Embed Size (px)

Citation preview

214 Int. J. Entrepreneurship and Small Business, Vol. 20, No. 2, 2013

Copyright © 2013 Inderscience Enterprises Ltd.

Strategic control and corporate entrepreneurship: an empirical study

O.L. Kuye Department of Business Administration, University of Lagos, Lagos State, Nigeria E-mail: [email protected]

Abstract: This paper examines the relationship between strategic control and corporate entrepreneurship in the manufacturing industry in Nigeria. A survey research method was used to generate data from a sample of manufacturing firms in Nigerian on strategic control and corporate entrepreneurship variables. Responses from the survey were statistically analysed using descriptive statistics, product moment correlation, regression analysis and Z-test (approximated with the independent sample t-test). The findings of the study show that there is a statistical significant relationship between strategic control and corporate entrepreneurship as well as a significant difference between the entrepreneurship of firms whose strategic control are low and the entrepreneurship of firms whose strategic control are high. These findings have practical applications for manufacturing firms that are attempting to become more entrepreneurial, and will also help researchers to better understand the relationship between strategic control and corporate entrepreneurship.

Keywords: Nigeria; strategic control; corporate entrepreneurship; manufacturing industry.

Reference to this paper should be made as follows: Kuye, O.L. (2013) ‘Strategic control and corporate entrepreneurship: an empirical study’, Int. J. Entrepreneurship and Small Business, Vol. 20, No. 2, pp.214–232.

Biographical notes: O.L. Kuye is an Associate Professor of the Department of Business Administration, University of Lagos, Nigeria. He received his PhD in Business Administration from the University of Lagos, Nigeria. His main areas of research are strategic management and entrepreneurship. His papers have appeared in several journals.

1 Introduction

Increasing globalisation of markets and rapid technological progress has exerted concurrent pressures for manufacturing firms to increase their profits by devoting resources to corporate innovation (Gabrielsson and Politis, 2007). The manufacturing sector is one of the major sources of economic propeller through the production and export contribution (Sangosanya, 2011). It acts as a catalyst to transform the economic structure of countries, from simple, slow-growing and low-value activities to more productive activities that enjoy greater margins, and have higher growth prospects. But its potential benefits are even greater in present times. With rapid technological change

Strategic control and corporate entrepreneurship 215

and far-reaching liberalisation, manufacturing has become the major means for developing countries to benefit from globalisation and bridge the income gap with the industrialised world (Mike, 2010). But the question for the manufacturing sector is how to keep its entrepreneurial spirits and stimulate and foster innovation in phase of uncertainty.

Environmental uncertainty, turbulence, heterogeneity and the quest for sustainable competitive advantage create a host of strategic and operational challenges for today’s organisations. New business conditions require fundamental and constant transformation of the way in which companies function in order to find new paths and sources of sustainable competitive advantage, whose primary support is the development of internal capacity for continuous innovation of products, services, technologies, markets, and processes (Singer et al., 2011). All these have heightened the need for firms to become more entrepreneurial to survive and flourish. It is therefore necessary for managers at all levels to actively participate in designing and implementing a strategy for corporate entrepreneurship actions (Zeqiri, 2010). Thus the imperativeness of strategic control in promoting corporate entrepreneurship cannot be overemphasised.

Strategic control bases performance on strategically relevant criteria which include customer satisfaction, progress on product innovations, and achievement of quality control standards. A well-designed strategic control system will accomplish rewarding employees and firms for incremental but substantive progress on product or process innovation (Hoskisson and Hitt, 1988; Hitt et al., 1996; Li et al., 2009).

This paper appears to be the first comprehensive study on the relationship between strategic control and corporate entrepreneurship in the manufacturing sector in Nigeria. Most studies in this area have been on developed economies. This paper contributes to existing literature by focusing on the manufacturing industry in Nigeria, a developing economy, to ascertain whether there is a relationship between strategic control and corporate entrepreneurship.

1.1 Scope of the study

This paper examines the relationship between strategic control and corporate entrepreneurship in the manufacturing industry in Nigeria. The choice of manufacturing industry was made because of its relevance and potential to Nigeria’s economic development (Kuye and Sulaimon, 2011). Sample was drawn from manufacturing firms in Lagos state. Lagos state was the focus because it is no doubt the commercial heart of Nigeria, with the largest concentration of businesses (Iwugo et al., 2003), and over 55% of manufacturing firms in Nigeria have their head offices located in Lagos state (MAN, 1994; 2003; 2006). Hence, Lagos proffers an attractive place for the study.

2 Literature review

2.1 Strategic control

2.1.1 Concept of strategic control

Management goes beyond the organisation’s internal operations to include the industry and the general environment. The key emphasis, among other things, is on issues related

216 O.L. Kuye

to a system of strategic control (Afsar, 2011). As Goold and Quinn (1990, p.43) put it, strategic control system is described as:

“The process which allows senior management to determine whether a business unit is performing satisfactorily, and which provides motivation for business unit management to see that it continues to do so. It therefore normally involves the agreement of objectives for the business between different levels of management; monitoring of performance against these objectives; and feedback on results achieved, together with incentives and sanctions for business management”.

Singh (2006) defines strategic control as the formal target-setting, measurement, and feedback that allows strategic managers to evaluate whether a firm is achieving superior efficiency, quality, innovation, and customer responsiveness and implementing its strategy successfully.

Strategic control is applied by top management to determine when intervention is required in divisional, middle and lower-level management, the type of interventions necessary, and the role that should be played by senior managers in providing strategic direction (Simons, 1990; Kuye and Oghojafor, 2011). Indeed, Goold and Quinn (1990) advocate three main reasons for establishing a strategic control system which are: to coordinate all planning activities at different levels in the organisation; to motivate managers to seek and achieve the established goals; and to guide top management on when and how to intervene in firm activities and goal performance.

According to Preble (1992), changes in internal and external circumstances require to be monitored on a continuous basis and strategic direction evaluated critically in the light of those changing conditions. Hence, managers have the opportunity to enhance their roles in the strategic management process by legitimising the measurements deployed as strategic control systems and ensure that these systems evolve in a dynamic manner to keep pace with the changing business environment (Solieri, 2000; Kuye and Oghojafor, 2011).

2.1.2 The roles of strategic control

1 Strategic control facilitates an organisational climate with more open reporting of firm data and increased willingness to share sensitive information, which in turn can provide a more constructive alternative to traditional hierarchical control (Gabrielsson and Politis, 2007).

2 Strategic control helps to determine the degree to which strategies fulfil goals and objectives (Dhliwayo and van Vuuren, 2011; Rwigena and Venter, 2004).

3 Goold and Quinn (1993 in Yaacob, 2008) assert that strategic control plays a vital role in making a firm strategy implementation successful. They believe that strategic control helps firms to:

a establish precise and clear plans on what needs to be performed b guide managers to think specifically on what they need to do next in the

subsequent years to reach their stipulated long-term objectives c provide more motivation to managers, so that managers can constantly put

high commitment on strategic plan

Strategic control and corporate entrepreneurship 217

d prevent performance monitoring from focusing too much on yearly financial objectives, so that they do not destroy long-term strategic objectives

e provide early indicator of emerging problem, therefore needing less final inspection

f define job responsibility and expectation more clearly, consequently making empowerment to work better.

These benefits of strategic control system can only be accomplished by focusing on the critical features of strategic control system, specifically periodic strategic review, selection of strategic objectives, setting target achievement level, formal monitoring of strategic target, personal rewards, and central intervention (Ittner and Larcker, 1997).

For a firm to be strategically in-control and achieve its strategic goals, it must establish three broad control conditions with respect to their strategy (Solieri, 2000; Fiegner, 1990):

• Strategic direction: Maintaining the dynamic alignment of strategies. The establishment and maintenance of controls and control systems that are sufficiently broad and reactive to changes in the strategy deployed and that strategy’s underlying objectives to attain a dynamic alignment in real-time.

• Strategic effectiveness: Make certain that the strategies that are formulated are potentially effective and they remain effective over time. The establishment and maintenance of controls that generate effective strategies, challenge existing and proposed strategies and their underlying assumptions on a continuous basis to provide feedback and feed-forward information on adjustments needed to the strategy in real-time.

• Strategic integration: Ensure that strategy implementation is carried out in an integrated manner throughout the firm. Controls are established and maintained to make sure that all elements of the organisation display an adequate level of strategic harmony and that these controls are internally consistent with operational and tactical controls at all levels.

2.1.3 Framework and model of strategic control

Simons (1995) has developed a framework for strategic control which is based on four control levers that are put together as they are working simultaneously even though for different purposes (Tuomela, 2005):

1 Beliefs systems are used to enhance core values related to business strategy and to encourage search for new opportunities in accordance with these values. It is an explicit et of organisational meanings that senior managers communicate formally and emphasise systematically to provide basic values, purposes, and direction of the organisations. It is argued that these can motivate people to search for new ways to create values (Chau and Witcher, 2005; Simons, 1995).

2 Boundary systems lessen risks by setting limits to strategically undesirable behaviours. They are regulations and sanction that restrict search. The most crucial are those that impose codes of business conduct (Chau and Witcher, 2005).

218 O.L. Kuye

3 Diagnostic control systems ensure the communication and monitoring of critical success factors. They are the formal informational systems that managers use to monitor firms’ performance and correct deviations from standards (Chau and Witcher, 2005).

4 Interactive control systems are used to discuss strategic uncertainties and to learn new strategic responses to a changing environment. They are formal informational systems that managers employ to involve themselves frequently and personally in the decision activities of subordinates (Chau and Witcher, 2005).

While beliefs systems and interactive control systems are used to promote innovative behaviour, boundary systems and diagnostic control systems are used to make sure that people behave according to pre-established standards and plans. Hence, the essence of this strategic control framework is that it balances needs for innovation and constraints (Simons, 1995; Tuomela, 2005).

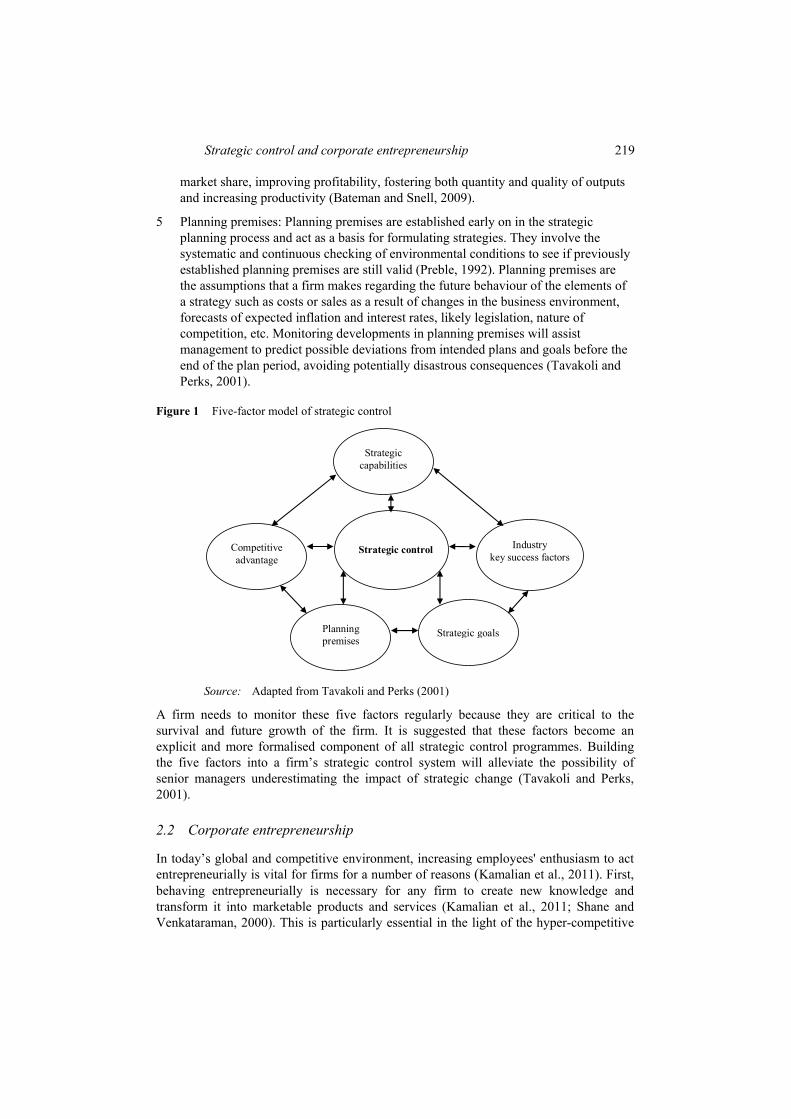

Tavakoli and Perks (2001) develop a five-factor model of strategic control (see Figure 1) which in their view will assist managers in assessing, anticipating and responding to changes in industry structures and competitive forces:

1 Competitive advantage factors: Competitive advantage factors are the features and benefits that customers experience and value. A competitive advantage arises when the firm is able to deliver the same benefits as competitors but at a lower cost (cost advantage), or deliver benefits that exceed those of competing products (differentiation advantage) (Wang et al., 2011).To sustain their positions, industry leaders need to continuously monitor the variables that promote their competitive posture. Firms need to monitor how they are performing in the context of their competitive advantage factors. In other words, on whatever basis a firm chooses to compete in its industry and gain superiority over its immediate competitors, whether via differentiation, cost–price superiority, or speed of response, it must ensure that the competitive advantage is sustained. The drivers of competitive advantage should form the control components (Tavakoli and Perks, 2001).

2 Strategic capabilities: Strategic capabilities are the skills and accumulated knowledge that allow firms to deploy their assets and coordinate their activities (Raymond et al., 2010; Desarbo et al., 2005). In other words, strategic capabilities are internal to the firm. They are the skills and resources that support a firm’s competitive advantage. They are part of the processes and assets that deliver the features and benefit that customers experience and value (Tavakoli and Perks, 2001).

3 Industry key success factors: Key success factors are a set of capabilities and assets that, at the very least, ensure survival or average performance for a firm in its industry (Tavakoli and Perks, 2001). They are events, circumstances, conditions or actions that require special attention from a company (Dickinson et al., 1984). The main idea of the key success factors is the identification, assessment, and analysis of these key areas in order to make specific steps to ensure a firm’s success (Auruskeviciene et al., 2007).

4 Strategic goals: Strategic goals are end results that relate to the long-term survival, values, and growth of the firm. They reflect both effectiveness and efficiency and are usually established by top level managers. Strategic goals include growth, increasing

Strategic control and corporate entrepreneurship 219

market share, improving profitability, fostering both quantity and quality of outputs and increasing productivity (Bateman and Snell, 2009).

5 Planning premises: Planning premises are established early on in the strategic planning process and act as a basis for formulating strategies. They involve the systematic and continuous checking of environmental conditions to see if previously established planning premises are still valid (Preble, 1992). Planning premises are the assumptions that a firm makes regarding the future behaviour of the elements of a strategy such as costs or sales as a result of changes in the business environment, forecasts of expected inflation and interest rates, likely legislation, nature of competition, etc. Monitoring developments in planning premises will assist management to predict possible deviations from intended plans and goals before the end of the plan period, avoiding potentially disastrous consequences (Tavakoli and Perks, 2001).

Figure 1 Five-factor model of strategic control

Strategic capabilities

Competitive advantage

Strategic control Industry

key success factors

Planning premises

Strategic goals

Source: Adapted from Tavakoli and Perks (2001)

A firm needs to monitor these five factors regularly because they are critical to the survival and future growth of the firm. It is suggested that these factors become an explicit and more formalised component of all strategic control programmes. Building the five factors into a firm’s strategic control system will alleviate the possibility of senior managers underestimating the impact of strategic change (Tavakoli and Perks, 2001).

2.2 Corporate entrepreneurship

In today’s global and competitive environment, increasing employees' enthusiasm to act entrepreneurially is vital for firms for a number of reasons (Kamalian et al., 2011). First, behaving entrepreneurially is necessary for any firm to create new knowledge and transform it into marketable products and services (Kamalian et al., 2011; Shane and Venkataraman, 2000). This is particularly essential in the light of the hyper-competitive

220 O.L. Kuye

landscape that many firms have to deal with in the 21st century (Kamalian et al., 2011). Second, for firms to respond to certain environmental conditions such as hostility and dynamism, they must pursue an entrepreneurial strategic posture and engage in corporate entrepreneurship (Covin and Slevin, 1989; Ireland and Hitt, 1999; Kamalian et al., 2011). Third, an entrepreneurial mindset of employees allows for recognition of new, uncertain, and high potential business opportunities which the firm may fail to spot otherwise (McGrath and MacMillan, 2000; Kamalian et al., 2011).

It is widely accepted that entrepreneurship contributes to development, with a positive impact on society, creating employment, economic expansion, a larger tax base, and more consumer well-being (Dana, 2000). The efficacy of the entrepreneur (Dibie and Okonkwo, 2000) and indeed, a healthy entrepreneurship sector is paramount in the drive for economic development of a nation (Dana, 2000; Kuye, 2008).

Entrepreneurship can be defined as the process by which individuals, spurred by the desire for personal satisfaction or some rewards, act differently by adding value to an already existing venture or create an entirely new one not minding the risk involved (Kuye, 2008).

Abilities of adaptation, creativity, flexibility, aggressiveness, speed and innovativeness are the features of entrepreneurial activity, which must be applied at the individual, organisational and societal level, as the response to the increasing level of uncertainty and complexity of the environment we live in (Gibb, 2000; Singer et al., 2011).

Whereas entrepreneurship is primarily regarded as an individual pursuit and in relation to start-up entrepreneurs (Thornberry, 2001), corporate entrepreneurship is viewed as acting entrepreneurially within the boundaries of an established firm (Kenney and Mujtaba, 2007; Kuye et al., 2012).

Kanter (1984) describes corporate entrepreneurship as that which relates to how firm stimulates innovation, enterprise, and initiative from people in the organisation, and the subsequent contribution of individual behaviour to firm success. Corporate entrepreneurship embodies renewal activities that enhance a firm’s ability to compete and take risks, which may or may not involve the addition of new businesses to a firm (Phan et al., 2009; Kuye et al., 2012).

2.2.1 Underlying dimensions of entrepreneurial orientation

Most studies have supported Covin and Slevin’s (1988, 1989) findings that the entrepreneurial orientation has three dimensions: innovativeness, proactiveness, and risk-taking. Focus have been on these three dimensions in the large majority of conceptual and empirical research studies (Morris et al., 2006). Thus, the imperativeness to consider the issues that will likely enhance a firm’s entrepreneurial orientation, as enunciated by Dess and Lumpkin (2005) (see Table 1).

Scholars have suggested that the pursuit of corporate entrepreneurship requires established organisations to strike a balance between engaging in activities that make use of existing knowledge, while at the same time challenging themselves to embark upon new adventures, seeking new knowledge and opportunities to rejuvenate themselves (Hannan and Freeman, 1989; Floyd and Woolridge, 1999; Lassen, 2007). Indeed, successful entrepreneurial ventures are the ones that meet a previously neglected or unforeseen need or do something better than it was done before (UNDP, 1999). Firms that have developed entrepreneurial capabilities are the ones who can sustain growth and

Strategic control and corporate entrepreneurship 221

innovation, which are critical competitive advantages in the 21st century (Scheepers et al., 2008). Table 1 Issues to consider in enhancing a firm’s entrepreneurial orientation

Innovativeness

• Does your firm support and stimulate technological, product-market, and administrative innovation?

• How does your firm encourage creativity and experimentation?

• Does your firm properly invest in new technology, R&D, and continuous improvement?

• Are your firm’s innovative initiatives hard for competitors to successfully imitate?

• Does your firm ‘safeguard’ investments in R&D during difficult economic periods or are they generally the first area where significant cuts are made?

Proactiveness

• Does your firm constantly monitor trends and identify future needs of customers and/or anticipate future demand conditions?

• Does your firm strive to be a ‘first mover’ to capture the benefits of being an industry pioneer?

• Is your firm aware of the downside of being a first mover, such as customer resistance to novel ideas and bearing the costs associated with unforeseen technological problems?

• Does your firm effectively use the following methods to act proactively: introducing new products and technologies ahead of the competition and continuously seeking out new product or service offerings?

Risk–taking

• Does your firm promote and encourage a proper level of business, financial, and personal risktaking?

• Does your firm enhance its competitive risk position by researching and assessing risk factors in order to minimize uncertainty?

• Does your firm enhance its competitive risk position by applying techniques and processes that have worked in other domains?

• Overall, does your firm carefully manage risks and avoid taking actions without sufficient forethought, research and planning?

Source: Adapted from Dess and Lumpkin (2005)

2.3 The link between strategic controls and corporate entrepreneurship

The findings of Barringer and Bluedorn (1999) confirm the notion that strategic controls are capable of rewarding creativity and the pursuit of opportunity via innovation which are an important part of the entrepreneurial process. According to Gabrielsson and Politis (2007), strategic controls are more capable of facilitating innovation and creativity and can be expected to be more consistent with supporting entrepreneurial processes. Unlike the common view that strategic control is inconsistent with entrepreneurship, it actually facilitates it (Morris et al., 2008).

Conversely, the results of the study by Dhliwayo and van Vuuren (2011) show that businesses that practice strategic controls do not necessarily show high levels of entrepreneurial orientation. This is consistent with the findings of Li et al. (2009) which suggest that strategic control does not positively influence corporate entrepreneurship.

222 O.L. Kuye

Also, for conservative firms, strategic controls are less important. Conservative firms do not gain their competitive advantage by pursuing opportunities through innovation. There are costs involved in maintaining strategic controls in terms of managerial time and effort (Goold and Quinn, 1990; Hayes and Abernathy, 1980) which conservative firms may find unnecessary. In view of this discussion, the following hypotheses are proposed:

H1 There is no significant relationship between strategic control and corporate entrepreneurship.

H2 Strategic control has no significant impact on corporate entrepreneurship.

H3 There is no significant difference between the entrepreneurship of firms whose strategic control are high and the entrepreneurship of firms whose strategic control are low.

3 Methodology

The relationships that exist between strategic control and corporate entrepreneurship was examined. A cross-sectional survey design was used in the study. The use of survey research method is justified since it follows a correlational research strategy and helps in predicting behaviour (Bordens and Abbott, 2002). It also helps to ascertain whether or not a relationship exists between the variables of study (Kerlinger, 1973). Responses were sought from manufacturing firms on a wide range of issues concerning strategic control and corporate entrepreneurship.

The study population consisted of manufacturing firms in Nigeria. Since 55.2% of Nigeria’s 2,250 manufacturing firms are based in Lagos state (MAN, 1994, 2003), Lagos was considered a good representation of manufacturing firms in Nigeria. Therefore, the population sample was taken from Lagos state. With the help of field research assistants, the questionnaire was administered on the manufacturing firms.

Manufacturing firms in Lagos state constitute the sample frame which is a representative subset of the population from which the sample was drawn. A senior manager or chief executive officer (CEO) of every selected firm was approached and persuaded to fill the questionnaire. The manufacturing firms which did not participate were uninterested and unwilling to divulge information. Some adduced reasons such as management policy and suspicion to justify there lack of cooperation.

Simple random sampling technique was used in selecting the participating firms. A total of 740 copies of the questionnaire were administered on the firms but 670 were completed and returned. This represents 90.54% response rate. According to Saunders et al. (2003), sampling is a part of the entire population carefully selected to represent that population. The justification for using random sampling technique is that it eliminates the likelihood that the sample is biased by the preference of the individual selecting the sample (Bordens and Abbott, 2002). Another justification is that it is particularly essential when one wants to apply research findings directly to a population (Mook, 1983).

The participating manufacturing firms constituted the units of analysis. The administration of the questionnaire was done on one senior manager or CEO at each firm surveyed. The use of primary data method is justified since according to (Cowton, 1998), it is the quickest and simplest of the tools to use, if publication is the objective.

Strategic control and corporate entrepreneurship 223

4 Empirical results

4.1 Empirical results

4.1.1 Strategic control

Concerning strategic control, a five-point Likert scale involving three items developed by Barringer and Bluedorn (1999) was adapted. The scale ranging from “not important” to “very important” was applied to assess a firm’s emphasis on strategic control. Respondents’ rating on all the items were summed up and averaged to obtain a strategic controls index. Strategic control index is classified high when the index is equal to or greater than 4.0 and low when it is lower than 4.0. A reliability score of 0.91 was obtained from the Cronbach’s alpha test using the adapted scale from Barringer and Bluedorn (1999).

4.1.2 Corporate entrepreneurship

For corporate entrepreneurship, a five-point Likert scale of fifteen items was adapted from Miller (1983); Morris and Kuratko (2002); and Ireland et al. (2006). The scale ranging from “strongly disagree to strongly agree”, and “significantly less to significantly more” was applied to measure a firm’s tendency towards (innovation, risk-taking and proactiveness) entrepreneurship. The scores on the fifteen items were summed up and averaged to determine an index of entrepreneurship. An index of less than 4.0 was considered as low entrepreneurship while an index of 4.0 and above was considered as high entrepreneurship. The scale had a reliability score of 0.89 generated from Cronbach’s alpha test).

4.2 Analytical tools and hypotheses tests and results

In order to obtain useful meaning from the data and examine the propositions of this study, data from the survey were analysed using statistical package for social sciences (SPSS) as well as the following descriptive and inferential statistical techniques:

The use of descriptive statistics such as mean, percentages and frequencies in the study was to measure demographic characteristics of respondents, to answer research questions relating to strategic control and corporate entrepreneurship. They are not meant to test a formal research hypothesis, but rather the summaries from a sample that characterise that sample (Simon, 2002). In the view of Kerlinger (1973), studying sets of numbers in their present state is cumbersome; thus, it is essential to reduce the sets in two ways: calculating the averages and calculating the measures of variability.

Product-moment correlation was used to examine the existence of relationship between strategic control and corporate entrepreneurship.

Regression analysis was used to establish the amount of variations in the dependent variable which can be associated with changes in the value of an independent or predictor variable in the absence of other variables.

Z-test (approximated with the independent sample t-test in the SPSS package) was used to test the hypothesised relationship as stated in null hypothesis 3. In view of the fact that the data were collected on a rating scale which is ‘presumed to be interval scale’, this parametric test is considered appropriate (Emory and Cooper, 1991). Also, going by the central limit theorem,

224 O.L. Kuye

“for sufficiently large samples (n = 30), the sample mean will be distributed around the population mean approximately in a normal distribution. Even if the population is not normally distributed, the distribution of sample mean will be normal if there is a large enough set of samples” (Cooper and Schindler, 2001).

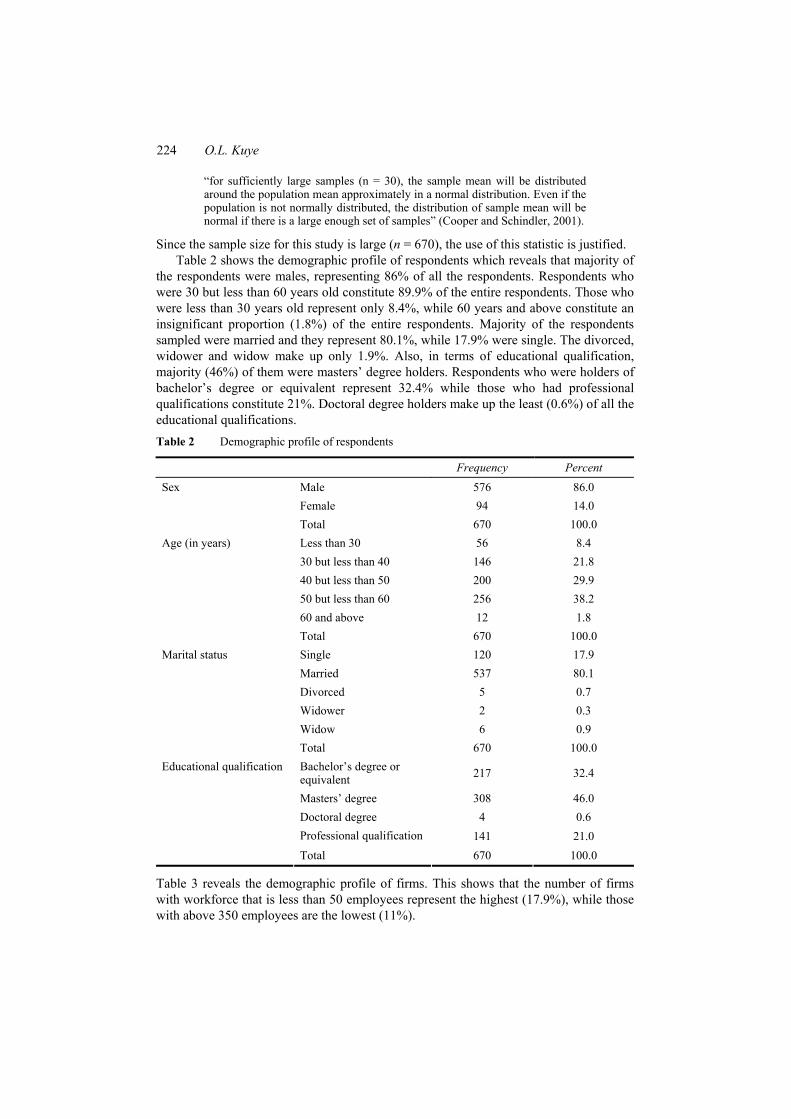

Since the sample size for this study is large (n = 670), the use of this statistic is justified. Table 2 shows the demographic profile of respondents which reveals that majority of

the respondents were males, representing 86% of all the respondents. Respondents who were 30 but less than 60 years old constitute 89.9% of the entire respondents. Those who were less than 30 years old represent only 8.4%, while 60 years and above constitute an insignificant proportion (1.8%) of the entire respondents. Majority of the respondents sampled were married and they represent 80.1%, while 17.9% were single. The divorced, widower and widow make up only 1.9%. Also, in terms of educational qualification, majority (46%) of them were masters’ degree holders. Respondents who were holders of bachelor’s degree or equivalent represent 32.4% while those who had professional qualifications constitute 21%. Doctoral degree holders make up the least (0.6%) of all the educational qualifications. Table 2 Demographic profile of respondents

Frequency Percent Male 576 86.0 Female 94 14.0

Sex

Total 670 100.0 Less than 30 56 8.4 30 but less than 40 146 21.8 40 but less than 50 200 29.9 50 but less than 60 256 38.2 60 and above 12 1.8

Age (in years)

Total 670 100.0 Single 120 17.9 Married 537 80.1 Divorced 5 0.7 Widower 2 0.3 Widow 6 0.9

Marital status

Total 670 100.0 Bachelor’s degree or equivalent 217 32.4

Masters’ degree 308 46.0 Doctoral degree 4 0.6 Professional qualification 141 21.0

Educational qualification

Total 670 100.0

Table 3 reveals the demographic profile of firms. This shows that the number of firms with workforce that is less than 50 employees represent the highest (17.9%), while those with above 350 employees are the lowest (11%).

Strategic control and corporate entrepreneurship 225

Table 3 Demographic profile of firms

Frequency Percent

Fewer than 50 120 17.9 50–100 110 16.4 101–150 102 15.2 151–200 98 14.6 201–250 89 13.3 251–350 77 11.5 Above 350 74 11.0

Number of employees

Total 670 100.0 Less than 5 16 2.4 5 but less than 20 198 29.6 20 but less than 30 206 30.7 30 years and above 250 37.3

Age of organisation (in years)

Total 670 100.0

In terms of the age of the firms, those who are 30 years and above constitute the highest (37.3%). Organisations that are less than 5 years old constitute only 2.4% of the entire participating firms.

4.2.1 Mean indices, correlation coefficient, regression analysis and independent samples test

Table 4 Mean index of strategic control

Strategic control indicators Frequency Average weight

Formal face-to-face meetings between top managers and business unit or functional area personnel in meeting predetermined objectives

670 4.04

Informal face-to-face meetings between top managers and business unit or functional area personnel in meeting predetermined objectives

670 3.70

Measuring performance against subjective strategic criteria, such as improvements in customer satisfaction or progress on product innovations in meeting predetermined objectives

670 4.12

Mean of means 3.95

With respect to strategic control and corporate entrepreneurship, the mean index of participating firms were 3.95 and 3.79 respectively (see Tables 4 and 5).

H1 was tested through correlations coefficients test. Pearson’s product moment correlations coefficient (0.722**) indicates that strategic control and corporate entrepreneurship are significantly and positively correlated with each other at 0.01 level of significance. Therefore, the null hypothesis of no significant relationship is rejected. Hence, there is a significant relationship between strategic control and corporate entrepreneurship.

226 O.L. Kuye

Table 5 Mean index of corporate entrepreneurship

Corporate entrepreneurship indicators Frequency Average weight

High rate of new product/service introduction, compared to competitors

670 3.72

Emphasis on continuous improvement in methods of production and/or service delivery

670 4.17

Risk-taking by key executives in seizing and exploring growth opportunities

670 3.83

A very competitive ‘undo-the-competitor’ posture 670 3.53

Seeking of unusual, novel solutions by senior executives to problems, via the use of “idea people”,

670 3.39

A strong emphasis on R&D, technological leadership, andinnovation;

670 3.85

A bold, aggressive posture, in order to maximize the probability of exploiting potential when faced with uncertainty

670 3.75

Active search for big opportunities 670 4.12

Rapid growth as the dominant goal; 670 3.90

Large, bold decisions, despite uncertainties of the outcome 670 3.53

Steady growth and stability as primary concerns 670 4.23

Number of new products introduced during the past five years 670 3.72

Number of product improvement or revisions introduced during the past five years

670 3.82

Comparison of new product introductions with those of major competitors

670 3.54

Level of significance of new methods or operational processes implemented during the past five years

670 3.81

Mean of means 3.79

H2 was tested through a regression analysis. The results of the regression analysis of the relationship between strategic control and corporate entrepreneurship are shown in Table 6. Table 6(b) above shows that the analysis of variance of the fitted regression equation is significant with F value of 728.131. This is an indication that the model is a good one. Since the p-value is less than 0.05, it shows a statistically significant relationship between the variables at 95% confidence level. Therefore, the null hypothesis of no significant impact is rejected. This shows that strategic control has a significant impact on corporate entrepreneurship.

The R2 statistic in Table 6(a) indicates that the model as fitted explains 52.2% of the total variability in corporate entrepreneurship. In other words, 52.2% of the total variability in corporate entrepreneurship can be explained by strategic control. The value of R2 = 0.522 shows that strategic control is a good predictor of corporate entrepreneurship.

The standardised coefficients (Beta) value in Table 6(c) reveals that the independent variable is statistically significant at 0.05 significant level.

Strategic control and corporate entrepreneurship 227

Table 6 Regression analysis of strategic control and corporate entrepreneurship

(a) Model summary

Model R R square Adjusted R square Std. error of the estimate

.722 .522 .521 7.087

(b) ANOVA

Model Sum of squares Mean square F Sig.

Regression 36,575.557 1 36,575.557 728.131 .000 Residual 33,555.069 668 50.232 Total 70,130.627 669

(c) Coefficients

Model Unstandardised coefficients Standardised coefficients Sig. B Std. error Beta t P

(Constant) 17.427 1.489 11,707 .000 Strategic

control 3.330 .123 .722 26.984 .000

Notes: Dependent variable: corporate entrepreneurship p < 0.05

Table 7 Independent samples test on entrepreneurship of firms with high strategic control and entrepreneurship of firms with low strategic control

(a) Group statistics

Strategic control N Mean Std. deviation Std. error mean Corporate entrepreneurship Low 244 3.3080 .85441 0.05470

High 426 4.0728 .32245 0.01562

(b) Independent samples test

t-test for equality of means

95% confidence interval of the difference

t df Sig.

(2-tailed)Mean

differenceLower Upper

Corporate entrepreneurship –16.538 668 .000 –.76474 –0.85553 –0.67394

H3 was tested using independent samples test. The results of the independent sample t-test as revealed in Table 7(a) show that entrepreneurship mean index (4.07) of firms with high strategic control is different from the entrepreneurship mean index (3.30) of firms with low strategic control. This difference between the two mean was found to be statistically significant at p < .05 [Table 7(b)]. Therefore, the null hypothesis of no significant difference is rejected. Thus, there is a significant difference between the

228 O.L. Kuye

entrepreneurship of firms whose strategic control are high and the entrepreneurship of firms whose strategic control are low.

5 Conclusions and implications for management

In present times, manufacturing remains one of the most critical engines for economic growth. It acts as a catalyst to transform the economic structure of countries. However, the success of firms in performing these roles is partly a function of strategic control. Firms need to understand the consequences of strategic control so as to adopt it to become competitive and more entrepreneurial.

The results of the study revealed that on the average, participating firms scored low in strategic control. The low involvement was probably because the firms were unwilling or lack the capacity to constantly monitor their strategies to see whether the strategies were effective or not. This implies the possibility of the firms not being critical about strategic control, and unwilling to keep pace with the changing business environment and demands of the strategy implementation process. The involvement of participating firms in entrepreneurship was also found to be low. This implies that the firms were perhaps conservative, unwilling to take risk and commit a lot of resources to foster innovativeness and proactiveness.

The findings of this study revealed a positive and statistically significant relationship between strategic controls and entrepreneurship. This is also consistent with the findings of Barringer and Bluedorn (1999) which confirms the notion that control systems capable of rewarding creativity and the pursuit of opportunity via innovation are an important part of the entrepreneurial process. The findings also indicated that firms with high strategic control are more entrepreneurial and outperform firms with low strategic control.

This study provides important implications for the management of manufacturing organisations. In order to promote and improve corporate entrepreneurship, manufacturing firms need to demonstrate high level of commitment to strategic controls. This study can also help researchers to better understand the relationship between strategic control and corporate entrepreneurship in the manufacturing industry in Nigeria. Hence, if the manufacturing sector must survive, grow and be competitive, its managers should encourage increased involvement in strategic controls activities.

5.1 Limitations and future research direction

Limitations of this study should be recognised. First, this paper does not offer the sufficient diversity required to enable generalisation. This study focused on the manufacturing sector. Rather than this restriction, future studies may need to expand to cover the service industry.

Second, future study should also take cognisance of the analysis of firm size, firm age, and their impact on strategic controls. These might be relevant and imperative in making policy decisions for the firm.

Third, future research to examine the effect of corporate entrepreneurship on strategic control might also be considered.

Strategic control and corporate entrepreneurship 229

Finally, the sample was taken from Lagos State, Nigeria. This limits the generalisation of the findings. Hence, the suggestion that future research should extend the study to cover the entire country.

References Afsar, B (2011) ‘Strategic management in today’s complex world’, Business Intelligence Journal,

Vol. 4, No. 1, pp.143–149. Auruskeviciene, V., Salciuviene, L., Kuvykaite, R. and Zilys, L. (2007) ‘Identification of key

success factors in free economic zone development in Lithuania’, Economics and Management, Vol. 12, pp.277–284.

Barringer, B.R. and Bluedorn, A.C. (1999) ‘The relationship between corporate entrepreneurship and strategic management’, Strategic Management Journal, Vol. 20, No. 5, pp.421–444.

Bateman, T.S. and Snell, S.A. (2009) Management: Leading and Collaborating in the Competitive World (8th Ed), McGraw-Hill/Irwin, New York, NY.

Bordens, S.K and Abbott, B.B. (2002) Research Design and Methods: A Process Approach (5th ed.), McGraw-Hill, New York.

Chau, V.S. and Witcher, B.J. (2005) ‘Implications of regulation policy incentives for strategic control: an integrative model’, Annals of Cooperative Economics, Vol. 76, No. 1, pp.85–119.

Cooper, D.R. and Schindler, P.S. (2001) Business Research Methods (7th ed), McGraw-Hill companies, New York.

Covin, J.G. and Slevin, D.P. (1988) ‘The influence of organisation structure on the utility of an entrepreneurial top management style’, Journal of Management Studies, Vol. 25, No. 3, pp.217–234.

Covin, J.G. and Slevin, D.P. (1989) ‘Strategic management of small firms in hostile and benign environments’, Strategic Management Journal, Vol. 10, No. 1, pp.75–87.

Cowton, C.J. (1998) ‘The use of secondary data in business ethics research’, Journal of Business Ethics, Vol. 17, No. 4, pp.423–434.

Dana, L.P. (2000) ‘Economic sectors in Egypt and their managerial implications’, Journal of African Business, Vol. 1, No. 1, pp.65–81.

Desarbo, W.S., Di Benedetto, C.A., Song, M. and Sinha, I. (2005) ‘Revisiting the miles and snow strategic framework: uncovering interrelationships between strategic types, capabilities, environmental uncertainty and firm performance’, Strategic Management Journal, Vol. 26, No. 1, pp.47–74.

Dess, G.G. and Lumpkin, G.T. (2005) ‘The Role of entrepreneurial orientation in stimulating effective corporate entrepreneurship’, Academy of Management Executive, Vol. 19, No. 1, pp.147–156.

Dhliwayo, S. and van Vuuren, J. (2011) ‘the relationship between strategic planning and entrepreneurship: a paradox’, Asian Journal of Business and Management, Vol. 1, No. 3, pp.23–33.

Dibie, R. and Okonkwo, P. (2000) ‘Aligning private business development and economic growth in Nigeria’, Journal of African Business, Vol. 1, No. 1, pp.83–111.

Dickinson, R., Ferguson, C.R. and Sircar, S. (1984) ‘CSFs and small business’, American Journal of Small Business, Vol. 8, No. 3, pp.49–58.

Emory, C.W. and Cooper, D.R. (1991) Business Research Methods (4th Ed.), Richard D. Irwin Inc., Illinois.

Fiegener, M.K. (1990) Towards a Descriptive Theory of Strategic Control, UMI Dissertation Services, Michigan, A Bell and Howell Company.

230 O.L. Kuye

Floyd, S.W. and Woolridge, B. (1999) ‘Knowledge creation and social networks in corporate entrepreneurship: the renewal of organizational capability’, Entrepreneurship: Theory and Practice, Vol. 23, No. 3, pp.123–144.

Gabrielsson, J. and Politis, D. (2007) ‘Board control and corporate innovation: an empirical study of small technology-based firms’, Paper no. 2006/07, LUND University.

Gibb, A.A. (2000) ‘Corporate restructuring and entrepreneurship: What can large organisations learn from small?’, Entrepreneurship and Innovation Management Studies, Vol. 1, No. 1, pp.19–35, DOI: 10.1080/146324400363509.

Goold, M. and Quinn, J. (1990) ‘The paradox of strategic controls’, Strategic Management Journal, Vol. 11, No. 1, pp.43–57.

Goold, M. and Quinn, J. (1993) Strategic Control: Establishing Milestones for Long-term Performance, Addison-Wesley, Reading, MA.

Hannan, M. and Freeman, J. (1989) Organizational Ecology, Harvard University Press, Cambridge, MA.

Hayes, R.H. and Abernathy, W.J. (1980) ‘Managing our way to economic decline'’, Harvard Business Review, Vol. 58, No. 4, pp.67–77.

Hitt, M.A., Hoskisson, R.E., and Moesel, D.D. (1996) ‘The market for corporate control and firm innovation’, Academy of Management Journal, Vol. 39, No. 5, pp.1084–1119.

Hoskisson, R.E. and Hitt, M.A. (1988) ‘Strategic control systems and relative R&D investment in large multiproudct firms’, Strategic Management Journal, Vol. 9, No. 6, pp.605–621.

Ireland, R.D. and Hitt, M.A. (1999) ‘Achieving and maintaining strategic competitiveness in the 21st century: the role of strategic leadership’, Academy of Management Executive, Vol. 19, No. 4, pp.63–77.

Ireland, R.D., Kuratko, D.F. and Moris, M.H. (2006) ‘A health audit for corporate entrepreneurship: innovation at all levels: Part II’, Journal of Business Strategy, Vol. 27, No. 2, pp.21–29.

Ittner, C.D. and Larcker, D.F. (1997) ‘Quality strategy, strategic control systems and organisational performance’, Accounting, Organisations and Society, Vol. 22, Nos. 3/4, pp.395–314.

Iwugo, K.O., D’Arcy and Andoh, R. (2003) ‘Aspects of land-based pollution of an African Coastal Megacity of Lagos’, Diffuse Pollution Conference, Dublin.

Kamalian, A., Yaghoubi, N. and Poori, M. (2011) ‘Emotional intelligence and corporate entrepreneurship: an empirical study’, Journal of Basic and Applied Scientific Research, Vol. 1, No. 6, pp.471–478.

Kanter, R.M. (1984) The Change Masters, Simon and Schuster, NY. Kenney, M. and Mujtaba, B.G. (2007) ‘Understanding corporate entrepreneurship and

development: a practitioner view of organisational intrapreneurship’, Journal of Applied Management and Entrepreneurship, Vol. 12, No. 3, pp.73–88.

Kerlinger, F.N. (1973) Foundations of Behavioural Research, Holt, Rinehart and Winston, Inc., New York.

Kuye, O.L. (2008) ‘Entrepreneurship, strategic management practices and firms’ performance in manufacturing firms in Nigeria’, unpublished Doctoral Degree Theses, University of Lagos.

Kuye, O.L. and Oghojafor, B.E.A. (2011) ‘Strategic control and corporate performance in the manufacturing industry: evidence from Nigeria’, European Journal of Social Science, Vol. 22, No. 2, pp.177–187.

Kuye, O.L. and Sulaimon, A.A. (2011) ‘Employee involvement in decision making and firms’ performance in the manufacturing sector in Nigeria’, Serbian Journal of Management, Vol. 6, No. 1, pp.1–15.

Kuye, O.L., Oghojafor, B.EA. and Sulaimon, A.A. (2012) ‘Planning flexibility and corporate entrepreneurship in the manufacturing sector in Nigeria’, International Journal of Business Excellence, Vol. 5, No. 4, pp.323–337.

Strategic control and corporate entrepreneurship 231

Lassen, A.H (2007) ‘Corporate entrepreneurship: an empirical study of the importance of strategic considerations in the creation of radical innovation’, Managing Global Transitions, Vol. 5, No. 2, pp.109–139.

Li, L., Tse, E.C. and Zhao, J. (2009) ‘An empirical study of corporate entrepreneurshipin hospitality companies’, International Journal of Hospitality and Tourism Administration, Vol. 10, No. 3, pp.213–231.

MAN (1994) ‘Nigeria industrial directory’, Manufacturing Association of Nigeria. MAN (2003) ‘Nigerian business directory: under the auspices of the commonwealth heads of

government meeting’, Manufacturing Association of Nigeria. MAN (2006) ‘Manufacturing Association of Nigeria’, MAN Economic Review 2003–2006, Vol. 28. McGrath, R.G. and MacMillan, I.C. (2000) The Entrepreneurial Mindset, Harvard Business School

Press, MA. Mike, J.A. (2010) ‘The structure of the Nigerian manufacturing industry’, The National Workshop

on Strenghtening Innovation & Capacity Building in the Nigerian Manufacturing Sector, [online] http://www.uneca.org/istd/documents/NigeriaManufacturing (accessed on 10 December 2010).

Miller, D. (1983) ‘The correlates of entrepreneurship in three types of firms’, Management Science, Vol. 29, No. 3, pp.770–791.

Mook, D.G. (1983) ‘In defence of external validity’, American Psychologist, Vol. 38, No. 4, pp.379–387.

Morris M.H. and Kuratko, D.E. (2002) Corporate Entrepreneurship, Harcourt College Publishers, Florida.

Morris, M.H., Allen, J., Schindehutte, M. and Avila, R. (2006) ‘Balanced management control systems as a mechanism for achieving corporate entrepreneurship’, Journal of Managerial Issues, Vol. 18, No. 4, pp.468–493.

Morris, M.H., Kuratko, D.F. and Covin, J.G. (2008) Corporate Entrepreneurship: Entrepreneurial Development within Organisations (2nd Ed), Thompson South Western, London.

Phan, P.H., Wright, M., Ucbasaran, D. and Tan, W. (2009) ‘Corporate entrepreneurship: current research and future directions’, Journal of Business Venturing, Vol. 24, No. 3, pp.197–205.

Preble, J.F. (1992) ‘Towards a comprehensive system of strategic control’, Journal of Management Studies, Vol. 29, No. 4, pp.391–409.

Raymond, I., St-pierre, J., Fabi, B. and Lacoursière, R. (2010) ‘Strategic capabilities for the growth of manufacturing smes: a configurational perspective’, Journal of Developmental Entrepreneurship, Vol. 15, No. 2, pp.123–142.

Rigwema, H. and Venter, R. (2004) Advanced Entrepreneurship, Oxford, Cape Town. Sangosanya, A.O. (2011) ‘Firms growth dynamics in Nigeria’s manufacturing industry: a panel

analysis’, Journal of Applied Econometric Review, Vol. 1, No. 1, pp.1–18. Saunders, M., Lewis, P. and Thornhill, A. (2003) Research Methods for Business Students (3rd ed),

Pitman Publishing, England. Scheepers, M.J., Hough, J. and Bloom, J.Z. (2008) ‘Nurturing the corporate entrepreneurship

capability’, Southern African Business Review, Vol. 12, No. 3, pp.50–76. Shane, S. and Venkataraman, S. (2000) ‘The promise of entrepreneurship as a field of research’,

Academy of Management Review, Vol. 25, No. 1, pp.217–226. Simon, S. (2002) Descriptive Statistics [online] www.childrensmercy.orgwww.people.ex.ac.uk

(accessed 20 August 2008). Simons, R. (1990) ‘Rethinking the role of systems in controlling strategy’, Harvard Business

School Teaching Note, No. 9-191-091. Simons, R. (1995) Levers of Control: How Managers Use Innovative Control Systems to Drive

Strategic Renewal, Harvard Business School Press, Harvard.

232 O.L. Kuye

Singer, S. Alpeza, M. and Balkic, M. (2011) ‘Corporate entrepreneurship: Is entrepreneurial behavior possible in a large company?’, [online] http://www.bib.irb.hr/datoteka/387599.Singer_Alpeza_Balkic_ (accessed on 19 May 2011).

Singh, S.P. (2006) Strategic Management, AITBS Publishers, Delhi. Solieri, S.A. (2000) ‘Strategy, strategic control system and firm performance: a multiple case study

approach’, unpublished Doctoral Dissertation, State University of New York, Binghamton, USA.

Tavakoli, I and Perks, K.J. (2001) ‘The development of a strategic control system for the management of strategic change’, Strategic Change, Vol. 10, No. 5, pp.297–305.

Thornberry, N.E. (2001) ‘Corporate entrepreneurship: antidote or oxymoron’, [online] http://www.leadershipforuminc.com/corporateEntrepreneurship (accessed on 7 September 2010).

Tuomela, T-S. (2005) ‘The Interplay of different levers of control: a case study of introducing a new performance measurement system’, Management Accounting Research, Vol. 16, No. 3, pp.293–320.

UNDP (1999) ‘Entrepreneurship development’, United Nations Development Programmes (UNDP) [online] http://www.undp.org/eo/documents/essential-onentrepreneurship.pdf (accessed 18 September 2008).

Wang, W., Lin, C. and Chu, Y. (2011) ‘Types of competitive advantage and analysis’, International Journal of Business and Management, Vol. 6, No. 5, pp.100–104.

Yaacob, Z. (2008) ‘A structural relationship between total quality management, strategic control systems and performance of Malaysian local governments’, unpublished PhD thesis, University of Utara, Malaysia.

Zeqiri, I. (2010) ‘A theoretical overview of the interactions between entrepreneurship and strategic management’, MPRA Paper No. 21943, [online] http://www.mpra.ub.uni-muenchen.de/21943/ (accessed 10 February2011).

![Strategic management & entrepreneurship[ppt]](https://img.pdfslide.us/doc/110x75/5455640caf7959b8038b8a79/strategic-management-entrepreneurshipppt.jpg)