Embed Size (px)

Citation preview

Page 1 | November 6, 2014 Page 1

November 6, 2014

Press Presentation

Q3 2014

Page 2 | November 6, 2014 Page 2

At a Glance

Q3 2014

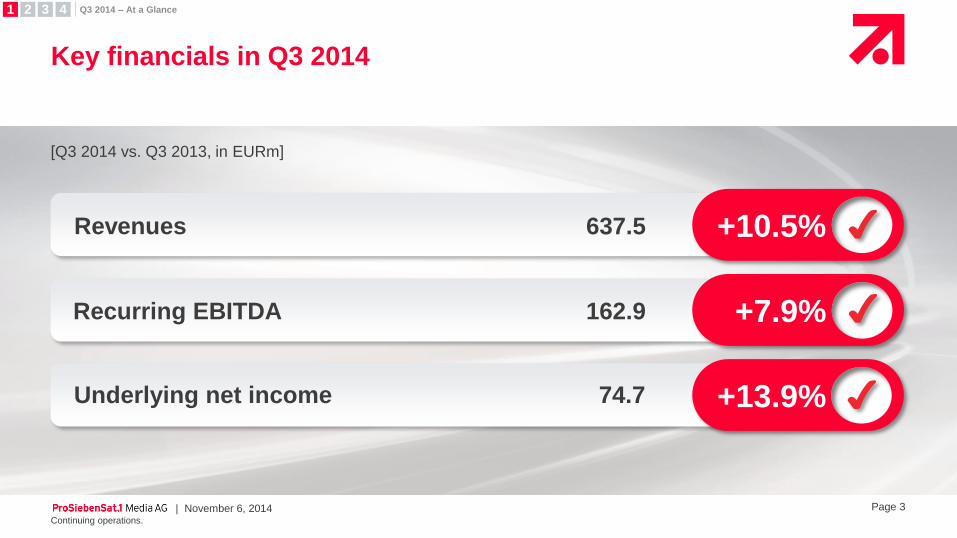

Page 3 | November 6, 2014

Key financials in Q3 2014

[Q3 2014 vs. Q3 2013, in EURm]

Revenues

Recurring EBITDA

Underlying net income

Continuing operations.

637.5

162.9

74.7

1 2 3 4 Q3 2014 – At a Glance

+10.5% ✔

+7.9% ✔

+13.9% ✔

Page 4 | November 6, 2014

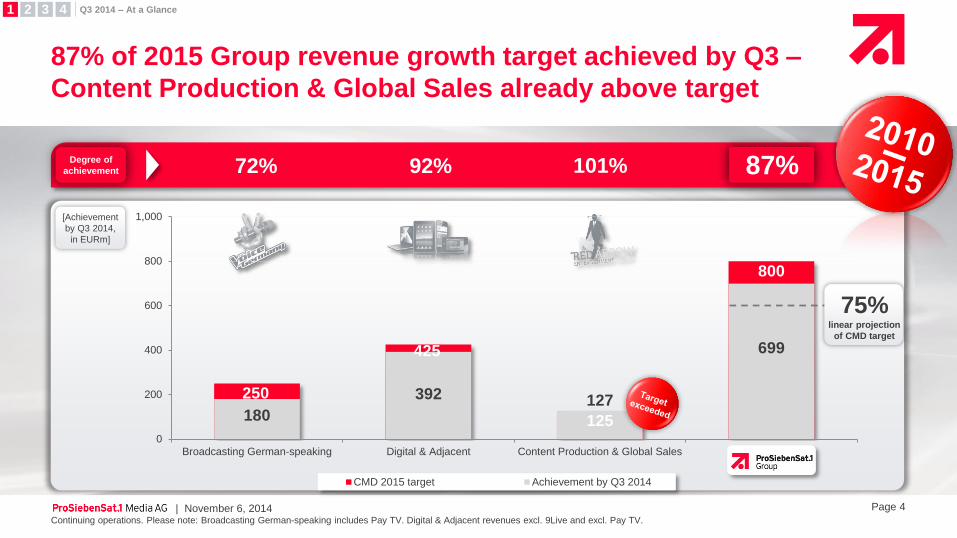

87% of 2015 Group revenue growth target achieved by Q3 –

Content Production & Global Sales already above target

1 2 3 4 Q3 2014 – At a Glance

Continuing operations. Please note: Broadcasting German-speaking includes Pay TV. Digital & Adjacent revenues excl. 9Live and excl. Pay TV.

[Achievement

by Q3 2014,

in EURm]

72% 101% 92% Degree of

achievement 87%

250

425

125

800

180

392 127

699

0

200

400

600

800

1,000

Broadcasting German-speaking Digital & Adjacent Content Production & Global Sales Group

CMD 2015 target Achievement by Q3 2014

linear projection

of CMD target

75%

Page 5 | November 6, 2014

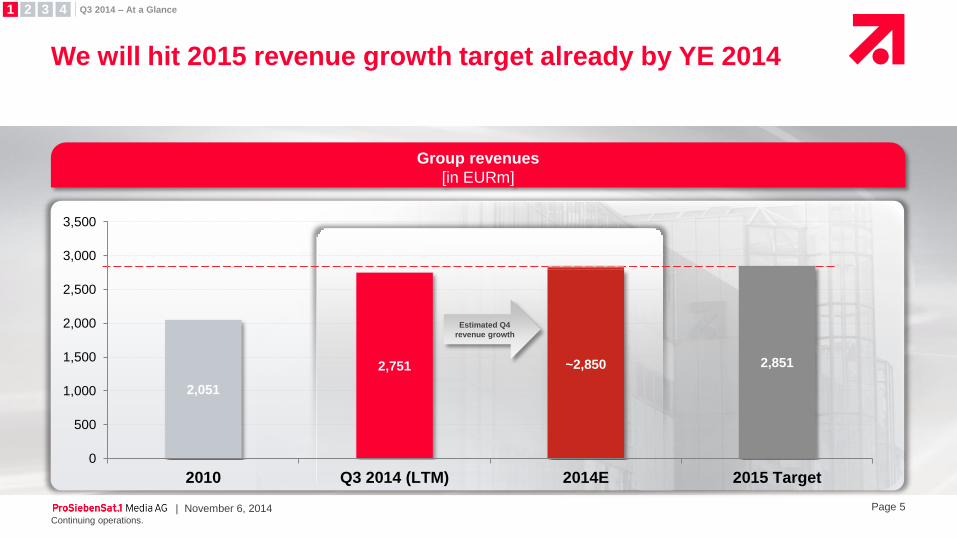

We will hit 2015 revenue growth target already by YE 2014

Continuing operations.

1 2 3 4 Q3 2014 – At a Glance

Group revenues

[in EURm]

~2,850

2,051

2,751 2,851

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2010 Q3 2014 (LTM) 2014E 2015 Target

Estimated Q4

revenue growth

Page 6 | November 6, 2014

Already 39% of our 2018 revenue growth target achieved

Continuing operations.

300

600

100

1,000

120 229

45

394

0

200

400

600

800

1,000

Broadcasting German-speaking Digital & Adjacent Content Production & Global Sales Group

CMD 2018 target Achievement by Q3 2014

1 2 3 4 Q3 2014 – At a Glance

39% 40% 45% 38%

29% linear projection

of CMD target

[Achievement

by Q3 2014,

in EURm]

Degree of

achievement

Page 7 | November 6, 2014

Q3/9M 2014 Financial Performance

Review

Page 8 | November 6, 2014

0

200

400

600

800

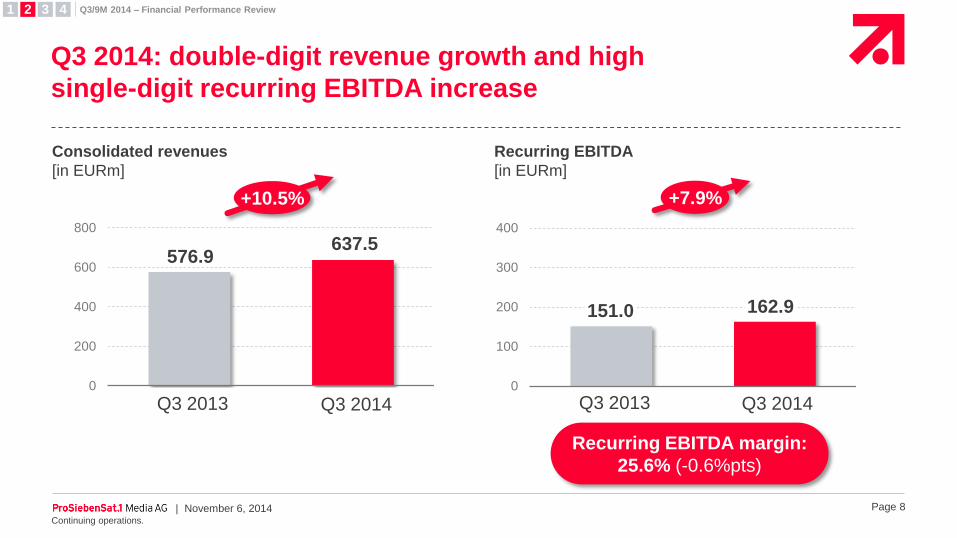

Continuing operations.

637.5 576.9

0

100

200

300

400

162.9 151.0

+10.5% +7.9%

Consolidated revenues

[in EURm]

Recurring EBITDA

[in EURm]

Q3 2014 Q3 2013 Q3 2014 Q3 2013

Recurring EBITDA margin:

25.6% (-0.6%pts)

1 2 3 4 Q3/9M 2014 – Financial Performance Review

Q3 2014: double-digit revenue growth and high

single-digit recurring EBITDA increase

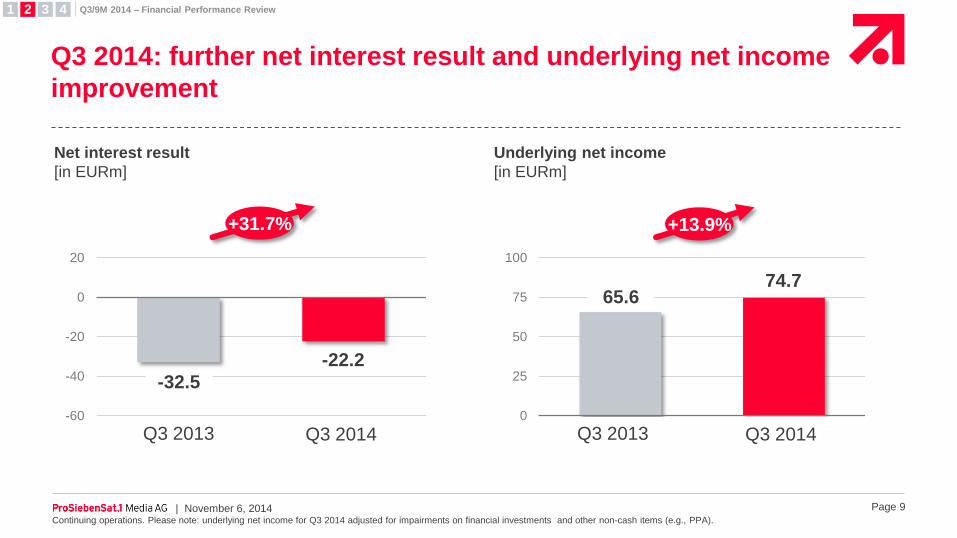

Page 9 | November 6, 2014 Continuing operations. Please note: underlying net income for Q3 2014 adjusted for impairments on financial investments and other non-cash items (e.g., PPA).

1 2 3 4 Q3/9M 2014 – Financial Performance Review

Underlying net income

[in EURm]

0

25

50

75

100

74.7 65.6

+13.9%

Q3 2014 Q3 2013 -60

-40

-20

0

20

-22.2

-32.5

+31.7%

Net interest result

[in EURm]

Q3 2014 Q3 2013

Q3 2014: further net interest result and underlying net income

improvement

Page 10 | November 6, 2014

0

400

800

1,200

1,600

2,000

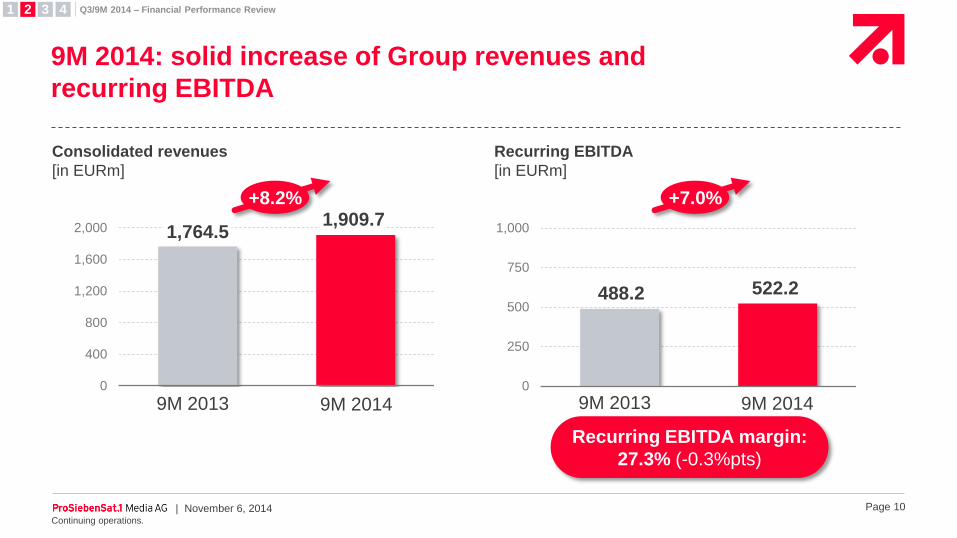

Continuing operations.

1,909.7 1,764.5

0

250

500

750

1,000

522.2 488.2

+7.0%

Consolidated revenues

[in EURm]

Recurring EBITDA

[in EURm]

9M 2014 9M 2013 9M 2014 9M 2013

Recurring EBITDA margin:

27.3% (-0.3%pts)

+8.2%

9M 2014: solid increase of Group revenues and

recurring EBITDA

1 2 3 4 Q3/9M 2014 – Financial Performance Review

Page 11 | November 6, 2014 Continuing operations.

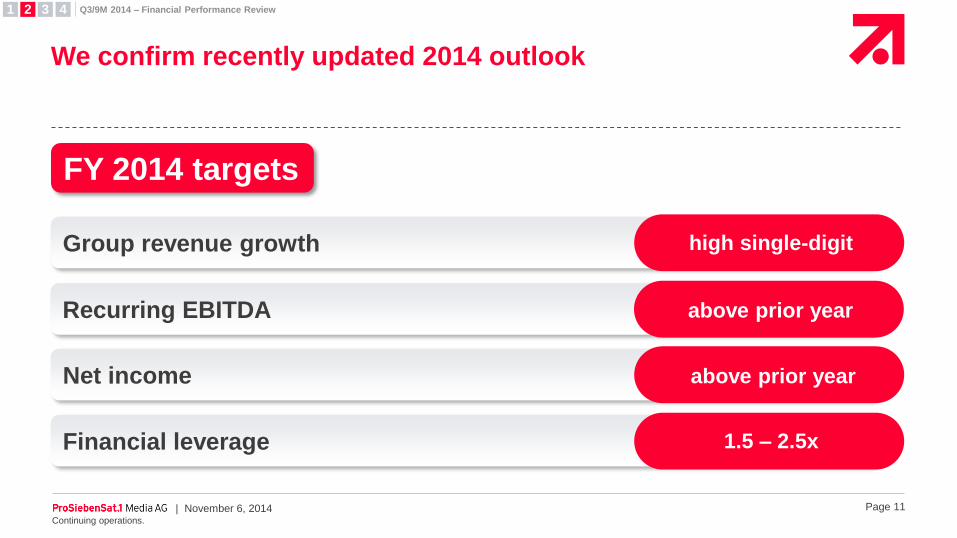

Financial leverage

Net income

Recurring EBITDA

Group revenue growth

FY 2014 targets

high single-digit

above prior year

above prior year

1.5 – 2.5x

We confirm recently updated 2014 outlook

1 2 3 4 Q3/9M 2014 – Financial Performance Review

Page 12 | November 6, 2014

Broadcasting

German-speaking

Page 13 | November 6, 2014

Viewer share growth in Germany and Austria

Switzerland

Austria

Germany

Q3 2013 Q3 2014

18.4%

28.5%

21.3%

17.7%

29.3%

22.1%

Basis for GER: All German TV households (Germany + EU), A 14-49 years; Mon-Sun, 3-3 h. Source: AGF in cooperation with GfK / TV Scope / ProSiebenSat.1 TV Deutschland Strategy & Operations. Basis for CH: D-CH, A 15-49;

Source: Mediapulse TV-Panel, D-CH, A 15-49. Basis for A: Austrian channels S1, P7, k1, PULS 4, sixx (from Jul 3, 2012, onwards) and P7 MAXX and S1 Gold Austria (both from Jul 15, 2014, onwards). Figures for A are based on 24 hours in key demographics (Mon-Sun).

1 2 3 4 Broadcasting German-speaking / TV Performance

Audience shares

Page 14 | November 6, 2014

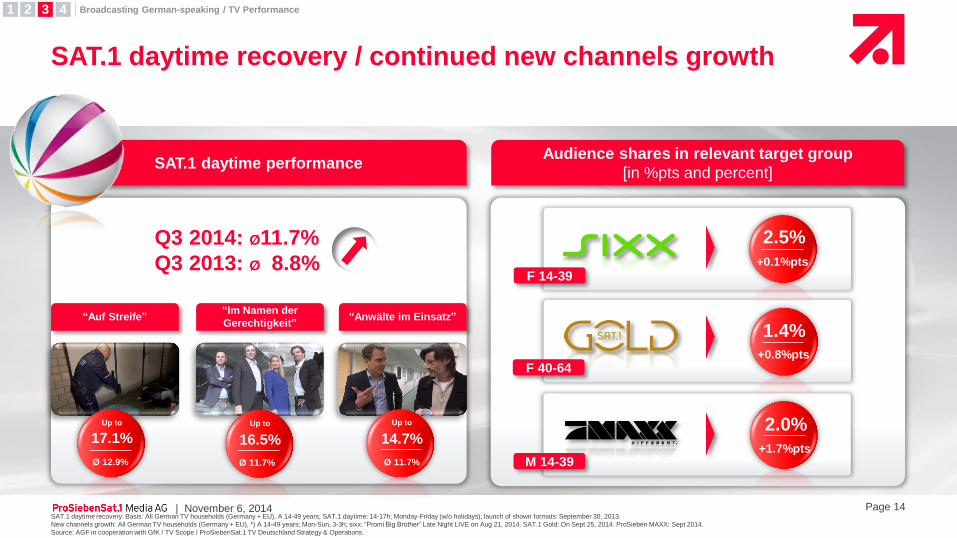

SAT.1 daytime recovery / continued new channels growth

1 2 3 4 Broadcasting German-speaking / TV Performance

SAT.1 daytime performance Audience shares in relevant target group

[in %pts and percent]

Q3 2014: Ø11.7%

Q3 2013: Ø 8.8%

“Auf Streife” “Im Namen der

Gerechtigkeit” “Anwälte im Einsatz”

17.1%

Up to

Ø 12.9%

16.5%

Up to

Ø 11.7%

14.7%

Up to

Ø 11.7%

F 40-64

M 14-39

F 14-39

2.5%

+0.1%pts

1.4% +0.8%pts

2.0%

+1.7%pts

SAT.1 daytime recovery: Basis: All German TV households (Germany + EU), A 14-49 years; SAT.1 daytime: 14-17h; Monday-Friday (w/o holidays); launch of shown formats: September 30, 2013.

New channels growth: All German TV households (Germany + EU), *) A 14-49 years; Mon-Sun, 3-3h; sixx: “Promi Big Brother“ Late Night LIVE on Aug 21, 2014. SAT.1 Gold: On Sept 25, 2014. ProSieben MAXX: Sept 2014.

Source: AGF in cooperation with GfK / TV Scope / ProSiebenSat.1 TV Deutschland Strategy & Operations.

Page 15 | November 6, 2014

Continued leading ad share positions

Switzerland

Austria

Germany

Q3 2013 Q3 2014

26.2%

43.9%

24.4%

43.8%

P7S1 gross TV advertising market share

[in percent]

1 2 3 4 Broadcasting German-speaking / Ad Market Performance

33.4% 36.7%

Source: Nielsen Media Research (Germany), Focus Media (Switzerland, Austria): Jul-Sep 2014 vs Jul-Sep 2013.

Page 16 | November 6, 2014

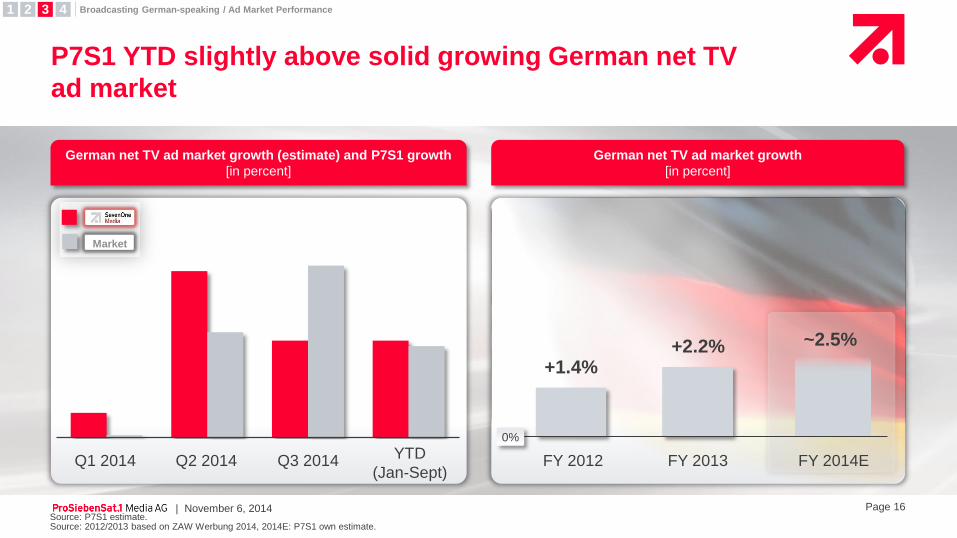

P7S1 YTD slightly above solid growing German net TV

ad market

German net TV ad market growth (estimate) and P7S1 growth

[in percent]

German net TV ad market growth

[in percent]

1 2 3 4 Broadcasting German-speaking / Ad Market Performance

Market

Q1 2014 Q3 2014 Q2 2014 YTD

(Jan-Sept) FY 2012 FY 2013

+2.2% +1.4%

FY 2014E

~2.5%

Source: P7S1 estimate. Source: 2012/2013 based on ZAW Werbung 2014, 2014E: P7S1 own estimate.

0%

Page 17 | November 6, 2014

Continued strong growth of P7S1 HD subscriber base

+30%

5.1m subscribers

in Q3 2014

HD subscriber growth

[Q1 2012 – Q3 2014; in m]

P7S1 HD FTA

subscriber growth [Q3 2014 vs. Q3 2013; Germany]

Note: Paying subscriber figures as reported by platform partners (EoP; subject to subsequent adjustments by the partners).

1 2 3 4 Broadcasting German-speaking / Distribution

1.2

1.8

2.3

2.8

3.3

3.7 3.9

4.2 4.6

4.8 5.1

Q1

2014

Q1

2012

Q1

2013

Q2

2012

Q3

2012

Q3

2014

Q2

2014

Q3

2013

Q4

2013

Q4

2012

Q2

2013

Page 18 | November 6, 2014

New platform partnerships driving reach of our assets

1 2 3 4 Broadcasting German-speaking / Distribution

HD+ partnership

Further extension

of HD+ partnership

7TV app

7TV catch-up content

available through Google

chromecast

MyVideo

Exclusive MyVideo content

pre-installed on Smart TVs of

market leader Samsung

Switzerland

ProSieben FUN and

kabel eins CLASSICS

now available in Switzerland

Free-to-air, Pay TV & VoD

* Based on UPC Cablecom Q2 2014 Report. ** Based on total base of Samsung Smart TV sets in Germany, 2013.

5m Samsung Smart TV population **

Page 19 | November 6, 2014

Digital & Adjacent

Page 20 | November 6, 2014

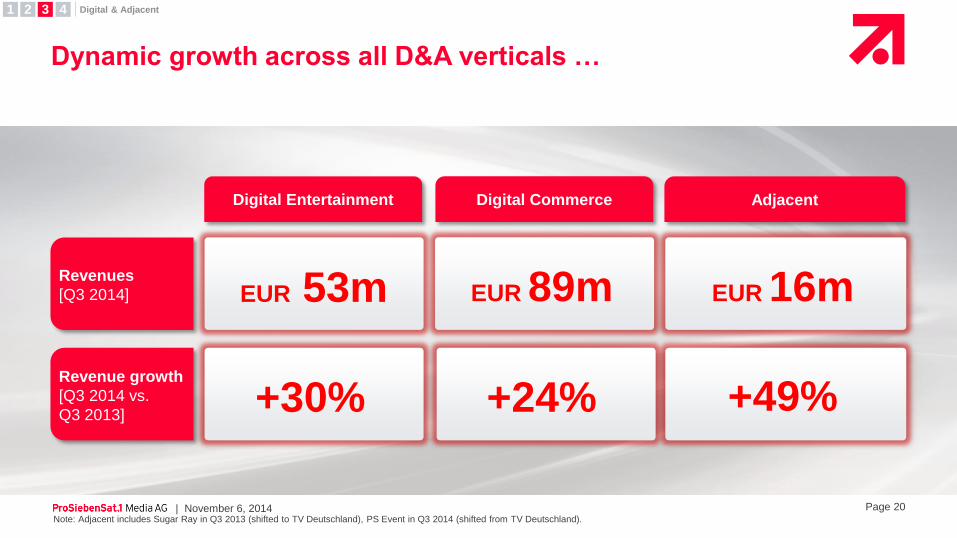

Dynamic growth across all D&A verticals …

Digital Commerce Adjacent Digital Entertainment

EUR 89m EUR 53m EUR 16m Revenues

[Q3 2014]

Revenue growth

[Q3 2014 vs.

Q3 2013] +30% +49% +24%

1 2 3 4 Digital & Adjacent

Note: Adjacent includes Sugar Ray in Q3 2013 (shifted to TV Deutschland), PS Event in Q3 2014 (shifted from TV Deutschland).

Page 21 | November 6, 2014

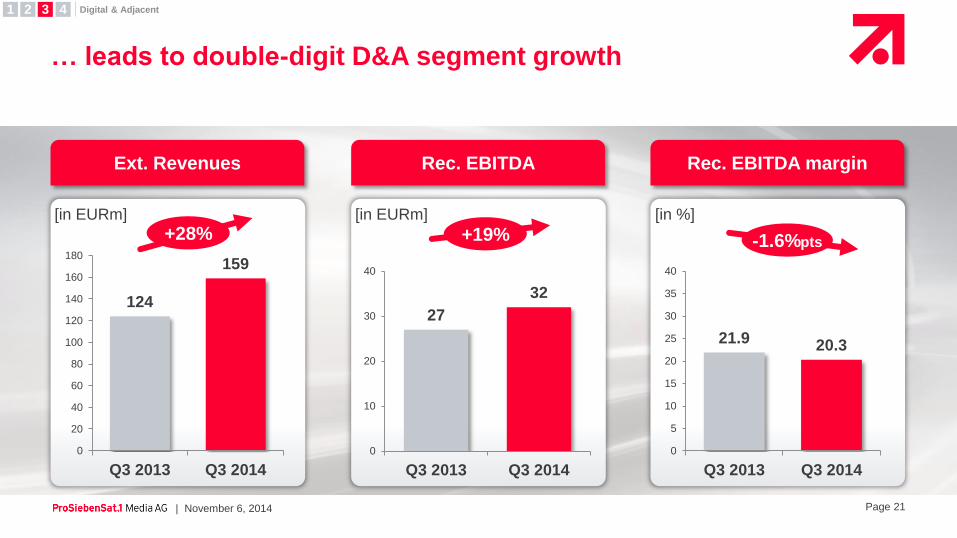

… leads to double-digit D&A segment growth

1 2 3 4 Digital & Adjacent

Ext. Revenues Rec. EBITDA Rec. EBITDA margin

+28% +19% [in EURm] [in EURm] [in %]

-1.6%pts

124

159

0

20

40

60

80

100

120

140

160

180

Q3 2013 Q3 2014

27

32

0

10

20

30

40

Q3 2013 Q3 2014

21.9 20.3

0

5

10

15

20

25

30

35

40

Q3 2013 Q3 2014

Page 22 | November 6, 2014

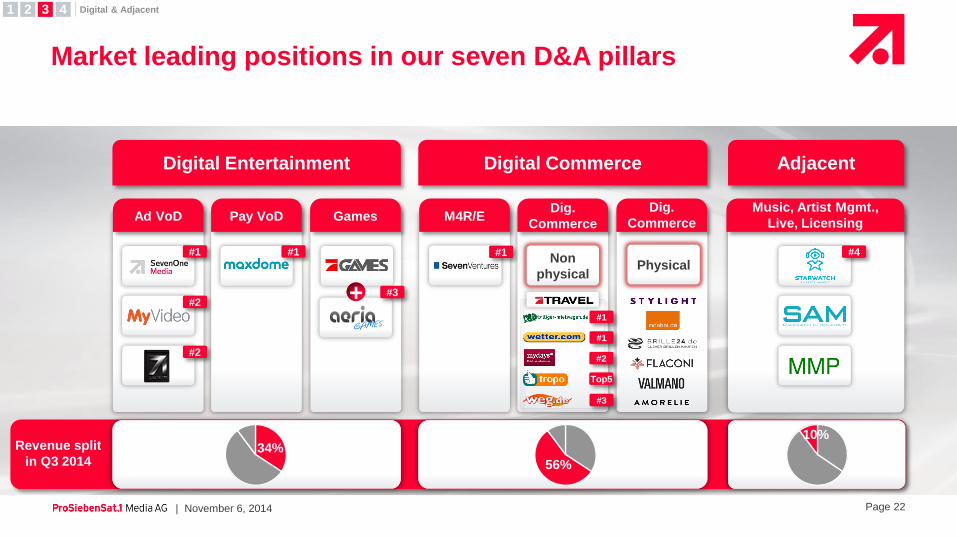

Market leading positions in our seven D&A pillars

Adjacent

Digital Entertainment 1 2 3 4 Digital & Adjacent

Digital Entertainment Digital Commerce Adjacent

Ad VoD Pay VoD Games M4R/E Dig.

Commerce

Dig.

Commerce

Music, Artist Mgmt.,

Live, Licensing

Non

physical

+

Physical

#3

#1 #1 #1

#2

#2

Revenue split

in Q3 2014 34%

56%

10%

#4

#3

#1

#2

#1

Top5

Page 23 | November 6, 2014

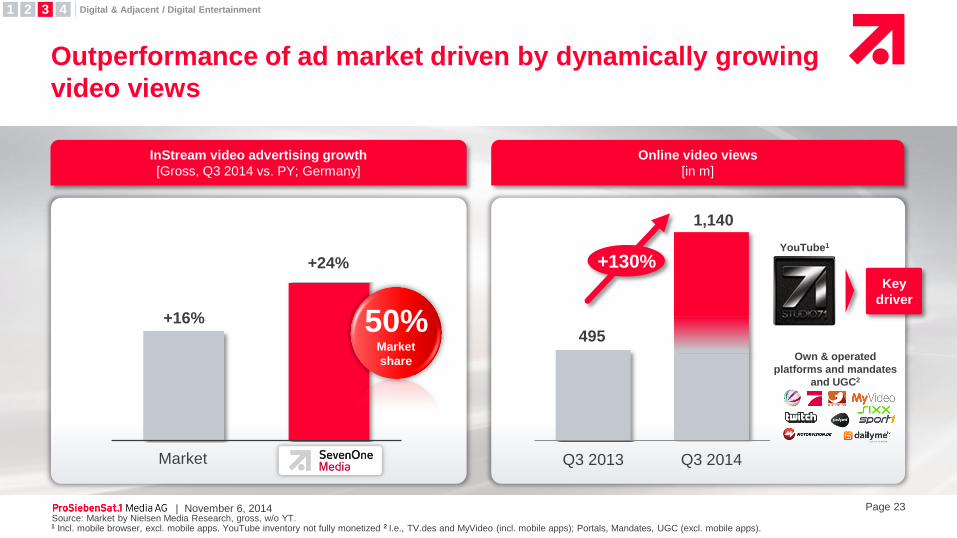

Outperformance of ad market driven by dynamically growing

video views

InStream video advertising growth

[Gross, Q3 2014 vs. PY; Germany]

Online video views

[in m]

1 2 3 4 Digital & Adjacent / Digital Entertainment

+16%

+24%

Market

50% Market

share

495

1,140

Q3 2013 Q3 2014

+130%

Own & operated

platforms and mandates

and UGC2

YouTube1

Key

driver

Source: Market by Nielsen Media Research, gross, w/o YT. 1 Incl. mobile browser, excl. mobile apps. YouTube inventory not fully monetized 2 I.e., TV.des and MyVideo (incl. mobile apps); Portals, Mandates, UGC (excl. mobile apps).

Page 24 | November 6, 2014

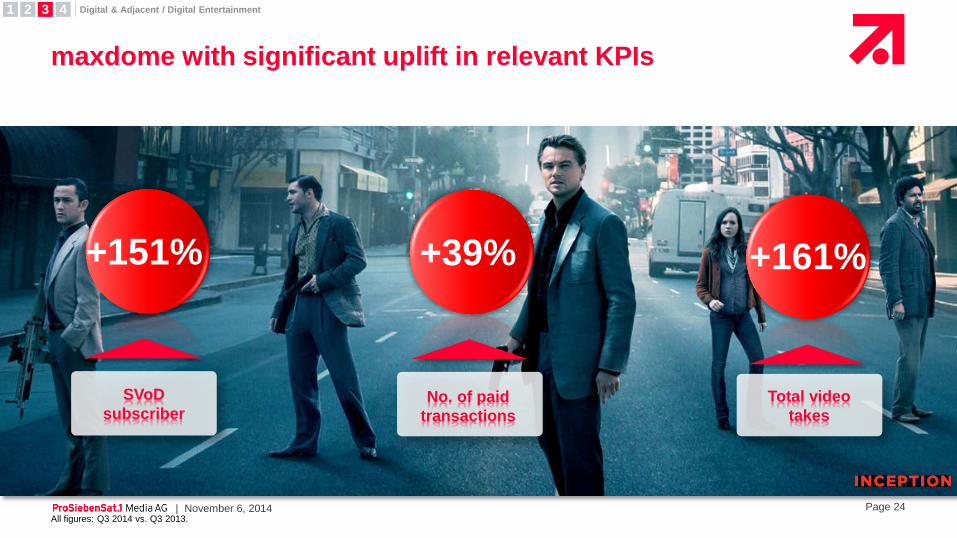

maxdome with significant uplift in relevant KPIs

+39%

No. of paid

transactions

Total video

takes

+161% +151%

SVoD

subscriber

All figures: Q3 2014 vs. Q3 2013.

1 2 3 4 Digital & Adjacent / Digital Entertainment

Page 25 | November 6, 2014 All figures: 26 August - 15 September 2014 vs. 16 September - 06 October 2014.

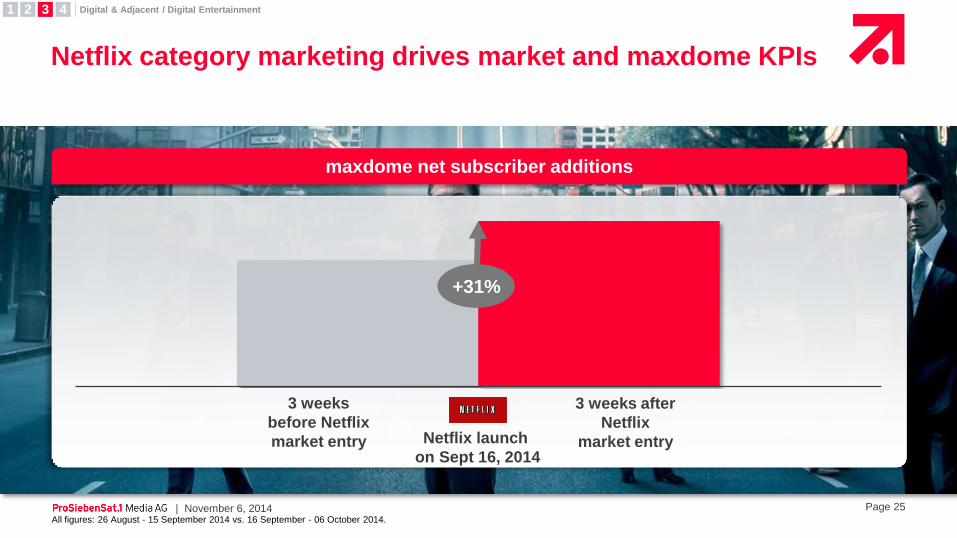

Netflix category marketing drives market and maxdome KPIs

1 2 3 4 Digital & Adjacent / Digital Entertainment

3 weeks after

Netflix

market entry

3 weeks

before Netflix

market entry

maxdome net subscriber additions

Netflix launch

on Sept 16, 2014

+31%

Page 26 | November 6, 2014

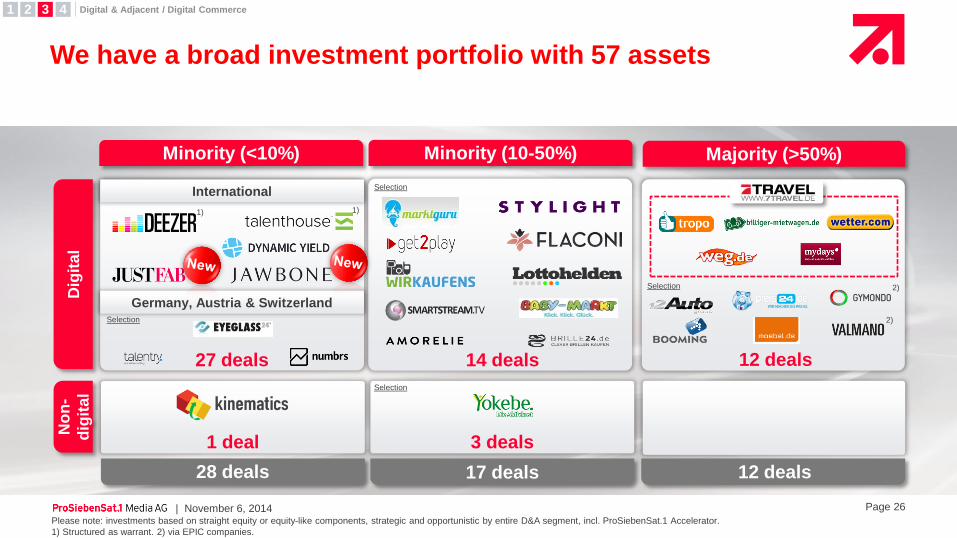

We have a broad investment portfolio with 57 assets

1 2 3 4 Digital & Adjacent / Digital Commerce

Please note: investments based on straight equity or equity-like components, strategic and opportunistic by entire D&A segment, incl. ProSiebenSat.1 Accelerator.

1) Structured as warrant. 2) via EPIC companies.

Minority (10-50%) Majority (>50%) Minority (<10%)

28 deals 12 deals

27 deals 14 deals 12 deals

1 deal 3 deals

Selection International

1)

Germany, Austria & Switzerland Selection

17 deals

Dig

ital

No

n-

dig

ital

Selection

1)

Selection

2)

2)

Page 27 | November 6, 2014

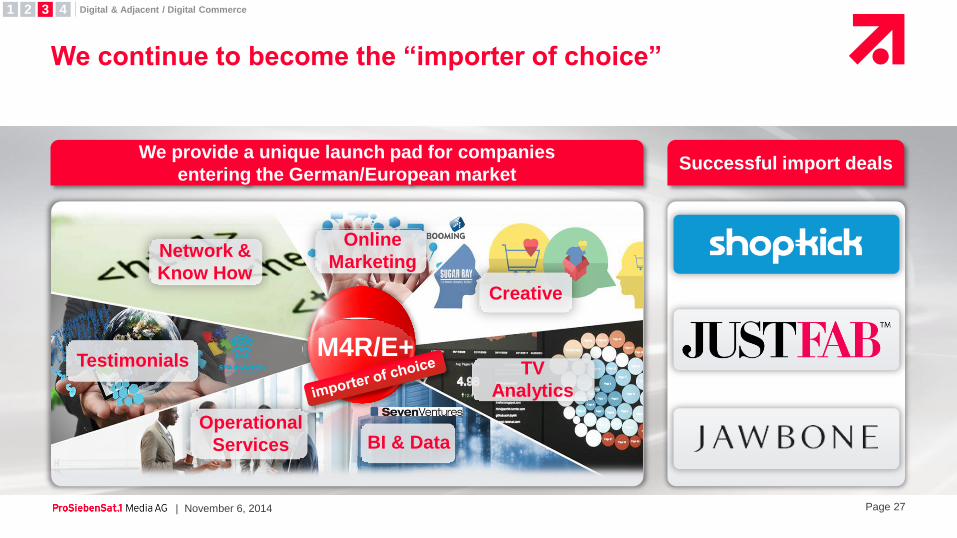

We continue to become the “importer of choice”

1 2 3 4 Digital & Adjacent / Digital Commerce

We provide a unique launch pad for companies

entering the German/European market

M4R/E+

Network &

Know How

Testimonials TV

Analytics

Creative

BI & Data

Online

Marketing

Operational

Services

Successful import deals

Page 28 | November 6, 2014

Key travel assets benefit from strong value-add of P7S1

1 Overall market growth through mydays success. 2 mydays: 2010-2012; weg.de: 2012-2013 (FC). 3 mydays: 2012-2014 (FC); weg.de: 2013-2014 (FC).

Revenue / market CAGR development in % – examples mydays and weg.de

8 2

201

5 2 4

19

29

We add value through

• Media

• Cash

• Shared services

• Knowledge sharing

• Data analytics

• Technology

Market CAGR

mydays/weg.de CAGR After P7S1 entry3 Pre P7S1 entry2

1 2 3 4 Digital & Adjacent / Digital Commerce

Page 29 | November 6, 2014

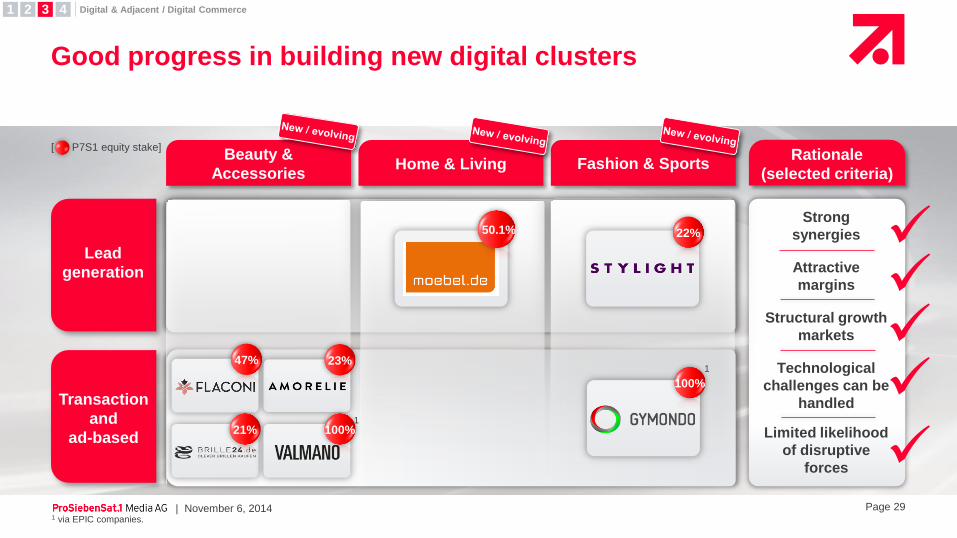

Good progress in building new digital clusters

Fashion & Sports Beauty &

Accessories Home & Living

1 via EPIC companies.

Lead

generation

Transaction

and

ad-based

[ P7S1 equity stake]

47% 23%

21%

50.1%

100% 1

100%

1

22%

Strong

synergies

Attractive

margins

Structural growth

markets

Technological

challenges can be

handled

Limited likelihood

of disruptive

forces

Rationale

(selected criteria)

1 2 3 4 Digital & Adjacent / Digital Commerce

Page 30 | November 6, 2014

Content Production &

Global Sales

Page 31 | November 6, 2014

Q3 on-air successes and re-commissions

Married at First Sight:

THE FIRST YEAR

Spinn-off

commis-

sioned

Sold to 50+

territories in

Latin

America

Sold to

the USA

1 2 3 4 Content Production & Global Sales

Season 2

commis-

sioned

Page 32 | November 6, 2014

Upcoming US format highlights

1 2 3 4 Content Production & Global Sales

“Escape Your Life”

Extreme social experiment

where 4 couples opt to

change their lives forever

“Lost in Love”

An epic worldwide search

for lost loves – that one

person who got away

“Curvy Brides”

Bridal salon owners Yukia

and Yuneisia help curvy

brides find the gown of

their dreams

“Midnight Feast”

Competitive cooking event

set in a food hall after-

hours

Producer:

HALF YARD Productions

Producer:

NERD

Producer:

NERD

Producer:

Kinetic Content

| November 6, 2014 Page 33

Summary & Outlook

| November 6, 2014 Page 34

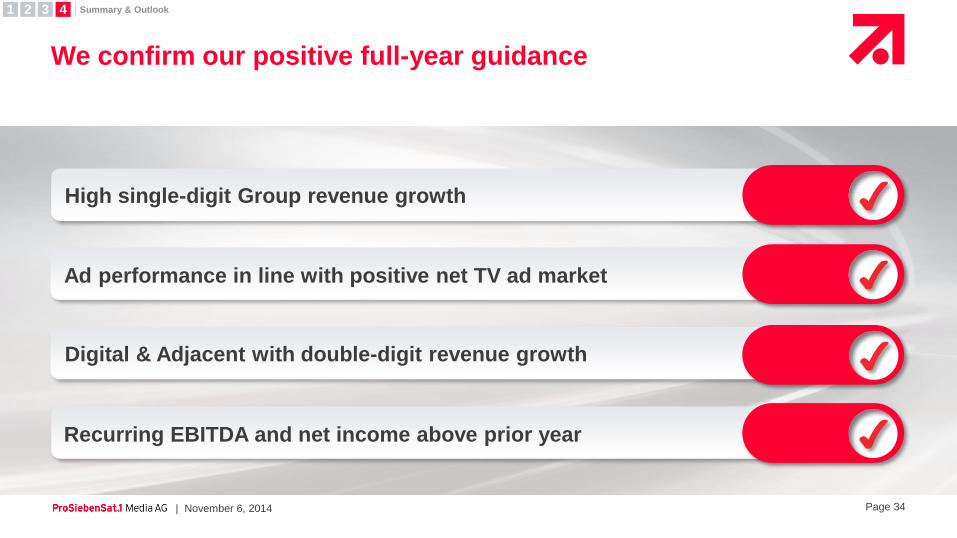

We confirm our positive full-year guidance

1 2 3 4 Summary & Outlook

Ad performance in line with positive net TV ad market ✔

✔

✔

Digital & Adjacent with double-digit revenue growth

High single-digit Group revenue growth

Recurring EBITDA and net income above prior year ✔

| November 6, 2014 Page 35

Disclaimer

This presentation contains "forward-looking statements" regarding ProSiebenSat.1 Media AG ("ProSiebenSat.1") or ProSiebenSat.1 Group, including opinions, estimates and projections regarding ProSiebenSat.1's or ProSiebenSat.1 Group's financial position, business strategy, plans and objectives of management and future operations. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause the actual results, performance or achievements of ProSiebenSat.1 or ProSiebenSat.1 Group to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements. These forward-looking statements speak only as of the date of this presentation and are based on numerous assumptions which may or may not prove to be correct.

No representation or warranty, expressed or implied, is made by ProSiebenSat.1 with respect to the fairness, completeness, correctness, reasonableness or accuracy of any information and opinions contained herein. The information in this presentation is subject to change without notice, it may be incomplete or condensed, and it may not contain all material information concerning ProSiebenSat.1 or ProSiebenSat.1 Group. ProSiebenSat.1 undertakes no obligation to publicly update or revise any forward-looking statements or other information stated herein, whether as a result of new information, future events or otherwise.

| November 6, 2014 Page 36