Embed Size (px)

Citation preview

Structural Dynamic Analysis of

Systematic Risk

Laurent Calvet, Veronika Czellar and Christian Gourieroux∗

First version: August 2014

This version: December 27, 2015

Preliminary version

∗Calvet: Department of Finance, HEC Paris; [email protected]. Czellar: Department of Accounting,Law, Finance and Economics, EDHEC Business School; [email protected]. Gourieroux:CREST, Paris and Department of Economics, University of Toronto; [email protected]. We grate-fully acknowledge the computer support of EUROFIDAI.

Abstract

This paper introduces a structural dynamic factor model (SDFM) for stock

returns. Compared to standard linear factor models, structural modeling ac-

counts for nonlinear effects of common factors when the distance-to-default

is small. Such a SDFM has a rather complicated form, especially since the

underlying factors are unobservable and have nonlinear effects. We develop

appropriate methods to estimate such models and use them for prediction,

filtering and smoothing purposes, such as indirect inference or Approximate

Bayesian Computation (ABC) filtering and smoothing. These SDFM are ap-

plied to the analysis of systematic risk of financial institutions and to obtain

their rating of default and speculative features.

Keywords: Systematic Risk, SIFI, Merton’s Model, Value-of-the-Firm, Indi-

rect Inference, Rating, ABC Filtering and Smoothing.

1 Introduction

The analysis of systematic risk from stock returns is usually based on dynamic linear

factor models, where the factors can feature conditional heteroscedasticity. Typi-

cal examples are models derived from the Capital Asset Pricing Model (CAPM),

in which the linear factors can be interpreted in terms of market portfolio returns

(Markowitz, 1959; Sharpe, 1964; Lintner, 1965). Such models are used to separate

risk and required capital into two components: the systematic risk component mea-

sures the effects of the systematic factors, taking into account the sensitivities to

the factors (or betas); the specific risk corresponds to the residual risk once the

systematic component is taken into account.

However, the hypothesis of linear effect of the systematic factors has been ques-

tioned, in particular for factor values, which might create default of important finan-

cial institutions, the so-called systematically important financial institutions (SIFI).

Indeed, if a firm is close to default, the stock price will integrate the cost of default-

risk with a nonlinear impact of the systematic factor.1 The nonlinear effect is due

to the interpretation of a stock as a call option written on the asset component of

the balance sheet of the firm with strike its liability component. According to the

literature, this option can be either a European call (Merton, 1974), or an American

call (Black and Cox, 1976).

The nonlinear effect is expected to be more significant for financial institutions,

which have to support not only inappropriate direct credit granting, but also the often

huge investments in credit derivatives such as Mortgage Backed Securities (MBS),

Collateral Debt Obligations (CDO) and other Sovereign Credit Default Swaps (CDS).

The objective of our paper is to include the option interpretation when analyzing

systematic risk in the stock returns of financial institutions and intermediaries. Our

structural approach is in the spirit of the rating models developed by KMV (see

e.g. Crosbie and Bohn (2004)), but with more focus on the factor dynamics and the

possibility of stochastic volatility. It is also related to the structural extension of

multivariate GARCH models developed in Engle and Siriwardane (2015).

We base our analysis on stock returns of ten financial institutions. The data are

presented and discussed in Section 2. In particular, we focus on: the static linear

1We prefer to use the terminology systematic instead of systemic for the common factors. Indeed,a shock on a common factor does not necessarily imply a risk of destruction of the financial system(see e.g. Hansen (2012) for a discussion of the two notions).

2

factor, which can be exhibited and its link with the S&P 500 market return.

We consider in Section 3 a one-factor linear model for analyzing jointly the re-

turn of the financial institutions. This linear factor model differs from the standard

Sharpe-Lintner model, since it accounts for stochastic volatility effects. Two types of

stochastic volatilities are introduced, that are a stochastic volatility for the common

factor and stochastic volatilities specific to each financial institution. We assume

that both the common linear factor and the volatilities are latent. Thus we get a

nonlinear multifactor model due to the introduction of stochastic volatilities. In par-

ticular, the likelihood function of this nonlinear state-space model has a complicated

form, which involves multidimensional integrals, with a dimension increasing with

the number of observations. We develop an appropriate indirect inference approach

(Gourieroux, Monfort and Renault, 1993; Smith, 1993) to estimate the model, i.e. to

capture the factor sensitivities as well as the dynamics of the factor and volatilities.

This approach is applied to the return data. In particular, we discuss the dynamic

link between the filtered factor and the submarket portfolio derived from the static

approach.

The factor model of Section 3 does not account for default risk. Default risk is

introduced in Section 4 and creates an additional source of nonlinearity. We first

review the Value-of-the Firm model, the effect of the distance-to-default on stock

values, and approximate this nonlinear effect to get a link between the changes in

the log asset/liability rates, and the stock returns. Then, the analysis is extended to

the multiasset framework. From the modelling point of view, this leads to a model

defined in two components. The linear factor model with stochastic volatilities of

Section 3 is used to define the joint dynamics of the unobserved changes in the log

asset/liability ratios. Then a nonlinear measurement equation relates the observed

stock returns to these changes and includes the nonlinear effect of the distance-to-

3

default. This structural dynamic factor model (SDFM) is estimated and the results

are compared with the outputs of the dynamic model without option of default. Then

it is used to construct different ratings, that are a solvency rating, a rating based on

the market price of the insurance against default, and a rating for speculative feature

of the associated stock.

Section 5 concludes.

2 Data

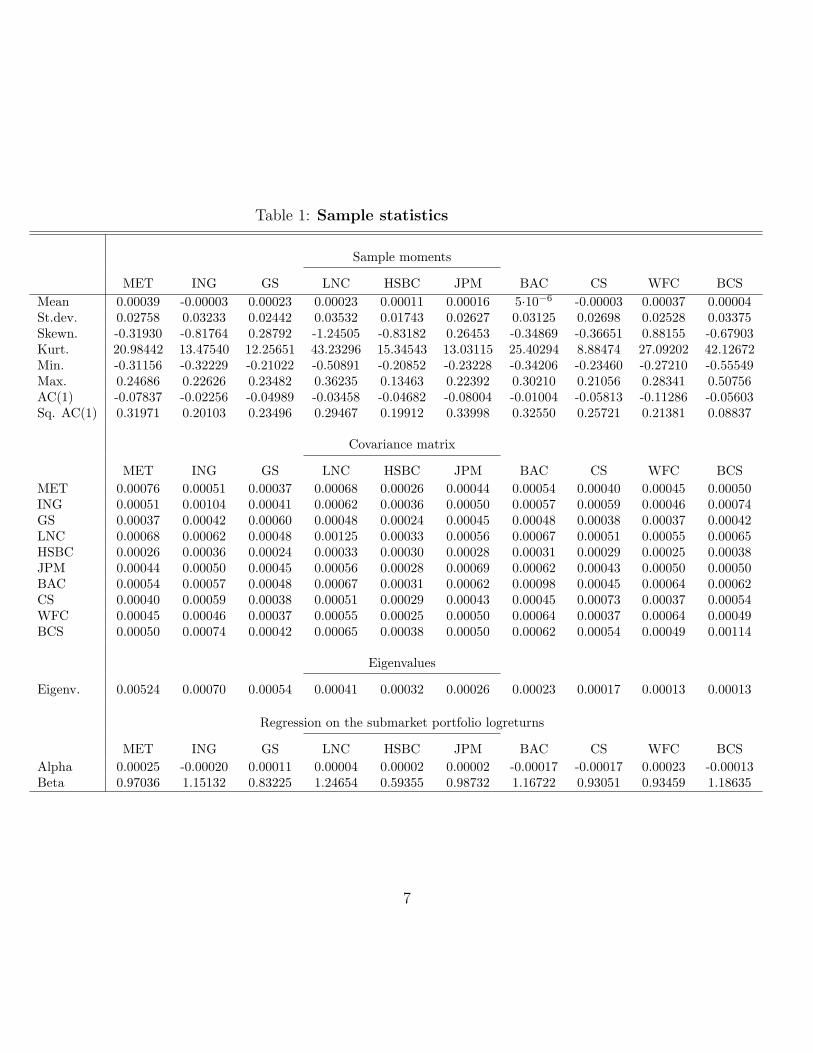

We consider the daily logreturns between April 6, 2000, and July 31, 2015, of ten

financial institutions: MetLife Inc. (MET), ING Group (ING), Goldman Sachs

Group Inc. (GS), Lincoln National Corp. (LNC), HSBC Holdings plc. (HSBC),

JPMorgan Chase & Co. (JPM), Bank of America Corp. (BAC), Credit Suisse Group

AG (CS), Wells Fargo & Co. (WFC), Barclays plc. (BCS). The daily logreturns are

log(Pit/Pi,t−1), where Pit is the closing price of financial stock i at date t adjusted for

dividends and splits, downloaded from Yahoo Finance.2 All returns are computed

in U.S. dollars. The logreturn series are plotted in Figure 1. The sample size of the

logreturn series is T = 3, 853 (trading days). Table 1 reports sample statistics of the

return series.

We immediately observe in Figure 1 stochastic and persistent volatilities. Large

volatilities arise to all series at the period of the recent financial crisis, i.e. 2008-2010,

and also for several series in 2012.

The mean returns are between -1% and 10% per year on this period, with large

kurtosis revealing fat tails. These tail features are partly due to the crises, with

negative daily returns up to 50% (for LNC and BCS), which corresponds to a decrease

2finance.yahoo.com

4

−0.

60.

00.

4

HS

BC

−0.

60.

00.

4

ING

−0.

60.

00.

4

CS

−0.

60.

00.

4

BC

S

2000 2005 2010 2015

−0.

60.

00.

4

BA

C

−0.

60.

00.

4

ME

T

−0.

60.

00.

4

GS

−0.

60.

00.

4

LNC

−0.

60.

00.

4

JPM

2000 2005 2010 2015

−0.

60.

00.

4

WF

C

Figure 1: Logreturn series.

of 40% of the price. However, we also observe large log-returns, up to a price increase

of 60% for BCS. The skewnesses are negative, except for GS, JPM and WFC. This

negative sign can be due to a crash going faster than the recovery.

The dynamics of the series are summarized by the autocorrelations of the returns

5

and squared returns, respectively. The first-order autocorrelations of the returns are

very small (the largest one in absolute value is 6.7 ·10−20 per month), as expected for

an efficient market. At the opposite, the autocorrelations of the squared returns are

larger (between 0.20 and 0.34, except for BCS), indicating the volatility persistence.

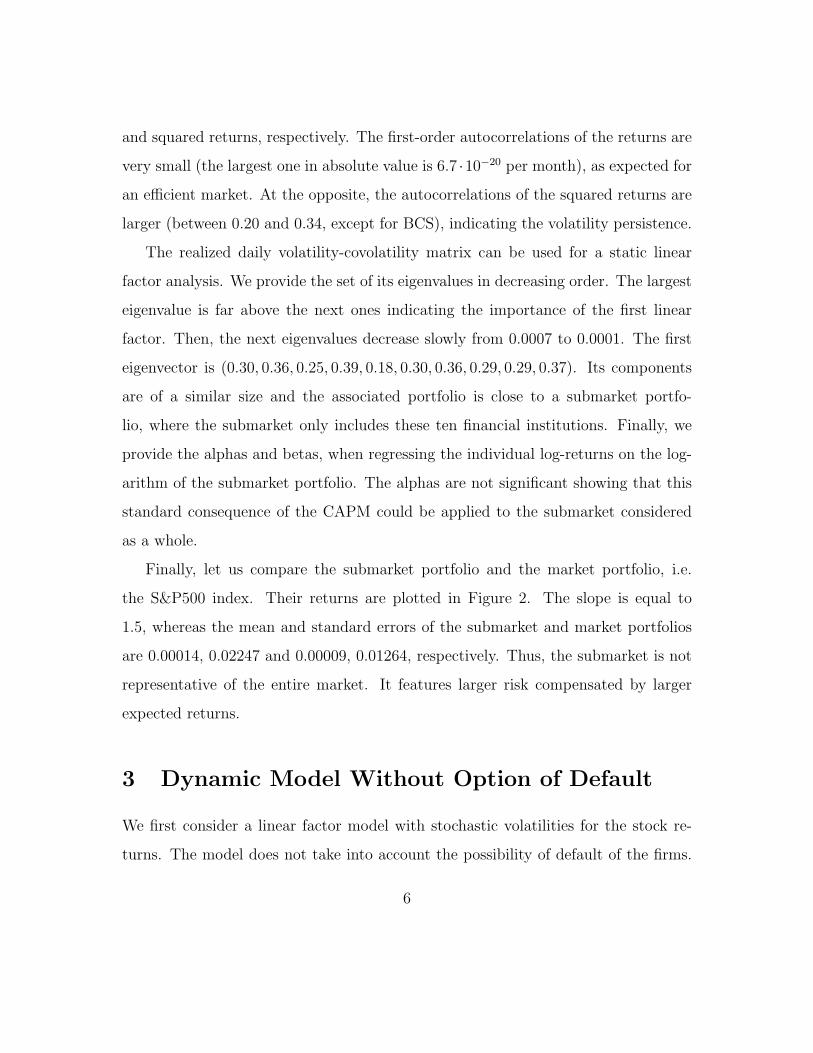

The realized daily volatility-covolatility matrix can be used for a static linear

factor analysis. We provide the set of its eigenvalues in decreasing order. The largest

eigenvalue is far above the next ones indicating the importance of the first linear

factor. Then, the next eigenvalues decrease slowly from 0.0007 to 0.0001. The first

eigenvector is (0.30, 0.36, 0.25, 0.39, 0.18, 0.30, 0.36, 0.29, 0.29, 0.37). Its components

are of a similar size and the associated portfolio is close to a submarket portfo-

lio, where the submarket only includes these ten financial institutions. Finally, we

provide the alphas and betas, when regressing the individual log-returns on the log-

arithm of the submarket portfolio. The alphas are not significant showing that this

standard consequence of the CAPM could be applied to the submarket considered

as a whole.

Finally, let us compare the submarket portfolio and the market portfolio, i.e.

the S&P500 index. Their returns are plotted in Figure 2. The slope is equal to

1.5, whereas the mean and standard errors of the submarket and market portfolios

are 0.00014, 0.02247 and 0.00009, 0.01264, respectively. Thus, the submarket is not

representative of the entire market. It features larger risk compensated by larger

expected returns.

3 Dynamic Model Without Option of Default

We first consider a linear factor model with stochastic volatilities for the stock re-

turns. The model does not take into account the possibility of default of the firms.

6

Table 1: Sample statistics

Sample moments

MET ING GS LNC HSBC JPM BAC CS WFC BCS

Mean 0.00039 -0.00003 0.00023 0.00023 0.00011 0.00016 5·10−6 -0.00003 0.00037 0.00004St.dev. 0.02758 0.03233 0.02442 0.03532 0.01743 0.02627 0.03125 0.02698 0.02528 0.03375Skewn. -0.31930 -0.81764 0.28792 -1.24505 -0.83182 0.26453 -0.34869 -0.36651 0.88155 -0.67903Kurt. 20.98442 13.47540 12.25651 43.23296 15.34543 13.03115 25.40294 8.88474 27.09202 42.12672Min. -0.31156 -0.32229 -0.21022 -0.50891 -0.20852 -0.23228 -0.34206 -0.23460 -0.27210 -0.55549Max. 0.24686 0.22626 0.23482 0.36235 0.13463 0.22392 0.30210 0.21056 0.28341 0.50756AC(1) -0.07837 -0.02256 -0.04989 -0.03458 -0.04682 -0.08004 -0.01004 -0.05813 -0.11286 -0.05603Sq. AC(1) 0.31971 0.20103 0.23496 0.29467 0.19912 0.33998 0.32550 0.25721 0.21381 0.08837

Covariance matrix

MET ING GS LNC HSBC JPM BAC CS WFC BCS

MET 0.00076 0.00051 0.00037 0.00068 0.00026 0.00044 0.00054 0.00040 0.00045 0.00050ING 0.00051 0.00104 0.00041 0.00062 0.00036 0.00050 0.00057 0.00059 0.00046 0.00074GS 0.00037 0.00042 0.00060 0.00048 0.00024 0.00045 0.00048 0.00038 0.00037 0.00042LNC 0.00068 0.00062 0.00048 0.00125 0.00033 0.00056 0.00067 0.00051 0.00055 0.00065HSBC 0.00026 0.00036 0.00024 0.00033 0.00030 0.00028 0.00031 0.00029 0.00025 0.00038JPM 0.00044 0.00050 0.00045 0.00056 0.00028 0.00069 0.00062 0.00043 0.00050 0.00050BAC 0.00054 0.00057 0.00048 0.00067 0.00031 0.00062 0.00098 0.00045 0.00064 0.00062CS 0.00040 0.00059 0.00038 0.00051 0.00029 0.00043 0.00045 0.00073 0.00037 0.00054WFC 0.00045 0.00046 0.00037 0.00055 0.00025 0.00050 0.00064 0.00037 0.00064 0.00049BCS 0.00050 0.00074 0.00042 0.00065 0.00038 0.00050 0.00062 0.00054 0.00049 0.00114

Eigenvalues

Eigenv. 0.00524 0.00070 0.00054 0.00041 0.00032 0.00026 0.00023 0.00017 0.00013 0.00013

Regression on the submarket portfolio logreturns

MET ING GS LNC HSBC JPM BAC CS WFC BCS

Alpha 0.00025 -0.00020 0.00011 0.00004 0.00002 0.00002 -0.00017 -0.00017 0.00023 -0.00013Beta 0.97036 1.15132 0.83225 1.24654 0.59355 0.98732 1.16722 0.93051 0.93459 1.18635

7

−0.2 −0.1 0.0 0.1 0.2

−0.

2−

0.1

0.0

0.1

0.2

S&P 500

Sub

mar

ket p

orfo

lio

Figure 2: Submarket portfolio versus S&P500. The submarket portfolio log-returnis plotted versus the S&P500 log-return. A simple linear regression provides anintercept of 10−5 and a slope of 1.5011.

Let us denote by Yit, i = 1, . . . , n, t = 1, . . . , T the returns at date t for firm (stock)

8

i. The return dynamics is defined by:Yit = αi + βiFt + σitϵit , i = 1, . . . , n ,

Ft = γFt−1 + ηtut ,

(3.1)

where Ft is a common unobservable linear factor, the ϵits and uts are indepen-

dent standard normal variables, the σits and ηts are specific and factor stochastic

volatilities, respectively. The stochastic volatilities are assumed mutually indepen-

dent, and independent of the standardized specific and factor innovations ϵ, u, with

autoregressive gamma (ARG) dynamics: η2t ∼ ARG[δ, ρ, (1 − ρ)(1 − γ2)/δ] and

σ2it ∼ ARG(δ, ρ, c), where νt ∼ARG(a, b, c) is equivalent with νt ∼Gamma(a+zt, c)

and zt ∼Poisson(bνt−1/c). The parameters a, b, c of the ARG(a, b, c) can be inter-

preted as a degree of freedom, a measure of serial dependence and a scale parameter,

respectively. The ARG processes are exact time discretized Cox, Ingersoll, Ross

(CIR) processes, usually employed for the modelling of stochastic volatility in con-

tinuous time [see Cox, Ingersoll and Ross (1985) for the CIR process and Gourieroux

and Jasiak (2006) and Appendix 5.1 for the properties of ARG processes].

Since a dynamic factor is defined up to a linear affine transformation, without loss

of generality the linear factor dynamics can be constrained to satisfy E(Ft) = 0 and

V (Ft) = 1, ∀t. These identification restrictions have been taken into account in the

dynamic model above. The condition E(Ft) = 0 is due to the absence of intercept in

the autoregression satisfied by the factor; the condition V (Ft) = 1 is a consequence

of the link between the three parameters of the ARG process satisfied by ηt.

The model above involves different parameters: the αis are the expected stock

returns, whereas the βis provide the sensitivities of the stock returns with respect to

the common linear factor, and γ is a measure of the factor persistence. The remaining

9

parameters characterize the volatility dynamics. The model differs from the standard

linear factor model [see e.g. Darolles and Gourieroux (2015), Chapter 3] by the

introduction of the stochastic volatilities. In this respect this is a multifactor model

with n+2 factors (state variables): Ft, ηt, σit. The factor dynamics is linear for

Ft, but nonlinear for the unobservable volatilities. We get a nonlinear state space

model (see Appendix 5.1 for the state space representation of the ARG process),

to which the standard Kalman filter does not apply. In particular, the likelihood

function corresponding to the observation of Yt = (Y1t, . . . , Ynt)′, t = 1, . . . , T , has

an integral form, since the unobservable factor paths have to be integrated out. This

likelihood involves an integral of a huge dimension equal to (n+2)T , which increases

with the number T of observation dates. To avoid the numerical optimization of

the complicated likelihood function, we consider below a simple two-step estimation

approach.

3.1 The Estimation Approach

We first consider an estimation approach of both the parameter and factor values,

which would be close to consistency if both n and T were large [see Gagliardini and

Gourieroux (2014) for the so-called granularity theory]. However, in our framework,

the number of stocks is fixed and the approach is not consistent. In a second step,

this method is adjusted for asymptotic bias by indirect inference, since model (3.1)

is easy to simulate.

3.1.1 Auxiliary Method of Moments Estimation

Our first estimation of the parameter and factor values is based on moment restric-

tions.

10

(i) Estimation of α

The vector α = (α1, . . . , αn)′ can be estimated by the first moment of observa-

tions. We have:

E(Yt) = α ,

which leads to the method of moments estimator:

α = Y ,

where Y = 1T

∑Tt=1 Yt.

(ii) Estimation of Ft

Denote the demeaned row vector by Zt = Yt−α. Denote also Z·t = n−1∑n

i=1 Zit

and its standardized version by:

Ft = Z·t/

√√√√T−1

T∑t=1

Z2·t .

(iii) Estimation of β and γ

We then estimate β by:

βi =1

T

T∑t=1

ZitFt ,

and parameter γ by:

γ =1

T − 1

T∑t=2

FtFt−1 .

11

(iv) Estimation of the parameters characterizing the dynamics of ηt

We estimate ηtut by ηtut = Ft − γFt−1. Since

E[(ηtut)4] = 3(

1

δ+ 1)(1− γ2)2 ,

and

E[(ηtut)2(ηt−1ut−1)

2] = (ρ

δ+ 1)(1− γ2)2 ,

ρ and δ can be estimated by their associated sample counterparts:

δ =

(T − 1)−1

T∑t=2

ηtut4/[3(1− γ2)2]− 1

−1

,

ρ = δ

((T − 2)−1

T∑t=3

ηtut2 ηt−1ut−1

2/[(1− γ2)2]− 1

).

(v) Estimation of the parameters characterizing the dynamics of σit

A natural estimator of σitϵit is:

σitϵit = Zit − βiFt .

Since

E[n∑

i=1

σ2itϵ

2it] = nA ,

E[n∑

i=1

σ4itϵ

4it] = 3nA2(1 + δ−1) ,

E[n∑

i=1

(σitϵit)2(σi,t−1ϵi,t−1)

2] = nA2(1 + ρ/δ) ,

12

with A = cδ/(1− ρ), the ARG parameters can be estimated by:

ˆδ =

T−1

∑Tt=1

∑ni=1 σitϵit

4

3nA2− 1

−1

,

ˆρ = ˆδ

[(T − 1)−1

∑Tt=2

∑ni=1 σitϵit

2 σi,t−1ϵi,t−12

nA2− 1

],

ˆc = (1− ˆρ)A/ˆδ ,

with A = n−1∑n

i=1

∑Tt=1 σitϵit

2.

The approach above is computationally simple and easy to interpret, since all estima-

tors have closed-form expressions. However, as mentioned above, this method is not

consistent, due to the approximate filtered value Ft, which differs from Ft for fixed

n. This explains why the results of this estimation approach have to be adjusted to

eliminate the asymptotic bias. Since the nonlinear state-space model (3.1) is easy to

simulate, this adjustment can be done by indirect inference.

3.1.2 Indirect inference estimation

Let us now describe the indirect inference adjustment and denote the vector of struc-

tural parameters by:

θ = (αini=1, βini=1, γ, δ, ρ, δ, ρ, c)′ .

Denote also the empirical dataset by Y1:T = Yiti=1,...,n, t=1,...,T and the associated set

of auxiliary statistics, non consistent moment estimators of the first step approach

given in 3.1.1, by:

µ = (α, β, γ, 1/δ, ρ/δ, 1/ˆδ, ˆρ/ˆδ, A)′ .

13

The indirect inference adjustment is based on a comparison of the auxiliary statistics

computed from the data and those computed using simulated data generated from the

structural model (3.1). More precisely, let us consider independent simulated pseudo-

data samples: Y(s)1:T (θ) = Y (s)

t (θ)Tt=1, s = 1, . . . , S, satisfying the data-generating

process (3.1), where S is the number of replications. The auxiliary estimator based

on simulated data is defined by:

µS(θ) = S−1

S∑s=1

µ[Y(s)1:T (θ)] .

The indirect inference (II) estimator of θ is defined as:

θII = argminθ[µ− µS(θ)]

′Ω[µ− µS(θ)] ,

where Ω is a symmetric, positive-definite weighting matrix. Since we use a just-

identified auxiliary estimator, the II estimator does not depend on Ω and Ω can

be conveniently replaced by the identity matrix. This two-step estimator θII is

consistent of θ.

Hereafter, in all our empirical and Monte Carlo II estimations, we use S = 10

pseudo-data samples.

3.2 Monte Carlo results

Let us illustrate the properties of the first step method of moment (MM) estimation

and of the II estimation by Monte Carlo study. We consider n = 10 stocks and a

sample size T = 3, 853 like in our empirical dataset. The true parameters are set to

the empirical estimates obtained in the following subsection and reported in Table 2,

second column.

14

We generate independently 100 datasets and for each of them we compute the

MM estimate and the II estimate. We provide in Figure 3 the boxplots corresponding

to the finite sample (T = 3, 853) properties of both estimates. The true values of

the parameters are set to the empirical estimates (see later in the second column of

Table 2) and are reported with continuous lines. We only display α1 and β1 among

the αs and βs.

Let us first consider the MM estimates. We see that the boxes do not necessarily

include the true values of the parameters, as a consequence of the nonconsistency.

This arises for parameters characterizing the volatility dynamics, especially the δ and

δ parameters. When the estimates are adjusted by indirect inference, we observe that

the boxes now all include the true parameter values.

3.3 Empirical Results

Let us now apply the estimation approach to the real dataset. Table 2 reports

auxiliary MM and II estimate. We observe that the estimated values are rather

stable with respect to the number S of replications. The estimated betas can be

directly compared with the estimated betas derived in the static analysis of Section 2.

Note that in Section 2, the submarket portfolio has not been standardized. Since

the standard error of the return of the submarket portfolio is equal to 0.022, after

standardization these betas are provided in the last column of Table 2 . We see

that the betas estimated from the static model, the auxiliary moment method and

the indirect inference estimates are rather close to each other. Thus, the interest of

the approach is essentially in the parameters characterizing the dynamics of factor

and volatilities. These parameters are required for the prediction of future rates and

in particular for the computation of the term structure of the Value-at-Risk and

15

Aux II−0.

0010

0.00

000.

0010

α 1

Aux II

0.02

00.

022

0.02

40.

026

β 1

Aux II

−0.

10−

0.05

0.00

0.05

γ

Aux II

0.05

0.10

0.15

0.20

0.25

δAux II

0.4

0.6

0.8

1.0

ρ

Aux II

0.04

0.06

0.08

0.10

δ~

Aux II

0.2

0.4

0.6

0.8

1.0

ρ~

Aux II0.

000

0.00

10.

002

0.00

30.

004

c~

Figure 3: Method of Moments and Indirect Inference Estimates. This figure illus-trates 100 MM and corresponding II estimates for n = 10 and sample size T = 3, 853as in the empirical dataset. The true parameters are set to the empirical estimatesand are reported with continuous lines.

and their sensitivities with respect to shocks on either the systematic, or specific

standardized innovations.

The estimated γ is small and negative. It has to be compared with the autore-

gressive coefficient corresponding to the return of the submarket portfolio derived

by the static approach. This coefficient is -0.053, thus has the same order as the II

16

estimates of γ.3

We observe a strong persistence, that is large ρ coefficients, for both systematic

and specific volatilities. The estimated δ and δ coefficients provide information on

the behaviour of the (marginal and conditional) distribution of volatilities in the tail

and in the neighborhood of volatility zero.

Using the II parameter estimates, we simulate series of the same size as the

original dataset. The related sample statistics are reported in Table 3.

The comparison of Tables 1 and 3 shows a reasonable goodness of fit for the

different characteristics of historical distribution, including the measures of state

dependence between returns, and of their dynamic features by means of first-order

autocorrelations of returns and squared returns.

3.4 Imputation of the hidden states (factors)

Using the II parameter estimates, let us now turn to the imputation of the hidden

states x1:T = (x1, . . . , xT ), where xt = (Ft, σitni=1, ηt), on the in-sample period April

6, 2000 and July 31, 2015.

3.4.1 Filtering

To estimate the distribution of xt|Y1:t at a given date t, we use an Approximate

Bayesian Computation (ABC) filter4 (Calvet and Czellar, 2011, 2015; Jasra et al.,

2012) with optimal kernel and bandwidth choices given in Calvet and Czellar (2015).5

3The autoregressive coefficient for the return of the S&P 500 is -0.084.4Calvet and Czellar (2011) called it State-Observation Sampling (SOS) filter.5A bootstrap particle filter (Gordon, Salmond and Smith, 1993) is theoretically applicable.

However, since the observation density f(Yt|xt) in our model is a n-variate Gaussian with largen, the bootstrap filter encounters numerical weight degeneracy problems whenever an outlier inthe return process is observed. In addition, in the structural dynamic factor model of Section 4.7,f(Yt|xt) will not be available anymore and a standard particle filtering will be inapplicable.

17

Table 2: Empirical estimates

AuxNo optionof default

With optionof default

Staticmodel

αMET 0.000395 0.000362 0.000606αING -0.000032 0.000059 0.000198αGS 0.000232 0.000200 0.000596αLNC 0.000227 0.000118 0.000358αHSBC 0.000111 0.000163 -0.000122αJPM 0.000164 0.000074 -0.000212αBAC 0.000005 -0.000047 0.000440αCS -0.000028 0.000047 0.000159αWFC 0.000366 0.000372 0.000694αBCS 0.000043 -0.000053 -0.000950βMET 0.021806∗ 0.021840∗ 0.026920 0.021348βING 0.025872∗ 0.026084∗ 0.034525 0.025329βGS 0.018702∗ 0.018239∗ 0.020364 0.018309βLNC 0.028012∗ 0.028496∗ 0.035498 0.027424βHSBC 0.013338∗ 0.012607∗ 0.016979 0.013058βJPM 0.022187∗ 0.022368∗ 0.036311 0.021721βBAC 0.026229∗ 0.026669∗ 0.034107 0.025679βCS 0.020910∗ 0.020599∗ 0.026767 0.020471βWFC 0.021002∗ 0.020969∗ 0.023378 0.020561βBCS 0.026659∗ 0.026857∗ 0.050174 0.026100γ -0.053297 -0.044679 -0.054902δ 0.162371∗ 0.129703∗ 0.161184ρ 0.787698∗ 0.742651∗ 0.869338

δ 0.077740∗ 0.064702∗ 0.077236ρ 0.815843∗ 0.842556∗ 0.856746c 0.000687 0.000792 0.000786ω 1.861301

Empirical Estimates for daily logreturns between April 6, 2000, and July 31,2015, a sample size of 3,853. Each reported II estimate is the global minimum ofthe II objective function among 1,000 local minimizations with starting valueschosen at random. In the Aux and No option of default columns, numbers withan asterix indicate significant parameters at the 5% level, where significanceis measured by means of robust standard errors IQR/1.349 where IQR is theinterquartile range over 100 Monte Carlo estimates.

18

Table 3: Sample statistics of simulated series

Sample moments

MET ING GS LNC HSBC JPM BAC CS WFC BCS

Mean 0.00070 0.00037 0.00105 0.00029 0.00039 0.00044 -8·10−6 -2·10−5 0.00056 0.00030St.dev. 0.02653 0.02931 0.02688 0.03260 0.01967 0.02718 0.03115 0.02680 0.02648 0.03060Skewn. -0.37902 -0.65573 -0.04512 -0.12469 -0.22193 -0.37643 -0.76003 -0.75318 -0.79803 -0.81506Kurt. 14.18529 14.94072 21.18191 17.27276 15.01790 15.93163 15.70523 12.95755 18.91468 18.59897Min. -0.22352 -0.27242 -0.24653 -0.29785 -0.16614 -0.25429 -0.27710 -0.21414 -0.30902 -0.34973Max. 0.16933 0.20106 0.32663 0.30655 0.16804 0.22008 0.20753 0.18743 0.25635 0.22679AC(1) -0.09970 -0.07468 -0.03627 -0.06953 -0.07767 -0.06166 -0.06460 -0.06251 -0.01950 -0.05747Sq. AC(1) 0.23862 0.25440 0.20127 0.25253 0.32141 0.26033 0.27648 0.32238 0.22400 0.27619

Covariance matrix

MET ING GS LNC HSBC JPM BAC CS WFC BCS

MET 0.00070 0.00053 0.00037 0.00059 0.00026 0.00046 0.00055 0.00042 0.00042 0.00054ING 0.00053 0.00089 0.00044 0.00070 0.00032 0.00056 0.00067 0.00050 0.00051 0.00065GS 0.00037 0.00044 0.00072 0.00049 0.00022 0.00038 0.00045 0.00035 0.00035 0.00046LNC 0.00059 0.00070 0.00049 0.00106 0.00034 0.00062 0.00074 0.00055 0.00056 0.00072HSBC 0.00026 0.00032 0.00022 0.00034 0.00039 0.00027 0.00032 0.00024 0.00025 0.00032JPM 0.00046 0.00056 0.00038 0.00062 0.00027 0.00074 0.00057 0.00043 0.00044 0.00056BAC 0.00055 0.00067 0.00045 0.00074 0.00032 0.00057 0.00097 0.00051 0.00052 0.00067CS 0.00042 0.00050 0.00035 0.00055 0.00024 0.00043 0.00051 0.00072 0.00039 0.00051WFC 0.00042 0.00051 0.00035 0.00056 0.00025 0.00044 0.00052 0.00039 0.00070 0.00052BCS 0.00054 0.00065 0.00046 0.00072 0.00032 0.00056 0.00067 0.00051 0.00052 0.00094

Eigenvalues

Eigenv. 0.00523 0.00041 0.00033 0.00030 0.00028 0.00028 0.00027 0.00026 0.00024 0.00022

Regression on mean logreturns

MET ING GS LNC HSBC JPM BAC CS WFC BCS

Alpha 0.00031 -0.00009 0.00071 -0.00022 0.00015 0.00004 -0.00049 -0.00040 0.00018 -0.00017Beta 0.96396 1.14046 0.84320 1.26499 0.58183 0.99771 1.18975 0.92071 0.92748 1.16992

Sample statistics of the simulated series using empirical estimates.

19

The idea of ABC filtering is to replace in Step 2 of the filtering algorithm the un-

available conditional distribution f(Yt|xt) by the distance of simulated observations

Y (i)t Ni=1 to the empirical observation Yt. The distance is measured by a strictly pos-

itive kernel K : Rdim y → R integrating to unity, where dim y denotes the dimension

of y. For any bandwidth ht > 0, define Kht(y) = K(

yht

)/hdim y

t . The ABC filtering

algorithm is as follows.

Step 1 (Initialization): At date t = 0, simulate x(i)0 , i = 1, . . . , N , from

the initial density f(x0).

For t = 1, . . . , T , iterate Steps 2-4.

Step 2 (Sampling): Simulate a state-observation pair (x(i)t , Y

(i)t ) from

f(xt, Yt|x(i)t−1, Y1:t−1), i = 1, . . . , N .

Step 3 (Importance weights): Observe Yt and compute the weights

ω(i)t =

1

hdim yt

K

(Y

(i)t − Yt

ht

), i = 1, . . . , N.

Step 4 (Multinomial resampling): Draw x(1)t , . . . , x

(N)t from x

(1)t , . . . , x

(N)t

with probabilitiesω(1)t∑i ω

(i)t

, . . . ,ω(N)t∑i ω

(i)t

.

ABCFiltering Algorithm

We use the quasi-Cauchy kernel K and plug-in bandwidth ht (Calvet and Czellar,

2015):

K(u) = (1 + c u⊤u)−(dimu+3)/2 and h∗t (N) =

[c2B(K) dimu

N Pt

]1/(dimu+4)

, (3.2)

where dimu is the dimension of u, c = π1+1/dimu/2Γ[(dimu+3)/2]2/dimu, B(K) =

20

2 Γ(dim u/2+3) Γ[(dim u+3)/2]/[√πΓ(dimu+3)], Γ(·) is the gamma function, and

Pt =2 tr(Σ−2

t ) + [tr(Σ−1t )]2

2dimu+2 πdimu/2 [det(Σt)]1/2, (3.3)

where Σt is the sample covariance matrix calculated with the simulated Y (i)t i=1,...,N

in Step 2 of the ABC filter.

The empirical distribution of Step 2 particles x(i)t Ni=1 finitely estimates the dis-

tribution f(xt|Y1:t−1) and the empirical distribution of Y (i)t Ni=1 estimates the dis-

tribution f(Yt|Y1:t−1), which can be used for forecasting purposes. Moreover, the

empirical distribution of Step 4 particles x(i)t Ni=1 finitely estimates the distribution

f(xt|Y1:t).

3.4.2 Smoothing

To impute the distribution of x1:T using observations Y1:T , we use a particle smooth-

ing method. If the transition density f(xt|xt−1) were available in closed form, we

could use a standard particle smoothing algorithm (Godsill et al., 2004) as given

below.

21

Step 1 (Particle filtering): Use a particle filter to obtain an approximate

particle representation of f(xt|Y1:t) at each date t = 1, . . . , T . Denote

these particles by x(i)t i=1,...,N

t=1,...,T .

For m = 1, . . . ,M , replicate Steps 2-4.

Step 2 (Positioning of the backward simulation): Choose x(m)T = x

(i)T

with probability 1/N .

Step 3 (Backward simulation): For t = T−1, . . . , 1 and each i = 1, . . . , N

(i) compute the importance weights

ω(i,m)t|t+1 = f(x

(m)t+1|x

(i)t ), i = 1, . . . , N ;

(ii) choose x(m)t = x

(i)t with probability ω

(i,m)t|t+1.

Step 4 (Path drawing): x(m)1:T = (x

(m)1 , . . . , x

(m)T ) is an approximate real-

ization from f(x1:T |Y1:T ).

Godsill et al. (2004)’s Smoothing Algorithm

In our model defined in Section 3, this transition density is not available and

a standard smoothing method is inapplicable. We therefore construct a variant of

Godsill et al. (2004)’s smoothing algorithm which is applicable in models in which

the transition kernel is intractable, but can be easily simulated from.

Godsill et al. (2004)’s algorithm is based on Bayes’ rule and on the assumption

that f(xt+1|xt) is available in closed-form:

f(xt|xt+1, Y1:T ) =f(xt|Y1:T )f(xt+1|xt) .

f(xt+1|Y1:t). (3.4)

Formula (3.4) suggests that at each date t, we need a filter x(i)t i=1,...,N estimating

22

f(xt|Y1:T ). This is provided in Step 1 of the smoothing algorithm. The numerator in

formula (3.4) then suggests that given a date t+1 state xt+1 and observations Y1:T , we

can impute the hidden states xt in a backward manner by reweighting the particles

by f(xt+1|x(i)t ). This backward reweighting procedure is summarized in Steps 2-4 in

Godsill’s algorithm.

However, in our model, f(xt+1|xt) is not available in closed form, but we can con-

veniently simulate from it. We therefore consider the joint distribution of (xt+1, xt)

where xt+1 is a pseudo-particle generated from f(xt+1|xt):

f(xt+1, xt|xt+1, Y1:t) =δ(xt+1 − xt+1)f(xt+1, xt|Y1:t)

f(xt+1|Y1:t), (3.5)

where δ denotes de Dirac distribution on Rdimx.

This suggests a variant of Godsill et al. (2004)’s algorithm in which the weights

ω(i)t|t+1 should be replaced by δ(x

(i)t+1 − xt+1) and pseudo-particles x

(i)t+1 are generated

from f(xt+1|x(i)t ). However, the Dirac function gives degenerate weights. Therefore,

we replace it by the positive kernel defined in (3.2)6. The new smoothing algorithm,

called Approximate Bayesian Computation (ABC) smoothing, is as follows.

6The quasi-Cauchy kernel with plug-in bandwidth satisfies an optimality property given in Calvetand Czellar (2015). The optimality property is likely not to be satisfied in the smoothing context.

23

Step 1 (Particle filtering): Use a particle filter to obtain an approximate

particle representation of f(xt|Y1:t) at each date t = 1, . . . , T . Denote

these particles by x(i)t i=1,...,N

t=1,...,T .

For m = 1, . . . ,M , replicate Steps 2-4.

Step 2 (Positioning of the backward simulation): Choose x(m)T = x

(i)T

with probability 1/N .

Step 3 (Backward simulation): For t = T−1, . . . , 1 and each i = 1, . . . , N

(i) generate a pseudo-particle x(i,m)t+1 from f(xt+1|x(i)

t );

(ii) compute the importance weights:

ω(i,m)t|t+1 =

Kht

(x(m)t+1 − x

(i,m)t+1

)∑Ni′=1Kht

(x(m)t+1 − x

(i′,m)t+1

) , i ∈ 1, . . . , N ;

(iii) choose x(m)t = x

(i)t with probability ω

(i,m)t|t+1.

Step 4 (Path drawing): x(m)1:T = (x

(m)1 , . . . , x

(m)T ) is an approximate real-

ization from f(x1:T |Y1:T ).

ABCSmoothing Algorithm

In Step 1 of the ABC smoothing algorithm, we apply an ABC filter to generate

particles x(i)t i=1,...,N

t=1,...,T . In Step 3, we use the kernel and bandwidth defined in (3.2),

where we naturally replace Σt by the sample covariance matrix calculated with the

simulated x(i)t i=1,...,N in Step 3 of the ABC smoothing algorithm.

We useN = 10, 000 particles in both ABC filtering and smoothing algorithms and

generate M = 100 paths (F(m)t , σitni=1, ηt, t = 1, . . . , T ), m = 1, . . . ,M in the ABC

smoothing algorithm. In Figures 4-7 we report the smoothed 90% confidence bands

for Ft, whose bounds are the 5th and 95th percentiles of the sample distribution of

24

Table 4: Goodness-of-fit measure of thelinear factor

Static model Dynamic modelMET 0.62513 0.25282ING 0.64071 0.25170GS 0.58649 0.22973LNC 0.62914 0.25735HSBC 0.58584 0.22771JPM 0.71357 0.26583BAC 0.70451 0.26740CS 0.60075 0.24063WFC 0.69037 0.25688BCS 0.62410 0.24433

the F(m)t , m = 1, . . . ,M .

In Figure 8 we report the smoothed 90% confidence bands for the various σ2it.

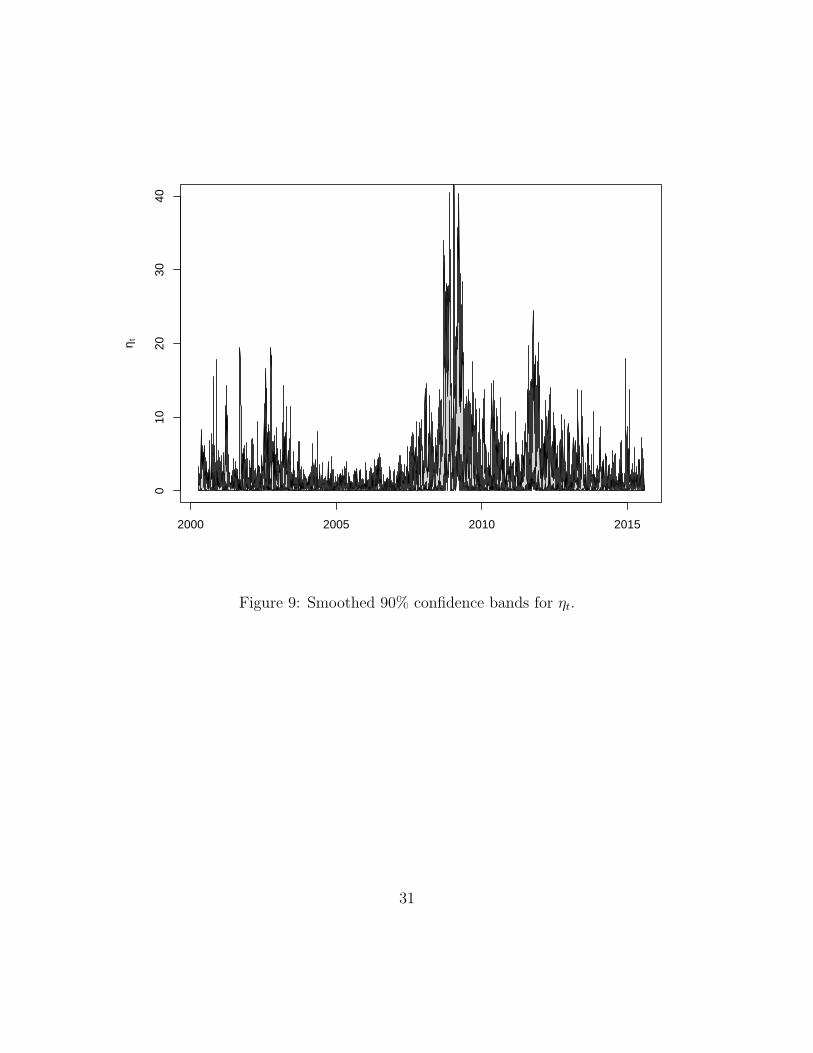

Finally, in Figure 9 we report the smoothed 90% confidence bands for ηt.

Table 4 reports the goodness-of-fit measure of the linear factor Ft:

R2i =

∑Tt=1(βi Ft)

2∑Tt=1(βi Ft)2 + (σit ϵt)2

,

where βi Ft in the numerator is replaced by βi times the median of the smoothed

F (m)t Mm=1 and σit ϵt is replaced by the median of Yit − αi − βi F

m)t Mm=1. We report

these measures in the second column of Table 4. As a matter of comparison, we

measure the same proportions when using a static factor model and calculate the

R2s associated with regressions of the returns on the submarket portfolio. We report

these R2 measures in the first column of Table 4.

25

May Jul Sep Nov Jan

−2

02

2000

Jan Mar May Jul Sep Nov

−3

−1

1

2001

Nov Jan Mar May Jul

−2

02

2001

/02

Sep Nov Jan Mar May

−2

02

2002

/03

May Jul Sep Nov Jan

−1.

50.

01.

5

2003

/04

Figure 4: Smoothed Ft for the period between April 6, 2000 and February 10, 2004.Smoothed 0.05th and 0.95th quantiles of the cumulated factor Ft are reported withblack lines and median Ft is reported in red.

3.4.3 In-sample forecasts

Let us now investigate the accuracy of the VaR forecasts on the in-sample pe-

riod April 6, 2000 and July 31, 2015. Using the ABC particle filter with N =

26

Mar May Jul Sep Nov

−1.

50.

0

2004

Jan Mar May Jul Sep

−0.

50.

5

2004

/05

Sep Nov Jan Mar May

−1.

00.

01.

0

2005

/06

Jul Sep Nov Jan Mar

−1.

50.

01.

5

2006

Mar May Jul Sep Nov

−2

02

2006

/07

Figure 5: Smoothed Ft for the period between February 11, 2004 and December 10,2007. Smoothed 0.05th and 0.95th quantiles of Ft are reported with black lines andmedian Ft is reported in red.

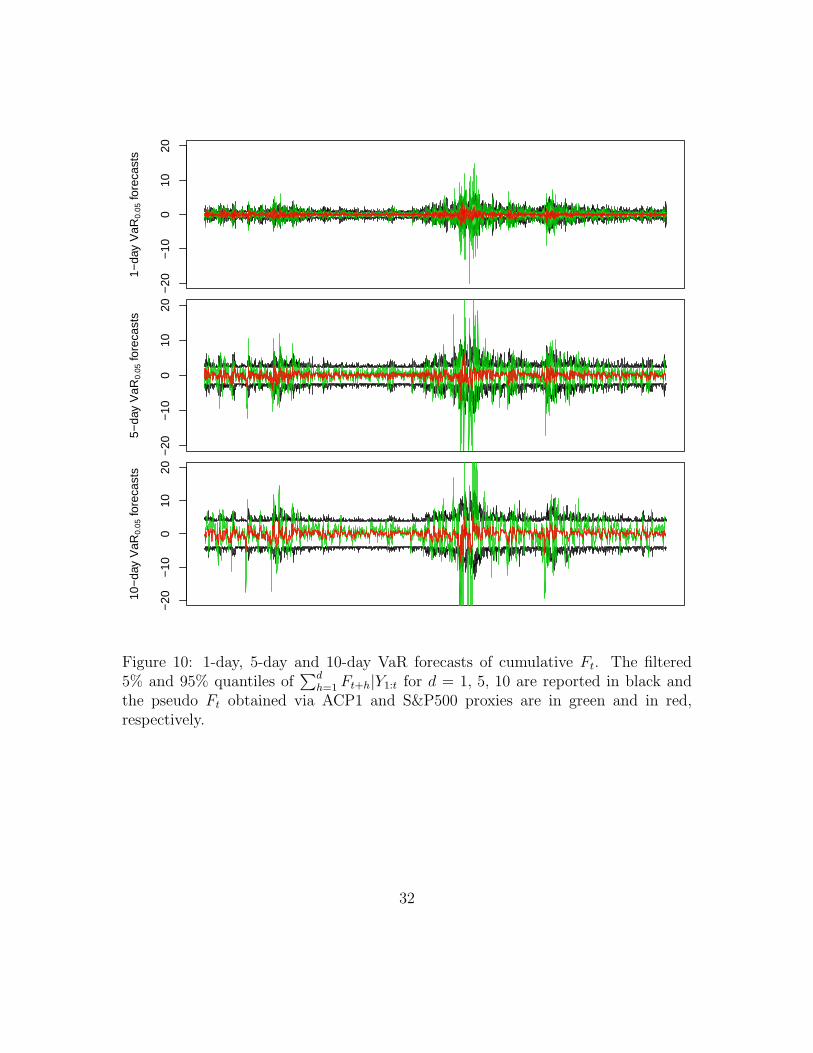

10, 000 we first forecast the 0.05th and 0.95th quantiles of∑d

h=1 Ft+h|Y1:t for d =

1, 5, 10, 20, 40, 60 (1-day, 5-day, 10-day, 20-day, 40-day and 60-day horizons) that

are the VaR for the systematic risk component. Figures 10-11 report the VaR fore-

casts of cumulative Ft along with the pseudo values of Ft obtained via ACP1 and

27

Jan Mar May Jul Sep

−4

04

2007

/08

Nov Jan Mar May Jul

−10

0

2008

/09

Jul Sep Nov Jan Mar

−3

02

2009

May Jul Sep Nov Jan

−3

02

4

2009

/10

Jan Mar May Jul Sep

−6

−2

2

2010

/11

Figure 6: Smoothed Ft for the period between December 11, 2007 and October 7,2011. Smoothed 0.05th and 0.95th quantiles of Ft are reported with black lines andmedian Ft is reported in red.

S&P500 proxies, defined as

• ACP1 proxy: FACP1t =

∑ni=1 aiYit√

T−1∑T

t=1(∑n

i=1 aiYit)2, where (a1, . . . , an) is the eigen-

vector associated with the largest eigenvalue of the covariance matrix of Yit;

28

Nov Jan Mar May Jul

−4

04

2011

/12

Sep Nov Jan Mar May

−3

−1

1

2012

/13

May Jul Sep Nov Jan

−2

01

2

2013

/14

Mar May Jul Sep Nov

−1.

50.

0

2014

Nov Jan Mar May Jul

−1.

50.

01.

5

2014

/15

Figure 7: Smoothed Ft for the period between October 10, 2011 and July 30, 2015.Smoothed 0.05th and 0.95th quantiles of Ft are reported with black lines and medianFt is reported in red.

• S&P 500 proxy: F S&P500t =

YS&P500,t√T−1

∑Tt=1 Y

2S&P500,t

, where YS&P500,t is the return on

the S&P 500 at date t.

29

0.00

00.

020

ME

T

0.00

00.

020

ING

0.00

00.

020

GS

0.00

00.

020

LNC

2000 2005 2010 2015

0.00

00.

020

HS

BC

0.00

00.

020

JPM

0.00

00.

020

BA

C

0.00

00.

020

CS

0.00

00.

020

WF

C

2000 2005 2010 2015

0.00

00.

020

BC

S

Figure 8: Smoothed 90% confidence bands for σ2it.

30

2000 2005 2010 2015

010

2030

40

η t

Figure 9: Smoothed 90% confidence bands for ηt.

31

−20

−10

010

20

1−da

y V

aR0.

05 fo

reca

sts

−20

−10

010

20

5−da

y V

aR0.

05 fo

reca

sts

−20

−10

010

20

10−

day

VaR

0.05

fore

cast

s

Figure 10: 1-day, 5-day and 10-day VaR forecasts of cumulative Ft. The filtered5% and 95% quantiles of

∑dh=1 Ft+h|Y1:t for d = 1, 5, 10 are reported in black and

the pseudo Ft obtained via ACP1 and S&P500 proxies are in green and in red,respectively.

32

−30

−10

1030

20−

day

VaR

0.05

fore

cast

s

−30

−10

010

2030

40−

day

VaR

0.05

fore

cast

s

2000 2005 2010 2015

−30

−10

1030

60−

day

VaR

0.05

fore

cast

s

Figure 11: 20-day, 40-day and 60-day VaR forecasts of cumulative Ft. The filtered5% and 95% quantiles of

∑dh=1 Ft+h|Y1:t for d = 1, 5, 10 are reported in black and

the pseudo Ft obtained via ACP1 and S&P500 proxies are in green and in red,respectively.

33

4 Model With Default Risk

4.1 The Basic Model

4.1.1 Value of the Firm Model

The structural model or Value-of-the-Firm model has been initially introduced by

Black and Scholes (1973) and Merton (1974). This is a two-period model based on a

description of the balance sheet of the firm at the second period. Since the structural

model is now extended to a dynamic framework, we denote by (t, t + 1) the period

of interest. The balance sheet of the firm at date t + 1 is summarized by the asset

and liability values At+1, Lt+1, respectively. The value of the firm at date t + 1

for the shareholders is (At+1 − Lt+1)+ = max(At+1 − Lt+1, 0), taking into account

their limited liability. Thus the stock can be considered as a European call option

written on the underlying asset value with strike the level of liability. This explains

the pricing formula for the stock under the absence of arbitrage opportunity as:

Pt =Q

E[exp(−rt)(At+1 − Lt+1)

+ | It], (4.1)

where Pt is the capitalization (equity value) at date t, rt the riskfree rate for period

(t, t + 1), known at date t, It the information available at date t, and Q is the

pricing measure. In a discrete time framework, the market is incomplete, and there

is an infinite number of pricing measures compatible with the condition of absence

of arbitrage opportunity. Thus we have some flexibility on the choice of Q. Formula

(4.1) can be applied to the total number of shares, or be standardized per share, as

long as the number of shares is independent of time.

This basic model is structural, since it is based on an economic definition of

34

default from the balance sheet information. It involves three types of variables, that

can be either latent, or observable. These variables are:

1. the components A, L of the balance sheet. The asset component is assumed

unobservable and so is often the liability component7;

2. the state variables in the information set, known by the investors, but often

unobserved by the econometrician;

3. the equity value Pt, which is observable whenever the stock of the firm is quoted

on a liquid competitive market.

In the initial Value-of-the-Firm model, the liability is assumed predetermined. We

denote Lt|t+1 the value of Lt+1 assumed known at date t. Thus, formula (4.1) can be

equivalently written as:

Pt = exp(−rt)Lt|t+1

Q

E[(At+1/Lt|t+1 − 1)+ | It

]. (4.2)

Let us now choose the form of the pricing measure Q. We follow the basic Black-

Scholes-Merton formula. The information set includes only the values ofAt, rt, Lt|t+1,

and, between t and t + 1, under the pricing measure, the asset value satisfies the

geometric Brownian motion, with fixed known volatility ω2t , corresponding to the

standard Black-Scholes model. We deduce the following closed-form expression for

Pt as:

Pt = gBS(At, Lt|t+1, rt, ω2t ) , (4.3)

7When A and L are latent, we do not have to be more precise on the way they are defined.Typically, the asset component is marked-to-market, whereas the debt is generally book valued.Similarly, the debts can have different maturities. The L component has to be interpreted as thepart of the debt to be reimbursed at date t + 1. Similarly, A may be the part of assets liquid atdate t+ 1.

35

where:

gBS(At, Lt|t+1, rt, ω2t ) = AtΦ(d1,t)− LtΦ(d2,t) exp(−rt) , (4.4)

with

• d1,t =1ωt

log(

At

Lt|t+1

)+ rt +

ω2t

2

;

• d2,t = d1,t − ω2t .

In the modelling above, it is important to distinguish two time frequencies. The

discrete dates t = 1, 2, . . . are the times at which the debt is due. They define the

maturity date of the call option. The underlying continuous time model concerns

the evolution of prices and values within the period and is just introduced to get the

link with the Black-Scholes formula.

4.1.2 The Effects of Levels

The above Merton’s formula (4.3)-(4.4) will be used in a simplified way following

common practices. We set the short term rate rt = 0, assume that the intraperiod

volatility ωt = ω is constant to focus later on on the intraperiod volatilities and fix

a constant level of liability Lt|t+1 = L. Thus we get:

logPt = logL+ log

At

LΦ

[1

ωlog

(At

L

)+

ω

2

]− Φ

[1

ωlog

(At

L

)− ω

2

]≡ logL+ h

[log

(At

L− 1

);ω

],

say, and the associated stock return becomes:

Yt = log(Pt/Pt−1) = h

[log

(At

L− 1

);ω

]− h

[log

(At−1

L− 1

);ω

]. (4.5)

36

(i) Let us consider the extreme case where the asset/liability ratio is large and the

intraperiod volatility is small. In such a case, the firm is far from default and

it is easily checked that we have:

logPt ∼ logL+ log(At/L− 1) ,

and

Yt ∼ log(At/L− 1)− log(At−1/L− 1) ≡ ∆ log(At/L− 1) . (4.6)

Therefore, the relative change in firm value is equal to the relative change in

At/L−1. In particular, if these latter changes are stationary, the stock returns

are also stationary.

(ii) However, in the general case, formula (4.5) shows that the stock return depends

not only on the changes ∆ log(At/L − 1), but also on the leverage At−1/L −

1, and this leverage effect will increase with the proximity to default. As a

consequence, if the changes ∆ log(At/L − 1) are stationary, the stock returns

will become nonstationary. This nonstationary feature has to be taken into

account in the analysis.

In our application, this leverage effect can be significant, while staying limited,

since we consider financial institutions, which have not experimented default

during all the period, and thus are still at some distance to default.

37

4.2 The Structural Dynamic Factor Model (SDFM)

The effect of the distance-to-default8 will be taken into account by modifying the

linear factor model (3.1) as follows:

The State Equation

An analogue of model (3.1) will be written on the changes ait = ∆ log(Ait/L − 1)

instead of being written on the stock returns:ait = αi + βiFt + σitϵit , i = 1, . . . , n ,

Ft = γFt−1 + ηtut ,

(4.7)

with the same dynamic assumptions as in (3.1). Compared to (3.1), this dynamic

model includes new state variables that are the ait. As usual, it will be interesting

to try to reconstitute these variables, that are the implied financial leverages, from

the stock return data only.

The Measurement Equations

They are given by:

Yit = h [log (Ait/L− 1) ;ωi]− h [log (Ai,t−1/L− 1) ;ωi] , i = 1, . . . , n . (4.8)

The model includes additional parameters, that are the intraperiod volatilities ωi

appearing in the measurement equations. It is known from the theoretical model

that such a parameter ωi can be difficult to identify if the firm is very far from

default [see equation (4.6), where the effect of ωi disappears]. For this reason, we

8We use distance-to-default in its general meaning and not with the specific definition by KMV[see Crosbie and Bohn (2004)].

38

assume ωi = ω, independent of the firm, in the illustration below.

Note also that the measurement equations involve the levels log(Ait/L−1), which

will have to be reconstructed from the changes ait. This demands the introduction

of initial conditions on log(Ait/L− 1). Since the institutions under analysis are not

on default during the considered period, we can select initial values sufficiently high

to avoid default at the initial date. The results are weakly dependent on this initial

choice, which corresponds to the extreme situation of stationarity.

Finally, as noted above, the discrete time dynamic model (4.7) for the asset liabil-

ity ratios, written under the historical distribution is compatible with the Merton’s

pricing equations derived under the risk-neutral distribution. Indeed, a discrete time

framework implies an incomplete market framework, that is an infinity of discrete

time risk-neutral distribution compatible with a given historical distribution. In our

framework the risk-neutral log-normal distribution for ait given ai,t−1 is compati-

ble with the historical distribution for ait given ai,t−1 by choosing the appropriate

stochastic discount factor. Since the riskfree interest rate is set to zero, the stochastic

discount factor is just the ratio of the risk-neutral and historical transition densities.

Finally, in our specification, the investors have the information on the balance sheets

ait and on the intraperiod volatility (not only on the returns), but they do not have

the information on the underlying factors Ft, σit, ηt. In contrast, the econometrician

has only the information on the stock returns.

4.3 Comparison with the Literature

A dynamic structural model has recently been introduced in Engle and Siriwardane

(2015). Their full recursive model is deduced from expansions of the risk-neutral

dynamics and structural pricing formulas underlying a stochastic volatility model

39

written on the process of asset value. This expansion provides a simplified dynamics

for the equity returns, but its validity can be questioned, when distance-to-default

is small and nonlinear effects potentially important. For instance, the expansion

neglects the effect of time-to-maturity, the effect of the drift and of the volatility

shocks to focus on the link between equity and asset volatilities. Moreover, the

expansion is performed in continuous time, and the impact of this expansion for

discrete time data, that is the time aggregation effect, is not really taken into account.

Another difference compared to our model is the ARCH specification introduced for

the estimated econometric model, which is not in line with the underlying structural

model, where the volatilities were stochastic with their own shocks. Finally, the set

of observable variables is not the same, since the authors assumed observable by the

econometrician both the equity and asset values, whereas we preferred to assume

observable the equity values only. This is more in line with the Moody’s-KMV

practice. Moreover, our approach solves the question of the different frequencies in

which these data are available and avoid the use of proxies for the monthly asset

values9.

4.4 Estimation Results

As mentioned above, for identification reasons, we assume that ωi = ω are constant

for all i = 1, . . . , n10. We follow an approach similar to the approach in Section 3.1.

We first consider a set of moment restrictions to calibrate the parameters and the

underlying factors. This step can lead to inconsistent estimators. This lack of con-

sistency is adjusted for by indirect inference in the second step. In the first step, in

9In Engle and Siriwardane (2015) the monthly book value of the debt is obtained by an automaticexponential average with smoothing parameter of 0.01

10We have checked that the objective function of the estimation problem was poorly informativeon the individual heterogeneity of the intraperiod volatilities.

40

addition to our (2n + 6) auxiliary statistics in µ of Section 3.1.2, we need an addi-

tional statistic to identify ω. For this purpose, we use the mean standard deviation

of individual returns:

ω =1

n

n∑i=1

√√√√ 1

T − 1

T∑t=1

(exp(Yit)− exp(Yi)

)2. (4.9)

Clearly, this auxiliary moment ω will not be a consistent estimator of ω. Indeed, ω

has the interpretation of an interperiod volatility averaged on the banks and differ

from the intraperiod volatility. However, this lack of consistency will be solved by

indirect inference. Thus, we use the augmented auxiliary vector µOD = (µ′, ω)′ and

estimate the structural parameter θOD = (θ′, ω)′ by indirect inference as described

in Section 3.1.2.

The estimation results are reported in Table 2, column 4. From this table we can

compare the estimates for the models with and without option of default. The esti-

mates of the beta coefficients are significantly different for Barclays and JP Morgan.

We also observe more persistence in the stochastic volatility ηt and a value of the

intraperiod volatility indicates the need to adjust for the option of default.

To complete the comparison between the naive and structural models, we report

in Figures 12-15 the smoothed Ft values obtained via the SDFM model and in Fig-

ure 16 the smoothed median Ft via SDFM plotted against the smoothed median Ft

via the naive dynamic model.

Then, the estimated model can be used:

(i) to get the smoothed values of the state variables ait, i = 1, . . . , n, t = 1, . . . , T ;

(ii) then deduce the smoothed values of the asset/liability ratios Ait/L, i = 1, . . . , n,

t = 1, . . . , T , that are the implied financial leverages;

41

May Jul Sep Nov Jan

−2

02

2000

Jan Mar May Jul Sep Nov

−3

−1

1

2001

Nov Jan Mar May Jul

−2

02

2001

/02

Sep Nov Jan Mar May

−2

02

2002

/03

May Jul Sep Nov Jan

−1.

50.

01.

5

2003

/04

Figure 12: Smoothed Ft for the period between April 6, 2000 and February 10, 2004.Smoothed 0.05th and 0.95th quantiles of Ft are reported with black lines and medianFt is reported in red.

(iii) then we can deduce measures of distance-to-default for the different banks and

analyze how they evolved over time. Such measures are:

42

Mar May Jul Sep Nov

−1.

50.

01.

0

2004

Jan Mar May Jul Sep

−0.

60.

00.

6

2004

/05

Sep Nov Jan Mar May

−1.

00.

01.

0

2005

/06

Jul Sep Nov Jan Mar

−1.

50.

01.

5

2006

Mar May Jul Sep Nov

−2

02

2006

/07

Figure 13: Smoothed Ft for the period between February 11, 2004 and December 10,2007. Smoothed 0.05th and 0.95th quantiles of Ft are reported with black lines andmedian Ft is reported in red.

the excess asset liability ratio:

ALit = Ait/L− 1 , (4.10)

43

Jan Mar May Jul Sep

−4

02

4

2007

/08

Nov Jan Mar May Jul

−10

05

2008

/09

Jul Sep Nov Jan Mar

−3

−1

13

2009

May Jul Sep Nov Jan

−3

02

4

2009

/10

Jan Mar May Jul Sep

−4

02

2010

/11

Figure 14: Smoothed Ft for the period between December 11, 2007 and October 7,2011. Smoothed 0.05th and 0.95th quantiles of Ft are reported with black lines andmedian Ft is reported in red.

and the risk premia of the insurance against default:

DDit = hi[log(Ait/L− 1); ω]− log(Ait/L− 1) , (4.11)

44

Nov Jan Mar May Jul

−4

02

4

2011

/12

Sep Nov Jan Mar May

−3

−1

1

2012

/13

May Jul Sep Nov Jan

−2

01

2

2013

/14

Mar May Jul Sep Nov

−1.

50.

01.

0

2014

Nov Jan Mar May Jul

−1.

50.

01.

5

2014

/15

Figure 15: Smoothed Ft for the period between October 10, 2011 and July 30, 2015.Smoothed 0.05th and 0.95th quantiles of Ft are reported with black lines and medianFt is reported in red.

where ω denotes the indirect inference estimator of the intraperiod volatility.

Compared to the asset/liability ratios, this measure takes into account the

uncertainty on the ratio as evaluated by the market. The change in the risk

45

−5 0 5 10

−10

−5

05

Dynamic model Ft

SD

FM

Ft

Figure 16: Ft of the SDFM against Ft of the simple dynamic model. This figure plotsthe smoothed median of Ft obtained via the SDFM against the smoothed median ofFt obtained via the simple dynamic model.

premia is defined by:

∆DDit = hi[log(Ait/L− 1); ω]− hi[log(Ai,t−1/L− 1); ω]−∆ log(Ait/L− 1) .

(4.12)

46

The risk premia DDit capture the magnitude of the nonlinear impact of the leverage

on stock returns. In particular, when DDit is close to zero, the equity return Yit

is close to ait, and then coincides with the value of a stationary process. In other

words, we can consider that the stock SDFM is a switching regime model, passing

from an almost stationary regime to a nonstationary regime in an endogenous way.

The different measures above can be further summarized by computing their

average and volatility either over time for a given bank, or across banks for a given

date.

For each institution i and date t, the ait in step (i) is replaced by the median

ait of the smoothed a(m)it Mm=1 using M = 100 paths and N = 10, 000 particles in

the ABC smoothing algorithm (see Section 3.4). To recover the Ait/L − 1 from

the ait, we use the initial condition log(Ai0/L − 1) = 1, ∀i. The Ait/L − 1 values

are reported in Figure 17. For comparison, we also report in Figure 18 the naive

AL measures obtained by using the simple dynamic model of Section 3. Red lines

indicate the naive ALit = exp(∑t

k=1 Yik) obtained with the nonstructural model,

while black ones indicate the structural ALit measures. The evolution of the implied

asset/liability ratios are very different according to the financial institution. We

observe for several institutions a regular increase of the ratios after the financial crisis,

likely due to the more severe demand of required capital (see e.g. GS, LNC, WFC),

but several institutions (HSBC, BCS, ING, JPM) still have rather small implied

excess asset/liability ratios. The patterns for MET is expected for all insurance

companies, with on average more protection before the crisis. So the need of liquidity

during the financial crisis is partly fulfilled by their reserves, which are reconstructed

later on at a rather high level.

The comparison of the financial leverages for the two types of models show sig-

nificant differences between the naive and structural measures. This is due to the

47

option of default, which is automatically included in the misspecified naive series.

We see that this misleading effect can be either positive, or negative, according to

the institution.

To understand the differences between the two models, more information is pro-

vided by the series of distance-to-default DD. The average risk premia of the insur-

ance over the ten firms are reported in the top panel of Figure 19. Note the similarity

between the average DDt series and the VIX volatility index (bottom panel), which

is a measure of implied volatility on the S&P500 option, usually referred as the fear

index. However, we do not have a complete similarity, especially since the level of the

average risk premia is significantly higher after the financial crisis. However, these

almost similar patterns do not account for the heterogeneity among the financial

institutions.

The risk premia of the insurance for each financial institution are reported in

Figure 20. These results show that the jump in the average DD in Figure 19 (top

panel) was mainly due to two institutions: JP Morgan and Barclays. The jump in

DD for JP Morgan is likely due to its 2008 acquisitions of Bear Sterns (for 1.5 billion

dollars) and Washington Mutual (for 1.9 billion dollars), both on bankruptcy. Simi-

larly, the jump in Barclays is likely due to its 2008 acquisition of Lehman Brothers

(for 1.7 billion dollars) after its bankruptcy. The other bumps on risk premia, smaller

though, correspond to the European sovereign debt crisis. As expected, this effect is

significant for Barclay’s, which has supported a loss of about 2 billions of dollars by

speculating on the Greek and Spanish debts by means of derivatives.

Finally, Figure 21 reports the changes in insurance risk premia. We cannot rea-

sonably interpret these results obtained by analyzing stock returns, without having

in mind derivatives written on the default of these firms and, in particular, the Credit

Default Swaps (CDS). We know that these products are often used for arbitrage and,

48

015

30

AL

for

ME

T

015

30

AL

for

ING

015

30

AL

for

GS

015

30

AL

for

LNC

2000 2005 2010 2015

015

30

AL

for

HS

BC

015

30

AL

for

JPM

015

30

AL

for

BA

C

015

30

AL

for

CS

015

30

AL

for

WF

C

2000 2005 2010 2015

015

30

AL

for

BC

S

Figure 17: Implied asset/liability ratios.

hence, for speculation. In a neighborhood of the default, we expect to have more

volatility on these insurance products and this increase in volatility should appear in

the evolution of (∆DDit)2. This behaviour indeed appears in the series of Figure 21.

When the implied asset/liability ratio decreases, the variability in ∆DDit increases.

This negative correlation between A/L and (∆DDit)2 translates the financial lever-

age effect discussed by Black (1976) and Hasanhodzic and Lo (2011). More precisely,

as suggested by Black, the stylized negative correlation between return and volatility

49

510

15

Nai

ve A

L, M

ET

13

5

Nai

ve A

L, IN

G

515

25

Nai

ve A

L, G

S

510

20

Nai

ve A

L, L

NC

2000 2005 2010 2015

13

5

Nai

ve A

L, H

SB

C

02

4

Nai

ve A

L, J

PM

24

68

Nai

ve A

L, B

AC

13

57

Nai

ve A

L, C

S

515

Nai

ve A

L, W

FC

2000 2005 2010 2015

02

46

8

Nai

ve A

L, B

CS

Figure 18: Naive asset/liability ratios. Red lines indicate the naive ALit =exp(

∑tk=1 Yik), while black ones the structural ALit measures.

is likely an indirect effect by means of the balance sheet. This is this effect of A/L,

which is noted in our framework.

The three measures above, that are AL, DD and (∆DD)2, can be used to rank

50

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Ave

rage

DD

t

2000 2005 2010 2015

1020

3040

5060

7080

VIX

Figure 19: Average risk premia of the insurance and VIX.

the financial institutions. They define rankings with different interpretations: by

the implied financial leverage for AL, by the distance-to-default as evaluated by the

market for DD, and as a measure of the magnitude of speculation for (∆DD)2. It

is important to get multiple rankings with different interpretations. For instance,

this will allow to distinguish an institution with small excess asset/liability ratio

51

0.0

1.0

2.0

DD

for

ME

T

0.0

1.0

2.0

DD

for

ING

0.0

1.0

2.0

DD

for

GS

0.0

1.0

2.0

DD

for

LNC

2000 2005 2010 2015

0.0

1.0

2.0

DD

for

HS

BC

0.0

1.0

2.0

DD

for

JPM

0.0

1.0

2.0

DD

for

BA

C

0.0

1.0

2.0

DD

for

CS

0.0

1.0

2.0

DD

for

WF

C

2000 2005 2010 2015

0.0

1.0

2.0

DD

for

BC

S

Figure 20: Risk premia of the insurance.

and small insurance premium, which is not necessarily risky for default from an

institution where both are large and which can be riskier. These rankings are a

solvency ranking, a ranking for the default insurance, and a ranking for speculative

asset, respectively.

The comparison of the financial institutions can be cross-sectional at a given date,

or be performed with respect to both institution and time. We successively consider

the two approaches.

52

0.00

0.08

∆2 DD

for

ME

T

0.00

0.08

∆2 DD

for

ING

0.00

0.08

∆2 DD

for

GS

0.00

0.08

∆2 DD

for

LNC

2000 2005 2010 2015

0.00

0.08

∆2 DD

for

HS

BC

0.00

0.08

∆2 DD

for

JPM

0.00

0.08

∆2 DD

for

BA

C

0.00

0.08

∆2 DD

for

CS

0.00

0.08

∆2 DD

for

WF

C

2000 2005 2010 2015

0.00

0.08

∆2 DD

for

BC

S

Figure 21: Squared change in default risk premia.

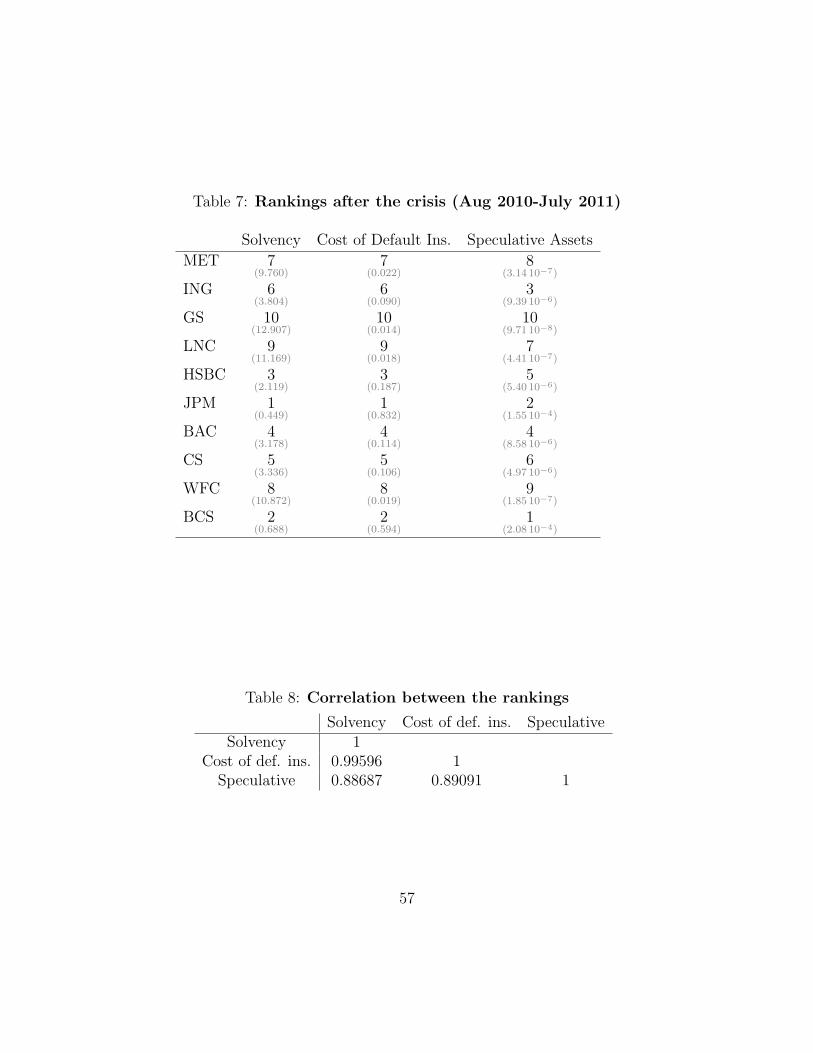

Tables 5-7 report the rankings associated with the three risk measures, respec-

tively, before the crisis (August 2006 - July 2007), during the crisis (August 2008 -

July 2009) and after the crisis (August 2010 - July 2011). The higher the rank, the

more secure and less speculative is the financial institution. As expected, the insur-

ance companies MET and LNC introduced in our set of institutions are uniformly

in the top, even if we observe a downgrade of two levels before and after the crisis

for MET. Barclays and JP Morgan are the least secure and also the most specula-

53

tive. Whereas improving its solvency and cost of default insurance ranks, ING is still

speculative. We also report the correlation between the three rankings in Table 8.

These results show that the AL and DD measures provide almost identical rankings

while ∆DD2 provides slightly different rankings.

Let us now provide ratings of these ten financial institutions that will allow for

a comparison with respect to both institution and time. Let us collect all the values

ALiti=1,...,nt=1,...,T , DDiti=1,...,n

t=1,...,T and ∆DD2iti=1,...,n

t=1,...,T and calculate selected quantiles of

the associated sample distribution. These quantiles can be used to define a risk seg-

mentation, with different ratings associated with the segments. The rating categories

are defined in Table 9 with 10 different ratings. We have noted them as usual by

aaa, aa, . . . , but they have interpretations which may be different from the ratings of

S&P and Moody’s for instance, not only since they are based on different measures.

In particular, we denote c− the last rating to avoid the notation d meaning default.

Then, we compare the values in Tables 5-7 to the subintervals. We report the

appropriate ratings in Tables 10-12. When we compare to the whole period of ob-

servations, we see that even in the period August 2006-August 2007, that is between

the drop in the price of the US real estate and the announcement of frozen funds by

Bnp Paribas and AXA, only two institutions were bbb, and the speculative ratings

systematically smaller than the two other ratings, which might be an advanced in-

dication of a future bubble crash. The bad ratings during the crisis period are not

surprising. Finally, Table 12 shows the slow recovery after the crisis, with still very

high risks on HSBC, JPM and BCS.

54

Table 5: Rankings before the crisis (Aug 2006-July 2007)

Solvency Cost of Default Ins. Speculative Assets

MET 10(15.979)

10(0.010)

10(1.75 10−8)

ING 4(5.490)

4(0.053)

3(6.73 10−7)

GS 7(9.481)

7(0.024)

6(2.05 10−7)

LNC 9(13.428)

9(0.013)

8(4.26 10−8)

HSBC 3(3.326)

3(0.106)

4(6.10 10−7)

JPM 1(2.099)

1(0.188)

1(5.99 10−6)

BAC 6(7.661)

6(0.032)

7(1.80 10−7)

CS 5(6.440)

5(0.043)

5(3.31 10−7)

WFC 8(11.075)

8(0.018)

9(3.84 10−8)

BCS 2(3.051)

2(0.119)

2(4.71 10−6)

55

Table 6: Rankings during the crisis (Aug 2008-July 2009)

Solvency Cost of Default Ins. Speculative Assets

MET 9(7.097)

8(0.050)

8(6.36 10−5)

ING 4(2.365)

4(0.203)

4(8.85 10−4)

GS 10(7.367)

10(0.038)

10(1.89 10−5)

LNC 7(5.471)

7(0.070)

5(3.26 10−4)

HSBC 3(1.951)

3(0.216)

7(1.65 10−4)

JPM 1(0.459)

1(0.972)

2(5.07 10−3)

BAC 5(2.619)

5(0.198)

3(9.19 10−4)

CS 6(2.996)

6(0.150)

6(3.09 10−4)

WFC 8(7.025)

9(0.042)

9(3.07 10−5)

BCS 2(0.606)

2(0.843)

1(9.35 10−3)

56

Table 7: Rankings after the crisis (Aug 2010-July 2011)

Solvency Cost of Default Ins. Speculative Assets

MET 7(9.760)

7(0.022)

8(3.14 10−7)

ING 6(3.804)

6(0.090)

3(9.39 10−6)

GS 10(12.907)

10(0.014)

10(9.71 10−8)

LNC 9(11.169)

9(0.018)

7(4.41 10−7)

HSBC 3(2.119)

3(0.187)

5(5.40 10−6)

JPM 1(0.449)

1(0.832)

2(1.55 10−4)

BAC 4(3.178)

4(0.114)

4(8.58 10−6)

CS 5(3.336)

5(0.106)

6(4.97 10−6)

WFC 8(10.872)

8(0.019)

9(1.85 10−7)

BCS 2(0.688)

2(0.594)

1(2.08 10−4)

Table 8: Correlation between the rankings

Solvency Cost of def. ins. SpeculativeSolvency 1

Cost of def. ins. 0.99596 1Speculative 0.88687 0.89091 1

57

Table 9: Rating categories

AL DD ∆DD2

aaa · ≥ qAL99% · ≤ qDD

1% · ≤ q∆DD2

1%

aa qAL99% > · ≥ qAL

97% qDD3% > · ≥ qDD

1% q∆DD2

3% > · ≥ q∆DD2

1%

a qAL97% > · ≥ qAL

95% qDD5% > · ≥ qDD

3% q∆DD2

5% > · ≥ q∆DD2

3%

bbb qAL95% > · ≥ qAL

90% qDD10% > · ≥ qDD

5% q∆DD2

10% > · ≥ q∆DD2

5%

bb qAL90% > · ≥ qAL

80% qDD20% > · ≥ qDD

10% q∆DD2

20% > · ≥ q∆DD2

10%

b qAL80% > · ≥ qAL

70% qDD30% > · ≥ qDD

20% q∆DD2

30% > · ≥ q∆DD2

20%

ccc qAL70% > · ≥ qAL

60% qDD40% > · ≥ qDD

30% q∆DD2

40% > · ≥ q∆DD2

30%

cc qAL60% > · ≥ qAL

50% qDD50% > · ≥ qDD

40% q∆DD2

50% > · ≥ q∆DD2

40%

c qAL50% > · ≥ qAL

40% qDD60% > · ≥ qDD

50% q∆DD2

60% > · ≥ q∆DD2

50%

c− · ≤ qAL40% qDD

60% ≤ · q∆DD2

60% ≤ ·

Table 10: Ratings before the crisis (Aug 2006-July 2007)

Solvency Cost of Default Ins. Speculative Assets

MET bbb bbb bING ccc ccc cGS bb bb ccLNC bbb bbb cccHSBC c c cJPM c− c− c−

BAC b b ccCS b b ccWFC bb bb bBCS c c c−

58

Table 11: Ratings during the crisis (Aug 2008-July 2009)

Solvency Cost of Default Ins. Speculative Assets

MET b ccc c−

ING c− c− c−

GS b b c−

LNC ccc ccc c−

HSBC c− c− c−

JPM c− c− c−

BAC c− c− c−

CS c c− c−

WFC b b c−

BCS c− c− c−

Table 12: Ratings after the crisis (Aug 2010-July 2011)

Solvency Cost of Default Ins. Speculative Assets

MET bb bb ccING cc cc c−

GS bbb bbb cccLNC bb bb ccHSBC c− c− c−

JPM c− c− c−

BAC c c c−

CS c c c−

WFC bb bb ccBCS c− c− c−

59

5 Conclusion

We have introduced a structural dynamic factor model (SDFM), which accounts for

linear common factor, stochastic volatilities, and also to their nonlinear impacts on

equity returns, when the distance-to-default is small. This leads to a state space

model, in which the state dynamics is stationary and the measurement equation

possibly creates nonstationarity. Due to the structural Value-of-the-Firm model,

defining the measurement equation, some latent variables such as the asset/liability

ratio have an economic interpretation in terms of balance sheets. The SDFM allows to

deduce from the observation of equity returns only approximations of these financial

ratios, the so-called implied asset/liability ratios. The model also allows for defining

different risk measures and associated rankings: a solvency ranking, a cost of default

insurance ranking and a speculative assets ranking.

Clearly, such an approach is only based on market data, as are for instance the

SRISK ranking produced by the volatility lab (see Brownlees and Engle (2012)). It

would be nice to use jointly the information on returns with the information on the

balance sheets. As mentioned in the main text, this is difficult challenge. First, the

observation frequencies are not the same; second, it is difficult to deduce from the

balance sheet the financial ratio involved in Merton’s model, that are the part of

debt to be recovered immediately and the part of asset sufficiently liquid. Finally,

several lines of the balance sheet of a bank contain financial assets, such as stock,

bonds, or derivatives, which are often marked-to-market values. Thus, they are also

partly market data.