Embed Size (px)

Citation preview

Stock Compensation Accounting under FAS 123: What We’ve Learned

Murray S. Akresh and Kevin P. Hassan

Munuy S. Akreeh, CPA, is a director in Coopers & Lybrand L.L.P.’s Human Resources Advisory Technical Services Unit, New York. He was a coauthor of Coopers & Lybrand‘s 1993 study, “Stock Options: Accounting, Valua- tion and Management Issues,” and their monograph “Under- standing FASB Statement No. 123: Accounting for Stock- Based Compensation,” and is a fiequent author and speaker on benefits-related accounting issues. Kevin P. Haasan, CPA, is a senior consultant with Coopers & Lybrand L.L.P.3 Human Resources Advisory Technical Service Unit, New York. He was formerly an audit manager and member of Coopers & Lybmnd‘s National hcount- ing and SEC Directomte, with extensive experience in em- ployee benefits-related auditing and accounting.

The authors wish to thank Marilyn Daitch of Coopers & Lybrand L.L.P., who con- ducted the surveys discussed in this article.

The authors reviewed over 250 annual reports, comparing FAS No. 123’s impacts and assumptions on mature versus emerging high-technology companies.

n 1995, the Financial Accounting Standards Board (FASB) issued Statement of Financial Accounting Standard (FAS) No. 123, “Accounting for Stock-Based Compensation.” FAS No. 123

gives companies a choic-ither continue using the current rules for reporting compensation expense under Accounting Principles Board (APB) Opinion No. 25, “Accounting for Stock Issued to Employees,” which typically results in no expense for traditional stock options, or adopt new and more complex fair value accounting rules under FAS 123. If a company elects to continue to record expense under APB 25, FAS 123 still requires that the fair value of stock compensation awards be measured and that pro fonna net income and earnings per share (EPSWetermined as if the new fair value accounting had been applied-should be disclosed in a footnote to the financial statements. Additionally, FAS 123 requires other disclosures regarding stock compensation regardless of whether the company elects to recognize compensation expense under FAS 123 or APB 25. FAS 123 was generally effective starting with 1996 annual reports.

Two earlier articles in this journal-”Stock-Based Compensation: Understanding the New Rules of FAS 123,” by Murray S. Akresh and Janet Fuersich, Winter 1995-6, and “Understanding FAS 123’s New Disclosure Requirements for Stock-Based Compensation,” by Murray S. Akresh, Summer 199Mscussed the requirements of FAS 123 in detail. The first article analyzed key FAS 123 provisions and the second article focused on FAS 123 disclosure requirements. This article focuses on the actual implementation of FAS 123 and presents the results of a survey of over 250 annual reports, comparing FA8 123 impacts and assumptions on mature versus emerging (high- technology) companies.

CCC 1044-8 136/97/080473-11 Q 1997 John Wiley & Sons, Inc.

The Journal of Corporate Accounting and F’inancdSummer 1997 73

Murray S. Akresh and Kevin P. Hcurscm

T h decision to adopt FAS 123 should be based on a review of existing andplanned changes to stock- based programs and related impacts on net income and EPS.

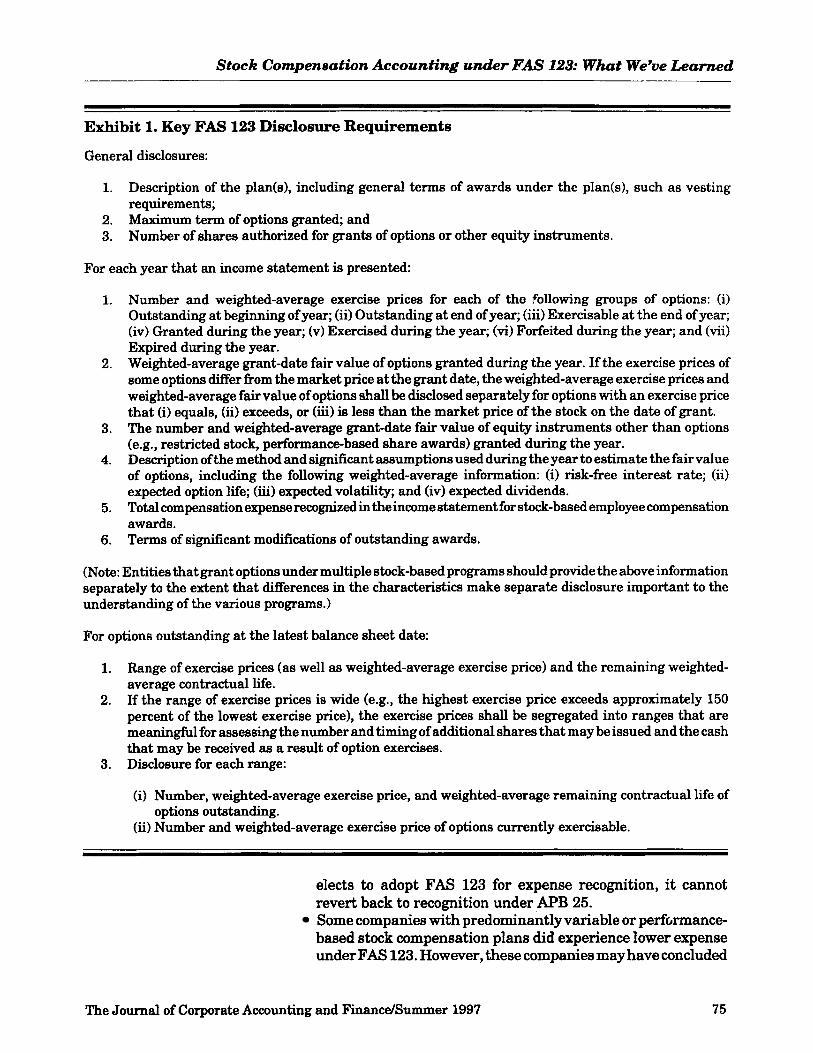

DISCLOSURE REQUIREMENTS Exhibit 1 summarizes the disclosures that are required under

FAS 123. These disclosures, as well as the pro forma net income and EPS disclosures required if FAS 123 is not adopted for expense recognition, were generally required starting with the 1996 annual report for calendar year-end companies (or for fiscal years beginning after December 15,1995, for other companies). As shown in Exhibit 1, FAS 123 disclosures generally fall under three broad categories:

Expanded description of each stock-based compensation plan, including fixed stock options, performance-based plans, restricted stock plan,s and employee stock-purchase plans. Information on each plan’s activity during the year, including expanded information on exercises, new grants, and their fair value. Information on options outstanding at the balance sheet date, including exercise price ranges and remaining contractual lives.

In addition to those disclosures, FAS 123 requires that if APB 25 is continued for expense recognition, pro forma net income and EPS (if the company presents EPS) should be disclosed based on FAS 123’s fair value approach applied to all grants awarded after January 1, 1995 (for calendar year-end companies or awards for fiscal years beginning aRer December 31, 1994, for other companies). The pro forma amounts should be reflected for both 1995 and 1996. For years 1997 and thereafter, it will be necessary to disclose the same information for each year in which an income statement is presented.

ADOPTION OF FAS 123 Our survey first focused on the issue of adoption of FAS 123’s fair

value accounting approach for expense recognition in the company’s income statement. In general, the decision to adopt FAS 123 should be based on a review of existing and planned changes to stock-based programs and related impacts on net income and EPS. Increased expense will be experienced by most companies under FAS 123, especially those offering traditional fixed-price stock options and employee stock-purchase plans. However, companies with variable or performance-related stock plans will generally experience lower expense under FAS 123, and we therefore expected some companies to consider adopting FAS 123 for expense recognition.

Our survey of 151 mature companies and 100 emerging companies revealed that not one company adopted FAS 123 for expense recognition. We believe that several factors may have contributed to the virtually unanimous decision not to change companies’ current accounting under APB 25, including the following:

FAS 123 is viewed as preferable when changing accounting policy for stock compensation. As a result, once a company

74 The Journal of Corporate Accounting and Finance/Sumrner 1997

Stock Compensation Accounting under FAS 123: What We've Learned

Exhibit 1. Key FAS 123 Disclosure Requirements

General disclosures:

1.

2. 3.

Description of the plan(s), including general terms of awards under the plan(s), such as vesting requirements; Maximum term of options granted; and Number of shares authorized for grants of options or other equity instruments.

For each year that an income statement is presented:

1.

2.

3.

4.

5.

6.

Number and weighted-average exercise prices for each of the following groups of options: (i) Outstanding at beginning of year; (ii) Outstanding at end of year; (iii) Exercisable at the end of year; (iv) Granted during the year; (v) Exercised during the year; (vi) Forfeited during the year; and (vii) Expired during the year. Weighted-average grant-date fair value of options granted during the year. If the exercise prices of some options differ fkom the market price at the grant date, the weighted-average exercise prices and weighted-average fair value of options shall be disclosed separately for options with an exercise price that (i) equals, (ii) exceeds, or (iii) is less than the market price of the stock on the date of grant. The number and weighted-average grant-date fair value of equity instruments other than options (e.g., restricted stock, performance-based share awards) granted during the year. Description of the method and significant assumptions used during the year to estimate the fair value of options, including the following weighted-average information: (i) risk-free interest rate; (ii) expected option life; (iii) expected volatility; and (iv) expected dividends. Total compensation expense recognized in the income statement for stock-based employee compensation awards. Terms of sigdicant modifications of outstanding awards.

(Note: Entities that grant options under multiple stock-based programs should provide the above information separately to the extent that differences in the characteristics make separate disclosure important to the understanding of the various programs.)

For options outstanding at the latest balance sheet date:

1.

2.

3.

Range of exercise prices (as well as weighted-average exercise price) and the remaining weighted- average contractual life. If the range of exercise prices is wide (e.g., the highest exercise price exceeds approximately 150 percent of the lowest exercise price), the exercise prices shall be segregated into ranges that are meaningful for assessing the number and timing of additional shares that may be issued and the cash that may be received as a result of option exercises. Disclosure for each range:

(i) Number, weighted-average exercise price, and weighted-average remaining contractual life of

(ii) Number and weighted-average exercise price of options currently exercisable. options outstanding.

elects to adopt FAS 123 for expense recognition, it cannot revert back to recognition under APB 25. Some companies with predominantly variable or perfcrmance- based stock compensation plans did experience lower expense under FAS 123. However, these companies may have concluded

The Journal of Corporate Accounting and FinancdSummer 1997 75

Murray s. Akm8h and Kevin P. Haasan

that their plans may change in the future-moving to the more traditional fixed stock options, for example-especially due to possible future acquisitions or new management initiatives.

IMPACT ON NET INCOME AND EPS After finding no companies that adopted FAS 123 for expense

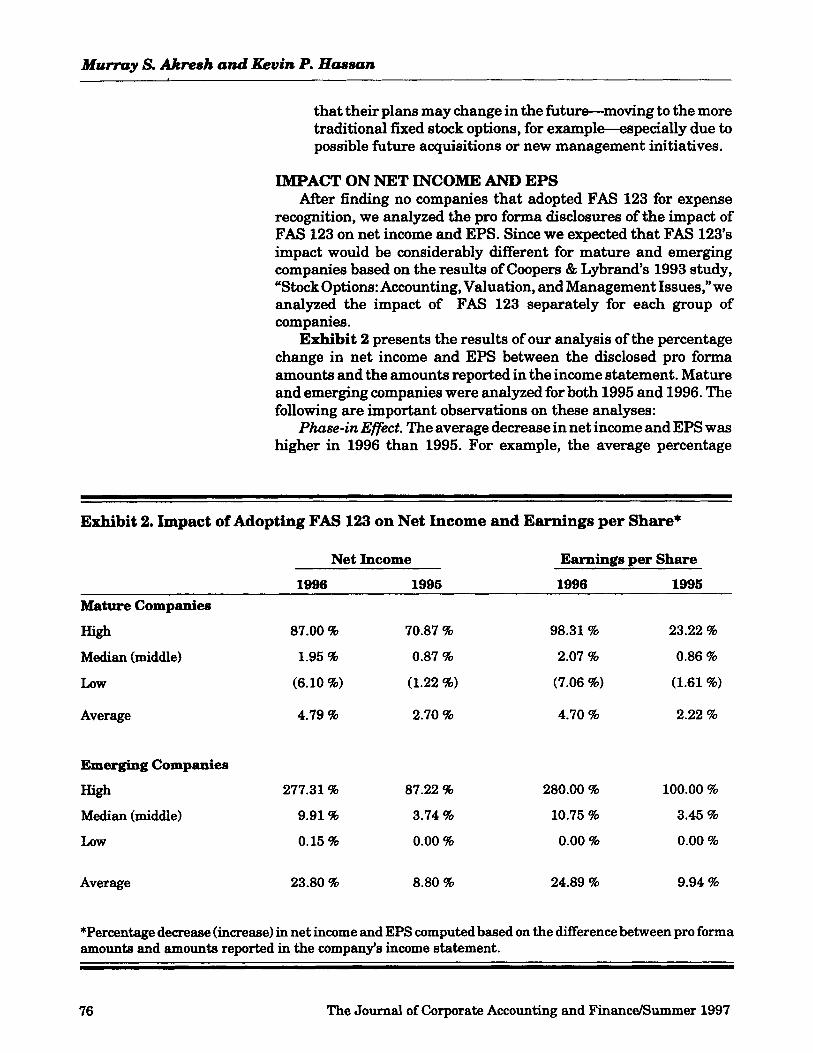

recognition, we analyzed the pro forma disclosures of the impact of FAS 123 on net income and EPS. Since we expected that FAS 123's impact would be considerably different for mature and emerging companies based on the results of Coopers & Lybrand's 1993 study, "StockOptions: Accounting, Valuation, and Management Issues," we analyzed the impact of FAS 123 separately for each group of companies.

Exhibit 2 presents the results of our analysis of the percentage change in net income and EPS between the disclosed pro forma amounts and the amounts reported in the income statement. Mature and emerging companies were analyzed for both 1995 and 1996. The following are important observations on these analyses:

P h e - i n Effect. The average decrease in net income and EPS was higher in 1996 than 1995. For example, the average percentage

~~~ ~ ~ ~~

Exhibit 2. Impact of Adopting FAS 123 on Net Income and Earnings per Share*

Net Income Earnings per Share

1996 1995 1996 1995

Mature Companies

High 87.00 % 70.87 % 98.31 % 23.22 %

Median (middle) 1.95 % 0.87 % 2.07 % 0.86 %

LOW (6.10 %) (1.22 %I (7.06 95) (1.61 %)

Average 4.79 % 2.70 % 4.70 % 2.22 %

Emerging Companies

High 277.31 % 87.22 % 280.00 % 100.00 %

Median (middle) 9.91 % 3.74 % 10.75 8 3.45 %

LOW 0.15 % 0.00 8 0.00 % 0.00 %

Average 23.80 96 8.80 % 24.89 % 9.94 %

*Percentage decrease (increase) in net income and EPS computed based on the difference between pro forma amounta and amounts reported in the companfs income statement.

76

~

"he Journal of Corporate Accounting and FinancdSummer 1997

Stock Compensation Accounting under FAS 123: What We’ve Learned

The impact of FAS 123 on emerging companies was signimantly different than on mature companies.

reduction in net income increased to 4.79 percent in 1996 fkom 2.70 percent in 1995 for mature companies, and to 23.80 percent in 1996 fkom 8.80 percent in 1995 for emerging companies (the reduction in EPS increased in a similar fashion). This increasing pattern of expense under FAS 123 is generally due to the fact that FAS 123 requires compensation cost to be recognized over the vesting or service period. The reduction in net income and EPS should increase each year, assuming annual grants, and should stabilize at the end of the vesting cycle (the “phase-in” period). We expect that the phase-in effect of FAS 123 will continue over the next two or three years because most companies have stock-based awards that vest over three to five years.

Company Maturity. Theimpact of FA3 123 onemergingcompanies was significantly different than on mature companies. For example, the average reduction in net income was 23.80 percent for emerging companies in 1996 compared with a reduction of 4.79 percent for mature companies. For 1995, the effect on emerging companies was similarly greater than on mature companies. These differences were predictable for a number of reasons. First, emerging companies tend to have lower net income (or often losses) than mature entities, so a small reduction may result in a significant percentage decrease. Second, as discussed further later in this article, emerging companies chose considerably different assumptions than mature companies, with considerably higher volatility and lower (or no) assumed dividends-generally resulting in higher option values per share for emerging companies. Third, emerging companies tend to use stock- based compensation programs (e.g., both stock options and employee stock-purchase plans) more than mature companies since they generally lack cash to pay compensation.

Range ofResuZts. We found a wide ranges of results from company to company, for both mature and emerging companies. For mature companies, the 1996 impact on net income ranged from a high of 87.0 percent to a low of a 6.1 percent loss; emerging companies had a 1996 reduction of net income ranging from a high of 277.31 percent to a low of 0.15 percent. However, even excluding these extremes, results vaned widely. For example, we found a wide range between the 20th and 80th percentiles-the reduction in net income is as follows:

Mature companies: 20th percentile, .82 percent reduction; 80th percentile, 4.94 percent; Emerging companies: 20th percentile, 3.11 percent reduction; 80th percentile, 26.25 percent.

Some key reasons for this wide variability may include:

Level of net income or loss before calculating the effects of adopting FAS 123. The percentage change is much greater when the entity has a low net income or loss. Even within the categories ofmature and emerging, assumptions varied considerably from company to company. For example,

The Journal of Corporate Accounting and FinancdSummer 1997 77

Murray S. Akresh and a v i n P. Haaaan

expected volatility for mature companies was 39.5 percent at the 20th percentile and 70 percent at the 80th percentile. Underlying stock programs. The types of plans and the extent to which they use stockcompensation awards differ substantially from company to company even within the categories of mature and emerging. We noted that many companies that sponsored multiple stock-based compensation programs disclosed different assumptions for each plan.

Materiality. We noted that 19 mature companies did not quantify the impact of adopting FAS 123, stating that the effect of adoption was immaterial. FAS 123 does not provide any materiality thresholds and companies were given latitude to apply judgment in disclosure. Because a commonly used materiality criterion is often 5 percent of reported net income, one may assume that for the companies that did not present FAS 123 pro forma amdunts, the impact on net income and EPS may be less than 5 percent of reported net income. However, it is unclear whether these companies assessed materiality in terms of the current year‘s impact, rather than on the potential impact after the phase-in period. As noted earlier, the impact of FAS 123 may become more material as the company moves through the phase-in period.

ANALYSIS OF ASSUMPTIONS FAS 123 requires the disclosure of the assumptions and methods

used in determining the fair value of stock options. Our survey noted that all of the companies surveyed disclosed that they used the Black- Scholes Option pricing model. The following assumptions were used in calculating fair value:

Expected Option Life (or expected term): The average length of time until the assumed date of exercise, generally a period somewhere between the end of the vesting period and the maturity of the option. Expected Volatility: The amount, expressed as an annualized standard deviation percentage, by which the company’s stock price is expected to fluctuate over the expected option life. Expected Dividends: The expected dividend yield or expected dividend payments on the underlying stock. Risk-Free Interest Rate: The rate currently available on zero- coupon U.S. government issues with a remaining term equal to the expected life of the options.

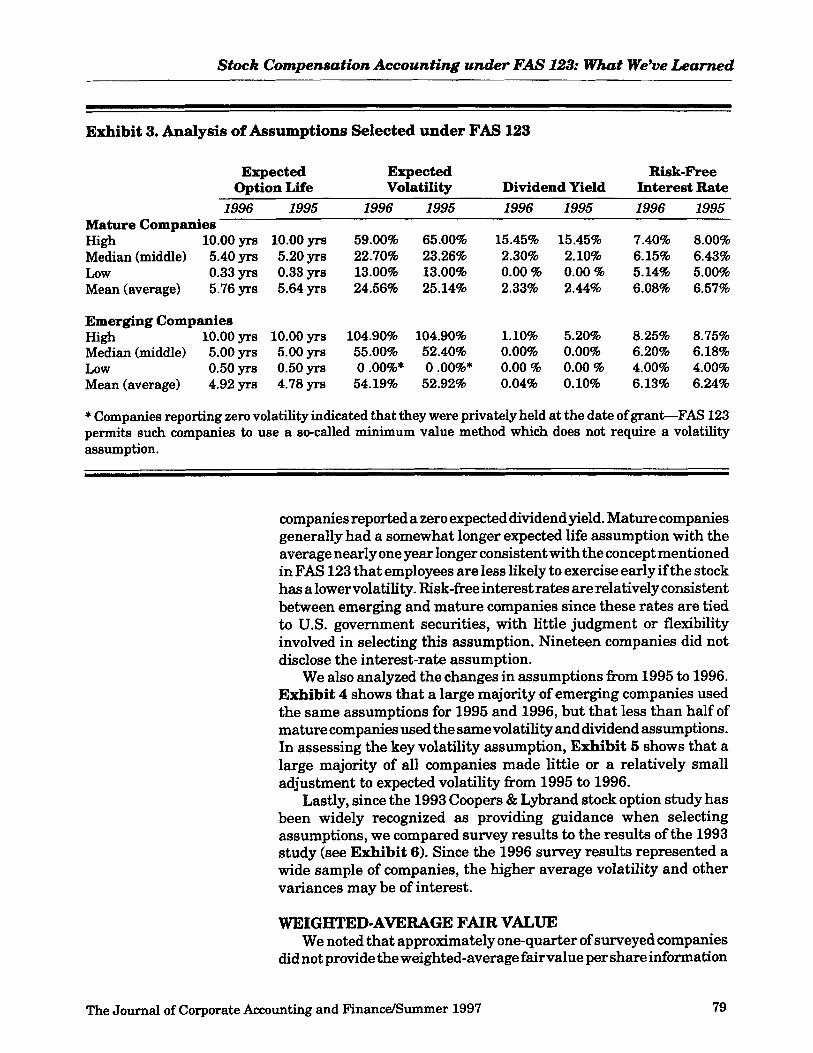

Exhibit 3 summarizes the assumptions selected by mature and emerging companies, showing the disclosed amounts in 1996 and 1995. As noted above, the key assumptions, such as expectedvolatility and dividend yield,varied considerably between emerging and mature companies. Average volatility for emerging companies was more than double thevolatility for mature companies, while most emerging

78 The Journal of Corporate Accounting and FinancdSummer 1997

Stock Compensation Accounting under FAS 123: What We've Learned

~~ ~

Exhibit 3. Analysis of Assumptions Selected under FAS 123

Expected Expected Risk-Free ODtion Life Volatility Dividend Yield Interest Rate

1996 1995 1996 1995 1996 1995 1996 1995 Mature Companies High 10.00 yrs 10.00 yrs 59.00% 65.00% 15.45% 15.45% 7.40% 8.00% Median (middle) 5.40 yrs 5.20 yrs 22.70% 23.26% 2.30% 2.10% 6.15% 6.43% LOW 0.33 yrs 0.33 yrs 13.00% 13.00% 0.00 % 0.00 % 5.14% 5.00% Mean (average) 5.76 yrs 5.64 yrs 24.56% 25.14% 2.33% 2.44% 6.08% 6.57%

Emerging Companies High 10.00 yrs 10.00 yrs 104.90% 104.90% 1.10% 5.20% 8.25% 8.75% Median (middle) 5.00 yrs 5.00 y r s 55.00% 52.40% 0.00% 0.00% 6.20% 6.18% LOW 0.50yrs 0.50yrs 0 .OO%* 0 .OO%* 0.00 % 0.00 % 4.00% 4.00% Mean (average) 4.92 yrs 4.78 ym 54.19% 52.92% 0.04% 0.10% 6.13% 6.24%

* Companies reporting zero volatility indicated that they were privately held at the date of grant-FAS 123 permits such companies to use a so-called minimum value method which does not require a volatility assumption.

companies reported a zero expected dividend yield. Mature companies generally had a somewhat longer expected life assumption with the average nearly one year longer consistent with the concept mentioned in FAS 123 that employees are less likely to exercise early if the stock has a lowervolatility. Risk-free interest rates are relatively consistent between emerging and mature companies since these rates are tied to U.S. government securities, with little judgment or flexibility involved in selecting this assumption. Nineteen companies did not disclose the interest-rate assumption.

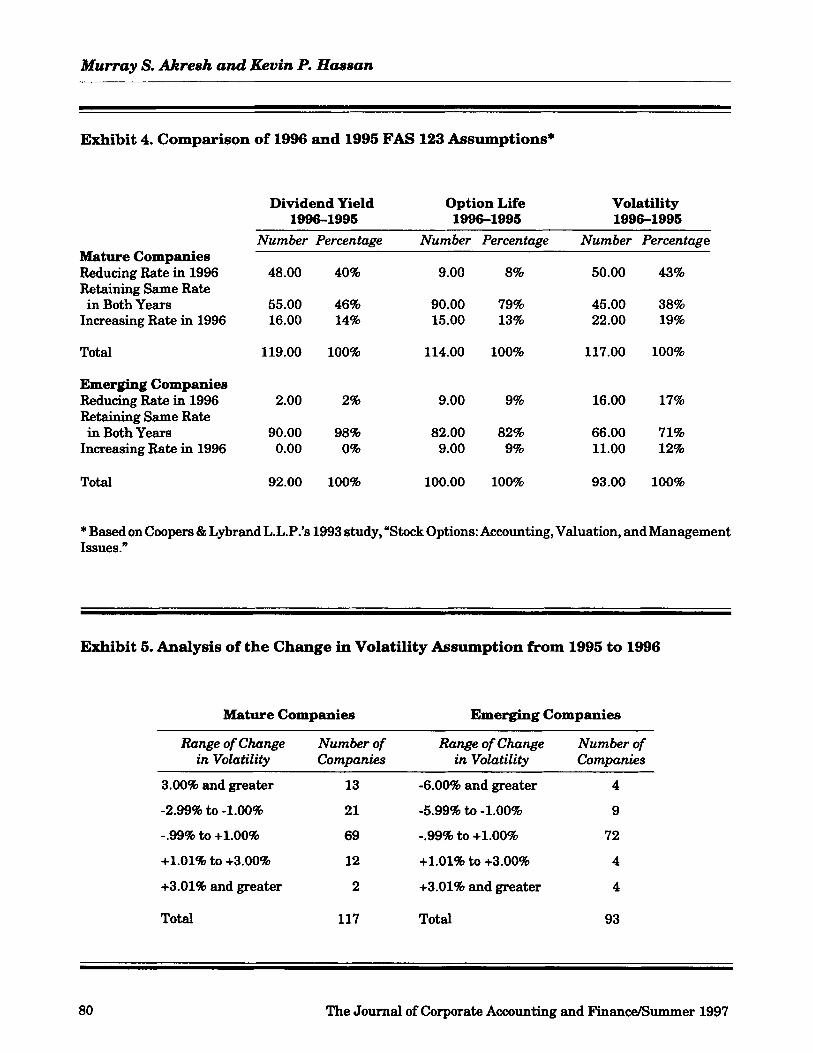

We also analyzed the changes in assumptions from 1995 to 1996. Exhibit 4 shows that a large majority of emerging companies used the same assumptions for 1995 and 1996, but that less than half of mature companies used the samevolatility and dividend assumptions. In assessing the key volatility assumption, Exhibit 5 shows that a large majority of all companies made little or a relatively small adjustment to expected volatility from 1995 to 1996.

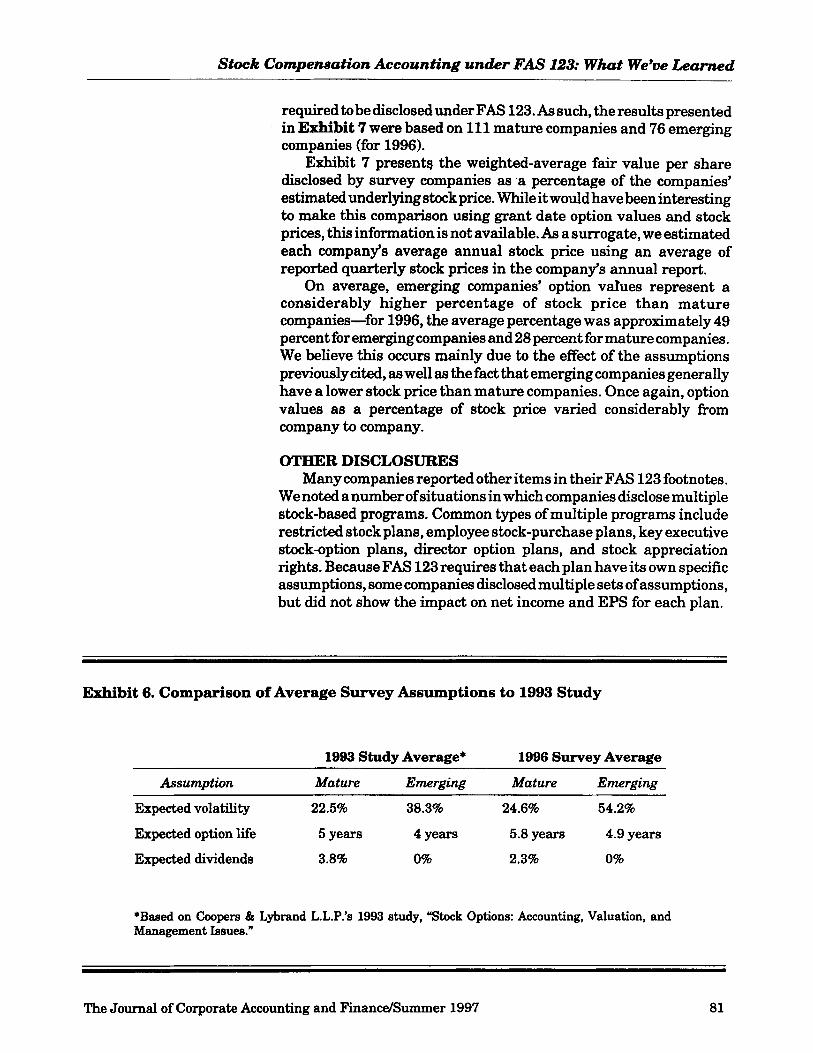

Lastly, since the 1993 Coopers & Lybrand stock option study has been widely recognized as providing guidance when selecting assumptions, we compared survey results to the results of the 1993 study (see Exhibit 6). Since the 1996 survey results represented a wide sample of companies, the higher average volatility and other variances may be of interest.

WEIGHTED-AVERAGE FAIR VALUE We noted that approximately one-quarter of surveyed companies

did not provide the weighted-average fair value per share information

The Journal of Corporate Accounting and F'inancdSummer 1997 79

Murray S. Akresh and Kevin P. Haasan

Exhibit 4. Comparison of 1996 and 1995 FAS 123 Assumptions*

Dividend Yield Option Life 1996-1995 1996-1995

Volatility 1996-1995

Mature Companies Reducing Rate in 1996 Retaining Same Rate

Increasing Rate in 1996 in Both Years

Total

Emerging Companies Reducing Rate in 1996 Retaining Same Rate

Increasing Rate in 1996 in Both Years

Total

Number Percentage Number Percentage Number Percentage

48.00 40% 9.00 8% 50.00 43%

55.00 46% 90.00 79% 45.00 38% 16.00 14% 15.00 13% 22.00 19%

119.00 100% 114.00 100% 117.00 100%

2.00 2% 9.00 9% 16.00 17%

90.00 98% 82.00 82% 66.00 71% 0.00 0% 9.00 9% 11.00 12%

92.00 100% 100.00 100% 93.00 100%

* Based on Coopers & Lybrand L.L.P.’s 1993 study, “Stock Options: Accounting, Valuation, and Management Issues.”

Exhibit 6. Analysis of the Change in Volatility Assumption from 1995 to 1996

Mature Companies Emerging Companies

Range of Change Number of Range of Change Number of in Volatility Companies in Volatility Companies

~ ~~ ~ ~~

3.00% and greater 13 -6.00% and greater 4

-2.99% to -1.00% 21 -5.99% to -1.00% 9

-.99% to +1.00% 69 -99% to +1.00% 72

+1.01% to +3.00% 12 +1.01% to +3.00% 4

+3.01% and greater 2 +3.01% and greater 4

Total 117 Total 93

80 The Journal of Corporate Accounting and Financ&ummer 1997

Stock Compensation Accounting under FAS 123: What We’ve Learned

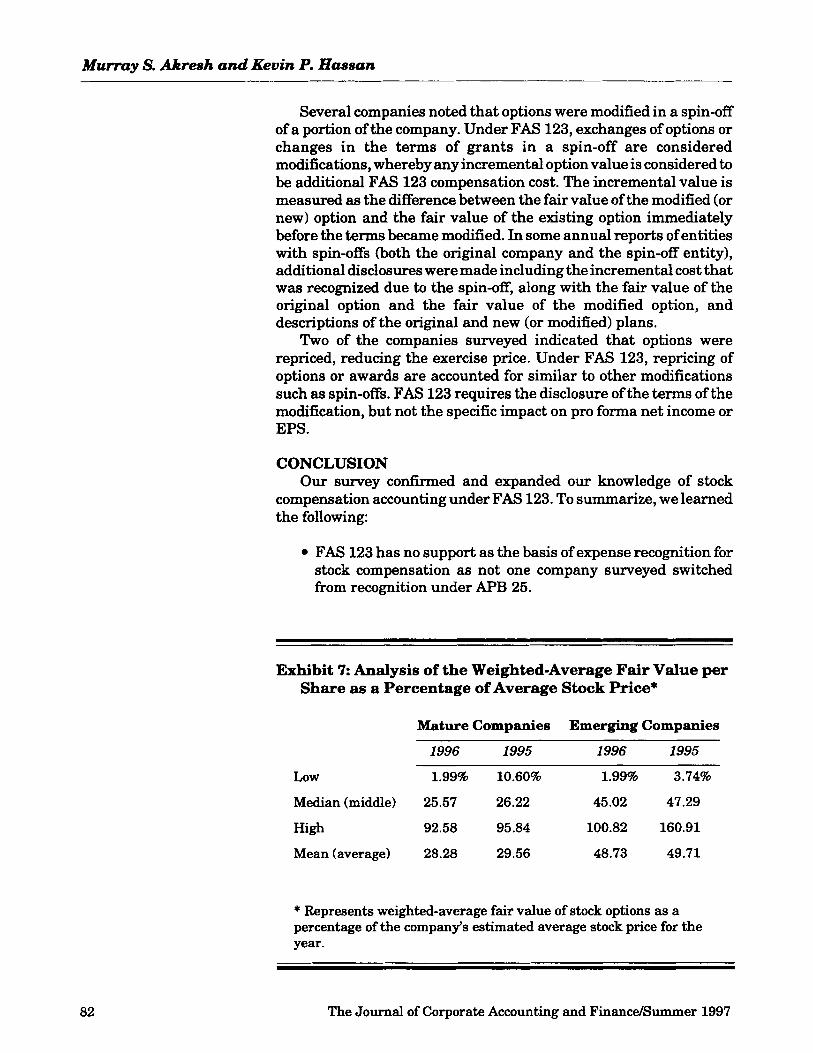

required to be disclosed under FAS 123. As such, the results presented in Exhibit 7 were based on 111 mature companies and 76 emerging companies (for 1996).

Exhibit 7 present4 the weighted-average fair value per share disclosed by survey companies as a percentage of the companies’ estimated underlying stuck price. While it would have been interesting to make this comparison using grant date option values and stock prices, this informationis not available. As a surrogate, we estimated each company’s average annual stock price using an average of reported quarterly stock prices in the company’s annual report.

On average, emerging companies’ option values represent a conaiderably higher percentage of stock price than mature companies-for 1996, the average percentage was approximately 49 percent for emerging companies and 28 percent for mature companies. We believe this occurs mainly due to the effect of the assumptions previously cited, as well as the fact that emerging companies generally have a lower stock price than mature companies. Once again, option values as a percentage of stock price varied considerably from company to company.

OTHER DISCLOSURES Many companies reported other items in their FAS 123 footnotes.

We noted a number ofsituations in which companies disclose multiple stock-based programs. Common types of multiple programs include restricted stock plans, employee stock-purchase plans, key executive stock-option plans, director option plans, and stock appreciation rights. Because FAS 123 requires that each plan have its own specific assumptions, some companies disclosed multiple sets of assumptions, but did not show the impact on net income and EPS for each plan.

Exhibit 6. Comparison of Average Survey Assumptions to 1993 Study

1993 Study Average* 1996 Survey Average

Assumption Mature Emerging Mature Emerging

Expected volatility 22.5% 38.3% 24.6% 54.2%

Expected option life 5 years 4 years 5.8 years 4.9 years

Expected dividends 3.8% 0% 2.3% 0%

*Based on Coopers & Lybrand L.L.P.’s 1993 study, “Stock Options: Accounting, Valuation, and Management Issues.”

The Journal of Corporate Accounting and FinancdSummer 1997 81

Murray S. Akresh and Kevin P. Haasan

Several companies noted that options were modified in a spin-off of a portion of the company. Under FAS 123, exchanges of options or changes in the terms of grants in a spin-off are considered modifications, whereby any incremental option value is considered to be additional FAS 123 compensation cost. The incremental value is measured as the difference between the fair value of the modified (or new) option and the fair value of the existing option immediately before the terms became modified. In some annual reports of entities with spin-offs (both the original company and the spin-off entity), additional disclosures were made including the incremental cost that was recognized due to the spin-off, along with the fair value of the original option and the fair value of the modified option, and descriptions of the original and new (or modified) plans.

Two of the companies surveyed indicated that options were repriced, reducing the exercise price. Under FAS 123, repricing of options or awards are accounted for similar to other modifications such as spin-offs. FAS 123 requires the disclosure of the tenns of the modification, but not the specific impact on pro fonna net income or EPS .

CONCLUSION Our survey confirmed and expanded our knowledge of stock

compensation accounting under FAS 123. To summarize, we learned the following:

FAS 123 has no support as the basis of expense recognition for stock compensation as not one company surveyed switched from recognition under APB 25.

Exhibit 7: Analysis of the Weighted-Average Fair Value per Share as a Percentage of Average Stock Price*

Mature Companies Emerging Companies

1996 1995 1996 1995

LOW 1.99% 10.60% 1.99% 3.74%

Median (middle) 25.57 26.22 45.02 47.29

High 92.58 95.84 100.82 160.91

Mean (average) 28.28 29.56 48.73 49.71

* Represents weighted-average fair value of stock options as a percentage of the company’s estimated average stock price for the year.

82 The Journal of Corporate Accounting and FinancdSummer 1997

Stock Compensation Accounting under FAS 123: What We've Learned

The impact of computing pro forma net income and EPS varied considerably between mature and emerging companies-and within those categories there are significant differences from company to company. Going forward, gauging FAS 123 results is not intuitive and companies need to "run the numbers" to fully understand the effect of new stock awards or assumption changes. FAS 123's rules are complex and in some cases difficult to apply in practice. For example, modification of awards due to a spin- off or exercise price reduction requires complex modeling and special disclosures. Disclosure requirements are extensive under FAS 123, but our survey indicated that companies found sufficient flexibility in terms of format and extent of the disclosure, which varied from company to company.

While much was learned from our survey, we still continue to have few answers to some questions. In particular, it is unclear whether analysts, shareholders, or other financial statement users will place significance on the pro forma amounts disclosed under FAS 123. In addition, FAS 123's impact on the design and granting of new stock-based awards is still to be seen. These key issues are critical in ultimately gauging FAS 123's impact on corporate America. +

The Journal of Corporate Accounting and F'inancdSummer 1997 83

![1 Pensions (FAS 87); Post Retirement Benefits (FAS 106); Post Employment Benefits (FAS 112); Disclosure about Pensions, etc. (FAS 132 [R]) – amendment](https://img.pdfslide.us/doc/110x75/56649d1f5503460f949f3b1c/1-pensions-fas-87-post-retirement-benefits-fas-106-post-employment-benefits.jpg)