Embed Size (px)

DESCRIPTION

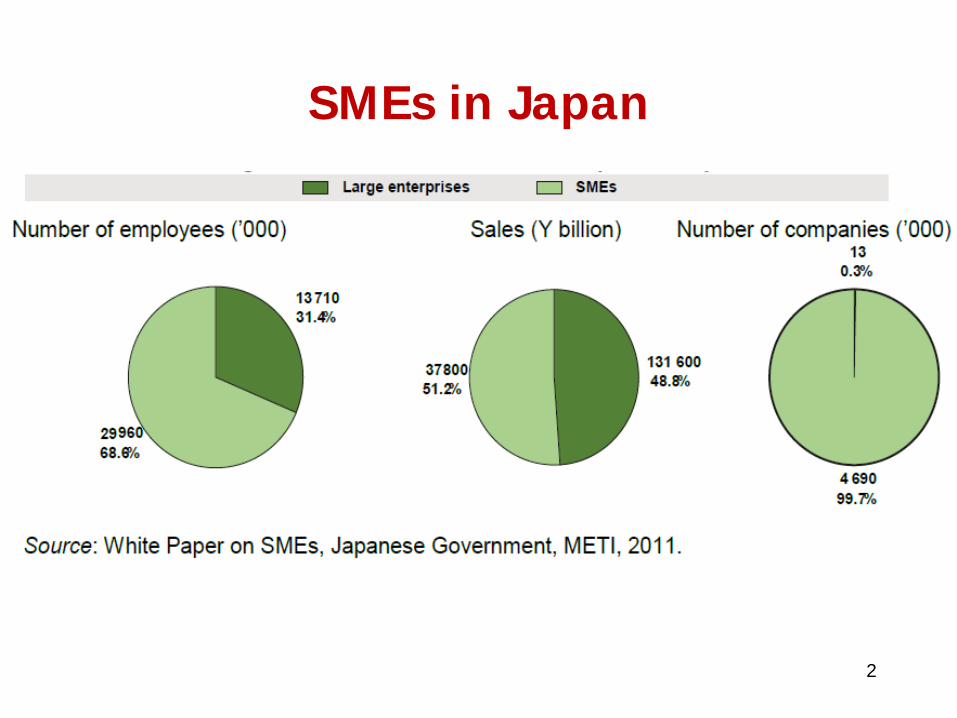

Small and medium-sized enterprises (SMEs) drive growth and development, creating opportunities for innovators. However, Azerbaijan lacks data on SMEs, including what sectors they dominate and how difficult it is for them to borrow money, said ADBI Dean Naoyuki Yoshino at a workshop in Baku, Azerbaijan, on 20–21 May. In his presentation, which was part of ADBI's contribution to the joint study with ADB, Good Jobs for Inclusive Growth in Central and West Asia, he explained that Japan publishes an annual white paper on SMEs containing this information.

Citation preview

Strengthening SMEs’ Employment and

Financial Education

Naoyuki Yoshino Dean, Asian Development Bank Institute (ADBI)

Professor Emeritus, Keio University, Japan [email protected], [email protected]

Farhad Taghizadeh-Hesary Assistant Professor, Keio University, Japan

Peter Morgan Research Consultant, ADBI, Japan

The views expressed in this presentation are the views of the author and do not necessarily reflect the views or policies of the Asian Development Bank Institute (ADBI), the Asian Development Bank (ADB), its Board of Directors, or the governments they represent. ADBI does not guarantee the accuracy of the data included in this paper and accepts no responsibility for any consequences of their use. Terminology used may not necessarily be consistent with ADB official terms.

2

SMEs in Japan

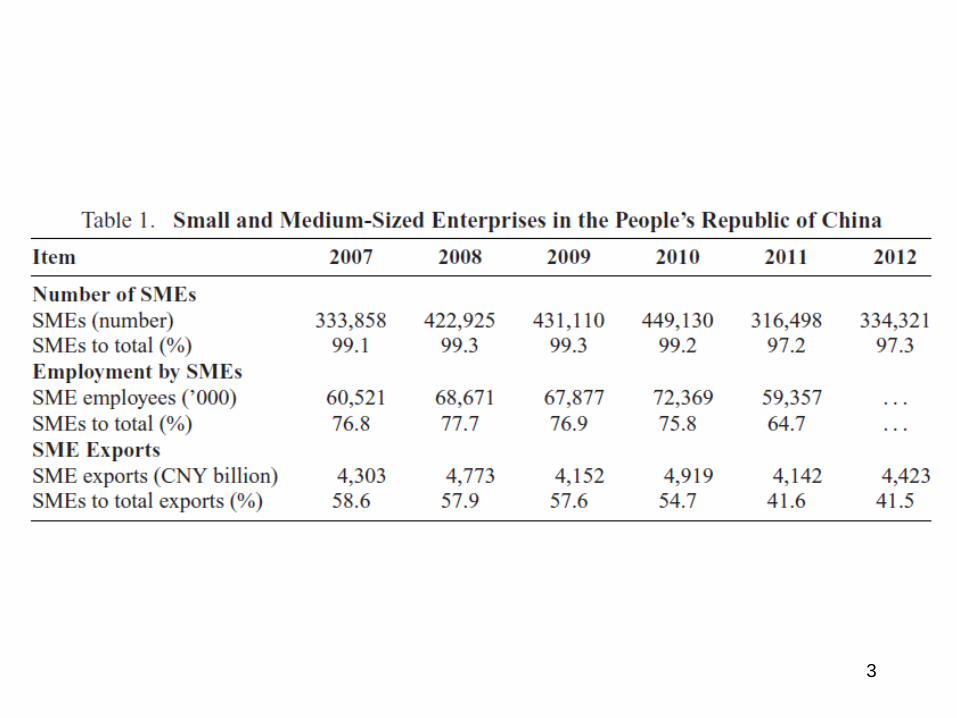

3

4

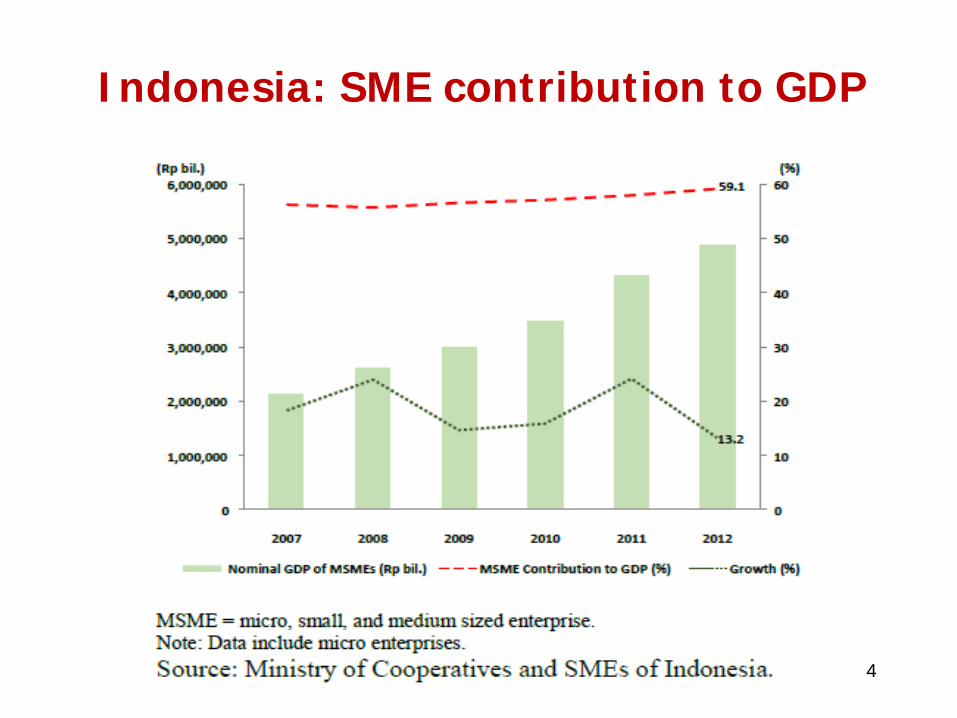

Indonesia: SME contribution to GDP

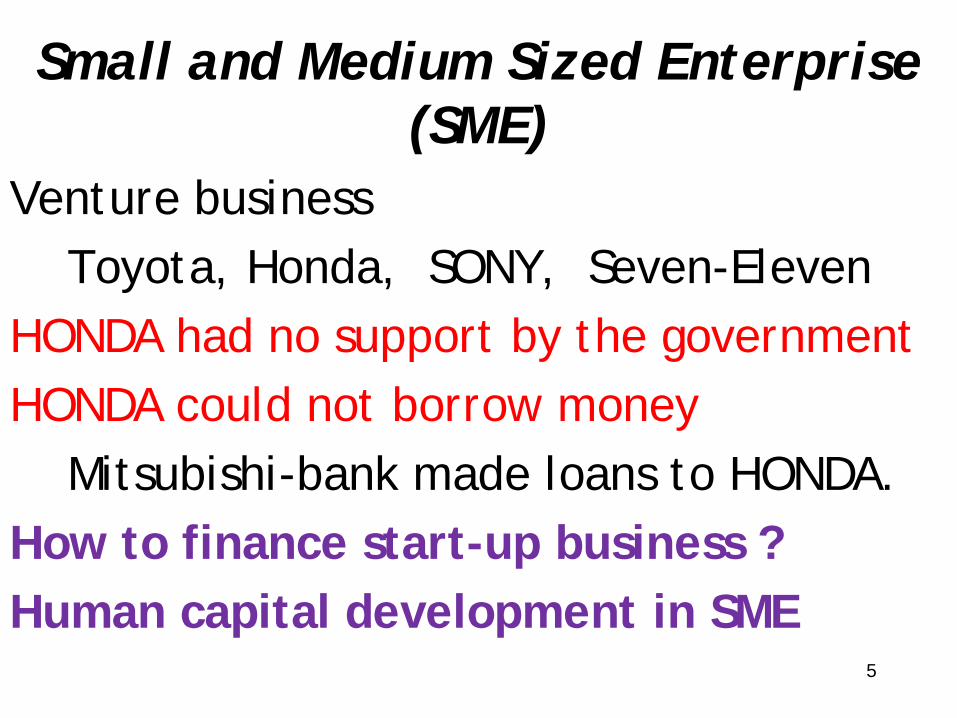

Small and Medium Sized Enterprise (SME)

Venture business Toyota, Honda, SONY, Seven-Eleven HONDA had no support by the government HONDA could not borrow money Mitsubishi-bank made loans to HONDA. How to finance start-up business ? Human capital development in SME

5

6

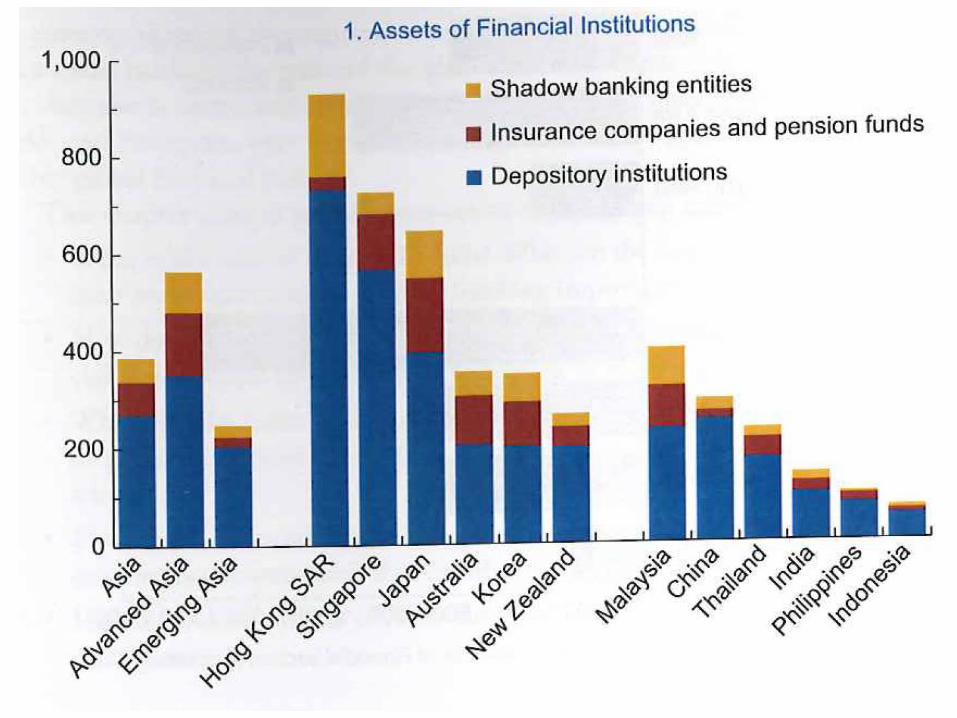

Asian Financial Markets’ Main Features 1. Bank-dominated financial system 2. Small share of bond markets ---> Needs for long term financing 3. Lack of long-term investors such as

pension funds and Life insurance 4, Bench mark bond market (soverign bond) Infrastructure bond, corporate bond 5. High percentage of SMEs 6. Large share or Microcredit (finance

companies); Lack of venture capital

7

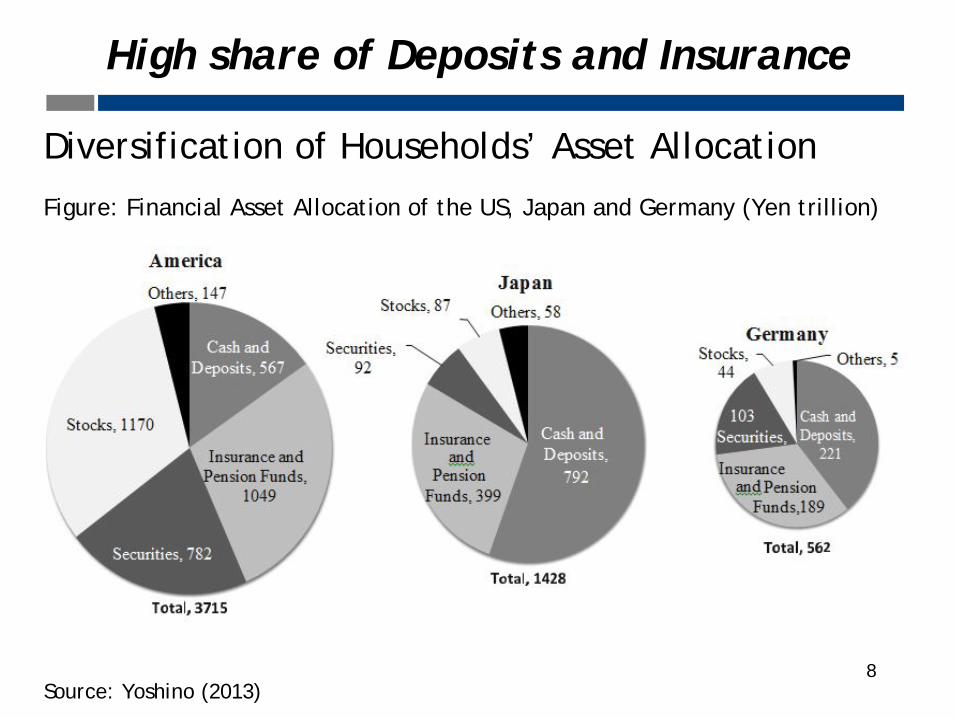

High share of Deposits and Insurance

Diversification of Households’ Asset Allocation

Figure: Financial Asset Allocation of the US, Japan and Germany (Yen trillion)

Source: Yoshino (2013)

8

9

Very high savings rate in Asia

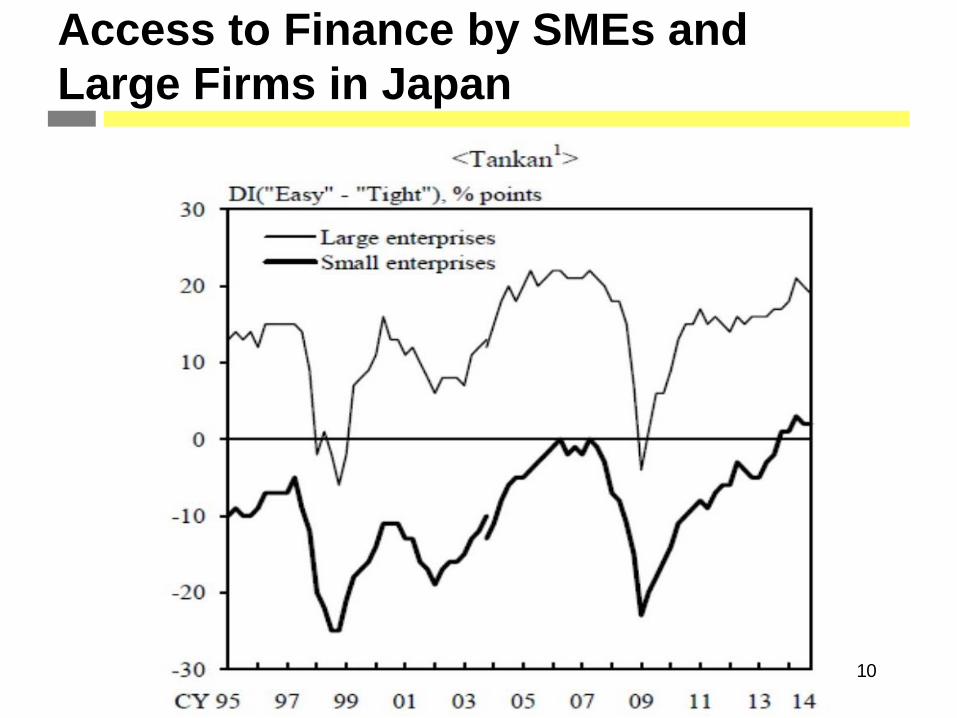

Access to Finance by SMEs and Large Firms in Japan

10

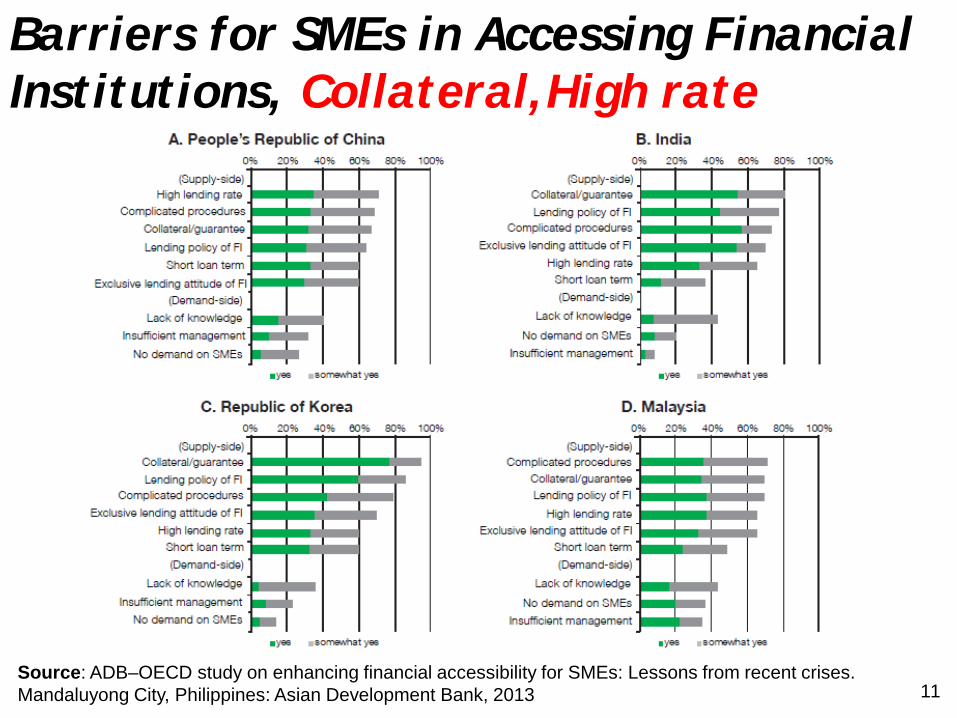

Barriers for SMEs in Accessing Financial Institutions, Collateral,High rate

11 Source: ADB–OECD study on enhancing financial accessibility for SMEs: Lessons from recent crises. Mandaluyong City, Philippines: Asian Development Bank, 2013

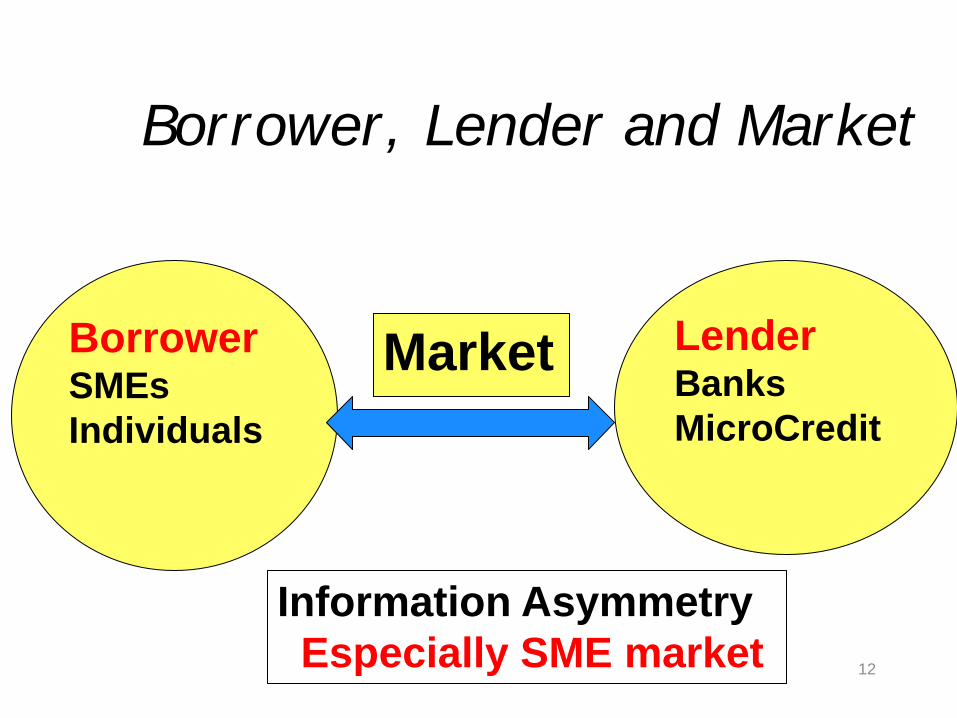

Borrower, Lender and Market

12

Borrower SMEs Individuals

Lender Banks MicroCredit

Market

Information Asymmetry Especially SME market

Four Accounts by SME

1, Account to show Bankers 2, Account to show tax authority 3, His own account 4, Account to show to his wife

13

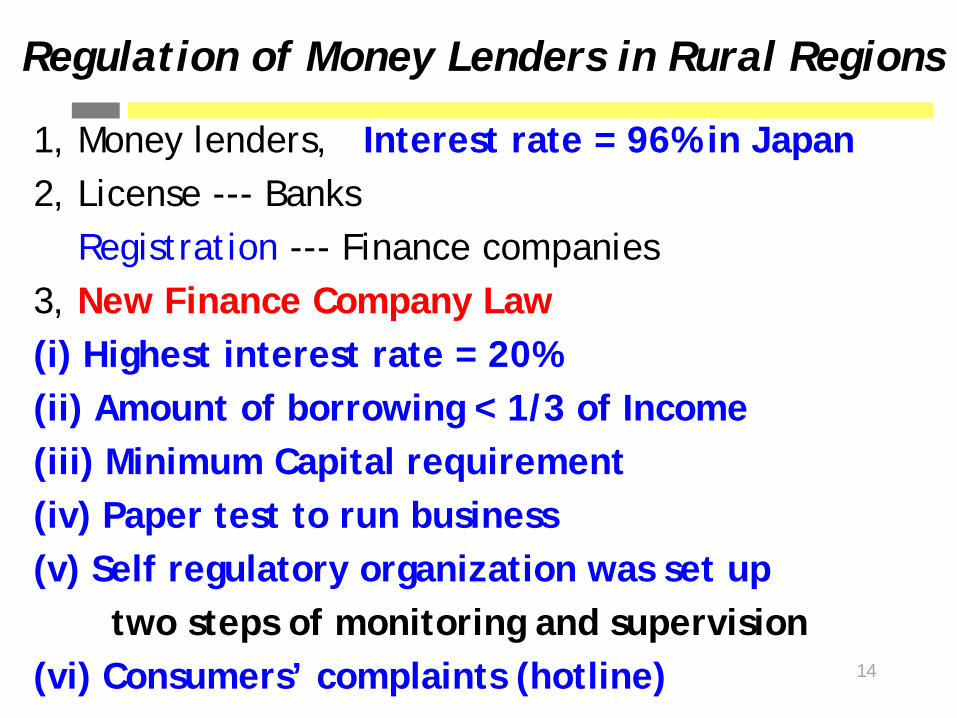

Regulation of Money Lenders in Rural Regions

1, Money lenders, Interest rate = 96% in Japan 2, License --- Banks Registration --- Finance companies 3, New Finance Company Law (i) Highest interest rate = 20% (ii) Amount of borrowing < 1/3 of Income (iii) Minimum Capital requirement (iv) Paper test to run business (v) Self regulatory organization was set up two steps of monitoring and supervision (vi) Consumers’ complaints (hotline) 14

15

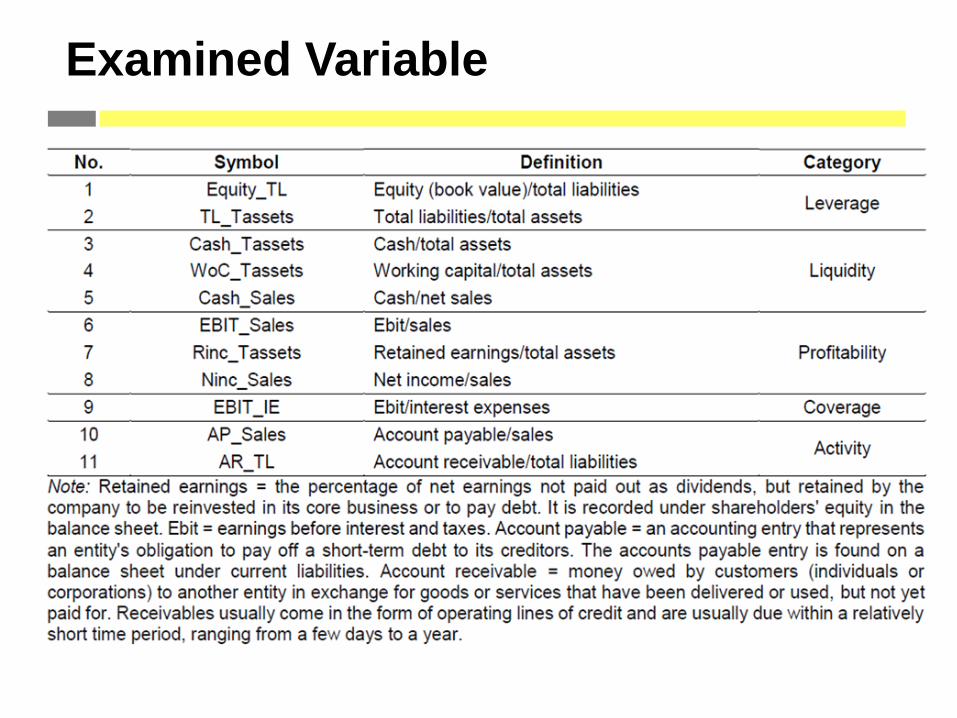

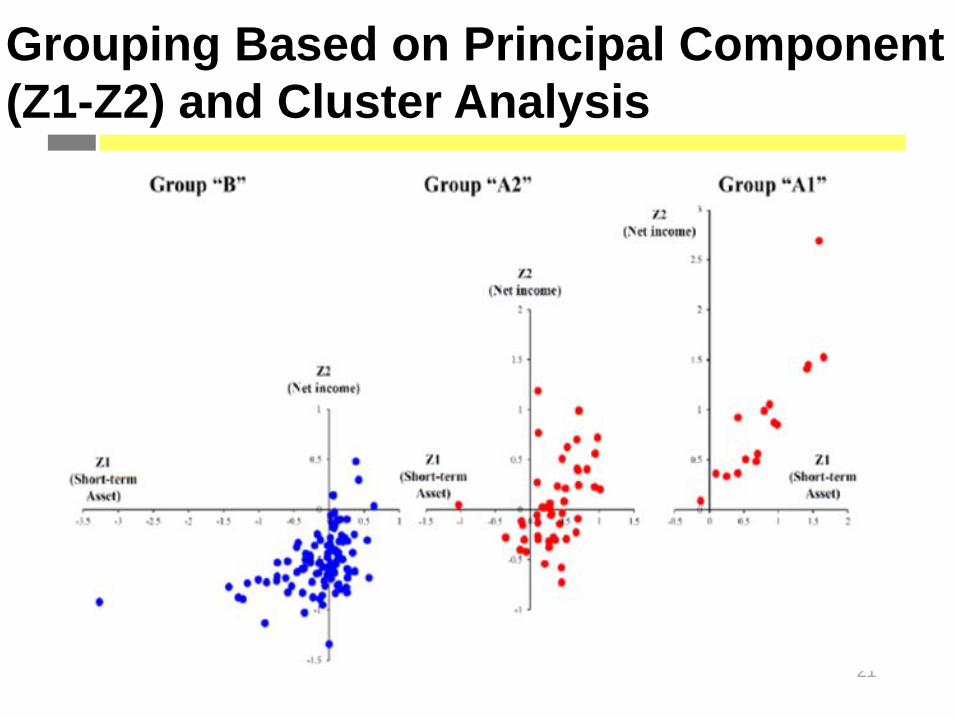

Selection of the variables Principal Component Analysis Cluster Analysis

16

Analysis of SME credit risk using Asian data

17

Examined Variable

18

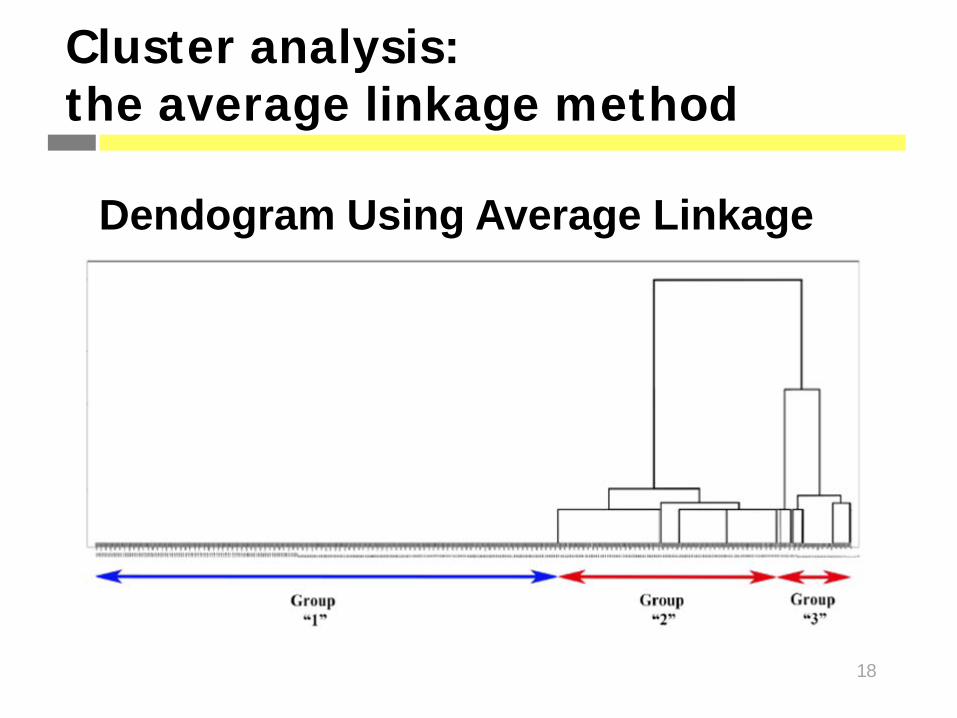

Cluster analysis: the average linkage method

Dendogram Using Average Linkage

19

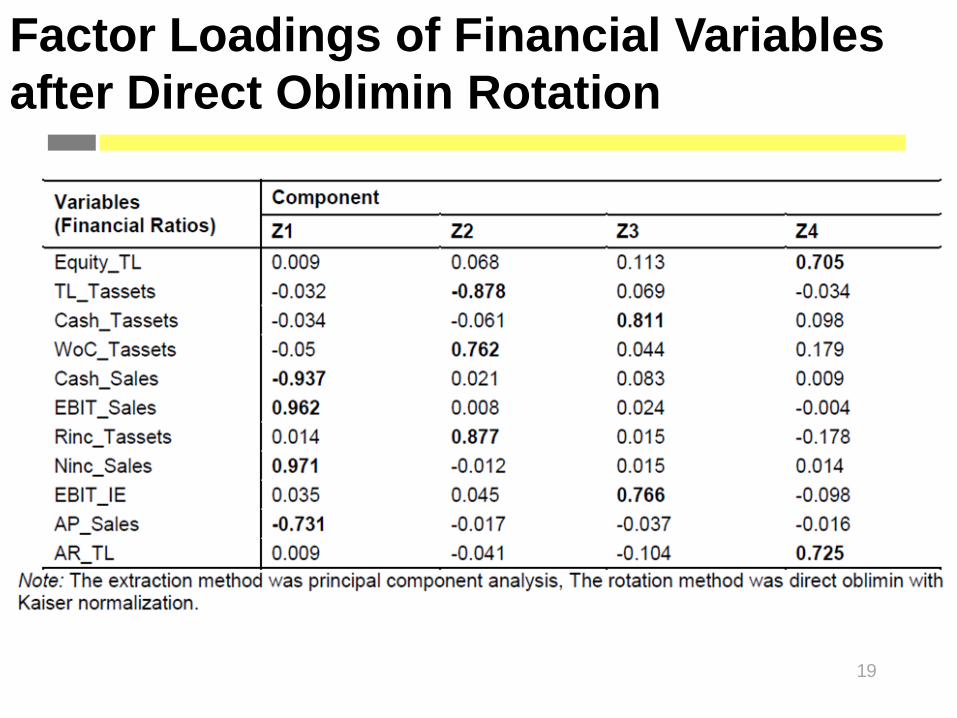

Factor Loadings of Financial Variables after Direct Oblimin Rotation

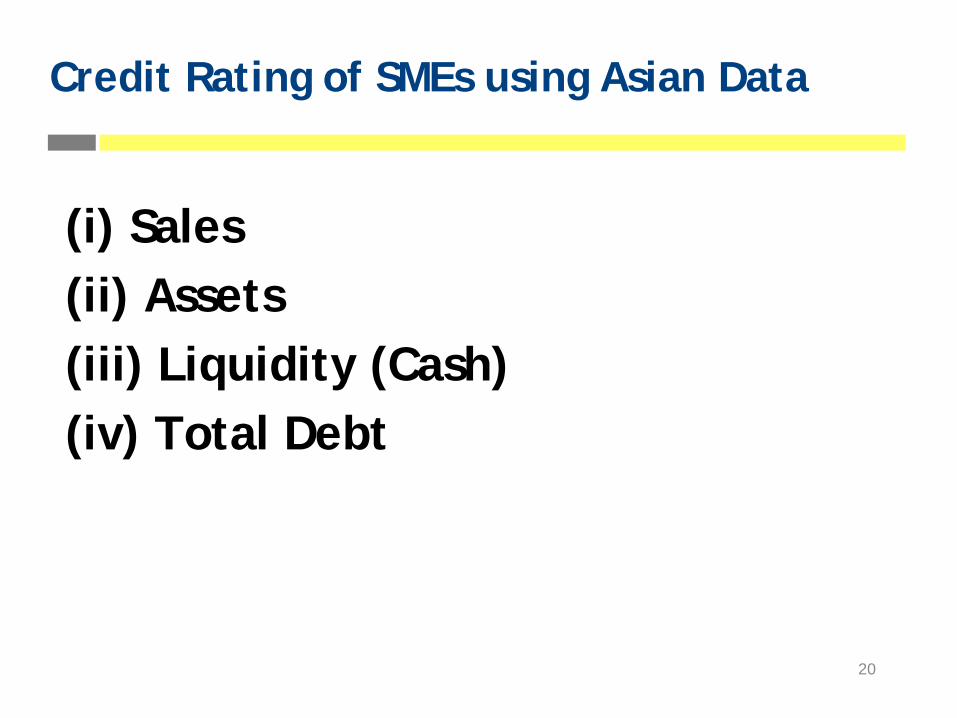

Credit Rating of SMEs using Asian Data

(i) Sales (ii) Assets (iii) Liquidity (Cash) (iv) Total Debt

20

21

Grouping Based on Principal Component (Z1-Z2) and Cluster Analysis

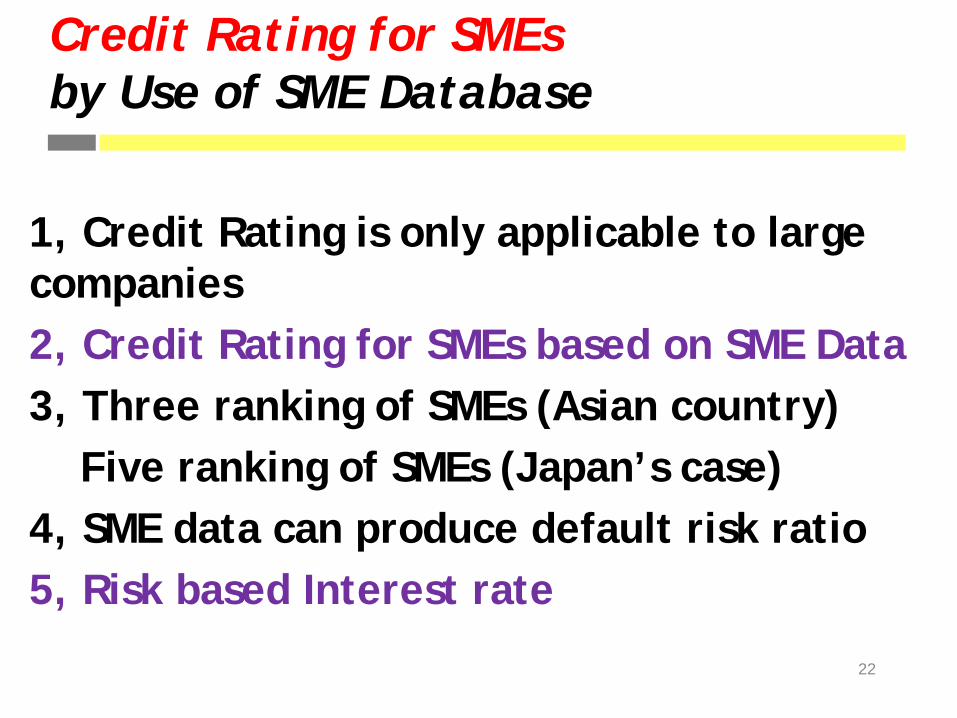

Credit Rating for SMEs by Use of SME Database

1, Credit Rating is only applicable to large companies 2, Credit Rating for SMEs based on SME Data 3, Three ranking of SMEs (Asian country) Five ranking of SMEs (Japan’s case) 4, SME data can produce default risk ratio 5, Risk based Interest rate

22

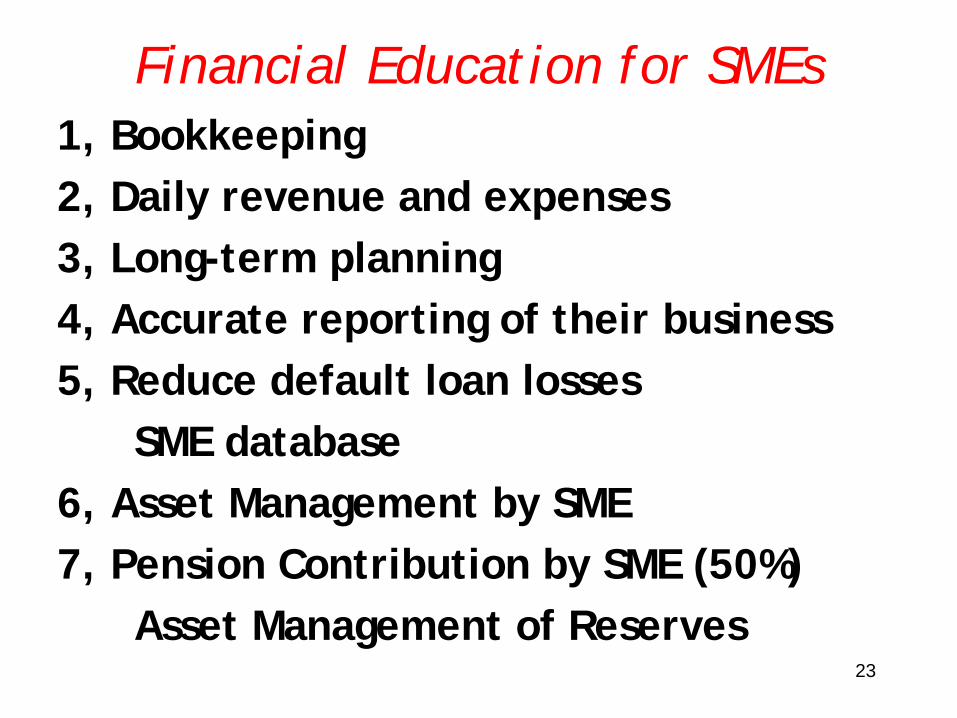

Financial Education for SMEs 1, Bookkeeping 2, Daily revenue and expenses 3, Long-term planning 4, Accurate reporting of their business 5, Reduce default loan losses SME database 6, Asset Management by SME 7, Pension Contribution by SME (50%) Asset Management of Reserves

23

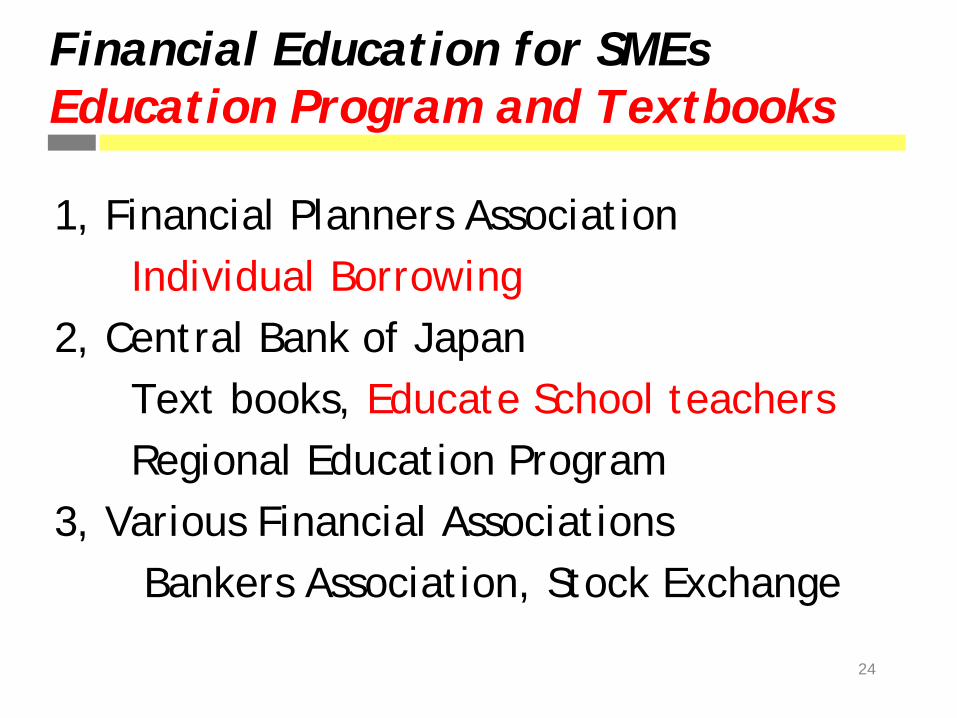

Financial Education for SMEs Education Program and Textbooks

1, Financial Planners Association Individual Borrowing 2, Central Bank of Japan Text books, Educate School teachers Regional Education Program 3, Various Financial Associations Bankers Association, Stock Exchange

24

25

Possible Solutions Start up businesses, farmers

Hometown Investment Trust Funds -------------------------------------------------- A Stable Way to Supply Risk Capital

Yoshino, Naoyuki; Kaji Sahoko (Eds.) 2013, IX, 98 p. 41 illus.,20 illus. in color Available Formats: ebook Hardcover Japan, Cambodia Springer Vietnam, Peru

Investment in SMEs and start up businesses

26

28

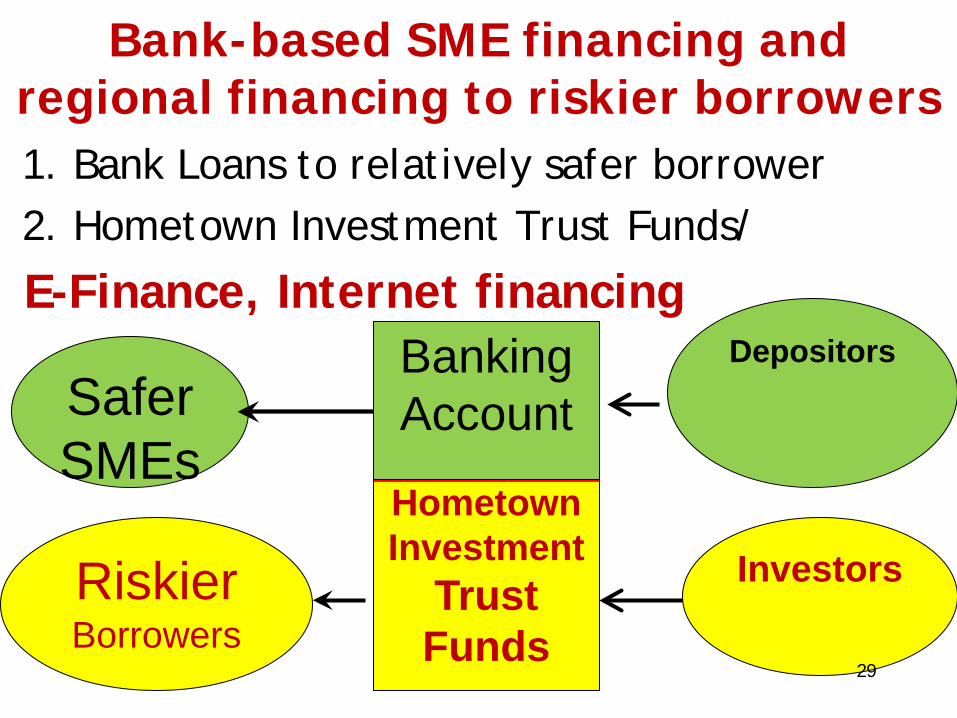

Bank-based SME financing and regional financing to riskier borrowers 1. Bank Loans to relatively safer borrower 2. Hometown Investment Trust Funds/

E-Finance, Internet financing Banking

Account

Hometown Investment

Trust Funds

Riskier Borrowers

Investors

Depositors Safer SMEs

Banking Account

29

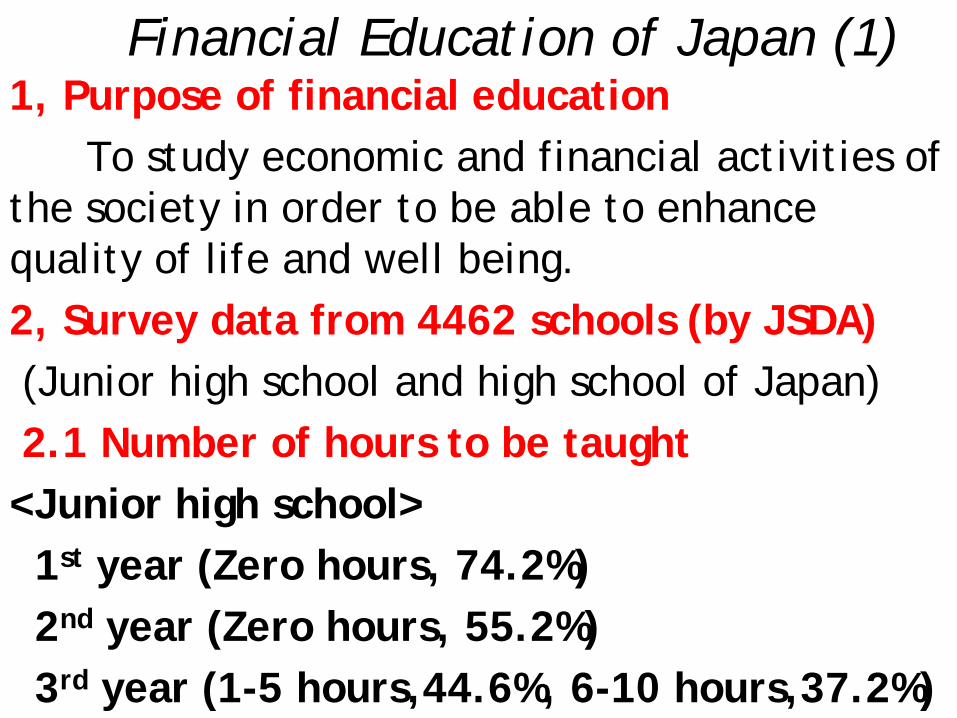

Financial Education of Japan (1) 1, Purpose of financial education To study economic and financial activities of the society in order to be able to enhance quality of life and well being. 2, Survey data from 4462 schools (by JSDA) (Junior high school and high school of Japan) 2.1 Number of hours to be taught <Junior high school> 1st year (Zero hours, 74.2%) 2nd year (Zero hours, 55.2%) 3rd year (1-5 hours,44.6%, 6-10 hours,37.2%)

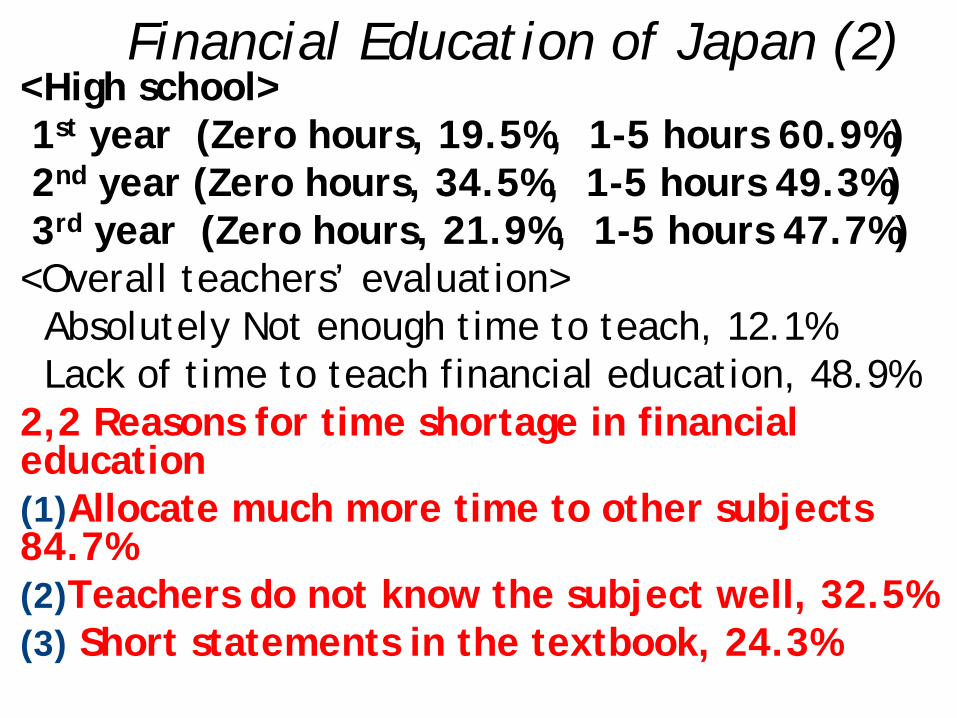

Financial Education of Japan (2) <High school> 1st year (Zero hours, 19.5%, 1-5 hours 60.9%) 2nd year (Zero hours, 34.5%, 1-5 hours 49.3%) 3rd year (Zero hours, 21.9%, 1-5 hours 47.7%) <Overall teachers’ evaluation> Absolutely Not enough time to teach, 12.1% Lack of time to teach financial education, 48.9% 2,2 Reasons for time shortage in financial education (1)Allocate much more time to other subjects 84.7% (2)Teachers do not know the subject well, 32.5% (3) Short statements in the textbook, 24.3%

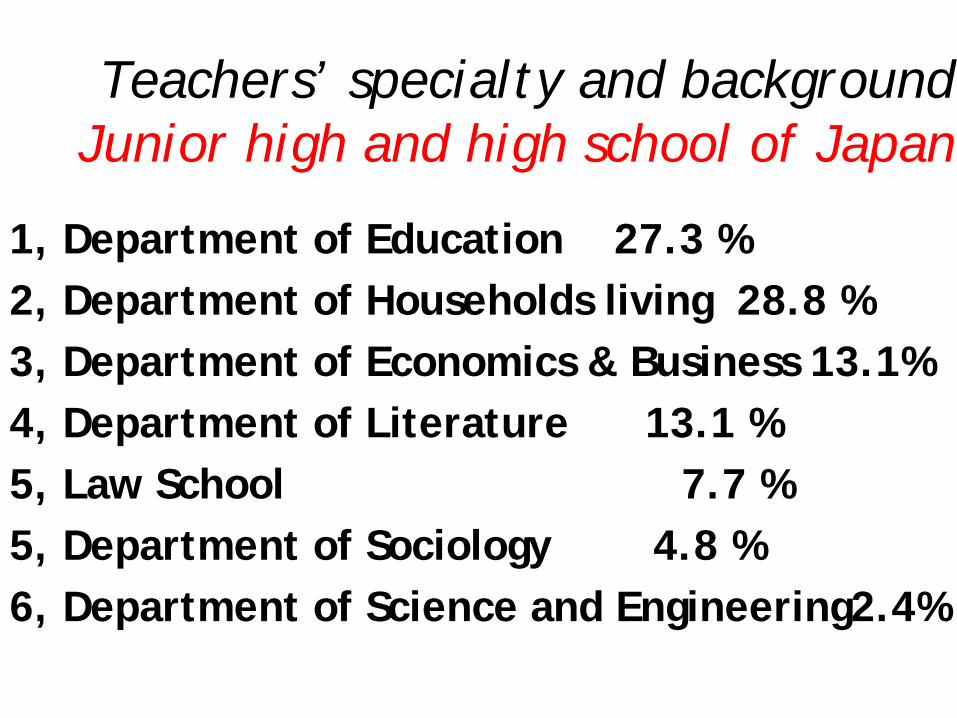

Teachers’ specialty and background Junior high and high school of Japan

1, Department of Education 27.3 % 2, Department of Households living 28.8 % 3, Department of Economics & Business 13.1% 4, Department of Literature 13.1 % 5, Law School 7.7 % 5, Department of Sociology 4.8 % 6, Department of Science and Engineering2.4%

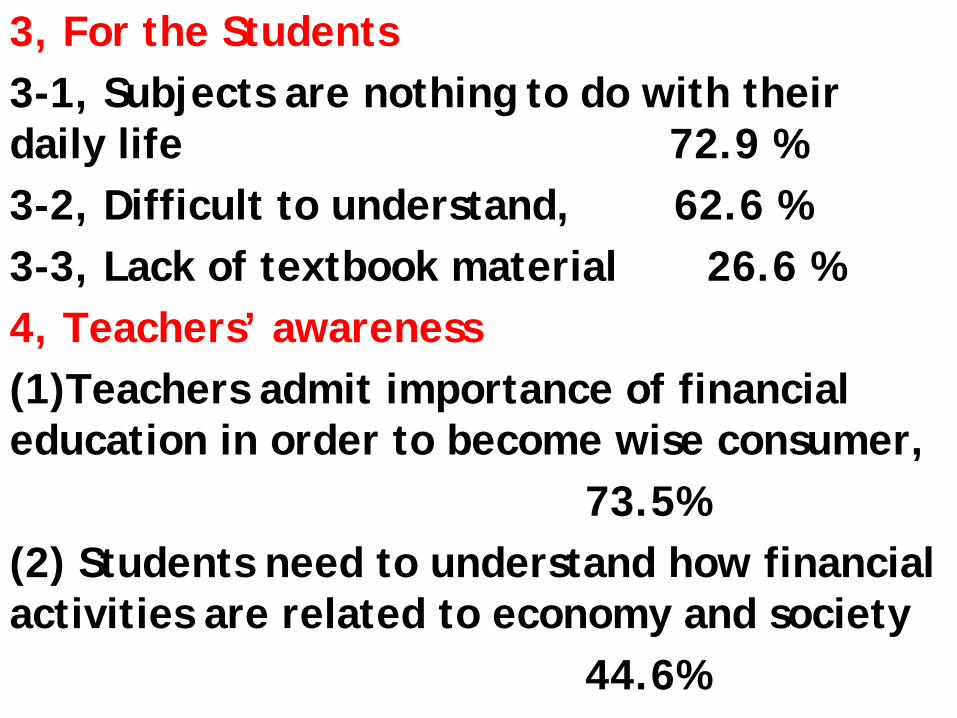

3, For the Students 3-1, Subjects are nothing to do with their daily life 72.9 % 3-2, Difficult to understand, 62.6 % 3-3, Lack of textbook material 26.6 % 4, Teachers’ awareness (1)Teachers admit importance of financial education in order to become wise consumer, 73.5% (2) Students need to understand how financial activities are related to economy and society 44.6%

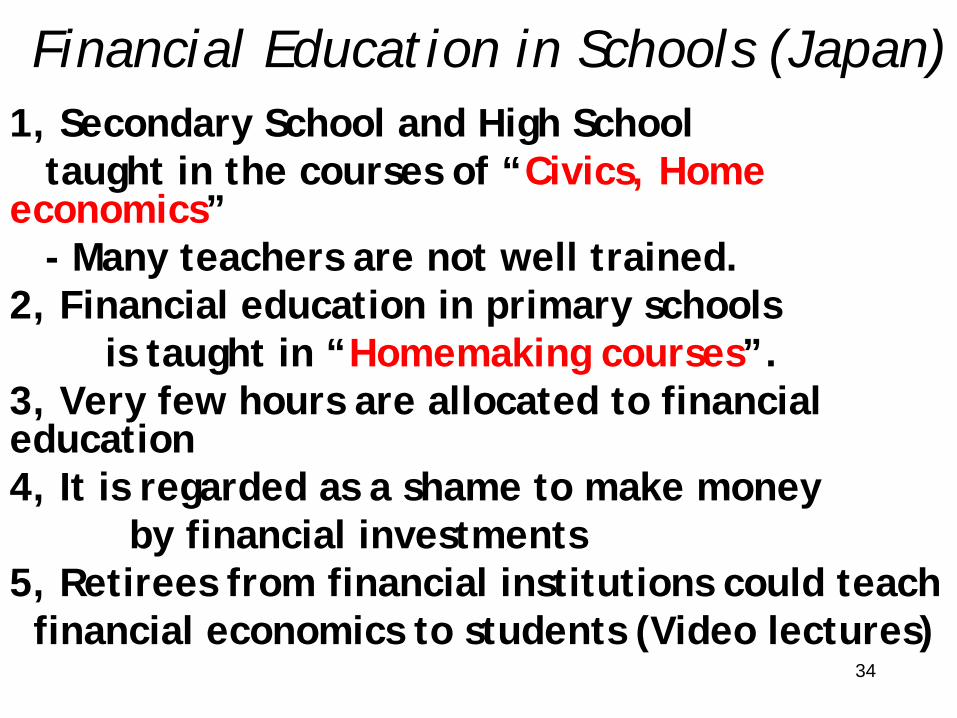

Financial Education in Schools (Japan) 1, Secondary School and High School taught in the courses of “Civics, Home economics” - Many teachers are not well trained. 2, Financial education in primary schools is taught in “Homemaking courses”. 3, Very few hours are allocated to financial education 4, It is regarded as a shame to make money by financial investments 5, Retirees from financial institutions could teach financial economics to students (Video lectures)

34

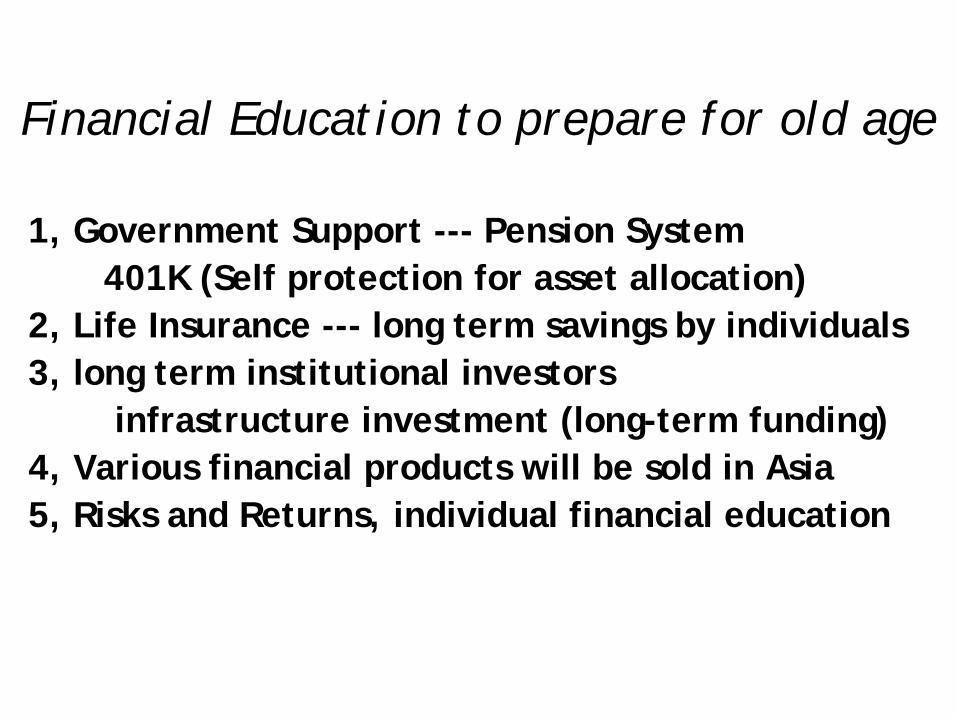

Financial Education to prepare for old age

1, Government Support --- Pension System 401K (Self protection for asset allocation) 2, Life Insurance --- long term savings by individuals 3, long term institutional investors infrastructure investment (long-term funding) 4, Various financial products will be sold in Asia 5, Risks and Returns, individual financial education

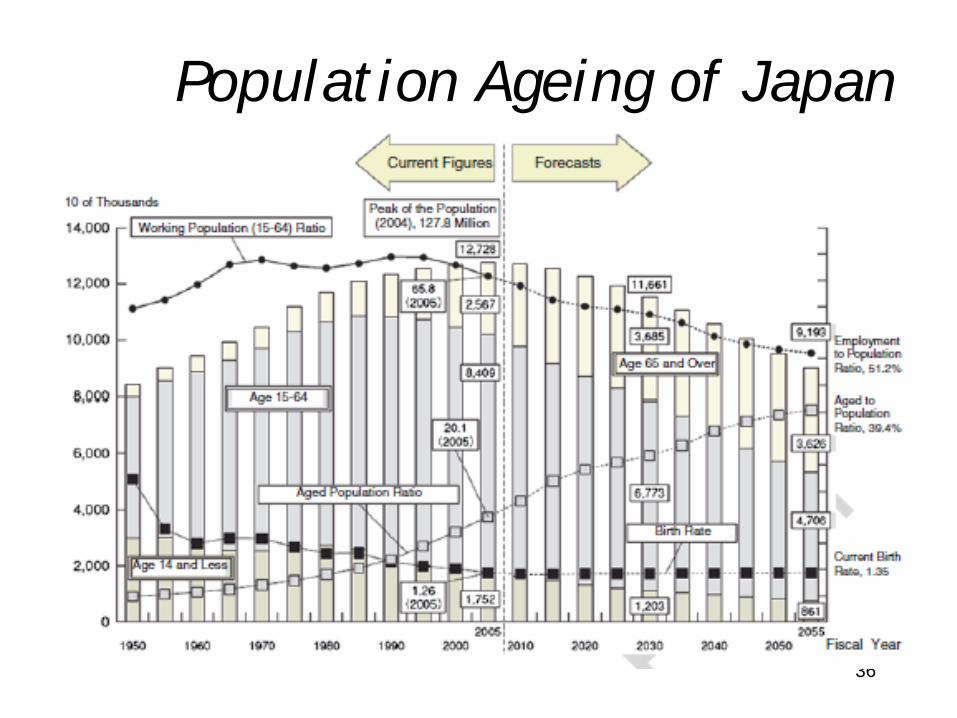

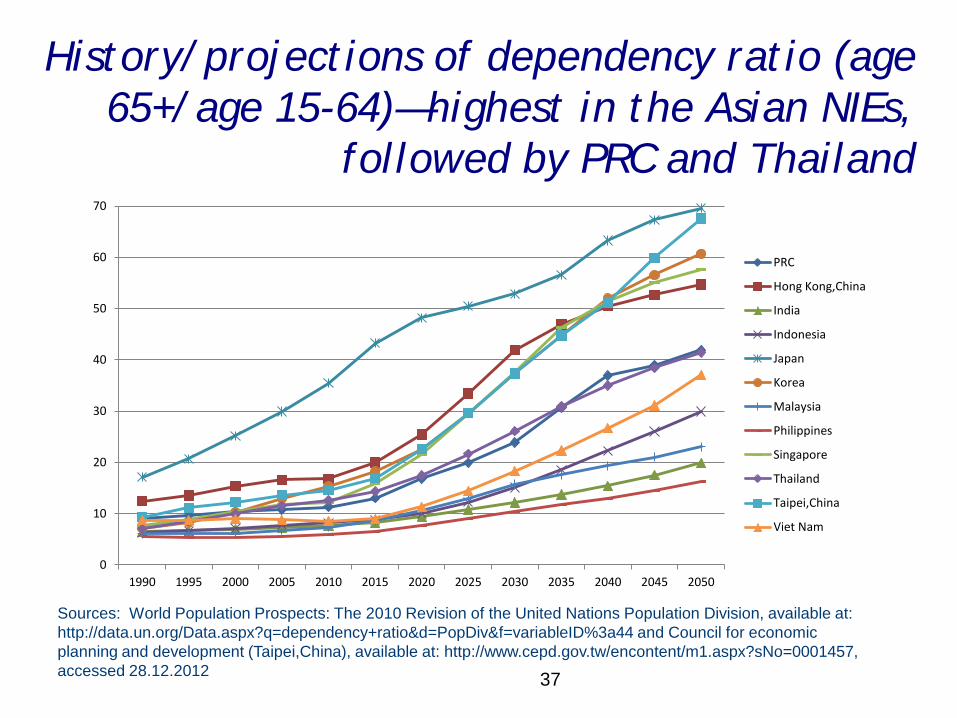

Population Ageing of Japan

36

History/projections of dependency ratio (age 65+/age 15-64)—highest in the Asian NIEs,

followed by PRC and Thailand

37

0

10

20

30

40

50

60

70

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

PRC

Hong Kong,China

India

Indonesia

Japan

Korea

Malaysia

Philippines

Singapore

Thailand

Taipei,China

Viet Nam

Sources: World Population Prospects: The 2010 Revision of the United Nations Population Division, available at: http://data.un.org/Data.aspx?q=dependency+ratio&d=PopDiv&f=variableID%3a44 and Council for economic planning and development (Taipei,China), available at: http://www.cepd.gov.tw/encontent/m1.aspx?sNo=0001457, accessed 28.12.2012

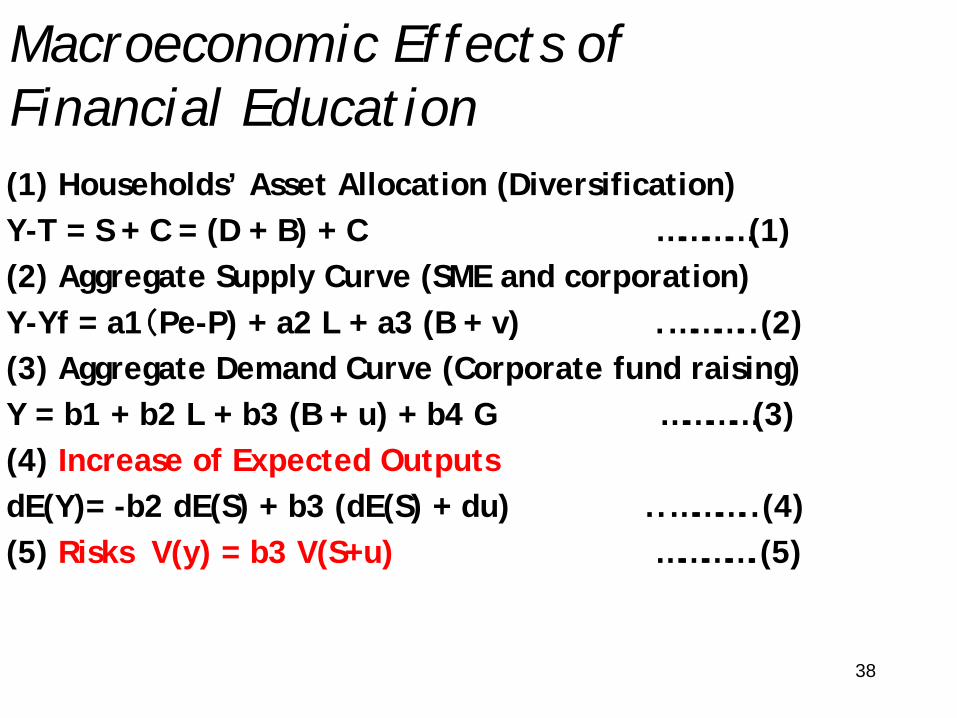

Macroeconomic Effects of Financial Education (1) Households’ Asset Allocation (Diversification) Y-T = S + C = (D + B) + C …………(1) (2) Aggregate Supply Curve (SME and corporation) Y-Yf = a1(Pe-P) + a2 L + a3 (B + v) .………..(2) (3) Aggregate Demand Curve (Corporate fund raising) Y = b1 + b2 L + b3 (B + u) + b4 G …………(3) (4) Increase of Expected Outputs dE(Y)= -b2 dE(S) + b3 (dE(S) + du) ..………..(4) (5) Risks V(y) = b3 V(S+u) ………….(5)

38

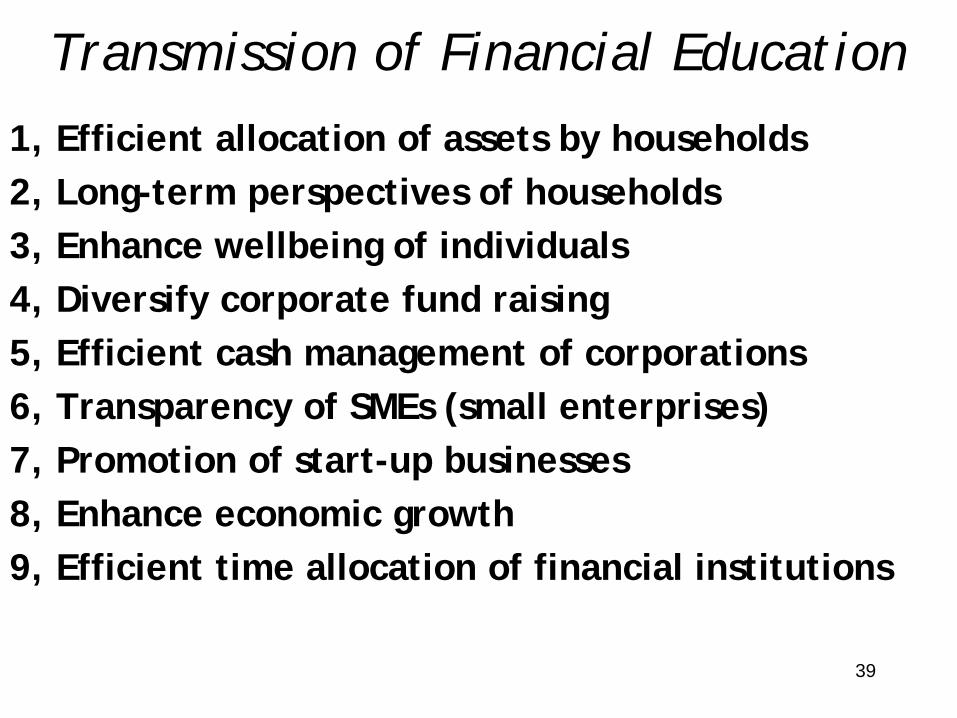

Transmission of Financial Education 1, Efficient allocation of assets by households 2, Long-term perspectives of households 3, Enhance wellbeing of individuals 4, Diversify corporate fund raising 5, Efficient cash management of corporations 6, Transparency of SMEs (small enterprises) 7, Promotion of start-up businesses 8, Enhance economic growth 9, Efficient time allocation of financial institutions

39

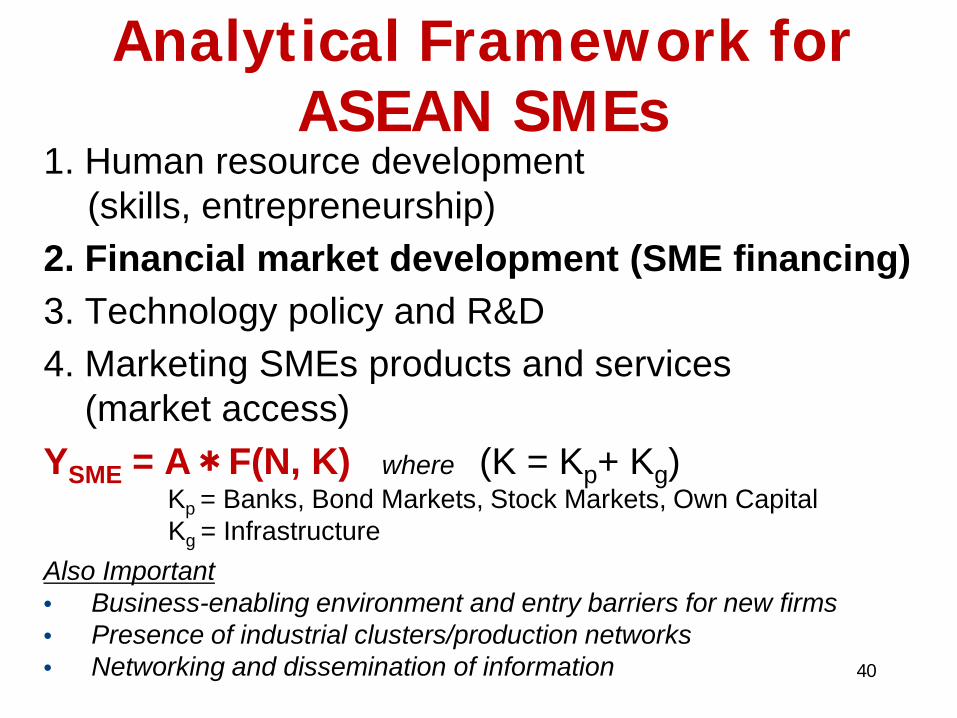

Analytical Framework for ASEAN SMEs

1. Human resource development (skills, entrepreneurship) 2. Financial market development (SME financing) 3. Technology policy and R&D 4. Marketing SMEs products and services (market access) YSME = A*F(N, K) where (K = Kp+ Kg) Kp = Banks, Bond Markets, Stock Markets, Own Capital Kg = Infrastructure Also Important • Business-enabling environment and entry barriers for new firms • Presence of industrial clusters/production networks • Networking and dissemination of information

40

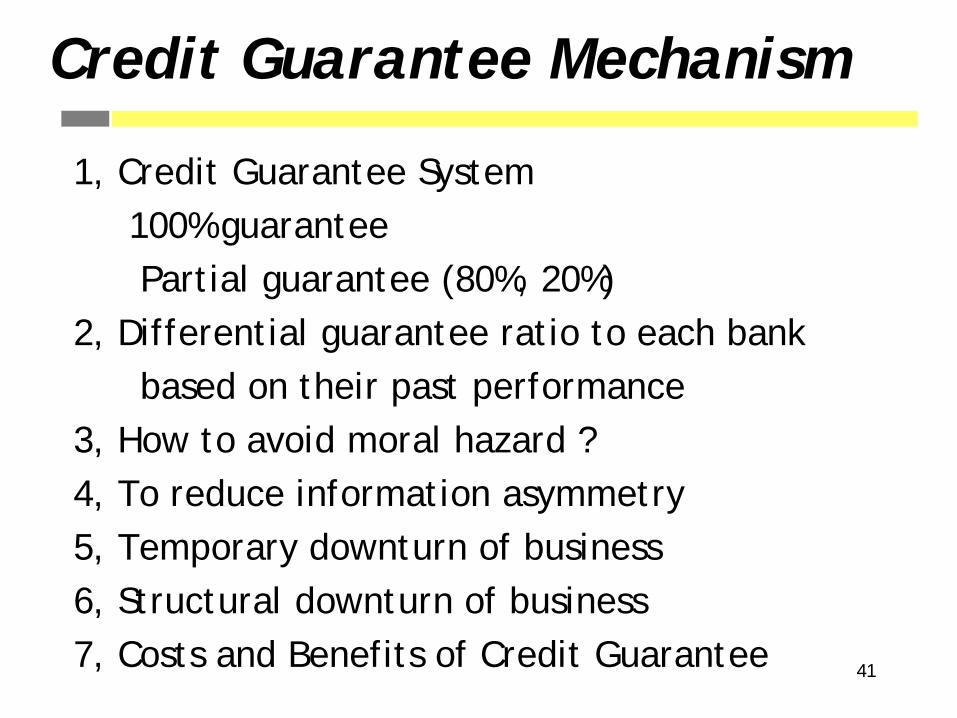

Credit Guarantee Mechanism

1, Credit Guarantee System 100% guarantee Partial guarantee (80%, 20%) 2, Differential guarantee ratio to each bank based on their past performance 3, How to avoid moral hazard ? 4, To reduce information asymmetry 5, Temporary downturn of business 6, Structural downturn of business 7, Costs and Benefits of Credit Guarantee

41

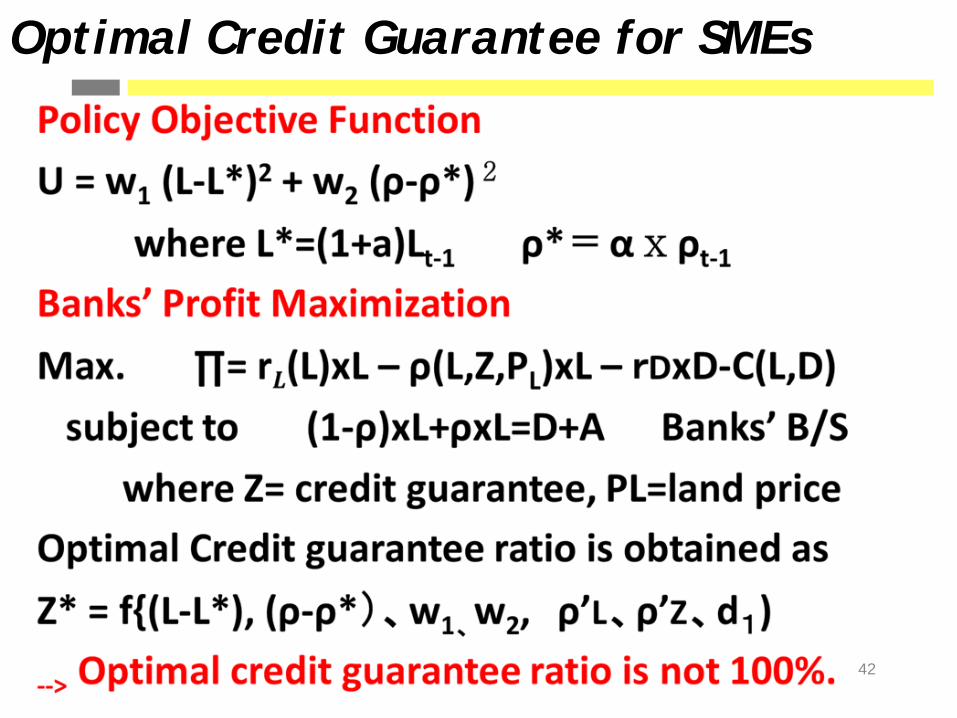

Optimal Credit Guarantee for SMEs

42

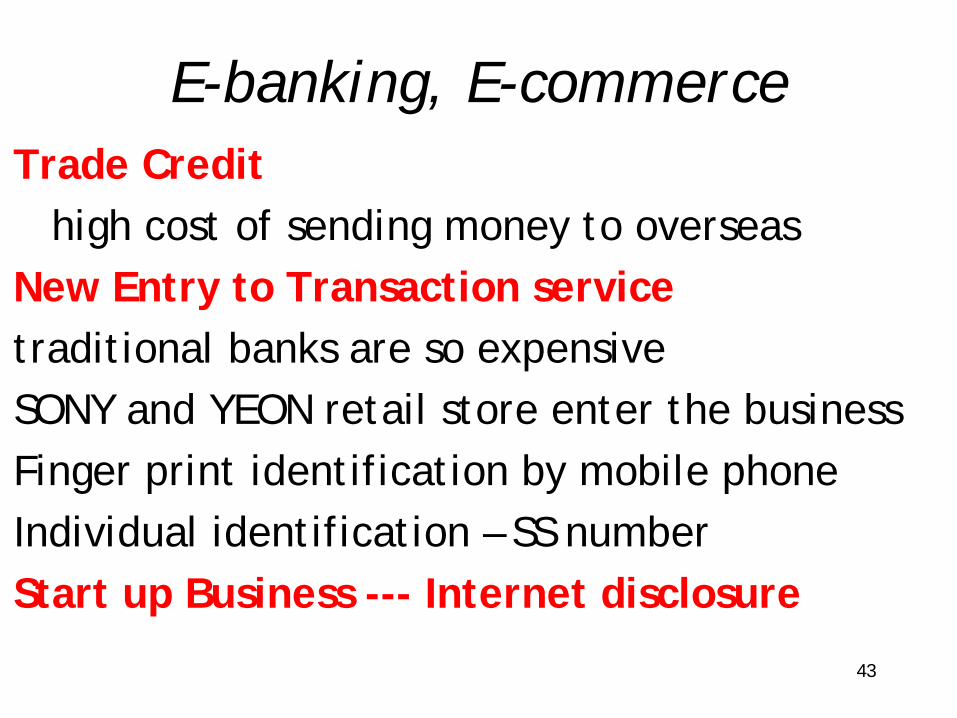

E-banking, E-commerce Trade Credit high cost of sending money to overseas New Entry to Transaction service traditional banks are so expensive SONY and YEON retail store enter the business Finger print identification by mobile phone Individual identification – SS number Start up Business --- Internet disclosure

43

44

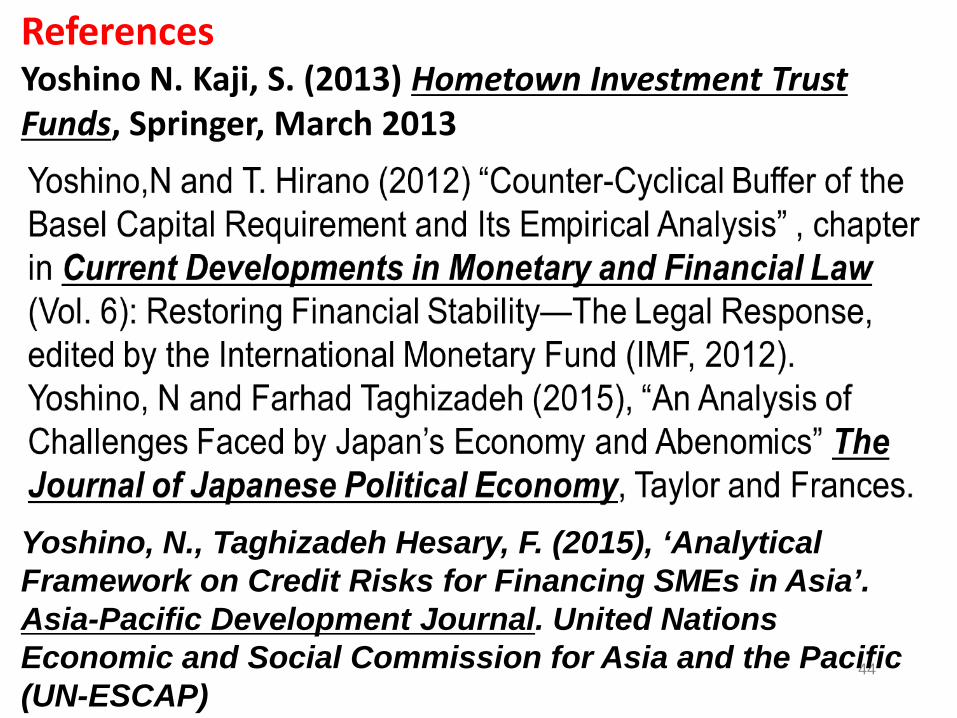

References Yoshino N. Kaji, S. (2013) Hometown Investment Trust Funds, Springer, March 2013

Yoshino, N., Taghizadeh Hesary, F. (2015), ‘Analytical Framework on Credit Risks for Financing SMEs in Asia’. Asia-Pacific Development Journal. United Nations Economic and Social Commission for Asia and the Pacific (UN-ESCAP)