Embed Size (px)

Citation preview

NICHOLAS HALL & COMPANY

SUCCESSFUL OTC BRANDS

Volume 2Investigating Strategies for Success

Successful OTC Brands 2: Investigating Strategies for Success Published by Nicholas Hall’s Reports, October 2014 © Nicholas Hall & Company Guernsey

Nicholas Hall’s Reports™ ® is a registered trademark belonging to Nicholas Hall

Nicholas Hall & Company 35 Alexandra Street Southend-on-Sea SS1 1BW, UK

T: +44 (0) 1702 220 200 F: +44 (0) 1702 430 787

This report may not be reproduced in any form or for any purpose without prior knowledge and consent of the publisher.

The information in this report is believed to be correct at the time of publication. However, no responsibility can be accepted by the publisher for its completeness or accuracy. If you would like clarification of any information in this report, or would like to point out any inaccuracies or omissions, please contact: Ian Crook, Managing Editor e: [email protected]

For information on other products and services provided by Nicholas Hall & Company, or for additional copies of this report, please contact: Val Tsang, Group Director of Marketing & Sales T: +44 (0) 1702 220 223 e: [email protected]

3

Definitions & Methodology

Definitions

An oblique mark (/) is used to show the ultimate owner of a company, e.g. “McNeil / Johnson & Johnson”; the term “for” is used to indicate that the former company markets a brand under license from the latter, e.g. “Novartis for Boehringer Ingelheim”.

The term “mass market” is used to mean sales through non-pharmacy retail outlets.

“Principal markets” or “key markets” for a given company are examples of some of the most important countries or regions where the company generates sales, rather than an exhaustive list of countries where it markets products.

OTC Market Definition

Market sizes, growth rates and brand sales are, unless stated otherwise, based on Nicholas Hall & Company’s global OTC database, DB6. All data is being updated continually, and is believed to be accurate at the time of going to press.

All OTC market data contained in this report is expressed at manufacturer’s selling prices (MSP), although it relates to consumer purchases. Sales data includes all non-prescription sales. Data includes retail sales in all outlets. Mail order, multi-level, e-commerce and other non-retail sales are not included.

Sales data is for the calendar year January-December for each year shown, unless otherwise stated. All data is calculated in local currency and converted to US dollars at the exchange rate that applied on 31 December 2013. The symbol $ refers to United States dollars unless otherwise stated.

Under-the-counter (UTC) sales are not included except in countries where there are few or no legal OTCs (such as Turkey) where UTC sales are included for products that fall within the DB6 category definition and would be considered consumer items in most established OTC markets.

Non-prescribed sales of semi-ethical brands (which can be sold both with and without a prescription) are included in all sales estimates. Prescription sales of OTC-registered brands are included where these sales are significant. Sales of traditional medicines (e.g. TCM, jamu and ayurvedic), homeopathic medicines, food supplements and medical devices are included where they are packaged and positioned alongside registered OTCs.

A+P advertising & promotion

BTC behind-the-counter

j-v joint-venture

L&A licensing & acquisition

MSP manufacturer’s selling price

M&A merger & acquisition

OTC over-the-counter

POS point-of-sale

Rx prescription

SPD separation of prescribing and dispensing

UTC under-the-counter (illegal OTC sales of Rx-only products)

Abbreviations

4

OTC Market Definition (continued)

Manufacturers’ sales data is based on branded products alone. Manufacturers’ sales do not include any private label sales to retailers or bulk sales of unbranded products to other manufacturers or distributors. Sales of individual private labels are included in “others” in each sub-category.

Sales data for each manufacturer includes sales made by any national or international subsidiaries.

All acquisitions are added to manufacturers’ historical data so growth excludes the effect of M&A activity.

Volume sales, where available, represent the absolute number of packs sold (unadjusted for size / dosage).

All forecasts take into account published socio-economic and demographic forecasts plus OTC-specific factors such as switch, regulatory change and historical trends.

5

Table of Contents

Definitions & Methodology 3

Introduction 10

Alka-Seltzer (Bayer) 11

Overview 11

2014 developments 12

Key market: the US 13

Heartburn relief 14

Tackling competition head on 16

Hangover cure? 18

A look to the future 19

Asepxia (Genomma Lab) 20

Overview 20

2014 developments 21

Key market: Brazil 22

Cross-marketing 23

Genomma’s A+P engine 24

Scientific backing 26

A look to the future 27

Aveeno (J&J) 28

Overview 28

2014 developments 29

Key market: the US 30

OTC expansion 31

Natural 32

Jennifer Aniston 33

Healthcare professionals 34

Digital tools 35

Look to the future 37

6

Berocca (Bayer) 38

Overview 38

2014 developments 39

Key market: the UK 40

Advertising trends 41

Targeting a new audience 43

Innovative sampling techniques 44

Digital integration 46

Providing convenience 47

US launch 49

Look to the future 51

Blackmores (Blackmores) 52

Overview 52

2014 developments 53

Key market: Australia 54

Concept stores 55

The natural health experts 56

Strong promotional support 57

Michelle Bridges 59

The importance of community 60

Geographical expansion 61

Look to the future 62

Dulcolax (BI) 63

Overview 63

2014 developments 64

Key market: the US 65

Extensive range 66

Global marketing 67

Striking A+P 68

Tackling consumer perceptions 69

Cancer awareness campaigns 71

Look to the future 72

7

Elevit (Bayer) 73

Overview 73

2014 developments 74

Key market: China 75

Brand development 76

Targeting all women 77

Partnerships 78

Online tools 80

Look to the future 81

Fenistil (Novartis) 82

Overview 82

2014 developments 83

Key market: Germany 84

Brand developments 85

What’s in a name? 86

Tinted cold sore cream 87

Paediatric focus 88

Memorable A+P 89

A look to the future 91

MegaRed (Reckitt Benckiser) 92

Overview 92

2014 developments 93

Key market: the US 94

Distinguishing the brand 95

Ethically sound 98

Putting the heart in heart health 99

UK launch 102

Look to the future 103

Nexium (Pfizer) 104

Overview 104

US launch 105

Sponsorship 107

Worldwide developments 108

Challenges for Nexium 109

The power of purple 110

A look to the future 111

8

Nicorette (J&J, GSK) 112

Overview 112

2014 developments 113

Key market: the US 114

Brand developments 115

A personal connection 117

Tobacco-free India 118

Quitting tools 119

Marketing to healthcare professionals 120

Tackling e-cigarettes 121

A look to the future 122

No-Spa (Sanofi) 123

Overview 123

2014 developments 124

Key market: Russia 125

50 years in Russia 126

Educative A+P 127

Mothers and daughters 128

Reaching a new audience 129

A look to the future 130

Panadol (GSK) 131

Overview 131

2014 developments 132

Key market: Australia 133

Speed of relief 135

Looking beyond pain relief 136

Reaching out to mothers 138

Thinking globally and locally 139

Headaches in Malaysia 140

Brand diversification 141

Panadol Cosy Corner 142

A look to the future 143

9

Solpadeine (Omega Pharma) 144

Overview 144

2014 developments 145

Key market: the UK 146

Codeine issues 147

Traditional advertising 148

A return for Solpadeine 149

Pharmacists 150

A look to the future 151

ZzzQuil (P&G) 152

Overview 152

2014 developments 153

Launch success 154

One focus 155

A love letter to sleep 156

Bored to sleep 157

Social media 158

The wider P&G machine 159

A look to the future 160

10

Many leading OTC brands are finding it tough: they face mounting competition from cheaper private labels and consumers looking for more value-conscious options alongside changing regulatory conditions that are, for some brands, restricting sales avenues. However, the fifteen brands profiled in this report have held strong despite these challenging market conditions.

Looking at the world’s Top 20 OTC markets in the 12 months to June 2014, growth was up by just +3.7% overall. Yet the brands profiled in this report together posted a topline increase of +7.8% in those same markets. This is despite the fact that each brand faced significant challenges, be it the competition for Nicorette that arose not only within the smoking control category but also from outside factors such as electronic-cigarettes, or that Nexium launched in a market where a wealth of PPI options were already available.

There is no quick-fix solution, but the following case studies provide insight into best practices and techniques that have propelled these brands to success. They illustrate the importance of building brand loyalty, the possibilities of extending a brand into new OTC categories and the opportunities that arise from powerful promotional support.

Introduction

145

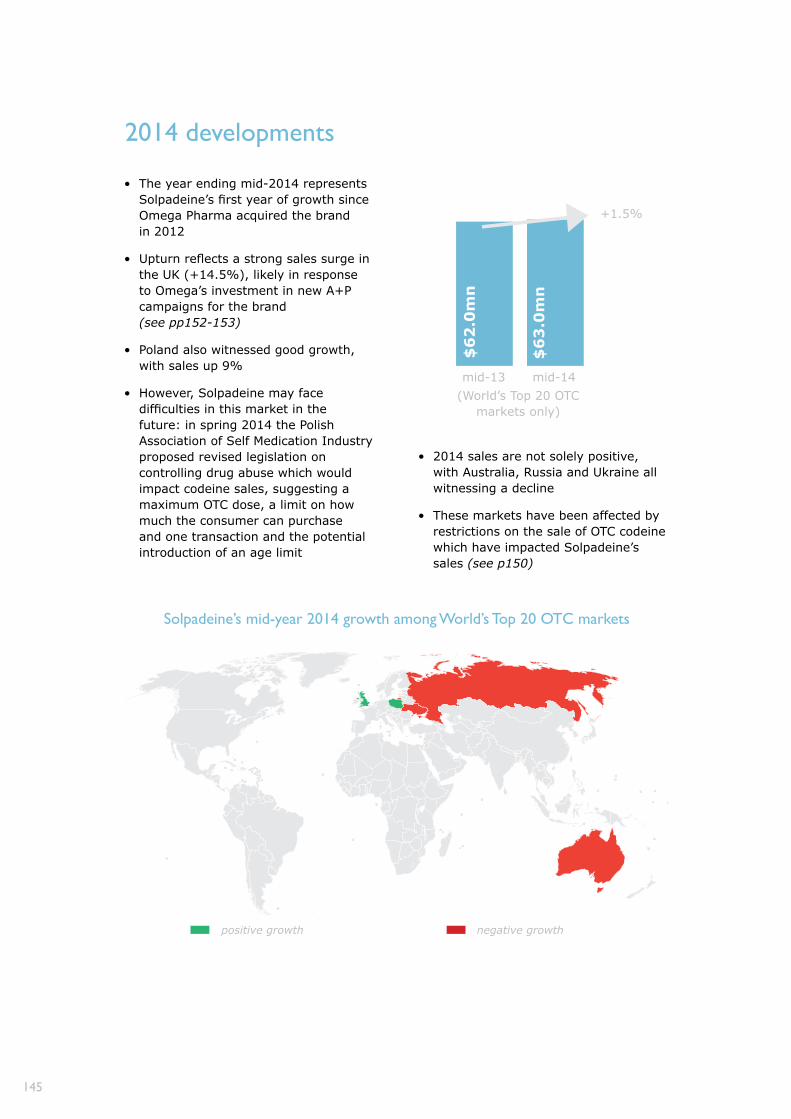

2014 developments

$6

2.0

mn

mid-13 mid-14

$6

3.0

mn

+1.5%

(World’s Top 20 OTC markets only)

• The year ending mid-2014 represents Solpadeine’s first year of growth since Omega Pharma acquired the brand in 2012

• Upturn reflects a strong sales surge in the UK (+14.5%), likely in response to Omega’s investment in new A+P campaigns for the brand (see pp152-153)

• Poland also witnessed good growth, with sales up 9%

• However, Solpadeine may face difficulties in this market in the future: in spring 2014 the Polish Association of Self Medication Industry proposed revised legislation on controlling drug abuse which would impact codeine sales, suggesting a maximum OTC dose, a limit on how much the consumer can purchase and one transaction and the potential introduction of an age limit

• 2014 sales are not solely positive, with Australia, Russia and Ukraine all witnessing a decline

• These markets have been affected by restrictions on the sale of OTC codeine which have impacted Solpadeine’s sales (see p150)

Solpadeine’s mid-year 2014 growth among World’s Top 20 OTC markets

positive growth negative growth

56

• Maurice Blackmore, the founder of Blackmores, developed his whole healthcare system on naturopathic principles and this remains a core component of Blackmores’ ethos, advertising and company development

• The focus on naturopathy is clear in Blackmores’ home market; the company offers the “Ask a Naturopath” service in Australia, where consumers can contact a natural health specialist via phone, online chat or email to receive advice on health & wellbeing

• Consumers can also create a personalised healthcare programme, with naturopaths on hand to advise on progress

• Looking at the concept stores, a key point of difference in Blackmores stores from other VMS retail specialists such as GNC and Eu Yan Sang is the option for consumers to have a naturopathic health consultation for RM100 (US$29.90), carried out by a trained naturopath

• The service is aimed at consumers who want to improve fitness, achieve better nutrition, optimise general health or get advice on certain health conditions

• The four elements to the service are:

» Health assessment: the consumer answers a set of questions about their diet and lifestyle and then speaks to the in-store naturopath about the state of their health

» Iridology test: the naturopath examines the consumer’s irises to identify factors relating to any health issues

» Lifestyle plan: the naturopath analyses the information gathered in the first and second stages and identifies areas of health that need optimising and recommends holistic changes to lifestyle, exercise habits and diet to achieve this aim

» Product recommendations: the consumer is given recommendations by the naturopath about which Blackmores supplements to take (where necessary)

• The consumer is invited to come back 1-3 weeks after the consultation to assess their progress in sticking to the recommendations and improving their health

• Consumers have so far reported that the personalised service has been helpful and view it as a credible way of fulfilling the need for preventive healthcare

• This interest in natural health education is not just consumer-focused

• In August 2012, the company announced the establishment of the Blackmores Institute with the purpose of becoming a centre of excellence in the field of natural health research and education

• Blackmores Institute has produced guides on how VMS products can interact with other drugs / OTCs that consumers are taking to ensure that pharmacists can appropriately guide their customers

• It also offers CPD-accredited courses on a range of topics for pharmacists and doctors

The natural health experts

28

Aveeno (J&J)

Global OTC Ranking 146

Category derma range

Leading MarketsUS (82%)

UK (14%)

Sales 2013 $95.3mn

Growth 13/12 +12.0%

CAGR 13/09 +18.0%$

49

.2m

n

09 10 12 1311

+17%

+28%

+16%

+12%

$8

5.1

mn

$7

3.6

mn

$5

7.4

mn

$9

5.3

mn

• Cosmeceutical skin care range Aveeno is one of J&J’s most successful (and its fastest-growing) derma umbrella brands

• However, when J&J acquired the brand in 1999 its bright future was not a certainty

• J&J worked hard to leverage the power of its natural formulation (colloidal oatmeal is the key original ingredient) to sway both consumers and dermatologists

• In addition, the product line-up was significantly expanded, with a widening cosmetic range and expansion into the OTC field

• Brand spans a wide variety of OTC derma categories, with the range most diversified in its largest market, the US

Overview

86%North America; CAGR +18.2%

Western Europe; CAGR +16.4%

14%

13

Key market: the US$

13

4.0

mn

09 10 12 mid-1311

-6%+9%

+27%

+23%

$2

15

.9m

n

$1

38

.5m

n

$1

26

.5m

n

$1

75

.8m

n

13 mid-14

$2

09

.6m

n

$2

24

.0m

n

Sales 2013 $215.9mn

Growth 13/12 +22.8%

CAGR 13/09 +12.7%

Sales mid-14 $224.0mn

Growth mid-14/mid-13

+6.9%

• While Alka-Seltzer’s heritage is in the antacids category it is actually its cold & flu presentation that is the key growth driver in the US market

• The Alka-Seltzer Plus range reached sales of $163.4mn in 2013 following years of dynamic double-digit growth

• In contrast, the brand has struggled in the antacids category, although did return to growth in 2013

• Recent activity in the antacids category has focused on taste and texture

• The range was expanded in 2013 with new Fruit Chews tablets that are smooth, not chalky or gritty, in an assortment of three flavours per pack (subsequently rebranded Relief Chews)

• This competes directly with GSK’s popular Tums Smoothie option

• 2014 also saw the brand extend into antiflatulents with a dual action option for relief from heartburn and gas

• The Plus systemic cold & flu range was in part boosted by the misfortune of rivals, with Novartis’ Theraflu affected by recalls and manufacturing issues over 2012-14, and Tylenol cold & flu range similarly affected by troubles plaguing J&J in 2011

• Bayer supported the Plus range with a very strong advertising campaign over 2012-14, directly comparing presentations to their branded competition and illustrating the benefits of the Alka-Seltzer options (see p16)

• In addition to this A+P, the range has been supported by product innovation

• Bayer launched its first behind-the-counter, PSE-based cold & flu remedy in summer 2013, unveiling Alka-Seltzer Plus-D Multi-Symptom Sinus & Cold, in packs of 20 liquigels

• Launches continued in 2014, with Alka-Seltzer Plus Severe Sinus & Cold hot drink powder hitting the shelves