Embed Size (px)

Citation preview

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

NOTE: If you are seeking CPE credit, you must listen via your computer — phone listening is no

longer permitted.

Structuring Special Needs Trusts as IRA

Beneficiaries: Avoiding Tax Traps in

Funding SNTs With Retirement Accounts

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

TUESDAY, APRIL 19, 2016

Presenting a live 90-minute webinar with interactive Q&A

Elizabeth L. Gray, Principal, McCandlish Lillard, Fairfax, Va.

Scott K. Tippett, Attorney, The Tippett Law Firm, Oak Ridge, N.C.

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-961-9091 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address the

problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

NOTE: If you are seeking CPE credit, you must listen via your computer — phone

listening is no longer permitted.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email that you

will receive immediately following the program.

For CPE credits, attendees must participate until the end of the Q&A session and

respond to five prompts during the program plus a single verification code. In addition,

you must confirm your participation by completing and submitting an Attendance

Affirmation/Evaluation after the webinar and include the final verification code on the

Affirmation of Attendance portion of the form.

For additional information about continuing education, call us at 1-800-926-7926 ext.

35.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

5

Structuring Special Needs Trusts as

IRA Beneficiaries

Elizabeth L. Gray, Esq.

Why? SNTs avoid many of the costly mistakes people

make when planning for a child with special needs, such

as: • Disinheriting your child

• Relying on your other children to provide for child with

special needs

• Failing to provide privacy for the child with special needs

• Inheritances = over-resources

• Personal Injury settlements = over-resources/spending all

the funds at young age leaving child destitute

Special Needs Trusts

6

Criteria for eligibility for means-based benefits:

</= $2,000 Resources & Low Income

Options:

Accept the Money

Transfer penalty period issues

Spend down the Money

No Government benefits

Special Needs Trusts

7

Benefits of SNTS:

Protects eligibility for government benefits

i. Required to be disregarded as

available income and resources for

eligibility purposes

ii. Assets in SNT are NOT owned by the

beneficiary

iii. No transfer penalty period for funding

the SNT

Special Needs Trusts

8

Benefits of SNTS, continued:

• Provides for a higher quality of life

• Provides framework for care and

management of assets

• Allows the parent to express his/her

desires for child with special needs

(Memorandum of Intent)

• Protects assets from creditors and

predators

• Extends life of assets

Special Needs Trusts

9

2 Types of Special Needs Trusts

First-party Trust

Self-settled Trust

1396p(d)(4)(A) Trust

Payback Trust

Pooled or (d)(4)(C) Trust

(d)(4)(B) or Miller Trust

Special Needs Trusts

10

2 Types of Special Needs Trusts

Third-Party Trust

Family Funded Trust

Non-Payback Trust

Special Needs Trusts

11

1st Party Special Needs Trusts

• Protects the resources of individuals with disabilities without sacrificing

their government benefits;

• Must be in writing;

• Must be irrevocable;

• Must be Inter-Vivos.

Special Needs Trusts

12

1st Party Special Needs Trusts

A trust created for the sole benefit of an individual with disabilities

when such an individual is under the age of sixty-five (65).

Trust established by the individual’s parent, grandparent, legal

guardian or court; Assets not available;

Distributions not considered income;

No penalty period for SSI & Medicaid;

Special Needs Trusts

13

1st Party Special Needs Trusts

• Gifts to this type of trust should NOT be made by third parties!

• Sole Benefit Rule: the disabled individual must be the sole

beneficiary of the trust during his/her lifetime

• Payback Provision: funeral expenses cannot be paid after death;

Multiple states = pro rata

Special Needs Trusts

14

1st Party Special Needs Trusts

Why do it?

• Reimbursement is only for Medicaid, not all public benefits

• Reimbursement is based on the actual Medicaid expenditures, not

prevailing market costs

• No interest

• Some services not covered by Medicaid

Special Needs Trusts

15

1st Party Special Needs Trusts

Please see the Fact Guide for National Trust Training

Special Needs Trusts

16

3rd-Party Special Needs Trusts

• Can direct corpus at death of the beneficiary to any individual (no

payback requirement!)

• Not described in any federal statute

• Designed to supplement, rather than supplant, government benefits

for which the individual is otherwise eligible

Special Needs Trusts

17

3rd-Party Special Needs Trusts

Why do it?

• Improves the quality of life of an individual with disabilities

• Medicaid has no right of recovery/No payback requirement

• Can be Inter-Vivos or Testamentary

• Can be for the benefit of an individual of any age

• At death of the beneficiary, any remaining money can go to other

family members

Special Needs Trusts

18

Drafting Practices & Funding the Trust

1. Where the trust is being established by a parent or

grandparent, the parent/grandparent MUST execute the

trust and SEED the trust:

Initial funding MUST be from the parent/grandparent

and NOT the beneficiary

2. Where the trust is being established by a court the order

MUST establish and direct the transfer of the beneficiary’s

assets.

Special Needs Trusts

19

Drafting Practices & Funding the Trust, continued

3. In defining the term “special needs” for distribution

purposes, SNT attorneys have traditionally included a

list of specific distributions that could be made from the

trust. This “laundry list” has proven problematic when it

includes items which Social Security later deems

improper.

Special Needs Trusts

20

Drafting Practices & Funding the Trust, continued

4. A 3rd party special needs trust must be irrevocable

to the beneficiary (POMS Rule). It was believed

that this required the trust be initially irrevocable,

but today we know that a revocable 3rd party SNT

is allowed so long as the beneficiary cannot have

access to the trust assets.

5. Even when the trust converts to irrevocable, needs

to include flexibility:

• Trust Protector

• Trust Advisory Committee

• Trustee

Special Needs Trusts

21

Drafting Practices & Funding the Trust, continued

4. A 3rd party special needs trust must be irrevocable

to the beneficiary (POMS Rule). It was believed

that this required the trust be initially irrevocable,

but today we know that a revocable 3rd party SNT

is allowed so long as the beneficiary cannot have

access to the trust assets.

5. Even when the trust converts to irrevocable, needs

to include flexibility:

• Trust Protector

• Trust Advisory Committee

• Trustee

Special Needs Trusts

22

Drafting Practices & Funding the Trust, continued

6. The advantages of the trust being revocable to the

grantor:

• Changes can easily be made

• No tax return

• Assets – if any are taxed to the grantor

• Assets get a step up in basis upon the death of the

grantor – Example – trust holding real estate

Special Needs Trusts

23

Drafting Practices & Funding the Trust, continued

6. IRA Distributions to SNT

• Accumulation Language

• Not Conduit Language

7. Crummy Powers vs. Cristofani Powers

8. ABLE Accounts together with SNTs

Special Needs Trusts

24

Drafting Practices & Funding the Trust, continued

9. The drafter of a first-party SNT should:

• immediately report the creation and funding of the

trust to the SSA and local Medicaid eligibility office

or make sure that he or she documents in writing

that he or she has educated the trustee and

beneficiary about these rules, and

• designate professional trustees who know the SSI,

Medicaid and Section 8 housing distribution rules,

or document in writing that he or she has educated

the trustee about these rules.

Special Needs Trusts

25

Drafting Practices & Funding the Trust, continued

10.With the passage of the National Defense

Authorization Act of 2015, Congress has, for the

first time, allowed military members to name

special needs trusts as beneficiaries of Survivor

Benefit Plans (SBP). This means that military

families will finally be able to direct SBPs to their

children with special needs without compromising

the childrens’ ability to access government

disability and medical benefits.

Special Needs Trusts

26

27

Thank you

Elizabeth L. Gray, Esq.

McCandlish Lillard

11350 Random Hills Road, Suite 500

Fairfax, Virginia 22030

(703) 934-1104

Structuring Special Needs Trusts as IRA

Beneficiaries

Scott K. Tippett

Why are IRAs and Qualified Plans so

important? • Approximately $14 Trillion Dollars in Qualified Plans right now;

• Approximately $5 Trillion Dollars in IRAs;

• Second most popular account in households behind checking account;

• Comprise a large percentage of personal wealth;

• Special income tax, GST and estate tax considerations;

• Governed by federal and state law;

• Beneficiaries are determined by designation form provided by the trustee/custodian.

29

What Laws Govern IRAs?

• Federal Law:

– IRC §408 and §408A – Requirements

– IRC §401 – Distribution Rules

– Other Tax Law – Income Tax, Estate Tax, GST

– Bankruptcy Law

– Private Letter Rulings, Revenue Rulings, etc.

30

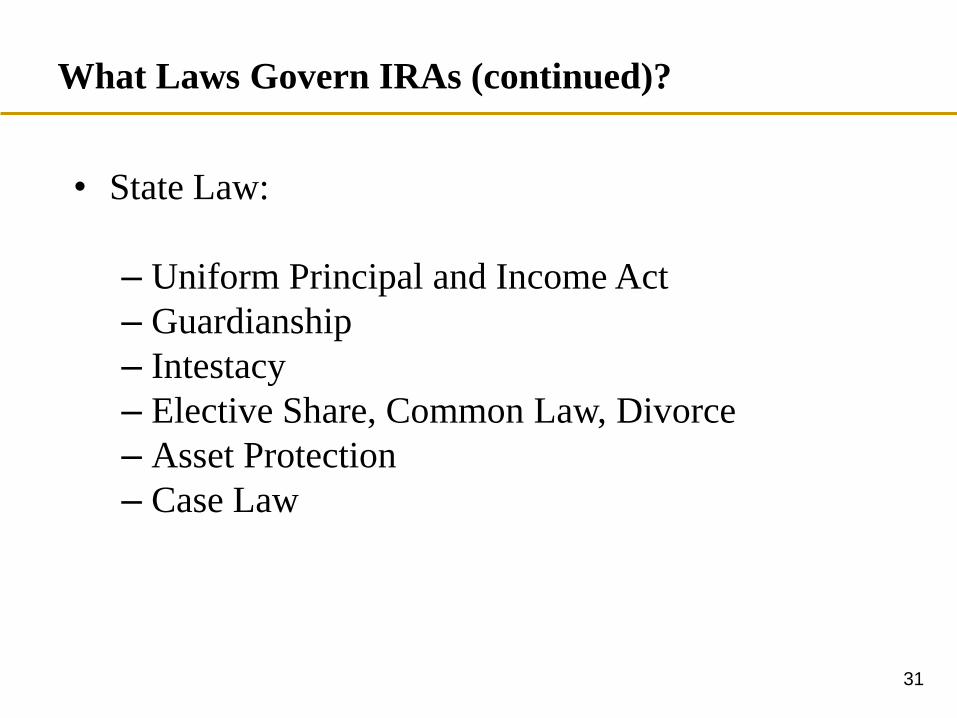

What Laws Govern IRAs (continued)?

• State Law:

– Uniform Principal and Income Act

– Guardianship

– Intestacy

– Elective Share, Common Law, Divorce

– Asset Protection

– Case Law

31

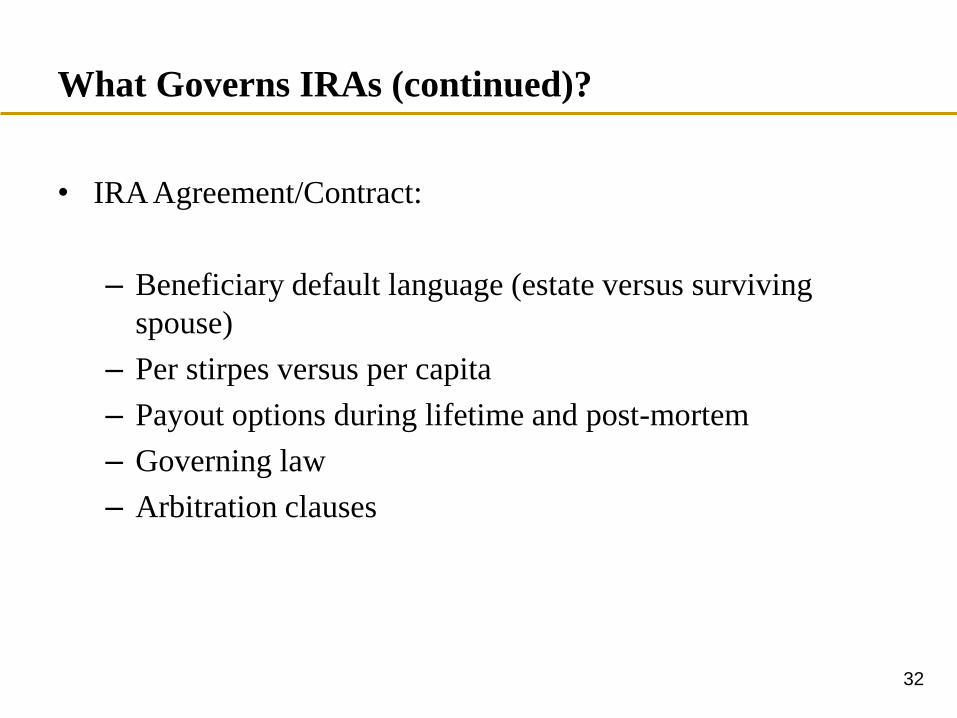

What Governs IRAs (continued)?

• IRA Agreement/Contract:

– Beneficiary default language (estate versus surviving

spouse)

– Per stirpes versus per capita

– Payout options during lifetime and post-mortem

– Governing law

– Arbitration clauses

32

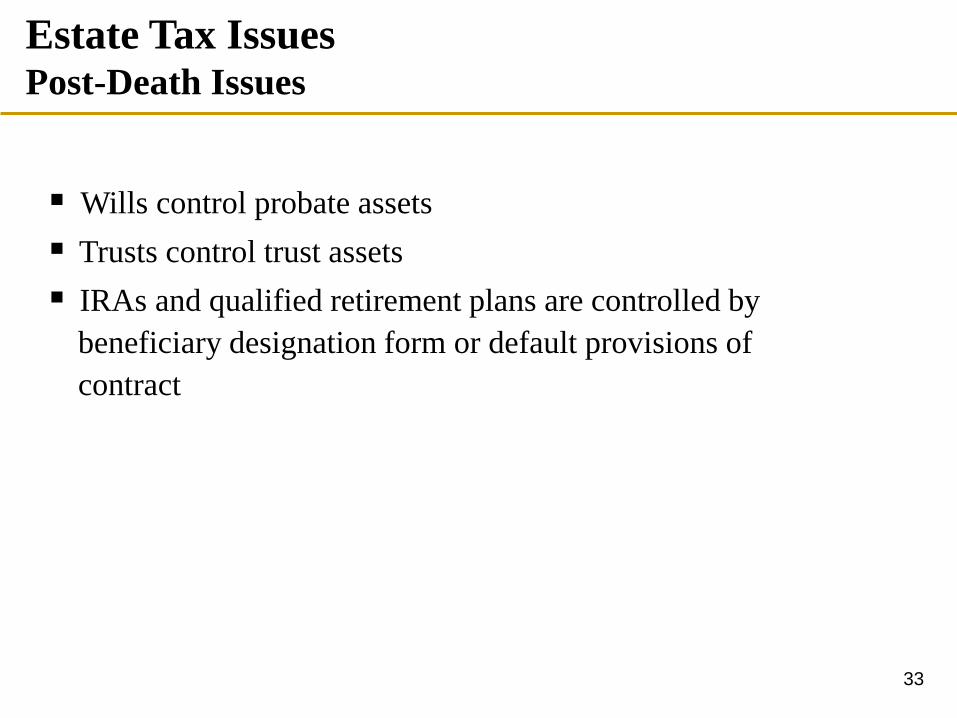

Estate Tax Issues Post-Death Issues

Wills control probate assets

Trusts control trust assets

IRAs and qualified retirement plans are controlled by

beneficiary designation form or default provisions of

contract

33

Estate Tax Issues Post-Death Issues

Post-death RMDs based on whether “designated beneficiary” exists

• Only “individuals” with quantifiable life expectancy can be “designated beneficiaries”

• If trust qualifies, look through to underlying trust beneficiaries

Distribution out of trust to beneficiary does not make the beneficiary the “designated beneficiary”

34

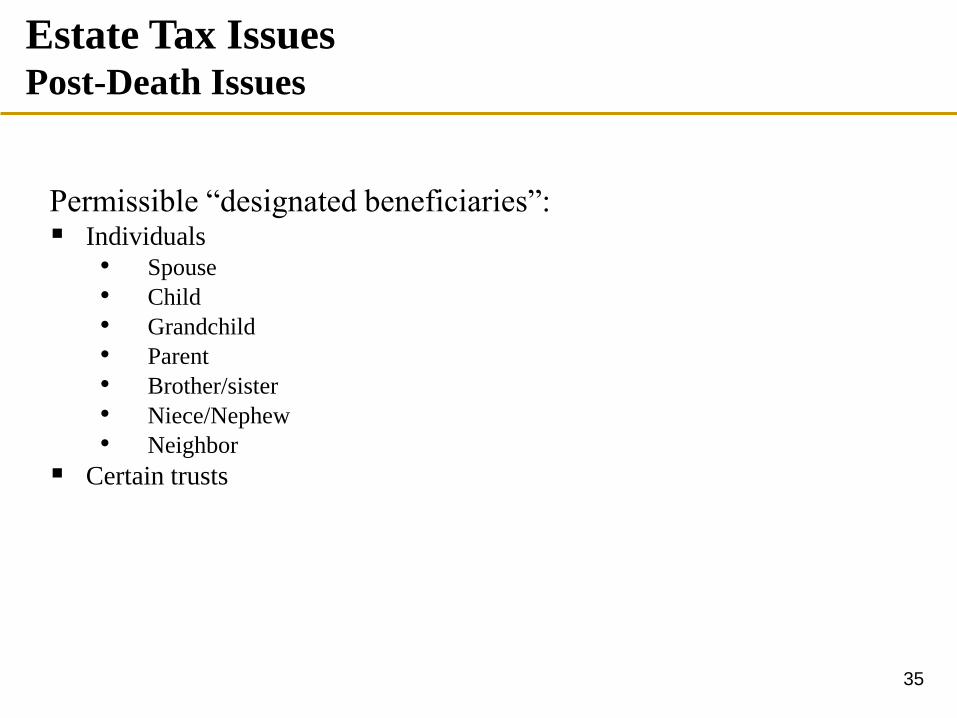

Foundation Concepts Estate Tax Issues Post-Death Issues

Permissible “designated beneficiaries”: Individuals

• Spouse

• Child

• Grandchild

• Parent

• Brother/sister

• Niece/Nephew

• Neighbor

Certain trusts

35

Foundation Concepts Estate Tax Issues Post-Death Issues

Death before age 70½

Five-year rule

Exceptions to the five-year rule

Delayed distributions – spousal beneficiary

Spousal beneficiary – special trust problem

Death after age 70½

Life expectancy distributions if you have a designated beneficiary

Distributions must begin by December 31st of the year after death

Year of death distribution – life expectancy of IRA owner

36

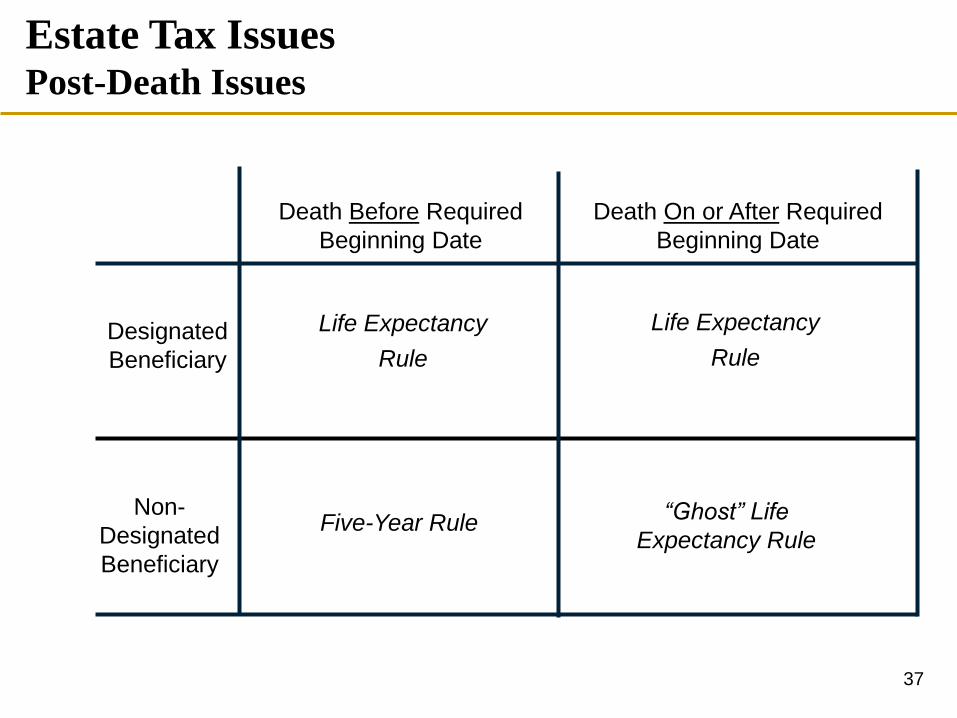

Life Expectancy

Rule

Five-Year Rule

Death Before Required

Beginning Date

Death On or After Required

Beginning Date

Designated

Beneficiary

Non-

Designated

Beneficiary

“Ghost” Life

Expectancy Rule

Foundation Concepts

Life Expectancy

Rule

Estate Tax Issues Post-Death Issues

37

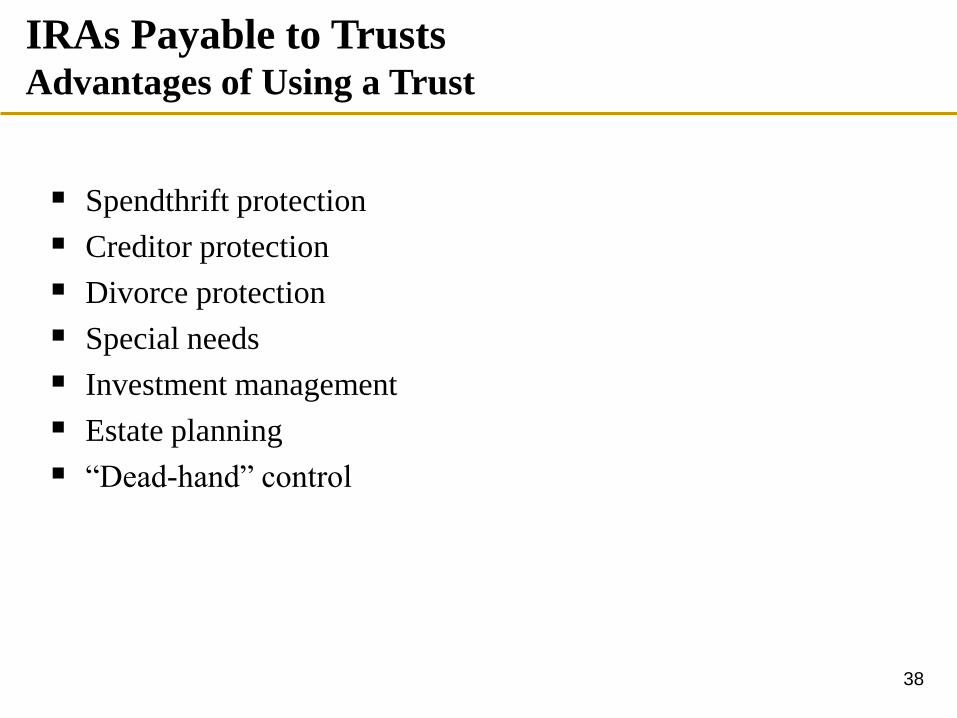

IRAs Payable to Trusts Advantages of Using a Trust

Spendthrift protection

Creditor protection

Divorce protection

Special needs

Investment management

Estate planning

“Dead-hand” control

38

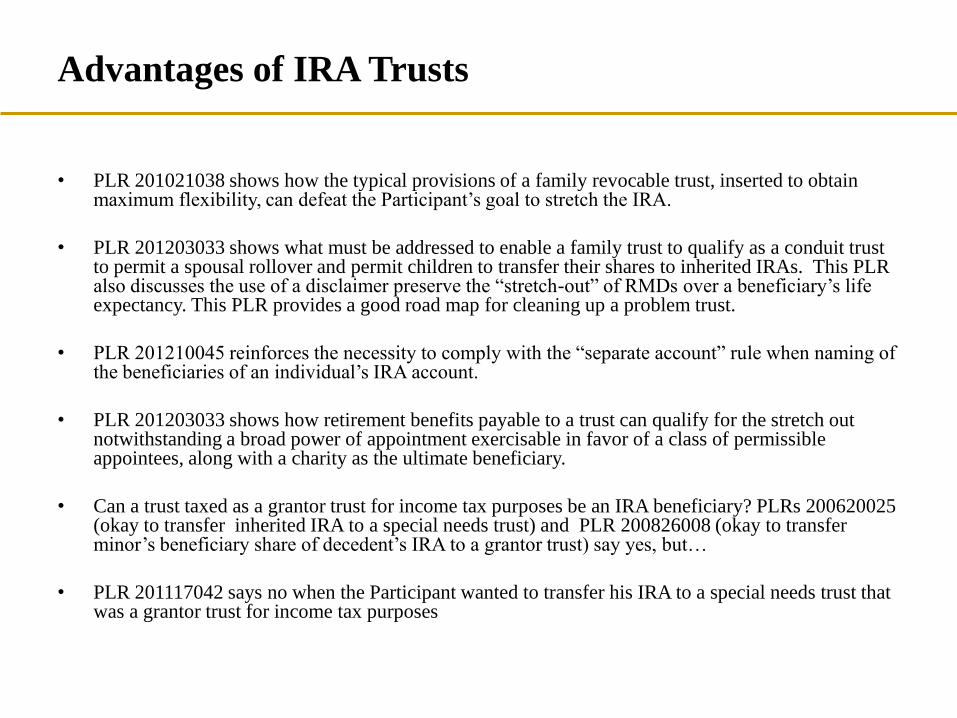

Advantages of IRA Trusts

• PLR 201021038 shows how the typical provisions of a family revocable trust, inserted to obtain maximum flexibility, can defeat the Participant’s goal to stretch the IRA.

• PLR 201203033 shows what must be addressed to enable a family trust to qualify as a conduit trust to permit a spousal rollover and permit children to transfer their shares to inherited IRAs. This PLR also discusses the use of a disclaimer preserve the “stretch-out” of RMDs over a beneficiary’s life expectancy. This PLR provides a good road map for cleaning up a problem trust.

• PLR 201210045 reinforces the necessity to comply with the “separate account” rule when naming of the beneficiaries of an individual’s IRA account.

• PLR 201203033 shows how retirement benefits payable to a trust can qualify for the stretch out notwithstanding a broad power of appointment exercisable in favor of a class of permissible appointees, along with a charity as the ultimate beneficiary.

• Can a trust taxed as a grantor trust for income tax purposes be an IRA beneficiary? PLRs 200620025 (okay to transfer inherited IRA to a special needs trust) and PLR 200826008 (okay to transfer minor’s beneficiary share of decedent’s IRA to a grantor trust) say yes, but…

• PLR 201117042 says no when the Participant wanted to transfer his IRA to a special needs trust that was a grantor trust for income tax purposes

IRAs Payable to Trusts Disadvantages of Using a Trust

Trust tax rates

Legal and trustee fees

Trust income tax returns

• 1041

• 1099

• K-1

Greater complexity

40

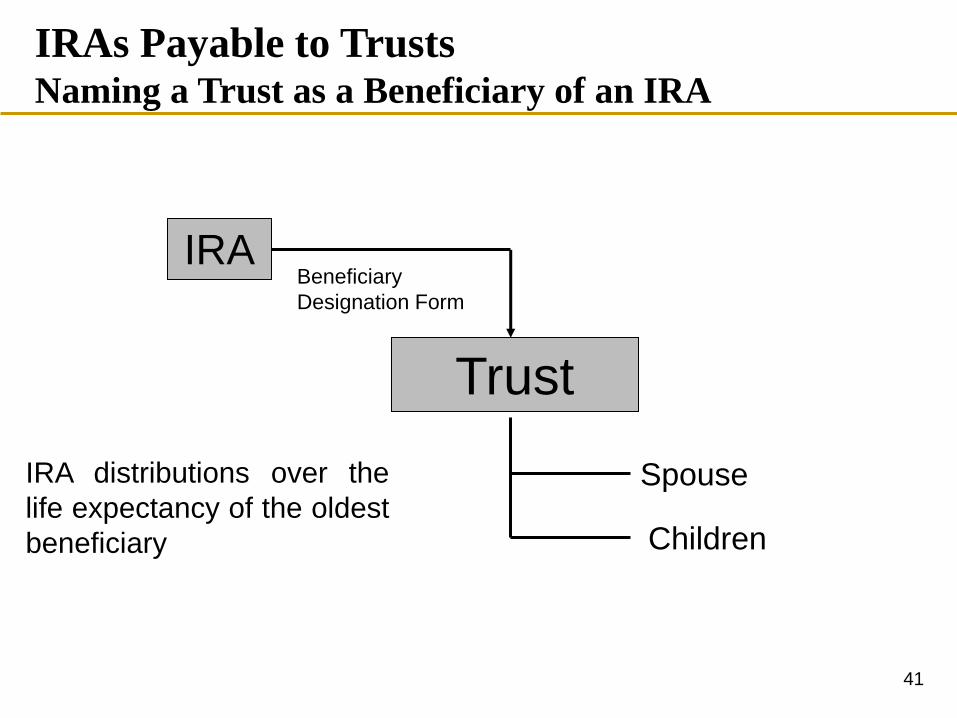

IRA distributions over the

life expectancy of the oldest

beneficiary

Trust

IRA Beneficiary

Designation Form

Spouse

Children

IRAs Payable to Trusts Naming a Trust as a Beneficiary of an IRA

41

2. Trust is irrevocable upon death of owner

− Treas. Reg. § 1.401(a)(9)-4, Q&A 5(b)(2)

3. Beneficiaries of the trust are identifiable from the trust instrument − Treas. Reg. § 1.401(a)(9)-4, Q&A 5(b)(3)

4. Documentation requirement is satisfied − Treas. Reg. § 1.401(a)(9)-4, Q&A 5(b)(4)

IRAs Payable to Trusts Naming a Trust as a Beneficiary of an IRA

Four Requirements

1. Trust is valid under state law − Treas. Reg. § 1.401(a)(9)-4, Q&A 5(b)(1)

42

IRAs Payable to Trusts Naming a Trust as a Beneficiary of an IRA

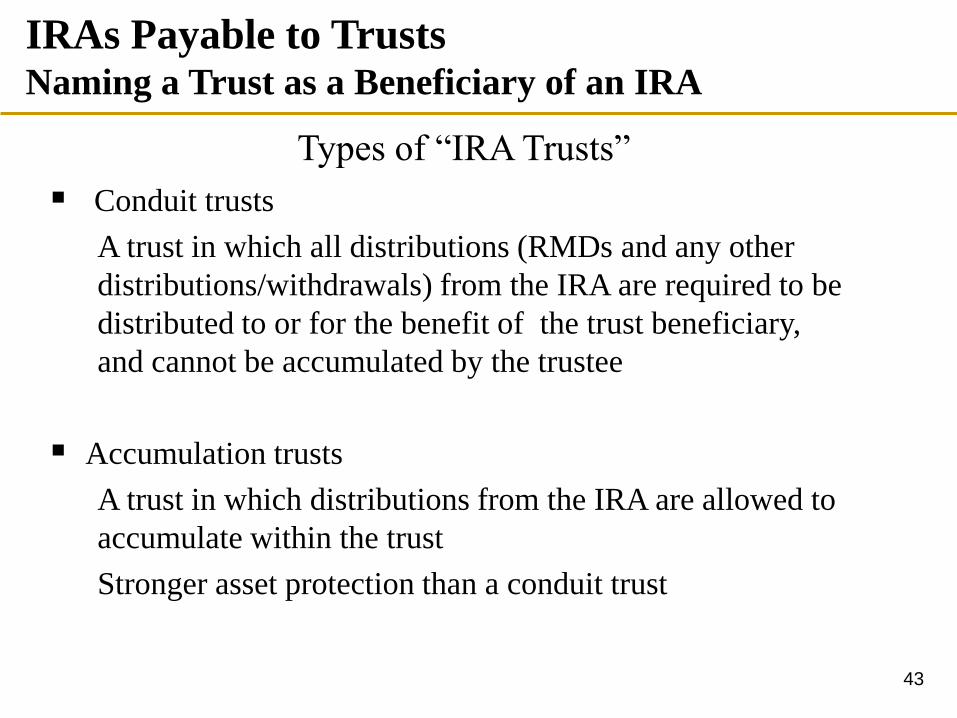

Types of “IRA Trusts”

Conduit trusts

A trust in which all distributions (RMDs and any other

distributions/withdrawals) from the IRA are required to be

distributed to or for the benefit of the trust beneficiary,

and cannot be accumulated by the trustee

Accumulation trusts

A trust in which distributions from the IRA are allowed to

accumulate within the trust

Stronger asset protection than a conduit trust

43

Conduit Trusts as SNTs

Conduit Trusts

-- Conduit beneficiary could potentially receive the entire IRA balance if the beneficiary lives to full life expectancy.

-- Contingent trust beneficiaries (charities, the conduit bene’s spouse, siblings, issue, appointees under a testamentary general or limited power of appointment are “mere potential successors” and do not have to be counted.

Conduit Trusts as SNTs

• If the trust document allows the trustee to

withdraw more than the RMDs, then any of

those withdrawals must also be distributed to

or for the benefit of the conduit trust

beneficiary.

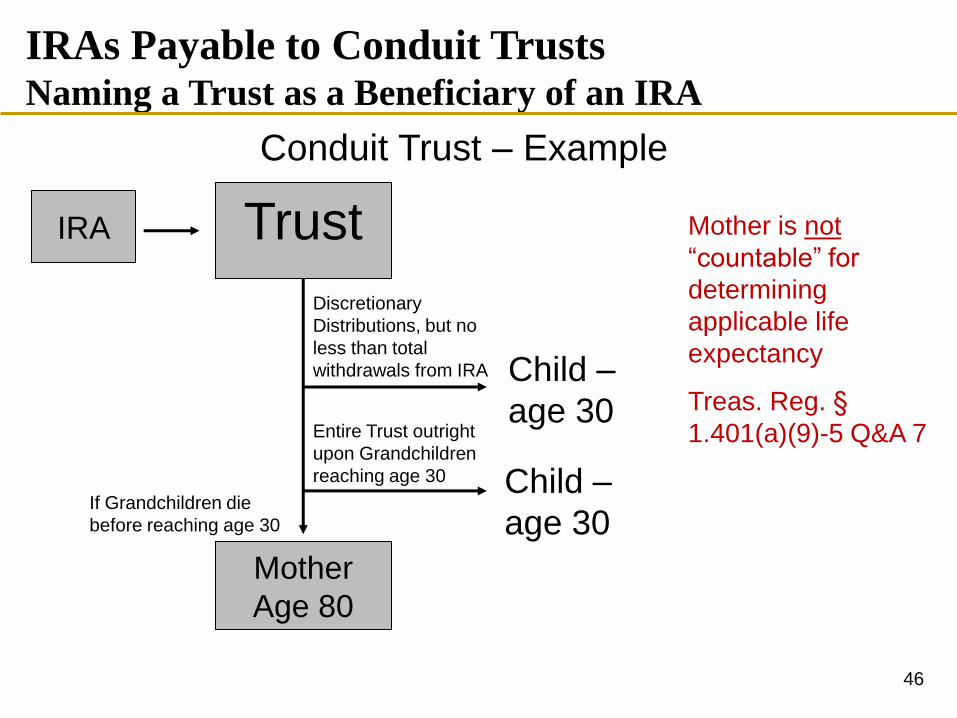

Mother

Age 80

Trust

Discretionary

Distributions, but no

less than total

withdrawals from IRA

Entire Trust outright

upon Grandchildren

reaching age 30

If Grandchildren die

before reaching age 30

Mother is not

“countable” for

determining

applicable life

expectancy

Treas. Reg. §

1.401(a)(9)-5 Q&A 7

Child –

age 30

Child –

age 30

IRA

IRAs Payable to Conduit Trusts Naming a Trust as a Beneficiary of an IRA

Conduit Trust – Example

46

Conduit Trusts as SNTs

Is a conduit trust appropriate for a

special needs child who is receiving

and depends upon means tested

government benefits (SSI and

Medicaid)?

47

Conduit Trusts as SNTs

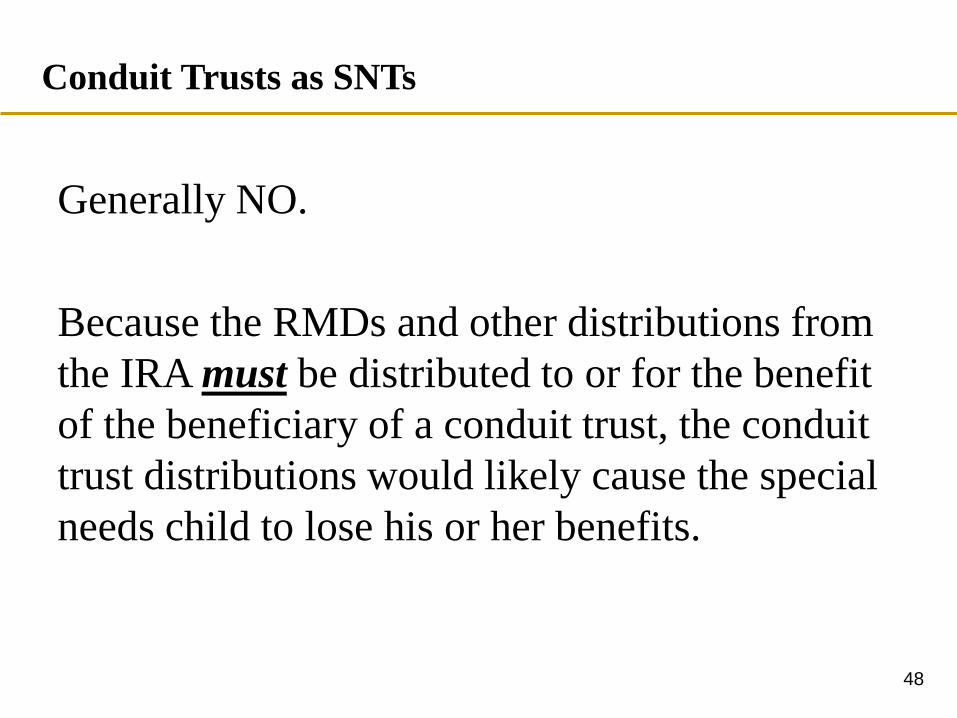

Generally NO.

Because the RMDs and other distributions from

the IRA must be distributed to or for the benefit

of the beneficiary of a conduit trust, the conduit

trust distributions would likely cause the special

needs child to lose his or her benefits.

48

Conduit Trusts as SNTs

If loss of means tested benefits is not an issue, a

conduit trust could be used to insure the benefits

are paid over the special needs beneficiary’s life

expectancy.

49

Conduit Trusts as SNTs

In this case, trust should be drafted to give the trustee broad powers to invade the IRA for changing medical, psychological, and social needs of the special needs beneficiary.

Trust should also give the trustee power to spend down the assets, as opposed to continuing the stretch-out, if the receipt of SSI and Medicaid benefits would be of greater benefit to the special needs beneficiary.

50

Conduit Trusts as SNTs

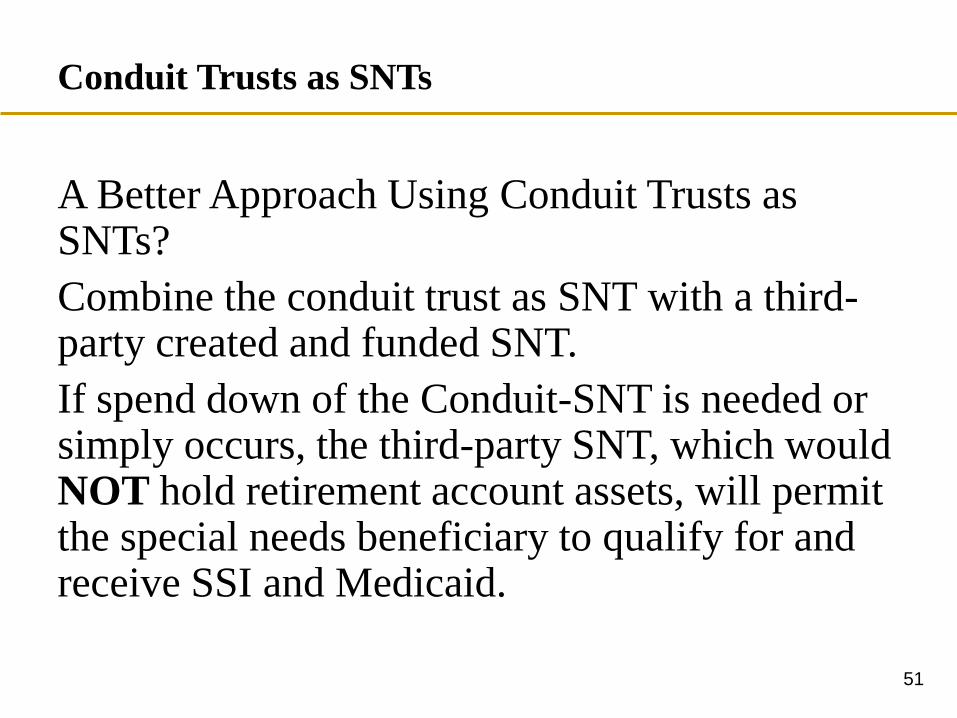

A Better Approach Using Conduit Trusts as SNTs?

Combine the conduit trust as SNT with a third-party created and funded SNT.

If spend down of the Conduit-SNT is needed or simply occurs, the third-party SNT, which would NOT hold retirement account assets, will permit the special needs beneficiary to qualify for and receive SSI and Medicaid.

51

IRAs Payable to Accumulation Trusts Naming a Trust as a Beneficiary of an IRA

Accumulation Trust

An “accumulation trust” is any trust that is not a conduit

trust, which means the trustee has the power to

“accumulate” plan distributions within the trust.

As the name implies, an accumulation trust permits the

trustee to accumulate (not distribute) RMDs and other

withdrawals to the beneficiaries.

Trustee still must be able to look through the trust and

determine which beneficiaries will receive the retirement

account proceeds.

52

Accumulation Trusts as SNTs

– The key issue in analyzing an accumulation trust is

to determine which beneficiaries are “countable.”

- All beneficiaries are countable unless such

beneficiary is deemed to be a “mere

potential successor” beneficiary.

53

Accumulation Trusts as SNTs

What if the accumulation trust is a dynasty trust so that the trust does not distribute assets outright to a beneficiary living at the account holder’s death?

Typical dynasty trust default contingent beneficiaries are charities or the grantor’s heirs at law.

These default contingent beneficiaries would probably have to be included in determining whether the trust qualifies as a see-through trust and whether the default contingent beneficiaries will be treated as “designated beneficiaries.”

54

Accumulation Trusts as SNTs

Problems: - Charity as Contingent Bene.

If a charity is named as a default contingent

beneficiary, the trust will fail as a see-through

trust because the charity is not an individual,

unless the trustee can convince the contingent

beneficiary charity to disclaim its interest by

9/30 of the year following the year of the

participant’s death.

See PLR 9820021.

55

Accumulation Trusts as SNTs

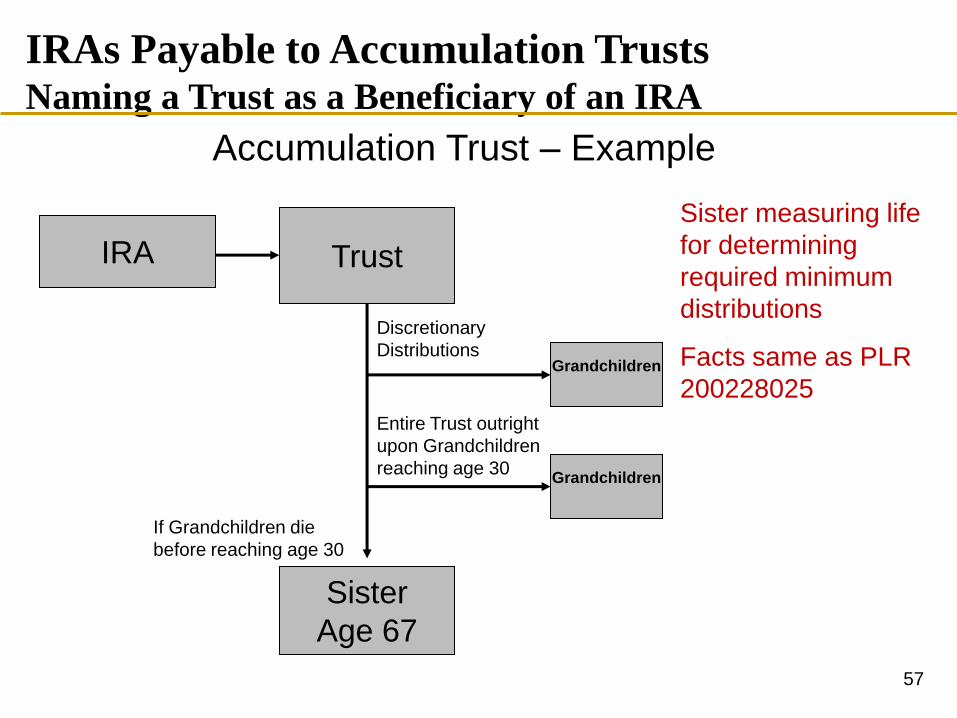

Problems: - Heirs at Law as Contingent Bene

If the account holder’s heirs at law are much

older than the intended trust beneficiary, the

payout could be over a much shorter time frame.

Recall, unless the separate share rule applies,

you must use the oldest beneficiary as the

measuring life.

56

IRA

Sister

Age 67

Grandchildren

Trust

Discretionary

Distributions

Grandchildren

Entire Trust outright

upon Grandchildren

reaching age 30

If Grandchildren die

before reaching age 30

Sister measuring life

for determining

required minimum

distributions

Facts same as PLR

200228025

IRAs Payable to Accumulation Trusts Naming a Trust as a Beneficiary of an IRA

Accumulation Trust – Example

57

Accumulation Trusts

as SNTs – Advantages

• Issues With Accumulation Trusts

• Some or all of the potential remainder beneficiaries are not

disregarded for RMD purposes, which means an accumulation

trust should not include remainder beneficiaries older than the

lifetime beneficiary.

• Contingent beneficiaries may not include one or more charities

or an undetermined surviving spouse, otherwise it may be

deemed to have no designated oldest beneficiary.

• An accumulation trust may not include a limited testamentary

power of appointment in favor of charities, surviving spouses,

or older beneficiaries.

58

Accumulation Trusts as SNTs

Accumulation trusts, where drafted as a third-party created and funded SNT usually work well for a special needs beneficiary because:

The trustee can be given sole discretion to accumulate or distribute income or principal over the special needs beneficiary’s lifetime in a manner that would not cause the loss or reduction of means tested benefits.

59

Accumulation Trusts

as SNTs-Advantages

• Modified Accumulation Trust*

• Features of a Modified Accumulation Trust

• An A share and a B share; the A share receives benefits from

all qualified plans and IRAs, the B share is everything else

• Testamentary appointees of the A share are limited to

descendants of the primary current beneficiary in the same or

younger generation as the primary current beneficiary.

• If surviving spouse is permitted appointee of the A share,

specify that surviving spouse is no older than a designated

number of years older than the primary beneficiary.

60

Accumulation Trusts

as SNTs-Advantages

• Modified Accumulation Trust

• Provides that certain remaindermen are

deemed to be predeceased in the event the

current beneficiary dies before the trust

terminates. These remindermen can receive a

preferential distribution of the B share. Can

provide for an adjustment mechanism to offset

any difference in tax consequences between

the A share and B share beneficiaries.

61

Accumulation Trusts as SNTs

• Solution to This Varied Landscape?

• An accumulation trust or modified accumulation

trust.

• With the power to accumulate, the trustee can elect to

accumulate the retirement benefits instead of passing

the benefits out to the beneficiary.

• Possible to draft trust that starts out as a conduit trust,

but a triggering event turns it into an accumulation

trust.

62

Accumulation Trusts as SNTs

Drafting Tips:

1. DO name as remainder beneficiaries, only those individuals who are younger or close in age to the special needs beneficiary.

2. DO NOT name a charity as a beneficiary or include a GPOA that can be exercised in favor of the beneficiary’s estate or another entity.

3. DO NOT give the special needs beneficiary a GPOA because that may cause the entire IRA as an available asset, thereby causing a reduction or loss of means tested benefits.

4. DO NOT give the special needs beneficiary a limited power of appointment without restricting the power to be exercised only in favor of appointees younger than the special needs beneficiary as of the date of the account owner’s death.

63

Other Drafting Considerations

• Revocable vs. Irrevocable

– Revocable

• Allows easy changes to trust

• May open IRA to account owner’s creditors at death

(Commerce Bank v. Bolander, 2007 WL 1041760, Kan.

App. 2007) – UTC state

– Irrevocable

• May not be changed, but a new trust can be drafted and

the beneficiary designation simply changed

• Protects against Commerce Bank case problem

64

Separate Share Rule

• Payable to single trust

• No separate shares identified in the beneficiary designation form

• IRA paid over oldest life expectancy

Paying IRAs to Trusts

65

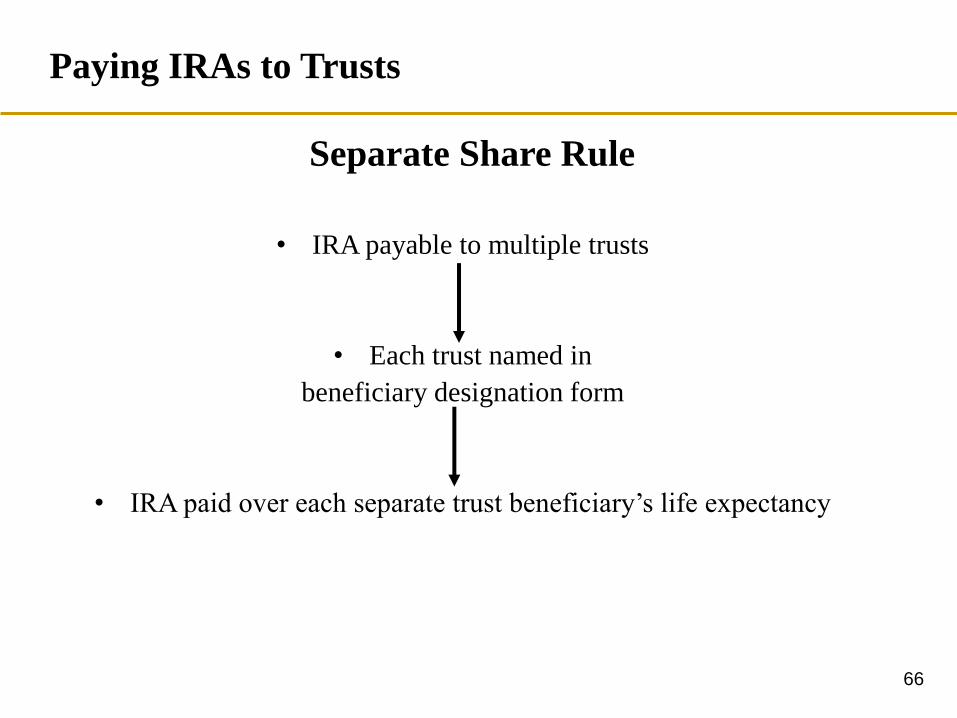

Separate Share Rule

• IRA payable to multiple trusts

• Each trust named in

beneficiary designation form

• IRA paid over each separate trust beneficiary’s life expectancy

Paying IRAs to Trusts

66

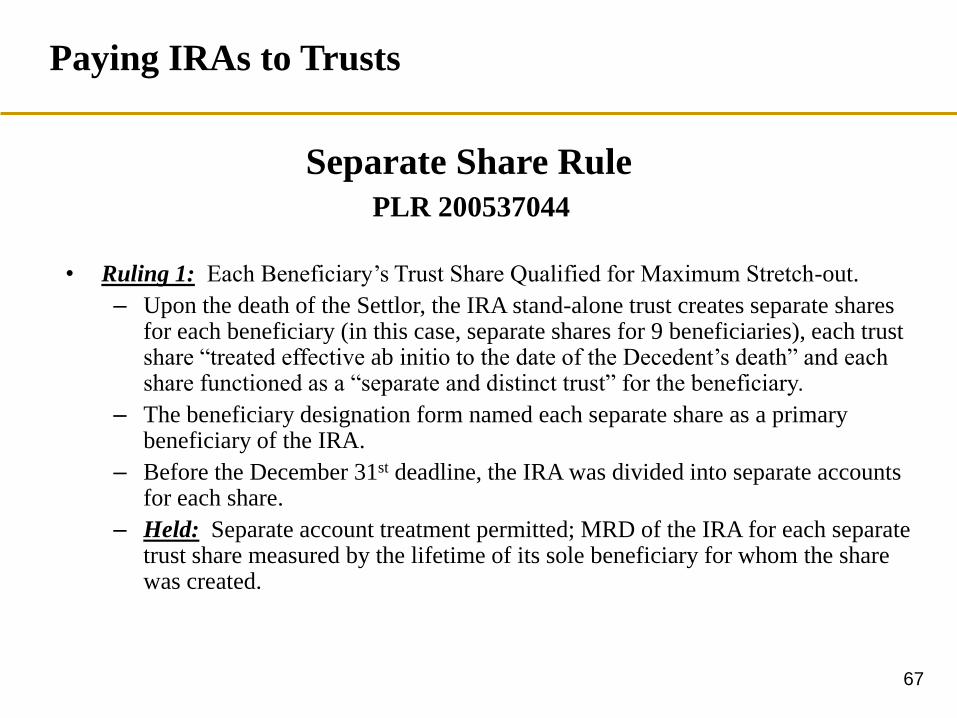

• Ruling 1: Each Beneficiary’s Trust Share Qualified for Maximum Stretch-out.

– Upon the death of the Settlor, the IRA stand-alone trust creates separate shares for each beneficiary (in this case, separate shares for 9 beneficiaries), each trust share “treated effective ab initio to the date of the Decedent’s death” and each share functioned as a “separate and distinct trust” for the beneficiary.

– The beneficiary designation form named each separate share as a primary beneficiary of the IRA.

– Before the December 31st deadline, the IRA was divided into separate accounts for each share.

– Held: Separate account treatment permitted; MRD of the IRA for each separate trust share measured by the lifetime of its sole beneficiary for whom the share was created.

Separate Share Rule

PLR 200537044

Paying IRAs to Trusts

67

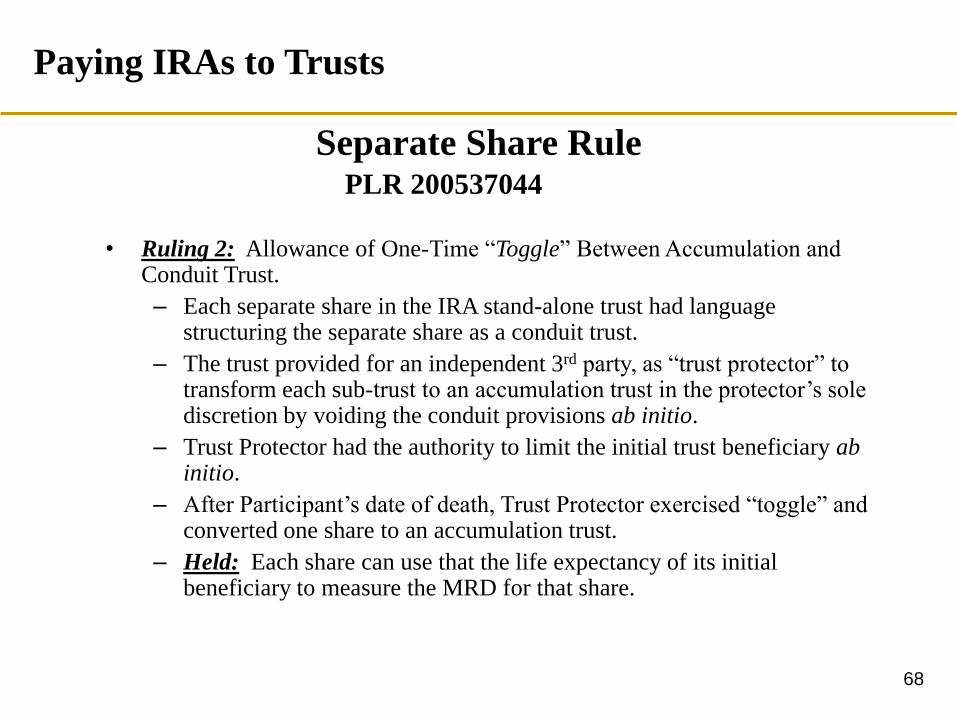

• Ruling 2: Allowance of One-Time “Toggle” Between Accumulation and Conduit Trust.

– Each separate share in the IRA stand-alone trust had language structuring the separate share as a conduit trust.

– The trust provided for an independent 3rd party, as “trust protector” to transform each sub-trust to an accumulation trust in the protector’s sole discretion by voiding the conduit provisions ab initio.

– Trust Protector had the authority to limit the initial trust beneficiary ab initio.

– After Participant’s date of death, Trust Protector exercised “toggle” and converted one share to an accumulation trust.

– Held: Each share can use that the life expectancy of its initial beneficiary to measure the MRD for that share.

Separate Share Rule PLR 200537044

Paying IRAs to Trusts

68

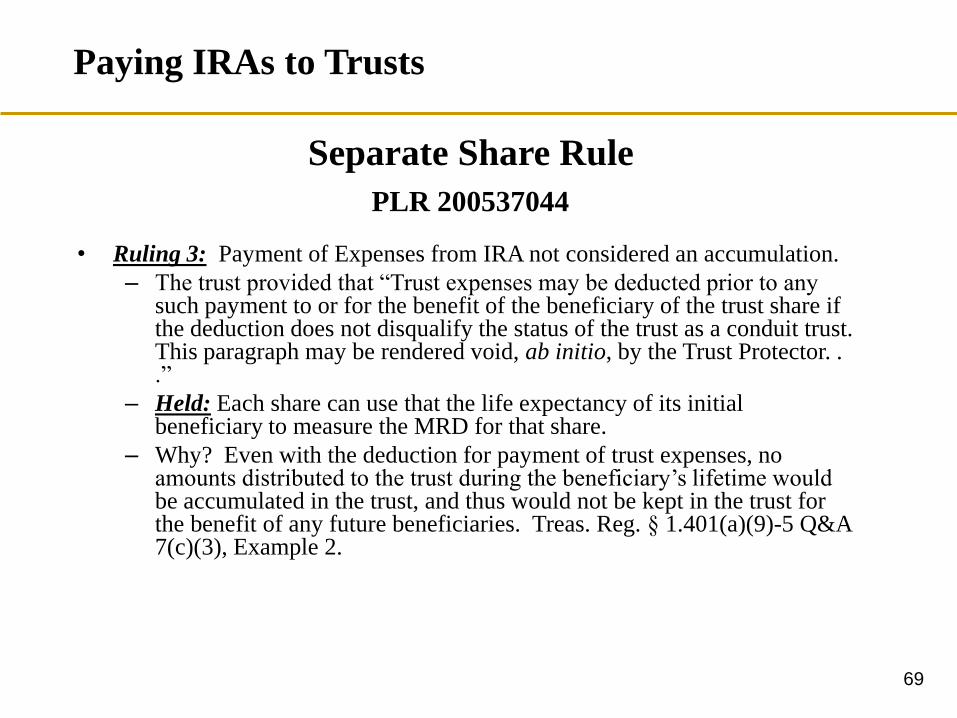

• Ruling 3: Payment of Expenses from IRA not considered an accumulation.

– The trust provided that “Trust expenses may be deducted prior to any such payment to or for the benefit of the beneficiary of the trust share if the deduction does not disqualify the status of the trust as a conduit trust. This paragraph may be rendered void, ab initio, by the Trust Protector. . .”

– Held: Each share can use that the life expectancy of its initial beneficiary to measure the MRD for that share.

– Why? Even with the deduction for payment of trust expenses, no amounts distributed to the trust during the beneficiary’s lifetime would be accumulated in the trust, and thus would not be kept in the trust for the benefit of any future beneficiaries. Treas. Reg. § 1.401(a)(9)-5 Q&A 7(c)(3), Example 2.

Separate Share Rule

PLR 200537044

Paying IRAs to Trusts

69

• Ruling 4: The trust assets will not be included in the estate of the primary beneficiary of a share upon that beneficiary’s death.

– Each trust share would accumulate the net income of the trust, and distributions of income and principal could distribute accumulated income and principal to the primary beneficiary for his or her health, education, maintenance and support only.

– The document did not grant any beneficiary a general power of appointment over his or her share.

– Held: The provisions of the trust could not result in estate inclusion for the estate of a primary beneficiary upon his death.

Separate Share Rule PLR 200537044

Paying IRAs to Trusts

70

Reforming Beneficiary Designations

PLR 200616039-41

• Daughter's life expectancy could be used. Even though no

contingent beneficiaries were named, court reformed beneficiary

designation to name daughters as contingent beneficiaries of IRA.

• IRS is currently rethinking this position.

Paying IRAs to Trusts

71

• Service ruled that the retroactive reformation of a trust would not be

respected for purposes of section 401(a)(9) and the related regulations.

• The trustee reformed the trust pursuant to a state court order to remove

charities under a limited power of appointment granted to first tier

beneficiaries.

• The adverse ruling means the trust was not treated as a “designated

beneficiary trust” (“DBT”) and that the trust beneficiary’s life expectancy

could not be used for determining required minimum distributions.

Reforming Beneficiary Designations

PLR 201021038

Paying IRAs to Trusts

72

Resources on IRA Rules

• Life and Death Planning for Retirement

Benefits by Natalie Choate 2011- 7th Ed.

www.ataxplan.com

• www.irahelp.com (Ed Slott, CPA)

• Robert Keebler, CPA

www.keeblerandassociates.com

• IRS Publication 590

http://www.irs.gov/pub/irs-pdf/p590.pdf

73

Resources on Estate Planning for

Special Needs Beneficiaries

• Estate Planning for a Family with a Special

Needs Child, Sebastian V. Grassi, Jr., Probate

and Property (July/August 2009)

• Estate Planning for a Family with a Special

Needs Child: Part 2 – Trusts as Beneficiaries

of Retirement Plan Benefits, Sebastian V.

Grassi and Nancy H. Welber, Jr., Probate and

Property (September/October 2009)

74

Contact Information:

Scott K. Tippett*

The Tippett Law Firm, PLLC

T: (336) 643-044

F:(336) 458-3215

Thank you for attending!

* Admitted in Georgia, North Carolina, and United States Tax Court

75