Embed Size (px)

Citation preview

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 1

STUDENT TEXT

FULLY INTEGRATED VERSION

(MM, PP, SD, FI/CO, HR)

Flya Kite Case: Processing transactions through the

logistics and support processes of SAP

Ross Quarles Fawzi Noman

Version 4.0 03/01/2009

Sam Houston State University

Huntsville, Texas

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 2

Table of Contents – Student Text

I. Chapter 1: Introduction

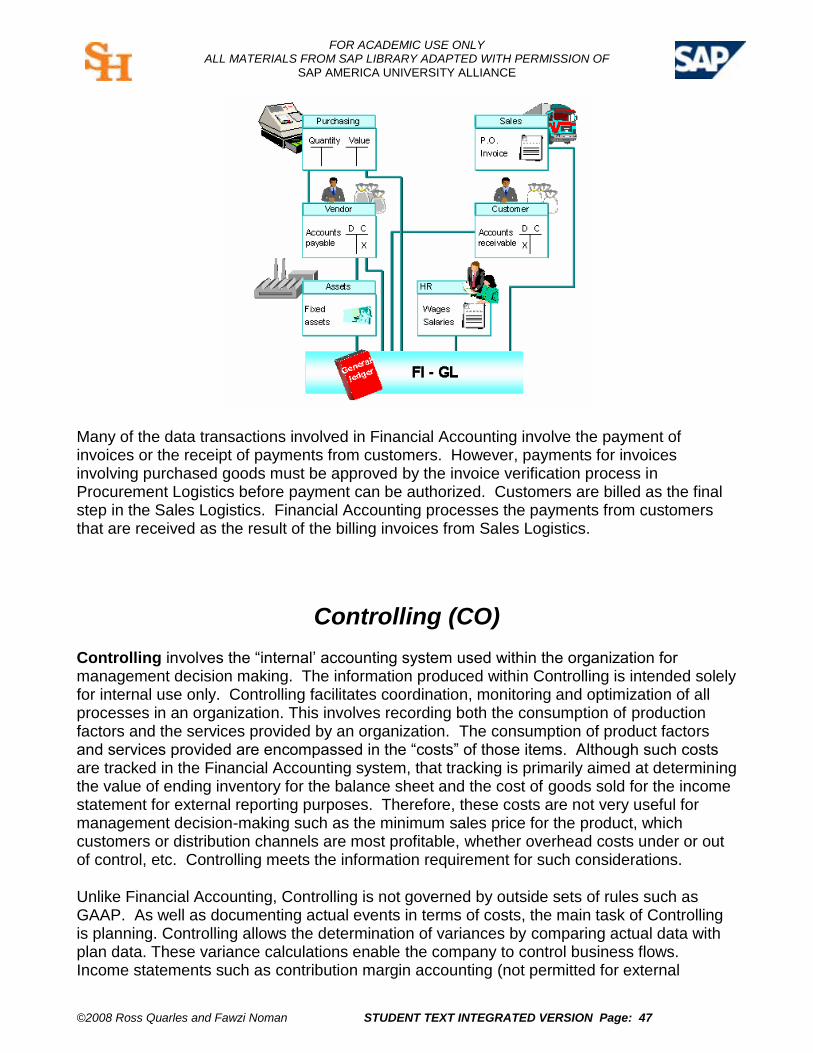

General description of case for students and introduction to basic SAP modules and terminology, business processes, and types of data.

II. Chapter 2: Procurement Logistics (MM) Discussion of the procurement process in SAP along with descriptions of the exercises in the Student Exercises document that require students to create vendor and material master records and go through the purchasing cycle from purchase requisition to logistics invoice verification.

III. Chapter 3: Production Logistics (PP) Discussion of the production logistics process along with descriptions of the exercises in the Student Exercises document that require students to create MRP views for materials, BOM, routing, run MRP, convert planned orders, issue goods to manufacturing, confirmation of completion, and order settlement.

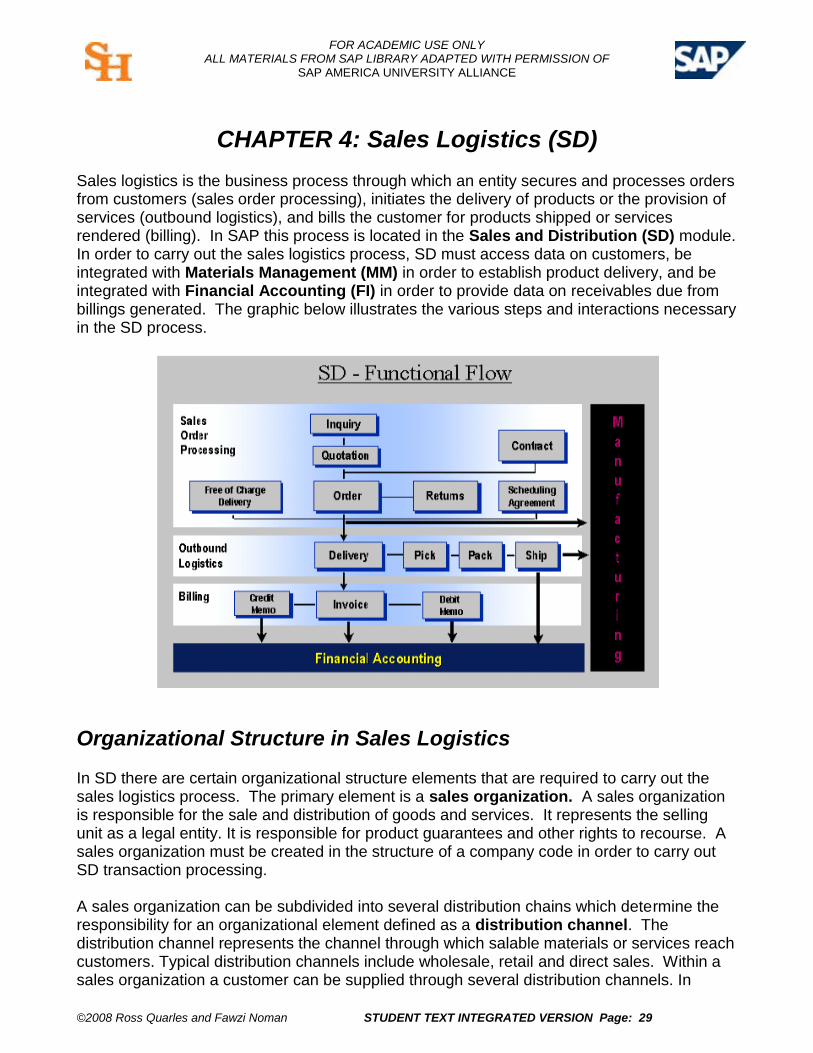

IV. Chapter 4: Sales Logistics (SD) Contains description of the sales and distributions logistics process along with descriptions of the exercises in the Student Exercises document that require students to create customers, create sales views for trading goods and finished products, material prices, discounts, customer material info records, item proposal, customer inquiry, create sale orders, create delivery, pick goods, post goods issue, and bill the customer.

V. Chapter 5: Financial Accounting and Controlling (FI and CO) Contains discussion of both the financial accounting and controlling administrative processes along with descriptions of the exercises in the Student Exercises document that require students to create and/or process general ledger accounts, primary cost elements, vendor records, general ledger document entry, posting vendor invoices, posting outgoing payments, receiving customer payments, distribution cycle, and assessment cycle.

VI. Chapter 6: Human Resources (HR)1 Contains discussion of human resources administrative process along with descriptions of the exercises in the Student Exercises document that require creation of HR organizational structure, creation of jobs and positions, entering job evaluations and pay grades, entering initial applicant data, and hiring an applicant.

1 This chapter was developed by Professor Kathy Utecht of Sam Houston State University

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 3

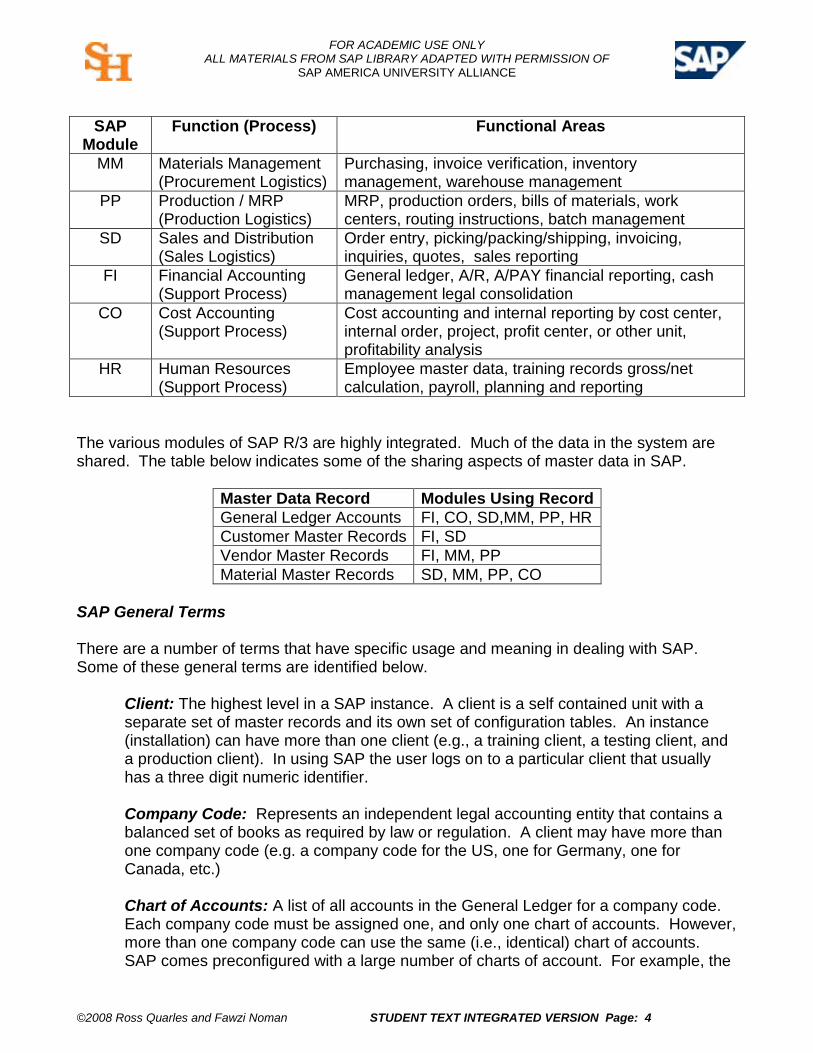

CHAPTER 1: Introduction Case Overview Flya Kite is an integrated case with exercises that allow participants to process transactions for sales logistics, production logistics, procurement logistics, accounting/controlling, and human resources. The case is preconfigured with all control/configuration data and master data necessary to process those transactions. However, for each area, the case has optional exercises that can be used by participants to set up the master data required for transaction processing. Each participant will utilize his/her own set of master data (either self-created or pre-established) to process transactions within Flya Kite. The case can be used in its entirety (all sets of exercises – either with pre-established master data or with self-created master data) in classes that have the objective of addressing the primary business processes of sales, production, procurement and materials management, etc. Alternatively, each set of exercises addressing a particular logistics or support area can be used independently in classes where only that business area is of concern (again with or without master data creation exercises). Through the use of the Flya Kite case, in total or in part, students are introduced to SAP navigation, master data use (and optional creation), transaction processing, the flow of data through each business process, and the integration of the various processes with one another. This feature allows the use of the case across disciplines with minimum detailed knowledge of the complete SAP system on the part of the instructor. Its best use would be to introduce students to how transactions are processed and how processing makes use of master data to process transactions across the value chain. SAP Overview SAP (Systems, Applications and Products in Data Processing) started operations in Germany in 1972. It is the world’s largest vendor of standard application software, the fourth largest software vendor in the world, and the market leader in enterprise applications software. The most current version of R/3 utilizes client server technology and contains over 30,000 relational data tables that enable a company to link its business processes in a real-time environment. Each instance (installation) of SAP can be distinctively configured to fit the needs and requirements of customer operations (within limits). Basic SAP Modules Flya Kite utilizes the five “basic” modules of SAP R/3 as described in the following table.

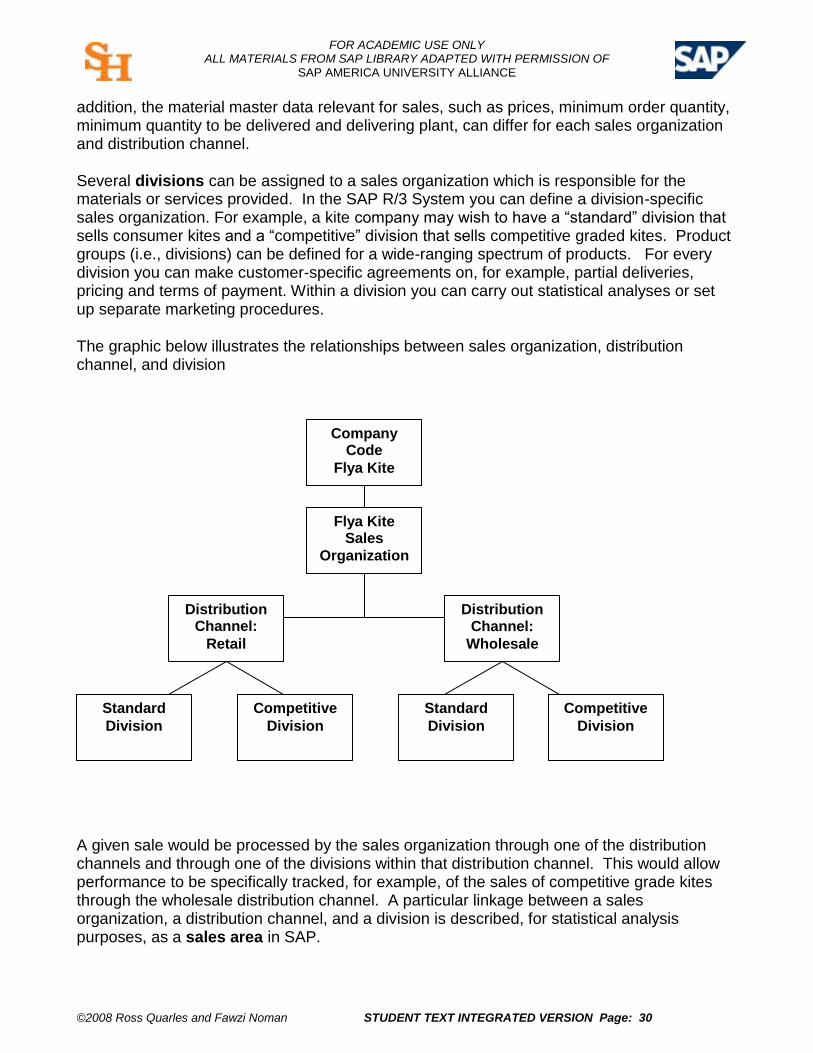

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 4

SAP Module

Function (Process) Functional Areas

MM Materials Management (Procurement Logistics)

Purchasing, invoice verification, inventory management, warehouse management

PP Production / MRP (Production Logistics)

MRP, production orders, bills of materials, work centers, routing instructions, batch management

SD Sales and Distribution (Sales Logistics)

Order entry, picking/packing/shipping, invoicing, inquiries, quotes, sales reporting

FI Financial Accounting (Support Process)

General ledger, A/R, A/PAY financial reporting, cash management legal consolidation

CO Cost Accounting (Support Process)

Cost accounting and internal reporting by cost center, internal order, project, profit center, or other unit, profitability analysis

HR Human Resources (Support Process)

Employee master data, training records gross/net calculation, payroll, planning and reporting

The various modules of SAP R/3 are highly integrated. Much of the data in the system are shared. The table below indicates some of the sharing aspects of master data in SAP.

Master Data Record Modules Using Record

General Ledger Accounts FI, CO, SD,MM, PP, HR

Customer Master Records FI, SD

Vendor Master Records FI, MM, PP

Material Master Records SD, MM, PP, CO

SAP General Terms There are a number of terms that have specific usage and meaning in dealing with SAP. Some of these general terms are identified below.

Client: The highest level in a SAP instance. A client is a self contained unit with a separate set of master records and its own set of configuration tables. An instance (installation) can have more than one client (e.g., a training client, a testing client, and a production client). In using SAP the user logs on to a particular client that usually has a three digit numeric identifier. Company Code: Represents an independent legal accounting entity that contains a balanced set of books as required by law or regulation. A client may have more than one company code (e.g. a company code for the US, one for Germany, one for Canada, etc.) Chart of Accounts: A list of all accounts in the General Ledger for a company code. Each company code must be assigned one, and only one chart of accounts. However, more than one company code can use the same (i.e., identical) chart of accounts. SAP comes preconfigured with a large number of charts of account. For example, the

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 5

delivered US chart of accounts is CAUS. Accounts can be added to, deleted from, or modified in the delivered chart of accounts as desired by the user. Passwords: Each user has his or her own password. On the initial log in to the system, the user must change a generic delivered password to his/her own. The password must be at least three characters long, cannot begin with a “!” or “?”, and the first three characters unique and not contained in the user name. Roles and Profiles: Roles specify the sets of tasks or activities that can be performed by a particular user within the system. A role is assigned to each user. When the user logs on, the system automatically presents a specific menu for that user’s assigned role. For example, a receiving clerk can perform only certain tasks within the SAP system. When a receiving clerk logs on, that user’s role will define what the user will be allowed to view, create, change, delete, etc. Profiles work in the same manner as do roles to restrict authorization for access to the system. User profiles and roles are entered by system administrators into user master records thus enabling users to access and use specific functions within the system. In the Flya Kite case, users will have authorization to all master data and transaction processing applications. This would be highly unusual in actual practice given the need for internal controls and separation of duties. Session: Each instance in which a user is connected to the SAP system is known as a session. A user can have up to nine sessions open at any given time (but each session is logged into the same client and company code). Configuration: Configuration is table-driven customization of the SAP system to meet specific customer requirements. In configuration the user sets values in tables to cause the system to function in a desired manner. Configuration is somewhat like setting the defaults in a word process or spreadsheet application. It does not change the underlying source code in the system. In the Flya Kite case there are no configuration exercises. The case system has been preconfigured.

Business Processes A business process can be described as a set of linked activities that transform an input into a more valuable output thus creating value. In many cases business processes are classified as operational processes or as support processes. At the most basic level, a typical business utilizes three operational processes: procurement (purchasing and materials management), production, and sales and distribution (customer order management). The typical support processes include accounting/controlling and human resources. While these processes have specific identities, they are linked together (integrated) in order to carry out the day to day activities of a business. For example, the sale of a manufactured product involves not only the sales process but also production (the creation of the product), procurement (of necessary raw materials), accounting/controlling to determine the profit on the sale, and human resources to ensure the operations are staffed with qualified or trained employees. These linkages of activities across business processes necessitate the sharing of data across those processes, regardless of which process created the data initially. For example, data

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 6

related to a finished product may be initially created in the production process, but the data are also required in the procurement process and, of course, in accounting/controlling for costing purposes, as well as in calculating pay based on work production hours. SAP as an integrated ERP system utilizes the principle of a common data record for a given object that can be accessed by any process that has need of the various attributes contained in that common record. Business processes are often viewed as elements of a logistics value chains. From this perspective the operational processes are defined as sales logistics, production logistics, and procurement logistics. This is the approach taken in the overall structure of the Flya Kite case. The case is separated into the sections as outlined below. Types of Data There are three differing types of data within the SAP system: control or configuration data, master data, and transaction data. Control or configuration data include system and technical functions of the SAP system itself. These data drive the logic of the applications within the system and is primarily used for defining the details of business processes. For the Flya Kite case, all control/configuration data have been pre-established so that no configuration is necessary to complete the case exercises. Master data represent the various business entities present in the system, both internal and external. For example, master data include internal entities such as the company, a plant, a sales area, a cost center, an account, a material, a routing, a bill of material, or a personnel file. In addition there are external entities that are a part of the system’s master data such as vendors, customers, employees, and even competitors. From one perspective, master data can be thought of as providing the “which” or the “what” that is of interest in the activities of the business process. The attributes of the fields within master data are relatively stable. For example, the master data for a customer containing specific values for the customer’s attributes such as name, address, delivery priority, terms of payment, etc. vary little over time. Once the master data record for the customer is set up in the system, it is rarely changed. Also, once set up within the system, it can also be accessed by any business process that may have use for the master data. For example, a customer master record may be used in sales, transportation and shipping, production, marketing, accounting, or any other process that may have use for data contained in the master record. The sets of exercises in Flya Kite contain optional exercises that can be used to set up master data for each of the logistics areas and for accounting. If these optional exercises are not assigned or completed, the case contains pre-established master data records for each process that can be used to process transactions in the transaction processing exercises. As an additional alternative, the optional exercises involving creation of master data can also be used to create additional master data beyond that contained in the case. This allows creation of transaction processing exercises in addition to those already contained in the case. Transaction data describe a business event or may be the result of a business process. For example, a sales order would contain transaction data that have resulted from a customer placing an order to purchase a product from the company. The various attributes necessary to process that sales order transaction would include such data as the customer (which allows detailed customer data to be drawn from the customer master record), the item or

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 7

items being sold (which would draw data from the material master records for those items), the quantities being sold, the desired delivery date, the customer PO number, etc. While the customer master data for this transaction would be the same for various sales orders to that customer, the other data such as items wanted, quantities, delivery dates, etc. would most likely vary from order to order. For this reason, transaction data vary from event to event. Transaction data may also arise as the result of the outcome of a completed business process. For example, the system may process an inquiry to determine the current stock quantity level for a raw material. That inquiry is a transaction that extracts the data for the quantity on hand in the warehouse. This too, of course, will vary over time. Other examples, pertaining to human resources, would involve the hiring of employees and pay transactions. From one perspective, therefore, transaction data can be viewed as resulting from the events or activities that are taking place in the business. The transaction data represent the recorded attributes, elements, and results or outcomes of business events and activities, and, as a result is the most volatile and frequently used data in day to day business operations. Each of the logistics and support processes addressed in Flya Kite contains exercises that require the processing of transactions through the particular process. References: Curran, Thomas A., and Andrew Ladd. SAP R/3 Business Blueprint. Upper Saddle River, NJ, Prentice Hall, 2000. McDonald, Kevin, et al. Mastering the SAP Business Information Warehouse. New York: John Wiley & Sons, 2002. Hernandez, Jose A., Jim Keogh, and Franklin F. Martinez. SAP R/3 Handbook. 3rd ed. New York: McGraw-Hill, 2006. Hayen, Roger. SAP R/3 Enterprise Software, An Introduction. New York: McGraw-Hill, 2007. SAP Help Portal. <http//help.sap.com>

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 8

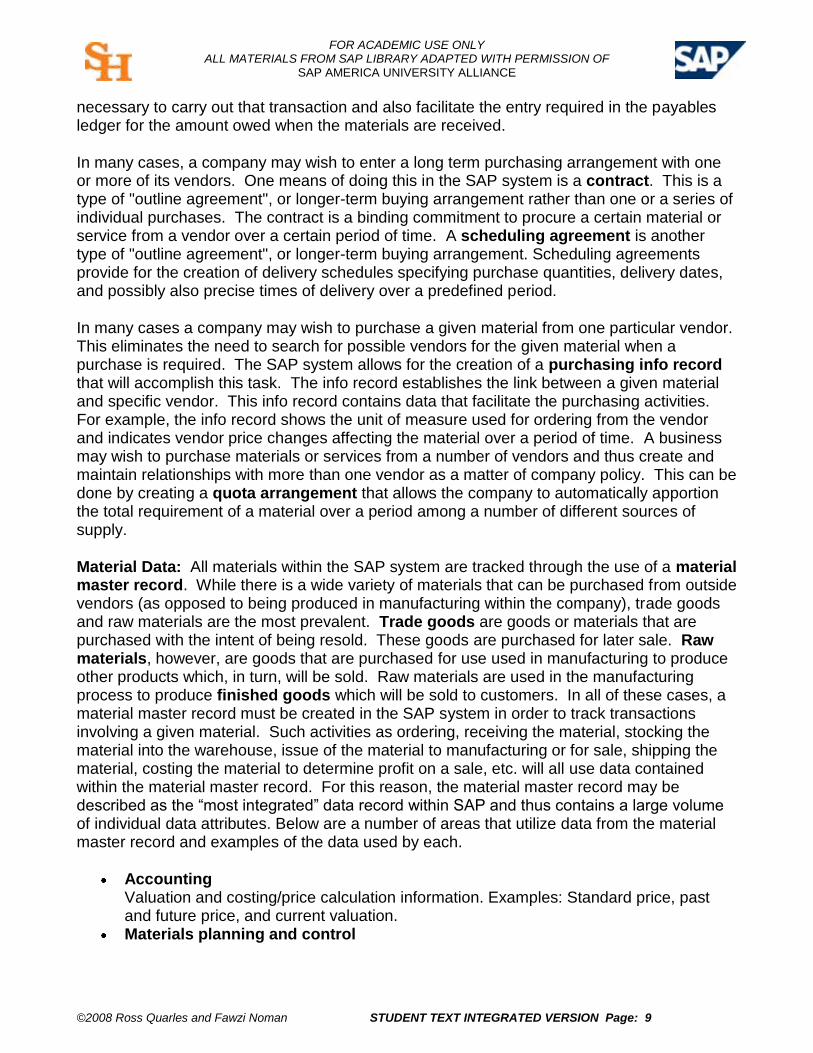

CHAPTER 2: Procurement Logistics (MM) Procurement logistics, defined as Materials Management (MM) in R/3, involves purchasing, inventory management, and warehouse operations. Materials must be ordered from vendors, received into the warehouse, issued from the warehouse for sale or for use in manufacturing, and the vendor must be paid. In all of these processes the quantities ordered and on hand, the prices to be paid, and the costs to be charged to sales or manufacturing must be tracked. The high level of integration in R/3 simplifies many of the tasks associated with these activities such as determination of the optimum source of supply, analyzing and comparing vendor pricing, issuing purchase orders, managing authorizations for purchase requisitions, and processing invoices for payment. In addition, for manufacturing firms, inventory management must be highly integrated with production planning to ensure that raw materials and components are available when production is scheduled. The graphic below identifies the process flows and master data requirements for procurement logistics processing. Vendor Data: Vendors are business partners that are suppliers of materials or services to the firm. While vendors can be internal (components of the same company), the vendors in this case are external – parties that are independent entities that are not affiliated with or a part of Flya Kite. In order to facilitate purchases from these external vendors, a vendor master record is set up within the SAP system. The attributes that are needed within the vendor master record include items such as the vendor name, address, tax jurisdiction code, language, payment terms, currency to be used, etc. These are the data items that will be of use each time a purchase is initiated with the particular vendor and do not change frequently. When a vendor master record is created in SAP, the choice can be made to let the system assign a vendor number or the user can assign the vendor number. It is generally better to allow the system to assign the vendor number thereby letting the system track numbers and thus prevent duplications. Once the vendor number is assigned, that becomes the key value used to track business activities with the vendor. The vendor number not only tracks the purchasing transactions with the vendor, it also serves as that vendor’s account number in the accounts payable subsidiary ledger in the Financial Accounting (FI) module of SAP. If the company wishes to purchase something from a given vendor, inputting that vendor’s number in the purchase order will automatically reference and access all vendor master data

Vendor Data

Invoice

Verification

Goods

Receipt Purchasing Purchase

Requisition

Material Data

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 9

necessary to carry out that transaction and also facilitate the entry required in the payables ledger for the amount owed when the materials are received.

In many cases, a company may wish to enter a long term purchasing arrangement with one or more of its vendors. One means of doing this in the SAP system is a contract. This is a type of "outline agreement", or longer-term buying arrangement rather than one or a series of individual purchases. The contract is a binding commitment to procure a certain material or service from a vendor over a certain period of time. A scheduling agreement is another type of "outline agreement", or longer-term buying arrangement. Scheduling agreements provide for the creation of delivery schedules specifying purchase quantities, delivery dates, and possibly also precise times of delivery over a predefined period.

In many cases a company may wish to purchase a given material from one particular vendor. This eliminates the need to search for possible vendors for the given material when a purchase is required. The SAP system allows for the creation of a purchasing info record that will accomplish this task. The info record establishes the link between a given material and specific vendor. This info record contains data that facilitate the purchasing activities. For example, the info record shows the unit of measure used for ordering from the vendor and indicates vendor price changes affecting the material over a period of time. A business may wish to purchase materials or services from a number of vendors and thus create and maintain relationships with more than one vendor as a matter of company policy. This can be done by creating a quota arrangement that allows the company to automatically apportion the total requirement of a material over a period among a number of different sources of supply.

Material Data: All materials within the SAP system are tracked through the use of a material master record. While there is a wide variety of materials that can be purchased from outside vendors (as opposed to being produced in manufacturing within the company), trade goods and raw materials are the most prevalent. Trade goods are goods or materials that are purchased with the intent of being resold. These goods are purchased for later sale. Raw materials, however, are goods that are purchased for use used in manufacturing to produce other products which, in turn, will be sold. Raw materials are used in the manufacturing process to produce finished goods which will be sold to customers. In all of these cases, a material master record must be created in the SAP system in order to track transactions involving a given material. Such activities as ordering, receiving the material, stocking the material into the warehouse, issue of the material to manufacturing or for sale, shipping the material, costing the material to determine profit on a sale, etc. will all use data contained within the material master record. For this reason, the material master record may be described as the “most integrated” data record within SAP and thus contains a large volume of individual data attributes. Below are a number of areas that utilize data from the material master record and examples of the data used by each.

Accounting Valuation and costing/price calculation information. Examples: Standard price, past and future price, and current valuation.

Materials planning and control

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 10

Information for material requirements planning (MRP) and consumption-based planning/inventory control. Examples: Safety stock level, planned delivery time, and reorder level for a material.

Purchasing Data provided by Purchasing for a material. Examples: Purchasing group (group of buyers) responsible for a material, over- and underdelivery tolerances, and the order unit.

Engineering Engineering and design data on a material. Examples: CAD drawings, basic dimensions, and design specifications.

Storage Information relating to the storage/warehousing of a material. Examples: unit of issue, storage conditions, and packaging dimensions.

Forecasting Information for predicting material requirements. Examples: How the material is procured, forecasting period, and past consumption/usage.

Sales and distribution Information for sales orders and pricing. Examples: Sales price, minimum order quantity, and the name of the sales department responsible for a certain material

For each of these and for all areas that access material master records for transaction processing, only the data pertinent for that particular area are presented in a view for the area. The view for each area must be created. For example, the sales view for a material must be created that includes items such as the transportation group for route determination and the loading group for determination of the type of equipment required in order to move the material into the shipping area from the warehouse.

A unique number is assigned to each material master record. This number identifies a specific material. Material numbers can be assigned internally or externally. Internal number assignment means that the system assigns material numbers, whereas external number assignment means that the person creating the material master record does so. Once this number is assigned, it is used to track the material throughout the SAP system.

The material master record contains attributes of the given material such as the description of the material, the units of measure (e.g., base or stockkeeping unit, order unit, sales unit, unit of issue), material type (e.g. trading, finished, raw material), gross and net weight (with and without packaging, respectively) and weight units (e.g., lbs, ounces, kilos, etc.), price (e.g., standard, moving average), packaging material required for sale, loading group (e.g., forklift, crane, handcart), country of origin, shelf life, and transportation group (e.g., on pallets, in liquid form, etc).

Procurement logistics transaction process flows: From an overall perspective, the logistics value chain processes involve obtaining purchased materials from suppliers, monitoring the status of those purchases, and receiving the items into inventory. The process involves the creation of a purchase requisition followed by the creation of a purchase order, the receipt of goods into inventory, the receipt of an invoice for the acquisition, and the payment of that invoice.

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 11

Purchase Requisition

A purchase requisition is an internal document (one that is used within the company only) that instructs the purchasing department to initiate steps to buy a material or procure a service by a certain date. This request may come from an individual who is authorized to request such a purchase or it may come from the MRP (materials requirement planning) system. The MRP system uses a number of statistical methods to anticipate future demand for a given stock item. That demand is balanced with the current quantity and other demand needs of the item to determine the need to acquire a given additional quantity of the item at some date in the future. If the company has not yet determined the vendor for the item and created a vendor master record in the SAP system, the purchasing department must identify the appropriate vendor and create that master record. If the vendor has been previously identified and the appropriate record created in the system, purchasing can then proceed to the processing of a purchase order to acquire the material from the vendor. The integration within the SAP system allows the data from the requisition such as the material number, quantity needed, desired delivery date, etc. to automatically populate the purchase order.

Purchasing (Purchase Order)

A purchase order is a legally binding instruction from a purchasing organization to a vendor to delivery a quantity of material or to perform a service at a given time at an agreed upon price. The purchase order contains data such as the required material, the quantity to be delivered, the price, terms of delivery, etc. The purchase order can also include a storage location in the warehouse where the material will be stored when received. This storage location is, of course, for internal use only and is of no use to the vendor. If the vendor accepts the purchase order, the material will be delivered as per the requirements established in the purchase order.

Goods Receipt

When ordered materials arrive from the vendor, a goods receipt must be processed in order to receive the material into inventory and update the quantity records for the material. As soon as the ordered goods arrive, the goods receipt is posted. The material is thus recorded in the inventory management system. The goods receipt triggers quality inspection and placement of the material into storage (stock putaway), and settlement with regard to the goods received.

If a material is delivered for a purchase order, it is important for all of the departments involved that the goods receipt entry in the system references this purchase order, for the following reasons:

Goods receiving can check whether the delivery actually corresponds to the order. The system can propose data from the purchase order during entry of the goods

receipt (for example, the material ordered, its quantity, and so on). This simplifies both data entry and checking (overdeliveries and underdeliveries).

The delivery is marked in the purchase order history. This allows the Purchasing department to monitor the purchase order history and initiate reminder procedures in the event of a late delivery.

The vendor invoice is checked against the ordered quantity and the delivered quantity.

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 12

The goods receipt is valuated on the basis of the purchase order price or the invoice price.

If material is intended for stocking into the warehouse, the purchase order data can define a storage location for it. This storage location is then automatically proposed by the system during entry of the goods receipt and can be accepted or changed. If no storage location is entered in the purchase order, the storage location must be specified when the goods receipt is entered.

Goods receipts for the warehouse can be posted to three different stock types: To unrestricted-use stock: stock located in the warehouse that is not subject to any

kind of usage restrictions. To stock in quality inspection: stock that has been received but is in the process of

incoming quality inspection and which has not yet been released for unrestricted use. To blocked stock: stock that is present in the company but, for various reasons, is not

to be used and cannot be classified as unrestricted.

The purchase order data can define whether or not the material is to be posted to stock in quality inspection. However, at the time of goods receipt the decision as to which stock type the material is posted can be revised.

When a goods receipt is entered into the system a number of other activities occur and updates take place.

Creation of a Material Document: When the goods receipt is posted, the system automatically creates a material document which serves as proof of the goods movement from receiving to the warehouse. Creation of an Accounting Document: Parallel to the material document, the system creates an accounting document. The accounting document contains the posting lines (for the corresponding accounts) that are necessary for the movement. Creation of a Goods Receipt/Issue Slip: When the goods receipt is entered, a goods receipt/issue slip can be printed at the same time. Sending a Mail Message to Purchasing: If the goods receipt message indicator has been set in the purchase order, the buyer automatically receives a message informing him/her of the delivery. Stock Update: Which stocks are updated in the material master record depends on the destination of the goods:

Goods receipt into the warehouse: If the goods are destined for the warehouse, the system increases total valuated stock and the stock type (for example, the unrestricted-use stock) by the delivered quantity. The stock value is updated at the same time.

Goods receipt into consumption: If the goods are destined for consumption, only the consumption statistics are updated in the material master record.

Goods receipt into goods receipt blocked stock: If the goods receipt is posted into goods receipt blocked stock, the stock level remains the same. The goods are recorded only in goods receipt blocked stock of the purchase order history.

Goods receipt into a new storage location: If goods are posted into a storage location that does not yet exist for this material, the storage location is

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 13

automatically created in the material master record when the goods receipt is posted (if automatic creation of the storage location is allowed for both the plant). If automatic creation is not allowed, the user must add the new storage location to the material master record before a goods receipt to it can be posted.

Update of General Ledger Accounts: When the goods receipt is posted, the system automatically updates the G/L accounts by the value of the goods receipt. Updates can also occur in other related applications. In the case of a goods receipt to consumption, for example, the account assignment object (such as a cost center, order, asset, etc.) is debited. Updates in the Purchase Order: When a goods receipt is posted, the following purchasing data are updated:

Purchase order history: During goods receipt posting, a purchase order history record is automatically created. This record contains data essential for Purchasing, such as: the delivered quantity, the material document number and item, the movement type, and the posting date of the goods receipt.

Purchase order item: If the "delivery completed" indicator is set in the material document, the order item is considered closed, and the open purchase order quantity is set to zero.

Other Updates: Depending on the characteristics of the material, movement, and components used, additional updates are carried out in other components. For example, a goods receipt is relevant for:

Entries to be made in the planning file or independent requirements reduction in materials planning

Statistical data in Inventory Controlling Vendor evaluation data in Purchasing Transfer requirements and quantities in the Warehouse Management System Inspection lots in Quality Management

Invoice Verification

The invoice verification component of the Materials Management (MM) system provides the link between the Materials Management and the Financial Accounting, Controlling, and Asset Accounting components.

Invoice Verification in Materials Management serves the following purposes: It completes the materials procurement process - which starts with the purchase

requisition, continues with purchasing and goods receipt, and ends with the invoice receipt

It allows invoices that do not originate in materials procurement (for example, services, expenses, course costs, etc.) to be processed

It allows credit memos to be processed, either as invoice cancellations or discounts Invoice Verification does not handle the payment or the analysis of invoices. The information required for these processes is passed on to other departments. Invoice Verification tasks include:

Entering invoices and credit memos that have been received Checking the accuracy of invoices with respect to contents, prices, and arithmetic

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 14

Executing the account postings resulting from an invoice Updating certain data in the SAP system such as open items and material prices Checking invoices that were blocked because they varied too greatly from the

purchase order

Each invoice contains various items of information. To post an invoice, this information is entered into the system. If an invoice refers to an existing transaction, certain items of information will already be available in the system. The system proposes this information as default data so that the user only needs to compare it and, if necessary, correct any possible variances. If an invoice refers to a purchase order, for example, the user only needs to enter the number of the purchase order. The system selects the right transaction and proposes data from the purchase order, including the vendor, material, quantity ordered, terms of delivery, terms of payment. This default data can be overwritten if there are variances. The system can display the purchase order history to show, for example, which quantities have been delivered and how much has already been invoiced.

If variances exist between the purchase order or goods receipt and the invoice, the system will issue a warning on the screen. If the variances are within the preset tolerance limits, the system will allow the invoice to be posted but will automatically block it for payment. The invoice must then be released in a separate step. If the variances are not within the tolerances, the system will not allow the invoice to be posted.

When the invoice is entered, the system also finds the relevant account. Automatic postings for sales tax, cash discount clearing, and price variances are also generated and the posting records displayed. If a balance is created, the user is required to make corrections, as an invoice can only be posted if the balance equals zero.

As soon as the invoice is posted, certain data, such as the average price of the material ordered and the purchase order history, are updated in the system.

The invoice posting completes invoice verification. The data necessary for the invoice to be paid are now contained in the system. The accounting department can retrieve the data and make the appropriate payments with the aid of the Financial Accounting component.

As a rule, an invoice refers to a transaction for which the issuing party requests payment. Invoice Verification differs depending on the type of invoice involved.

Invoices based on purchase orders: With purchase-order-based Invoice Verification, all the items of a purchase order can be settled together, regardless of whether an item has been received in several partial deliveries. All the deliveries are totaled and posted as one item.

Invoices based on goods receipt: With goods-receipt-based Invoice Verification, each individual goods receipt is invoiced separately.

Invoices without an order reference: When there is no reference to a purchase order, it is possible to post the transaction directly to a material account, a G/L account, or an asset account.

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 15

Procurement Logistics Master Data and Transaction Exercises for Flya Kite

The following discussion outlines the general flow of the exercises that will be completed in creating master data and processing procurement logistics transactions in this case. Flya Kite will be doing business with a number of vendors (suppliers) that will provide the raw materials and trade goods used and sold by the company. In order to do business with these vendors, a master record for each must be created in the system. Master vendor records can be set up basically in two ways: (1) for each individual application separately or (2) centrally. For example, a vendor master record can be created for accounting’s use. In that case, only the accounting attributes (view) of the record will be created. If another functional area of the company wants to create a particular set of data for the same vendor, that area can add its data to existing record. For example, if accounting has already set up a vendor master record (and created a vendor master number in the system), the purchasing function can access that vendor record using the vendor number and add the purchasing data (view) it required. In cases where the vendor is to be set up centrally, all data attributes for all functions will be created at one time for the vendor. In some cases a vendor will not supply goods but will provide a service such as rental space. A vendor master record for this type of vendor is set up in the same manner as the master record for a supplier of tangible goods. These services are generally purchased under some type of contractual agreement and will not involve the physical receipt of goods from the vendor. In order to purchase raw materials from vendors, there must be a raw material master record. This master record will contain all of the basic data needed to acquire the good from the vendor. A material master record must be created for each trade good that will be purchased. Raw materials are goods that will be used in production to create finished products. Trade goods are generally sold separately as independent products, but trade goods may also be used in production as component parts of a given manufactured product. In creating finished goods from raw materials, the system must have some means of recording the use of the raw materials to produce the finished goods. This requires that a master record for each finished product be created so that the physical quantities materials used and the related costs can be transferred in the system from raw materials to finished goods as the products are completed in production. When a good is to be acquired, a decision must be made to determine what vendor will supply that good. In order to save time and resources, the company may decide to always buy a particular good from the same vendor. This eliminates the need to search for vendors for that good, to obtain bids, or to work out other details of the purchase. In the case of Flya Kite, the company has decided to acquire all raw materials and trade goods from one vendor. To create the necessary linkages in the system between the goods and that vendor, there must be a purchasing info record set up. After the creation of this record, the only user decision will be to determine when and how many items are to be purchased; the system automatically determines the vendor for these items.

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 16

When the company determines the need to acquire goods, a purchasing requisition is initiated. This requisition is an internal document in that it does not leave the company. It notifies the purchasing department that something must be acquired and allows the individual who is in the position to authorize the acquisition to do so. Once the purchase requisition has been approved, the company creates a purchase order that is sent to the vendor. A purchase order is a binding offer to buy the goods listed on the purchase order, at the stated prices, and at the other conditions specified in the purchase order. This purchase order can be delivered to the vendor by mail or electronically. Upon its receipt, the vendor will pack the requested goods and deliver them to the company under the terms of the purchase order. When goods are delivered to the company as requested in the purchase order, they must be received into the company’s inventory. Only items that have been authorized to be purchased (e.g., those that have a purchase order associated with them) should be received by the company. Otherwise, unscrupulous vendors might send goods that were not ordered and then demand payment if the company had accepted delivery of the goods. This is why the purchase order to which the goods receipt applies must be input into the system at the time of the goods receipt. Only if the goods are recorded into the company’s inventory records will the various interested parties be aware that the goods have been received and can now be used. This is accomplished by completing a receiving report identifying how many items and of what type was received in reference to a specific purchase order number. Vendors that supply goods to the company have a nasty habit of wanting to be paid for those goods. In order to ensure they get paid, they send an invoice to the company outlining what is to be paid for, when, and how much. The vendor invoice will reference the original purchase order sent in order to facilitate the processing of the invoice for payment. Invoices are not paid unless the quantities, prices, and other aspects of the invoice agree with the purchase order data and also with the receiving report. Ensuring the agreement among these three is the role of purchasing logistics invoice verification. For this reason, the purchase order must be input in the invoice receipt process to establish the linkage between the purchase order and the vendor invoice. Before an invoice can be released to accounting to make a payment, the data from the purchase order, the receiving report, and the vendor invoice must be in agreement. For example, if the purchase order requested 100 items of a particular good, the receiving report indicated that 125 were received, and the vendor invoice indicated that 150 were to be paid for, the company would not wish to make this payment until these discrepancies were resolved.

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 17

CHAPTER 3: Production Logistics (PP)

The primary elements of production logistics are material requirements planning and production planning. Their main function is to guarantee material availability, that is, it is used to procure or produce the requirement quantities on time both for internal purposes and for sales and distribution. This process involves the monitoring of stocks and, in particular, the automatic creation of procurement proposals for purchasing and production. In doing so, MRP tries to strike the best balance possible between optimizing the service level and minimizing costs and capital lockup.

The type of order proposal which is automatically generated during materials planning depends on the procurement type of the material. For materials that are produced internally, a planned order is always created. For materials procured externally, the MRP controller has the choice between creating a planned order or a purchase requisition. If the MRP controller decides to create a planned order, the planned order must then be converted into a purchase requisition to make it available for use by the purchasing department.

The MRP component of R/3 assists MRP controllers in their area of responsibility. The MRP controller is responsible for all activities related to specifying the type, quantity, and time of the requirements, in addition to calculating when and for what quantity an order proposal has to be created to cover these requirements. The MRP controller needs all the information on stocks, stock reservations, and stocks on order to calculate quantities, and also needs information on lead times and procurement times to calculate dates. The MRP controller defines a suitable MRP and lot-sizing procedure for each material to determine procurement proposals.

The Demand Management component of MRP is needed to define requirement quantities and requirements dates for finished products and important assemblies. Demand Management also determines the strategy used for planning, procuring, or producing a certain finished product. Demand Management serves to determine requirement quantities and delivery dates for finished product assemblies. Customer requirements are created in sales order management. To create a demand program, Demand Management uses planned independent requirements and customer requirements. To create the demand program, the user must define the planning strategy for a product. Planning strategies represent the methods of production for planning and manufacturing or procuring a product. Using these strategies, the user can decide if production is triggered by sales orders (make-to-order production or assemble-to-order production), or if it is not triggered by sales orders (make-to-stock production). The user can designate sales orders and stock orders in the demand program. If the production time is long in relation to the standard market delivery time, the company can produce and stock the product or certain assemblies before they are needed to fill sales orders. In this case, sales quantities are planned, for example, with the aid of a sales forecast.

The make-to-stock strategy is appropriate if the materials are not segregated (i.e., not assigned to specific sales orders) and costs need to be tracked at material level, not at sales order level. Make-to-stock production should be used if stock is to be produced independently

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 18

of orders so that customers can be immediately provided with goods from that stock at a later time. The company may even want to produce goods without related sales orders if there is an expectation of future customer demand. This means that make-to-stock strategies can support a very close customer-vendor relationship because the objective here is to provide customers with goods from stock as quickly as possible. In a make-to-stock environment, smoothing of production can be an important feature. This means irregular requirements flow resulting from different customer requirements quantities can be smoothed and simply produced to stock.

Make-to-stock strategies are usually combined with a lot-size key or a rounding value. For instance, it may be desirable to produce the entire amount for the whole month once a month only, or to produce full pallets only. No specific product structures are required for make-to-stock strategies. In other words, the material may or may not have a BOM. The material can be produced in-house or procured externally.

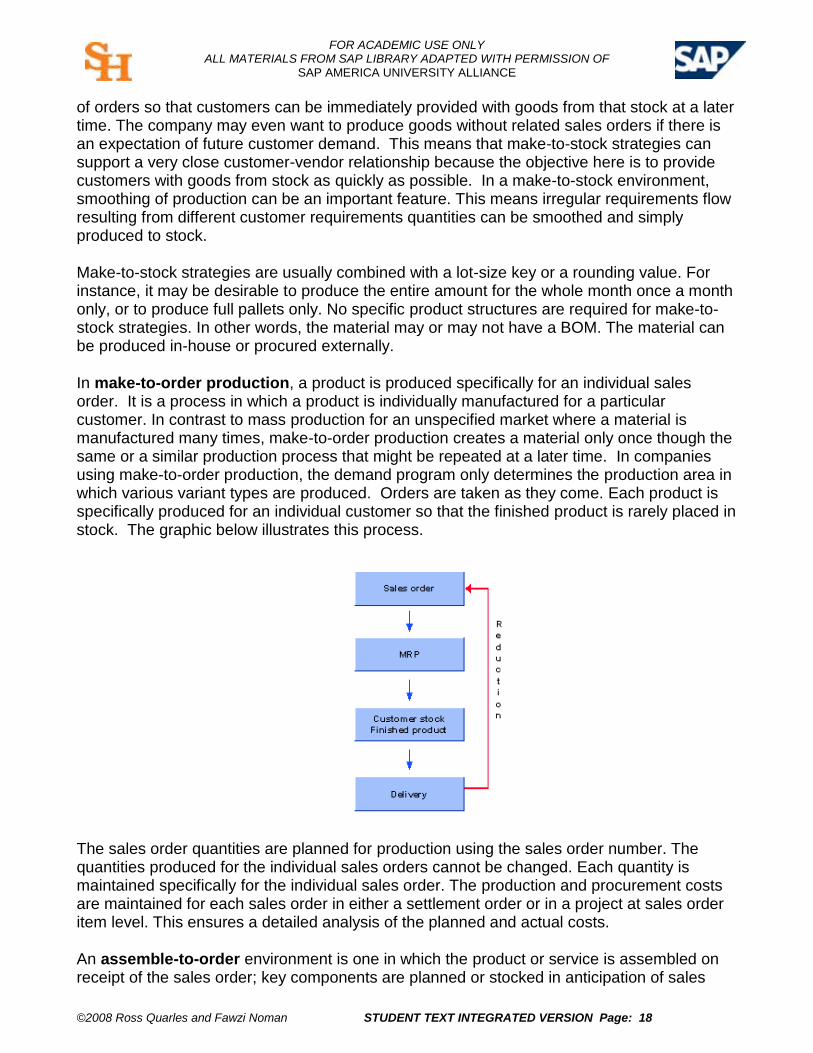

In make-to-order production, a product is produced specifically for an individual sales order. It is a process in which a product is individually manufactured for a particular customer. In contrast to mass production for an unspecified market where a material is manufactured many times, make-to-order production creates a material only once though the same or a similar production process that might be repeated at a later time. In companies using make-to-order production, the demand program only determines the production area in which various variant types are produced. Orders are taken as they come. Each product is specifically produced for an individual customer so that the finished product is rarely placed in stock. The graphic below illustrates this process.

The sales order quantities are planned for production using the sales order number. The quantities produced for the individual sales orders cannot be changed. Each quantity is maintained specifically for the individual sales order. The production and procurement costs are maintained for each sales order in either a settlement order or in a project at sales order item level. This ensures a detailed analysis of the planned and actual costs.

An assemble-to-order environment is one in which the product or service is assembled on receipt of the sales order; key components are planned or stocked in anticipation of sales

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 19

orders. Receipt of a sales order initiates the assembly of the customized product. Assemble-to-order is useful where a large number of finished products can be assembled from common components. In the R/3 System, assemble-to-order is a special type of make-to-order planning strategy. If an assemble-to-order strategy is used, material and resource availability is checked at the moment when the sales order is created. The company can quote reliable delivery dates to customers because it is known whether the desired quantity will be available on the desired date. If the complete quantity cannot be committed, the system specifies when the total quantity will be available and whether a partial quantity can be committed at an alternative date.

An important factor for ensuring that customers are provided with reliable due dates is continuous feedback between sales and production. In the R/3 System, changes to quantities or dates for production or procurement of components are passed back to the sales order of the finished product where the committed quantity or confirmation date is also changed. Similarly, changes to quantities or dates in the sales order are passed on to production and/or procurement.

Master Data in Production Logistics

The Production Planning application component provides a solution for both the production plan (type and quantity of the products) and the production process. Preparations for production include the procurement, storage, and transportation of materials and intermediate products. Integral to that process are the MRP views of master materials, bills of material, routings, and work center master data records.

MRP VIEWS FOR MATERIAL MASTER RECORDS: MRP views for material master records set up the data necessary for materials requirements planning and production planning within the raw materials and finished products master records that generally have been created in the Procurement Logistics process.2

BILLS OF MATERIALS: Bills of material (BOMs) and routings contain essential master data for integrated materials management and production control. In the design department, a new product is designed to be suitable for production and for its intended purpose. The result of this product phase is drawings and a list of all the parts required to produce the product. This list is the bill of material.

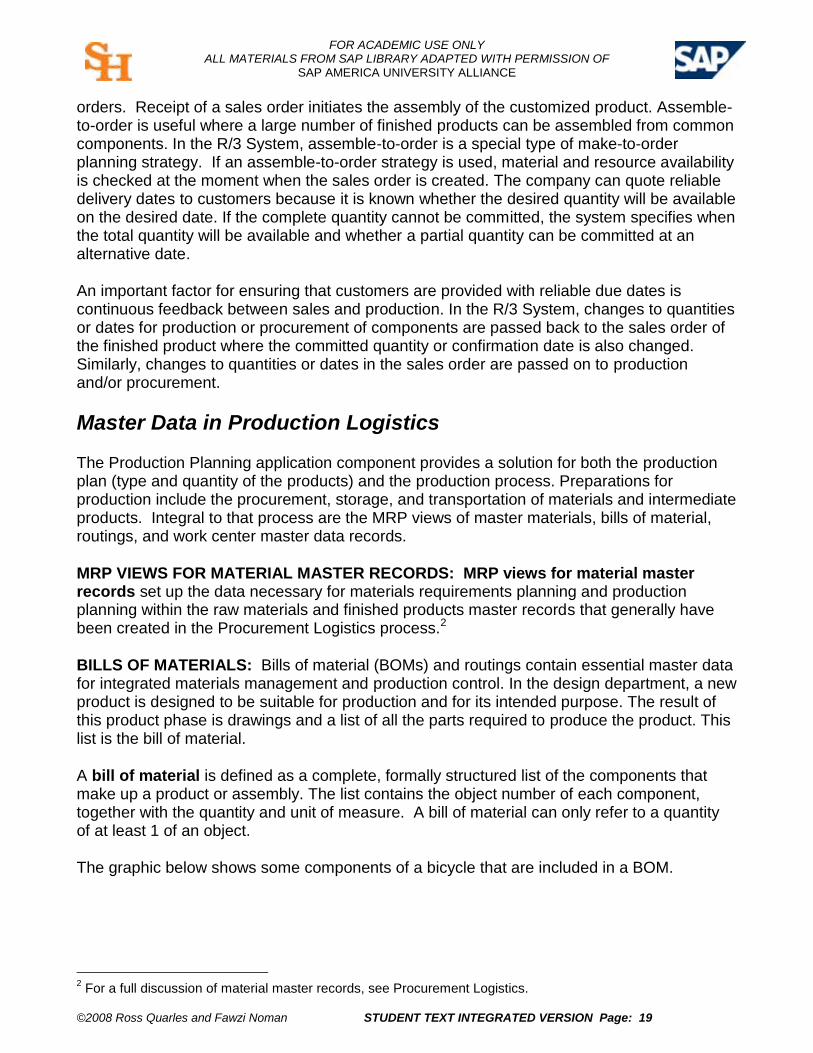

A bill of material is defined as a complete, formally structured list of the components that make up a product or assembly. The list contains the object number of each component, together with the quantity and unit of measure. A bill of material can only refer to a quantity of at least 1 of an object.

The graphic below shows some components of a bicycle that are included in a BOM.

2 For a full discussion of material master records, see Procurement Logistics.

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 20

Bills of material are used in their different forms in various situations where a finished product is assembled from several component parts or materials. Depending on the industry sector, they may also be called recipes or lists of ingredients. The structure of the product determines whether the bill of material is simple or very complex.

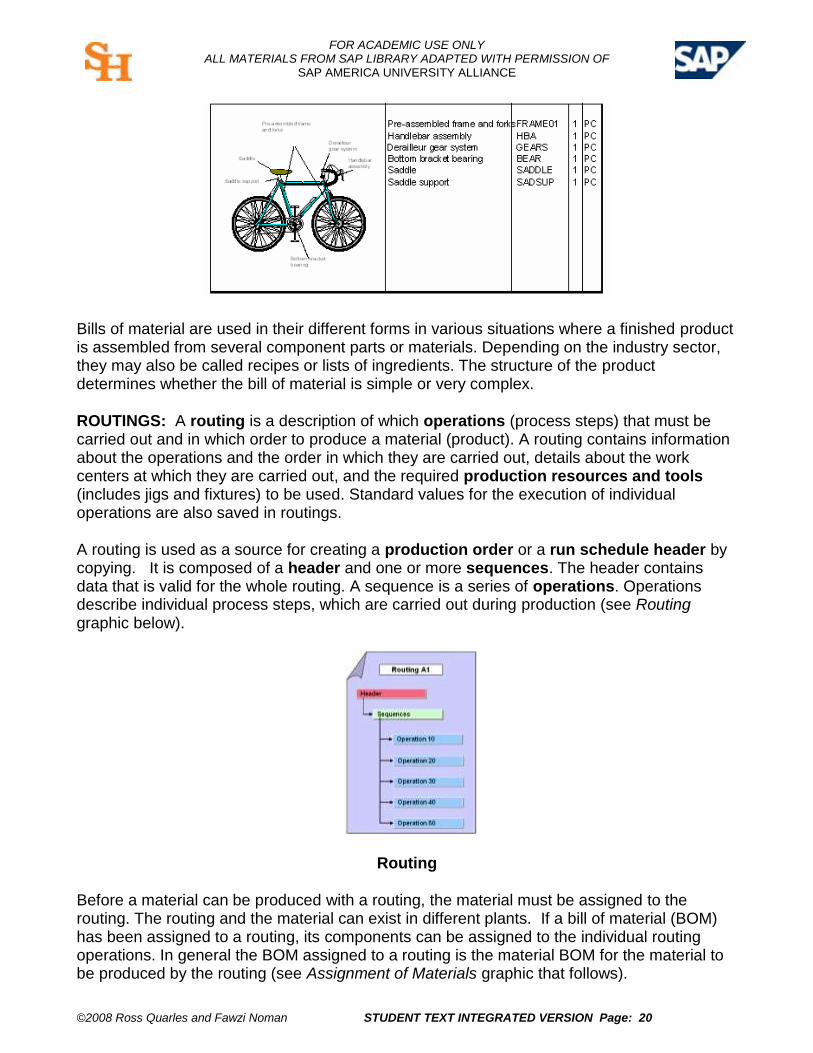

ROUTINGS: A routing is a description of which operations (process steps) that must be carried out and in which order to produce a material (product). A routing contains information about the operations and the order in which they are carried out, details about the work centers at which they are carried out, and the required production resources and tools (includes jigs and fixtures) to be used. Standard values for the execution of individual operations are also saved in routings.

A routing is used as a source for creating a production order or a run schedule header by copying. It is composed of a header and one or more sequences. The header contains data that is valid for the whole routing. A sequence is a series of operations. Operations describe individual process steps, which are carried out during production (see Routing graphic below).

Routing

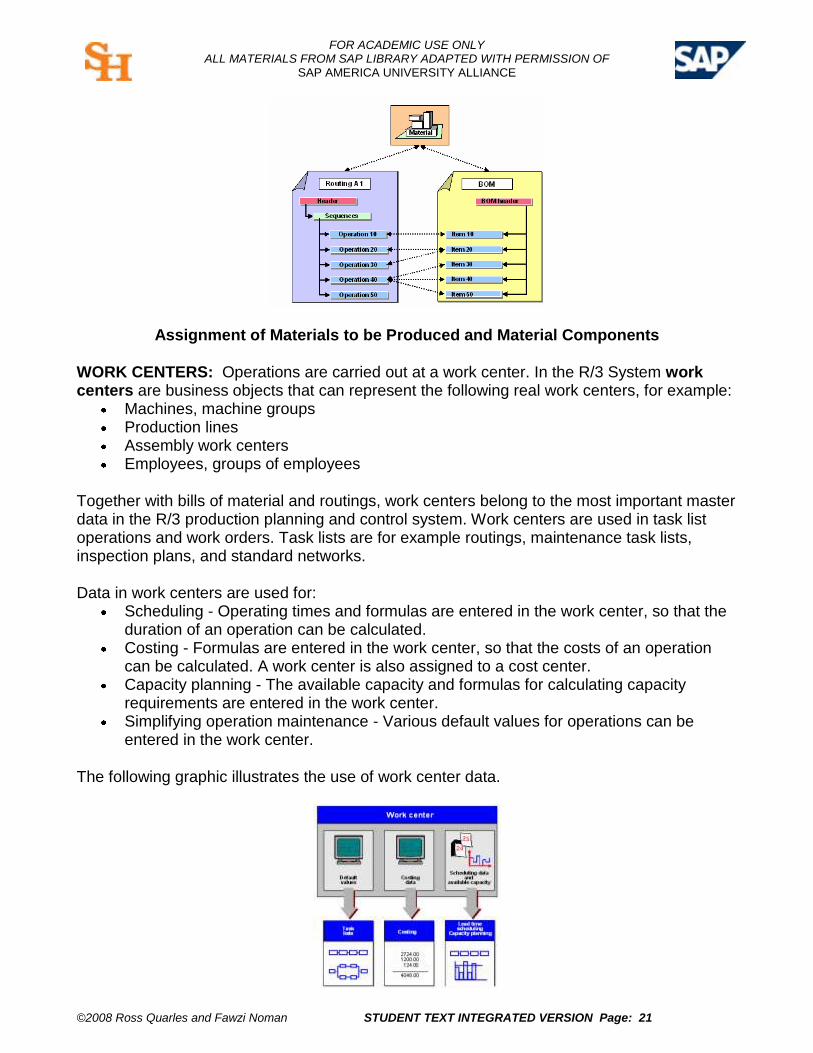

Before a material can be produced with a routing, the material must be assigned to the routing. The routing and the material can exist in different plants. If a bill of material (BOM) has been assigned to a routing, its components can be assigned to the individual routing operations. In general the BOM assigned to a routing is the material BOM for the material to be produced by the routing (see Assignment of Materials graphic that follows).

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 21

Assignment of Materials to be Produced and Material Components

WORK CENTERS: Operations are carried out at a work center. In the R/3 System work centers are business objects that can represent the following real work centers, for example:

Machines, machine groups Production lines Assembly work centers Employees, groups of employees

Together with bills of material and routings, work centers belong to the most important master data in the R/3 production planning and control system. Work centers are used in task list operations and work orders. Task lists are for example routings, maintenance task lists, inspection plans, and standard networks.

Data in work centers are used for: Scheduling - Operating times and formulas are entered in the work center, so that the

duration of an operation can be calculated. Costing - Formulas are entered in the work center, so that the costs of an operation

can be calculated. A work center is also assigned to a cost center. Capacity planning - The available capacity and formulas for calculating capacity

requirements are entered in the work center. Simplifying operation maintenance - Various default values for operations can be

entered in the work center.

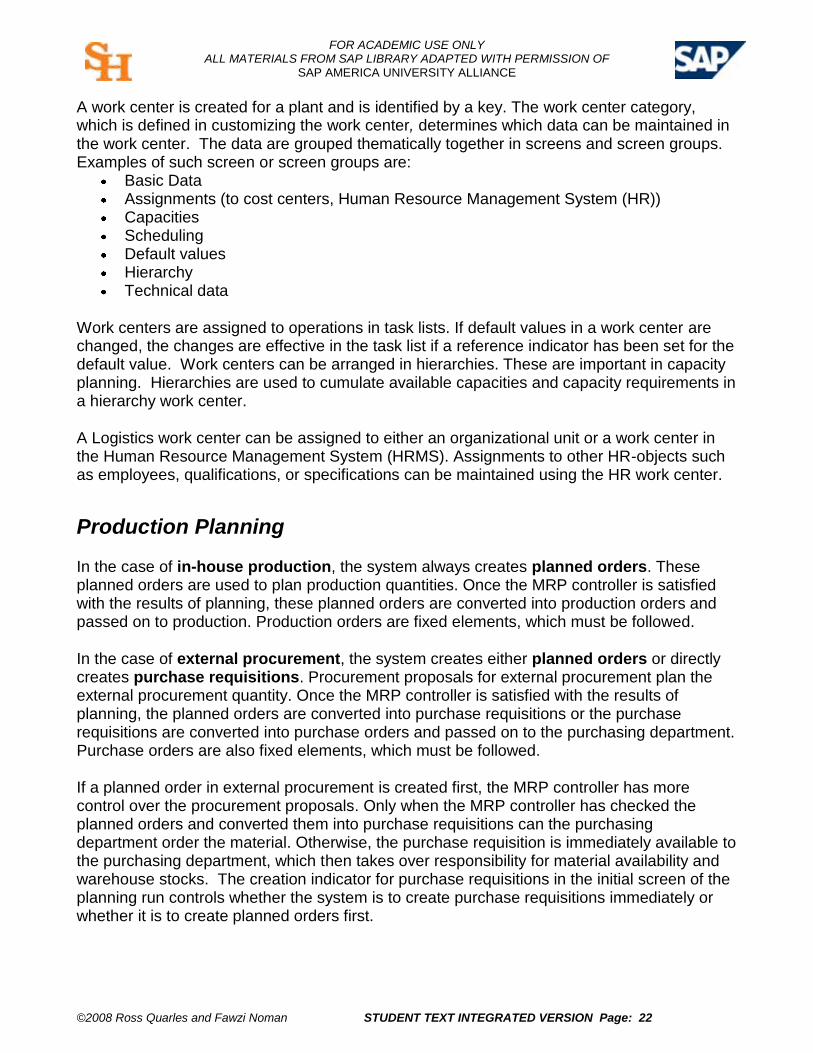

The following graphic illustrates the use of work center data.

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 22

A work center is created for a plant and is identified by a key. The work center category, which is defined in customizing the work center, determines which data can be maintained in the work center. The data are grouped thematically together in screens and screen groups. Examples of such screen or screen groups are:

Basic Data Assignments (to cost centers, Human Resource Management System (HR)) Capacities Scheduling Default values Hierarchy Technical data

Work centers are assigned to operations in task lists. If default values in a work center are changed, the changes are effective in the task list if a reference indicator has been set for the default value. Work centers can be arranged in hierarchies. These are important in capacity planning. Hierarchies are used to cumulate available capacities and capacity requirements in a hierarchy work center.

A Logistics work center can be assigned to either an organizational unit or a work center in the Human Resource Management System (HRMS). Assignments to other HR-objects such as employees, qualifications, or specifications can be maintained using the HR work center.

Production Planning

In the case of in-house production, the system always creates planned orders. These planned orders are used to plan production quantities. Once the MRP controller is satisfied with the results of planning, these planned orders are converted into production orders and passed on to production. Production orders are fixed elements, which must be followed.

In the case of external procurement, the system creates either planned orders or directly creates purchase requisitions. Procurement proposals for external procurement plan the external procurement quantity. Once the MRP controller is satisfied with the results of planning, the planned orders are converted into purchase requisitions or the purchase requisitions are converted into purchase orders and passed on to the purchasing department. Purchase orders are also fixed elements, which must be followed.

If a planned order in external procurement is created first, the MRP controller has more control over the procurement proposals. Only when the MRP controller has checked the planned orders and converted them into purchase requisitions can the purchasing department order the material. Otherwise, the purchase requisition is immediately available to the purchasing department, which then takes over responsibility for material availability and warehouse stocks. The creation indicator for purchase requisitions in the initial screen of the planning run controls whether the system is to create purchase requisitions immediately or whether it is to create planned orders first.

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 23

If a scheduling agreement3 exists for a material and if an entry exists in the source list that is relevant to MRP, the user can also instruct the system to create delivery schedules in the planning run.

A planned order is sent to a plant and is an MRP request for the procurement of a particular material at a determined time. It specifies when the inward material movement should be made and the quantity of material that is expected.

A planned order has the following characteristics: It is a procurement proposal in MRP for requirements coverage, that is, an internal

planning element. It is not binding and does not trigger procurement directly; it serves for planning purposes only.

It can be changed or deleted at any time (exceptions: planned orders for direct production and for direct procurement).

Whether a material will later be produced in-house or procured externally is left open. For materials produced in-house, it represents the pegged requirement for dependent

requirements and can be used in the capacity calculation. For materials produced in-house, it specifies the basic dates for production.

Planned orders are converted into production orders for in-house production and into purchase requisitions for external procurement. In contrast to planned orders, production orders and purchase requisitions are fixed receipt elements, which commit to the procurement.

Automatic Creation of Planned Orders

During the MRP planning run, the system automatically calculates the materials to be procured as well as the requirements quantity and date. The system then creates the corresponding planned order.

The system also explodes the BOM for materials that are produced in-house and uses the BOM components as material components for the planned order. The system creates a corresponding dependent requirement for these components. If the quantity or the date of the planned order changes or if the bill of material changes, the bill of material is re-exploded in the next planning run and the dependent requirements of the material components are adjusted accordingly.

When the MRP system is executed, the system produces an MRP list which provides an overview of the results of the run. Any changes that have occurred between planning runs are ignored on this list. In addition, the system creates a stock/requirements list that displays all changes in stock, receipts and issues which have currently occurred. By using the MRP list and stock/requirements list comparison these two evaluations can be compared. This

3 Outline agreement on the basis of which materials are procured at a series of predefined points in time over a

certain period.

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 24

means that the user can compare the situation at the last planning run to the current stock/requirements situation.

Manual Creation of Planned Orders

Planned orders can also be created manually. For this, the material to be procured must be determined along with the quantity to be procured, the date it should be available, and whether it is to be procured externally or internally. If a planned order is created or changed manually, the user can also explode the BOM manually and adjust the material components.

The planned order consists of the following: Order data (quantities, dates, account assignment, material data, procurement data,

etc.), and Component overview.

Conversion of Planned Orders to Production Orders

Planned orders are created in material requirements planning to meet production requirements. Planned orders represent a demand to procure or produce a material. Planned orders for materials that are to be produced in-house are converted to production orders. The material components required for production are contained as items in the planned order and are copied directly when the planned order is converted to a production order.

Planned orders are internal planning elements for planning purposes and do not trigger any procurements. The system only triggers procurement, once planned orders are converted into fixed receipt elements such as purchase requisitions or production orders. Planned orders can be converted individually (one at a time) or collectively (several simultaneously).

For materials that are to be produced in-house, the planned order is converted into a production order. Production orders are a fundamental part of Production Planning and Control (PP). PP is fully integrated in the Logistics (LO) component and has, among others, interfaces to:

Sales and Distribution (SD) Materials Management (MM) Controlling (CO)

A production order defines the material to be processed, the location, the time, and how much work is required. It also defines which resources are to be used and how the order costs are to be settled. As soon as a planned order or a company-internal requirement is generated from previous planning levels (material requirements planning), shop floor control takes over the information available and adds the order-relevant data to guarantee complete order processing. Production orders are used to control production within a company and also to control cost accounting.

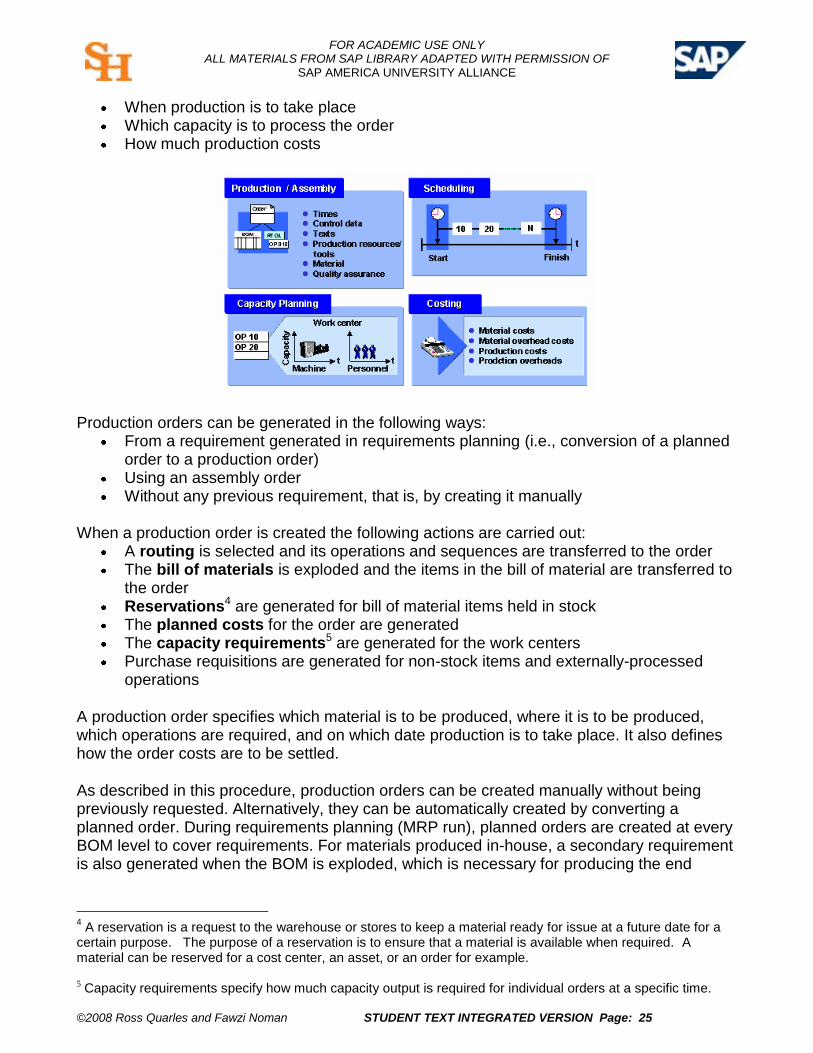

The production order can be used to specify: What is to be produced

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 25

When production is to take place Which capacity is to process the order How much production costs

Production orders can be generated in the following ways: From a requirement generated in requirements planning (i.e., conversion of a planned

order to a production order) Using an assembly order Without any previous requirement, that is, by creating it manually

When a production order is created the following actions are carried out:

A routing is selected and its operations and sequences are transferred to the order The bill of materials is exploded and the items in the bill of material are transferred to

the order Reservations4 are generated for bill of material items held in stock The planned costs for the order are generated The capacity requirements5 are generated for the work centers Purchase requisitions are generated for non-stock items and externally-processed

operations

A production order specifies which material is to be produced, where it is to be produced, which operations are required, and on which date production is to take place. It also defines how the order costs are to be settled.

As described in this procedure, production orders can be created manually without being previously requested. Alternatively, they can be automatically created by converting a planned order. During requirements planning (MRP run), planned orders are created at every BOM level to cover requirements. For materials produced in-house, a secondary requirement is also generated when the BOM is exploded, which is necessary for producing the end

4 A reservation is a request to the warehouse or stores to keep a material ready for issue at a future date for a

certain purpose. The purpose of a reservation is to ensure that a material is available when required. A material can be reserved for a cost center, an asset, or an order for example. 5 Capacity requirements specify how much capacity output is required for individual orders at a specific time.

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 26

product or assembly. For externally produced materials, an ordering transaction is initiated when a purchase requisition is generated.

Planned orders generated in the MRP run can be converted individually into production orders from the current stock/requirements list. Planned orders can also be grouped together by the MRP run and converted into production orders together. These production orders can be released together. In a partial conversion, a planned order is reduced in partial quantities into several production orders. Partial conversion is described separately.

If, when converting the planned order, changes are made to the required quantity or if the basic finish date is changed, then a planning file entry is generated. When material requirements planning is executed again, the material and its components are planned again.

The material components required for production are contained as items in the planned order and are copied directly when the planned order is converted to a production order. The BOM is not exploded again. On conversion, the secondary requirements for the components are converted to reservations. The operation data and production resource/tool data are copied as usual from the routing for the material to be produced.

Preliminary Costing

When a production order is created and after each subsequent change to the order, the system calculates the planned order costs expected to be incurred during production. The planned costs are assigned to cost elements. Those cost elements are primary costs and secondary costs. Primary costs (material costs and costs for external procurement/external processing) are assigned to the order, for example, via primary costs, such as material withdrawals or the purchasing of externally processed parts. Secondary costs (production costs, material overhead costs, and production overhead costs) are allocated to the order via internal cost allocation. When a production order is settled (after the production is completed), the actual costs incurred for the order are settled to one or more receiver cost-objects (for example, to the account for the material produced or to a sales order). Offsetting entries are generated automatically to credit the production order. If the costs for the production order are settled to a material account, the order is credited each time material is delivered to stock. The material stock account is debited accordingly. If the costs for the production order are settled to another receiver (for example to a sales order), the production order is credited automatically at the time of settlement. The cost-objects (material account or sales order) are debited accordingly. The debit posting remains in the order and can be displayed even after the costs have been settled. The settled costs are updated in the corresponding receiver cost-object and can be displayed in reporting.

Scheduling

The plant activities involved in the production of materials must be scheduled to meet the promised delivery times and to optimize the production resources of the plant. In scheduling,

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 27

the system calculates the start and finish dates of orders or of operations within an order. The time of an operation can be divided into the queue time, setup time, processing time, teardown time, and wait time. In addition to these operation segments, a move time can be defined in the system. The move time is the time needed to move a material from one work center to the next one. Move time is always between two operations and is assigned to the preceding operation. These times along with the required delivery date, the available capacity in the plant, and the raw materials availability dates are used to determine when the actual production will begin and be completed.

Scheduling can be order-related or non order-related:

Order-related scheduling is carried out for planned orders. Planned orders can be scheduled using the in-house production time in a material master record and the routing. The determined dates are saved.

Non order-related scheduling is carried out using routings. This type of scheduling can be used to calculate the in-house production time of a material and compare it to the lot size-independent in-house production time from the material master record. The lot size-independent in-house production time from the material master record can then be automatically or manually adjusted.

Completion of Production

When the production of the order is completed, a completion confirmation is entered into the system to confirm both the completion of the order and the quantity of materials produced. In order to track the movement of the completed goods from production into, for example, the warehouse and also into finished goods inventory, a goods receipt is posted. This automatically creates a material document which serves as proof of the goods movement. Parallel to the creation of the material document, the system creates an accounting document that contains the posting lines to record the movement of the cost of the goods from production to finished goods inventory.

Factory Calendar

The SAP system contains a calendar in which working days are numbered sequentially. The factory calendar is defined on the basis of a public holiday calendar. The validity period of a factory calendar must be within the validity period of the public holiday calendar. The weekdays that are working days must also be specified in this calendar.

Examples: Monday through Friday are working days. Saturday, Sunday and public holidays are non-working days.

The system will not allow production orders to be released on non-work days or on holidays. For the Flya Kite case, where users may be working on weekends and holidays, the system has been configured with a special factory calendar that ignores these non-working days so that the exercises can be completed at any time.

FOR ACADEMIC USE ONLY ALL MATERIALS FROM SAP LIBRARY ADAPTED WITH PERMISSION OF

SAP AMERICA UNIVERSITY ALLIANCE

©2008 Ross Quarles and Fawzi Noman STUDENT TEXT INTEGRATED VERSION Page: 28

Production Logistics Master Data and Transaction Exercises for Flya Kite