Embed Size (px)

Citation preview

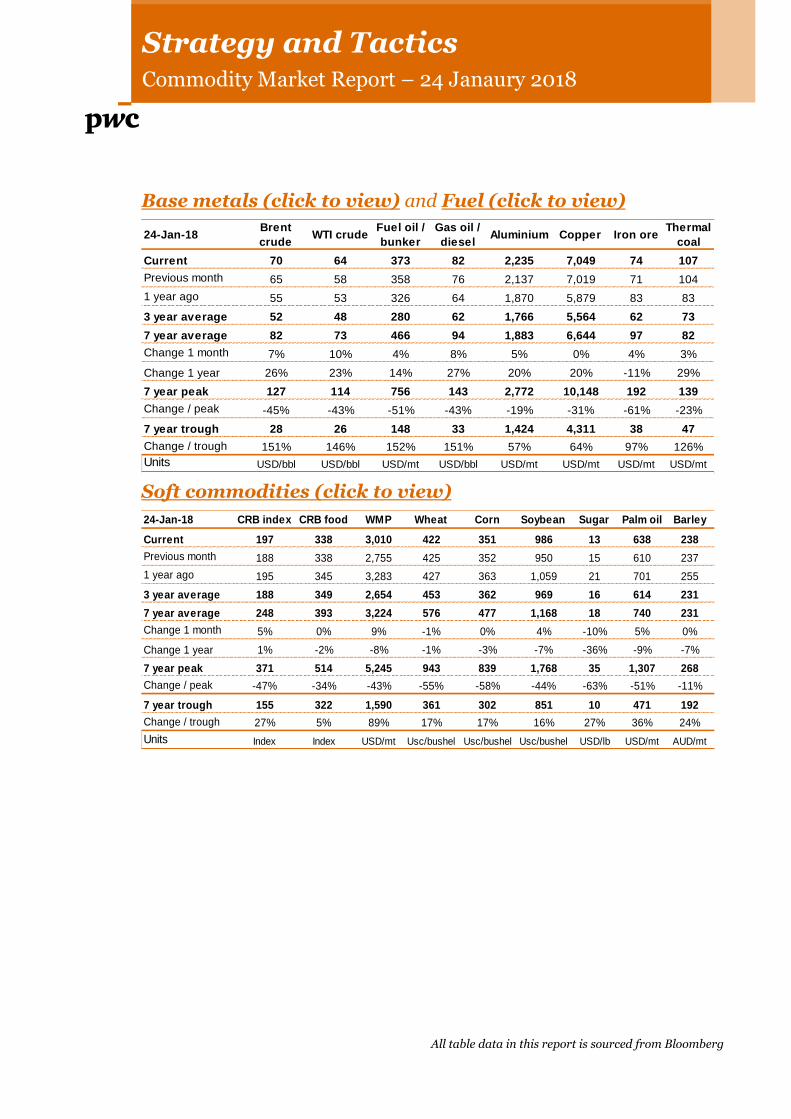

Strategy and Tactics Commodity Market Report – 24 Janaury 2018

All table data in this report is sourced from Bloomberg

Base metals (click to view) and Fuel (click to view)

Soft commodities (click to view)

24-Jan-18Brent

crudeWTI crude

Fuel oil /

bunker

Gas oil /

dieselAluminium Copper Iron ore

Thermal

coal

Current 70 64 373 82 2,235 7,049 74 107

Previous month 65 58 358 76 2,137 7,019 71 104

1 year ago 55 53 326 64 1,870 5,879 83 83

3 year average 52 48 280 62 1,766 5,564 62 73

7 year average 82 73 466 94 1,883 6,644 97 82

Change 1 month 7% 10% 4% 8% 5% 0% 4% 3%

Change 1 year 26% 23% 14% 27% 20% 20% -11% 29%

7 year peak 127 114 756 143 2,772 10,148 192 139

Change / peak -45% -43% -51% -43% -19% -31% -61% -23%

7 year trough 28 26 148 33 1,424 4,311 38 47

Change / trough 151% 146% 152% 151% 57% 64% 97% 126%

Units USD/bbl USD/bbl USD/mt USD/bbl USD/mt USD/mt USD/mt USD/mt

24-Jan-18 CRB index CRB food WMP Wheat Corn Soybean Sugar Palm oil Barley

Current 197 338 3,010 422 351 986 13 638 238

Previous month 188 338 2,755 425 352 950 15 610 237

1 year ago 195 345 3,283 427 363 1,059 21 701 255

3 year average 188 349 2,654 453 362 969 16 614 231

7 year average 248 393 3,224 576 477 1,168 18 740 231

Change 1 month 5% 0% 9% -1% 0% 4% -10% 5% 0%

Change 1 year 1% -2% -8% -1% -3% -7% -36% -9% -7%

7 year peak 371 514 5,245 943 839 1,768 35 1,307 268

Change / peak -47% -34% -43% -55% -58% -44% -63% -51% -11%

7 year trough 155 322 1,590 361 302 851 10 471 192

Change / trough 27% 5% 89% 17% 17% 16% 27% 36% 24%

Units Index Index USD/mt Usc/bushel Usc/bushel Usc/bushel USD/lb USD/mt AUD/mt

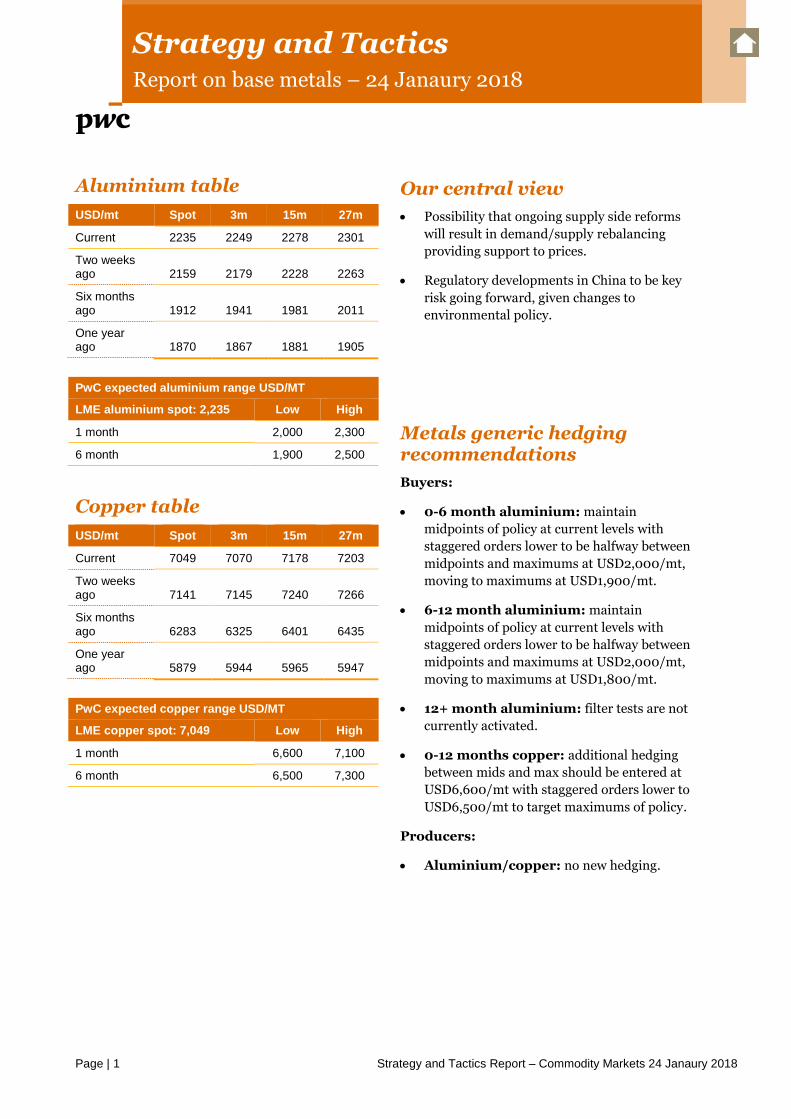

Strategy and Tactics Report on base metals – 24 Janaury 2018

Page | 1 Strategy and Tactics Report – Commodity Markets 24 Janaury 2018

Aluminium table

USD/mt Spot 3m 15m 27m

Current 2235 2249 2278 2301

Two weeks ago 2159 2179 2228 2263

Six months ago 1912 1941 1981 2011

One year ago 1870 1867 1881 1905

PwC expected aluminium range USD/MT

LME aluminium spot: 2,235 Low High

1 month 2,000 2,300

6 month 1,900 2,500

Copper table

USD/mt Spot 3m 15m 27m

Current 7049 7070 7178 7203

Two weeks ago 7141 7145 7240 7266

Six months ago 6283 6325 6401 6435

One year ago 5879 5944 5965 5947

PwC expected copper range USD/MT

LME copper spot: 7,049 Low High

1 month 6,600 7,100

6 month 6,500 7,300

Our central view

Possibility that ongoing supply side reforms

will result in demand/supply rebalancing

providing support to prices.

Regulatory developments in China to be key

risk going forward, given changes to

environmental policy.

Metals generic hedging recommendations

Buyers:

0-6 month aluminium: maintain

midpoints of policy at current levels with

staggered orders lower to be halfway between

midpoints and maximums at USD2,000/mt,

moving to maximums at USD1,900/mt.

6-12 month aluminium: maintain

midpoints of policy at current levels with

staggered orders lower to be halfway between

midpoints and maximums at USD2,000/mt,

moving to maximums at USD1,800/mt.

12+ month aluminium: filter tests are not

currently activated.

0-12 months copper: additional hedging

between mids and max should be entered at

USD6,600/mt with staggered orders lower to

USD6,500/mt to target maximums of policy.

Producers:

Aluminium/copper: no new hedging.

Strategy and Tactics Report on base metals – 24 Janaury 2018

Page | 2 Strategy and Tactics Report – Commodity Markets 24 Janaury 2018

Base metals charts of the week

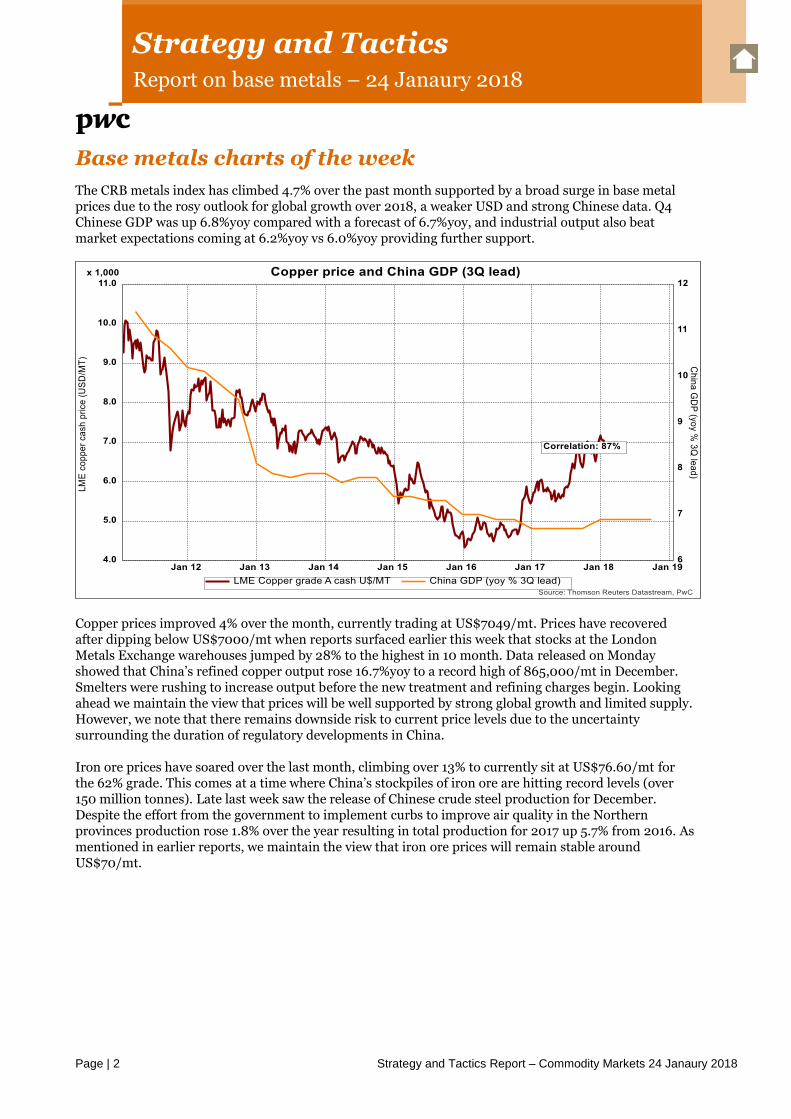

The CRB metals index has climbed 4.7% over the past month supported by a broad surge in base metal prices due to the rosy outlook for global growth over 2018, a weaker USD and strong Chinese data. Q4 Chinese GDP was up 6.8%yoy compared with a forecast of 6.7%yoy, and industrial output also beat market expectations coming at 6.2%yoy vs 6.0%yoy providing further support.

Copper prices improved 4% over the month, currently trading at US$7049/mt. Prices have recovered after dipping below US$7000/mt when reports surfaced earlier this week that stocks at the London Metals Exchange warehouses jumped by 28% to the highest in 10 month. Data released on Monday showed that China’s refined copper output rose 16.7%yoy to a record high of 865,000/mt in December. Smelters were rushing to increase output before the new treatment and refining charges begin. Looking ahead we maintain the view that prices will be well supported by strong global growth and limited supply. However, we note that there remains downside risk to current price levels due to the uncertainty surrounding the duration of regulatory developments in China.

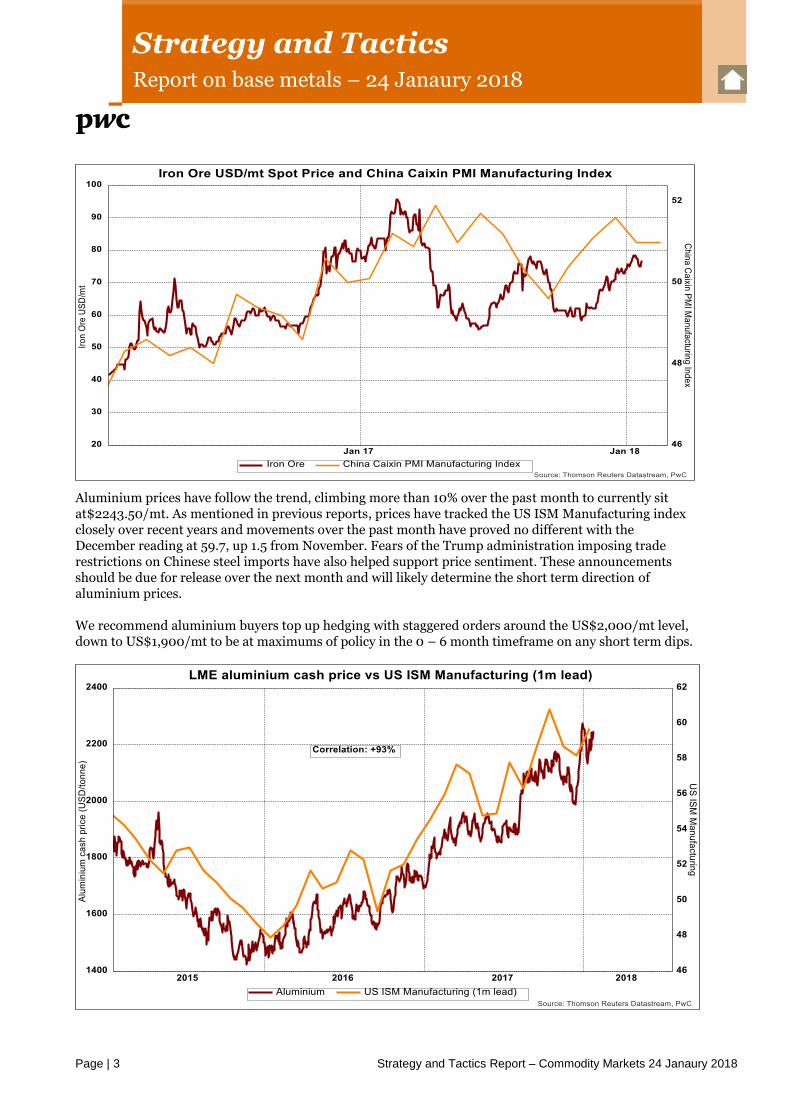

Iron ore prices have soared over the last month, climbing over 13% to currently sit at US$76.60/mt for the 62% grade. This comes at a time where China’s stockpiles of iron ore are hitting record levels (over 150 million tonnes). Late last week saw the release of Chinese crude steel production for December. Despite the effort from the government to implement curbs to improve air quality in the Northern provinces production rose 1.8% over the year resulting in total production for 2017 up 5.7% from 2016. As mentioned in earlier reports, we maintain the view that iron ore prices will remain stable around US$70/mt.

Strategy and Tactics Report on base metals – 24 Janaury 2018

Page | 3 Strategy and Tactics Report – Commodity Markets 24 Janaury 2018

Aluminium prices have follow the trend, climbing more than 10% over the past month to currently sit at$2243.50/mt. As mentioned in previous reports, prices have tracked the US ISM Manufacturing index closely over recent years and movements over the past month have proved no different with the December reading at 59.7, up 1.5 from November. Fears of the Trump administration imposing trade restrictions on Chinese steel imports have also helped support price sentiment. These announcements should be due for release over the next month and will likely determine the short term direction of aluminium prices.

We recommend aluminium buyers top up hedging with staggered orders around the US$2,000/mt level, down to US$1,900/mt to be at maximums of policy in the 0 – 6 month timeframe on any short term dips.

Strategy and Tactics Report on fuels – 24 Janaury 2018

Page | 4 Strategy and Tactics Report – Commodity Markets 24 Janaury 2018

Brent table

USD/bbl Spot 3m 6m 12m 24m

Current 70 69 68 66 62

2wks ago 69 68 67 65 61

6m ago 53 52 53 53 54

1y ago 55 56 57 57 57

Gas oil table

USD/bbl Spot 3m 6m 12m 24m

Current 74 82 81 79 77

2wks ago 81 81 79 78 76

6m ago 64 64 63 63 64

1y ago 64 66 67 68 69

LFO table

USD/bbl Spot 3m 6m 12m 24m

Current 435 453 450 439 382

2wks ago 449 451 449 441 393

6m ago 355 364 362 362 367

1y ago 378 373 376 374 371

PwC expected Brent crude range USD/bbl

Brent crude spot: 70 Low High

1 month 60 70

6 month 55 75

Our central view

Prices are expected to remain range bound

(Brent US$60/bbl – US$70/bbl) over the

coming months based on fundamentals (limited

upward pressure).

We remain sceptical over OPECs ability to

maintain compliance to the production cutting

deal and their ability to materially influence

prices over the coming months as US shale

output grows.

Concerns around US rising shale

production/non-OPEC led production and the

impact on fuel prices continue to negatively

affect market sentiment.

Fuels generic hedging recommendations

Buyers:

0-12 months; buyers maintain midpoints under

USD60/bbl, moving to maximums at USD55/bbl

in the 0-12 months’ time frame.

12-24 months; Stagger low levels of base 12-24

month hedging at prices from USD55/bbl down

to USD50/bbl.

Strategy and Tactics Report on fuels – 24 Janaury 2018

Page | 5 Strategy and Tactics Report – Commodity Markets 24 Janaury 2018

Fuels chart of the week

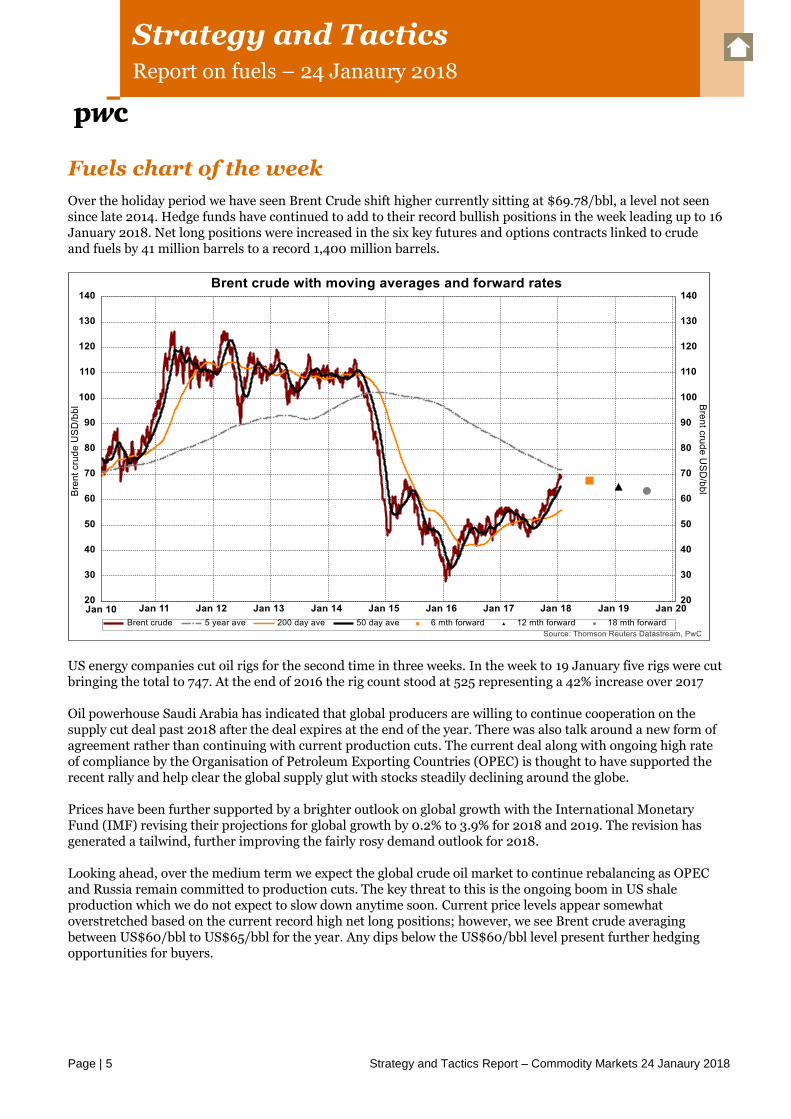

Over the holiday period we have seen Brent Crude shift higher currently sitting at $69.78/bbl, a level not seen since late 2014. Hedge funds have continued to add to their record bullish positions in the week leading up to 16 January 2018. Net long positions were increased in the six key futures and options contracts linked to crude and fuels by 41 million barrels to a record 1,400 million barrels.

US energy companies cut oil rigs for the second time in three weeks. In the week to 19 January five rigs were cut bringing the total to 747. At the end of 2016 the rig count stood at 525 representing a 42% increase over 2017

Oil powerhouse Saudi Arabia has indicated that global producers are willing to continue cooperation on the supply cut deal past 2018 after the deal expires at the end of the year. There was also talk around a new form of agreement rather than continuing with current production cuts. The current deal along with ongoing high rate of compliance by the Organisation of Petroleum Exporting Countries (OPEC) is thought to have supported the recent rally and help clear the global supply glut with stocks steadily declining around the globe.

Prices have been further supported by a brighter outlook on global growth with the International Monetary Fund (IMF) revising their projections for global growth by 0.2% to 3.9% for 2018 and 2019. The revision has generated a tailwind, further improving the fairly rosy demand outlook for 2018.

Looking ahead, over the medium term we expect the global crude oil market to continue rebalancing as OPEC and Russia remain committed to production cuts. The key threat to this is the ongoing boom in US shale production which we do not expect to slow down anytime soon. Current price levels appear somewhat overstretched based on the current record high net long positions; however, we see Brent crude averaging between US$60/bbl to US$65/bbl for the year. Any dips below the US$60/bbl level present further hedging opportunities for buyers.

Strategy and Tactics Report on softs – 24 Janaury 2018

Page | 6 Strategy and Tactics Report – Commodity Markets 24 Janaury 2018

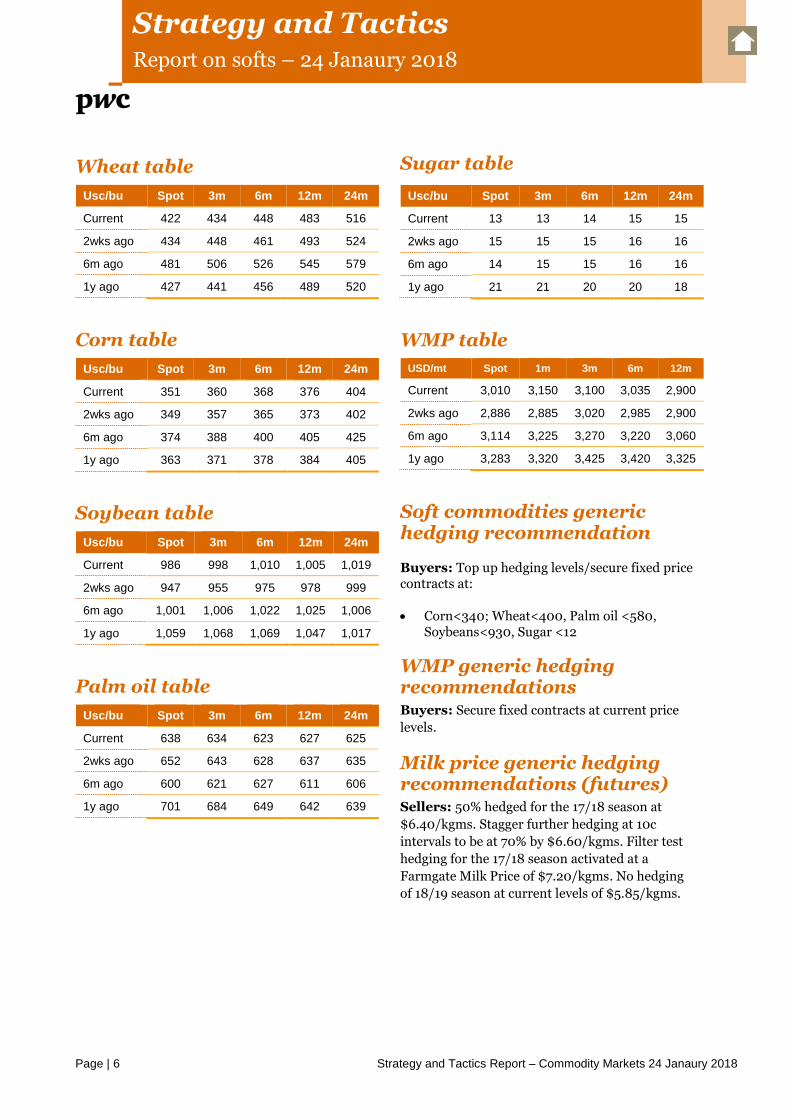

Wheat table

Usc/bu Spot 3m 6m 12m 24m

Current 422 434 448 483 516

2wks ago 434 448 461 493 524

6m ago 481 506 526 545 579

1y ago 427 441 456 489 520

Corn table

Usc/bu Spot 3m 6m 12m 24m

Current 351 360 368 376 404

2wks ago 349 357 365 373 402

6m ago 374 388 400 405 425

1y ago 363 371 378 384 405

Soybean table

Usc/bu Spot 3m 6m 12m 24m

Current 986 998 1,010 1,005 1,019

2wks ago 947 955 975 978 999

6m ago 1,001 1,006 1,022 1,025 1,006

1y ago 1,059 1,068 1,069 1,047 1,017

Palm oil table

Usc/bu Spot 3m 6m 12m 24m

Current 638 634 623 627 625

2wks ago 652 643 628 637 635

6m ago 600 621 627 611 606

1y ago 701 684 649 642 639

Sugar table

Usc/bu Spot 3m 6m 12m 24m

Current 13 13 14 15 15

2wks ago 15 15 15 16 16

6m ago 14 15 15 16 16

1y ago 21 21 20 20 18

WMP table

USD/mt Spot 1m 3m 6m 12m

Current 3,010 3,150 3,100 3,035 2,900

2wks ago 2,886 2,885 3,020 2,985 2,900

6m ago 3,114 3,225 3,270 3,220 3,060

1y ago 3,283 3,320 3,425 3,420 3,325

Soft commodities generic hedging recommendation

Buyers: Top up hedging levels/secure fixed price contracts at:

Corn<340; Wheat<400, Palm oil <580, Soybeans<930, Sugar <12

WMP generic hedging recommendations Buyers: Secure fixed contracts at current price

levels.

Milk price generic hedging recommendations (futures) Sellers: 50% hedged for the 17/18 season at

$6.40/kgms. Stagger further hedging at 10c

intervals to be at 70% by $6.60/kgms. Filter test

hedging for the 17/18 season activated at a

Farmgate Milk Price of $7.20/kgms. No hedging

of 18/19 season at current levels of $5.85/kgms.

Strategy and Tactics Report on softs – 24 Janaury 2018

Page | 7 Strategy and Tactics Report – Commodity Markets 24 Janaury 2018

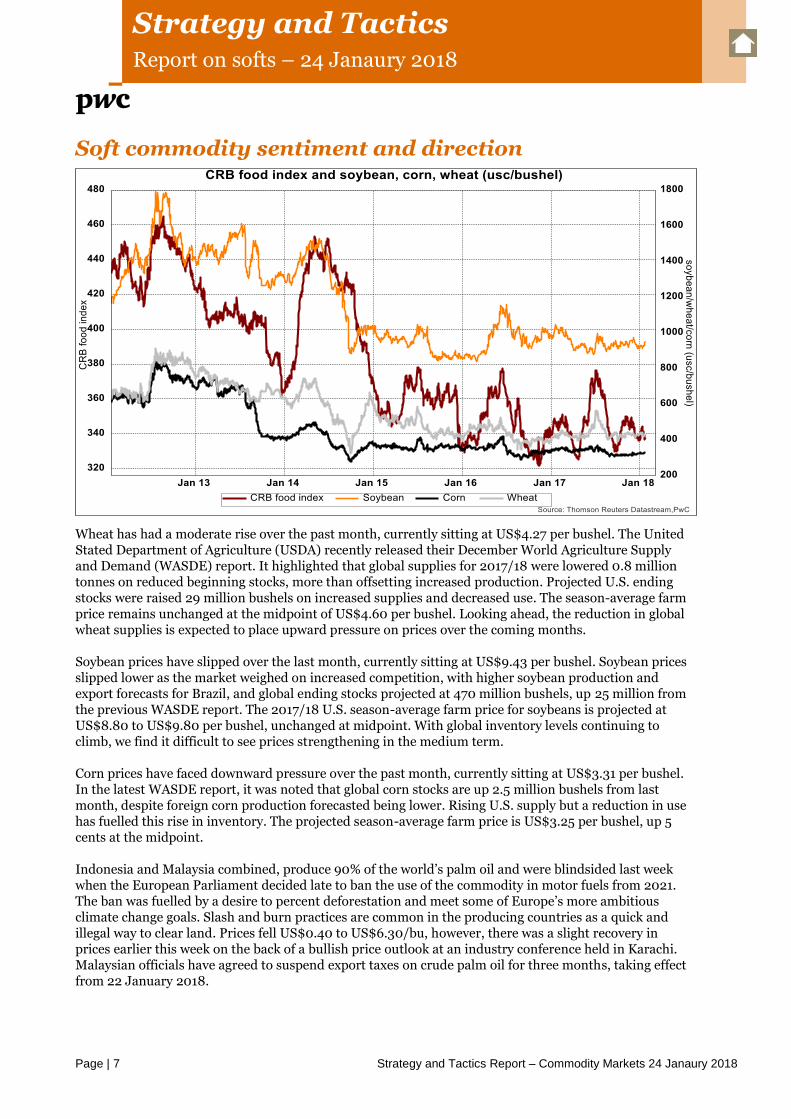

Soft commodity sentiment and direction

Wheat has had a moderate rise over the past month, currently sitting at US$4.27 per bushel. The United Stated Department of Agriculture (USDA) recently released their December World Agriculture Supply and Demand (WASDE) report. It highlighted that global supplies for 2017/18 were lowered 0.8 million tonnes on reduced beginning stocks, more than offsetting increased production. Projected U.S. ending stocks were raised 29 million bushels on increased supplies and decreased use. The season-average farm price remains unchanged at the midpoint of US$4.60 per bushel. Looking ahead, the reduction in global wheat supplies is expected to place upward pressure on prices over the coming months.

Soybean prices have slipped over the last month, currently sitting at US$9.43 per bushel. Soybean prices slipped lower as the market weighed on increased competition, with higher soybean production and export forecasts for Brazil, and global ending stocks projected at 470 million bushels, up 25 million from the previous WASDE report. The 2017/18 U.S. season-average farm price for soybeans is projected at US$8.80 to US$9.80 per bushel, unchanged at midpoint. With global inventory levels continuing to climb, we find it difficult to see prices strengthening in the medium term.

Corn prices have faced downward pressure over the past month, currently sitting at US$3.31 per bushel. In the latest WASDE report, it was noted that global corn stocks are up 2.5 million bushels from last month, despite foreign corn production forecasted being lower. Rising U.S. supply but a reduction in use has fuelled this rise in inventory. The projected season-average farm price is US$3.25 per bushel, up 5 cents at the midpoint.

Indonesia and Malaysia combined, produce 90% of the world’s palm oil and were blindsided last week when the European Parliament decided late to ban the use of the commodity in motor fuels from 2021. The ban was fuelled by a desire to percent deforestation and meet some of Europe’s more ambitious climate change goals. Slash and burn practices are common in the producing countries as a quick and illegal way to clear land. Prices fell US$0.40 to US$6.30/bu, however, there was a slight recovery in prices earlier this week on the back of a bullish price outlook at an industry conference held in Karachi. Malaysian officials have agreed to suspend export taxes on crude palm oil for three months, taking effect from 22 January 2018.

Strategy and Tactics Report on softs – 24 Janaury 2018

Page | 8 Strategy and Tactics Report – Commodity Markets 24 Janaury 2018

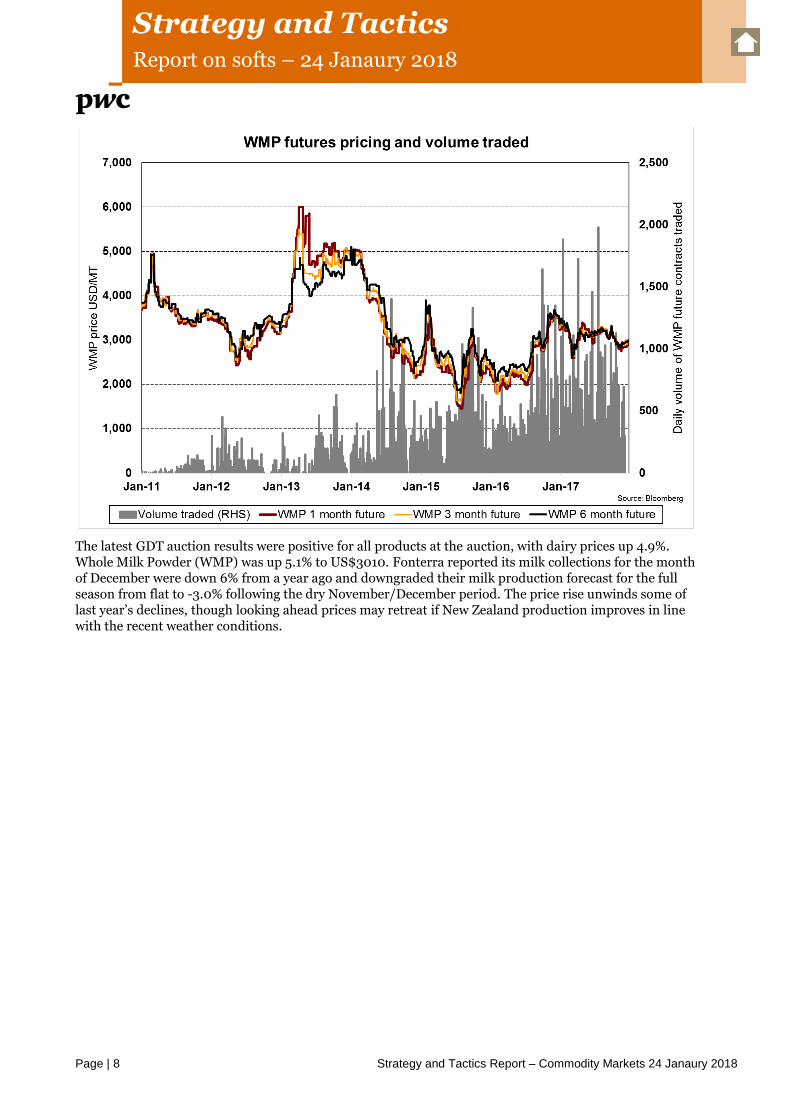

The latest GDT auction results were positive for all products at the auction, with dairy prices up 4.9%. Whole Milk Powder (WMP) was up 5.1% to US$3010. Fonterra reported its milk collections for the month of December were down 6% from a year ago and downgraded their milk production forecast for the full season from flat to -3.0% following the dry November/December period. The price rise unwinds some of last year’s declines, though looking ahead prices may retreat if New Zealand production improves in line with the recent weather conditions.

DISCLAIMER: This report is for PwC retained treasury clients and is subject to the individual agreed engagement letter and

the following restrictions. This report should not be reproduced or supplied to any other party without first obtaining our (PwC

New Zealand) written consent. We accept no responsibility for any reliance that may be placed on our report should it be

used for any purpose other than that set out below and in any event we will accept no liability to any party other than you in

respect of its contents.

The purpose of the report is to document our current financial market views and generic hedging recommendations. The

statements and opinions contained in this report are based on data obtained from the financial markets and are so contained

in good faith and in the belief that such statements, opinions and data are not false or misleading. In preparing this report, we

have relied upon information which we believe to be reliable and accurate. We reserve the right (but will be under no

obligation) to review our assessment and if we consider it necessary, to revise our opinion in the light of any information

existing at the date of this report which becomes known to us after that date. This report must be read in its entirety. Individual

sections of this report could be misleading if considered in isolation from each other.

128002243

Get in touch

Stuart Henderson Partner T: +64 9 425 0158 M:+64 21 343 423 E: [email protected]

Roger Kerr Consultant T: +64 9 355 8181 M:+64 21 935 288 E: [email protected]

Brett Johanson Partner T: +64 4 462 7234 M:+64 21 771 574 E: [email protected]

Chris Hedley Director T: +64 9 355 8183 M: +64 21 479 680 E: [email protected]

James McHardy Director T: +64 4 462 7153 M: +64 21 263 4282 E: [email protected]

Tom Lawson Associate Director T: +64 9 355 8144 M: +64 27 421 0733 E: [email protected]

Alex Wondergem Associate Director T: +64 9 355 8252 M: +64 21 041 2127 E: [email protected]

Hasthika Ekneligoda Treasury Analyst T: +64 9 355 88855 E: [email protected]

James Butler Treasury Advisor T: +64 9 355 8265 E: [email protected]

Tom North Treasury Analyst T: +64 9 355 8497 E: [email protected]

Ollie McDowell Treasury Advisor T:+64 9 355 8702 E: [email protected]

Matt Stewart Treasury Analyst T: +64 5 462 7037 E: [email protected]

www.pwc.co.nz/treasury-and-debt-advisory