Embed Size (px)

Citation preview

Sub-Saharan Africa • Kenya

K-REP Bank: Alleviating Poverty through Micro-Finance Prepared by • Winifred N. Karugu & Diane Nduta Kanyagia (Kenya) Sector • Financial Services Enterprise Class • Local SME

Summary Half of Kenya’s population of 32 million lives below the poverty line– on less than a dollar a day. Poverty is a self-perpetuating cycle characterized by low levels of education, increased deprivation, and low standards of living. In Kenya there are many interventions underway attempting to break the poverty cycle, with mixed results. One of the interventions yielding real results is micro-finance. K-REP Bank is one of the more successful Micro-finance Institutions (MFIs) in the country. Micro-finance is a development intervention that has evolved to operate on a commercially viable basis by providing banking and financial services to low-income populations. K-REP Bank grew from an MFI into Kenya’s first micro-finance bank. K-REP Bank, which started operations in 1999, offers several products and services including micro-credit facilities to low-income populations, individual loans, wholesale loans to micro-finance providers, deposit facilities, letters of credit and bank guarantees. The micro-credit loans are based on the Grameen Bank group-lending model, and they can be categorized into three levels. Ideally, a group would start at Level 1 (juhudi), progress to Level 2 (chikola) and finally end up at Level 3 (kati kati). Beyond Level 3 an individual is deemed ready for normal commercial bank loans.

Introduction Half of Kenya’s population of 32 million lives below the poverty line– on less than a dollar a day. Poverty is a self-perpetuating cycle characterized by low levels of education, increased deprivation and low standards of living. Developing countries have long endeavoured to break the poverty cycle, and these undertakings have been met with mixed results. In Kenya there are many interventions in progress attempting to break the poverty cycle, again with mixed results. One of the interventions yielding real results is micro-finance. K-REP Bank is one of the more successful Micro-Finance Institutions (MFIs) in the country.

K-REP Bank K-REP Bank is a licensed commercial bank that specializes in micro-finance. It was the first micro-finance commercial bank in Kenya. Micro-finance is a development intervention that has evolved over time to operate on a commercially viable basis by providing banking and financial services to poor people. The bank is distinguished from other commercial banks or financial institutions by its social mission of addressing poverty by supporting employment, income generation and savings mobilization among low-income and poor people. These economic development measures act as a means of building an asset base for poor households.

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 2

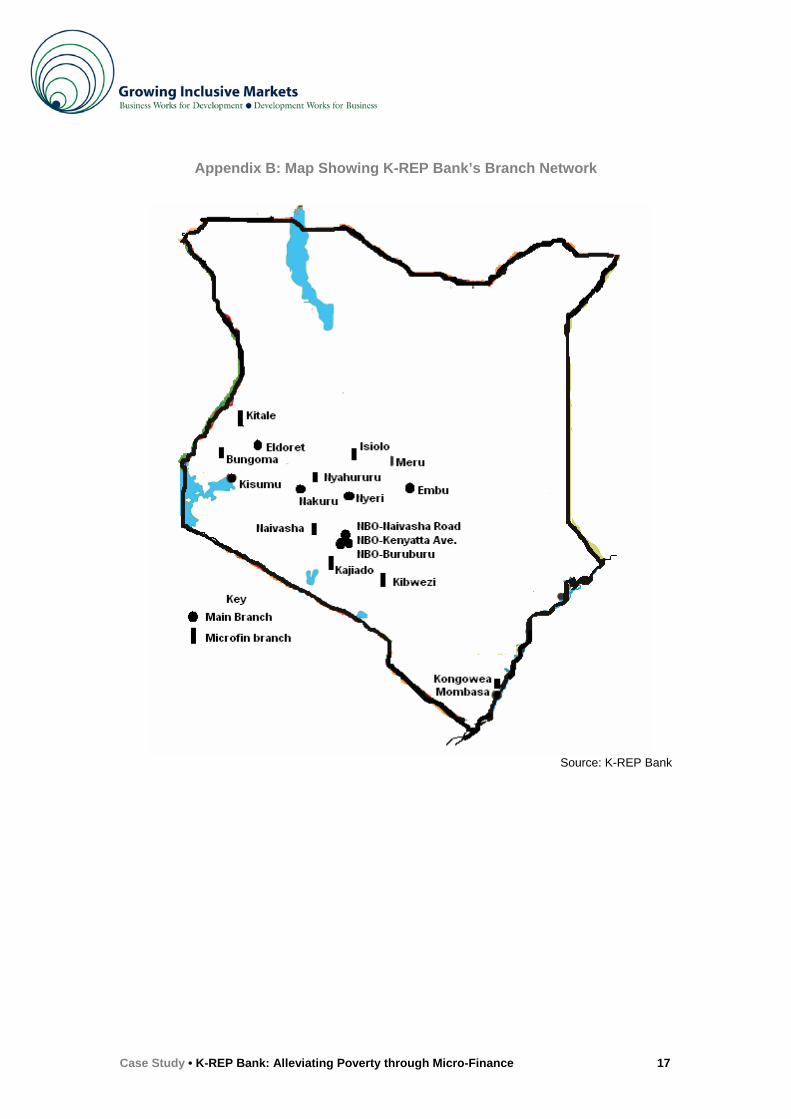

Traditionally, micro-finance activities focused on the development of micro-enterprises and small businesses. This has since evolved to include a broad range of financial services required by poor people. These services enable low-income populations to better organize their financial lives and propel themselves out of poverty. K-REP Bank was established as part of the K-REP Bank Group Limited, a micro-finance development agency, involved in research, advisory services and the development of micro-finance products. For more information on the historical origins of K-REP Bank, see Appendix A. The philosophy of the bank is that banking and financial services are basic human rights, and every Kenyan, especially low-income people, must have adequate access to these services. The bank believes that the micro-entrepreneurs are bankable and that accessible banking and financial services are commercially viable. K-REP Bank also believes that low-income people do not need handouts; what they do need is access to appropriately delivered financial services. It further believes that this service is an essential ingredient for development. The Bank therefore aims to bring micro-finance to the mainstream of the financial banking arena, as opposed to the peripheral where it has hitherto been perceived to exist. K-REP Bank has become the largest micro-finance bank in Kenya, serving over 32 districts1 with additional clients in over 15 African countries (see Appendix B for a map of Kenya showing K-REP Bank branches). In 2005, it disbursed a total of US$34 million in small loans to 69,000 poor clients throughout Kenya and held clients savings to the tune of US$15 million. K-REP Bank’s lending activities support 1.5 percent of Kenya’s 900,000 micro-enterprises. Fifty-five percent of K-REP Bank’s borrowers are women. K-REP Bank has 397 employees, each serving an average of 175 borrowers. (See Appendix C for further information on K-REP Bank’s performance indicators and Appendix D for financial statements.)

The Business Model K-REP Bank offers the following products and services: MICRO-FINANCE GROUP LOANS K-REP Bank offers micro-finance loan facilities that are based on the Grameen Bank lending model. The loans are made available to specific groups whose members ensure that fellow members repay their loans on a set schedule. Members must also save weekly in personal accounts with K-REP Bank, with the minimum amount being US$3 per week. K-REP Bank’s micro-finance portfolio consists of three types of group loans,2 which are progressive in

1 Kenya has a total of 68 districts (Republic of Kenya, 2004). 2 In order to benefit from the micro-credit facility, an individual must belong to a group. Groups must meet regularly and they guarantee one another for loans. The group will be unable to borrow again until the outstanding group loan is paid back. However each member can also take a personal loan on top of the group loan depending on his or her savings in their K-REP Bank account and their credit history. A personal loan must have personal collateral, i.e. the group does not guarantee it.

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 3

nature. Ideally, a group would start at Level 1, progress to Level 2 and finally end up at Level 3. Beyond Level 3, an individual is deemed to be ready for normal commercial loans. The three types of micro-finance loans are: • Group Loan, Level 1 (Juhudi): The Juhudi scheme provides loans based on a

modification of the group-lending methodology used by the Grameen Bank in Bangladesh. K-REP Bank facilitates the formation of five-member groups called watanos3 whose members meet on a weekly basis and contribute Kshs 200 (US$3) each, which goes into the group savings account. Members borrow small amounts of money ranging from US$150 to US$400. The loans are made to a few members to in the beginning. As they repay, other members are able to access loans. Loans must be paid back within 6 to 18 months. Up to six watanos confederate into a kiwa, which is registered by the Ministry of Culture and Social Services as a self-help group. After a Juhudi group has been in existence for some time, it may seek approval to transform into a Chikola group.

• Group Loan, Level 2 (Chikola): The Chikola scheme provides credit to individual entrepreneurs through rotating savings and credit associations (ROSCAs). ROSCAs are groups in which members save a set sum during a specified time period such as every day or week or month. One member takes up the total amount saved each time, hence the rotating nature of the model. ROSCAs are very popular in Kenya, and this is why MFIs have incorporated them into their activities. Under the Chikola scheme, K-REP Bank provides a single loan to an established ROSCA group (there is an average membership of 20 persons) that retails the loan to its individual members. This group meets once per month and loans must be repaid to K-REP Bank within 12 to 24 months.

• Group Loan, Level 3, Solidarity Loan (Kati-Kati): This type of loan is made to voluntarily formed solidarity groups (five to ten existing K-REP Bank clients). Usually this group has evolved from a Chikola group. The group meets about once per month, and a K-REP Bank official is present during all group meetings. Kati-Kati group members borrow relatively large sums of money (ranging from US$1,200 to US$30,000 per person) and they are soon ready to evolve into normal commercial banking activities.

INDIVIDUAL LOANS K-REP Bank’s individual loans are designed for both existing group clients and new individual clients, as well as for organizations. They are offered through the Bank’s branches. Individual loans require collateral, while group loans require members to guarantee one another. The three types of individual loans can be summarized as follows: • Retail Loans: Loans are made to individuals and institutions such as companies,

partnerships, government institutions, associations/clubs and NGOs. The loans range from US$3,205 to US$64,103 and are repayable within three years. Applicants pay a one

3 Despite the name watano, which means five people in Swahili, members making up a Juhudi group may be as few as three or as many as eight depending on the circumstances.

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 4

percent commitment fee, and the loans are charged annual interest between 15 percent and 17 percent on a declining balance. Retail loans are made to organizations that will lend to low-income clients.

• Consumer Loans: Loans are made to salaried employees with the loan size (which begins at US$321) not exceeding four times the employee’s net monthly pay. The term is one to two years, and the client must save a minimum of 15 percent of the repayment amount each month. There is a one percent commitment fee, and the interest rate varies from 14 percent to 17 percent (on a declining balance).

• Overdraft Facility: K-REP Bank offers this facility to current account holders who have a good track record in servicing term loans. The interest rate charged is 15 percent - 17 percent per annum on a declining balance.

In general, for an individual to secure a loan, he or she must have saved 20 percent of the loan amount. This applies for both individual and group loans. For individual loans the borrower must also provide collateral such as a title deed for land or the log book of a car that is being hired out and earning rental income. Interest is charged in one of two ways: either 30 percent on reducing balance or 16 percent flat rate. On average, if the loan amount is Ksh 100,000 (US$1,400) the repayment period is one year. If the loan amount is between Ksh 100,000- 250,000 (US$1,400 to $3,500) the repayment period is 18 months, and if the loan amount is above Ksh 250,000 (US$3,500) the repayment period is 24 months. For loan amounts exceeding Ksh 700,000 (US$10,000), security or collateral is needed, such as motor vehicle logbook or title deed. WHOLESALE LOANS K-REP Bank makes wholesale loans to other MFIs, cooperative societies and other associations who, in turn, on-lend to their own micro-finance clients. The loan term is one to three years, and interest rates range from 12 percent to 15 percent (on a declining balance). DEPOSIT FACILITIES K-REP Bank offers a wide range of customer deposit (savings) accounts, which include conventional savings accounts, conventional current accounts with cheque facilities, and group savings accounts. OTHER SERVICES K-REP Bank also offers other services such as safe deposit custody, foreign currency exchange facilities, letters of credit and bank guarantees.

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 5

K-REP Bank Client Profiles: Jericho New Fashion Group To further illustrate K-REP Bank’s work, profiles of two of the Bank’s clients are given below. Both clients belong to the Jericho New Fashion Group, which is based in the low-income Jericho housing estate of Nairobi. The Jericho New Fashion Group is made up of 30 women who have improved themselves over the years due to strategic thinking and taking advantage of opportunities. One of the opportunities the group has taken advantage of is K-REP Bank lending facilities. Fifteen women formed the Jericho New Fashion Group in 1993 with the sole objective of accessing K-REP Bank micro-finance loans. Originally, the members took loans in the low-end of the market (juhudi), but over the years the members have evolved to Kati Kati status and now borrow sums around US$22,000. The members engage in various forms of business including importing ready-made clothes and fabrics, operating hair and beauty salons, car hire and operating green groceries and fast food outlets. Originally every member of the group shared the K-REP Bank loans. The first loan to the group was Ksh 15,000 (US$214), from which every member borrowed Ksh 1,000 (US$14). Over time the sum lent to the group grew to Ksh 50,000 (US$714, with individual members borrowing US$47) and then to Ksh 300,000 (US$4,286, with individual members borrowing US$289) all without security, except for the members guaranteeing each other. As their businesses grew the group-lending system eventually proved to be a problem, because the group could not take a lump sum loan again until every member in the group had finished paying back the previous loan. Some members would repay their loans within two months, while others took perhaps ten months to repay. Yet a fully paid member could not borrow more money until everyone in the group had repaid their loans. This caused many of the original members of the group to withdraw from the group due to frustration. Luckily for the remaining members of the group (especially those who were also thinking of leaving), K-REP Bank began giving individual loans to group members4 (in other words, the group attained kati kati status). This was to have great impact on the businesses of the members. The members of Jericho New Fashion Group reinvented themselves after K-REP Bank offered individual loans. Although they must function as a K-REP Bank group, they have gained confidence and cohesiveness as a group in its own right and engage in many activities outside of K-REP Bank. A case in point is the ROSCA5 that they formed which

4 Kati Kati members are able to borrow relatively large amounts of money as individuals using additional collateral. But they must still remain members of a group with the required group activities such as regular meetings, mandatory saving, etc. Kati Kati status prepares an individual to evolve into ordinary bank borrowing as a lone individual. 5 ROSCAs (Rotating Savings and Credit Associations) are a common feature of Kenyan social life at all echelons, particularly among women. Such groups save money for various purposes including investment, and members receive funds periodically. ROSCAs are gaining recognition as a serious

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 6

seeks out investment opportunities for members such as investing in the Initial Public Offerings of Kenyan companies. The members meet weekly and are a force to be reckoned with locally, because they support each other’s business and are now financially successful. Some of the members were the pioneers who first imported denim into Kenya, while others have ventured into businesses that women traditionally shied away from such as public service transport. Two of the members of the Jericho New Fashion Group are profiled below. NANCY MUTHONI MURIITHI: NANCY’S FABRICS

Nancy Muthoni is a founding member of the Jericho New Fashion Group. When Nancy joined the group the initial contribution was Ksh 2,000 (US$29) per person, and the total amount raised was Ksh 30,000 (US$435). This sum enabled the group to open an account with K-REP Bank. After the account was opened, each member saved Ksh 220 (US$3.10) per month, of which 200 shillings was banked in the K-REP Bank account, while Ksh 20 (US$0.30) was retained by the group for administrative expenses.

Source: Winifred N Karugu and Diane Nduta Kanyagia

At the time that Nancy joined the group she was a tailor who was not making much money, and her motivation in joining was to access a loan from K-REP Bank in order to try and increase her income. She could not have foreseen the impact this would have on her business and her life. When K-REP Bank began giving individual loans, Nancy borrowed what was for her a large amount of money and started selling ready-made clothes instead of being a tailor. As she successfully repaid the loans that she took, she was able to borrow successively larger sums of money, and thus made bigger profits. This enabled her to move on to selling a variety of fabrics. These included fabric for clothes, upholstery and curtains. She now sources all these fabrics from Dubai and India and travels extensively. The largest loan she has borrowed from K-REP Bank was US$14,300. Looking back on the last decade, Nancy is grateful to K-REP Bank for helping her to achieve so much. She says that K-REP Bank trusted her and gave her a loan when no other bank would. She jokes that K-REP Bank trusted her even more than her husband did.6 Nancy is very proud of her financial independence which has enabled her to educate one of her

financial reality. For example, some major fund managers acknowledge ROSCA funds as making up 30% of their portfolios. 6 Initially Nancy’s husband was skeptical of the whole K-REP Bank micro-finance concept and was worried that she would end up in trouble. Over time he has become appreciative of the groups’ achievements. The same has happened in many households within the group.

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 7

children in a private university without having to worry about the fees. She has even bought herself a car for personal transport. Nancy has also started a public address hiring business for her son to give him financial independence, as well as a retail clothes business for her daughter-in-law. She has been able to successfully bid for maximum share allocation for herself and her daughter in recent initial public offerings at the Nairobi stock exchange. Because of K-REP Bank’s innovations, Nancy is a happy and confident woman. BEATRICE AGORO: AFRICAN PRIDE

Beatrice Agoro joined K-REP Bank as part of the Jericho New Fashion Group in 1993 but dropped out after three years due to the limitations on group-lending. She rejoined later in the year 2000 and took out an individual loan of Ksh 20,000 (US$285), which was a great deal of money for her at that time. Currently she has an individual loan of Ksh 1.5 million (US$22,000).

Source: Winifred N Karugu and Diane Nduta Kanyagia

A tailor by profession, Beatrice dropped out of high school because her parents could not afford to pay her school fees. She initially borrowed money to

buy fabric and sewing machines in order to grow her tailoring business. Over the years she has continued to borrow progressively larger amounts of money from K-REP Bank, which has helped her to grow her business, and she currently has two tailoring stalls with five employees and several sewing machines. Her tailoring business is quite busy because she has a reputation for high-quality clothes made from the finest fabrics. Beatrice travels a great deal in order to source the best fabrics from India, Dubai, the United States and West Africa. Sometimes she buys the fabrics brought in by other members, but in general she is less satisfied with these than she is with her own selections. Her clothing line ranges from business suits to casual wear and retails for a price range that extends from US$50 to US$350. Her business is so busy that Beatrice sometimes has to turn away customers or, if they are agreeable, keep them waiting for a while. Beatrice has also recently expanded into the car hire business. She thus became the biggest borrower of her group by borrowing US$22,000, which she services by paying US$714 to K-REP Bank every fortnight. She has been repaying this loan for the past one and a half years, and she used it to purchase two cars that she hires out. Like Nancy, Beatrice is of full of praise for K-REP Bank, crediting the bank with her success in business. She likewise praises Jericho New Fashion Group saying that they help one another through the sharing of ideas, encouragement and trouble-shooting problems. She is thankful that she came across both entities.

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 8

Success Factors and Lessons Learned In the World Bank case study entitled “The Case of K-REP Bank Nairobi, Kenya”7 the authors provide a full description of the success factors that enabled K-REP Bank to scale up its activities and transform itself from a non-profit organization to a commercial bank. The World Bank case lists institutional commitment to pro-poor policies, political commitment to poverty alleviation, ability to adapt to change and external catalysts as the main success factors. Furthermore, K-REP Bank has learned valuable lessons along the way as it evolved from a small MFI to a pro-poor commercial bank. Increasingly, K-REP Bank has learned that it must charge interest rates sufficient to cover operating and financial costs. The decision was informed by lessons learned from poor performance in a few of its lending schemes.8 K-REP Bank has also learned that although its Chikola scheme offers the advantage of tapping into existing groups of entrepreneurs with existing businesses, sufficient time must be given for new Chikola groups to form the required group cohesiveness necessary for their smooth operation and stability. K-REP Bank has also learned lessons about minimizing causes on non-repayment of loans. After investigation, some of K-REP Bank’s own institutional practices were found to contribute to default such as subsidized interest rates and credit programmes associated with other social welfare services. Additionally, delegating credit assessment to the groups themselves yields poor results since group members are not objective regarding their colleagues. Insufficient screening of potential borrowers by the credit officer and poor appraisals of investments were also found to increase the default rate. The use of group member savings as collateral may also cause default, because borrowers do not like to forfeit their savings on account of their peers. Other major factors that may cause default were found to be theft or destruction of business assets, mismatches between loan size and expected income flow, diversion of loan purpose, fraud and death or sickness.

Innovations K-REP Bank’s primary innovations include client input, monitoring and group cohesiveness. CLIENT INPUT Client input is necessary to assess performance and to formulate institutional policy. Through client interaction and internal research and evaluation, K-REP Bank has pursued innovations to provide greater access and outreach, lower intermediation costs and better the prospects for continued growth. Some of the promising innovations that K-REP Bank has adopted, such as more flexible loan size and

7 Nyerere, J., K. Mutua, F.S. Steele, A. Dondo, and J. Kahashangaki. 2004. The case of K-REP Bank Nairobi, Kenya. Proceedings of Scaling Up Poverty Reduction: A global Learning Process and Conference. . Shanghai, May 25-27, 2004. World Bank. 8 For example, K-REP Bank was affected by declining repayment rates in the Chikola scheme in Nyeri (a rural agrarian district). K-REP averages loan repayment rates above 90 percent, but in 1995 in Nyeri the rate had fallen below 80 percent.

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 9

increased group meeting frequency, surfaced initially through interactions with clients. MONITORING AND EVALUATION K-REP Bank has also implemented a monitoring system that identifies appropriate operating and financial performance indicators and feeds the resulting information back into its operations. GROUP COHESIVENESS Membership in a Rotating Savings and Credit Association (ROSCA) group is a requirement for some K-REP Bank clients as this encourages them to develop social funds for emergencies. K-REP Bank builds the capacity of ROSCAs and other community based financial structures and makes them effective systems for delivering financial services to low-income groups. Group or social activities among members of a ROSCA group increases cohesion. ROSCAs also encourage their members to operate bank accounts for processing their loan cheques. Many clients are using these accounts very actively.

Barriers and Challenges Although there is a general consensus among clients that credit from K-REP Bank has resulted in improved incomes and growth in their businesses, K-REP Bank still faces many challenges as described below. TAILORING FINANCIAL PRODUCTS TO MEET DIVERSE CLIENT NEEDS Not all financial products identified for communities may be suitable, and K-REP Bank continues to adapt its offerings to best meet the needs of its clients. For example, farmers engage in seasonal production and therefore need loan products that are suitably tailored to this reality. Street hawkers, on the other hand, may require loans that are repaid on a daily basis. K-REP Bank also faces pressure for larger loans from some clients. In striving to meet all client needs, K-REP Bank seeks to strike a balance between maintaining its mission to serve the poor and also servicing clients who are no longer poor and those who want to borrow greater amounts. Different levels of poverty need different approaches. CAPACITY BUILDING FOR CLIENTS In some of the more under-privileged districts and communities, capacity building to understand micro-finance is still extremely difficult due to low levels of education. K-REP Bank clients undergo training in financial management during regular group meetings. However, sometimes this is not enough to make some clients comfortable with micro-finance. COMPETITION Because of the success of the micro-finance industry in Kenya, K-REP Bank faces increasing competition for clients from other MFIs such as Faulu Kenya and Kenya Women’s Finance Trust among many others. The competitors are constantly developing new products and innovating in other ways. For example, Faulu Kenya now has a client base of 100,000 low-

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 10

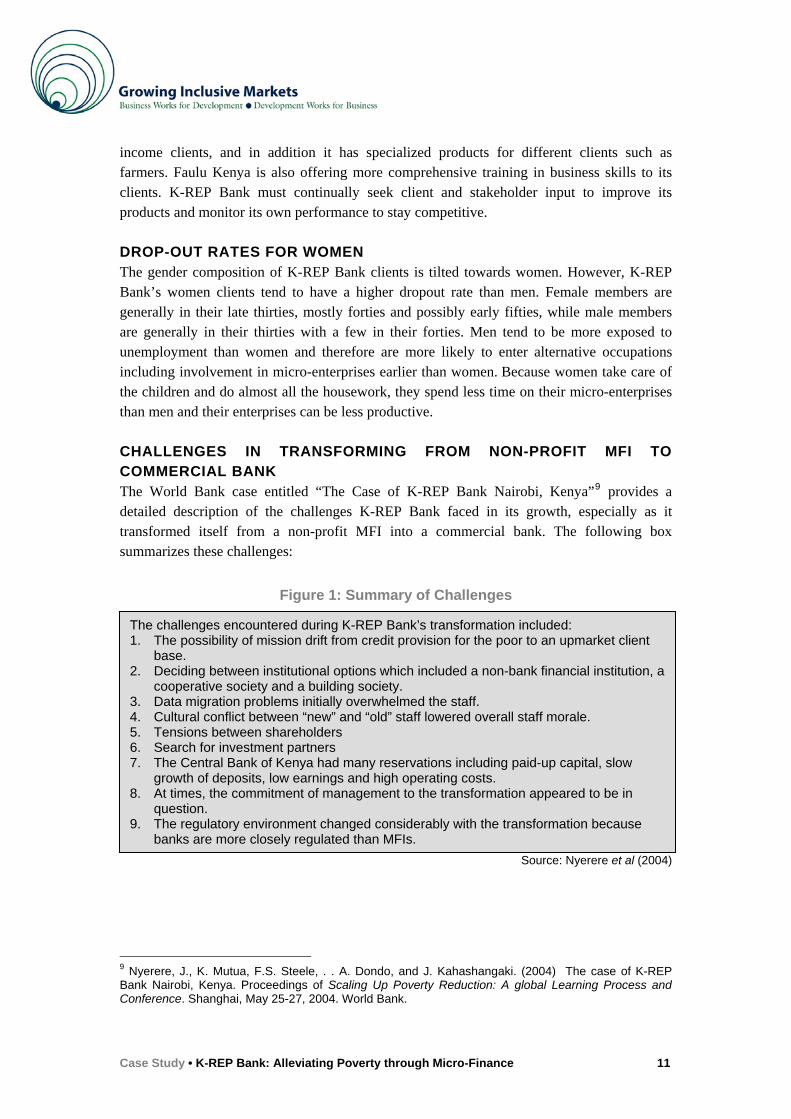

income clients, and in addition it has specialized products for different clients such as farmers. Faulu Kenya is also offering more comprehensive training in business skills to its clients. K-REP Bank must continually seek client and stakeholder input to improve its products and monitor its own performance to stay competitive. DROP-OUT RATES FOR WOMEN The gender composition of K-REP Bank clients is tilted towards women. However, K-REP Bank’s women clients tend to have a higher dropout rate than men. Female members are generally in their late thirties, mostly forties and possibly early fifties, while male members are generally in their thirties with a few in their forties. Men tend to be more exposed to unemployment than women and therefore are more likely to enter alternative occupations including involvement in micro-enterprises earlier than women. Because women take care of the children and do almost all the housework, they spend less time on their micro-enterprises than men and their enterprises can be less productive. CHALLENGES IN TRANSFORMING FROM NON-PROFIT MFI TO COMMERCIAL BANK The World Bank case entitled “The Case of K-REP Bank Nairobi, Kenya”9 provides a detailed description of the challenges K-REP Bank faced in its growth, especially as it transformed itself from a non-profit MFI into a commercial bank. The following box summarizes these challenges:

Figure 1: Summary of Challenges

Source: Nyerere et al (2004)

The challenges encountered during K-REP Bank’s transformation included: 1. The possibility of mission drift from credit provision for the poor to an upmarket client

base. 2. Deciding between institutional options which included a non-bank financial institution, a

cooperative society and a building society. 3. Data migration problems initially overwhelmed the staff. 4. Cultural conflict between “new” and “old” staff lowered overall staff morale. 5. Tensions between shareholders 6. Search for investment partners 7. The Central Bank of Kenya had many reservations including paid-up capital, slow

growth of deposits, low earnings and high operating costs. 8. At times, the commitment of management to the transformation appeared to be in

question. 9. The regulatory environment changed considerably with the transformation because

banks are more closely regulated than MFIs.

9 Nyerere, J., K. Mutua, F.S. Steele, . . A. Dondo, and J. Kahashangaki. (2004) The case of K-REP Bank Nairobi, Kenya. Proceedings of Scaling Up Poverty Reduction: A global Learning Process and Conference. Shanghai, May 25-27, 2004. World Bank.

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 11

Development Impact K-REP Bank has directly or indirectly provided credit for 1.5% of Kenya’s 900,000 micro-enterprises, and the potential for further growth is considerable. The loans are mostly used for small and micro-business activity, household development, education and healthcare. K-REP Bank currently serves 69,000 active borrowers and 23,000 savers with its asset base of over US$50 million. These are people who would otherwise not have access to either credit or savings facilities. K-REP Bank has grown steadily over the last five years (see Appendices C and D) as it aims to fulfill its mission of providing micro-finance services to low-income people.

Overall, micro-enterprise finance serves primarily commerce, trade, manufacturing and the service sectors. K-REP Bank also serves a wide variety of other clients ranging from non-governmental organizations, government agencies, and international organizations to private sector clients. The ripple effect in the economy is significant, because the small businesses employ people, produce goods and services and pay taxes. Small businesses thus play an important role in the growth and development of Kenya, with an estimated six million people – a fifth of the population – depending on them for their livelihood.10 The K-REP Bank methodology has benefited their clients in a number of ways including the following: • Clients are introduced to the banking system and their productive activity is integrated

into the formal financial system. • K-REP Bank involves clients in making major decisions, such as loan approvals and

improving the services offered. • K-REP Bank builds capacity in community based financial structures and makes them

effective systems for delivering financial services to low-income groups. • K-REP Bank has established rural community banks throughout Kenya in some very

remote rural areas that are otherwise not served. • K-REP Bank has spread from rural to urban areas and now includes multiple financial

services that cater for multi-sectored needs. The group-lending model has great potential for development because it enables poor people to achieve together what they cannot achieve individually. Most groups in Kenya are started with a welfare objective. But even when groups are formed directly for the purpose of accessing financial services, as in the case of Juhudi groups, close friendships develop and increase involvement in each other's fortunes and misfortunes as characterised by involvement in household events such as weddings and funerals.

10 Republic of Kenya (2006) Economic Survey

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 12

Sustainability and Replicability To achieve sustainable growth, overcome obstacles and increase client outreach, K-REP Bank will focus on the following: • Further refine the Juhudi and Chikola schemes on the basis of client inputs • Develop different methodologies and varied loan terms to deal with the larger loans

needed by micro-enterprises that need such loans • Further develop its intermediary role so that it can provide a more complete set of

financial services to micro-enterprises • Improve its Management Information System • Develop simple but comprehensive processes and instruments to guide its lending

operations • Identify alternative forms of collateral and ways to incorporate that collateral into its

lending schemes • Devise ways to access funds from the financial markets In addition to K-REP Bank’s own growth, the micro-finance model continues to be replicated throughout Kenya and beyond. In fact, MFIs in Kenya have grown to such an extent (there are currently 14 MFIs in the country) that there is currently a bill in the Kenyan Parliament undergoing discussion to regulate the industry. One of the outcomes of the bill will be to protect consumers from unethical or “pseudo” MFIs, and another outcome will be to create a conducive, enabling environment for the micro-finance industry. In addition, the K-REP Bank model is extending to other financial services such as insurance, mortgages and money transfers.

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 13

References K-REP Bank. 2005. “Review of Global Experiences in Transformation.” K-REP Bank. 2006. K-REP Bank Company Report, 2005. K-REP Bank. 2004. A brief on K-REP Bank. K-REP Bank. 1996. “Kenya Rural Enterprises Program: Case study of Micro Finance Scheme.” Nyerere, J., K. Mutua, F.S. Steele, . A. Dondo, and J. Kahashangaki, . 2004. “The case of K-REP Bank Nairobi, Kenya.” Proceedings of Scaling up Poverty Reduction: A global Learning Process and Conference. Shanghai, 25 to 27 May 2004. World Bank. Available at http://www.microfinancegateway.org/files/39321_file_56.pdf Republic of Kenya. 2004. “Statistical Abstracts: 2004.” Central Bureau of Statistics, Ministry of Planning and National Development. Government, Printer Nairobi.

Interviews Agoro, Beatrice. Client, K-REP Bank. January 2007 Kimani, Felix. Officer, K-REP Bank. Nairobi. December 2006 Mashaka, Rhoda. Officer, K-REP Bank. Nairobi. January 2007 Michira, Carol. Branch Manager, K-REP Bank. Nairobi. January 2007 Muriithi, Nancy Muthoni. Client, K-REP Bank. January 2007 Mwaniki, Rosemary. Officer, K-REP Bank. Nairobi. November 2006

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 14

Appendix A: Historical Development of K-REP Bank K-REP Bank’s earliest origins can be traced to 1984 and a five-year “Rural Private Enterprise” project which was initiated by World Education Inc., a non-governmental organization (NGO) based in Boston with a strong focus on the development of small micro-enterprises in rural areas. The project was established to address the financial, management and technical shortfalls experienced by existing non-governmental organizations in Kenya involved in small and micro-enterprise, after a study conducted by USAID in 1983 to assess the institutional needs of NGOs. K-REP Bank began its operations in 1984 by providing loans and grants for on-lending and technical assistance to other NGOs to promote growth and generate employment in the micro-enterprise sector. K-REP Bank provided loans to NGO clients who would otherwise find it extremely difficult to access credit from commercial banks and other formal financial institutions. Over its first five years of existence, the project was solely funded by USAID, focusing on providing grants and technical assistance to its partner NGOs and largely relying on them for its performance and impact on development. In 1986, a USAID mid-term evaluation of the project concluded that the project had limited development impact and that it should be terminated. The USAID evaluation of 1986 marked the turning point for K-REP Bank, which over the next decade embarked on the following series of changes that culminated in the present day K-REP Bank and K-REP Bank Group:11 • Changing the original strategy from channelling USAID funds as grants to other NGOs to that

of advancing loans to the NGOs. Eventually, K-REP Bank ceased wholesale lending12 to other non-governmental organizations in 1994 and concentrated on retail and direct lending.

• Establishing its own micro-finance activities in 1989 and establishing this as the core business and growth area of the organization.

• Expanding its activities to include research and product development, as well as changing its technical assistance activities to a fee-for-service model.

• Developing a five-year growth plan in 1991 which envisioned K-REP Bank growing into a large NGO.

• Discarding the plan in 1994 because it did not address critical issues such as the long-term sustainability, growth, dependency and, most importantly, the appropriateness of an NGO providing financial services.

• Deciding on establishing a bank in 1994, following a study that explored the various institutional forms and the pros and cons of such a transformation.

11 K-REP Bank did enter into another five-year cooperative agreement with USAID in 1987 named Private Enterprise Development (PED) project. With well-founded support from USAID, PED was registered as WEREP, a Kenyan owned company limited by guarantee and with no share capital. In 1992, WEREP changed its name to K-REP Bank, an abbreviation for Kenya Rural Enterprise Programme. 12 Wholesale lending refers to lending large sums of capital to other organisations (in this case NGOs) to lend out in smaller amounts to individuals or small businesses (retail lending).

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 15

• Developing a business plan for the bank in 1996 and embarking on a three-year period of searching for and negotiating with investors.

• Concluding negotiations with investors in 1998 and selling assets to the bank in 1999. • Acquiring a bank license in April 1999, and starting operating as K-REP Bank in December

1999. Through this process of transformation, K-REP Bank’s activities became distinctly categorized into two divisions, namely the financial and non-financial divisions: (i) The financial division dealt with both retail and wholesale lending (though the latter

ceased in 1994). K-REP Bank’s financial division generated income through interest rate earnings, which was ploughed back to the programme. K-REP Bank’s goal was not to maximize profits but to ensure sustainability.

(ii) The research and evaluation department monitored the performance of the credit programme providing recommendations and policies. Research was conducted to deeply understand the small and micro-enterprises’ operations, and the results were used to expand the programme. Consulting services involved extending advisory services to other organizations interested in designing, implementing and researching micro-enterprise related development activities. The popularity and growth of consulting services stemmed from the wealth of experience that K-REP Bank had gathered over many years.

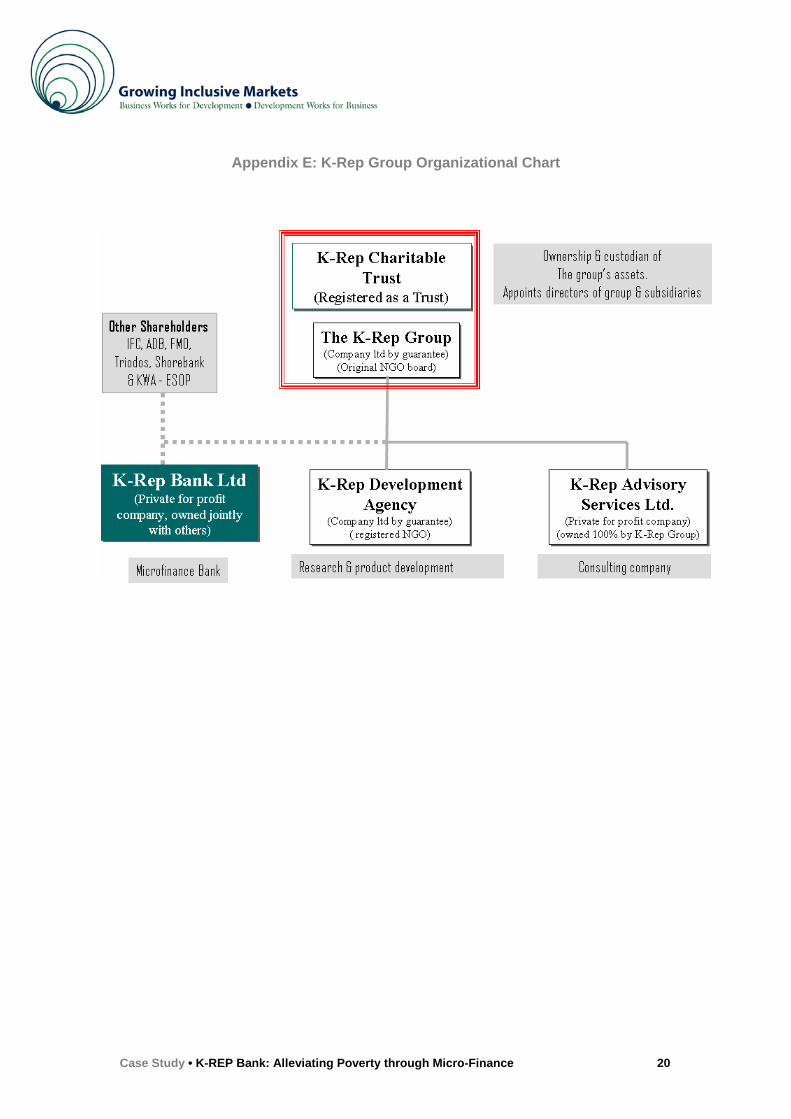

The financial division has emerged as K-REP Bank Limited, the first micro-finance bank in Kenya. The non-financial services division has evolved into two entities namely K-REP Bank Development Agency and K-REP Bank Advisory Services Limited. All three entities are run under one umbrella organisation known as the K-REP Bank Group (See Appendix E or the organisation diagram). The activities of the K-REP Bank Development Agency and K-REP Bank Advisory Services are described briefly below.

K-REP Bank Development Agency

A non-profit micro-finance development organization, K-REP Bank Development Agency (KDA) is the research and development arm of the K-REP Bank Group. Its core activities include research, monitoring and evaluating pilot projects, supporting grassroots micro-finance development organizations and disseminating information on micro-finance and micro-enterprise development. KDA also develops new methods of assisting small and micro-enterprise development.

K-REP Bank Advisory Services

This is the consulting and business development arm of the K-REP Bank Group and is incorporated as a for-profit company under the K-REP Bank Group. Together the Bank, the Development Agency, and the Consulting Company strive towards the attainment of the overall mission of the K-REP Bank Group: "To empower low-income people, promote their participation in the development process and enhance their quality of life."

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 16

Appendix B: Map Showing K-REP Bank’s Branch Network

Source: K-REP Bank

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 17

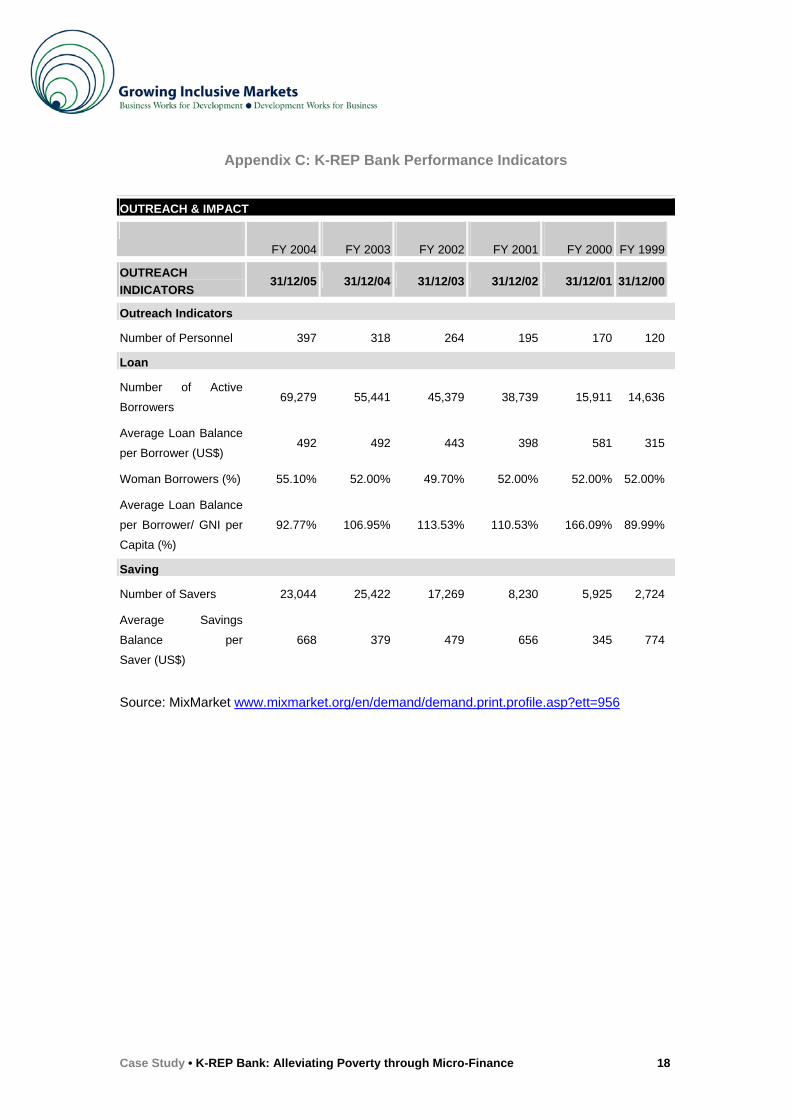

Appendix C: K-REP Bank Performance Indicators

OUTREACH & IMPACT

FY 2004 FY 2003 FY 2002 FY 2001

FY 2000 FY 1999

OUTREACH INDICATORS

31/12/05 31/12/04 31/12/03 31/12/02 31/12/01 31/12/00

Outreach Indicators

Number of Personnel 397 318 264 195 170 120

Loan

Number of Active

Borrowers

69,279 55,441 45,379 38,739 15,911 14,636

Average Loan Balance

per Borrower (US$)

492 492 443 398 581 315

Woman Borrowers (%) 55.10% 52.00% 49.70% 52.00% 52.00% 52.00%

Average Loan Balance

per Borrower/ GNI per

Capita (%)

92.77% 106.95% 113.53% 110.53% 166.09% 89.99%

Saving

Number of Savers 23,044 25,422 17,269 8,230 5,925 2,724

Average Savings

Balance per

Saver (US$)

668 379 479 656 345 774

Source: MixMarket www.mixmarket.org/en/demand/demand.print.profile.asp?ett=956

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 18

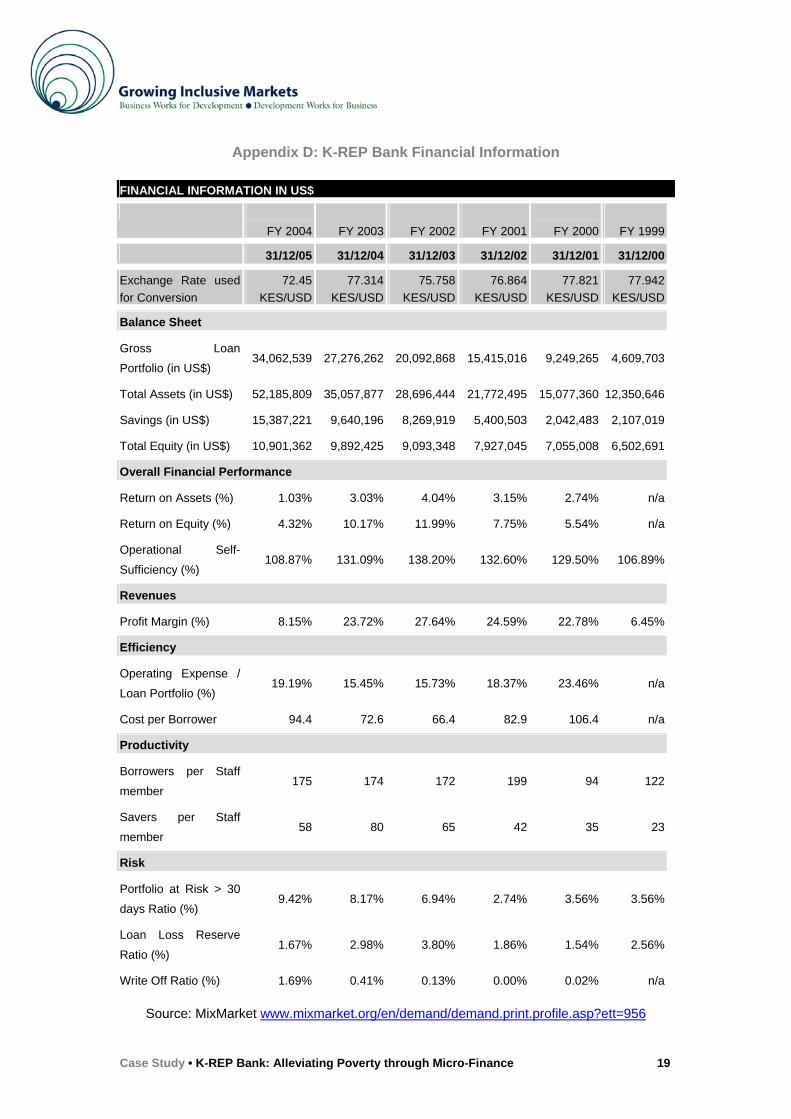

Appendix D: K-REP Bank Financial Information

FINANCIAL INFORMATION IN US$

FY 2004 FY 2003 FY 2002 FY 2001

FY 2000 FY 1999

31/12/05 31/12/04 31/12/03 31/12/02 31/12/01 31/12/00

Exchange Rate used for Conversion

72.45 KES/USD

77.314KES/USD

75.758KES/USD

76.864KES/USD

77.821 KES/USD

77.942KES/USD

Balance Sheet

Gross Loan

Portfolio (in US$) 34,062,539 27,276,262 20,092,868 15,415,016 9,249,265 4,609,703

Total Assets (in US$) 52,185,809 35,057,877 28,696,444 21,772,495 15,077,360 12,350,646

Savings (in US$) 15,387,221 9,640,196 8,269,919 5,400,503 2,042,483 2,107,019

Total Equity (in US$) 10,901,362 9,892,425 9,093,348 7,927,045 7,055,008 6,502,691

Overall Financial Performance

Return on Assets (%) 1.03% 3.03% 4.04% 3.15% 2.74% n/a

Return on Equity (%) 4.32% 10.17% 11.99% 7.75% 5.54% n/a

Operational Self-

Sufficiency (%)

108.87% 131.09% 138.20% 132.60% 129.50% 106.89%

Revenues

Profit Margin (%) 8.15% 23.72% 27.64% 24.59% 22.78% 6.45%

Efficiency

Operating Expense /

Loan Portfolio (%)

19.19% 15.45% 15.73% 18.37% 23.46% n/a

Cost per Borrower 94.4 72.6 66.4 82.9 106.4 n/a

Productivity

Borrowers per Staff

member

175 174 172 199 94 122

Savers per Staff

member

58 80 65 42 35 23

Risk

Portfolio at Risk > 30

days Ratio (%)

9.42% 8.17% 6.94% 2.74% 3.56% 3.56%

Loan Loss Reserve

Ratio (%)

1.67% 2.98% 3.80% 1.86% 1.54% 2.56%

Write Off Ratio (%) 1.69% 0.41% 0.13% 0.00% 0.02% n/a

Source: MixMarket www.mixmarket.org/en/demand/demand.print.profile.asp?ett=956

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 19

Appendix E: K-Rep Group Organizational Chart

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 20

September 2007 The information presented in this case study has been reviewed and signed-off by the company to ensure its accuracy. The views expressed in the case study are the ones of the author and do not necessarily reflect those of the UN, UNDP or their Member States. Copyright @ 2007 United Nations Development Programme All rights reserved. No part of this document may be reproduced, stored in a retrieval system or transmitted, in any form by any means, electronic, mechanical, photocopying or otherwise, without prior permission of UNDP. Design: Suazion, Inc. (N, USA) For more information on Growing Inclusive Markets: www.growinginclusivemarkets.org or [email protected] United Nations Development Programme Private Sector Division, Partnerships Bureau One United Nations Plaza, 23rd floor New York, NY 10017, USA

Case Study • K-REP Bank: Alleviating Poverty through Micro-Finance 21