Embed Size (px)

Citation preview

PROJECT ON

STOCK EXCHANGE SCAM IN INDIA WITH REFERENCE TO

HARSHAD MEHTA

BACHELOR OF COMMERCE

FINANCIAL MARKETS

SEMISTER V

2010 – 2011

PROJECT GUIDE AND COURSE CO-ORDINATOR:

Prof. Mahek. Mansuri

Prof. Shruti. Chavarkar

SUBMITTED BY

ASHISH. MANSUKHBHAI. THAKKAR

ROLL NO. 51

S.K.SOMAIYA COLLEGE OF

ARTS, SCIENCE & COMMERCE

MUMBAI UNIVERSITY

ACKNOWLEDGEMENT

The success of any project is never limited to individual undertaking

project; it is a collective effort at people around, that spell success. This

acknowledgement is humble attempt of earnestly thanking all those who

were directly or indirectly involved in this project.

We would like to extend our sincere, heartfelt gratitude to our head of

department, Prof. Shruti Charvarkar and our internal guide Prof. Mahek.

Mansuri under whose guidance we had the privilege of working and

learning and whose constant inspiration at all faces of the project lead to

the successful completion of our work.

Last but not the last we express our deepest regards to our principal Dr.

Sangitha Kohli . I also want to thank to all the staff members who had

helped me to make this project worthfull.

INDEX

SR.

No

TOPIC PAGE

1 EXECUTIVE SUMMARY

2 PURPOSE, SCOPE & OBJECTIVE

3 INTRODUCTION TO BOMBAY STOCK EXCHANGE

4 INTORDUCTION TO NATIONAL STOCK EXCHANGE

5 ORIGIN OF INDIAN STOCK MARKET

6 Securities and Exchange Board of India (SEBI)

7 THE 1992 SECURITIES SCAM

8 Conclusion

Executive Summary:-

The project deals with the biggest scam in the history of Indian Securities Market.

HARSHAD MEHTA SCAM.

The first chapter deals with the introduction to the STOCK EXCHANGE,

in which shows the exact meaning of stock. It also deals in the working of the

stock market and how the stock are traded in the stock exchanges.

The second chapter deals with the National Stock Exchange and its existience ,

how it functions and what types of regulations are imposed on companies inorder

to trade in the stock exchange is concerned.

The third chapter deals with the Origin Of Indian Stock Exchange, as and when

our stock market started and history of the stock exchange.

The fourth chapter deals with the regulations of the securities market , deals with

SEBI functions & powers .

Last but not the least , the fifth chapter confronts the actual scam of HARSHAD

MEHTA , the making , the exposure , the history of the concerned person and the

end of the culprit .

This project throws the light on the scam of Mr. HARSHAD MEHTA, what

exactly was he trying to do and at what point he ended .

Purpose and Scope of study:-

To analyze the way that how did the scam came into existience and what

things have instigate this man to end up with a huge scam in the history

of Indian Stock Market.

Objective :-

To throw a light on the scam .

To know how the legal procedures goes on .

To know about the ultimate outcome of the scam.

STOCK EXCHANGE SCAM IN INDIA

WITH REFERENCE TO

HARSHAD MEHTA

1. INTRODUCTION TO BOMBAY STOCK

EXCHANGE:-

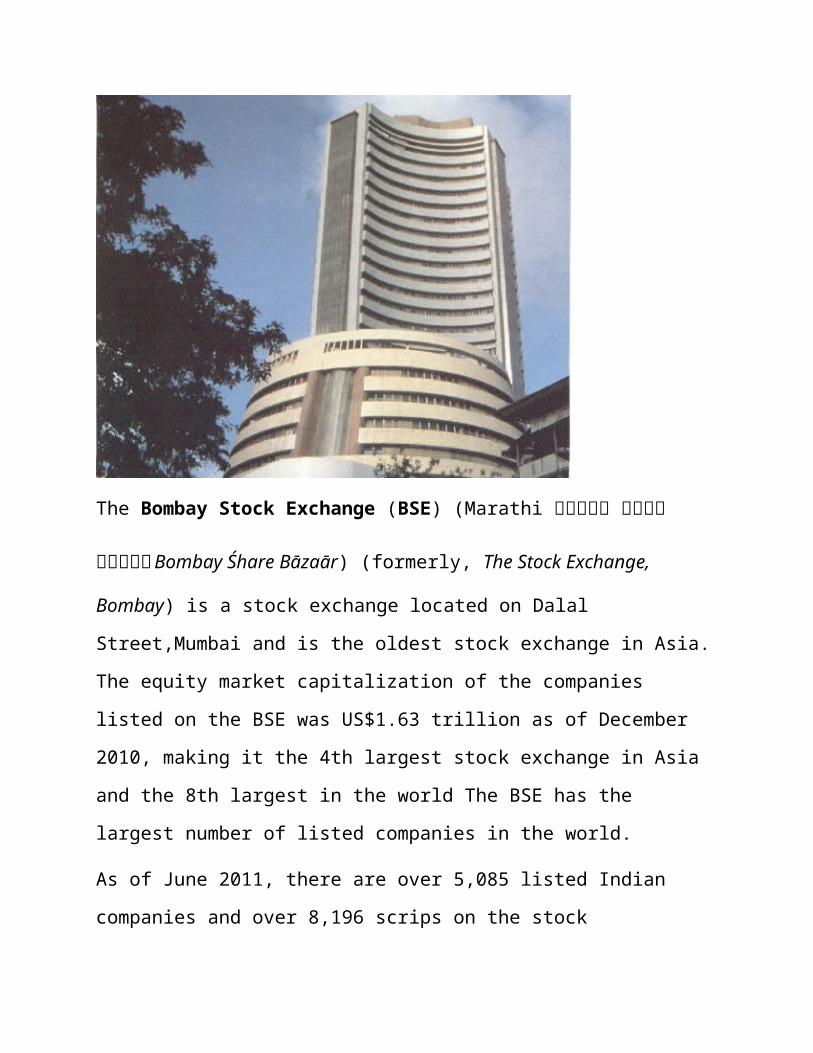

1.1 BOMBAY STOCK EXCHANGE:-

The Bombay Stock Exchange (BSE) (Marathi मुं��बई शे�अर बजार Bombay Śhare

Bāzaār) (formerly, The Stock Exchange, Bombay) is a stock exchange located

on Dalal Street,Mumbai and is the oldest stock exchange in Asia. The

equity market capitalization of the companies listed on the BSE

was US$1.63 trillion as of December 2010, making it the 4th largest stock

exchange in Asia and the 8th largest in the world The BSE has the largest number

of listed companies in the world.

As of June 2011, there are over 5,085 listed Indian companies and over

8,196 scrips on the stock exchange, the Bombay Stock Exchange has a significant

trading volume. The BSE SENSEX, also called "BSE 30", is a widely used market

index in India and Asia. Though many other exchanges exist, BSE and

the National Stock Exchange of India account for the majority of the equity

trading in India. While both have similar total market capitalization (about USD

1.6 trillion), share volume in NSE is typically two times that of BSE.

1.2 Share Market:-

A Share market or Stock market, is a private or public market for the trading

of company stock and derivatives of company stock at an agreed price; these are

securities listed on a stock exchange as well as those only traded privately.The

stocks are listed and traded on stock exchanges which are entities a corporation or

mutual organization specialized in the business of bringing buyers and sellers of

the organizations to a listing of stocks and securities together.

Stock market is known as the cradle of capitalism. It is a place where

companies come to raise their share capital and investors go to invest their surplus

funds. Stock market essentially discharges the functions of "the invisible hand" that

channels investment into the most productive ventures so as to optimize the overall

productivity of the economy.

Stock Market is a place where financial instruments like shares, debentures,

commercial papers, bonds etc are bought and sold. Stock markets are popularly

known as stock exchanges. There are many popular stock markets in the world.

NASDQ, Tokyo Stock Exchange, London Stock Exchange are the most popular of

the lot. There are many participants in a stock market. Investors, Speculators,

Arbitrators, Traders are different type of participants of a Stock

Market. Brokers are intermediaries who bring together various participants

in a Stock Market.

Most important function of the stock market is to facilitate trading of

financial instruments. Brokers submit a quote at the stock market on behalf of

their clients. Quotes are specific to the scrip. The quote of the buyer is matched to

the quote of the seller and the transaction takes place. All transactions entered in a

stock market are guaranteed by the Stock Exchange. That means if the buyer or

seller fails to meet his obligation, the stock exchange steps in and meets the

commitment of the participant. This instills a lot of confidence and credibility

about the sanctity of the transaction amongst the investing public. That is the

reason why a stock exchange is preferred by investing public to a gray market in

shares even though the latter has much lower transaction cost.

All the participants in the stock market have the same objective i.e. to make

a profit. Investors invest in the stock market with the hope that market value of

their investment will go up and they will be able to make higher returns than in

bank deposits. Arbitrages buy in one market and sell in another market with an

objective of making a profit. For example if the shares of Caltex are quoting at a

lesser price at Amsterdam Stock Exchange in comparison to London Stock

Exchange, arbitrages will buy at Amsterdam and sell at London. This will result in

a rise in share price at Amsterdam and fall in share price at London, thus bringing

in price equilibrium among various stock markets in the world.

Speculators operate in the stock market with an objective to make quick

money by guessing the direction of the stock market. If they expect the market to

rise, they buy shares with a very small investment horizon. Similarly if they expect

a correction in stock market, they sell shares, thus imparting an essential element

of liquidity in the market. Those who expect a rise in the stock market and buy

relentlessly are known as bulls. Bulls keep the buying pressure and attempt to

take the stock market to dizzy heights. Bull market is a market scenario where

bulls have complete control over the stock markets. When bull market reaches its

peak, investors will make huge profit. Many investors start booking their profit by

selling the investments. Slowly the bulls find that there are more shares than

they could perhaps buy in the stock market. When supply of shares exceeds the

demand in the stock market prices start coming down. This is called correction.

Correction is a normal phenomenon in any bull market. Some times if the sellers

are huge in numbers, a negative sentiment takes over the stock market. Every

one attempts to sell their investments with an objective to salvage profit or

reduce losses. When this phase set in, bulls loose control. Sellers will control

stock market. This phase is popularly known are bear run. Bull and Bear runs

follow a cyclical pattern in a stock market.

Normally in a booming economy, companies make huge profits, so markets tend to

be bullish. When the trend of the economy reverses Stock Market experience a

bear hug. Thus the Stock markets reflect the health if the economy and are often

called as "barometers" of the economy.

1.3 Stock

Plain and simple, a “stock” is a share in the ownership of a company. A

stock represents a claim on the company's assets and earnings. As you acquire

more stocks, your ownership stake in the company becomes greater.

(Note: Some times different words like shares, equity, stocks etc. are used.

All these words mean the same thing.)

1.4 Shares in the Share Market are either traded through

(a) Stock Exchange

(b) Over-the -Counter (OTC)

(a) Stock Exchange

These are organized market places where stocks, bonds are other equivalents

are traded between the buyers and sellers where exchange acts as a counter-party to

both the participants in case of any default. The contracts are standardized and not

customized ones. For example, NYSE, NASDAQ, NSE, NIKKEI, etc.

(b) Over-the -Counter (OTC)

These are not centralized exchanges. Here, the trade takes place

through a network of dealers. Generally, the OTC contracts are bilateral

customized contracts and not standardized ones.

Important Participants of Share Market Trading are :-

Buyer An investor who buys a script in the belief that the market will

rise. If his hinge becomes right then he makes profit otherwise he suffers

loss.

Seller Seller of a stock sells in the hope that the stock price will go

down.

Stock Broker Brokers are persons or firms who execute buy/sell

order on behalf of the investors and charge a commission for rendering

the service.

1.5 Share Trading are done in three ways

(a)Offline Share Trading

(b)Online Share Trading

(c) Open Outcry Trading

(a) Offline Share Trading

In this form of trading the customer either goes to the share broker's place

and sits before the share trading terminal and asks the dealer to place orders in his

account. or rings the share broker, asks the share quotes and other relevant

informations, and accordingly places orders over the phone.

(b) Online Share Trading

The client could avail the share market and could place his order on his own

from any place he wants, provided he has a computer with an Internet connection.

(c) Open Outcry Trading

Here, the investors put their orders through the brokers and these share

brokers in turn place and execute orders on behalf of them on the floor of the

exchange. These brokers gather in a particular place on the trading floor known as

Trading Post. There is a person called as the Specialist present in the trading post

who does the matching of the buy and sell orders. This type of auction method is

called Open Outcry Method.

1.6 Online Share Trading

Online Share Trading is becoming the order of the day in share trading.

Now-a-days one could hardly see a person going to the stock exchange floor and

placing his order. Electronic media has played an important role in flourishing the

share market. In case of online share trading an investor could place his order from

his own house if he has internet connection.

There are two types of trading that can be done through online

share trading

1. Intra-day Trading

2. Delivery Trading

(1) Intra-day Trading

They enter and exit out of the market like the thief in the night. Traders

continuously have a watch on the market during the trading hours and the moment

they see any opportunity arising they pounce on it for scalping the profit out. These

type of trading generally are risky in nature. They buy and sell stocks during the

same day.

Intra day Traders are of two types :-

a. Scalp Traders

b. Momentum Traders

a. Scalp Traders

Investors who perform many trades per day for scalping out small profits out of the

bid-ask spread from each trade are known as scalp traders.

b. Momentum Traders

Investors who pounce on those stocks which move significantly in one

direction and book desired profit are called momentum traders. They do this within

a day.

1.7 Delivery trading

The investor buys the share for holding purposes. The brokerage charges are

a bit more than the intraday ones. Delivery Traders are :

a. Technical Traders

b. Fundamental Traders

c. Swing Traders

a. Technical Traders

They believe that buying/selling signals are present within the graphs and

charts of the stock.

b. Fundamental Traders

They perform trade on the basis of study of fact-sheets of the company like

historical profit graph, balance sheet, anticipated earning reports, stock splits,

mergers and acquisitions, etc.

c. Swing Traders

They are basically fundamental traders who take delivery of trades

for a span of short period generally more than one day.

In this electronic form of trading, the shares are not in the physical

form for their inconvenience to handle. So, they are now converted to

dematerialized form . So, one investor does not have to worry about the

safety of the physical shares because the bought shares get transferred to

the respective D-mat account . Thus, online share trading has helped the

investors a lot as it is hassle-free and time efficient.

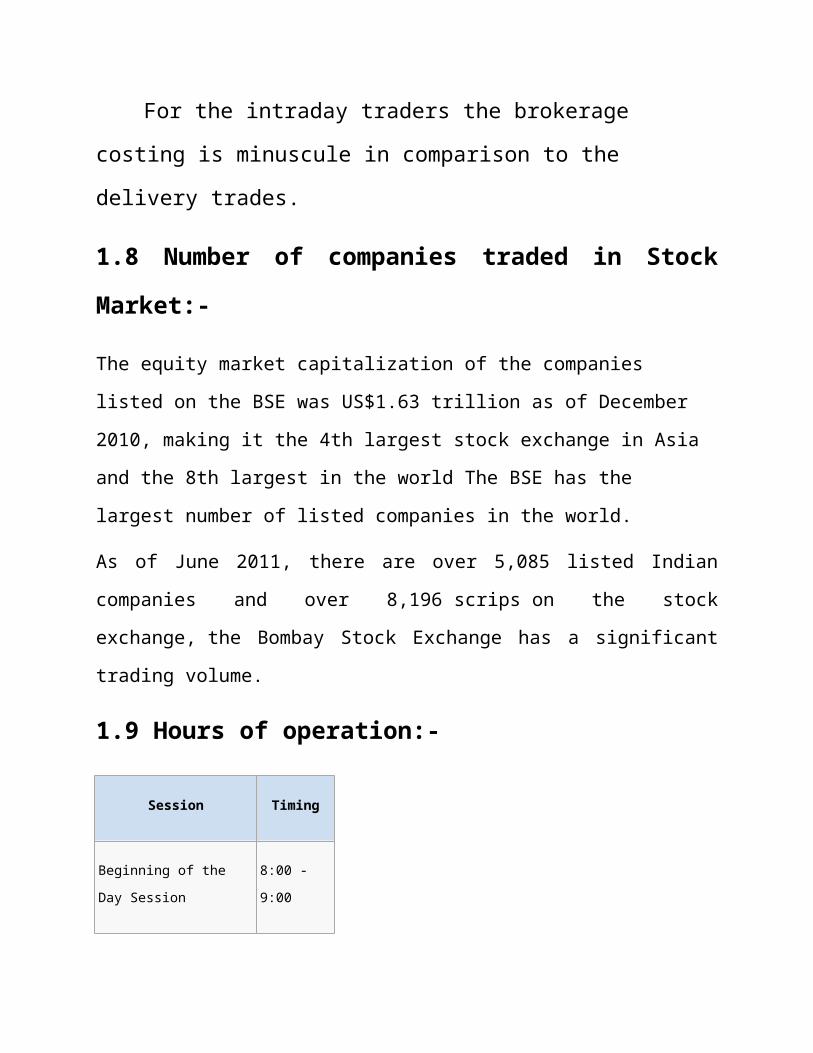

For the intraday traders the brokerage costing is minuscule in

comparison to the delivery trades.

1.8 Number of companies traded in Stock Market:-

The equity market capitalization of the companies listed on the BSE

was US$1.63 trillion as of December 2010, making it the 4th largest stock

exchange in Asia and the 8th largest in the world The BSE has the largest number

of listed companies in the world.

As of June 2011, there are over 5,085 listed Indian companies and over

8,196 scrips on the stock exchange, the Bombay Stock Exchange has a significant

trading volume.

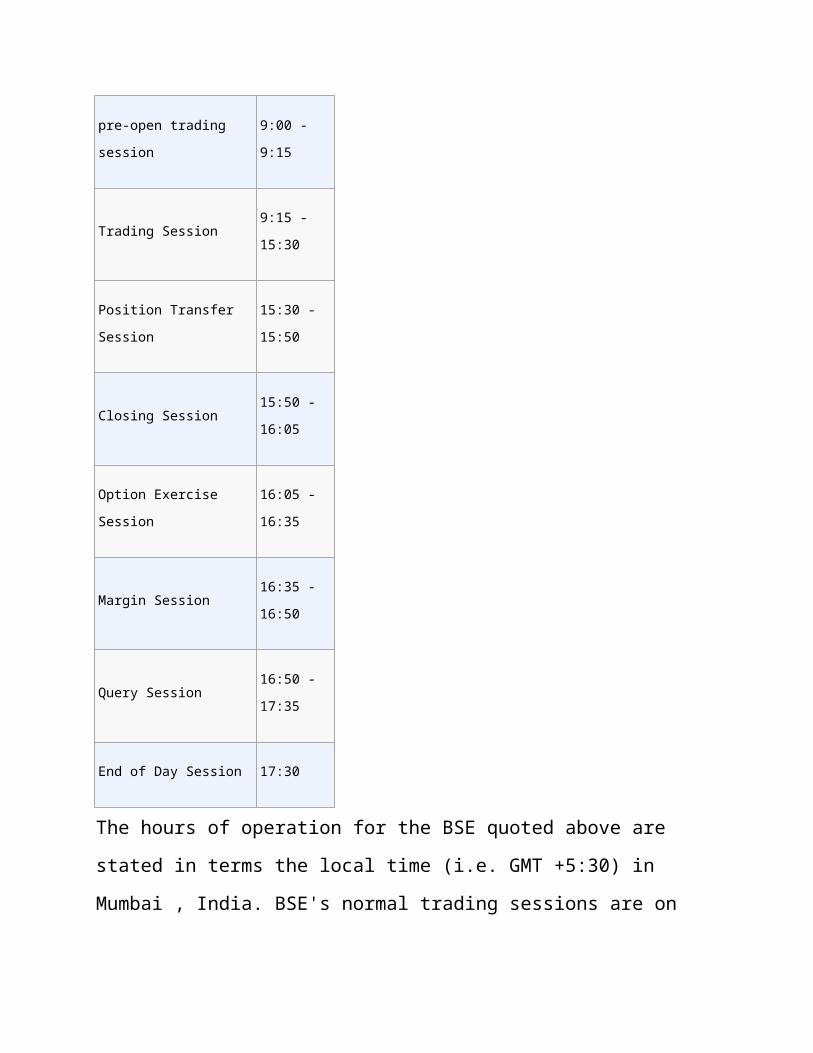

1.9 Hours of operation:-

Session Timing

Beginning of the Day Session 8:00 - 9:00

pre-open trading session 9:00 - 9:15

Trading Session 9:15 - 15:30

Position Transfer Session 15:30 - 15:50

Closing Session 15:50 - 16:05

Option Exercise Session 16:05 - 16:35

Margin Session 16:35 - 16:50

Query Session 16:50 - 17:35

End of Day Session 17:30

The hours of operation for the BSE quoted above are stated in terms the local time

(i.e. GMT +5:30) in Mumbai , India. BSE's normal trading sessions are on all days

of the week except Saturday, Sundays and holidays declared by the Exchange in

advance.

2. INTORDUCTION TO NATIONAL STOCK

EXCHANGE:-

NATIONAL STOCK EXCHANGE:-

The National Stock Exchange (NSE) (Hindi रष्ट्री य शे�अर बज़ार Rashtriya Śhare

Bāzaār) is astock exchange located at Mumbai, Maharashtra, India. It is the 9th

largest stock exchange in the world by market capitalization and largest in India by

daily turnover and number of trades, for both equities and derivative trading. NSE

has a market capitalization of aroundUS$1.59 trillion and over 1,552 listings as of

December 2010. Though a number of other exchanges exist, NSE and the Bombay

Stock Exchange are the two most significant stock exchanges in India, and

between them are responsible for the vast majority of share transactions. The

NSE's key index is the S&P CNX Nifty, known as the NSE NIFTY (National

Stock Exchange Fifty), an index of fifty major stocks weighted by market

capitalisation.

NSE is mutually-owned by a set of leading financial institutions, banks, insurance

companies and other financial intermediaries in India but its ownership and

management operate as separate entities. There are at least 2 foreign investors

NYSE Euronext and Goldman Sachs who have taken a stake in the NSE. As of

2006, the NSE VSAT terminals, 2799 in total, cover more than 1500 cities across

India. NSE is the third largest Stock Exchange in the world in terms of the number

of trades in equities. It is the second fastest growing stock exchange in the world

with a recorded growth of 16.6%.

2.1 ORIGINS:-

The National Stock Exchange of India was promoted by leading Financial

institutions at the behest of the Government of India, and was incorporated in

November 1992 as a tax-paying company. In April 1993, it was recognized as

a stock exchange under the Securities Contracts (Regulation) Act, 1956. NSE

commenced operations in the Wholesale Debt Market(WDM) segment in June

1994. The Capital market (Equities) segment of the NSE commenced operations in

November 1994, while operations in the Derivatives segment commenced in June

2000.

2.2 INNOVATIONS:-

NSE pioneering efforts include:

Being the first national, anonymous, electronic limit order book (LOB)

exchange to trade securities in India. Since the success of the NSE, existent

market and new market structures have followed the "NSE" model.

Setting up the first clearing corporation "National Securities Clearing

Corporation Ltd." in India. NSCCL was a landmark in providing innovation on

all spot equity market (and later,derivatives markets) trades in India.

Co-promoting and setting up of National Securities Depository Limited, first

depository in India

Setting up of S&P CNX NIFTY.

NSE pioneered commencement of Internet Trading in February 2000, which led

to the wide popularization of the NSE in the broker community.

Being the first exchange that, in 1996, proposed exchange traded derivatives,

particularly on an equity index, in India. After four years of policy and

regulatory debate and formulation, the NSE was permitted to start trading

equity derivatives

Being the first and the only exchange to trade GOLD ETFs (exchange traded

funds) in India.

NSE has also launched the NSE-CNBC-TV18 media centre in association with

CNBC-TV 18

NSE.IT Limited, setup in 1999 , is a 100% subsidiary of the National Stock

Exchange of India. A Vertical Specialist Enterprise, NSE.IT offers end-to-end

Information Technology (IT) products, solutions and services.

NSE (National Stock Exchange) was the first exchange in the world to use

satellite communication technology for trading, using a client server based

system called National Exchange for Automated Trading (NEAT). For all

trades entered into NEAT system, there is uniform response time of less than

one second.

2.3MARKETS:-

Currently, NSE has the following major segments of the capital market:

EQUITY

Futures & Options

Retail Debt Market

Who;esale Debt Market

Currency Futures

Mutual Funds

Stock lending &borrowings

August 2008 Currency derivatives were introduced in India with the launch of

Currency Futures in USD INR by NSE. Currently it has also launched currency

futures in EURO, POUND & YEN. Interest Rate Futures was introduced for the

first time in India by NSE on 31 August 2009, exactly after one year of the launch

of Currency Futures.

NSE became the first stock exchange to get approval for Interest rate futures as

recommended by SEBI-RBI committee, on 31 August 2009, a futures contract

based on 7% 10 Year GOI bond (NOTIONAL) was launched with quarterly

maturities.

2.4 HOURS:-

NSE's normal trading sessions are conducted from 9:15 am India Time to 3:30 pm

India Time on all days of the week except Saturdays, Sundays and Official

Holidays declared by the Exchange (or by the Government of India) in

advance. The exchange, in association with BSE (Bombay Stock Exchange Ltd.),

is thinking of revising its timings from 9.00 am India Time to 5.00 pm India Time.

There were System Testing going on and opinions, suggestions or feedback on the

New Proposed Timings are being invited from the brokers across India. And

finally on 18 November 2009 regulator decided to drop their ambitious goal of

longest Asia Trading Hours due to strong opposition from its members.

On 16 December 2009, NSE announced that it would advance the market opening

to 9:00 am from 18 December 2009. So NSE trading hours will be from 9.00 am

till 3:30 pm India Time.

However, on 17 December 2009, after strong protests from brokers, the Exchange

decided to postpone the change in trading hours till 4 Jan 2010.

NSE new market timing from 4 Jan 2010 is 9:00 am till 3:30 pm India Time.

3. ORIGIN OF INDIAN STOCK MARKET:-

3.1 HISTORY:-

The Bombay Stock Exchange is the oldest exchange in Asia. It traces its history to

the 1850s, when four Gujarati and one Parsi stockbroker would gather under

banyan trees in front of Mumbai's Town Hall. The location of these meetings

changed many times, as the number of brokers constantly increased. The group

eventually moved to Dalal Street in 1874 and in 1875 became an official

organization known as 'The Native Share & Stock Brokers Association'. In 1956,

the BSE became the first stock exchange to be recognized by theIndian

Government under the Securities Contracts Regulation Act. The Bombay Stock

Exchange developed the BSE SENSEX in 1986, giving the BSE a means to

measure overall performance of the exchange. In 2000 the BSE used this index to

open its derivatives market, trading SENSEX futures contracts. The development

of SENSEX options along with equity derivatives followed in 2001 and 2002,

expanding the BSE's trading platform. Historically an open outcry floor trading

exchange, the Bombay Stock Exchange switched to an electronic trading system in

1995. It took the exchange only fifty days to make this transition. This automated,

screen-based trading platform called BSE On-line trading (BOLT) currently has a

capacity of 8 million orders per day. The BSE has also introduced the world's first

centralized exchange-based internet trading system, BSEWEBx.co.in to enable

investors anywhere in the world to trade on the BSE platform. The BSE is

currently housed in Phiroze Jeejeebhoy Towers at Dalal Street, Fort area.

3.2 INDICES:-

The launch of SENSEX in 1986 was later followed up in January 1989 by

introduction of BSE National Index (Base: 1983-84 = 100). It comprised 100

stocks listed at five major stock exchanges in India

- Mumbai, Calcutta, Delhi, Ahmedabad and Madras. The BSE National Index was

renamed BSE-100 Index from October 14, 1996 and since then, it is being

calculated taking into consideration only the prices of stocks listed at BSE. BSE

launched the dollar-linked version of BSE-100 index on May 22, 2006. BSE

launched two new index series on 27 May 1994: The 'BSE-200' and the 'DOLLEX-

200'. BSE-500 Index and 5 sectoral indices were launched in 1999. In 2001, BSE

launched BSE-PSU Index, DOLLEX-30 and the country's first free-float based

index - the BSE TECk Index. Over the years, BSE shifted all its indices to the free-

float methodology (except BSE-PSU index). BSE disseminates information on the

Price-Earnings Ratio, the Price to Book Value Ratio and the Dividend Yield

Percentage on day-to-day basis of all its major indices. The values of all BSE

indices are updated on real time basis during market hours and displayed through

the BOLT system, BSE website and news wire agencies. All BSE Indices are

reviewed periodically by the BSE Index Committee. This Committee which

comprises eminent independent finance professionals frames the broad policy

guidelines for the development and maintenance of all BSE indices. The BSE

Index Cell carries out the day-to-day maintenance of all indices and conducts

research on development of new indices.

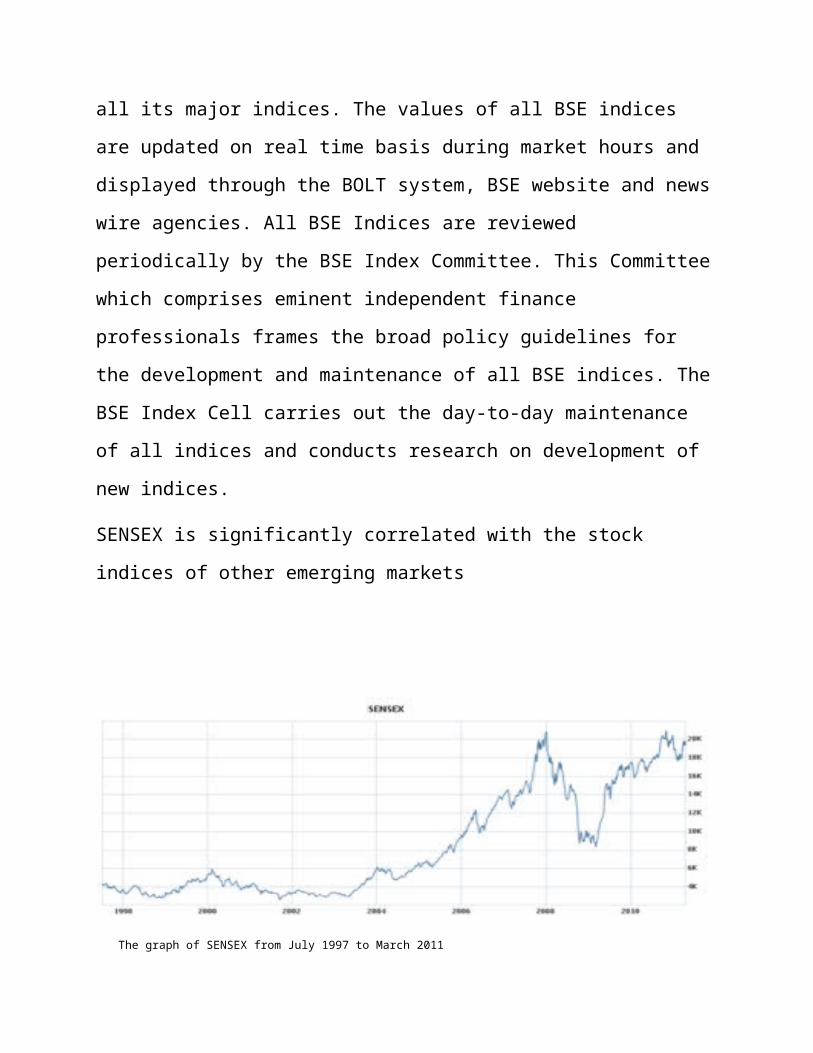

SENSEX is significantly correlated with the stock indices of other emerging

markets

The graph of SENSEX from July 1997 to March 2011

3.3 AWARDS:-

The World Council of Corporate Governance has awarded the Golden Peacock

Global CSR Award for BSE's initiatives in Corporate Social Responsibility

(CSR).

The Annual Reports and Accounts of BSE for the year ended March 31, 2006

and March 31, 2007 have been awarded the ICAI awards for excellence in

financial reporting.

The Human Resource Management at BSE has won the Asia - Pacific HRM

awards for its efforts in employer branding through talent management at work,

health management at work and excellence in HR through technology.

3.4 Rise & Rise of Indian Stock Market

Following is the timeline on the rise and rise of the Sensex through Indian

stock market history.

1978-79

Base year of Sensex, defined to be 100.

1986

Sensex first compiled using a market Capitalization-Weighted methodology

for 30 component stocks representing well-established companies across key

sectors.

Since 1990

1900s

July 25, 1990.

The Sensex touched the magical four-digit figure for the first time and

closed at 1,001 in the wake of a good monsoon season and excellent corporate

results.

July 1991 Rupee devalued by 18-19 %

January 15, 1992

The Sensex crossed the 2,000-mark and closed at 2,020 followed by the

liberal economic policy initiatives undertaken by the then finance minister and

current Prime Minister Dr Manmohan Singh.

February 29, 1992

The Sensex surged past the 3000 mark in the wake of the market-friendly

Budget announced by the then Finance Minister, Dr Manmohan Singh.

March 30, 1992

The Sensex crossed the 4,000-mark and closed at 4,091 on the expectations

of a liberal export-import policy. It was then that the Harshad Mehta scam hit the

markets and Sensex witnessed unabated selling.

October 8, 1999

The Sensex crossed the 5,000-mark as the BJP-led coalition won the

majority in the 13th Lok Sabha election.

2000s

February 11, 2000

The infotech boom helped the Sensex to cross the 6,000-mark and hit and all

time high of 6,006.

June 20, 2005

The news of the settlement between the Ambani brothers boosted investor

sentiments and the scrips of RIL, Reliance Energy, Reliance Capital, and IPCL

made huge gains. This helped the Sensex crossed 7,000 points for the first time.

September 8, 2005

The Bombay Stock Exchange's benchmark 30-share index -- the Sensex --

crossed the 8000 level following brisk buying by foreign and domestic funds in

early trading.

November 28, 2005

The Sensex on November 28, 2005 crossed the magical figure of 9000 to

touch 9000.32 points during mid-session at the Bombay Stock Exchange on the

back of frantic buying spree by foreign institutional investors and well supported

by local operators as well as retail investors.

February 6, 2006

The Sensex on February 6, 2006 touched 10,003 points during mid-session.

The Sensex finally closed above the 10K-mark on February 7, 2006.

March 21, 2006

The Sensex on March 21, 2006 crossed the magical figure of 11,000 and touched a

life-time peak of 11,001 points during mid-session at the Bombay Stock Exchange

for the first time. However, it was on March 27, 2006 that the Sensex first closed at

over 11,000 points.

April 20, 2006

The Sensex on April 20, 2006 crossed the 12,000-mark and closed at a peak

of 12,040 points for the first time.

October 30, 2006

The Sensex on October 30, 2006 crossed the magical figure of 13,000 and

closed at 13,024.26 points, up 117.45 points or 0.9%. It took 135 days for the

Sensex to move from 12,000 to 13,000 and 123 days to move from 12,500 to

13,000.

December 5, 2006

The Sensex on December 5, 2006 crossed the 14,000-mark to touch 14,028

points. It took 36 days for the Sensex to move from 13,000 to the 14,000 mark.

July 6, 2007

The Sensex on July 6, 2007 crossed the magical figure of 15,000 to touch

15,005 points in afternoon trade. It took seven months for the Sensex to move from

14,000 to 15,000 points.

September 19, 2007

The Sensex scaled yet another milestone during early morning trade on

September 19, 2007. Within minutes after trading began, the Sensex crossed

16,000, rising by 450 points from the previous close. The 30-share Bombay Stock

Exchange's sensitive index took 53 days to reach 16,000 from 15,000. Nifty also

touched a new high at 4659, up 113 points.

The Sensex finally ended with a gain of 654 points at 16,323. The NSE Nifty

gained 186 points to close at 4,732.

September 26, 2007

The Sensex scaled yet another height during early morning trade on

September 26, 2007. Within minutes after trading began, the Sensex crossed the

17,000-mark . Some profit taking towards the end, saw the index slip into red to

16,887 - down 187 points from the day's high. The Sensex ended with a gain of 22

points at 16,921.

October 09, 2007

The BSE Sensex crossed the 18,000-mark on October 09, 2007. It took just

8 days to cross 18,000 points from the 17,000 mark. The index zoomed to a new

all-time intra-day high of 18,327. It finally gained 789 points to close at an all-time

high of 18,280. The market set several new records including the biggest single

day gain of 789 points at close, as well as the largest intra-day gains of 993 points

in absolute term backed by frenzied buying after the news of the UPA and Left

meeting on October 22 put an end to the worries of an impending election.

October 15, 2007

The Sensex crossed the 19,000-mark backed by revival of funds-based

buying in blue chip stocks in metal, capital goods and refinery sectors. The index

gained the last 1,000 points in just four trading days. The index touched a fresh all-

time intra-day high of 19,096, and finally ended with a smart gain of 640 points at

19,059.The Nifty gained 242 points to close at 5,670.

October 29, 2007

The Sensex crossed the 20,000 mark on the back of aggressive buying by

funds ahead of the US Federal Reserve meeting. The index took only 10 trading

days to gain 1,000 points after the index crossed the 19,000-mark on October 15.

The major drivers of today's rally were index heavyweights Larsen and Toubro,

Reliance Industries, ICICI Bank, HDFC Bank and SBI among others. The 30-share

index spurted in the last five minutes of trade to fly-past the crucial level and

scaled a new intra-day peak at 20,024.87 points before ending at its fresh closing

high of 19,977.67, a gain of 734.50 points. The NSE Nifty rose to a record high

5,922.50 points before ending at 5,905.90, showing a hefty gain of 203.60 points.

January 8, 2008

The sensex peaks. It crossed the 21,000 mark in intra-day trading after 49

trading sessions. This was backed by high market confidence of increased FII

investment and strong corporate results for the third quarter. However, it later fell

back due to profit booking.

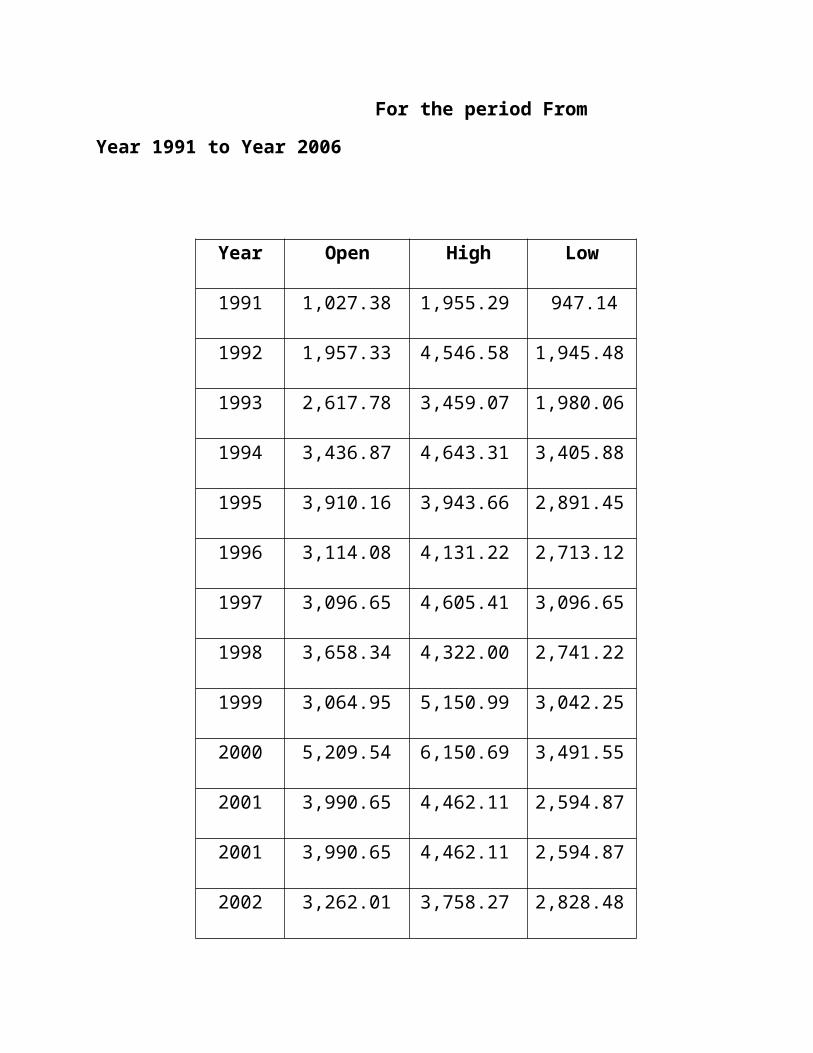

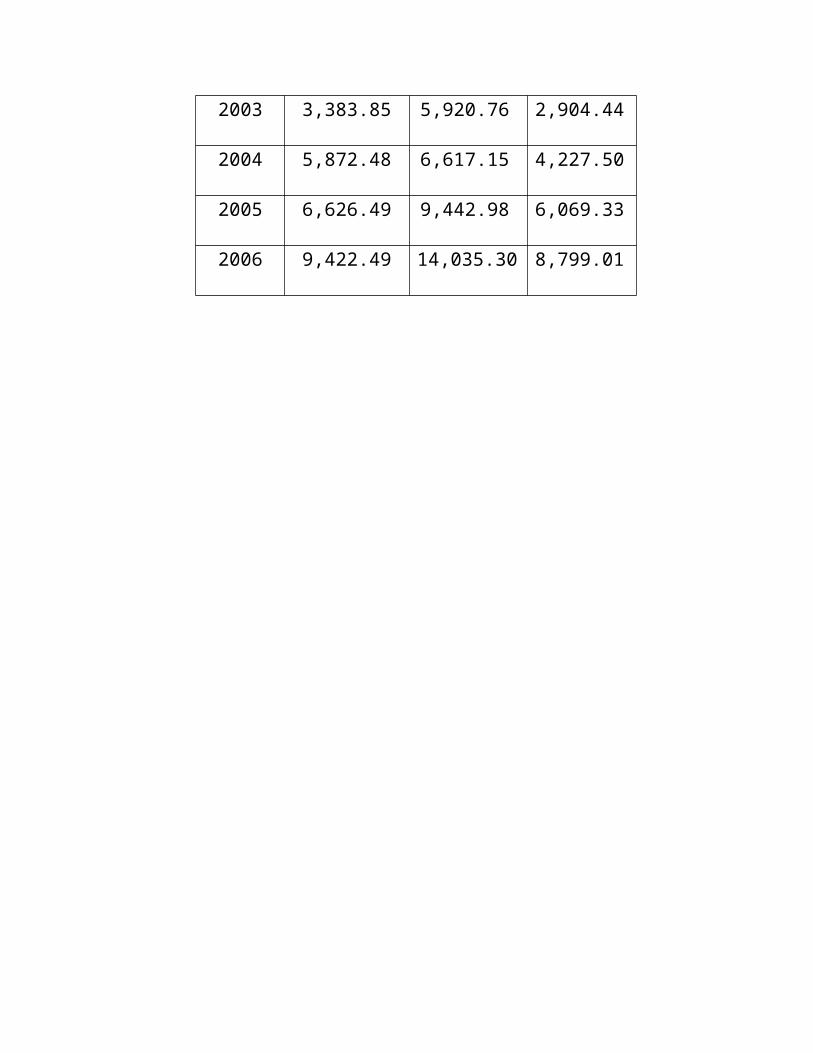

3.5 SENSEX Archives

For the period From Year 1991 to Year 2006

Year Open High Low

1991 1,027.38 1,955.29 947.14

1992 1,957.33 4,546.58 1,945.48

1993 2,617.78 3,459.07 1,980.06

1994 3,436.87 4,643.31 3,405.88

1995 3,910.16 3,943.66 2,891.45

1996 3,114.08 4,131.22 2,713.12

1997 3,096.65 4,605.41 3,096.65

1998 3,658.34 4,322.00 2,741.22

1999 3,064.95 5,150.99 3,042.25

2000 5,209.54 6,150.69 3,491.55

2001 3,990.65 4,462.11 2,594.87

2001 3,990.65 4,462.11 2,594.87

2002 3,262.01 3,758.27 2,828.48

2003 3,383.85 5,920.76 2,904.44

2004 5,872.48 6,617.15 4,227.50

2005 6,626.49 9,442.98 6,069.33

2006 9,422.49 14,035.30 8,799.01

4. Securities and Exchange Board of India (SEBI):-

4.1 Introduction

SEBI is the Regulator for the Securities Market in India. Originally set up by

the Government of India in 1988, it acquired statutory form in 1992 with SEBI Act

1992 being passed by the Indian Parliament.Chaired by C B Bhave, SEBI is

headquartered in the popular business district of Bandra-Kurla complex in

Mumbai, and has Northern, Eastern and Southern regional offices in New Delhi,

Kolkata and Chennai. It is in the news that a new Western Regional Office has

been proposed at Ahmedabad.

4.2 Function of SEBI

SEBI has to be responsive to the needs of three groups, which constitute the

market:

The issuers of securities

The investors

The market intermediaries.

SEBI has three functions rolled into one body quasi-legislative, quasi-

judicial and quasi-executive. It drafts regulations in its legislative capacity, it

conducts investigation and enforcement action in its executive function and it

passes rulings and orders in its judicial capacity. Though this makes it very

powerful, there is an appeals process to create accountability. There is a Securities

Appellate Tribunal which is a three member tribunal and is presently headed by a

former Chief Justice of a High court - Mr. Justice NK Sodhi. A second appeal lies

directly to the Supreme Court.

SEBI has enjoyed success as a regulator by pushing systemic reforms

aggressively and successively (e.g. the quick movement towards making the

markets electronic and paperless rolling settlement on T+2 basis). SEBI has been

active in seting up the regulations as required under law.

4.3 Objectives of SEBI:-

Primary objectives : to promote healthy & orderly growth of securities market &

protect investors.

To maintain steady flow of savings into capital markets.

To regulate securities market & ensure fair practice by issuers to help them raise

resources at minimum cost.

To promote efficient services by brokers, merchant bankers and other

intermediaries to make them professional and competitive.

4.4 Powers of SEBI:-

To call periodical returns from recognised stock exchanges

To ask explanation from recognised stock exchanges / their members

To direct enquiries on any stock exchange

To make / amend by laws of recognised stock exchanges

To compel listing of securities by public companies

To control * regulate stock exchanges

To levy fees or charges for carrying out the purpose of regulations

To declare applicability of Sec 17 of Securities contract (Regulation) Act to grant

licenses to dealers of securities.

5 THE 1992 SECURITIES SCAM:-

(a.k.a)Harshad Mehta Scandal:

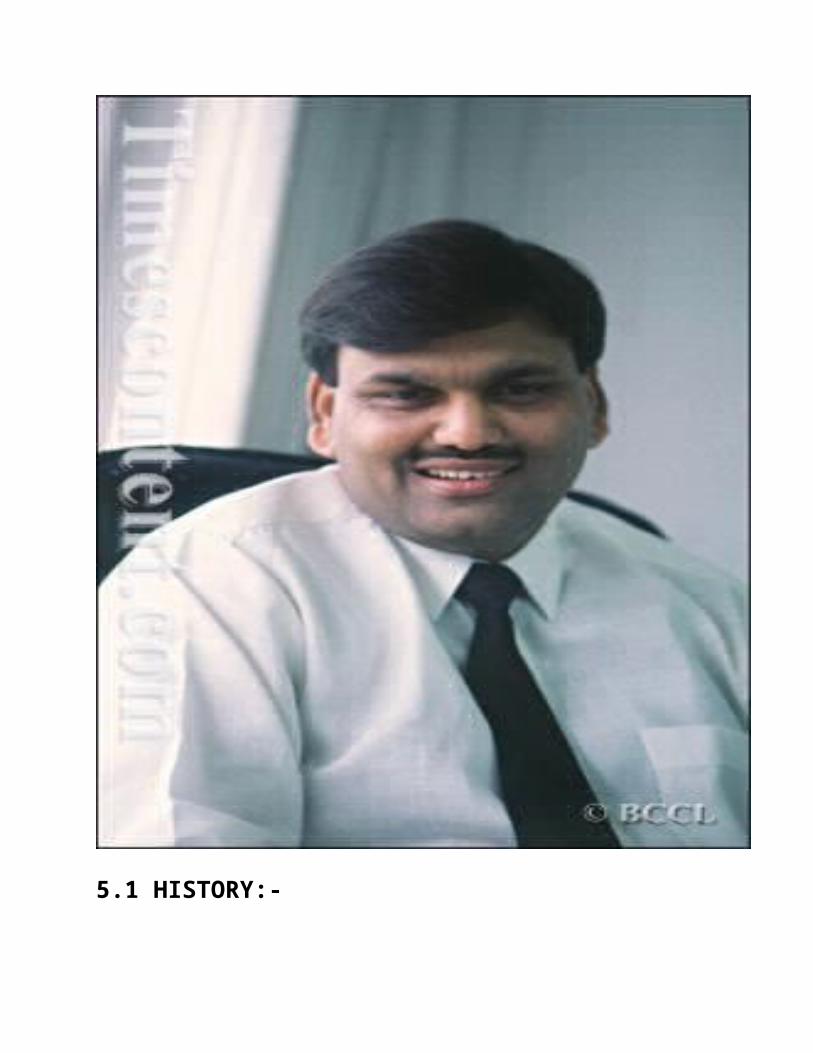

5.1 HISTORY:-

Harshad Mehta was an Indian stockbroker caught in a scandal beginning in 1992.

He died of a massive heart attack in 2001, while the legal issues were still being

litigated. Early life Harshad Shantilal Mehta was born in a Gujarati jain family of

modest means. His father was a small businessman. His mother's name was

Rasilaben Mehta. His early childhood was spent in the industrial city of Bombay.

Due to indifferent health of Harshad’s father in the humid environs of Bombay, the

family shifted their residence in the mid-1960s to Raipur, then in Madhya Pradesh

and currently the capital of Chattisgarh state. An Amul advertisement of

1999 during the conterversy over MUL saying it as "The Big Bhool" (Bhool in

Hindi means Blunder) He studied at the Holy Cross High School, located at Byron

Bazaar. After completing his secondary education Harshad left for Bombay. While

doing odd jobs he joined Lala Lajpat Rai College for a Bachelor’s degree in

Commerce.

After completing his graduation, Harshad Mehta started his working life as an

employee of the New India Assurance Company. During this period his family

relocated to Bombay and his brother Ashwin Mehta started to pursue graduation

course in law at Lala Lajpat Rai College. His youngest brother Hitesh is a

practising surgeon at the B.Y.L.Nair Hospital in Bombay. After his graduation

Ashwin joined (ICICI) Industrial Credit and Investment Corporation of India. They

had rented a small flat in Ghatkopar for living.

In the late seventies every evening Harshad and Ashwin started to analyze tips

generated from respective offices and from cyclostyled investment letters, which

had made their appearance during that time. In the early eighties he quit his job and

sought a job with stock broker P. Ambalal affiliated to Bombay Stock

Exchange (BSE) before becoming a jobber on BSE for stock broker P.D. Shukla.

In 1981 he became a sub-broker for stock brokers J.L. Shah and Nandalal Sheth.

After a while he was unable to sustain his overbought positions and decided to pay

his dues by selling his house with consent of his mother Rasilaben and brother

Ashwin. The next day Harshad went to his brokers and offered the papers

of the house as guarantee. The brokers Shah and Sheth were moved by his gesture

and gave him sufficient time to overcome his position. After he came out of this

big struggle for survival he became stronger and his brother quit his job to team

with Harshad to start their venture GrowMore Research and Asset Management

Company Limited. While a brokers card at BSE was being auctioned, the company

made a bid for the same with financial assistance from Shah and Sheth, who were

Harshad's previous broker mentors. He rose and survived the bear runs, this earned

him the nickname of the Big Bull of the trading floor, and his actions, actual or

perceived, decided the course of the movement of the Sensex as well as scrip-

specific activities. By the end of eighties the media started projecting him as

"Stock Market Success", "Story of Rags to Riches" and he too started to fuel his

own publicity. He felt proud of this accomplishments and showed off

his success to journalists through his mansion "Madhuli", which included a

billiards room, mini theatre and nine hole golf course. His brand new Toyota Lexus

and a fleet of cars gave credibility to his show off. This in no time made him the

nondescript broker to super star of financial world. During his heyday, in the early

1990s, Harshad Mehta commanded a large resource of funds and finances as

well as personal wealth. The fall In April 1992, the Indian stock market crashed,

and Harshad Mehta, the person who was all along considered as the architect of the

bull run was blamed for the crash. It transpired that he had manipulated

the Indian banking systems to siphon off the funds from the banking system, and

used the liquidity to build large positions in a select group of stocks. When the

scam broke out, he was called upon by the banks and the financial institutions to

return the funds, which in turn set into motion a chain reaction, necessitating

liquidating and exiting from the positions which he had built in various stocks. The

panic reaction ensued, and the stock market reacted and crashed within days.He

was arrested on June 5, 1992 for his role in the

scam.

His favorite stocks included

· ACC

· Apollo Tyres

· Reliance

· Tata Iron and Steel Co. (TISCO)

· BPL

· Sterlite

· Videocon.

The extent The Harshad Mehta induced security scam, as the media sometimes

termed it, adversely affected at least 10 major commercial banks of India, a

number of foreign banks operating in India, and the National Housing Bank, a

subsidiary of the Reserve Bank of India, which is the central bank of India.

As an aftermath of the shockwaves which engulfed the Indian financial sector, a

number of people holding key positions in the India's financial sector were

adversely affected, which included arrest and sacking of K.M. Margabandhu, then

CMD of the UCO Bank; removal from office of V. Mahadevan, one of the

Managing Directors of India’s largest bank, the State Bank of India. The end The

Central Bureau of Investigation which is India’s premier investigative agency, was

entrusted with the task of deciphering the modus operandi and the ramifications of

the scam. Harshad Mehta was arrested and investigations continued for a decade.

During his judicial custody, while he was in Thane Prison, Mumbai, he complained

of chest pain, and was moved to a hospital, where he died on 31st December 2001.

His death remains a mystery. Some believe that he was murdered ruthlessly by an

underworld nexus (spanning several South Asian countries including

Pakistan). Rumour has it that they suspected that part of the huge wealth that

Harshad Mehta commanded at the height of the 1992 scam was still in safe hiding

and thought that the only way to extract their share of the 'loot' was to pressurise

Harshad's family by threatening his very existence. In this context, it might be

noteworthy that a certain criminal allegedly connected with this nexus had

inexplicably surrendered just days after Harshad was moved to Thane Jail and

landed up in imprisonment in the same jail, in the cell next

to Harshad Mehta's.

Harshad Shantilal Mehta was born in a Gujarati Jain family of modest means. His

early childhood was spent

in Mumbai where his father was a small-time businessman. Later, the family

moved to Raipur in Madhya Pradesh after doctors advised his father to move to a

drier place on account of his indifferent health.

But Raipur could not hold back Mehta for long and he was back in the city after

completing his schooling, much against his father’s wishes. Mehta first started

working as a dispatch clerk in the New India Assurance Company. Over the years,

he got interested in the stock markets and along with brother Ashwin, who by

then had left his job with the Industrial Credit and Investment Corporation of India,

started investing heavily in the stock market. As they learnt the ropes of the trade,

they went from boom to bust a couple of times and survived. Mehta gradually rose

to become a stock broker on the Bombay Stock Exchange, who did very

well for himself. At his peak, he lived almost like a movie star in a 15,000 square

feet house, which had a swimming pool as well as a golf patch. He also had a taste

for flashy cars, which ultimately led to his

downfall. Newsmakers of the week: View Slideshow “The year was 1990. Years

had gone by and the driving ambitions of a young man in the faceless crowd had

been realised. Harshad Mehta was making waves in the stock market. He had been

buying shares heavily since the beginning of 1990. The shares which attracted

attention were those of Associated Cement Company (ACC),” write the authors.

The price of ACC was bid up to Rs 10,000. For those who asked, Mehta had the

replacement cost theory as an explanation. The theory basically argues that old

companies should be valued on the basis of the amount of money which would be

required to create another such company. Through the second half of 1991, Mehta

was the darling of the business media and earned the sobriquet of the ‘Big Bull’,

who was said to have started the bull run. But, where was Mehta getting his

endless supply of money from? Nobody had a clue.

On April 23, 1992, journalist Sucheta Dalal in a column in The Times of India,

exposed the dubious ways of

Harshad Metha. The broker was dipping illegally into the banking system to

finance his buying.“In 1992, when I broke the story about the Rs 600 crore that he

had swiped from the State Bank of India, it was his visits to the bank’s

headquarters in a flashy Toyota Lexus that was the tip-off. Those days, the Lexus

had just been launched in the international market and importing it cost a neat

package,” Dalal wrote

in one of her columns later. The authors explain: “The crucial mechanism through

which the scam was effected was the ready forward (RF) deal. The RF is in

essence a secured short-term (typically 15-day) loan from one bank to another.

Crudely put, the bank lends against government securities just as a pawnbroker

lends against jewellery….The borrowing bank actually sells the securities to the

lending bank and buys them back at the end of the period of the loan, typically at a

slightly higher price.” It was this ready forward deal that Harshad Mehta and his

cronies used with great success to channel money from the banking system. A

typical ready forward deal involved two banks brought together by a broker in

lieu of a commission. The broker handles neither the cash nor the securities,

though that wasn’t the case in the lead-up to the scam. “In this settlement process,

deliveries of securities and payments were made through the broker. That is, the

seller handed over the securities to the broker, who passed them to the buyer, while

the buyer gave the cheque to the broker, who then made the payment to the seller.

In this settlement process, the buyer and the seller might not even know whom they

had traded with, either being know only to the broker.” This the brokers could

manage primarily because by now they had become market makers and had started

trading on their account. To keep up a semblance of legality, they pretended

to be undertaking the transactions on behalf of a bank. Another instrument used in

a big way was the bank receipt (BR). In a ready forward deal, securities were not

moved back and forth in actuality. Instead, the borrower, i.e. the seller of

securities, gave the buyer of the securities a BR. As the authors write, a BR

“confirms the sale of securities. It acts as a receipt for the money received by the

selling bank. Hence the name - bank receipt. It promises to deliver the securities to

the buyer. It also states that in the mean time, the seller holds the securities in trust

of the buyer.” Having figured this out, Metha needed banks, which

could issue fake BRs, or BRs not backed by any government securities. “Two

small and little known banks - the Bank of Karad (BOK) and the Metorpolitan Co-

operative Bank (MCB) - came in handy for this purpose. These banks were willing

to issue BRs as and when required, for a fee,” the authors point out.

Once these fake BRs were issued, they were passed on to other banks and the

banks in turn gave money to Mehta, obviously assuming that they were lending

against government securities when this was not really the case. This money was

used to drive up the prices of stocks in the stock market. When time came to

return the money, the shares were sold for a profit and the BR was retired. The

money due to the bank was returned. The game went on as long as the stock prices

kept going up, and no one had a clue about Mehta’s modus operandi. Once the

scam was exposed, though, a lot of banks were left holding BRs which did not

have any value - the banking system had been swindled of a whopping Rs 4,000

crore. Mehta made a brief comeback as a stock market guru, giving tips on his own

website as well as a weekly newspaper column. This time around, he was in

cahoots with owners of a few companies and recommended only those shares. This

game, too, did not last long. Interestingly, however, by the time he died, Mehta had

been convicted in only one of the many cases filed against him.

5.2 The making of the 1992 security scam:-

Mehta, along with his associates, was accused of manipulating the rise in the

Bombay Stock Exchange (BSE) in 1992. They took advantage of the many

loopholes in the banking system and drained off funds from inter-bank

transactions. Subsequently, they bought huge amounts of shares at a premium

across many industry verticals causing the Sensex to rise dramatically. However,

this was not to continue. The exposure of Mehta's modus operandi led banks to

start demanding their money back, causing the Sensex to plunge almost

dramatically as it had risen. Mehta was later charged with 72 criminal offences

while over 600 civil action suits were filed against him. Significantly, the Harshad

Mehta security scandal also became the flavor of Bollywood with Sameer

Hanchate's film Gafla.

5.3 Huge Financial Scandal Shakes Indian Politics:-By EDWARD A. GARGAN

Published: June 09, 1992

A $1 billion banking and securities scandal, the largest in India's history, has

rapidly spread through the stock markets and banking system and is now creeping

onto the political landscape.

Several major banks, including the State Bank of India, the country's largest, have

found themselves short by hundreds of millions of dollars after making dubious

loans to stock speculators. In addition, one of the country's biggest securities

brokers is behind bars, the chairmen of several banks have been forced to resign

and one committed suicide.

Opposition political leaders, saying that the Government is covering up the scandal

or at least allowed it to occur through negligence, are demanding the resignation of

the Finance Minister and the head of the central bank. The Prime Minister, P. V.

Narasimha Rao, is fending off his opponents and has ordered a special court

created to try those associated with the scandal. Trying to Unravel the Fraud

For two months, investigators have been going through rooms-full of documents,

decoding computer disks and raiding homes and offices, all to try to unravel the

extent of the financial fraud. While they do so, the implications of it all are still

uncertain.

The investigations led to the filing of charges last week against 10 brokers and

bankers, including Harshad Mehta, Bombay's most flamboyant securities dealer.

He is charged with fraud in buying and selling securities, bribery, using forged

documents and conspiracy. Still, the exact nature and extent of the financial

misdeeds and bank losses have not been detailed.

But what is clear is that a half-dozen big banks lent hundreds of millions of dollars

to brokers in unsecured loans to finance speculation in the stock and bond markets.

By last week, more than $1 billion was missing from the ledgers, leaving some of

the banks technically insolvent.

While he has not granted interviews about the charges against him, Mr. Mehta sent

a letter to the Central Bureau of Investigation, India's equivalent of the F.B.I.,

vigorously defending himself. "Neither I nor any of my companies have done

anything in violation of any law," he said in the letter. "All our transactions have

been in accordance with prevailing practice -- a practice which is by no means

secret or clandestine."

Fueled by a buying frenzy, the Bombay Stock Exchange index more than doubled

in the last year. But in late April, news began to spread that Mr. Mehta might have

skated beyond even the fuzzy edges of Indian securities laws to gain control of

more than one-third of the State Bank of India's business in Government securities.

That is also when it and other banks were found to be holding worthless

promissory notes for hundreds of millions of dollars. The stock market began a

plunge that has not stopped.

The very size of the scandal, trumpeted daily across the front pages of the country's

newspapers, has created a climate of fear among political leaders and a spirit of

vengeance among the Government's left-wing opposition, which feels betrayed by

the yearlong march toward a free-market economy.

As a result, Mr. Mehta and the others arrested so far have been denied bail and are

being forced to sleep on the cement floor of holding cells in a Bombay police

station. A Government directive has ordered that his assets be confiscated.

When Prime Minister Rao announced the abandonment of the country's long

romance with socialism last year, no one was more delighted than the brokers and

traders of the Bombay Stock Exchange, people who believed that it was finally

permissible to make money in India.

For months, the customary bedlam of Dalal, or "Trader," Street, site of the stock

exchange, has approached a frenzy resembling a well-shaken beehive. On the

exchange floor, the normally unrestrained blue-jacketed traders have hustled with a

new-found ferocity that drove the exchange index up more than 60 percent in just

three months before the decline began. Stuffed along the exchange's gloomy

hallways are touts, tipsters and the tantalized, sweating and pushing and waving

fistfuls of money.

"The problem is not Mehta," said Debashis Basu, a financial writer for Business

Today. "This is a unique time in the economic history of India, when the old

control structures are being torn down. It is always at these moments that scamsters

creep out of the woodwork."

The chairman of the Securities and Exchange Board, G. V. Ramakrishna, said:

"Most players in the capital markets felt they were beyond regulation. We are now

trying to bring about some sensible regulations of the market in line with other

developing countries' capital markets."

5.4 The 1992 security scam and its exposure:-

Mehta's illicit methods of manipulating the stock market were exposed on April 23,

1992, when veteran columnist Sucheta Dalal wrote an article in India's national

daily The Times of India. Dalal’s column read: “The crucial mechanism through

which the scam was effected was the ready forward (RF) deal. The RF is in

essence a secured short-term (typically 15-day) loan from one bank to another.

Crudely put, the bank lends against government securities just as a pawnbroker

lends against jewelers. The borrowing bank actually sells the securities to the

lending bank and buys them back at the end of the period of the loan, typically at a

slightly higher price.” In a ready-forward deal, a broker usually brings together two

banks for which he is paid a commission. Although the broker does not handle the

cash or the securities, this was not the case in the prelude to the Mehta scam.

Mehta and his associates used this RF deal with great success to channel money

through banks.

The securities and payments were delivered through the broker in the settlement

process. The broker functioned as an intermediary who received the securities from

the seller and handed them over to the buyer; and he received the check from the

buyer and subsequently made the payment to the seller. Such a settlement process

meant that both the buyer and the seller may not even know the identity of the

other as only the broker knew both of them. The brokers could manage this method

expertly as they had already become market makers by then and had started trading

on their account. They pretended to be undertaking the transactions on behalf of a

bank to maintain a façade of legality.

Mehta and his associates used another instrument called the bank receipt (BR).

Securities were not traded in reality in a ready forward deal but the seller gave the

buyer a BR which is a confirmation of the sale of securities. A BR is a receipt for

the money received by the selling bank and pledges to deliver the securities to the

buyer. In the meantime, the securities are held in the seller’s trust by the buyer.

5.5 Where has all the money gone?

It is well known that while Harshad Mehta was the big bull in the stock market,

there was an equally powerful bear cartel, represented by Hiten Dalal, A.D.

Narottam and others, operating in the market with money cheated out of the banks.

Since the stock prices rose steeply during the period of the scam, it is likely that a

considerable part of the money swindled by this group would have been spent on

financing the losses in the stock markets.

It is rumored that a part of the money was sent out of India through the Havala

racket, converted into dollars/pounds, and brought back as India Development

Bonds. These bonds are redeemable in dollars/pounds and the holders cannot be

asked to disclose the source of their holdings. Thus, this money is beyond the reach

of any of the investigating agencies.

A part of the money must have been spent as bribes and kickbacks to the various

accomplices in the banks and possibly in the bureaucracy and in the political

system.

As stated earlier, a part of the money might have been used to finance the losses

taken by the brokers to window-dress various banks' balance sheets. In other

words, part of the money that went out of the banking system came back to it. In

sum, it appears that only a small fraction of the funds swindled is recoverable.

5.6 Impact of scam:-

Impact of the Scam The immediate impact of the scam was a sharp fall in the share

prices. The index fell from 4500 to 2500 representing a loss of Rs. 100,000 crores

in market capitalization. Since the accused were active brokers in the stock

markets, the number of shares which had passed through their hands in the last one

year was colossal. All these shares became "tainted" shares, and

overnight they became worthless pieces of paper as they could not be delivered in

the market. Genuine investors who had bought these shares well before the scam

came to light and even got them registered in their names found themselves being

robbed by the government. This resulted in a chaotic situation in the market since

no one was certain as to which shares were tainted and which were not.

The government's liberalization policies came under severe criticism after

the scam, with Harshad Mehta and others being described as the products of these

policies. Bowing to the political pressures and the bad press it received during the

scam, the liberalization policies were put on hold for a while by the government.

The Securities Exchange Board of India (SEBI) postponed sanctioning of private

sector mutual funds. The much talked about entry of foreign pension funds and

mutual funds became more remote than ever. The Euro-issues planned by several

Indian companies were delayed since the ability of Indian companies to raise

equity capital in world markets was severely compromised.

5.7 I-T, PSBs recover dues nine years after Mehta's death:-

Nine years after Harsad Mehta died, the I-T department and public sector banks

(PSBs) have successfully recovered a significant portion of their claims emerging

out of the securities scam from his liquidated assets. The Supreme Court directed

the Custodian of the attached properties and assets of the Harshad Mehta Group

(HMG) in March 2011 to make payments of Rs1,995.66-crore to the I-T

department and Rs 199.25-crore to the State Bank of India (SBI), making the two

institutions two of the earliest claimants to recover their dues.

While the SBI’s total principal amount claim of Rs 1,000-crore have been largely

settled, financial institutions have also received some money. However, Standard

Chartered Bank, which had claimed Rs 500-crore, has yet to recover its dues it was

one of the late claimants. Although the total claim over the HMG is of more than

Rs 20,000-crore, the apex court has said that for the present, it would only consider

claims towards the principal amount.

5.8 IT Recovery

The special court hearing the cases related to the securities scam 1992 involving

Harshad Mehta and others on Friday released Rs 400 crore from the custodian's

funds as pending arrears to the Income-Tax (I-T) department. This puts an end to

the 10-year-old legal battle of the I-T department for the Big Bull's arrears.

Confirming the development, senior IT officials said: "The State Bank of India

[SBI] vehemently opposed the special court's move to release Rs 400 crore to the I-

T department in the court." SBI had reportedly raised a claim of Rs 3,000 crore

from the custodian.

Sources in the custodian's office said as per the laid-down rules, the first priority

for availing of the share in the attached property of the notified parties goes to the

I-T department under the act of various government departments. The second

priority is given to banks and financial institutions (FIs).

Both the I-T department and SBI is now making all-out efforts to recover its funds

from the custodian, who looks after the attached properties of the notified parties

and is even ready to strike a compromise on the total interest valuation, which is

over Rs 1,500 crore. SBI has already made provisions for Rs 700 crore in its

books.

The bank is also looking for the share of the late Big Bull's real estate,

which can be attached by the custodian to settle the dues of the bank.

The I-T department had filed a suit way back in 1993 in the special court headed

by Justice S N Variava. The custodian has already sold benamishares of Mehta

worth Rs 750 crore.

The Associated Cement Company shares will the last in the benami lot after which

the custodian will target the real estate properties of the tainted broker (See '').

According to custodian sources, the sale of the real estate is expected to fetch

around Rs 100 crore. All these transactions are expected to be completed in the

next seven to eight months.

The majority of the benami shares have been purchased by FIs and banks (like Life

Insurance Corporation and State Bank of India). The FIs picked these shares at a

discounted price compared to the current market price.

5.9 END OF THE BIG BULL:-

Mumbai: Just as the year 2001 was coming to an end, Harshad Shantilal

Mehta, boss of Growmore Research and Asset Management, died of a massive

heart attack in a jail in Thane. And thus came to an end the life of

a man who is probably the most famous character ever to have emerged from the

Indian stock market. In the book, The Great Indian Scam: Story of the missing Rs

4,000 crore, Samir K Barua and Jayanth R Varma explain how Harshad Mehta

pulled off one of the most audacious scams in the history of the Indian stock

market.

5.10 Outcome:-

Mehta continued with his manipulative tactics, triggering a massive rise in the

prices of stock and thereby creating a feel-good market trajectory. However, upon

the exposure of the scam, several banks found they were holding BRs of no value

at all. Mehta had by then swindled the banks of a staggering Rs 4,000 crore. The

scam came under scathing criticism in the Indian Parliament, leading to Mehta's

eventual imprisonment. The scam’s exposure led to the death of the Chairman of

the Vijaya Bank who reportedly committed suicide over the exposure. He was

guilty of having issued checks to Mehta and knew the backlash of accusations he

would have to face from the public.

A few years later, Mehta made a brief comeback as a stock market expert and

started providing investment tips on his website and in a weekly newspaper

column. He worked with the owners of a few companies and recommended the

shares of those companies only. When he died in 2002, Mehta had been convicted

in only one of the 27 cases filed against him. What attracted the taxman’s attention

was Mehta's advance tax payment of Rs 28-crore for the financial year 1991-92.

Another eye-catcher was his extravagant lifestyle.

5.11 Journalist who expose the BIGG-BULL:-

Ms Sucheta Dalal is an award-winning business journalist and author

and her career is founded on many newsbreaks, insightful analysis and

high integrity. She has been a journalist for 25 years and was conferred

the prestigious Padma Shri for journalism in 2006. The 'Padma Awards',

announced on the eve of India's Republic Day, are among the highest

civilian awards in the country and are conferred for distinguished service

and excellence in various fields. She was awarded the Chameli Devi

Award instituted by the Media Foundation for excellence in journalism,

and Femina’s Woman of Substance award for her work on the Harshad

Mehta scam in 1992 and related writing.

Sucheta is a BSc. in Statistics from Karnatak College, followed up with

a graduate and post graduate degree in law (LLB and LLM) from

Bombay University. Her journalistic career began in 1984 with Fortune

India, an investment magazine. She has subsequently worked with

Business Standard and The Economic Times and then went on to

become Financial Editor of The Times of India. She has been a

columnist and consulting editor for The Indian Express group until 2008.

She is now a Consulting Editor for MoneyLIFE a personal finance

fortnightly (www.moneylife.in). Her columns are also published by

various publications including the Dainik Hindustan.

Sucheta's areas of interest are the capital market, investor related issues,

consumer issues and the infrastructure sector. She is well-known for her

numerous investigative pieces in all these areas and most notably for

breaking the securities scam in 1992 which was India’s biggest financial

scandal until then.

She has co-authored a book on the securities scam with her husband

Debashis Basu called The Scam: Who Won, Who lost, Who got away

(1993). This book, which was a best seller that year, has been revised,

updated and re-released in 2001 and again in 2005 (It is now called The

Scam: From Harshad Mehta To Ketan Parekh). In March 2000, she

wrote a biography of A.D.Shroff, who was considered a financial genius

in the 1950s. (Published by Viking books of Penguin). Pathbreakers -- a

book of 26 inspiring interviews with eminent Indians -- by Sucheta Dalal

and Debashis Basu was also released in July 2007.

Ms Dalal takes active interest in consumer and investor related issues.

She has been a Member of the Investor Protection and Education Fund

set up by the Government of India under the Department of Company

Affairs and a member of the Primary Market Advisory Committee of the

Securities and Exchange Board of India. She is a Trustee of the

Consumer Education and Research Centre of Ahmedabad, which is

among the largest consumer and investor advocacy groups in India. She

is also a Member of Bank of Baroda’s Standing Committee on consumer

services and on the board of Credibility Alliance, which is a consortium

of voluntary organisations committed towards enhancing accountability

and transparency in the voluntary sector through good governance.

Conclusion:-

Corporate Governance is the value framework, ethical framework and moral

framework within which businesses make decisions.

Business must harness the power of ethics which is assuming a new level of

importance and power.

When large sums of money are involved, greed causes people to become

unethical.

People should aleays keep in their mind that anything which have been started

with the wrong intention will give us a short term success and p;easure , but

ultimately the end woulb be very fatal .

As we have seen in the above project that Mr. HARSHAD MEHTA , a well

known broker, a multi-millioner has ended up his life in jail or in the judicial

custody .

Overall to conclude this , ethics should be given more importance than greed .

People should understand that their mistake are caused to end numbers of people

who r associated with them.

BIBLOGRAPHY:-

www.google.com

www.bseindia.com

www.nseindia.com

www.sebi.com

www.wikipedia.com