Embed Size (px)

DESCRIPTION

Structured Finance and the Global Financial Crisis. Which Crisis?. During the second half of the war, there was an explosion of easy credit, driven by capital from abroad. This resulted in lavish displays of wealth — and opulent living was seen, especially in New York. - PowerPoint PPT Presentation

Citation preview

Structured Finance and the Structured Finance and the Global Financial CrisisGlobal Financial Crisis

Feb 23, 2009Feb 23, 2009 Arjun Jayadev Assumption CollegeArjun Jayadev Assumption College22

Which Crisis?Which Crisis?

During the second half of the war, there was During the second half of the war, there was an explosion of easy credit, driven by capital an explosion of easy credit, driven by capital from abroad.from abroad.

This resulted in lavish displays of wealth — This resulted in lavish displays of wealth — and opulent living was seen, especially in New and opulent living was seen, especially in New York. York.

Housing prices soared during the war. Housing prices soared during the war. But when credit tightened afterward– collapse But when credit tightened afterward– collapse

of real estate bubble and generalized crisisof real estate bubble and generalized crisis

Feb 23, 2009Feb 23, 2009 Arjun Jayadev Assumption CollegeArjun Jayadev Assumption College33

Feb 23, 2009Feb 23, 2009 Arjun Jayadev Assumption CollegeArjun Jayadev Assumption College44

Structural Adjustment in the US after 1970

Decline in Real Wages

Hollowing out of Manufacturing

Collapse in Personal Savings

Increasing HouseholdIndebtedness

‘Market Keynesianism’

Finance and Market IdeologyReign Supreme

Intermediate Patterns

Increasing GlobalImbalances

Financial Deregulation

Monetary Policy alone

Proximate Causes

Global Savings Glut(Lower Long Term Rates

Accommodative MonetaryPolicy (Low Short Term Rate

Financial InnovationGrowth of Shadow Banking

= Housing Bubble

Collapsed Real WagesCollapsed Real Wages

Real Wage Per Hour

7.50

7.70

7.90

8.10

8.30

8.50

8.70

8.90

9.10

9.30

9.50

19641 19663 19691 19713 19741 19763 19791 19813 19841 19863 19891 19913 19941 19963 19991 20013Year (Q)

Destruction in Household Balance Destruction in Household Balance Sheets (Personal Savings Rates)Sheets (Personal Savings Rates)

Personal Savings Rate

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Growing Indebtedness of Growing Indebtedness of HouseholdsHouseholds

Ratio of Household Sector Debt to Personal Income

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1952-I 1957-I 1962-I 1967-I 1972-I 1977-I 1982-I 1987-I 1992-I 1997-I 2002-I 2007-I

Total Debt

Mortgage Debt

Finance and Manufacturing as Finance and Manufacturing as Percentage of National IncomePercentage of National Income

0%

5%

10%

15%

20%

25%

30%

35%

1948-I 1953-I 1958-I 1963-I 1968-I 1973-I 1978-I 1983-I 1988-I 1993-I 1998-I 2003-I 2008-I

Per

cent

of N

atio

nal I

ncom

e A

ccou

nted

for

Manufacturing

Finance, Insurance, Real Estate

Different Defn'

Global Global FFinancial inancial IImbalancesmbalances U.S. U.S. borrows 50 % of the worlds borrows 50 % of the worlds

capital that is exportedcapital that is exported

Deficits and DebtDeficits and Debt

“You mean to tell me that the success of the economic

program and my re-election hinges on the Federal Reserve

and a bunch of f***g bond traders?”

Bill Clinton- 1994From Woodward “ The

Agenda”

We’re Eisenhower Republicans here…We stand for lower deficits, free trade and the bond market. Isn’t that great?Bill Clinton-1998

Ideology

Feb 23, 2009Feb 23, 2009 Arjun Jayadev Assumption CollegeArjun Jayadev Assumption College1212

Financial DeregulationFinancial Deregulation

Gramm-Leach Bliley replaces Glass Gramm-Leach Bliley replaces Glass Steagall in 1998Steagall in 1998

Commodities Futures Modernization Commodities Futures Modernization Act (1999)Act (1999)

Sarbanes Oxley Rule (2002)Sarbanes Oxley Rule (2002) SEC deregulation of brokers (2004)SEC deregulation of brokers (2004) ‘‘Self Regulation’ and Trust in Ratings Self Regulation’ and Trust in Ratings

AgenciesAgencies

Proximate CausesProximate Causes

Easy CreditEasy Credit Search for YieldSearch for Yield Regulatory Loopholes (particularly CFMA Regulatory Loopholes (particularly CFMA

1999, SOX,2002 and Leverage Rule, 2004)1999, SOX,2002 and Leverage Rule, 2004) Shadow Banking/Securitization of Loan ChainShadow Banking/Securitization of Loan Chain Discovery of Enormous (Hidden) LeveragingDiscovery of Enormous (Hidden) Leveraging Inadequate capitalization leading to Liquidity Inadequate capitalization leading to Liquidity

and then Solvency Crisesand then Solvency Crises

Easy CreditEasy CreditFederal Funds Rate (Overnight)

0

1

2

3

4

5

6

7

8

1/1/

2000

5/1/

2000

9/1/

2000

1/1/

2001

5/1/

2001

9/1/

2001

1/1/

2002

5/1/

2002

9/1/

2002

1/1/

2003

5/1/

2003

9/1/

2003

1/1/

2004

5/1/

2004

9/1/

2004

1/1/

2005

5/1/

2005

9/1/

2005

1/1/

2006

5/1/

2006

9/1/

2006

1/1/

2007

5/1/

2007

9/1/

2007

1/1/

2008

5/1/

2008

9/1/

2008

Percent

Equity marketsEquity markets and the Search and the Search for Yieldfor Yield

Mortgage bubble took Mortgage bubble took off in the aftermath of off in the aftermath of declining yield from declining yield from sharesshares

Structured finance: Structured finance: The players in securitizationThe players in securitization

OriginatorOriginator

End borrowersEnd borrowers

Conduit/trust/ Conduit/trust/ SPV/SPE/SIVSPV/SPE/SIV

Investment bank Investment bank (underwriter)(underwriter)

Rating agencyRating agency Institutional Institutional investorinvestor

End lendersEnd lenders (wholesale)(wholesale)

Insurance Insurance companycompany

BrokerBroker

ServicerServicer

$$

$$

$$

$$

$$

MortgagesMortgages

MortgagesMortgages

MBSMBS

I&P ($)I&P ($)

I&P ($)I&P ($)

CDOsCDOs, I&P ($), I&P ($)

Financial Financial returns ($)returns ($)

LEGEND KEYLEGEND KEYO&G – interest and principalO&G – interest and principalSPV – special purpose vehicleSPV – special purpose vehicleSPE – special purpose enterpriseSPE – special purpose enterpriseSIV – SIV – specialspecial investment vehicle investment vehicleMBS – mortgage backed securitiesMBS – mortgage backed securities

Founder: loan originator or Founder: loan originator or investment bankinvestment bank

Purpose: transfering Purpose: transfering ownerhship of claims (loans) ownerhship of claims (loans) and collateral (mortgages) in and collateral (mortgages) in order to issue mortgage order to issue mortgage backed securities (bonds).backed securities (bonds).

Exposure of founder: implicit Exposure of founder: implicit guarantee in case of large guarantee in case of large losses.losses.

Assigns credit Assigns credit rating to issued rating to issued MBSs.MBSs.

Organizes issuing of Organizes issuing of MBSs and places MBSs and places MBSs to investors in MBSs to investors in financial markets.financial markets.

Broker places mortgage Broker places mortgage loans to borrowers for feeloans to borrowers for fee

Manages the flow of Manages the flow of interests and principal interests and principal (I&P); usually, but not (I&P); usually, but not necessarilly the Originator necessarilly the Originator

Typically a specialized Typically a specialized mortgage bankmortgage bank

Mutual funds, Mutual funds, pension funds, pension funds, hedge funds…hedge funds…

Can assume part of Can assume part of risks (insurance of risks (insurance of mortgage loans, mortgage loans, insurance of MBS insurance of MBS returns).returns).

Feb 23, 2009Feb 23, 2009 Arjun Jayadev Assumption CollegeArjun Jayadev Assumption College1717

A bank balance sheetA bank balance sheet

AssetsAssets

LoansLoans

LiabilitiesLiabilities

DepositsDeposits

CapitalCapital

Feb 23, 2009Feb 23, 2009 Arjun Jayadev Assumption CollegeArjun Jayadev Assumption College1818

A shadow banking balance A shadow banking balance sheetsheet

AssetsAssets

Asset Backed Asset Backed SecuritiesSecurities

Mortgage Backed Mortgage Backed SecuritiesSecurities

Credit Default Credit Default SwapsSwaps

Interest Rate SwapsInterest Rate Swaps

LiabilitiesLiabilities

Collateralized Debt Collateralized Debt ObligationsObligations

Asset Backed Asset Backed Commercial PaperCommercial Paper

Feb 23, 2009Feb 23, 2009 Arjun Jayadev Assumption CollegeArjun Jayadev Assumption College1919

Banking versus Shadow Banking versus Shadow BankingBanking

BankingBanking

FDICFDIC Risk Adjusted Capital Risk Adjusted Capital

Adequacy RatiosAdequacy Ratios Interbank Market sets Interbank Market sets

price of liquidity price of liquidity (money) (LIBOR)(money) (LIBOR)

Monetary Policy affects Monetary Policy affects price, interestprice, interest

rates, macro balancerates, macro balance

No Equivalent of No Equivalent of

FDICFDIC No Capital No Capital

Adequacy RatiosAdequacy Ratios No state control No state control

over liquidity over liquidity creationcreation

Shadow BankingShadow Banking

IB Leverage

The ‘Magic’ of Securitization The ‘Magic’ of Securitization and Structured Financeand Structured Finance

The CDS Market

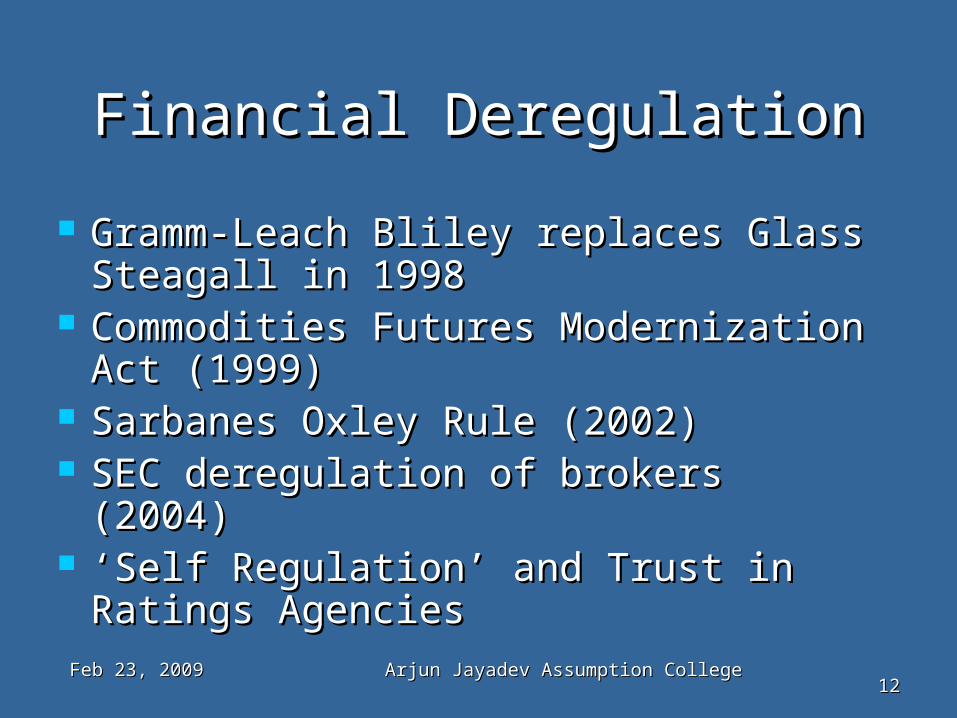

““Subprime” GrowthSubprime” Growth

SSubprime ubprime growth shot up in 2003-2005growth shot up in 2003-2005 By 2006, most Subprime mortgages were securitizedBy 2006, most Subprime mortgages were securitized

Share of subprimeShare of subprimeIn total U.S. economy In total U.S. economy (measured by GDP): (measured by GDP): 1% (2001), increasing 1% (2001), increasing to 5% (2005)to 5% (2005)

Bubble in Housing PricesBubble in Housing Prices

The Crisis Begins...The Crisis Begins...

In August 2007, Crisis begins with first wave of In August 2007, Crisis begins with first wave of sub prime Failuressub prime Failures

Overleveraged shadow banks (easy credit) were invested in very bad bets (subprime), at scale, with no liquidity backstop (unregulated credit markets).

Counterparty Risk was perceived as much larger. Liquidity starts freezing (Interbank markets start

to experience wild shifts in ability to borrow and lend and much higher rates for borrowing)

Residential Real Estate Prices Crash

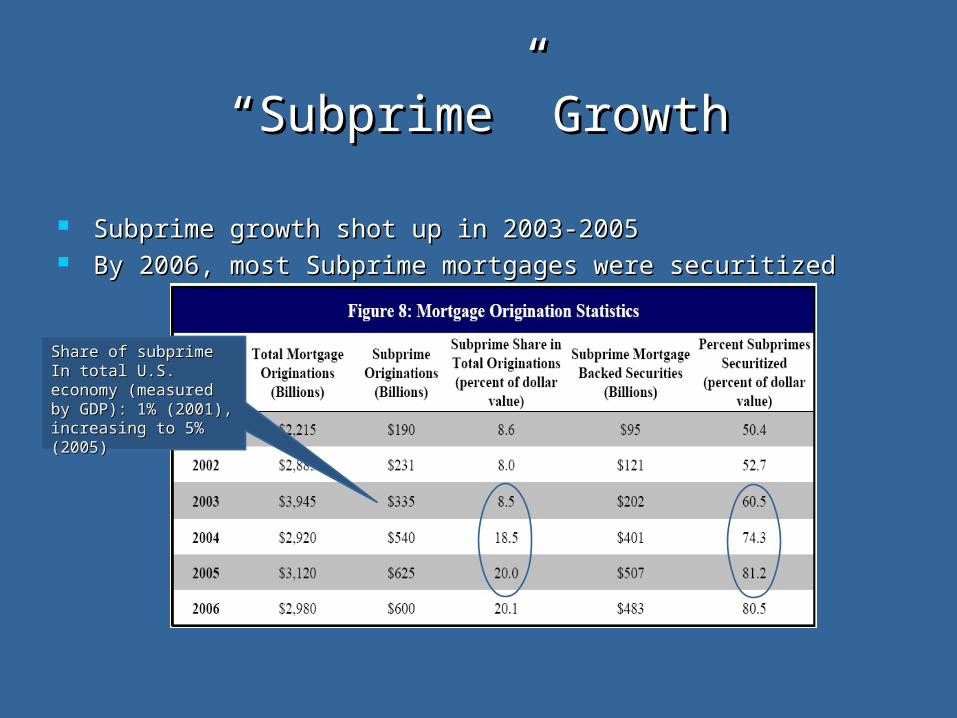

Crisis in Subprime LendingCrisis in Subprime Lending

Crisis in Subprime Crisis in Subprime LendingLending

% of % of delinquent delinquent loans (60+ loans (60+

days)days)

Months from originationMonths from origination

MBS’s lose valueMBS’s lose value

Total Predicted Losses 2.2-3.6 Total Predicted Losses 2.2-3.6 Trillion Dollars! (Oct 08)Trillion Dollars! (Oct 08)

Feb 23, 2009Feb 23, 2009 Arjun Jayadev Assumption CollegeArjun Jayadev Assumption College3131

TED-Spread: Liquidity Crisis

Feb 23, 2009Feb 23, 2009 Arjun Jayadev Assumption CollegeArjun Jayadev Assumption College3232

LIBOR-Overnight Interest Swaps spread (Measure of Interbank liquidity)

Global Declines in Stock Global Declines in Stock MarketsMarkets

Famous Last WordsFamous Last Words

"We have a good deal of comfort "We have a good deal of comfort about the capital cushions at these about the capital cushions at these firms at the moment."firms at the moment."

- Christopher Cox, chairman of the - Christopher Cox, chairman of the U.S. Securities and Exchange U.S. Securities and Exchange Commission, March 11, 2008.Commission, March 11, 2008.

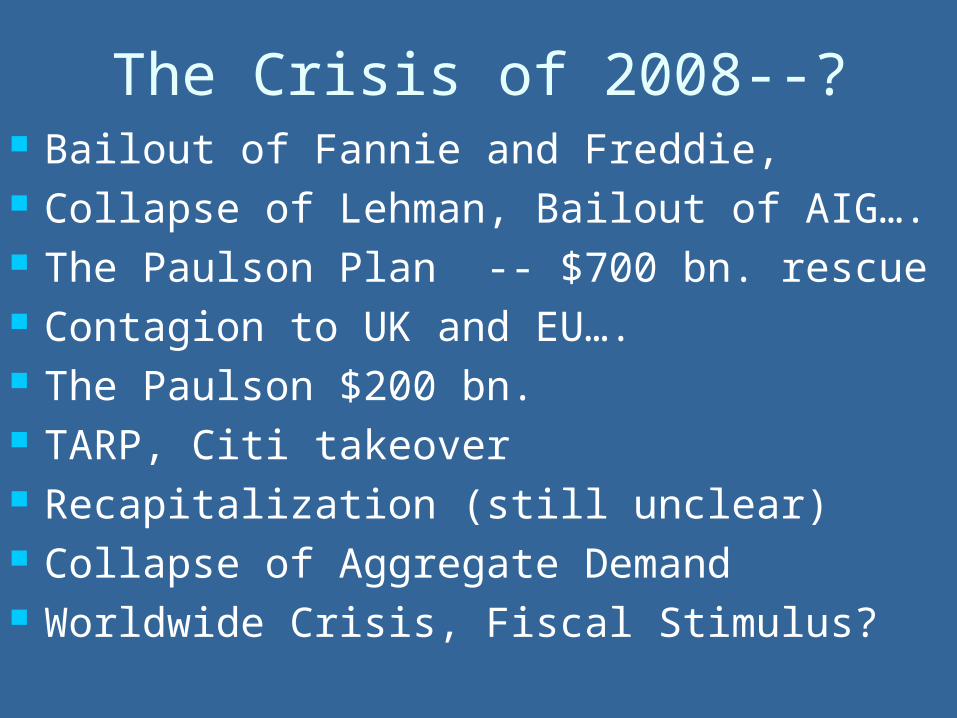

The Crisis of 2008--? Bailout of Fannie and Freddie, Collapse of Lehman, Bailout of AIG…. The Paulson Plan -- $700 bn. rescue Contagion to UK and EU…. The Paulson $200 bn. TARP, Citi takeover Recapitalization (still unclear) Collapse of Aggregate Demand Worldwide Crisis, Fiscal Stimulus?