Embed Size (px)

Citation preview

ecoDa’s EU Updates – November 2014

a.s.b.l.Confédération Européenne des Associations d’Administrateurs

European Confederation of Directors’ Associations

EU Updates – November 2014

1

ecoDa’s EU Updates – November 2014European Commission:

Objectives for the Commission:

The European Commission has issued its 2014 working programme."2014 will be a year of delivery and implementation", President Barroso said. The Commission will continue work on completing the banking union, and reinforcing economic governance. The adoption of the Single Resolution Mechanism Fund is a priority, and the Single Supervisory Mechanism becomes operational in 2014.

New European Commission:

Unit MARKT F2 (Corporate Governance, Social Responsibility) has moved from DG Internal Market and Services (MARKT) to the Directorate-General for Justice (JUST).

On October 1st, ecoDa and EuropeanIssuers sent a letter to Martin Selmayr, Head of Transition team, European Commission (Juncker’s Cabinet) to address their concerns highlighting that: “Much of corporate governance is not a matter of legislation, but of best practice, behavior and culture. Moving such a matter from MARKT to JUST would in this sense send the wrong signal against self-regulation and the role of national corporate governance codes”. See here. Briefing notes were also sent to Members of the European Parliament (MEPs) in advance of the Hearings of the Commissioners Designate.

On November 1st, the new Commission has come into force. See here the new structure.

Jonathan Hill, UK Leader of the upper house of the British parliament has been elected as the new Commissioner for the new Financial Stability, Financial Services and Capital Markets Union portfolio.

Věra Jourová, the former Czech minister for regional development, is now Commissioner for Justice, Consumers and Gender Equality.

See also the organization chart of the new DG Financial Stability, Financial Services and Capital Markets Union

European Parliament:

New European Parliament:

Pavel Svoboda (EPP, Czech Republic) has been appointed chair of the JURI Committee (legal affairs) – the full list of members can be found here

Roberto Gualtieri (S&D, Italian) has been appointed chair of the ECON Committee– the full list of members can be found here

2

ecoDa’s EU Updates – November 2014

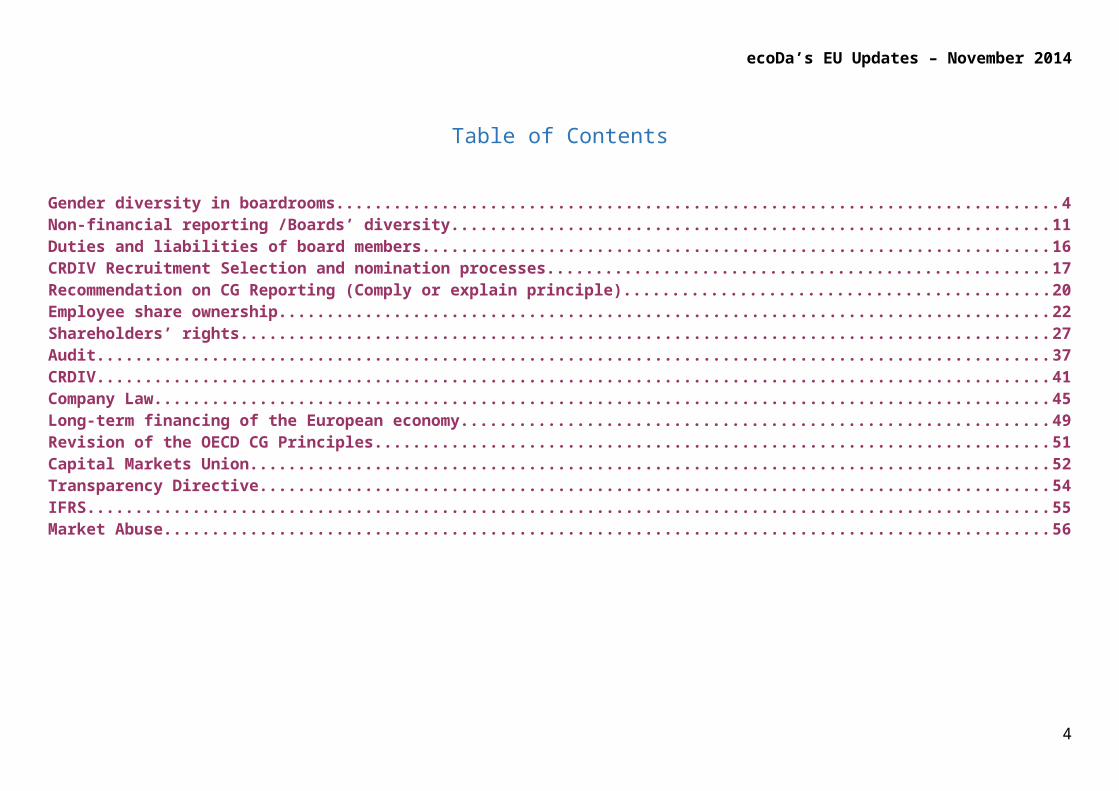

Table of Contents

Gender diversity in boardrooms............................................................................................................................................................................. 4Non-financial reporting /Boards’ diversity...........................................................................................................................................................11Duties and liabilities of board members.............................................................................................................................................................. 16CRDIV Recruitment Selection and nomination processes.................................................................................................................................17Recommendation on CG Reporting (Comply or explain principle)...................................................................................................................20Employee share ownership................................................................................................................................................................................... 22Shareholders’ rights.............................................................................................................................................................................................. 27Audit........................................................................................................................................................................................................................ 37CRDIV...................................................................................................................................................................................................................... 41Company Law......................................................................................................................................................................................................... 45Long-term financing of the European economy..................................................................................................................................................49Revision of the OECD CG Principles....................................................................................................................................................................51Capital Markets Union............................................................................................................................................................................................ 52Transparency Directive.......................................................................................................................................................................................... 54IFRS......................................................................................................................................................................................................................... 55Market Abuse.......................................................................................................................................................................................................... 56

3

ecoDa’s EU Updates – November 2014

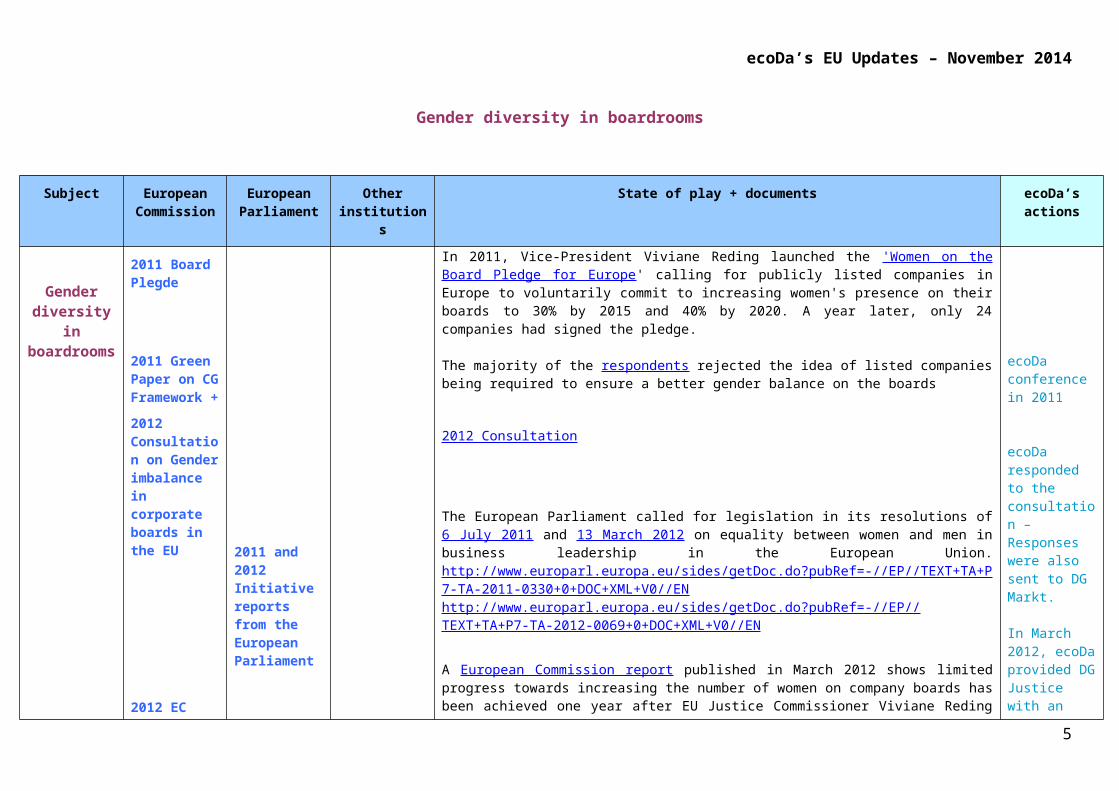

Gender diversity in boardrooms

Subject European Commission

European Parliament

Other institutions

State of play + documents ecoDa’s actions

Gender diversity in boardrooms

2011 Board Plegde

2011 Green Paper on CG Framework +2012 Consultation on Gender imbalance in corporate boards in the EU

2012 EC Report

2011 and 2012 Initiative reports from the European Parliament

In 2011, Vice-President Viviane Reding launched the 'Women on the Board Pledge for Europe' calling for publicly listed companies in Europe to voluntarily commit to increasing women's presence on their boards to 30% by 2015 and 40% by 2020. A year later, only 24 companies had signed the pledge.

The majority of the respondents rejected the idea of listed companies being required to ensure a better gender balance on the boards

2012 Consultation

The European Parliament called for legislation in its resolutions of 6 July 2011 and 13 March 2012 on equality between women and men in business leadership in the European Union. http://www.europarl.europa.eu/sides/getDoc.do?pubRef=-//EP//TEXT+TA+P7-TA-2011-0330+0+DOC+XML+V0//ENhttp://www.europarl.europa.eu/sides/getDoc.do?pubRef=-//EP//TEXT+TA+P7-TA-2012-0069+0+DOC+XML+V0//EN

A European Commission report published in March 2012 shows limited progress towards increasing the number of women on company boards has been achieved one year after EU Justice Commissioner Viviane Reding called for credible self-regulatory measures. Just one in seven board members at Europe's top firms is a woman (13.7%). This is a slight improvement from 11.8% in 2010. However, it would still take more than 40 years to reach a significant gender balance (at least 40% of both sexes) at this rate.

The Commission's Legislative Work Programme for 2012 announces a legislative initiative on improving the gender balance in companies listed on stock exchanges.

ecoDa conference in 2011

ecoDa responded to the consultation – Responses were also sent to DG Markt.

In March 2012, ecoDa provided DG Justice with an European benchmark on election mechanisms to company boards in EU Member states

ecoDa letter to

4

ecoDa’s EU Updates – November 2014Commission's Legislative Work Programme for 2012

Impact Assessment

14 Nov 2012 - Viviane Reding’s draft Directive

Discussion at the European Parliament

Exchange of view and workshop: 20.3.2013

Consideration of a draft report: 29.5.2013

19 June: JURI/FEMM with national parliaments: - 8/9 July: Presentation of draft report

Matrix Insight Ltd, a European Public Policy Consultancy based in London, carried out an external Impact Assessment.

The Commission has proposed legislation with the aim of attaining a 40% objective of the under-represented sex in non-executive board-member positions in publicly listed companies by 2020, with the exception of small and medium enterprises.

JURI and FEMM Committees (leading committees)On 22 March 2013, the Legal Affairs and Women's Rights and Gender equality Committees held a workshop to discuss the proposal for a directive aimed at improving the gender balance on corporate boards.

On April 22nd 2013, JURI and FEMM Committees had a joint meeting to discuss the Reding directive on women on boards.

The European Commission made it clear that the proposal is business friendly and proportionate. The directive does no impose strict quotas as such but targets accompanied by procedure obligations. The directive preserves the meritocratic character of directors’ appointments. The legal basis used by the European Commission to take this initiative is the same one as those taken to tackle self-employed people.

Rodi Kratsa-Tsagaropo (Group of the European People's Party (Christian Democrats) Greek, Rapporteur of the FEMM Committee- Main Committee) insisted on the need to stress that the directive is about procedure and that 40% of women on boards is an objective. According to her, since 40% is an objective, it should be applied to any listed companies even where the members of the under-represented sex represent less than 10 per cent of the workforce (contrary to the opinion of the Internal Market and Consumer Protection Committee- IMCO committee).

Evelyn Regner (Group of the Progressive Alliance of Socialists and Democrats, Austrian, co-Rapporteur for JURI Committee- Legal Affairs Committee, Main Committee) insisted on the fact that the European Commission has taken a cautious approach which takes into account the different national perceptions. The legal affairs committee will have to express itself on the legal basis of the directive to respond to the legal services of the Council which are critical about the legal basis used by the Commission. The legal services of the Parliament will provide elements but the legal affairs committee will have to take a political decision. The timetable is realistic and it is important to involve the national parliaments.

present the initiatives taken by ecoDa members

ecoDa and its members were consulted by Matrix

GNDI’s paper

Creation of an ecoDa WG on diversity on boards (process and selection)

Position paper in June 2013

5

ecoDa’s EU Updates – November 201429 August: AM deadline18 September: Consideration of AMs14 October: Vote20 November: Vote Plenary session

IMCO, EMPL, ECON Committees (Advisory Committees)

Marije Cornelissen (Group of the Greens/European Free Alliance, Dutch, Rapporteur for the EMPL Committee- Employee and Social Affairs Committee, Opinion committee) who presented her draft opinion at the EMPL Committee on April 23 rd mentioned that the Reding proposal requires descriptions on how the selection procedure should be. According to Mrs Cornelissen, the directive should leave freedom to companies to fill in what the adjustments should be. The draft directive is clear about reporting and explaining obligations. The Commission aims at targeting Member States and companies that don’t make enough efforts. Companies that do well will have light reporting obligations, while those companies that are not doing enough will have heavier obligations to explain why. The directive is therefore about comply or explain principle with sanctions if the explanations are not good.

Antonyia Parvanova (Group of the Alliance of Liberals and Democrats for Europe, Bulgarian, Rapporteur for the IMCO Committee, Internal Market and Consumer Protection Committee, Opinion Committee) who has already presented her draft opinion repeated that her opinion addresses three objectives: the functioning of the internal market: she wants to stress the importance of diversity for the profitability of companies, legal certainty: importance of having the same rules applied in Europe, economic situation in the EU: the importance of human capital. As you know, one of the main suggested amendments is the deletion of the exemption for listed companies where the members of the under-represented sex represent less than 10 per cent of the workforce. She mentioned that she received 66 proposals of amendments that will be examined on 29 May.

During the debate, one MEP insisted on the need for better transparency on selection procedures.

Olle Schmidt (Group of the Alliance of Liberals and Democrats for Europe, Swedish, Rapporteur for the ECON Committee, Economic and Monetary Committee, Opinion committee) presented his draft opinion on April 24th.Although the EMPL and the IMCO draft opinions are more or less in line with the Reding’s initiative, the ECON draft opinion goes in another direction.

The ECON draft opinion does not support quotas but is in the opinion that companies should be required to set individual targets for their gender balance among both executive and non-executive directors, as well as at all management levels in the company.

The ECON draft opinion also intends to extend the scope of companies targeted by the directive. The possibility of extending the scope to non-listed companies above SME threshold should be reviewed by the Commission two years after the implementation of this Directive.

6

ecoDa’s EU Updates – November 2014

Debate at the European Parliament with national Parliaments on the Reding initiative

ICAEW

The ECON draft opinion calls the EU institutions for leading by example and for integrating gender rules.

On May 14th, Vice-President Viviane Reding, the EU's Justice Commissioner, met with Markus Klimmer, Managing Director at Accenture, today to discuss how best to improve gender balance on company boards

Markus Klimmer, Managing Director at Accenture's said: "By 2025 Germany is expected to face a demographic gap in the labour market of 5 million people. One third of this could be filled by increasing the participation of women in the economy. Germany's and Europe's competitiveness critically depends on mobilising all talent available. Women's participation in the labour market is therefore not only a women's or an equality issue but a question of sound economic policy. This issue is too important to be left to the often arbitrary whims of men in leadership positions."

Vice-President Reding added:

"The proposal for a Directive that the Commission put on the table last year to make headway on gender equality strikes a reasonable balance. It is a fair deal both for the business world and for women who have the same right to pursue careers as men.

I am happy that Mr Klimmer and more and more men in the business world are recognising the importance of gender diversity and are supporting our objective. Key players in the business world like Accenture – which already has 36% of women on their board – are setting a good example that which companies should follow."

At the ICAW breakfast last week, Jeroen Hooijer from the Commission made it clear that the Reding initiative has no CG objective (contrary to the non-financial reporting draft directive) but will have impact on CG.

There was a debate at the European Parliament with national Parliaments on the Reding initiative. The European Commission mentioned that:

-One of the important features of the initiative is the emphasis on transparency of the selection procedure.

-The system is aimed to be based on the merits of women

-The European Commission has a clear competence on this topic: gender equality is not a new concern.

-All the surveys show that there is little progress (15.8% of female board members on average in 2012). The progress is too slow.

-Given that the point of departure can be different in every member states, the proposal

7

ecoDa’s EU Updates – November 2014

Vote at the plenary session of the European Parliament – 20 November 2013

includes flexibility. According to Article 8, Member states can suspend transparency requirements if their national solutions are as effective as the proposal or work better.

-The majority of national parliaments is rather positive.

-The initiative targets listed companies given that they are better structured to handle the process of transparent recruitment criteria.

The two main rapporteurs insisted on:

-The need to take advantage of workers talents which constitutes a major asset in terms of competitiveness,

-The need to get a framework for common action from member states,

-The directive respect the principles of proportionality and subsidiarity

-If the common goal for member states is to achieve certain quotas in their companies, they have the right to implement this in their own way,

-The draft directive does not burden further companies with bureaucratic measures.

-According to Evelyn Regner, the draft directive should be extended to smaller listed companies.

Most of the national parliaments were represented. For some of them, the main two parties were represented and expressed divergent opinions.

The European Economic and Social Committee and the European Committee of regions have already expressed positive opinion regarding the draft directive.

The European Parliament has voted with an overwhelming majority (459 for, 148 against and 81 abstentions) to back the European Commission’s proposed law to improve the gender balance in Europe’s company boardrooms. The strong endorsement by the Members of the European Parliament means the Commission’s proposal has now been approved by one of the European Union’s two co-legislators. Member States in the Council now need to reach agreement on the draft law, amongst themselves and with the European Parliament, in order for it to enter the EU statute book. The plenary vote follows a clear endorsement for the Commission’s initiative from the Parliament’s two leading committees, the Legal Affairs (JURI) and Women’s Rights & Gender Equality (FEMM) committee on 14 October 2013. The most recent figures confirm that, following the Commission's determined action in this area, the share of women on boards across the EU has been on the rise for the past three years and has now reached 16.6%, up from 15.8% in October 2012..

It confirms the Commission's approach to focus on a transparent and fair selection procedure

8

ecoDa’s EU Updates – November 2014

EPCSO Council –

EBA

(a so-called "procedural quota") rather than introducing a fixed quantitative quota.

- Small and medium-sized enterprises remain excluded from the scope of the directive but Member States are invited to support and incentivise them to significantly improve the gender balance at all levels of management and on boards.

- Departing from the Commission’s original proposal, there will be no possibility for Member States to exempt companies from the law where members of the underrepresented sex make up less than 10% of the workforce.

- The Parliament strengthened the provision on sanctions by adding a number of sanctions that should be obligatory, rather than indicative, as the Commission had proposed. Under the Parliament’s text, sanctions for failure to respect the provisions concerning selection procedures for board members should include exclusion from public procurement and partial exclusion from the award of funding from the European structural funds.

The Irish Presidency of the EU held a discussion at the meeting of Employment and Social Affairs ministers (EPSCO Council) on 20 June 2013.

The Council/Ministers are next due to discuss the draft law at their meeting on 9-10 December 2013.

The Council has not taken a formal position on the proposed Directive yet. The proposal was discussed under Irish and Lithuanian Presidency and a progress report by the Lithuanian Presidency was presented to the December EPSCO Council (http://register.consilium.europa.eu/doc/srv?l=EN&t=PDF&gc=true&sc=false&f=ST%2016437%202013%20INIT ). That work will continue under Greek Presidency. The recent elections in several Member States (notably in the Czech Republic and in Germany) that have led to a change in government may lead to a change in the dynamics of the Council deliberations.

No new developments under the Italian presidency

European Banking Authority (EBA): in the financial sector: Recital 60 of the CRDIV Directive:

“To facilitate independent opinions and critical challenge, management bodies of institutions should therefore be sufficiently diverse as regards age, gender, geographical provenance and educational and professional background to present a variety of views and experiences. Gender balance is of particular importance to ensure adequate representation of population. In particular, institutions not meeting a threshold for representation of the underrepresented gender should take appropriate action as a matter of priority”.

9

ecoDa’s EU Updates – November 2014

Hearing of Vera Jourova, Designated Commissioner for Justice

OECDEBA will develop Guidelines on diversity benchmarking

no specific CRD mandate, but harmonised data will enable better analysis

2014 ad hoc data collection – Guidelines to be expected 2015/2016

The OECD is conducting a survey on boards’ diversity (in a broad sense). They have already collected the data and are in the midst of drafting the report (should be issued in early 2015).

During her hearing, on 1st October 2014, Vĕra Jourova made it clear that she will support the initiative on gender balance in boardrooms and will try to interact with the Council for a positive outcome.

10

ecoDa’s EU Updates – November 2014

Non-financial reporting /Boards’ diversity

Subject European Commission

European Parliament

Other stake-holders

State of play + documents ecoDa’s actions

Non-financial reporting /Boards’ diversity

Directive amending Council Directives 78/660/EEC and 83/349/EECProcedure completed (awaiting publication in Official Journal)The expected expert group and public consultation on the implementation of the new directive will be launched early next year, not this autumn.

DG Financial Stability, Financial Services and Capital Markets Union (Unit F3 Accounting and financial reporting)

2011 Green Paper on CG Framework

2011 Consultation

2011 Communication "A renewed strategy 2011–2014 for Corporate Social Responsibility"

2011 Green Paper: Some of those favouring more specific recruitment policies were against regulation at EU level, considering either national level as more appropriate or even that the company should have the freedom to decide alone on such issues, for instance through its nomination committee.

An online public consultation was concluded in January 2011. Consultations showed different views ranging from some stakeholders calling for some improvements but advocating a voluntary approach, to other stakeholders highlighting the need to improve and clarify the existing legal framework at EU level, and to render information more transparent and comparable. Overall, the majority of respondents to the consultation said that legal regimes differ significantly across EU Member States, and that the current EU legislative framework lacks in transparency, making it difficult for shareholders and investors to properly assess EU companies or take full account of their CSR performances. Most stakeholders argue that better information would translate over time into more sustainable growth and employment in Europe. A summary report of the views expressed in the framework of the above mentioned public consultation is available

A measure was announced

The European Commission set up an Expert Group on Disclosure of Non-Financial

11

ecoDa’s EU Updates – November 2014

European Expert Group

2012 Action Plan for Company Law and Corporate Governance 2013 European

Parliament’s resolutions

information by EU Companies.

The Commission has commissioned the Centre for Strategy and Evaluation Services a specific study aiming at providing some qualitative analysis of current reporting practices in the EU.

Different questions have been raised, such as:

- the role of companies’ boards

- the need for integrated reporting

- the assessment of non-financial information by external auditors

- the demand in the financial markets for non-financial information

- and the reporting costs.

The EU 2020 Agenda on sustainable growth and jobs promotes the renewal of corporate social responsibility (CSR). The Single Market Act (SMA) which was adopted in April 2011 aims at opening the doors to new, greener and more inclusive growth. It stresses the importance of strengthening consumer trust and confidence in the EU market, and achieving a highly competitive social market economy with sustainable economic growth. In this framework the Commission is also currently developing a Social Business Initiative (SBI) and, as stated in the SMA, should present a legislative proposal on the transparency of the social and environmental information provided by companies in the course of 2012. Since 2006 the European Parliament has also called the Commission to put forward initiatives in order to strengthen the EU legal framework on social and environmental reporting.

On disclosure related to diversity in the Boards, the Expert Group specified that:The opportunity of including specific information concerning diversity policy in the Boards was also discussed in detail. Although most members agreed on the overall objective of increasing transparency in the board in order to avoid "group thinking", several experts suggested that such issue should be treated consistently with other nonfinancial aspects under discussion. Some experts also questioned the coherence with the other elements under discussion. The view that diversity-related disclosures should not be limited to gender only, but include other material aspects, was also shared by most experts. Two members questioned the opportunity to include diversity at all, and invited the Commission to duly consider all relevant legal implications.

A measure was announced in the Action plan.

On 6 February 2013, the European Parliament adopted two resolutions (“Corporate Social Responsibility: accountable, transparent and responsible business behaviour and sustainable growth” and “Corporate Social Responsibility: promoting society’s interests and a route to

12

ecoDa’s EU Updates – November 2014

16 April 2013- Draft directive on disclosure of non financialand diversity information

Proposal for a directive as regards disclosure of non-financial and diversity information by certain large companies and groups

EUROPEAN PARLIAMENT Committee on Legal AffairsDraft report17/10/2013- 19/20 June 2013 Exchange of views on the COM proposal;

- 15 October 2013: deadline to send the draft report to translation;

- 5 November

sustainable and inclusive recovery”), acknowledging the importance of company transparency on environmental and social matters.

http://www.europarl.europa.eu/sides/getDoc.do?pubRef=-//EP//NONSGML+REPORT+A7-2013-0017+0+DOC+PDF+V0//EN&language=EN

http://www.europarl.europa.eu/sides/getDoc.do?pubRef=-//EP//NONSGML+REPORT+A7-2013-0023+0+DOC+PDF+V0//EN&language=EN

The European Commission has proposed an amendment to existing accounting legislation in order to improve the transparency of certain large companies on social and environmental matters. Companies concerned will need to disclose information on policies, risks and results as regards environmental matters, social and employee-related aspects, respect for human rights, anti-corruption and bribery issues, and diversity on the boards of directors.

On 20 June, a first discussion was organised with the rapporteur (Raffaele Baldassaere) at the JURI Committee. The rapporteur mentioned that the draft directive has the objective to bring existing standards all together. The objectives are to increase transparency and the comparability of non-financial information. If flexibility is needed, it is important to set standards. If there is no comparability, there is no progress in terms of transparency. Proper standards will avoid companies to improve their façade but their substance. Transparency should allow companies to defend themselves on fair competitiveness. Some MEPS stressed the need for penalties for misleading or incorrect statements. Regarding supply chains, companies cannot report for all their suppliers but should provide due diligence and report on how they implement this due diligence.Mr Howit invited publicly BusinesEurope to support the draft directive

Draft report of Mr Baldassaere: The JURI Committee discussed the proposal. Mr Baldassaere made it clear that he supports the approach taken by the European Commission and the comply or explain approach. He suggests some amendments: -Technical amendments: to align the directive with the accountant directive,-Amendments on substance: to enhance the principles of flexibility and comparability.-One proposal on risks in order to make the concept more explicit. In order to avoid side effects on competition, companies should be able to limit the reporting if and when it might arm the interests of the companies. The directive represents for him a first step to more binding CSR. It fixes primary obligations to be developed later.-Regarding the new area of country by country information: he supports the introduction of these new requirements. He believes that greater transparency would help to increase

13

ecoDa’s EU Updates – November 20142013: presentation of draft report in JURI

- 12 November: deadline for Amendments

- 26 November: discussion of Amendments

17 December 2013: vote in JURI or discussion on AMC

February/March = vote in plenary.

ECON Committee (advisory committee)

Vote of their report on December 9.

consumers’ confidence in big companies and multinationals. It would also increase companies’ reputation. Investors would have access to more information.

Some MEPs (like Mr Cofferati) insisted on the importance to get information on the supply chain for sub contractors. Taking another approach will be contrary to the European policy on public tendering. Some other MEPS (like Mrs Thein) consider that more transparency will not provide more competitiveness. Companies have not enough time to implement all the new regulations. Mrs Thein is against the introduction of new requirements related to country by country information in that directive.The deadline for amendments: November 12.

Amendments tabled in committee on 15/11/2013. Rapporteur Mr Baldassarre (PPE) informed that ‘160’ amendments were presented to the proposal. Some MEPs want to make it clear that wants to make clear that the proposal does not legislate CSR. There seems to be different concepts of CSR in different European countries. A necessity of impact assessment was pointed out. The proposal looks not realistic at this point for some MEPs.

The Legal Affairs committee voted on Mr Baldassarre's report on 17th December 2013.Interinstitutional negotiations will probably start in January in order to adopt the directive in March (if first reading agreement possible).

The ECON Committee (advisory committee to the JURI Committee/ Rapporteur Sharon Bowles) has issued a draft report + proposed amendments:Amendments review:

Some of the amendments proposed either reducing or raising thresholds of employees in order to fall within this regulation.

There were also propositions to consider a turnover of a company rather than a number of its employees.

A lot of amendments are calling for country-by-country reporting in all sectors. ECON has a strong voice on that.

Mrs Bowels welcomed amendments on diversity requirements A safe harbour clause was introduced. Mrs Bowel warned that it could have huge

consequences on what was already agreed on the extracting companies as it could allow a blanket exemption.

For small companies this non-financial reporting could be a burden so there is a suggestion of introducing 3-tier approach, to differentiate companies. First level companies would be exempted from the regulation, 2nd tier would comply and explain, and for 3d tier it would be mandatory.

Shadow rapporteur stressed that in some countries at present the national authorities can prohibit the publication of certain information. So the question is what does the company has to do in this case?

ecoDa Position paper sent

14

ecoDa’s EU Updates – November 2014The vote was done on the 9th of December 2013.

On 26 February, the European Parliament and the Council have reached agreement on an amendment to existing accounting legislation to improve the transparency of certain large companies on social, environmental and diversity matters.Large public-interest entities (mainly listed companies and financial institutions) with more than 500 employees will be required to disclose relevant and useful environmental and social information in their management reports. This includes listed companies as well as some unlisted companies, such as banks, insurance companies, and other companies that are so designated by Member States because of their activities, size or number of employees. The scope includes approx. 6 000 large companies and groups across the EU. The approach taken ensures that administrative burden is kept to a minimum. Companies will be required to disclose concise, useful information necessary for an understanding of their development, performance, position and impact of their activity, rather than a fully-fledged and detailed report. Furthermore, disclosures may be provided at group level, rather than by each individual affiliate within a group. The draft Directive provides for further work by the Commission to develop guidelines in order to facilitate the disclosure of non-financial information by companies, taking into account current best practice, international developments and related EU initiatives.As regards diversity on company boards, large listed companies will be required to provide information on their diversity policy, such as, for instance: age, gender, educational and professional background. Disclosures will set out the objectives of the policy, how it has been implemented, and the results. Companies which do not have a diversity policy will have to explain why not.

The European Parliament adopted this legislation in plenary in April 2015.The Council formally adopted it on 29 September 2014. Member states will have 2 years to incorporate the new provisions into domestic law which will be applicable in 2017.

The expected expert group and public consultation on the implementation of the new directive will be launched early next year, not this autumn.

15

ecoDa’s EU Updates – November 2014

Duties and liabilities of board members

Subject European Commission

European Parliament

Other stakeholders

State of play + documents ecoDa’s actions

Duties and

liabilities of board members

External Survey for the European

Commission

London Business School conducted a study on the duties and liabilities of board members. The study is on line.Countries reports are available.The European Commission might look again at the study on Directors’ Duties & liabilities carried out for them by the London Business School as soon as they will have issued their initiatives on shareholders’ rights and CoE.

A WG with AIG on the related topic to be set out- An interim report at ecoDa’s 10th anniversary.

16

ecoDa’s EU Updates – November 2014

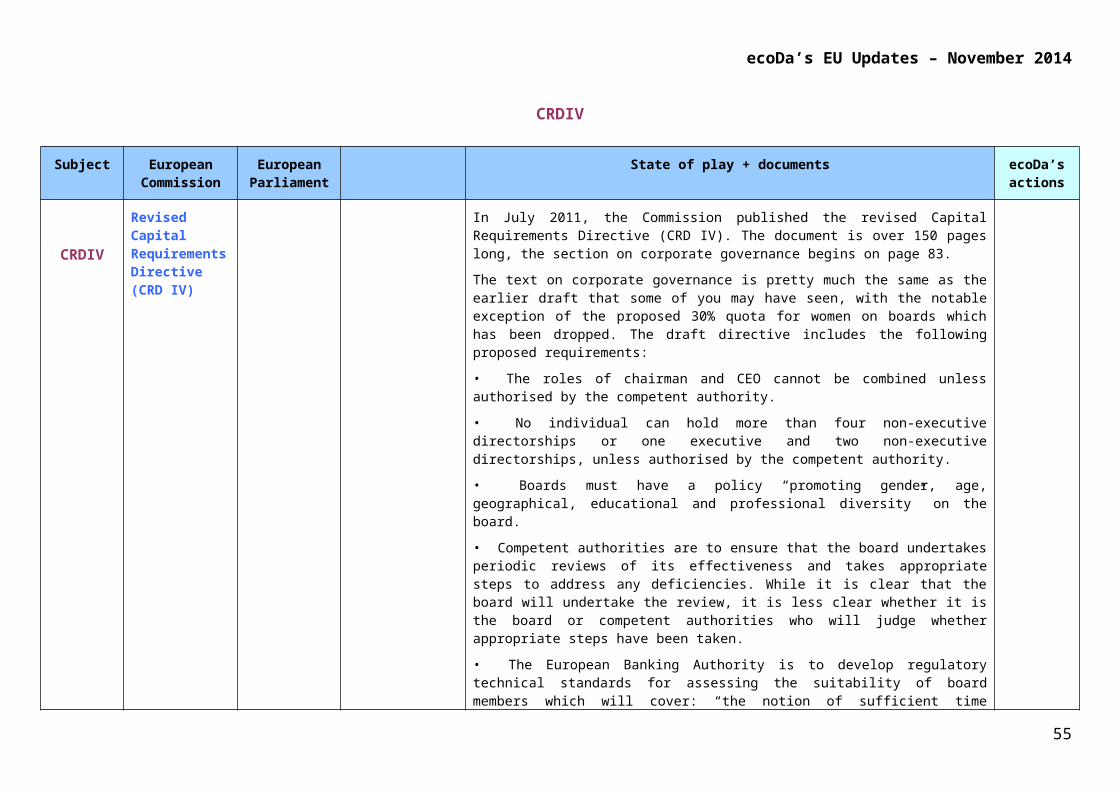

CRDIV Recruitment Selection and nomination processes

Subject European Commission

European Parliament

Other stakeholders

State of play + documents ecoDa’s actions

CRDIV Recruitment

Selection and

nomination processes

CRDIV Directive

CRD IV requirements and national company law to be met Recruitment processes:

important to find the best suited people start in time – succession planning define the competencies / profile needed assessments of conflicts of interest of potential candidates independent members and nominations in a group context

Selection needs to be done in the best interest of the institution: Nomination committee to play an active part in identifying and

recommending candidates and in increasing diversity Reputation and Experience – annual reassessment Soft skills and independence of mind Board composition – all business areas and risks covered Diversity (gender, age, educational and professional background) Interest of owners and other aspects

Diversity policy to be established: Improve diversity over time – policy to be

established (gender quotas) Possible conflicts between diversity and

nominating the best candidate Challenges for small boards

This directive limits the number of directorships and specifies in its article 91: “The number of directorships which may be held by a member of the management body at the same time shall take into account individual circumstances and the nature, scale and complexity of the institution's activities. Unless representing the Member State, members of the management body of an institution that is significant in terms of its size, internal organization and the nature, the scope and the complexity of its activities shall, from 1 July 2014, not hold more than one of the following combinations of directorships at the same time: (a) one executive directorship with two non-executive directorships; (b) four non-executive directorships.”

ecoDa Annual conference on April 29, 2014

A WG on boards’ selection and composition with Korn Ferry – A guidance to be issued at ecoDa’s 10th anniversary

17

ecoDa’s EU Updates – November 2014

EBA Guidelines

Update of the EBA

guidelinesDecember

2015

The CRDIV Directive was published on 27 June 2013 and fully enters into force on 17 July 2013. Institutions are required to apply the new rules from the 1 January 2014 with full implementation on 1 January 2019.

EBA Guidelines on Internal Governance:Management bodies (as defined by CRD) duties and responsibilities

organisational structure business and risk strategy control framework

Composition of the Management Body Adequate number and appropriate composition - proportionality Sufficient collective expertise – all business areas / control areas /

risks Planning of succession – policies for selecting members (incl.

competencies needed and proper process) Identification and management of conflicts of interest Functioning of the Management Body Regular meetings – sufficient time commitment Specialised committees (e.g. risk, audit, nomination, remuneration) Ongoing ability to function properly (e.g. Induction and training)

Regarding Art 91 – EBA to issue Guidelines by 31.12.2015

time commitment – how to assess time needed for mandates? number of directorships – how to define significant institutions? the notion of diversity to be taken into account for the selection of

members Guidelines on the suitability already in place: update needed regarding collective knowledge, skills and

experience (all business areas and risks) possibly update other aspects based on experience sufficient resources for induction and training – how to define?

The European Banking Authority (EBA) has to define the notion of “significant banks” before the end of 2015.Possible notion of significant banks:- The total value of its assets exceeds €30 billion. - The total value of its assets exceeds €5 billion and the ratio of its total assets over the GDP of the SSM state in which it is established exceeds 20%.

18

ecoDa’s EU Updates – November 2014- It is one of the three most significant credit institutions in a SSM state. - The national competent authority considers it to be significant with regard to the domestic economy and the ECB agrees. Proportionality applies in both ways – large and complex institutions need to fulfil higher governance standards than small and less complex institutions.

Even if the directive states that EBA has to define the notion of “significant banks”, national regulators like in Luxembourg don’t wait for EBA to define their own criteria. Luxembourg is in the process of implementing the CRDIV directive and has just defined by royal decree what they consider as significant banks. 10 banks have been already identified as such. The consequences for their board members are important and those decisions might impact the level of their remuneration.

19

ecoDa’s EU Updates – November 2014

Recommendation on CG Reporting (Comply or explain principle)

Subject European Commission

European Parliament

Other stakeholders

State of play + documents ecoDa’s actions

Recommendation on

CG Reporting (Comply or

explain principle)

DG Just. Unit F22011 Green Paper on CG Framework

2012 Action plan on CG and Company Law

2014 Recommendation

The Finnish Securities Markets AssociationThe Belgian Corporate Governance CommitteeThe Financial Reporting Council

A large majority of respondents to the 2011 Green Paper were in favour of requiring companies to provide better explanations for departing from codes’ recommendations

The Securities Markets Association issued on 20 January 2012 guidelines on explanations that companies should provide.

Independent study on the quality of explanation issued a numberof practical recommendations in 2012

In the UK, the Financial Reporting Council introduced guidelines on the 'comply or explain approach' in the Corporate Governance Code.

The Commission will take in 2014 an initiative, possibly in the form of a Recommendation, to improve the quality of corporate governance reports, and in particular the quality of explanations to be provided by companies that depart from the corporate governance codes.

The Recommendation was issued on April 9. The Commission’s Recommendation aims to provide guidance to listed companies, investors and other interested parties in order to improve the overall quality of corporate governance statements published by companies.

In November 2014, ICAEW has issued a paper entitled ‘Who should be covered by codes?’ makes a proposal to harness the energy behind the

In 2011, ecoDa took part in the ISS report for the European Commission together with BusinessEurope and Landwell.

ecoDa organised a high level confederation on comply or explain principle in 2012.

ecoDa issued a full report with recommendations for improvement in 2012.

Joint ecoDa, EuropeanIssuers and ACCA Conference on “The Action Plan on CG and Company Law: What’s in it and Why?”, 4 February 2013

20

ecoDa’s EU Updates – November 2014ICAEW growing number of group-specific governance codes related to

corporate governance, and explores how this energy can enhance public confidence in companies rather than creating complexity and confusion.

21

ecoDa’s EU Updates – November 2014

Employee share ownership

Subject European Commission

European Parliament/ other stakeholders

State of play + documents ecoDa’s actions

Employee share

ownershipCommission /

Parliament should take

action

DG JUST. Unit F2

Research studies

2011 Green Paper on CG Framework

Barnier’ declaration

2012 Action plan on CG and Company Law

Budget line in the 2013 budget for a pilot project

Various studies conducted by the Commission.

Responses indicate that employee share ownership schemes could play an important role in increasing the proportion of long-term oriented shareholders.

EFES managed to convince the European Parliament last year to add a specific budget line in the 2013 budget for a pilot project (on the model of what was done for the creation of Eurofinus and FinanzWatch). This pilot project was deemed necessary to develop training and education centers for share ownership in national European countries. EFES has already aggregated a platform of actors (around 50 associations) to develop the pilot project. Should it be finally decided by DG Trade, the platform would be happy to involve ecoDa in its reflection and actions.

“We have talked about the participation of the work force and ownership. We have to build greater social cohesion in companies because that is a key to unlock growth”

2012 Action plan: The Commission will identify and investigate potential obstacles to trans-national employee share ownership schemes, and will subsequently take appropriate action to encourage employee share ownership throughout Europe.

The tender consists of the following elements (see p.20):

1. Mapping and analysis. This part consists in the collection of information on the different national rules on employee ownership and

ecoDa approached EFES to offer its services for their submission to the EU tender / EFES was finally not awarded.

ecoDa attended conference “Taking Action: Promotion of Employee Share Ownership”

At ecoDa’s board meeting on 19 November 2014, presentation of Daniel Lebègue of IFA’s latest position on the related topic.

22

ecoDa’s EU Updates – November 2014April 2013 – Call for tender

participation together with a qualitative and a quantitative analysis of employee share ownership schemes. 2. Information sharing strategy and other policy initiatives. This part consist in the identification of the most appropriate methodology of enhancing knowledge of and access to the information with the aim of reducing the cost of designing efficient schemes, in particular for companies established in Member States where a legislative framework for employee share ownership is poor. 3. An outreach event (roundtable/conference): This part consists in organizing an outreach event to present the interim results of the mapping and analysis project and conclusions.

Questions about corporate governance are especially mentioned under "qualitative data" (page 25). It includes:

- identify the impact of financial participation on corporate governance and involvement of employees in corporate decision making, as well as more generally the relationship between corporate governance and employee financial participation (distinguishing senior management and employees more generally). Particular attention should be devoted to situations when employee pool their shares and therefore their decision making power (through vehicles);- identify the impact of financial participation on corporate governance and involvement of employees in corporate decision making, as well as more generally the relationship between corporate governance and employee financial participation (distinguishing senior management and employees more generally). Particular attention should be devoted to situations when employee pool their shares and therefore their decision making power (through vehicles); the impact of employee financial participation on employee satisfaction and on company performance. In particular, the Commission would like to have evidence on employee satisfaction and company performance taking into account: (i) transparency of the plan, (ii) eligibility and involvement of the employee and information made available (iii) information campaign carried out to promote the plan, (iv) corporate governance structure.

The European Commission has awarded the contract to Stiftung Europa-Universität Viadrina Frankfurt.

A Conference was organized in January 2014 to present the interim results of the mapping and analysis project and conclusions.

23

ecoDa’s EU Updates – November 2014

09/ 2014: ETUC Conference

According to the past surveys, firms with Employee Financial Participation (EFP) are more profitable, create more jobs and are better taxpayers than firms without. Firms with ESO gain a bloc of demanding but loyal shareholders who know better the company than the outsiders.The objective of the 29th regime for ESO is to have EU law and state law in parallel. Companies will be able to opt in or opt out. National or EU laws could be default rules. Companies will have the choice between two entire instruments (national or European) but without cherry picking.The European Commission has to find a way to eliminate barriers to the single market and to facilitate cross border operations. To avoid double taxation and discrimination, the EU should create a center of information (CETREPS) to provide both companies and governments with information. It would be a virtual centre for Employee Financial Participation (EFP) with comparative information among the member states and a feedback function to provide comments on the functioning of the system.

On 29 October 2014, the Commission published a comprehensive study on "The Promotion of Employee Ownership and Participation" that provides an overview of the development of employee financial participation, and in particular of employee share ownership, across EU-28 over the last decade. The study describes and analyses in depth a range of policy options to be considered at EU level to reduce the main obstacles to transnational employee financial participation and to encourage it throughout the EU. These options include the creation of a virtual information centre and establishing an optional European legal regime for employee share ownership. Overcoming cross-border barriers to employee financial participation schemes is particularly important in view of the potential for EU companies to implement such schemes and to benefit from their impact. Research presented in this study suggests that companies which are partly or entirely owned by their employees generate more profit, create more jobs and contribute more to tax revenue than companies without employee ownership. These companies also tend to relocate less and favour local production and business succession. See here.

At a conference organized by ETUC(the European Trade Union Confederation), the confederation mentioned that they want to work out a solution (and then to lobby the new EP and Commission) on a mandate to go further with employee representation not linked to the company form. They want not only to focus on economic arguments but instead link employee representation on boards to democracy at the workplace e.g. that workers’ rights’ at a company is part of the parcel of democracy. She also said that ETUC plans to link this debate to the “sustainable company

24

ecoDa’s EU Updates – November 2014model”. She also said that ETUC is pushing for directors’ duties to be reframed as long-term duties, rather than as “maximizing shareholder interest/value”.

EUROPEAN PARLIAMENT Committee Employment and Social Affairs

Deadline for amendments – December 3Discussion on 9 January, Vote on 22 January, Plenary on 2 February 2014

Draft opinion of Committee on Employment and Social Affairs (Leading Committee - Rapporteur: Fabrizio Bertot)The draft report calls on the Commission, in cooperation with employee ownership organisations, theMember States and the social partners to develop a non-binding framework concept on basic principles for successful EFP schemes + Calls on the Member States to engage employee ownership organisations and stakeholders more closely in dialogue between policy makers, employers and workers’ representatives, including the social partners where relevant, in order to ensure that existing examples of best practice at national level are taken into account in the development of nationalpolicies to facilitate the implementation of EFP by businesses;

Draft opinion of the Committee on Economic and Monetary Affairs (Advisory Committee)Proposed amendments:For a potential opt-in 29th regime: Parliament viewed with interest a potential opt-in 29th regime as an optional single legal framework open to employers throughout the EU, which would respect areas of Member State competence on fiscal and labour law, based on a market-based approach, improved transparency and access to information to facilitate equal implementation in different Member States. This model would be applicable at the national and/or EU level when needed and not being restricted to cross-border companies.It encouraged the Commission to present an independent impact assessment on such a regime. Following the publication of the independent impact assessment, Members called on the Commission to consider developing a set of basic guidelines for successful EFP schemes encompassing the following elements:

objective-led: companies should determine the objectives of an EFP scheme in order to select the model that is most appropriate for them;

flexible in operation and voluntary, operating differently in different sectors, companies of different sizes and types and offering employees a choice about how to benefit from a closer financial relationship with their employer;

25

ecoDa’s EU Updates – November 2014 additional/complementary to contractual remuneration; negotiated by social partners; clear information must be given to employees on the risks and

rights attached to opting into an EFP scheme.Involvement in governance should also be noted with workers enabled to become directly involved in the governance of a company.http://www.europarl.europa.eu/sides/getDoc.do?pubRef=-//EP//NONSGML+REPORT+A7-2013-0465+0+DOC+PDF+V0//EN

On the very last date of its mandate (30 Oct. 2014), Commissioner Barnier addressed a letter to the Chair of the ECON Committee, Mr Gualtieri, at the European Parliament to present the study on the "Promotion of Employee Ownership and Participation". He invites the European Parliament and the European Commission to work closely together when considering the next concrete steps in this area.

26

ecoDa’s EU Updates – November 2014

Shareholders’ rights

Subject European Commission

European Parliament

Other stakeholders

State of play + documents ecoDa’s actions

Shareholders’ rights

(See subsections below)

DG JUST. Unit F2

2014 Shareholders’ rights directive

The European Commission issued a new shareholders’ rights directive on April 9, 2014

The JURI Committee at the European Parliament will organise a hearing on the shareholders’ rights directive in 2014.

At the IC-A conference held on 13.11.2013, Jeroen Hooijer spoke about the upcoming shareholders’ directive and comply or explain recommendation to be issued in January 2014.He specified the following points related to:remuneration : the directive might:- Grant a say on pay to shareholders- Introduce a template to compare remuneration- Improve transparency on remuneration policies and individual remuneration of directors (ex ante or ex post).related party transactions:- The directive might request independent advisor for fairness opinion for transactions of 3 – 10% of the assets- Be also aware that the European Securities and Markets Authority (ESMA) has published a statement containing a white list of shareholder activities which will not amount to acting in concert in the context of the Takeover Directive. It also contains information on how shareholders may cooperate in order to secure board member appointments by setting out factors that national authorities may take into account when considering whether shareholders are acting in concert.http://www.esma.europa.eu/news/Press-Release-ESMA-clarifies-shareholder-cooperation-takeover-situations?t=326&o=home+ http://www.esma.europa.eu/system/files/2013-1645_esma_clarifies_shareholder_cooperation_in_takeover_situations.pdf - Be also aware that the OECD has published a report on the supervision and enforcement of corporate governance arrangements concerning related party transactions, takeover bids and shareholder meetings http://www.oecd.org/corporate/supervisionandenforcementincorporategovernance.htm

GNDI Paper on shareholders-board communication

ecoDa’s position Paper

Lutgart Van den Berghe and BRB meeting the assistant of Sergio Cofferatti, on October 15, 2014.

9/10/2014: Eurosif Conference (See EU Alert 41)

Lars-Erik Forsgardh speaking at the 15th CG Conference on October 28, 2014 in Milan (see Alert 46)

Dinner with the Kangourou Group at the European Parliament for Lars-Erik

27

ecoDa’s EU Updates – November 2014

JURI (lead) Rapporteur: Cofferati (S&D, IT)

Timeline:11/11/2014 Exchange of views

12/2014 Consideration of the draft report

02/12/2014 Hearing in EP

01/2015 Presentation of draft report

02/2015 Deadline for

The new proposal (issued on April 9, 2014) to revise the existing Shareholder Rights Directive tackles corporate governance shortcomings relating to listed companies and their boards, shareholders (institutional investors and asset managers), intermediaries and proxy advisors (i.e. firms providing services to shareholders, notably voting advice).http://ec.europa.eu/internal_market/company/docs/modern/cgp/shrd/140409-shrd_en.pdfThe original Shareholder Rights Directive agreed in 2007 improved shareholders’ access to company information and allowed them to vote by distance. This revision is more ambitious and includes proposals that straddle a number of different objectives such as increasing shareholder participation and promoting the Commission’s wider objective of improving the environment for the long term financing of the European economy. The proposal has much in common with the Kay Review in the UK. The disclosure of the relationship between the asset manager and institutional investor is a core element of the proposal. A second element is the requirement for greater disclosure of the remuneration of the directors’ of listed companies. The proposal broadly extends disclosure requirements that have been introduced to the financial services sector through the Capital Requirements Directive, the UCITS V directive and the Alternative Investment Fund Managers Directive to the directors of listed companies.

On 11 November, the JURI Committee gave a positive and constructive input. The Rapporteur Cofferati expressed that stakeholders should receive a similar attention as for shareholders from the regulators. He clearly supported the ratio with employee remuneration. The EPP shadow rapporteur stated that the new requirements on related party transactions should not damage the competitiveness of European companies.

The ECON Committee – the advisory committee for the shareholders’ rights directive (Olle Ludvigsson being the rapporteur) – has already drafted its opinion. The rapporteur would like to put this initiative into the overall context of stakeholder involvement in corporate governance. While this specific proposal focuses on shareholders, one should bear in mind that other actors – such as employees, consumers and local communities – are also highly relevant. For companies to be well-run, there has to be respect for and active engagement from all stakeholders. The draft opinion includes the following amendments:

Forsgardh and BRB on November 11, 2014. See EU Alert 46)

Lars-Erik Forsgardh and BRB meeting Olle Ludvigsson, the rapporteur for ECON Committee on November 18.

18/11/2014: A meeting with MEPs with Pervenche Berès (ECON Committee, French) + Virginie Rozière (JURI & IMCO Committee, French). Lars-Erik Forsgardh, Roger Barker, and BRB being present.

26/11/2014: BRB participated to the Policy Committee of EuropeanIssuers.

02/12/2014: Lutgart Van den Berghe speaking at the hearing organized by the JURI Committee on December 2,2014.

28

ecoDa’s EU Updates – November 2014amendments 24/03/2015 Committee Vote

Shadow rapporteurs:

Toti (EPP-IT)

Maštálka (GUE/NGL- CZ)

Pascal (Greens/EFA - FR)

Wikström (ALDE - SE)

ECON (opinion) Rapporteur : Ludvigsson (S&D - SE)

Shadow rapporteurs:

Fox (ECR – UK)

Schwab (PPE – DE)

Scott Cato (Verts/ALE – UK)

Van Nieuwenhuizen (ADLE – NL)

Timeline:

Council: Working Party on 26 November 2014

For a system with remuneration policies to be rational and meaningful, the policies cannot too often or too much be put to the side. Therefore, an exemption from a policy should be accepted only if it affects maximum amounts of remuneration and the situation is exceptional – for example if the company is in a leadership crisis (Article 9a). If a company has gone beyond a policy once and wants to do so again, it is reasonable that it presents a proposal for a revised policy to the shareholders.

With the aim of upholding transparency and maintaining a level playing field, the ratio between the remuneration of directors and employees should always be included in remuneration policies (Article 9a). This ratio will have to be interpreted differently depending on for example the business and geographical set-up of the company. However, it is always a useful metric which could and should be disclosed by all companies.

On related party transactions, the Commission’s proposal is a little too ambitious (Article 9c). There should be a proper European minimum level to counter a problematic pattern of abusive transactions, but that level does not have to be very high. A bit of back-tracking is needed. In particular, it seems reasonable to let it be up to Member States, depending on national conditions and practices, to decide if the requirement to hold a shareholder vote is proportionate for all 5%+ related party transactions, or if it should apply only to transactions which are not concluded on market terms.

The Italian presidency is very ambitious and would like to have a general approach by the end of its mandate. The European Commission and the Italian presidency work on redrafting related party transactions proposal (different Member States which have just implemented new national regulation are not interested by harmonization) + the remuneration part (judged too technical).

02/12/2014: Second meeting for Lutgart Van den Berghe and BRB with the assistant of Sergio Cofferati. 9/12/2014: Lars-Erik Forsgardh participating at the International Investors‘ Conference in Wiesbaden/Germany.

February 2015: Conference organized by ecoDa, EuropeanIssuers, ACCA and BusinessEurope

29

ecoDa’s EU Updates – November 201408/12/2014 Presentation of draft report

06/01/2015 Deadline for amendments

26-27/01/2015 Consideration of amendments

23-24/02/2015 Committee Vote

A possible compromise stated that: “Member States shall ensure that the vote of shareholders on the remuneration policy is binding. However they may provide that the vote is advisory provided hat where shareholders vote against the remuneration policy, a revised policy is submitted for approval by the shareholders at the next general meeting.”

.

Engaging shareholders

Green Paper Long-term financing of the European EconomyDeadline: 25 June 2013

Green Paper: On the basis of the outcome of this consultation, the Commission will consider the appropriate actions to pursue further.

Follow up of the Green Paper on long term financing: all options are possible, including whether they would include or not soft or hard law initiatives, which could cover both financial markets and intermediaries, as well as users of financial services, like SMEs.

Eurosif (European Sustainable and responsible investment Forum) has organised a conference on 24 September 2013 on long-term financing + shareholders’ rights. Jeroen Hooijer made it clear that shareholders’ engagement is a major branch of the European action plan. As reflected in the John Kay’s report, direct ownership is very limited in EU. The Commission has no illusion that one or two solutions will enable shareholders’ engagement but it is important to realign incentives.- increase the information screen,- asset owners should be more transparent,

30

ecoDa’s EU Updates – November 2014- companies need to be willing to be engaged in a positive dialogue (different approaches exist in Europe: German CEOs are reserved).- Transparency requirements / voting policies- Vote on remuneration policy- Disclosure of related party transactions,- Clarifications regarding proxy agencies.Eurosif has issued a report on active ownership: www.eurosif.orgEurosif recommends that policy-makers:o Mandate strong (ESG) corporate disclosure,o Incentivise investor stewardship via smart regulation (fiduciary duties, voluntary codes),o Remove technical barriers (share-blocking, investors’ identification, etc)o Impose investors’ disclosure on their voting policiesThe new shareholders’ directive (article 3f):

Sets out the need for institutional investors and assets mangers to develop a policy on shareholder engagement covering a number of actions set out in the article including policies to manage actual or potential conflicts of interests

Requires institutional investors and asset managers to publicly disclose their engagement policy on an annual basis along with its implementation and results

Better shareholder oversight of related party transactions

2011 Green Paper on CG Framework

2012 Action plan on CG and Company Law

2013 Review of the shareholders’ directive

European CG Forum

European CG Forum Issued a statement on related party transactions recommending of common principles across Europe

The 2011 Green Paper raised the question of providing more protection against related party transactions

2012 Action plan: The Commission will propose in 2013 an initiative aimed at improving shareholders’ control over related party transactions, possibly through an amendment to the shareholders’ rights Directive.

The new shareholders’ directive: Requires related party transactions representing more than 5% of

the companies’ assets or transactions which can have a significant impact on profits or turnover to be put up to a vote by shareholders before concluding the transaction

Requires companies to publicly announce transactions that represent more than 1% of their assets and accompany it with a report from an independent third party

31

ecoDa’s EU Updates – November 2014 Sets out that related party transactions with the same party within

12 months will be aggregated and if it exceeds 5% needs to be put up for a vote

Proxy advisors

2012 Action plan on CG and Company Law

2013 Review of the shareholders’ directive

ESMA19 February 2013 Final Report

ESMA’s Consultation

Best Practice Principles for Shareholder Voting Research

In 2012 ESMA issued a discussion paper on proxy advisors requesting views on possible regulatory options for proxy advisors, ranging from no action and voluntary measures to quasi-binding or binding EU instruments

2012 Action plan: The Commission will consider an initiative in 2013, possibly in the context of the revision of the shareholders’ rights Directive, with a view to improving the transparency and conflict of interest frameworks applicable to proxy advisors.

The Drafting Committee of the Best Practice Principles for Governance Research Providers has launched a public consultation on the draft Principles which concern activities associated with the provision of shareholder voting and analytical services. The Committee – which is independent from the European Securities and Markets Authority (ESMA) – has drafted the Principles following ESMA’s 19 February 2013 Final Report which states that the proxy advisory industry would benefit from increased disclosure and transparency regarding how it operates. The draft Principles can be found on the website of the Committee.The deadline for submitting responses to the consultation was 20 December 2013

6 Charter Signatories published Best Practice Principles for Shareholder Voting Research & Analysis service providers (issued in March 2014)

► Principle 1: Service QualitySignatories should aim to offer high-quality services that are

delivered in accordance with agreed-upon client specifications. Signatories should have and publicly disclose their research methodology and, if applicable, house voting policies.

► Principle2: Conflicts of Interest ManagementSignatories should have and publicly disclose a conflicts-of-interest

policy that details their procedures for addressing potential or actual conflicts of interest that may arise in connection with the provisions of

32

ecoDa’s EU Updates – November 2014services.

► Principle 3: Communication PolicySignatories should have and publicly disclose their policy (or

policies) for communication with issuers, shareholder proponents, other stakeholders, media and the publicSignatories will publish a Statement of Compliance, on a comply-or-explain basis

The new shareholders’ rights directive: Requires proxy advisors to adopt and implement measures to

guarantee that their voting recommendations are accurate, reliable and not affected by conflicts of interest

Requires proxy advisors to annually disclose to the public information in relation to the preparation of their voting recommendations

Sets out information proxy advisors need to disclose

Shareholder identification

2011 Green Paper on CG Framework

2012 Action plan on CG and Company Law

2013 Securities legislation+ shareholders’ rights directive

The 2011 Green Paper asked whether stakeholders saw a need for a European mechanism to help issuers identify their shareholders in order to facilitate dialogue on corporate governance issues. In addition, the Green Paper enquired whether this information should also be made available to other investors. A clear majority of respondents were in favour of such a mechanism.

2012 Action plan: The Commission will propose, in 2013, an initiative to improve the visibility of shareholdings in Europe as part of its legislative work programme in the field of securities law.

The new shareholders’ rights directive: Requires Member States to provide that companies have a right to

identify their shareholders, even when shareholders use intermediaries

Ensures that data protection rules are taken into account

In March 2014, the European Post Trade Group (EPTG) was set up on the recommendation of the European Group on Market Infrastructures (EGMI)

33

ecoDa’s EU Updates – November 2014

European Post Trade Group

ECB Shareholders Transparency Taskforce Report

that the dismantling of remaining obstacles to a safe, efficient, and competitive European post-trading landscape would require targeted cooperation between public authorities and the private sector.The EPTG is a joint initiative between the European Commission, the ECB, ESMA, and industry. Its members are representatives of the key players involved in post-trade issues. See here.

ECB Shareholders Transparency Taskforce Report(See here)

Acting in concert

2011 Green Paper on CG Framework

2012 Action plan on CG and Company Law

2014 Guidance (in close cooperation with ESMA and competent national authorities)

ESMA

Shareholders need to know when they can exchange information and cooperate with one another without running the risk that their actions may trigger unexpected legal consequences.

During 2013, the Commission will work closely with the competent nationalauthorities and ESMA with a view to developing guidance to increase legal certainty on the relationship between investor cooperation on corporate governance issues and the rules on acting in concert.

12 November 2013: ESMA clarifies shareholder cooperation in takeover situationsThe European Securities and Markets Authority (ESMA) has published a statement on practices governed by the Takeover Bid Directive (TBD), focused on shareholder cooperation issues relating to acting in concert and the appointment of board members.The statement contains a White List of activities that shareholders can cooperate on without the presumption of acting in concert. It also contains information on how shareholders may cooperate in order to secure board member appointments by setting out factors that national authorities may take into account when considering whether shareholders are acting in concert.

34

ecoDa’s EU Updates – November 2014The statement is in response to a request by the European Commission for clarity on these issues, following its 2012 report on the application of the TBD. It is based on information collected about the TBD’s application and common practices across the European Economic Area (EEA). The statement was prepared by the Takeover Bids Network, a permanent working group, under ESMA’s auspices, that promotes the exchange of information on practices and application of the TBD across EEA

Disclosure of voting and engagement policies

2011 Green Paper on CG Framework

2012 Action plan on CG and Company Law

2013 Review of the shareholders’ directive

UK Stewardship CodeDutch Eumedion best practices

EFAMA Code

ICGN Principles

Research conducted in preparation for the Commission Green Papers of 2010 and 2011 and the responses to them highlighted a need for improvement in the transparency of voting policies adopted by institutional investors, including asset management firms, and the exercise of these policies.

UK Stewardship Code

Dutch Eumedion best practices

EFAMA Code

ICGN Principles

The Commission will in 2013 come with an initiative, possibly through modification of the shareholders rights Directive35, on the disclosure of voting and engagement policies as well as voting records by institutional investors.

See above

Executive remuneration

2010 Resolution

European Parliament resolution of 7 July 2010 on remuneration of directors of listed companies and remuneration policies in the financial services sector

35

ecoDa’s EU Updates – November 2014

2011 Green Paper on CG Framework

2012 Action plan on CG and Company Law

2013 Review of the shareholders’ directive

ICGN’s Consultation

Green Paper: Shareholders need clear, comprehensive and comparable information on remuneration policies and individual remuneration of directors.

ICGN consulted its members on its latest guidance draft “ICGN Executive Remuneration Guidelines and Model Policy”.

The Commission will propose in 2013 an initiative, possibly through a modification of the shareholders’ rights Directive, to improve transparency on remuneration policies and individual remuneration of directors, as well as to grant shareholders the right to vote on remuneration policy and the remuneration report.

The Commission will have to expand the remuneration guiding principles (no rigid rules, no capes) stated in the CDRIV directive but they will not cut and paste these principles for listed companies

The new shareholders’ right directive: Ensures that shareholders have the right to vote on the

remuneration policy for directors Requires remuneration policy to be submitted to the approval of

shareholders every three years Requires criteria for the award of fixed and variable remuneration Requires remuneration policy to be publicly disclosed on the

company’s website after approval by the shareholders

Benchmark among ecoDa’s members of the say on pay

36

ecoDa’s EU Updates – November 2014

Audit

Subject European Commission

European Parliament

European Council

State of play + documents ecoDa’s actions

AuditDG Financial Stability Unit F4

2010 Green Paper on Audit

2011 Draft proposal

2011 Report

http://ec.europa.eu/internal_market/consultations/docs/2010/audit/green_paper_audit_en.pdf

Rapport of Mr Massip Hidalgo adopted in September 2011http://www.europarl.europa.eu/sides/getDoc.do?pubRef=-//EP//NONSGML+REPORT+A7-2011-0200+0+DOC+PDF+V0//EN&language=EN

The Commission issued its proposals in November 2011.

The purpose of these texts is threefold:

- to improve auditors’ independence and audit quality

- to get more dynamism in the audit market

- to reinforce supervisory

5 main elements in this big package of texts:

- mandatory rotation of audit firms after 6 years extended by further 2 years if authorized by supervisor and in situation where there is joint audit the rotation will be imposed after 9 years

- mandatory tendering: Public-interest entities will be obliged to have an open and transparent tender procedure when selecting a new auditor. The audit committee (of the audited entity) should be closely involved in the selection procedure. prohibition of certain non audit services. The Commission sets two categories (one basket of services prohibited and a basket of services that might generate conflict of interest depending of the extend of the job done). In addition, large audit firms will be obliged to separate audit activities from non-audit activities in order to avoid all risks of conflict of interest.

- pure audit for audit firms

ecoDa responded

Participation of Massip Hidalgo at ecoDa conference on 7 September 2011

ACCA (the Association of Chartered Certified Accountants) and ecoDa (the European Confederation of Directors' Associations) organised a joint roundtable on 6 December 2011

30/09/2014: BRB attending the ACCA and EGIAN Conference 'Implementing the new audit reform: how to ensure the creation of a

37

ecoDa’s EU Updates – November 2014

Discussion + Vote at the European Parliament

- Prohibition of “big firms” clauses

In addition:

- the audit report will have to be clearer and better adapted to the need of investors

- better supervision and improve coordination at EU level

- An European passport to improve opportunities in the single market + a European quality certificate for a European benchmark and provision on international standards