Embed Size (px)

Citation preview

Successful Crowdfunding: The Effects of Founder and Project Factors

Meng Hong Por One More Restaurant

#37 Street 315, Beoung Kak 1 Commune

Phnom Penh City, Cambodia +855-78-385-070

Sung-Byung Yang School of Management, Kyung Hee

University 26, Kyungheedae-ro, Dongdaemun-gu

Seoul, South Korea +82-2-961-9548

Taekyung Kim College of Business Administration,

The University of Suwon 17 Wauan-gil, Bongdam-eup Hwaseong-si, South Korea

+82-31-220-2149

ABSTRACT

Crowdfunding has been regarded as a novel way of collecting

money for innovators to launch products and services by opening

their ideas in online. This funding approach is differentiated from

a traditional fundraising alternative in terms of project evaluation

and risk management. In this paper, we question the reason why

some crowdfunding projects are more successful in the context of

a pre-ordering model, also known as a reward-based

crowdfunding. Data analysis results based on 704 Kickstarter

projects showed that founder’s prior experiences would influence

successful fundraising. User comments and update efforts have

positive effects on the increase of success rate. In addition, we

examined that the amount of funding goal had negative

association with fundraising success.

CCS Concepts

• Information systems ➝ Information systems applications ➝

Collaborative and computing systems and tools

• World wide web ➝ Web applications ➝ Crowdsourcing

Keywords

Crowdfunding; successful fundraising; crowdsourcing

1. INTRODUCTION One of the biggest problems of innovative projects is lack of

financial supports. This is true for scientific research projects, and

is also applicable for entrepreneurs who do not have credible

reputation. Traditional and even novice way to overcome this

issue is to borrow money from friends who know the project. Of

course, there are open chances to get financial supports from

banks and venture capitalists; however, proving potential values

about innovation is difficult for inexperienced founders. Moreover,

the idea is not usually validated in a test market, which means

backup data are lack of reality (Berger and Udell, 1998).

Thanks to collaborative technologies in the information system

domain, the desperate entrepreneur can have a new financial

supporting alternative, named by Crowdfunding. Crowdfunding

refers to a new way of collecting money from people in online

without personal contact (Fernandes, 2013). The process is simple.

An entrepreneur, known as a project founder in crowdfunding,

posts his or her business project on the Internet. Potential

investors (also known as backers) around the globe search or

browse projects to find out which one is interesting. A

crowdfunding platform helps entrepreneurs establish a semi-

structured webpage for advertising their idea, and it also provides

an opportunity for getting innovative products/services in advance

of marketization. The key idea behind crowdfunding is that

collective wisdom works well for evaluating a project. In

crowdfunding, entrepreneurs do not have to worry about losing

the control of a company while obtaining extra funds (Valanciene

and Jegeleviciute, 2013). In addition to raising fund,

crowdfunding has served as an indication whether or not there is a

market for a newly creative product (Mollick, 2014; Valanciene

and Jegeleviciute, 2013).

Although crowdfunding appears to be a winning strategy for

entrepreneurs, successfully reaching a funding goal is

challengeable. It should be noted that face-to-face communication

with project founders is replaced by computer-mediated

communication, which indicates that there are less social cues and

more ambiguity for judging quality of suggested project (Okdie et

al., 2011). Indeed, we should be aware that information sources

and investment experiences are limited in crowdfunding. There is

no guarantee that investors are specialists in funding innovative

idea. Returns of investment are settled down mainly by a founder.

Moreover, there are less physical evidences on credibility to the

business. Compared to buying an innovative product from a

matured company in online market, receiving goods or service

rights is not deterministic. Therefore, filtering out successful

projects in advance should be regarded as a key task for

improving fundraising quality.

In this study, we question why some of crowdfunding projects are

more successful than others. This research question is more

Permission to make digital or hard copies of all or part of this work for

personal or classroom use is granted without fee provided that copies are not made or distributed for profit or commercial advantage and that

copies bear this notice and the full citation on the first page. Copyrights

for components of this work owned by others than the author(s) must be honored. Abstracting with credit is permitted. To copy otherwise, or

republish, to post on servers or to redistribute to lists, requires prior

specific permission and/or a fee. Request permissions from [email protected]. ICEC '16, August 17 - 19, 2016, Suwon,

Republic of Korea.

Copyright is held by the owner/author(s). Publication rights licensed to ACM. ACM 978-1-4503-4222-3/16/08…$15.00

DOI: http://dx.doi.org/10.1145/2971603.2971611

described by the following sentence: which factors influence the

possibility of success? We collected a real world crowdfunding

data in order to answer the question based on 704 cases from

Kickstarter. The following section starts with a background study.

The next section explains our hypotheses. The following part

includes data descriptions and analysis results. This paper

concludes with theoretical and practical implications. Future

research agenda will be added.

2. BACKGROUND

2.1 Crowdfunding From 2011, approximately 1.5 billion dollars were collected

through around 500 crowdfunding platforms worldwide.

Crowdfunding becomes a primary channel for introducing

innovative products/services (Giudici et al., 2013). Schwienbacher

and Larralde (2010) describes crowdfunding as an open call,

essentially through the Internet, for the provision of financial

resources either in form of donation or in exchange for some form

of reward and/or voting rights in order to support initiatives for

specific purpose.

Stakeholders in crowdfunding are categorized into two types:

founders and investors (also known as backers). Based on a

crowdfunding project, those different sides meet together. Their

cooperation aims to make the project real so that innovative

activities keep going (Gerber et al., 2012).

According to Belleflamme et al. (2014), initial capital requirement

influences a decision on crowdfunding. The decision made by

entrepreneur on which model of crowdfunding to pursue for their

venture is depended on initial capital requirement. In the case

when the initial capital requirement is relatively small,

entrepreneurs prefer a pre-ordering model. If the initial capital

requirement is higher, founders may prefer a profit-sharing

mechanism. Profit-sharing is a kind of traditional funding

strategies. Investors can make bigger money when a project is

successfully done. Since the share counts on the total amount of

sale in market places, the startup investors in crowdfunding

should have full responsibility on failure. To the contrary, a pre-

ordering model is unique in terms of responsibility and return. In

this model, a founder sets a target funding goal. If investors do not

comply to put money over the goal, the project is not funded. In

other words, this type follows an all-or-nothing scheme. Before

the project sells products/services in a real market place, a

crowdfunding platform provides an initial test market by placing

reward plans. For example, a founder can differentiate rewards for

different types of investors. If an investor decides to pay only 5

dollars, a product will be delivered. For an investor who pays 10

dollars, two products with a special gift will be given. This

rewarding process is complete before a founder goes into a mass

market.

Mollick (2014) reveals that personal networks of project founder

are significantly correlated with the success of crowdfunding.

Fernandes (2013) insists using video clips is crucial for

crowdfunding success. Ward and Ramachandran (2010) show a

crowdfunding project can be influenced by a similar prior project.

A prior study on risks in crowdfunding reveals mechanisms for

reducing uncertainty influences success possibility (Ahlers et al.,

2015). Based on semi-structure interviews, Gerber et al. (2012)

found that extrinsic motivation would play an important role for

crowdfunding success. Those prior studies provide insightful

ideas on crowdfunding success especially on a pre-ordering model,

also known as a “reward-based” model; however, they are lack of

a synthesized and simple structure to test effects of a founder

dimension and a project dimension on success rate.

2.2 Theory Base To develop a theoretical model considering both founder and

project dimensions in order to predict the success rate of

crowdfunding, we adopted the model of online review credibility

(Racherla and Friske, 2012), and the model of online trust

(Corritore et al., 2003).

Racherla and Friske (2012)’s model explains what makes online

reviews helpful for users. Based on persuasive communication

and source-related influential factor literatures, the model

indicates that review usefulness is influenced mainly by two

dimensions: messenger dimension and message dimension. The

relationships are moderated by different types of users’ decision

contexts.

The model of online trust explains external factors in an online

website influences trust levels. Specifically, Corritore et al. (2003)

studies online transactions to understand effects of website design

factors and prior experiences on using similar artifacts. The model

indicates that both individual factors in a perception level and

environmental factors in a design level should be considered to

understand how trust influences transaction performance in online

markets.

The abovementioned models commonly indicate that design

elements influence the success of crowdfunding. Moreover, those

should be rooted in both individual perception levels and project

characteristic levels. Project related information provides

information proxies for trust, credibility and functionalities (Qiu

et al., 2012). According to Metzger et al. (2010), cognitive

heuristics are useful in assessing information for successful

transactions in a computer-mediated environment. In this study,

we use design elements to predict a success ratio instead of using

self-reported survey items.

3. HYPOTHESIS A usual e-commerce website has information sources for

credibility. Company identity information plays an important role

that gives a clear image about business mission and customer

value. Corporate Identity (CI) provides a unified image to

customers and investors in a stock market. In the context of

crowdfunding, an external link for providing personal information

of founder has been adopted to achieve similar effects. Identity

information can be associated with credibility in online. Fogg et al.

(2001) reveals that identity disclosure (by showing name and

photo) strongly affects how consumer perceives trust.

H1. Identification information of founder increases the

possibility of success in crowdfunding.

Hsu (2007) finds in his study that entrepreneurs who have prior

founding experiences, especially those with financially successful

ones, are both more likely to acquire funding and have higher

valuations from venture capitalists. Similar finding is also

supported by MacMillan et al. (1986) in whose study indicates

that one of the most important criteria used by venture capitalists

to determine funding decision is entrepreneur’s experience.

Accordingly, the following hypothesis is derived.

H2. The level of prior experiences of collecting fund increases

the possibility of success in crowdfunding.

Shoppers are likely to listen to the others who are independent

with a company to get trustful information (Utz et al., 2012). In

the context of online crowdfunding, we expect that word-of-

mouth plays an important role to rule out biased decisions. It

should be noted that investors usually raise various questions

since a crowdfunding project is likely to be uncertain. A prior

study on the effects of user-generated reviews shows positive

association with sales and productive discussions (Chen et al.,

2004). Thus, we hypothesize:

H3. The number of comments increases the possibility of

success in crowdfunding.

It should be noted that a crowdfunding project requires progress

tracking. Projects displayed in a crowdfunding website, such as

Indiegogo, Kickstarter and Gofundme to name a few, are work-in-

progress in terms of lack of financial support, technical

incompleteness and marketization. Project Update can be useful in

distributing information about progress. The increase of

interactivity makes investors positively involved in project

development (Dwyer, 2007). In turn, we can assume that the

extent of efforts to interact with investors influence positively a

crowdfunding project. Thus, we hypothesize:

H4. The number of project updates is positively associated

with the possibility of success in crowdfunding.

Trustworthiness of a website is highly correlated with the extent

of elaborating information (Shelat and Egger, 2002). Elaborating a

description refers to an act of adding details about key information

sources for influencing an investment decision. In a crowdfunding

website, video clips, blueprints and interviews are likely to be

added to present more information. According to Mudambi and

Schuff (2010), depth of review descriptions in an online store

results in positive outcomes.

H5. The extent of elaborating descriptions influences

positively the probability of success in crowdfunding.

Investors cannot get a product or enjoy a service before a

crowdfunding project is complete. Simply, they should wait until

the project campaign reaches a finish line. Although long duration

of funding seems to be a safe choice for a founder, the possibility

of lagging product/service delivery can give a negative image to

investors. The traditional research stream about consumer

motivation reveals that time is a key for promotion success under

uncertainty (Belleflamme et al., 2014; Spears, 2001). Thus, we

hypothesize:

H6. Campaign period negatively impacts the probability of

success in crowdfunding.

Funding goal is suggested to be set at the minimum requirement

level of the startup requirement of a project (Cebulski, 2013).

High funding goal indicates high initial capital requirement for

project, which eventually gives signal of higher risk. This might

convey distrust on founder’s ability to complete the project. Thus,

we hypothesize:

H7. Increase of a funding goal influences negatively on the

probability of success in crowdfunding.

4. METHODOLOGY Data were collected from Kickstarter. At the moment of 2016,

over 9 million investors put money into more than 260,000

projects. The total amount of fundraising exceeds $2 billion. This

crowdfunding platform has been grown up rapidly so that

numbers should be read as proxies of its impact with caution.

There are fifteen types of project categories such as art, comics,

crafts, dance, design, fashion, film & video, food, games,

journalism, music, photography, publishing, technology, and

theater on this platform. Kickstarter adopts a reward-based

crowdfunding style, which means that an investor get a reward

defined in a funding contract in public. In addition, the reward

follows the all-or-nothing scheme. If a project fails to reach a

funding goal, investors lose the chance of getting a reward. Of

course, a founder cannot collect money from the failed project.

4.1 Data To avoid possible issues relating to live projects, we limited the

data set to 755 samples within 60 days which were completed in

January 2015. It should be noted that any failed projects can have

additional chances of redeploying slightly different products and

services in Kickstarter; therefore, one year lagged data can

provide chances for filtering out biased samples. Totally, 51

projects were discarded after inspection in this sense.

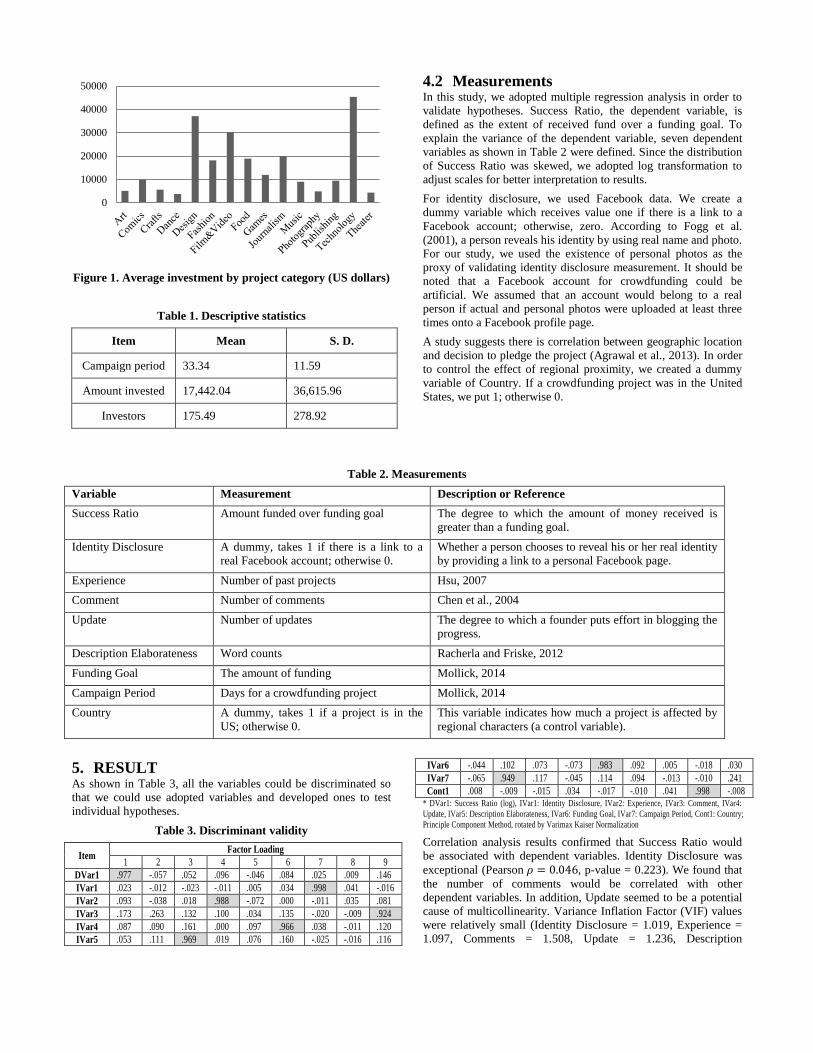

Descriptive statistics show that 79.4% projects are located in the

United States. Other regions include Australia, Canada, Denmark,

Great Britain, Ireland and New Zealand to name a few. As shown

in Figure 1, about 12 million USD were invested. Design and

technology were top-tier project categories with 37,150 USD and

45,361 USD in each on average (see also, Table 1).

Figure 1. Average investment by project category (US dollars)

Table 1. Descriptive statistics

Item Mean S. D.

Campaign period 33.34 11.59

Amount invested 17,442.04 36,615.96

Investors 175.49 278.92

4.2 Measurements In this study, we adopted multiple regression analysis in order to

validate hypotheses. Success Ratio, the dependent variable, is

defined as the extent of received fund over a funding goal. To

explain the variance of the dependent variable, seven dependent

variables as shown in Table 2 were defined. Since the distribution

of Success Ratio was skewed, we adopted log transformation to

adjust scales for better interpretation to results.

For identity disclosure, we used Facebook data. We create a

dummy variable which receives value one if there is a link to a

Facebook account; otherwise, zero. According to Fogg et al.

(2001), a person reveals his identity by using real name and photo.

For our study, we used the existence of personal photos as the

proxy of validating identity disclosure measurement. It should be

noted that a Facebook account for crowdfunding could be

artificial. We assumed that an account would belong to a real

person if actual and personal photos were uploaded at least three

times onto a Facebook profile page.

A study suggests there is correlation between geographic location

and decision to pledge the project (Agrawal et al., 2013). In order

to control the effect of regional proximity, we created a dummy

variable of Country. If a crowdfunding project was in the United

States, we put 1; otherwise 0.

Table 2. Measurements

Variable Measurement Description or Reference

Success Ratio Amount funded over funding goal The degree to which the amount of money received is

greater than a funding goal.

Identity Disclosure A dummy, takes 1 if there is a link to a

real Facebook account; otherwise 0.

Whether a person chooses to reveal his or her real identity

by providing a link to a personal Facebook page.

Experience Number of past projects Hsu, 2007

Comment Number of comments Chen et al., 2004

Update Number of updates The degree to which a founder puts effort in blogging the

progress.

Description Elaborateness Word counts Racherla and Friske, 2012

Funding Goal The amount of funding Mollick, 2014

Campaign Period Days for a crowdfunding project Mollick, 2014

Country A dummy, takes 1 if a project is in the

US; otherwise 0.

This variable indicates how much a project is affected by

regional characters (a control variable).

5. RESULT As shown in Table 3, all the variables could be discriminated so

that we could use adopted variables and developed ones to test

individual hypotheses.

Table 3. Discriminant validity

Item Factor Loading

1 2 3 4 5 6 7 8 9

DVar1 .977 -.057 .052 .096 -.046 .084 .025 .009 .146

IVar1 .023 -.012 -.023 -.011 .005 .034 .998 .041 -.016

IVar2 .093 -.038 .018 .988 -.072 .000 -.011 .035 .081

IVar3 .173 .263 .132 .100 .034 .135 -.020 -.009 .924

IVar4 .087 .090 .161 .000 .097 .966 .038 -.011 .120

IVar5 .053 .111 .969 .019 .076 .160 -.025 -.016 .116

IVar6 -.044 .102 .073 -.073 .983 .092 .005 -.018 .030

IVar7 -.065 .949 .117 -.045 .114 .094 -.013 -.010 .241

Cont1 .008 -.009 -.015 .034 -.017 -.010 .041 .998 -.008 * DVar1: Success Ratio (log), IVar1: Identity Disclosure, IVar2: Experience, IVar3: Comment, IVar4:

Update, IVar5: Description Elaborateness, IVar6: Funding Goal, IVar7: Campaign Period, Cont1: Country;

Principle Component Method, rotated by Varimax Kaiser Normalization

Correlation analysis results confirmed that Success Ratio would

be associated with dependent variables. Identity Disclosure was

exceptional (Pearson 𝜌 = 0.046, p-value = 0.223). We found that

the number of comments would be correlated with other

dependent variables. In addition, Update seemed to be a potential

cause of multicollinearity. Variance Inflation Factor (VIF) values

were relatively small (Identity Disclosure = 1.019, Experience =

1.097, Comments = 1.508, Update = 1.236, Description

0

10000

20000

30000

40000

50000

Elaboration = 1.225, Period = 1.120 and Goal = 1.439); therefore,

we concluded that the multicollinearity issue would not distort

results. In addition, we ran the Durbin-Watson test to understand

autocorrelation effects. The range of Durbin-Watson exists

normally from 0 to 4. If the value is close to 2, we accept it as no-

autocorrelation. The calculation result from our sample residuals

showed that autocorrelation would not be issue (DW = 2.003).

Fitness of regression model can be measured by an index for

coefficient determination. In our study, we used adjusted 𝑅2 to

understand how much the linear model was fitted into data. The

result was 20.3%.

Table 4. Correlation

Item Pearson Correlation

1 2 3 4 5 6 7 8 9

DVar1

IVar1 .046

IVar2 .204 -.020

IVar3 .315 -.034 .179

IVar4 .183 .066 .010 .304

IVar5 .124 -.044 .040 .301 .346

IVar6 -.085 .009 -.149 .095 .205 .171

IVar7 -.078 -.028 -.074 .489 .229 .266 .240

Cont1 .020 .081 .070 -.019 -.025 -.036 -.040 -.028 * Bold font refers to the Pearson correlation value is significant at 𝛼 = 0.05.

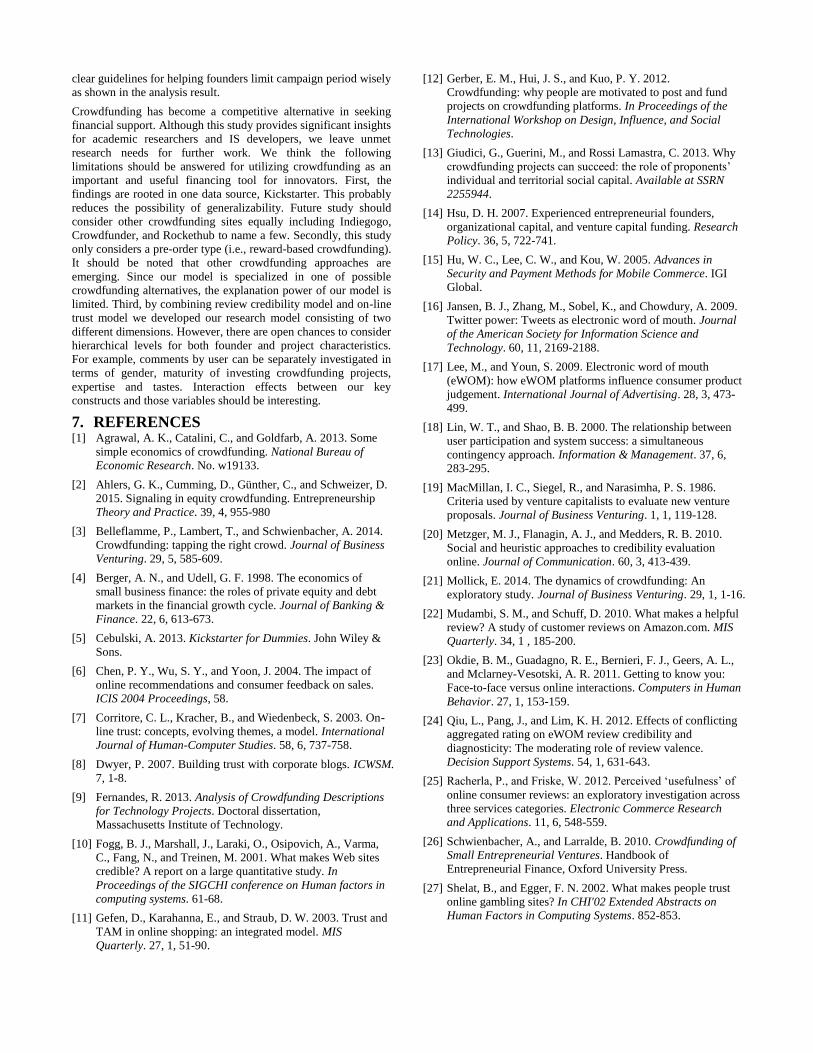

The regression model shows that H1 is not supported. Founder

Identity does not have significant effect on Success Rate (p-value

= 0.168). The first plausible explanation is that Facebook photos

are not adequate materials for identification, which does not give

significant clues for trustworthiness. The second explanation is

that a crowdfunding project has different characteristics that have

been reported in blog studies about the effect of Word-of-Mouth

on product sales (e.g., Jansen et al., 2009; Lee and Youn, 2009).

Social networking capabilities may not be correlated with the

success of crowdfunding since it does not deliver relevant

information on products or services (Giudici et al., 2013).

Hypothesis 2 is supported (p-value = 0.006). Experiences on prior

crowdfunding projects influence the next project. The historical

records of crowdfunding as a founder may give a positive signal

to potential investors about capability and competency. According

to Hu et al. (2005), reputation information increases trust with

reducing risks in a computer-mediate environment. Our result is in

line with the findings from the effects of prior experiences on

performance in the context of online shopping (e.g., Gefen et al.,

2003).

The number of comments is positively associated with Success

Ratio, which shows that H3 is supported (p-value < 0.000). User

participation has been studied as a key success factor in

information system research (Lin and Shao, 2000). The amount of

review comments can increase positive responses in terms of sales

(Ye et al., 2009). In the context of crowdfunding, the amount of

user-generated comment is a primary indicator to a possible

successful project.

The number of update is positively related with Success Rate (p-

value < 0.000). H4 is supported. According to Mollick (2014),

frequent update is considered as a positive indicator for quality.

Quick feedback to customer issues is required to recover service

failures (Zeithaml et al., 2010). Moreover, constant update gives a

good image on company’s innovation efforts (Xu et al., 2014).

Those can be good signals for project success; thus increasing

success rate.

H5 is not supported. The word count does not convey significant

meanings to explain the variance of Success Rate. The result

implies that variance of success and failure is not found in

quantity of explanation. We suspect that small quantity of

description can deliver key information sources for persuading

investors more successfully. However, this assertion was not

tested in this study. Further studies are needed to verify the effect

of various information cues that affect success.

H6 is supported. One plausible explanation is that time duration

affects project attractiveness. If a reward is expected several

months or even a year later, an investor may perceive a

crowdfunding project is uncertain. In addition, long duration

reflects the fact that a project is not mature enough for market

delivery. It gives a negative signal to investors about quality and

veracity. In line with H6, Funding Goal is negative associated

with Success Rate (p-value < 0.000), which shows that H7 is

supported. This result is in line with Mollick (2014). Increasing

goal is negatively correlated with success. Reward-based

crowdfunding projects usually have differentiated reward scheme.

For larger investors, a project founder promises bigger rewards. If

a person contributes only small money to the project, a reward is

small. The final goal is a sum of investment from different

schemes. It should be noted that even a big goal can have multiple

reward schemes that need to be supported by limited investors.

Since a return from participating in a crowdfunding project is

uncertain, small reward with small risk is naturally preferable. If

the pool of investors is limited, a large funding goal is probably

unrealistic; thus accelerating failure.

Figure 2. Analysis result

6. CONCLUDING REMARK Although crowdfunding provides a new approach for

entrepreneurs in funding innovative projects, how to make a

project being successful is not yet clear. The findings of this study

may contribute to knowledge accumulation in the research stream

of crowdfunding by offering clear insight on using design

elements. Our findings as also provide strategic insights to the

platform developers of crowdfunding. According to the analysis

result, prior successful stories in a founder dimension should be

highlighted to increase success rate. In addition, a searching tool

for discovering promising crowdfunding projects needs to

consider the amount of comments and updates. There should be

Identity Disclosure

Prior Experience

Country

Success Ratio

Comment

Update

Description Elaborateness

Campaign Period

Funding Goal

H1

H2

H3

H4

H5

H6

H7

Founder Dimension

Project Dimension

Control Variable

0.047

0.098**

0.393***

0.123***

0.050

-0.074*

-7.026***

0.010

clear guidelines for helping founders limit campaign period wisely

as shown in the analysis result.

Crowdfunding has become a competitive alternative in seeking

financial support. Although this study provides significant insights

for academic researchers and IS developers, we leave unmet

research needs for further work. We think the following

limitations should be answered for utilizing crowdfunding as an

important and useful financing tool for innovators. First, the

findings are rooted in one data source, Kickstarter. This probably

reduces the possibility of generalizability. Future study should

consider other crowdfunding sites equally including Indiegogo,

Crowdfunder, and Rockethub to name a few. Secondly, this study

only considers a pre-order type (i.e., reward-based crowdfunding).

It should be noted that other crowdfunding approaches are

emerging. Since our model is specialized in one of possible

crowdfunding alternatives, the explanation power of our model is

limited. Third, by combining review credibility model and on-line

trust model we developed our research model consisting of two

different dimensions. However, there are open chances to consider

hierarchical levels for both founder and project characteristics.

For example, comments by user can be separately investigated in

terms of gender, maturity of investing crowdfunding projects,

expertise and tastes. Interaction effects between our key

constructs and those variables should be interesting.

7. REFERENCES [1] Agrawal, A. K., Catalini, C., and Goldfarb, A. 2013. Some

simple economics of crowdfunding. National Bureau of

Economic Research. No. w19133.

[2] Ahlers, G. K., Cumming, D., Günther, C., and Schweizer, D.

2015. Signaling in equity crowdfunding. Entrepreneurship

Theory and Practice. 39, 4, 955-980

[3] Belleflamme, P., Lambert, T., and Schwienbacher, A. 2014.

Crowdfunding: tapping the right crowd. Journal of Business

Venturing. 29, 5, 585-609.

[4] Berger, A. N., and Udell, G. F. 1998. The economics of

small business finance: the roles of private equity and debt

markets in the financial growth cycle. Journal of Banking &

Finance. 22, 6, 613-673.

[5] Cebulski, A. 2013. Kickstarter for Dummies. John Wiley &

Sons.

[6] Chen, P. Y., Wu, S. Y., and Yoon, J. 2004. The impact of

online recommendations and consumer feedback on sales.

ICIS 2004 Proceedings, 58.

[7] Corritore, C. L., Kracher, B., and Wiedenbeck, S. 2003. On-

line trust: concepts, evolving themes, a model. International

Journal of Human-Computer Studies. 58, 6, 737-758.

[8] Dwyer, P. 2007. Building trust with corporate blogs. ICWSM.

7, 1-8.

[9] Fernandes, R. 2013. Analysis of Crowdfunding Descriptions

for Technology Projects. Doctoral dissertation,

Massachusetts Institute of Technology.

[10] Fogg, B. J., Marshall, J., Laraki, O., Osipovich, A., Varma,

C., Fang, N., and Treinen, M. 2001. What makes Web sites

credible? A report on a large quantitative study. In

Proceedings of the SIGCHI conference on Human factors in

computing systems. 61-68.

[11] Gefen, D., Karahanna, E., and Straub, D. W. 2003. Trust and

TAM in online shopping: an integrated model. MIS

Quarterly. 27, 1, 51-90.

[12] Gerber, E. M., Hui, J. S., and Kuo, P. Y. 2012.

Crowdfunding: why people are motivated to post and fund

projects on crowdfunding platforms. In Proceedings of the

International Workshop on Design, Influence, and Social

Technologies.

[13] Giudici, G., Guerini, M., and Rossi Lamastra, C. 2013. Why

crowdfunding projects can succeed: the role of proponents’

individual and territorial social capital. Available at SSRN

2255944.

[14] Hsu, D. H. 2007. Experienced entrepreneurial founders,

organizational capital, and venture capital funding. Research

Policy. 36, 5, 722-741.

[15] Hu, W. C., Lee, C. W., and Kou, W. 2005. Advances in

Security and Payment Methods for Mobile Commerce. IGI

Global.

[16] Jansen, B. J., Zhang, M., Sobel, K., and Chowdury, A. 2009.

Twitter power: Tweets as electronic word of mouth. Journal

of the American Society for Information Science and

Technology. 60, 11, 2169-2188.

[17] Lee, M., and Youn, S. 2009. Electronic word of mouth

(eWOM): how eWOM platforms influence consumer product

judgement. International Journal of Advertising. 28, 3, 473-

499.

[18] Lin, W. T., and Shao, B. B. 2000. The relationship between

user participation and system success: a simultaneous

contingency approach. Information & Management. 37, 6,

283-295.

[19] MacMillan, I. C., Siegel, R., and Narasimha, P. S. 1986.

Criteria used by venture capitalists to evaluate new venture

proposals. Journal of Business Venturing. 1, 1, 119-128.

[20] Metzger, M. J., Flanagin, A. J., and Medders, R. B. 2010.

Social and heuristic approaches to credibility evaluation

online. Journal of Communication. 60, 3, 413-439.

[21] Mollick, E. 2014. The dynamics of crowdfunding: An

exploratory study. Journal of Business Venturing. 29, 1, 1-16.

[22] Mudambi, S. M., and Schuff, D. 2010. What makes a helpful

review? A study of customer reviews on Amazon.com. MIS

Quarterly. 34, 1 , 185-200.

[23] Okdie, B. M., Guadagno, R. E., Bernieri, F. J., Geers, A. L.,

and Mclarney-Vesotski, A. R. 2011. Getting to know you:

Face-to-face versus online interactions. Computers in Human

Behavior. 27, 1, 153-159.

[24] Qiu, L., Pang, J., and Lim, K. H. 2012. Effects of conflicting

aggregated rating on eWOM review credibility and

diagnosticity: The moderating role of review valence.

Decision Support Systems. 54, 1, 631-643.

[25] Racherla, P., and Friske, W. 2012. Perceived ‘usefulness’ of

online consumer reviews: an exploratory investigation across

three services categories. Electronic Commerce Research

and Applications. 11, 6, 548-559.

[26] Schwienbacher, A., and Larralde, B. 2010. Crowdfunding of

Small Entrepreneurial Ventures. Handbook of

Entrepreneurial Finance, Oxford University Press.

[27] Shelat, B., and Egger, F. N. 2002. What makes people trust

online gambling sites? In CHI'02 Extended Abstracts on

Human Factors in Computing Systems. 852-853.

[28] Spears, N. 2001. Time pressure and information in sales

promotion strategy: conceptual framework and content

analysis. Journal of Advertising. 30, 1, 67-76.

[29] Utz, S., Kerkhof, P., and van den Bos, J. 2012. Consumers

rule: How consumer reviews influence perceived

trustworthiness of online stores. Electronic Commerce

Research and Applications. 11, 1, 49-58.

[30] Valanciene, L., and Jegeleviciute, S. 2013. Valuation of

crowdfunding: benefits and drawbacks. Economics and

Management. 18, 1, 39-48.

[31] Ward, C., and Ramachandran, V. 2010. Crowdfunding the

next hit: microfunding online experience goods. In Workshop

on Computational Social Science and the Wisdom of Crowds

at NIPS2010.

[32] Xu, A., Yang, X., Rao, H., Fu, W. T., Huang, S. W., and

Bailey, B. P. 2014. Show me the money! An analysis of

project updates during crowdfunding campaigns. In

Proceedings of the SIGCHI Conference on Human Factors

in Computing Systems. 591-600.

[33] Ye, Q., Law, R., and Gu, B. 2009. The impact of online user

reviews on hotel room sales. International Journal of

Hospitality Management. 28, 1, 180-182.

[34] Zeithaml, V. A., Bitner, M. J., and Gremler, D. D. 2010.

Services Marketing Strategy. John Wiley & Sons, Ltd.