Embed Size (px)

Citation preview

Strategic Innovation Management

Prof. Marc Gruber

January 27th, 2011

Financing & Controlling of Innovation- What can we learn from Venture Capital?

Financing/Controlling of innovative opportunities:Lessons from VCs

What can we learn from Venture Capital ?

Characteristics of Venture Capital:

• Equity (not debt); hence, shares risk of the entrepreneur

• Duration until exit: about 5-10 years (longer these days)

• Typically no (bank-type) securities

• No periodic payments of dividends/interest; instead, VC shares in the firm’s value increase

• Comes typically with (some) management support (“smart capital”)

Investment into innovative new firms („innovation projects“)

VCs assemble a portfolio of new firms

Management / Performance of Portfolios

VC

Background: Why Venture Capital?

• “Venture capital’s niche exists because of the structure and the rules of the capital

markets. Someone with an idea or a new technology often has no other institution to

turn to.” (p. 132)

• Due to usury laws, banks can not charge interest rates high enough to make up for

the high level of risk.

• Public capital markets are severely restricted: sales must be above some threshold,

and there must be a track record.

• Neither banks nor public capital markets can assess the prospects of a new venture,

particularly in a new industry.

• “Venture capital fills the void between sources of funds for innovation [...] and

traditional, lower-cost sources of capital available to ongoing concerns.” (p. 132)

Source: Zider, HBR 1998

Seedfinancing

develop-ment,

product concept

market analysis

Start-upfinancing

foundation,ramp-up of production

marketingconcept

First stagefinancing

start of

production

marketlaunch

own funds

businessangel

bank loans

Sta

ge

Cash Flow

Sou

rce

t

Depending on the stage of firm development, different financing sources dominate. Case of a high-growth venture

Source: B. Rudolph, 2001, p. 507

+

–

building / expandingdistributionchannels

Second stagefinancing

Third stagefinancing

Fourth stagefinancing

public support, venture capital

private equity bank loans,IPO

expanding production and distribution / sales

re-definition of corporate

governance

Early stage financing Expansion stage financing

Investors (pension funds, banks, insurance companies, university endowments, individuals, ...)

VC firms as mediators:

• Raise funds from investors willing to take calculated risks

• Find and select investment opportunities (right industry, team, idea)

• Build a portfolio (trade-offs: diversification, industry competence)

• Finance growth of the start-ups

• Provide advice, network, and management support

• Goal: Exit (trade sale, IPO) with high returns

Start-ups

VC firms act as mediators between investors and start-ups, collecting and investing funds into risky but promising new ventures.

Venture capital firms, example: Wellington’s portfolio

Source: www.wellington-partners.com

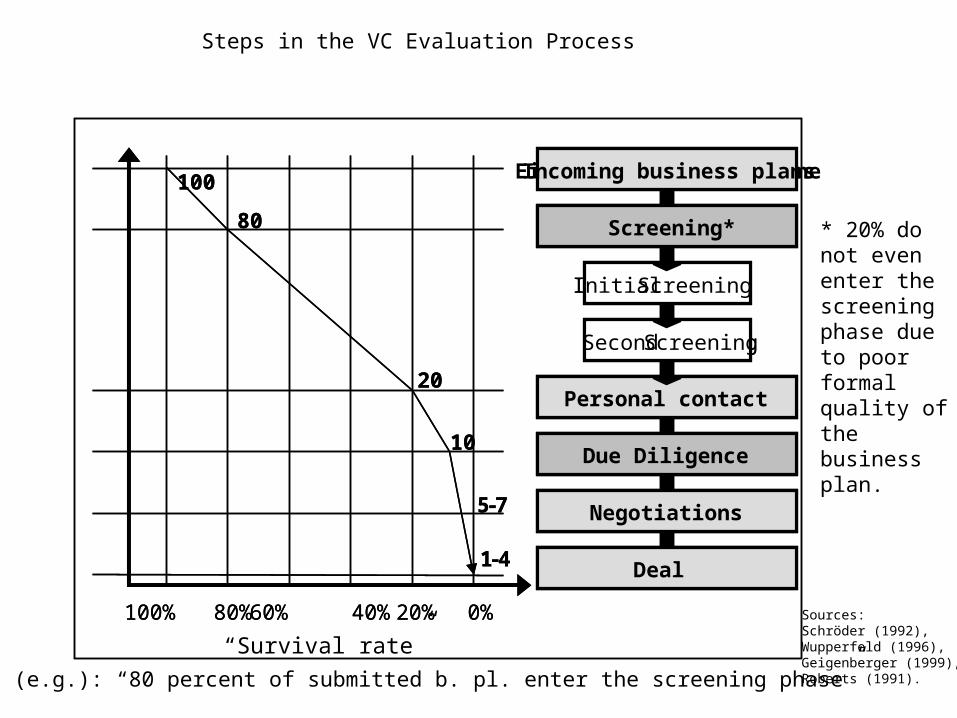

Steps in the VC Evaluation Process

Eingehende Businesspläne

Initial Screening

Second Screening

Screening

Due Diligence

Verhandlungen

Abschluß Beteiligung

Persönlicher Kontakt

Incoming business plans

Initial Screening

Second Screening

Screening

Due Diligence

Verhandlungen

Abschluß Beteiligung

Persönlicher Kontakt

Screening*

Due Diligence

Negotiations

Deal

Personal contact

100% 80% 60% 40% 20% 0%

100

80

20

10

5-7

1-4

“Survival rate”

100% 80% 60% 40% 20% 0%

100

80

20

10

5-7

1-4

Read (e.g.): “80 percent of submitted b. pl. enter the screening phase”

Sources: Schröder (1992), Wupperfeld (1996), Geigenberger (1999), Roberts (1991).

* 20% do not even enter the screening phase due to poor formal quality of the business plan.

Performance of a VC portfolio

Example: „10 in 5“

Example: Financing in 2005

Valuation 2009 100 Mio.Discount rate 60 %Financing 5 Mio.

Valuation 2005 100 Mio. = 15,3 Mio. 1,6 4

Equity Share of VC 5,0 = 32,7 % 15,3

Source: Extorel, Falk Strascheg

1st round of financing 11/96 2 Mio. DM 1 Mio. DM Technologieholding 1 Mio. DM BTU Programme (via tbg)

2nd round of financing 09/97 20 Mio. DM 1 Mio. DM Technologieholding 6 Mio. DM Vertex/TDF Singapur 13 Mio. DM Public Funds (BTU and Pre-IPO Programme via tbg)

Valuation 9,3 Mio. DM

Valuation 144 Mio. DM

3rd round of financing 09/98 80 Mio. DM 80 Mio. DM New Market

Valuation 514 Mio. DM

Example: BROKAT Infosystems AG

Source: Extorel, Falk Strascheg

So: Which Lessons can be drawn from the VC industry about thestrategic innovation management ?

Conclusions: VC and strategic innovation mgmt.

• Innovation is risky and differs from other functions of the firm

• Required competencies of firms differ by phase of the innovation process

• „Let a thousand flowers bloom“

• Ex ante vs. ex post

• Innovation manager – performance evaluation?

• Strategic Approach to Innovation Management: Portfolios of Real Options

Thank you!