Embed Size (px)

Citation preview

STRENGTH GROWTH DISCIPLINEMarch 2007

Disclaimer

The Transurban Group is a triple stapled security listed on the Australian Stock Exchange comprising Transurban Holdings Limited (ACN 098 143 429), Transurban Holdings Trust (ARSN 098 807 419) and Transurban International Limited (ARBN 121 746 825). The responsible entity of the Transurban Holdings Trust is Transurban Infrastructure Management Limited (ACN 098 147 678) which is the holder of Australian Financial Services Licence Number 246 585. Transurban Infrastructure Management Limited is a wholly owned subsidiary of Transurban Limited.

This publication has been prepared by the Transurban Group based on the information available. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness or correctness of the information, opinions and conclusions contained in this publication. To the maximum extent permitted by law, neither any member of the Transurban Group, their directors, employees or agents, nor any other persons accepts any liability for any loss arising from the use of this publication or its contents or otherwise arising in connection with it, including without limitation, any liability arising from fault or negligence on the part of any member of the Transurban Group, their directors, employees or agents.

The information contained in this publication does not take into account the investment objectives, financial situation and particular needs of any investor. Further, the information is not intended in any way to influence a person into the varying, acquisition or disposal of a financial product nor provide financial advice nor constitutes an offer to subscribe for securities in the Transurban Group. Any person intending to acquire an interest in the Transurban Group is strongly recommended to seek professional advice. The Transurban Group does not warrant or guarantee the performance, repayment of capital or a particular return of the Transurban Group.

United States

These materials do not constitute an offer of securities for sale in the United States, and the securities referred to in these materials have not been and will not be registered under the United States Securities Act of 1933, as amended, and may not be offered or sold in the United States absent registration or an exemption from registration.

© Copyright Transurban Limited ABN 96 098 143 410. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the written permission of The Transurban Group.

Introduction

The strength of the Transurban brand is based on the owner / operator model

The model has delivered for investors and positioned the Group for continued disciplined growth

Transurban today

• Top ten road investor globally• Premier assets generating strong cash flow• Well positioned for US growth• Group market cap ~ A$6.9B• FY07 forecast yield ~ 7% (1)

Asset Mix %

CityLink100% Ownership and

Operations

Hills M2100% Ownership and

Operations

Westlink M747.5% Ownership

100% Tolling

Pocahontas USA100% Ownership and

Operations

Pocahontas

Hills M231

CityLink54

4WM7

11

1. Based on $7.69 security price

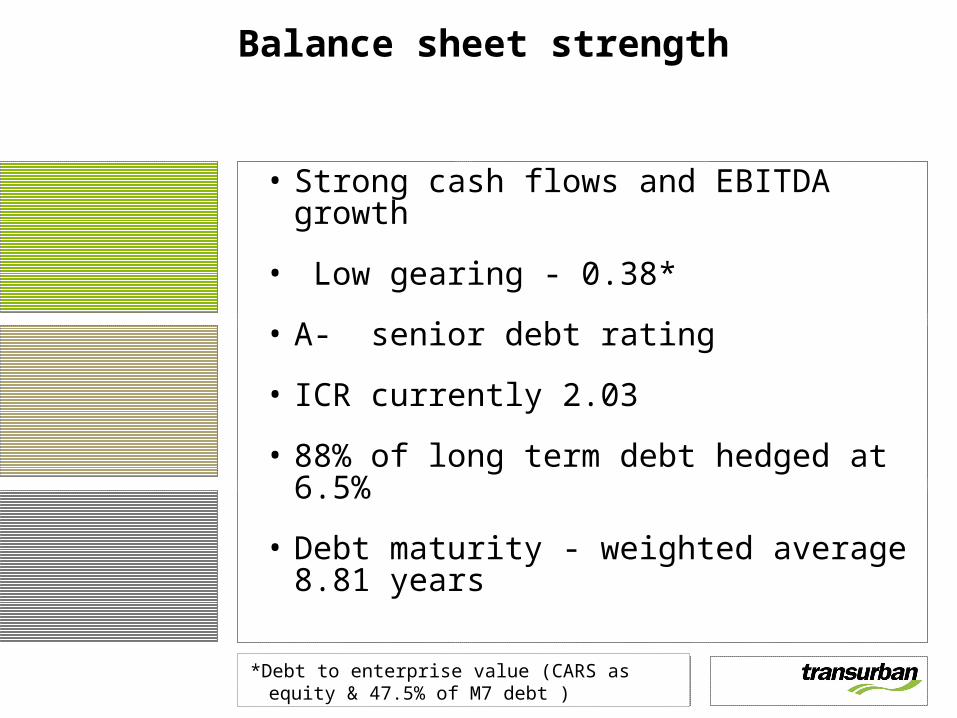

Balance sheet strength

• Strong cash flows and EBITDA growth

• Low gearing - 0.38*

• A- senior debt rating

• ICR currently 2.03

• 88% of long term debt hedged at 6.5%

• Debt maturity - weighted average 8.81 years

*Debt to enterprise value (CARS as equity & 47.5% of M7 debt )

Another successful half year

• EBITDA 19.4%

• Revenue 15.9%

• Operational costs 8.8%

• Corporate costs 5.2%

• Paid FY07 half year distribution of 26.5 cents – full year guidance of 54 cents

• FY08 distribution guidance of 57 cents

Growing distributions

FY07:

• Substantially tax deferred

• Forecast yield~ 7% (1)

0

10

20

30

40

50

60

2002 2003 2004 2005 2006 2007 2008

Cen

ts P

er S

ecur

ity

5.3

20

25.5

35

5054

1. Based on $7.69 security price

57

FOR

ECA

ST

FOR

ECA

ST

Select View/Master/Slide Master to type classification here

QUALITYASSETS

CityLink – Melbourne’s economic spine

1st Half FY 2007

• Traffic 3.3%

• Revenue 8.7%

Enhancements

• Tulla - Calder interchange

– Forecast traffic uplift of 1%

• West Gate – CityLink – Monash upgrade

– Forecast traffic uplift of 7%

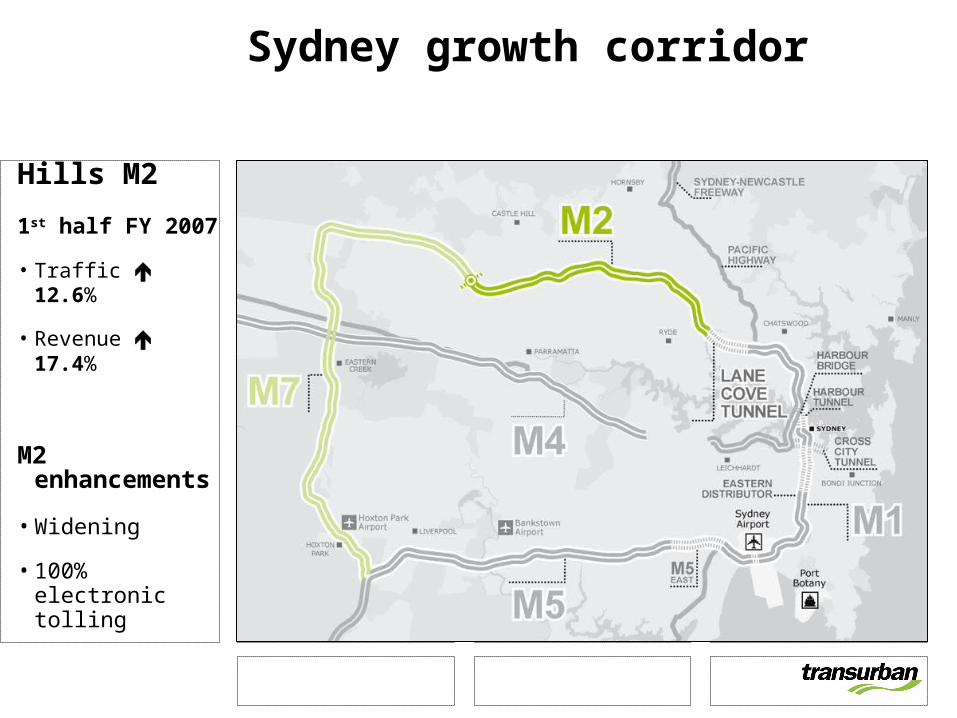

Sydney growth corridor

Westlink M7

Dec Quarter 2006

• Traffic 5.9%*

• Revenue 8.5%*

Future drivers

– Continued land use growth

– Local road congestion

*Percentage change over prior quarter

Sydney growth corridor

Hills M2

1st half FY 2007

• Traffic 12.6%

• Revenue 17.4%

M2 enhancements

• Widening

• 100% electronic tolling

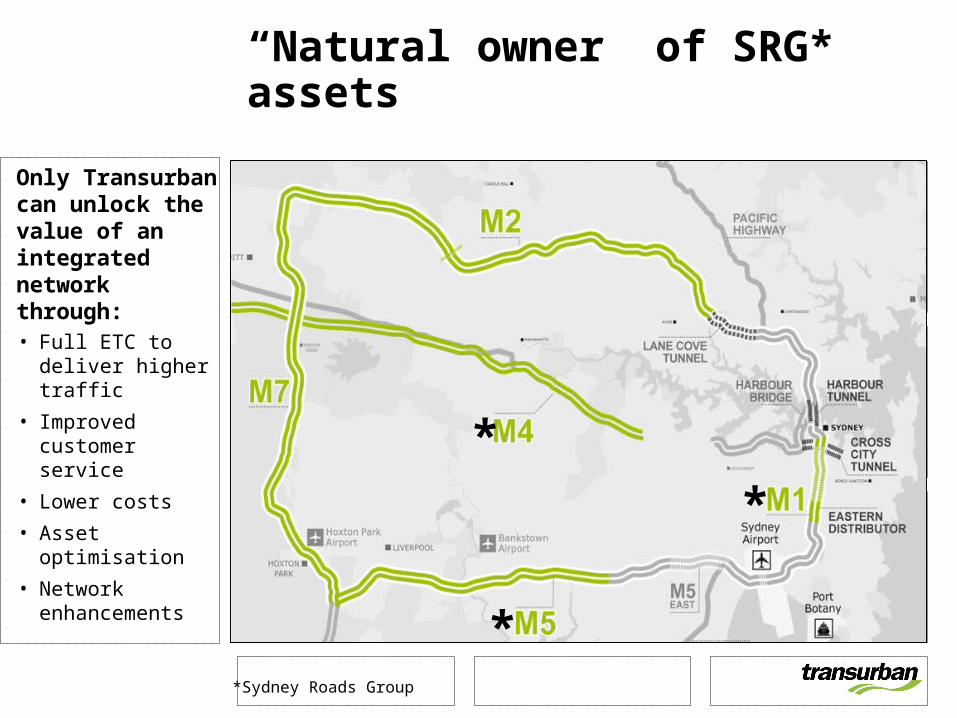

“Natural owner” of SRG* assets

Only Transurban can unlock the value of an integrated network through:• Full ETC to deliver

higher traffic • Improved customer

service• Lower costs• Asset optimisation• Network

enhancements

*Sydney Roads Group

*

*

*

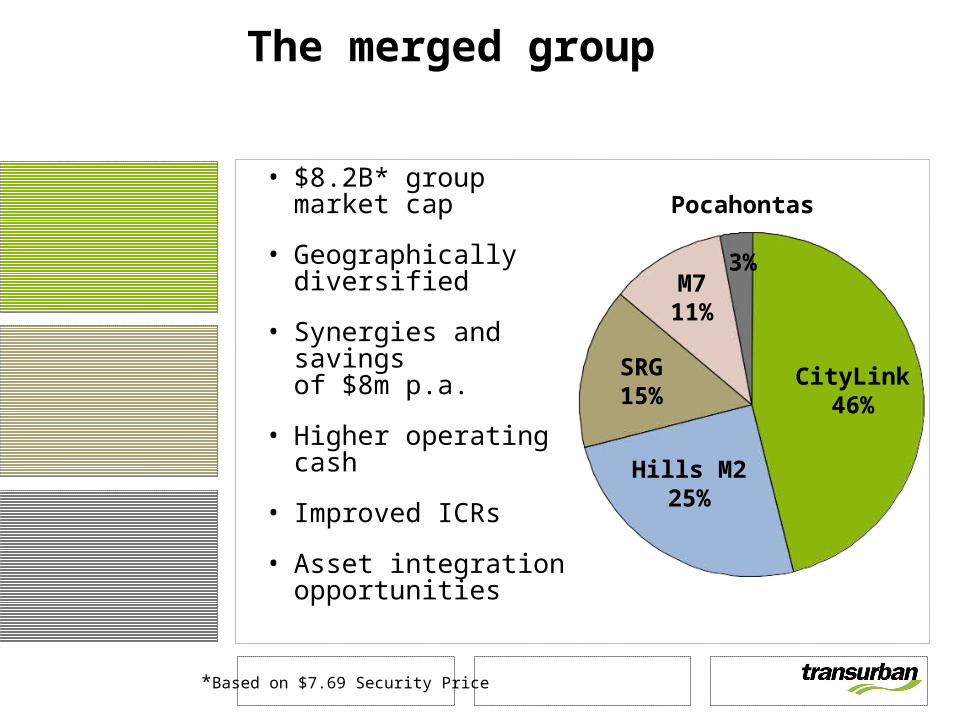

The merged group

• $8.2B* group market cap

• Geographically diversified

• Synergies and savings of $8m p.a.

• Higher operating cash

• Improved ICRs

• Asset integration opportunities

Pocahontas

3%

CityLink46%

Hills M225%

SRG15%

M711%

*Based on $7.69 Security Price

Select View/Master/Slide Master to type classification here

NORTH AMERICA

Virginia, USA projects

• Acquired Pocahontas Parkway

• Preferred status I-95 HOT Lanes

• Exclusive Capital Beltway HOT Lanes

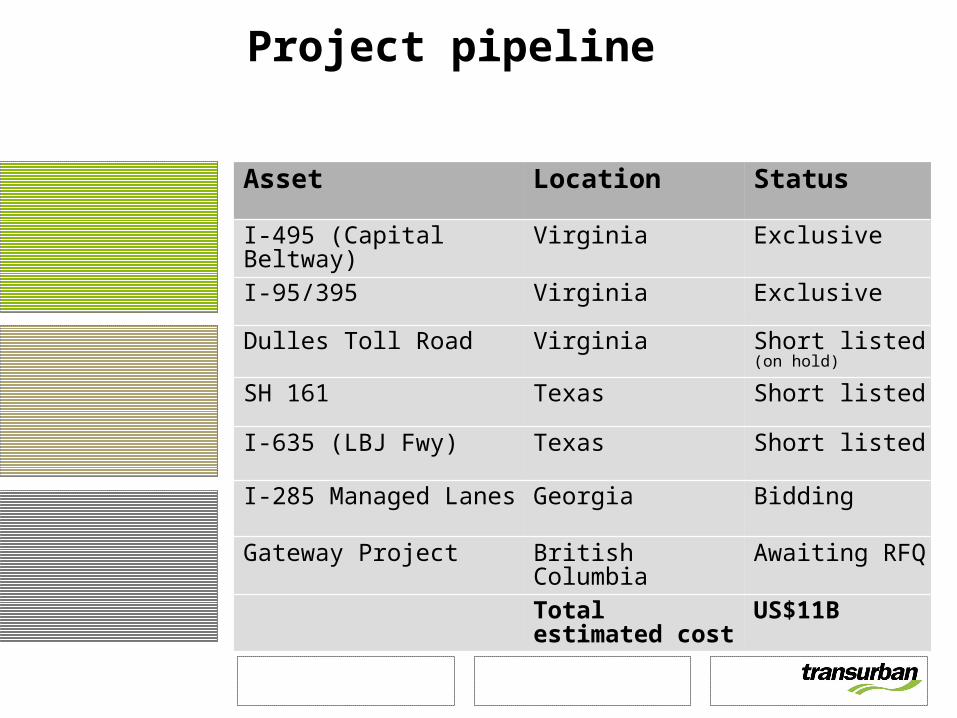

Project pipeline

Asset Location Status

I-495 (Capital Beltway) Virginia Exclusive

I-95/395 Virginia Exclusive

Dulles Toll Road Virginia Short listed (on hold)

SH 161 Texas Short listed

I-635 (LBJ Fwy) Texas Short listed

I-285 Managed Lanes Georgia Bidding

Gateway Project British Columbia Awaiting RFQ

Total estimated cost US$11B

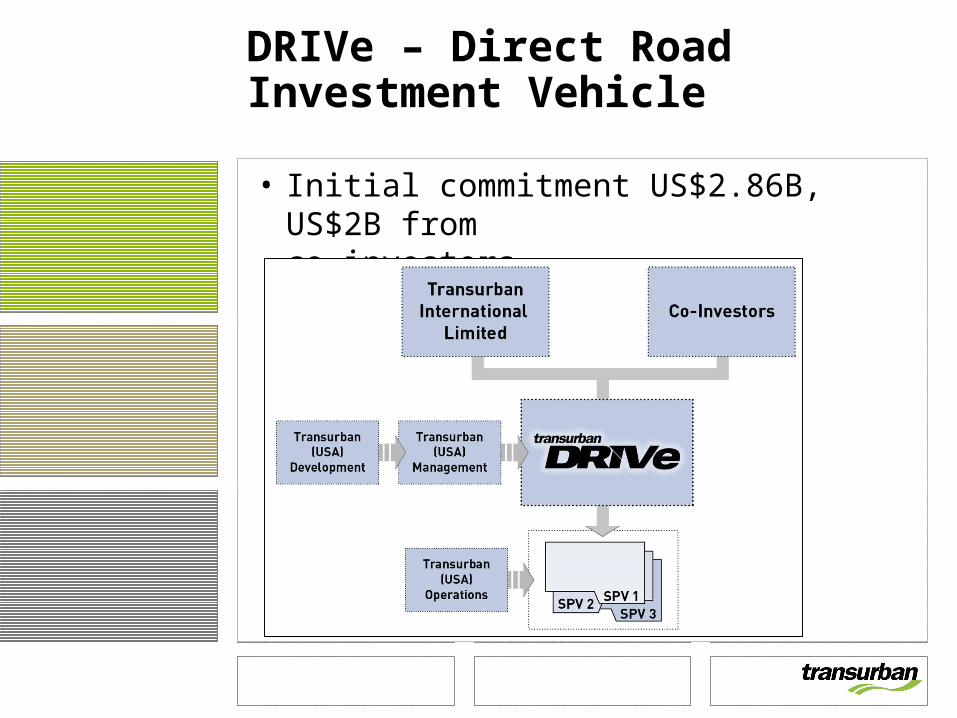

DRIVe – Direct Road Investment Vehicle

• Initial commitment US$2.86B, US$2B from co-investors

Conclusion

• Brand recognition

• Strong financial performance

• Balance sheet strength

• Continue to extract value from existing assets

• Global growth platform