Embed Size (px)

Citation preview

Strength in Numbers: Organizing a Loan Consortium to Support Affordable Housing and Community Investment in Your Community

OUR MEMBER BANKS:

Belonging to Community Lenders…Benefits:• Earn CRA Credit even if deal is not in bank’s footprint

• Participate in good quality loans and minimize bank’s risk • Member Banks are recognized on all promotional materials

• Receive monthly and annual reporting documenting activity

• Meets Lending Test, Investment Test, Service Test

Risks:• Interest rate risk

• Long term nature of our loans

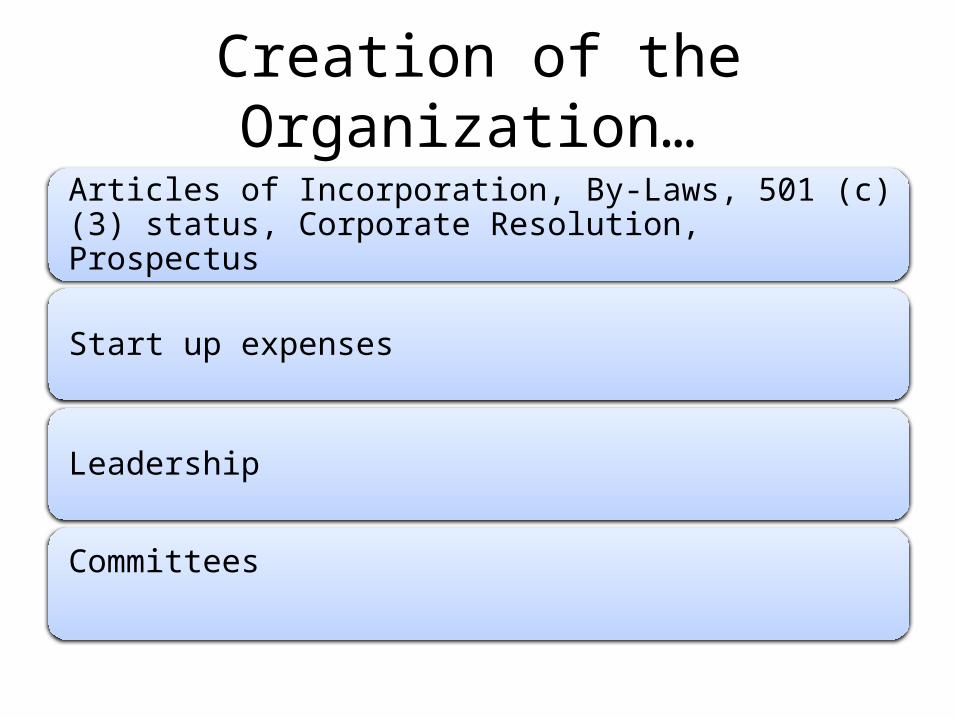

Creation of the Organization…

Articles of Incorporation, By-Laws, 501 (c) (3) status, Corporate Resolution, Prospectus

Start up expenses

Leadership

Committees

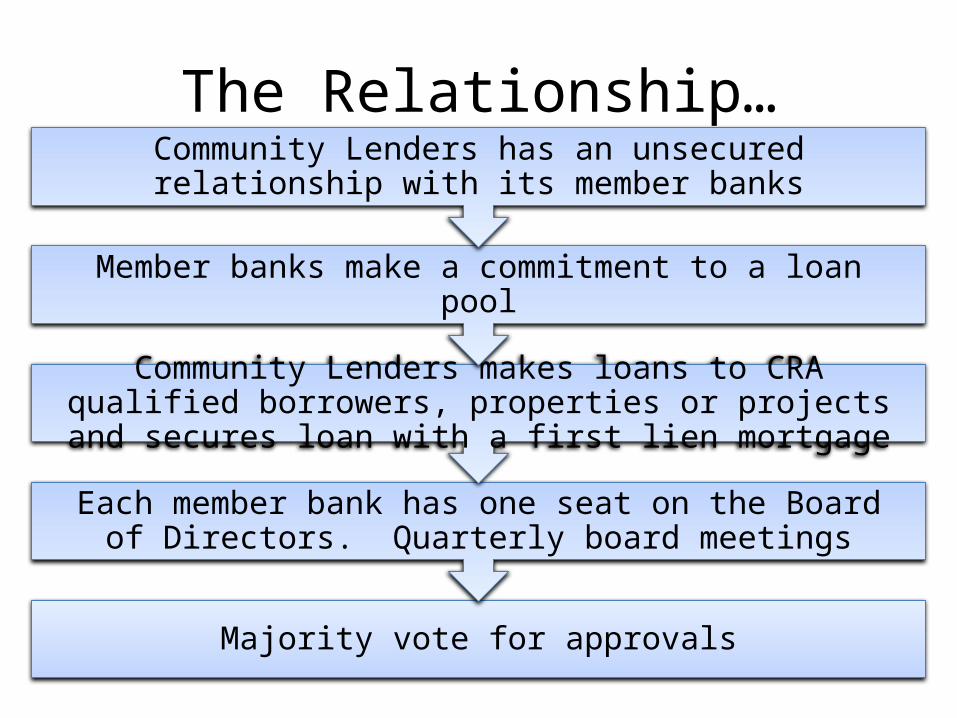

The Relationship…

Majority vote for approvals

Each member bank has one seat on the Board of Directors. Quarterly board meetings

Community Lenders makes loans to CRA qualified borrowers, properties or projects and secures loan with a first lien mortgage

Member banks make a commitment to a loan pool

Community Lenders has an unsecured relationship with its member banks

Loan Products…

Residential – 30 year fixed rate.

Commercial – 25 year fixed rate.

Mixed use – 25 or 30 year fixed rate.

Loan Application Received Loan

Committee

Funding From Member

Banks

Loan Closing

Adding loan to

portfolio

Receipt of Loan

Payments

Monthly Remittances to Member Banks less service fee

Loan Process...

Example of a typical project:Development of a 60 unit affordable senior housing project.

Cost to construct: $12,000,000.00

Sources of Funds:PennHOMES Financing $1,500,000Federal HOME Funds $1,200,000Limited Partner Equity $8,500,000Permanent Financing CLCDC $800,000 *

* Typically the only hard debt. Secured by a 1st lien on the real estate as well as an assignment of rents. Loan is made for a 30 year fixed-rate term.

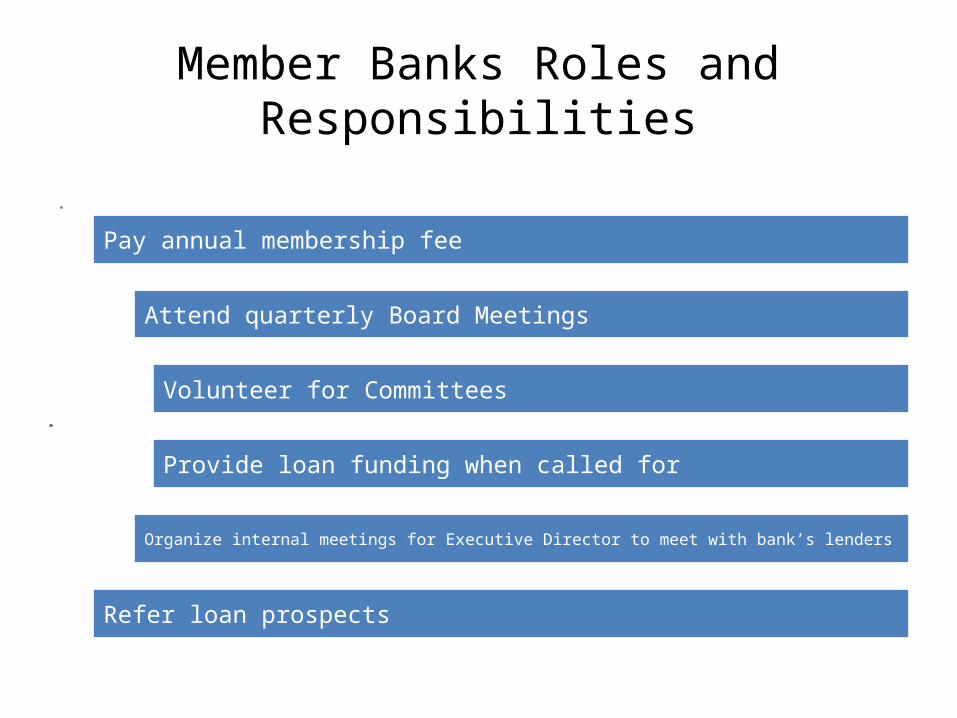

Member Banks Roles and Responsibilities

Pay annual membership fee

Attend quarterly Board Meetings

Volunteer for Committees

Provide loan funding when called for

Organize internal meetings for Executive Director to meet with bank’s lenders

Refer loan prospects

Organizational Goals…

Follow the footprint of our Member Banks.

Grow the loan portfolio to a size where monthly service fees support all expenses.

Be another lending tool for our Member Banks

Make loans which provide our Member Banks with CRA Credit

15

What’s happening in Central PA?

York Housing Advisory Commission - YHAC

Affordable Housing Committee - AHC

Community Lenders Task Force

Replication of Community Lenders?

Why?• Need for affordable housing • Resources shrinking• LIHTC projects are expiring• Can address gap in financing • Model already established

Goal: To serve as a vehicle for community revitalization by financing and investing in housing and related activities designed to address the needs of low to moderate income persons and areas.

Next Steps

• Find a Champion – Lead bank to discuss with other banks.

• Define the Product- Create term sheets to describe loan products.

• Define Projects Parameters- Pre-development? Construction? Housing only? Economic Development too? LITC credits?

• Decide on geographic focus area – York County plus Adams? Dauphin? Franklin?

• Establish a structure – Who will house this?

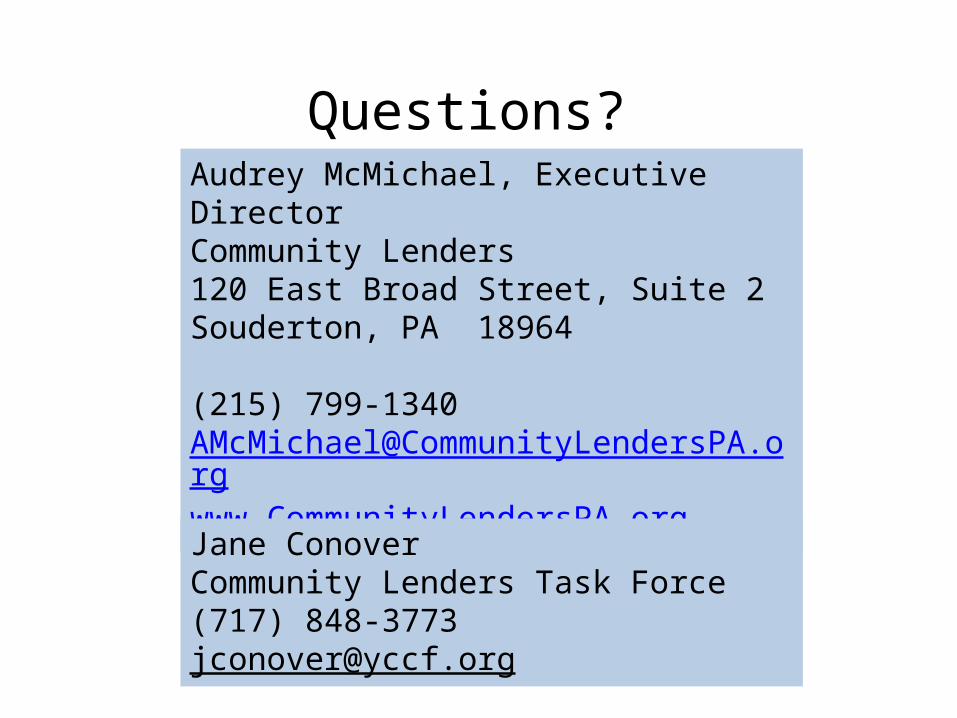

Audrey McMichael, Executive DirectorCommunity Lenders120 East Broad Street, Suite 2Souderton, PA 18964

(215) 799-1340AMcMichael@CommunityLendersPA.orgwww.CommunityLendersPA.org

Questions?

Jane ConoverCommunity Lenders Task Force(717) [email protected]