Embed Size (px)

Citation preview

STUDY ON AUSTRALIAN SPACE CAPABILITIES AND GLOBAL SUPPLY CHAINS

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 2 of 111

CONTENTS

1 Executive Summary ..................................................................................... 7

Background and Context of Study .......................................................................................................... 7

The Changing Global Space Economy ..................................................................................................... 7

Scope of Study ........................................................................................................................................ 9

Methodology ........................................................................................................................................... 9

Space Capability of Companies Interviewed ........................................................................................... 9

Character of Business Type of Companies Interviewed ....................................................................... 10

Industry Sectors Served by Australian Space Capabilities .................................................................... 11

Revenue Generated by Australian Space Activities .............................................................................. 11

Workforce Size Involved in Australian Space Activities ........................................................................ 11

Staff Demographics of Workforce Involved in Australian Space Activities .......................................... 11

Business Trends Identified By Companies Interviewed ........................................................................ 12

Current Australian Space Capabilities ................................................................................................... 12

Domestic and International Supply Chains ........................................................................................... 15

Supply Chain Opportunities for Australia ............................................................................................. 15

Regional Markets .......................................................................................................................... 16

New Space Markets ...................................................................................................................... 16

Key Issues for Australian Participation in Global Supply Chains ................................................... 16

Growth Opportunities in Space Applications Markets ......................................................................... 17

Conclusion ............................................................................................................................................. 18

2 Background and Context of Study ............................................................. 19

3 The Changing Global Space Economy ........................................................ 20

3.1 The Changing Face of Global Space Activity ................................................................................... 21

3.2 Evolutionary Phases of Global Space Activity ................................................................................. 21

3.3 The Growing Global Space Economy .............................................................................................. 22

3.4 The Changing Nature of Space Activity ........................................................................................... 23

3.5 The ‘New Space’ Era ........................................................................................................................ 27

4 Selective Review of Australian Companies Involved in Space .................... 29

4.1 Scope of Study................................................................................................................................. 30

4.2 Methodology ................................................................................................................................... 30

4.3 Overview of Companies Interviewed .............................................................................................. 32

4.3.1 Geographic Dispersion of Companies Interviewed .............................................................. 32

4.3.2 Categories of Space Capability of Companies Interviewed ................................................. 32

4.3.3 Character of Business Type of Companies Interviewed....................................................... 36

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 3 of 111

4.4 Industry Sectors Served by Australian Space Capabilities .............................................................. 38

4.5 Revenue Generated by Australian Space Activities ........................................................................ 40

4.5.1 Overall Revenue Generated by Australian Space Activities ................................................. 40

4.5.2 Export Revenue Generated From Australian Space Activities ............................................. 41

4.6 Workforce Size Involved in Australian Space Activities .................................................................. 42

4.7 Staff Demographics of Workforce Involved in Australian Space Activities .................................... 43

4.8 Business Trends Identified By Companies Interviewed .................................................................. 48

5 An Overview of Current Australian Space Capabilities ............................... 55

5.1 Defining Space Capabilities ............................................................................................................. 56

5.2 Classification of Space Capabilities ................................................................................................. 56

5.3 The Breadth of Australian Companies’ Space Capabilities ............................................................. 59

5.3.1 Overview of Australian Company’s Space Capabilities ........................................................ 59

6 Domestic and International Supply Chains ................................................ 79

6.1 Background and Definition of Supply Chains .................................................................................. 80

6.2 Where Australian Space Capabilities Map on Global Supply Chains .............................................. 80

6.2.1 Satellite Communications .................................................................................................... 80

6.2.2 Earth Observation ................................................................................................................ 82

6.2.3 Satellite Position Navigation and Timing ............................................................................. 85

7 Supply Chain Opportunities for Australia .................................................. 88

7.1 Opportunities for Australian Companies by Supply Chain Segment .............................................. 89

7.1.1 Supply Chain Opportunities in Satellite Ownership and Operations ................................... 89

7.1.2 Supply Chain Opportunities in the Space Systems Segment ............................................... 89

7.1.3 Supply Chain Opportunities in Launch Systems ................................................................... 90

7.1.4 Supply Chain Opportunities in the Ground Systems Segment ............................................ 91

7.1.5 Supply Chain Opportunities in Space Enabled Services and Applications ........................... 92

7.2 Regional Markets ............................................................................................................................ 99

7.3 New Space Markets ........................................................................................................................ 99

7.4 Key Issues for Australian Participation in Global Supply Chains ................................................... 102

8 Growth Opportunities in Space Applications for Domestic and International Markets ..................................................................................................... 105

8.1 Key Growth Markets in Space Applications .................................................................................. 106

8.1.1 Satellite Communications .................................................................................................. 106

8.1.2 Earth Observation .............................................................................................................. 107

8.1.3 Position Navigation & Timing ............................................................................................. 107

9.0 Conclusion ........................................................................................... 109

Appendix A – Companies Interviewed and Their Space Capabilities ........... 111

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 4 of 111

TABLES

Table 1 Space Capabilities of the 46 Companies Interviewed for this Study........................................ 10

Table 2 Breakdown of Key Subsectors in the Commercial Space Sector .............................................. 26

Table 3 Number of Companies Interviewed by State & Territory ........................................................ 32

Table 4 Number of Companies with Space Capabilities by Segment ................................................... 33

Table 5 Companies with Space Enabled Service Capabilities by Service Domain ................................ 34

Table 6 Interviewed Companies by Business Type ............................................................................... 36

Table 7 ANZSIC Industry Segments Served by Space Capabilities of Interviewed Companies ............. 39

Table 8 Number of Staff by Employee Category ................................................................................... 43

Table 9 Level of Qualification of Staff ................................................................................................... 44

Table 10 Workforce by Age Category ................................................................................................... 46

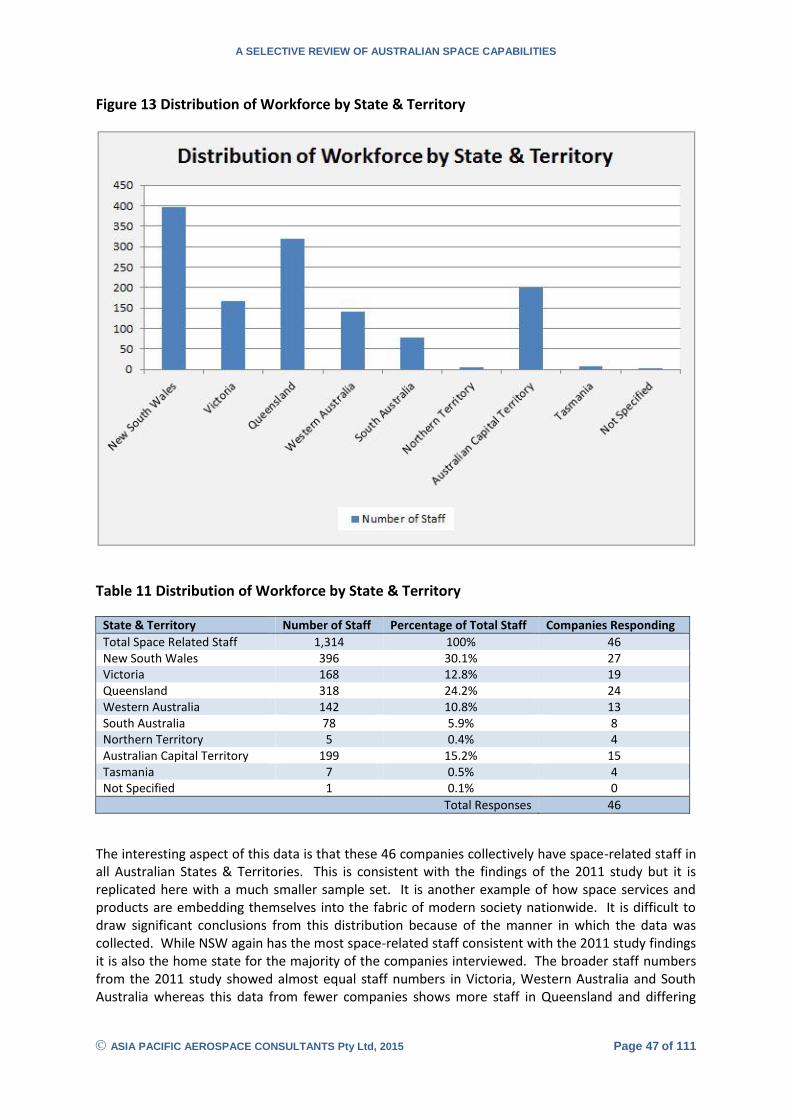

Table 11 Distribution of Workforce by State & Territory ..................................................................... 47

Table 12 Companies Revenue Growth .................................................................................................. 48

Table 13 Companies Export Revenue Growth ...................................................................................... 49

Table 14 Companies Staff Growth ........................................................................................................ 50

Table 15 Companies Highly Skilled Staff Growth .................................................................................. 50

Table 16 Skills Shortages in Australia .................................................................................................... 51

Table 17 Reported Skills Shortages in Australia .................................................................................... 52

Table 18 Countries Supplying Space-Related Skills Staff to Australia ................................................... 53

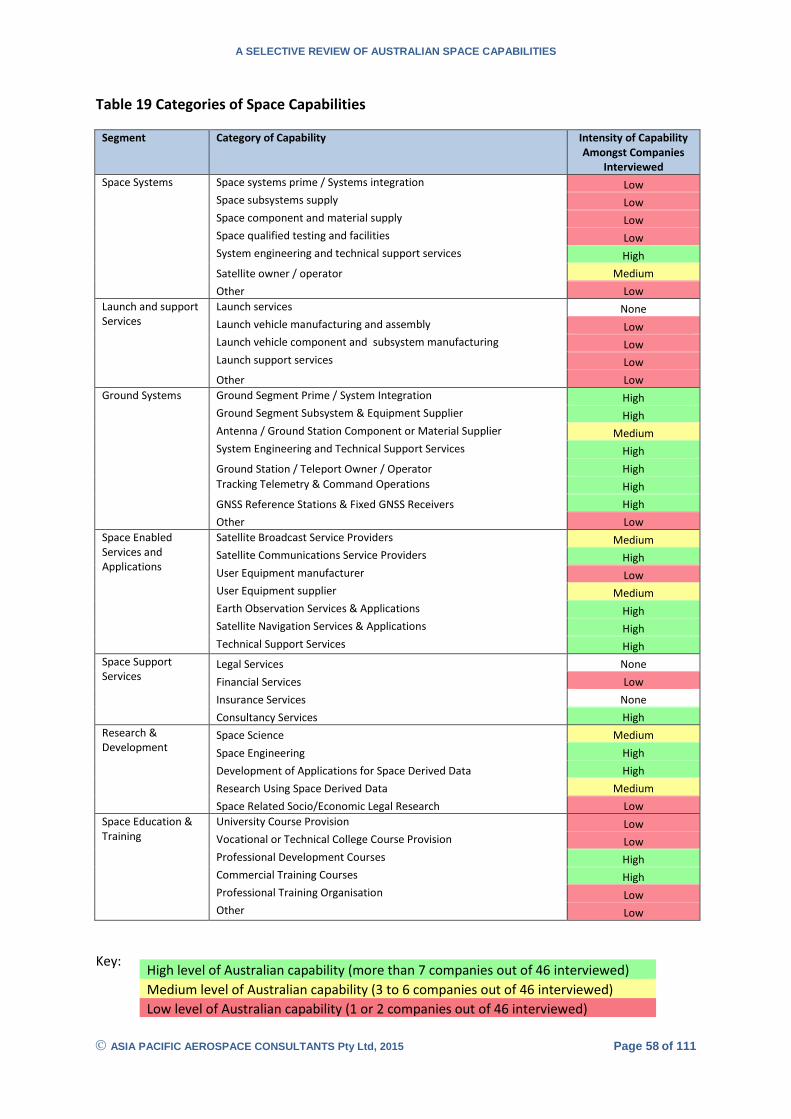

Table 19 Categories of Space Capabilities ............................................................................................ 58

Table 20 Capabilities of Australian Companies in the Space Systems Segment ................................... 60

Table 21 Capabilities of Australian Companies in Launch Systems ...................................................... 63

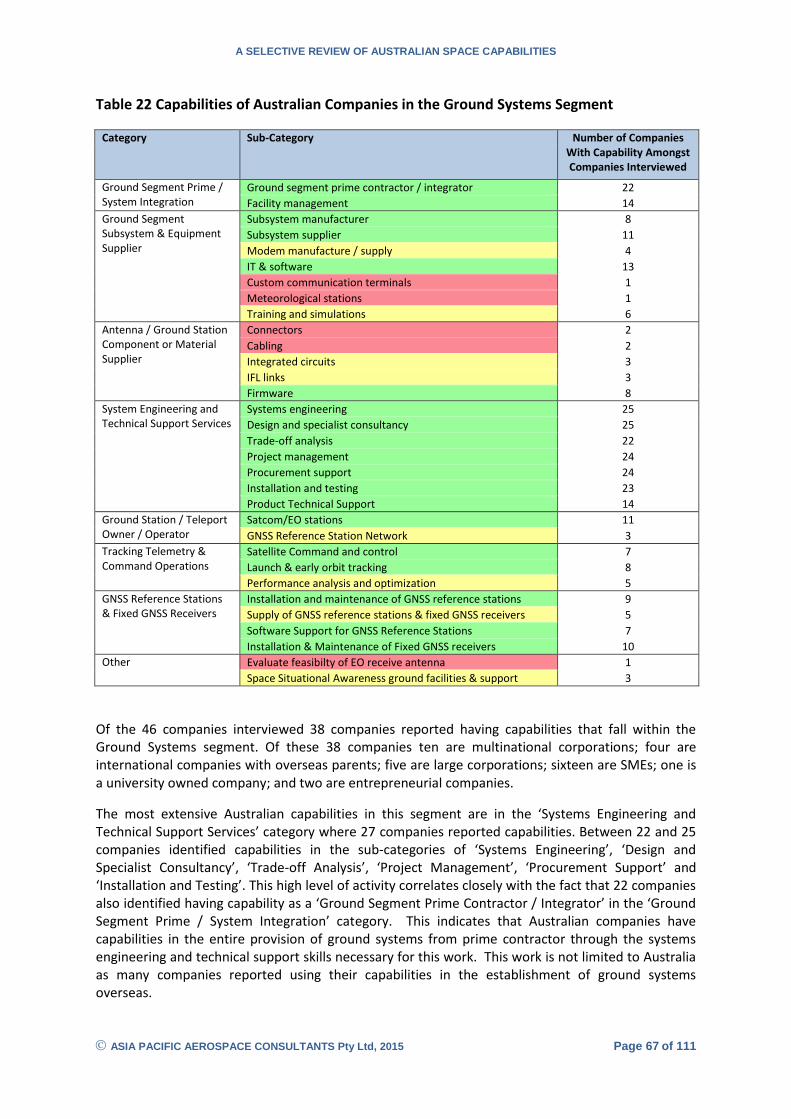

Table 22 Capabilities of Australian Companies in the Ground Systems Segment ................................ 67

Table 23 Capabilities of Australian Companies in the Segment of Space Enabled Services ................. 71

Table 24 Capabilities of Australian Companies in the Space Support Services Segment ..................... 74

Table 25 Capabilities of Australian Companies in Space Research & Development ............................ 76

Table 26 Capabilities of Australian Companies in Space Education & Training .................................... 78

Table 27 Global Supply Chain for Space Services ................................................................................. 80

Table 28 Global Supply Chain for Satellite Communications ................................................................ 81

Table 29 Global Supply Chain for the Earth Observation Segment ...................................................... 84

Table 30 Global Supply Chain for Satellite Position Navigation and Timing ......................................... 86

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 5 of 111

FIGURES

Figure 1 Global Space Revenue ............................................................................................................. 22

Figure 2 Composition of Global Space Activities .................................................................................. 24

Figure 3 Composition of Commercial Space Activities ......................................................................... 25

Figure 4 Number of Companies Interviewed by State & Territory ....................................................... 32

Figure 5 Number of Companies with Space Capabilities by Segment .................................................. 33

Figure 6 Companies with Space Enabled Service Capabilities by Service Domain ............................... 34

Figure 7 Interviewed Companies by Business Type ............................................................................. 36

Figure 8 ANZSIC Industry Segments Served by Space Capabilities of Interviewed Companies ............ 38

Figure 9 Number of Staff by Employee Category ................................................................................. 43

Figure 10 Level of Qualification of Staff ................................................................................................ 44

Figure 11 Space-Related Workforce by Gender.................................................................................... 45

Figure 12 Workforce by Age Category .................................................................................................. 46

Figure 13 Distribution of Workforce by State & Territory .................................................................... 47

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 6 of 111

CASE STUDIES

Case Study 1 – Space Systems: Silanna Semiconductor ....................................................................... 62

Case Study 2 – Launch Systems: Teakle Composites ............................................................................ 64

Case Study 3 – Ground Systems: Electro Optic Systems ....................................................................... 68

Case Study 4 – Satellite Communications: Skybridge ........................................................................... 93

Case Study 5 – Earth Observation: Tidetech ......................................................................................... 95

Case Study 6 – Position Navigation and Timing: Pod Trackers ............................................................. 98

Case Study 7 – New Space: Saber Astronautics .................................................................................. 100

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 7 of 111

1 Executive Summary

Background and Context of Study

Since the early days of the space age Australia has been an active participant in space activities. Australia’s geography and demographics define it as a country particularly well suited to the utilisation of space based technologies and consequently Australian companies and institutions are active across all three primary areas of space-enabled services, namely satellite communications, earth observation, and positioning, navigation and timing (PNT).

In recent years the Australian Government has recognised that space-related technologies are critical to the operation and ongoing productivity of a wide range of Australian industries and the broader fabric of Australian society. The Australian space sector encompasses diverse functions incorporating both services and production however, few Australian organisations have space-related activities as their dominant output. Therefore, statistics that are based on dominant outputs do not fully capture space activities as an industry.

In order to better understand the current capabilities of Australia’s commercial space industry and future industry opportunities the Department of Industry, Innovation and Science (the Department) engaged Asia Pacific Aerospace Consultants Pty. Ltd. (APAC) to perform a study of Australian space capabilities. The study was tasked to report on: Australia’s industry capability in commercial space; domestic and global supply chain opportunities in commercial space; growth opportunities in space applications for domestic and international markets; and case studies of Australian companies that have found success in commercial space activities.

The Changing Global Space Economy

When most Australians hear the words “space” or “space industry” or “space economy” it is usually the big Government space projects that first come to mind – the International Space Station (ISS), the Hubble Space Telescope, the NASA rovers on Mars, the New Horizons flyby of Pluto and the Rosetta Mission landing on a comet. However, this natural and understandable association of “space” with these big government missions actually masks a transformation that has taken place in the space industry over the last 50 years. Few people realise that these big government space projects are no longer the primary space activities. Government space projects are now dwarfed by the commercial activity taking place in the space industry. The inflection point took place around 15 years ago. Since then the quiet evolution of the commercial space industry has turned into a revolution with massive commercial growth that today is transforming the industry and has significant ramifications for Australia.

The process of opening new domains to industrial development typically goes through three distinct phases – the Exploration Phase, the Experimentation Phase and the Exploitation Phase1. The Exploration Phase is as described – a journey into the unknown. This phase is characterised by the high risks of addressing the unknown accompanied by high costs associated with attempting to access the new domain often with unproven technology. This phase is typically the realm of Governments which can accept the high costs and risks in the pursuit of national interests. The Experimentation Phase builds on the successes of the Exploration Phase. It is usually driven by the goals of understanding the new domain and learning to operate in the new environment including the development and perfection of new equipment. Activities in this phase are also generally led by

1 The authors wish to recognise Ms Doris Hamill for her introduction of these concepts in her paper

“Transitioning to the Commercial Exploitation of Space”, UNISPACE III, 27 July 1999.

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 8 of 111

Governments. The Exploitation Phase marks a major shift in the business paradigm for the new domain. At this point the technology and science of the new domain is generally well understood and there is a demonstrated value of operating in the new medium. Often unique products and services are possible. At this point industry takes over and begins to invest. In 1998 commercially derived space revenue equaled revenue from direct government expenditure in space. Since then space has well and truly entered the Exploitation Phase and the changes are dramatic.

According to the 2015 ’Space Report’, produced annually by The Space Foundation in the US, the global space economy, consisting of launch and ground services, satellite manufacturing and operations, satellite television and communications, government exploration, military spending, and other interests grew by 9% in 2014 reaching a total worldwide revenue of USD $330 billion. Since 1998 commercial space revenues have dramatically outpaced revenue from direct government space expenditure. Commercial space activities grew by 9.7% in 2014 and now constitute 76% of the global space economy. Commercial space revenues have achieved a compound annual growth rate over 15 years of 13.7% - which exceeds the compound annual growth rate of 9.7% that the Chinese economy sustained over the same time period2. This is the commercial exploitation of space and it is attracting serious attention from investment and venture capital firms worldwide.

Just as it is important to recalibrate the association of space being dominated by big government funded projects to reflect the modern commercial activities that drive the space economy today it is also important to recalibrate the common association that space is only about rockets and satellites. Today commercial space products and services – the use of the space systems and data derived from space or Space Enabled Services – generates 70% of space economic activities worldwide, based on the 2015 ‘Space Report’.

It is interesting to note that the three current largest space revenue streams – Satellite Direct to Home (DTH) TV, Global Navigation Satellite Systems (GNSS) equipment and services, and Satellite DTH Broadband & Mobile equipment - did not exist 30 years ago. They represent one of the massive transformations that has been taking place in the space industry - the move to the consumer market. This trend of providing space enabled services to the mass market has been the major driver of the commercial space industry over the last 15 years as it continues to introduce new services such as satellite broadband and GNSS positioning equipment and services.

There are now literally billions of devices in use around the world that incorporate satellite PNT data as part of their functionality which places space enabled services in to the hands of small businesses and individual consumers and not just Governments and large corporations. Ubiquitous access to this type of information allows innovative use of space enabled services and applications in ways never contemplated in the past.

There is another significant trend that has been gaining traction in the space industry over the last several years - the emergence of what is often referred to as ‘New Space’. The ‘New Space’ era was ushered in by a number of billionaires primarily in the United States (US) who chose to spend their own private wealth to pursue personal space ambitions but within the context of a commercial space business. A key facet of this new era of space activity was a change in the philosophy of product development which adopts more traditional commercial acceptance of risk and moves away from the previous Government procurement approach of ‘cost-plus’ contracting that existed within the aerospace industry for decades.

Concurrent with the fundamental philosophical change associated with the ‘New Space’ era is the growing capability of small satellites. As the capability of small spacecraft has grown and the costs decreased it has allowed a dramatic increase in the number of players capable of owning their own

2 Based on World Bank Statistics

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 9 of 111

space assets. The emergence of very low cost cubesat technology has placed the potential of satellite ownership into the hands of innovative small businesses, universities and even schools and individuals. A fundamental difference associated with this new class of satellite technology is a shift away from an emphasis on long life and high reliability towards shorter product cycles, achieving lower cost by accepting lower reliability with a plan to use the cost savings to build more satellites for quick replacement of the space assets. This new facet of the industry is often referred to as ‘Space 2.0’ and as the name connotes draws the moniker from the Information Technology (IT) world and the innovators and investors who see the potential of this new paradigm of space activity.

It is against this backdrop of the dramatic growth of the global space industry with increasing demand for innovative services and with technological breakthroughs lowering the barriers to entry that this report examines the space capabilities of Australian companies and their ability to participate in this rapidly growing space economy.

Scope of Study

This study is not a comprehensive look at the Australian space scene. While the Department recognises that many sectors play a role in the Australian space landscape the purpose of this study was to understand the aspects of the purely commercial space marketplace hence the terms of reference specifically excluded government and not-for-profit space activities as well as the research and academic sectors. The focus of this study was solely on Australian corporations with space capabilities with a goal of understanding their space capabilities, the markets they serve and the potential to expand both domestically and globally. This type of information is best collected directly from the company hence the study is based on direct interviews with Australian companies involved in space.

Methodology

Based on these terms of reference the results of this study are based on direct interviews conducted by APAC with 46 Australian companies active in the space industry.

The selection of the companies to interview was a key element of this study. The creation of a target list of companies to interview was determined by several considerations:

The goal of capturing the widest range of Australian space capabilities,

The goal of including a wide geographic spread of companies,

The goal of including a diverse range of businesses – small, medium and large as well as multinationals with operations in Australia,

At the specific request of the Department the goal of including businesses that represent some of the new applications and innovations in space.

The final aspect was timing and availability – the ability of companies to meet and complete the face-to-face interview process with APAC.

Space Capability of Companies Interviewed

APAC interviewed companies with space capabilities headquartered in every state and territory

except the Northern Territory that collectively had staff in every state and territory. The data shows

that Australian companies have space capabilities in all the seven major space segments targeted for

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 10 of 111

this study and across all three service domains of Satellite Communications, Earth Observation and

PNT.

Table 1 Space Capabilities of the 46 Companies Interviewed for this Study

No. of Companies with Capabilities by Segment

Space Systems

Launch Systems

Ground Systems

Space Enabled Services

Support Services

R&D Education & Training

Primary Activity 6 3 19 32 7 6 7

All Responses 15 10 38 42 23 33 14

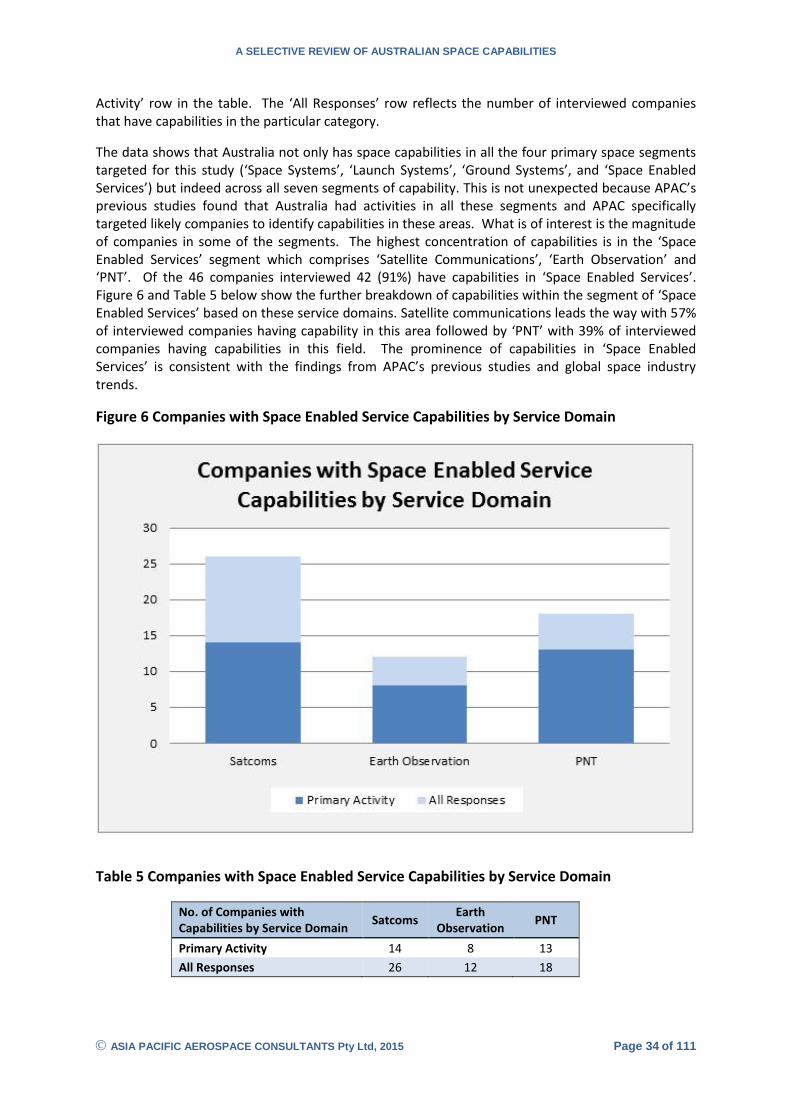

The highest concentration of capabilities is in the Space Enabled Services segment which comprises Satellite Communications, Earth Observation and PNT. Of the 46 companies interviewed 91% had capabilities in this segment showing that Australian industry mirrors the focus on Space Enabled Services seen globally. Satellite communications is most prominent with 57% of interviewed companies having capability in this area followed by PNT where 39% of interviewed companies have capabilities and Earth Observation where 26% of interviewed companies have capabilities.

The segment of Ground Systems also stands out where 83% of the respondents have capabilities. Also of note is that 32% of the companies interviewed indicated capabilities in Space Systems and 22% cited capabilities in Launch Systems.

A telling statistic to emerge from the interviews is that 72% of companies interviewed have capabilities in Space Research and Development (R&D) and 13% consider it a primary capability for the work they do in space. From the interviews it is clear that most of the companies feel that R&D is an essential part of their business and a critical means of gaining a competitive edge and maintaining differentiation in the marketplace. The other surprising result is the prominence of Space Education & Training capabilities where 30% of the interviewed companies indicated capability and 15% cited it as a primary capability for their organisation.

An interesting feature that emerged from the interview process is that some of the companies do not see themselves as part of the space industry per se but associate themselves more with the industry they serve such as Telecommunications or Defense. This occurred most often in the Space Enabled Services segment and it highlights the difficulty in capturing useful data about the space sector. It also highlights the fact that Space Enabled Services in particular have embedded themselves into the fabric of modern society and are a key element underpinning many significant industries.

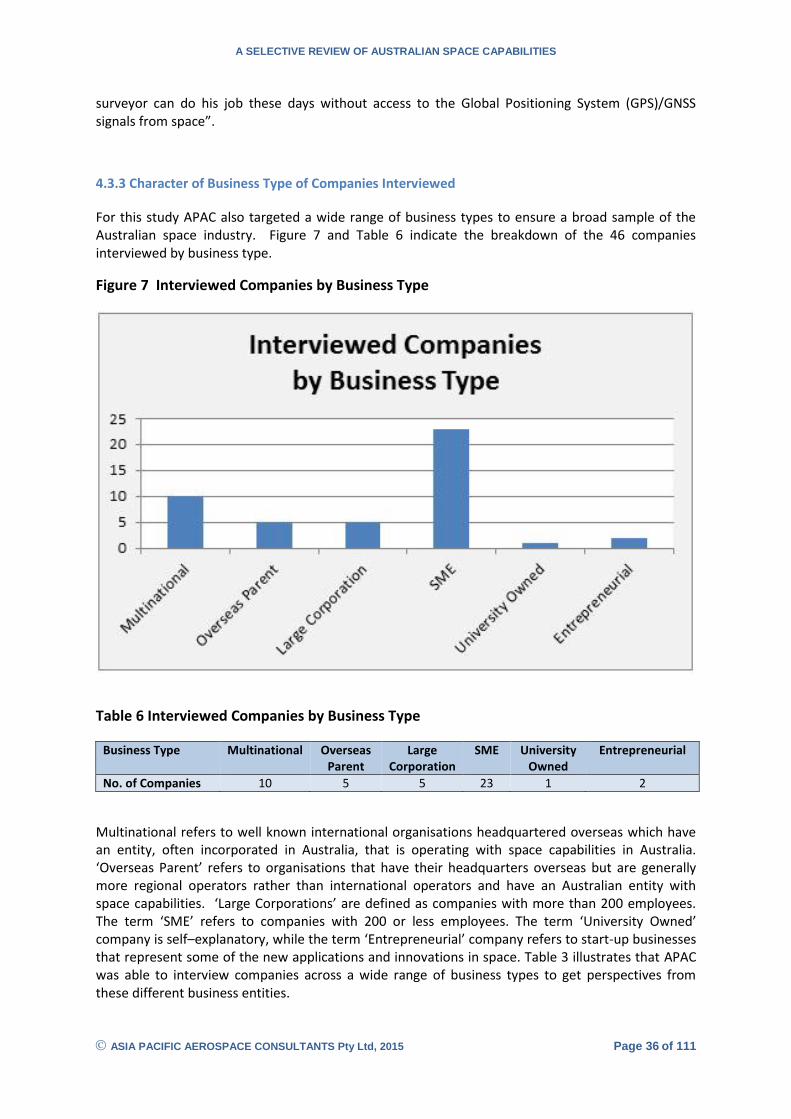

Character of Business Type of Companies Interviewed

In terms of business characteristics, the data also shows that 33% of the companies interviewed were Australian operations of multinational or overseas entities, while 50% of the companies interviewed were Small or Medium Enterprises (SME). It is clear that the Australian space industry is primarily comprised of SMEs or small to medium pockets of space capabilities within larger organisations.

It is also clear that this is a dynamic industry in terms of business activity. New companies are being formed, other companies are being bought, sold or merged. Of the 46 companies interviewed four have been founded within the last five years, 12 have been started within the last 10 years and 21,

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 11 of 111

nearly half of those interviewed, have been founded within the last 15 years since the start of the Commercial Exploitation Phase of space. There is also evidence from the interviews that North American and European companies are actively watching the Australian space SME and university sectors with a view to acquiring space intellectual property (IP) and incorporating it into their overseas operations.

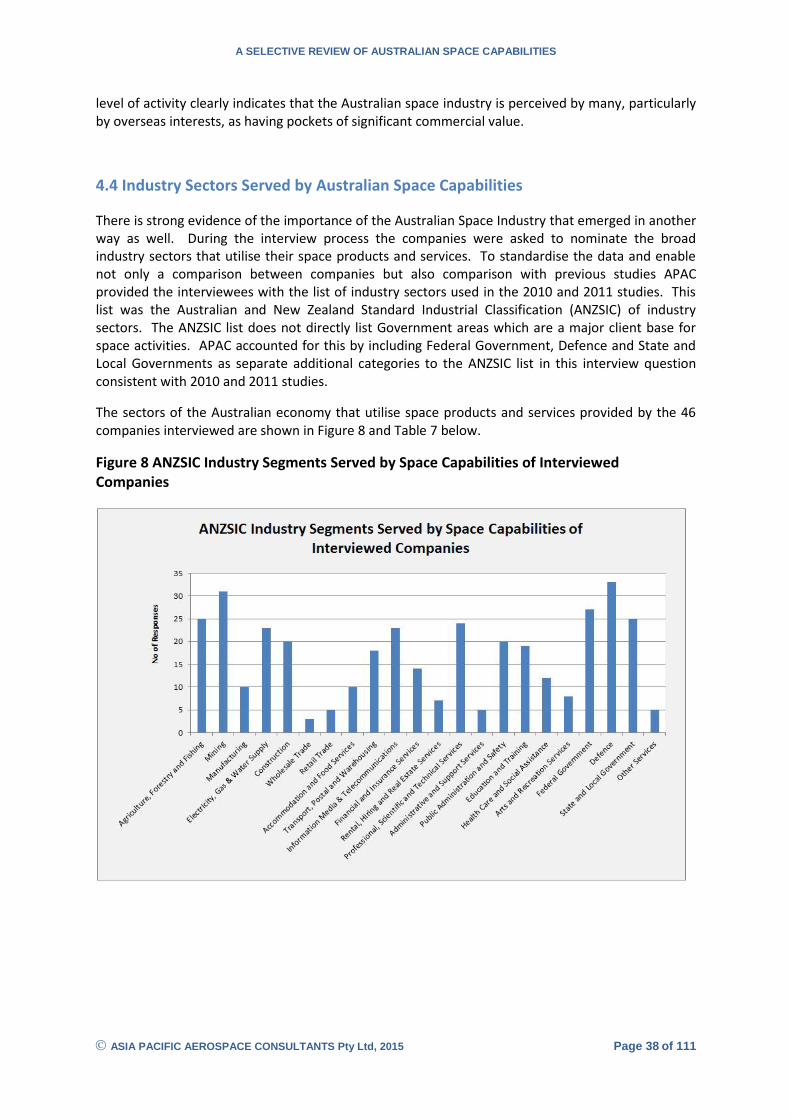

Industry Sectors Served by Australian Space Capabilities

During the interview process the companies were asked to nominate the industry sectors that utilise their space products and services. The responses reveal that space-related products and services are used in every sector of the Australian economy. Defence is the major industry sector for space companies in this study as 72% of the interviewed companies have Defence as a customer. Mining is the second most important industry sector for companies in this study with 67% of respondents providing space services to the mining sector while the Federal Government was the third largest sector with 59% of interviewed companies having the Federal Government as a customer for space products and services. Agriculture, Forestry & Fishing (54%), State & Local Government (54%), Professional, Technical and Scientific Services (52%), Electricity, Gas & Water Supply (50%) and Information, Media & Telecommunications (50%) are the other industry sectors that at least half of the companies interviewed have as customers.

Revenue Generated by Australian Space Activities

The 46 companies interviewed collectively generate nearly $2 billion in annual revenues from their space products and services. This matches the upper bound of Australian space industry revenue in APAC’s 2011 study that was based on revenue from 180 organisations indicating that the Australian space industry has grown since 2011. This growth has been led by the Position, Navigation and Timing sector as well as the satellite communications sector. Based on the data from the 2011 study and the more specific information on corporate revenue gained from this study APAC estimates that the total Australian space industry is now generating revenue in the range of $3 billion - $4 billion per annum. Most of the revenue generated by the 46 companies interviewed is earned in Australia. Although 63% of the companies interviewed generate revenue from overseas this export revenue constitutes only 8% of the nearly $2 billion in total revenue from the interviewed companies.

Workforce Size Involved in Australian Space Activities

Collectively the 46 companies employ 1,314 staff in space-related jobs by headcount and 1,190 Full Time Equivalent (FTE) staff in space-related jobs. Based on the data from the 2011 study and the more specific information on companies’ staff numbers gained from this study APAC estimates that the total Australian space industry employs between 9,500 – 11,500 staff

Staff Demographics of Workforce Involved in Australian Space Activities

The 46 companies interviewed have a highly technical workforce. Nearly all companies employ engineers and scientists which comprise 42% of the total space-related workforce of these companies. Technicians comprise another 24% of the total workforce. This is a high technology

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 12 of 111

industry where often the Sales, Marketing, Business Development and Business Management staff have technical backgrounds.

The space workforce is a highly educated workforce. The data reveals that 66% of the staff in these companies have tertiary qualifications and another 23% have certificates. Nearly half of the companies have staff with PhD’s. This is clearly an industry with very high levels of staff education and qualifications.

The space-related workforce within the 46 companies is predominantly male with women comprising only 16% of the workforce. The data shows that 73% of the space-related workforce is over 30 years old and 41% of the workforce is 40 years of age or older. Only 39% of the companies have space-related employees that are younger than 30 years of age. This is an industry where experience and longevity in the industry is valued. The workforce of these companies is spread across every state and territory in Australia with New South Wales (NSW) having the largest concentration of 30%.

Business Trends Identified By Companies Interviewed

The predominant business trend and sentiment of the interviewed companies is for revenue growth. Of these companies 78% reported revenue growth during the last three years with 61% of companies reporting more than 25% growth over that timeframe. Likewise 78% of companies are predicting revenue growth next year with 91% predicting growth over the next three years. Many companies anticipate significant revenue growth with 41% expecting revenue growth greater than 25% next year and 74% expecting revenue growth of greater than 25% over the next three years.

The Export Revenue Growth figures are slightly less robust with 52% of companies reporting export revenue growth over the last three years and 54% reporting export revenue growth last year. Export growth is a focus for most companies with 61% expecting export revenue growth next year and 67% of companies anticipating revenue growth over the next three years.

Staff growth is also a trend. Nearly three quarters of the companies reported staff growth over the last three years with 59% reporting staff growth of greater than 25% over the past three years and 28% reporting staff growth of greater than 25% last year. Staff growth is widely anticipated over the next three years with 89% of the companies expecting to increase their space-related staff and half of the companies expecting to grow their staff by more than 25% over the next three years. These company views indicate strong growth prospects for the Australian space industry consistent with global trends.

Current Australian Space Capabilities

In this study APAC analysed company space capabilities in the following functional segments:

1) Space Systems 2) Launch Systems 3) Ground Systems 4) Space Enabled Services 5) Space Support Services 6) Space Research & Development 7) Space Education & Training

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 13 of 111

Each of these segments of space capability is subdivided into categories and sub-categories of capability which cover the essential elements of capability necessary to produce the main output of the segment e.g. a satellite in the case of the Space Systems segment. The segment of Space Enables Services is subdivided into the three major space service domains: Satellite Communications; Earth Observation; and PNT. This tiered approach facilitates a detailed understanding of space capabilities of the interviewed companies.

The results show that the 46 Australian companies interviewed have capabilities in all seven space capability segments; have capabilities in all categories of space capability within each segment except for Launch Services; and have capabilities in most sub-categories of space capability within the segments.

While capabilities in most space segment subcategories exist within these Australian companies they tend to be concentrated in certain niche sub-categories of capability. To understand the extent of Australian space capabilities APAC has analysed them by segment of capability

Space Systems One third of the companies interviewed reported capabilities in ‘Space Systems’. The key areas of capability are in the category of system engineering and technical support services. There is also a strong representation of companies that either own or operate satellites. Other prominent areas are capabilities in supplying space subsystems including payloads, instruments and on-board computing, and capabilities to provide electronic and optical components.

Launch Systems The segment of ‘Launch Systems’ is the area where Australia has the least representation of space capabilities with only 22% of companies reporting capability in this segment. While Australia has been a significant user of launch services it has essentially no orbital or sub-orbital launch capability of its own. While there is a range of capabilities amongst the interviewed companies including niche capabilities in small launch system design and manufacture there is very little depth of capability. Most of the capability in this segment is in the area of Launch Support Services with the greatest capability concentration in the area of launch vehicle tracking.

Ground Systems The ‘Ground Systems’ segment is one of the two key areas where Australian companies have significant capabilities. Nearly 85% of the interviewed companies have capabilities in this segment across every sub-category of capability. The greatest concentration of capability is in the category of ‘Systems Engineering and Technical Support Services’ where more than half of the interviewed companies have capability. A similarly high percentage of the companies have capabilities as a ‘Ground Segment Prime Contractor / Integrator’. Australian companies have capabilities in the entire provision of ground systems from prime contractor through the systems engineering and technical support skills necessary for this work. A significant number of companies also report capability in the category of ‘Ground Segment Subsystem & Equipment Supplier’ including manufacturing of ground subsystems and development of software for ground systems. One of the key drivers behind the high presence of capability in the ‘Ground System’ segment is the extensive use of satellite communications in Australia which is in part driven by its unique demographics and global geographic location. As a consequence nearly one quarter of the companies have capabilities as ‘Ground Station /Teleport Owner / Operator’. Another corollary of Australia’s sophisticated involvement in owning and operating satellites is the fact that Australian companies have significant capabilities in the area ‘Tracking Telemetry & Command Operations’ necessary to operate the satellites in orbit.

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 14 of 111

Space Enabled Services Space Enabled Services is the largest sector of the space industry worldwide and it is also the largest sector of the space industry within Australia. This is the other major segment where Australian companies have significant space capabilities with 91% of interviewed companies reporting capabilities in this segment across almost all subcategories.

The greatest areas of strength for Australian companies in this segment are in the provision of services and applications although there are small pockets of manufacturing and the supply of user equipment. Australia has significant capabilities in each of the three service domains of Space Enabled Services namely Satellite Communications, Earth Observation and PNT. Of the 46 companies interviewed over half had capabilities in Satellite Communications, over one quarter had capabilities in Earth Observation and approximately 40% had capabilities in PNT.

Satellite communications is the major space activity worldwide and also in Australia so it is not surprising to find considerable local capability. Like the Ground Systems segment all capabilities needed to provide satellite communications services are available among the companies interviewed for this study.

Earth Observation is another area with considerable local expertise where Australia has longstanding capability serving significant users in the mining and environment sectors. All capabilities needed to provide earth observation services are available among the companies interviewed for this study including satellite image providers based in Australia.

Satellite PNT services have been one of the key areas of major growth for the space industry over the last 15 years. Australia is one of the few countries that have access to all GNSS constellations and has developed significant GNSS capabilities across all subcategories in this area. Capabilities include Australian development centres for multinational companies providing software for major product lines of precision GNSS equipment sold globally to the mining, construction and agriculture industries; development and manufacture of equipment detecting GNSS signal interference; development of local PNT reference systems for precision agriculture and construction.

Nearly two thirds of the interviewed companies identified capabilities in ‘Technical Support Services’– the highest single capability category for ‘Space Enabled Services’. Over 40% of the companies interviewed reported capabilities as a ‘User Equipment Supplier’ and 17% of the companies have capabilities as a ‘User Equipment Manufacturer’.

Space Support Services Half the companies interviewed reported capabilities in this segment with the greatest areas of emphasis being in technical consulting and services relating to satellite communications and earth observation. Australian companies have considerable capabilities to support local space projects with technical consulting.

Space Research & Development Previous studies have shown that Australia does have significant capability in ‘Space Research & Development’ generally centred around the academic and research sectors. One of the surprising results of this study was the extent of Space R&D capability among the 46 companies interviewed where 72% of the companies reported active R&D capabilities as a key element of their commercial success. The prominent areas of capability are in engineering research in the Satcoms, EO and PNT domains.

Space Education & Training Another surprising finding of the study was that 30% of companies identified capabilities in ‘Space Education and Training’ as a commercial operation. Prominent capabilities include delivery of Professional Training Courses and Commercial Training Courses on space topics.

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 15 of 111

Domestic and International Supply Chains

The global space supply chain reaches from the owner / operator of a satellite through the companies that supply the spacecraft that flies in space, the launch service that launches it, the ground equipment that supports it, and the services that it enables. Australian space capabilities map onto these supply chains in almost all of the categories used for the key service domains of Satellite Communications, Earth Observation and Position Navigating and Timing. Australia is already participating in these supply chains at some level, either domestically or internationally. The highest concentrations of Australian capabilities for all three of these service domains are in the ‘Ground Systems’ and ‘Space Enabled Services’ segments which correspond to the areas of highest space industry activity and revenue generation in the international space industry. From this perspective Australia has capabilities concentrated in the appropriate areas to grow its participation in the global space industry internationally.

Supply Chain Opportunities for Australia

Australian space capabilities provide opportunities for Australian companies to participate in global space supply chains in all major segments and service domains.

In the ‘Space Systems’ segment the greatest potential opportunities lie in the areas of payloads, space components and space qualified testing. There are also opportunities for Australian companies in the construction, ownership and operation of small satellites.

In the ‘Launch Systems’ segment the opportunities for Australian companies lie predominantly in early tracking of satellites launched overseas and manufacture of components for small launch systems. Australian capability in tracking space debris also presents a significant opportunity for launch and satellite support given the growing problem with space debris.

The ‘Ground Systems’ segment represents both an area where Australian companies have significant capabilities and where there are real opportunities for further penetration of the global supply chain both domestically and internationally. Software and network management systems for ground stations; local suppliers for hardware in ground systems; and local suppliers for long term maintenance and support were areas identified where Australian companies fit well in the global supply chain. Experience in Australia working with large international companies then opens the door for partnering with those same companies in other countries.

The ‘Space Enabled Services’ segment is effectively the end of the overall global supply chain and is the point of interface with actual end markets and customers in each of the three primary service domains of satellite communications, earth observation, and position navigation and timing. All of the companies with satellite communications capability in Australia are involved in the supply chain for satellite communications in the domestic market and are actively expanding these opportunities in the international market. There are opportunities in working with multiple equipment suppliers and adding value by developing software and equipment to enable different equipment to operate seamlessly. Other opportunities exist in expanding overseas by partnering with telecommunications and satellite service providers and in the Machine-to-Machine (M2M) market in mining and transport for tracking of remote assets.

Australian companies already are part of the global supply chain associated with delivery of earth observation data as local capability is required to distribute and manipulate the data coming into

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 16 of 111

Australia. Developing products from earth observation imagery is one of the real growth areas of the space industry. The majority of planned and announced cubesat constellations are focused on providing earth observation imagery in new and more pervasive ways such as virtual real time imagery. Another strong growth trend in this area is the collection and presentation of earth observation imagery to the consumer market. An additional strong trend is the fusion of various sensors to create a composite picture such as a combined picture using optical and infrared sensors or hyperspectral sensors. There is a lot of growth in the new uses of earth observation imagery worldwide. Australia has significant expertise in this sector particularly in the development of products for specific industries and hence is well placed to deliver new earth observation imagery and data presentation into global supply chains.

The PNT domain is the fastest growing sector in the global space industry. Demand for increasing accuracy in precision location continues to grow in many different industries including mining, construction, agriculture and transport. Australia has significant capability in PNT particularly in GNSS software and firmware development. By partnering with the OEMs on Australian projects Australian companies have already become part of the PNT global supply chain and will continue to expand into international markets as a result.

Regional Markets

The space activities of countries in the Asia-Pacific region present unique supply chain opportunities for Australia. Many Asia Pacific countries are developing domestic satellite programs based on the growth in capability of small satellites. While these countries intend to develop domestic space capabilities most have not been able to develop a spacecraft exclusively with domestic capabilities. Inevitably some capabilities of the spacecraft and its deployment have been acquired through the global marketplace. Many people working in these national programs have received part of their space education in Australia and hence there is greater openness to Australian participation and acceptance of Australian capabilities presenting potential opportunities for Australian company involvement in regional supply chains.

New Space Markets

The ‘Space 2.0’ revolution centred on exploiting the lower cost capabilities of smaller spacecraft, whether that be cubesats, small satellites, or swarms of spacecraft is an important emerging opportunity. It is based on the rapid development of new capabilities with much lower technology thresholds leading to much lower capital costs and faster time to market. Often these ventures seek to serve completely new niche markets with very simple technology or explore new dimensions to an existing market. The ‘Space 2.0’ revolution is extremely important for the Australian space industry as it lowers the capital cost to participate and also lowers the technology threshold to a level where Australian companies can directly compete globally.

Key Issues for Australian Participation in Global Supply Chains

Australian companies do face challenges in participating in global supply chains. At a global level the space industry is a highly regulated industry due to the potential military applications of space technology. Constraints on technology transfer can be an impediment for international business and can cause issues for many companies, particularly SMEs who struggle with the costs associated with

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 17 of 111

compliance. However, they might also present opportunities for Australian companies as one multinational company observed that it was easier for their corporation to operate into Asia from Australia than from the US due to International Traffic in Arms Regulations (ITAR) restrictions on their US staff. Regulatory issues were also something singled out within the satellite communications domain. One of the key inhibitors cited in the interviews for Australian companies pursuing opportunities in international markets are difficulties in obtaining licenses to operate in overseas countries.

Given the high number of SMEs in the space industry some of the most pervasive issues were those that relate to difficulties that confront SMEs due to their limited staff size, revenue and balance sheet. It should be noted that many of the challenges confronting space industry SMEs are common to SMEs across many industry sectors. SMEs often face challenges dealing with large prime contractors with more elaborate business processes and major contract work with significant compliance requirements and costs.

Industry credibility is an important factor and Australia is generally not perceived by the companies as being active in space which creates a credibility hurdle for Australian companies trying to participate in global supply chains. Participation with major partners on space projects is one of the key methods to gain recognition by global supply chains in this industry. Companies felt that Australia is not perceived as a contributor in these ventures hence Australian companies find it harder to gain experience and credibility that is visible to prospective international partners.

In spite of these various issues and challenges this study shows that there are examples of Australian companies that are operating successfully in the global space industry.

Growth Opportunities in Space Applications Markets

In the satellite communications domain the main growth applications are based on the corporate arena and enhancing communications in the consumer markets. Key applications are associated with: the growing need for connectivity in remote locations; the ever growing demands for data; the rapidly burgeoning machine-to-machine (M2M) market; and mobility services via satellite.

In the earth observation domain new sectors are emerging such as insurance, agriculture, maritime surveillance, and environmental monitoring along with growth in the resources sector. The EO industry is growing worldwide particularly with the emergence of more consumer oriented applications including the development of systems providing near real time EO data. These readily available images are generating new applications, management tools and ways of doing business.

The mining industry, agriculture and intelligent transportation systems are some of the key existing markets for satellite derived PNT. New areas of focus are automated ports, construction and the use of autonomous vehicles. The mass market penetration of GNSS enabled devices delivers geospatial data at the consumer level enabling many new applications. One Australian example is the integration of Global Positioning Satellite (GPS) enabled tags to monitor the location of pets which has turned into a rapidly growing business with international markets. The ubiquitous availability of GPS enabled devices combined with other data sets means that a huge array of potential markets are waiting to be identified and developed by innovative companies.

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 18 of 111

Conclusion

This study has shown that Australian companies have relevant capabilities and world class skills in areas that feed into the rapidly growing global space economy. While there are certain challenges to entering the space global supply chains this study has identified a number of Australian companies that have already achieved various levels of success and that there are exciting opportunities for Australian companies in the space industry of the future.

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 19 of 111

2 Background and Context of Study

Since the early days of the space age Australia has been an active participant in space activities. Australia’s geography and demographics define it as a country particularly well suited to the utilisation of space based technologies and consequently Australian companies and institutions are active across all three primary areas of space-enabled services, namely satellite communications (Satcoms), earth observation (EO), and positioning, navigation and timing (PNT). In fact Australia was among the first nations to have international satellite communications and was one of the first countries to have its own domestic satellite. To this day Australia continues to be a contributor to and user of space systems and services.

In recent years the Australian Government has recognised that space-related technologies are critical to the operation and ongoing productivity of a wide range of Australian industries and the broader fabric of Australian society. Between 2009 and 2011 the Department of Industry, Innovation and Science (the Department) commissioned several studies to provide an evidentiary base for the formulation of a new space policy for Australia. In that context, Asia Pacific Aerospace Consultants Pty. Ltd. (APAC) was engaged to conduct studies in 2010 and again in 2011 to identify Australia’s current space activities at that time and to perform an assessment of the (then) current value of these space activities to the Australian economy and associated trends.

These reports were the first extensive investigation of Australian space activities since the early 1990’s. They identified 631 organisations involved in space activities in Australia generating collectively around $2 billion revenue per annum.

It has been recognised that the Australian space sector encompasses diverse functions incorporating both services and production. However, few Australian organisations have space-related activities as their dominant output. Therefore, statistical collections that are based on dominant outputs do not fully capture space activities as an industry.

In order to better understand the current capabilities of Australia’s commercial space industry and future industry opportunities the Department engaged APAC in 2015 to conduct this study of current Australian space capabilities with a focus on the commercial sector. The objective was to report on: Australia’s industry capability in commercial space; domestic and global supply chain opportunities in commercial space; growth opportunities in commercial space applications for domestic and international markets; and case studies of Australian companies that have found success in commercial space activities.

This report covers the findings of this study.

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 20 of 111

3 The Changing Global Space Economy

This chapter examines the evolution of the global space economy describing trends in the type of activity taking place, the size of the market in general, the major shift from Governments to commercial entities being the vastly predominant share of the global space economy; and the fact that consumer markets are now a major driver behind the growth in space activity. This chapter also examines the ‘New Space’ era, the key elements that are different about it and the implications that flow from it. It also notes the changes that arise from the increasing capability of smaller and smaller satellites.

In This Chapter: - 3.1 The Changing Face of Global Space Activity - 3.2 Evolutionary Phases of Global Space Activity - 3.3 The Growing Global Space Economy - 3.4 The Changing Nature of Space Activity - 3.5 The ‘New Space’ Era

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 21 of 111

3.1 The Changing Face of Global Space Activity

When most Australians hear the words “space” or “space industry” or “space economy” it is usually the big space projects that first come to mind – the International Space Station (ISS), the now retired Space Shuttle, the Voyager missions to the outer planets and the New Horizons spacecraft flyby of Pluto, the Hubble Space Telescope, the National Aeronautics and Space Administration (NASA) Spirit, Opportunity and Curiosity rovers on Mars, the Rosetta Mission with the landing of the Philae space probe on comet 67P/Churyumov-Gerasimenko. This association of “space” with these large government funded missions is completely understandable – these large government funded space exploration missions are incredibly challenging, push the boundaries of existing science by attempting things never done before and captivate people worldwide with their technological achievements and scientific breakthroughs. These government funded space missions first brought major attention to space with the launch of Sputnik in 1957, amplified this attention with the Space race and Moon landings in the 1960’s and 1970’s and have continued to dominate our collective consciousness of space ever since.

However, this natural and understandable association of “space” with these big government missions actually masks a quiet evolution and transformation that has been taking place in the space industry over the last 50 years. Few people realise that these big government space projects are no longer the primary space activities. Government space projects are now dwarfed by the commercial activity taking place in the space industry. The inflection point took place around 15 years ago. Since then the quiet evolution of the commercial space industry has turned into a revolution with massive commercial growth that today is transforming the industry and has significant ramifications for Australia.

3.2 Evolutionary Phases of Global Space Activity

In order to understand what is currently taking place in the space industry it is useful to recognise that this is the evolution of a new industry in a new domain. Examples of this type of evolution include the discovery and opening of the New World of the Americas and Far East in the 1500’s, the development of Aviation, Undersea Exploration and of course Space. The process of opening new domains to industrial development typically goes through three distinct phases – the Exploration Phase, the Experimentation Phase and the Exploitation Phase3. The borders between these phases are not necessarily well defined (they can often overlap and can certainly coexist) and are really more of a continuum rather than distinct boundaries. The phases are recognisable by a different paradigm and mindset which determines the drivers and rationale for business engagement.

The Exploration Phase is as described – a journey into the unknown. This phase is characterised by the high risks of addressing the unknown accompanied by high costs associated with attempting to access the new domain often with unproven technology. Given the high cost, high risk nature of this phase generally governments must take the lead in these endeavours and supply the funding for the basic infrastructure of exploration. Business is generally willing to assist by being paid to produce equipment and services in support of the mission but governments drive the agenda often driven by military, national security or national prestige considerations. This was certainly the case with space in the 1940’s, 1950’s and 1960’s.

The Experimentation Phase builds on the successes of the Exploration Phase. It is usually driven by the goals of understanding the new domain and learning to operate in the new environment

3 The authors wish to recognise Ms Doris Hamill for her introduction of these concepts in her paper

“Transitioning to the Commercial Exploitation of Space”, UNISPACE III, 27 July 1999.

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 22 of 111

including the development and perfection of new equipment. This phase is generally still characterised by high cost but with a lower risk aspect due to the achievements of the Exploration Phase. Governments typically remain the key drivers and financiers of this phase but industry, in addition to supplying the government’s needs, begins to examine and cautiously pursue ideas for commercial exploitation. This was the case with the space industry in the 1970’s, 1980’s, and 1990’s.

The Exploitation Phase marks a major shift in the business paradigm for the new domain. At this point the technology and science of the new domain is generally well understood and there is a demonstrated value of operating in the new medium. Often unique products and services are possible. At this point industry takes over and begins to invest. The costs might remain high but industry perceives that it can produce a superior commercial return that is worth the investment. Industry leverages off existing government infrastructure or begins to build its own. At this stage it is market forces that become the dominant factor. This is an industry in a new domain that is reaching maturity and often explosive growth is possible. This is the state of the space industry today. Space has well and truly entered the Exploitation Phase and the changes are dramatic.

3.3 The Growing Global Space Economy

Figure 1 illustrates the explosive revenue growth of the global space industry in recent years. The chart is based on three discrete data points of total space industry revenue in 1973, 1998 and 2013. The use of only three data points creates straight lines hence is not a true reflection of the common fluctuations that total revenue numbers tend to have, however these provide a very graphic representation of the space industry revenues through the Experimentation Phase and the Exploitation Phase and the dramatic effect that occurs once an industry reaches the Exploitation Phase.

Figure 1 Global Space Revenue

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 23 of 111

1973 is a good approximation for the start of the Experimental Phase of space. Apollo 17, the last moon landing, had completed its mission in December 1972 and the Apollo program was winding down. The Soviets and the US were moving to the phase of space stations in Low Earth Orbit (Salyut 1 and Skylab) with the objective of learning how to live and work in space. At the same time the initial traces of the exploitation of space began to appear. Telesat Canada launched the first domestic telecommunications satellite in 1972 followed in 1974 by Western Union and AT&T in the US and then Palapa in Indonesia in 1976 (Australia became the 7th nation to launch a domestic satellite with Aussat-A1 in 1985). According to Euroconsult, the leading European space consulting firm, the global space revenue in 1973 was USD $15 billion. Of this revenue, 80% was derived from direct government expenditure on space.

3.4 The Changing Nature of Space Activity

1998 marks a watershed year for the space industry. According to Euroconsult 1998 is the first time that commercially derived space revenue equalled revenue from direct government expenditure in space. This marks the end of the Experimentation Phase and the start of the Exploitation Phase. At this point global space revenues reached USD $68.8 billion. In the 25 years since 1973 global space revenue had grown at a compound annual growth rate of 6.3% - a very healthy growth rate.

Figure 1 clearly shows the massive growth in space revenue that has occurred since the space industry entered the Exploitation Phase. In the 15 years since 1998 global space industry revenues have grown from USD $68.8 billion in 1998 to USD $314 billion in 2013 according to the 2014 “Space Report”, produced annually by The Space Foundation in the US. This represents a compound annual growth rate of 10.7%. But the bulk of this growth has come from the commercial sector. Figure 1 illustrates the dramatic growth in commercial space revenue over the last 15 years compared to the much more modest growth in government expenditure. Commercial space revenue has grown from a position in 1973 when it constituted only 20% of global space revenue to a position in 2013 where it accounts for 75% of global space revenue despite the fact that government spending has continued to increase. Since 1998 commercial space revenue has grown from USD $34.4 to USD $235 in 2013. This represents a compound annual growth rate over 15 years of 13.7% - which exceeds the compound annual growth rate of 9.7% that the Chinese economy sustained over the same time period4. This is what the commercial exploitation of space looks like and it is attracting the serious attention of Wall Street and the venture capital firms in Silicon Valley who are now actively looking at the space sector as a hot new market with lots of upside.

The latest figures show a continuation of this trend. The 2015 edition of “The Space Report”, , reports that the global space economy, consisting of launch and ground services, satellite manufacturing, satellite television and communications, government exploration, military spending, and other interests grew by 9% in 2014 reaching a total worldwide revenue of USD $330 billion. Commercial space activities continue their trend of outpacing government activities in space. Revenue from commercial space activities grew by 9.7% in 2014 and now constitutes 76% of the global space economy. Revenue from Government space activities continue to play an important role and grew at a very respectable rate of 7.3% in 2014 but they now constitute less than a quarter of global space revenue. The transition to the Exploitation Phase is evident with commercial activities based on market conditions now the dominant features of the space economy.

Figure 2 illustrates the predominance of the commercial space sector by showing the breakdown of the global space market into its three principle categories: Military space activities, Civil space activities (defined by the industry as non-military Government activities – generally agencies like

4 Based on World Bank Statistics

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 24 of 111

NASA, The European Space Agency (ESA), Japanese Aerospace Exploration Agency (JAXA), etc.) and Commercial space activities. Military space activities comprise 11% of the total space economy with the US military alone generating nearly 7% of the global space revenue. Civil space activities (non-military Government activities) account for 13% of global space revenue with the US Government alone generating 6% of global revenue. Commercial space activities, as noted above, constitute 76% of the global space economy.

Figure 2 Composition of Global Space Activities

Source: Figures derived from data in “The Space Report 2015”

Just as it is important to recalibrate the association of space being dominated by big government funded projects to reflect the modern commercial activities that drive the space economy today it is also important to recalibrate the common association that space is only about rockets and satellites. The launch systems that transport objects to space, the satellites that operate in space and the ground stations that communicate with space are the key infrastructure that underpins the industry – they will always be an essential part of the space economy. But the economic activity associated with the construction and operation of these space, launch and ground systems is small compared to the products and services produced by these systems both from space and on the ground. Commercial space infrastructure (manufacture and operation of satellites, launch vehicles and large earth stations for commercial space activities) constitutes around 6% of global space activities by revenue. Government space infrastructure (both military and non-military) is not as easily identified

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 25 of 111

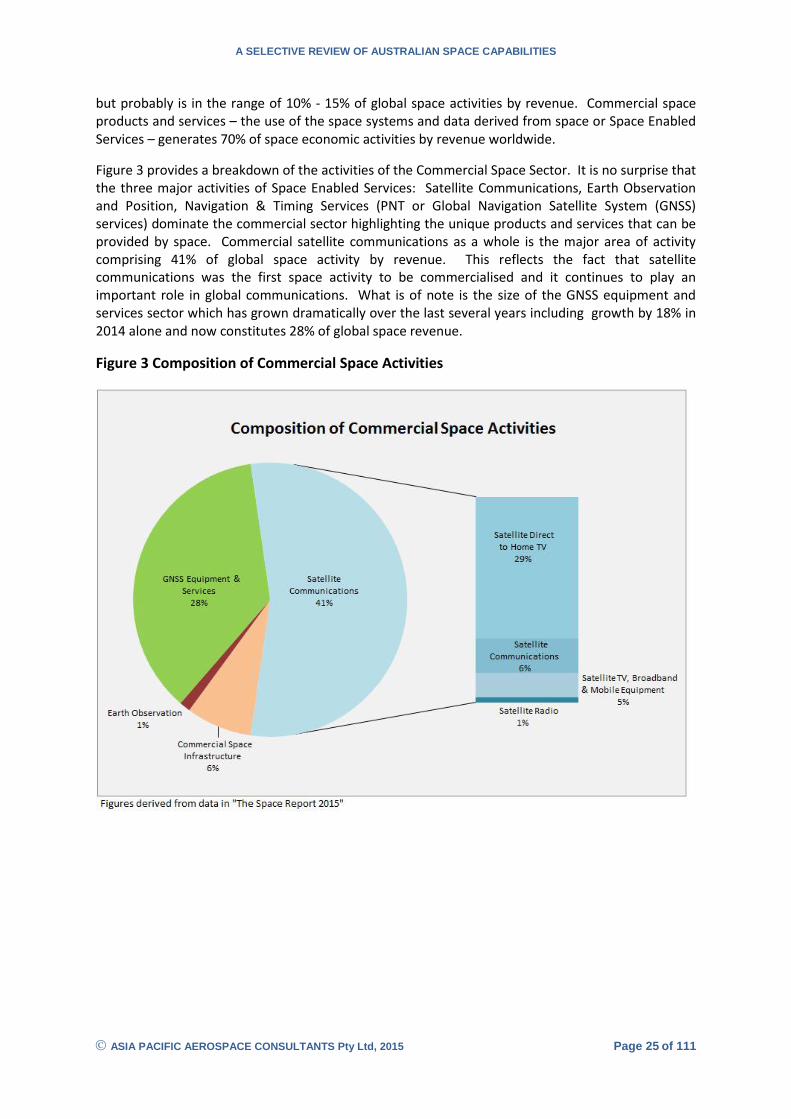

but probably is in the range of 10% - 15% of global space activities by revenue. Commercial space products and services – the use of the space systems and data derived from space or Space Enabled Services – generates 70% of space economic activities by revenue worldwide.

Figure 3 provides a breakdown of the activities of the Commercial Space Sector. It is no surprise that the three major activities of Space Enabled Services: Satellite Communications, Earth Observation and Position, Navigation & Timing Services (PNT or Global Navigation Satellite System (GNSS) services) dominate the commercial sector highlighting the unique products and services that can be provided by space. Commercial satellite communications as a whole is the major area of activity comprising 41% of global space activity by revenue. This reflects the fact that satellite communications was the first space activity to be commercialised and it continues to play an important role in global communications. What is of note is the size of the GNSS equipment and services sector which has grown dramatically over the last several years including growth by 18% in 2014 alone and now constitutes 28% of global space revenue.

Figure 3 Composition of Commercial Space Activities

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 26 of 111

Table 2 Breakdown of Key Subsectors in the Commercial Space Sector

Commercial Space Activities USD Billions Percentage of Global

Space Activities

Total 250.83 76%

Commercial Space Infrastructure 18.42 6%

Satellite Communications

Satellite Direct to Home TV 95.00 29%

Satellite Communications 21.70 6%

Satellite TV, Broadband & Mobile Equipment 17.90 5%

Satellite Radio 4.18 1%

Earth Observation 2.40 1%

GNSS Equipment & Services 91.33 28% Figures derived from data in “The Space Report 2015”

It is interesting to note that four of the seven activities listed in Table 2, including the two biggest activities, did not exist 30 years ago. The activities associated with Satellite Direct to Home TV, Satellite TV Broadband & Mobile Equipment, Satellite Radio and GNSS Equipment & Services are all new areas of activity which highlight the ability of this industry to continue to innovate and provide unique services. They also represent one of the massive transformations that has been taking place in the space industry - the move to the consumer market.

Thirty years ago commercial satellite activities were almost exclusively a wholesale activity where operators sold satellite bandwidth to large telecommunications companies as part of a telecommunications network or Earth Observation images to large Government mapping agencies. The development of higher power satellites and small rooftop mountable dishes changed all this. With these new technologies satellite became the preferred method to provide point to multipoint communications – ideal for television broadcasting – and the satellite Direct to Home TV industry was born. This is now the largest sub-segment within global space activities. This trend of providing space enabled services to the mass market has been the major driver of the commercial space industry over the last 15 years as it continues to introduce new services such as satellite broadband and GNSS equipment and services.

There are now literally billions of devices in use around the world that incorporate PNT data as part of their functionality which places space enabled services in to the hands of small businesses and individual consumers and not just Governments and large corporations. Ubiquitous access to this type of information allows innovative use of space enabled services and applications in ways never contemplated in the past. For example it is now possible for an individual consumer to receive a high resolution satellite image on their smart phone for US$20 which is a far cry from the days of only a few years ago where only large organisations could afford to use, or indeed gain access to, satellite imagery. Equally satellite PNT data is available so readily at a consumer level that it allows innovative businesses to emerge which make use of that availability. Over the last 15 years there has been an explosion of innovation across all aspects of the space market combining space derived services with other information sources to create new products & services for the consumer market generating massive economic growth. This is the power of the Exploitation Phase of space in full flight.

A SELECTIVE REVIEW OF AUSTRALIAN SPACE CAPABILITIES

ASIA PACIFIC AEROSPACE CONSULTANTS Pty Ltd, 2015 Page 27 of 111

3.5 The ‘New Space’ Era