Embed Size (px)

Citation preview

STRATEGIC

UPDATEDelivering

sustainable value

Neal Froneman

Chief Executive Officer

28 July 2016

Disclaimer

The information in this presentation may include forward-looking statements, which are based on current expectations and

projections about future events. These statements may include, without limitation, any statements preceded by, followed by or

including words such as “target,” “expect,” “may,” “anticipate,” “estimate,” “will,” and other words and terms of similar

meaning or the negative thereof. These forward-looking statements, as well as those included in any other material discussed

at the meeting, are subject to risks, uncertainties and assumptions, including, among other things, the development of

Sibanye’s business, general economic conditions and actions of regulators. In light of these risks, uncertainties and

assumptions, the events in the forward-looking statements may not occur. No representation or warranty is made that any

forward-looking statement will come to pass and no reliance should be placed on any forward-looking statement. No one

undertakes to publicly update or revise any such forward-looking statement.

2

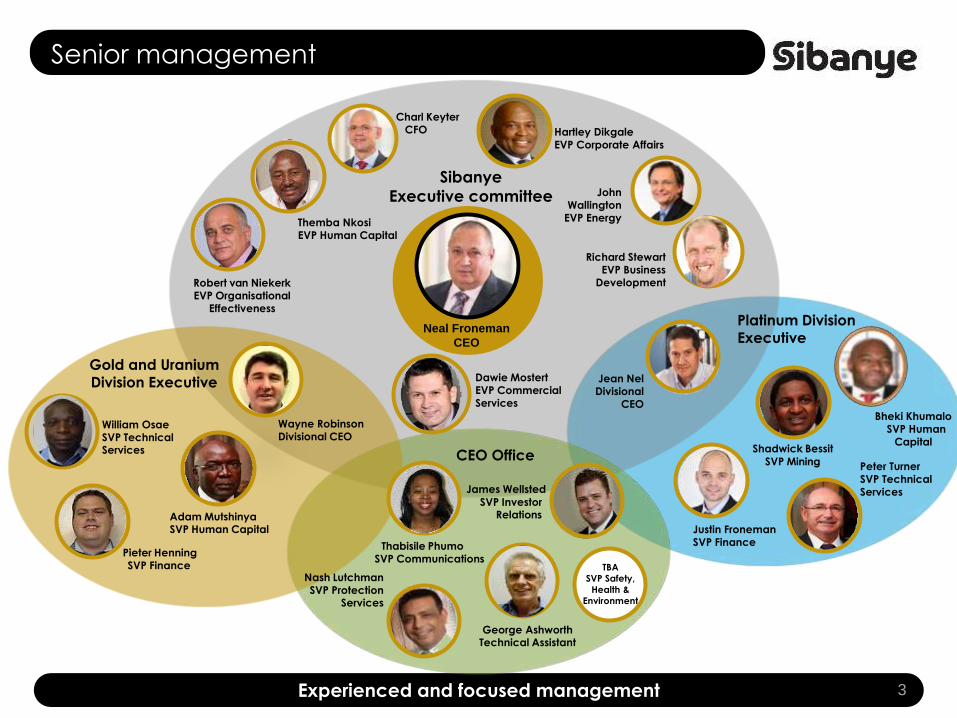

Senior management

3Experienced and focused management

Sibanye

Executive committee

Charl KeyterCFO

Dawie MostertEVP Commercial Services

Robert van NiekerkEVP Organisational

Effectiveness

Richard StewartEVP Business

Development

Hartley DikgaleEVP Corporate Affairs

Jean NelDivisional

CEO

Themba NkosiEVP Human Capital

John Wallington

EVP Energy

Wayne RobinsonDivisional CEO

Neal Froneman

CEO

Platinum Division Executive

Justin FronemanSVP Finance

Shadwick Bessit

SVP Mining Peter TurnerSVP Technical Services

Gold and Uranium

Division Executive

Pieter HenningSVP Finance

Adam MutshinyaSVP Human Capital

William OsaeSVP Technical Services

George AshworthTechnical Assistant

Thabisile PhumoSVP Communications

CEO Office

TBA

SVP Safety,

Health &

Environment

James Wellsted

SVP Investor Relations

Nash LutchmanSVP Protection

Services

Bheki KhumaloSVP Human

Capital

Our vision

SUPERIOR VALUE CREATION

FOR ALL OUR STAKEHOLDERS

Through mining our mult i -commodity

resources predominantly in

South Afr ica

4Underpinned by clear values

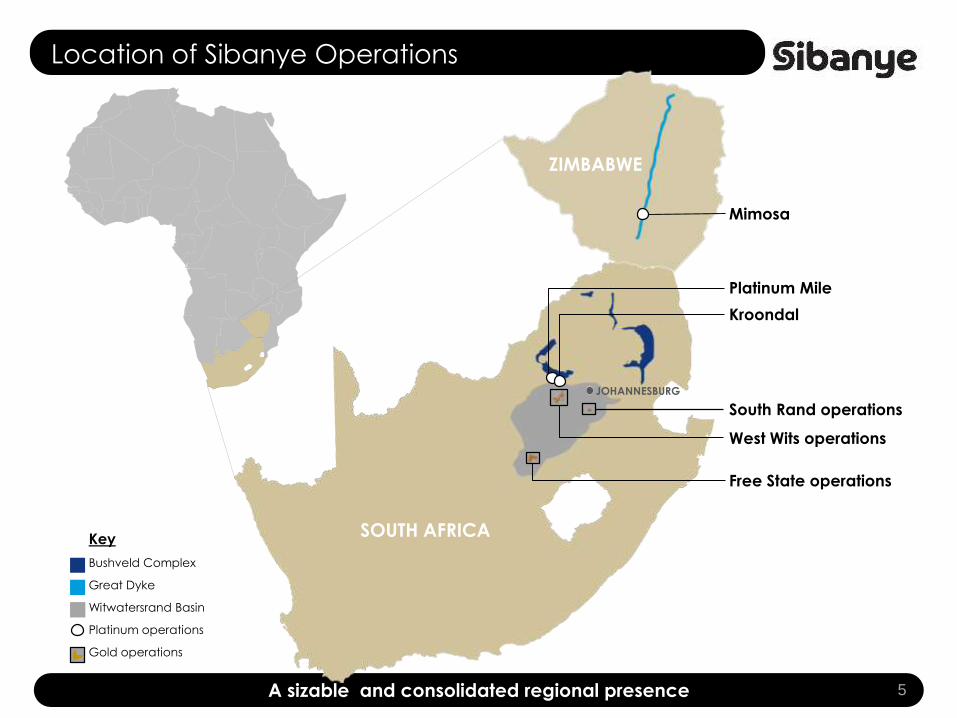

Location of Sibanye Operations

5A sizable and consolidated regional presence

Mimosa

Platinum Mile

Kroondal

SOUTH AFRICA

ZIMBABWE

JOHANNESBURG

Free State operations

West Wits operations

South Rand operations

Key

Bushveld Complex

Great Dyke

Witwatersrand Basin

Platinum operations

Gold operations

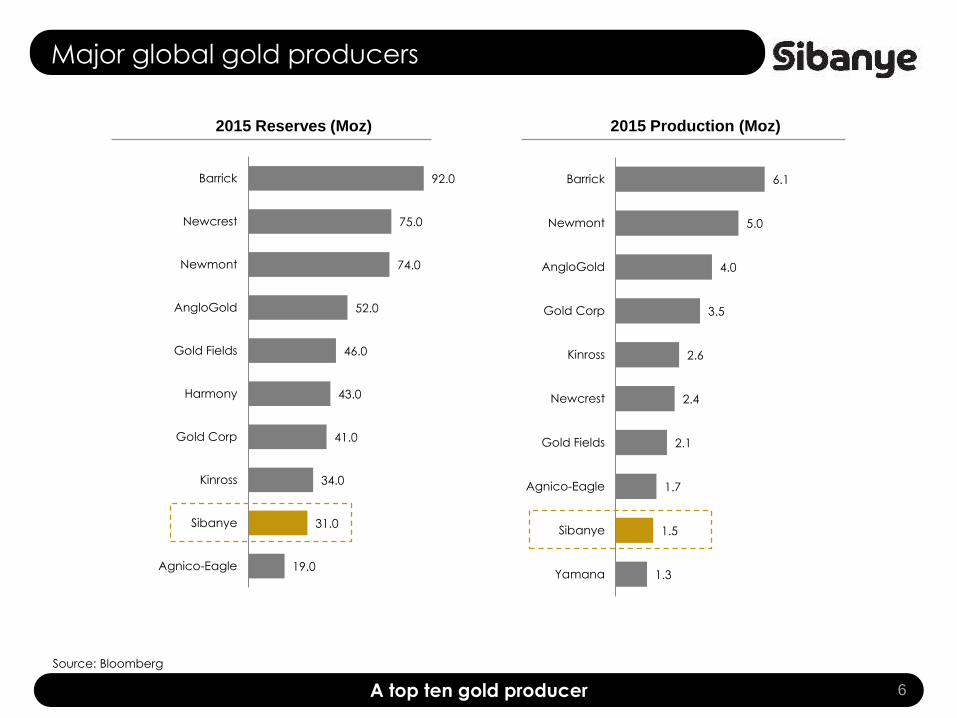

Major global gold producers

6A top ten gold producer

Source: Bloomberg

2015 Reserves (Moz) 2015 Production (Moz)

19.0

31.0

34.0

41.0

43.0

46.0

52.0

74.0

75.0

92.0

Agnico-Eagle

Sibanye

Kinross

Gold Corp

Harmony

Gold Fields

AngloGold

Newmont

Newcrest

Barrick

1.3

1.5

1.7

2.1

2.4

2.6

3.5

4.0

5.0

6.1

Yamana

Sibanye

Agnico-Eagle

Gold Fields

Newcrest

Kinross

Gold Corp

AngloGold

Newmont

Barrick

Global PGM producer rankings

7A leading PGM producer

0.3

0.4

1.1

1.2

2.2

3.3

3.6

RBPlats

Northam

Sibanye

Lonmin

Implats

Norilsk Nickel

AMPLATS- ex Rustenburg

Mines

10.8

19.2

34.4

36.6

46.3

125.5

155.8

RBPlats

Northam

Sibanye

Lonmin

Implats

Norilsk Nickel

AMPLATS- ex Rustenburg

Mines³

Implats

4E Reserves1,2 (Moz) 2015A 4E Production1,4 (Moz)

(of which 0.7Mozis platinum)

(Rustenburg

+ Aquarius5)

(Rustenburg

+ Aquarius)

Source: Companies’ disclosures, Broker reports

Notes:1. Platinum, palladium, rhodium and gold (together referred to as 3E+Au or 4E). Sibanye related data includes Rustenburg Operations and Aquarius2. Reserves and resources are latest reported by the companies and are on an attributable basis; resources include reserves3. Prior to conclusion of the latest PSA agreement with Aquarius4. Based on broker consensus5. Aquarius reserves and resources include 50% of the Kroondal PSA extension; Total Resources also include managed resources from projects and Blue Ridge

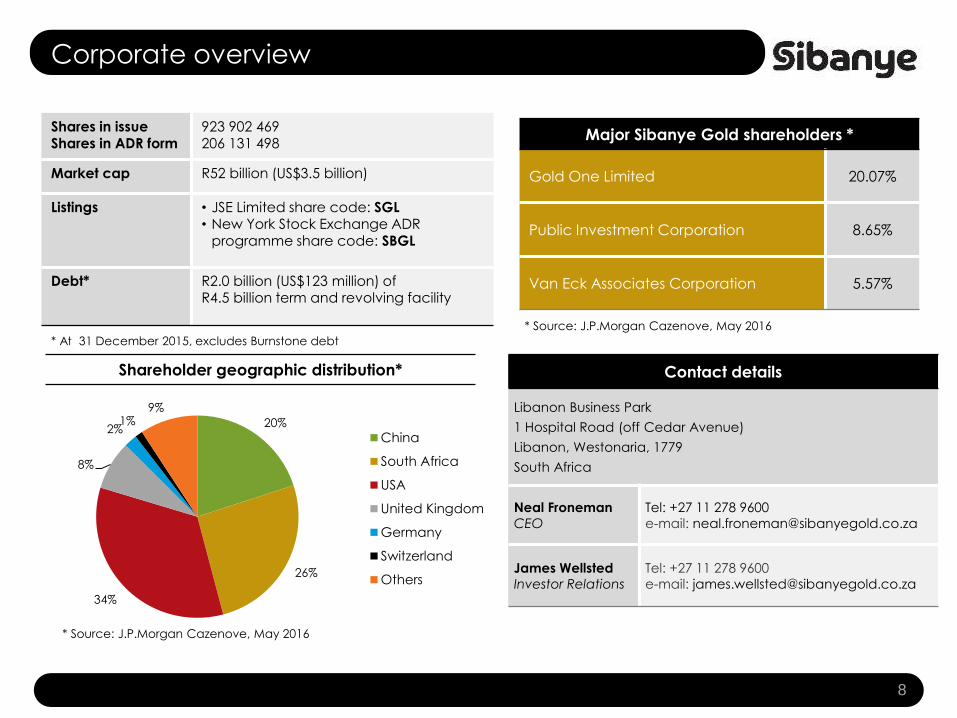

Corporate overview

8

Shares in issueShares in ADR form

923 902 469206 131 498

Market cap R52 billion (US$3.5 billion)

Listings • JSE Limited share code: SGL • New York Stock Exchange ADR

programme share code: SBGL

Debt* R2.0 billion (US$123 million) of R4.5 billion term and revolving facility

Major Sibanye Gold shareholders *

Gold One Limited 20.07%

Public Investment Corporation 8.65%

Van Eck Associates Corporation 5.57%

Contact details

Libanon Business Park

1 Hospital Road (off Cedar Avenue)

Libanon, Westonaria, 1779

South Africa

Neal Froneman

CEO

Tel: +27 11 278 9600

e-mail: [email protected]

James Wellsted

Investor Relations

Tel: +27 11 278 9600

e-mail: [email protected]

* Source: J.P.Morgan Cazenove, May 2016

* At 31 December 2015, excludes Burnstone debt

20%

26%

34%

8%

2%1%

9%

China

South Africa

USA

United Kingdom

Germany

Switzerland

Others

* Source: J.P.Morgan Cazenove, May 2016

Shareholder geographic distribution*

What differentiates Sibanye

• Significant free cash generation – underpins dividend commitment

• Delivery of superior, sustainable returns to stakeholders

• Primary South Africa focussed – strategic advantages

• A track record of environmentally responsible, sustainable, operational delivery

• Recognise importance of all stakeholders in delivery of sustainable success

9Uniquely positioned in industry

Leading the way to a modern mining industry

“A modern mining industry will optimally extract and beneficiate the country’s

natural resources, causing no harm to people or the planet. It benefits both the

local community as well as the national economy. It procures locally, it is a

preferred employer of well skilled people and creates appropriate risk-adjusted

returns for investors. Regulations, taxation and incentives are consistent,

transparent and recognise mining as a long- term driver of economic growth.”

Source: Joburg Indaba” October 2015

10The recipe for realising our vision

A track record

of delivery

What we inherited on unbundling

• A strong safety culture with a good safety record

• Large, high-grade resources but relatively small reserves

• Well-maintained assets

• A declining production profile

• Unacceptably high costs

• Sub-optimal operational effectiveness:

– inefficient organisational structures

– a service function too large for sustainable operational requirements

• Opportunity to extend the operating life and enhance cash flow by:

– reducing costs

– increasing operational efficiency and productivity

12The 'Good, the Bad and the Ugly'

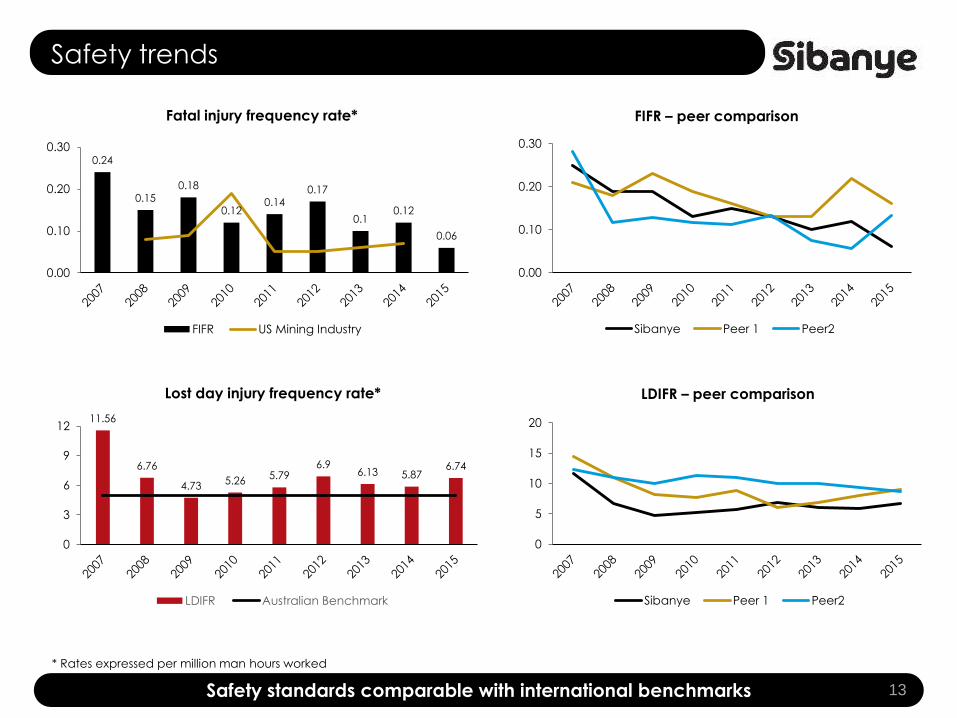

Safety trends

13Safety standards comparable with international benchmarks

0.24

0.150.18

0.120.14

0.17

0.10.12

0.06

0.00

0.10

0.20

0.30

Fatal injury frequency rate*

FIFR US Mining Industry

0.00

0.10

0.20

0.30

FIFR – peer comparison

Sibanye Peer 1 Peer2

11.56

6.76

4.735.26

5.796.9

6.13 5.876.74

0

3

6

9

12

Lost day injury frequency rate*

LDIFR Australian Benchmark

* Rates expressed per million man hours worked

0

5

10

15

20

LDIFR – peer comparison

Sibanye Peer 1 Peer2

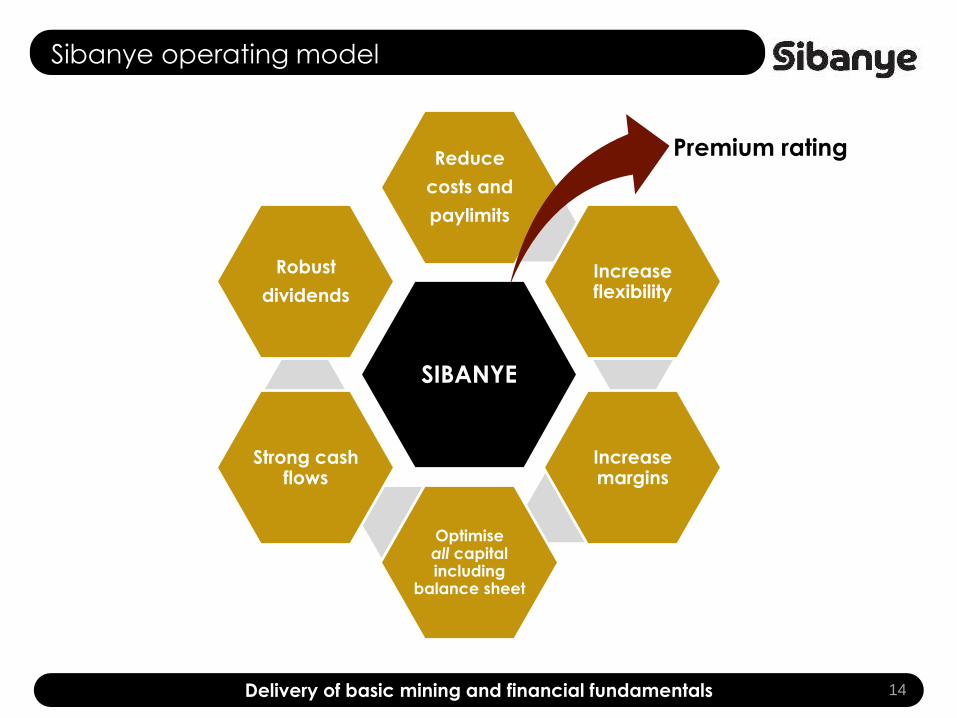

Sibanye operating model

14Delivery of basic mining and financial fundamentals

SIBANYE

Reduce

costs and

paylimits

Increase flexibility

Increase margins

Optimise all capital including

balance sheet

Strong cash flows

Robust

dividends

Premium rating

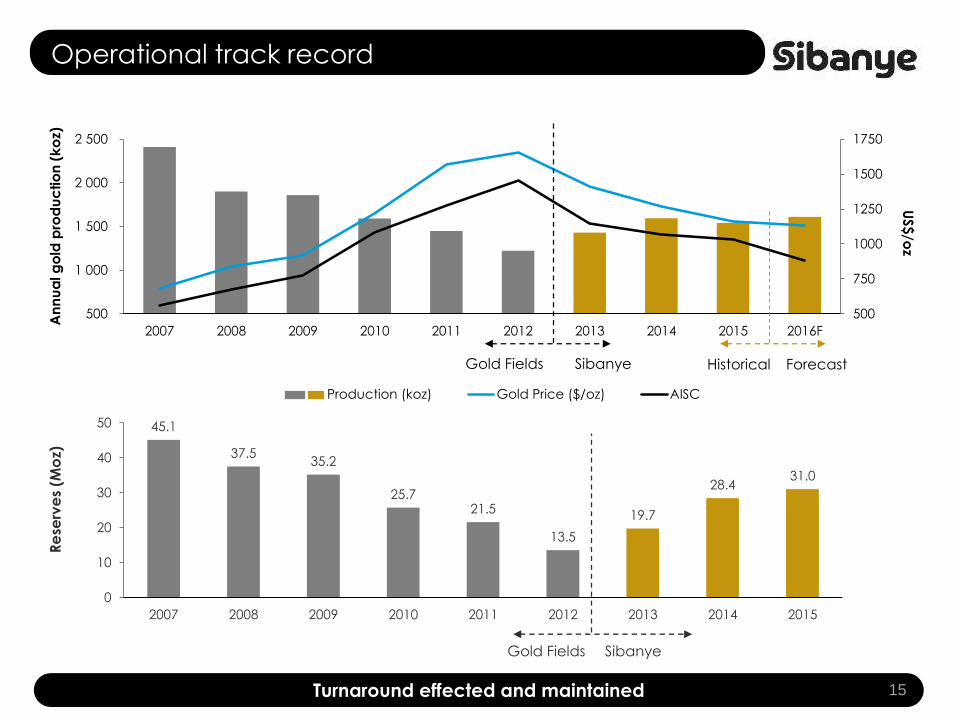

45.1

37.535.2

25.721.5

13.5

19.7

28.431.0

0

10

20

30

40

50

2007 2008 2009 2010 2011 2012 2013 2014 2015

Gold Fields Sibanye

Re

serv

es

(Mo

z)Operational track record

15Turnaround effected and maintained

500

750

1000

1250

1500

1750

500

1 000

1 500

2 000

2 500

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016F

Production (koz) Gold Price ($/oz) AISC

An

nu

al g

old

pro

du

ctio

n (

ko

z)U

S$/o

z

Historical ForecastGold Fields Sibanye

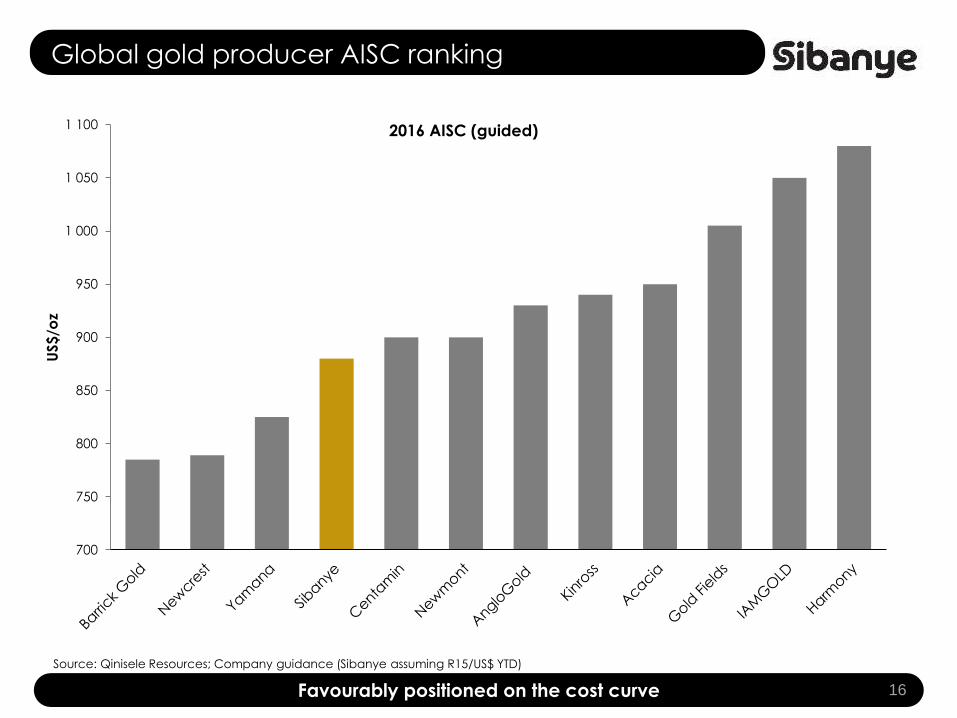

Global gold producer AISC ranking

16Favourably positioned on the cost curve

700

750

800

850

900

950

1 000

1 050

1 100

US$

/oz

2016 AISC (guided)

Source: Qinisele Resources; Company guidance (Sibanye assuming R15/US$ YTD)

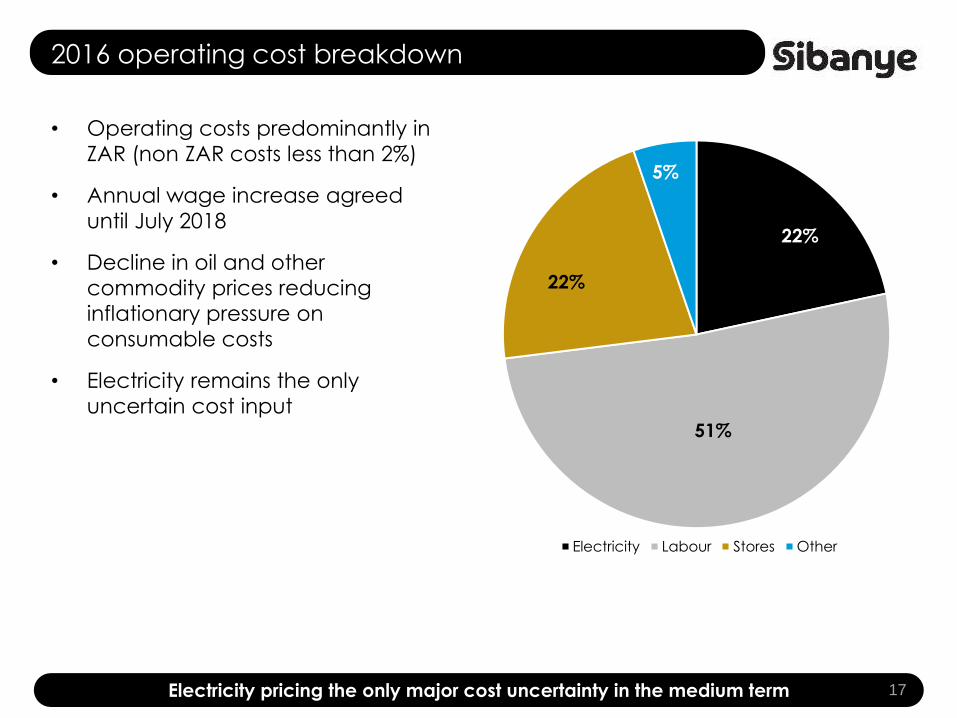

2016 operating cost breakdown

• Operating costs predominantly in

ZAR (non ZAR costs less than 2%)

• Annual wage increase agreed

until July 2018

• Decline in oil and other

commodity prices reducing

inflationary pressure on

consumable costs

• Electricity remains the only

uncertain cost input

17Electricity pricing the only major cost uncertainty in the medium term

22%

51%

22%

5%

Electricity Labour Stores Other

Divisional structure

18Structured to support and deliver on strategy

Gold and Uranium Division Platinum Division Energy Division

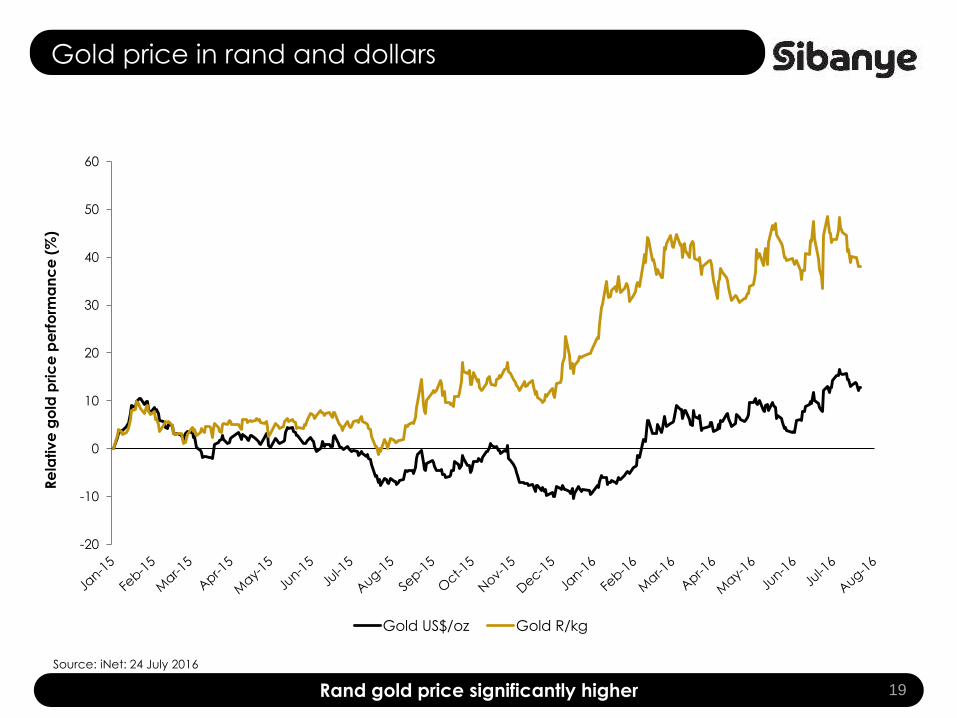

Gold price in rand and dollars

19Rand gold price significantly higher

Source: iNet: 24 July 2016

-20

-10

0

10

20

30

40

50

60

Re

lativ

e g

old

pric

e p

erf

orm

an

ce

(%

)

Gold US$/oz Gold R/kg

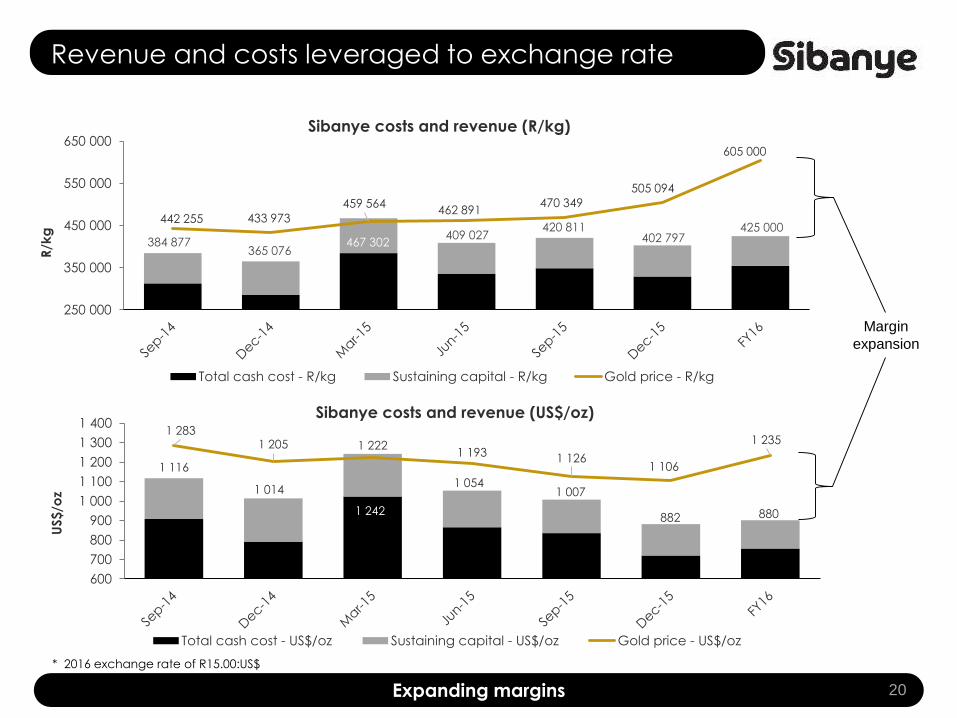

1 2831 205 1 222

1 193 1 1261 106

1 235

600

700

800

900

1 000

1 100

1 200

1 300

1 400

US$/o

z

Sibanye costs and revenue (US$/oz)

Total cash cost - US$/oz Sustaining capital - US$/oz Gold price - US$/oz

1 116

1 014

1 242

1 0541 007

882 880

Revenue and costs leveraged to exchange rate

20Expanding margins

* 2016 exchange rate of R15.00:US$

442 255 433 973

459 564462 891

470 349

505 094

605 000

250 000

350 000

450 000

550 000

650 000

R/k

g

Sibanye costs and revenue (R/kg)

Total cash cost - R/kg Sustaining capital - R/kg Gold price - R/kg

384 877365 076

467 302409 027

420 811402 797

425 000

Margin

expansion

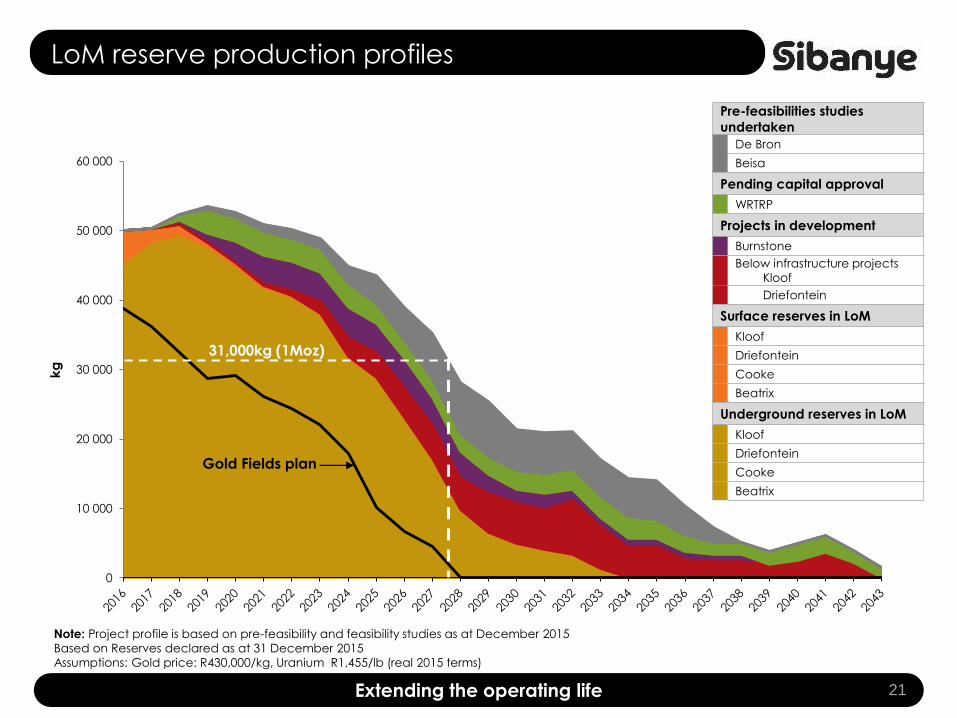

LoM reserve production profiles

21Extending the operating life

0

10 000

20 000

30 000

40 000

50 000

60 000

kg

Pre-feasibilities studies

undertaken

De Bron

Beisa

Pending capital approval

WRTRP

Projects in development

Burnstone

Below infrastructure projects

Kloof

Driefontein

Surface reserves in LoM

Kloof

Driefontein

Cooke

Beatrix

Underground reserves in LoM

Kloof

Driefontein

Cooke

Beatrix

Note: Project profile is based on pre-feasibility and feasibility studies as at December 2015

Based on Reserves declared as at 31 December 2015

Assumptions: Gold price: R430,000/kg, Uranium R1,455/lb (real 2015 terms)

Gold Fields plan

31,000kg (1Moz)

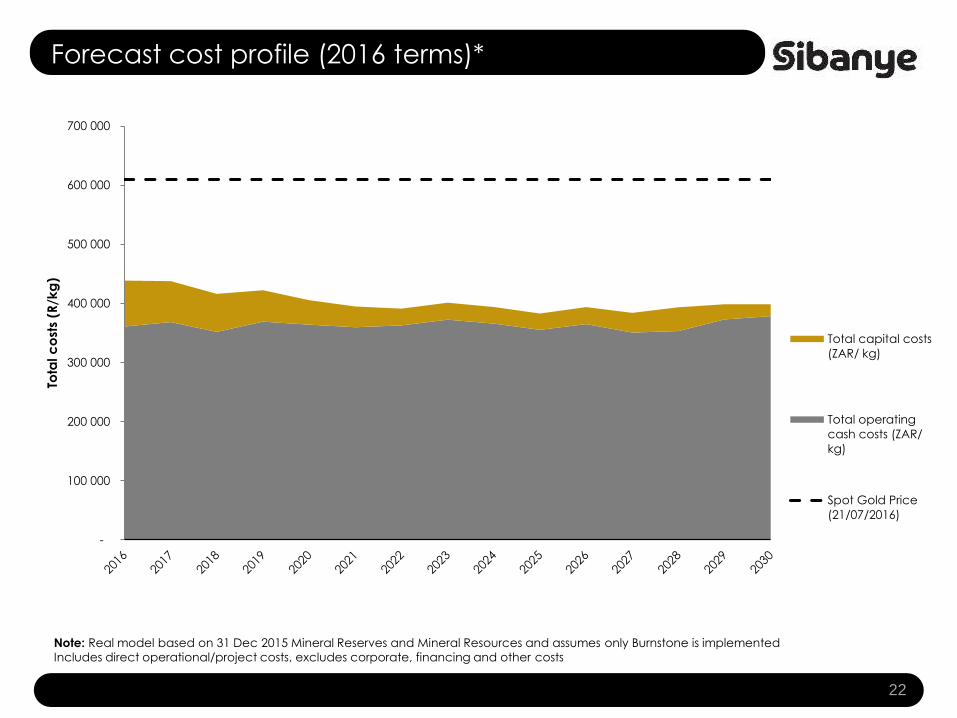

Forecast cost profile (2016 terms)*

22

-

100 000

200 000

300 000

400 000

500 000

600 000

700 000

Tota

l c

ost

s (R

/kg

)

Total capital costs

(ZAR/ kg)

Total operating

cash costs (ZAR/

kg)

Spot Gold Price

(21/07/2016)

Note: Real model based on 31 Dec 2015 Mineral Reserves and Mineral Resources and assumes only Burnstone is implemented

Includes direct operational/project costs, excludes corporate, financing and other costs

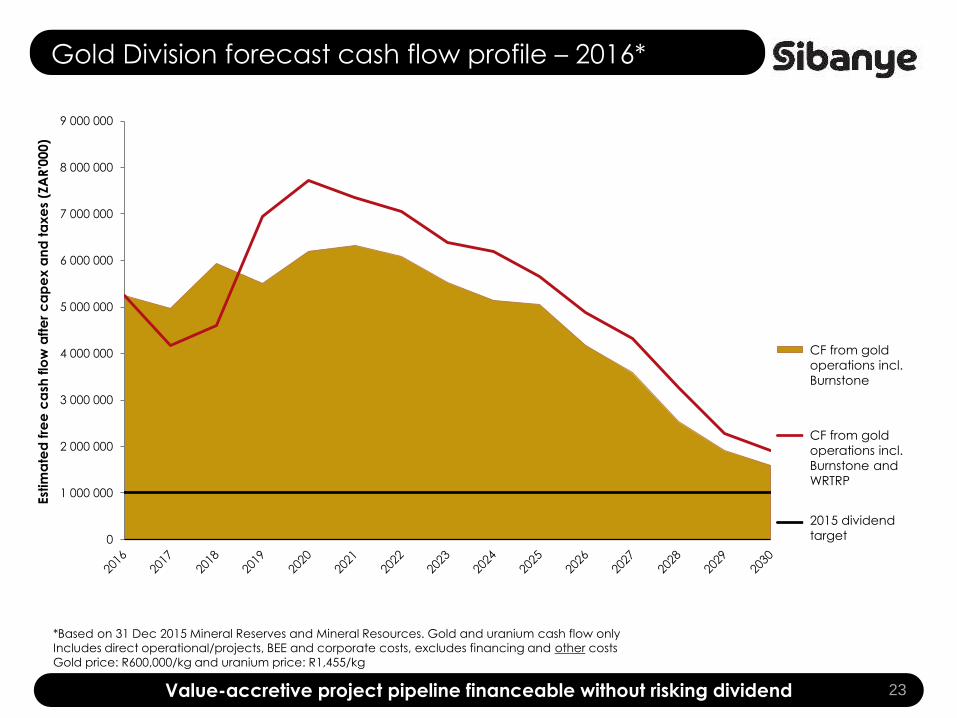

Gold Division forecast cash flow profile – 2016*

23Value-accretive project pipeline financeable without risking dividend

0

1 000 000

2 000 000

3 000 000

4 000 000

5 000 000

6 000 000

7 000 000

8 000 000

9 000 000

Est

ima

ted

fre

e c

ash

flo

w a

fte

r c

ap

ex a

nd

ta

xe

s (Z

AR

'000)

Operations including

Burnstone

Operations including

Burnstone and WRTRP

2015 Gross Dividend

*Based on 31 Dec 2015 Mineral Reserves and Mineral Resources. Gold and uranium cash flow only

Includes direct operational/projects, BEE and corporate costs, excludes financing and other costs

Gold price: R600,000/kg and uranium price: R1,455/kg

CF from gold

operations incl.

Burnstone

CF from gold

operations incl.

Burnstone and

WRTRP

2015 dividend

target

Delivering

value to all

stakeholders

Superior value for all stakeholders

• Shareholders: superior return on investment – dividends and capital appreciation

• Employees: good health and prosperity, sustainable employment

• Communities: service delivery, housing, infrastructure, jobs and peace

• Unions and associations: growing and satisfied membership

• Suppliers and customers: ability to transact on a transparent, sustainable and fair basis

• Government: transformation, economic growth, poverty alleviation and political control

• Management: satisfied stakeholders and strategic success

25Building a track record of delivery for all stakeholders

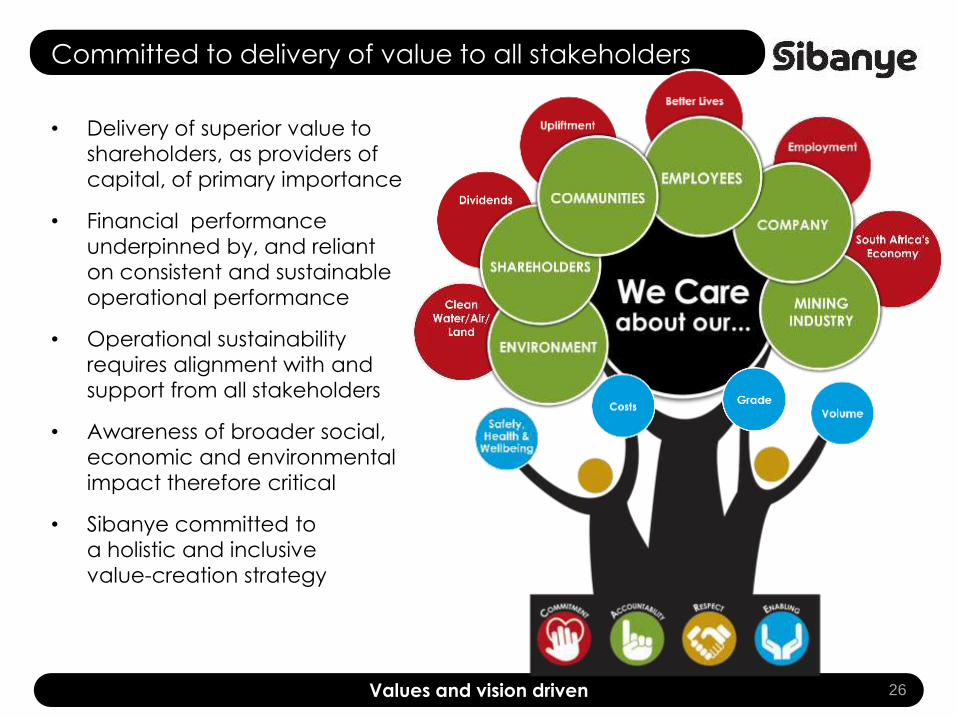

Committed to delivery of value to all stakeholders

• Delivery of superior value to

shareholders, as providers of

capital, of primary importance

• Financial performance

underpinned by, and reliant

on consistent and sustainable

operational performance

• Operational sustainability

requires alignment with and

support from all stakeholders

• Awareness of broader social,

economic and environmental

impact therefore critical

• Sibanye committed to

a holistic and inclusive

value-creation strategy

26Values and vision driven

Environmental value delivery

• WRTRP: reprocessing of West Wits surface tailings facilities

• Sibanye AMANZI: proactive and innovative water

management strategy

• Photovoltaic project: environmentally friendly, renewable

energy generation

• Gas flaring for power at Beatrix and powered underground locos

and bus fleet

27

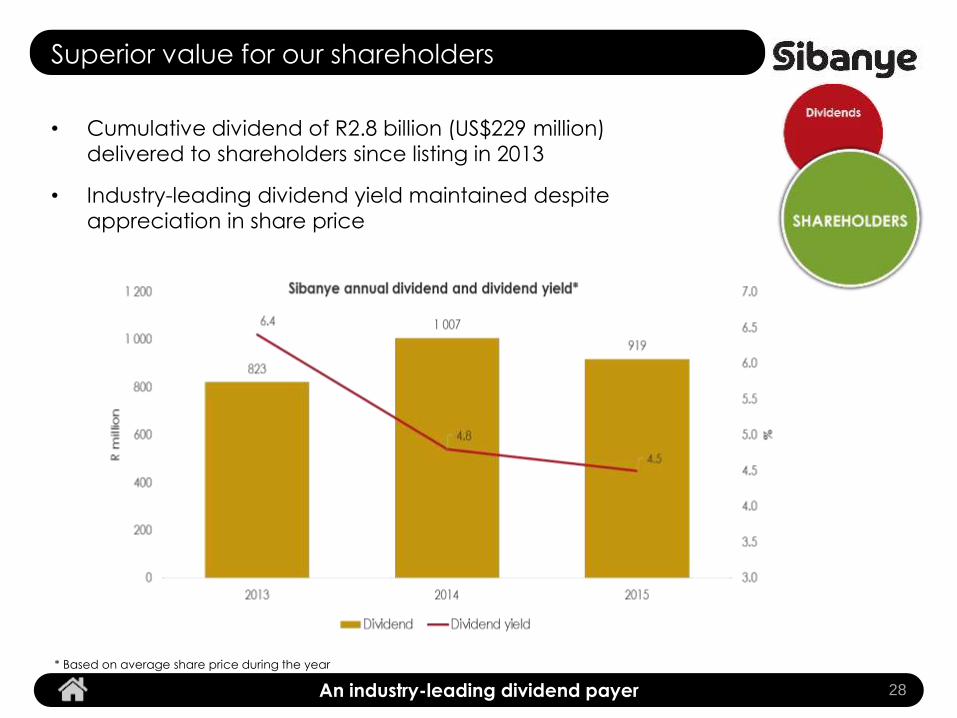

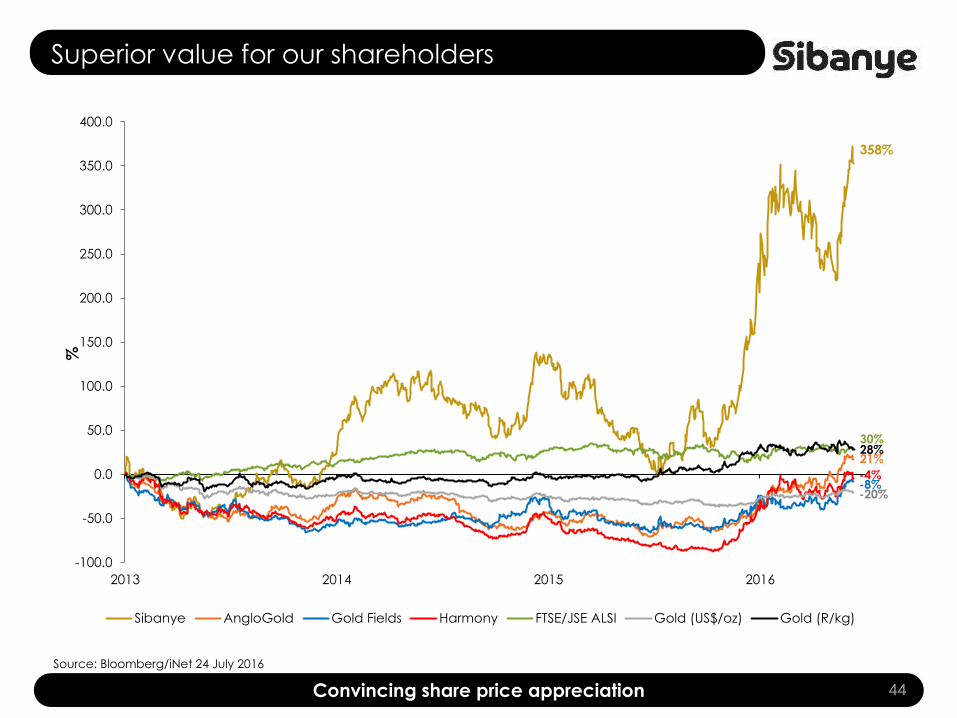

Superior value for our shareholders

• Cumulative dividend of R2.8 billion (US$229 million)

delivered to shareholders since listing in 2013

• Industry-leading dividend yield maintained despite

appreciation in share price

28An industry-leading dividend payer

* Based on average share price during the year

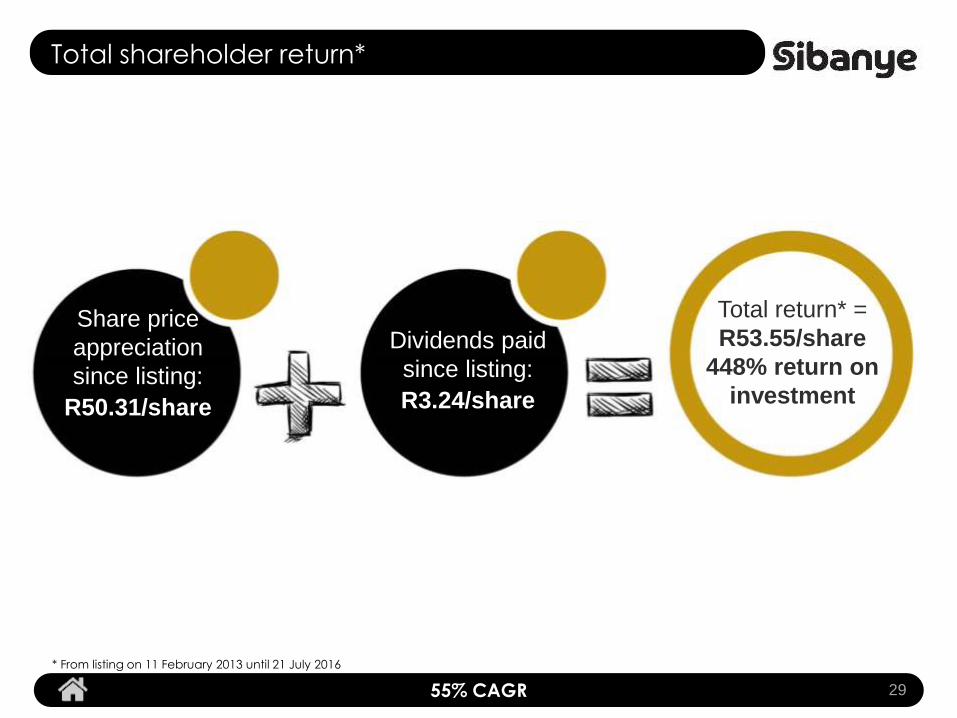

Total shareholder return*

2955% CAGR

* From listing on 11 February 2013 until 21 July 2016

Share price

appreciation

since listing:

R50.31/share

Dividends paid

since listing:

R3.24/share

Total return* =

R53.55/share

448% return on

investment

Delivering value to communities

• Public Private Partnerships to facilitate high impact regional

projects in local and labour sending areas

• Job creation and skills development key drivers

– >640 jobs created

– >20 000 beneficiaries in bursaries, learnerships, AET and

portable skills

• Broad-based empowerment of local communities

– agricultural hub concept launched on the West Rand

30Ensuring community development in areas we operate

Delivering value for employees

• Care for iMali improving personal financial management

– benefitted over 22,000 employees and community members

– garnishee orders decreased by 49%

• Affordable home ownership benefited over 300 families since 2015

• Progress towards a Social and Economic Compact

– sharing of profits with employees and protecting

the company during economic downturns

31

Delivering value for the company

• Increased reserves and extended operating life

• A leading position on the global cost curve

• Sustainable employment opportunities enhanced

by local investment

• Strong cash flows with prudent debt supporting job sustainability

through capital investment in projects

32

Creating value in the mining industry

• Championing and driving the principles which define a modern

mining industry

• Creating a safer and more productive work environment through

the advancement of technology and R&D

• Active participation in critical stakeholder forums such as

the Phakisa process

• Driving change in the industry through active leadership

of industry bodies such as the Chamber of Mines

• Adopting a firm but fair approach to stakeholder engagement –

redefining the role of the mining industry

33

Value creation

strategy

Value creation strategy

• Continue to drive operational excellence on existing asset base

– a proven operating model

– robust cash flow

– strong balance sheet

• Create additional value by leveraging off its core competencies in other

appropriate commodities

• Mining companies globally are divesting assets in order to reduce debt

and leverage

• Opportunities to conclude favourably priced transactions at a low point

in the commodity price cycle

35Well-positioned to realise further value

Platinum a logical first step

• Many operational similarities with gold mining

• Long-term PGM supply and demand fundamentals remain robust

• Low PGM prices and escalating costs (labour, utilities) have put balance sheets

under strain

• Opportunity to leverage Sibanye’s successful operating model and hard rock,

tabular, labour intensive mining competency to realise further value

• Innovative approach to structuring transactions and projects

36

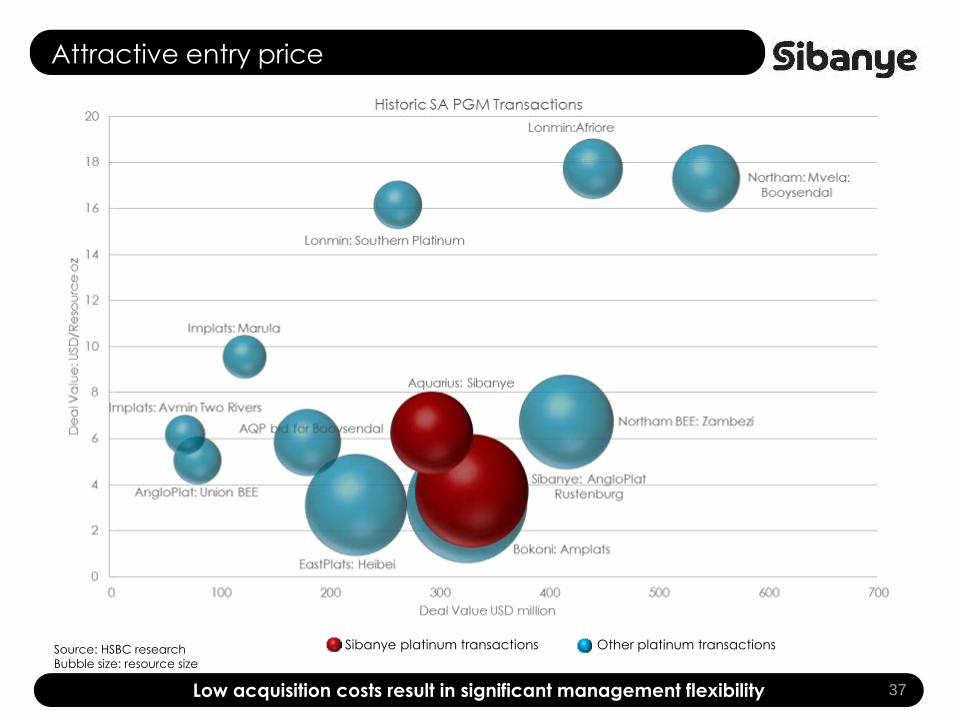

Attractive entry price

37Low acquisition costs result in significant management flexibility

Source: HSBC research

Bubble size: resource size

Sibanye platinum transactions Other platinum transactions

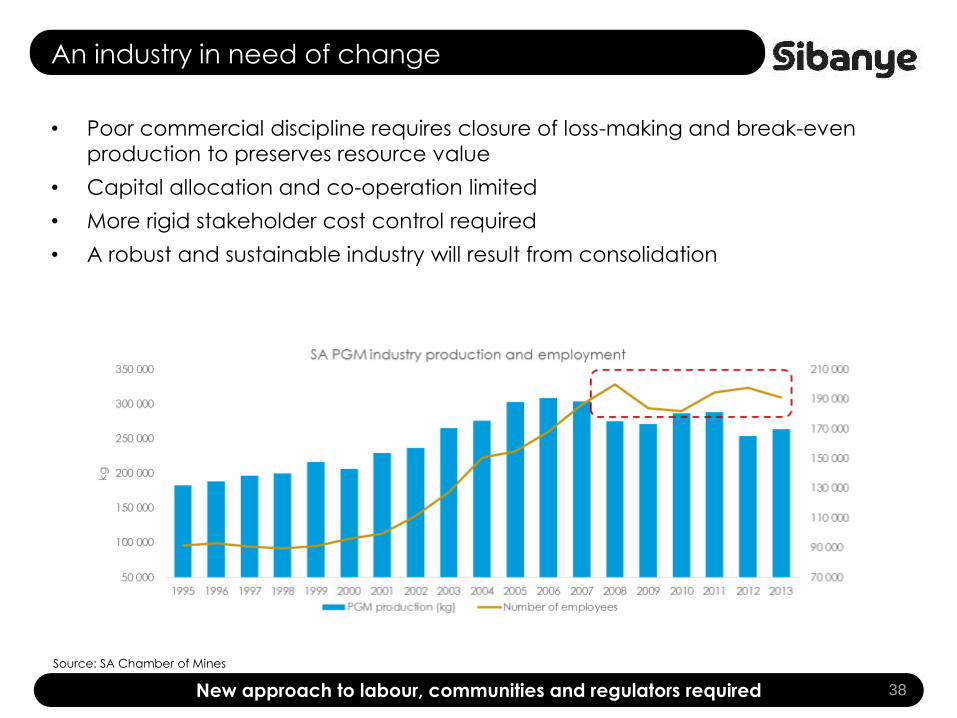

An industry in need of change

• Poor commercial discipline requires closure of loss-making and break-even

production to preserves resource value

• Capital allocation and co-operation limited

• More rigid stakeholder cost control required

• A robust and sustainable industry will result from consolidation

38New approach to labour, communities and regulators required

Source: SA Chamber of Mines

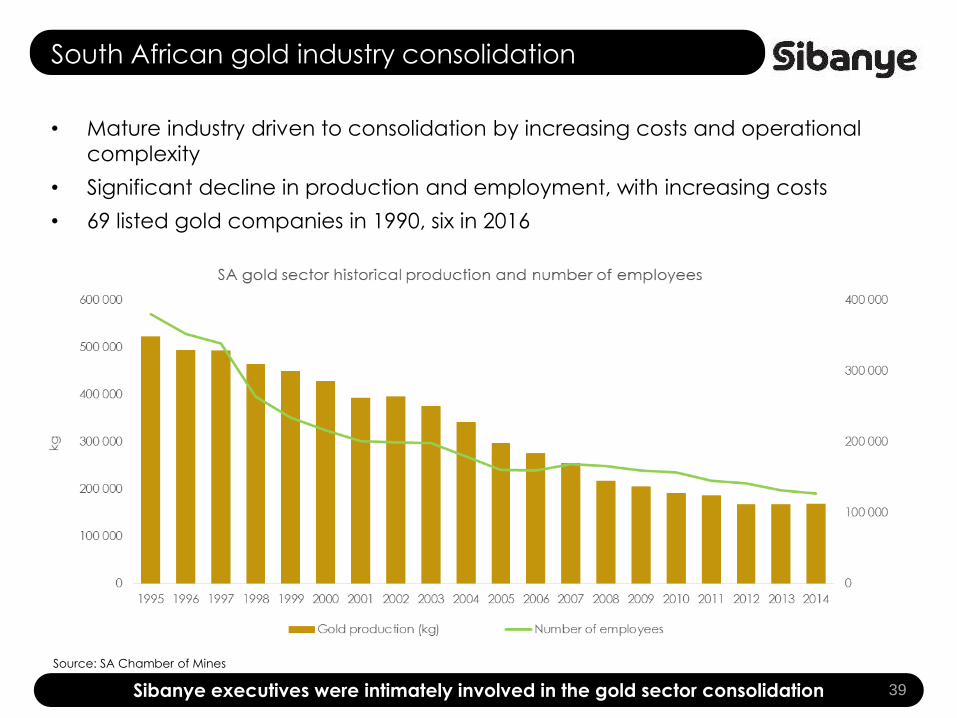

South African gold industry consolidation

• Mature industry driven to consolidation by increasing costs and operational

complexity

• Significant decline in production and employment, with increasing costs

• 69 listed gold companies in 1990, six in 2016

39Sibanye executives were intimately involved in the gold sector consolidation

Source: SA Chamber of Mines

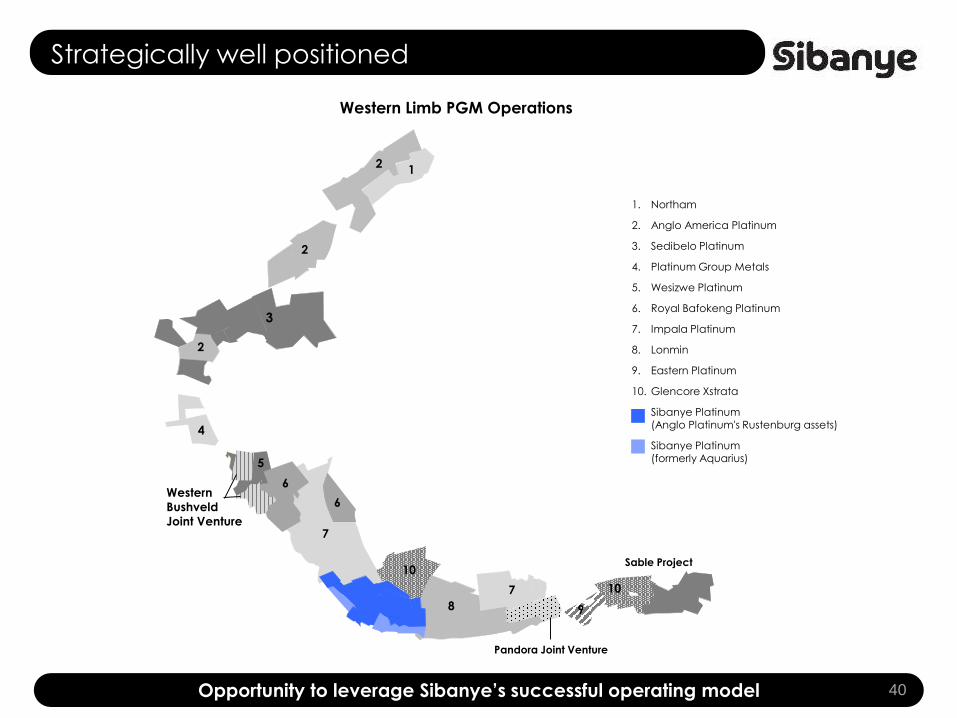

Strategically well positioned

40Opportunity to leverage Sibanye’s successful operating model

1. Northam

2. Anglo America Platinum

3. Sedibelo Platinum

4. Platinum Group Metals

5. Wesizwe Platinum

6. Royal Bafokeng Platinum

7. Impala Platinum

8. Lonmin

9. Eastern Platinum

10. Glencore Xstrata

Sibanye Platinum (Anglo Platinum's Rustenburg assets)

Sibanye Platinum (formerly Aquarius)

12

2

2

3

4

Sable Project

Western

Bushveld

Joint Venture

Pandora Joint Venture

7

7

6

6

5

10

8

10

9

Western Limb PGM Operations

Consolidation benefits

• Planning and ore body extraction optimised by breaking down farm

boundaries

• Improved capacity utilisation and rationalisation of infrastructure

• Remove duplicated/unnecessary overhead structures and costs

• Rationalise replicated support services

• Optimise capital allocation

• Flexibility to close loss making production

• Enhance financial capacity

– access to capital markets improved

– cost of capital reduced

41Consolidation is logical and necessary

0

2 000 000

4 000 000

6 000 000

8 000 000

10 000 000

Est

ima

ted

fre

e c

ash

flo

w a

fte

r c

ap

ex a

nd

ta

xe

s (Z

AR

'000)

Operations including

Burnstone

Operations including

Burnstone and WRTRP

2015 Gross Dividend

Operations including

Burnstone and WRTRP

and PGMs

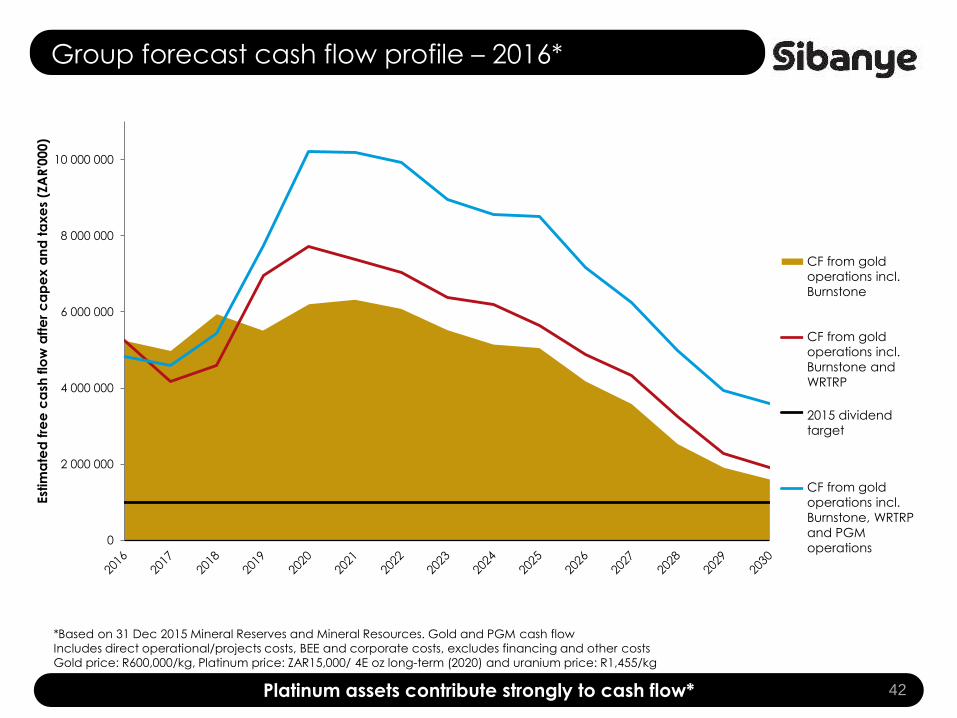

Group forecast cash flow profile – 2016*

42Platinum assets contribute strongly to cash flow*

*Based on 31 Dec 2015 Mineral Reserves and Mineral Resources. Gold and PGM cash flow

Includes direct operational/projects costs, BEE and corporate costs, excludes financing and other costs

Gold price: R600,000/kg, Platinum price: ZAR15,000/ 4E oz long-term (2020) and uranium price: R1,455/kg

CF from gold

operations incl.

Burnstone

CF from gold

operations incl.

Burnstone and

WRTRP

2015 dividend

target

CF from gold

operations incl.

Burnstone, WRTRP

and PGM

operations

Relative

valuation

43

-100.0

-50.0

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

2013 2014 2015 2016

%

Sibanye AngloGold Gold Fields Harmony FTSE/JSE ALSI Gold (US$/oz) Gold (R/kg)

Superior value for our shareholders

44Convincing share price appreciation

Source: Bloomberg/iNet 24 July 2016

358%

30%

-8%

21%

-20%

-4%

28%

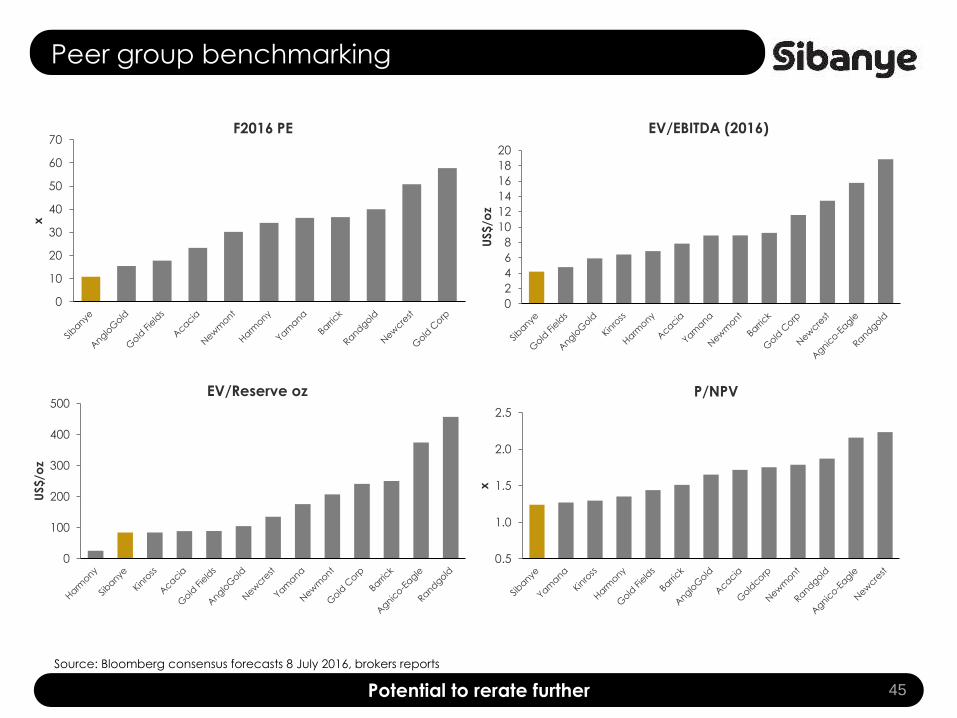

Peer group benchmarking

45Potential to rerate further

Source: Bloomberg consensus forecasts 8 July 2016, brokers reports

0

10

20

30

40

50

60

70

x

F2016 PE

0

2

4

6

8

10

12

14

16

18

20

US$

/oz

EV/EBITDA (2016)

0

100

200

300

400

500

US$/o

z

EV/Reserve oz

0.5

1.0

1.5

2.0

2.5

x

P/NPV

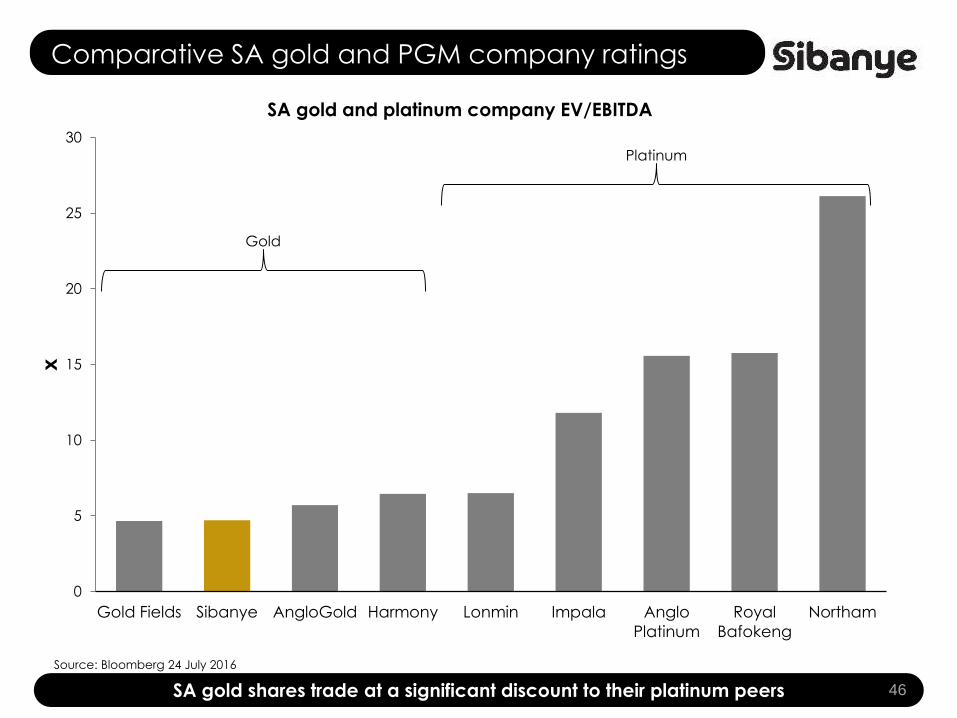

Comparative SA gold and PGM company ratings

46SA gold shares trade at a significant discount to their platinum peers

Source: Bloomberg 24 July 2016

0

5

10

15

20

25

30

Gold Fields Sibanye AngloGold Harmony Lonmin Impala Anglo

Platinum

Royal

Bafokeng

Northam

x

SA gold and platinum company EV/EBITDA

Gold

Platinum

Strategic

outlook and

conclusion

47

Strategic principles

• Dividend underpins investment case and will not be compromised

• Investment discipline regarding M&A and capital allocation to ensure

industry leading dividend sustainability

• Industry leading dividend underpins long-term returns to investors and will drive

rerating

• Sustainability only possible if value is created for all stakeholders

• Focus on sustainable value over longer term rather than reacting to short-term

exogenous issues

48A clear and focused strategy

Sibanye's key strategic thrusts 2016

• Enabling consistent, safe operational delivery

• Continuous business improvement

• Integration of platinum acquisitions

• Retain balance sheet strength and flexibility

• Respectful relationships with stakeholders and stakeholder communications

• Value-accretive growth to increase and sustain shareholder returns

• Focus on environmentally beneficial business practices

• Strategic and leadership role in repositioning the South African mining industry

49

Conclusion

• Sibanye is committed to creating superior value for ALL stakeholders

• Gold division is generating substantial cash flows

• Platinum acquisitions will realise significant value in the medium term

• Robust financial position and strong balance sheet at an opportune

point in the commodity cycle

• Industry-leading dividend yield investment thesis remains

the cornerstone building block

50A secure and prosperous future

Questions