Embed Size (px)

Citation preview

Structural change in a globalized Asia: macrotrends and US policy challenges$

Michael G. Plummer*

Johns Hopkins University SAIS-Bologna, Via Belmeloro, 11, 40126 Bologna, Italy

Received 5 January 2003; received in revised form 4 February 2003; accepted 25 February 2003

Abstract

In this paper, we focus on directional and structural change in developing Asian trade patterns, with a

focus on economic interaction with the United States (and using the EU as a benchmark). Several

important results from the analysis are that: (1) while private-sector-led regional integration in Asia has

increased for most developing Asian countries (in some cases, impressively), the United States remains

the region’s single most important export market; (2) the trade structure of developing Asian countries

has changed significantly over the past decade, a result that resonates with the literature on structural

transformation in developing Asia; (3) the economic dynamism of developing Asian exports is

consistent with the changes in trade with the United States (and the EU); and (4) SITC 7, which is the

most sophisticated sector of the SITC groups, has become the most important sector for most

developing Asian exports (and imports), and the US market has been a key protagonist in this process.

In addition, the paper considers emerging policy challenges in developing the US–Asian economic

relationship at various levels, using the Viet Nam–US Bilateral Trade Agreement (BTA) as an ex post

case study and considering a number of ex ante initiatives that are currently being developed.

# 2003 Elsevier Science Inc. All rights reserved.

Keywords: Globalization; US economic policy; Asian economic development

1. Introduction

The global economy has been stagnating over the past year with no clear sign of

future direction. After the longest economic expansion in its history, the United States

Journal of Asian Economics 14 (2003) 243–281

$ This paper was first presented at the joint American Economic Association/American Committee for Asian

Economic Studies panel, ‘‘Asia-US Interdependence: Effects of the US Recession,’’ 3 January 2003,

Washington, DC.* Tel.: þ39-051-2917-811; fax: þ39-051-228-505.

E-mail address: [email protected] (M.G. Plummer).

1049-0078/03/$ – see front matter # 2003 Elsevier Science Inc. All rights reserved.

doi:10.1016/S1049-0078(03)00024-1

experienced an economic downturn in the third-quarter of 2001. Since then, the US

economy continues to offer a variety of confusing and contradictory economic signals. For

example, in December 2002, markets could cheer the rebound in consumer confidence,

high productivity growth of over 5%, and revised third-quarter GDP growth of 4%, but

despair over sluggish job creation and the increase in the unemployment rate to 6%. The

US stock markets have been highly volatile; the broadest oft-quoted index of US stocks, the

S&P 500, was down approximately 40% from its absolute high and by 24% over 2002. As

of end-January 2003, the dollar had depreciated against the euro by over 20% relative to its

peaks in 2001, and while the US current account deficit improved marginally toward the

end of 2002, it is estimated to reach 4.8 and 5.0% of GDP in 2002 and 2003, respectively.1

The US economy is expected to expand between 2.3 and 2.6% in 2002 and 2.0 and 3.3% in

2003. In the Euro Area and Japan, the economic indicators are even worse, with growth

forecasts of less than 1% over 2002–2003 for the former and probably continued recession

(�1.1 to 0% in 2002; �0.1 to 2.0 in 2003) in the latter.2

Moreover, Asia has been hit by a series of ‘‘policy shocks.’’ Developed-country

protection in areas in which East Asian countries have comparative advantage (e.g.

agriculture, textiles, and steel) continues to be high and, despite Uruguay Round cuts,

in some cases rising (e.g. in the case of agriculture in the United States and the EU; steel in

case of the United States). Moreover, the EU has been negotiating many preferential trade

arrangements with countries competing with East Asia (the United States has also been

doing this, albeit at a less ambitious pace and with more East Asian countries). The cost of

trade diversion due to such agreements has been high in certain sectors in the past and will

likely be so in the future (see, e.g. Kreinin & Plummer, 2002).

Nevertheless, Asia is doing fairly well, at least relative to what one might have guessed

given the region’s dependence on the global economy. True, 2001 was not a good year for

most economies in the region: growth in East Asia fell from 6.9% in 1999 and 7.6% in 2000

to only 4.3% in 2001.3 ASEAN (excluding Brunei and Myanmar) growth fell from 6.0% in

2000 to only 1.9% in 2001, with Singapore experiencing its first significant recession (GDP

fell by 2%) since the mid-1980s.4 Export growth fell considerably in the region; over 2000

and 2001 it plummeted from 28 to 7% for China, an average of about 19 to �7% for the

NIEs and 19 to �8% in the ASEAN-4. With such a dismal external performance it is

surprising that outward-oriented economies like those in East Asia did not experience even

deeper cuts in output growth, as was predicted by many economists. Moreover, economic

growth in Asia picked up considerably in 2002, despite volatility of growth in its major

markets. Most predictions currently maintain that the region had overcome the worst of the

business cycle by mid-2002. Revised forecasts in October 2002 from Consensus Forecasts5

suggest that East Asian economic growth should hit a respectable 6% in 2002, better than

1 ‘‘The Economist Poll of Forecasters, December 2002 Averages,’’ The Economist, 7 December 2002, p. 106.2 Ibid.3 Data in this paragraph come from the Asian Development Bank: (1) Asian Economic Monitor, July 2002 and

October 2002, and Key Economic Indicators 2002.4 Singapore output growth contacted by 0.1% in 1998, i.e. in the middle of the Asian Crisis.5 Consensus Forecasts bases its forecasts on estimates from 200 economic and financial forecasters in 70

countries and is used by the Asian Development Bank in its Asian Economic Monitor publication as a broad-

based source of economic forecasts for the region.

244 M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281

double the forecast for the United States and triple that for Europe, and for 2003, the region

is now expected to expand by 5.9%.

These trends are somewhat puzzling; the real-side hit of the global slowdown was

predicted to cause a much larger external shock to the region’s economies. The financial

shock of falling equity and fixed-income markets in the West should have had an even more

significant effect. Despite attempts after the Asian Crisis to develop equity and fixed-income

markets, Asian capital markets continue to be under-developed relative to those in the United

States and Europe. Asia relies on financial intermediation in the West, leaving it exposed to

the significant volatility and persistent weakness in the US and European equity markets.

So why this economic resilience? Two possible explanations as to why developing Asia

continues to expand beyond predictions in light of economic slowdown/crises in the

developed countries are that: (1) intra-regional trade has been picking up, leaving the

region far less vulnerable to real-side external shocks; and (2) structural changes in the

composition of developing Asian exports have rendered the region less vulnerable.

In this paper, we will address (in Section 2) the first question briefly, as much has already

been done on the subject. Instead, we will concentrate on structural change in Asian trade.

We begin with a cursory analysis of intra-regional trade, followed by an assessment of the

changes in the overall structure of Asian trade and, in particular, bilateral trade with the

United States, both because of the key role of the United States as a trading partner and the

focus on US–Asian trade in this issue. We will undertake parallel analysis with the EU as a

‘‘control’’ country (over a shorter time period). Next, in Section 3 we will discuss some real

and policy implications of these changes for the dependence of Asia on the US market,

particularly in light of recent macroeconomic volatility, as well as issues in US–Asian

economic cooperation. We use the case study of the recent Viet Nam–US trade agreement

as an example of change in bilateral policy relationships and strategies. Finally, we offer

some concluding remarks in Section 4, including a discussion of US policy challenges in

Asia.

2. Trends in trade patterns: direction, composition and structural change

It is uncontroversial that exports have been an important engine of growth in Asia over

the past three decades. World Bank (1993) gives an excellent survey of the role of exports

in the Asian success story, but it is not alone. The Asian Crisis of 1997–1999 may have

expelled the myth that, somehow, Asian economic growth defied economic gravity, but it

did nothing to reduce the strong empirical evidence that exports have played a critical role

in regional growth. In fact, as Grilli (2002), Montes (1998), Parker and Lee (2001), and

others have pointed out, the fall in export growth in Asia actually contributed to the onset of

the Crisis.

Das (2000) gives an important historical perspective to the remarkable export perfor-

mance of Asia over the past three decades. His data show that, in real terms, from 1965 to

1980, world exports grew by 170%, followed by increases of 40% over the 1980s and 70%

from 1989 to 1997. On the other hand, real exports of developing Asian countries increased

by 207, 190, and 123% over these respective periods. The developing Asian share of world

exports grew from 7% in 1965 to 19% in 1997 (a total of US$ 1.009 trillion in 1990), with

M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281 245

the NIEs leading the way (from 1.6 to 10.4%) followed by the ASEAN-4 (1.9–3.9%) and

China (1.5–3.3%). The relatively-closed South Asia-3 (Bangladesh, India and Pakistan)

actually saw their share fall from 1.3 to 0.9%.

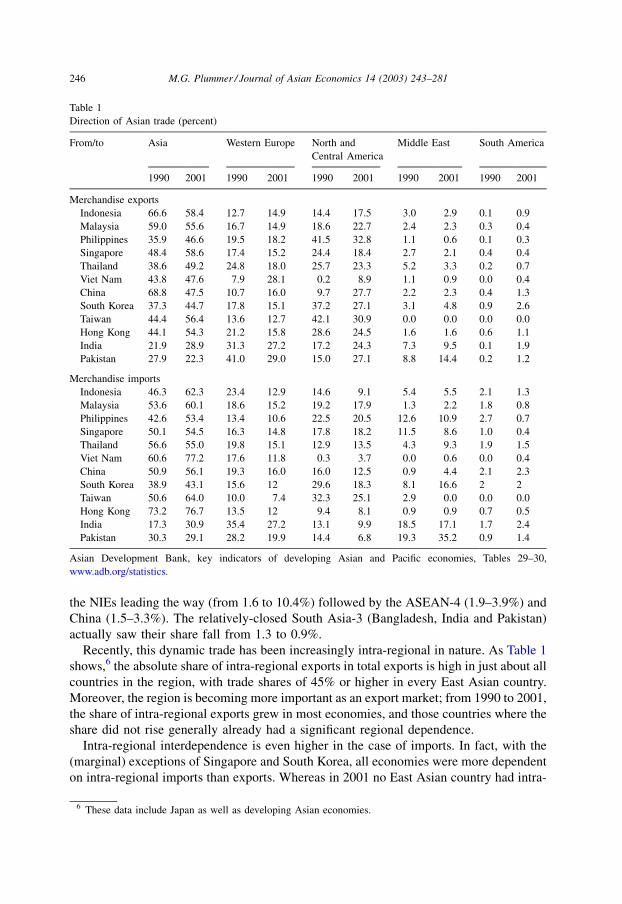

Recently, this dynamic trade has been increasingly intra-regional in nature. As Table 1

shows,6 the absolute share of intra-regional exports in total exports is high in just about all

countries in the region, with trade shares of 45% or higher in every East Asian country.

Moreover, the region is becoming more important as an export market; from 1990 to 2001,

the share of intra-regional exports grew in most economies, and those countries where the

share did not rise generally already had a significant regional dependence.

Intra-regional interdependence is even higher in the case of imports. In fact, with the

(marginal) exceptions of Singapore and South Korea, all economies were more dependent

on intra-regional imports than exports. Whereas in 2001 no East Asian country had intra-

Table 1

Direction of Asian trade (percent)

From/to Asia Western Europe North and

Central America

Middle East South America

1990 2001 1990 2001 1990 2001 1990 2001 1990 2001

Merchandise exports

Indonesia 66.6 58.4 12.7 14.9 14.4 17.5 3.0 2.9 0.1 0.9

Malaysia 59.0 55.6 16.7 14.9 18.6 22.7 2.4 2.3 0.3 0.4

Philippines 35.9 46.6 19.5 18.2 41.5 32.8 1.1 0.6 0.1 0.3

Singapore 48.4 58.6 17.4 15.2 24.4 18.4 2.7 2.1 0.4 0.4

Thailand 38.6 49.2 24.8 18.0 25.7 23.3 5.2 3.3 0.2 0.7

Viet Nam 43.8 47.6 7.9 28.1 0.2 8.9 1.1 0.9 0.0 0.4

China 68.8 47.5 10.7 16.0 9.7 27.7 2.2 2.3 0.4 1.3

South Korea 37.3 44.7 17.8 15.1 37.2 27.1 3.1 4.8 0.9 2.6

Taiwan 44.4 56.4 13.6 12.7 42.1 30.9 0.0 0.0 0.0 0.0

Hong Kong 44.1 54.3 21.2 15.8 28.6 24.5 1.6 1.6 0.6 1.1

India 21.9 28.9 31.3 27.2 17.2 24.3 7.3 9.5 0.1 1.9

Pakistan 27.9 22.3 41.0 29.0 15.0 27.1 8.8 14.4 0.2 1.2

Merchandise imports

Indonesia 46.3 62.3 23.4 12.9 14.6 9.1 5.4 5.5 2.1 1.3

Malaysia 53.6 60.1 18.6 15.2 19.2 17.9 1.3 2.2 1.8 0.8

Philippines 42.6 53.4 13.4 10.6 22.5 20.5 12.6 10.9 2.7 0.7

Singapore 50.1 54.5 16.3 14.8 17.8 18.2 11.5 8.6 1.0 0.4

Thailand 56.6 55.0 19.8 15.1 12.9 13.5 4.3 9.3 1.9 1.5

Viet Nam 60.6 77.2 17.6 11.8 0.3 3.7 0.0 0.6 0.0 0.4

China 50.9 56.1 19.3 16.0 16.0 12.5 0.9 4.4 2.1 2.3

South Korea 38.9 43.1 15.6 12 29.6 18.3 8.1 16.6 2 2

Taiwan 50.6 64.0 10.0 7.4 32.3 25.1 2.9 0.0 0.0 0.0

Hong Kong 73.2 76.7 13.5 12 9.4 8.1 0.9 0.9 0.7 0.5

India 17.3 30.9 35.4 27.2 13.1 9.9 18.5 17.1 1.7 2.4

Pakistan 30.3 29.1 28.2 19.9 14.4 6.8 19.3 35.2 0.9 1.4

Asian Development Bank, key indicators of developing Asian and Pacific economies, Tables 29–30,

www.adb.org/statistics.

6 These data include Japan as well as developing Asian economies.

246 M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281

regional export shares exceeding 60% of total trade, fully one-half had intra-regional

import shares exceeding that figure.

There are a variety of ways that one might analyze further this change in intra-regional

trade dependence. For example, if one normalizes these trade shares by the size of these

economies, as proxied by their share of international trade, one might get a better picture of

this intra-regional trade ‘‘bias.’’ The literature has generated a number of estimates in this

regard (e.g. Frankel, 1993; Kreinin & Plummer, 2002; Petri, 1993) and most find a strong

bias for intra-regional trade, a bias which has generally been increasing over time.

Moreover, certain authors (e.g. Frankel, 1997; Kreinin, Plummer, & Abe, 1999; Plummer,

2002) have taken an econometric approach to analyzing the determinants of intra-regional

trade and they generally come to the same result: there exists a trade bias in Asian trade.

Assuming that this relationship remains stable, it is likely that faster growth rates in Asia

relative to the world will increasingly show up in trade-share figures. No doubt this is

already happening and may be interpreted as one reason why the region seems to be

becoming more insulated from extra-regional macroeconomic shocks. Indeed, Asian

regional integration over this period is unique in a global context as it is driven almost

exclusively through informal, market-led initiatives, rather than policy initiatives through

preferential-trading arrangements.7

However, the significance of these changes in trade patterns is also a function of the

composition of trade. If intra-regional trade were predominately a function of changes in

agricultural and national-resource-intensive goods, as it arguably has been in the past, the

trade numbers would be somewhat deceiving. In addition, for a variety of reasons, an

increase in the share of manufactured exports relative to primary exports, as well as the

progressive increase in the share of more sophisticated manufactured goods, constitutes an

important part of the economic development process, as well as reducing the susceptibility

of exports and, hence, economic growth to vicissitudes in the international marketplace

(due to, for example, less volatile and secular improvements in terms of trade, less exposure

to natural shocks, and technology-related benefits). Indeed, promotion of manufactures is a

key motivation behind the outward-oriented development policies that East Asia—and,

progressively, much of South Asia—has embraced.

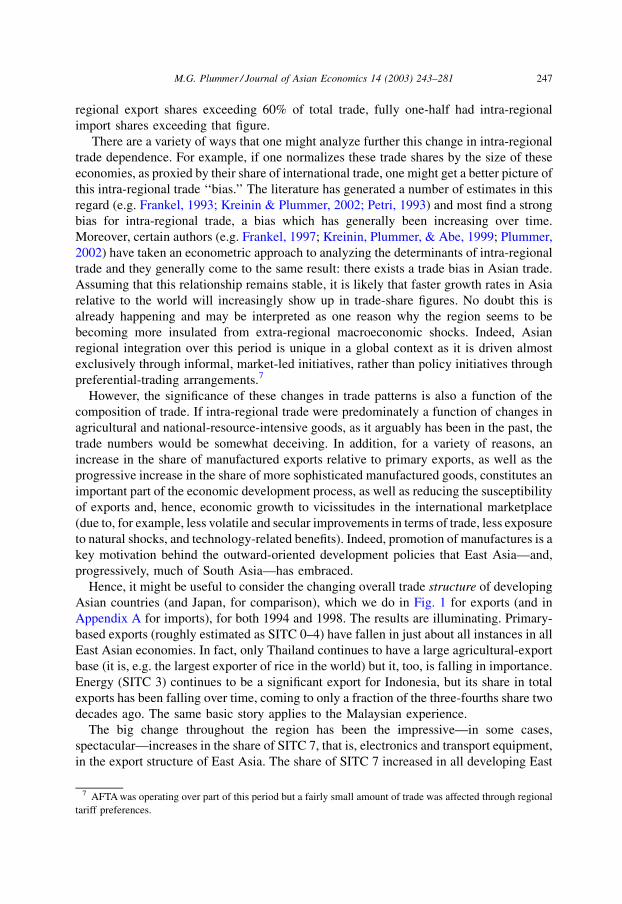

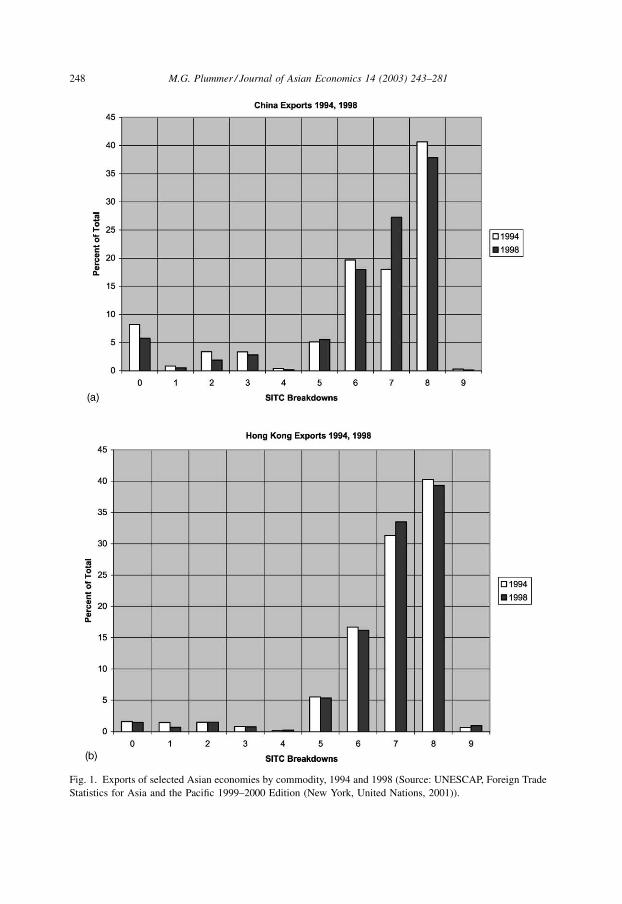

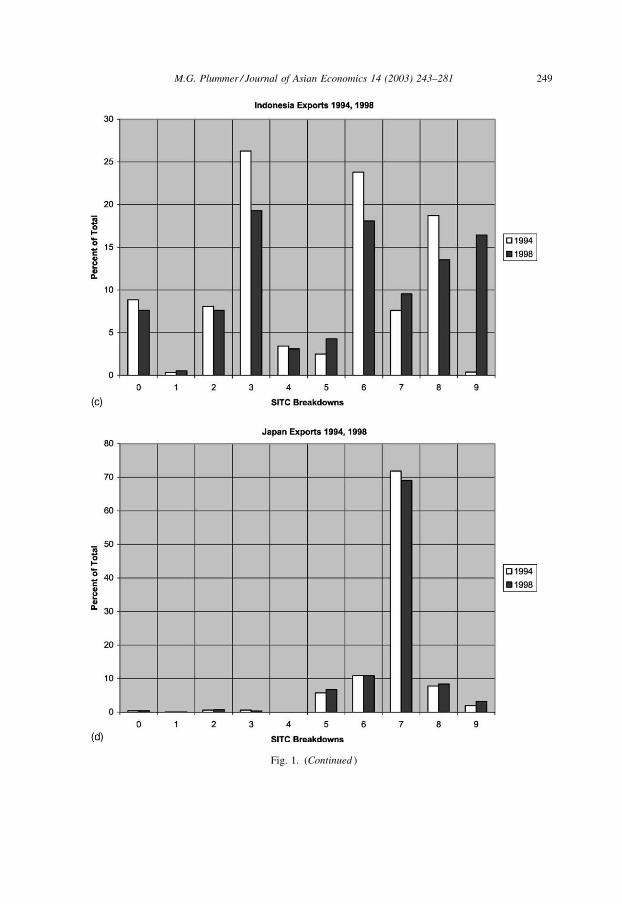

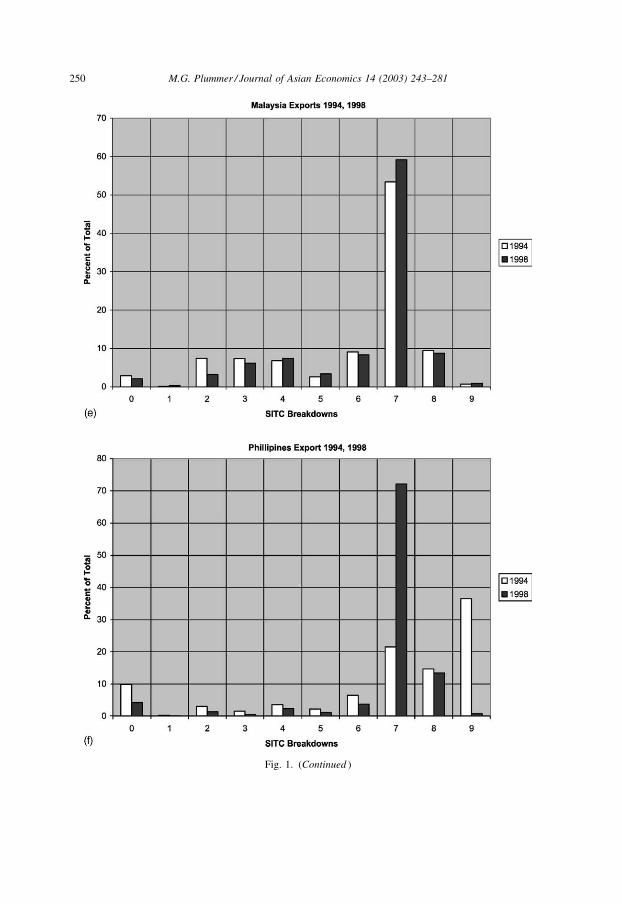

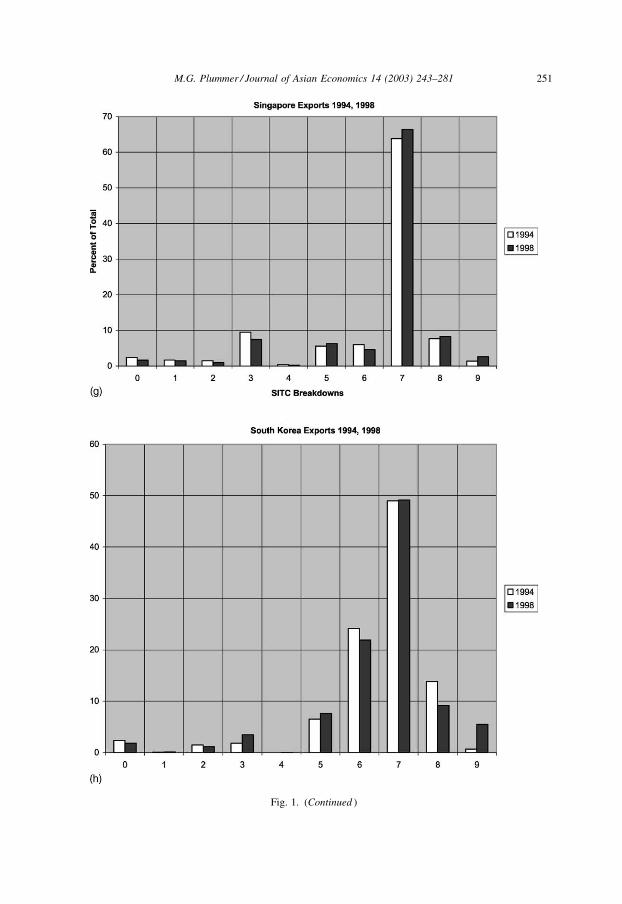

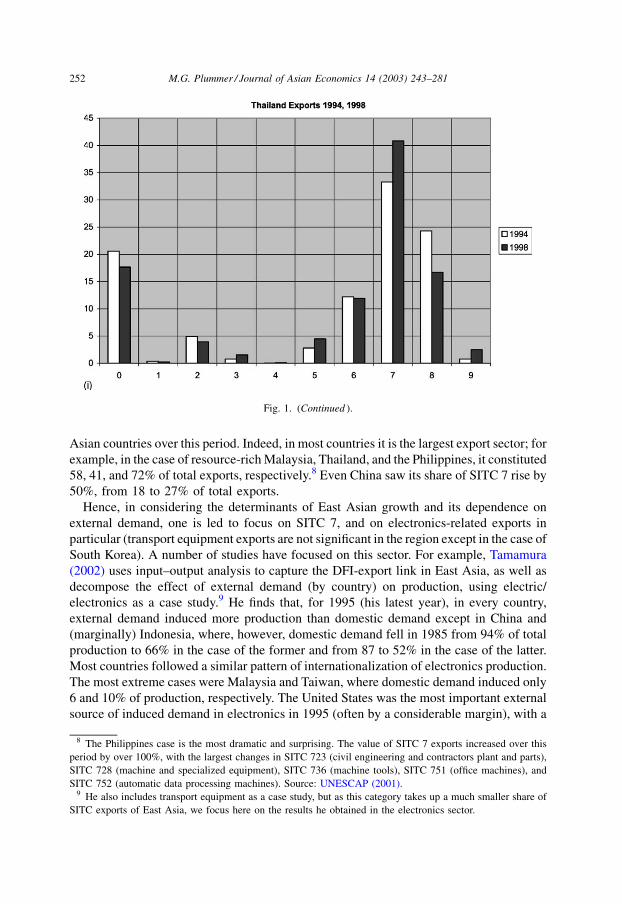

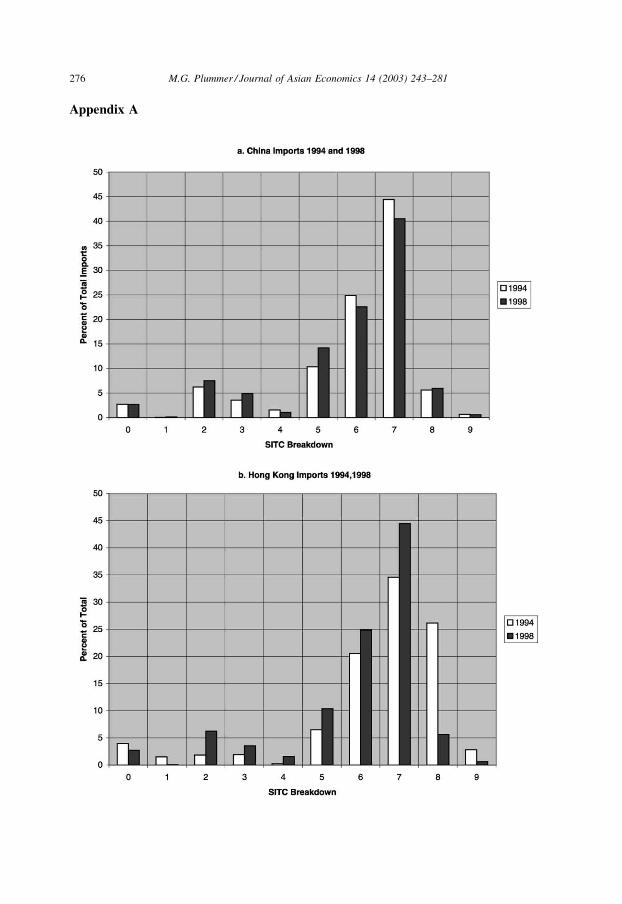

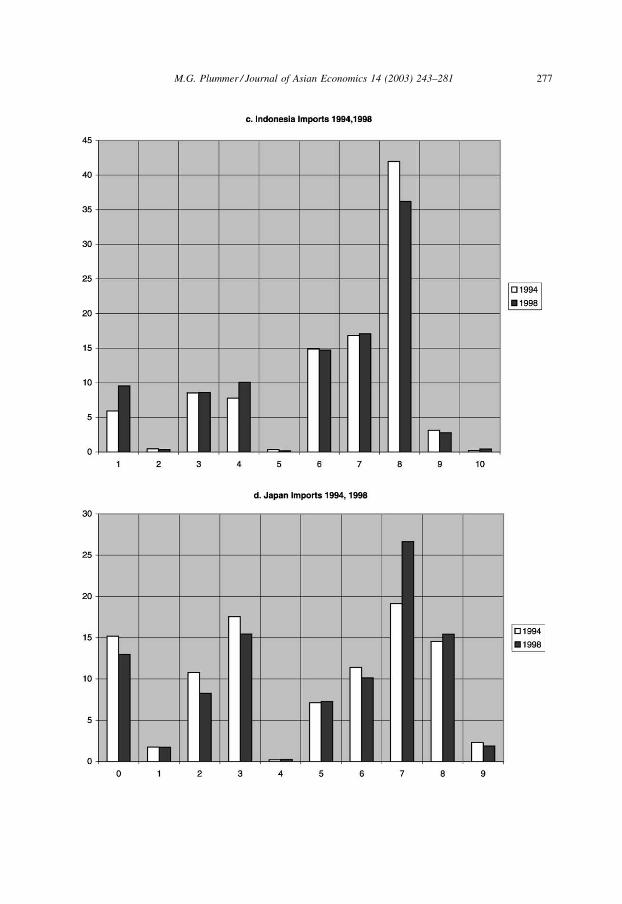

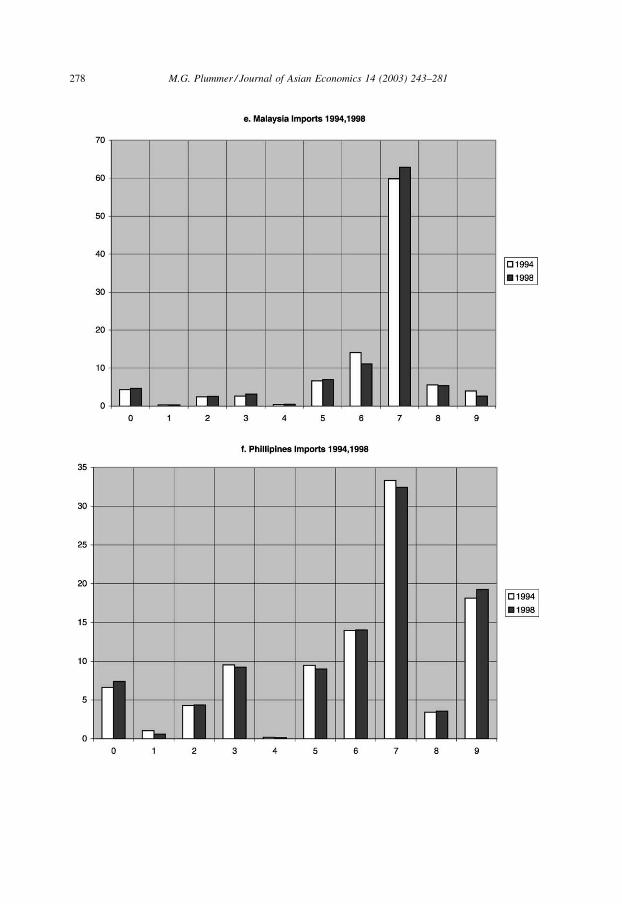

Hence, it might be useful to consider the changing overall trade structure of developing

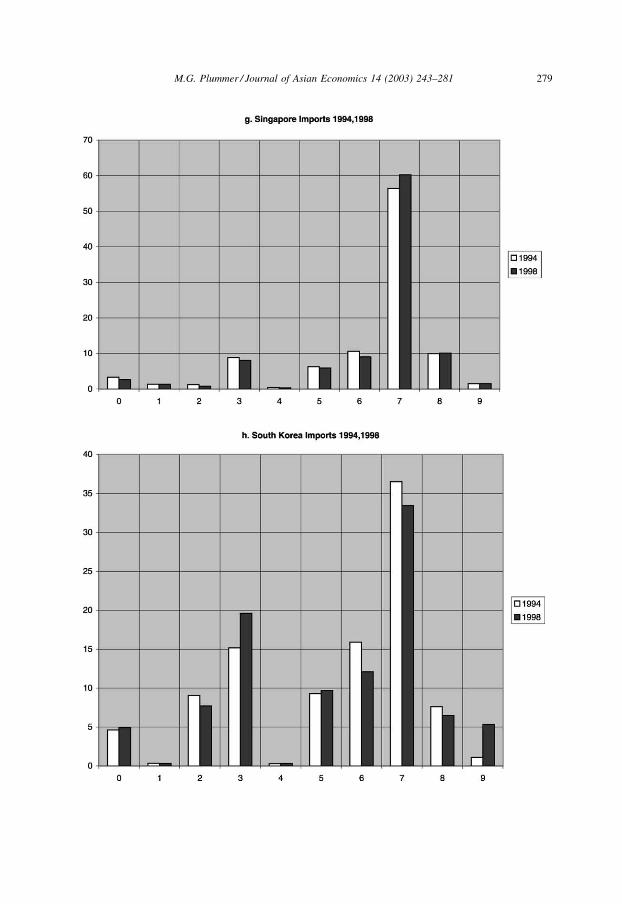

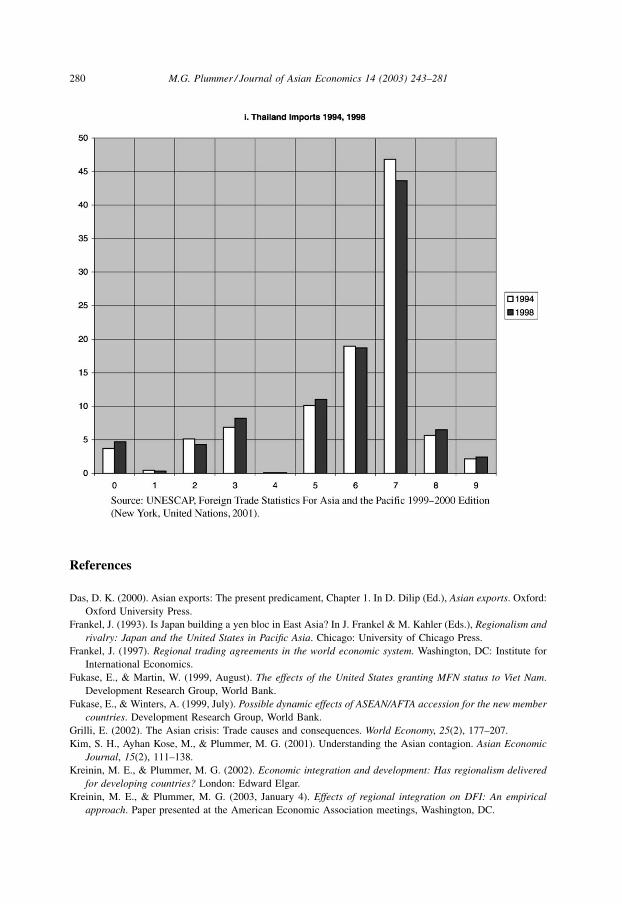

Asian countries (and Japan, for comparison), which we do in Fig. 1 for exports (and in

Appendix A for imports), for both 1994 and 1998. The results are illuminating. Primary-

based exports (roughly estimated as SITC 0–4) have fallen in just about all instances in all

East Asian economies. In fact, only Thailand continues to have a large agricultural-export

base (it is, e.g. the largest exporter of rice in the world) but it, too, is falling in importance.

Energy (SITC 3) continues to be a significant export for Indonesia, but its share in total

exports has been falling over time, coming to only a fraction of the three-fourths share two

decades ago. The same basic story applies to the Malaysian experience.

The big change throughout the region has been the impressive—in some cases,

spectacular—increases in the share of SITC 7, that is, electronics and transport equipment,

in the export structure of East Asia. The share of SITC 7 increased in all developing East

7 AFTA was operating over part of this period but a fairly small amount of trade was affected through regional

tariff preferences.

M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281 247

Fig. 1. Exports of selected Asian economies by commodity, 1994 and 1998 (Source: UNESCAP, Foreign Trade

Statistics for Asia and the Pacific 1999–2000 Edition (New York, United Nations, 2001)).

248 M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281

Fig. 1. (Continued )

M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281 249

Fig. 1. (Continued )

250 M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281

Fig. 1. (Continued )

M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281 251

Asian countries over this period. Indeed, in most countries it is the largest export sector; for

example, in the case of resource-rich Malaysia, Thailand, and the Philippines, it constituted

58, 41, and 72% of total exports, respectively.8 Even China saw its share of SITC 7 rise by

50%, from 18 to 27% of total exports.

Hence, in considering the determinants of East Asian growth and its dependence on

external demand, one is led to focus on SITC 7, and on electronics-related exports in

particular (transport equipment exports are not significant in the region except in the case of

South Korea). A number of studies have focused on this sector. For example, Tamamura

(2002) uses input–output analysis to capture the DFI-export link in East Asia, as well as

decompose the effect of external demand (by country) on production, using electric/

electronics as a case study.9 He finds that, for 1995 (his latest year), in every country,

external demand induced more production than domestic demand except in China and

(marginally) Indonesia, where, however, domestic demand fell in 1985 from 94% of total

production to 66% in the case of the former and from 87 to 52% in the case of the latter.

Most countries followed a similar pattern of internationalization of electronics production.

The most extreme cases were Malaysia and Taiwan, where domestic demand induced only

6 and 10% of production, respectively. The United States was the most important external

source of induced demand in electronics in 1995 (often by a considerable margin), with a

Fig. 1. (Continued ).

8 The Philippines case is the most dramatic and surprising. The value of SITC 7 exports increased over this

period by over 100%, with the largest changes in SITC 723 (civil engineering and contractors plant and parts),

SITC 728 (machine and specialized equipment), SITC 736 (machine tools), SITC 751 (office machines), and

SITC 752 (automatic data processing machines). Source: UNESCAP (2001).9 He also includes transport equipment as a case study, but as this category takes up a much smaller share of

SITC exports of East Asia, we focus here on the results he obtained in the electronics sector.

252 M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281

simple average share of approximately 25% for the sample. In the key cases of Malaysia,

the Philippines, and Taiwan, US demand was even more important than domestic demand,

and in the case of Thailand, they are about the same.

In short, SITC 7 is leading the way in the restructuring of Asian exports, and the United

States is a key protagonist in this process.

We are able to derive some additional insight by analyzing the changes in the structure of

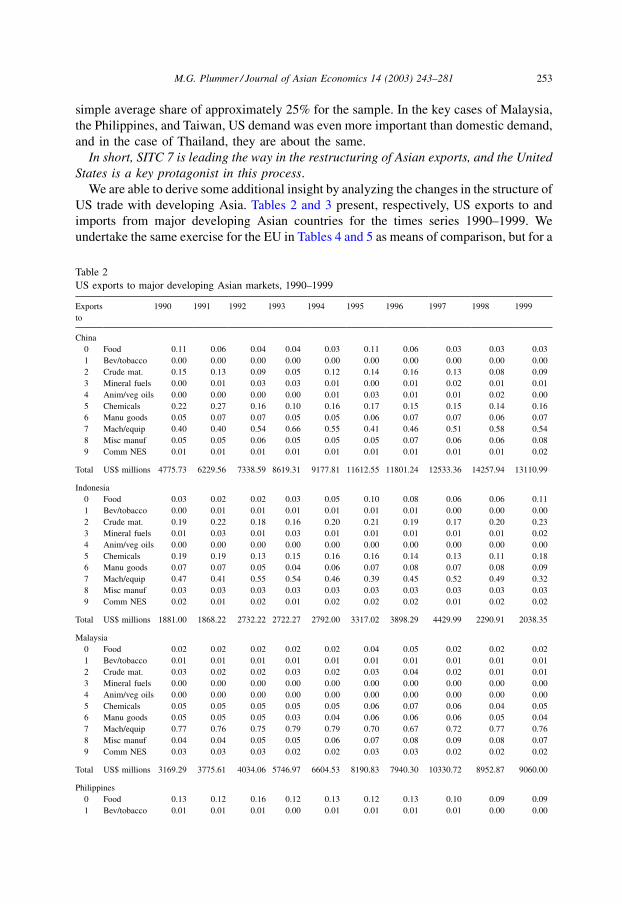

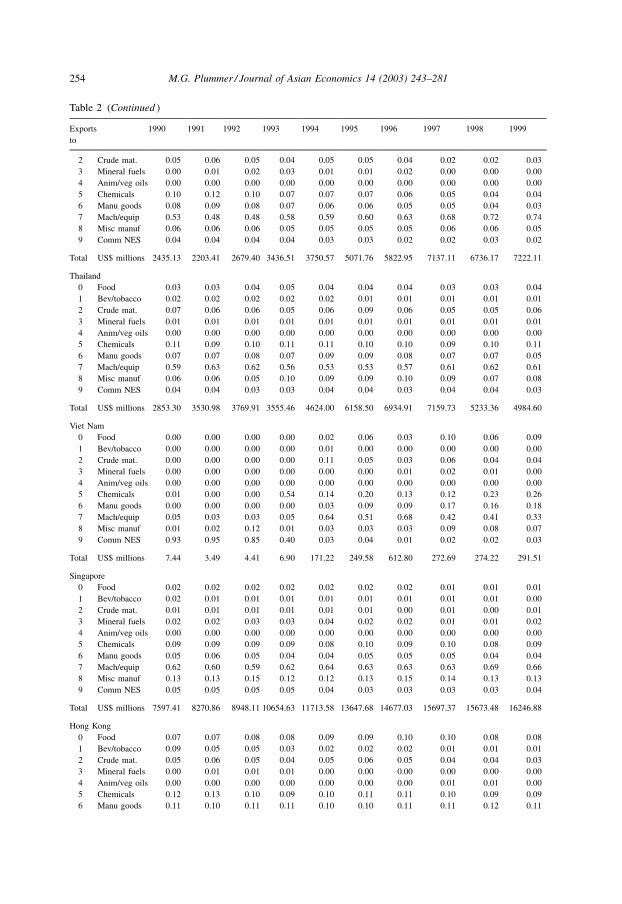

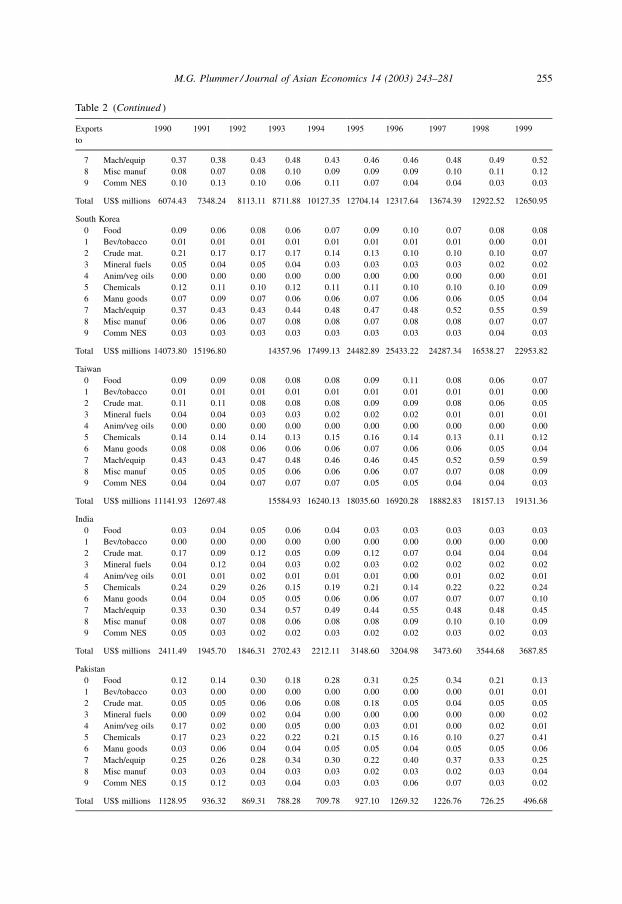

US trade with developing Asia. Tables 2 and 3 present, respectively, US exports to and

imports from major developing Asian countries for the times series 1990–1999. We

undertake the same exercise for the EU in Tables 4 and 5 as means of comparison, but for a

Table 2

US exports to major developing Asian markets, 1990–1999

Exports

to

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

China

0 Food 0.11 0.06 0.04 0.04 0.03 0.11 0.06 0.03 0.03 0.03

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.15 0.13 0.09 0.05 0.12 0.14 0.16 0.13 0.08 0.09

3 Mineral fuels 0.00 0.01 0.03 0.03 0.01 0.00 0.01 0.02 0.01 0.01

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.01 0.03 0.01 0.01 0.02 0.00

5 Chemicals 0.22 0.27 0.16 0.10 0.16 0.17 0.15 0.15 0.14 0.16

6 Manu goods 0.05 0.07 0.07 0.05 0.05 0.06 0.07 0.07 0.06 0.07

7 Mach/equip 0.40 0.40 0.54 0.66 0.55 0.41 0.46 0.51 0.58 0.54

8 Misc manuf 0.05 0.05 0.06 0.05 0.05 0.05 0.07 0.06 0.06 0.08

9 Comm NES 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.02

Total US$ millions 4775.73 6229.56 7338.59 8619.31 9177.81 11612.55 11801.24 12533.36 14257.94 13110.99

Indonesia

0 Food 0.03 0.02 0.02 0.03 0.05 0.10 0.08 0.06 0.06 0.11

1 Bev/tobacco 0.00 0.01 0.01 0.01 0.01 0.01 0.01 0.00 0.00 0.00

2 Crude mat. 0.19 0.22 0.18 0.16 0.20 0.21 0.19 0.17 0.20 0.23

3 Mineral fuels 0.01 0.03 0.01 0.03 0.01 0.01 0.01 0.01 0.01 0.02

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.19 0.19 0.13 0.15 0.16 0.16 0.14 0.13 0.11 0.18

6 Manu goods 0.07 0.07 0.05 0.04 0.06 0.07 0.08 0.07 0.08 0.09

7 Mach/equip 0.47 0.41 0.55 0.54 0.46 0.39 0.45 0.52 0.49 0.32

8 Misc manuf 0.03 0.03 0.03 0.03 0.03 0.03 0.03 0.03 0.03 0.03

9 Comm NES 0.02 0.01 0.02 0.01 0.02 0.02 0.02 0.01 0.02 0.02

Total US$ millions 1881.00 1868.22 2732.22 2722.27 2792.00 3317.02 3898.29 4429.99 2290.91 2038.35

Malaysia

0 Food 0.02 0.02 0.02 0.02 0.02 0.04 0.05 0.02 0.02 0.02

1 Bev/tobacco 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01

2 Crude mat. 0.03 0.02 0.02 0.03 0.02 0.03 0.04 0.02 0.01 0.01

3 Mineral fuels 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.05 0.05 0.05 0.05 0.05 0.06 0.07 0.06 0.04 0.05

6 Manu goods 0.05 0.05 0.05 0.03 0.04 0.06 0.06 0.06 0.05 0.04

7 Mach/equip 0.77 0.76 0.75 0.79 0.79 0.70 0.67 0.72 0.77 0.76

8 Misc manuf 0.04 0.04 0.05 0.05 0.06 0.07 0.08 0.09 0.08 0.07

9 Comm NES 0.03 0.03 0.03 0.02 0.02 0.03 0.03 0.02 0.02 0.02

Total US$ millions 3169.29 3775.61 4034.06 5746.97 6604.53 8190.83 7940.30 10330.72 8952.87 9060.00

Philippines

0 Food 0.13 0.12 0.16 0.12 0.13 0.12 0.13 0.10 0.09 0.09

1 Bev/tobacco 0.01 0.01 0.01 0.00 0.01 0.01 0.01 0.01 0.00 0.00

M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281 253

Table 2 (Continued )

Exports

to

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

2 Crude mat. 0.05 0.06 0.05 0.04 0.05 0.05 0.04 0.02 0.02 0.03

3 Mineral fuels 0.00 0.01 0.02 0.03 0.01 0.01 0.02 0.00 0.00 0.00

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.10 0.12 0.10 0.07 0.07 0.07 0.06 0.05 0.04 0.04

6 Manu goods 0.08 0.09 0.08 0.07 0.06 0.06 0.05 0.05 0.04 0.03

7 Mach/equip 0.53 0.48 0.48 0.58 0.59 0.60 0.63 0.68 0.72 0.74

8 Misc manuf 0.06 0.06 0.06 0.05 0.05 0.05 0.05 0.06 0.06 0.05

9 Comm NES 0.04 0.04 0.04 0.04 0.03 0.03 0.02 0.02 0.03 0.02

Total US$ millions 2435.13 2203.41 2679.40 3436.51 3750.57 5071.76 5822.95 7137.11 6736.17 7222.11

Thailand

0 Food 0.03 0.03 0.04 0.05 0.04 0.04 0.04 0.03 0.03 0.04

1 Bev/tobacco 0.02 0.02 0.02 0.02 0.02 0.01 0.01 0.01 0.01 0.01

2 Crude mat. 0.07 0.06 0.06 0.05 0.06 0.09 0.06 0.05 0.05 0.06

3 Mineral fuels 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.11 0.09 0.10 0.11 0.11 0.10 0.10 0.09 0.10 0.11

6 Manu goods 0.07 0.07 0.08 0.07 0.09 0.09 0.08 0.07 0.07 0.05

7 Mach/equip 0.59 0.63 0.62 0.56 0.53 0.53 0.57 0.61 0.62 0.61

8 Misc manuf 0.06 0.06 0.05 0.10 0.09 0.09 0.10 0.09 0.07 0.08

9 Comm NES 0.04 0.04 0.03 0.03 0.04 0.04 0.03 0.04 0.04 0.03

Total US$ millions 2853.30 3530.98 3769.91 3555.46 4624.00 6158.50 6934.91 7159.73 5233.36 4984.60

Viet Nam

0 Food 0.00 0.00 0.00 0.00 0.02 0.06 0.03 0.10 0.06 0.09

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.01 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.00 0.00 0.00 0.00 0.11 0.05 0.03 0.06 0.04 0.04

3 Mineral fuels 0.00 0.00 0.00 0.00 0.00 0.00 0.01 0.02 0.01 0.00

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.01 0.00 0.00 0.54 0.14 0.20 0.13 0.12 0.23 0.26

6 Manu goods 0.00 0.00 0.00 0.00 0.03 0.09 0.09 0.17 0.16 0.18

7 Mach/equip 0.05 0.03 0.03 0.05 0.64 0.51 0.68 0.42 0.41 0.33

8 Misc manuf 0.01 0.02 0.12 0.01 0.03 0.03 0.03 0.09 0.08 0.07

9 Comm NES 0.93 0.95 0.85 0.40 0.03 0.04 0.01 0.02 0.02 0.03

Total US$ millions 7.44 3.49 4.41 6.90 171.22 249.58 612.80 272.69 274.22 291.51

Singapore

0 Food 0.02 0.02 0.02 0.02 0.02 0.02 0.02 0.01 0.01 0.01

1 Bev/tobacco 0.02 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.00

2 Crude mat. 0.01 0.01 0.01 0.01 0.01 0.01 0.00 0.01 0.00 0.01

3 Mineral fuels 0.02 0.02 0.03 0.03 0.04 0.02 0.02 0.01 0.01 0.02

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.09 0.09 0.09 0.09 0.08 0.10 0.09 0.10 0.08 0.09

6 Manu goods 0.05 0.06 0.05 0.04 0.04 0.05 0.05 0.05 0.04 0.04

7 Mach/equip 0.62 0.60 0.59 0.62 0.64 0.63 0.63 0.63 0.69 0.66

8 Misc manuf 0.13 0.13 0.15 0.12 0.12 0.13 0.15 0.14 0.13 0.13

9 Comm NES 0.05 0.05 0.05 0.05 0.04 0.03 0.03 0.03 0.03 0.04

Total US$ millions 7597.41 8270.86 8948.11 10654.63 11713.58 13647.68 14677.03 15697.37 15673.48 16246.88

Hong Kong

0 Food 0.07 0.07 0.08 0.08 0.09 0.09 0.10 0.10 0.08 0.08

1 Bev/tobacco 0.09 0.05 0.05 0.03 0.02 0.02 0.02 0.01 0.01 0.01

2 Crude mat. 0.05 0.06 0.05 0.04 0.05 0.06 0.05 0.04 0.04 0.03

3 Mineral fuels 0.00 0.01 0.01 0.01 0.00 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.01 0.01 0.00

5 Chemicals 0.12 0.13 0.10 0.09 0.10 0.11 0.11 0.10 0.09 0.09

6 Manu goods 0.11 0.10 0.11 0.11 0.10 0.10 0.11 0.11 0.12 0.11

254 M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281

Table 2 (Continued )

Exports

to

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

7 Mach/equip 0.37 0.38 0.43 0.48 0.43 0.46 0.46 0.48 0.49 0.52

8 Misc manuf 0.08 0.07 0.08 0.10 0.09 0.09 0.09 0.10 0.11 0.12

9 Comm NES 0.10 0.13 0.10 0.06 0.11 0.07 0.04 0.04 0.03 0.03

Total US$ millions 6074.43 7348.24 8113.11 8711.88 10127.35 12704.14 12317.64 13674.39 12922.52 12650.95

South Korea

0 Food 0.09 0.06 0.08 0.06 0.07 0.09 0.10 0.07 0.08 0.08

1 Bev/tobacco 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.00 0.01

2 Crude mat. 0.21 0.17 0.17 0.17 0.14 0.13 0.10 0.10 0.10 0.07

3 Mineral fuels 0.05 0.04 0.05 0.04 0.03 0.03 0.03 0.03 0.02 0.02

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.01

5 Chemicals 0.12 0.11 0.10 0.12 0.11 0.11 0.10 0.10 0.10 0.09

6 Manu goods 0.07 0.09 0.07 0.06 0.06 0.07 0.06 0.06 0.05 0.04

7 Mach/equip 0.37 0.43 0.43 0.44 0.48 0.47 0.48 0.52 0.55 0.59

8 Misc manuf 0.06 0.06 0.07 0.08 0.08 0.07 0.08 0.08 0.07 0.07

9 Comm NES 0.03 0.03 0.03 0.03 0.03 0.03 0.03 0.03 0.04 0.03

Total US$ millions 14073.80 15196.80 14357.96 17499.13 24482.89 25433.22 24287.34 16538.27 22953.82

Taiwan

0 Food 0.09 0.09 0.08 0.08 0.08 0.09 0.11 0.08 0.06 0.07

1 Bev/tobacco 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.00

2 Crude mat. 0.11 0.11 0.08 0.08 0.08 0.09 0.09 0.08 0.06 0.05

3 Mineral fuels 0.04 0.04 0.03 0.03 0.02 0.02 0.02 0.01 0.01 0.01

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.14 0.14 0.14 0.13 0.15 0.16 0.14 0.13 0.11 0.12

6 Manu goods 0.08 0.08 0.06 0.06 0.06 0.07 0.06 0.06 0.05 0.04

7 Mach/equip 0.43 0.43 0.47 0.48 0.46 0.46 0.45 0.52 0.59 0.59

8 Misc manuf 0.05 0.05 0.05 0.06 0.06 0.06 0.07 0.07 0.08 0.09

9 Comm NES 0.04 0.04 0.07 0.07 0.07 0.05 0.05 0.04 0.04 0.03

Total US$ millions 11141.93 12697.48 15584.93 16240.13 18035.60 16920.28 18882.83 18157.13 19131.36

India

0 Food 0.03 0.04 0.05 0.06 0.04 0.03 0.03 0.03 0.03 0.03

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.17 0.09 0.12 0.05 0.09 0.12 0.07 0.04 0.04 0.04

3 Mineral fuels 0.04 0.12 0.04 0.03 0.02 0.03 0.02 0.02 0.02 0.02

4 Anim/veg oils 0.01 0.01 0.02 0.01 0.01 0.01 0.00 0.01 0.02 0.01

5 Chemicals 0.24 0.29 0.26 0.15 0.19 0.21 0.14 0.22 0.22 0.24

6 Manu goods 0.04 0.04 0.05 0.05 0.06 0.06 0.07 0.07 0.07 0.10

7 Mach/equip 0.33 0.30 0.34 0.57 0.49 0.44 0.55 0.48 0.48 0.45

8 Misc manuf 0.08 0.07 0.08 0.06 0.08 0.08 0.09 0.10 0.10 0.09

9 Comm NES 0.05 0.03 0.02 0.02 0.03 0.02 0.02 0.03 0.02 0.03

Total US$ millions 2411.49 1945.70 1846.31 2702.43 2212.11 3148.60 3204.98 3473.60 3544.68 3687.85

Pakistan

0 Food 0.12 0.14 0.30 0.18 0.28 0.31 0.25 0.34 0.21 0.13

1 Bev/tobacco 0.03 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.01 0.01

2 Crude mat. 0.05 0.05 0.06 0.06 0.08 0.18 0.05 0.04 0.05 0.05

3 Mineral fuels 0.00 0.09 0.02 0.04 0.00 0.00 0.00 0.00 0.00 0.02

4 Anim/veg oils 0.17 0.02 0.00 0.05 0.00 0.03 0.01 0.00 0.02 0.01

5 Chemicals 0.17 0.23 0.22 0.22 0.21 0.15 0.16 0.10 0.27 0.41

6 Manu goods 0.03 0.06 0.04 0.04 0.05 0.05 0.04 0.05 0.05 0.06

7 Mach/equip 0.25 0.26 0.28 0.34 0.30 0.22 0.40 0.37 0.33 0.25

8 Misc manuf 0.03 0.03 0.04 0.03 0.03 0.02 0.03 0.02 0.03 0.04

9 Comm NES 0.15 0.12 0.03 0.04 0.03 0.03 0.06 0.07 0.03 0.02

Total US$ millions 1128.95 936.32 869.31 788.28 709.78 927.10 1269.32 1226.76 726.25 496.68

M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281 255

Table 3

US imports from major developing Asian markets, 1990–1999

Import

to

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

China

0 Food 0.04 0.02 0.03 0.02 0.01 0.01 0.01 0.01 0.01 0.01

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.02 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01

3 Mineral fuels 0.04 0.03 0.02 0.01 0.01 0.01 0.01 0.01 0.01 0.00

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.02 0.02 0.02 0.02 0.02 0.02 0.02 0.02 0.02 0.02

6 Manu goods 0.10 0.10 0.09 0.09 0.09 0.10 0.09 0.09 0.10 0.10

7 Mach/equip 0.16 0.17 0.17 0.19 0.23 0.26 0.27 0.28 0.30 0.32

8 Misc manuf 0.62 0.64 0.65 0.66 0.62 0.58 0.58 0.57 0.54 0.52

9 Comm NES 0.01 0.01 0.02 0.01 0.01 0.01 0.01 0.01 0.01 0.01

Total US$ millions 16260.81 20276.39 27450.24 33673.22 41345.78 48505.59 54396.46 62532.15 75094.92 81776.20

Indonesia

0 Food 0.09 0.13 0.10 0.08 0.08 0.07 0.09 0.10 0.10 0.09

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.14 0.14 0.12 0.11 0.10 0.14 0.12 0.09 0.08 0.05

3 Mineral fuels 0.27 0.14 0.11 0.10 0.12 0.09 0.07 0.05 0.05 0.06

4 Anim/veg oils 0.01 0.00 0.01 0.01 0.01 0.00 0.01 0.01 0.01 0.01

5 Chemicals 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01

6 Manu goods 0.16 0.16 0.15 0.15 0.14 0.12 0.11 0.12 0.14 0.13

7 Mach/equip 0.01 0.04 0.08 0.11 0.14 0.16 0.18 0.20 0.21 0.24

8 Misc manuf 0.30 0.37 0.41 0.43 0.39 0.39 0.40 0.41 0.38 0.39

9 Comm NES 0.00 0.01 0.00 0.00 0.00 0.00 0.01 0.00 0.01 0.01

Total US$ millions 3681.36 3569.50 4914.13 5886.85 7020.22 7954.81 8742.58 9173.80 9973.03 9525.36

Malaysia

0 Food 0.02 0.02 0.02 0.01 0.01 0.01 0.00 0.01 0.01 0.01

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.04 0.03 0.02 0.02 0.02 0.02 0.02 0.01 0.01 0.01

3 Mineral fuels 0.06 0.02 0.01 0.00 0.00 0.00 0.01 0.01 0.01 0.01

4 Anim/veg oils 0.02 0.02 0.02 0.01 0.01 0.01 0.01 0.01 0.01 0.01

5 Chemicals 0.01 0.01 0.01 0.01 0.01 0.01 0.02 0.02 0.02 0.01

6 Manu goods 0.04 0.04 0.04 0.04 0.03 0.03 0.03 0.03 0.03 0.03

7 Mach/equip 0.61 0.65 0.69 0.73 0.75 0.78 0.76 0.77 0.77 0.80

8 Misc manuf 0.18 0.20 0.18 0.17 0.15 0.13 0.14 0.13 0.14 0.11

9 Comm NES 0.01 0.01 0.01 0.01 0.01 0.02 0.01 0.01 0.02 0.02

Total US$ millions 5496.11 6346.15 8594.72 10922.50 14418.62 17980.83 18330.71 18016.86 19518.78 21424.31

Philippines

0 Food 0.11 0.12 0.09 0.08 0.06 0.06 0.05 0.04 0.04 0.04

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.01 0.01 0.01 0.01 0.01 0.01 0.00 0.00 0.00 0.00

3 Mineral fuels 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.04 0.04 0.06 0.03 0.03 0.04 0.04 0.03 0.03 0.01

5 Chemicals 0.01 0.01 0.01 0.01 0.01 0.01 0.00 0.00 0.00 0.00

6 Manu goods 0.05 0.04 0.03 0.03 0.03 0.03 0.03 0.02 0.02 0.03

7 Mach/equip 0.29 0.32 0.34 0.39 0.43 0.47 0.55 0.63 0.63 0.66

8 Misc manuf 0.47 0.46 0.44 0.44 0.42 0.38 0.31 0.25 0.25 0.23

9 Comm NES 0.01 0.01 0.01 0.01 0.02 0.01 0.01 0.01 0.03 0.02

Total US$ millions 3622.51 3706.60 4623.00 5175.52 6025.15 7364.30 8496.43 10435.52 12334.75 12352.76

Thailand

0 Food 0.18 0.20 0.18 0.17 0.17 0.15 0.14 0.13 0.14 0.14

1 Bev/tobacco 0.00 0.00 0.01 0.00 0.00 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.02 0.02 0.02 0.02 0.03 0.04 0.03 0.03 0.02 0.02

256 M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281

Table 3 (Continued )

Import

to

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

3 Mineral fuels 0.02 0.02 0.00 0.01 0.01 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.00 0.00 0.00 0.00 0.00 0.01 0.01 0.01 0.01 0.01

6 Manu goods 0.11 0.11 0.10 0.10 0.09 0.08 0.08 0.08 0.09 0.10

7 Mach/equip 0.31 0.32 0.35 0.36 0.40 0.42 0.44 0.47 0.46 0.45

8 Misc manuf 0.32 0.31 0.32 0.32 0.29 0.29 0.28 0.27 0.27 0.27

9 Comm NES 0.01 0.01 0.01 0.01 0.01 0.01 0.02 0.02 0.01 0.01

Total US$ millions 5588.85 6447.44 7926.80 8982.30 10799.18 11854.39 11798.40 12595.02 13970.54 14329.88

Viet Nam

0 Food 0.00 0.00 0.00 0.00 0.82 0.84 0.51 0.54 0.49 0.48

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.00 0.00 0.00 0.00 0.01 0.01 0.00 0.01 0.01 0.01

3 Mineral fuels 0.00 0.00 0.00 0.00 0.03 0.00 0.25 0.09 0.20 0.17

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.03 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.00 0.00 0.00 0.00 0.00 0.01 0.00 0.00 0.00 0.00

6 Manu goods 0.00 0.00 0.00 0.00 0.01 0.01 0.01 0.01 0.02 0.02

7 Mach/equip 0.00 0.00 0.00 0.00 0.01 0.00 0.00 0.00 0.00 0.01

8 Misc manuf 0.00 0.00 0.00 0.00 0.07 0.11 0.21 0.33 0.26 0.31

9 Comm NES 0.00 0.00 0.00 0.00 0.01 0.01 0.02 0.02 0.02 0.01

Total US$ millions 0.00 0.00 0.00 0.00 54.62 210.02 341.69 388.19 596.05 608.34

Singapore

0 Food 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

3 Mineral fuels 0.02 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.04 0.05 0.05 0.04 0.04 0.03 0.03 0.04 0.02 0.03

6 Manu goods 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01

7 Mach/equip 0.77 0.78 0.79 0.81 0.83 0.86 0.87 0.86 0.85 0.82

8 Misc manuf 0.10 0.11 0.11 0.09 0.07 0.06 0.05 0.05 0.06 0.07

9 Comm NES 0.04 0.03 0.02 0.03 0.03 0.03 0.03 0.04 0.04 0.06

Total US$ millions 10095.28 10196.03 11560.07 13049.16 15656.27 18897.17 20648.26 20067.14 18653.95 18191.20

Hong Kong

0 Food 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

3 Mineral fuels 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.00 0.00 0.01 0.00 0.00 0.00 0.00 0.00 0.00 0.00

6 Manu goods 0.06 0.06 0.06 0.06 0.06 0.06 0.06 0.07 0.07 0.07

7 Mach/equip 0.23 0.22 0.22 0.24 0.24 0.27 0.27 0.28 0.24 0.22

8 Misc manuf 0.65 0.66 0.67 0.64 0.65 0.61 0.60 0.58 0.63 0.63

9 Comm NES 0.03 0.03 0.04 0.04 0.04 0.05 0.05 0.06 0.05 0.06

Total US$ millions 9950.55 9730.47 10265.15 10000.13 10141.44 10744.72 10261.98 10296.52 10934.99 10527.48

South Korea

0 Food 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.00

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.00 0.00 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.00

3 Mineral fuels 0.00 0.00 0.01 0.01 0.01 0.01 0.00 0.01 0.01 0.01

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.01 0.01 0.02 0.02 0.02 0.02 0.02 0.02 0.03 0.02

6 Manu goods 0.12 0.13 0.13 0.11 0.11 0.10 0.10 0.11 0.15 0.11

7 Mach/equip 0.40 0.42 0.45 0.51 0.59 0.68 0.68 0.68 0.61 0.69

M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281 257

shorter time span (5 years, from 1995 to 1999, corresponding to the most recent

enlargement of the EU to include Austria, Sweden, and Finland).

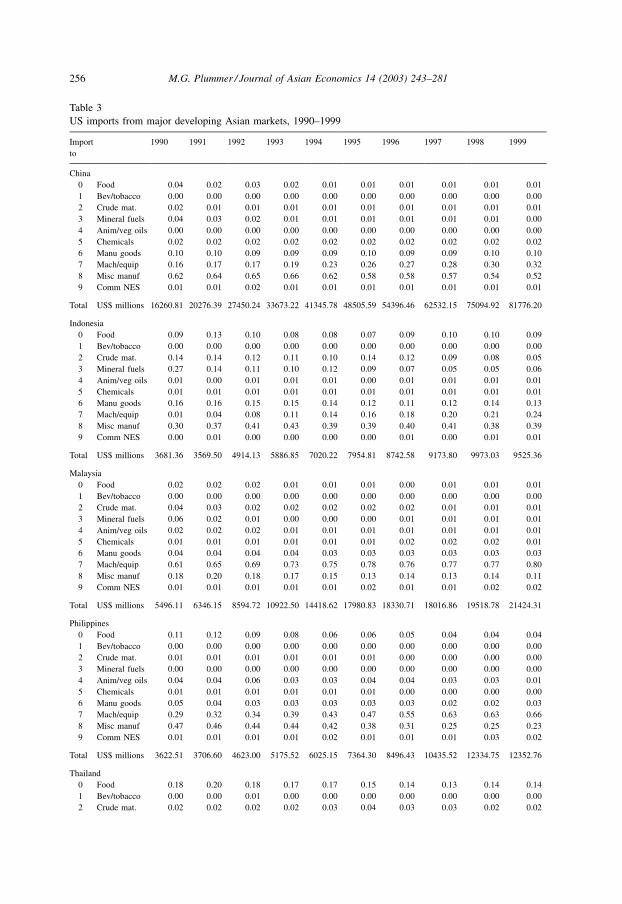

As Table 3 shows, US imports from developing Asian countries grew rapidly in all cases,

with the most impressive increases coming from the transitional economies of China and

Viet Nam. Chinese exports to the United States quadrupled from US$ 16 billion to US$ 82

billion, and exports from Viet Nam rose from 0 (due to the US embargo, discussed below)

as late as 1993 to US$ 608 million in 1999. Other countries also generally experienced high

growth rates, with the possible exception of already-important exporters to the United

States, such as Hong Kong, whose exports to the United States only grew by 6% but came

Table 3 (Continued )

Import

to

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

8 Misc manuf 0.44 0.41 0.38 0.32 0.24 0.18 0.16 0.15 0.16 0.14

9 Comm NES 0.01 0.01 0.01 0.01 0.01 0.01 0.02 0.02 0.02 0.02

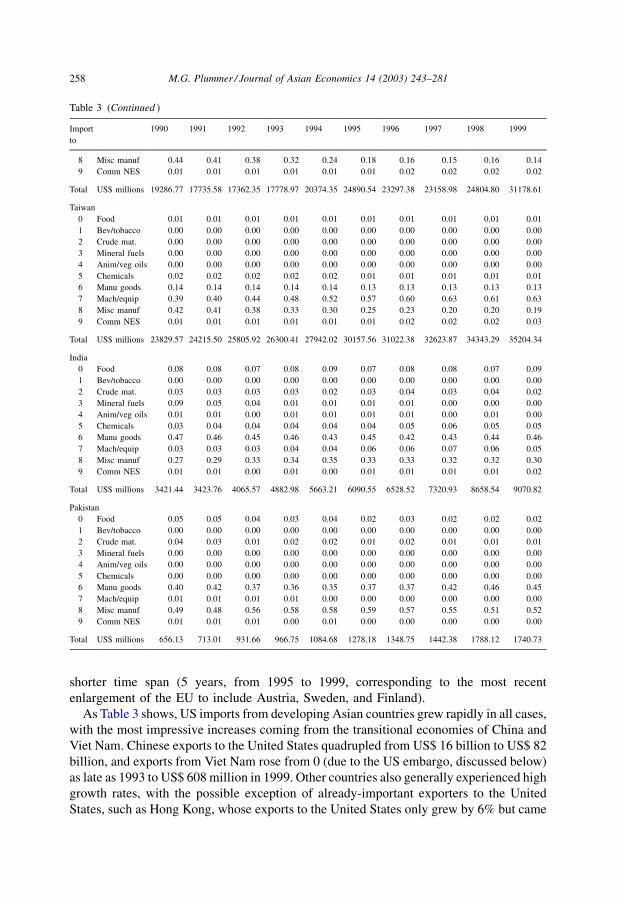

Total US$ millions 19286.77 17735.58 17362.35 17778.97 20374.35 24890.54 23297.38 23158.98 24804.80 31178.61

Taiwan

0 Food 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01 0.01

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

3 Mineral fuels 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.02 0.02 0.02 0.02 0.02 0.01 0.01 0.01 0.01 0.01

6 Manu goods 0.14 0.14 0.14 0.14 0.14 0.13 0.13 0.13 0.13 0.13

7 Mach/equip 0.39 0.40 0.44 0.48 0.52 0.57 0.60 0.63 0.61 0.63

8 Misc manuf 0.42 0.41 0.38 0.33 0.30 0.25 0.23 0.20 0.20 0.19

9 Comm NES 0.01 0.01 0.01 0.01 0.01 0.01 0.02 0.02 0.02 0.03

Total US$ millions 23829.57 24215.50 25805.92 26300.41 27942.02 30157.56 31022.38 32623.87 34343.29 35204.34

India

0 Food 0.08 0.08 0.07 0.08 0.09 0.07 0.08 0.08 0.07 0.09

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.03 0.03 0.03 0.03 0.02 0.03 0.04 0.03 0.04 0.02

3 Mineral fuels 0.09 0.05 0.04 0.01 0.01 0.01 0.01 0.00 0.00 0.00

4 Anim/veg oils 0.01 0.01 0.00 0.01 0.01 0.01 0.01 0.00 0.01 0.00

5 Chemicals 0.03 0.04 0.04 0.04 0.04 0.04 0.05 0.06 0.05 0.05

6 Manu goods 0.47 0.46 0.45 0.46 0.43 0.45 0.42 0.43 0.44 0.46

7 Mach/equip 0.03 0.03 0.03 0.04 0.04 0.06 0.06 0.07 0.06 0.05

8 Misc manuf 0.27 0.29 0.33 0.34 0.35 0.33 0.33 0.32 0.32 0.30

9 Comm NES 0.01 0.01 0.00 0.01 0.00 0.01 0.01 0.01 0.01 0.02

Total US$ millions 3421.44 3423.76 4065.57 4882.98 5663.21 6090.55 6528.52 7320.93 8658.54 9070.82

Pakistan

0 Food 0.05 0.05 0.04 0.03 0.04 0.02 0.03 0.02 0.02 0.02

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.04 0.03 0.01 0.02 0.02 0.01 0.02 0.01 0.01 0.01

3 Mineral fuels 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

6 Manu goods 0.40 0.42 0.37 0.36 0.35 0.37 0.37 0.42 0.46 0.45

7 Mach/equip 0.01 0.01 0.01 0.01 0.00 0.00 0.00 0.00 0.00 0.00

8 Misc manuf 0.49 0.48 0.56 0.58 0.58 0.59 0.57 0.55 0.51 0.52

9 Comm NES 0.01 0.01 0.01 0.00 0.01 0.00 0.00 0.00 0.00 0.00

Total US$ millions 656.13 713.01 931.66 966.75 1084.68 1278.18 1348.75 1442.38 1788.12 1740.73

258 M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281

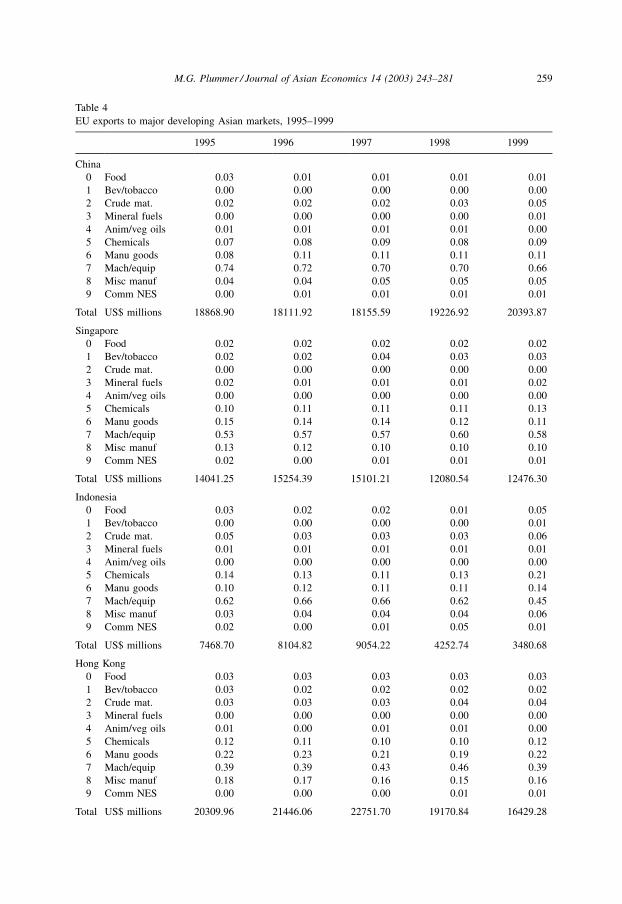

Table 4

EU exports to major developing Asian markets, 1995–1999

1995 1996 1997 1998 1999

China

0 Food 0.03 0.01 0.01 0.01 0.01

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.02 0.02 0.02 0.03 0.05

3 Mineral fuels 0.00 0.00 0.00 0.00 0.01

4 Anim/veg oils 0.01 0.01 0.01 0.01 0.00

5 Chemicals 0.07 0.08 0.09 0.08 0.09

6 Manu goods 0.08 0.11 0.11 0.11 0.11

7 Mach/equip 0.74 0.72 0.70 0.70 0.66

8 Misc manuf 0.04 0.04 0.05 0.05 0.05

9 Comm NES 0.00 0.01 0.01 0.01 0.01

Total US$ millions 18868.90 18111.92 18155.59 19226.92 20393.87

Singapore

0 Food 0.02 0.02 0.02 0.02 0.02

1 Bev/tobacco 0.02 0.02 0.04 0.03 0.03

2 Crude mat. 0.00 0.00 0.00 0.00 0.00

3 Mineral fuels 0.02 0.01 0.01 0.01 0.02

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.10 0.11 0.11 0.11 0.13

6 Manu goods 0.15 0.14 0.14 0.12 0.11

7 Mach/equip 0.53 0.57 0.57 0.60 0.58

8 Misc manuf 0.13 0.12 0.10 0.10 0.10

9 Comm NES 0.02 0.00 0.01 0.01 0.01

Total US$ millions 14041.25 15254.39 15101.21 12080.54 12476.30

Indonesia

0 Food 0.03 0.02 0.02 0.01 0.05

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.01

2 Crude mat. 0.05 0.03 0.03 0.03 0.06

3 Mineral fuels 0.01 0.01 0.01 0.01 0.01

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.14 0.13 0.11 0.13 0.21

6 Manu goods 0.10 0.12 0.11 0.11 0.14

7 Mach/equip 0.62 0.66 0.66 0.62 0.45

8 Misc manuf 0.03 0.04 0.04 0.04 0.06

9 Comm NES 0.02 0.00 0.01 0.05 0.01

Total US$ millions 7468.70 8104.82 9054.22 4252.74 3480.68

Hong Kong

0 Food 0.03 0.03 0.03 0.03 0.03

1 Bev/tobacco 0.03 0.02 0.02 0.02 0.02

2 Crude mat. 0.03 0.03 0.03 0.04 0.04

3 Mineral fuels 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.01 0.00 0.01 0.01 0.00

5 Chemicals 0.12 0.11 0.10 0.10 0.12

6 Manu goods 0.22 0.23 0.21 0.19 0.22

7 Mach/equip 0.39 0.39 0.43 0.46 0.39

8 Misc manuf 0.18 0.17 0.16 0.15 0.16

9 Comm NES 0.00 0.00 0.00 0.01 0.01

Total US$ millions 20309.96 21446.06 22751.70 19170.84 16429.28

M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281 259

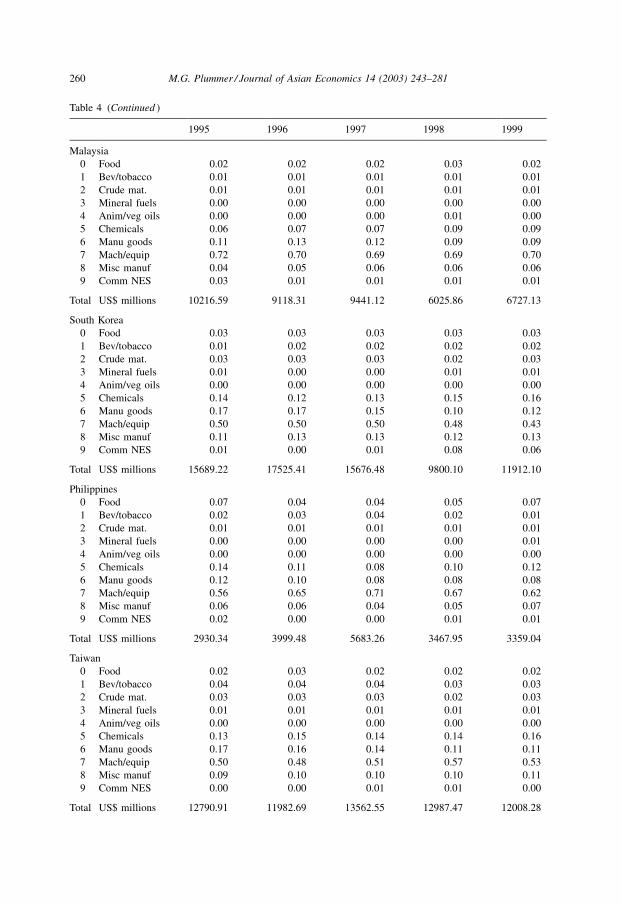

Table 4 (Continued )

1995 1996 1997 1998 1999

Malaysia

0 Food 0.02 0.02 0.02 0.03 0.02

1 Bev/tobacco 0.01 0.01 0.01 0.01 0.01

2 Crude mat. 0.01 0.01 0.01 0.01 0.01

3 Mineral fuels 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.00 0.00 0.00 0.01 0.00

5 Chemicals 0.06 0.07 0.07 0.09 0.09

6 Manu goods 0.11 0.13 0.12 0.09 0.09

7 Mach/equip 0.72 0.70 0.69 0.69 0.70

8 Misc manuf 0.04 0.05 0.06 0.06 0.06

9 Comm NES 0.03 0.01 0.01 0.01 0.01

Total US$ millions 10216.59 9118.31 9441.12 6025.86 6727.13

South Korea

0 Food 0.03 0.03 0.03 0.03 0.03

1 Bev/tobacco 0.01 0.02 0.02 0.02 0.02

2 Crude mat. 0.03 0.03 0.03 0.02 0.03

3 Mineral fuels 0.01 0.00 0.00 0.01 0.01

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.14 0.12 0.13 0.15 0.16

6 Manu goods 0.17 0.17 0.15 0.10 0.12

7 Mach/equip 0.50 0.50 0.50 0.48 0.43

8 Misc manuf 0.11 0.13 0.13 0.12 0.13

9 Comm NES 0.01 0.00 0.01 0.08 0.06

Total US$ millions 15689.22 17525.41 15676.48 9800.10 11912.10

Philippines

0 Food 0.07 0.04 0.04 0.05 0.07

1 Bev/tobacco 0.02 0.03 0.04 0.02 0.01

2 Crude mat. 0.01 0.01 0.01 0.01 0.01

3 Mineral fuels 0.00 0.00 0.00 0.00 0.01

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.14 0.11 0.08 0.10 0.12

6 Manu goods 0.12 0.10 0.08 0.08 0.08

7 Mach/equip 0.56 0.65 0.71 0.67 0.62

8 Misc manuf 0.06 0.06 0.04 0.05 0.07

9 Comm NES 0.02 0.00 0.00 0.01 0.01

Total US$ millions 2930.34 3999.48 5683.26 3467.95 3359.04

Taiwan

0 Food 0.02 0.03 0.02 0.02 0.02

1 Bev/tobacco 0.04 0.04 0.04 0.03 0.03

2 Crude mat. 0.03 0.03 0.03 0.02 0.03

3 Mineral fuels 0.01 0.01 0.01 0.01 0.01

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.13 0.15 0.14 0.14 0.16

6 Manu goods 0.17 0.16 0.14 0.11 0.11

7 Mach/equip 0.50 0.48 0.51 0.57 0.53

8 Misc manuf 0.09 0.10 0.10 0.10 0.11

9 Comm NES 0.00 0.00 0.01 0.01 0.00

Total US$ millions 12790.91 11982.69 13562.55 12987.47 12008.28

260 M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281

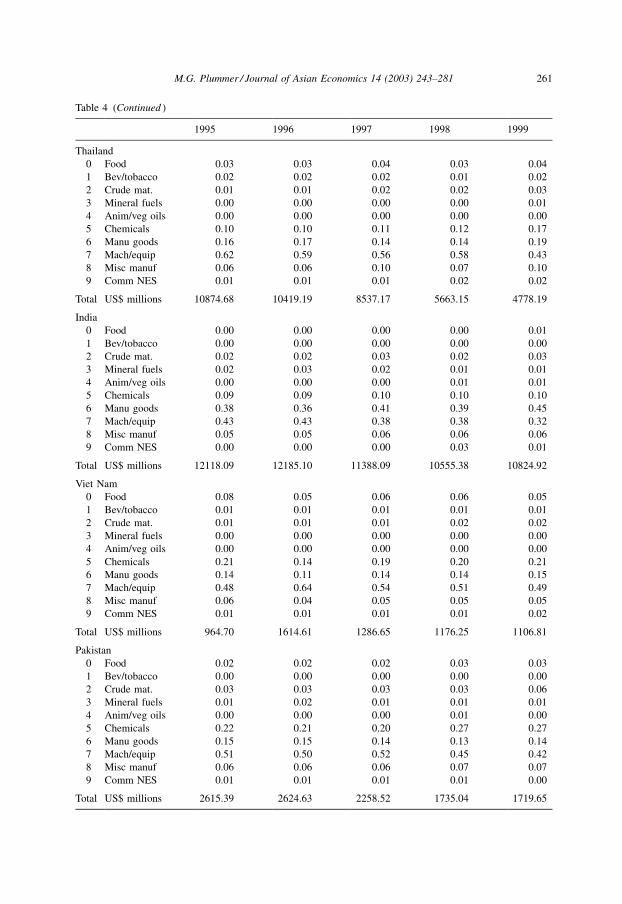

Table 4 (Continued )

1995 1996 1997 1998 1999

Thailand

0 Food 0.03 0.03 0.04 0.03 0.04

1 Bev/tobacco 0.02 0.02 0.02 0.01 0.02

2 Crude mat. 0.01 0.01 0.02 0.02 0.03

3 Mineral fuels 0.00 0.00 0.00 0.00 0.01

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.10 0.10 0.11 0.12 0.17

6 Manu goods 0.16 0.17 0.14 0.14 0.19

7 Mach/equip 0.62 0.59 0.56 0.58 0.43

8 Misc manuf 0.06 0.06 0.10 0.07 0.10

9 Comm NES 0.01 0.01 0.01 0.02 0.02

Total US$ millions 10874.68 10419.19 8537.17 5663.15 4778.19

India

0 Food 0.00 0.00 0.00 0.00 0.01

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.02 0.02 0.03 0.02 0.03

3 Mineral fuels 0.02 0.03 0.02 0.01 0.01

4 Anim/veg oils 0.00 0.00 0.00 0.01 0.01

5 Chemicals 0.09 0.09 0.10 0.10 0.10

6 Manu goods 0.38 0.36 0.41 0.39 0.45

7 Mach/equip 0.43 0.43 0.38 0.38 0.32

8 Misc manuf 0.05 0.05 0.06 0.06 0.06

9 Comm NES 0.00 0.00 0.00 0.03 0.01

Total US$ millions 12118.09 12185.10 11388.09 10555.38 10824.92

Viet Nam

0 Food 0.08 0.05 0.06 0.06 0.05

1 Bev/tobacco 0.01 0.01 0.01 0.01 0.01

2 Crude mat. 0.01 0.01 0.01 0.02 0.02

3 Mineral fuels 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.21 0.14 0.19 0.20 0.21

6 Manu goods 0.14 0.11 0.14 0.14 0.15

7 Mach/equip 0.48 0.64 0.54 0.51 0.49

8 Misc manuf 0.06 0.04 0.05 0.05 0.05

9 Comm NES 0.01 0.01 0.01 0.01 0.02

Total US$ millions 964.70 1614.61 1286.65 1176.25 1106.81

Pakistan

0 Food 0.02 0.02 0.02 0.03 0.03

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.03 0.03 0.03 0.03 0.06

3 Mineral fuels 0.01 0.02 0.01 0.01 0.01

4 Anim/veg oils 0.00 0.00 0.00 0.01 0.00

5 Chemicals 0.22 0.21 0.20 0.27 0.27

6 Manu goods 0.15 0.15 0.14 0.13 0.14

7 Mach/equip 0.51 0.50 0.52 0.45 0.42

8 Misc manuf 0.06 0.06 0.06 0.07 0.07

9 Comm NES 0.01 0.01 0.01 0.01 0.00

Total US$ millions 2615.39 2624.63 2258.52 1735.04 1719.65

M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281 261

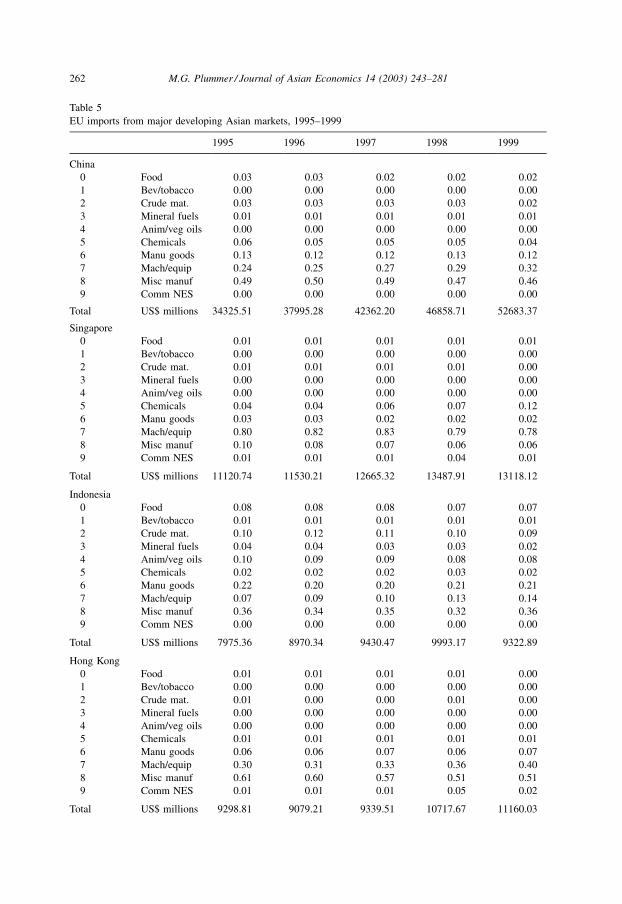

Table 5

EU imports from major developing Asian markets, 1995–1999

1995 1996 1997 1998 1999

China

0 Food 0.03 0.03 0.02 0.02 0.02

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.03 0.03 0.03 0.03 0.02

3 Mineral fuels 0.01 0.01 0.01 0.01 0.01

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.06 0.05 0.05 0.05 0.04

6 Manu goods 0.13 0.12 0.12 0.13 0.12

7 Mach/equip 0.24 0.25 0.27 0.29 0.32

8 Misc manuf 0.49 0.50 0.49 0.47 0.46

9 Comm NES 0.00 0.00 0.00 0.00 0.00

Total US$ millions 34325.51 37995.28 42362.20 46858.71 52683.37

Singapore

0 Food 0.01 0.01 0.01 0.01 0.01

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.01 0.01 0.01 0.01 0.00

3 Mineral fuels 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.04 0.04 0.06 0.07 0.12

6 Manu goods 0.03 0.03 0.02 0.02 0.02

7 Mach/equip 0.80 0.82 0.83 0.79 0.78

8 Misc manuf 0.10 0.08 0.07 0.06 0.06

9 Comm NES 0.01 0.01 0.01 0.04 0.01

Total US$ millions 11120.74 11530.21 12665.32 13487.91 13118.12

Indonesia

0 Food 0.08 0.08 0.08 0.07 0.07

1 Bev/tobacco 0.01 0.01 0.01 0.01 0.01

2 Crude mat. 0.10 0.12 0.11 0.10 0.09

3 Mineral fuels 0.04 0.04 0.03 0.03 0.02

4 Anim/veg oils 0.10 0.09 0.09 0.08 0.08

5 Chemicals 0.02 0.02 0.02 0.03 0.02

6 Manu goods 0.22 0.20 0.20 0.21 0.21

7 Mach/equip 0.07 0.09 0.10 0.13 0.14

8 Misc manuf 0.36 0.34 0.35 0.32 0.36

9 Comm NES 0.00 0.00 0.00 0.00 0.00

Total US$ millions 7975.36 8970.34 9430.47 9993.17 9322.89

Hong Kong

0 Food 0.01 0.01 0.01 0.01 0.00

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.01 0.00 0.00 0.01 0.00

3 Mineral fuels 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.01 0.01 0.01 0.01 0.01

6 Manu goods 0.06 0.06 0.07 0.06 0.07

7 Mach/equip 0.30 0.31 0.33 0.36 0.40

8 Misc manuf 0.61 0.60 0.57 0.51 0.51

9 Comm NES 0.01 0.01 0.01 0.05 0.02

Total US$ millions 9298.81 9079.21 9339.51 10717.67 11160.03

262 M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281

Table 5 (Continued )

1995 1996 1997 1998 1999

Malaysia

0 Food 0.03 0.03 0.02 0.02 0.02

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.08 0.07 0.07 0.05 0.05

3 Mineral fuels 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.04 0.04 0.04 0.06 0.05

5 Chemicals 0.02 0.02 0.02 0.02 0.02

6 Manu goods 0.07 0.06 0.06 0.06 0.05

7 Mach/equip 0.61 0.63 0.65 0.67 0.69

8 Misc manuf 0.13 0.13 0.14 0.12 0.12

9 Comm NES 0.00 0.00 0.00 0.00 0.00

Total US$ millions 11767.59 11619.13 11650.56 13452.02 13446.17

South Korea

0 Food 0.01 0.01 0.01 0.01 0.01

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.01 0.01 0.01 0.01 0.01

3 Mineral fuels 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.06 0.05 0.06 0.06 0.04

6 Manu goods 0.11 0.11 0.12 0.14 0.12

7 Mach/equip 0.68 0.68 0.69 0.67 0.72

8 Misc manuf 0.13 0.12 0.11 0.09 0.09

9 Comm NES 0.00 0.01 0.01 0.02 0.01

Total US$ millions 14213.46 13965.97 14816.18 17883.30 19251.45

Philippines

0 Food 0.06 0.05 0.04 0.03 0.03

1 Bev/tobacco 0.01 0.00 0.00 0.00 0.00

2 Crude mat. 0.04 0.04 0.05 0.03 0.02

3 Mineral fuels 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.11 0.07 0.04 0.05 0.03

5 Chemicals 0.01 0.01 0.00 0.00 0.00

6 Manu goods 0.05 0.05 0.04 0.03 0.03

7 Mach/equip 0.39 0.50 0.59 0.70 0.75

8 Misc manuf 0.27 0.22 0.21 0.13 0.12

9 Comm NES 0.05 0.05 0.03 0.03 0.01

Total US$ millions 3027.56 3802.82 4240.09 6157.97 6007.89

Taiwan

0 Food 0.00 0.00 0.00 0.01 0.00

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.01 0.01 0.01 0.01 0.00

3 Mineral fuels 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.03 0.02 0.02 0.02 0.02

6 Manu goods 0.15 0.14 0.14 0.15 0.13

7 Mach/equip 0.62 0.66 0.66 0.67 0.69

8 Misc manuf 0.18 0.17 0.17 0.15 0.16

9 Comm NES 0.00 0.00 0.00 0.00 0.00

Total US$ millions 15129.97 16541.91 17492.46 19833.09 20764.95

M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281 263

Table 5 (Continued )

1995 1996 1997 1998 1999

Thailand

0 Food 0.16 0.17 0.15 0.15 0.14

1 Bev/tobacco 0.00 0.01 0.00 0.00 0.00

2 Crude mat. 0.05 0.05 0.04 0.03 0.03

3 Mineral fuels 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.01 0.01 0.01 0.02 0.02

6 Manu goods 0.16 0.14 0.14 0.14 0.13

7 Mach/equip 0.32 0.37 0.39 0.41 0.44

8 Misc manuf 0.29 0.25 0.24 0.23 0.23

9 Comm NES 0.01 0.00 0.03 0.02 0.00

Total US$ millions 8474.13 9419.19 9492.54 10218.36 10449.04

India

0 Food 0.09 0.10 0.10 0.08 0.09

1 Bev/tobacco 0.00 0.00 0.01 0.01 0.00

2 Crude mat. 0.04 0.04 0.05 0.05 0.05

3 Mineral fuels 0.01 0.01 0.00 0.00 0.00

4 Anim/veg oils 0.01 0.01 0.01 0.01 0.01

5 Chemicals 0.07 0.07 0.08 0.08 0.08

6 Manu goods 0.37 0.36 0.37 0.39 0.37

7 Mach/equip 0.07 0.09 0.10 0.09 0.10

8 Misc manuf 0.34 0.31 0.29 0.29 0.30

9 Comm NES 0.00 0.00 0.00 0.00 0.00

Total US$ millions 10110.23 10837.40 10720.28 10954.07 10655.45

Viet Nam

0 Food 0.21 0.13 0.15 0.17 0.14

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.02 0.01 0.01 0.01 0.01

3 Mineral fuels 0.02 0.01 0.01 0.01 0.01

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.01 0.01 0.01 0.01 0.00

6 Manu goods 0.06 0.06 0.06 0.06 0.07

7 Mach/equip 0.01 0.01 0.02 0.03 0.03

8 Misc manuf 0.68 0.77 0.75 0.71 0.73

9 Comm NES 0.00 0.00 0.00 0.00 0.00

Total US$ millions 1503.97 1818.78 2545.47 2922.20 3360.80

Pakistan

0 Food 0.08 0.06 0.07 0.08 0.07

1 Bev/tobacco 0.00 0.00 0.00 0.00 0.00

2 Crude mat. 0.04 0.05 0.04 0.04 0.03

3 Mineral fuels 0.00 0.00 0.00 0.00 0.00

4 Anim/veg oils 0.00 0.00 0.00 0.00 0.00

5 Chemicals 0.00 0.00 0.00 0.00 0.00

6 Manu goods 0.45 0.46 0.46 0.47 0.47

7 Mach/equip 0.01 0.01 0.02 0.02 0.02

8 Misc manuf 0.41 0.41 0.41 0.40 0.41

9 Comm NES 0.00 0.00 0.00 0.00 0.00

Total US$ millions 2579.30 2616.30 2586.06 2601.13 2366.14

264 M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281

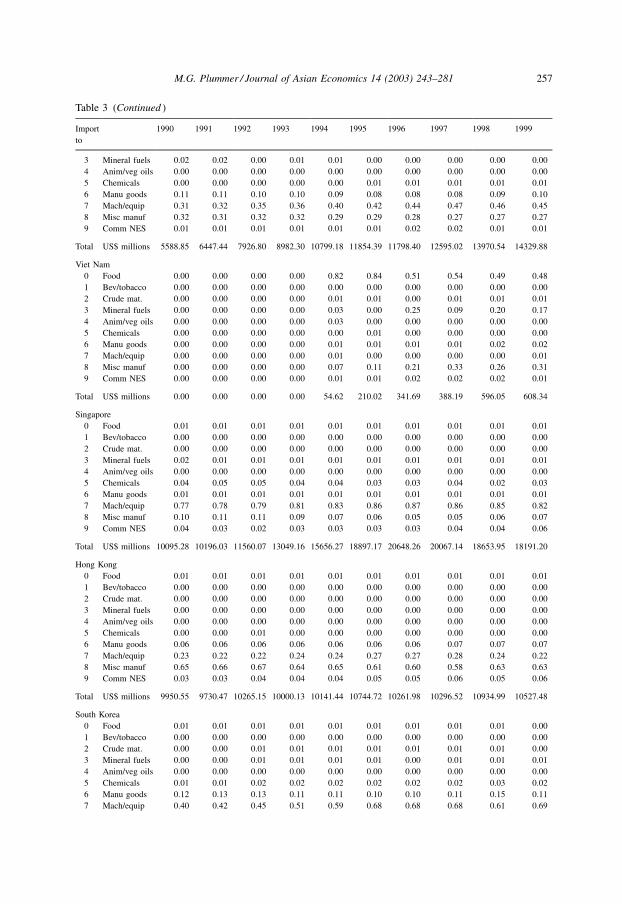

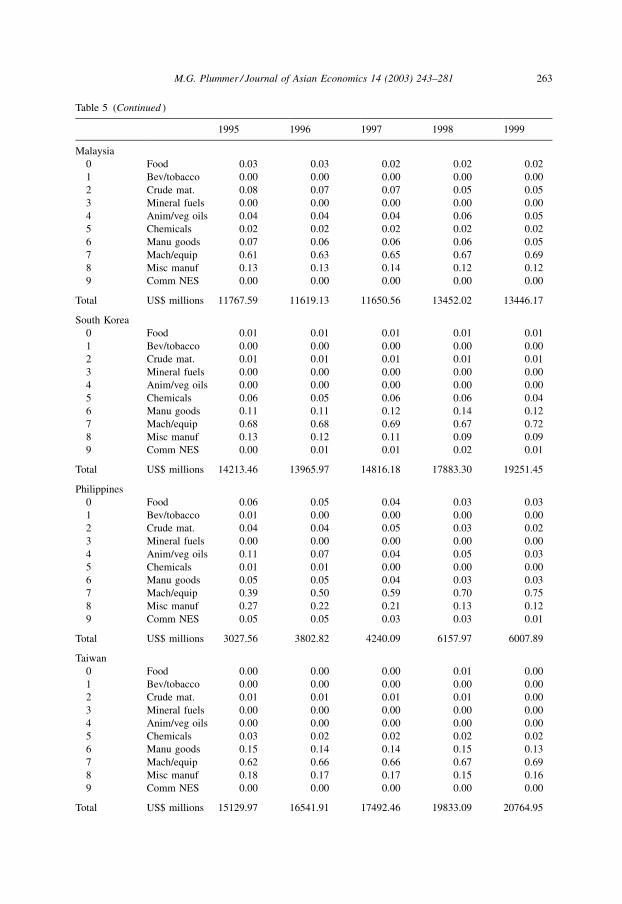

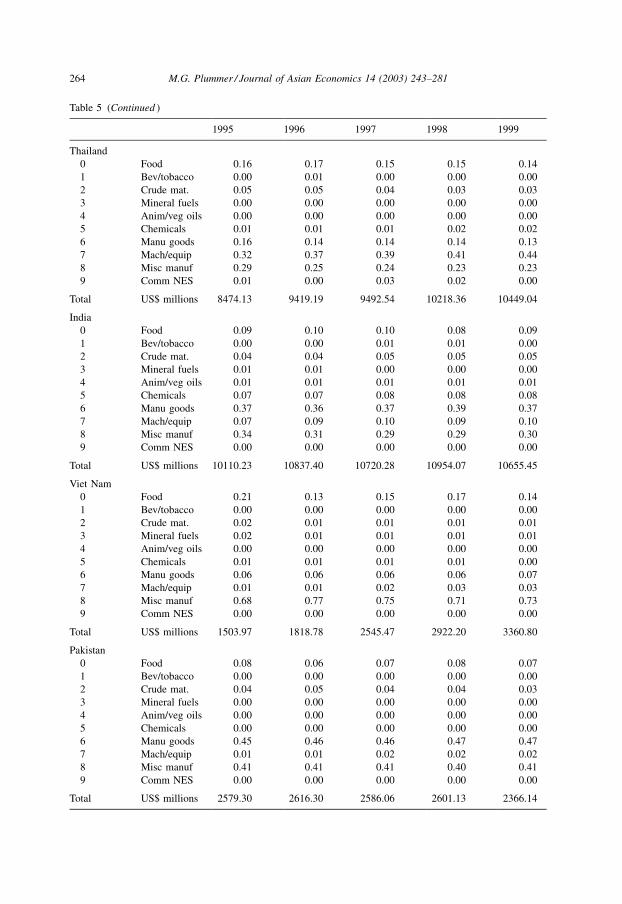

to US$ 11 billion in 1999. Regarding changes in the structure of these imports, SITC 7, as

expected, dominates in almost all markets, with shares that are generally significantly

higher than in 1990. In fact, in 1999 SITC 7 constituted over three-fourths of all imports

from Malaysia and Singapore, and two-thirds of imports from the Philippines, South Korea

and Taiwan. Where shares are relatively low in East Asia (i.e. China, Indonesia, and Viet

Nam), they have risen considerably over time, for example doubling in the case of China

and increasing by 24-fold in the case of Indonesia.10 Only in India and Pakistan do SITC 7

exports appear to be insignificant.

As is apparent in Table 5, a similar but generally less-pronounced trend is in evidence

over the mid-late 1990s in the case of Asian exports to the EU, where SITC 7 also made

important gains in bilateral export structures. The share of SITC 7 in East Asian exports

was almost always higher in the case of the United States, with the exception of Hong

Kong.

It is interesting to note that, in the case of both the United States (Table 2) and the EU

(Table 4), East Asian imports also showed an increase in the share of more sophisticated

commodities, with SITC 7 generally becoming more important over time. For example, the

share of SITC 7 exports from the United States rose in all countries save Malaysia, where it

stayed the same (at a dominant 77%). Even the shares in the less-developed countries such

as India, Pakistan and Viet Nam saw these shares increase substantially, though the levels

were still relatively low in these countries.

It isnocoincidence thatexportsandimports tendtoshowthesameevolution.Thetraditional

explanation would be that the structure of exports and imports are both correlated with per

capita income; the more developed the country, the greater the share of sophisticated exports

generated from a more sophisticated economy, and the more sophisticated are the tastes of the

population (and, hence, imports tend to be more sophisticated). But with the increasing global

division of labor, a country’s imports may end up as its exports with a small amount of value

added.Directforeigninvestment(DFI)playsanimportantroleinthisprocess; indeed,asiswell

documented in the literature (e.g. Lee & Roland-Holst, 1999), the trade–DFI link is not only

important but in some cases dominating, a result that would be congruent with Tamamura

(2002). In addition, the economic literature is increasingly respecting the important role that

imports play in the process of technology transfer.

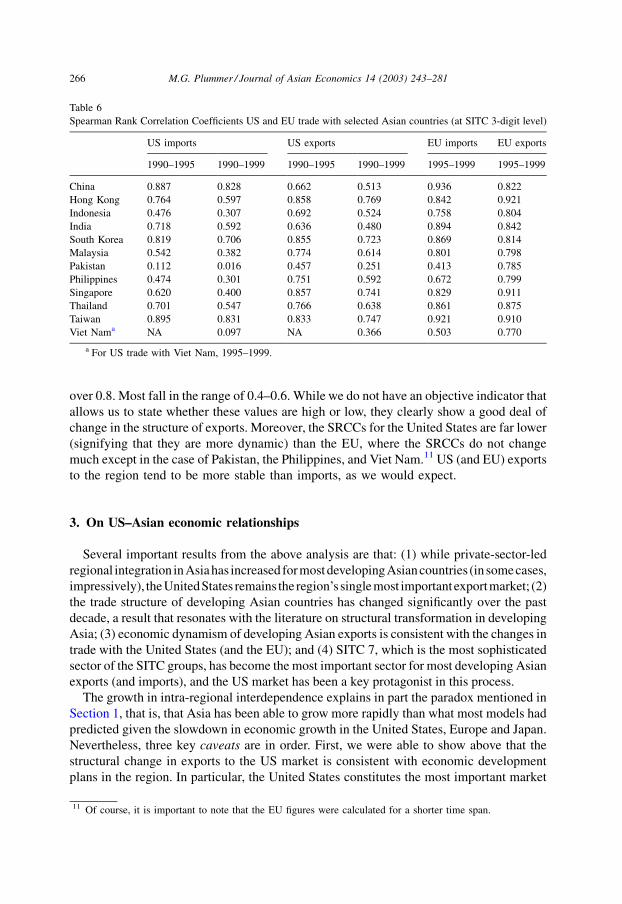

Finally, in order to get a better idea of the dynamism of US trade with Asia, we calculate

Spearman Rank Correlation Coefficients (SRCCs) to capture changes in trade structure over

time(Table6).TheSRCCisanon-parametricestimate, showinghowtherankingsoftwoseries

are correlated with each other. The estimates range from �1 to þ1: perfect rank correlation

would be unity in absolute value, while complete lack of correlation would be zero. Here, we

rank exports (imports) according to their importance between two years (1990 and 1995, 1990

and 1999 for the United States; 1995 and 1999 for the EU) to capture this effect. The lower the

SRCC,thegreater thechangeinexport(import)structure.Asthere isaclearaggregationbias in

such calculations, we undertake this exercise at the three-digit SITC level.

As expected, US imports from developing Asia display a considerable amount of

structural change in all cases save China and Taiwan, where the SRCCs are fairly high at

10 The case of Hong Kong is difficult to decipher, as its role as a key entrepot center increased substantially

with its economic and political integration with China.

M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281 265

over 0.8. Most fall in the range of 0.4–0.6. While we do not have an objective indicator that

allows us to state whether these values are high or low, they clearly show a good deal of

change in the structure of exports. Moreover, the SRCCs for the United States are far lower

(signifying that they are more dynamic) than the EU, where the SRCCs do not change

much except in the case of Pakistan, the Philippines, and Viet Nam.11 US (and EU) exports

to the region tend to be more stable than imports, as we would expect.

3. On US–Asian economic relationships

Several important results from the above analysis are that: (1) while private-sector-led

regional integration inAsiahas increased formostdeveloping Asiancountries (in somecases,

impressively), theUnitedStates remains the region’s singlemost importantexportmarket; (2)

the trade structure of developing Asian countries has changed significantly over the past

decade, a result that resonates with the literature on structural transformation in developing

Asia; (3) economic dynamism of developing Asian exports is consistent with the changes in

trade with the United States (and the EU); and (4) SITC 7, which is the most sophisticated

sector of the SITC groups, has become the most important sector for most developing Asian

exports (and imports), and the US market has been a key protagonist in this process.

The growth in intra-regional interdependence explains in part the paradox mentioned in

Section 1, that is, that Asia has been able to grow more rapidly than what most models had

predicted given the slowdown in economic growth in the United States, Europe and Japan.

Nevertheless, three key caveats are in order. First, we were able to show above that the

structural change in exports to the US market is consistent with economic development

plans in the region. In particular, the United States constitutes the most important market

Table 6

Spearman Rank Correlation Coefficients US and EU trade with selected Asian countries (at SITC 3-digit level)

US imports US exports EU imports EU exports

1990–1995 1990–1999 1990–1995 1990–1999 1995–1999 1995–1999

China 0.887 0.828 0.662 0.513 0.936 0.822

Hong Kong 0.764 0.597 0.858 0.769 0.842 0.921

Indonesia 0.476 0.307 0.692 0.524 0.758 0.804

India 0.718 0.592 0.636 0.480 0.894 0.842

South Korea 0.819 0.706 0.855 0.723 0.869 0.814

Malaysia 0.542 0.382 0.774 0.614 0.801 0.798

Pakistan 0.112 0.016 0.457 0.251 0.413 0.785

Philippines 0.474 0.301 0.751 0.592 0.672 0.799

Singapore 0.620 0.400 0.857 0.741 0.829 0.911

Thailand 0.701 0.547 0.766 0.638 0.861 0.875

Taiwan 0.895 0.831 0.833 0.747 0.921 0.910

Viet Nama NA 0.097 NA 0.366 0.503 0.770

a For US trade with Viet Nam, 1995–1999.

11 Of course, it is important to note that the EU figures were calculated for a shorter time span.

266 M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281

for SITC 7 items. Tamamura’s (2002) results, reviewed above, show that an impressive

amount of growth in this sector has been spurred by demand-side considerations in the US

market. Hence, the United States market continues to be important not only in terms of

quantity but also quality. Moreover, it is important to point out that while Asian countries

have grown faster than what was predicted, growth has still slowed at least in part due to the

generally poor performance of the US economy. Indeed, Singapore, the most open market

in the region (along with Hong Kong) and having two-thirds of its exports falling under

SITC 7, actually experienced a strong recession in 2001.

Second, while it has been shown that there is a tendency for the price of manufactures

relative to that of primary products to rise, relative prices within manufactures continue to

be quite volatile. Indeed, the prices of many electronics-related products have been subject

to considerable oscillations. For example, as is pointed out in Kim, Ayhan Kose, and

Plummer (2001), a key terms of trade shock contributing to the Asian Crisis was the fall in

certain electronics prices, including a precipitous decline in DRAM prices.

Third, while intra-regional trade has been increasing, there is no evidence that intra-

regional financial transactions have risen, at a time when finance has been shown to be the

Achilles’ Heel of regional development. Indeed, Japan has become a less important actor in

supplying DFI to developing Asia (indeed, for the first time, Japan is becoming an

important recipient of global DFI inflows), while the United States and Europe continue to

increase their DFI flows to the region at fairly robust rates (Kreinin & Plummer, 2003). This

is not only true at the regional level but also globally. For example, in 2000, US and EU DFI

outflows came to US$ 139 billion and US$ 773 billion, respectively, whereas Japanese DFI

outflows came to only US$ 33 billion.12 Moreover, while reliable data on bilateral financial

flows by type are difficult to come by, it is clear that external financial intermediation of

developing Asia countries tends to take place principally in the United States, followed by

the EU and Japan. Some speak of a resurgence in EU finance once markets become more

comfortable with the euro, an argument that might be supported by the strong appreciation

of the euro over 2002 and early 2003. However, a resurgence in Japanese finance does not

seem to be on the radar screen in the short-medium run, given the financial crisis in the

country as well as relatively-closed (though obviously opening), illiquid financial markets.

Hence, the region will continue to be exposed to the vicissitudes of the US (and, potentially,

EU) financial markets.

This brings us to a fourth (and related) caveat: there is some question as to the

sustainability of the US current account deficit. Economists have been increasingly asking

the question of whether or not the United States can continue to run current account deficits

of 4% of GDP. The United States has had large current account deficits essentially for the

past two decades; the flip-side of these deficits is the huge increase in the holdings of US

financial assets, particularly sovereign debt, in foreign hands. If, indeed, the US economy

can sustain large current account deficits over the medium-long-term (a prospect that many

economists doubt), it may very well be that its politics cannot. Moreover, this large

proportion of liquid debt in the hands of non-residents creates, ceteris paribus, a greater

potential for wide swings in the dollar and/or crisis. Hence, even if the economy could take

it, the markets may not believe it.

12 UNCTAD (2003).

M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281 267

Does this leave the dollar exposed to a crisis? Such an expenditure-switching policy

might have an important bearing on the US trade balance through the relative price effect

on tradable and non-tradable goods, but it could lead to significant negative consequence

for Asian exports to the United States. While most Asian developing countries do have

managed floats or even exchange-rate pegs, the role of the dollar has been declining in most

of these targeting schemes. Hence, a fall in the dollar could affect the competitiveness of

Asian exports to the US market (and other markets as well), especially since these countries

increasingly compete with the United States in similar product lines (e.g. within SITC 7).

Former Secretary of the Treasury Larry Summers once quipped that the United States

cannot continue to be an ‘‘importer of last resort.’’ If not the United States, then who? Both

Europe and Japan look like unlikely candidates. It may be that in the medium term that

intra-regional exports in Asia will increase significantly but in an unexpected, and

deleterious, way.

Still, while such a crisis in the United States is possible, it is unlikely, at least in the short-

run. The fundamentals of the US economy are generally strong; indeed, as was noted

above, the US economy seems to be showing fairly encouraging signs of economic growth

in the second half of 2002 and first quarter of 2003, though the Iraqi war is weighing

heavily on the markets and consumer/business confidence. Nevertheless, from a policy

perspective, it seems to be sensible both for developing Asia and the United States to build

a strong relationship. The United States and Asia have ostensibly chosen the path of

bilateral-trading arrangements as a means of enhancing cooperation in the region. The

literature is replete with discussions of the economics of the new regionalism, ‘‘building

bloc versus stumbling bloc’’ issues, and empirical studies; hence, we do not deal with these

issues here, though we will consider emerging issues in US–Asian regionalism in Section

4.13 Rather, we concentrate here on the case study of Viet Nam, which provides an

interesting example of how the United States is using bilateral agreements. It is also the

only bilateral arrangement that the United States has successfully completely in the region,

though it is in the final phase of a few other arrangements.14

3.1. Case study of Viet Nam15

Viet Nam presents an interesting case study in US–Asian relations. Between the end of

the US military involvement in Viet Nam in 1975 and the end of the Vietnamese occupation

13 See, for example, Scollay and Gilbert (2002) for an excellent review of new regional pacts in the region as

well ex ante, CGE estimates of their effects. Moreover, Kreinin and Plummer (2002), among many, review the

economics of the new regionalism, with a focus on developing countries.14 For example, as of the end of 2002, the United States and Singapore were in the final throes of free-trade area

negotiations. An agreement has been reached on the real side—the fact that Singapore is not a threat to US

agriculture, textiles, or steel facilitated negotiations significantly on the US side—but not yet on the financial

side, as Singapore has resisted some aspects of capital market liberalization which may create greater volatility

in Singaporean capital markets, particularly the foreign exchange market (Singapore has always been wary of

internationalization of the Singapore dollar).15 This case study derives in part from the author’s presentation at the conference, ‘‘Bridging Capacity Gaps in

Vietnam’s Economic Integration Program,’’ February 28, 2002. It uses as a source the NCIEC/UNDP

(unpublished) study, ‘‘Stock-Taking Report: Vietnam’s Economic Integration Commitments, Government’s

Action Plans and Donors’ Current Assistance.’’

268 M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281

of Cambodia, US–Vietnamese relations were ice-cold. The United States had imposed a

trade embargo on Viet Nam that was not lifted until the early 1990s, when the process of

establishing diplomatic relations began. Since then, the United States has supported the

economic reform process in Viet Nam and has increasingly endeavored to help integrate it

into the world economy. This process culminated in the Viet Nam–US Bilateral Trade

Agreement (BTA) in October 2001, 2 months before Viet Nam presented its initial offering

to the WTO, which presents an interesting example of the use of a regional agreement to

promote multilateral aims.

A brief bit of recent economic history is in order. Following the economic reform process

unleashed by doi moi in 1986, liberalization of commercial policies in Viet Nam has

gathered considerable momentum over the past 15 years. As mentioned in UNDP (2001),

these reforms have taken place on five main fronts: (1) phasing-out of foreign-exchange

controls and financial restructuring; (2) liberalization of controls regarding foreign-trading

activities; (3) reform of the import and export tax structures and controls used to manage

imports and exports; (4) adoption of measures designed to bring in DFI; and (5) establish-

ing bilateral, regional and multilateral trading agreements.

In many ways, bilateral and regional arrangements have been fuelling reform in other

areas: in order to meet its commitments under the ASEAN Free-Trade Area (AFTA) and

the ASEAN Investment Area (AIA), for example, Viet Nam has had to reform the way in

which it regulates its imports and exports and DFI. The BTA will encourage Viet Nam to

conform to most international norms regarding trade in goods and services, a big step on

the road to reaching the ultimate goal of WTO accession.

Hence, bilateral and plurilateral agreements are increasingly shaping commercial-policy

reform in Viet Nam. This is not unusual; many developing countries are choosing the same

strategy. The 1990s saw a large upswing in the number of preferential-trading agreements,

with the biggest ‘‘spikes’’ in such deals coming in the late 1990s. The WTO homepage

reports over 200 Free-Trade Area (FTAs). And almost all of these new agreements involve

at least one developing or transitional economy.

In addition to AFTA and the BTA, Viet Nam has negotiated special (non-preferen-

tial) accords under: APEC,16 ASEM,17 the World Bank/IMF,18 and the Miyazawa

16 Viet Nam’s commitments under APEC are voluntary and the time-line for implementation of various

policies, indefinite. The most salient commitment that Viet Nam has is to adhere to ‘‘open trade and investment’’

by 2020, though, as discussed later, the lack of definition of what this means leaves things ambiguous.17 While ASEM has no long-term free trade commitments in the way that APEC supposedly does, areas that

have been agreed to include: adoption of international standards regarding sanitary and psytosanitary measures;

continued services liberalization; adopting international standards and conformance measures; simplification of

customs procedures; reduction in differences in intellectual property protection and enforcement standards;

provision of greater transparency in government procurement procedures; and the consideration of the issuance

of an ASEM travel card for businesspeople.18 Viet Nam’s commitments under World Bank and IMF programs in the area of trade generally reinforce the

process of economic integration set out in other agreements, especially AFTA. Moreover, the list of

liberalization measures included under the World Bank/IMF agreement is consistent with what Viet Nam will

have to accept for WTO accession. Coverage, however, is not complete in this sense; the focus is on creating

greater efficiency in the ‘‘real’’ sector as well as advocacy of greater competition and openness in the financial

area. For example, tariff-barrier provisions mirror commitments under AFTA, and those under non-tariff barriers

generally mirror AFTA and BTA commitments.

M.G. Plummer / Journal of Asian Economics 14 (2003) 243–281 269

Initiative.19 But the ‘‘deepest’’ accord that Viet Nam has negotiated is with AFTA. Viet

Nam joined ASEAN in 1995 and agreed to join AFTA in 1996, with a 10-year schedule to

create a free-trade area with its ASEAN neighbors. While this is 3 years later than for the

ASEAN-6, these latter countries began implementation 3 years earlier than Viet Nam. Of

all Viet Nam’s agreements, clearly AFTA has led to the most ex post ‘‘value added,’’ as Viet

Nam has been in AFTA the longest and the country continues to have much to do in

meeting its exigencies: as of early 2002, less than two-thirds of its inclusion-list items were

in the required 0–5% range. According to Viet Nam’s AFTA agreement, it must reduce

tariffs on all ‘‘normal track’’ items (which tend to be the more sensitive ones, e.g. machines,

equipment, iron and steel) by January 2006 and ‘‘fast track’’ items by January 2003. Items

included in the temporary exclusion list are to be gradually phased-out over the 2004–2013

period, after which all commodities should be included in AFTA.

Although AFTA is principally a trade agreement, many protagonists supported AFTA

more as a means of luring DFI inflows, rather than stimulating intra-regional trade (which,

after all, is only about one-fourth of total ASEAN trade). Hence, it is no accident that AFTA

has an ancillary investment agreement, the ASEAN Investment Area. Under this agree-

ment, Viet Nam will: grant immediate and unconditional MFN status for investors (with the

exception of special arrangements such as in a ‘‘growth triangle’’ framework); open up just

about all industries to ASEAN investors; and participate in regional investment promotion

activities, such as the ASEAN Investment Report, the Compendium of Investment Policies

and Measures, and the ASEAN Investment facilitation series.

As Viet Nam and the United States only normalized diplomatic relations in 1994,

the BTA is important not merely in terms of its economic content but also in its heralding

a new era in US–Vietnamese relations. While Viet Nam’s trade with the United States

has been relatively small (from Table 1 and its sources, about 8% of its total exports

and 3% of total imports in 2001), bilateral trade is expected to pick up considerably as

trade relations are stabilized. Moreover, the United States has become an increasingly-

important source of DFI inflows, and will be an important player in Viet Nam’s bid to

become a member of the WTO. In addition, with the potential for trade and investment

diversion from NAFTA and other possible preferential-trading arrangements that the

United States is contemplating, Viet Nam risks being increasingly isolated (at least at the

margin) from the US market. Stable relations are deemed to be of the essence. Hence, the

BTA has been understandably an important priority in the Vietnamese economic-integra-

tion strategy.

19 The ‘‘Miyazawa Initiative’’ builds on cooperation in the area of finance spurred by the Asian Financial

Crisis, beginning with the ‘‘Chiang Mai Initiative’’ (CMI). As part of its agreement with Japan under the rubric

of the Miyazawa Initiative, Viet Nam has agreed to undertake a number of liberalization measures, beginning

‘‘as soon as possible’’ but to be finished no later than 2010. These include the tariffication of 19 groups of goods

currently subject to import license, as well as allowing businesses to export and import all eligible goods with

equal access to export and import quotas; relaxation of local content requirements applied to foreign ventures,

termination of the ‘‘dual price’’ system, and expansion of the list of sectors open to foreign investment;