Embed Size (px)

Citation preview

STORMY WEATHER

Marcin Kujawski

Economist Central & Eastern Europe

STORMY WEATHER

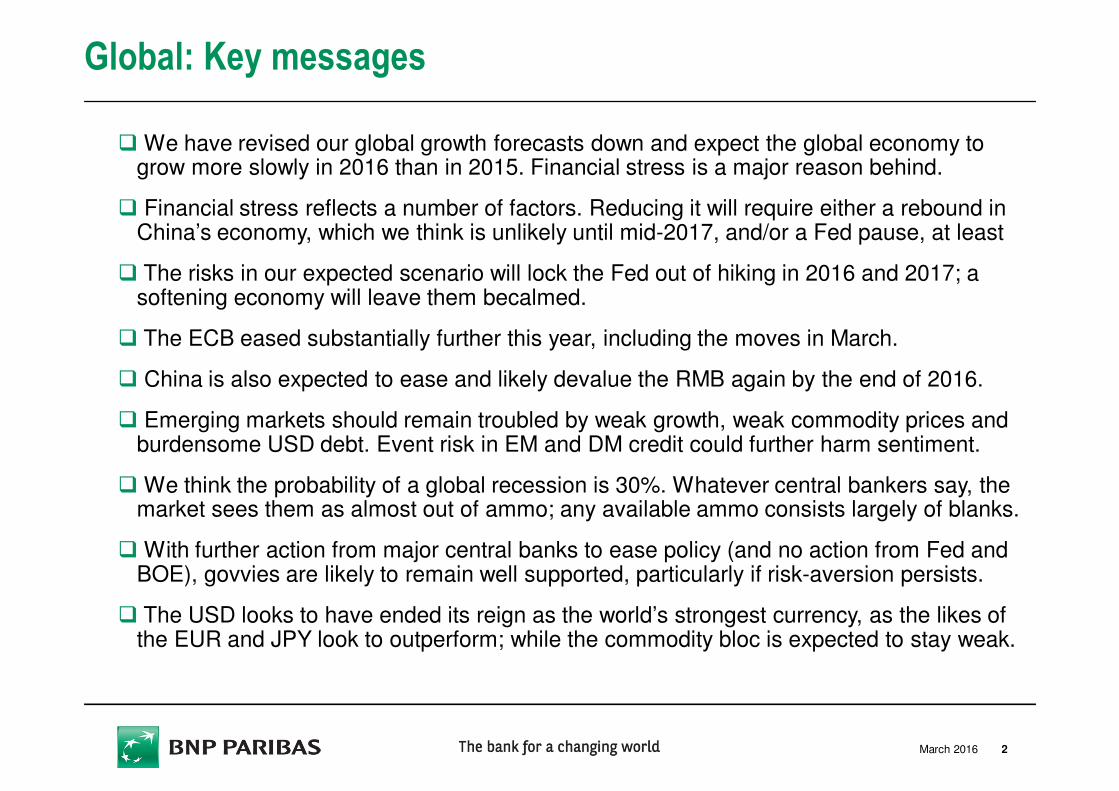

Global: Key messages

� We have revised our global growth forecasts down and expect the global economy to grow more slowly in 2016 than in 2015. Financial stress is a major reason behind.

� Financial stress reflects a number of factors. Reducing it will require either a rebound in China’s economy, which we think is unlikely until mid-2017, and/or a Fed pause, at least

� The risks in our expected scenario will lock the Fed out of hiking in 2016 and 2017; a softening economy will leave them becalmed.

� The ECB eased substantially further this year, including the moves in March.

� China is also expected to ease and likely devalue the RMB again by the end of 2016.

� Emerging markets should remain troubled by weak growth, weak commodity prices and burdensome USD debt. Event risk in EM and DM credit could further harm sentiment.

� We think the probability of a global recession is 30%. Whatever central bankers say, the market sees them as almost out of ammo; any available ammo consists largely of blanks.

� With further action from major central banks to ease policy (and no action from Fed and BOE), govvies are likely to remain well supported, particularly if risk-aversion persists.

� The USD looks to have ended its reign as the world’s strongest currency, as the likes of the EUR and JPY look to outperform; while the commodity bloc is expected to stay weak.

March 2016 2

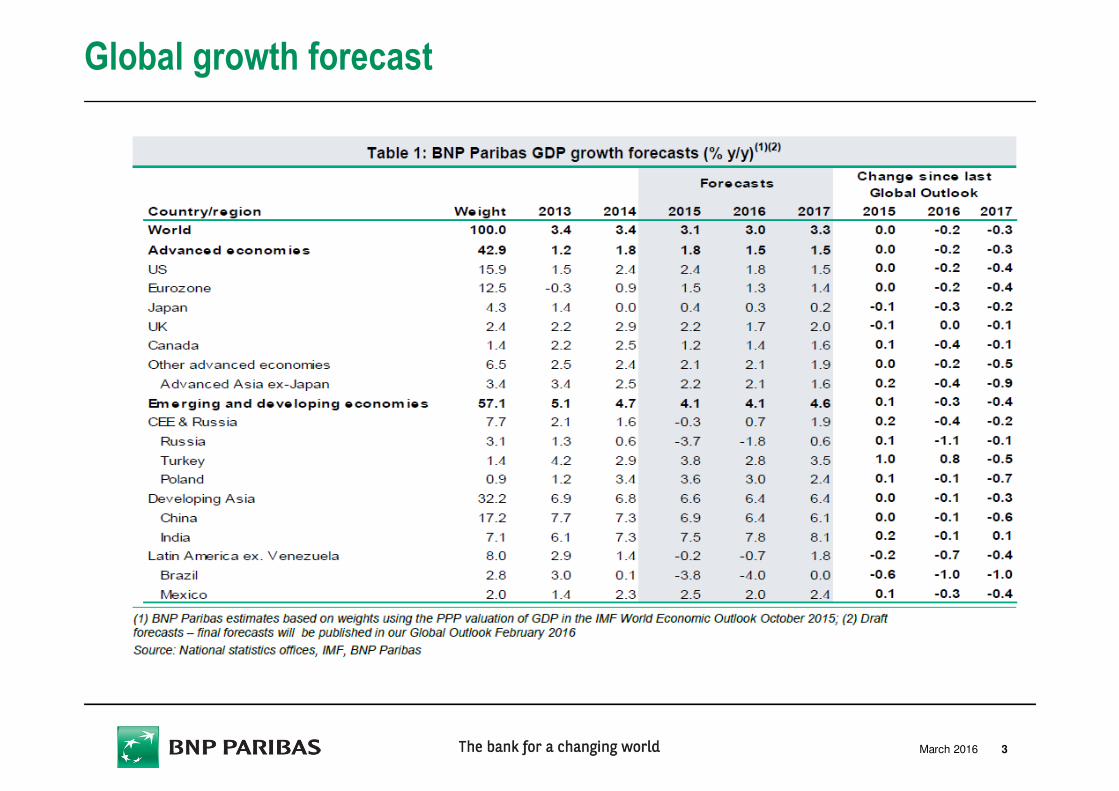

Global growth forecast

3March 2016

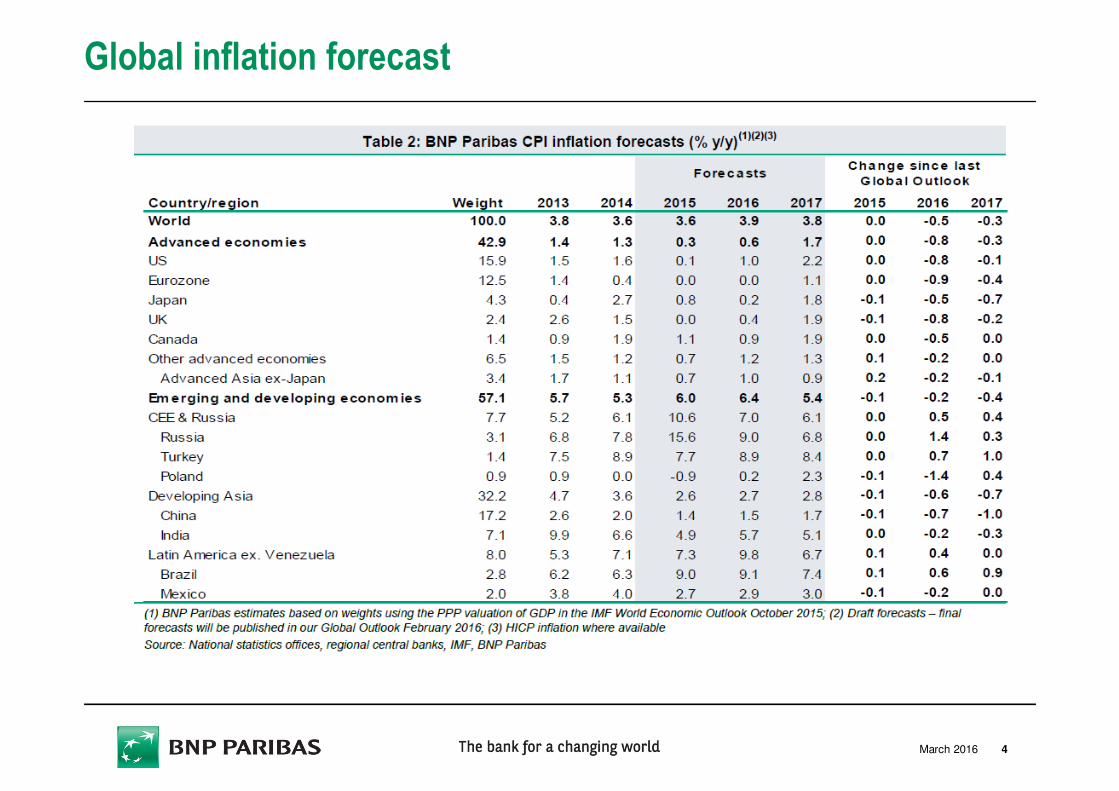

Global inflation forecast

4March 2016

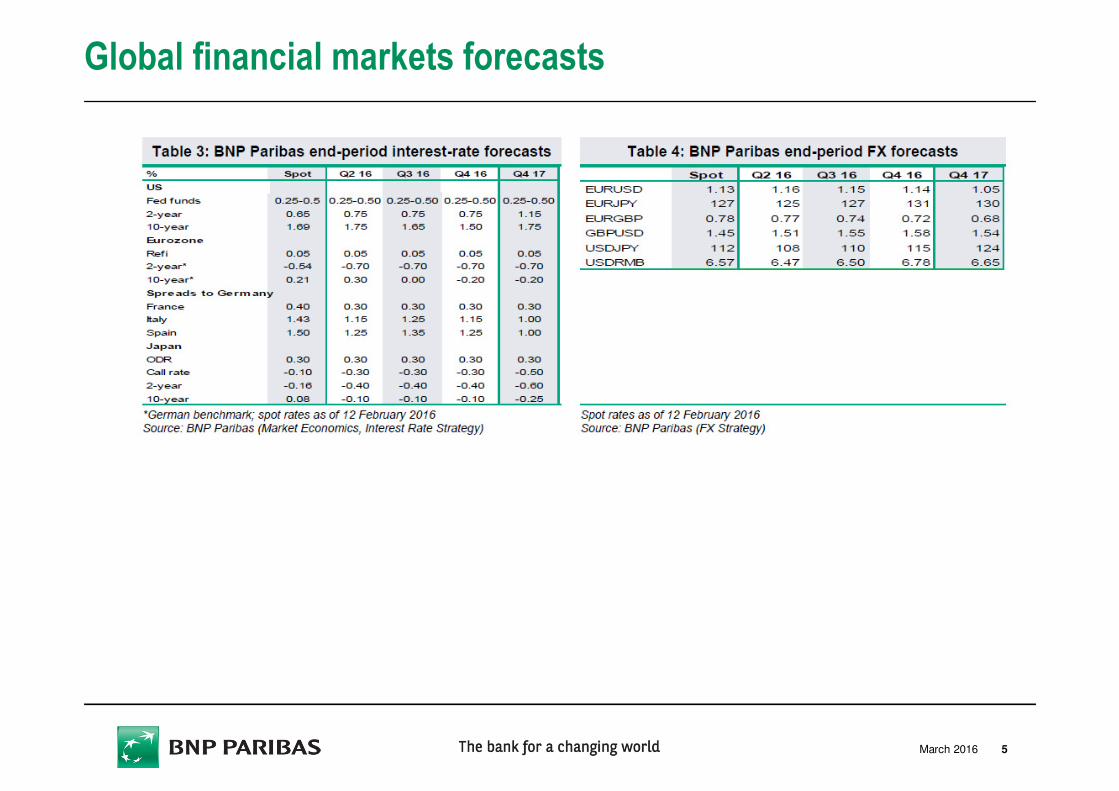

Global financial markets forecasts

5March 2016

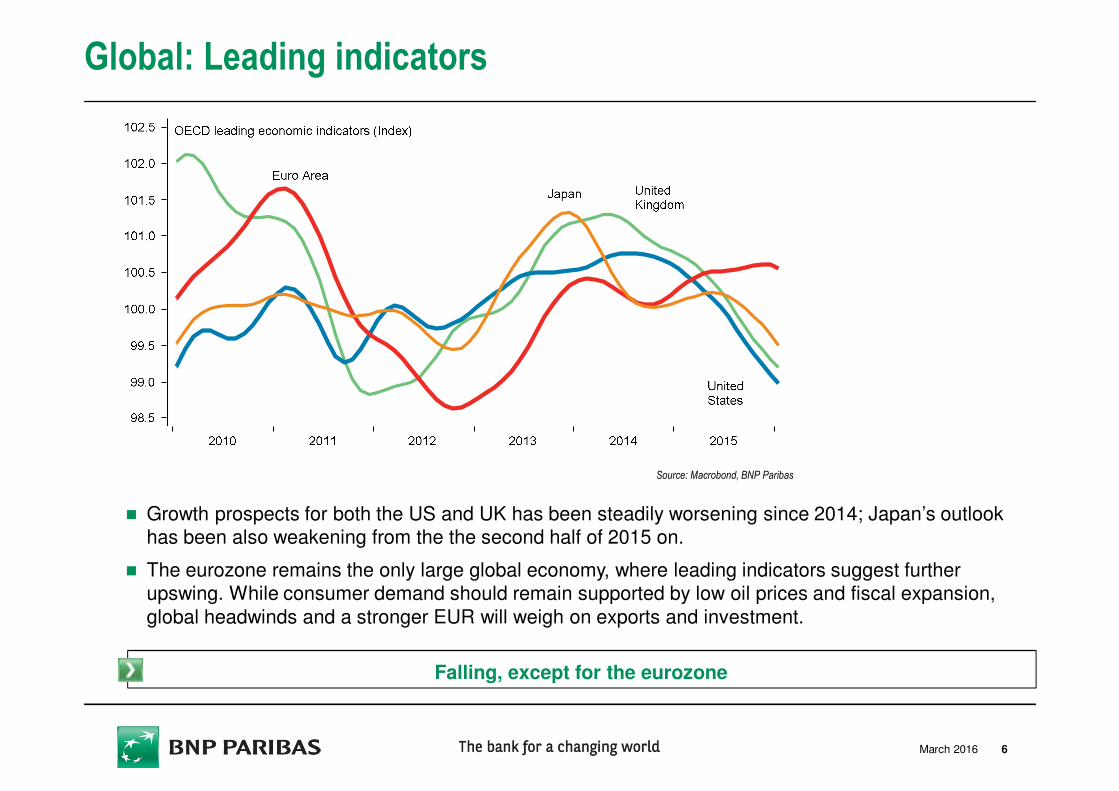

Global: Leading indicators

Source: Macrobond, BNP Paribas

� Growth prospects for both the US and UK has been steadily worsening since 2014; Japan’s outlook has been also weakening from the the second half of 2015 on.

� The eurozone remains the only large global economy, where leading indicators suggest further upswing. While consumer demand should remain supported by low oil prices and fiscal expansion,

global headwinds and a stronger EUR will weigh on exports and investment.

Falling, except for the eurozone

6March 2016

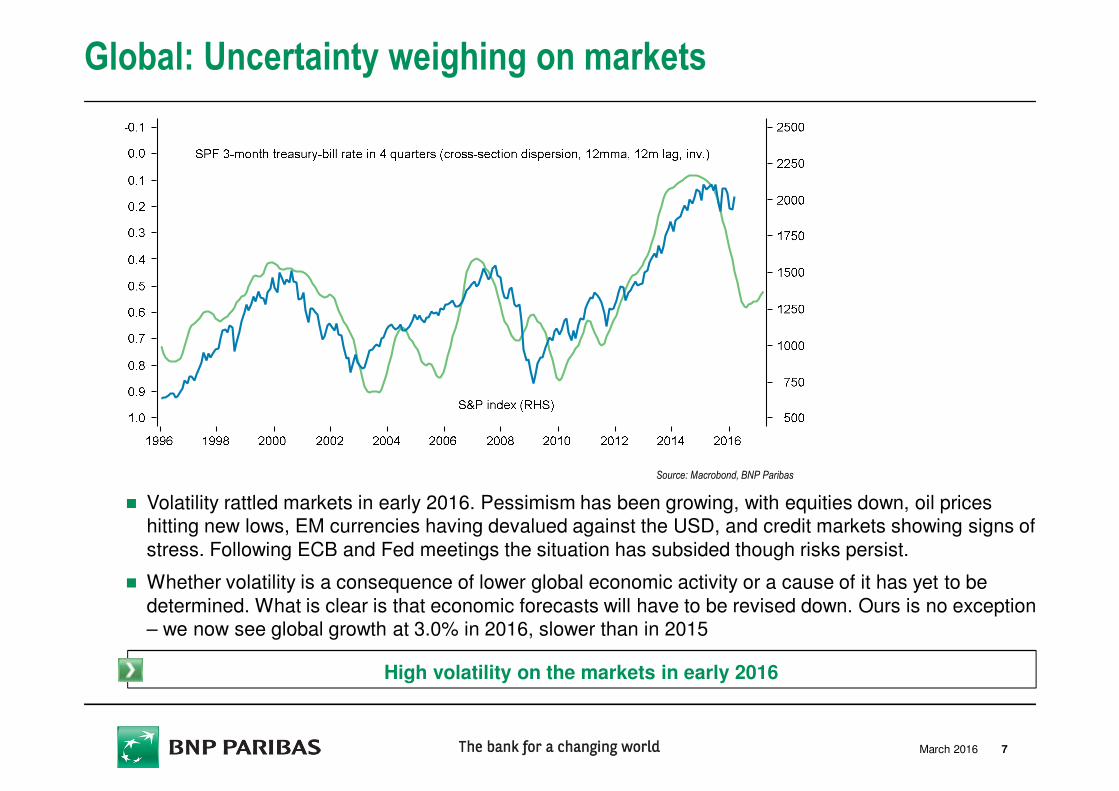

Global: Uncertainty weighing on markets

Source: Macrobond, BNP Paribas

� Volatility rattled markets in early 2016. Pessimism has been growing, with equities down, oil prices hitting new lows, EM currencies having devalued against the USD, and credit markets showing signs of

stress. Following ECB and Fed meetings the situation has subsided though risks persist.

� Whether volatility is a consequence of lower global economic activity or a cause of it has yet to be

determined. What is clear is that economic forecasts will have to be revised down. Ours is no exception – we now see global growth at 3.0% in 2016, slower than in 2015

High volatility on the markets in early 2016

7March 2016

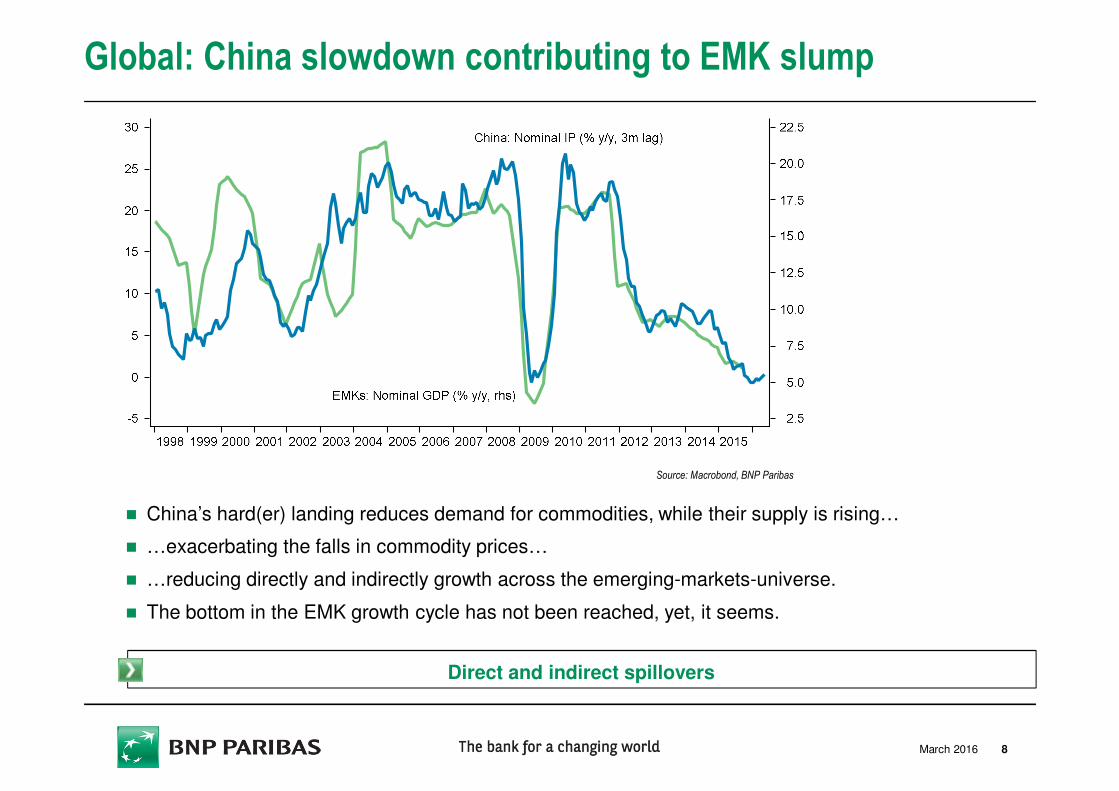

Global: China slowdown contributing to EMK slump

Source: Macrobond, BNP Paribas

� China’s hard(er) landing reduces demand for commodities, while their supply is rising…

� …exacerbating the falls in commodity prices…

� …reducing directly and indirectly growth across the emerging-markets-universe.

� The bottom in the EMK growth cycle has not been reached, yet, it seems.

Direct and indirect spillovers

8March 2016

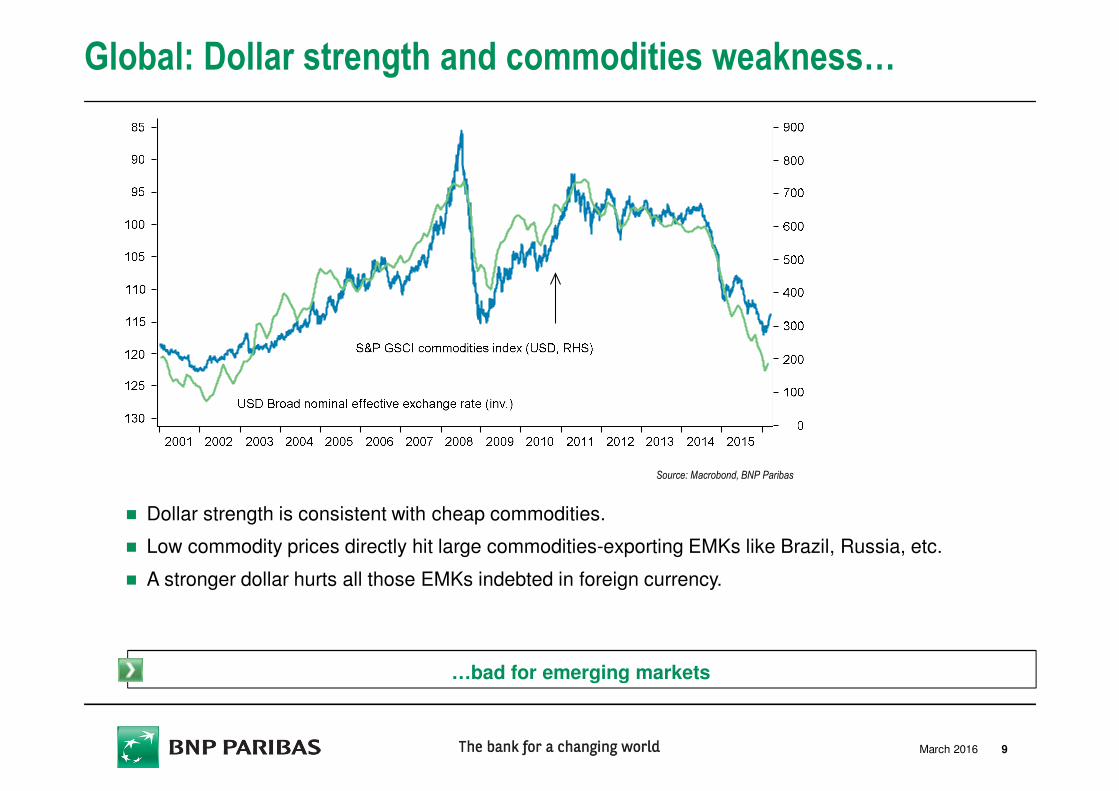

Global: Dollar strength and commodities weakness…

Source: Macrobond, BNP Paribas

� Dollar strength is consistent with cheap commodities.

� Low commodity prices directly hit large commodities-exporting EMKs like Brazil, Russia, etc.

� A stronger dollar hurts all those EMKs indebted in foreign currency.

…bad for emerging markets

9March 2016

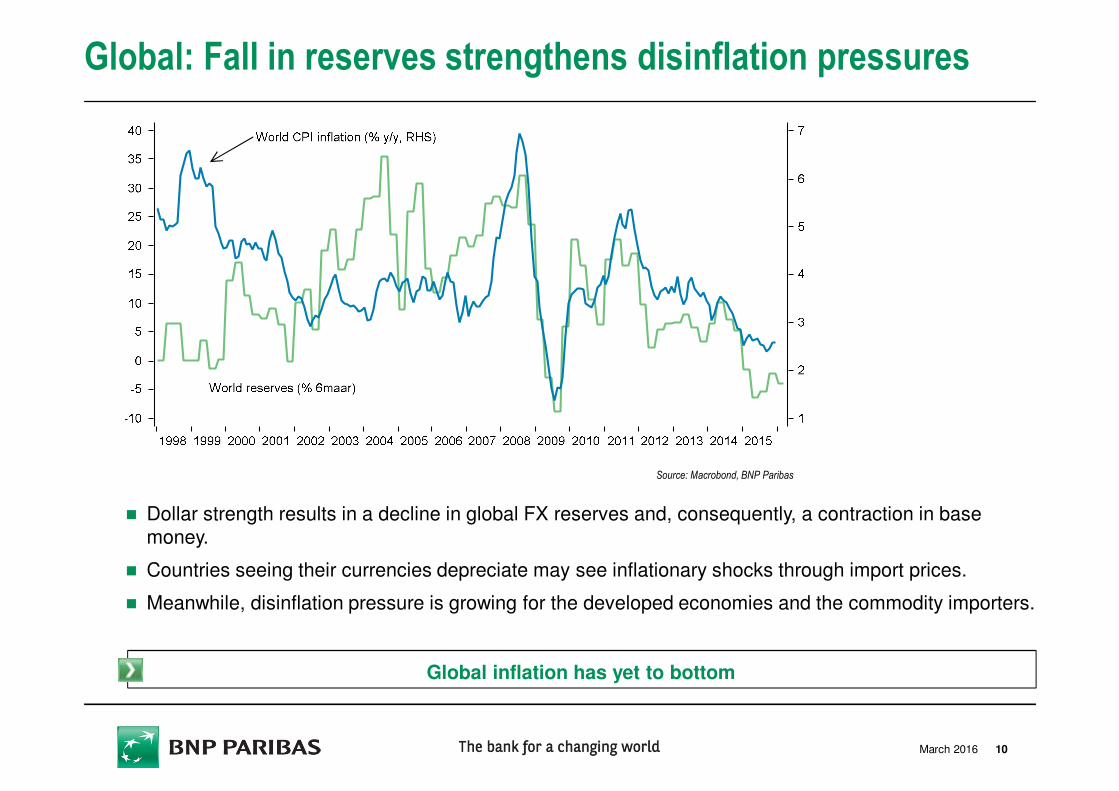

Global: Fall in reserves strengthens disinflation pressures

Source: Macrobond, BNP Paribas

� Dollar strength results in a decline in global FX reserves and, consequently, a contraction in base money.

� Countries seeing their currencies depreciate may see inflationary shocks through import prices.

� Meanwhile, disinflation pressure is growing for the developed economies and the commodity importers.

Global inflation has yet to bottom

10March 2016

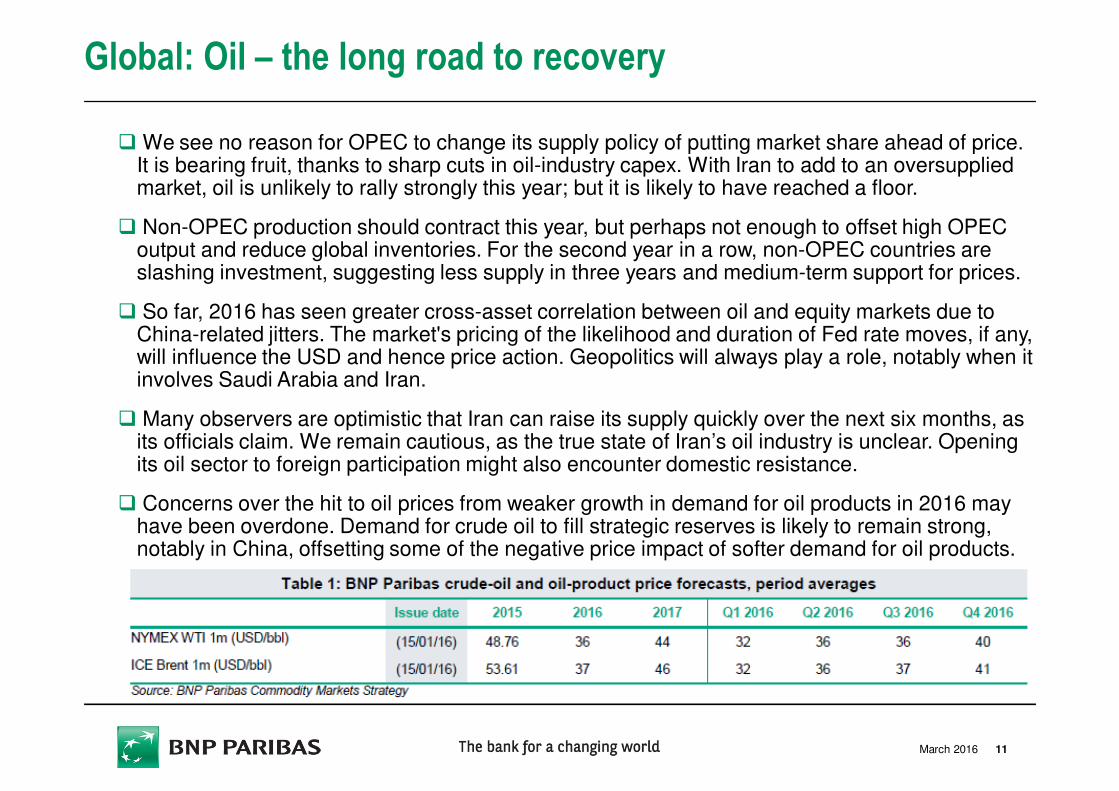

Global: Oil – the long road to recovery

� We see no reason for OPEC to change its supply policy of putting market share ahead of price. It is bearing fruit, thanks to sharp cuts in oil-industry capex. With Iran to add to an oversupplied market, oil is unlikely to rally strongly this year; but it is likely to have reached a floor.

� Non-OPEC production should contract this year, but perhaps not enough to offset high OPEC output and reduce global inventories. For the second year in a row, non-OPEC countries are slashing investment, suggesting less supply in three years and medium-term support for prices.

� So far, 2016 has seen greater cross-asset correlation between oil and equity markets due to China-related jitters. The market's pricing of the likelihood and duration of Fed rate moves, if any, will influence the USD and hence price action. Geopolitics will always play a role, notably when it involves Saudi Arabia and Iran.

� Many observers are optimistic that Iran can raise its supply quickly over the next six months, as its officials claim. We remain cautious, as the true state of Iran’s oil industry is unclear. Opening its oil sector to foreign participation might also encounter domestic resistance.

� Concerns over the hit to oil prices from weaker growth in demand for oil products in 2016 may have been overdone. Demand for crude oil to fill strategic reserves is likely to remain strong, notably in China, offsetting some of the negative price impact of softer demand for oil products.

11March 2016

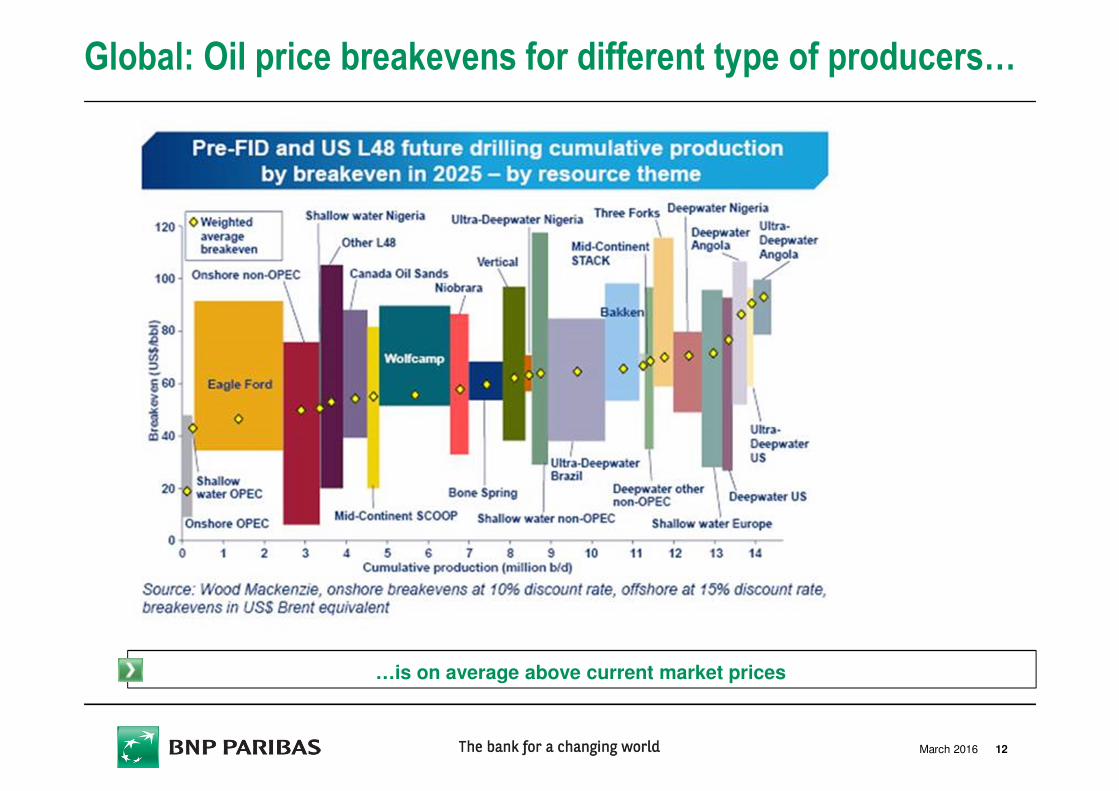

Global: Oil price breakevens for different type of producers…

…is on average above current market prices

12March 2016

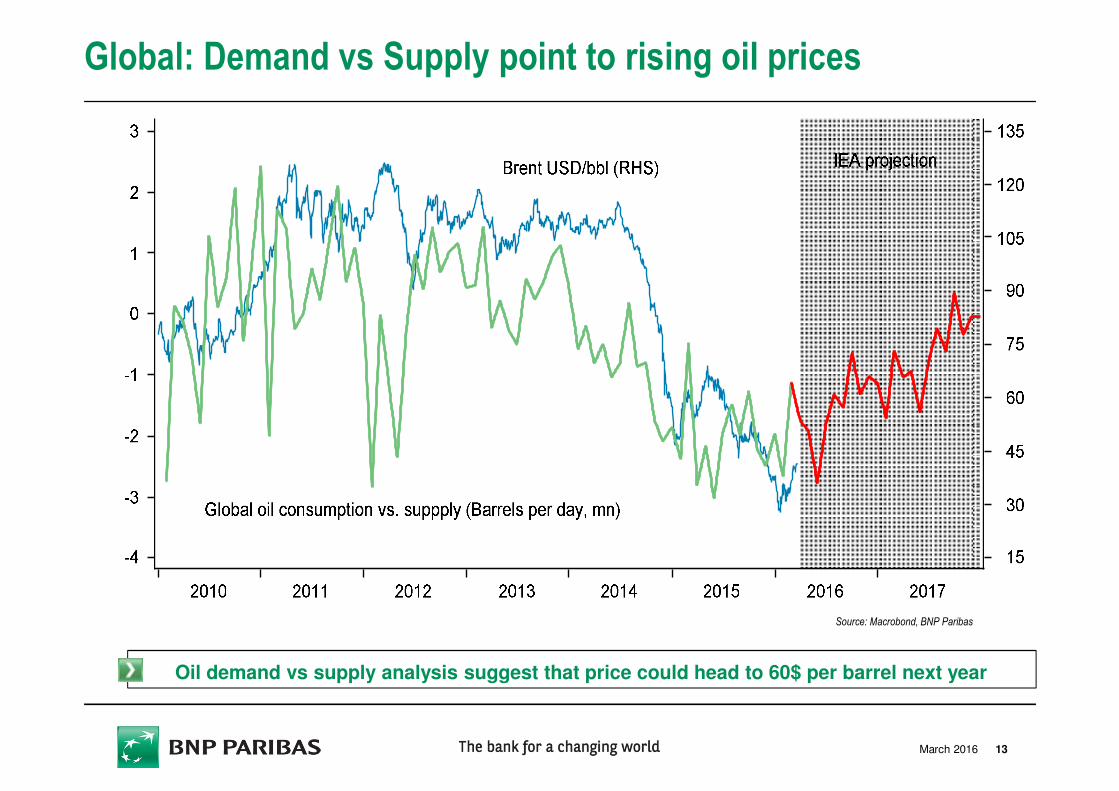

Global: Demand vs Supply point to rising oil prices

Oil demand vs supply analysis suggest that price could head to 60$ per barrel next year

13

Source: Macrobond, BNP Paribas

March 2016

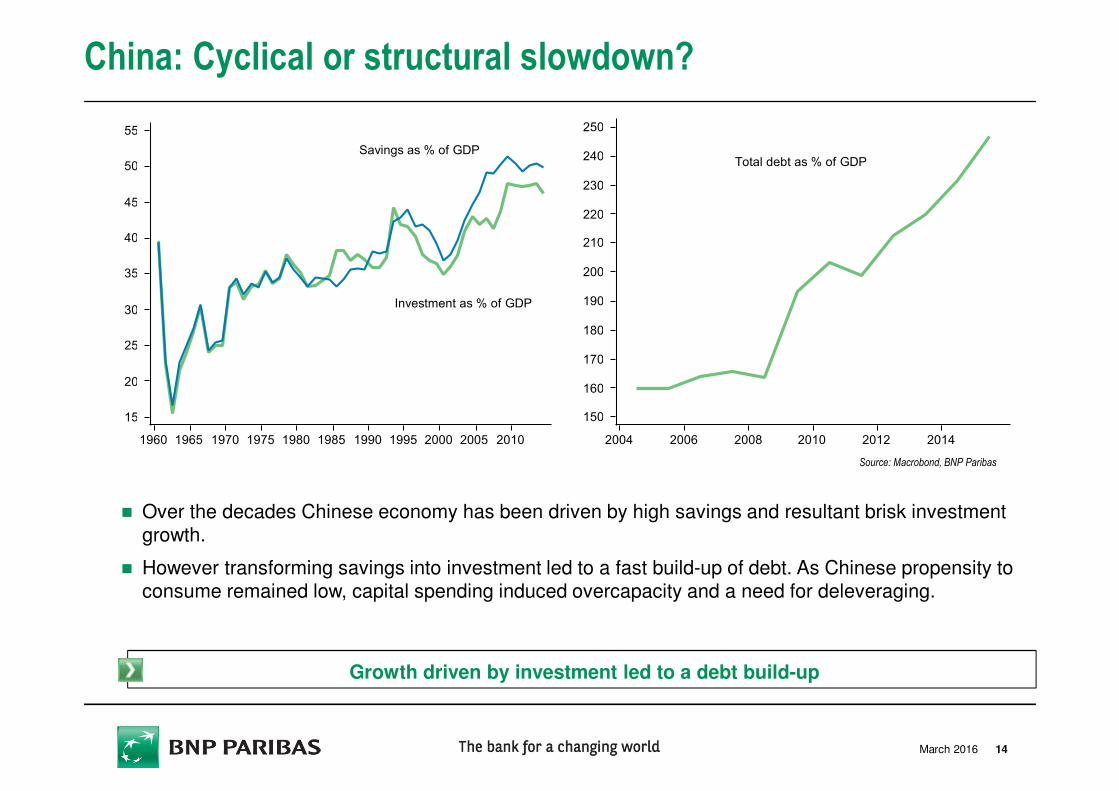

China: Cyclical or structural slowdown?

Source: Macrobond, BNP Paribas

� Over the decades Chinese economy has been driven by high savings and resultant brisk investment growth.

� However transforming savings into investment led to a fast build-up of debt. As Chinese propensity to consume remained low, capital spending induced overcapacity and a need for deleveraging.

Growth driven by investment led to a debt build-up

14

Savings as % of GDP

Investment as % of GDP

15

20

25

30

35

40

45

50

55

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Total debt as % of GDP

150

160

170

180

190

200

210

220

230

240

250

2004 2006 2008 2010 2012 2014

March 2016

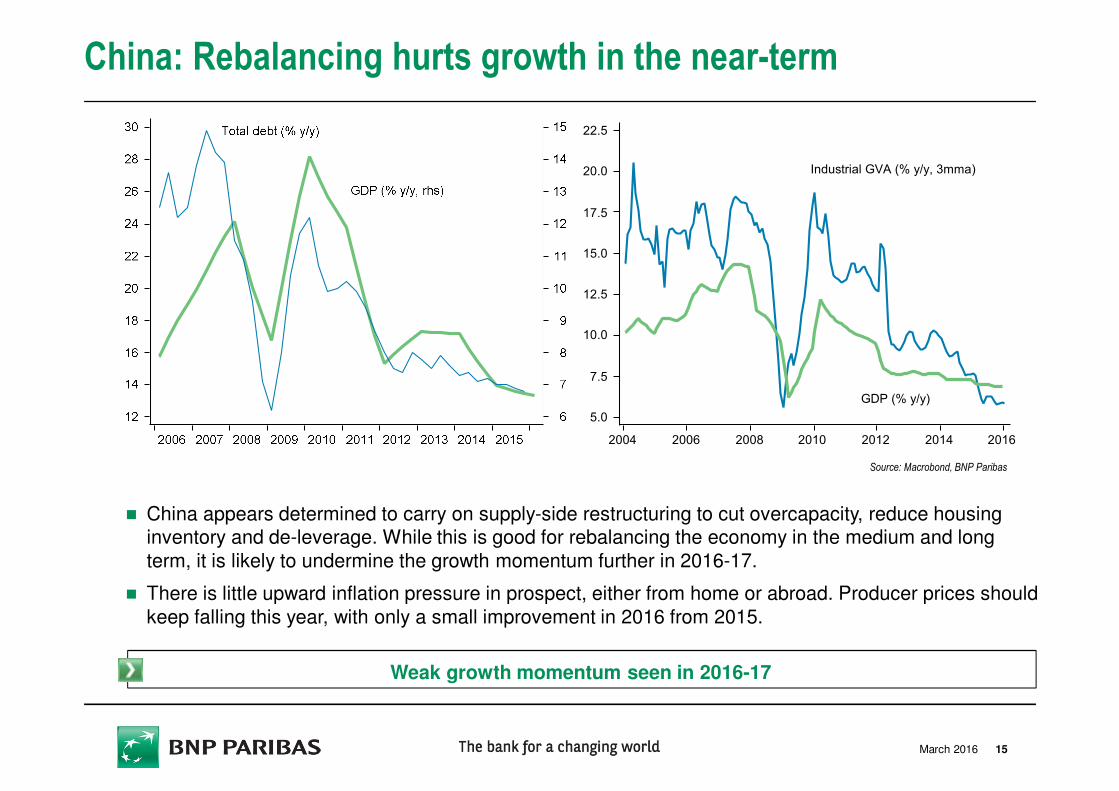

China: Rebalancing hurts growth in the near-term

Source: Macrobond, BNP Paribas

� China appears determined to carry on supply-side restructuring to cut overcapacity, reduce housing inventory and de-leverage. While this is good for rebalancing the economy in the medium and long

term, it is likely to undermine the growth momentum further in 2016-17.

� There is little upward inflation pressure in prospect, either from home or abroad. Producer prices should

keep falling this year, with only a small improvement in 2016 from 2015.

Weak growth momentum seen in 2016-17

15

Industrial GVA (% y/y, 3mma)

GDP (% y/y)

5.0

7.5

10.0

12.5

15.0

17.5

20.0

22.5

2004 2006 2008 2010 2012 2014 2016

March 2016

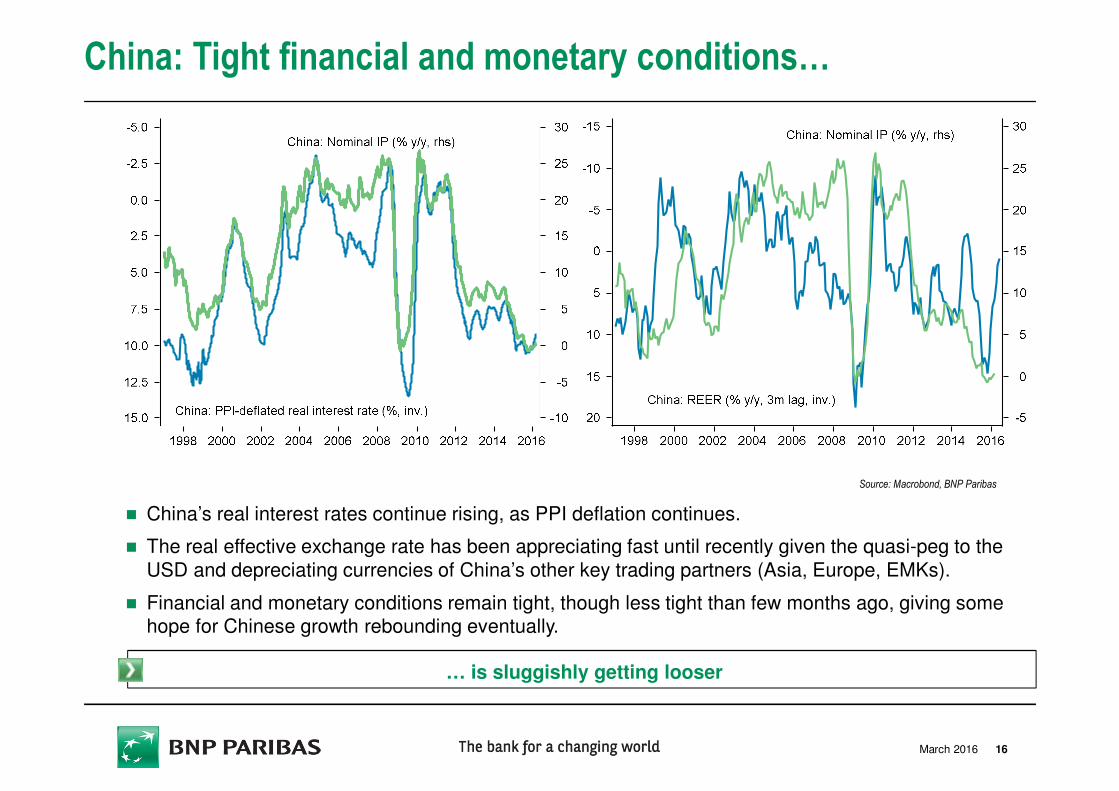

China: Tight financial and monetary conditions…

Source: Macrobond, BNP Paribas

� China’s real interest rates continue rising, as PPI deflation continues.

� The real effective exchange rate has been appreciating fast until recently given the quasi-peg to the

USD and depreciating currencies of China’s other key trading partners (Asia, Europe, EMKs).

� Financial and monetary conditions remain tight, though less tight than few months ago, giving some hope for Chinese growth rebounding eventually.

… is sluggishly getting looser

16March 2016

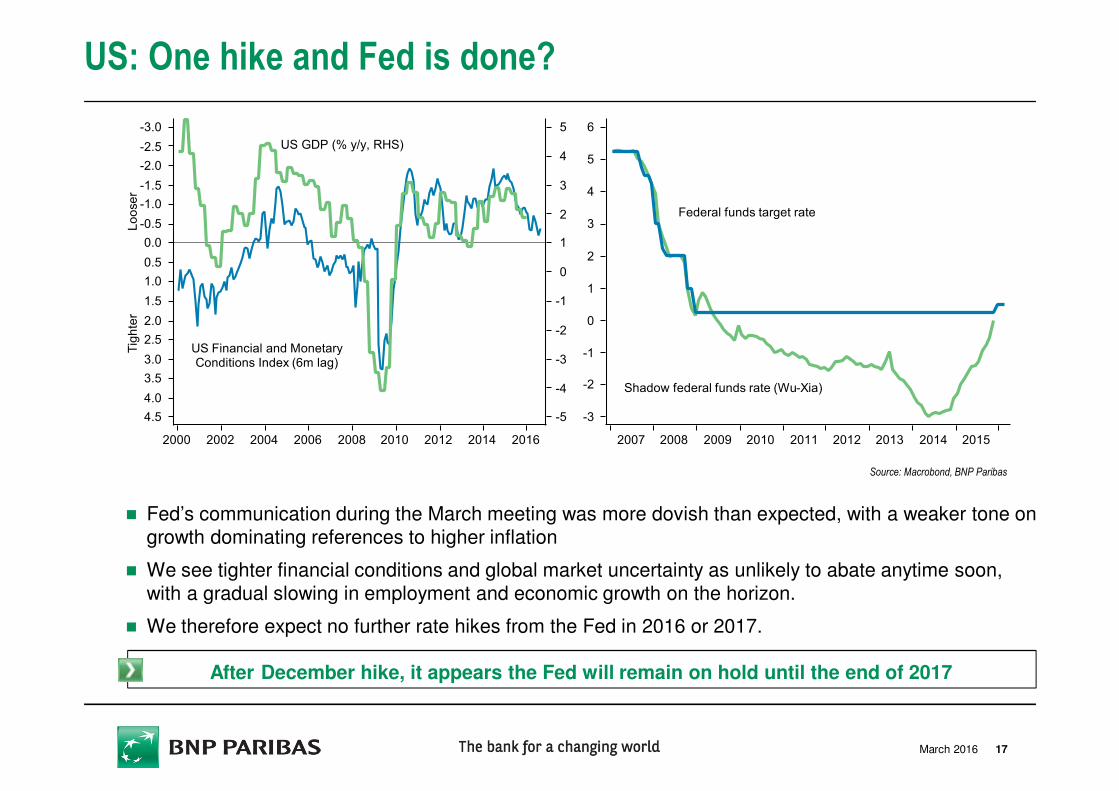

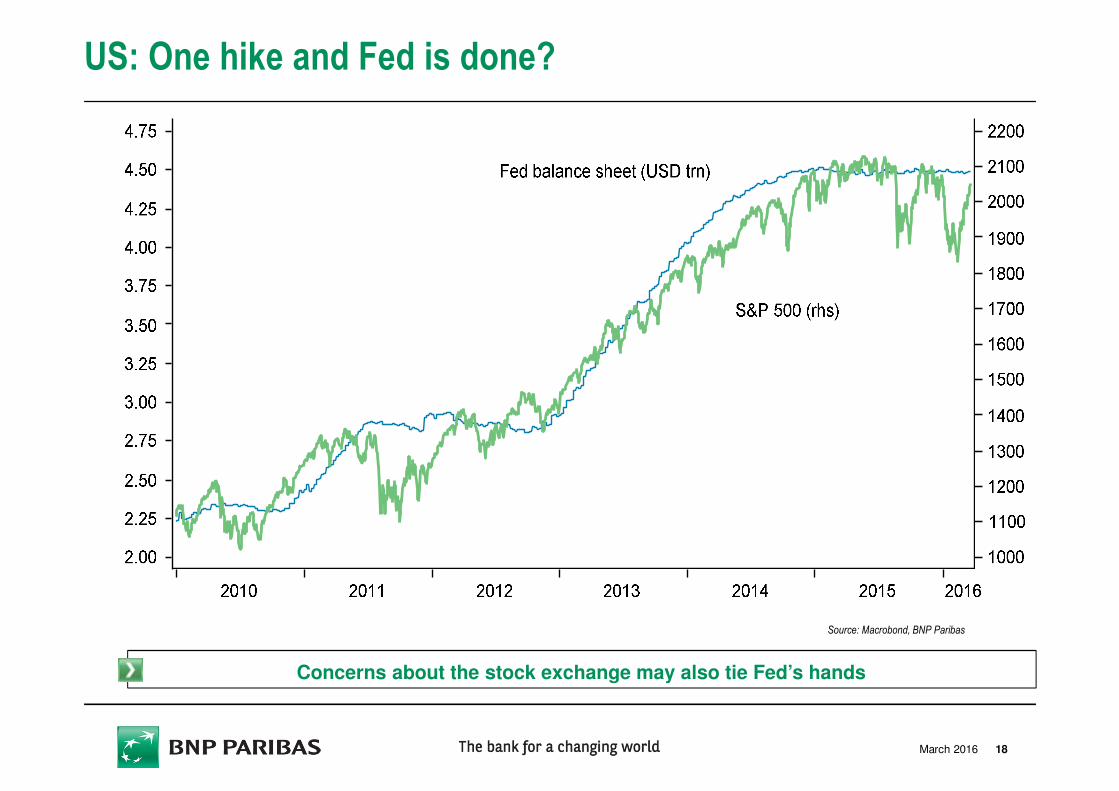

US: One hike and Fed is done?

Source: Macrobond, BNP Paribas

� Fed’s communication during the March meeting was more dovish than expected, with a weaker tone on growth dominating references to higher inflation

� We see tighter financial conditions and global market uncertainty as unlikely to abate anytime soon, with a gradual slowing in employment and economic growth on the horizon.

� We therefore expect no further rate hikes from the Fed in 2016 or 2017.

After December hike, it appears the Fed will remain on hold until the end of 2017

17

Shadow federal funds rate (Wu-Xia)

Federal funds target rate

-3

-2

-1

0

1

2

3

4

5

6

2007 2008 2009 2010 2011 2012 2013 2014 2015

US GDP (% y/y, RHS)

US Financial and MonetaryConditions Index (6m lag)

Tighter Looser

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5 -5

-4

-3

-2

-1

0

1

2

3

4

5

2000 2002 2004 2006 2008 2010 2012 2014 2016

March 2016

US: One hike and Fed is done?

Source: Macrobond, BNP Paribas

Concerns about the stock exchange may also tie Fed’s hands

18March 2016

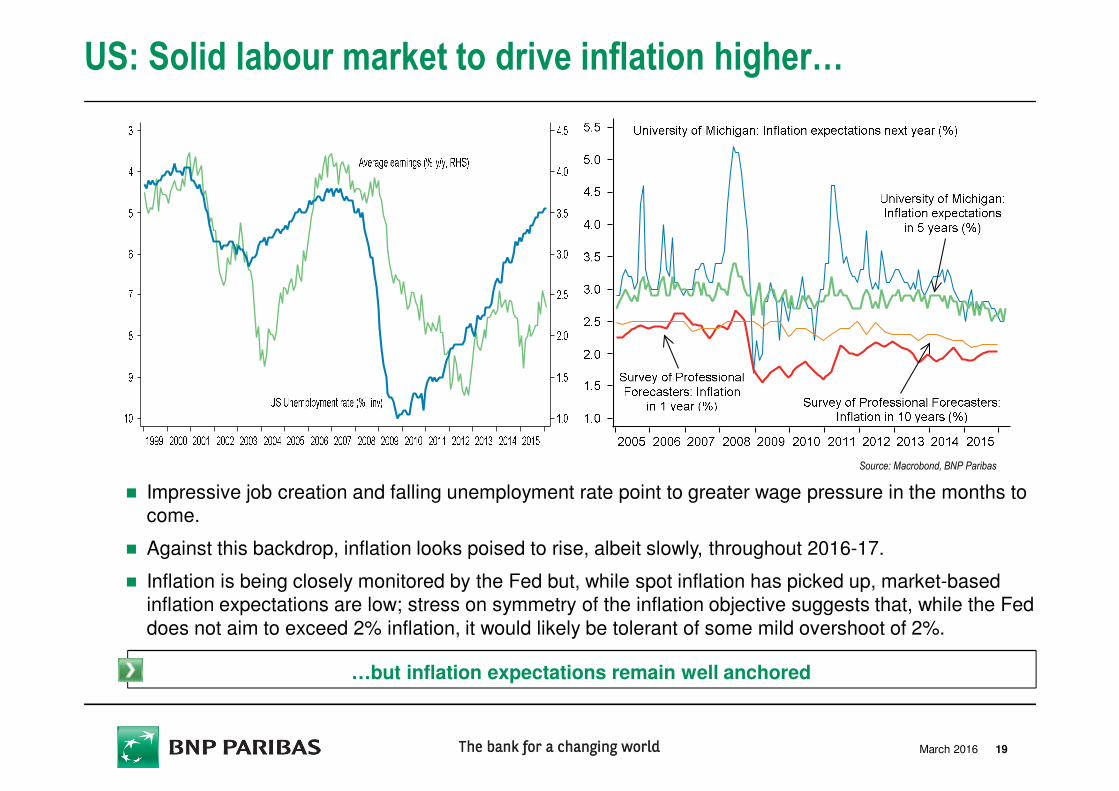

US: Solid labour market to drive inflation higher…

Source: Macrobond, BNP Paribas

� Impressive job creation and falling unemployment rate point to greater wage pressure in the months to come.

� Against this backdrop, inflation looks poised to rise, albeit slowly, throughout 2016-17.

� Inflation is being closely monitored by the Fed but, while spot inflation has picked up, market-based inflation expectations are low; stress on symmetry of the inflation objective suggests that, while the Fed

does not aim to exceed 2% inflation, it would likely be tolerant of some mild overshoot of 2%.

…but inflation expectations remain well anchored

19March 2016

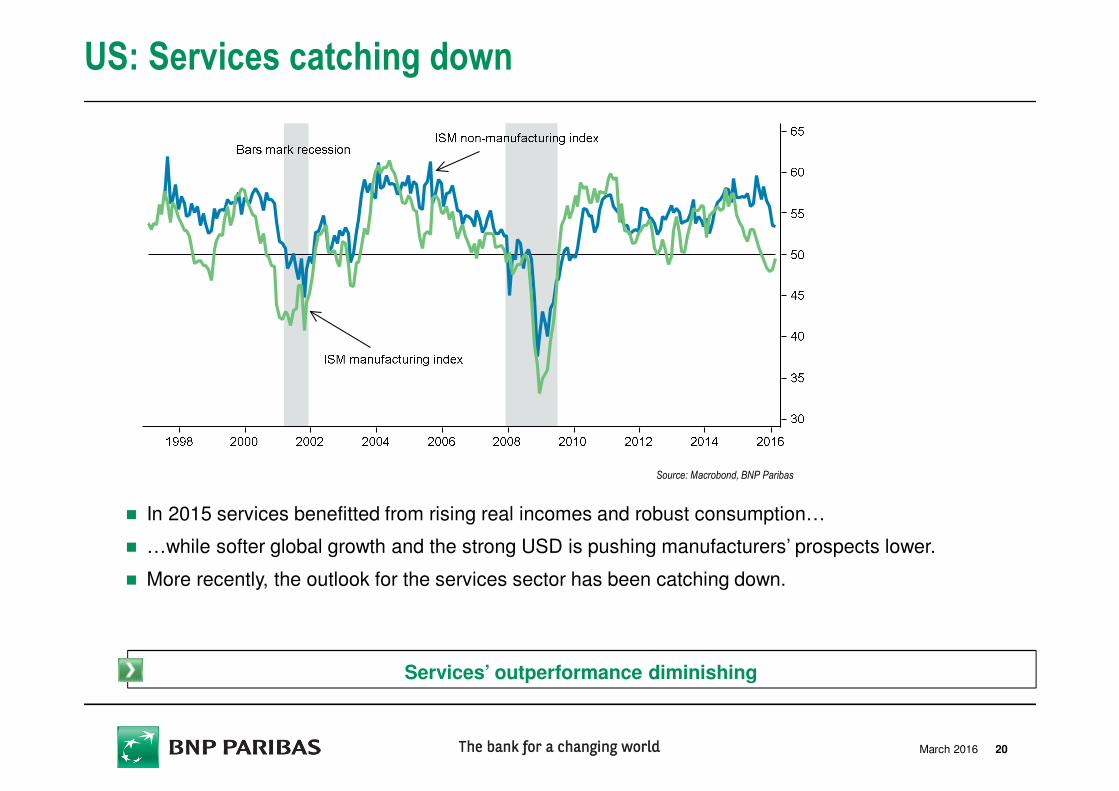

US: Services catching down

Source: Macrobond, BNP Paribas

� In 2015 services benefitted from rising real incomes and robust consumption…

� …while softer global growth and the strong USD is pushing manufacturers’ prospects lower.

� More recently, the outlook for the services sector has been catching down.

Services’ outperformance diminishing

20March 2016

Eurozone: Key messages

� While consumer demand should remain supported by low oil prices and fiscal expansion,

global headwinds and a stronger EUR will weigh on exports and investment.

� Our growth forecasts are already below consensus, but the risk is to the downside. A key

judgement underlying the numbers is that consumers will spend the income gained from

lower oil prices; raised concerns about the external backdrop could boost saving instead.

� With the output gap hardly closing and low oil prices and a stronger currency weighing on

goods prices, we expect core inflation to remain broadly flat and headline inflation to hover

around zero this year, the same level as in 2015.

� Our inflation forecasts are below the consensus both for this year and next. In our view,

the risk highlighted by the ECB of inflation expectations becoming unanchored is

significant.

� The first- and second-round effects of low oil prices on inflation drove ECB easing in

March (a lower deposit rate and more asset purchases), in tandem with downward

revisions to staff projections.

� Further easing is likely beyond March due to persistent low inflation.

� The perceived effectiveness of unconventional measures is diminishing, however.

21March 2016

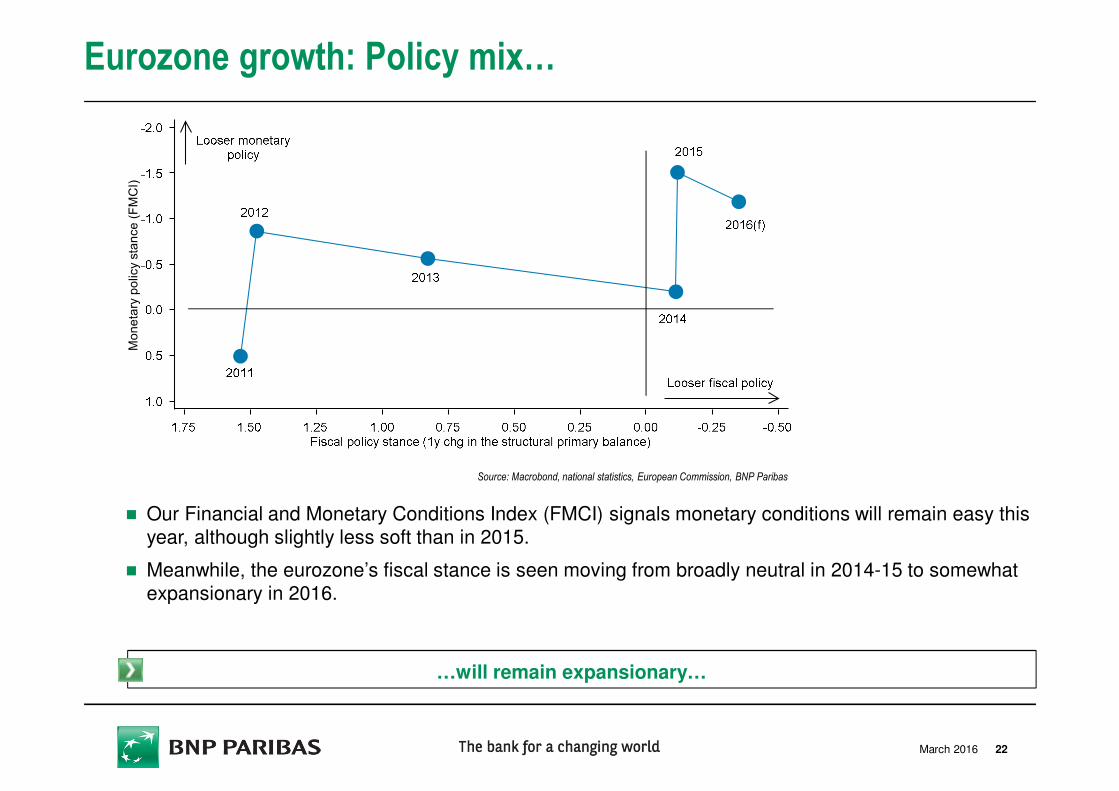

Eurozone growth: Policy mix…

Source: Macrobond, national statistics, European Commission, BNP Paribas

� Our Financial and Monetary Conditions Index (FMCI) signals monetary conditions will remain easy this year, although slightly less soft than in 2015.

� Meanwhile, the eurozone’s fiscal stance is seen moving from broadly neutral in 2014-15 to somewhat expansionary in 2016.

…will remain expansionary…

Monetary policy stance (FMCI)

22March 2016

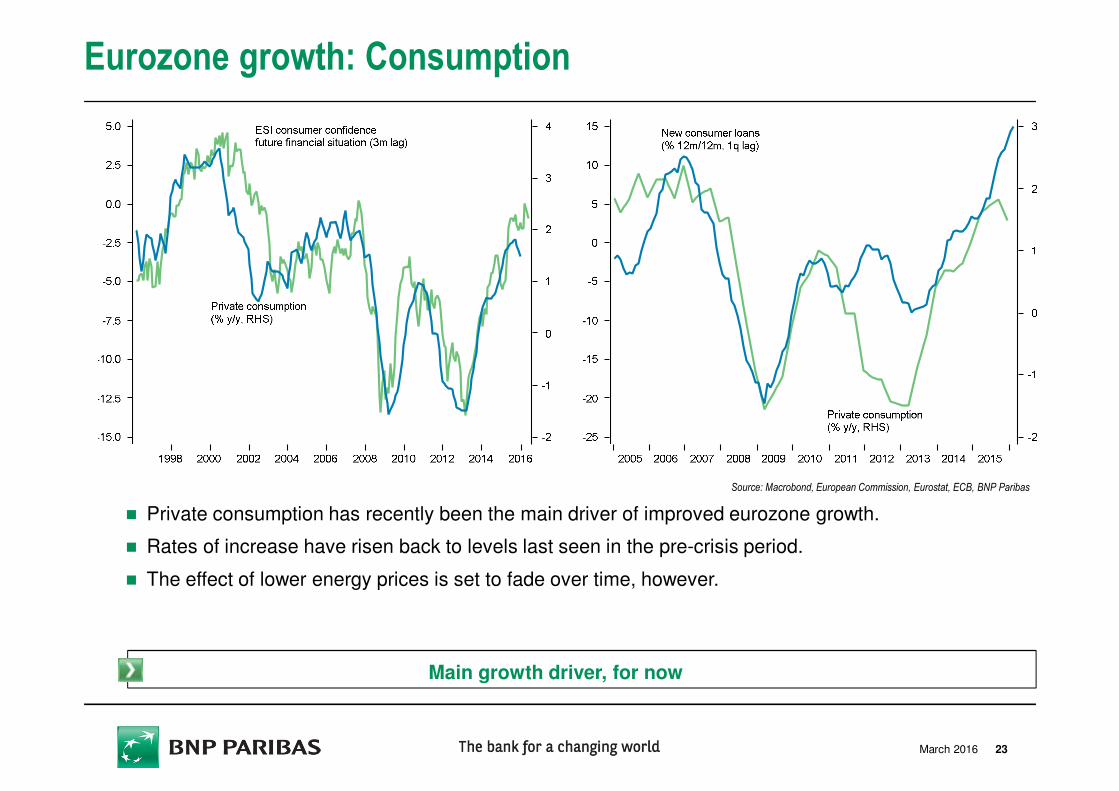

Eurozone growth: Consumption

Source: Macrobond, European Commission, Eurostat, ECB, BNP Paribas

� Private consumption has recently been the main driver of improved eurozone growth.

� Rates of increase have risen back to levels last seen in the pre-crisis period.

� The effect of lower energy prices is set to fade over time, however.

Main growth driver, for now

23March 2016

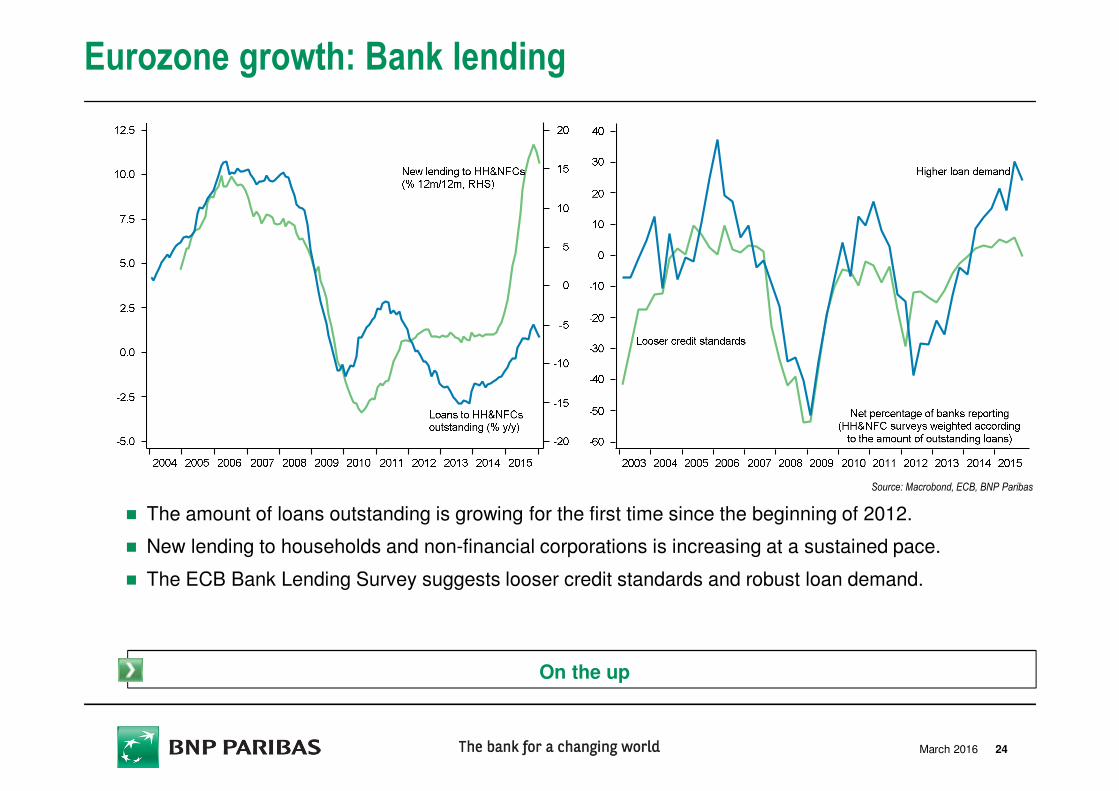

Eurozone growth: Bank lending

Source: Macrobond, ECB, BNP Paribas

� The amount of loans outstanding is growing for the first time since the beginning of 2012.

� New lending to households and non-financial corporations is increasing at a sustained pace.

� The ECB Bank Lending Survey suggests looser credit standards and robust loan demand.

On the up

24March 2016

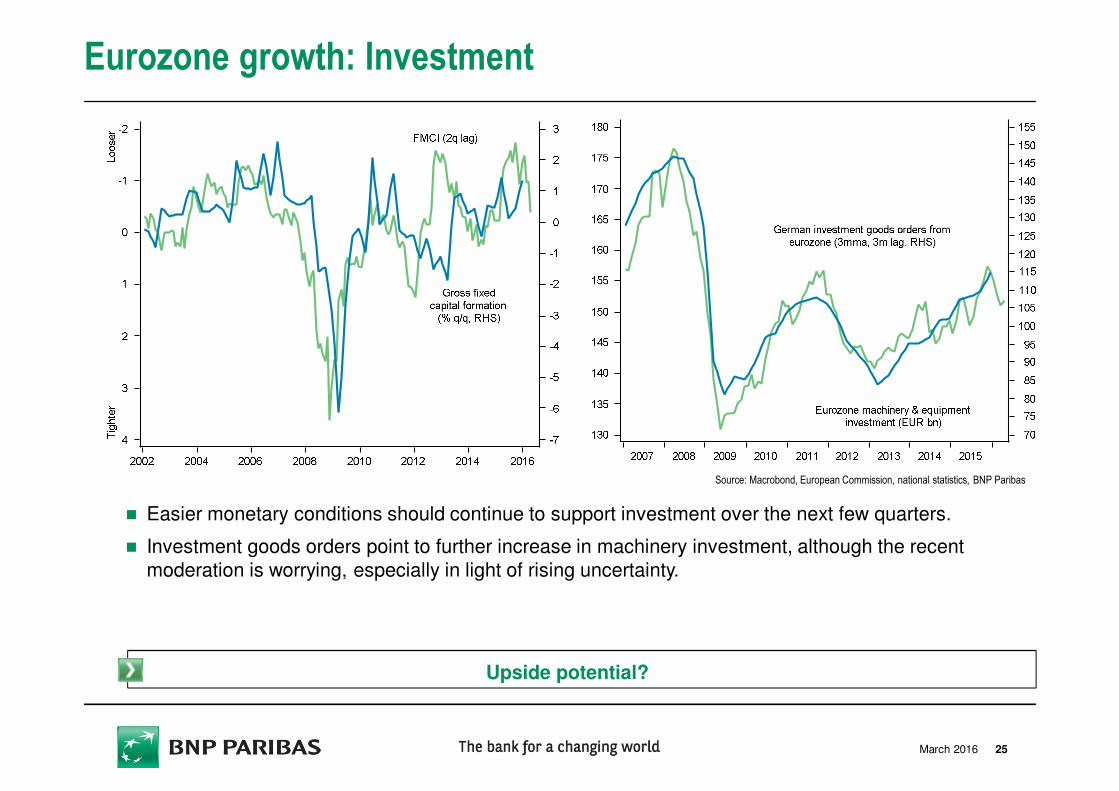

Eurozone growth: Investment

Source: Macrobond, European Commission, national statistics, BNP Paribas

� Easier monetary conditions should continue to support investment over the next few quarters.

� Investment goods orders point to further increase in machinery investment, although the recent

moderation is worrying, especially in light of rising uncertainty.

Upside potential?

25March 2016

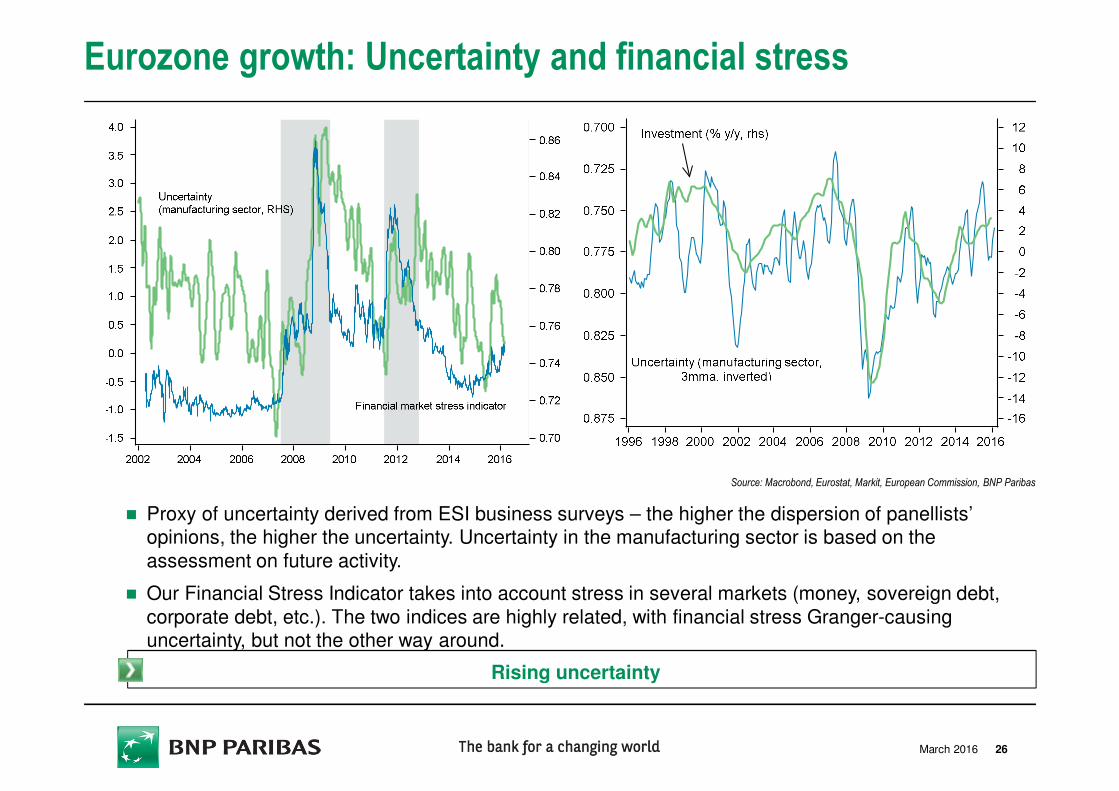

Eurozone growth: Uncertainty and financial stress

Source: Macrobond, Eurostat, Markit, European Commission, BNP Paribas

Rising uncertainty

� Proxy of uncertainty derived from ESI business surveys – the higher the dispersion of panellists’ opinions, the higher the uncertainty. Uncertainty in the manufacturing sector is based on the

assessment on future activity.

� Our Financial Stress Indicator takes into account stress in several markets (money, sovereign debt,

corporate debt, etc.). The two indices are highly related, with financial stress Granger-causing uncertainty, but not the other way around.

26March 2016

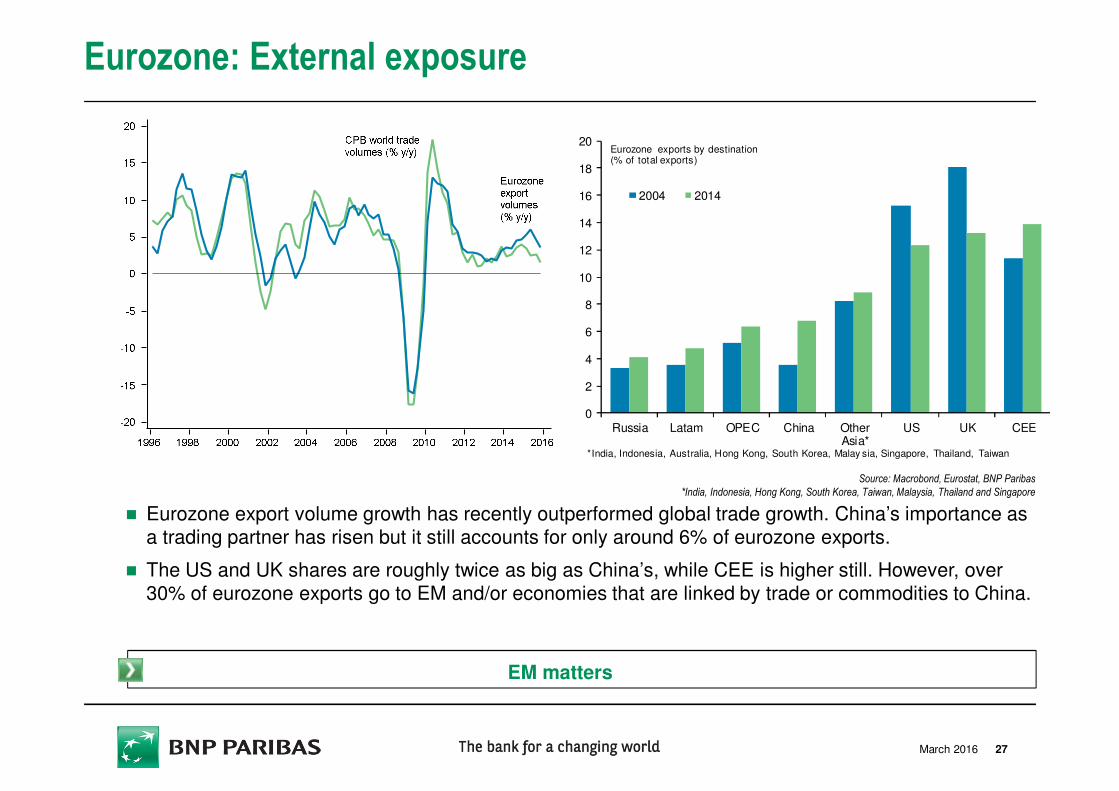

Eurozone: External exposure

Source: Macrobond, Eurostat, BNP Paribas

*India, Indonesia, Hong Kong, South Korea, Taiwan, Malaysia, Thailand and Singapore

� Eurozone export volume growth has recently outperformed global trade growth. China’s importance as a trading partner has risen but it still accounts for only around 6% of eurozone exports.

� The US and UK shares are roughly twice as big as China’s, while CEE is higher still. However, over 30% of eurozone exports go to EM and/or economies that are linked by trade or commodities to China.

EM matters

0

2

4

6

8

10

12

14

16

18

20

Russia Latam OPEC China OtherAsia*

US UK CEE

2004 2014

Eurozone exports by destination(% of total exports)

*India, Indonesia, Australia, Hong Kong, South Korea, Malay sia, Singapore, Thailand, Taiwan

27March 2016

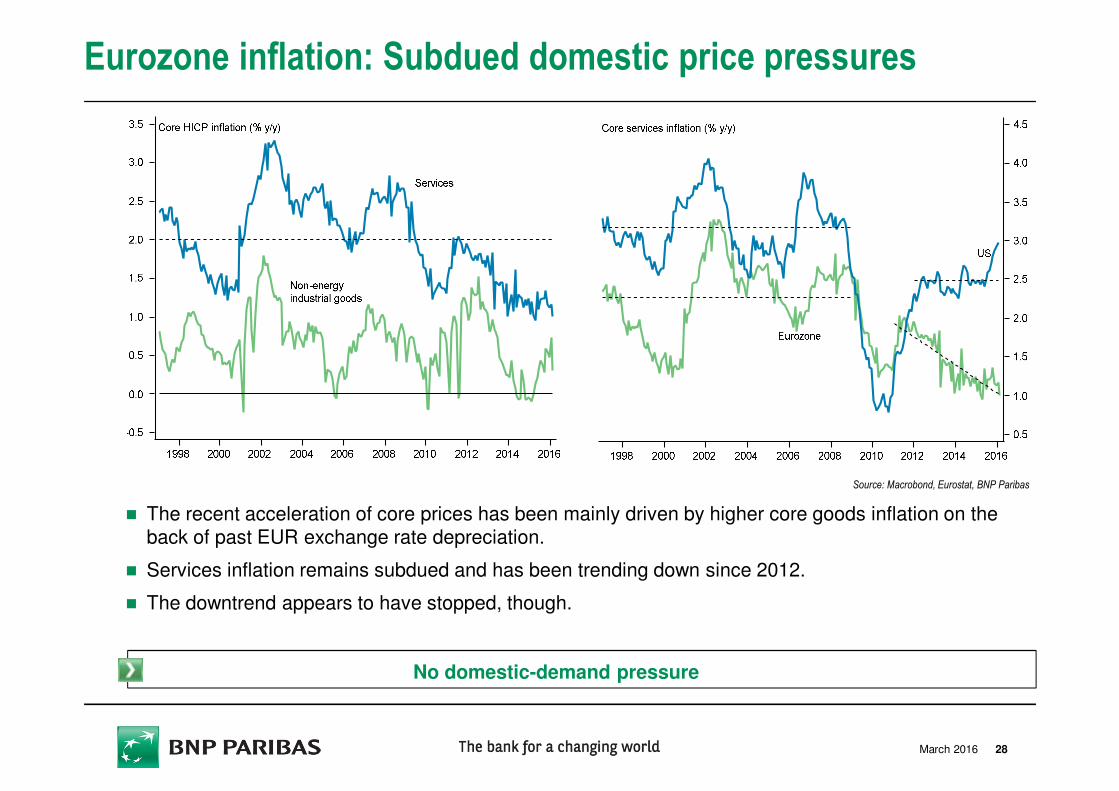

Eurozone inflation: Subdued domestic price pressures

� The recent acceleration of core prices has been mainly driven by higher core goods inflation on the back of past EUR exchange rate depreciation.

� Services inflation remains subdued and has been trending down since 2012.

� The downtrend appears to have stopped, though.

Source: Macrobond, Eurostat, BNP Paribas

No domestic-demand pressure

28March 2016

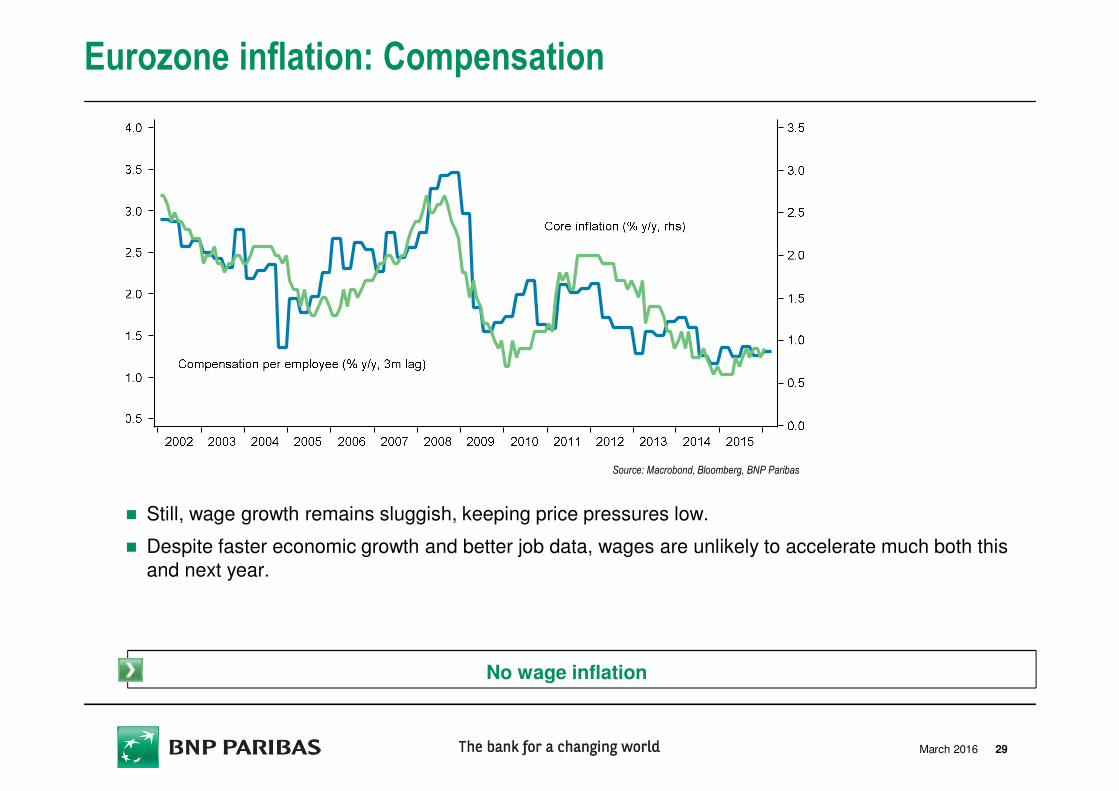

Eurozone inflation: Compensation

Source: Macrobond, Bloomberg, BNP Paribas

� Still, wage growth remains sluggish, keeping price pressures low.

� Despite faster economic growth and better job data, wages are unlikely to accelerate much both this

and next year.

No wage inflation

29March 2016

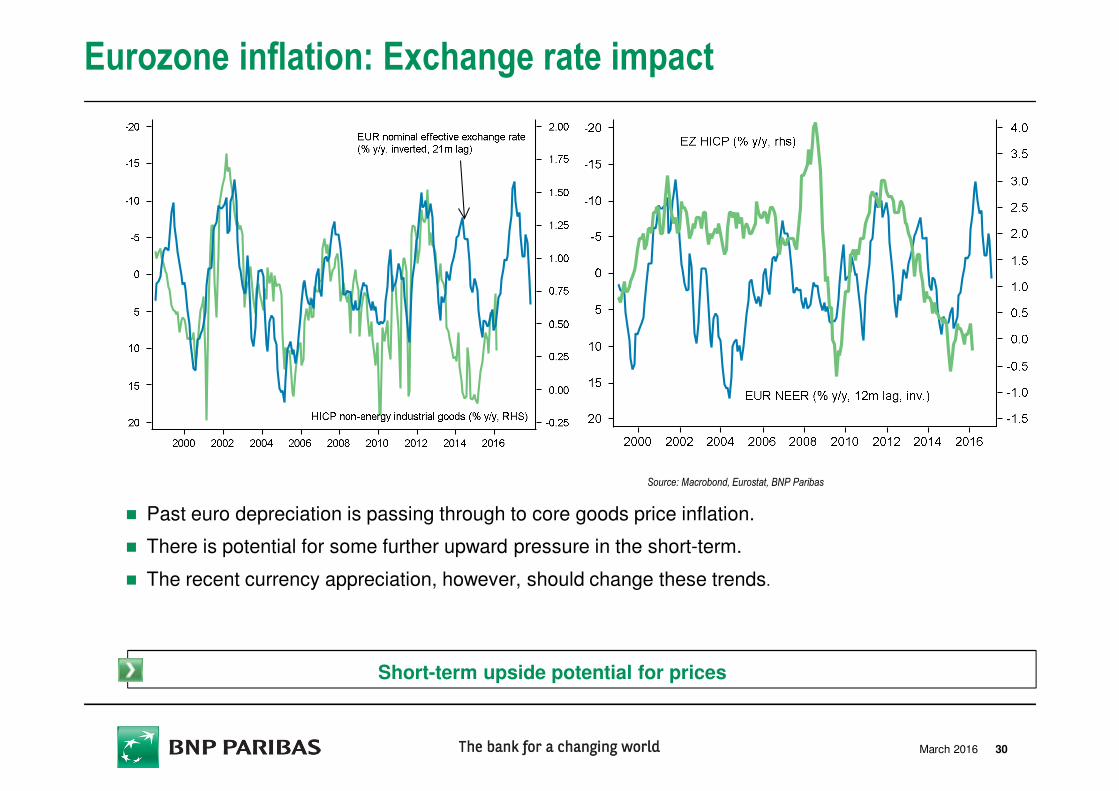

Eurozone inflation: Exchange rate impact

� Past euro depreciation is passing through to core goods price inflation.

� There is potential for some further upward pressure in the short-term.

� The recent currency appreciation, however, should change these trends.

Source: Macrobond, Eurostat, BNP Paribas

Short-term upside potential for prices

30March 2016

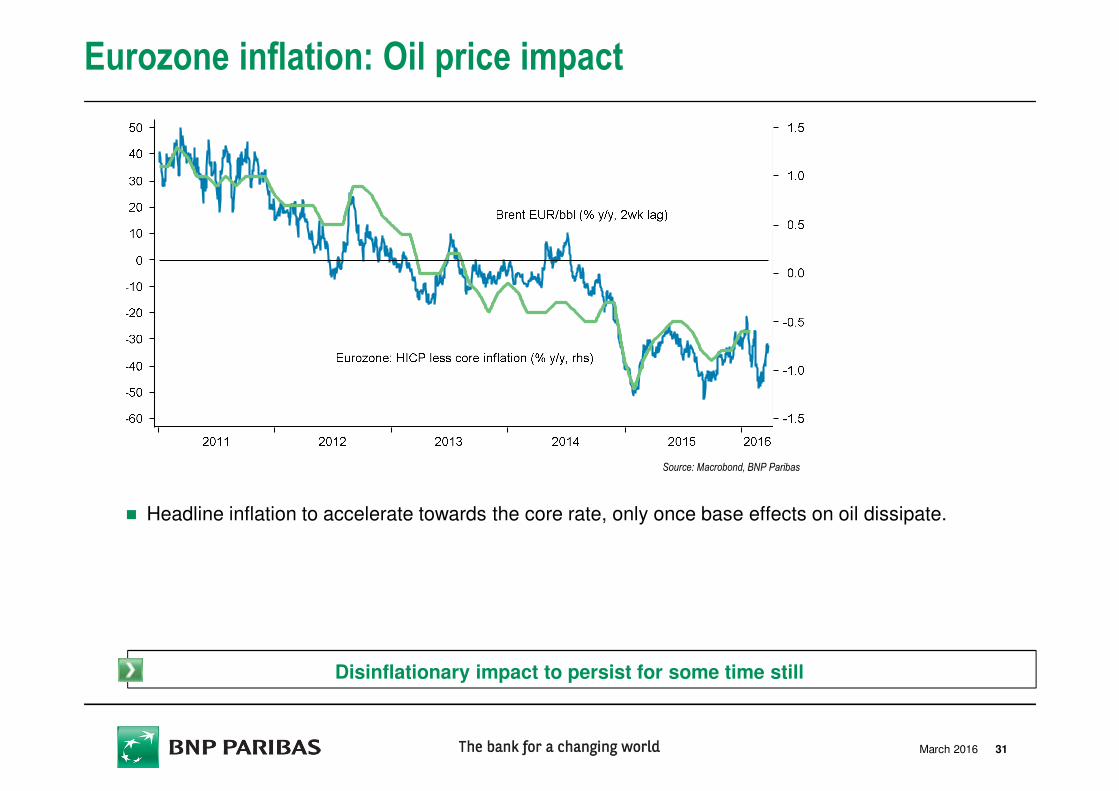

Eurozone inflation: Oil price impact

� Headline inflation to accelerate towards the core rate, only once base effects on oil dissipate.

Source: Macrobond, BNP Paribas

Disinflationary impact to persist for some time still

31March 2016

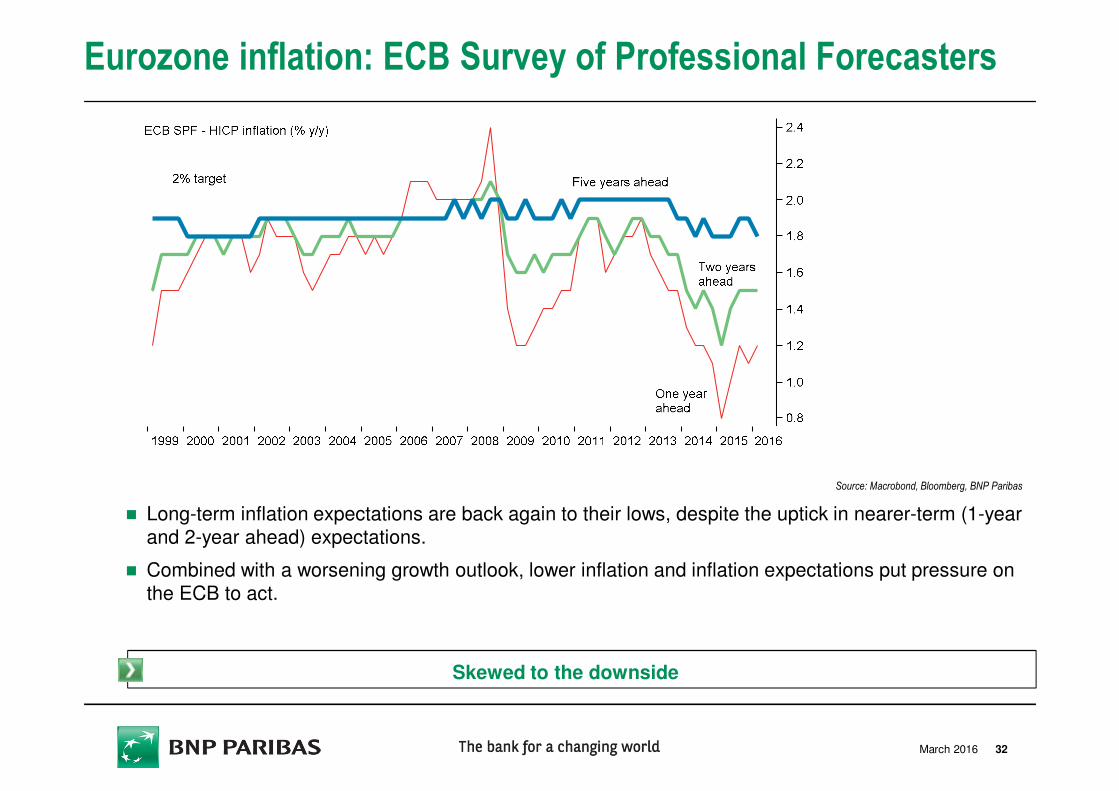

Eurozone inflation: ECB Survey of Professional Forecasters

Source: Macrobond, Bloomberg, BNP Paribas

� Long-term inflation expectations are back again to their lows, despite the uptick in nearer-term (1-year and 2-year ahead) expectations.

� Combined with a worsening growth outlook, lower inflation and inflation expectations put pressure on the ECB to act.

Skewed to the downside

32March 2016

Eurozone: Monetary policy

� Tighter financial and monetary conditions and building downside risks to growth and

inflation justified a more substantial, broader-based package of ECB measures on 10

March.

� The ECB delivered a 10bp deposit-rate cut to -0.40%.

� The monthly run-rate of asset purchases was risen by EUR 20bn, to EUR 80bn per

month.

� With policy transmission at risk of impairment due to banking-sector stress, measures

aimed at this area have also been announced, including new long-term liquidity provisions.

� The ECB’s mandate offers plenty of scope to expand its array of unconventional tools. But

the more exotic the policy, the higher the likelihood of opposition within the Governing

Council, with some members of the view that even some of the existing measures ought to

have been used only as a last resort, if deflation is imminent.

� Concern about the diminished potency of unconventional policy measures has contributed

to more turbulent markets recently. The longer it takes for such measures to be deployed,

the less likely they would be to have the desired effects.

33March 2016

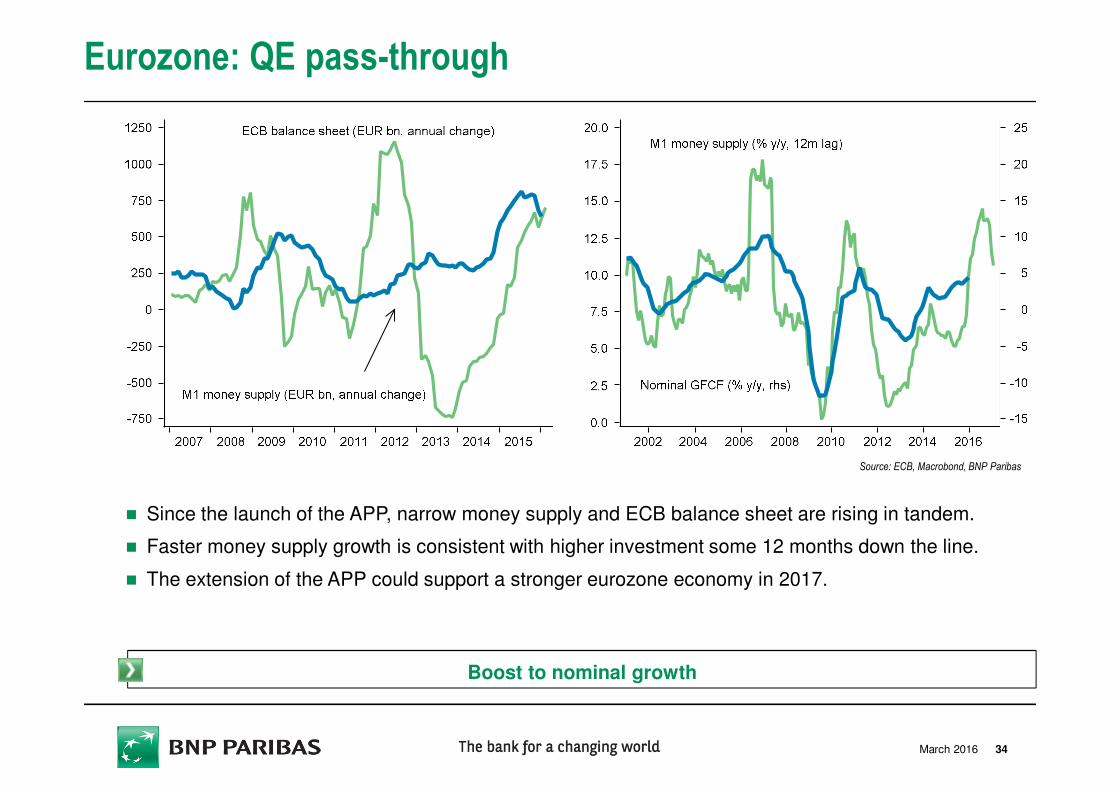

� Since the launch of the APP, narrow money supply and ECB balance sheet are rising in tandem.

� Faster money supply growth is consistent with higher investment some 12 months down the line.

� The extension of the APP could support a stronger eurozone economy in 2017.

Eurozone: QE pass-through

Source: ECB, Macrobond, BNP Paribas

Boost to nominal growth

34March 2016

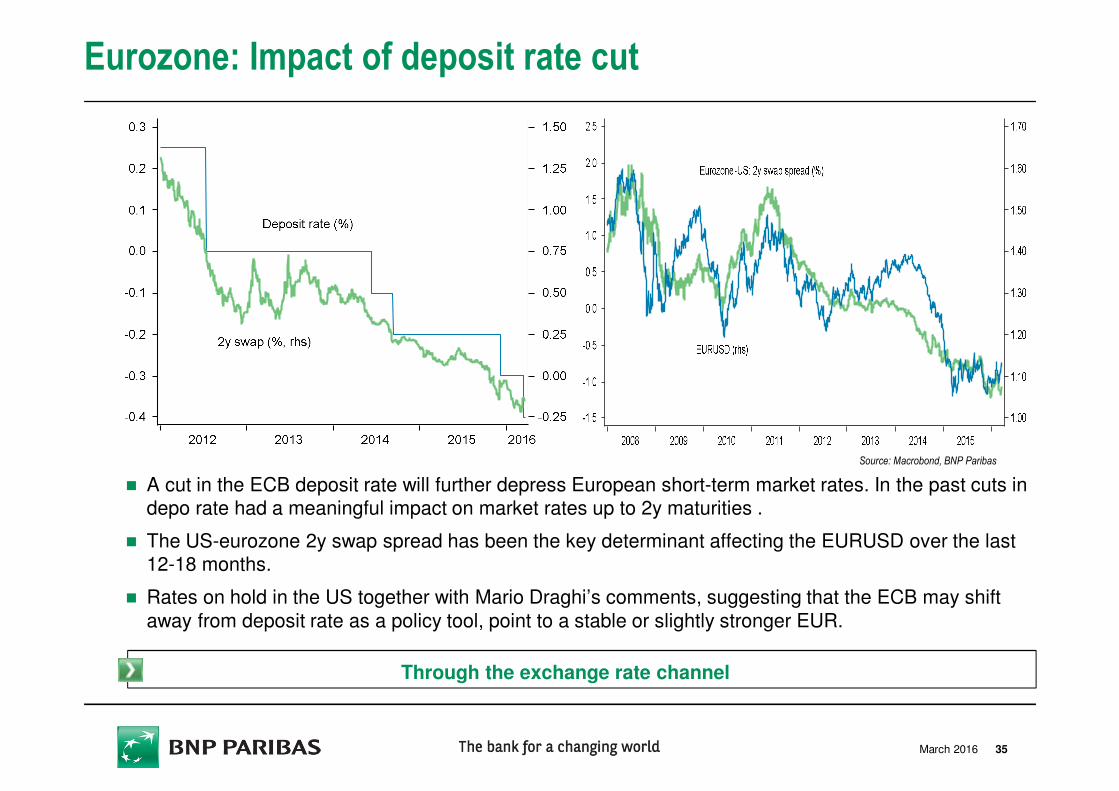

Eurozone: Impact of deposit rate cut

Source: Macrobond, BNP Paribas

� A cut in the ECB deposit rate will further depress European short-term market rates. In the past cuts in depo rate had a meaningful impact on market rates up to 2y maturities .

� The US-eurozone 2y swap spread has been the key determinant affecting the EURUSD over the last12-18 months.

� Rates on hold in the US together with Mario Draghi’s comments, suggesting that the ECB may shift

away from deposit rate as a policy tool, point to a stable or slightly stronger EUR.

Through the exchange rate channel

35March 2016

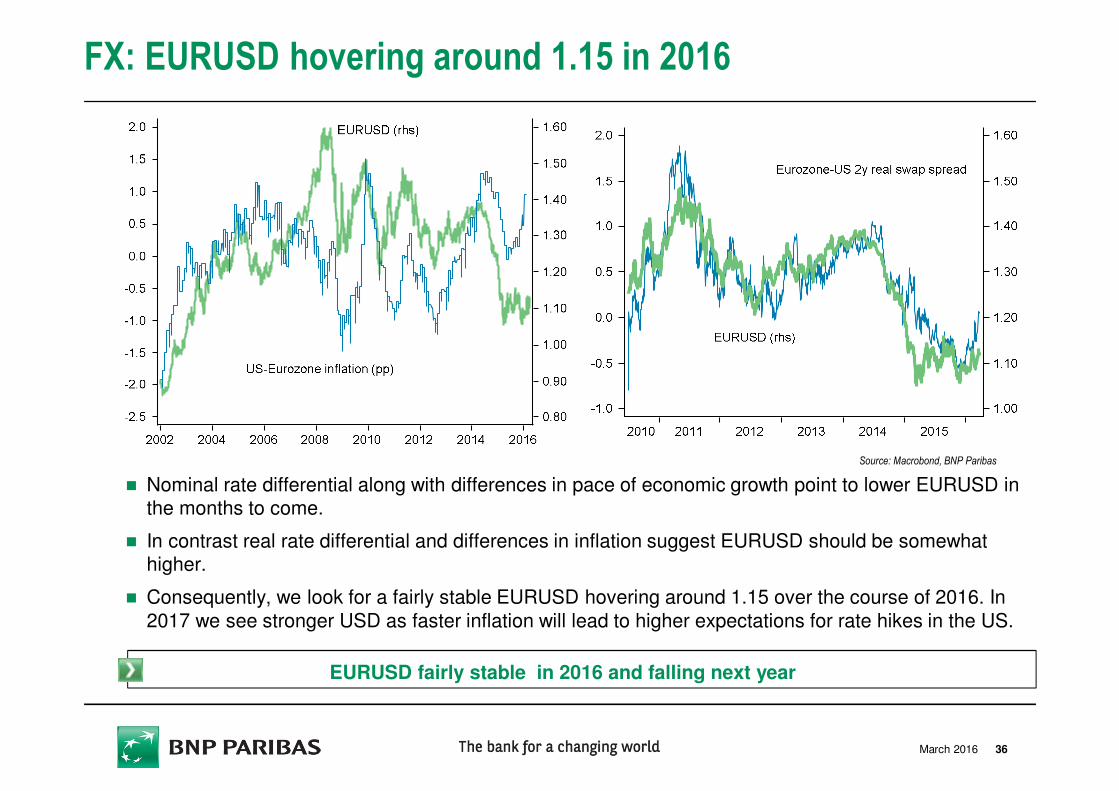

FX: EURUSD hovering around 1.15 in 2016

Source: Macrobond, BNP Paribas

� Nominal rate differential along with differences in pace of economic growth point to lower EURUSD in the months to come.

� In contrast real rate differential and differences in inflation suggest EURUSD should be somewhathigher.

� Consequently, we look for a fairly stable EURUSD hovering around 1.15 over the course of 2016. In

2017 we see stronger USD as faster inflation will lead to higher expectations for rate hikes in the US.

EURUSD fairly stable in 2016 and falling next year

36March 2016

Central Europe: Growth to remain robust

Source: Macrobond, BNP Paribas

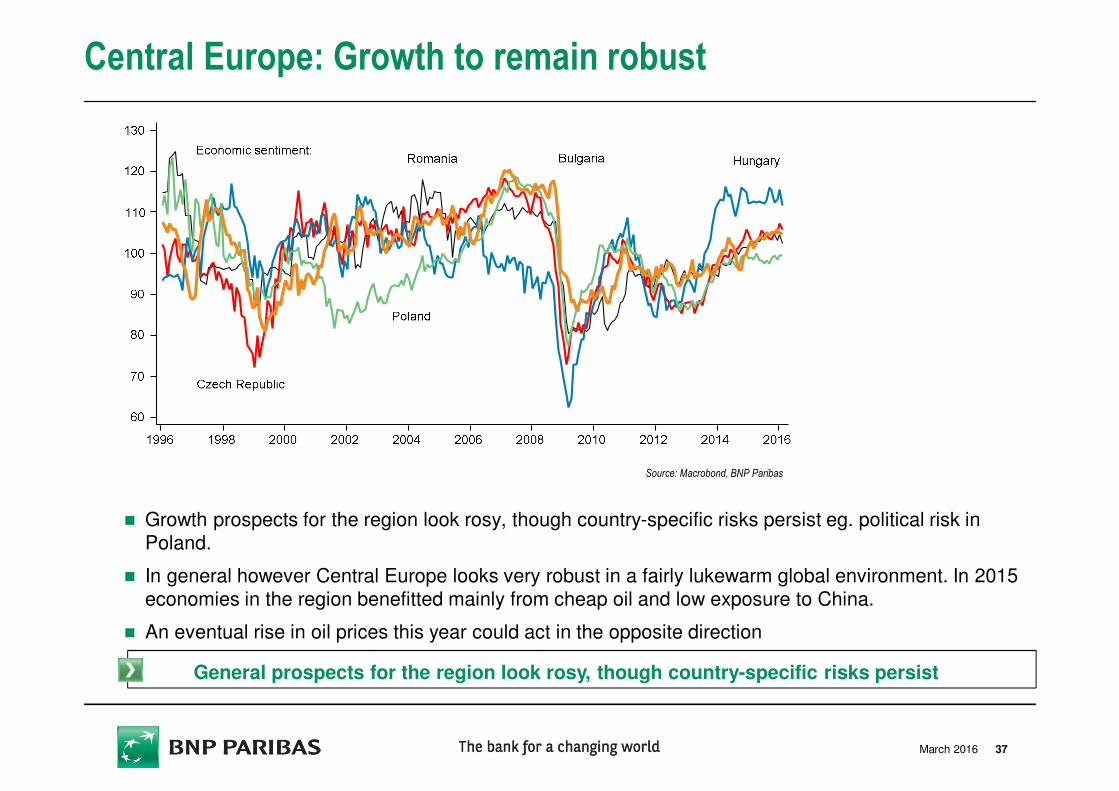

� Growth prospects for the region look rosy, though country-specific risks persist eg. political risk in Poland.

� In general however Central Europe looks very robust in a fairly lukewarm global environment. In 2015 economies in the region benefitted mainly from cheap oil and low exposure to China.

� An eventual rise in oil prices this year could act in the opposite direction

General prospects for the region look rosy, though country-specific risks persist

37March 2016

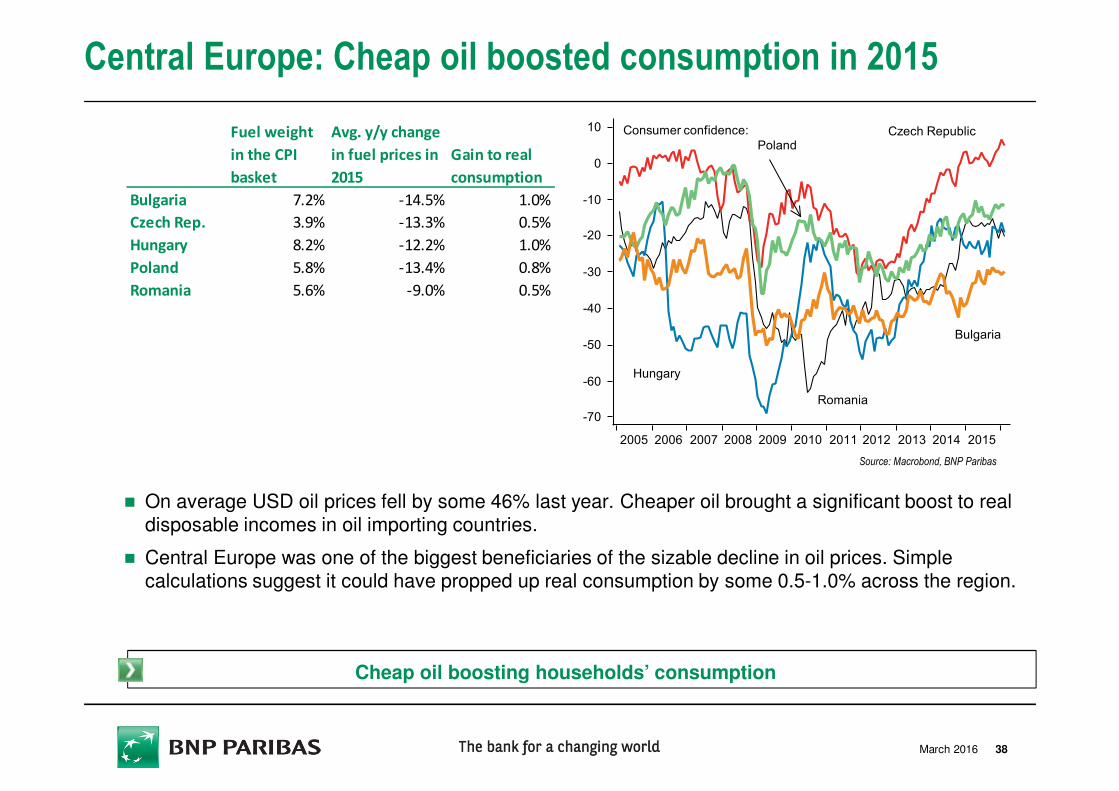

Central Europe: Cheap oil boosted consumption in 2015

Source: Macrobond, BNP Paribas

� On average USD oil prices fell by some 46% last year. Cheaper oil brought a significant boost to real disposable incomes in oil importing countries.

� Central Europe was one of the biggest beneficiaries of the sizable decline in oil prices. Simple calculations suggest it could have propped up real consumption by some 0.5-1.0% across the region.

Cheap oil boosting households’ consumption

38

Consumer confidence:

Romania

Czech Republic

Hungary

Poland

Bulgaria

-70

-60

-50

-40

-30

-20

-10

0

10

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Fuel weight

in the CPI

basket

Avg. y/y change

in fuel prices in

2015

Gain to real

consumption

Bulgaria 7.2% -14.5% 1.0%

Czech Rep. 3.9% -13.3% 0.5%

Hungary 8.2% -12.2% 1.0%

Poland 5.8% -13.4% 0.8%

Romania 5.6% -9.0% 0.5%

March 2016

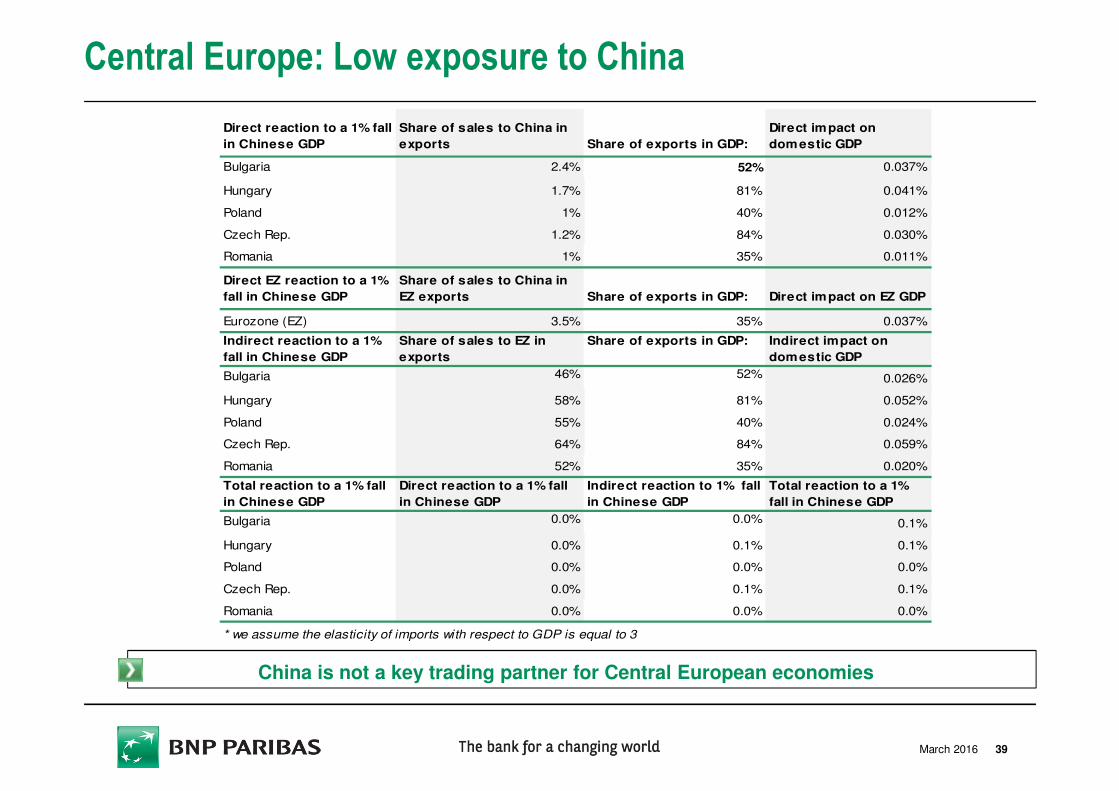

Central Europe: Low exposure to China

China is not a key trading partner for Central European economies

39

Direct reaction to a 1% fall

in Chinese GDP

Share of sales to China in

exports Share of exports in GDP:

Direct impact on

domestic GDP

Bulgaria 2.4% 52% 0.037%

Hungary 1.7% 81% 0.041%

Poland 1% 40% 0.012%

Czech Rep. 1.2% 84% 0.030%

Romania 1% 35% 0.011%

Direct EZ reaction to a 1%

fall in Chinese GDP

Share of sales to China in

EZ exports Share of exports in GDP: Direct impact on EZ GDP

Eurozone (EZ) 3.5% 35% 0.037%

Indirect reaction to a 1%

fall in Chinese GDP

Share of sales to EZ in

exports

Share of exports in GDP: Indirect impact on

domestic GDP

Bulgaria 46% 52% 0.026%

Hungary 58% 81% 0.052%

Poland 55% 40% 0.024%

Czech Rep. 64% 84% 0.059%

Romania 52% 35% 0.020%

Total reaction to a 1% fall

in Chinese GDP

Direct reaction to a 1% fall

in Chinese GDP

Indirect reaction to 1% fall

in Chinese GDP

Total reaction to a 1%

fall in Chinese GDP

Bulgaria 0.0% 0.0% 0.1%

Hungary 0.0% 0.1% 0.1%

Poland 0.0% 0.0% 0.0%

Czech Rep. 0.0% 0.1% 0.1%

Romania 0.0% 0.0% 0.0%

* we assume the elasticity of imports with respect to GDP is equal to 3

March 2016

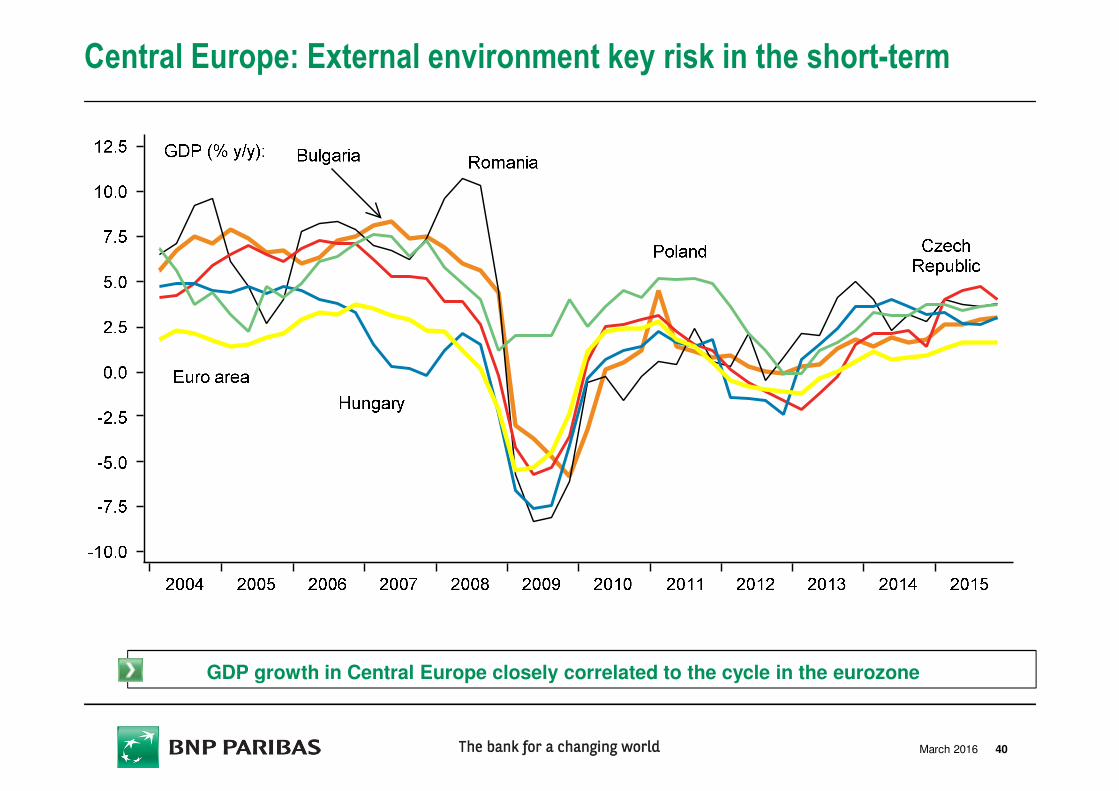

Central Europe: External environment key risk in the short-term

GDP growth in Central Europe closely correlated to the cycle in the eurozone

40March 2016

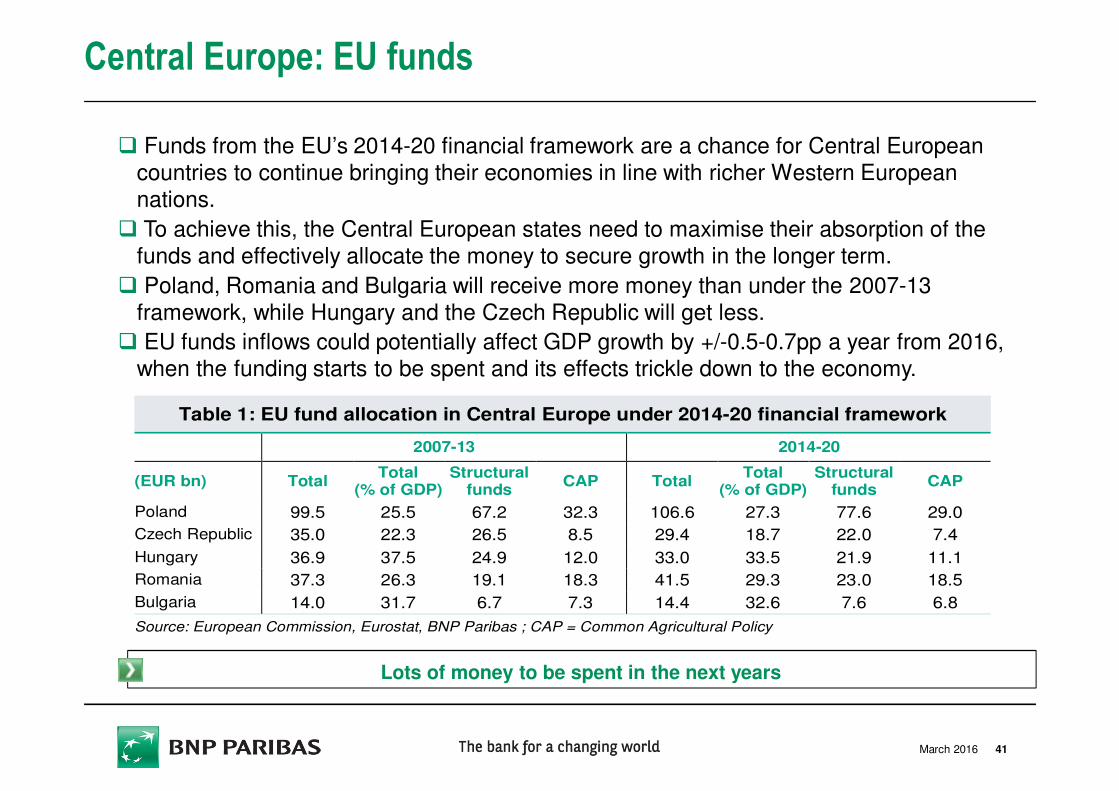

� Funds from the EU’s 2014-20 financial framework are a chance for Central European

countries to continue bringing their economies in line with richer Western European

nations.

� To achieve this, the Central European states need to maximise their absorption of the

funds and effectively allocate the money to secure growth in the longer term.

� Poland, Romania and Bulgaria will receive more money than under the 2007-13

framework, while Hungary and the Czech Republic will get less.

� EU funds inflows could potentially affect GDP growth by +/-0.5-0.7pp a year from 2016,

when the funding starts to be spent and its effects trickle down to the economy.

Central Europe: EU funds

Lots of money to be spent in the next years

41

Table 1: EU fund allocation in Central Europe under 2014-20 financial framework

2007-13 2014-20

(EUR bn) Total Total

(% of GDP) Structural

funds CAP Total

Total (% of GDP)

Structural funds

CAP

Poland 99.5 25.5 67.2 32.3 106.6 27.3 77.6 29.0

Czech Republic 35.0 22.3 26.5 8.5 29.4 18.7 22.0 7.4

Hungary 36.9 37.5 24.9 12.0 33.0 33.5 21.9 11.1

Romania 37.3 26.3 19.1 18.3 41.5 29.3 23.0 18.5

Bulgaria 14.0 31.7 6.7 7.3 14.4 32.6 7.6 6.8

Source: European Commission, Eurostat, BNP Paribas ; CAP = Common Agricultural Policy

March 2016

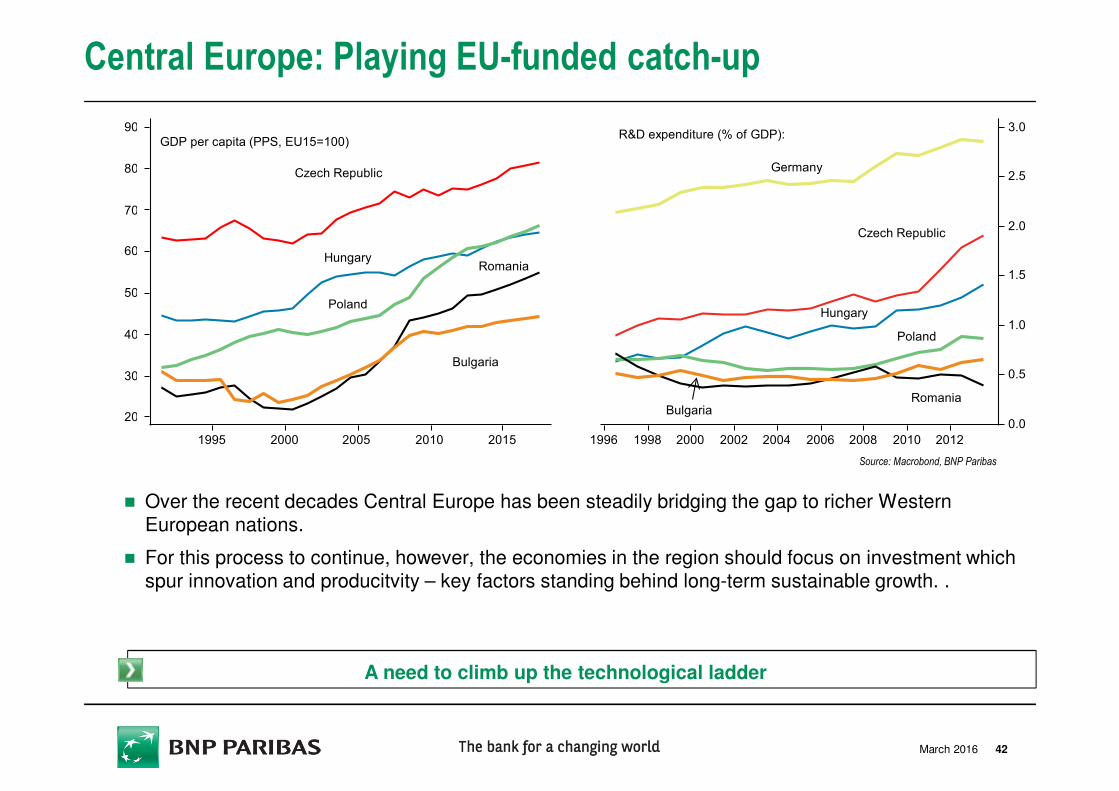

Central Europe: Playing EU-funded catch-up

Source: Macrobond, BNP Paribas

� Over the recent decades Central Europe has been steadily bridging the gap to richer Western European nations.

� For this process to continue, however, the economies in the region should focus on investment whichspur innovation and producitvity – key factors standing behind long-term sustainable growth. .

A need to climb up the technological ladder

42

GDP per capita (PPS, EU15=100)

Czech Republic

HungaryRomania

Poland

Bulgaria

20

30

40

50

60

70

80

90

1995 2000 2005 2010 2015

R&D expenditure (% of GDP):

Czech Republic

Hungary

Poland

Germany

RomaniaBulgaria

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1996 1998 2000 2002 2004 2006 2008 2010 2012

March 2016

Disclaimer

February 2016

IMPORTANT DISCLOSURES: Please see important disclosures in the text of this report

The information and opinions contained in this report have been obtained from, or are based on, public sourcesbelieved to be reliable, but no representation or warranty, express or implied, is made that such information isaccurate, complete or up to date and it should not be relied upon as such. This report does not constitute anoffer or solicitation to buy or sell any securities or other investment. Information and opinions contained in thereport are published for the assistance of recipients, but are not to be relied upon as authoritative or taken insubstitution for the exercise of judgement by any recipient, are subject to change without notice and notintended to provide the sole basis of any evaluation of the instruments discussed herein. Any reference to pastperformance should not be taken as an indication of future performance. To the fullest extent permitted by law,no BNP Paribas group company accepts any liability whatsoever (including in negligence) for any direct orconsequential loss arising from any use of or reliance on material contained in this report. All estimates andopinions included in this report are made as of the date of this report. Unless otherwise indicated in this reportthere is no intention to update this report. BNP Paribas SA and its affiliates (collectively “BNP Paribas”) maymake a market in, or may, as principal or agent, buy or sell securities of any issuer or person mentioned in thisreport or derivatives thereon. Prices, yields and other similar information included in this report are included forinformation purposes. Numerous factors will affect market pricing and there is no certainty that transactionscould be executed at these prices.BNP Paribas may have a financial interest in any issuer or person mentioned in this report, including a long orshort position in their securities and/or options, futures or other derivative instruments based thereon, or viceversa. BNP Paribas, including its officers and employees may serve or have served as an officer, director or inan advisory capacity for any person mentioned in this report. BNP Paribas may, from time to time, solicit,perform or have performed investment banking, underwriting or other services (including acting as adviser,manager, underwriter or lender) within the last 12 months for any person referred to in this report. BNP Paribasmay be a party to an agreement with any person relating to the production of this report. BNP Paribas, may tothe extent permitted by law, have acted upon or used the information contained herein, or the research oranalysis on which it was based, before its publication. BNP Paribas may receive or intend to seekcompensation for investment banking services in the next three months from or in relation to any personmentioned in this report. Any person mentioned in this report may have been provided with sections of thisreport prior to its publication in order to verify its factual accuracy.This report was produced by a BNP Paribas group company. This report is for the use of intended recipientsand may not be reproduced (in whole or in part) or delivered or transmitted to any other person without the priorwritten consent of BNP Paribas. By accepting this document you agree to be bound by the foregoinglimitations.Certain countries within the European Economic Area:This report is solely prepared for professional clients. It is not intended for retail clients and should not bepassed on to any such persons.UK: This report has been approved for publication in the United Kingdom by BNP Paribas London Branch. 10Harewood Avenue, London NW1 6AA; tel: +44 20 7595 2000; fax: +44 20 7595 2555- www.bnpparibas.com.Incorporated in France with Limited Liability. Registered Office: 16 boulevard des Italiens, 75009 Paris, France.662 042 449 RCS Paris. BNP Paribas London Branch is lead supervised by the European Central Bank (ECB)and the Autorité de Contrôle Prudentiel et de Résolution (ACPR). BNP Paribas London Branch is authorised bythe ECB, the ACPR and the Prudential Regulation Authority and subject to limited regulation by the FinancialConduct Authority and Prudential Regulation Authority. Details about the extent of our authorisation andregulation by the Prudential Regulation Authority, and regulation by the Financial Conduct Authority areavailable from us on request. BNP Paribas London Branch is registered in England and Wales under no.FC13447.France: This report has been approved for publication in BNP Paribas, incorporated in France with LimitedLiability (Registered Office: 16 boulevard des Italiens, 75009 Paris, France, 662 042 449 RCS Paris,www.bnpparibas.com) is authorized and supervised by European Central Bank (ECB) and by Autorité deContrôle Prudentiel et de Résolution (ACPR) in respect of supervisions for which the competence remains atnational level, in terms of Council Regulation n°1024/2013 of 15 October 2013 conferring specific tasks on theECB concerning policies relating to the prudential supervision of credit institutions.Germany: This report is being distributed in Germany by BNP Paribas S.A. Niederlassung Deutschland, abranch of BNP Paribas S.A. whose head office is in Paris, France. 662 042 449 RCS Paris,

www.bnpparibas.com). BNP Paribas Niederlassung Deutschland is authorized and lead supervised by theEuropean Central Bank (ECB) and by Autorité de Contrôle Prudentiel et de Résolution (ACPR) and issubject to limited supervision and regulation by Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin) inrespect of supervisions for which the competence remains at national level, in terms of Council Regulationn° 2013/1024 of 15 October 2013 conferring specific tasks on the ECB concerning policies relating to theprudential supervision of credit institutions as well as Council Directive n°2013/36/EU of 26 June, 2013 andSection 53b German Banking Act (Kreditwesengesetz - KWG) providing for the principles of sharedsupervision between the national competent authorities in case of branches and applicable national rulesand regulations. BNP Paribas Niederlassung Deutschland is registered with locations at Europa Allee 12,60327 Frankfurt (commercial register HRB Frankfurt am Main 40950) and Bahnhofstrasse 55, 90429Nuremberg (commercial register Nuremberg HRB Nürnberg 31129).Belgium: BNP Paribas Fortis SA/NV is authorized and supervised by European Central Bank (ECB) and bythe National Bank of Belgium, boulevard de Berlaimont 14, 1000 Brussels, and is also under the supervisionon investor and consumer protection of the Financial Services and Markets Authority (FSMA), rue ducongrès 12-14, 1000 Brussels and is authorized as insurance agent under FSMA number 25789 AIreland: This report is being distributed in Ireland by BNP Paribas S.A., Dublin Branch. BNP Paribas isincorporated in France as a Société Anonyme and regulated in France by the European Central Bank andby the Autorité de Contrôle Prudentiel et de Résolution.Netherlands: This report is being distributed in the Netherlands by BNP Paribas Fortis SA/NV, NetherlandsBranch, a branch of BNP Paribas SA/NV whose head office is in Brussels, Belgium. BNP Paribas FortisSA/NV, Netherlands Branch, Herengracht 595, 1017 CE Amsterdam, is authorised and supervised by theEuropean Central Bank (ECB) and the National Bank of Belgium and is also supervised by the BelgianFinancial Services and Markets Authority (FSMA) and it is subject to limited regulation by the NetherlandsAuthority for the Financial Markets (AFM) and the Dutch Central Bank (De Nederlandsche Bank).Portugal: BNP Paribas – Sucursal em Portugal Avenida 5 de Outubro, 206, 1050-065 Lisboa, Portugal.www.bnpparibas.com. Incorporated in France with Limited Liability. Registered Office: 16 boulevard desItaliens, 75009 Paris, France. 662 042 449 RCS Paris. BNP Paribas – Sucursal em Portugal is leadsupervised by the European Central Bank (ECB) and the Autorité de Contrôle Prudentiel et de Résolution(ACPR). BNP Paribas - Sucursal em Portugal is authorized by the ECB, the ACPR and Resolution and it isauthorized and subject to limited regulation by Banco de Portugal and Comissão do Mercado de ValoresMobiliários. BNP Paribas - Sucursal em Portugal is registered in C.R.C. of Lisbon under no. NIPC980000416. VAT Number PT 980 000 416.”Spain: This report is being distributed in Spain by BNP Paribas S.A., S.E., a branch of BNP Paribas S.A.whose head office is in Paris, France (Registered Office: 16 boulevard des Italiens, 75009 Paris, France).BNP Paribas S.A., S.E., C/Ribera de Loira 28, Madrid 28042 is authorised and supervised by the EuropeanCentral Bank (ECB) and the Autorité de Contrôle Prudentiel et de Résolution (ACPR) and subject to limitedregulation by the Bank of Spain.United States: This report is being distributed to US persons by BNP Paribas Securities Corp., or by asubsidiary or affiliate of BNP Paribas that is not registered as a US broker-dealer to US major institutionalinvestors only. BNP Paribas Securities Corp., a subsidiary of BNP Paribas, is a broker-dealer registered withthe U.S. Securities and Exchange Commission and a member of the Financial Industry Regulatory Authorityand other principal exchanges. For the purposes of, and to the extent subject to, §§ 1.71 of the U.S.Commodity Exchange Act, this report is a general solicitation of derivatives business. BNP ParibasSecurities Corp. accepts responsibility for the content of a report prepared by another non-U.S. affiliate onlywhen distributed to U.S. persons by BNP Paribas Securities Corp.Brazil: This report was prepared by Banco BNP Paribas Brasil S.A. or by its subsidiaries, affiliates andcontrolled companies, together referred to as "BNP Paribas", for information purposes only and do notrepresent an offer or request for investment or divestment of assets. Banco BNP Paribas Brasil S.A. is afinancial institution duly incorporated in Brazil and duly authorized by the Central Bank of Brazil and by theBrazilian Securities Commission to manage investment funds. Notwithstanding the caution to obtain andmanage the information herein presented, BNP Paribas shall not be responsible for the accidentalpublication of incorrect information, nor for investment decisions taken based on the information containedherein, which can be modified without prior notice. Banco BNP Paribas Brasil S.A. shall not be responsibleto update or revise any information contained herein. Banco BNP Paribas Brasil S.A. shall not beresponsible for any loss caused by the use of any information contained herein. 43

Disclaimer (cont)

February 2016

IMPORTANT DISCLOSURES: Please see important disclosures in the text of this report

Israel: BNP Paribas does not hold a licence under the Investment Advice and Marketing Law of Israel, to offerinvestment advice of any type, including, but not limited to, investment advice relating to any financial products”

South Africa: BNP Paribas Securities South Africa (Pty) Ltd (Registration number 1996/009716/07) is a licensedmember of the Johannesburg Stock Exchange and an authorised Financial Services Provider (FSP 29451) interms of the Financial Advisory and Intermediary Services Act, 37 of 2002. Any view or opinion expressed in thisreport does not constitute advice and the recipient should obtain their own advice prior to making any decision ortaking any action whatsoever based hereon.

Japan: This report is being distributed to Japanese based firms by BNP Paribas Securities (Japan) Limited or bya subsidiary or affiliate of BNP Paribas not registered as a financial instruments firm in Japan, to certain financialinstitutions defined by article 17-3, item 1 of the Financial Instruments and Exchange Law Enforcement Order.BNP Paribas Securities (Japan) Limited is a financial instruments firm registered according to the FinancialInstruments and Exchange Law of Japan and a member of the Japan Securities Dealers Association and theFinancial Futures Association of Japan. BNP Paribas Securities (Japan) Limited accepts responsibility for thecontent of a report prepared by another non-Japan affiliate only when distributed to Japanese based firms byBNP Paribas Securities (Japan) Limited. Some of the foreign securities stated on this report are not disclosedaccording to the Financial Instruments and Exchange Law of Japan.

Hong Kong: This report is being distributed in Hong Kong by BNP Paribas Hong Kong Branch, a branch of BNPParibas whose head office is in Paris, France. BNP Paribas Hong Kong Branch is registered as a Licensed Bankunder the Banking Ordinance and regulated by the Hong Kong Monetary Authority. BNP Paribas Hong KongBranch is also a Registered Institution regulated by the Securities and Futures Commission for the conduct ofRegulated Activity Types 1, 4 and 6 under the Securities and Futures Ordinance.

Singapore: BNP Paribas Singapore Branch is regulated in Singapore by the Monetary Authority of Singaporeunder the Banking Act, the Securities and Futures Act and the Financial Advisers Act. This report may not becirculated or distributed, whether directly or indirectly, to any person in Singapore other than (i) to an institutionalinvestor pursuant to Section 274 of the Securities and Futures Act, Chapter 289 of Singapore ("SFA"), (ii) to anaccredited investor or other relevant person, or any person under Section 275(1A) of the SFA, pursuant to and inaccordance with the conditions specified in Section 275 of the SFA or (iii) otherwise pursuant to, and inaccordance with the conditions of, any other applicable provisions of the SFA.

South Korea: Branch: BNP Paribas Seoul Branch is regulated by the Financial Services Commission andFinancial Supervisory Service for the conduct of its financial investment business in the Republic of Korea.This report does not constitute an offer to sell to or the solicitation of an offer to buy from any person anyfinancial products where it is unlawful to make the offer or solicitation in South Korea.Securities: BNP Paribas Securities Korea is registered as a Licensed Financial Investment Business Entityunder the FINANCIAL INVESTMENT SERVICES AND CAPITAL MARKETS ACT and regulated by theFinancial Supervisory Service and Financial Services Commission. This report does not constitute an offerto sell to or the solicitation of an offer to buy from any person any financial products where it is unlawful tomake the offer or solicitation in South Korea.

Taiwan: BNP Paribas Taipei Branch is registered as a licensed bank under the Banking Act and regulatedby the Financial Supervisory Commission, R.O.C. This report is directed only at Taiwanese counterpartieswho are licensed or who have the capacities to purchase or transact in such products. This report does notconstitute an offer to sell to or the solicitation of an offer to buy from any person any financial productswhere it is unlawful to make the offer or solicitation in Taiwan.

Australia: This material, and any information in related marketing presentations (the Material), is beingdistributed in Australia by BNP Paribas ABN 23 000 000 117, a branch of BNP Paribas 662 042 449 R.C.S.,a licensed bank whose head office is in Paris, France. BNP Paribas is licensed in Australia as a ForeignApproved Deposit-taking Institution by the Australian Prudential Regulation Authority (APRA) and deliversfinancial services to Wholesale clients under its Australian Financial Services Licence (AFSL) No. 238043which is regulated by the Australian Securities & Investments Commission (ASIC).The Material is directed toWholesale clients only and is not intended for Retail clients (as both terms are defined by the CorporationsAct 2001, sections 761G and 761GA). The Material is subject to change without notice and BNP Paribas isunder no obligation to update the information or correct any inaccuracy that may appear at a later date.

Some or all of the information contained in this report may already have been published onhttps://globalmarkets.bnpparibas.com

© BNP Paribas (2016). All rights reserved.

44