Embed Size (px)

Citation preview

Annals of Operations Research 114, 203–227, 2002 2002 Kluwer Academic Publishers. Manufactured in The Netherlands.

Strategic Experimentation in Financial Intermediationwith Threat of Entry ∗

NEELAM JAIN [email protected] School of Management, Rice University, Houston, TX 77251, USA

THOMAS D. JEITSCHKO [email protected] of Economics, Michigan State University, East Lansing, MI 48824, USA

LEONARD J. MIRMAN [email protected] of Economics, University of Virginia, Charlottesville, VA 22903, USA

Abstract. We study how the threat of entry affects financial contracting between an incumbent firm anda bank, in a stochastic and dynamic environment. Contracts are short term and public. We determinethe effects of the first period financial contract on the first period outputs in face of the threat of entry.Specifically, it is shown that the distance between first period outputs is increased due to potential entry.This is due to two underlying effects: first, the threat of entry reduces the signal dampening effect and thusthe surplus left to the low cost incumbent is reduced. Second, learning is more valuable as it decreasesthe probability of entry. Indeed, experimentation takes on a strategic form, since the bank must take intoaccount the impact of the possible game on its expected profits. This work integrates the agency problembetween a firm and its financial intermediary with the issue of entry-deterrence under uncertainty.

Keywords: experimentation, strategic experimentation, signal dampening, financial intermediation, limitpricing, entry deterrence

AMS subject classification: 60, 90

1. Introduction

Information and learning play an important role in many economic environments. In-deed, they are the crucial element in understanding the different aspects of observedbehavior in many instances. The role of information and learning has been modelled invarious ways in the economic literature. Two examples of research that have informationas their key element are the principal-agent literature, in particular, the literature dealingwith the ratchet effect or more importantly, dynamic aspects of principal-agent modelsand the literature on entry deterrence. Indeed, the results established in the literature de-pend crucially on how the informational aspects are treated. For example, in the initialphase of the development of principal-agent models, whenever agents’ actions separate

∗ Earlier versions of the paper were presented under different titles at the Wissenschaftszentrum Berlin(June, 1999) and the Mid-West Economic Theory Conference at the University of Illinois (October, 1999).

204 JAIN ET AL.

their types, all uncertainty is resolved at the conclusion of the first period.1 While in laterliterature, noise yields incomplete learning and thus makes the informational content ofthe decision more important than in the noiseless models.2

There is another aspect of the noiseless models that determines the effect of infor-mation on economic decisions, namely, the role played by expectations. In particular,consider the entry literature studied, for example, by Milgrom and Roberts (MR) [7]. Inthese models, many equilibrium points, each depending on the beliefs of the potentialentrant, are implied. Or, put another way, the beliefs of the potential entrant dictate theequilibrium outcomes of the model. With the addition of noise in these entry models,e.g., in Matthews and Mirman (MM) [6], beliefs do not dictate the equilibrium. In fact,noise allows the underlying information to be used as a strategic tool in decision making.This is also true of the dynamic principal-agent literature in which the addition of noiseallows one to study the effect of information on decisions, as in JMS and JM.

In this paper, we combine principal-agent and entry models in a noisy environment,as is done for the noiseless case by Jain, Jeitschko, and Mirman (JJM) [1].3 Our pur-pose is to study how the subtle interplay of information and learning impact short-termcontracts based on a stochastic signal, when the principal-agent relationship is affectedby the possible entry of a third party, and compare these results to the models withoutentry (JMS and JM) and the noiseless case in JJM. Specifically, we study the impact ofpotential future entry on the current financial contracts between an incumbent firm anda lender, referred to as a bank. We also study the impact of financial contracting on theoutcome of the entry game, in particular limit pricing, when in addition to the lender, theentrant is aware of the contract between the bank and the firm and observes the stochas-tic signal. In order to study how the informational effects studied in JMS and JM playout in this environment, we do not consider the possibility that the bank offers a menu ofcontracts. Instead, we study a single contract based on publicly observable market data(the market price) between the bank and incumbent firm.

Since the contract is based on a stochastic signal, not all uncertainty need be re-solved after the conclusion of the first period. This is a crucial difference between ourmodel and that of JJM. Indeed, as a consequence of this, manipulating the flow of infor-mation generated by the first period contract becomes a critical feature of the contractbetween the bank and the incumbent monopolist. Not only does the bank account forthe incumbent’s incentives in attempting to preserve informational rents over time (signaldampening), the bank also attempts to actively learn about the incumbent firm (experi-mentation). Moreover, since the contract is devised under the threat of entry, the bankaccounts for how the threat of entry affects the incumbent’s incentives and also accountsfor the impact of the flow of information on the entrant’s actions in the second period(strategic experimentation). That is, the contract between the bank and the incumbent ismanipulated in order to affect the probability of entry into the market.

1 See, e.g., Laffont and Tirole [5].2 See, Jeitschko, Mirman and Salgueiro (JMS) [4] and Jeitschko and Mirman (JM) [3].3 See JJM for a review of the literature concerning the interplay of financial and real decision in determin-

istic environments.

STRATEGIC EXPERIMENTATION 205

The addition of noise to the JJM model has an important effect on results. Unlikethe model in MR and JJM, the equilibrium is no longer dictated by the beliefs of theentrant. Indeed, the entrant must now adjust his beliefs using Bayes’ rule. To isolateand emphasize this effect, we allow the bank to publicly contract with the incumbentfirm. In this case, the bank can use both the information structure and its control overthe incumbent to decrease the probability of entry.

The fact that the bank effectively controls the output of both types of incumbentalso affects our equilibrium. Indeed, our results generalize those of JMS and JM tothe situation in which there is a game outside of the principal-agent relationship in thesecond period. JMS and JM show that in a principal-agent setting with noise and there-fore learning, there is a significant change in the results of the noiseless principal-agentmodel. Among the effects of a noisy environment is that both the “good” and the “bad”agent’s actions are manipulated by the principal. One implication of this effect is that the“good” agent no longer chooses the first best action in the first period. More importantly,JMS and JM show that the addition of noise reduces both the up-front payments madeto the agent, as well as the principal’s second period expected payoff, since due to thenoise, the principal is unable to infer the agent’s type.

The interaction of the noisy environment and the second-period game in ourprincipal-agent model implies several results. The first is that the principal and entrantmay not have full information about the incumbent’s type. As a consequence, even inthe second period the (static) contract between the bank and incumbent firm specifies asmaller output than the first best output of a standard Bayesian–Nash equilibrium, andconsequently less than in the second period of the noiseless model of JJM. The reason forthis is that due to the remaining uncertainty, the principal’s contract implies distortionsaway from the first best (lowering production) for the “bad” agent. As these distortionsfeed into the game, the entrant accounts for them and consequently deviates from itsstandard Bayesian–Nash output (increases output). This, in turn, implies that the prin-cipal induces the “good” agent to deviate from the first-best outcome. Thus, the goodagent produces less than the standard Bayesian–Nash amount.

The effects of the addition of noise (to JJM) and the addition of the game in the sec-ond period (to JMS) reinforce each other. The payoff to the “good” agent is decreased inthe first period both because the noise makes deception less profitable and preserves fu-ture rents and because the game in the second period makes the future more competitive(less profitable), which also makes deception less worthwhile. Similarly, the principal’ssecond period profits are reduced compared to the full information state in the absenceof noise, and due to increased competition whenever entry occurs. Interestingly, both ofthe reasons for decreased payoffs of the bank in the second period feed back into the firstperiod contract. On the one hand, the principal wants to learn about the incumbent’s typein order to reduce second period uncertainty, and on the other, he wants to deter entry tokeep the second period market profitable – both ends are achieved simultaneously in themodel due to the interaction of the noise and the second-period game.

206 JAIN ET AL.

2. The model

We briefly outline the sequence of events and then turn to the equilibrium notion that isemployed to study the question of how financial intermediation may impact real vari-ables in a dynamic model of entry.

2.1. The first period

Consider a market in which inverse demand is given by p = a−bq+ε, where a and b areknown parameters and ε is a random, unobservable term that is known to be distributeduniformly on the interval [−η, η], where η > 0.

Firms in this market supply the quantity q and thereafter ε and hence the price arerealized. The price p is publicly observable, but the quantity, q, is private informationof the producing firm(s) and unverifiable to others.

The market is initially supplied by a single firm – an incumbent. In order to produceany output, the incumbent requires outside funding in the amount of F . A financialintermediary, i.e., a bank, provides these funds in exchange for later repayment in theamount of R. For simplicity, and without loss of generality, we normalize F to be equalto zero, without, however, changing the fact that the incumbent must go through the bankin order to produce.4

The relationship between the bank and the incumbent firm is modelled as aprincipal-agent interaction in which the bank acts as a principal that offers the incumbentfirm, the agent, a take-it-or-leave-it repayment schedule in exchange for the funds F .Specifically, following JMS and JM, it is assumed that the bank publicly offers a re-payment schedule that maps the observed market price p into an amount R(p) that theincumbent must pay to the bank after the market has cleared.

Both the incumbent and the bank are risk-neutral expected profit maximizers withunlimited liability.5 Hence, the bank’s objective is to maximize its expected net incomefrom the transaction with the incumbent, which having normalized F to equal zero isrepresented as ub = R(p). The incumbent’s objective is to maximize the expecteddifference between profit generated in the market and the net transaction with the bank,denoted by ui = πi − R(p), where πi is the profit generated by the incumbent firm inthe market. Both bank and incumbent have a reservation utility of zero, that is, if nocontract comes to pass between the two, both receive a payoff of zero.

The problem faced by the bank is trivial if the bank and the incumbent have thesame information regarding the circumstance of the interaction. Indeed, the bank simplyinduces the incumbent to obtain the “first best” level of market profit and then demandsthis amount in repayment R in exchange for its initial lending of the amount F . Instead,and more realistic for most instances, we suppose that the incumbent is better informed

4 F is an (essentially) arbitrary constant. All results follow provided that the market generates sufficientprofit to cover F .

5 Although in the model there are states of the world in which one of the firms has negative profits, thisdoes not mean that the firm is bankrupt but only that it is below its opportunity costs or normal profits.

STRATEGIC EXPERIMENTATION 207

about one aspect of the market. Specifically, suppose that the technology used to providethe good implies a constant unit cost, and that there are two possible levels that the unitcost might be, denoted by c and c, with c < c < a, the demand intercept. The incumbentknows its own cost, the bank has beliefs ρ that the incumbent’s cost is low, and 1 − ρ

that the cost is high.6 We subsequently refer to the two “types” of incumbent as low(marginal) cost and high (marginal) cost.

2.2. The second period

After one such interaction between the bank and the incumbent the market price is pub-licly observable and the incumbent pays the bank based on this price, in accordance withthe repayment scheme R(p).

Since the price is publicly observable, the price allows inferences about the output.Based on the observable price, the bank draws inferences about the marginal cost of theincumbent. That is, the bank updates its beliefs about the incumbent’s type.

Suppose that a second firm, referred to as the entrant, is aware of the contract thatis in place between the bank and the incumbent firm. The entrant also observes the firstperiod price and draws its inferences about the incumbent’s cost type. Based on its up-dated beliefs about the incumbent’s cost and its beliefs about the second period contractbetween the bank and the incumbent, the entrant decides whether or not to enter the mar-ket. This entry decision is made on the basis of the entrant’s expectation of profits, whichdepends on there being two firms in the market that engage in simultaneous move quan-tity (Cournot) competition. Moreover, the bank observes the entrant’s decision beforedesigning an incentive scheme for the incumbent in the second period.

The entrant can also be of high marginal cost, c, or low marginal cost, c.7 Theentrant knows his own cost type. However, neither the incumbent nor the bank knowthe entrant’s type, and have beliefs µ that the entrant has low marginal cost and 1 − µ

that it has high marginal cost. In addition to its production cost, the firm incurs a type-dependent fixed cost of entry, denoted by K and K, that it can finance internally. Theentrant is also a risk-neutral profit maximizing entity, with payoff denoted by ue. Weassume that the entrant’s fixed cost of entry is such that if the entrant believes that theincumbent firm has low marginal cost, he does not enter the market, regardless of hisown type. Otherwise he enters.

Suppose finally that all players’ time preference is captured in the common dis-count factor δ.

2.3. The equilibrium notion

The equilibrium we study is a perfect Bayesian–Nash equilibrium in pure strategies.This implies that all beliefs about agents’ types and actions are mutually consistent with

6 Similar insights and results are obtained whether the asymmetric information is about cost, or on thedemand side of the market. For simplicity and in keeping with MR we model cost uncertainty.

7 The assumption that the entrant can be of two types is not necessary for our results. However, it is madeto ensure consistency with the MR model.

208 JAIN ET AL.

the actions taken in equilibrium, including beliefs about actions taken in accordance withwhich contracts are in place between the bank and the incumbent firm. Moreover, beliefsare updated using Bayes’ rule.

Since the purpose of the paper is to examine how the dissemination of informationimpacts a firm’s real decisions via its financial decisions, given financial intermediation,we consider contracts between the bank and the incumbent firm in which only the ob-served market price is contractible. Moreover, the parameters of the model are restrictedso that the following assumptions hold:

Assumption 1. The probability that the incumbent firm has low marginal cost is small;that is, ρ is small.

Assumption 2. Given market output, the range of possible prices is large; that is, η islarge.

The implication of assumption 1 is that the bank finds it profitable to contract withboth types of incumbent firm. If assumption 1 is not met, then there is complete andimmediate learning, because one type of incumbent (the one with high marginal cost)reveals its type by not producing.

Assumption 2 also assures that there is not immediate and complete learning, be-cause for sufficiently large support of the noise term, ε, there are equilibrium prices thatcould stem from either type of firm’s equilibrium output. Moreover, as demonstratedin JMS, assumption 2 guarantees that it is optimal for the bank to entice the two typesof firm to produce distinct levels of output. Consequently, the equilibrium repaymentscheme in both periods has the low cost firm’s incentive compatibility and the high costfirm’s individual rationality constraint binding – all other constraints are slack.

Following JMS, since there are an infinite number of repayment schemes that im-plement the second best outputs at equally low cost for the bank, we present only the realimplications of the equilibrium contract, i.e., the equilibrium outputs, expected profits,and expected payoffs.8

Before deriving the results in this case, we consider a useful benchmark. Specif-ically, we consider the model when there is no second firm and thus no threat of entry.This allows us to determine the impact of the threat of entry on the contracts betweenthe bank and the incumbent firm.

3. The model without the threat of entry

In each period the bank’s objective is to maximize the repayment obtained from the firmin exchange for providing the funds F to the firm, accounting for the flow of informationin each of the two periods. In particular, this means that in the second period the bankwill design the repayment schedule on the basis of its updated beliefs about the marginal

8 See JMS for an example of how an equilibrium contract is derived.

STRATEGIC EXPERIMENTATION 209

cost of the firm given its observation of the first period price. Moreover, since boththe bank and the firm are forward–looking in taking their first period decisions, it isnecessary to consider how these decisions affect the flow of information and secondperiod outcomes. That is, it is necessary to focus on the possible second period outcomesbefore turning to the solution of the first period.

3.1. The benchmark second period

After observing the first period price and updating its beliefs about the marginal cost ofthe firm, there are only two possible scenarios for beliefs in the second period: either thebank believes it has inferred the type of the firm, or it has not. We consider the two casesin turn.

3.1.1. The bank is sure about the firm’s costsAlthough the firm can have either high, or low marginal cost, let c generically stand forc or c. Given that the bank believes it knows the type of the firm, it simply calculatesthe highest expected profit that each type of firm can make (the “first best” level ofprofit), and demands this amount as repayment in return for the second period lendingof funds F . That is, the bank demands R = (a − c)2/(4b) in return for second periodfinancing. Consequently, the bank obtains a second period expected payoff of

ub = (a − c)2

4b. (1)

If the bank’s beliefs are correct, and in equilibrium they are of course, the payoff of thefirm is its reservation level of utility, namely 0. We assume that this is enforced througha forcing contract in the second period with substantial penalties for out-of-equilibriumprice observations. Consequently, should the bank incorrectly believe the firm has highcost when indeed it has low cost, the firm’s expected payoff is

u = (c − c )q∗. (2)

That is, the firm’s payoff is its cost advantage over the high cost type multiplied by thefirst-best level of output of a high cost firm, q∗.

3.1.2. The bank is unsure about the firm’s typeSince noise is distributed uniformly, if the bank cannot infer the firm’s type from thefirst period’s price, then the bank’s posterior beliefs coincide with its prior beliefs. Inthis case, the bank maximizes its second period profit, ρR + (1 − ρ)R, where R and R

are the expected repayments of the low cost and the high cost incumbent respectively,subject to the firm’s incentive compatibility and individual rationality constraints.

As is standard and straightforward to verify, of the two individual rationality con-straints, only the high cost firm’s constraint binds at the optimum. The reservation utility

210 JAIN ET AL.

of the firm is 0, so the high cost type will expect to repay the entire profit generated. Let-ting q denote the equilibrium output, the binding individual rationality constraint is

R = (a − bq − c )q. (3)

Similarly, at the optimum only the low cost firm’s incentive compatibility constraintbinds. Using analogous notation this can be written as

(a − bq − c )q − R = (a − bq − c )q − R;or, using (3),

R = (a − bq − c )q − (c − c )q. (4)

Substituting for R and R in the bank’s expected second-period profit, ρR +(1 − ρ)R, the bank’s maximization problem is to choose q and q, in order to maximize

ρ((a − bq − c )q − (c − c )q

) + (1 − ρ)(a − bq − c )q.

The first-order-conditions are sufficient and the solution to this problem is given by9

q = a − c

2b, (5)

q = a − c

2b− ρ

1 − ρ

c − c

2b. (6)

That is, the low cost firm produces the first best level of output, whereas the high costfirm produces less than the first best amount.

After substituting back into the binding constraints, some algebraic manipulationsyield the benchmark expected repayments:

R = (a − c )2

4b+

(1 + ρ

1 − ρ

)(c − c )2

4b,

R = (a − c )2

4b−

(ρ

1 − ρ

)2(c − c )2

4b.

That is, the low cost firm repays more than the high cost firm – a reflection of the fact thatit generates higher profits. And the high cost firm repays less than its first best amountof profit – a reflection of the fact that it produces below the first best level.

Letting ub, u, and u denote the second period expected payoff to the bank, the lowcost and the high cost firm, respectively,

ub = (a − c )2

4b+ ρ

1 − ρ

(c − c )2

4b,

(7)u = (c − c )q, u = 0.

9 Assumption 1 assures that these are both positive; and consequently, a necessary condition for assump-tion 1 to hold is that ρ < (a − c )/(a − c ).

STRATEGIC EXPERIMENTATION 211

Due to the restriction imposed on ρ implied by assumption 1, the bank’s payoff liesbetween the high cost and low cost firm’s first-best amount of profit. If ρ = 0 the bank’spayoff equals the first best level of the high cost firm’s profit, and if ρ is equal to theupper bound imposed by assumption 1 the bank obtains the payoff it gets when ignoringthe possibility that there is a high cost type, i.e., ρ(a − c )2/(4b).

The high cost firm’s repayment is equal to its profit, so its payoff is 0. The payoffof the low cost firm is its cost advantage over the high cost firm multiplied by the highcost firm’s output. That is, it is the amount of market profit the low cost firm could retainif it pretended to be the high cost firm and produced the high cost firm’s output and thenpaid R.

Thus, the contract yields the standard features – an information rent for the lowcost firm, which produces the “first best” level of output and output below the “firstbest” level if the firm is high cost. These features are relevant in the analysis of the fullmodel. But another property also plays a crucial role.

Proposition 1. If the bank has not inferred the incumbent’s type, the expected output ofthe incumbent is equal to the first best level of output of a high cost firm. Formally,

q ≡ ρq + (1 − ρ)q = a − c

2b≡ q∗.

3.2. The benchmark first period

Having solved the second period problem, we now determine the optimal first-periodcontract between the bank and the firm. The bank’s objective is to choose a repaymentscheme in order to maximize its expectation of both the current and future payoff, givenits prior belief ρ that the firm has low marginal cost of production.

Thus, letting R and R denote the expected repayments of the respective types ofincumbent in the first period, the bank maximizes

ρR + (1 − ρ)R + δEub, (8)

subject to the two individual rationality and incentive compatibility constraints of thefirst period.

In order to determine the effect of the second period on the first-period constraintsand the bank’s future expected payoff, one needs the bank’s belief function and theequilibrium probabilities of the various second period scenarios.

Letting q and q denote the respective first period levels of output, and expandingthe domain to include out-of-equilibrium observations, the following lemma gives theposterior belief function and the associated equilibrium probability of observations basedon Bayes’ rule:10

10 Assumption 2 assures that the three intervals have positive length and the associated probabilities arepositive.

212 JAIN ET AL.

Lemma 1. The posterior is given by

ρ2(p1|q, q) =

1, if p1 ∈ (−∞, a − bq − η),

ρ, if p1 ∈ [a − bq − η, a − bq + η],0, if p1 ∈ (a − bq + η,∞).

The equilibrium ex ante respective probabilities of the three possible states in the secondperiod are

Pr{ρ2 = 1} = ρb(q − q )

2η,

Pr{ρ2 = ρ} = 2η − b(q − q )

2η,

Pr{ρ2 = 0} = (1 − ρ)b(q − q )

2η.

The probabilities in combination with the bank’s payoffs ub for the possiblesecond-period scenarios derived in the previous subsections allow one to determine Eub

as a function of q and q. Specifically, the two possible scenarios of obtaining first bestrepayment, whose case-dependent amount is given in (1), as well as the case of remain-ing uncertainty, (7), in conjunction with lemma 1 yield

Eub = (a − c )2

4bρ

b(q − q )

2η+ (a − c )2

4b(1 − ρ)

b(q − q )

2η

+(

(a − c )2

4b+ ρ

1 − ρ

(c − c )2

4b

)2η − b(q − q )

2η

= ρ

((a − c )2

4− (a − c )2

4− (c − c )2

4(1 − ρ)

)q − q

2η+ A, (9)

where A does not depend on q or q.Consider now the high cost firm’s binding individual rationality constraint. Since

the high cost firm’s second period payoff is zero, regardless of the bank’s beliefs, theindividual rationality constraint of this type is as before and given by (3).

Suppose now that the firm has low marginal cost. Since its individual rationalityconstraint is slack, one needs only consider its incentive compatibility constraint. Thisconstraint differs from the static second period constraint in that the low cost firm mustbe paid up-front its discounted potential gain from deception. If the low cost firm mimicsthe high cost firm and produces q in the first period, then for sufficiently large ε the bankwill believe that the firm has high cost and will thus offer the first best contract for thehigh cost firm in the second period. Due to its cost advantage the low cost firm accepting

STRATEGIC EXPERIMENTATION 213

this contract in the second period obtains a payoff of (c − c )q∗ = (c − c )(a − c)/2b,see (2). Taking into consideration the probability that ε is large enough for such a suc-cessful deception to occur (see lemma 1), the incentive compatibility constraint of theincumbent firm with low marginal cost yields

R = (a − bq − c )q − (c − c )q − δ(c − c )

(a − c

2b

)b(q − q )

2η. (10)

Substituting the bank’s future expected payoff, (9), and the two binding con-straints, (3) and (10), into the bank’s maximization problem (8), yields the first periodoptimization problem in which the bank chooses q and q. The first order conditions ofthe bank’s problem are sufficient and yield

q = a − c

2b+ δ

2bB

1

2η, (11)

q = a − c

2b− ρ

1 − ρ

(c − c

2b+ δ

2bB

1

2η

), (12)

where B = −(c − c )2/[4(1 − ρ)].Notice that compared to the optimal outputs in a static contract under uncertainty,

i.e., equations (5) and (6), the outputs are shifted by a multiple of B < 0. Consequentlythe low cost firm’s output is ratcheted upward from the first to the second period. Thisis, of course, the classic ratchet effect as derived in JMS, where it is shown that this isthe end result of the interplay of conflicting incentives of the bank when considering theimplications of the flow of information in the course of the interaction. These incen-tives are briefly discussed in the next subsection. We then consider how potential entryimpacts these effects in the interaction between the bank and the firm.

3.3. Informational effects in the benchmark

When comparing the first period problem of the bank to a static problem of asymmetricinformation, such as that faced by the bank in the second period when it remains unin-formed, two significant differences emerge. The first stems from the altered incentivecompatibility constraint of the low cost firm due to the two-period problem. The otherarises due to the bank taking into account its expected second period payoff when settingfirst period outputs. We consider each in turn.

3.3.1. Signal dampeningCompared to the second period repayment of the low cost firm, given in (4), the firstperiod repayment is smaller in order to get the low cost incumbent to reveal its type,see (10). Of course, lowering the first period repayment of the low cost incumbent iscostly for the bank in the short run. However, the bank can influence the amount of thereduction in the repayment by its choice of the first period induced outputs. Indeed, if thebank induces outputs that are close together, then if the firm produces q the likelihoodthat the bank believes that the firm has high marginal cost (Pr{ρ2 = 0} in lemma 1),

214 JAIN ET AL.

is small. Consequently, the reduction in the first period repayment of the low cost firmis small. Since the increased payment to the bank is brought about by reducing theinformativeness of the first period price, this process is called signal dampening. Thisprocess is formalized in the following proposition.

Proposition 2 (Signal dampening, JMS theorem 2). In order to increase the first periodexpected repayments, the bank induces output levels closer together, compared to thestatic contract under asymmetric information.

In other words, the bank increases the first period repayment, by decreasing theprobability that it will infer the incumbent’s type, thereby preserving future expectedinformational rents of a truthful low cost incumbent and thwarting future expected gainsof a deceptive low cost incumbent.

3.3.2. Active learningThe other part of the bank’s first period problem that has a dynamic element arises fromthe bank’s ability to manipulate the first-period repayment schedule in order to increaseits future expected payoff. That is, the first period equilibrium outputs also affect thebank’s ability to infer the incumbent’s type (also referred to as active learning) and thusincrease the bank’s second-period expected profits.

Indeed, the bank engages in experimentation, or active learning. In particular thebank increases the distance between the two possible first period outputs to reduce theprobability that the incumbent’s type remains unknown (Pr{ρ2 = ρ} in lemma 1), andthus makes the observed first period price more informative.

Proposition 3 (Experimentation, JMS theorem 1). In order to enhance the flow of in-formation (i.e., learn), the bank increases the distance between the first period outputs,compared to the static contract under asymmetric information. That is,

d

dqEub > 0,

d

dqEub < 0.

Note that assumption 1 is relevant to this proposition since assumption 1 impliesthat the bank accounts for both types of firm in the optimal contract. If the bank does notintend to consider both types of incumbent, then there is no need to experiment in orderto learn about the type of the incumbent.

Next we analyze the full model and consider how the optimal contract betweenthe bank and the incumbent firm is affected when there is potential entry in the secondperiod.

STRATEGIC EXPERIMENTATION 215

4. The equilibrium under the threat of entry

We begin with the analysis of the second period game.

4.1. The second period contract

In this section, we assume that the incumbent’s output is given by qi and the entrant’soutput by qe. Similarly, wherever necessary, we distinguish the incumbent’s marginalcost, ci , from the entrant’s, ce.

As before, the principal’s posterior can take on at most three distinct values inequilibrium. Indeed, while the first period outputs q and q are different from the no-entrycase, lemma 1 still applies. Moreover, since the first period optimal contract betweenthe bank and the incumbent firm is known to the entrant, the entrant’s and the bank’sposterior beliefs coincide.

The bank’s optimal second period contract with the incumbent firm depends notonly on the bank’s beliefs about the cost structure of the incumbent, but also on whetherthe second firm has entered the market. This, in turn, depends on the entrant’s beliefsabout the incumbent’s cost structure, given that after entry occurs, the firms compete inCournot fashion.

It turns out that a result analogous to proposition 1 obtains in the second period.Specifically, the incumbent’s expected output under uncertainty is equal to the first bestlevel of the high cost firm, after entry has occurred. Consequently, since the entrant isalso risk neutral, the entry rule specifies the same action whether the posterior is equalto ρ or 0. In other words, although beliefs take on three possible values, due to ananalogous result to proposition 1, the entry rule only distinguishes between two cases:the incumbent is believed to have low cost (ρ2 = 1) and the incumbent may have highcost (ρ2 = ρ, 0).

For all parameter values (i.e., values of fixed cost associated with entry) such thatthe entrant’s decision is distinct for two of the three possible posterior beliefs, the qual-itative insights are the same. We focus on the following specification as it most closelymirrors MR. That is, the entrant’s cost structure is such that, in equilibrium, his decisionis independent of his type.

Lemma 2. The entrant’s decision rule is given by

e = {e, e} =

{1, 1}, if ρ2 = 0,

{1, 1}, if ρ2 = ρ,

{0, 0}, if ρ2 = 1.

Here, 1 denotes the event that the firm enters and 0 denotes the case where the firmstays out of the market.

Proposition 4. The probability of entry is decreasing in the distance between the outputsproduced by the low cost and the high cost incumbent.

216 JAIN ET AL.

The proof is straightforward from lemma 1 and lemma 2.An implication of this proposition is that an increase in learning by the bank leads

to a decrease in the probability of entry, since an increase in distance between the twotarget outputs also leads to greater learning by the bank.

The connection between making the first period price more informative by increas-ing the distance between the two levels of output on the one hand and reducing the prob-ability of entry on the other hand, may not be immediately clear, since making the pricemore informative not only increases the probability that the entrant discovers that theincumbent has low marginal cost, but it also increases the probability that the incumbentis revealed to have high marginal cost.

The reason that despite this apparent symmetry entry deterrence occurs, stems fromthe implications of a result analogous to proposition 1. That is, under uncertainty in thesecond period (ρ2 = ρ), the expected output of the incumbent, qi , equals the first bestlevel of output of a high cost firm, q∗. Consequently, any information-sensitive entryrule such as lemma 2 has the feature that entry is deterred if and only if the incumbent isrevealed to have low cost. Hence, increasing the informativeness of the signal increasesthe probability of successful entry deterrence.

Next, we determine the value function of the bank under entry by considering thethree scenarios of learning.

4.1.1. Incumbent is believed to have low marginal costSuppose ρ2 = 1, that is, the bank and entrant believe that the incumbent has low marginalcost. In this case, the entrant does not enter the market and the second period is as insection 3.1.1, where there is no second firm and the bank believes the incumbent firm haslow marginal cost. Hence, the bank simply demands as repayment the monopoly profitof a low marginal cost firm in the market. Thus, the equilibrium repayment scheduleyields

ub = (a − c )2

4b, (13)

Again there are no informational rents, so that the incumbent is left with a payoff ofzero.

4.1.2. Incumbent is believed to have high marginal costSuppose that ρ2 = 0, so that both the entrant and the bank believe that the incumbenthas high marginal cost. The entrant’s cost of entry is such that he enters the marketregardless of his type. Given the bank’s belief that the incumbent has high marginal cost,the bank calculates the highest (i.e., “first best”) level of profit that the high marginal costincumbent can obtain in Cournot competition when facing the entrant. This is the secondperiod repayment that the bank demands from the firm in return for financing the secondperiod amount, F .

In deriving the optimal repayment of the second period, the bank calculates theCournot solution to the two-firm problem, assuming that its beliefs, that the incumbent

STRATEGIC EXPERIMENTATION 217

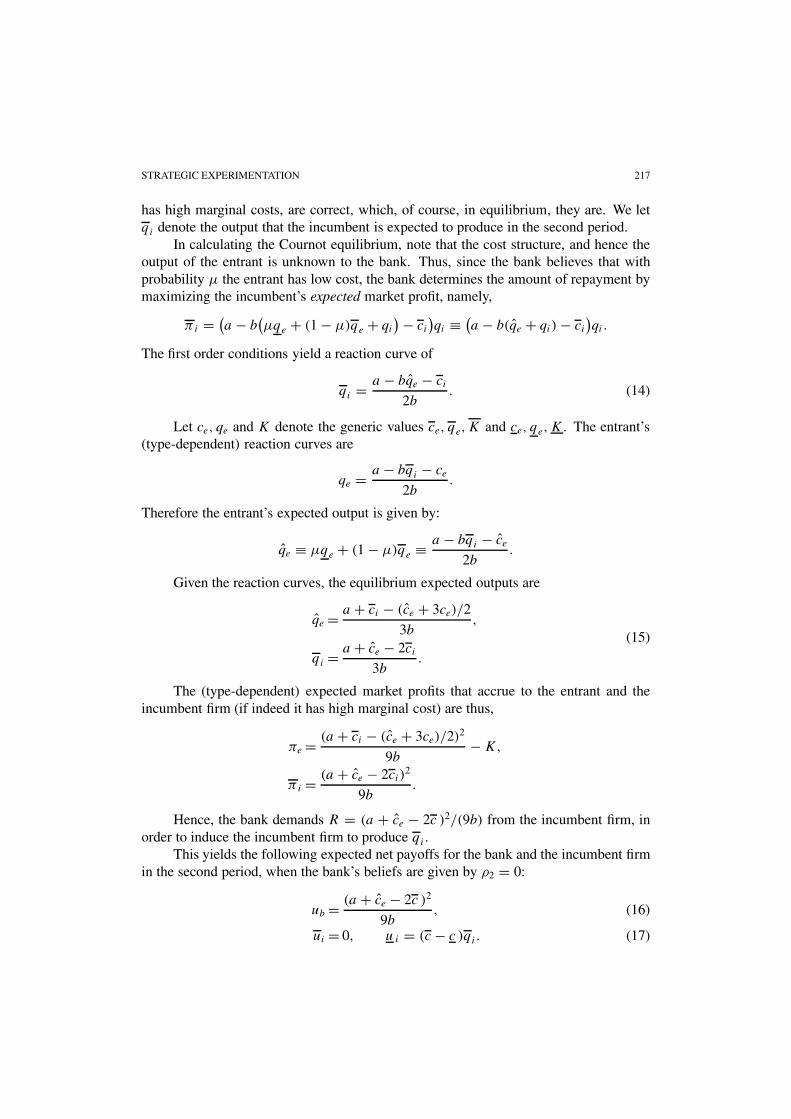

has high marginal costs, are correct, which, of course, in equilibrium, they are. We letqi denote the output that the incumbent is expected to produce in the second period.

In calculating the Cournot equilibrium, note that the cost structure, and hence theoutput of the entrant is unknown to the bank. Thus, since the bank believes that withprobability µ the entrant has low cost, the bank determines the amount of repayment bymaximizing the incumbent’s expected market profit, namely,

πi = (a − b

(µqe + (1 − µ)qe + qi

) − ci

)qi ≡ (

a − b(qe + qi) − ci

)qi.

The first order conditions yield a reaction curve of

qi = a − bqe − ci

2b. (14)

Let ce, qe and K denote the generic values ce, qe,K and ce, qe,K. The entrant’s(type-dependent) reaction curves are

qe = a − bqi − ce

2b.

Therefore the entrant’s expected output is given by:

qe ≡ µqe + (1 − µ)qe ≡ a − bqi − ce

2b.

Given the reaction curves, the equilibrium expected outputs are

qe = a + ci − (ce + 3ce)/2

3b,

(15)

qi = a + ce − 2ci

3b.

The (type-dependent) expected market profits that accrue to the entrant and theincumbent firm (if indeed it has high marginal cost) are thus,

πe = (a + ci − (ce + 3ce)/2)2

9b− K,

πi = (a + ce − 2ci)2

9b.

Hence, the bank demands R = (a + ce − 2c )2/(9b) from the incumbent firm, inorder to induce the incumbent firm to produce qi .

This yields the following expected net payoffs for the bank and the incumbent firmin the second period, when the bank’s beliefs are given by ρ2 = 0:

ub = (a + ce − 2c )2

9b, (16)

ui = 0, u i = (c − c )qi. (17)

218 JAIN ET AL.

That is, the high cost incumbent has no informational rent. Notice, however, thatwe have included a payoff to an incumbent firm that has low marginal cost. Although,in equilibrium, the incumbent has high marginal cost when ρ2 = 0, out-of-equilibriumthe incumbent may have low marginal cost. Given the equilibrium repayment scheme ofthe second period, u i denotes the expected payoff that the low marginal cost incumbentobtains in the second period. As before, this payoff is the cost advantage of the low costincumbent over the high cost incumbent (c − c ) multiplied by the amount produced, qi .

4.1.3. Incumbent of unknown typeFinally, suppose that ρ2 = ρ. In this case both the bank and the entrant do not know theincumbent’s marginal cost. It will be shown that it is optimal for both types of entrant toenter the market.

As will become clear, an analogue to proposition 1 holds. Consequently, the in-cumbent’s expected output is the same as the output produced when it is known that theincumbent has high marginal cost.

Again, letting (ce, qe) ∈ {(ce, qe), (ce, qe)}, the entrant’s profit function yields thetype-dependent reaction curves,

qe = a − b(ρqi + (1 − ρ)qi) − ce

2b≡ a − bqi − ce

2b,

and hence expected output is

qe ≡ µqe + (1 − µ)qe ≡ a − bqi − ce

2b.

In designing the optimal contract, the bank must keep track of two separate issues.First, due to the remaining uncertainty, it must account for the incentive constraint ofthe incumbent. And second, due to entry and the implied game, it must account for thereaction curves of the entrant.

As before, one can think of the bank’s problem as choosing expected repay-ments, R, in order to maximize

ρR + (1 − ρ)R. (18)

Again, only the high cost incumbent’s individual rationality constraint and the low costincumbent’s incentive compatibility constraint are binding. They imply

R = (a − b

(qi + qe

) − c)qi (19)

and

R = (a − b

(qi + qe

) − c i

)qi − (c − c )qi . (20)

STRATEGIC EXPERIMENTATION 219

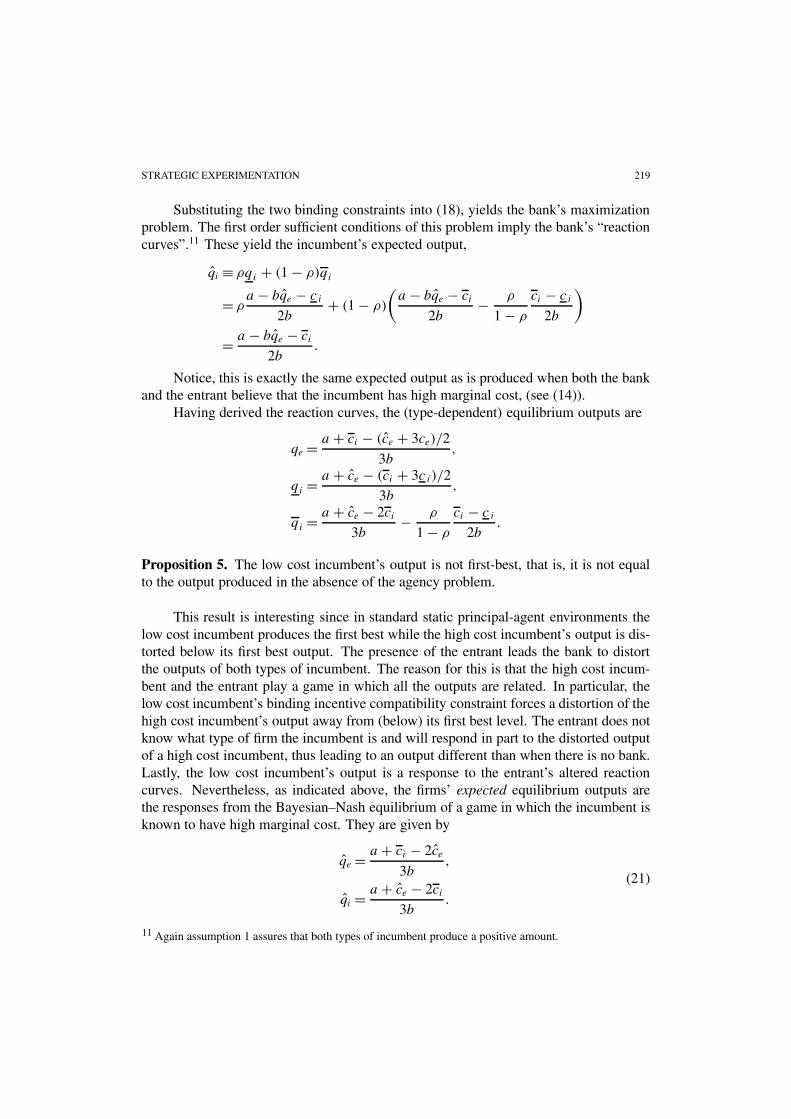

Substituting the two binding constraints into (18), yields the bank’s maximizationproblem. The first order sufficient conditions of this problem imply the bank’s “reactioncurves”.11 These yield the incumbent’s expected output,

qi ≡ ρqi + (1 − ρ)qi

= ρa − bqe − c i

2b+ (1 − ρ)

(a − bqe − ci

2b− ρ

1 − ρ

ci − c i

2b

)

= a − bqe − ci

2b.

Notice, this is exactly the same expected output as is produced when both the bankand the entrant believe that the incumbent has high marginal cost, (see (14)).

Having derived the reaction curves, the (type-dependent) equilibrium outputs are

qe = a + ci − (ce + 3ce)/2

3b,

qi = a + ce − (ci + 3c i)/2

3b,

qi = a + ce − 2ci

3b− ρ

1 − ρ

ci − c i

2b.

Proposition 5. The low cost incumbent’s output is not first-best, that is, it is not equalto the output produced in the absence of the agency problem.

This result is interesting since in standard static principal-agent environments thelow cost incumbent produces the first best while the high cost incumbent’s output is dis-torted below its first best output. The presence of the entrant leads the bank to distortthe outputs of both types of incumbent. The reason for this is that the high cost incum-bent and the entrant play a game in which all the outputs are related. In particular, thelow cost incumbent’s binding incentive compatibility constraint forces a distortion of thehigh cost incumbent’s output away from (below) its first best level. The entrant does notknow what type of firm the incumbent is and will respond in part to the distorted outputof a high cost incumbent, thus leading to an output different than when there is no bank.Lastly, the low cost incumbent’s output is a response to the entrant’s altered reactioncurves. Nevertheless, as indicated above, the firms’ expected equilibrium outputs arethe responses from the Bayesian–Nash equilibrium of a game in which the incumbent isknown to have high marginal cost. They are given by

qe = a + ci − 2ce

3b,

(21)

qi = a + ce − 2ci

3b.

11 Again assumption 1 assures that both types of incumbent produce a positive amount.

220 JAIN ET AL.

Hence the entrant’s output decision is independent of the value of ρ, given that the firmhas entered the market. That is, qi in the above equation is equal to qi in (15). This isthe result analogous to proposition 1.

The (type-dependent) expected market profits in this case are

πe = (a + ci − (ce + 3ce)/2)2

9b− K,

π i = (a + ce − (ci + 3c i)/2)2

9b,

πi = (a + ce − 2ci)2

9b−

(ρ

1 − ρ

)2(ci − c i)

2

4b.

Substituting the expected outputs into the binding constraints (19) and (20) somealgebraic manipulation yields

R = (a + ce − 2ci)2

9b+

(1 + ρ

1 − ρ

)(ci − c i)

2

4b,

R = (a + ce − 2ci)2

9b−

(ρ

1 − ρ

)2(ci − c i)

2

4b.

We summarize the incumbent’s and the bank’s payoff in the second period whenthe incumbent’s marginal cost remains unknown to the bank and entrant:

ub = (a + ce − 2c )2

9b+ ρ

1 − ρ

(c − c )2

4b,

(22)ui = 0, u i = (c − c )qi .

4.2. The first period

The bank’s objective in the first period is to choose a repayment scheme in order tomaximize both the current and the future expected payoff, given its prior belief ρ thatthe incumbent firm has low marginal cost of production.

Thus, as before, letting R and R denote the expected repayments of the respectivetypes of incumbent in the first period, the bank maximizes ρR + (1 − ρ)R + δEub,subject to the two individual rationality and incentive compatibility constraints.

The posterior beliefs and ex ante equilibrium probabilities of the three possible sec-ond period outcomes are as in the benchmark, lemma 1. These probabilities, in combi-nation with the bank’s payoffs ub for the three possible second-period scenarios derivedin the previous section establish Eub as a function of q and q. Specifically, (13), (16)

STRATEGIC EXPERIMENTATION 221

and (22), in conjunction with lemma 1, jointly determine

Eub = (a − c )2

4bρ

b(q − q )

2η+ (a + ce − 2c )2

9b(1 − ρ)

b(q − q )

2η+

+(

(a + ce − 2c )2

9b+ ρ

1 − ρ

(c − c )2

4b

)2η − b(q − q )

2η

= ρ

((a − c )2

4− (a + ce − 2c )2

9− (c − c )2

4(1 − ρ)

)q − q

2η+ A′, (23)

where A′ does not depend on q or q.Consider now the constraints of the two types of incumbent. Since the high cost

incumbent’s expected payoff is zero regardless of the bank’s beliefs, his individual ra-tionality constraint is as before, given by (3). Consequently, only the low cost firm’sdynamic incentive compatibility constraint needs to be determined.

The payoff relevant dynamic aspect of the low cost incumbent’s first period choiceis found when it mimics the high cost firm, thus (possibly) inducing beliefs of ρ2 = 0.Utilizing (17) and lemma 1, the incentive compatibility constraint of the incumbent firmwith low marginal cost yields

R = (a − bq − c )q − (c − c )q − δ(c − c )

(a + ce − 2c

3b

)b(q − q )

2η. (24)

Substituting the bank’s future expected payoff, (23), and the two binding con-straints, (3) and (24), into the bank’s maximization problem yields the restated problemin which the bank chooses q and q. That is, after consolidation, the bank’s problem is tochose q and q in order to maximize

ρ((a − bq − c )q − (c − c )q

) + (1 − ρ)(a − bq − c )q + δρB ′ q − q

2η+ δA′,

where

B ′ =(

(a − c )2

4− (a + c − 2c )(a + c − 3c + c )

9− (c − c )2

(1 − ρ)4

).

The first order conditions are sufficient and yield the following outputs:

q = a − c

2b+ δ

2bB ′ 1

2η,

q = a − c

2b− ρ

1 − ρ

(c − c

2b+ δ

2bB ′ 1

2η

).

These outputs differ from those derived in the benchmark, given in (11) and (12),since B ′ > B. The reason for this stems from the potential of entry and the implieddynamic incentives of both the low cost incumbent and the bank in light of possibleentry.

222 JAIN ET AL.

5. The impact of the threat of entry

As information becomes available from the first to the second period through the publiclyobserved first-period price, all three players’ payoffs are affected. Thus, what the bankinfers about the incumbent from observing the first period price determines how much,if any, informational rents accrue to the incumbent in the second period. In addition,the amount of information also affects the bank’s second period expected payoff. Lastly,the entrant’s payoff depends on the information gleaned from the first period in that itdetermines whether or not it is profitable for the firm to enter the market and competewith the incumbent firm.

5.1. The impact of potential entry on the incumbent’s incentives

In section 3.3.1 the impact of the bank’s learning on the low cost incumbent’s incentivesis captured in proposition 2. In this section we assess how the bank’s learning is changedby potential entry.

The magnitude of the reduction in first period repayment for the low cost incum-bent is determined by the difference between the payoff in the contract that the in-cumbent faces in the second period when his type has been inferred and the payoff hereceives when he attempts to deceive the bank and is subsequently mistakenly believedto have high cost.

With potential entry, the two possibilities – either the incumbent reveals that heis a low cost firm or he deceives the bank into believing that he is a high cost firm12 –not only affect the beliefs of the bank, but also lead to two distinct games in the secondperiod. Specifically, if his type is revealed the incumbent is the only firm in the market,whereas if the bank and the entrant are deceived, entry is triggered, so that the two firmscomplete in Cournot fashion.

An immediate consequence of the incumbent’s altered incentives to deceive is cap-tured in the following proposition, where it is shown that due to potential entry the in-cumbent must make higher repayments in the first period, for fixed, first-period outputs.

Proposition 6. Due to potential entry, the low cost incumbent’s first period repaymentis greater than in the benchmark, for given outputs in the first period.

Proof. The low cost incumbent’s first period repayment is given in (10), when thereis no threat of entry. This payment changes to (24) due to potential entry. The firsttwo terms on the right-hand side of these two equations are identical, since the outputsare held fixed. The third term is the amount by which the repayment of the low costincumbent is reduced in order to induce him to choose the output that may reveal histype. Clearly, this is greater when there is no threat of entry. �12 The third possibility of the bank not learning at all from the observed price has the same effect on entry

as the case of the incumbent being revealed to be the high cost type.

STRATEGIC EXPERIMENTATION 223

The reason for the increased repayment from the incumbent to the bank underthe threat of entry (holding outputs fixed) is that if the incumbent attempts to deceivethe bank, entry is triggered and the profitability of the market subsequently diminished.This reduces the incumbent’s incentives to produce the high cost incumbent’s first periodoutput.

In addition to affecting payoffs for given levels of outputs, potential entry also af-fects the bank’s choice of outputs. Recall that, regarding the flow of information from thefirst to the second period, propositions 2 and 3 demonstrate that first period outputs areused to affect the dissemination of information. Indeed, potential entry has a quantitativeimpact on both the signal dampening and experimentation effects, as well as adding astrategic consideration to experimentation, which affects the probability of entry. Thatis, the possibility of deception when there is potential entry also has an effect on thebank’s structuring of the first period outputs in order to affect the flow of informationfrom the first to the second period.

Recall, from proposition 2, that in order to increase the bank’s first period repay-ments, the bank deviates from the static optimal outputs by moving q and q closer to-gether in order to obtain a less informative price and consequently preserve expectedinformational rents in the second period. Since the threat of entry already has the effectof increasing the first period repayments, the manipulation of first period outputs is lessimportant, so that only smaller deviations from the static outputs are made.

Proposition 7. The threat of entry reduces the signal dampening effect. That is, theincentive to choose outputs closer together is smaller than in the benchmark.

Proof. Since noise is distributed uniformly, the informational effects in the model areall linear. Therefore the magnitude of the coefficient on the probability that the bankbelieves the incumbent has high cost (Pr{ρ2 = 0} in lemma 1) determines the size of theinformational effect. From (10) and (24),∣∣∣∣−δ(c − c )

a − c

2b

∣∣∣∣ >

∣∣∣∣−δ(c − c )a + ce − 2c

3b

∣∣∣∣,so signal dampening is more pronounced when there is no threat of entry. And conse-quently the bank’s incentive to move the outputs of the two types of incumbent closertogether are diminished. �

The intuition for this proposition is straightforward. If the low cost incumbentmimics the high cost incumbent in the first period and successfully deceives the bank,he simultaneously deceives the second firm and triggers entry. Profit and hence theincumbent’s payoffs are lower after entry occurs. Thus, deception is not as rewardingfor the low cost incumbent when there is a threat of entry. Consequently, the bank doesnot have to alter the first period outputs as much in order to lower the value of deceptionand thus to increase the first period repayment of the low cost incumbent. Put anotherway, signal dampening is not as large a concern in the presence of the threat of entry.

224 JAIN ET AL.

We now consider how the dynamics of information transmission affect the firstperiod output via the bank’s future expected payoff.

5.2. Strategic experimentation and entry deterrence

In instances where monopoly power is threatened by potential entry, economic theoryhas long studied strategies that may limit entry. Traditionally, limit pricing has beensuggested to effectively curtail the “amount” of entry in these instances. Limit pricingrefers to an incumbent firm increasing output beyond the myopic first best level in orderto lower the price (or, equivalently, choosing a price below the myopic first best), withthe intent to deter other firms from entering the market. Specifically, the incumbentattempts to signal to potential entrants that entry would not be profitable, due to, forinstance, lower costs of production for the incumbent than for the entrant.

In the present model, the incumbent firm’s incentives have already been accountedfor by the bank in the first period, as is outlined in the previous subsection. Consequently,the incumbent has no incentive to manipulate his output in order to attempt to affect theentrant’s decision. In other words, the incumbent firm simply responds to the contractproposed by the bank.

The bank, on the other hand does not have any private information or any othertype of informational advantage compared to the entrant, so the bank cannot engage in“signaling” of any sort. Nevertheless, the bank, in addition to inducing the incumbent toreveal its type, has an interest in deterring entry, because without entry profit is higherand the bank can extract a greater repayment from the incumbent. Thus, despite the factthat the bank cannot “signal” information to the entrant, the question arises whether thebank uses the first period contract in order to affect the dissemination of information andthus attempt to affect the probability of entry.

From proposition 3 we know that when there is no threat of entry the bank choosesfirst period outputs that increase its second period payoff, that is, the bank experiments.We now consider whether the bank also uses the first period outputs to increase itssecond-period payoff, when it accounts for possible entry, that is, when the bank ac-counts for the strategic interaction with the entrant.

When the bank manipulates the incumbent’s first period outputs in order to learnand, thus, increase its first period payoff, we say that the bank engages in active learningor experimentation. If at the same time this manipulation of the flow of information af-fects the nature of the subsequent game, in this instance whether the incumbent remainsthe only firm in the market, or entry is triggered and firms compete in Cournot fashion,and the bank accounts for this impact of information on the nature of the game, we termthe bank’s actions “strategic experimentation”.

Proposition 8. In determining the first period levels of output, the bank strategicallyexperiments. Specifically, compared to the model without entry, the bank moves theoutputs of the two types of incumbent further apart.

STRATEGIC EXPERIMENTATION 225

Proof. To determine strategic experimentation, one needs to consider the differencebetween the bank’s future expected payoff when there is no threat of entry, given in (9),with the equilibrium expected second period payoff of the model, given in (23). The twoexpected payoff functions differ in the second term in the parentheses. Moreover, sincec � c < a,

−(a + ce − 2c )2

9> −(a − c )2

4,

where the former term is the one arising under the threat of entry. Since the former termis larger, under the threat of entry the bank chooses first period outputs that are moreinformative than without entry (cf. proposition 3). �

By moving the outputs of the two types of incumbent further apart, the bank bothreduces entry and learns more about the incumbent’s type.

We now combine the effects of the propositions on signal dampening and strategicexperimentation. JMS have shown that the signal dampening effect dominates the ex-perimentation effect and thus the first period outputs are set closer together in a dynamicmodel than in the static model. We have shown here in propositions 7 and 8, respec-tively, that the signal dampening effect is weaker and that the strategic experimentationeffect is stronger. Thus we have the following result:

Proposition 9. The first period outputs are set further apart in equilibrium with entrythan without.

This result is significant since it shows that the threat of entry leads the bank tolearn more. The intuition is straightforward: the signal dampening effect is weaker sincethe low cost incumbent has less of an incentive to mimic the high cost incumbent. Atthe same time, information is valuable since the probability of entry goes down as thepotential entrant learns more. Thus, the overall effect of the threat of entry is to increaselearning and thus reduce the probability of entry.13

Notice that the reduction in the probability of entry due to strategic experimenta-tion, is different from traditional limit pricing. Most notably, as stated above, the bankdoes not have superior information that it could signal to the incumbent. However, it alsodiffers in how it manipulates the outputs and hence the price. Specifically, it increasesthe low cost incumbent’s output – just as in traditional limit pricing – but it decreases thehigh costs incumbent’s output relative to the model without the threat of entry. This isdue to the fact that the bank is not only interested in deterring entry but also in gatheringinformation about the incumbent.

13 Here we are not comparing the probability of entry in this model with any other model but simplypointing out that the probability of entry is lower than it would have been if outputs had been chosen tobe closer together.

226 JAIN ET AL.

6. Conclusion and outlook

Although the main focus of the paper is on the informational impact of the threat of entryon the first period contract between the bank and the incumbent firm – specifically thereal implications of signal dampening and strategic experimentation – some additionalinteresting results emerge in the context of our model that are worth repeating.

First, unlike much work in the principal-agent framework, in our setting the prin-cipal and the agent do not have opposing desires, such as the amount of effort that theagent is to exert. Instead, both have an interest in increasing profits of the incumbent– the bank, because the higher the expected profit, the higher the repayment, and theincumbent, because it retains all the profit in excess of the required repayment. In partas a consequence of this, the expected output is always at a “first best” level – at leastfrom the perspective of the bank. Specifically, if the bank knows the incumbent’s typethe first best level of profit is readily obtained, and if there is uncertainty regarding theincumbent’s type, then the expected output is identical to the first best level of output ofthe high cost firm.

Second, if entry occurs after the first period, the resulting interaction is betweena principal and an agent who is participating in a game with a third party (the entrant).In this static setting, the “good” agent is induced to deviate from what would be a “firstbest” action, were there no principal. This is unusual, since absent the game betweenthe agent and the third party, the “good” agent is always induced to the take the first bestaction in any static principal-agent relationship. The reason for this departure from firstbest for the good agent is that the deviations from first best actions for the “bad” agentinfluence the game that is played with the third party. This yields distorted replies of thethird party, provided that he does not know the true type of the agent. Lastly, the “good”type then “first best” responds to the induced distortions in the game.

Third, the possible game outside of the principal agent relationship in the secondperiod yields a discontinuous value function for the bank (the discontinuity occurringwhere beliefs of the entrant just trigger entry). Consequently, the standard theoremsfrom information economics regarding the value of information need not apply. In themodel, the solution to this problem lies in the distributional assumption of noise. Due tothe uniform distribution of the noise term, all informational effects enter linearly into theproblem. Thus, sufficiency of first order conditions on the objective functions are easilyverified, as they are trivially satisfied.14

While these points are primarily of theoretical interest, the model raises some inter-esting economic issues that are worth exploring. We have deliberately chosen to restrictthe bank to contracting only on the observable price, as opposed to allowing menu–based contracts. The reasons for this are manifold, most importantly, however, becauseit focuses the effect informational considerations (signal dampening and strategic exper-imentation) play in the interaction between the bank and the incumbent, when faced withpotential entry. Moreover, we have postulated that the entrant can observe the contracts

14 This issue arises also in [8], where a monopolist who is threatened by entry experiments about marketdemand.

STRATEGIC EXPERIMENTATION 227

between the bank and the incumbent, as opposed to having to infer them. This frame-work (which is in the bank’s interest) dispenses with the multitude of possible equilib-rium outcomes that originate solely on the basis of the entrant’s beliefs, since now thecontract dictates the equilibrium beliefs and not the other way around. Nevertheless,other contractual specifications may be worth exploring in future research.

First, consider the banks optimal first period contract when it cannot be crediblymade public or otherwise be brought to the attention of the potential entrant. In this case,the entrant’s belief function must rely on equilibrium conjectures regarding the contractbetween the bank and the incumbent firm. Consequently, another element is introducedinto the considerations of the bank, namely the attempt to alter the first period outputsin order to “jam” the publicly observable signal, that is, affect the distribution of marketprices to reduce the probability of entry – a fundamentally different (and in this caseadditional) form of strategic experimentation. This issue is discussed in [2].

Second, suppose that the bank indeed chooses to offer a menu of contracts, whichthe potential entrant may or may not observe, in order to elicit the incumbent’s type.15

Then, unlike the signal jamming scenario from above, in the second period the entrantand the bank may have different beliefs about the incumbent’s type, since although theyboth observe the market price and the menu of contracts may very well be public, thebank also observes a (type-revealing) choice of the incumbent firm.

References

[1] N. Jain, Th.D. Jeitschko and L.J. Mirman, Financial intermediation and entry deterrence, MSU Work-ing paper (2002).

[2] N. Jain, Th.D. Jeitschko and L.J. Mirman, Financial contracting, signal-jamming and entry deterence,MSU Working paper (2002).

[3] Th.D. Jeitschko and L.J. Mirman, Information and experimentation in short-term contracting, Eco-nomic Theory 19(2) (2002) 311–331.

[4] Th.D. Jeitschko, L.J. Mirman and E. Salgueiro, The simple analytics of information and experimenta-tion in dynamic agency, Economic Theory 19(3) (2002) 549–570.

[5] J.-J. Laffont and J. Tirole, A Theory of Incentives in Procurement and Regulation (MIT Press, Cam-bridge, 1993).

[6] S. Matthews and L.J. Mirman, Equilibrium limit pricing: The effects of private information and sto-chastic demand, Econometrica 51(4) (1983) 981–996.

[7] R. Milgrom and J. Roberts, Limit pricing under incomplete information, Econometrica 50 (1981) 443–460.

[8] H. Patron, Monopoly experimentation and entry deterrence, Working paper, Emory University, Atlanta,GA (2002).

15 Whether or not this is in the interest of the bank depends not only on the exact contractual optionsavailable to the bank, but also on the parameters of the environment.