Embed Size (px)

Citation preview

Volume 5 | Pre-Sale planning

Strategic wealth management for entrepreneurs and business owners

Wealth and Investment Management

Who should be on the pre-sale advisory team, and what specific roles do they play in assisting a business owner? pg. 6

How should one address the question of restricted stock within the context of the sale of a business? pg. 15

What are some of the charitable solutions that should be considered within the context of the sale of a company? pg. 17

What are some of the issues – from an income tax perspective – that need to be considered when

structuring the sale of a business for cash? pg. 26

How should a business owner coordinate the vast range of information and considerations that apply when selling

a company? pg. 33

How should post-sale entrepreneurs begin to prepare for the next phase of their wealth management journeys? pg. 36

ContentsIntroduction .................................................................................................................... 2

About this volume ......................................................................................................... 4

Step 1: Select a pre-sale advisory team .................................................................... 5

Key questions to consider when assembling a pre-sale advisory team ........................................7

Step 2: Review trust and estate planning needs .................................................... 9

Coordinating trust and estate planning with the sale of a business ........................................... 10

Common wealth transfer techniques that business owners engage in .....................................12

Types of stock option vehicles ............................................................................................................. 15

Charitable solutions to be considered ............................................................................................... 17

Step 3: Analyze the elements of the sale ............................................................... 18

Reasons to sell a business ....................................................................................................................20

Sale structuring options........................................................................................................................21

Comparing an asset sale to a stock sale ...........................................................................................23

Key concerns that may disrupt a sale ................................................................................................31

Step 4: Consider “next steps” ................................................................................... 35

Key questions to contemplate when evaluating “next steps” .......................................................36

Conclusion ....................................................................................................................38

“ Good fortune is what happens when opportunity meets with planning.”

Thomas Edison

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 2

“Good fortune is what happens when opportunity meets with planning.” – Thomas Edison

Perspective – possibilities and probabilitiesAdvisors will often point out to clients that the only thing which matters more than how much they

make from a transaction is how much they ultimately keep. Nowhere is this concept more evident

than within the context of the sale of a business.

Despite this, a substantial number of entrepreneurs embark upon business endeavors without the

guidance necessary to benefit from the remarkable and unique wealth-creation opportunities

that such transactions afford. In this regard, many business owners inadvertently discover the answer

to the question, “What happens when opportunity meets with poor planning?”

Challenge and opportunity – function and focusThis publication – Strategic wealth management for entrepreneurs and business owners (Volume

5: Pre-Sale planning) – provides entrepreneurs who are considering a sale of their business with the

insight required to align such an undertaking with their personal wealth management plans.

Holistic wealth management – the Barclays approachAt Barclays, we appreciate the fact that your strategic vision has allowed you to successfully launch

and grow your business. We seek to provide you with a clear understanding of how best to sell it.

After all, what value is vision without clarity?

We look forward to working with you as you embark upon the sale of your business.

Christopher Johnson

Head of Wealth Advisory and Strategic Solutions, Americas

3

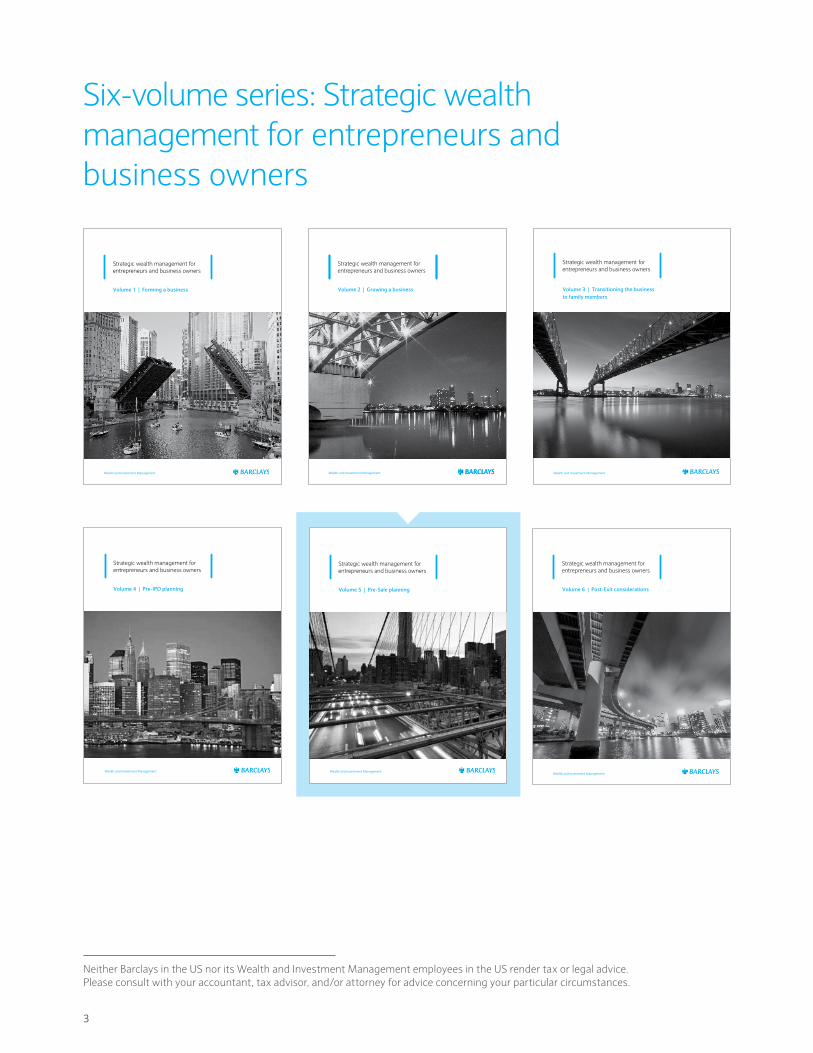

Six-volume series: Strategic wealth management for entrepreneurs and business owners

Neither Barclays in the US nor its Wealth and Investment Management employees in the US render tax or legal advice. Please consult with your accountant, tax advisor, and/or attorney for advice concerning your particular circumstances.

Wealth and Investment ManagementWealth and Investment Management

Wealth and Investment Management

Strategic wealth management for entrepreneurs and business owners

Volume 3 | Transitioning the businessto family members

Wealth and Investment Management

Strategic wealth management for entrepreneurs and business owners

Volume 2 | Growing a business

Strategic wealth management for entrepreneurs and business owners

Volume 5 | Pre-Sale planning

Wealth and Investment Management

Strategic wealth management for entrepreneurs and business owners

Volume 6 | Post-Exit considerations

Wealth and Investment Management

Strategic wealth management for entrepreneurs and business owners

Volume 1 | Forming a business

Strategic wealth management for entrepreneurs and business owners

Volume 4 | Pre-IPO planning

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 4

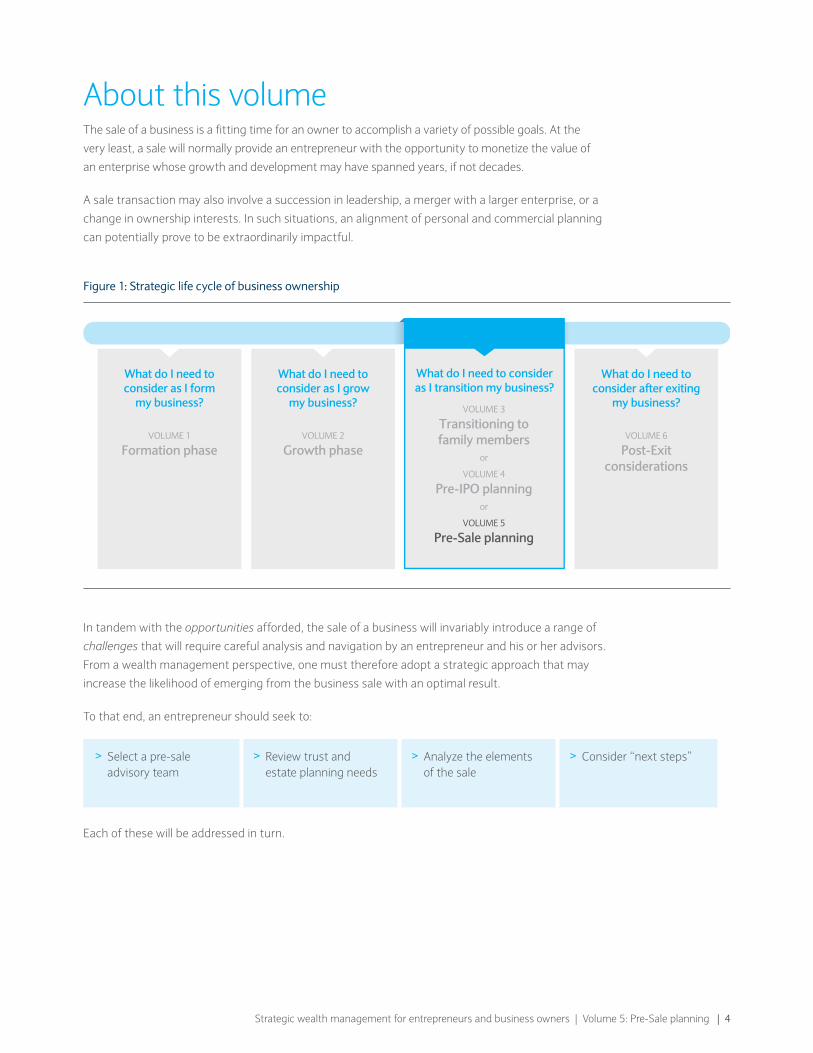

About this volumeThe sale of a business is a fitting time for an owner to accomplish a variety of possible goals. At the

very least, a sale will normally provide an entrepreneur with the opportunity to monetize the value of

an enterprise whose growth and development may have spanned years, if not decades.

A sale transaction may also involve a succession in leadership, a merger with a larger enterprise, or a

change in ownership interests. In such situations, an alignment of personal and commercial planning

can potentially prove to be extraordinarily impactful.

In tandem with the opportunities afforded, the sale of a business will invariably introduce a range of

challenges that will require careful analysis and navigation by an entrepreneur and his or her advisors.

From a wealth management perspective, one must therefore adopt a strategic approach that may

increase the likelihood of emerging from the business sale with an optimal result.

To that end, an entrepreneur should seek to:

> Select a pre-sale advisory team

> Review trust and estate planning needs

> Analyze the elements of the sale

> Consider “next steps”

Each of these will be addressed in turn.

Figure 1: Strategic life cycle of business ownership

What do I need to consider as I form

my business?

VOLUME 1

Formation phase

What do I need to consider as I grow

my business?

VOLUME 2

Growth phase

What do I need to consider after exiting

my business?

VOLUME 6

Post-Exitconsiderations

What do I need to consider as I transition my business?

VOLUME 3

Transitioning to family members

or

VOLUME 4

Pre-IPO planningor

VOLUME 5

Pre-Sale planning

5

Step 1Select a pre-sale advisory team

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 6

Q: What is a pre-sale advisory team?

The pre-sale advisory team consists of various advisors whose skill sets and expertise can be

leveraged by an entrepreneur who is preparing to sell his or her business.

Q: Who should be on the pre-sale advisory team, and what specific roles do they play in assisting a business owner?

Although the term “sale” is used generically to refer to the disposition of an entrepreneur’s

company, the actual nature of the deal can consist of a range of merger, acquisition or other

transactional undertakings. As a result, the specific makeup of each business owner’s advisory

team can vary considerably based upon the specific terms of the contemplated deal.

7

The Certified Public Accountant (“CPA”)

CPAs are among an entrepreneur’s most important advisors.

This is especially true during the sale of a business when a

CPA’s knowledge of relevant tax, compliance and financial

matters becomes invaluable.

Consultants

Given the complexities associated with the sale of a

business, entrepreneurs will occasionally call upon

professionals with particular skill sets to assist with an

especially challenging commercial or strategic scenario.

Consultants can provide pivotal support in this capacity

and can serve to augment the existing skill sets of current

internal or external advisors.

The Corporate Attorney

As a company prepares for a sale transaction, it will

normally require the services of a Corporate Attorney to

assist in the oversight of various structural, contractual

and regulatory undertakings.

The Corporate Trustee

Corporate Trustees can provide valuable objectivity,

professional oversight and continuity for trusts established

by entrepreneurs.

The Investment Banker

For larger sales, mergers, acquisitions and divestitures,

Investment Bankers can provide the expertise necessary

to help ensure a successful transaction.

The Investment Representative (“IR”)

Investment Representatives can serve as a vital bridge to

Investment Bankers (especially when there is a pre-existing

relationship with a business owner) and other members of

the bank’s Mergers & Acquisitions (“M&A”) group. Of equal

importance is an Investment Representative’s ability to

coordinate and facilitate the investment of funds that may

accrue from the liquidity event.

The Tax Attorney

The financial benefits that accrue from the sale of a

company are partially derived from the tax structuring that

is undertaken in conjunction with the deal. As such, a team

of skilled Tax Attorneys should be retained to develop and

direct the tax strategy that will be employed by the parties

to the transaction.

The Trust & Estate Attorney (“T&E Attorney”)

An integrated estate plan that addresses an individual’s

personal and commercial business interests is an essential

component of any entrepreneur’s wealth management

undertaking. A primary architect of such a plan should be

an experienced Trust & Estate Attorney.

The Valuation Consultant

An expert and impartial valuation of a business serves

as a key planning component for several estate, tax and

pre-exit strategies. This is especially true in the case of

pre-sale planning. These are best obtained through the

utilization of an experienced Valuation Consultant.

The Wealth Advisor

A Wealth Advisor, by virtue of his or her training in tax,

trust and estate planning, will normally partner with

an Investment Representative (and other advisors) to

optimize pre-sale preparation and to explain the impact

that certain techniques might have upon a client’s

wealth management plan.

Although the specific configuration of the team will vary depending upon the circumstances, the advisory team of a business owner who is preparing for a business sale will normally consist of some (or all) of the following advisors:

Neither Barclays in the US nor its Wealth and Investment Management employees in the US render tax or legal advice. Please consult with your accountant, tax advisor, and/or attorney for advice concerning your particular circumstances.

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 8

Figure 2: Business owners should leverage a core advisory team to resolve key business issues

Outline a pre-sale checklist

Review trustand estateplanning

Prepare thecompany for

the transaction

Engage in pre-sale

structuring

Trust & EstateAttorney

TaxAttorney

WealthAdvisor

CorporateAttorney

Accountant

InvestmentBanker

Consultant

InvestmentRepresentative

CorporateTrustee

ValuationConsultant

Pre-salebusiness owner

9

Step 2Review trust and estate planning needs

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 10

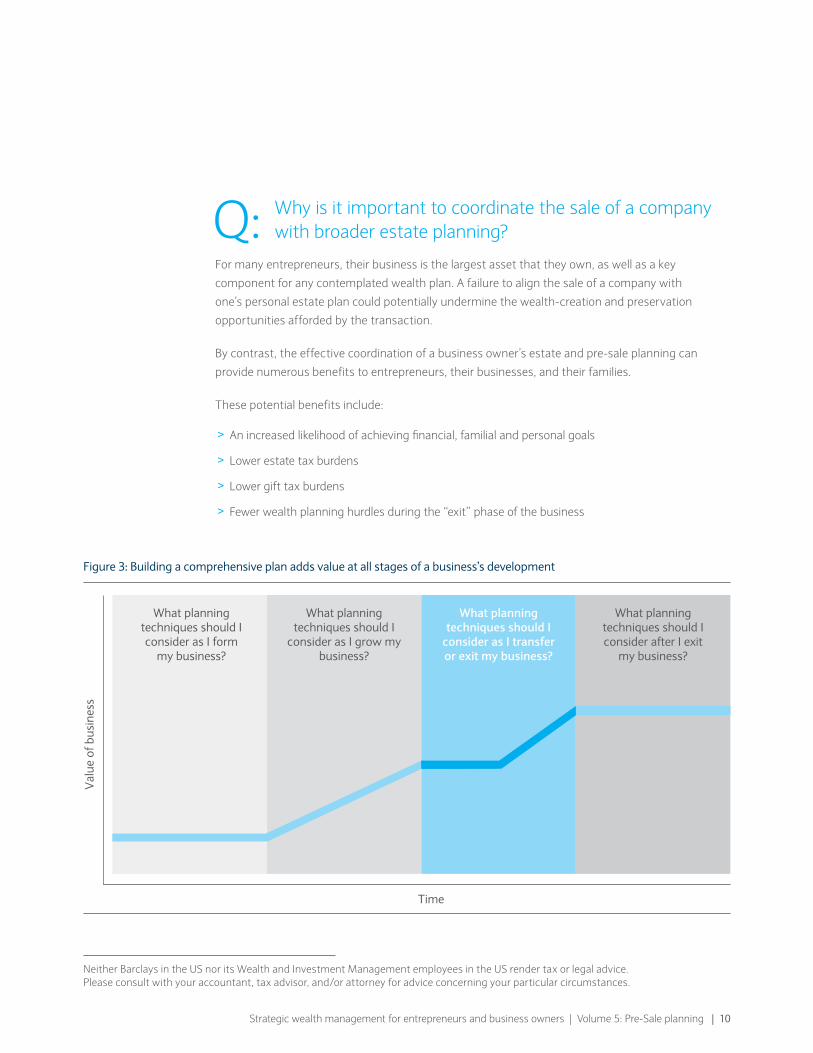

Q: Why is it important to coordinate the sale of a company with broader estate planning?

For many entrepreneurs, their business is the largest asset that they own, as well as a key

component for any contemplated wealth plan. A failure to align the sale of a company with

one’s personal estate plan could potentially undermine the wealth-creation and preservation

opportunities afforded by the transaction.

By contrast, the effective coordination of a business owner’s estate and pre-sale planning can

provide numerous benefits to entrepreneurs, their businesses, and their families.

These potential benefits include:

> An increased likelihood of achieving financial, familial and personal goals

> Lower estate tax burdens

> Lower gift tax burdens

> Fewer wealth planning hurdles during the “exit” phase of the business

Figure 3: Building a comprehensive plan adds value at all stages of a business’s development

Time

Val

ue o

f bus

ines

s

What planning techniques should I consider as I form

my business?

What planning techniques should I

consider as I grow my business?

What planning techniques should I

consider as I transfer or exit my business?

What planning techniques should I consider after I exit

my business?

Neither Barclays in the US nor its Wealth and Investment Management employees in the US render tax or legal advice. Please consult with your accountant, tax advisor, and/or attorney for advice concerning your particular circumstances.

11

Q: How conducive is the current tax landscape toward estate and gift planning?

Fortunately for business owners, the current estate and gift tax legislation offers entrepreneurs

a favorable environment within which they can undertake sophisticated estate structuring. By virtue

of the passage of The American Taxpayer Relief Act of 2012, (the “Act”) the current estate planning

environment is characterized by:

> High estate, GST, and gift tax exemption amounts (in excess of $5 million per person)

> Relatively modest estate and gift tax rates of 40%

As a result, business owners who undertake thoughtful, timely and coordinated business and

personal estate planning may be able to pass significant amounts of wealth to desired beneficiaries

in a tax-efficient manner.

The chart below summarizes the historical federal estate, GST, and gift tax exemptions.

Q: How might trusts be used to assist a business owner with estate planning?

In light of the generous estate and gift tax exemption amounts afforded by the Act, families are

currently able to pass significant wealth to their heirs – even without any tax planning. All families,

however, must still account for the risks associated with leaving such wealth to beneficiaries in the

absence of adequate protective measures. Those risks include:

> Lawsuits

> Future changes to the estate and gift tax

> Divorce

> Beneficiaries who are unprepared to inherit and manage such wealth

Calendar year

Estate tax exemption

GST tax exemption

Gift tax exemption

Top estate, GST, and gift tax rates

2003 $1 million $1.12 million $1 million 49%

2004 $1.5 million $1.5 million $1 million 48%

2005 $1.5 million $1.5 million $1 million 47%

2006 $2 million $2 million $1 million 46%

2007 and 2008 $2 million $2 million $1 million 45%

2009 $3.5 million $3.5 million $1 million 45%

2010 (taxes repealed) (taxes repealed) $1 million 35% (gift tax)

2011 $5 million $5 million $5 million 35%

2012 $5.12 million $5.12 million $5.12 million 35%

2013 $5.25 million $5.25 million $5.25 million 40%

2014* $5.34 million $5.34 million $5.34 million 40%

Figure 4: Historical estate, GST, and gift exemption values and rates

*Exemption figures will be inflation-adjusted in subsequent years. Source Data: Internal Revenue Service (IRS) as of April 2014.

Neither Barclays in the US nor its Wealth and Investment Management employees in the US render tax or legal advice. Please consult with your accountant, tax advisor, and/or attorney for advice concerning your particular circumstances.

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 12

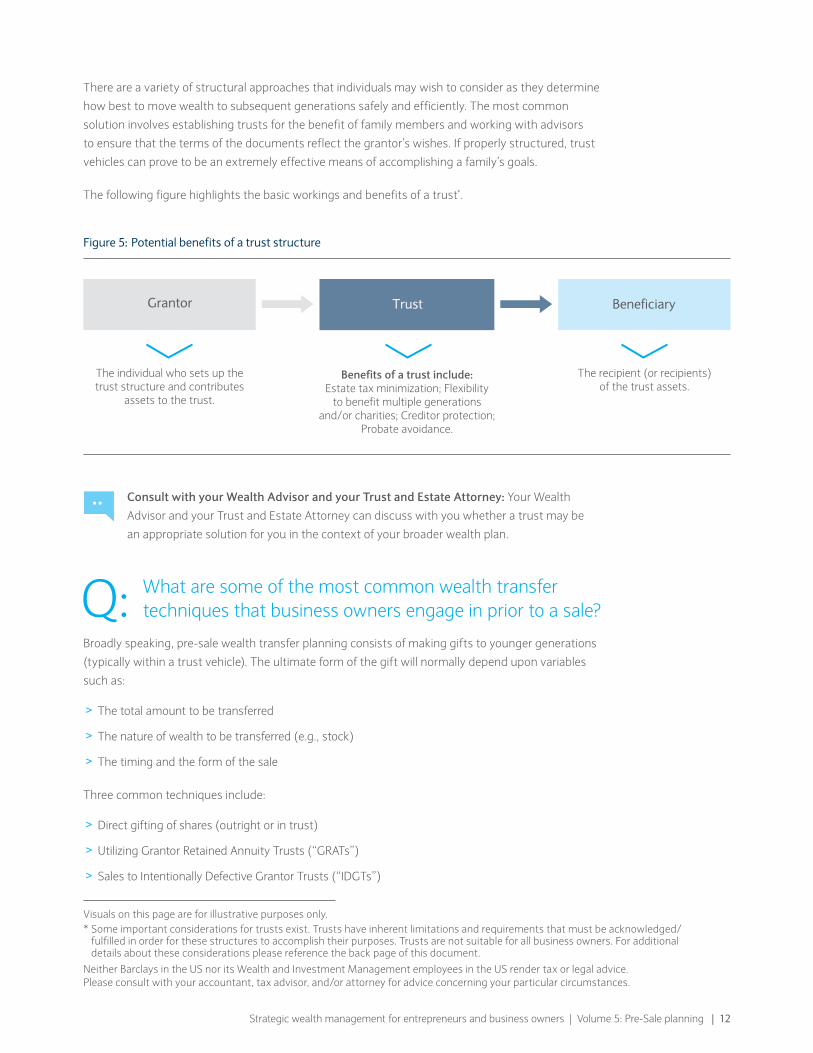

There are a variety of structural approaches that individuals may wish to consider as they determine

how best to move wealth to subsequent generations safely and efficiently. The most common

solution involves establishing trusts for the benefit of family members and working with advisors

to ensure that the terms of the documents reflect the grantor’s wishes. If properly structured, trust

vehicles can prove to be an extremely effective means of accomplishing a family’s goals.

The following figure highlights the basic workings and benefits of a trust*.

Consult with your Wealth Advisor and your Trust and Estate Attorney: Your Wealth

Advisor and your Trust and Estate Attorney can discuss with you whether a trust may be

an appropriate solution for you in the context of your broader wealth plan.

Q: What are some of the most common wealth transfer techniques that business owners engage in prior to a sale?

Broadly speaking, pre-sale wealth transfer planning consists of making gifts to younger generations

(typically within a trust vehicle). The ultimate form of the gift will normally depend upon variables

such as:

> The total amount to be transferred

> The nature of wealth to be transferred (e.g., stock)

> The timing and the form of the sale

Three common techniques include:

> Direct gifting of shares (outright or in trust)

> Utilizing Grantor Retained Annuity Trusts (“GRATs”)

> Sales to Intentionally Defective Grantor Trusts (“IDGTs”)

Figure 5: Potential benefits of a trust structure

Benefits of a trust include:Estate tax minimization; Flexibility

to benefit multiple generations and/or charities; Creditor protection;

Probate avoidance.

Grantor Trust Beneficiary

The individual who sets up the trust structure and contributes

assets to the trust.

The recipient (or recipients) of the trust assets.

Visuals on this page are for illustrative purposes only.* Some important considerations for trusts exist. Trusts have inherent limitations and requirements that must be acknowledged/

fulfilled in order for these structures to accomplish their purposes. Trusts are not suitable for all business owners. For additional details about these considerations please reference the back page of this document.

Neither Barclays in the US nor its Wealth and Investment Management employees in the US render tax or legal advice. Please consult with your accountant, tax advisor, and/or attorney for advice concerning your particular circumstances.

13

Q: How does direct gifting of shares work within the context of pre-sale wealth transfer planning?

In many instances, a direct transfer of shares in a business to family members will serve as the

simplest and most direct form of wealth transfer. Generally, a trust structure (and potentially a

corporate fiduciary) will be used to further augment the benefits of the gift. So long as the total value

of the gift does not cause the grantor (i.e., the business owner) to exceed his or her lifetime federal

gift tax exemption limit (currently in excess of $5 million), the gift will not result in any taxation.

By using exemption amounts to fund gifts to younger generations, business owners can remove

the shares from their estates, thereby allowing any future appreciation of the stock to accrue for

the benefit of younger generations. Further, by engaging in strategic gifting early on (i.e., when the

value of the business is poised for the greatest potential appreciation in value), business owners can

effectively reduce or even eliminate the gift and estate tax consequences associated with the sale

of a company.

Consult with your Accountant: Your accountant will normally keep track of the gift

tax returns that will determine whether or not direct gifting is suitable for you in your

particular circumstances.

Consult with your Valuation Specialist: In many instances, a gift of shares can be made

using a discounted valuation. There are a number of factors that will determine the extent to

which such a discount is applicable, including the time until an expected sale, the structure of

the gift and even the level of profitability for the company.

Q: How can GRATs and IDGTs be used to benefit from the (anticipated) appreciation in a company’s value over time?

As the value of a company appreciates leading up to a sale, it can become increasingly difficult to

redistribute the resultant wealth among family members effectively (without incurring an unwanted tax

liability). One solution to this problem involves establishing structures that permit beneficiaries to profit

from the growth in company value while still minimizing the negative impact of estate and gift taxes.

As noted, two planning structures* that are commonly used in this regard include:

> Grantor Retained Annuity Trusts (“GRATs”)

> Intentionally Defective Grantor Trusts (“IDGTs”)

The following descriptions and figures outline some of the specific characteristics associated with

GRATs and IDGTs.

* Some important considerations for trusts exist. Trusts have inherent limitations and requirements that must be acknowledged/ fulfilled in order for these structures to accomplish their purposes. Trusts are not suitable for all business owners. For additional details about these considerations please reference the back page of this document.

Neither Barclays in the US nor its Wealth and Investment Management employees in the US render tax or legal advice. Please consult with your accountant, tax advisor, and/or attorney for advice concerning your particular circumstances.

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 14

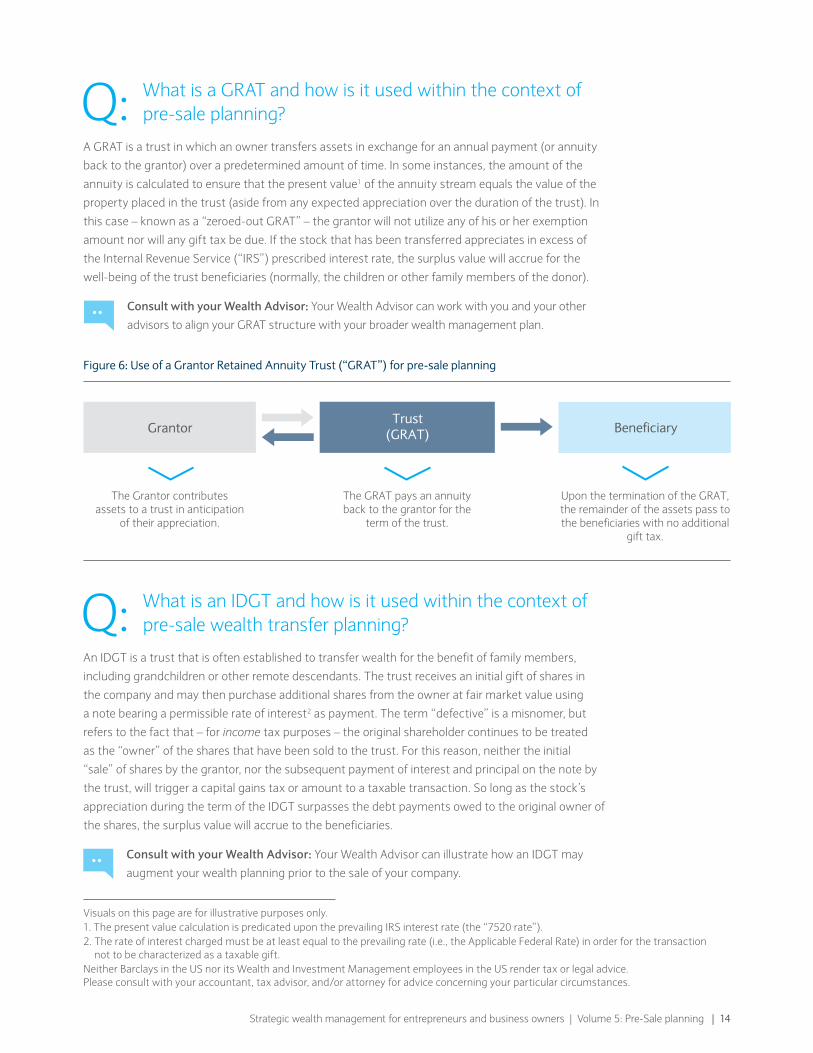

Q: What is a GRAT and how is it used within the context of pre-sale planning?

A GRAT is a trust in which an owner transfers assets in exchange for an annual payment (or annuity

back to the grantor) over a predetermined amount of time. In some instances, the amount of the

annuity is calculated to ensure that the present value1 of the annuity stream equals the value of the

property placed in the trust (aside from any expected appreciation over the duration of the trust). In

this case – known as a “zeroed-out GRAT” – the grantor will not utilize any of his or her exemption

amount nor will any gift tax be due. If the stock that has been transferred appreciates in excess of

the Internal Revenue Service (“IRS”) prescribed interest rate, the surplus value will accrue for the

well-being of the trust beneficiaries (normally, the children or other family members of the donor).

Consult with your Wealth Advisor: Your Wealth Advisor can work with you and your other

advisors to align your GRAT structure with your broader wealth management plan.

Q: What is an IDGT and how is it used within the context of pre-sale wealth transfer planning?

An IDGT is a trust that is often established to transfer wealth for the benefit of family members,

including grandchildren or other remote descendants. The trust receives an initial gift of shares in

the company and may then purchase additional shares from the owner at fair market value using

a note bearing a permissible rate of interest2 as payment. The term “defective” is a misnomer, but

refers to the fact that – for income tax purposes – the original shareholder continues to be treated

as the “owner” of the shares that have been sold to the trust. For this reason, neither the initial

“sale” of shares by the grantor, nor the subsequent payment of interest and principal on the note by

the trust, will trigger a capital gains tax or amount to a taxable transaction. So long as the stock’s

appreciation during the term of the IDGT surpasses the debt payments owed to the original owner of

the shares, the surplus value will accrue to the beneficiaries.

Consult with your Wealth Advisor: Your Wealth Advisor can illustrate how an IDGT may

augment your wealth planning prior to the sale of your company.

Figure 6: Use of a Grantor Retained Annuity Trust (“GRAT”) for pre-sale planning

The Grantor contributes assets to a trust in anticipation

of their appreciation.

The GRAT pays an annuity back to the grantor for the

term of the trust.

Upon the termination of the GRAT, the remainder of the assets pass to the beneficiaries with no additional

gift tax.

GrantorTrust

(GRAT) Beneficiary

Visuals on this page are for illustrative purposes only. 1. The present value calculation is predicated upon the prevailing IRS interest rate (the “7520 rate”).2. The rate of interest charged must be at least equal to the prevailing rate (i.e., the Applicable Federal Rate) in order for the transaction

not to be characterized as a taxable gift.Neither Barclays in the US nor its Wealth and Investment Management employees in the US render tax or legal advice. Please consult with your accountant, tax advisor, and/or attorney for advice concerning your particular circumstances.

15

Q: How should one address the question of restricted stock within the context of the sale of a business?

Restricted stock can refer to shares of stock that a company has awarded or sold to an employee,

which remain subject to a vesting condition. Normally, the award of stock is not a taxable event;

instead, the employee recognizes income when the vesting restrictions lapse (and the value of the

shares at that time is taxable). A sale of restricted stock before the end of the vesting period triggers

ordinary income.

Consult with your Accountant: A primary planning opportunity for restricted stock is what is

known as an “IRC Section 83(b) election”. This approach allows an individual to recognize the

value of the stock as income when received. Although the election accelerates the tax event, the

election is favorable if the value of the stock appreciates significantly before the end of the vesting

period. By making the IRC Section 83(b) election, the stockholder can capture the resultant

appreciation as long-term capital gains upon eventual sale. One nuance to the IRC Section 83(b)

election is that the shareholder must make it within 30 days of receiving the stock.

Consult with your Accountant: Although a sale of the business prior to the end of the

vesting period will cause the individual to realize ordinary income upon the sale of restricted

stock, in the event that the shareholder remains with the company after the transaction,

there may be planning opportunities for the restricted stock (e.g., charitable planning).

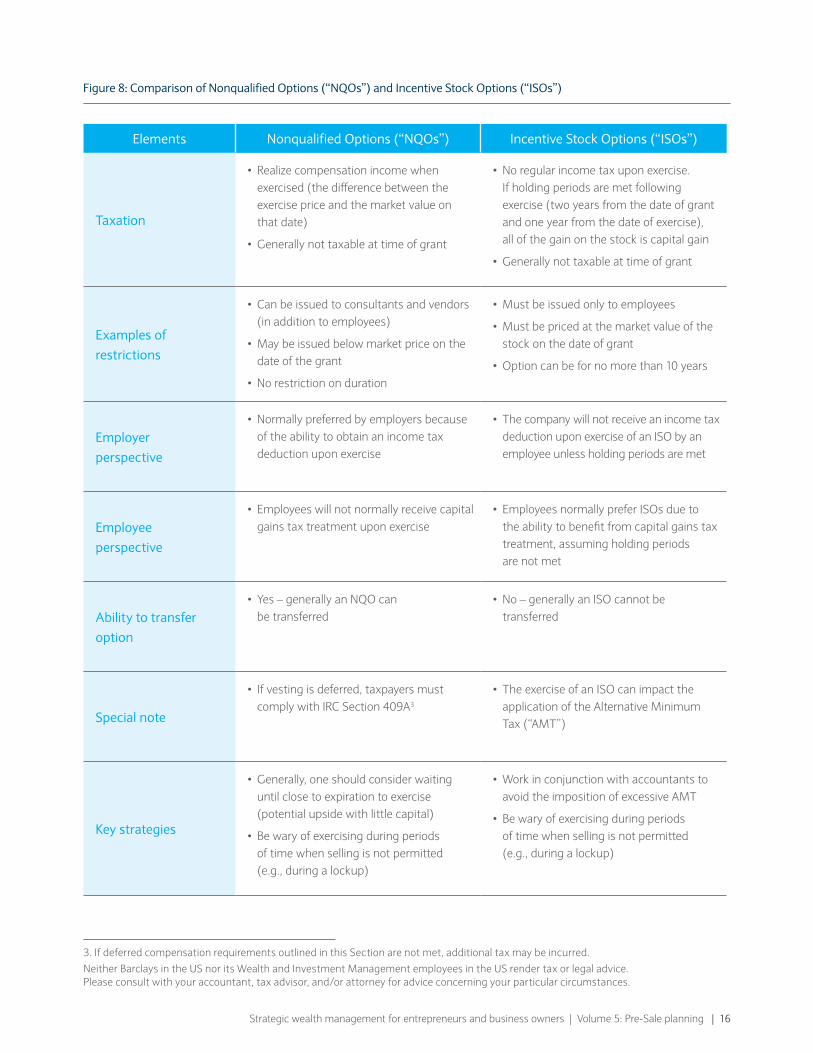

Q: How do stock options factor into the sale of a company?

There are two types of stock option vehicles – incentive stock options (“ISOs”) and nonqualified

options (“NQOs”). The chart on the following page outlines some of the basic distinctions between

the two types of options.

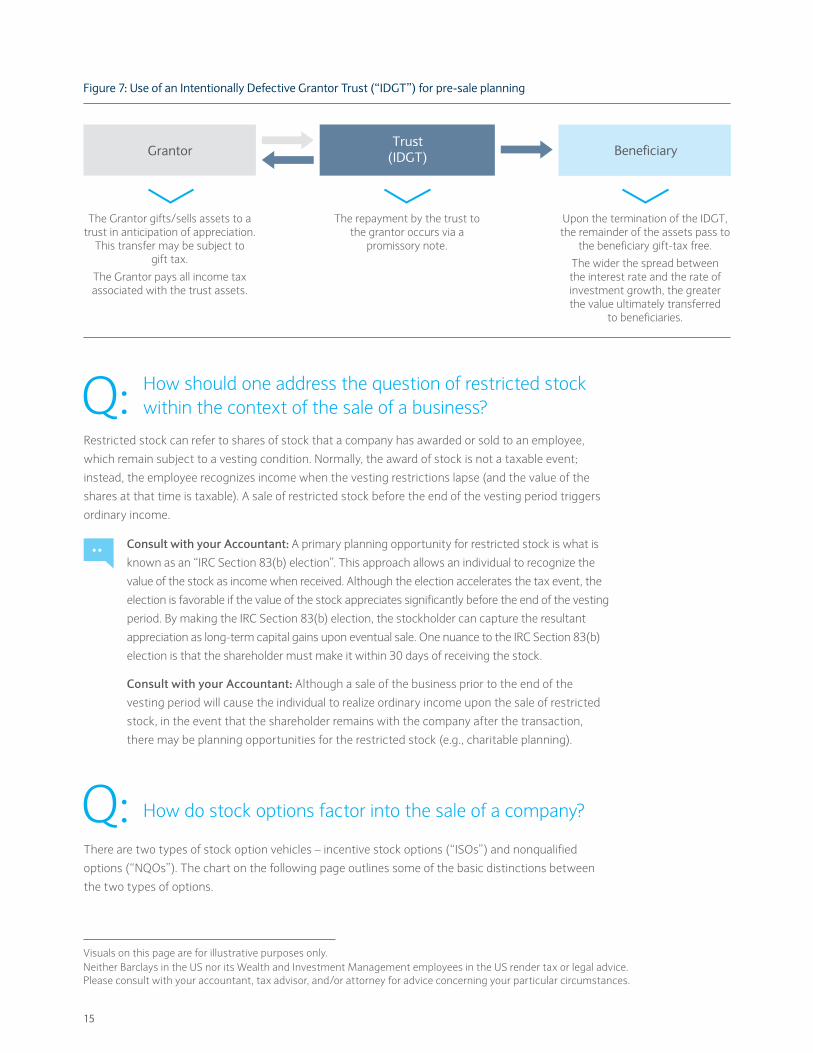

Figure 7: Use of an Intentionally Defective Grantor Trust (“IDGT”) for pre-sale planning

The Grantor gifts/sells assets to a trust in anticipation of appreciation.

This transfer may be subject to gift tax.

The Grantor pays all income tax associated with the trust assets.

The repayment by the trust to the grantor occurs via a

promissory note.

Upon the termination of the IDGT, the remainder of the assets pass to

the beneficiary gift-tax free.

The wider the spread between the interest rate and the rate of investment growth, the greater the value ultimately transferred

to beneficiaries.

GrantorTrust

(IDGT) Beneficiary

Visuals on this page are for illustrative purposes only.Neither Barclays in the US nor its Wealth and Investment Management employees in the US render tax or legal advice. Please consult with your accountant, tax advisor, and/or attorney for advice concerning your particular circumstances.

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 16

Figure 8: Comparison of Nonqualified Options (“NQOs”) and Incentive Stock Options (“ISOs”)

Elements Nonqualified Options (“NQOs”) Incentive Stock Options (“ISOs”)

Taxation

• Realize compensation income when exercised (the difference between the exercise price and the market value on that date)

• Generally not taxable at time of grant

• No regular income tax upon exercise. If holding periods are met following exercise (two years from the date of grant and one year from the date of exercise), all of the gain on the stock is capital gain

• Generally not taxable at time of grant

Examples of restrictions

• Can be issued to consultants and vendors (in addition to employees)

• May be issued below market price on the date of the grant

• No restriction on duration

• Must be issued only to employees

• Must be priced at the market value of the stock on the date of grant

• Option can be for no more than 10 years

Employer perspective

• Normally preferred by employers because of the ability to obtain an income tax deduction upon exercise

• The company will not receive an income tax deduction upon exercise of an ISO by an employee unless holding periods are met

Employee perspective

• Employees will not normally receive capital gains tax treatment upon exercise

• Employees normally prefer ISOs due to the ability to benefit from capital gains tax treatment, assuming holding periods are not met

Ability to transfer option

• Yes – generally an NQO can be transferred

• No – generally an ISO cannot be transferred

Special note

• If vesting is deferred, taxpayers must comply with IRC Section 409A3

• The exercise of an ISO can impact the application of the Alternative Minimum Tax (“AMT”)

Key strategies

• Generally, one should consider waiting until close to expiration to exercise (potential upside with little capital)

• Be wary of exercising during periods of time when selling is not permitted (e.g., during a lockup)

• Work in conjunction with accountants to avoid the imposition of excessive AMT

• Be wary of exercising during periods of time when selling is not permitted (e.g., during a lockup)

3. If deferred compensation requirements outlined in this Section are not met, additional tax may be incurred.

Neither Barclays in the US nor its Wealth and Investment Management employees in the US render tax or legal advice. Please consult with your accountant, tax advisor, and/or attorney for advice concerning your particular circumstances.

17

Consult with your Accountant: Often, pre-sale planning for NQOs attempts to balance the

total cost of exercise (option price plus taxes payable) against the potential for capital gains

treatment on subsequent appreciation. If the stock has a low value, this may prove to be a

favorable trade-off. Normally, a business owner’s accountant can provide insight into how

best to quantify this analysis for his or her particular circumstances.

Consult with your Accountant: Individuals should work with their advisors to understand the

potential impact of an impending sale upon holding periods for their options. For example, ISO

rules require the employee to sell his or her stock more than two years after the date of the option

grant and one year after the date of exercise. As with NQOs, the timing of a sale may make it

impossible to comply with the holding period rules. Individuals may then find themselves in the

position of paying substantially higher taxes on their equity incentive packages.

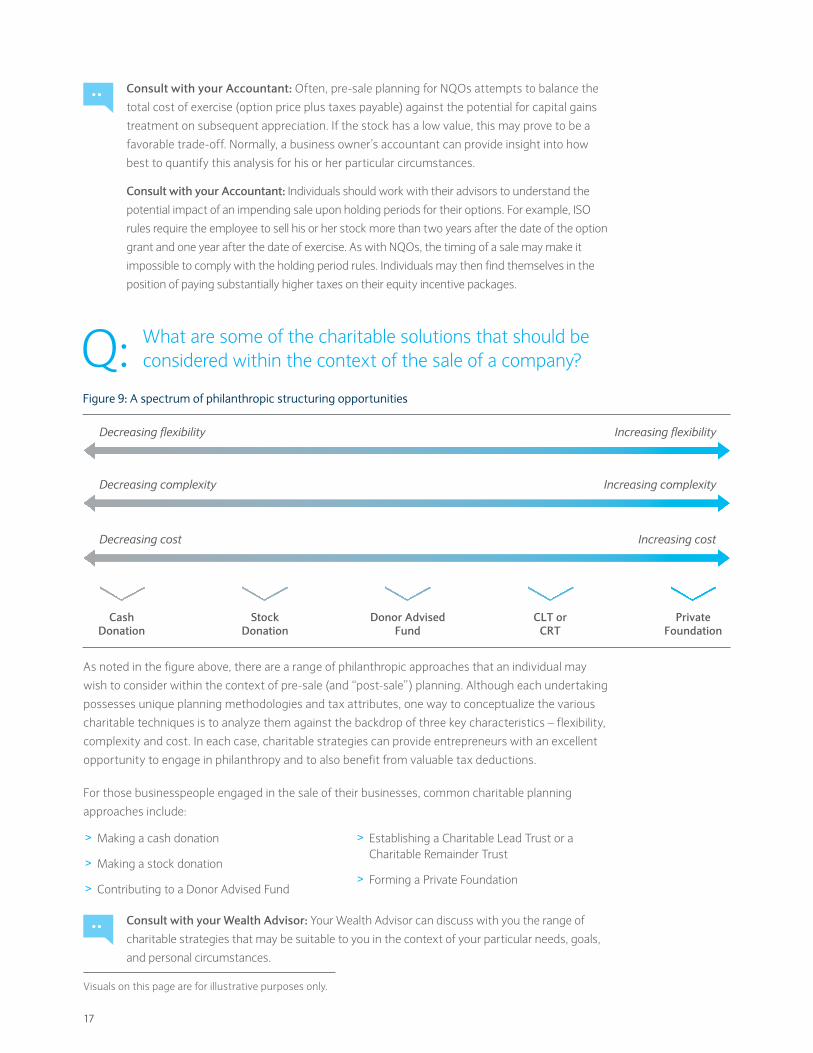

Q: What are some of the charitable solutions that should be considered within the context of the sale of a company?

As noted in the figure above, there are a range of philanthropic approaches that an individual may

wish to consider within the context of pre-sale (and “post-sale”) planning. Although each undertaking

possesses unique planning methodologies and tax attributes, one way to conceptualize the various

charitable techniques is to analyze them against the backdrop of three key characteristics – flexibility,

complexity and cost. In each case, charitable strategies can provide entrepreneurs with an excellent

opportunity to engage in philanthropy and to also benefit from valuable tax deductions.

For those businesspeople engaged in the sale of their businesses, common charitable planning

approaches include:

Consult with your Wealth Advisor: Your Wealth Advisor can discuss with you the range of

charitable strategies that may be suitable to you in the context of your particular needs, goals,

and personal circumstances.

Figure 9: A spectrum of philanthropic structuring opportunities

CashDonation

StockDonation

PrivateFoundation

Donor AdvisedFund

CLT orCRT

Decreasing flexibility Increasing flexibility

Decreasing complexity Increasing complexity

Decreasing cost Increasing cost

> Making a cash donation

> Making a stock donation

> Contributing to a Donor Advised Fund

> Establishing a Charitable Lead Trust or a Charitable Remainder Trust

> Forming a Private Foundation

Visuals on this page are for illustrative purposes only.

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 18

Step 3Analyze the elements of the sale

19

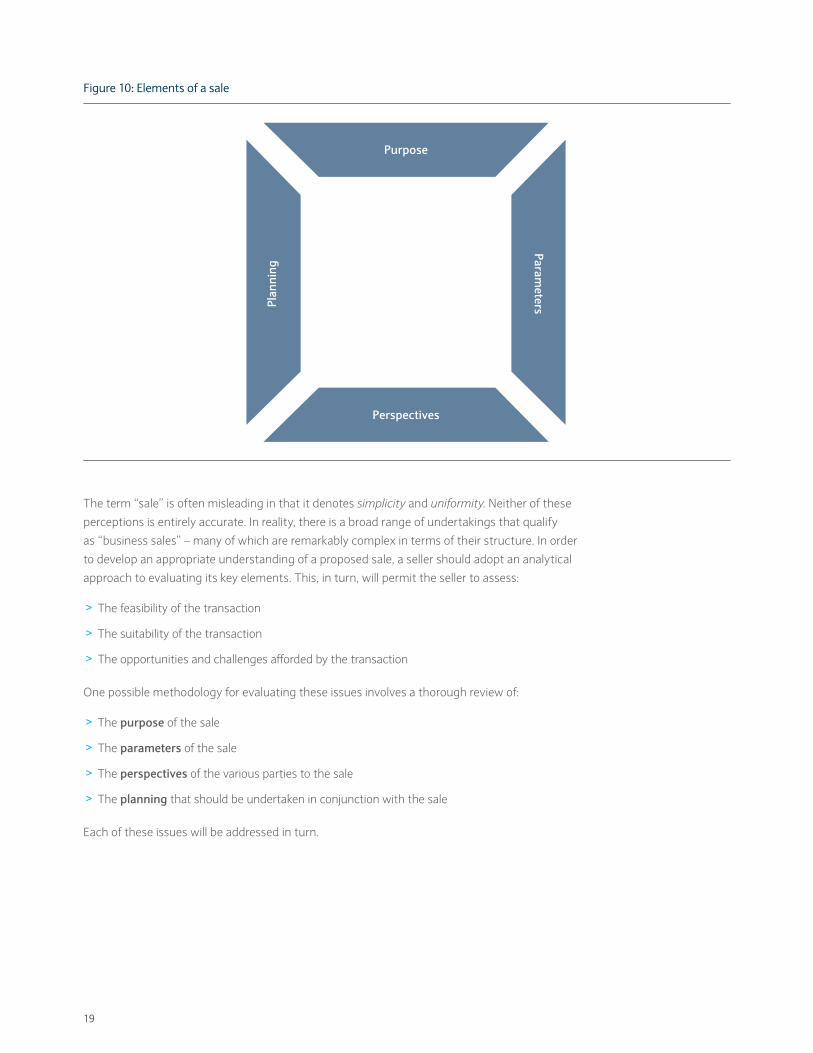

The term “sale” is often misleading in that it denotes simplicity and uniformity. Neither of these

perceptions is entirely accurate. In reality, there is a broad range of undertakings that qualify

as “business sales” – many of which are remarkably complex in terms of their structure. In order

to develop an appropriate understanding of a proposed sale, a seller should adopt an analytical

approach to evaluating its key elements. This, in turn, will permit the seller to assess:

> The feasibility of the transaction

> The suitability of the transaction

> The opportunities and challenges afforded by the transaction

One possible methodology for evaluating these issues involves a thorough review of:

> The purpose of the sale

> The parameters of the sale

> The perspectives of the various parties to the sale

> The planning that should be undertaken in conjunction with the sale

Each of these issues will be addressed in turn.

Figure 10: Elements of a sale

Purpose

Perspectives

ParametersPl

anni

ng

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 20

Q: What are some of the questions that should normally be addressed when analyzing the purpose of a sale?

Q: Why do you want to sell your business?

There are a variety of reasons why individuals normally decide to sell their business. Some of the more

common motivations for seeking to exit an ownership role include:

> A desire to diversify holdings

> A desire to seek out new entrepreneurial challenges

> Age

> Financial pressures

> Illness

> Retirement

> Underperformance of the business

Regardless of the underlying motivation, business owners should ask themselves whether or not

there is an alignment between:

> The rationale for the sale and

> The sale itself

In some instances, the goals of the entrepreneur can (or should) be achieved through the use of an

approach or technique other than a sale.

Figure 11: Elements of a sale – Purpose

> Why sell?

> IPO vs. sale

> Alternatives to a sale

Purpose

Perspectives

ParametersPl

anni

ng

21

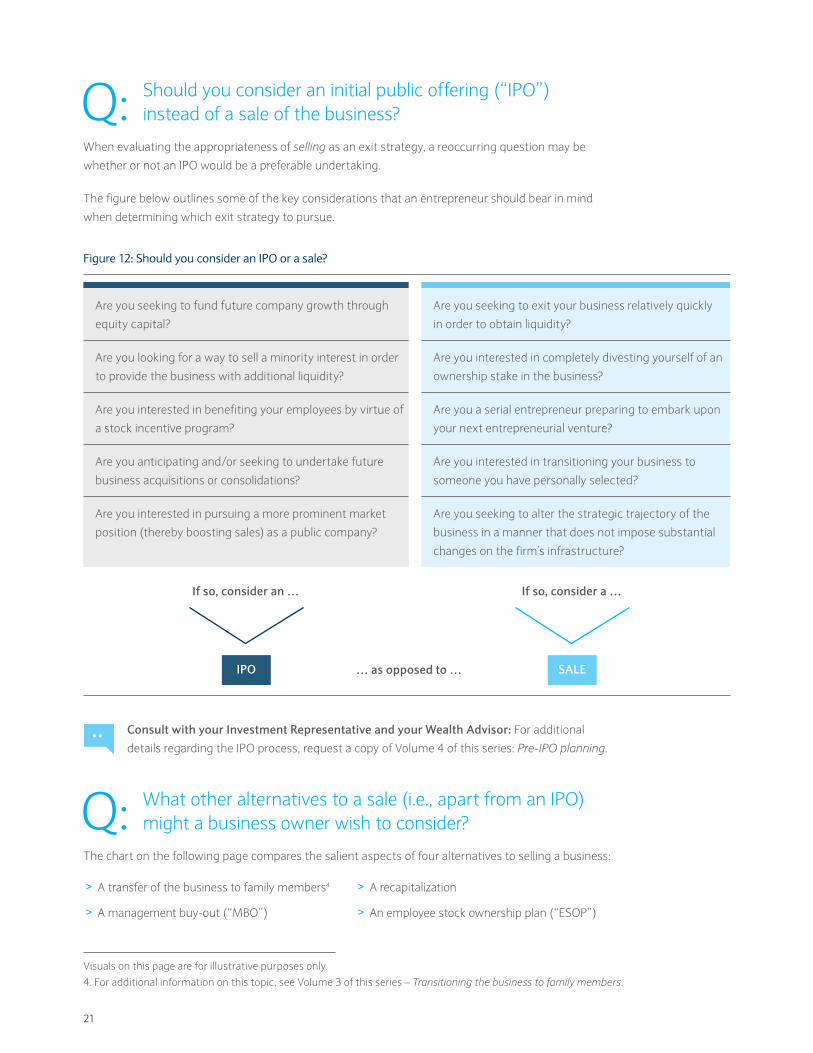

Q: Should you consider an initial public offering (“IPO”) instead of a sale of the business?

When evaluating the appropriateness of selling as an exit strategy, a reoccurring question may be

whether or not an IPO would be a preferable undertaking.

The figure below outlines some of the key considerations that an entrepreneur should bear in mind

when determining which exit strategy to pursue.

Consult with your Investment Representative and your Wealth Advisor: For additional

details regarding the IPO process, request a copy of Volume 4 of this series: Pre-IPO planning.

Q: What other alternatives to a sale (i.e., apart from an IPO) might a business owner wish to consider?

The chart on the following page compares the salient aspects of four alternatives to selling a business:

> A transfer of the business to family members4

> A management buy-out (“MBO”)

> A recapitalization

> An employee stock ownership plan (“ESOP”)

Figure 12: Should you consider an IPO or a sale?

Are you seeking to fund future company growth through

equity capital?

Are you seeking to exit your business relatively quickly

in order to obtain liquidity?

Are you looking for a way to sell a minority interest in order

to provide the business with additional liquidity?

Are you interested in completely divesting yourself of an

ownership stake in the business?

Are you interested in benefiting your employees by virtue of

a stock incentive program?

Are you a serial entrepreneur preparing to embark upon

your next entrepreneurial venture?

Are you anticipating and/or seeking to undertake future

business acquisitions or consolidations?

Are you interested in transitioning your business to

someone you have personally selected?

Are you interested in pursuing a more prominent market

position (thereby boosting sales) as a public company?

Are you seeking to alter the strategic trajectory of the

business in a manner that does not impose substantial

changes on the firm’s infrastructure?

If so, consider an …

… as opposed to …

If so, consider a …

IPO SALE

Visuals on this page are for illustrative purposes only.

4. For additional information on this topic, see Volume 3 of this series – Transitioning the business to family members.

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 22

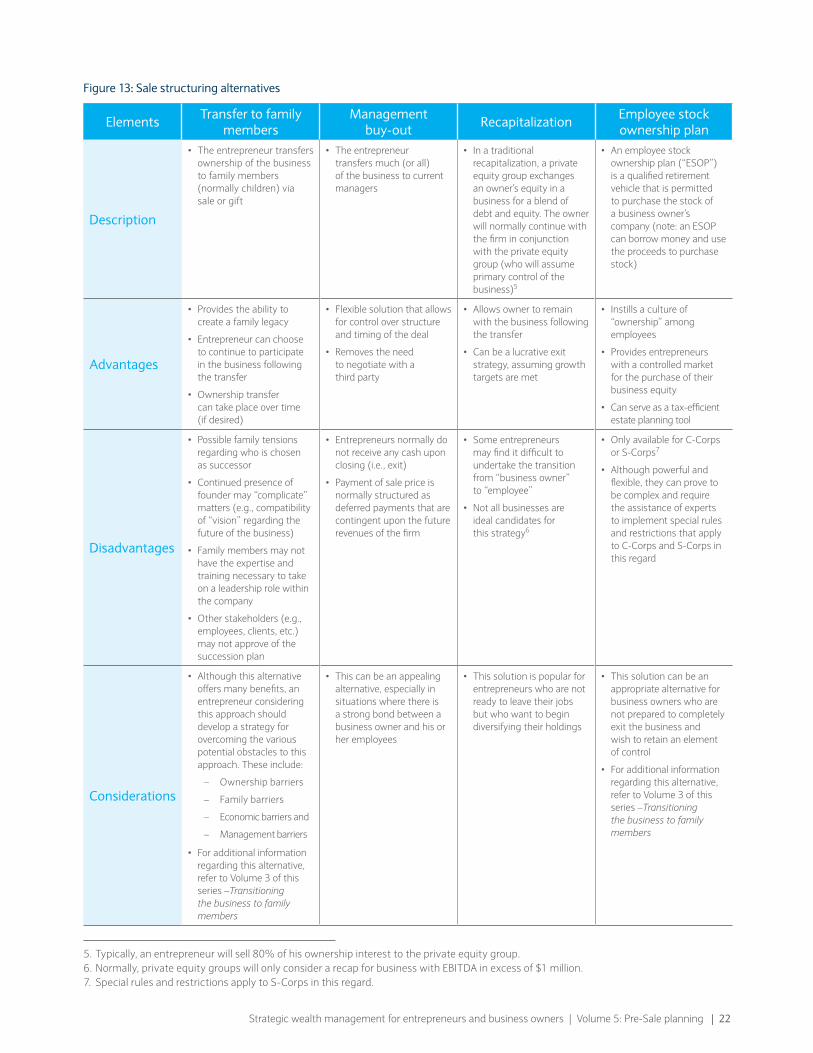

Figure 13: Sale structuring alternatives

Elements Transfer to family members

Management buy-out Recapitalization Employee stock

ownership plan

Description

• The entrepreneur transfers ownership of the business to family members (normally children) via sale or gift

• The entrepreneur transfers much (or all) of the business to current managers

• In a traditional recapitalization, a private equity group exchanges an owner’s equity in a business for a blend of debt and equity. The owner will normally continue with the firm in conjunction with the private equity group (who will assume primary control of the business)5

• An employee stock ownership plan (“ESOP”) is a qualified retirement vehicle that is permitted to purchase the stock of a business owner’s company (note: an ESOP can borrow money and use the proceeds to purchase stock)

Advantages

• Provides the ability to create a family legacy

• Entrepreneur can choose to continue to participate in the business following the transfer

• Ownership transfer can take place over time (if desired)

• Flexible solution that allows for control over structure and timing of the deal

• Removes the need to negotiate with a third party

• Allows owner to remain with the business following the transfer

• Can be a lucrative exit strategy, assuming growth targets are met

• Instills a culture of “ownership” among employees

• Provides entrepreneurs with a controlled market for the purchase of their business equity

• Can serve as a tax-efficient estate planning tool

Disadvantages

• Possible family tensions regarding who is chosen as successor

• Continued presence of founder may “complicate” matters (e.g., compatibility of “vision” regarding the future of the business)

• Family members may not have the expertise and training necessary to take on a leadership role within the company

• Other stakeholders (e.g., employees, clients, etc.) may not approve of the succession plan

• Entrepreneurs normally do not receive any cash upon closing (i.e., exit)

• Payment of sale price is normally structured as deferred payments that are contingent upon the future revenues of the firm

• Some entrepreneurs may find it difficult to undertake the transition from “business owner” to “employee”

• Not all businesses are ideal candidates for this strategy6

• Only available for C-Corps or S-Corps7

• Although powerful and flexible, they can prove to be complex and require the assistance of experts to implement special rules and restrictions that apply to C-Corps and S-Corps in this regard

Considerations

• Although this alternative offers many benefits, an entrepreneur considering this approach should develop a strategy for overcoming the various potential obstacles to this approach. These include:

– Ownership barriers

– Family barriers

– Economic barriers and

– Management barriers

• For additional information regarding this alternative, refer to Volume 3 of this series –Transitioning the business to family members

• This can be an appealing alternative, especially in situations where there is a strong bond between a business owner and his or her employees

• This solution is popular for entrepreneurs who are not ready to leave their jobs but who want to begin diversifying their holdings

• This solution can be an appropriate alternative for business owners who are not prepared to completely exit the business and wish to retain an element of control

• For additional information regarding this alternative, refer to Volume 3 of this series –Transitioning the business to family members

5. Typically, an entrepreneur will sell 80% of his ownership interest to the private equity group.6. Normally, private equity groups will only consider a recap for business with EBITDA in excess of $1 million.7. Special rules and restrictions apply to S-Corps in this regard.

23

If, after having addressed the purpose and alternatives to a sale, an entrepreneur wishes to proceed

with the disposition of his or her business, the next question that requires resolution is, “What are the

parameters of the proposed sale?”

Q: What are some of the questions that should normally be addressed when analyzing the parameters of a sale?

Q: Should the sale be structured as an asset sale or a stock sale? How do the two differ?

In an asset sale, the buyer purchases some or all of the individual assets of the target company,

such as:

> Licenses

> Goodwill

> Inventory

In the case of a stock (or equity) sale, the buyer obtains ownership of the company stock.

For reasons that will be explained further, buyers normally wish to purchase a company’s assets.

By contrast, sellers normally wish to sell their stock in a business.

Figure 14: Elements of a sale – Parameters

> Sale structure

> Asset vs. stock sale

> Taxable vs. tax-free

> Income tax considerations

Purpose

Perspectives

ParametersPl

anni

ng

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 24

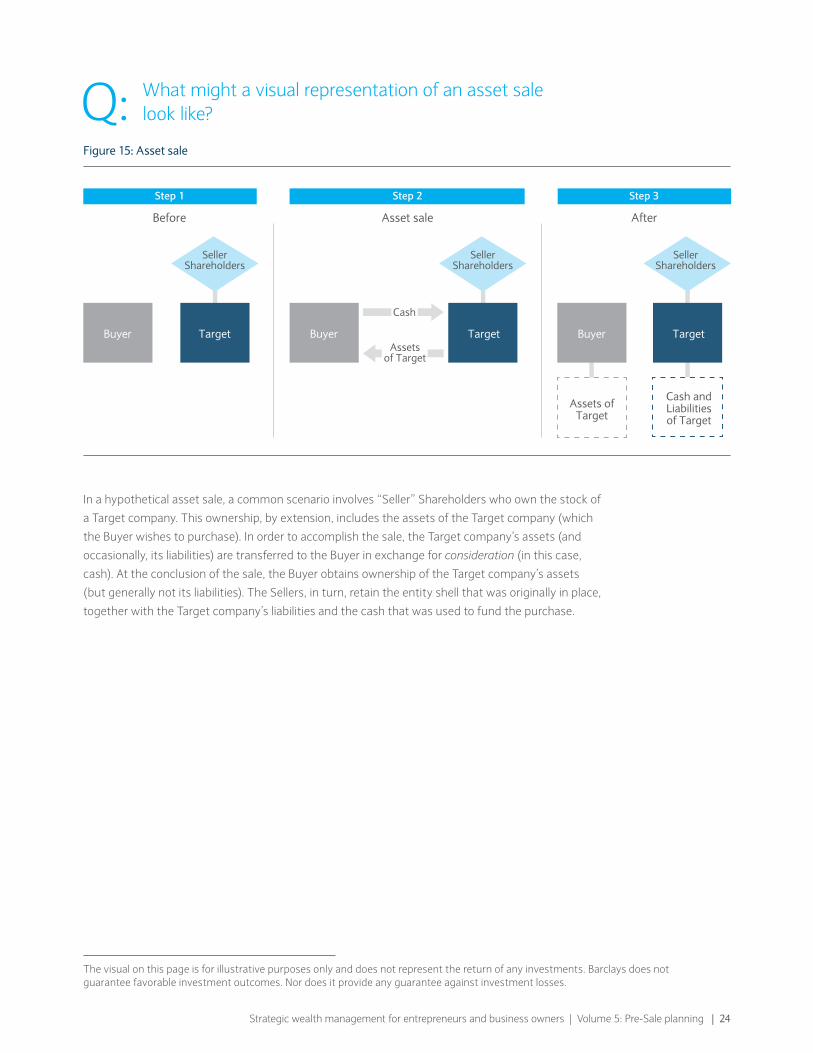

Q: What might a visual representation of an asset sale look like?

In a hypothetical asset sale, a common scenario involves “Seller” Shareholders who own the stock of

a Target company. This ownership, by extension, includes the assets of the Target company (which

the Buyer wishes to purchase). In order to accomplish the sale, the Target company’s assets (and

occasionally, its liabilities) are transferred to the Buyer in exchange for consideration (in this case,

cash). At the conclusion of the sale, the Buyer obtains ownership of the Target company’s assets

(but generally not its liabilities). The Sellers, in turn, retain the entity shell that was originally in place,

together with the Target company’s liabilities and the cash that was used to fund the purchase.

Figure 15: Asset sale

Before

Buyer

SellerShareholders

Target

Step 1

Asset sale

Buyer

SellerShareholders

Target

Cash

Assetsof Target

Step 2

After

Buyer

SellerShareholders

Target

Cash andLiabilitiesof Target

Assets ofTarget

Step 3

The visual on this page is for illustrative purposes only and does not represent the return of any investments. Barclays does not guarantee favorable investment outcomes. Nor does it provide any guarantee against investment losses.

25

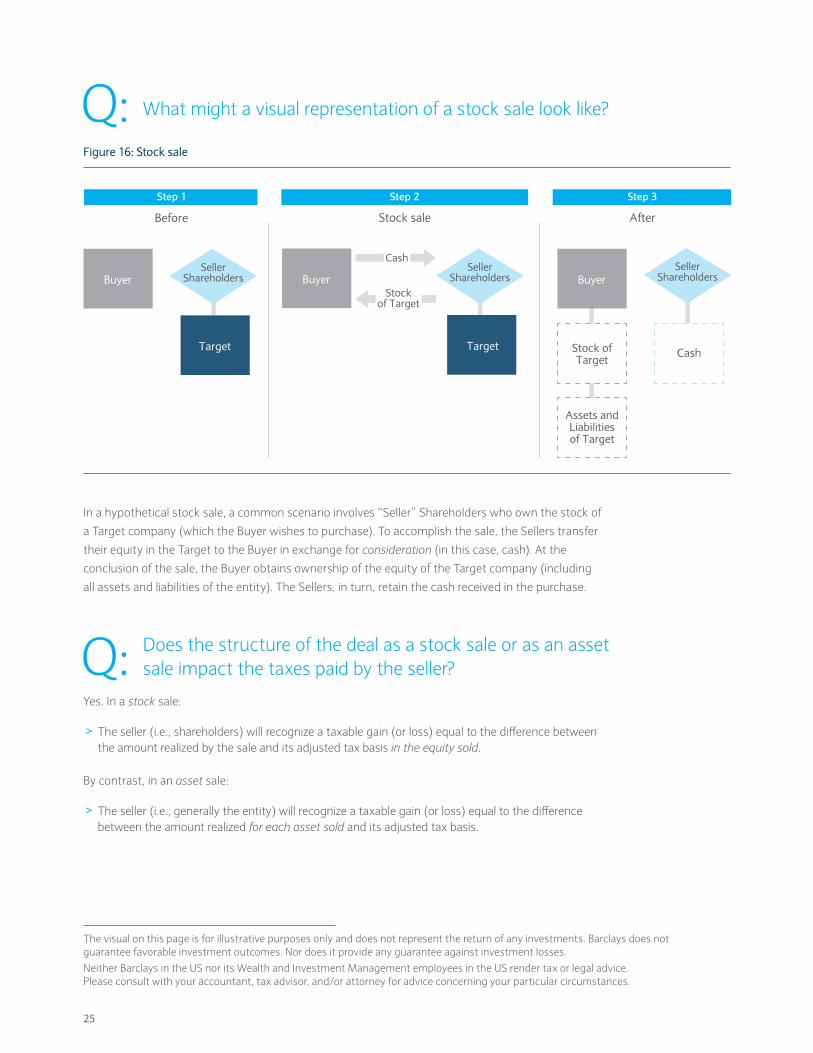

Q: What might a visual representation of a stock sale look like?

In a hypothetical stock sale, a common scenario involves “Seller” Shareholders who own the stock of

a Target company (which the Buyer wishes to purchase). To accomplish the sale, the Sellers transfer

their equity in the Target to the Buyer in exchange for consideration (in this case, cash). At the

conclusion of the sale, the Buyer obtains ownership of the equity of the Target company (including

all assets and liabilities of the entity). The Sellers, in turn, retain the cash received in the purchase.

Q: Does the structure of the deal as a stock sale or as an asset sale impact the taxes paid by the seller?

Yes. In a stock sale:

> The seller (i.e., shareholders) will recognize a taxable gain (or loss) equal to the difference between the amount realized by the sale and its adjusted tax basis in the equity sold.

By contrast, in an asset sale:

> The seller (i.e., generally the entity) will recognize a taxable gain (or loss) equal to the difference between the amount realized for each asset sold and its adjusted tax basis.

Figure 16: Stock sale

Before Stock sale After

Step 1 Step 2 Step 3

BuyerSeller

Shareholders

Target

BuyerSeller

Shareholders

CashStock ofTarget

Assets andLiabilitiesof Target

BuyerSeller

Shareholders

Target

Cash

Stockof Target

The visual on this page is for illustrative purposes only and does not represent the return of any investments. Barclays does not guarantee favorable investment outcomes. Nor does it provide any guarantee against investment losses.

Neither Barclays in the US nor its Wealth and Investment Management employees in the US render tax or legal advice. Please consult with your accountant, tax advisor, and/or attorney for advice concerning your particular circumstances.

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 26

Q: Is it possible to structure a sale in such a way as to make it tax-free?

Yes. In contrast to situations where a company is sold and a taxable gain (or loss) is realized by the

seller, there are also instances where taxation can be minimized (or deferred). In general, transactions

that qualify for this form of tax treatment are known as tax-free “reorganizations”8 and include a

range of undertakings including mergers, consolidations, and acquisitions. The differentiation in tax

treatment arises by virtue of the fact that a tax-free transaction can qualify as a “continuation of

interest in the old property”. By contrast, a taxable sale is perceived to be a “complete disposition”

of the business.

Broadly speaking, tax-free reorganizations exhibit two key attributes:

> Both the acquirer and the seller are corporations

> Some (or all) of the consideration paid for the purchase includes the buyer’s stock

In instances where both of these criteria are satisfied, the transaction may normally be structured as a

tax-free reorganization.

Q: What are some of the issues – from an income tax perspective – that need to be considered when structuring

the sale of a business for cash?

Cash transactions provide a significant trade-off to business owners. On one hand, they provide a

true “liquidity” event (unlike, for example, an IPO, wherein true liquidity may not arise for months or

even years after the transaction).

However, sellers who participate in a cash transaction will face an immediate tax liability on the

transaction (versus, for example, a tax-free reorganization), and any missteps in the structuring or

executing of the sale can result in significant (and costly) problems.

Consult with your Tax Attorney and your CPA: Business owners who are considering the sale

of their company should work very closely with their tax advisors to ensure compliance with the

various guidelines set forth in the Internal Revenue Code.

After having analyzed the parameters of a sale, the next question that requires resolution is,

“What are the perspectives of the parties to a sale?”

8. See IRC Sec. 368(a)(1) for a more precise definition.

Neither Barclays in the US nor its Wealth and Investment Management employees in the US render tax or legal advice. Please consult with your accountant, tax advisor, and/or attorney for advice concerning your particular circumstances.

27

Q: What are some of the questions that should normally be addressed when analyzing the perspectives of the parties

to a sale?

Q: From a seller’s perspective, which is preferable – a stock sale or an asset sale (and why)?

In most instances, sellers prefer stock sales.

As discussed earlier in this chapter, when a stock sale occurs, the buyer purchases the seller’s

corporate stock in the target entity. This can be beneficial to the seller for a couple of reasons:

> From a tax perspective, stock sales are preferable to the seller because the proceeds of the transaction are generally taxed at (lower) capital gains rates.

> From a liability perspective, stock sales are preferable to the seller because potential future liabilities (e.g., lawsuits) are transferred to the buyer.

Figure 17: Elements of a sale – Perspectives

> Seller preferences

> Buyer preferences

> The basis step-up

> Structural considerations

Purpose

Perspectives

ParametersPl

anni

ng

Neither Barclays in the US nor its Wealth and Investment Management employees in the US render tax or legal advice. Please consult with your accountant, tax advisor, and/or attorney for advice concerning your particular circumstances.

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 28

Q: From a buyer’s perspective, which is preferable – a stock sale or an asset sale (and why)?

In most instances, buyers prefer asset sales.

As discussed earlier in this chapter, when an asset sale occurs, the buyer purchases some or all of the

individual assets of the target entity. This can be beneficial to the buyer for a couple of reasons:

> From a tax perspective, asset sales are preferable to the buyer because they can obtain a “basis step-up” on the assets purchased (which will provide advantageous future tax deductions).

> From a liability perspective, asset sales are preferable to the buyer because this approach eliminates the concern that they may inadvertently assume any unknown liabilities of the seller (i.e., they can “cherry pick” assets).

Q: Can buyers and sellers freely choose whether to structure a sale as a stock sale or as an asset sale?

If the business being considered for sale is structured as a sole proprietorship, partnership or LLC,

then the transaction must generally take the form of an asset sale.

If the business being considered for sale is structured as a C-Corporation or an S-Corporation, then

the buyer and seller may elect whether to structure the sale as a stock sale or as an asset sale.

Consult with your Investment Representative and your Wealth Advisor: For additional

details regarding the various entity structuring options available to entrepreneurs,

request a copy of Strategic wealth management for entrepreneurs and business owners

(Volume 1: Forming a business).

Neither Barclays in the US nor its Wealth and Investment Management employees in the US render tax or legal advice. Please consult with your accountant, tax advisor, and/or attorney for advice concerning your particular circumstances.

29

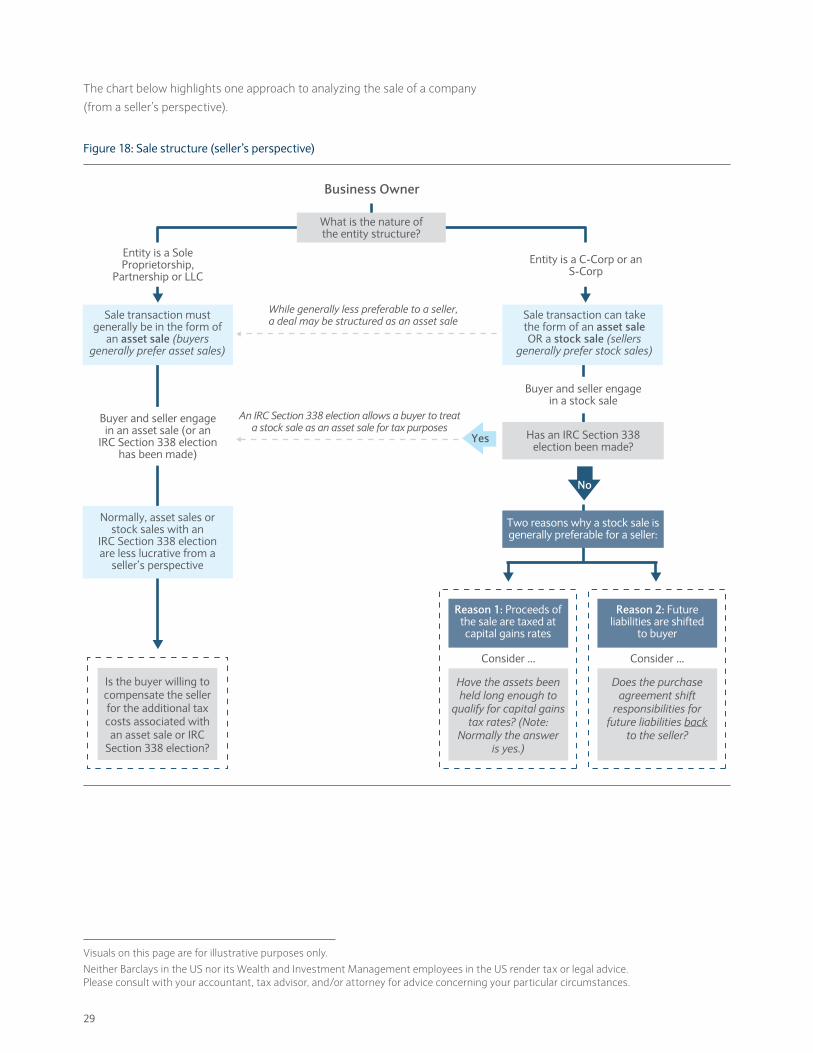

The chart below highlights one approach to analyzing the sale of a company

(from a seller’s perspective).

Figure 18: Sale structure (seller’s perspective)

Business Owner

What is the nature of the entity structure?

While generally less preferable to a seller, a deal may be structured as an asset sale

An IRC Section 338 election allows a buyer to treat a stock sale as an asset sale for tax purposes

Entity is a C-Corp or an S-Corp

Buyer and seller engage in a stock sale

Consider ... Consider ...

Has an IRC Section 338 election been made?

Two reasons why a stock sale is generally preferable for a seller:

Reason 1: Proceeds of the sale are taxed at capital gains rates

Reason 2: Future liabilities are shifted

to buyer

Entity is a Sole Proprietorship,

Partnership or LLC

Buyer and seller engage in an asset sale (or an

IRC Section 338 election has been made)

Sale transaction must generally be in the form of

an asset sale (buyers generally prefer asset sales)

Sale transaction can take the form of an asset saleOR a stock sale (sellers

generally prefer stock sales)

Normally, asset sales or stock sales with an

IRC Section 338 election are less lucrative from a

seller’s perspective

Is the buyer willing to compensate the seller for the additional tax costs associated with an asset sale or IRC

Section 338 election?

Have the assets been held long enough to

qualify for capital gains tax rates? (Note:

Normally the answer is yes.)

Does the purchase agreement shift

responsibilities for future liabilities back

to the seller?

No

Yes

Visuals on this page are for illustrative purposes only.

Neither Barclays in the US nor its Wealth and Investment Management employees in the US render tax or legal advice. Please consult with your accountant, tax advisor, and/or attorney for advice concerning your particular circumstances.

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 30

Q: How relevant is the issue of the “basis step-up” to buyers and sellers?

From the perspective of a “buyer”, a sale that allows a step-up in asset basis to reflect the purchase

price can make the transaction significantly more valuable.9 In order to achieve a basis step-up, the

transaction must take the form of either a purchase of assets or a stock purchase in conjunction with

what is known as an “IRC Section 338 election.”10

From the seller’s perspective, however, the cost of a basis step-up is that the seller must recognize

gain on the asset sale. In some instances, this can dramatically impact the financial and commercial

appeal of the undertaking.

Consult with your Accountant: The type of legal structure (e.g., S-Corp, C-Corp, etc.)

associated with the selling entity will have a significant impact upon the ultimate tax treatment

of the transaction. If possible, work with your accountant at the time of inception to mitigate

the potential issues that can arise during the course of a sale of a company.

Consult with your Valuation Consultant and your Accountant: In some instances, a

company may begin as a C-Corp but convert to an S-Corp at some point in its development.

If this is the case, a subsequent sale of the company’s assets within the following 10-year

period will trigger a “built-in” corporate tax on that gain. If the gain is large relative to the

overall size of the deal, the additional corporate tax could make a basis step-up election

unfeasible for the parties.11

Consult with your Accountant: Even if a company has been an S-Corp for the duration of its

existence, owners should still be mindful of the form of the sale transaction. Selling stock for

cash will lock in “capital gains” treatment; however, selling assets (or making an IRC Section

338 election) can trigger ordinary income treatment on a portion of the gain and clients

should work with their accountants to address this issue (if applicable).12

Consult with your Accountant: A buyer may be willing to compensate the seller of the

company for the additional tax costs associated with an asset sale/Sec. 338 transaction. The

main point of negotiation will normally stem from the quantification of the “ordinary income

recapture amount” and the calculation of the payment needed to produce the same after-tax

result as a stock sale.

After having analyzed the perspectives of the parties to a sale, the next question that requires

resolution is, “What are issues that need to be analyzed when considering the planning associated

with a sale?”

9. One way in which this is achieved is by virtue of federal tax law provisions regarding the amortization of certain intangible assets.10. Normally, when a buyer enters into a stock sale, they will not be entitled to a step-up in tax basis of the assets (i.e., to fair market

value). Instead, they receive the assets with a carryover basis. In instances where an IRC Section 338 election is made, the transaction is treated (for hypothetical tax purposes) as if it was an asset sale. This allows the buyer’s basis to be adjusted to reflect the price paid for the purchase.

11. As a result, one of the earliest due diligence tasks for an advisor is to determine the tax history of the S-Corp. If there has been a conversion to S-status within the past 10 years, it is crucial to quantify the built-in gain amount that might be triggered through a sale.

For business owners with sufficient foresight, it is often advisable to appraise the company’s value at the time of the conversion to S-status. In that way, there is a contemporaneous record of the asset values, allowing the company to quantify the built-in gain amount. Absent the appraisal, the IRS will have additional latitude to argue that the appreciation accrued prior to the conversion (amounting to a built-in gain that is therefore taxable), as opposed to afterward.

12. To the extent that the company has inventory or receivables in excess of tax basis, the sale will produce ordinary income. There may also be depreciation recapture that will be taxable at ordinary rates.

Neither Barclays in the US nor its Wealth and Investment Management employees in the US render tax or legal advice. Please consult with your accountant, tax advisor, and/or attorney for advice concerning your particular circumstances.

31

Q: What are some of the questions that should normally be addressed when analyzing the planning elements of a sale?

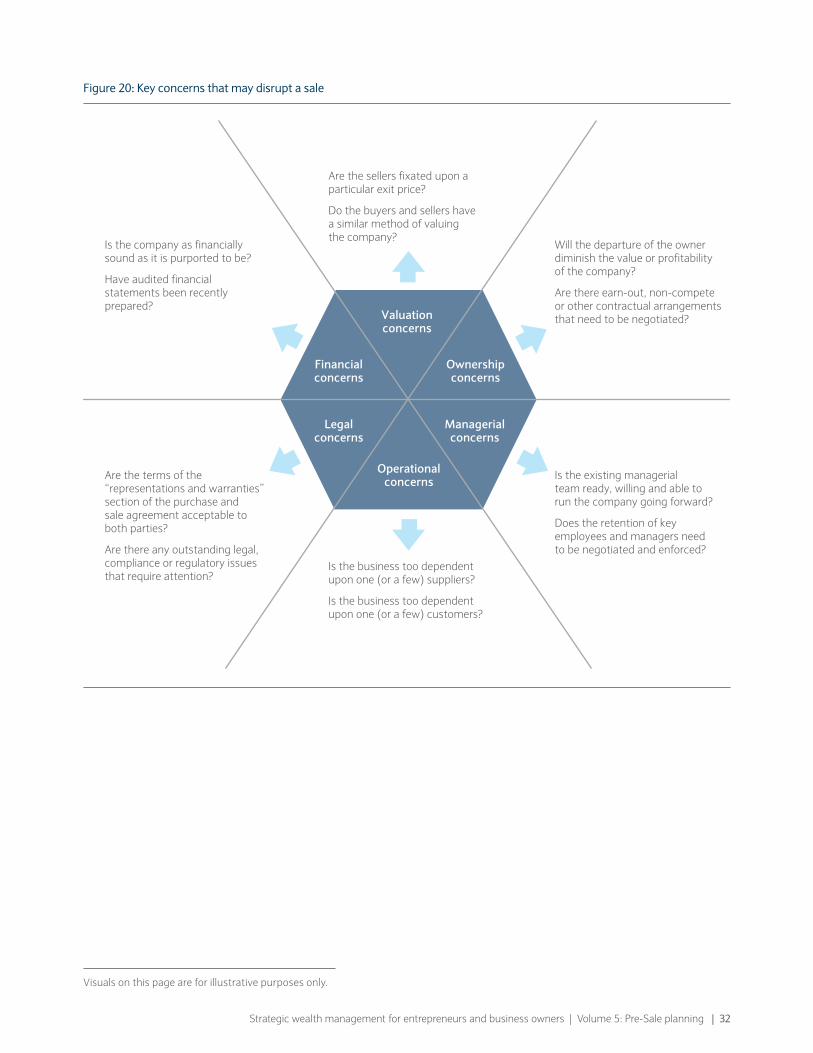

Q: What are some of key concerns that may disrupt a sale?

When preparing to finalize a sale, sellers should be aware that there are particular issues that can arise

which may adversely affect the price, timing or even the viability of the transaction. This can be due

to a variety of causes, including:

> A divergence of perspective between buyer and seller

> An inadvertent oversight

> A lack of resolution regarding a key issue or question

In attempting to anticipate (and avoid) such problems, a seller may wish to pay close attention to

elements of the business deal that often elicit the greatest degree of concern among buyers, such as:

> Valuation concerns

> Ownership concerns

> Managerial concerns

> Operational concerns

> Legal concerns

> Financial concerns

The figure on the following page outlines some of the key questions that buyers and sellers must

often address prior to finalizing a sale.

Figure 19: Elements of a sale – Planning

> Potential disruptions to a sale

> Integrated pre-sale checklist

Purpose

Perspectives

ParametersPl

anni

ng

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 32

Figure 20: Key concerns that may disrupt a sale

Are the sellers fixated upon a particular exit price?

Do the buyers and sellers have a similar method of valuing the company?

Will the departure of the owner diminish the value or profitability of the company?

Are there earn-out, non-compete or other contractual arrangements that need to be negotiated?

Is the existing managerialteam ready, willing and able to run the company going forward?

Does the retention of key employees and managers need to be negotiated and enforced?

Is the business too dependent upon one (or a few) suppliers?

Is the business too dependent upon one (or a few) customers?

Valuation concerns

Financialconcerns

Ownershipconcerns

Legalconcerns

Managerialconcerns

OperationalconcernsAre the terms of the

“representations and warranties” section of the purchase and sale agreement acceptable to both parties?

Are there any outstanding legal, compliance or regulatory issues that require attention?

Is the company as financially sound as it is purported to be?

Have audited financial statements been recently prepared?

Visuals on this page are for illustrative purposes only.

33

Consult with your advisors: In practice, many business sales progress to the point of near-

completion, only to be derailed by unforeseen hurdles and challenges. To help avoid this,

business owners should work closely with their advisory group in order to anticipate and

address any key concerns that may prove to be problematic as negotiations progress.

Q: How should a business owner coordinate the vast range of information and considerations that apply when selling

a company?

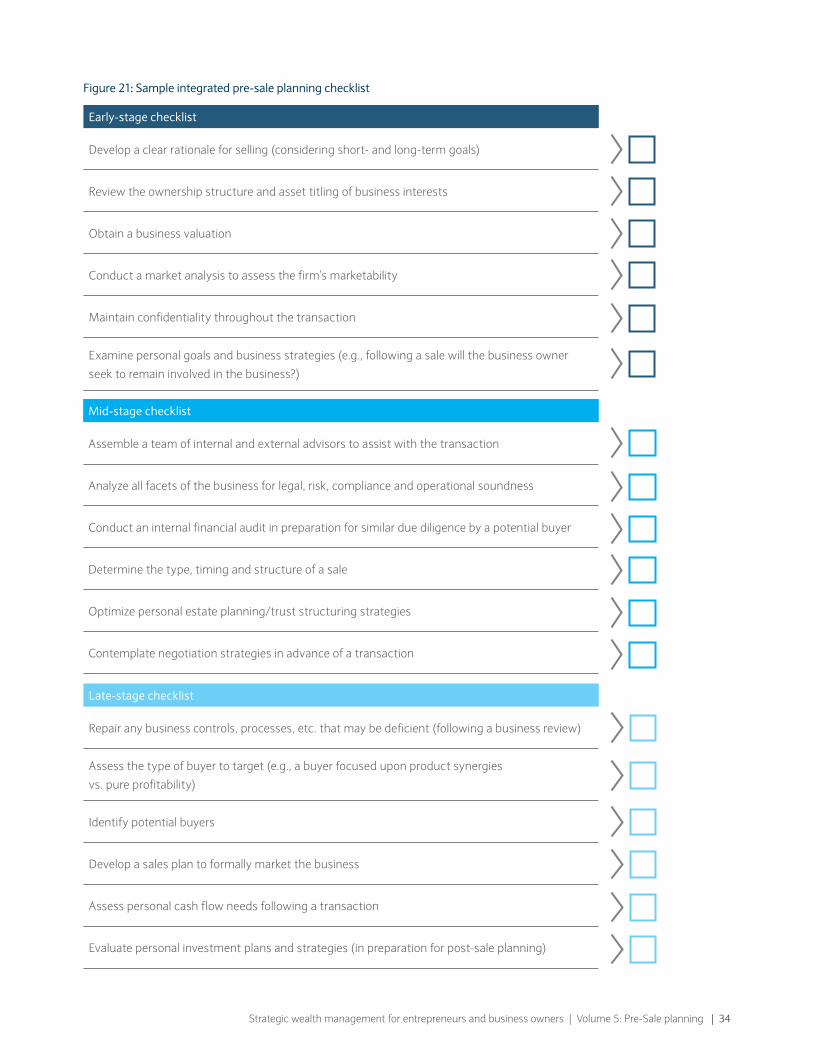

An integrated pre-sale planning checklist is a common solution to outlining the range of tasks

that need to be addressed in the months and weeks leading up to a sale. This document should be

prepared in conjunction with advisors and – if properly designed – can serve to effectively help

align an entrepreneur’s commercial and personal wealth-management planning.

A sample checklist appears in Figure 21.

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 34

Figure 21: Sample integrated pre-sale planning checklist

Early-stage checklist

Develop a clear rationale for selling (considering short- and long-term goals)

Review the ownership structure and asset titling of business interests

Obtain a business valuation

Conduct a market analysis to assess the firm’s marketability

Maintain confidentiality throughout the transaction

Examine personal goals and business strategies (e.g., following a sale will the business owner

seek to remain involved in the business?)

Mid-stage checklist

Assemble a team of internal and external advisors to assist with the transaction

Analyze all facets of the business for legal, risk, compliance and operational soundness

Conduct an internal financial audit in preparation for similar due diligence by a potential buyer

Determine the type, timing and structure of a sale

Optimize personal estate planning/trust structuring strategies

Contemplate negotiation strategies in advance of a transaction

Late-stage checklist

Repair any business controls, processes, etc. that may be deficient (following a business review)

Assess the type of buyer to target (e.g., a buyer focused upon product synergies

vs. pure profitability)

Identify potential buyers

Develop a sales plan to formally market the business

Assess personal cash flow needs following a transaction

Evaluate personal investment plans and strategies (in preparation for post-sale planning)

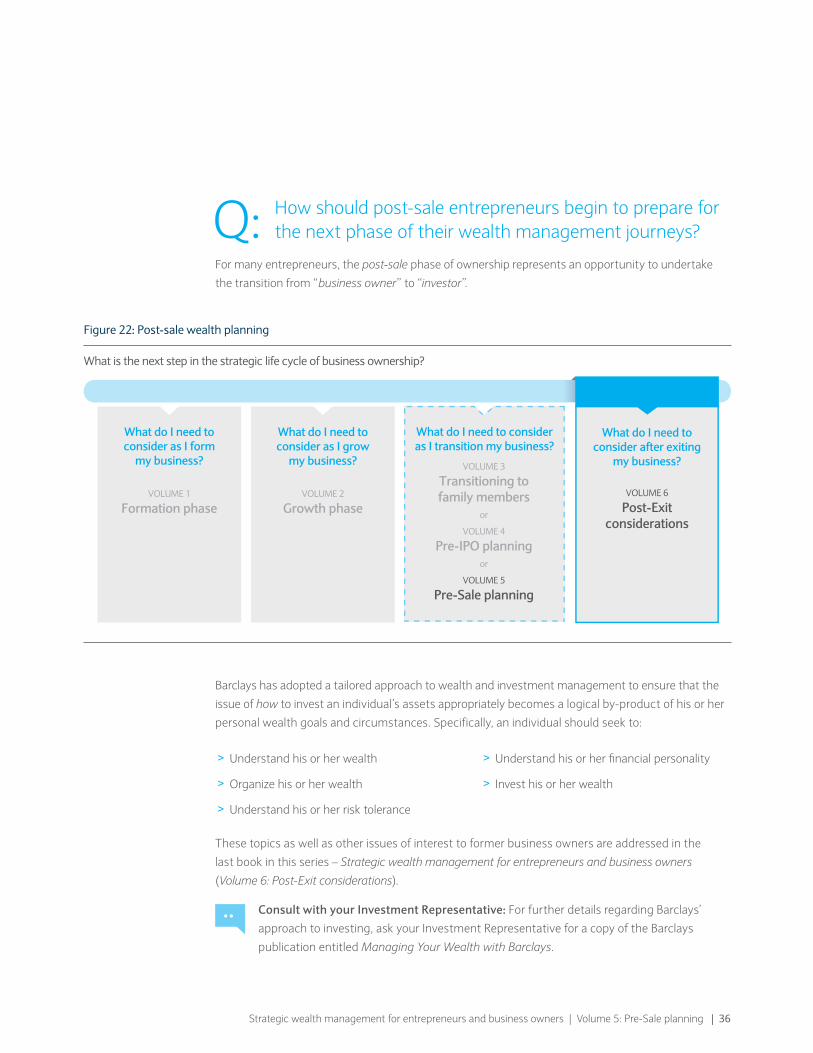

35

Step 4Consider “next steps”

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 36

Figure 22: Post-sale wealth planning

What do I need to consider as I form

my business?

VOLUME 1

Formation phase

What do I need to consider as I grow

my business?

VOLUME 2

Growth phase

What do I need to consider after exiting

my business?

VOLUME 6

Post-Exitconsiderations

What do I need to consider as I transition my business?

VOLUME 3

Transitioning to family members

or

VOLUME 4

Pre-IPO planningor

VOLUME 5

Pre-Sale planning

What is the next step in the strategic life cycle of business ownership?

Q: How should post-sale entrepreneurs begin to prepare for the next phase of their wealth management journeys?

For many entrepreneurs, the post-sale phase of ownership represents an opportunity to undertake

the transition from “business owner” to “investor”.

Barclays has adopted a tailored approach to wealth and investment management to ensure that the

issue of how to invest an individual’s assets appropriately becomes a logical by-product of his or her

personal wealth goals and circumstances. Specifically, an individual should seek to:

> Understand his or her wealth

> Organize his or her wealth

> Understand his or her risk tolerance

> Understand his or her financial personality

> Invest his or her wealth

These topics as well as other issues of interest to former business owners are addressed in the

last book in this series – Strategic wealth management for entrepreneurs and business owners

(Volume 6: Post-Exit considerations).

Consult with your Investment Representative: For further details regarding Barclays’

approach to investing, ask your Investment Representative for a copy of the Barclays

publication entitled Managing Your Wealth with Barclays.

37

“ Affairs are easier of entrance than of exit; and it is but common prudence to see our way out before we venture in.”

Aesop

Strategic wealth management for entrepreneurs and business owners | Volume 5: Pre-Sale planning | 38

Conclusion

Words or wisdomAesop once noted that, “Affairs are easier of entrance than of exit; and it is but common prudence to

see our way out before we venture in.”

For entrepreneurs contemplating the disposition of their businesses, the way out may appear,

at first blush, to be self-evident. As we have discovered, however, the implicit complexity of pre-sale

planning underscores the fact that there can be a vast difference between a way out and

the best way out.

It is for this reason that one should not endeavor to sell his or her business without a carefully

crafted plan.

Guidance and focusThis document seeks to provide entrepreneurs with the insight required to formulate a thoughtful

and integrated plan for selling their businesses.

At Barclays, we realize that selling a business is a uniquely demanding task. However, we also

appreciate the strategic opportunities that the undertaking provides. All that is required to

leverage such opportunities is dedication, preparation, and the partnership of professional advisors

who are capable of crafting solutions that are aligned to their clients’ particular goals, needs

and circumstances.

We look forward to working with you now and following the sale of your company.

Important considerations

Trust Structure:A trust is a useful tool for the purpose of estate and wealth planning; however, trusts may not be suitable for all business owners. Many trusts are irrevocable and cannot be retracted once they are put in place. There may also be a mortality risk associated with some trust planning. In such instances, the purpose of a trust may not be fulfilled if the grantor passes away prior to the trust’s termination date. Consult with your legal and tax advisors for more complete information.

Grantor Retained Annuity Trust (GRAT):If the stock that has been transferred to a GRAT does not appreciate over the term of the trust, then all assets in the trust will revert back to the grantor at the end of the GRAT term. A GRAT is an irrevocable trust which will terminate only by the end of the stipulated term or in the event of the death of the grantor (where any trust assets will revert back into the grantor’s estate). Keep in mind that although a GRAT can be used to minimize the impact of gift and estate taxes for the purpose of effective business succession planning, it may not be suitable for all business owners. The applicability of a GRAT could be curtailed if legislation changes in the future. Consult with your legal and tax advisors for more complete information.

Intentionally Defective Grantor Trust (IDGT):Although an IDGT seeks to minimize gift and estate tax consequences, it may not be a suitable structure for all business owners. There are limitations, considerations and inherent risks in utilizing an IDGT. An IDGT is an irrevocable trust and there is no guarantee for asset appreciation within the structure. When setting up an IDGT, it is important for a business owner to note that a portion of his or her annual gift tax exemption may be used up by establishing the trust. The applicability of an IDGT could be curtailed if legislation changes in the future. Consult with your legal and tax advisors for more complete information.

Important DisclosuresDiversification does not guarantee a profit or protect against a loss.

Investing in securities involves a certain amount of risk. You are urged to review all prospectuses and other offering information prior to investing. Past performance is not a guarantee of future performance.

This material is provided by Barclays for information purposes only, and does not constitute tax advice.

Neither Barclays in the US nor its Wealth and Investment Management employees in the US render tax or legal advice. Please consult with your accountant, tax advisor, and/or attorney for advice concerning your particular circumstances.

Not all products described in these materials are offered by Barclays and not all products are suitable for all clients.

Barclays does not guarantee favorable investment outcomes. Nor does it provide any guarantee against investment losses.

“Barclays” refers to any company in the Barclays PLC group of companies.

Barclays offers wealth management products and services to its clients through Barclays Bank PLC (“BBPLC”) and functions in the United States through Barclays Capital Inc. (“BCI”), an affiliate of BBPLC. BCI is a registered broker dealer and investment adviser, regulated by the U.S. Securities and Exchange Commission, with offices at 745 Seventh Avenue, New York, New York 10019. Member FINRA and SIPC.

The wealth management products offered by Barclays in the United States clear through, and where applicable, assets are custodied by, Pershing LLC, a subsidiary of the Bank of New York Mellon Corporation. Pershing LLC is a member of FINRA, NYSE and SIPC.

Barclays Bank PLC is registered in England and authorized by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Registered No. 1026167. Registered Office: 1 Churchill Place, London E14 5HP.

©Copyright 2015 Barclays.

CSNY489396 v14 | July 2015

Retirement Account General DisclosureThis report is intended to provide only investment education and information and is not intended to constitute “investment advice” or an investment recommendation within the meaning of the Employee Retirement Income Security Act of 1974 (“ERISA”) or Section 4975 of the Internal Revenue Code of 1986 (the “Code”). Any investment products or managers specified in this report are for illustrative purposes only and other products or managers may be available or appropriate to fulfill the particular asset class. You are solely responsible for evaluating and acting upon the education and information contained in this report, and you will not rely on this report, the information contained herein, or Barclays as a primary basis for your investment decisions. Moreover; any discussion, analyses, or information furnished by Barclays regarding its advisory services, including sample asset allocations or discussions of potential investment options or alternatives, should not be considered investment advice or part of any advisory service offered by Barclays. Such discussion, analyses and information is provided for educational purposes only and for the purpose of allowing you to understand and evaluate Barclays’ various advisory services and available investment alternatives. Accordingly, you acknowledge and agree that: (i) any and all discussions, analyses, and information furnished by Barclays in connection with your retention of Barclays or investment in an investment alternative was not intended to and shall not serve as a primary basis for your decision with respect to any investment determination; (ii) Barclays is not providing investment advice or otherwise acting as a fiduciary under the Investment Advisers Act of 1940, ERISA, or Section 4975 of the Code in connection with such discussions, analyses, or information; and (iii) any and all asset allocation and investment option decisions, both initial and ongoing, are made independently by you and without reliance upon any advice or recommendations of Barclays.

![How Entrepreneurs Create Wealth in Transition Economies [and Executive Commentary]mikepeng/documents/Peng01AME.pdf · · 2017-03-27How Entrepreneurs Create Wealth in Transition](https://img.pdfslide.us/doc/110x75/5a9fd1007f8b9a6c178d3b03/how-entrepreneurs-create-wealth-in-transition-economies-and-executive-commentary.jpg)