Embed Size (px)

Citation preview

Strategic Environmental Assessment (SEA) for Industry Sector Himachal Pradesh, India

Draft Final Report

Disaster Risk Management & Climate Change Unit

South Asia Sustainable Development Department

The World Bank, Washington

December 2013 (version 23/12/13)

Draft report for internal use only. Do not cite.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Confidential Draft – Do Not Cite

HP Industry SEA Page ii December 2013 (Draft 23/12/13)

Copyright © 201# The International Bank for Reconstruction and Development/The World Bank 1818 H Street, N.W. Washington, D.C. 20433, U.S.A. All rights reserved

Manufactured in _____ First Printing: ____ 201# printed on recycled paper

[Standard text and additional disclaimers will come here along the following lines: World Bank Country Studies, Strategic Environmental Assessments, and similar diagnostic studies are among the many reports originally prepared for internal use as part of the continuing analysis by the Bank of the economic and related conditions of its developing member countries and to facilitate its dialogs with the governments. Some of the reports are published in this series with the least possible delay for the use of governments, and the academic, business, financial, and development communities. The manuscript of this paper therefore has not been prepared in accordance with the procedures appropriate to formally edited texts. Some sources cited in this paper may be informal documents that are not readily available. The findings, interpretations, and conclusions herein are those of the author(s) and do not necessarily reflect the views of the International Bank for Reconstruction and Development/The World Bank and its affiliated organizations, or those of the Executive Directors of The World Bank or the governments they represent. The World Bank does not guarantee the accuracy of the data included in this work. The boundaries, colors, denominations and other information shown on any map in this work do not imply any judgment on the part of The World Bank of the legal status of any territory, or the endorsement or acceptance of such boundaries. The material in this publication is copyrighted. Copying and/or transmitting portions or all of this work without permission may be a violation of applicable law. The International Bank for Reconstruction and Development/The World Bank encourages dissemination of its work and will normally grant permission promptly to reproduce portions of the work. For permission to photocopy or reprint any part of this work, please send a request with complete information to the Copyright Clearance Centre, Inc., {insert correct address and contacts} All other queries on rights and licenses, including subsidiary rights, should be addressed to the Office of the Publisher, The World Bank, 1818 H Street NW, Washington, DC 20433 USA {insert correct contacts}] LC Cataloging-‐in-‐Publication Data

Confidential Draft – Do Not Cite

HP Industry SEA Page iii December 2013 (Draft 23/12/13)

Acknowledgements The World Bank Task Team for this SEA work includes Muthukumara S. Mani (TTL), Camille Bann, Cynthia Cartier, Jack Ruitenbeek, and Vaideeswaran Sankaran.1 This work was undertaken over the

period April-‐December 2013, including extensive consultations and interactions with stakeholders in Himachal Pradesh, India. The SEA Team gratefully acknowledges the presence of all those participating in workshops and information sessions. Specifically, contributions from the following

are acknowledged, who provided leadership and guidance during those events and subsequent data gathering exercises: Mr Mohan Chauhan (Director, Department of Industry); Dr Rajinder Chauhan

(Sr. Industrial Advisor, Department of Industry); Dr SS Negi (Director, Environment, Department of Environment, Science and Technology – DEST); Mr Suresh Attri (DEST); Mr Vineet Kumar (IFS & Member-‐Secretary, HP State Pollution Control Board – SPCB, Shimla); Mr Sanjay Sood (IFS & Former

Member-‐Secretary, HP SPCB, Shimla); Mr Chetan Joshi (Senior Environmental Engineer, HP SPCB, Baddi); Mr Brij Bhushan (HP SPCB, Una); Mr Shandil SK (HP SPCB, Shimla); Mr Gopal Gautam (HP SPCB, Shimla); Mr Chetan Joshi (SPCB, Baddi); Mr Rajender Guleria (Chair, Baddi Barotiwala Nalagarh

Industrial Association – BBNIA); and, Pyush Dogra (Senior Environmental Specialist, World Bank, Delhi). The SEA Team is also appreciative of the assistance of the following in Baddi-‐Barotiwala-‐Nalagarh during the site visits: Mr Rajeshwar Goel (Additional CEO, Baddi Barotiwala Nalagarh

Development Authority – BBNDA); Mr Keshav Chandel (CEO, Baddi Infrastructure, BBNIA); and, Mr Ashok Kumar Sharma (CEO, Shivalik Solid Waste Management Ltd).

1 Contacts: Muthukumara S Mani ([email protected]); Camille Bann ([email protected]); Cynthia Cartier ([email protected]); Jack Ruitenbeek ([email protected]); Vaideeswaran Sankaran ([email protected]).

Confidential Draft – Do Not Cite

HP Industry SEA Page iv December 2013 (Draft 23/12/13)

Abbreviations AGiSAC Aryabhatta Geo-‐informatics & Space

Application Centre API Active Pharmaceutical Ingredients BBNDA Baddi Barotiwala Nalagarh Development

Authority BBNIA Baddi Barotiwala Nalagarh Industrial

Association BOD Biochemical Oxygen Demand CAC Command and Control CBA Cost Benefit Analysis CDM Clean Development Mechanism CEA Cost Effectiveness Analysis CEPI Comprehensive Environmental Pollution

Index CER Certified Emission Reduction CETP Common Effluent Treatment Plant CO2e carbon dioxide equivalent COD Chemical Oxygen Demand COPD Chronic Obstructive Pulmonary Disease CPCB Central Pollution Control Board CREP Corporate Responsibility for

Environmental Protection CTE Consent to Establish CTO Consent to Operate DALY Disability Adjusted Life Year DEST Department of Environment and Science

and Technology DOI Department of Industry DPL Development Policy Loan DPR Detailed Project Report EIA Environmental Impact Assessment EIRR economic internal rate of return EMP Environment Master Plan ESS Environment Surveillance Scheme FIRR financial internal rate of return GDP gross domestic product GHG greenhouse gas GoHP Government of Himachal Pradesh GOI Government of India HP Himachal Pradesh HSD High Speed Diesel IGG Inclusive Green Growth IPPS Industrial Pollution Projection System ISO International Organization for

Standardization KLPD kilo liter per day LADF Local Area Development Fund MBI Market Based Instrument

MINARS Monitoring of Indian National Aquatic Resources

MINAS Minimum National Standards MLD millions of liters a day MOEF Ministry of Environment and Forests MoUD Ministry of Urban Development MSME Micro, Small and Medium Enterprise MSW Municipal Solid Waste MT metric tonnes NAAQM National Air Quality Monitoring NGT National Green Tribunal NOx nitrous oxides NPV Net Present Value OECD Organisation for Economic Cooperation

and Development PES Payment for Ecosystem Services PIL Public Interest Litigation PM10 Particulate Matter ≤10 micrometers ppm parts per million RPM respirable particulate matter SCM supply chain management SEA Strategic Environmental Assessment SEAC State Expert Appraisal Committee SEIAA State Environmental Impact Assessment

Authority SIDBI Small Industries Development Bank of

India SME small or medium enterprise SOx sulphur oxides SPCB State Pollution Control Board SPM Suspended Particulate Matter SSI Small Scale Industry SWCM Single Window Clearance and Monitoring SWF Social Welfare Function SWM solid waste management TA Technical Assistance TDS Total Dissolved Solids TEV Total Economic Value TPD tonnes per day TSDF Treatment Storage and Disposal Facilities ULB Urban Local Body VOC volatile organic compound WAVES Wealth Accounting & Valuation of

Ecosystem Services WTAC Willingness to Accept Compensation WTP Willingness to Pay WWTP Wastewater Treatment Plant

Confidential Draft – Do Not Cite

HP Industry SEA Page v December 2013 (Draft 23/12/13)

Table of Contents Acknowledgements ............................................................................................................................................... iii Abbreviations ......................................................................................................................................................... iv Table of Contents .................................................................................................................................................... v

EXECUTIVE SUMMARY ..................................................................................................... vii §1 Introduction .................................................................................................................................................. 1

Part I FOUNDATIONS ....................................................................................................... 8 §2 Institutional Review ...................................................................................................................................... 9 §3 Pollution Hotspots & Priority Polluting Industries ...................................................................................... 18 §4 Health & Environmental Impacts of Industrial Pollution in Himachal Pradesh ........................................... 28 §5 Economic Instruments for Environmental Management in Himachal Pradesh .......................................... 32

Part II DIAGNOSTICS ....................................................................................................... 38 §6 MSME Scheme – Mid-‐Study Recommendation Report .............................................................................. 39 §7 Background to the Case Studies ................................................................................................................. 51 §8 Case Study 1 – Pharmaceuticals .................................................................................................................. 61 §9 Case Study 2 – Stone Crushing .................................................................................................................... 65 §10 Case Study 3 – Food Processing ................................................................................................................ 74 §11 Cost Effectiveness ..................................................................................................................................... 77

PART III WAY FORWARD ............................................................................................... 84 §12 Summary of Recommendations ................................................................................................................ 85

ANNEXES ......................................................................................................................... 89 Annex A References ......................................................................................................................................... 90 Annex B Key Meetings & Participants .............................................................................................................. 94 Annex C Supplementary Data – Industries & Criteria Pollutants ..................................................................... 95 Annex D Supplementary Valuation Sources & Information ........................................................................... 101 Annex E Economic Instruments Framework .................................................................................................. 105 Annex F Supplementary Data – Miscellaneous & Case Studies ..................................................................... 111 Annex G Cost Effectiveness Templates .......................................................................................................... 131 Annex H Maps (placeholder) ......................................................................................................................... 135 Internal Confidential Notes (remove before publication) ................................................................................. 143

Confidential Draft – Do Not Cite

HP Industry SEA Page vi December 2013 (Draft 23/12/13)

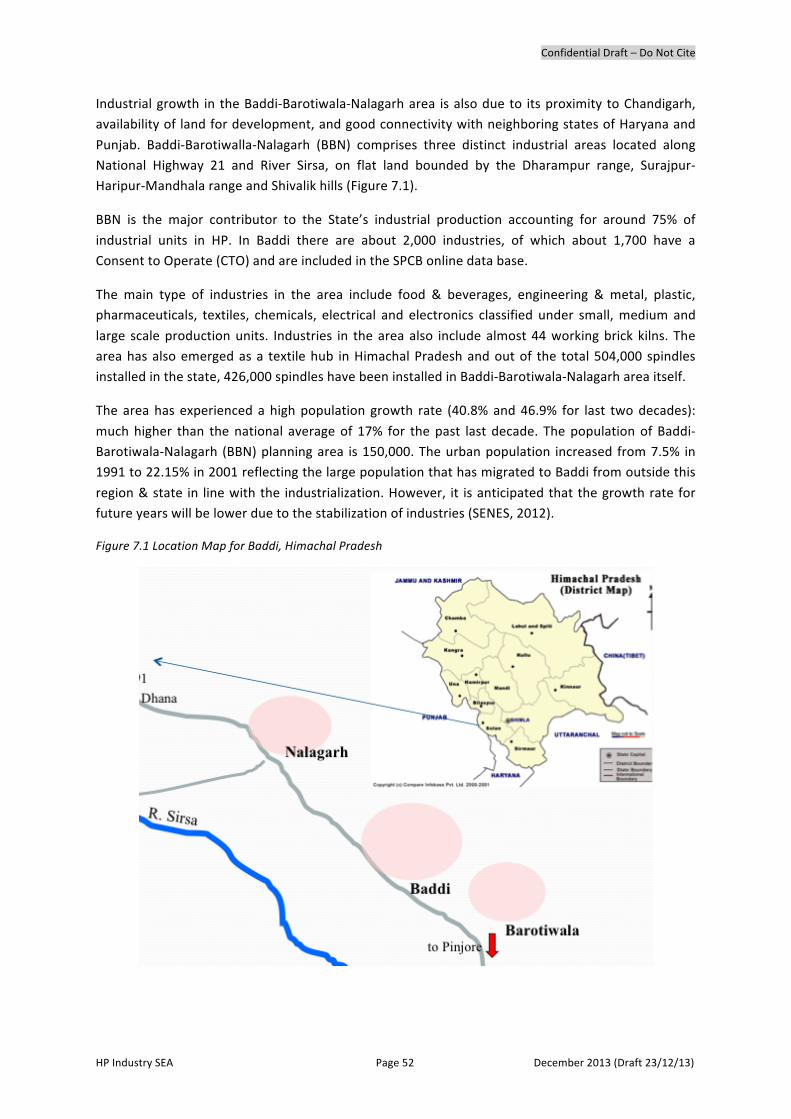

Map ES.1. Himachal Pradesh, India is a mountainous state in Northern India with an area of 55,673 km² and a population of 6,856,509 (2011 census). Main industrial corridors are developing along the border with Punjab and Haryana, where most of the urban population lives. The Districts of Solan, Sirmour and Kangra are of particular high priority due to current industrial concentrations, future growth prospects, and identified pollution concerns associated with both water and air pollution.

Confidential Draft – Do Not Cite

HP Industry SEA Page vii December 2013 (Draft 23/12/13)

EXECUTIVE SUMMARY

Background Himachal Pradesh (HP) is a rapidly industrializing

mountain state in northern India that also depends on its abundant natural and environmental resources as a basis for broad-‐based tourism and provision of services to its population of about 7 million people (Map ES.1). The HP Strategic Environmental Assessment (SEA) is a

technical assistance (TA) to identify priority industrial pollutants and economic instruments to minimize industrial waste. The TA involved a consultative process to obtain feedback on priority industries and pollutants, and to assist in information collection. The SEA complements a World Bank Development Policy Loan (DPL) that addresses “Inclusive Green Growth”: the DPL seeks to provide policy and programmatic support to promote environmentally sustainable industrial development by reducing pollution of existing industrial plants and to promote cleaner sources of economic growth. The specific objectives of the SEA are achieved

through a combination of research and analytical work based on secondary data and feedback from stakeholders in HP. The process has included priority-‐setting workshops, development of case studies, and advice on appropriate measures that can be taken to support the DPL through identifying options for implementing economic instruments that encourage cleaner production in the state’s micro-‐, small and medium enterprise (MSME) sector. In support of this, the SEA also conducted a best international practice review of economic instrument systems, and conducted selected economic valuations of potential health and environmental effects of pollution in HP. The SEA also updated existing institutional reviews to

provide a basis for recommendations relating to ongoing capacity building associated with any new policies. The capacity building is associated with greater integration of environmental economic methods into state policies: this ranges from use of cost-‐effectiveness analyses that reflect environmental costs, to development of better statistical infrastructure to conduct valuation, to enhanced training of local stakeholders in the use of such tools.

Himachal Pradesh can be a national leader in the adoption and implementation of modern methods

of pollution abatement and management.

Industrial Pollution Hotspots HP industrial development policies will result in

potentially significant contributions and growth from industries in the pharmaceutical and agro-‐processing sectors: while these will have potentially significant environmental impacts, addressing these through best-‐available practice at an early stage can improve overall economic efficiency and environmental sustainability. With the incentivized investment climate in HP, the

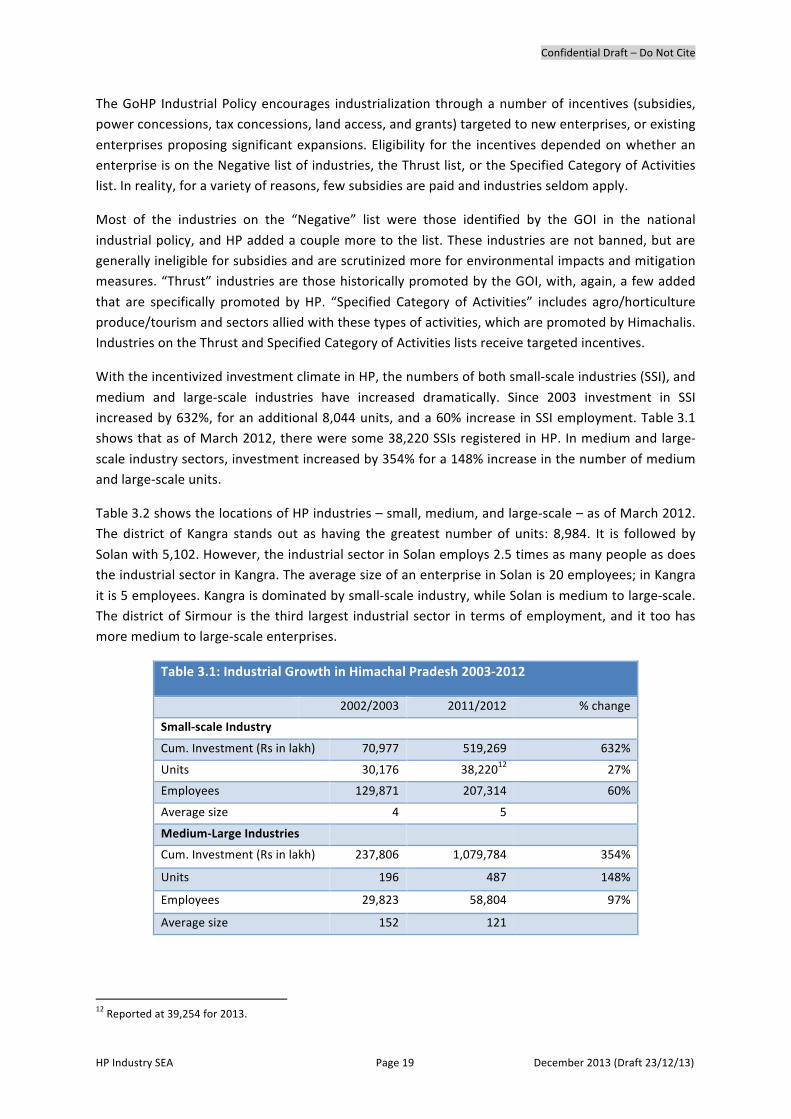

numbers of both small-‐scale industries (SSI), and medium and large-‐scale industries have increased dramatically. Since 2003 investment in SSI increased by 632% and a 60% increase in SSI employment. In medium and large-‐scale industry sectors, investment increased by 354% for a 148% increase in the number of medium and large-‐scale units.

Air, water and hazardous wastes from industries can generally be managed through best available technologies in larger industries. A significant challenge is the proliferation of micro and small enterprises engaged in, or allied to, chemical and textile production. Industry generates about one-‐quarter of GHGs in the

State and this share could rise in the absence of pro-‐active efforts. Such efforts could focus on enterprise energy efficiency, adoption of best available technologies for process design, and green building design mandated through building codes.

Industrial growth has been significant in Himachal Pradesh, largely in response to targeted incentives, with industrial hotspots arising in the Districts of

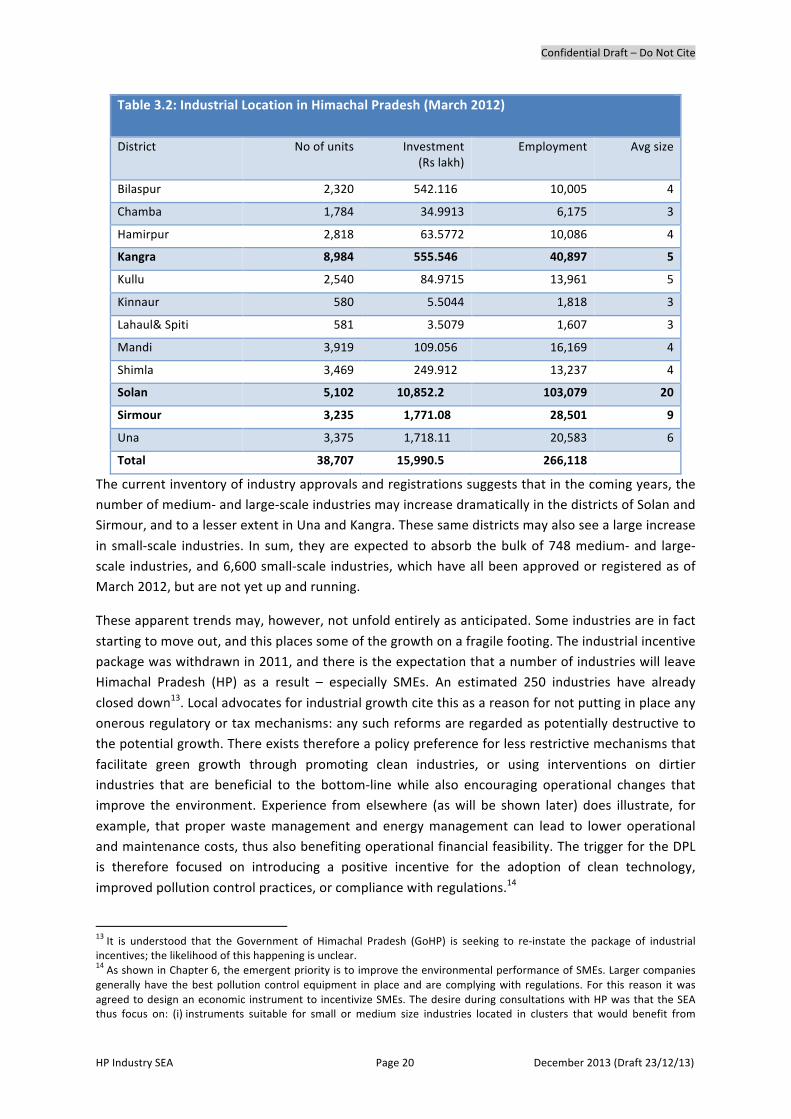

Solan, Sirmour, and Kangra.

Institutional Opportunities & Constraints The DEST (DEST) and State Pollution Control Board

(SPCB) are maturing into important policy and regulatory players in Himachal Pradesh. Recent initiatives have also culminated in 2013 in the development of an Environment Master Plan for HP, and notification of policies associated with Payment for Ecosystem Services (PES). Weaknesses in institutional monitoring capacity still

result in information gaps that hinder effective selection of optimal regulatory policies. Main gaps are associated with the scale and types of industrial sectors operating in the hotspots, and up-‐to-‐date pollution information and concentration data from these sectors. The existing information can, however, help guide the design of efficient economic instruments that can be tested in some of these hotspots and sectors. Recent initiatives have shown that DEST can work in

partnership with industry for proactive environmental management. Also, a commitment to multi-‐stakeholder collaboration can inform the development of State Environmental Policy.

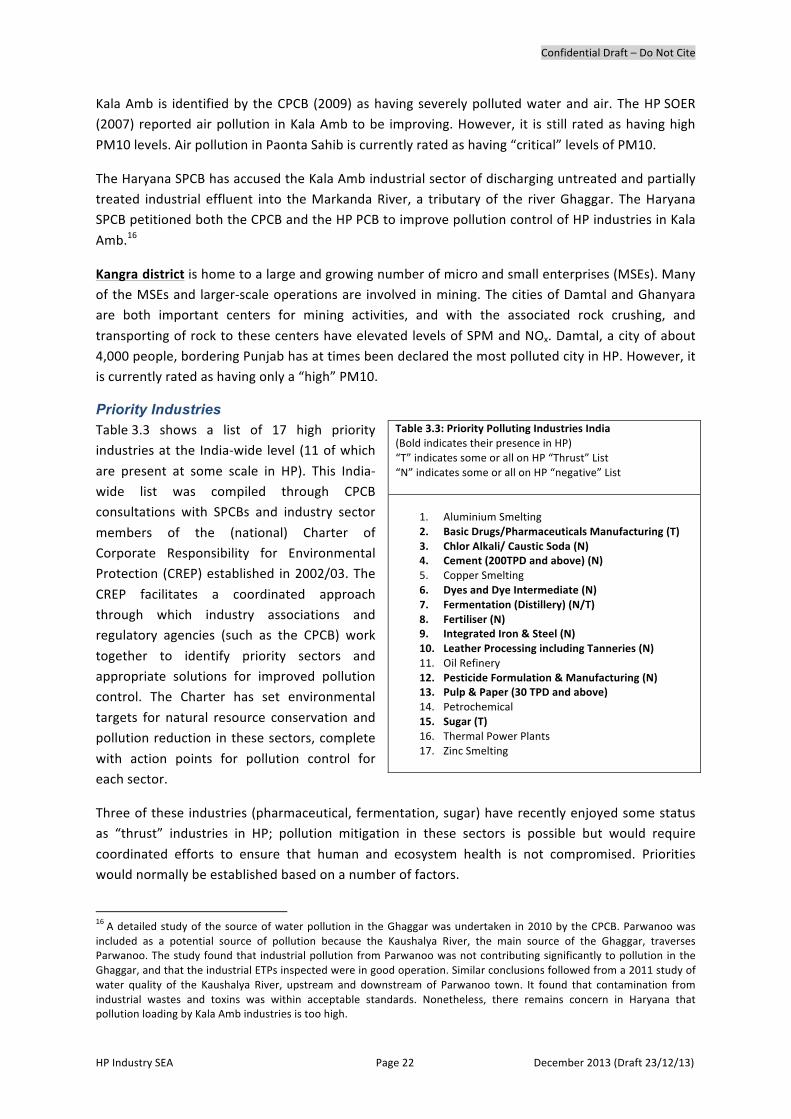

Priority Sectors Of 17 priority traditionally high polluting industries in

India, 11 are currently present in Himachal Pradesh. Three of these industries (pharmaceutical, fermentation, sugar) have recently enjoyed some status as “thrust” industries in HP; pollution mitigation in these sectors is possible but will require coordinated efforts to ensure that human and ecosystem health is not compromised. Some polluting industries on the negative list (e.g.,

those associated with dyes and tanneries) will be more difficult to address due to their high cost of intervention if they persist at a small scale. The use of thrust and negative lists is a useful means

for documenting and potentially regulating industries, but it should be recognized that even negative industries might grow and require regulation.

Incentives used to encourage thrust industries may also be directed more aggressively to those industries that have a potentially positive

environmental footprint: ecotourism, biotech, and nanotech are examples.

Confidential Draft – Do Not Cite

HP Industry SEA Page viii December 2013 (Draft 23/12/13)

Health Linkages Industrial pollution will have negative impacts on

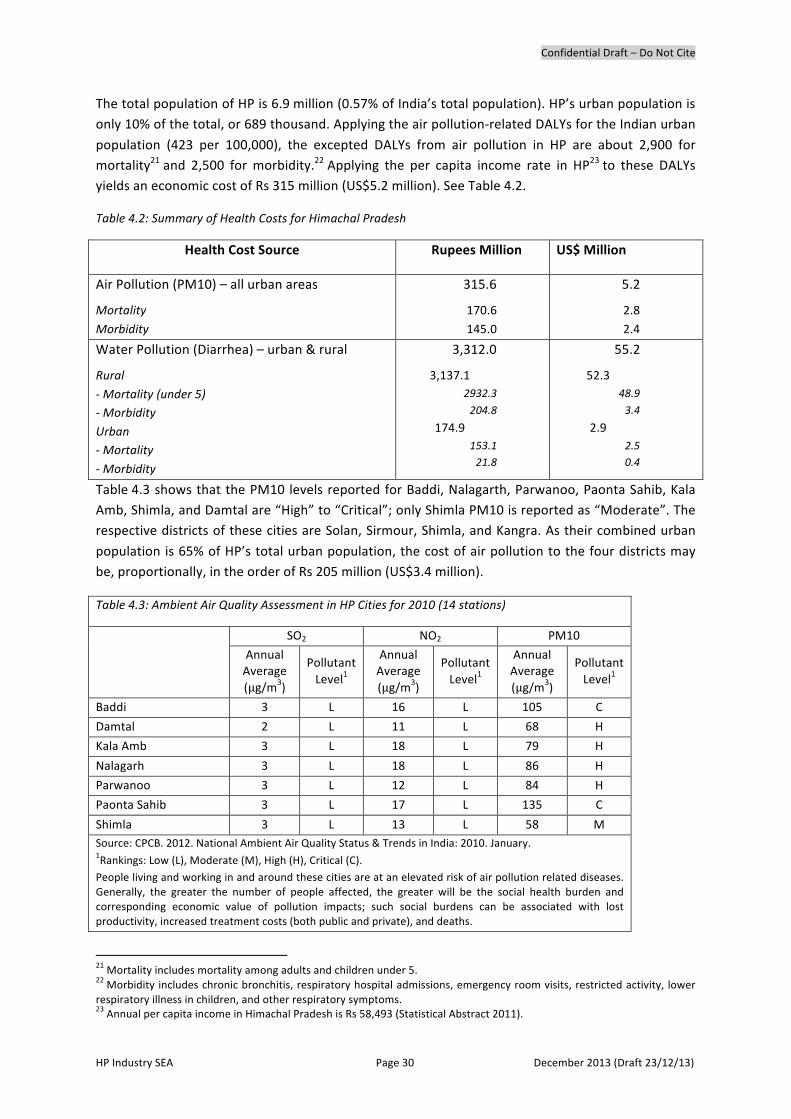

human and ecosystem health if not mitigated. Air pollution from PM10 is a leading cause of the disease burden in urban areas of HP; most water pollution disease burden is more associated with non-‐industrial sources. Benefits (including human and environmental health)

are still relevant in comparing pollutants but finding a common denominator in money or physical terms is problematic. Interventions for most pollutants are most cost effective if they are preventative – targeting future developments. In addition, especially for air pollution, they need to be restorative to address the pollution impacts from existing facilities. Economic valuation suggests that annual economic

losses associated with pollution in Himachal Pradesh may approach Rs 315 million (US$5.2 million) for air pollution and Rs 175 million (US$2.9 million) for water pollution in urban areas. These values are based on detailed India-‐wide work on direct impacts transferred using appropriate methods to Himachal Pradesh; they are regarded as lower-‐bound estimates due to the use of conservative methodologies. Beyond these direct impacts, however, it is generally acknowledged that indirect impacts on the state’s tourism potential would further increase these figures significantly.

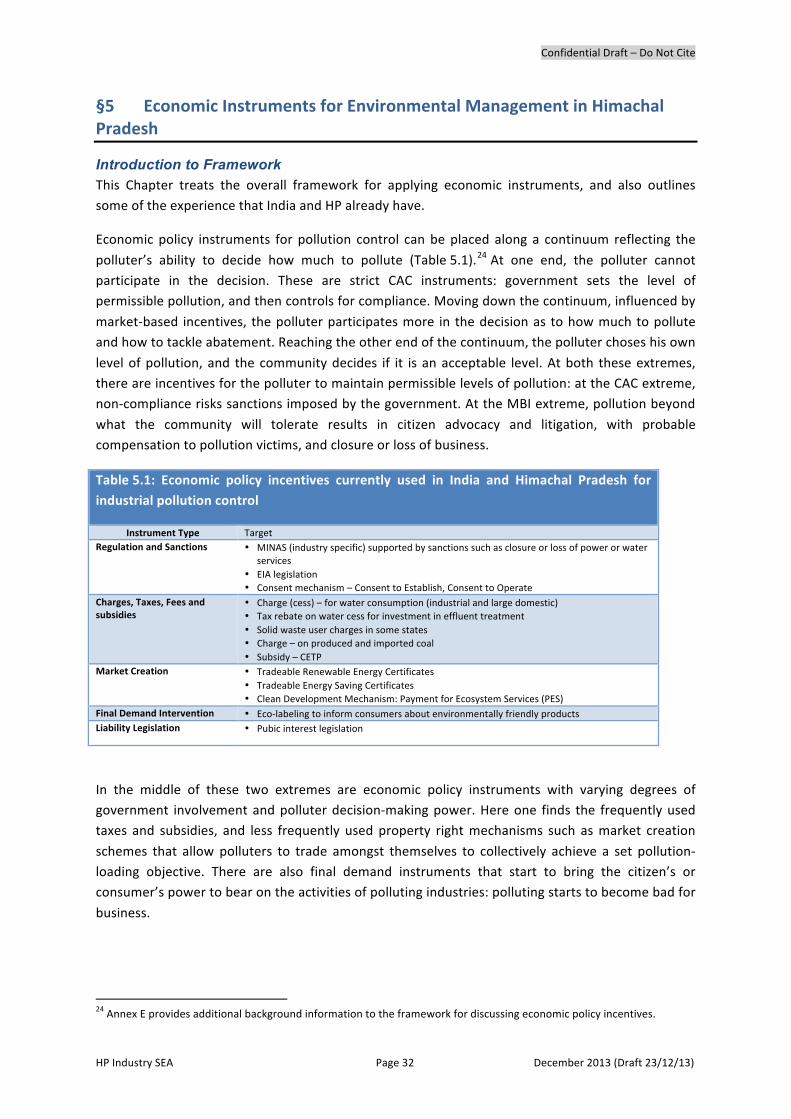

Economic Instruments – General Findings Command and Control (CAC) and Market-‐Based

Instruments (MBIs) both incentivize industry to control pollution: either or both can make policy sense in a given institutional context. A mix of CACs and MBIs can address different goals:

cost-‐effectiveness, pollution reduction, and revenue generation. Historical developments can generate a sub-‐optimal mix of approaches, implying that the first steps in policy involve reforming or changing “perverse incentives” that have unintended negative environmental impacts. India and Himachal Pradesh already have experience

with a number of CAC and MBIs; future initiatives in the State can build effectively on this experience. All of these approaches do, however, require well-‐developed institutional capacity to enforce or oversee the relevant instruments. Only voluntary mechanisms require relatively less institutional capacity, but even these benefit from complementary state programs that can support private initiatives. Not possible at this stage to conduct cost

effectiveness of different regulatory regimes as there is no information on compliance or transaction costs either within industry or within the regulatory setting. Comparisons of the cost effectiveness of different regulatory regimes require specific data on transactions, monitoring and compliance costs borne by industry and regulators in Himachal Pradesh. A number of approaches hold particular promise

including: ü Increased use of industrial parks within spatial zoning &

planning. ü Increased reliance on user fees/charges for treatment

with modifications to remove existing distortions and inefficiencies.

ü Increased reliance on budget neutral environmental taxation, including over the longer term a carbon (GHG) tax.

ü Aggressive incentives for net positive impact industries (e.g., biotech, nanotech) or activities.

ü Facilitate organization of small-‐scale industries to take advantage of branding opportunities and collective responsibility arrangements.

Ongoing support for awareness building and transparency in support of Public Interest Litigation is a cost effective means for addressing industrial

pollution.

New Sectoral Insights Case studies based on detailed data collection and

interviews of regulators and 18 firms (out of a potential >300) in Himachal Pradesh revealed a series of important insights, which inform future policy design.

ü Regulators in the Baddi SPCB regard incentive to individual firms as too difficult to monitor given current resources; they prefer that any incentives be given to common effluent treatment plants.

ü Voluntary certification programs can generate marketing benefits, decreased costs through better waste management, and greater environmental compliance. In the food processing survey, companies have already accessed ISO 22000 (a general derivative of the ISO 9000 system particular to the food safety industry) and ISO 14001; others are considering certification under ). A few companies are considering seeking ISO 900, ISO 14001 and OHSAS18001 certification.

ü Simple classification distortions can block effective use eligibility for incentives; stone crushers are not classified as an “industry” therefore do not enjoy the same benefits that others might.

New Approach for MSMEs Based on a survey of methods used in ten countries,

the SEA describes a hybrid scheme intended to improve control of pollution from MSMEs in Himachal Pradesh. The recommended scheme comprises elements of

five different economic instruments: ü environmental fee tied to operating permits (on pollution

discharge with exemptions) ü capital grant provisions for environmental technology ü soft loan scheme for MSME support ü accountability instruments ü economic incentives associated with supply-‐chain

management The final hybrid of these is a collection of options

described as the “Himachal Pradesh SME Green Incentive Scheme.” Flexibility permits targeting and phasing of politically sensitive elements; its design is such that it can be budget neutral, and altered to fit budget constraints.

Summary of Recommendations {to be completed – refer to action matrix Table ES.1} Elaborate/reiterate listing in §12, including among

others: MSME mechanism (as above) [short-‐medium term] Scaling of MSME mechanism [long term] Statistical infrastructure/Capacity building. [ASAP] Activities complementing PES notification. [ASAP] Closing statement of this SEA as resource for future

learning.

Confidential Draft – Do Not Cite

HP Industry SEA Page ix December 2013 (Draft 23/12/13)

Page intentionally left blank.

[insert recommendation action matrix Table ES.1: Theme, element, SML term priority & indication of budgetary needs

refer to §12 for full descriptions]

Confidential Draft – Do Not Cite

HP Industry SEA Page 1 December 2013 (Draft 23/12/13)

§1 Introduction

Context for SEA This SEA is a technical piece intended to assist in the current and future identification of priority industrial pollutants and economic instruments to minimize industrial waste. This industrial sector

SEA is one of six pieces of technical support envisioned by the HP Inclusive Green Growth (IGG) Development Policy Loan (DPL)2 to fill knowledge gaps and strengthen operational success of the DPL. The DPL acknowledges that industrial development is an important economic driver within HP,

and that such development must be consistent with maintaining the integrity of other natural resource assets on which human health depend. Moreover, maintenance of environmental integrity also supports policy aspirations for promoting tourism development as another economic driver.

The 4th Objective and Goal of the IGG DPL promotes environmentally sustainable industrial

development by reducing pollution of existing industrial plants and promoting cleaner sources of economic growth. The associated DPL 1 Prior Action requires a HP Cabinet amendment to the Industrial Policy (2004) that promotes cleaner production and environmental management systems,

disincentives to polluting industries, and public disclosure of the status of polluting units and clusters. The associated DPL 2 Trigger is the design and pilot by the State Department of Industrial Development of economic instruments for industrial pollution control for selected priority

pollutants. This SEA for the Industrial Sector is consistent with this objective of the IGG DPL, by providing guidance to facilitate selection of an appropriate DPL 2 Trigger.

Role of SEA The general objectives of the SEA Study are: (i) to assist in identification of priority pollutants and industries; (ii) to review existing institutional structures that address these pollutants; (iii) to identify and recommend potential reform options through the introduction of new policy approaches; and,

(iv) to identify complementary institutional support necessary to implement such a program. The work focuses on delivering insights and recommendations along the following broad themes.

Theme 1: Identification and diagnostic of key environmental issues in the industrial sector of HP, including identification of priority pollutants and polluters based on available information. This

includes listing and prioritization of primary polluting sources (i.e., industries and sectors), based in turn on a listing of contaminants of concern related to the industrial processes, industrial waste (solid and liquid) disposal practices and infrastructure and assessment of the key environmental and

health impacts. A large number of pollution problems have serious economic costs in terms of health, production costs, tourism, quality of life and ecology that exceed the alternative cost of pollution control; however, there is little prioritization of these problems in terms of their economic

impacts. Therefore, limited financial and institutional resources are dissipated and do not achieve the greatest possible effect. The SEA thus summarizes available economic valuations of selected environmental and health costs associated with pollutants with the aim to inform the identification

and rank of priority polluting industries and sectors. It should be noted that much of the ranking has already been undertaken through political processes that recognize the importance of various

2 World Bank. 2012. Development Policy Loan (DPL) to Promote Inclusive Green Growth and Sustainable Development in Himachal Pradesh. August 6.

Confidential Draft – Do Not Cite

HP Industry SEA Page 2 December 2013 (Draft 23/12/13)

industries, while also reflecting physical impacts on human health and environment; putting forward the economic values thus complements the information base on which these decisions are made

and priorities are set.

Theme 2: Identification and assessment of appropriate policy alternatives. New economic conditions require a reform of industrial pollution policies toward a more collaborative approach with industry, building on the synergy between more flexible regulation with effective enforcement on one hand,

and market driven incentives for improved environmental management systems, on the other hand. The SEA thus assesses various options in the context of HP to address the priority pollutants, including (i) economic instruments, (ii) command and control instruments, (iii) public disclosure

instruments, and (iv) other methods.3,4 Other methods are generally at a higher policy level and might include, for example, incentives for attracting cleaner industries or extending the negative list to other categories of industries. Given the continued environmental degradation of HP’s fragile

ecosystem it is pertinent to revisit the negative list and align incentives accordingly for both clean and dirty sectors. The SEA considers the pros and cons of different policy alternatives based on a series of general assessments that rely on experience internationally and within India, and upon

local institutional considerations.

Theme 3: Recommendations for institutional reforms to implement the suggested policy changes. This relies on a review of institutional frameworks governing the environmental aspects of the industrial sector in HP, including assessment of capacity for implementation and effectiveness of

implementation. The review is based on secondary sources and is intended to categorize and assess the relevance and effectiveness of existing institutional arrangements; the review builds on a comprehensive assessment undertaken in 2009. The institutional considerations are intended to

identify: (i) resources that will be required to address existing gaps in achieving effective environmental management; (ii) appropriate recommendations that can be implemented in the

short, medium and long term; (iii) identify potential opportunities and challenges to the implementation of such recommendations; and (iv) identify institutional roles and responsibilities for implementation. The recommendations also incorporate initiatives related to general

institutional capacity building within HP.

Approach The SEA was undertaken from April to December 2013 based on secondary data collection, existing

literature (Annex A), various consultative meetings with key stakeholders (Annex B), and diagnostic analyses of this information. The main elements of the SEA included the following.

3 The literature shows that economic instruments such as pollution taxes for environmental policy are the most efficient but their design requires significant amounts of primary data and a vast institutional capacity to implement. Introduction of pollution taxes may also require legal and institutional reforms, besides capacity to measure and monitor pollution. There are also risks that they invite rent seeking (corruption) as shown in the literature. The SEA thus examines the use of potential economic instruments that will be examined in the HP context to address industrial pollution issues in the broader context of efficacy, efficiency and sustainability. As HP is gearing up to adopt a Goods and Services Tax regime, it is also an appropriate time for addressing environmental considerations. 4 Public release and dissemination of emissions data and environmental performance ranking can be a powerful tool to promote pollution control. Programs of public disclosure of emissions aim to promote compliance with pollution regulations and reward good performance. Examples of such schemes include PROPER (Program for Pollution Control, Evaluation and Rating), which has been used in Indonesia and other similar schemes that have been used for monitoring and increased transparency of information that have been used for example, in Colombia and Ghana. There is an increasing appetite in HP to introduce public disclosure building on their existing online monitoring of pollution from key industrial sources.

Confidential Draft – Do Not Cite

HP Industry SEA Page 3 December 2013 (Draft 23/12/13)

Initial consultation meetings were held in Himachal Pradesh in June 2013 and included a broad range of stakeholders. In preparation for these consultations, key issues were initially identified by the SEA

Team based on desk reviews of data and literature. This provided a basis for outlining preliminary priorities and for narrowing down further analyses and associated information requirements.

The purpose of the consultations was to discuss the findings, issues and preliminary directions suggested by the desk reviews (presented in a power point presentation), and to initiate a work plan

for amassing additional information. These meetings also kicked off a broader consultative process, recognizing that GoHP has already embodied a consultative philosophy within its environmental policy program. It should be noted that the consultations paralleled preparation for appraisal of the

DPL.

The SEA Team worked closely with the State Pollution Control Board (SPCB) and the Department of Industry to collect available data and information to inform the SEA. Information collection involved those data routinely collected by the SPCB, as well as a series of case studies of priority polluting

industries. The case studies were selected in consultation with the Industry Department and the SPCB: those chosen covered the pharmaceutical industry in Baddi (Solan District), and the stone crushing and food processing industries in Una District. Cost effectiveness were subsequently

considered within these same industries but at a state wide level; information constraints relating to industrial compliance costs and institutional costs (described in this report) limit the scope and application of cost effectiveness analyses at this stage but the SEA does provide selected examples

and pro-‐forma templates that can potentially be used during ongoing institutional information collection and capacity building within HP. Such capacity building is regarded as a core requirement for moving forward and is described more fully in the recommendations arising from this SEA.

To help guide the selection of an economic instrument for pollution control to meet the DPL requirements in HP a literature review of existing practices and experiences across ten countries in Asia and South and Central America was undertaken. This experience was summarized within a mid-‐

study recommendation report to relevant stakeholders to assist in the design of an appropriate instrument for the DPL trigger.

The SEA has included participatory approaches to ensure that proposed policy changes are designed and implemented in a way that is responsive to the different segments of HP society. During the

course of the work, the SEA Team worked collaboratively in collecting industry information and providing quality control on that information. Various databases were collected, reviewed, and corrected to address issues associated with anomalies such as improper classification and

completeness. Feedback was also provided by the SEA Team through ongoing discussions relating to the design of an appropriate economic instrument specifically targeted to small and medium enterprises: these recommendations were subsequently validated within the context of this SEA and

form a core part of the overall recommendations arising from this study. The SEA also provides information aimed at enhancing future social learning processes through the use of case studies to permit evaluation of policy directions. A key aspect of this is the elaboration of a series of three case

studies – relating to the pharmaceutical, stone crushing and food processing sectors – and a preliminary review of cost-‐effectiveness considerations within these sectors. In this way, the SEA seeks to promote long-‐term sustainability of public policies beyond the mitigation of short-‐term

environmental impacts.

Confidential Draft – Do Not Cite

HP Industry SEA Page 4 December 2013 (Draft 23/12/13)

Country Context India’s gross domestic product (GDP) growth is likely to remain lower than what it was before the global financial crisis but high in international comparison. India’s GDP growth slowed to 6.5 percent in FY2011-‐12 from 8.4 percent during the two previous years. The slowdown was led by lower

investment, which reached 5.5 percent in FY2011-‐12 compared to 7.5 percent in the previous year. Over the next two years, GDP is expected to stay around 7 percent.

Most environmental indicators in India suggest that economic growth is extracting an increasing toll on the country's natural resources -‐ water, land, forests, soils and biodiversity -‐ and leaving a large

pollution footprint. India is highly vulnerable to climate change; cyclones, floods and droughts are happening with increasing frequency, and the Himalayan glaciers that feed India‘s largest rivers may be vulnerable to retreat. Indeed, climate change will impact India first and foremost through its

water resources. Rising temperatures will also affect agricultural yields, forests, and marine and coastal biodiversity. India will need to better manage these resources (particularly water) and reduce the burden that environmental degradation is imposing on the population, particularly on

the most vulnerable groups.

A World Bank (2013) diagnostic report estimated that environmental degradation costs India about US$80 billion a year, nearly 6% of its GDP. The biggest problems are air pollution, land degradation and poor water and sanitation. The study suggests that reducing PM10 particles by 30% would cut

average GDP growth by 0.04 percent, but would save US$47–US$105 billion in health costs annually [tbv if annual & check specific reference].

The World Bank support for the Himachal Pradesh Inclusive Green Growth (IGG) DPL breaks new ground, which could have significant demonstration effects in promoting the green growth agenda

throughout India.5 HP’s resource base and pro-‐active policy stance places it in a position to show leadership at the state level.

State Context – HP as Leader The Government of Himachal Pradesh (GoHP) has embarked on a program to make a transformational shift toward a model of environmentally sustainable economic growth, at the core of which is the objective to become carbon neutral by 2020. The State’s mountain environment

embodies the connectivity between different economic sectors; industry, together with energy, rural development and tourism sectors, is one of the key engines of economic growth in the state of Himachal Pradesh.6

Himachal Pradesh has witnessed exponential growth in industry development. From a modest base

of 22 large and medium enterprises and 6,969 small-‐scale industries in 1979-‐80, by 2012 the sector had accelerated to over 487 large and medium enterprises and about 38,220 small-‐scale industries,

5 The India/World Bank Country Assistance Strategy (CAS: Report No. 46509-‐IN), 2009-‐12, recognizes that while India needs to grow to reduce poverty and create employment, it has an opportunity to do so in a way that is sustainable and preserves the country‘s natural heritage. CAS identifies the following priorities for engagement: sustainable management of natural resources, climate change, and the inclusive green growth and sustainable development agenda. The CAS provides a framework to deal with the challenges of achieving rapid, inclusive growth, ensuring sustainable development, and improving service delivery, with a cross-‐cutting focus on improving the effectiveness of public spending and achieving monitorable results. The CAS suggests that special strategies are required for the Northeastern and Himalayan States. 6 GoHP is in the process of preparing a new Industrial Strategy, a draft of which was received and reviewed by the SEA Team in September. [If this is finalized, we need to add a proper reference and check it against statements in this SEA and add some text later in this Chapter.]

Confidential Draft – Do Not Cite

HP Industry SEA Page 5 December 2013 (Draft 23/12/13)

with direct employment of about 266,000 persons. To facilitate the establishment of new industries, a State Level Single Window Clearance and Monitoring Authority was constituted to clear projects

and ensure speedy approval from various departments. Additionally 41 Industrial Areas and 15 Industrial Estates were built to provide infrastructural facilities to the sector.

Industrial growth in HP has been fueled by incentives provided by the central and state governments. In the 1980s, subsidies and concessions were introduced to promote investment,

particularly by firms utilizing local raw materials and labor and compensate for the high costs of difficult terrain and inadequate industrial infrastructure. The approach however soon became unsustainable – as the experience with infant industry support has demonstrated globally. GoHP

recognizes that tax breaks and fiscal incentives have often led to creation of uncompetitive industries, and that its role in spurring industrial development should gradually shift from providing subsidies to creating a robust business environment with a level playing field.

Furthermore, rapid industrialization in HP has led to industrial clusters where environmental quality

(air and water pollution) is rapidly deteriorating and causing hazardous conditions for neighboring communities. While the State Pollution Control Board (SPCB) is mandated with the regulation of environmental compliance of industries and identification of interventions for areas which have

become “pollution hot spots”, the Industries Department promotes overall industrial development in the state with limited information on the environmental quality of the various industrial clusters. Further, communities themselves have little information on environmental performance of

neighboring facilities, so stakeholder monitoring pressures are absent.

The GoHP 2004 Industrial Policy and its 2006 amendments continue to provide an impetus to industrialization. The Policy includes a wide range of incentives aimed at boosting the investment

climate by creating and upgrading the existing infrastructure, rationalizing the provision of incentives and streamlining rules/procedures including the provision of land banks, cheap commercial power, skilled manpower, local labor, roads and transport accessibility, and information

technology access with good network penetration in the interiors. Priority industries that were deemed Clean (such as: environmentally sustainable tourism, information technology, bio-‐technology and fruit processing) are encouraged and financial incentives are available for investing

in end-‐of-‐pipe pollution control equipment and cleaner technologies.

Given the thrust on rapid industrial development, the inclusion of green elements and incentives in the 2006 amended Industrial Policy has been minimally effective for attracting cleaner industries and adoption of cleaner technologies. Recognizing the need for reducing the environmental

footprint of industrial growth, GoHP has agreed to create a joint government-‐industry body to review and update industrial policy focusing on environmental sustainability and clean production. In addition, GoHP recognizes the need to strengthen collaboration between the Industries

Department, the Department of Environment, Science and Technology and the State Pollution Control Board to reduce pollution from industrial sources, while also enhancing industrial competitiveness. Government agencies and the private sector have agreed to jointly review the

Industrial Policy 2004 in order to determine policy approaches to catalyze or accelerate climate-‐smart industrialization in the state. [If review is complete, describe and reference here; cf. Footnote earlier this chapter.]

Confidential Draft – Do Not Cite

HP Industry SEA Page 6 December 2013 (Draft 23/12/13)

Environmental degradation is particularly impacting the region’s natural tourism attractions and has become an impediment to HP achieving its full tourism potential. A major challenge has been lack of

coordination between the Tourism Department and the Departments of Urban Development, Town and Country Planning, Environment, Irrigation and Public Health in formulating a coherent strategy for improving tourism potential. While these problems are already evident, they are set to become

more severe and widespread without urgent actions and adequate planning.

The State‘s unique and fragile hill ecosystem, including its protected areas, supports many of the State‘s most popular tourist activities, including trekking, skiing, angling, mountaineering, rafting, and watching of flora and fauna. Pollution from wastewater and solid wastes, as well as unplanned

urban growth, not only threaten the fragile ecosystem, but also reduce the attractiveness of the natural and pristine areas that tourists travel to visit. The tourism sector has shown remarkable resilience despite over-‐crowding in some areas and has the potential to become one of Himachal

Pradesh’s main drivers of economic growth. In 2008, Himachal Pradesh received 9.37 million domestic tourists (1.6 percent of total domestic tourists in India) and 377 thousand international tourists (6.7 percent of total international tourists in India). Among Indian states, Himachal Pradesh

was the 10th most visited by international tourists and 12th most visited by domestic tourists. Between 2001 and 2008, visits by domestic tourists grew by 8.9 percent and those of international tourists by 20.9 percent.

Outline This Final Report is broadly presented in three parts. Part I forms a foundation for focusing subsequent diagnostic work by providing more extensive detail on the institutional context,

pollution situation, health and environmental linkages, and opportunities for using economic instruments. Part II performs additional diagnostic analyses to inform the core recommendations relating to options for new economic instruments, institutional reforms and capacity building; these

recommendations are presented in Part III (Chapter 12).

Part I “Foundations” continues in Chapter 2 with an institutional review and then in Chapter 3 presents a summary of findings relating to the industrial pollution hotspots, industries and criteria pollutants relevant to the prioritization exercise in Himachal Pradesh. The institutional review builds

on a detailed diagnostic first conducted in 2009, and was informed by participatory workshops and meetings conducted during the SEA and through parallel activities associated with the DPL. The work

relating to pollution hotspots and industries relies on secondary statistics collected by government and on validation through the stakeholder workshops. A discussion of health linkages in Chapter 4 is intended to provide background information on key health concerns that would come up in any

industrial context; this chapter also introduces findings of the valuation work related to human health and environmental quality in the context of the various pollutants. Chapter 5 introduces the framework for considering different types of economic instruments for environmental management;

it also highlights experience with such instruments in HP.

Part II “Diagnostics” commences in Chapter 6 with the mid-‐study recommendation report relating to options for developing an incentive system to improve environmental performance of MSMEs. Chapter 7 commences with the results of the quality-‐controlled and corrected information

assessment exercise conducted of all industry pollution and operational information for Himachal Pradesh; it subsequently provides more specific background information on the context for the case

Confidential Draft – Do Not Cite

HP Industry SEA Page 7 December 2013 (Draft 23/12/13)

studies. Chapters 8, 9 and 10 provide a separate discourse on each of the three case studies for the pharmaceutical, stone crushing and food processing sectors. Chapter 11 concludes with a diagnostic

of cost effectiveness issues addressed in this SEA.

Various Annexes provide supplementary information tables and background material.

Confidential Draft – Do Not Cite

HP Industry SEA Page 8 December 2013 (Draft 23/12/13)

Part I FOUNDATIONS

§2 Institutional Review

§3 Pollution Hotspots & Priority Polluting Industries

§4 Health & Environmental Impacts of Industrial Pollution in Himachal Pradesh

§5 Economic Instruments for Environmental Management in Himachal Pradesh

[insert photo]

Confidential Draft – Do Not Cite

HP Industry SEA Page 9 December 2013 (Draft 23/12/13)

§2 Institutional Review

Introduction This chapter summarizes the institutional structure for environmental management. An environmental institutional assessment was conducted to inform the Inclusive Green Growth DPL,

and to help operationalize the Department of Environment, Science, and technology (DEST), which was formed under the (now closed) Fiscal DPL. To ease capacity constraints, various institutional recommendations are contained in the IGG DPL (based on the institutional assessment done in

20097). This chapter thus summarizes and updates the state of institutional capacity: potential pollution control interventions will need to be considered in light of the institutional capacity for their implementation. This will provide guidance as to the practicality of different policy alternatives,

given the existing and evolving environmental governance capacity in the country. The chapter commences with a description of the current structure, including the main players and existing policy initiatives. The chapter then turns to the 2009 institutional assessment, which also provided a

series of recommendations for HP: the chapter indicates to what extent these have been implemented or the reasons for delay or rejection.

Current Structure

The main environmental players: DEST and SPCB The State Pollution Control Boards (SPCBs) were created as a part of the national legislation whereas the state governments, to protect the particular interests of the state, create the state departments of environment. The HP Department of Environment, Science and Technology (DEST) is responsible

for overall environmental management in the state, while the SPCB is the main implementing agency of pollution regulations in the state. DEST exercises administrative oversight to the functioning of the HP SPCB.

The HP DEST is relatively young. It was created in April 2007, in accordance with the TOR provided by

the GOI MOEF for setting-‐up a state DOE. The first World Bank DPL assisted in its capacity development, and the second DPL continues that assistance. The DEST mandate includes implementing all environmental legislation that the SPCB cannot implement. Hence its mandate

includes: (i) environment and pollution control; (ii) development/modification/adaptation and dissemination of new technologies for state development needs; and, (iii) formulation and implementation of a state biotechnology policy.

Under its environment and pollution control mandate, DEST is responsible for implementing the

Environmental Impact Assessment and monitoring associated Environmental Management Plans prepared by project proponents. DEST is responsible for certain categories of industries that require mandatory state-‐level environmental clearance. In accordance with the GOI EIA mechanism, the

State Environmental Impact Assessment Authority (SEIAA) and the State Expert Appraisal Committee (SEAC) have been established within DEST. DEST collaborates with the SPCB to implement national EIA legislation.

7 World Bank. 2009. Institutional Assessment – Environmental Sector. Part A: Issues – Priorities and their Management. A Report Draft Version. March; and Part B: Organizational Assessment. A Report. May. Prepared by Environment Team SASDI. New Delhi.

Confidential Draft – Do Not Cite

HP Industry SEA Page 10 December 2013 (Draft 23/12/13)

DEST is responsible for taking punitive action against industries that are in contravention of pollution laws, rules, or notification. It is DEST that directs water and electricity utilities to stop service to non-‐

compliant industrial units. In the case of PIL actions, DEST is the GoHP respondent to the High and Supreme Courts of India.

The DEST mandate also includes public awareness and educations programs, pro-‐active disclosure of environmental monitoring information and environmental management practice by project

proponents and regulators. DEST would be the body providing the Environmental Information System (ENVIS) node for the MOEF.

The SPCBs are the main implementing agency for both national and state prescribed pollution norms and standards. The CPCB sets environmental standards, and with the assistance of the SPCBs,

monitors environmental performance and develops and facilitates abatement and pollution control for all parts of the country. Although DEST provides administrative oversight to the SPCB, the latter functions as an autonomous body, financially independent from DEST. The SPCB relies on Consent

Fees and revenue from the water cess to cover its budget.

There are 10 regional SPCB offices in HP that:

• Monitor pollution sources and industries to ensure that the conditions of the Consent to

Establish (CTE) and Consent to Operate (CTO) are being met (see Chapter 5 on Economic Instruments). During 2010/11 the SPCB granted 355 CTE and 332 CTO.

• Conduct “surprise inspections” as per the Environment Surveillance Scheme (ESS) for the 17

categories of highly polluting industries.

• Conduct public hearings associated with EIA processes that are mandatory for certain categories of projects. During 2010/11, the SPCB was involved in 5 EIA processes.

• Respond to public complaints and mediate between industry and the public.

• Assess and collect the water cess.

• Monitor the generation and disposal and/or storage of biomedical and hazardous waste.

• Regulate the establishment of Sewage Treatment Plants and solid waste disposal sites.

The 2009 institutional assessment of the SPCB found that it was operating with three-‐quarters of its

staff positions filled.

Interaction between DEST, SPCB and Industries Department The HP Industries Department implements HP’s Industrial Policy (2004). It plans industrial belts, informed by a Zoning Atlas8 developed by the HP SPCB. DEST can provide the industrial sector with

incentives for cleaner production technologies or better pollution abatement technologies, or it can provide disincentives for dirtier, older technologies. Depending on the type of enterprise, it will need environmental clearance and/or an EIA from the SPCB, DEST, or the MOEF.

8 The Zoning Atlas provides information as to the carrying capacity of different regions.

Confidential Draft – Do Not Cite

HP Industry SEA Page 11 December 2013 (Draft 23/12/13)

Both DEST and SPCB will have input to the relevant “negative list” and “thrust list” of industries in HP. As described in Chapter 3, most of the industries on the “Negative” list are those identified by

the GOI in the national industrial policy; HP has added a couple more to the list. These industries are not banned, but are generally not eligible for subsidies and are scrutinized for environmental impacts and mitigation measures. They have to renew periodically their Consents to Operate, after

demonstrating their compliance with the relevant environmental standards. It is the responsibility of the SPCB to ensure that required renewals are undertaken.

Ministry of Micro, Small and Medium Enterprises The GOI Ministry of Micro, Small and Medium Enterprises (MSME) the MSME Development Act,

2006, which defines these three tiers of enterprises. The Ministry of MSME facilitates industrial growth throughout the country. The Act also provides a legal framework, a statutory consultative mechanism, and funds, schemes, and services for MSME promotion, development, and enhanced

competitiveness. Among the schemes to reduce the environmental impacts of MSMEs is the Micro and Small Enterprises Cluster Development Program where a number of service facilities are provided to clusters of MSMEs.

Environment Policy Guidelines

The HP Environmental Policy Guidelines have been developed as a precursor to the eventual formulation of a State Environmental Policy. The Guidelines summarize the issues in different environment and economic sectors, and for each, provide a list of required actions.

Environment Master Plan (EMP)

The formulation of an EMP was initiated in October 2008 and completed in 2013. It is based on vulnerability assessments and the identification of ecologically fragile zones. It is a tool intended to

guide strategic development planning, to promote interagency and community engagement, and to aid in monitoring regional and national environmental performance.

Main elements of the EMP (based on version dated __ 2013) reflect the following. ____ ____ ____ ________ ________ ________ ________ ________ ________ ________ ________ ________

________ ________ [brief summary to be inserted based on most recent version available] ____

Corporate Responsibility for Environmental Protection (CREP) The MOEF GOI launched the CREP program in March 2003 to provide a means for bringing government and industry together to develop measures for pollution reduction that go beyond

simple regulatory compliance. Within the CREP program, Action Plans to meet agreed pollution targets are to be developed for the 17 highly polluting industrial sectors. Sector-‐specific National Task Forces are constituted to monitor the implementation of each Action Plan. The CPCB tracks the

progress of the CREP.

Expeditious Clearance HP has established Single Window Clearance and Monitoring (SWCM) Agencies and a State-‐level SWCM Authority to ensure rapid clearances of industrial projects. The Agencies and the umbrella

Authority provide a forum where government authorities from different departments and agencies meet periodically to examine industry project proposals. Five SWCM Agencies were established in the industrial areas of Parwanoo, Baddi, Paonta Sahib, Kala Amb, and Golthai.

Confidential Draft – Do Not Cite

HP Industry SEA Page 12 December 2013 (Draft 23/12/13)

The 2009 Institutional Assessment In 2009 the World Bank undertook an Institutional Assessment in Himachal Pradesh9 as part of the ongoing Fiscal DPL. The draft findings of the Institutional Assessment were shared with the Principal Secretary (Environment) and with the DEST of GoHP. The report was not finalized due to other

priorities, however, it served as a reference point in the preparation of the State’s Environmental Master Plan 2013 (EMP) and, more importantly, as a basis for creating new positions within the DEST.

The following is a summary of recommendations arising from the Himachal Pradesh 2009

Institutional Review (Parts A & B) related to the Department of Industry and to DEST, and an update on these recommendations as of November 2013.

Industry Department – Update of 2009 Review Given that it had been difficult to ensure proper environmental management in the existing industrial development zones, the Institutional Assessment 2009 recommended that the Industry Department should outline a clear policy that eco-‐sensitive areas and its surroundings / vicinities will

be outside the purview of industries.

Currently the state operates a Single Window Clearance system for industry. The Principal Secretary (Environment) is a member and the PCB is a special invitee on the Single Window Clearance committee. If a project is located in an eco-‐sensitive area or its surroundings / vicinities, it is not

cleared. Further, as per the EIA notification 2006, any industry project located in eco-‐sensitive areas requires the permission of the MOEF to operate. The state level environmental clearance authority, the State Environment Impact Assessment Authority (SEIAA), cannot provide this clearance. The

implementation of both of these requirements was streamlined in 2009.

The 2009 Institutional Assessment found that Environmental laws addressed end-‐of-‐the-‐pipe pollution issues but did not encourage cleaner manufacturing. It was therefore recommended that the Industry Department provided a policy of disincentives for old, polluting dirty technologies and

incentives for cleaner technologies, production processes and practices. Industries in HP should be urged, facilitated and encouraged towards cleaner manufacturing and encouraged, through the upfront adoption of better approaches, to adopt the “polluter internalizes principle”. It was

recommended to explore the establishment of a Cleaner Technology Centre within the Industry Department with support from DEST. Given the major negative environmental impacts caused by mining, it was advised to select the mining sector to pilot cleaner manufacturing initiatives.

Incentives for cleaner technologies, production processes and practices were included as a trigger

for the DPL II. It is expected that the Industrial Policy will be suitably amended to include the incentive policy by early 2014 [check status].

DEST – Update of 2009 Review The specific recommendations of the 2009 Institutional Assessment for the DEST and subsequent related actions are provided below.

9 World Bank. 2009, Institutional Assessment – Environmental Sector. Part A: Issues – Priorities and their Management. A Report. Draft Version. March; and Part B: Organizational Assessment. A Report. May. Prepared by Environment Team SASDI. New Delhi.

Confidential Draft – Do Not Cite

HP Industry SEA Page 13 December 2013 (Draft 23/12/13)

Implementation Responsibility The 2009 Institutional Assessment recommended that DEST should assume a policy formulation, co-‐

ordination / facilitation / advisory, monitoring and compliance role without any implementation responsibility. If implementation experience is needed to enhance its advisory role, then it should be no more than at laboratory or pilot scale. Since 2009, the roles of the DEST have been streamlined.

All implementation initiatives related to environmental management are now being carried out by other organizations, e.g. Aryabhatta Geo-‐Informatics Space Application Centre (AGiSAC).

Multi-‐disciplinary Collaboration The 2009 Institutional assessment recommended the creation of multi-‐disciplinary working teams at

the operational level to promote integration and better enable cross-‐sector issues to be addressed. Initially, three working teams were recommended covering the following cross-‐sectoral issues: (i) urban, industry, transport and tourism; (ii) hydropower and roads; and, (iii) rural development,

agriculture and horticulture. Working teams should include representatives from the respective departments, and not only oversee activities such as studies initiated by DEST but also be proactive, through field visits and media about activities and practices that have environmental implications.

Their role should therefore be more hands-‐on than is customary of inter-‐departmental committees. The working teams should ensure that an integrated approach is developed in the short-‐term, which leads to a better prioritization of resource allocation and utilization in the medium term.

To date, multi-‐disciplinary teams have been created under the Climate Change Centre, which is an

organization under the Science and Technology Council. This has resulted in cross-‐sector issues being better addressed, which is critical in the context of climate change. Also, in the recently approved Environmental Master Plan, three broad sectors – Infrastructure, Natural Resources

Management and Services, encompassing 18 sub-‐sectors, are covered10. Guidelines based on socio-‐environmentally vulnerability assessment are in place. Implementation of these guidelines will

require a multi-‐disciplinary approach.

State of Environment Reporting The 2009 Assessment recommended that the periodic state of environment report (SOER) be expanded. Apart from addressing the environmental status issues, it should include a chapter on

institutional issues. It should also include: (i) information on the activities, outputs & outcomes achieved against pre-‐determined performance indicators and the priorities outlined for the future; and, (ii) the environmental sector’s contribution to the state’s GDP and the employment generation.

The last SOER was published in 2010. The next SOER is under preparation and planned for release in

2014; it includes a chapter on institutional actions, efforts and initiatives. This will include information on the activities, outputs and outcomes achieved against pre-‐determined performance indicators and the priorities outlined for the future, and the environment sector’s contribution to

the state’s GDP and employment generation.

10 Infrastructure includes – Road and transport, hydropower, tourism and ecotourism, industry, mining and geology, irrigation and public health, health, market infrastructure, rural and urban planning. Natural Resource Management includes – agriculture, horticulture, animal husbandry livestock, forest, wildlife and wetlands and fisheries. Services include – education and vocational training, IT and telecom, livelihoods, waste disposal.

Confidential Draft – Do Not Cite

HP Industry SEA Page 14 December 2013 (Draft 23/12/13)

Cumulative Impact Assessment It was recommended in the 2009 Assessment that DEST should identify specific geographical areas,

which are environmental problem areas. Essentially, these are areas where the cumulative effects have far exceeded the carrying capacity. In these problem areas, DEST should have in place enhanced monitoring and should focus on the containment of pollution. This enhanced monitoring

should include third-‐party involvement, preferably community monitoring or through community committees.

This is being implemented in relation to the key environmental issue in the state, i.e. river basin management. To determine the specific environmental problems and carrying capacity constraints,

cumulative impact assessments have been mandated and are underway in each of the river basins.

Extended Responsibility of Polluter The 2009 Assessment recommended that compliance penalties went beyond closures to making the polluter responsible for rectifying the pollution created, i.e. the polluter-‐internalizes principle. The

polluter must pay to rectify or clean up the negative outcomes of pollution. To date there has been no initiative taken in this regard, and no situations have arisen for the state to implement such compliance penalties.

Work Quality

The 2009 Assessment recommended the creation of additional special purpose vehicles / societies under DEST to strengthen and improve the quality of work. As a Government department, DEST is always under pressure to meet the day-‐to-‐day needs of the Government. However, this does not

promote a mindset for executing other Government responsibilities that require focused attention and commitment over a prolonged period of time. Special purpose vehicles or societies can address

this by providing financial resources as well as good technical assistance through collaborative partnerships with expert organizations. The day-‐to-‐day activities and management of these new organizations should be independent of the DEST but leverage on their linkages with DEST and the

GoHP to implement state-‐of-‐the art activities. In 2009 there were two special purpose vehicles under the DEST functioning at a limited scale. It was recommended that DEST expand the work of these special purpose vehicles to include new areas such as climate change. The mandate of these

new organizations should be large and be modeled based on the best-‐in-‐class organizations globally. Possible organizations along with their mandates for consideration cited in the 2009 Assessment were: (a) HP Environmental Assets Development Corporation – land availability and development for

environmental enhancements; (b) HP Climate Change Institute – adaptation and mitigation; (c) HP Environmental Management Institute – proactive facilitation, training and demonstration projects in Industry, Urban and Construction sectors; and, (d) HP Environmental Information & Awareness

Institute – a single-‐window information clearinghouse on environmental issues and promoting awareness on a regular basis in all sections of society.

Creation of special purpose vehicles is the approach adopted by the DEST since 2009. Two specific examples are the HP Climate Change Centre and the Aryabhatta Geo-‐Informatics Space Application

Centre (AGiSAC). Both these organizations have been established by the DEST through the State Council for Science & Technology.

Confidential Draft – Do Not Cite

HP Industry SEA Page 15 December 2013 (Draft 23/12/13)

Payment for Ecosystem Services (PES) The 2009 Assessment recommended that DEST initiate a feasibility analysis on raising additional

financial resources for environmental management in HP. DEST should be proactive in raising funds from bilateral and multilateral sources, as well as from innovative mechanisms such as carbon-‐linked revenue sources and payment for ecosystem services (PES). Financial resources should be used to

conserve the environmental assets of the state and mitigate the environmental impacts of developmental activities.

Currently, a PES initiative is being developed as a part of the DPL. A cross-‐department team of technical experts from the Forest Department has worked to produce an assessment of water

regulation and soil retention services of forests for hydropower generation. Also, the GoHP piloted a Payment for Environmental Services (PES) scheme in Palampur and provided for PES in the current Catchment Area Treatment Plan Implementation Guidelines, which includes a provision for PES. A

GoHP policy on PES was notified in November 201311. Among its objectives, the notification calls for a sustained flow of ecosystem services, and enabling experimentation and pilots that inform and refine ecosystem service approaches; incentives are linked to the sustained flow of ecosystem

services. Immediate priority elements of the PES program include quantification of ecosystem service flows; (ii) stakeholder identification; (iii) stakeholder engagement; (iv) determination of institutional arrangements; (v) determination of types and levels of payments; and,

(vi) incorporating the ecosystem approach into decision-‐making.

Public Feedback The 2009 Assessment recommended that DEST evolve as one of the departments that act as a conduit for public opinion and feedback to the GOHP. To begin with, DEST should have a division

that specializes in seeking public and stakeholder opinion in relation to various initiatives (e.g. DEST work or major public investments). This division should network with key non-‐governmental

organizations and community groups across various districts in the state. Through this network, this division should be capable of obtaining public and stakeholder opinion and feedback as required, and to communicate this to the GoHP. DEST should also maintain excellent documentation,

preferably electronic and web-‐based, and should operationalize a transparent form of governance.

There have been no follow-‐up initiatives pertaining to this recommendation. However, work under the DPL II on public disclosure should improve the documentation of information and data and facilitate communications between stakeholders.

DEST Structure – Functions

The 2009 Assessment recommended that DEST’s environment division be organized along functional lines. The three main functions are policy, advisory and co-‐ordination. The Business of GoHP (Allocation) Rules, 1971 for the DEST Environment Division covers all these activities. However, when

these rules were to be next revised, the 2009 Assessment found that it would be preferable to structure it as per the above functions. In addition, the 2009 Assessment asserted that DEST Environment Division needed an internal systems and procedural manual that outlined work flow

and work prioritization.

11 Government of Himachal Pradesh Department of Forests. Notification number FFE-‐B-‐C (15)-‐3/2005-‐11. 2 November 2013.

Confidential Draft – Do Not Cite

HP Industry SEA Page 16 December 2013 (Draft 23/12/13)

Finally, the 2009 Assessment recommended retaining a healthy balance among different functions. For instance, the DEST Environment Division should not solely focus on the regulatory functions and

become a “policing” department, but work with the other line departments to resolve environmental issues proactively through its Advisory and Co-‐ordination functions. It should not degenerate to only providing clearances, monitoring environmental compliance and participating in

litigations on behalf of the State Government.

The functions-‐based organizational restructuring of the DEST Environment Division was considered but was not implemented, as it was not viewed as a priority. As restructuring did not happen, there was also no direct initiative to create a “balanced” structure. However, the roles, responsibilities and

authorities of each position in DEST have been clearly laid out since 2009 and there are no implementation overlaps.

DEST Structure – Staffing The 2009 Assessment recommended that DEST create limited staff positions initially, and that DEST

adopt a needs-‐based growth informed by periodic performance effectiveness reviews. At the outset, one Division leader and two staff for each function were recommended.

Also, the 2009 Assessment recommended that dual staff positions be avoided, given the workload for the proposed positions in the DEST Environment Division. For instance, the activities started

under the Society for Environment Protection and Sustainable Development should be managed by separate staff and should not become a part-‐time activity of the staff of the DEST Environment Division. Strict avoidance of dual roles has two benefits: (i) full attention of the appointed staff on

the management aspects of the three functions; and, (ii) more individuals are involved in addressing the growing environmental problems and issues confronting the state. If the same individuals are

involved in more than one role, then there are two concerns: (i) conflict of interest situations; and, (ii) fewer people involved in addressing environmental problems and issues, when the involvement of a larger number of core people is required.

In 2010, 9 entry-‐level positions were created (in addition to the Director, PSO, SSO-‐Planning and

Environment Engineer positions). Of these 9 positions, 5 appointments have been made. For the remaining 4 positions, DEST is still seeking the right candidate. The creation of middle-‐level positions was not approved. Also, dual roles involving day-‐to-‐day functions no longer exist. Certain

supervisory responsibilities continue, e.g. Director, DEST is also the Member-‐Secretary of the State Council of Science & Technology. This is found to be necessary to ensure co-‐ordination.

DEST Structure – Role Attribution The 2009 Assessment recommended that the DEST Environment Division focus on the management

aspects of the three functions: policy, advisory and co-‐ordination. Hence information and awareness and research & development functions should continue with the State Council for Science & Technology. In addition, DEST Environment Division should only have oversight of the Society for

Environment Protection and Sustainable Development, which engages in consulting type activities beyond the proposed mandate of the DEST Environment Division.

In line with these recommendations a clear distinction of roles has been in place since 2009. The State Council for Science & Technology handles scientific research activities and is under the Joint

Member-‐Secretary who manages it independently. There is no overlap in implementation with the

Confidential Draft – Do Not Cite

HP Industry SEA Page 17 December 2013 (Draft 23/12/13)

DEST Environment Division. The same is the case with the Society for Environment Protection and Sustainable Development, which engages in monitoring and third party evaluation activities. The