing process to focus on each category of activities that must be completed, to understand not only how long they take, but also how they are impacted by other steps in the closing process. Some of these measurements by activity type are: Time for subsidiaries to forward their results to corporate headquarters

• Time to close the processing of period-end cash

Road Blocks Encountered Along the Way

•Failure of staff to prioritize (ABCDE)

•CEO requests – “the close is not important”

•Colleagues in other departments and chasing butterflies

•Illness, Time off, Attitude

Do you have the guts to get rid of the a bad employee?

•Work from home – one day per quarter if not more.

Outside Reading

• Time management – Brian Tracy

• Essentialism – The Disciplined Pursuit of Less• Buffers - 50% longer,

• identify the bottlenecks,

• boy scout example

• Getting Things Done: The Art of Stress Free Productivity