Embed Size (px)

Citation preview

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 1/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 1

STRUCTURED FINANCE DEFINITION Structured finance is a term that evolved in 1980s to refer to a wide varietyof debt and related securities whose promise to repay is backed by the

value of some form of financial asset or credit support from a third party

transaction. Very often, both types of backing are used to achive a desired

credit rating. Structured finance is a broad term used to describe a sector of finance that

was created to help transfer risk using complex legal and corporate entities.

This risk transfer as applied to securitization of various financial assets(e.g. mortgages, credit card receivables, auto loans, etc.) has helped to

open up new sources of financing to consumers. However, it arguably

contributed to the degradation in underwriting standards for these financial

assets, which helped give rise to both the inflationary credit bubble of the

mid-2000s and the credit crash and financial crisis of 2007-2009.

Structured finance encompasses all advanced private and public financial

arrangements that serve to efficiently refinance and hedge any profitable

economic activity beyond the scope of conventional forms of on-balancesheet securities (debt, bonds, equity) in the effort to lower cost of capital

and to mitigate agency costs of market impediments on liquidity. Most

structured investments combine traditional asset classes with contingent

claims, such as risk transfer derivatives and/or derivative claims on

commodities, currencies or receivables from other reference assets, or

replicate traditional asset classes through synthetication. Structured finance

is invoked by financial and non-financial institutions in both banking and

capital markets if established forms of external finance are either

unavailable (or depleted) for a particular financing need, or traditional

sources of funds are too expensive for issuers to mobilize sufficient fund for

what would otherwise be an unattractive investment based on the issuer‘s

desired cost of capital. Structured finance offers the issuers‘ enormous

flexibility in terms of maturity structure, security design and asset types,

which allows issuers to provide enhanced return at a customized degree of

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 2/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 2

diversification commensurate to an individual investor‘s appetite for risk.

Hence, structured finance contributes to a more complete capital market by

offering any mean-variance trade-off along the efficient frontier of optimal

diversification at lower transaction cost. However, the increasing

complexities of the structured finance market, and the ever growing rangeof products being made available to investors, invariably create challenges

in terms of efficient assembly, management and dissemination of

information. Structured finance has become a major segment in the

financial industry since the mid-1980s. Collateralized bond obligations

(CBOs), collateralized debt obligations (CDOs), syndicated loans and

synthetic financial instruments are examples of structured financial

instruments.

The Main Advantages of Using Structured Finance Include Lowering Funding Cost Changes In Debt And Equity Composition Of Balance sheet Taking Companies Public Or Private Financing Assets Tax Management Hedge Fund Speculation Sheltering Corporations From Operating Liabilities

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 3/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 3

SECURITIZATION

Securitisation is the process of pooling and repackaging of homogenous

illiquid financial assets into marketable securities that can be sold to

investors. Inshort, securitisation is the process of conversion of illiquid

loans into tradable securities. The process leads to the creation of financial

instruments that represent ownership interest in, or are secured by a

segregated income producing asset or pool of assets. The pool of assets

collateralises securities. These assets are generally secured by personal or

real property (e.g. automobiles, real estate, or equipment loans), but in

some cases are unsecured (e.g. credit card debt, consumer loans).

Traditionally, a lender advances a loan to a borrower and gets repayment

of principal, along with interest, over a period of time. In securitisation, the

lender sells his right to receive the future payments from the borrowers to a

third party and receives consideration for the same much earlier than the

maturity of the original loans. These future cash flows from borrowers are

sold to investors in the form of marketable securities.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 4/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 4

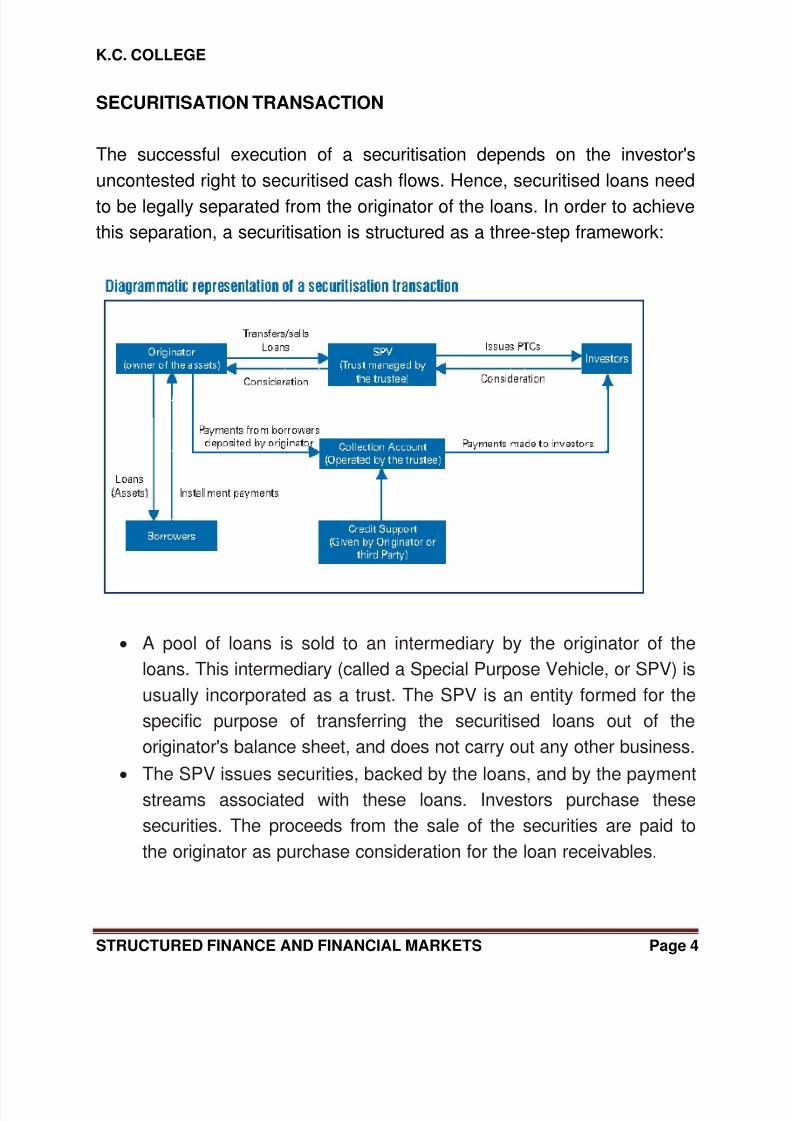

SECURITISATION TRANSACTION

The successful execution of a securitisation depends on the investor's

uncontested right to securitised cash flows. Hence, securitised loans need

to be legally separated from the originator of the loans. In order to achieve

this separation, a securitisation is structured as a three-step framework:

A pool of loans is sold to an intermediary by the originator of the

loans. This intermediary (called a Special Purpose Vehicle, or SPV) is

usually incorporated as a trust. The SPV is an entity formed for the

specific purpose of transferring the securitised loans out of the

originator's balance sheet, and does not carry out any other business.

The SPV issues securities, backed by the loans, and by the payment

streams associated with these loans. Investors purchase these

securities. The proceeds from the sale of the securities are paid to

the originator as purchase consideration for the loan receivables.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 5/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 5

The cash flows generated by the loans over a period of time are used

to repay investors. There could also be some credit support built into

the transaction to protect investors against possible losses in the

pool. However, the investors will typically have no recourse to the

originator.

The keyelements of securitization are

Legal true sale of assets to an SPV

Issuance of securities by the SPV to the investors collateralized by

the underlying assets

Reliance by the investors on the performance of the assets forrepayment - rather than the credit of their Originator (the seller) or the

issuer (the SPV)

Consequent to the above, ―Bankruptcy Remoteness‖ (no right over

the sold out loan in case of Bankruptcy) from the Originator.

Apart from the above, the following additional characteristics are

generally noticed: Administration of the assets, including continuation

of relationships with obligors support for timely interest and principal

repayments in the form of suitable credit enhancements ancillary

facilities to cover interest rate / forex risks, guarantee, etc.

Formal rating from one or more rating agencies

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 6/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 6

PARTIES INVOLVED IN A SECURITISATION TRANSACTION

The entities involved in a securitisation deal, and their role, are briefly

explained below. It is possible for a single party in any transaction to

perform multiple roles.

Originator

The originator is the original lender and the seller of the receivables. It is

the entity on whose books the assets to be securitised exist. It is the prime

mover of the deal i.e. it sets up the necessary structures to execute the

deal. It sells the assets on its books and receives the funds generated from

such sale. In a true sale, the Originator transfers both the legal and thebeneficial interest in the assets to the SPV.

Seller

The seller pools the assets in order to securitise them. Usually, the

originator and the seller are the same, but, in some cases, originators sell

their loans to other companies that securities them.

Obligors/borrowers

The borrower is the counter party to whom the originator makes the loan.

The amount outstanding from the Obligor is the asset that is transferred to

the SPV. The payments made by borrowers are the source of cash flows

used for making investor payments.

Investors

The investors may be in the form of individuals or institutional investors like

FIs, mutual funds, provident funds, pension funds, insurance companies,

etc. They buy a participating interest in the total pool of receivables and

receive their payment in the form of interest and principal as per agreed

pattern.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 7/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 7

Issuer

The issuer in a securitisation deal is the special purpose vehicle (SPV),

which is typically set up as a trust. The trust issues securities, which

investors subscribe to.

Servicer

The servicer collects the periodic installments due from individual

borrowers in the pool, makes payouts to investors, and follows up on

delinquent accounts. The servicer also furnishes periodic information to the

rating agency and the trustee on pool performance. There is a service fee

payable to the servicer.

Trustee

Trustees are normally reputed Banks, Financial Institutions or independent

trust companies set up for the purpose of settling trusts. Trustees oversee

the performance of the transaction till maturity, and are vested with the

necessary powers to protect investors' interests.

Arrangers

These are Investment banks responsible for structuring the securities to be

issued, and liasoning with other parties such as investors, credit enhancers

and rating agencies to successfully execute the securitization transaction.

Rating agencies

Independent rating agencies analyse the risks associated with a

securitisation transaction and assign a credit rating to the instrument

issued. Since the investors take on the risk of the asset pool rather than the

Originator, an external credit rating plays an important role. The rating

process would assess the strength of the cash flow and the mechanism

designed to ensure full and timely payment by the process of selection of

loans of appropriate credit quality, the extent of credit and liquidity support

provided and the strength of the legal framework.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 8/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 8

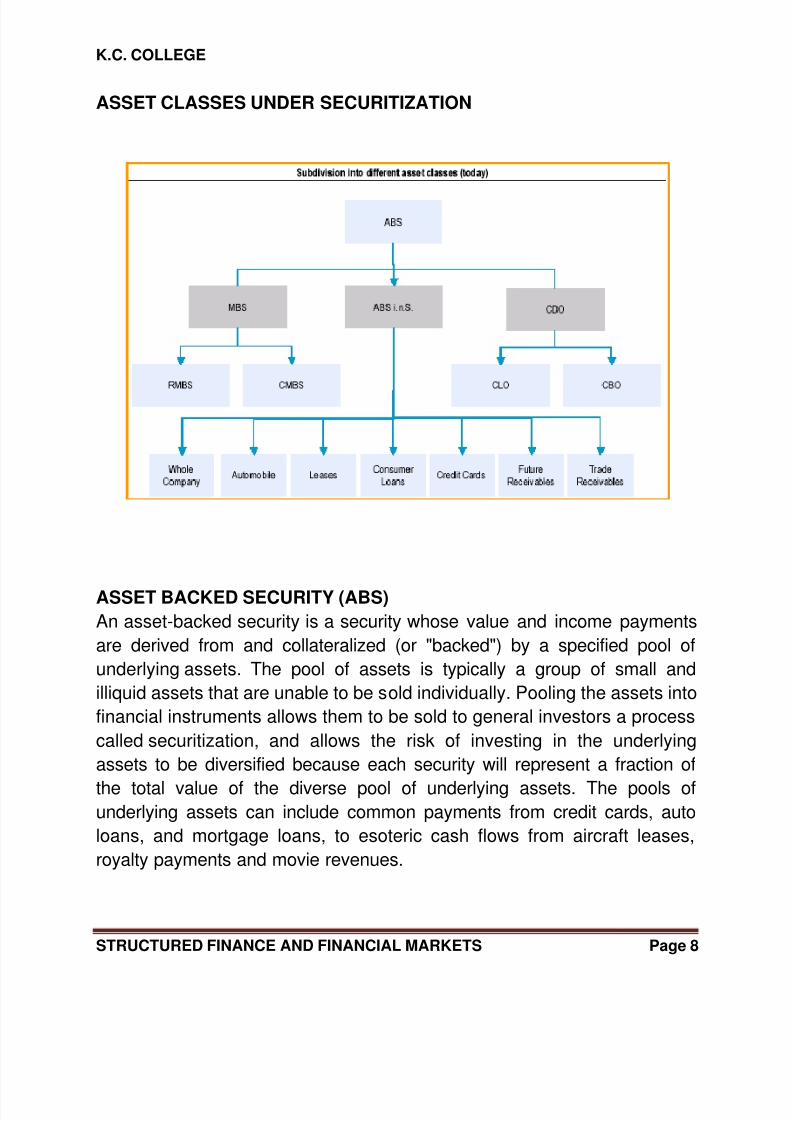

ASSET CLASSES UNDER SECURITIZATION

ASSET BACKED SECURITY (ABS)

An asset-backed security is a security whose value and income payments

are derived from and collateralized (or "backed") by a specified pool of

underlying assets. The pool of assets is typically a group of small and

illiquid assets that are unable to be sold individually. Pooling the assets into

financial instruments allows them to be sold to general investors a process

called securitization, and allows the risk of investing in the underlying

assets to be diversified because each security will represent a fraction of

the total value of the diverse pool of underlying assets. The pools ofunderlying assets can include common payments from credit cards, auto

loans, and mortgage loans, to esoteric cash flows from aircraft leases,

royalty payments and movie revenues.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 9/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 9

MORTGAGE BACKED SECURITY (MBS) A mortgage-backed security (MBS) is an asset-backed security or debt

obligation that represents a claim on the cash flows from mortgage

loans through a process known as securitization.Most bonds backed by

mortgages are classified as an MBS. This can be confusing, because asecurity derived from an MBS is also called an MBS. To distinguish the

basic MBS bond from other mortgage-backed instruments the

qualifier pass-through is used, in the same way that "vanilla" designates

an option with no special features. COLLATERALIZED DEBT OBLIGATIONS (CDO) Collateralized debt obligations are securitized interests in pools of generally

non-mortgage assets. Assets called collateral usually comprise loans ordebt instruments. A CDO may be called acollateralized loan

obligation (CLO) or collateralized bond obligation (CBO) if it holds only

loans or bonds, respectively. Investors bear the credit risk of the collateral.

Multiple tranches of securities are issued by the CDO, offering investors

various maturity and credit risk characteristics. Tranches are categorized

as senior, mezzanine, and subordinated /equity, according to their degree of

credit risk. If there are defaults or the CDO's collateral otherwise

underperforms, scheduled payments to senior tranches take precedence

over those of mezzanine tranches, and scheduled payments to mezzanine

tranches take precedence over those to subordinated/equity tranches.

RESIDENTIAL MORTGAGE-BACKED SECURITIES (RMBS)

Residential mortgage-backed securities (RMBS) are a type

of bond commonly issued in American security markets. They are a type

of mortgage-backed security which is backed by mortgages on residential

rather than commercial real estate. COMMERCIAL MORTGAGE-BACKED SECURITIES (CMBS) Commercial mortgage-backed securities (CMBS) are a type of mortgage-

backed security backed by mortgages on commercial rather than

residential real estate. CMBS issues are usually structured as

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 10/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 10

multiple tranches, similar to CMOs, rather than typical residential

"passthroughs." The typical structure for the securitization of commercial

real estate loans is a Real Estate Mortgage Investment Conduit (REMIC), a

creation of the tax law that allows the trust to be a pass-through entity

which is not subject to tax at the trust level.

COLLATERALIZED LOAN OBLIGATION (CLO)

Collateralized loan obligations are the same as collateralized mortgage

obligations (CMOs) except for the assets securing the obligation. CLOs

allow banks to reduce regulatory capital requirements by selling large

portions of their commercial loan portfolios to international markets,

reducing the risks associated with lending. COLLATERALIZED BORROWING OBLIGATIONS (CBO) Collateralized borrowing obligations (CBOs) are a type of structured asset-

backed security (ABS) whose value and payments are derived from a

portfolio of fixed-income underlying assets. CBOs securities are split into

different risk classes, or tranches, whereby "senior" tranches are

considered the safest securities. Interest and principal payments are made

in order of seniority, so that junior tranches offer higher coupon payments

(and interest rates) or lower prices to compensate for additional default risk.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 11/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 11

ECONOMIC BENEFITS OF SECURITIZATION

FOR ORIGINATOR

Efficient financing

Through securitisation, companies holding financial assets like loans have

ready access to low-cost sources of funds, and can reduce their

dependence on financial intermediaries for their capital requirements. This

translates into lower interest costs, the benefits of which are also passed

on to end consumers. In securitisation, it is possible to achieve a much

higher target rating for instruments than the originator's credit rating, by

providing credit enhancements for the transaction. Thus the borrower canobtain funding at lower interest rates applicable to highly rated instruments,

and gain a pricing advantage.

Off-balance sheet funding

For accounting purposes, securitisation is treated as a sale of assets, and

not as financing. Therefore the originator does not record the transaction as

a liability on its balance sheet. Such off-balance sheet transactions raise

funds without increasing the originator's leverage or debt-to-equity ratio.

Lower capital requirements

Securitisation enables banks and financial institutions to meet regulatory

capital adequacy norms by transferring assets, and their associated risks,

off the balance sheet. The capital supporting the assets is released and the

proceeds from securitisation can be used for further growth and

investment.

Liquidity management

Tenor mismatch due to long term assets funded by short-term liabilities can

be rectified by securitisation, as long-term assets are converted into cash.

Thus, securitisation is a tool for Asset Liability management.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 12/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 12

Improvement in financial ratios

Since securitisation helps in undertaking larger transaction volumes with

the same capital, profitability and return on investment ratios increase post

securitisation.

Profit on sale

Securitisation helps in up-fronting profits, which would otherwise accrue

over the tenor of the loans. Profits arise from the spread between the

interest rate received on underlying loans and the coupon rate paid on the

securitised instruments backed by those loans. This interest spread is

booked as profit, leading to increased earnings in the year of securitisation.

FOR INVESTORS

Return on investment/Yield

Securitized assets offer a combination of attractive Return on

investments/yields (compared with other instruments of similar quality),

increasing secondary market liquidity, and generally more protection by

way of collateral overages and/or guarantees by entities with high and

stable credit ratings. Yields of ABS/MBS/CDOs are higher than those of

other debt instruments with comparable ratings. Spreads of securitised

instruments are typically in the range of 50 - 100 basis points over

comparable AAA corporate paper.

Flexibility

An important advantage of securitisation is the flexibility to tailor the

instrument to meet the investor's risk and tenor appetite.

Durations can range from few months to many years.

Repayments are usually made on a monthly basis but can also be

structured on a quarterly or semiannual basis.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 13/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 13

Interest rates can be fixed or floating depending on investor

preferences.

Safety FeaturesSecuritisation offers investors a diversification of risk, since the exposure is

to a pool of assets. Most issuances are also highly rated by independent

credit rating agencies, and have credit support built into the transactions.

Investors get the benefit of a payment structure closely monitored by an

independent trustee, which may not always be the case in traditional debt

instruments.

Performance track record

Securitised instruments have demonstrated consistently good performance,

with no downgrades or defaults on any securitised instrument in India till

date.

EFFECTS ON THE NATIONAL ECONOMY

In those countries where a high proportion of residential montages andother claims have been securitized, the gains to the national economy can

be measured in the billions of dollars.

The effect of securitization on the economies of different countries is still

difficult to assess because the technique is in its infancy in many parts of

the world. Asset securitization, if introduced in a transparent and orderly

fashion, offers Asian countries additional gains from:

Capital market development, as more high-quality securities are

added to the fixed-income market.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 14/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 14

A source of funds for rapidly growing, capital-constrained, banks,

finance companies and industrial companies whose expansion

depends on the extension of credit to their customers.

An expanded source of financing for residential home ownership.

The potential for financing of infrastructure projects, such as toll

roads, that produce reliable revenue streams capable of being

contractually assigned to a separate legal entity.

There is a strong argument favoring the growth of asset securitization

in those nations with developing capital markets as well as in the

more mature ones.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 15/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 15

DIFFERENCE BETWEEN SECURITISATION AND TRADITIONAL DEBT

INSTRUMENTS

Securitised instruments have some distinct features, which distinguish

them from traditional debt:

Isolation of pool of assets

In a securitisation, the securitised assets are separated from the original

lender through a sale to a separate legal entity called a Special Purpose

Vehicle (SPV), which acts as an intermediary.

Claim against a pool of assetsTraditional debt instruments represent claims against the company that

issues the debt. Investors rely entirely on the borrower company's credit

quality for repayment of their debt. In securitisation transactions, investor

payouts are made from collections on securitised assets, and the

instruments are thus claims on the assets securitised. Investors do not

typically have recourse to the originator.

Credit enhancement

Credit enhancement is an additional source of funds that can be used if

collections on the assets are insufficient to pay investors their dues in full.

Credit enhancement thus supports the credit quality of the securitised

instrument, and enables it to achieve a higher credit rating than the pool of

assets on its own; in many cases the rating would also be higher than that

of the originator. This is not possible in conventional debt.

Payment Mechanisms

Securitised instruments typically incorporate structural features to ensure

that scheduled payments reach investors in a timely manner.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 16/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 16

Operational & administrative requirements

As the SPV is only a shell entity; the administration of the pool of

securitised loans involves multiple parties performing various functions.

These functions include collection, accounting, loan servicing, legal

compliance etc that need to be performed throughout the life of the

transaction.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 17/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 17

RISKS INVESTORS FACE IN SECURITISATION DEALS

Investors in securitised instruments can take advantage of the benefits that

these instruments offer; however, they also need to be aware of the

inherent risks in these transactions. These risks can be classified into:

Asset pool risks

These arise due to the unpredictable behaviour of underlying borrowers.

However, the payment behaviour of underlying borrowers can be estimated

with a reasonable degree of accuracy based on historical data

Counter party risksThese arise as a securitisation transaction involves multiple parties

throughout the tenure of the instrument. The investor's returns can be

impacted by nonperformance or bankruptcy of any of these counter parties.

Investment risks

Like all other investments, securitised instruments are subject to market

related risks. Investors are protected against these risks by means of

structural features and credit enhancements, which enable the instruments

to achieve high credit ratings.

Credit risk

Investors have a direct exposure to the repayment ability of the underlying

borrowers whose loans have been securitised. If borrowers default on

payments of instalments, or make delayed payments, collections will be

inadequate to service scheduled investor payouts. Thus, timely investor

payments will depend on the credit quality of the pool borrowers.

Risk of prepayments

Investors face the risk that underlying borrowers may prepay all or part of

the principal outstanding on their loans. When prepayments occur, they are

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 18/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 18

passed on to the investor (unless the instrument structure provides for a

separate class of PTCs to absorb prepayments). This can affect the

investor in two ways:

Reinvestment risk: If there are heavy prepayments in the pool, the

average tenure of the instrument reduces, resulting in reinvestment

risk for the investor.

Prepayment loss: If the investor has paid an additional consideration

to receive 1 excess interest spreads generated by the pool, the

investor's principal outstanding is greater than the pool principal

outstanding. Hence, when a contract is prepaid, this excess interest

spread payable to the investor from that contract is lost.

Property/asset price risk

Assets backing securitised instruments may be prepossessed and sold

post securitisation. The proceeds and loss on sale depends upon market

values of the assets, which fluctuate.

Legal riskIn any securitisation transaction, it is essential that the transfer of

receivables is a ―true sale‖, i.e. the or iginator should not retain any control

over the receivables or any claim to the receivables that could override the

claim of the PTC holders. Further, the transfer of receivables should not in

any way vitiate the terms of the underlying loan documents. It should also

be ensured that investors have unrestricted access to the cash collateral.

CRISIL conducts its own due diligence to ascertain that the transaction

structure conforms to a true sale. However, in the absence of any judicial

precedent in India on the subject of true sale, CRISIL also bases its

analysis on an independent legal opinion from an external legal counsel,

certifying that:

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 19/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 19

The assignment of receivables is valid in terms of the underlying loan

documents;

The transfer of receivables to the trust constitutes a true sale,

That the structure ensures that receivables are bankruptcy remote

from the originator in light of the originator continuing as the servicer;

The cash collateral is bankruptcy remote from the originator;

The transaction complies with all applicable laws;

All transaction documents are valid and enforceable have been

executed in accordance with the relevant stamp duty and registration

laws.

Servicer Risk The investor faces the risk of bankruptcy and non-performance of the

servicer, since the servicer is critical in ensuring robust collections from

underlying borrowers. The transaction documents give the trustee the

authority to appoint an alternate servicer in case of nonperformance or

downgrade of the existing servicer.

Commingling risk

This risk arises on account of time lag between pool collections and

investor payouts (typically a month), during which the servicer continues to

hold the pool collections. In this interim period, collections from the

securitised loans may mingle with the normal funds of the servicer. In case

of bankruptcy of the servicer, there could be problems in recovery of these

funds and additional costs, which the investor will bear.

Swap Counterparty Risk In transactions where a swap is required to convert interest rate from fixed

to floating or vice-versa, the rating of the instrument is dependent on the

timely discharge of obligations by the swap counterparty which agrees to

swap the cash flows.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 20/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 20

Interest Rate Risk

If PTCs have a floating rate yield linked to a benchmark market rate, while

the underlying pool of loans contains fixed rate contracts, there is a basis

risk. The risk arises due to the possibility of a fluctuation in interest rates in

the economy. This risk is generally borne by floating rate PTC investors.

Interest rate risk could be mitigated by an interest rate swap or adequately

covered by the credit enhancement.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 21/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 21

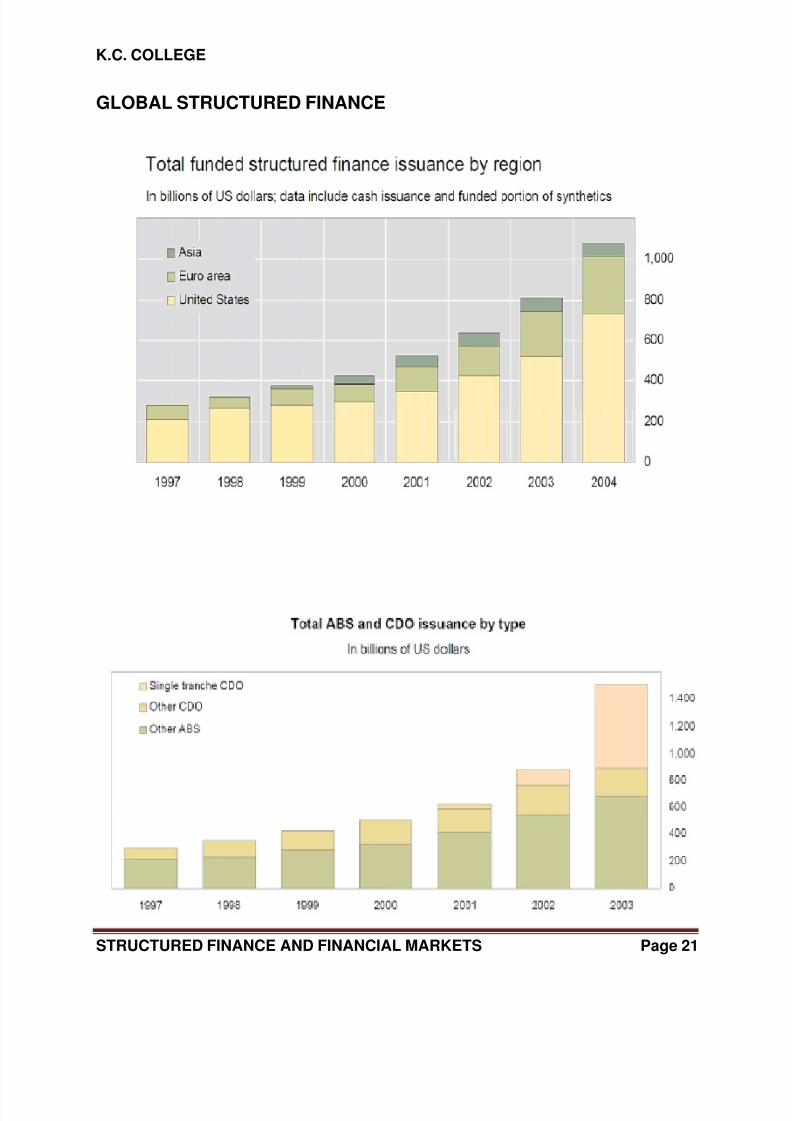

GLOBAL STRUCTURED FINANCE

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 22/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 22

The United States is the largest, deepest and widest securitization market

in the world Australia has a market size of A $10bn. and is dominated by

residential mortgages and commercial property leases. In Japan,

securitization is largely undeveloped with transactions confined to about

US$4.8bn In Asia, assets worth only US$2bn. has been securitized, half of

which were in Hong Kong. India, Indonesia, and Thailand are the future

markets on horizon with a few deals of low volume having been concluded

in each country. In Latin America, securitization transactions were up from

about US$3.67bn. In 1995 to 10.3bn in 1996. In South Africa, very few

transactions have taken place although the Government has enacted a

special law in 1992.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 23/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 23

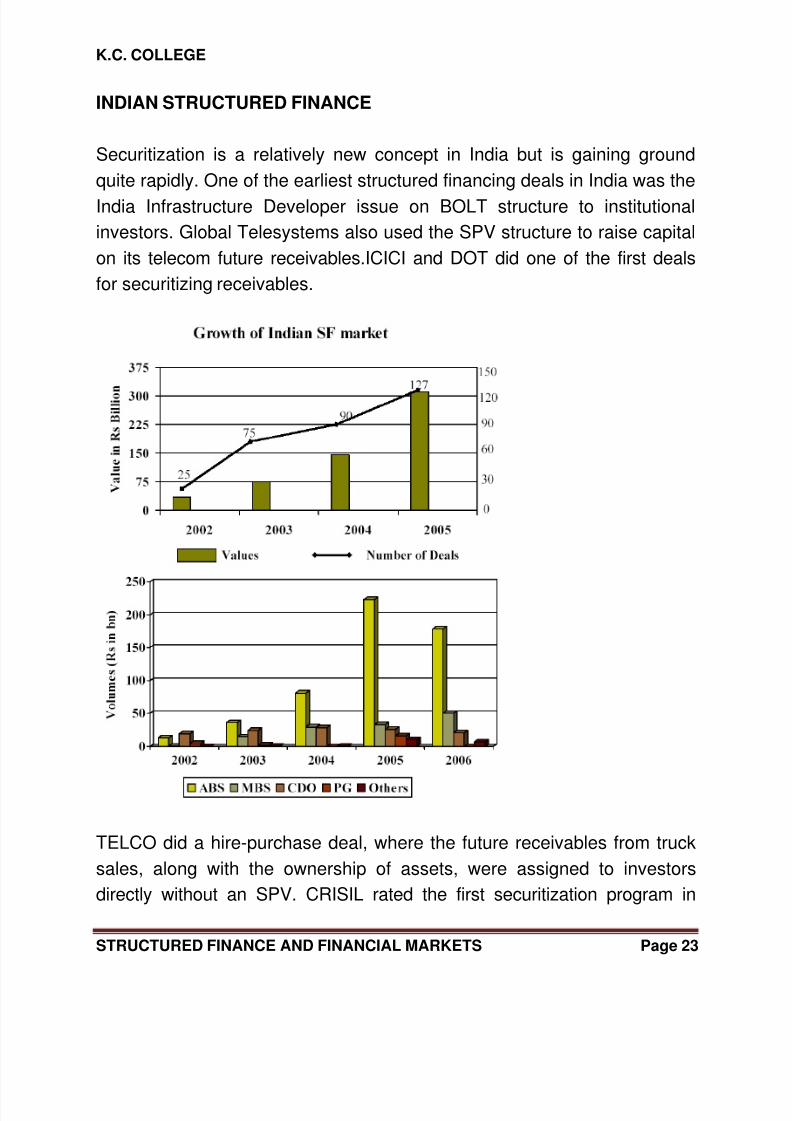

INDIAN STRUCTURED FINANCE

Securitization is a relatively new concept in India but is gaining ground

quite rapidly. One of the earliest structured financing deals in India was the

India Infrastructure Developer issue on BOLT structure to institutional

investors. Global Telesystems also used the SPV structure to raise capital

on its telecom future receivables.ICICI and DOT did one of the first deals

for securitizing receivables.

TELCO did a hire-purchase deal, where the future receivables from truck

sales, along with the ownership of assets, were assigned to investors

directly without an SPV. CRISIL rated the first securitization program in

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 24/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 24

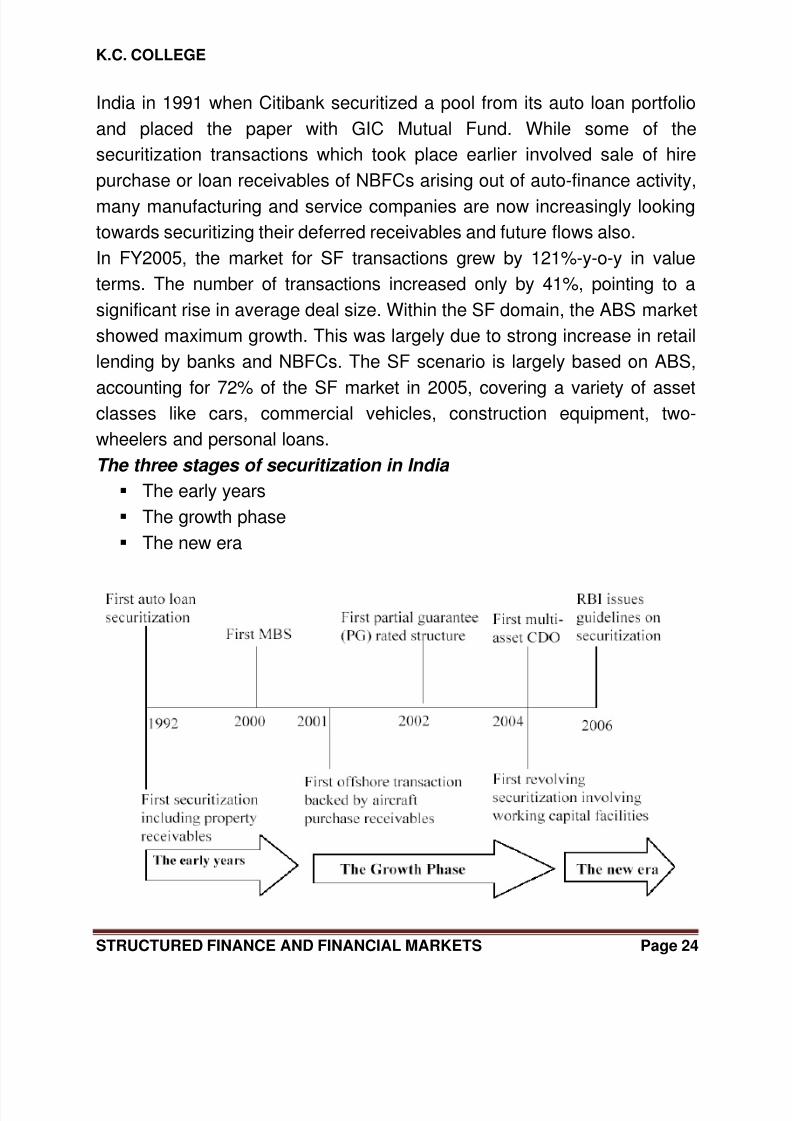

India in 1991 when Citibank securitized a pool from its auto loan portfolio

and placed the paper with GIC Mutual Fund. While some of the

securitization transactions which took place earlier involved sale of hire

purchase or loan receivables of NBFCs arising out of auto-finance activity,

many manufacturing and service companies are now increasingly looking

towards securitizing their deferred receivables and future flows also.

In FY2005, the market for SF transactions grew by 121%-y-o-y in value

terms. The number of transactions increased only by 41%, pointing to a

significant rise in average deal size. Within the SF domain, the ABS market

showed maximum growth. This was largely due to strong increase in retail

lending by banks and NBFCs. The SF scenario is largely based on ABS,

accounting for 72% of the SF market in 2005, covering a variety of assetclasses like cars, commercial vehicles, construction equipment, two-

wheelers and personal loans.

The three stages of securitization in India

The early years

The growth phase

The new era

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 25/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 25

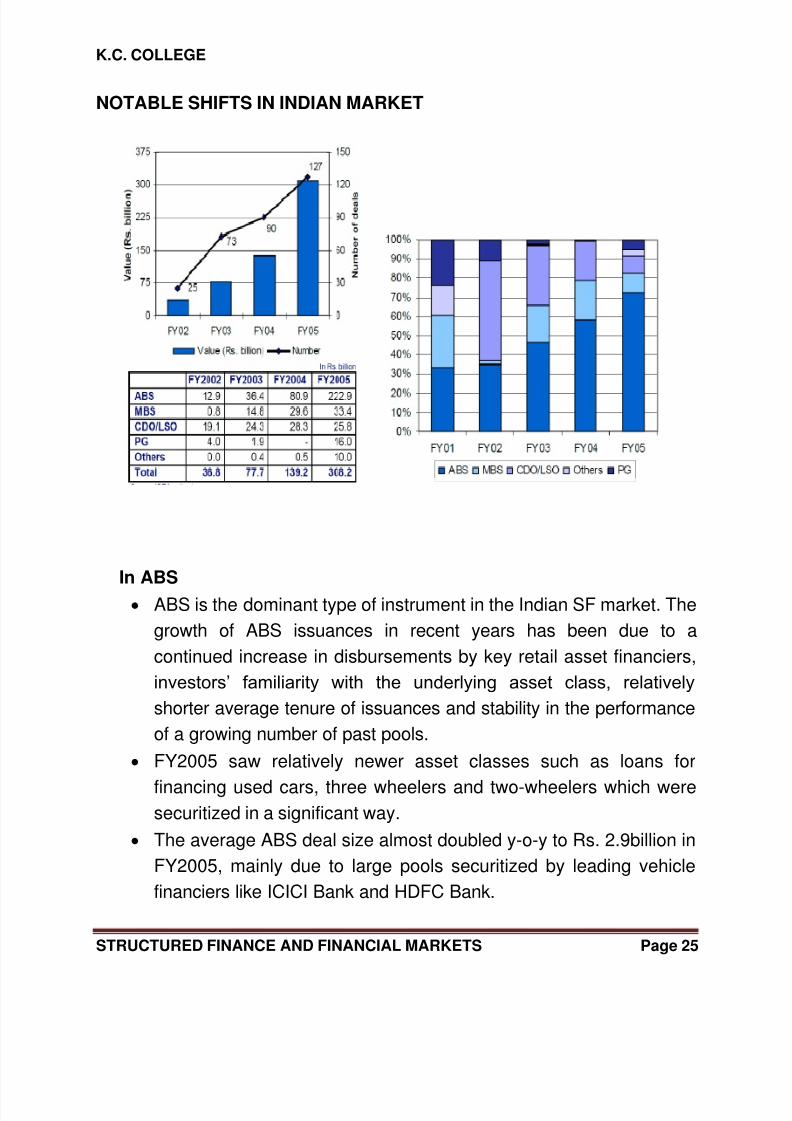

NOTABLE SHIFTS IN INDIAN MARKET

In ABS

ABS is the dominant type of instrument in the Indian SF market. The

growth of ABS issuances in recent years has been due to a

continued increase in disbursements by key retail asset financiers,

investors‘ familiarity with the underlying asset class, relatively

shorter average tenure of issuances and stability in the performance

of a growing number of past pools.

FY2005 saw relatively newer asset classes such as loans for

financing used cars, three wheelers and two-wheelers which weresecuritized in a significant way.

The average ABS deal size almost doubled y-o-y to Rs. 2.9billion in

FY2005, mainly due to large pools securitized by leading vehicle

financiers like ICICI Bank and HDFC Bank.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 26/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 26

There is a growing preference for floating-rate yields, given the

volatile interest rate conditions.

Time-tranching is increasingly becoming the norm: during FY2005,

64% of ABS issuances involved multiple tranches with different

tenures.

In MBS

The largest ever MBS transaction in India, a RS. 12billion mortgage-

backed pool of ICICI Bank happened in FY2005.

MBS has the potential for maximum growth, given the significant

expansion in the underlying housing finance business underway.

However, the long tenure of MBS papers and the lack of secondary

market liquidity still deter investors.

In CDO

Investment decisions influenced by the rating of the underlying

corporate exposures in a CDO pool (and not purely the rating of the

instrument) have impeded the growth of CDO in India. Corporate loan

securitization has been far lower than that in retail securitization.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 27/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 27

FINANCIAL MARKETSIn economics, a financial market is a mechanism that allows people to buyand sell (trade) financial securities (such as stocks and bonds),commodities (such as precious metals or agricultural goods), and otherfungible items of value at low transaction costs and at prices that reflect theefficient-market hypothesis.Both general markets (where many commodities are traded) andspecialized markets (where only one commodity is traded) exist. Marketswork by placing many interested buyers and sellers in one "place", thusmaking it easier for them to find each other. An economy which reliesprimarily on interactions between buyers and sellers to allocate resourcesis known as a market economy in contrast either to a command economyor to a non-market economy such as a gift economy.

DefinitionFinancial markets can be found in nearly every nation in the world. Someare very small, with only a few participants, while others – like the NationalStock Exchange (NSE).Most financial markets have periods of heavy trading and demand forsecurities in these periods, prices may rise above historical norms. Theconverse is also true downturns may cause prices to fall past levels ofintrinsic value, based on low levels of demand or other macroeconomicforces like tax rates, national production or employment levels .Informationtransparency is important to increase the confidence of participants andtherefore foster an efficient financial marketplace.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 28/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 28

TYPES OF FINANCIAL MARKETSThe financial markets can be divided into different subtypes

Capital markets which consist of

o Stock markets, which provide financing through the issuance of

shares or common stock, and enable the subsequent tradingthereof.

Bond markets, which provide financing through the issuance of

bonds, and enable the subsequent trading thereof.

Commodity markets, which facilitate the trading of commodities.

Money markets, which provide short term debt financing and

investment.

Derivatives markets, which provide instruments for the management

of financial risk. Futures markets, which provide standardized forward contracts for

trading products at some future date see also forward market.

Insurance markets, which facilitate the redistribution of various risks.

Foreign exchange markets, which facilitate the trading of foreign

exchange.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 29/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 29

CAPITAL MARKETSA market in which individuals and institutions trade financial securities.Organizations/institutions in the public and private sectors also often sellsecurities on the capital markets in order to raise funds. Thus, this type ofmarket is composed of both the primary and secondary markets. Whenreferring to a capital market, it is important to note that the term can refer toa rather broad range of products and services that are associated withfinances and investments. To that end, a capital market will include suchcomponents as the stock market, commodities exchanges, the bondmarket, and just about any physical or virtual facility or medium where debtand equity securities can be bought or sold. s a market for securities with avery broad reach, the capital market is an ideal environment for thecreation of strategies that can result in raising long-term funds for bondissues or even mortgages. At the same time, the capital market provides

the medium for short-term fund strategies as well. Essentially, any type offinancial transaction that is meant to result in the buying and selling ofsecurities and commodities for profit can rightly be considered part of thecapital market.Institutions are also part of the framework of the capital market. Stockexchanges are one of the more visible examples of established operationsthat give form and function to the capital market. Along with the stockexchanges, support organizations such as brokerage firms also form part ofthe capital market. Over the counter markets are also included in theworking definition for a capital market. By providing the mechanisms thatmake trading possible, these outward expressions of the capital marketmake it possible to keep the process ethical and more easily governedaccording to local laws and customs. Because of the broad structure of thecapital market, investors of all types have the opportunity to participate infinancial strategies that can strengthen the general economy as well createfinancial security. Persons who wish to focus on investment opportunitiesthat are very stable and more or less ensure a modest return can findplenty of different offerings to choose from. At the same time, investors whotend to be more adventurous can also find a wide array of investment types

that will allow them to take some additional risk and possibly realize largerreturns on their investments. While the overall structure of the capitalmarket may be broad, there are a number of checks and balances that helpto keep the market on an even keel, ensuring that the capital marketfunctions in a manner that is both ethical and legal.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 30/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 30

Capital Markets is divided in to Primary Markets

Secondary Markets

Primary marketA market that issues new securities on an exchange. Companies,governments and other groups obtain financing through debt or equitybased securities. Primary markets are facilitated by underwriting groups,which consist of investment banks that will set a beginning price range for agiven security and then oversee its sale directly to investors.Also known as "New issue market" (NIM).The primary markets are where investors can get first crack at a newsecurity issuance. The issuing company or group receives cash proceeds

from the sale, which is then used to fund operations or expand thebusiness. Exchanges have varying levels of requirements which must bemet before a security can be sold.Once the initial sale is complete, further trading is said to conduct on thesecondary market, which is where the bulk of exchange trading occurseach day. Primary markets can see increased volatility over secondarymarkets because it is difficult to accurately gauge investor demand for anew security until several days of trading have occurred.

Secondary MarketA market where investors purchase securities or assets from otherinvestors, rather than from issuing companies themselves. The nationalexchanges - such as the National Stock Exchange and the Bombay StockExchange are secondary markets. In any secondary market trade, thecash proceeds go to an investor rather than to the underlyingcompany/entity directly. A newly issued IPO will be considered a primarymarket trade when the shares are first purchased by investors directly from

the underwriting investment bank after that any shares traded will be on thesecondary market, between investors themselves. In the primary marketprices are often set beforehand, whereas in the secondary market onlybasic forces like supply and demand determine the price of the security.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 31/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 31

BOND MARKETThe bond market also known as the debt, credit, or fixed income market isa financial market where participants buy and sell debt securities, usually inthe form of bonds. As of 2009, the size of the worldwide bond market totaldebt outstanding is an estimated $82.2 trillion, of which the size of theoutstanding U.S. bond market debt was $31.2 trillion according to BISNearly all of the $822 billion average daily trading volume in the U.S. bondmarket takes place between broker-dealers and large institutions in adecentralized, over-the-counter (OTC) market. However, a small number ofbonds, primarily corporate, are listed on exchanges.References to the "bond market" usually refer to the government bondmarket, because of its size, liquidity, lack of credit risk and, therefore,sensitivity to interest rates. Because of the inverse relationship betweenbond valuation and interest rates, the bond market is often used to indicate

changes in interest rates or the shape of the yield curve.Market structureBond markets in most countries remain decentralized and lack commonexchanges like stock, future and commodity markets. This has occurred, inpart, because no two bond issues are exactly alike, and the variety of bondsecurities outstanding greatly exceeds that of stocks.However, the New York Stock Exchange (NYSE) is the largest centralizedbond market, representing mostly corporate bonds. The NYSE migratedfrom the Automated Bond System (ABS) to the NYSE Bonds tradingsystem in April 2007 and expects the number of traded issues to increasefrom 1000 to 6000.Besides other causes, the decentralized market structure of the corporateand municipal bond markets, as distinguished from the stock marketstructure, results in higher transaction costs and less liquidity. A studyperformed by Profs Harris and Piwowar in 2004, Secondary Trading Costsin the Municipal Bond Market, reached the following conclusions"Municipal bond trades are also substantially more expensive than similarsized equity trades. We attribute these results to the lack of pricetransparency in the bond markets. Additional cross-sectional analyses

show that bond trading costs decrease with credit quality and increase withinstrument complexity, time to maturity, and time since issuance."Ourresults show that municipal bond trades are significantly more expensivethan equivalent sized equity trades. Effective spreads in municipal bondsaverage about two percent of price for retail size trades of 20,000 dollarsand about one percent for institutional trade size trades of 200,000 dollars."

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 32/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 32

Types of bond marketsThe Securities Industry and Financial Markets Association (SIFMA) classifythe broader bond market into five specific bond markets.

Corporate

Government & agency Municipal

Mortgage backed, asset backed, and collateralized debt obligation

Funding

BOND MARKET PARTICIPANTSBond market participants are similar to participants in most financialmarkets and are essentially either buyers (debt issuer) of funds or sellers

(institution) of funds and often both.Participants include Institutional investors

Governments

Traders

Individuals

Because of the specificity of individual bond issues, and the lack of liquidityin many smaller issues, the majority of outstanding bonds are held by

institutions like pension funds, banks and mutual funds. In the UnitedStates, approximately 10% of the market is currently held by privateindividuals.

Bond indicesA number of bond indices exist for the purposes of managing portfolios andmeasuring performance, similar to the S&P 500 or Russell Indexes forstocks. The most common American benchmarks are the BarclaysAggregate, Citigroup BIG and Merrill Lynch Domestic Master. Most indicesare parts of families of broader indices that can be used to measure global

bond portfolios, or may be further subdivided by maturity and/or sector formanaging specialized portfolios.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 33/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 33

COMMODITY MARKETCommodity markets are markets where raw or primary products areexchanged. These raw commodities are traded on regulated commoditiesexchanges, in which they are bought and sold in standardized contracts.

Commodity Market in IndiaIndia has a long history of future trading in commodities. In India, tradinginCommodity future has been existence from the 19th Century withorganized tradingin Cotton, through the establishment at Bombay CottonAssociation Ltd. in 1875.Over a period of time other commodities werepermitted to be traded in futureexchanges. Spot trading in India occursmostly in regional mandis and unorganized market, which are fragmentedand isolated. There were booming activities in these market at one time asmany as 100 unorganised exchanges were conducting forward trade in

various commodities.The securities market was a poor competitor of thismarket as there were not manypapers to be traded at that time. However,many feared that derivatives fuelled unnecessary speculation and weredetrimental to the healthy functioning of the market for the underlyingcommodities. As a result, after independence, commodity option tradingand cash settlement of commodity future were banned in 1952. A furtherblow come in 1960‘s when following several years of several droughts hasforced many farmers to default on forward contact and even caused somesuicides, forward trading was banned in many commodities consideredprimary or essential. Consequently, the commodities derivatives marketdismantled and remained dormant for about four decades until the newmillennium when the Govt. in a complete change in policy, started activelyencouraging the commodity derivatives market. The year 2003 marked thereal turning point in the policy frame work for commodity market when thegovernment issued notifications for withdrawing all prohibitions andopening up forward trading in all commodities. This period also witnessedother reforms, such as, amendments to the Essential Commodities Act,Securitas (contract) Rules, which have reduced bottlenecks in thedevelopment and growth of commodity markets of the country is total GDP,

commodities related and dependent industries constitute about roughly 50-60% which itself cannot be ignored.

Modern Commodity Exchange-To make up the loss of growth and development during the four decadesofrestrictive Govt. policies, FMC and the government encouraged settingupcommodity exchanges using the most modern system and practices in

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 34/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 34

the world.Some of the main regulatory measures imposed in the FMCinclude daily market tomarket system of margins, creation of tradeguarantee fund, back office computerization for the existing singlecommodity exchanges , online trading for thenew exchanges,demutualization for the new exchanges and one thirdrepresentation ofindependent Directions the Board of existing Exchanges etc.National Level Commodity Exchanges in India are

NMCE National Multi Commodity Exchange of India.

NCDEX National Commodity Derivatives Exchange Ltd.

MCX Multi Commodity Exchange of India Ltd.

ICEX Indian Commodity Exchange Ltd.

Regulator of Commodity exchangesFMCL forward Market commission headquarted in Mumbai, isregulationauthority which is overseen by the minister of consumer affairs,food and publicdistribution Govt. of India, It is station body set up in 1953under the forwardcontract (Regulation) Act 1952.

Key Factors for success of commodities marketThe following are source of the key factors for the success of thecommodities market

How are can make the business grow? How many products are covered?

How many people participate in the Platform?

Key Factors for success of commodity exchangesStrategy, method of execution, background of promoters, credibility oftheinstitution, transparency of platforms, scale able technology, robustnessofsettlement structure wider participation of Hedgers speculators and

arbitragers,acceptable clearing mechanism, financial soundness andcapability, covering awide range of commodity, reach of the organizationand adding value on theground.In addition to his, if the Indian Commodityexchanges needs to be competitive inthe Global Market, then it should bebacked with proper ―capital accountconvertibility‖.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 35/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 35

MONEY MARKETMoney market means market where money or its equivalent can be traded.Money is synonym of liquidity. Money market consists of financialinstitutions and dealers in money or credit who wish to generate liquidity. Itis better known as a place where large institutions and governmentmanage their short term cash needs. For generation of liquidity, short termborrowing and lending is done by these financial institutions and dealers.Money Market is part of financial market where instruments with highliquidity and very short term maturities are traded. Due to highly liquidnature of securities and their short term maturities, money market is treatedas a safe place. Hence, money market is a market where short termobligations such as treasury bills, commercial papers and banker‘sacceptances are bought and sold.

Benefits and functions of Money MarketMoney markets exist to facilitate efficient transfer of short-term fundsbetween holders and borrowers of cash assets. For the lender/investor, itprovides a good return on their funds. For the borrower, it enables rapidand relatively inexpensive acquisition of cash to cover short-term liabilities.One of the primary functions of money market is to provide focal point forRBI‘s intervention for influencing liquidity and general levels of interestrates in the economy. RBI being the main constituent in the money marketaims at ensuring that liquidity and short term interest rates are consistentwith the monetary policy objectives.

Money Market InstrumentsInvestment in money market is done through money marketInstruments.Money market instrument meets short term requirements of the borrowersand provides liquidity to the lenders. Common Money Market Instrumentsare as follows

Treasury Bills

Treasury Bills, one of the safest money market instruments, are short termborrowing instruments of the Central Government of the Country issuedthrough the Central Bank (RBI in India). They are zero risk instruments,and hence the returns are not so attractive. It is available both in primarymarket as well as secondary market. It is a promise to pay a said sum aftera specified period. T-bills are short-term securities that mature in one yearor less from their issue date. They are issued with three-month, six-month

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 36/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 36

and one-year maturity periods. The Central Government issues T- Bills at aprice less than their face value (par value). They are issued with a promiseto pay full face value on maturity. So, when the T-Bills mature, thegovernment pays the holder its face value.

Commercial Papers Commercial paper is a low-cost alternative to bank loans. It is a short termunsecured promissory note issued by corporates and financial institutionsat a discounted value on face value. They are usually issued with fixedmaturity between one to 270 days and for financing of accountsreceivables, inventories and meeting short term liabilities.They yield higherreturns as compared to T-Bills as they are less secure in comparison tothese bills however chances of default are almost negligible but are notzero risk instruments.

Certificate of Deposit It is a short term borrowing more like a bank term deposit account. It is apromissory note issued by a bank in form of a certificate entitling the bearerto receive interest. The certificate bears the maturity date, the fixed rate ofinterest and the value. It can be issued in any denomination. They arestamped and transferred by endorsement. Its term generally ranges fromthree months to five years and restricts the holders to withdraw funds ondemand. However, on payment of certain penalty the money can bewithdrawn on demand also. The returns on certificate of deposits are higherthan T-Bills because it assumes higher level of risk.

Bankers Acceptance It is a short term credit investment created by a non financial firm andguaranteed by a bank to make payment. It is simply a bill of exchangedrawn by a person and accepted by a bank. It is a buyer‘s promise to payto the seller a certain specified amount at certain date. The same isguaranteed by the banker of the buyer in exchange for a claim on thegoods as collateral. The person drawing the bill must have a good credit

rating otherwise the Banker‘s Acceptance will not be tradable. The mostcommon term for these instruments is 90 days. However, they can veryfrom 30 days to180 days.

An individual player cannot invest in majority of the Money MarketInstruments, hence for retail market, money market instruments arerepackaged into Money Market Funds.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 37/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 37

It is like a mutual fund, except the fact mutual funds cater to capital marketand money market funds cater to money market. Money Market funds canbe categorized as taxable funds or non taxable funds.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 38/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 38

DERIVATIVES MARKETSA derivative security is a financial contract whose value is derived from thevalue of something else, such as a stock price, a commodity price, anexchange rate, an interest rate, or even an index of prices. Derivatives maybe traded for a variety of reasons. A derivative enables a trader to hedgesome preexisting risk by taking positions in derivatives markets that offsetpotential losses in the underlying or spot market. In India, most derivativesusers describe themselves as hedgers and Indian laws generally requirethat derivatives be used for hedging purposes only. Another motive forderivatives trading is speculation (i.e. taking positions to profit fromanticipated price movements). In practice, it may be difficult to distinguishwhether a particular trade was for hedging or speculation, and activemarkets require the participation of both hedgers and speculators.

Development of derivatives market in IndiaThe first step towards introduction of derivatives trading in India was thepromulgation of the Securities Laws (Amendment) Ordinance, 1995, whichwithdrew the prohibition on options in securities. The market for derivatives,however, did not take off, as there was no regulatory framework to governtrading of derivatives. SEBI set up a 24 –member committee under theChairmanship of Dr.L.C.Gupta on November 18, 1996 to developappropriate regulatory framework for derivatives trading in India. Thecommittee submitted its report on March 17, 1998 prescribing necessarypre –conditions for introduction of derivatives trading in India. Thecommittee recommended that derivatives should be declared as ‗securities‘so that regulatory framework applicable to trading of ‗securities‘ could alsogovern trading of securities. SEBI also set up a group in June 1998 underthe Chairmanship of Prof.J.R.Varma, to recommend measures for riskcontainment in derivatives market in India. The report, which was submittedin October 1998, worked out the operational details of margining system,methodology for charging initial margins, broker net worth, depositrequirement and real –time monitoring requirements. The SecuritiesContract Regulation Act (SCRA) was amended in December 1999 to

include derivatives within the ambit of ‗securities‘ and the regulatoryframework was developed for governing derivatives trading. The act alsomade it clear that derivatives shall be legal and valid only if such contractsare traded on a recognized stock exchange, thus precluding OTCderivatives. Derivatives trading commenced in India in June 2000 afterSEBI granted the final approval to this effect in May 2001. SEBI permittedthe derivative segments of two stock exchanges, NSE and BSE, and their

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 39/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 39

clearing house/corporation to commence trading and settlement inapproved derivatives contracts. To begin with, SEBI approved trading inindex futures contracts based on S&P CNX Nifty and BSE –30(Sensex)index.The trading in BSE Sensex options commenced on June 4, 2001 andthe trading in options on individual securities commenced in July 2001.Futures contracts on individual stocks were launched in November 2001.The derivatives trading on NSE commenced with S&P CNX Nifty Indexfutures on June 12, 2000. The trading in index options commenced onJune 4, 2001 and trading in options on individual securities commenced onJuly 2, 2001. Single stock futures were launched on November 9, 2001.The index futures and options contract on NSE are based on S&P CNX.

Types of Derivatives

Forwards

A forward contract is a customized contract between two entities,where settlement takes place on a specific date in the future at

today‘s pre-agreed price.

Futures

A futures contract is an agreement between two parties to buy or sell

an asset at a certain time in the future at a certain price. Futures

contracts are special types of forward contracts in the sense that the

former are standardized exchange-traded contracts

OptionsOptions are of two types - calls and puts. Calls give the buyer the

right but not the obligation to buy a given quantity of the

underlyingasset, at a given price on or before a given future date.

Puts give the buyer the right, but not the obligation to sell a given

quantity of the underlying asset at a given price on or before a given

date.

Warrants

Options generally have lives of upto one year, the majority of optionstraded on options exchanges having a maximum maturity of nine

months. Longer-dated options are called warrants and are generally

traded over-the-counter.

Leaps

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 40/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 40

The acronym LEAPS means Long-Term Equity Anticipation

Securities. These are options having a maturity of upto three years.

Baskets

Basket options are options on portfolios of underlying assets. The

underlying asset is usually a moving average or a basket of assets.Equity index options are a form of basket options.

Swaps

Swaps are private agreements between two parties to exchange cash

flows in the future according to a prearranged formula. They can be

regarded as portfolios of forward contracts. The two commonly used

swaps are

o Interest rate swaps

These entail swapping only the interest related cash flowsbetween the parties in the same currency.

o Currency swaps

These entail swapping both principal and interest between

theparties, with the cashflows in one direction being in a

different currency than those in the opposite direction.

o Swaptions

Swaptions are options to buy or sell a swap that will become

operative at the expiry of the options.Rather than have callsand puts, the swaptions market has receiver swaptions and

payer swaptions. A receiver swaption is an option to receive

fixed and pay floating. A payer swaption is an option to pay

fixed and receive floating.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 41/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 41

FORWARDSA forward contract or simply a forward is a contract between two parties tobuy or sell an asset at a certain future date for a certain price that is pre-decided on the date of the contract. The future date is referred to as expirydate and the pre-decided price is referred to as Forward Price. It may benoted that Forwards are private contracts and their terms are determinedby the parties involved. A forward is thus an agreement between twoparties in which one party, the buyer, enters into an agreement with theother party, the seller that he would buy from the seller an underlying asseton the expiry date at the forward price. Therefore, it is a commitment byboth the parties to engage in a transaction at a later date with the price setin advance. This is different from a spot market contract, which involvesimmediate payment and immediate transfer of asset. The party that agreesto buy the asset on a future date is referred to as a long investor and is said

to have a long position. Similarly the party that agrees to sell the asset in afuture date is referred to as a short investor and is said to have a shortposition. The price agreed upon is called the delivery price or the ForwardPrice. Forward contracts are traded only in Over the Counter (OTC) marketand not in stock exchanges. OTC market is a private market whereindividuals/institutions can trade through negotiations on a one to onebasis.

Settlement of forward contractsWhen a forward contract expires, there are two alternate arrangementspossible to settle the obligation of the parties physical settlement and cashsettlement. Both types of settlements happen on the expiry date and a regiven below.

Physical SettlementA forward contract can be settled by the physical delivery of the underlyingasset by a short investor (i.e. the seller) to the long investor (i.e. the buyer)and the payment of the agreed forward price by the buyer to the seller onthe agreed settlement date.

Cash SettlementCash settlement does not involve actual delivery or receipt of the security.Each party either pays (receives) cash equal to the net loss (profit) arisingout of their respective position in the contract.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 42/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 42

Default risk in forward contractsA drawback of forward contracts is that they are subject to default risk.Regardless of whether the contract is for physical or cash settlement, thereexists a potential for one party to default, i.e. not honor the contract. It couldbe either the buyer or the seller. This results in the other party suffering aloss. This risk of making losses due to any of the two parties defaulting isknown as counter party risk. The main reason behind such risk is theabsence of any mediator between the parties, who could have undertakenthe task of ensuring that both the parties fulfill their obligations arising out ofthe contract. Default risk is also referred to as counter party risk or creditrisk.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 43/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 43

FUTURESLike a forward contract, a futures contract is an agreement between twoparties in which the buyer agrees to buy an underlying asset from theseller, at a future date at a price that is agreed upon today. However, unlikea forward contract, a futures contract is not a private transaction but getstraded on a recognized stock exchange. In addition, a futures contract isstandardized by the exchange. All the terms, other than the price, are setby the stock exchange rather than by individual parties as in the case of aforward contract. Also, both buyer and seller of the futures contracts areprotected against the counter party risk by an entity called the ClearingCorporation. The Clearing Corporation provides this guarantee to ensurethat the buyer or the seller of a futures contract does not suffer as a resultof the counter party defaulting on its obligation. In case one of the partiesdefaults, the Clearing Corporation steps in to fulfill the obligation of this

party, so that the other party does not suffer due to non-fulfillment of thecontract. To be able to guarantee the fulfillment of the obligations under thecontract, the Clearing Corporation holds an amount as a security from boththe parties. This amount is called the Margin money and can be in the formof cash or other financial assets. Also, since the futures contracts aretraded on the stock exchanges, the parties have the flexibility of closing outthe contract prior to the maturity by squaring off the transactions in themarket.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 44/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 44

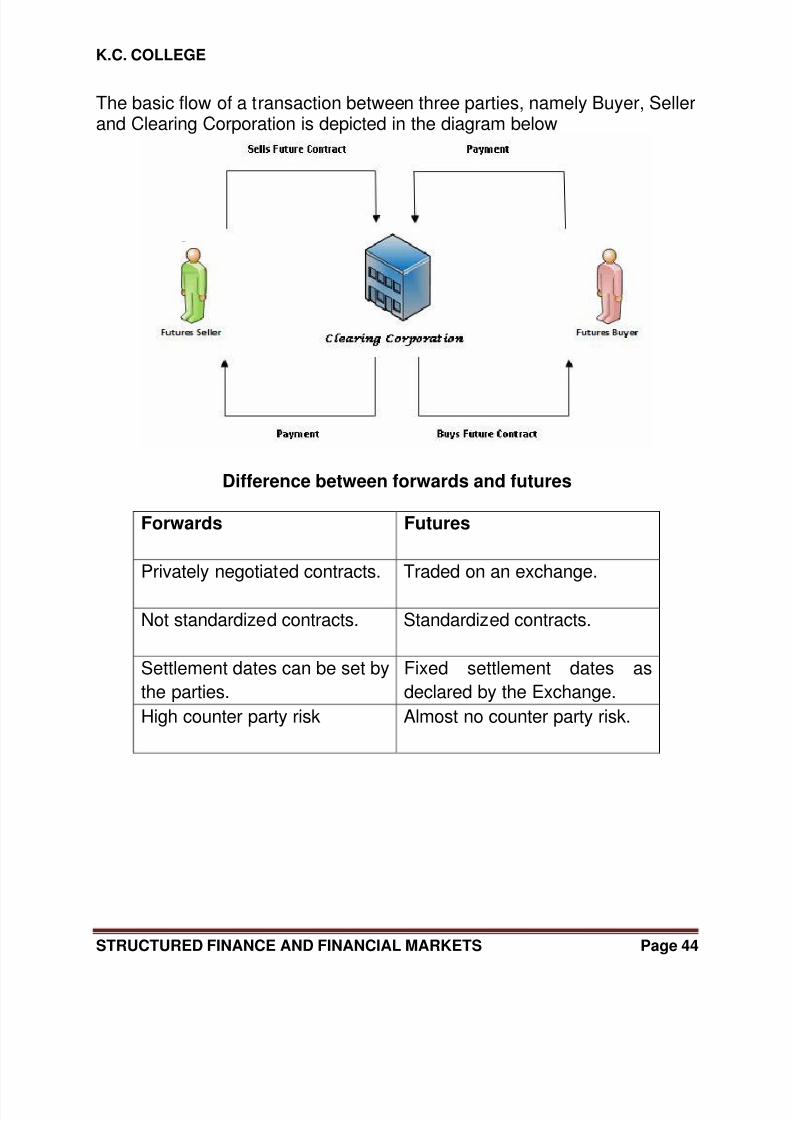

The basic flow of a transaction between three parties, namely Buyer, Sellerand Clearing Corporation is depicted in the diagram below

Difference between forwards and futures

Forwards Futures

Privately negotiated contracts. Traded on an exchange.

Not standardized contracts. Standardized contracts.

Settlement dates can be set by

the parties.

Fixed settlement dates as

declared by the Exchange.

High counter party risk Almost no counter party risk.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 45/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 45

OPTIONSAn option is a derivative contract between a buyer and a seller, where oneparty (say First Party) gives to the other (say Second Party) the right, butnot the obligation, to buy from (or sell to) the First Party the underlyingasset on or before a specific day at an agreed-upon price. In return forgranting the option, the party granting the option collects a payment fromthe other party. This payment collected is called the ―premium‖ or price of the option. The right to buy or sell is held by the ―option buyer‖ (also ca lledthe option holder) the party granting the right is t he ―option seller‖ or ―option writer‖. Unlike forwards and futures contracts, options require acash payment (called the premium) upfront from the option buyer to theoption seller. This payment is called option premium or option price.Options can be traded either on the stock exchange or in over the counter

(OTC) markets. Options traded on the exchanges are backed by theClearing Corporation thereby minimizing the risk arising due to default bythe counter parties involved. Options traded in the OTC market howeverare not backed by the Clearing Corporation.

There are two types of options Call options

Put options

Call optionA call option is an option granting the right to the buyer of the option to buythe underlying asset on a specific day at an agreed upon price, but not theobligation to do so. It is the seller who grants this right to the buyer of theoption. It may be noted that the person who has the right to buy theunderlying asset is known as the ―buyer of the call option‖. The price atwhich the buyer has the right to buy the asset is agreed upon at the time ofentering the contract. This price is known as the strike price of the contract(call option strike price in this case). Since the buyer of the call option has

the right (but no obligation) to buy the underlying asset, he will exercise hisright to buy the underlying asset if and only if the price of the underlyingasset in the market is more than the strike price on or before the expirydate of the contract. The buyer of the call option does not have anobligation to buy if he does not want to.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 46/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 46

Put optionA put option is a contract granting the right to the buyer of the option to sellthe underlying asset on or before a specific day at an agreed upon price,but not the obligation to do so. It is the seller who grants this right to thebuyer of the option. The person who has the right to sell the underlyingasset is known as the ―buyer of the put option‖. The price at which thebuyerhas the right to sell the asset is agreed upon at the time of enteringthe contract. This price is known as the strike price of the contract (putoption strike price in this case). Since the buyer of the put option has theright (but not the obligation) to sell the underlying asset, he will exercise hisright to sell the underlying asset if and only if the price of the underlyingasset in the market is less than the strike price on or before the expiry dateof the contract. The buyer of the put option does not have the obligation tosell if he does not want to.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 47/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 47

Differences between futures and options

Futures Options

Both the buyer and the seller areunder an obligation to fulfill the

Contract.

The buyer of the option has theright and not an obligation

whereas the seller is under

obligation to fulfill the contract if

and when the buyer Exercises

his right.

The buyer and the seller are

Subject to unlimited risk of loss.

The seller is subjected to

unlimited risk of losing whereas

the buyer has limited potential to

lose(This is the option premium).

The buyer and the seller have

potential to make unlimited gain

or

Loss.

The buyer has potential to make

unlimited gain while the seller

has a potential to make unlimited

Gain. On the other hand the

buyer has a limited loss potential

and the seller has an unlimited

loss potential.

8/8/2019 Structured Finance and Financial Markets

http://slidepdf.com/reader/full/structured-finance-and-financial-markets 48/57

K.C. COLLEGE

STRUCTURED FINANCE AND FINANCIAL MARKETS Page 48

COMMODITY DERIVATIVES MARKETWhy is Commodity Derivatives Required? India is among the top-5 producers of most of the commodities, in additionto being a major consumer of bullion and energy products. Agriculturecontributes about 22% to the GDP of the Indian economy. It employeesaround 57% of the labor force on a total of 163 million hectares of land.Agriculture sector is an important factor in achieving a GDP growth of 8-10%. All this indicates that India can be promoted as a major center fortrading of commodity derivatives. It is unfortunate that the policies of FMCduring the most of 1950s to 1980s suppressed the very markets it wassupposed to encourage and nurture to grow with times. However, it is not inIndia alone that derivatives were suspected of creating too muchspeculation that would be to the detriment of the healthy growth of the

markets and the farmers. Such suspicions might normally arise due to amisunderstanding of the characteristics and role of derivative product. It iscommon knowledge that prices of commodities, metals, shares andcurrencies fluctuate over time. The possibility of adverse price changes infuture creates risk for businesses. Derivatives are used to reduce oreliminate price risk arising from unforeseen price changes. A derivative is afinancial contract whose price depends on, or is derived from, the price ofanother asset.Two important derivatives are futures and options.

Commodity Futures ContractsA futures contract is an agreement for buying or selling a commodity

for a predetermined delivery price at a specific future time. Futures

are standardized contracts that are traded on organized futures

exchanges that ensureperformance of the contracts and thus remove

the default risk. The commodity futureshave existed since the

Chicago Board of Trade (CBOT, www.cbot.com) was establishedin

1848 to bring farmers and merchants together. The major function of

futures markets is to transfer price risk from hedgers to speculators.

For example, suppose a farmer isexpecting his crop of wheat to be

ready in two months time, but is worried that the priceof wheat may

decline in this period. In order to minimize his risk, he can enter into

afutures contract to sell his crop in two months‘ time at a price

determined now. This wayhe is able to hedge his risk arising from a