Embed Size (px)

Citation preview

Strategic Focus on Small-Scale FinanceRedesigning Finance

September 7th, 2020

Agenda

2

Strategies of Shinsei Bank Group --------------- P 3

Small-Scale Finance: Strategic Focus ----------P 7

Progress of Small-scale Finance

Value Co-creation with Partners

Provision of Neo-bank Platform

Reference -----------------------------------------------P 15

Strategies of Shinsei Bank Group

Individual BusinessesInstitutional Business

Hybrid and seamless products and services portfolio

4

Private Equity

Leasing Unsecured Loans

Shopping Credit

Credit Cards

Payment Services

Housing Loans

Mutual Funds, Insurance

JPY/FCY Deposits, Structured Deposits

Products and Services for Corporate and

Financial Institutions

Real Estate Finance

Project Finance

Medium-term management plan (FY16-18): Focused on leveraging our core strengths

5

Source of our Strengths

Self-Contained ModelB to B to C

B to C

Quick, flexible business deployment

Value creation frominternal resources

Internalized products / services

Flexible response to

customer needs

Growth business areas operating assets balance grew at 10% CAGR

1,183.21,643.6

428.5

509.9

0

1,000

2,000

3,000

16.3 19.3

Unsecured Loans

Structured Finance

CAGR 10%

(Unit: JPY billion)

Value Co-Creation Model

Medium-term strategies (FY19-21):Value co-creation with partners leveraging our strengths

6

Source of our Strengths

Self-Contained Model

Deployproducts/services

know-how

Enhanceproducts/services

know-how

B to B to CB to C

Quick, flexible business deployment

Value creation frominternal resources

Internalized products / services

Flexible response to

customer needs

Greater value for our customers

Generation of synergies by integrating data, know-how with

external services

Finance as a Service

Deeper understanding of

our customers

B x B to C

Opportunities for Growth

Small-Scale Finance: Strategic Focus

Strategies of small-scale finance:Value co-creation with partners, leveraged by our strengths and capabilities

8

What is Small-Scale Finance?

Core CustomersIndividuals and small businesses

Product / Service LineupSmall-size, high-frequency credit and payment transactions:

• Unsecured loans, shopping credit• Credit guarantee, rent guarantee• Credit cards, prepaid cards• Other cashless payments

Our Capabilities

• Data science leveraging AI including data linkage between financial data and behavioral data owned by partners

• Know-how in loan collection, operations and IT capabilities which are not easily replicated

Value Co-Creation ModelInitiatives with partners

Self-Contained ModelInitiatives by Shinsei Bank Group

Streamline and speed-up existing processes• Unsecured loan business by Lake ALSA as an example

1

Strengthen core capabilities, integrate with payment platforms

2

Build / participate in ecosystems, share data to better understand our customers• Provide loan collection, operational capabilities and IT

systems as a functional part of the product based on partner needs

3

Self-contained model: Lake ALSA expands basic earnings power

9

Providing unsecured loans by using credit managementknow-how and digitalizationNew brand called ”Lake ALSA” was launched in April 2018

Digital strategies(UI・UX)

Operation to support the strategies

Increase in new customersAGrowth drivers

Maintain or improve

retention rateB Improve write-

off rateC

Launch of Lake ALSA1

Acquisition of new customers and retention of existing customers by

advanced digitalization2

Acquisition of new customers and retention of existing customers by advanced strategies of credit and collection

3

Improve loan

collection capability as identified by a task force

4

Gradual improvement of approval rate as per the task force Reengineering (restructuring) of the operating processes

Lake ALSA increased new customers through digitalization and credit management know-how

10

23.0 26.5 30.5 33.0 36.3 34.1 33.5 34.3

22.4

28.9% 29.5% 30.8% 30.1% 30.2% 29.8% 29.4% 30.6%33.2%

18.4-6 18.7-9 18.10-12 19.1-3 19.4-6 19.7-9 19.10-12 20.1-3 20.4-6

Approval Rate (%) The Number of New Customer Acquisition (K)

4.3%

3.3%

3%

4%

5%

18.4

18.5

18.6

18.7

18.8

18.9

18.1

18.1

118

.12

19.1

19.2

19.3

19.4

19.5

19.6

19.7

19.8

19.9

19.1

19.1

119

.12

20.1

20.2

20.3

20.4

20.5

20.6

Lake Portfolio Write-off (WO) Rate

Gross WO Rate

Net WO Rate

Lake ALSA New Customer Acquisition

27.073.2

38.777.5

376.1338.7

367.4322.2

403.1 411.9 406.1 399.7

19.3 20.3 19.6 20.6

Old Lake brand

Lake Loan Balance

Lake ALSA

2x

(Unit: JPY billion)

Recoveries of Written-off Claims

Lake ALSA loan balance continues to grow while total Lake loan balance decreased YoY in June 2020 reflecting COVID-19 impact

Lending functions for individuals

“Shinsei Bank Smart Money Lending” for Docomo Users

Credit scoring based on data owned by Docomo

Objectives

Features

Provide optimized financial services to Docomo users through access to a new

customer segment which is different from conventional money lender segment

For Docomo usersShinsei Bank Smart Money Lending

11

Data analytics in marketing, credit management including loan collection,

based on Lake’s know-how

Capabilities

Value co-creation business: Developing initiatives with partners (1)

Various financial services to micro and small enterprises (MSE)A joint financial business with USEN-NEXT HOLDINGS was established to provide financial services

Objectives

Credit services to foreign residents in JapanCredd Finance, Ltd. was established with Seven Bank, Ltd. to provide financial services

Features

• To access 750,000 customer base of USEN-NEXT GROUP

• Integration of USEN-NEXT GROUP’s comprehensive store support services and Shinsei’s initiatives to create value through collaboration with partners

• To provide financial services such as shopping credit, vendor leasing, business credit cards and lending to the MSE customers

• Commenced shopping credit and credit card services from August 2020

Objectives

Features

• To access foreign residents customer base of Seven Bank, Ltd.

• Jointly with Seven Bank, Ltd. provide new credit-related services such as loans and credit cards, to meet the funding needs of foreign residents in Japan

• Commenced credit card services from August 2020

Value co-creation business: Developing initiatives with partners (2)

12

Seamlessly provide the functions and strengths of Group companies to the partner companies and their customers

Objectives Capabilities

To collaborate with partner companies with customer bases by utilizing Shinsei‘s financial licensing and leveraging financial and payment systems capabilities

Neo-bank platform BANKIT® was launched

Features

To provide financial services platform with “cafeteria style” in accordance with the needs of partners

To reduce pain points for partner companies to enter the financial business

13

Image of cafeteria style reflecting partners’ needs on the platform

Value co-creation business: Developing initiatives with partners (3)

14

Value co-creation business: Utilizing functions and technologies in small-scale finance

Data

Group data strategies AI technology and analytics

Providing necessary financial functions to compliment partners’ products and services

Loan collection, operations, IT systems and marketing constitute indispensable functions to offer products and services. These capabilities are utilized in the value co-creation business

To process big data AI technology and data analytics are utilized

Data

Data

Data

Data

AI

AIAI

AI

AI

Pattern A

Providing a set of necessary financial functions and services with BANKIT@ platform, and

connecting with the partners via APIPattern B

Products and services

AI

Data

IT system

CollectionCredit

IT system

MarketingCredit

OperationCollection

Credit guarantee

Unsecured Loan

Neo-bank platformAPI API

API API

Loan Settlement Credit

Asset Management

Products

Reference

For Docomo usersShinsei Bank Smart Money Lending

Footsteps of value co-creation business

16

Value Co-creation with Partners

FY2016 FY2019 FY2020

Development of Small-Scale Finance

Commenced small-scale finance in Vietnam (m credit)

In 2016, small-sale finance business started through a JV with a major private commercial bank in Vietnam (i.e. Military Commercial Joint Stock Bank) Financial platform BANKIT® was launched

Mar. 2020: Started neo-bank platform BANKIT@ which enables to connect to smartphone apps and client’s system with API

Acquired UDC Finance, a leading company in non-bank industry in New Zealand Sep. 2020 : Completed share transfer and made it a 100%

owned subsidiary

Providing lending functions for individuals Aug. 2019:Commenced “Shinsei Bank Smart Money Lending” for Docomo Users

Providing various financial services to micro and small enterprises (MSE) Dec. 2019 : Announced a joint financial business with USEN-NEXT HOLDINGS Aug. 2020 : Launched shopping credit and credit card services to corporate customers of USEN-NEXT GROUP

Providing credit services to foreign residents in Japan Jan. 2020 : Established Credd Finance, Ltd. with Seven Bank, Ltd. Aug. 2020 : Started issuance of credit cards

Shinsei Bank Group business at a glance

17

OBP1 after Net Credit CostsTotal Revenue

65%FY2019

47%FY2019

32%FY2019

48%FY2019

156.6

0

40

80

120

160

17 18 190

10

20

30

17 18 19(FY)

23.9

0

20

40

60

80

17 18 19

76.8

0

10

20

30

17 18 19

24.6

OBP1 after Net Credit CostsTotal Revenue

(Unit: JPY billion)Individual Business Institutional Business

Yen / foreign currency deposits, structured deposits, investment trusts, securities brokerage services (through a partner institution), life and nonlife insurance (through partner institutions), housing loans and other financial services for individuals

Corporate Business

Structured Finance Real estate-related nonrecourse finance and corporate finance, project finance, specialty finance including M&A-related finance

Principal Transactions

Financial products and services focused around lease financeShowa Leasing

Securities business, asset management business, wealth management businessOther Global Markets Businesses

Foreign exchange, derivatives, equity-related and other capital markets businessMarkets Business

Private equity, credit trading, business succession finance and asset-backed investment, etc.

1 Ordinary Business Profit

Major Businesses

Shinsei Financial

APLUS FINANCIAL

Other IndividualBusiness

Unsecured loans and credit guarantees(Lake ALSA, Shinsei Financial, Shinsei Bank Card Loan L (former Shinsei Bank Lake), NOLOAN)

Shopping credit, credit cards, loans and payment services

Other subsidiaries

Major Businesses

Retail Banking Providing financial products, services and advisory services for corporations, public-sector entities and financial institutions, healthcare finance business, trust banking business

(FY) (FY) (FY)

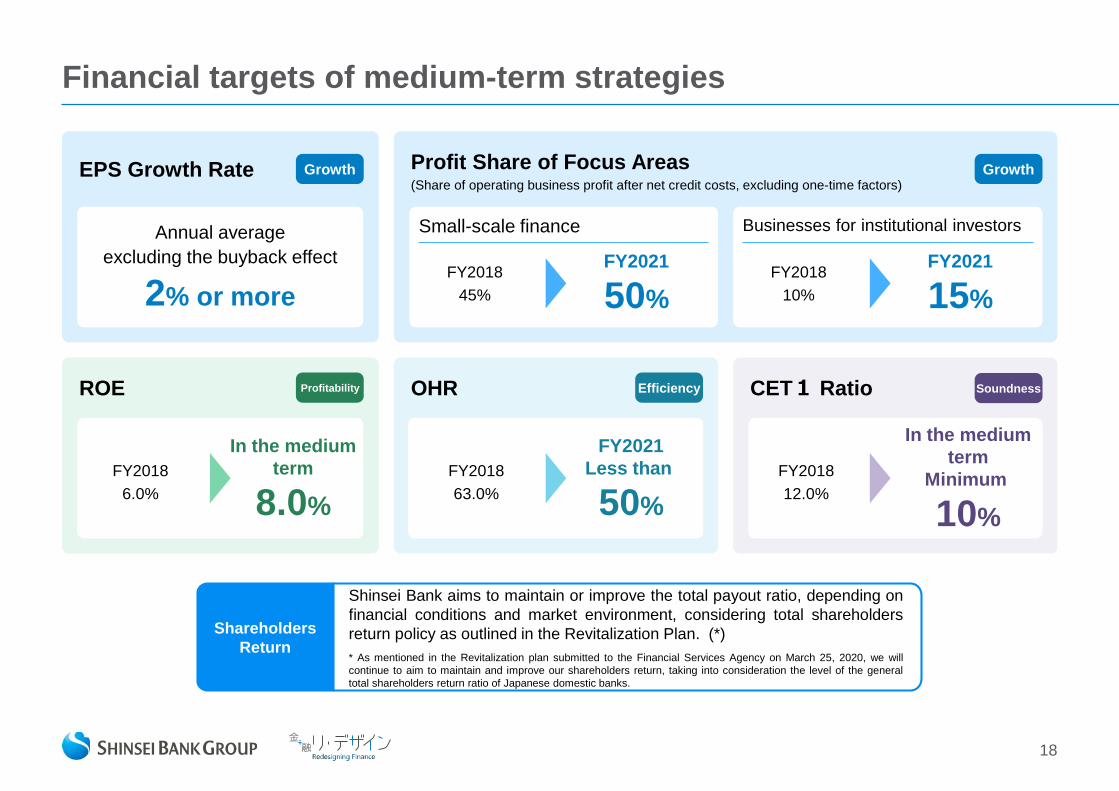

Financial targets of medium-term strategies

18

EPS Growth Rate

Annual averageexcluding the buyback effect

2% or more

Growth Profit Share of Focus Areas(Share of operating business profit after net credit costs, excluding one-time factors)

Growth

Small-scale finance

FY201845%

FY2021

50%

Businesses for institutional investors

FY201810%

FY2021

15%

ROE Profitability

FY20186.0%

In the mediumterm

8.0%

OHR Efficiency

FY201863.0%

FY2021Less than

50%

CET1 Ratio Soundness

FY201812.0%

In the mediumterm

Minimum

10%

Shareholders Return

Shinsei Bank aims to maintain or improve the total payout ratio, depending onfinancial conditions and market environment, considering total shareholdersreturn policy as outlined in the Revitalization Plan. (*)* As mentioned in the Revitalization plan submitted to the Financial Services Agency on March 25, 2020, we willcontinue to aim to maintain and improve our shareholders return, taking into consideration the level of the generaltotal shareholders return ratio of Japanese domestic banks.

Unsecured loan market: Nonbank market remains flatwhile overall market appears to decrease

19

-6%

0%

9%8% 8% 7%4%

0% -1%-5%

-40%

-30%

-20%

-10%

0%

10%

20%

10.3 11.3 12.3 13.3 14.3 15.3 16.3 17.3 18.3 19.3 20.3 20.6

8.4

6.8 6.3 6.2

6.8 7.3

7.9 8.5 8.8 8.8 8.8

8.4

0

5

10

10.3 11.3 12.3 13.3 14.3 15.3 16.3 17.3 18.3 19.3 20.3 20.6

Unsecured Loan Market: Growth Rate (YoY) Unsecured Loan Market: Size(Unit: JPY trillion)

(Data Source) Bank of Japan, Japan Financial Service Association

“Unsecured loan market”= “Bank card loan balance” + “Nonbank unsecured loan balance”“Bank card loan balance”: Statistics aggregated by the Bank of Japan; Balance of consumer card loans extended by domestic banks and credit unions“Nonbank unsecured loan balance”: Statistics aggregated by the Japan Financial Services Association; Unsecured loans (consumer finance sector) month end balance (excludes housing loans)

YoY: Unsecured Loan Market Growth RateYoY: Nonbank Unsecured Loan Growth Rate

YoY: Bank Card Loan Growth Rate

Nonbank Unsecured Loan BalanceBank Card Loan Balance

(Data Source) Bank of Japan, Japan Financial Service Association

The preceding description of Shinsei Bank Group’s Medium-Term Strategies contains forward-lookingstatements regarding the intent, belief and current expectations of our management with respect to ourfinancial condition and future results of operations. These statements reflect our current views withrespect to future events that are subject to risks, uncertainties and assumptions. Should one or more ofthese risks or uncertainties materialize, or should underlying assumptions prove incorrect, our actualresults may vary materially from those we currently anticipate. Potential risks include those described inour annual securities report filed with the Kanto Local Finance Bureau, and you are cautioned not toplace undue reliance on forward-looking statements.

Unless otherwise noted, the financial data contained in these materials are presented under JapaneseGAAP. Shinsei Bank Group disclaims any obligation to update or to announce any revision to forward-looking statements to reflect future events or developments. Unless otherwise specified, all thefinancials are shown on a consolidated basis.

Information concerning financial institutions and their subsidiaries other than Shinsei Bank Group arebased on publicly available information.

These materials do not constitute an invitation or solicitation of an offer to subscribe for or purchase anysecurities and neither this document nor anything contained herein shall form the basis for any contractor commitment whatsoever.

Disclaimer

20