Embed Size (px)

Citation preview

Stimulus and the great recession

Sinclair Davidson

Economics, Finance and Marketing 2

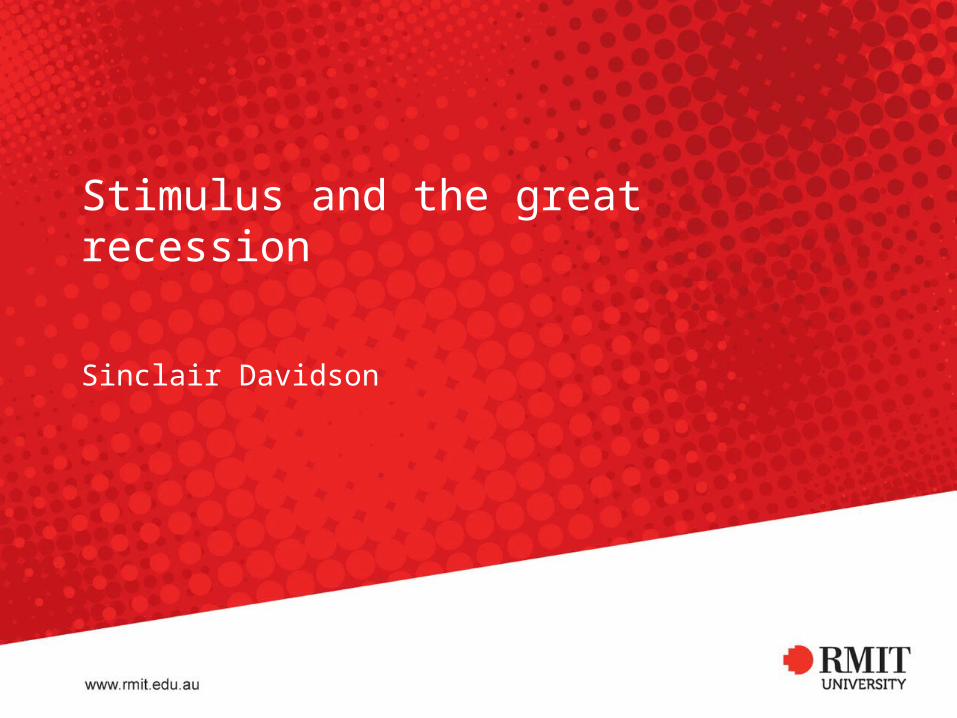

On the use of language

RMIT University © 2013

Economics, Finance and Marketing 3RMIT University © 2013

Adam Smith on Government

• The statesman who should attempt to direct private people in what manner they ought to employ their capitals, would … assume an authority which could safely be trusted, not only to no single person, but to no council or senate whatever, and which would nowhere be so dangerous as in the hands of a many who had folly and presumption enough to fancy himself fit to exercise it. (Book IV, Chapter II)

• It is the highest impertinence and presumption, therefore, in kings and ministers, to pretend to watch over the œconomy of private people…. They are themselves always, and without any exception, the greatest spendthrifts in the society. Let them look well after their own expence, and they may safely trust private people with theirs. If their own extravagance does not ruin the state, that of their subjects never will. (Book II, Chapter III)

Economics, Finance and Marketing 4RMIT University © 2013

Adam Smith on Economic Growth

• Great nations are never impoverished by private, though they sometimes are by publick prodigality and misconduct. The whole, or almost the whole publick revenue, is in most countries employed in maintaining unproductive hands. Such are the people who compose a numerous and splendid court, a great ecclesiastical establishment, great fleets and armies, who in time of peace produce nothing, and in time of war acquire nothing which can compensate the expence of maintaining them, even while the war lasts. Such people, as they themselves produce nothing, are all maintained by the produce of other men's labour. … Those unproductive hands, who should be maintained by a part only of the spare revenue of the people, may consume so great a share of their whole revenue, and thereby oblige so great a number to encroach upon their capitals, upon the funds destined for the maintenance of productive labour, that all the frugality and good conduct of individuals may not be able to compensate the waste and degradation of produce occasioned by this violent and forced encroachment. … (Book II, Chapter III)

Economics, Finance and Marketing 5RMIT University © 2013

Adam Smith on Economic Growth

• The annual produce of the land and labour of any nation can be increased in its value by no other means, but by increasing either the number of its productive labourers, or the productive powers of those labourers who had before been employed. The number of its productive labourers, it is evident, can never be much increased, but in consequence of an increase of capital, or of the funds destined for maintaining them. The productive powers of the same number of labourers cannot be increased, but in consequence either of some addition and improvement to those machines and instruments which facilitate and abridge labour; or of a more proper division and distribution of employment. In either case an additional capital is almost always required. (Book II, Chapter III)

Economics, Finance and Marketing 6

The role of fiscal policy

• Fiscal policy represents the spending and taxation (including borrowing) decisions taken by government.

– Provision of public goods.

– Provision of merit goods.

– Redistribution.

• Question: should fiscal policy be used as a tool to manage the economy?

– Can fiscal policy be used for counter-cyclical policy?

– Yes.– Keynesian theory suggests that government can successfully

intervene in the economy.

– No. – Ricardian equivalence suggests that government cannot

successfully intervene in the economy.

RMIT University © 2013

Economics, Finance and Marketing 7RMIT University © 2013

A digression on the Great Depression

• Popular Understanding of the Great Depression

– Capitalism lead to excesses in the 1920s.

– Economic growth was unsustainable.

– Stock Market crash of 1929 started the depression.

– Irresponsible application of orthodox policy worsened the depression.

– FDR saved the world by spending.

– A slightly more sophisticated view would have FDR and JM Keynes saving the world.

– When FDR did try to balance the budget he made things worse.

– WWII ended the Great Depression.

Economics, Finance and Marketing 8RMIT University © 2013

Popular Understanding of the Great Depression

• This is a very American view of the Great Depression.

• Probably exported to the world by popular culture and Hollywood.

• But even as a history of the US it is misleading.

• Amity Shlaes in The Forgotten Man: A New History of the Great Depression has a far more nuanced view of the Great Depression (pg. 392).

– ‘But what really stands out when you step back from the 1930s picture is not how much the New Deal public works achieved. It is how little. … The story of the mid-1930s is the story of a heroic economy struggling to recuperate but failing to do so because of perverse federal policy. The worst factor was Roosevelt’s war on business. But one can also make the argument that lawmakers’ pre-occupation with public works got in the way of allowing productive business to expand and pull the rest forward.’

• In February 1931 Ludwig von Mises had written– ‘All attempts to emerge from the crisis by new interventionalist measures

are completely misguided. There is only one way out of the crisis: Forgo every attempt to prevent the impact of market prices on production.’

Economics, Finance and Marketing 9RMIT University © 2013

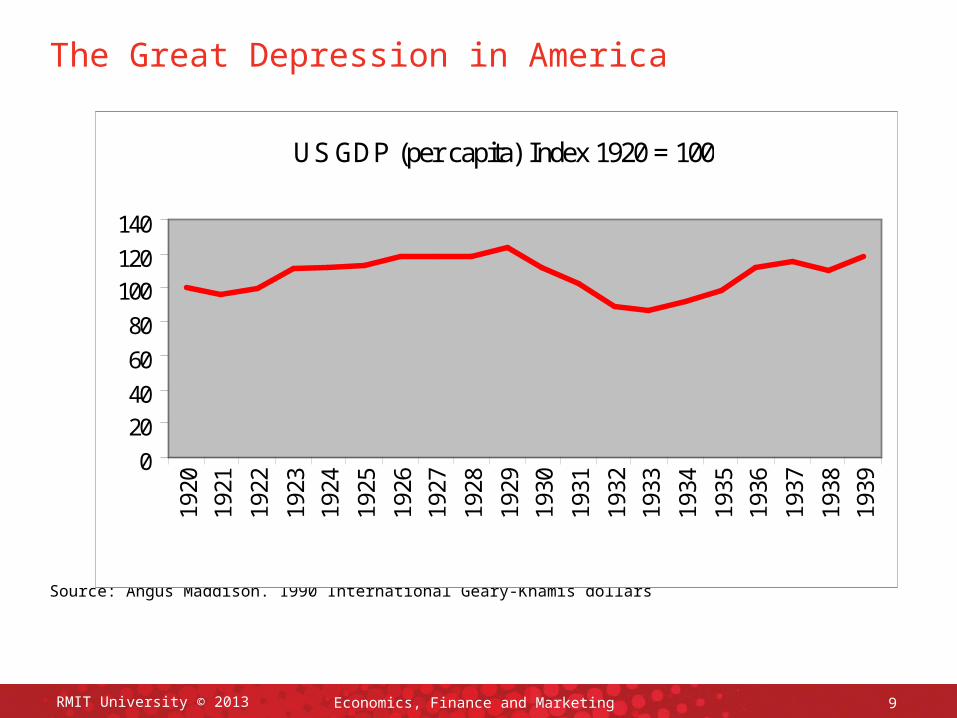

The Great Depression in America

Source: Angus Maddison. 1990 International Geary-Khamis dollars

US GDP (per capita) Index 1920 = 100

0

20

40

60

80

100

120

140

1920

1921

1922

1923

1924

1925

1926

1927

1928

1929

1930

1931

1932

1933

1934

1935

1936

1937

1938

1939

Economics, Finance and Marketing 10RMIT University © 2013

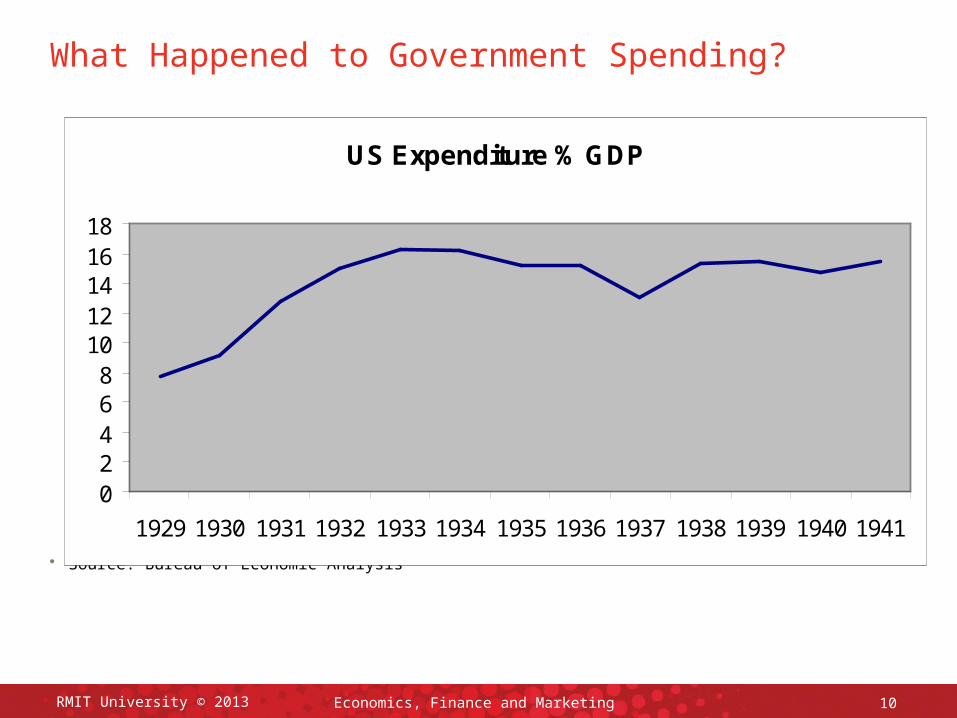

What Happened to Government Spending?

• Source: Bureau of Economic Analysis

US Expenditure % GDP

02468

1012141618

1929 1930 1931 1932 1933 1934 1935 1936 1937 1938 1939 1940 1941

Economics, Finance and Marketing 11RMIT University © 2013

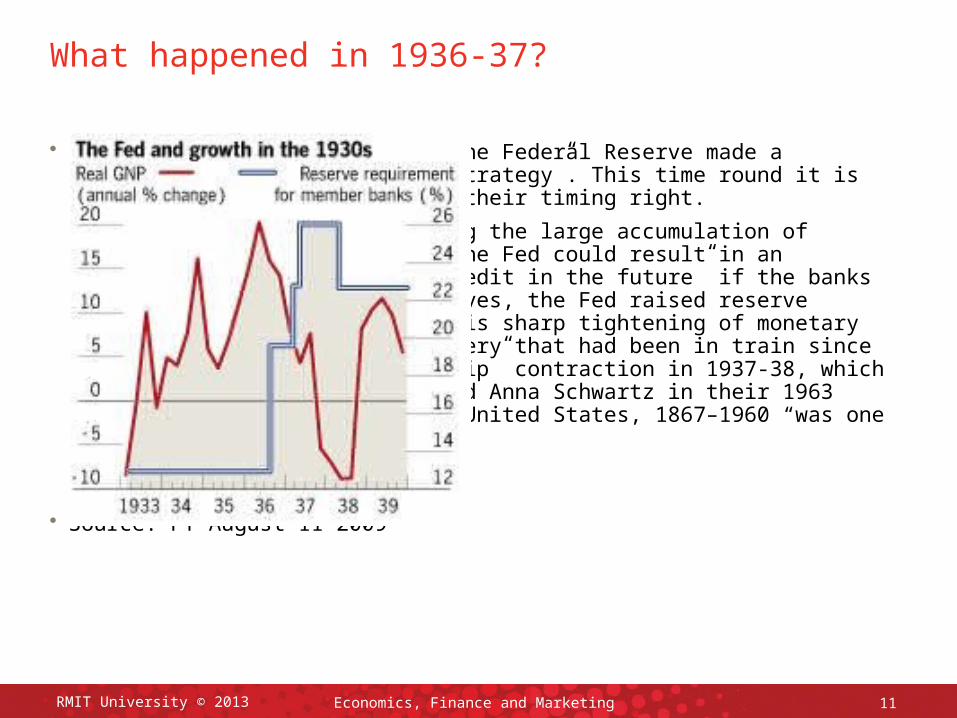

What happened in 1936-37?

• Source: FT August 11 2009

• Randall Kroszner “In 1936-37, the Federal Reserve made a colossal mistake in its “exit strategy”. This time round it is crucial that central banks get their timing right.

Seventy-three years ago, fearing the large accumulation of reserves held by the banks at the Fed could result in an “uncontrollable expansion of credit in the future” if the banks decided to lend out those reserves, the Fed raised reserve requirements to absorb them. This sharp tightening of monetary policy stopped the robust recovery that had been in train since 1933, precipitating a “double-dip” contraction in 1937-38, which according to Milton Friedman and Anna Schwartz in their 1963 book A Monetary History of the United States, 1867–1960 “was one of the sharpest on record”.”

Economics, Finance and Marketing 12RMIT University © 2013

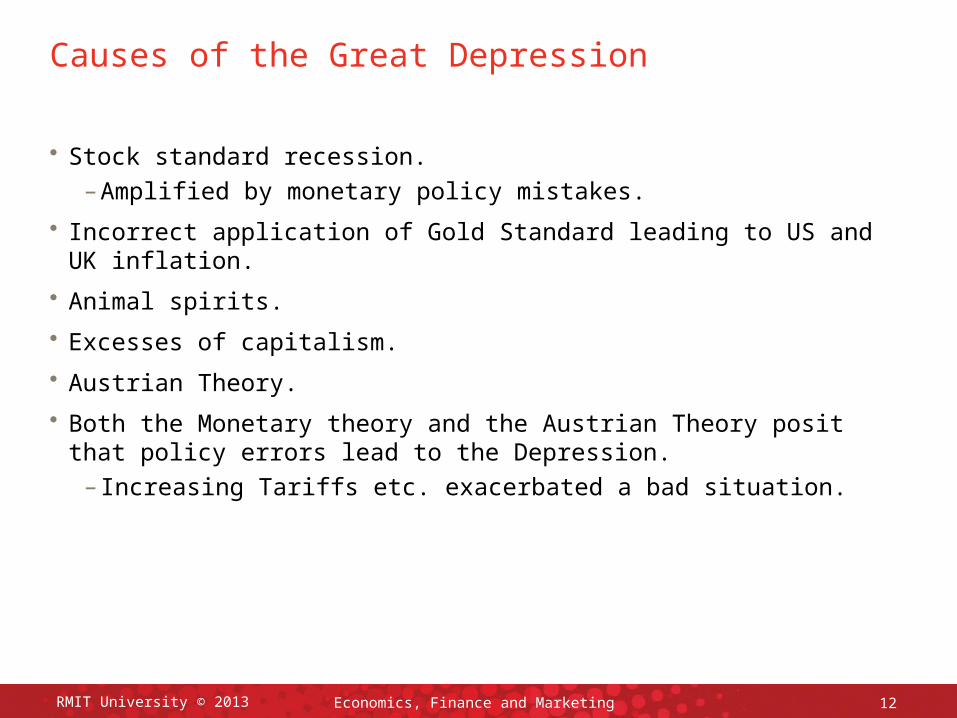

Causes of the Great Depression

• Stock standard recession.

– Amplified by monetary policy mistakes.

• Incorrect application of Gold Standard leading to US and UK inflation.

• Animal spirits.

• Excesses of capitalism.

• Austrian Theory.

• Both the Monetary theory and the Austrian Theory posit that policy errors lead to the Depression.

– Increasing Tariffs etc. exacerbated a bad situation.

Economics, Finance and Marketing 13RMIT University © 2013

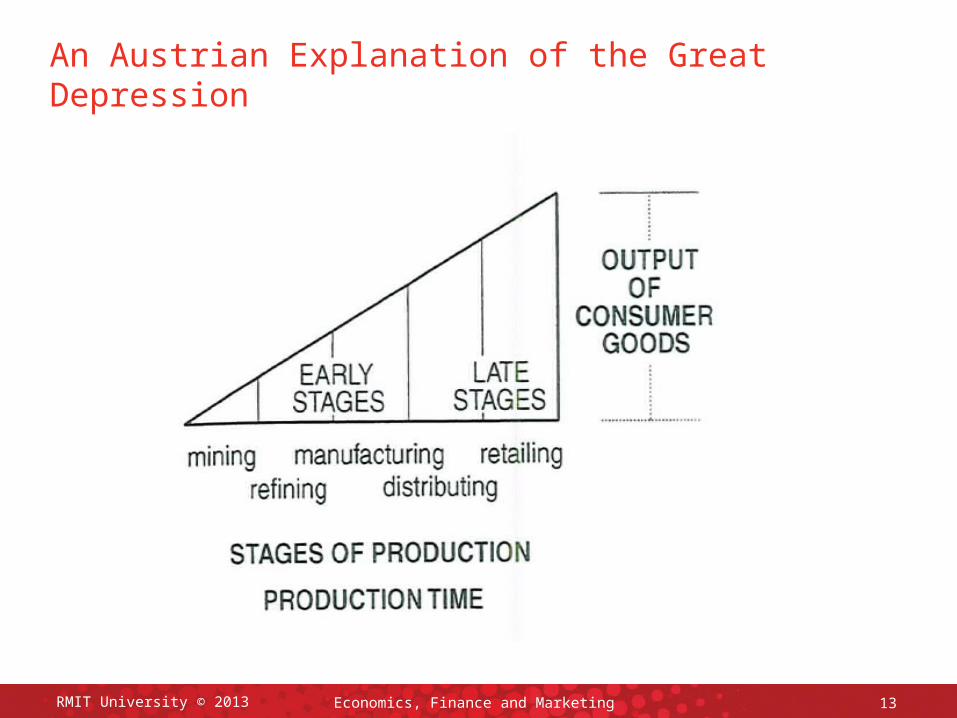

An Austrian Explanation of the Great Depression

Economics, Finance and Marketing 14RMIT University © 2013

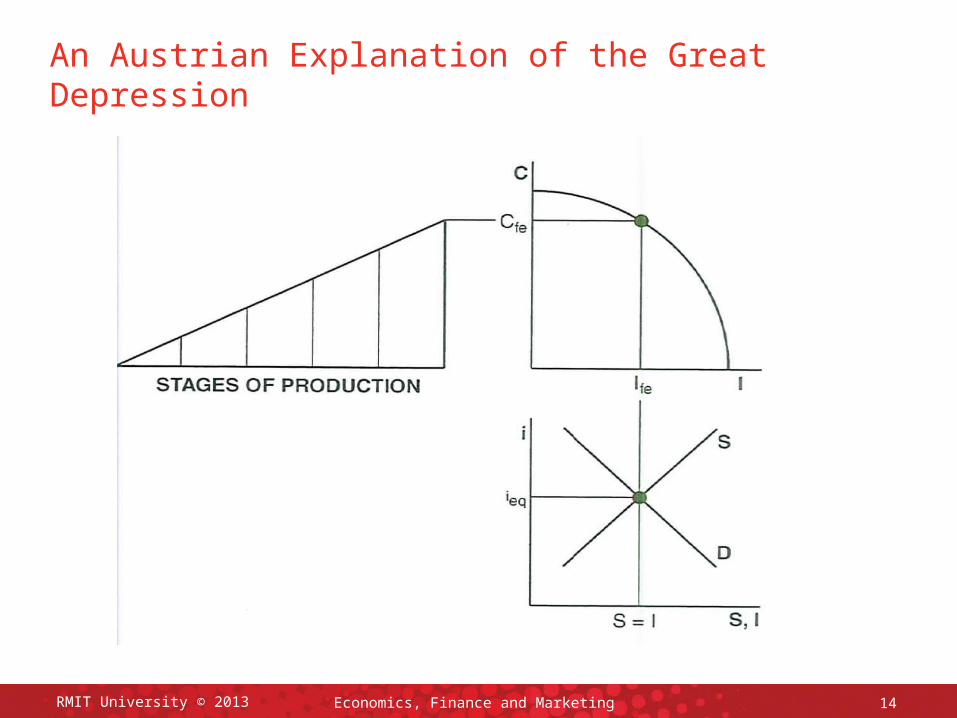

An Austrian Explanation of the Great Depression

Economics, Finance and Marketing 15RMIT University © 2013

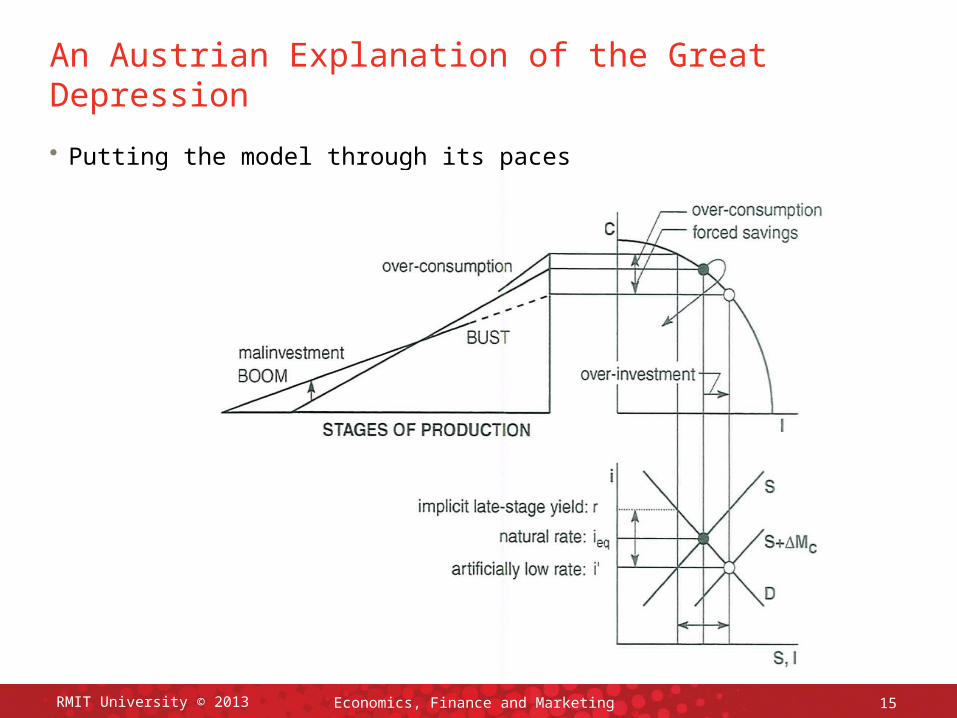

An Austrian Explanation of the Great Depression

• Putting the model through its paces

Economics, Finance and Marketing 16RMIT University © 2013

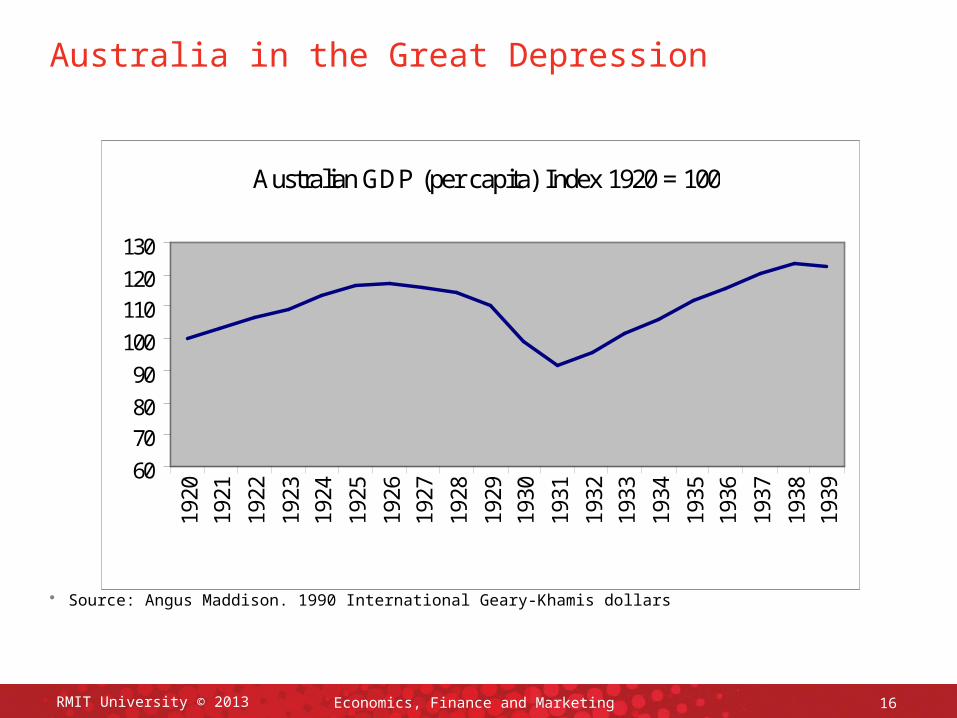

Australia in the Great Depression

• Source: Angus Maddison. 1990 International Geary-Khamis dollars

Australian GDP (per capita) Index 1920 = 100

60

70

80

90

100

110

120

130

1920

1921

1922

1923

1924

1925

1926

1927

1928

1929

1930

1931

1932

1933

1934

1935

1936

1937

1938

1939

Economics, Finance and Marketing 17RMIT University © 2013

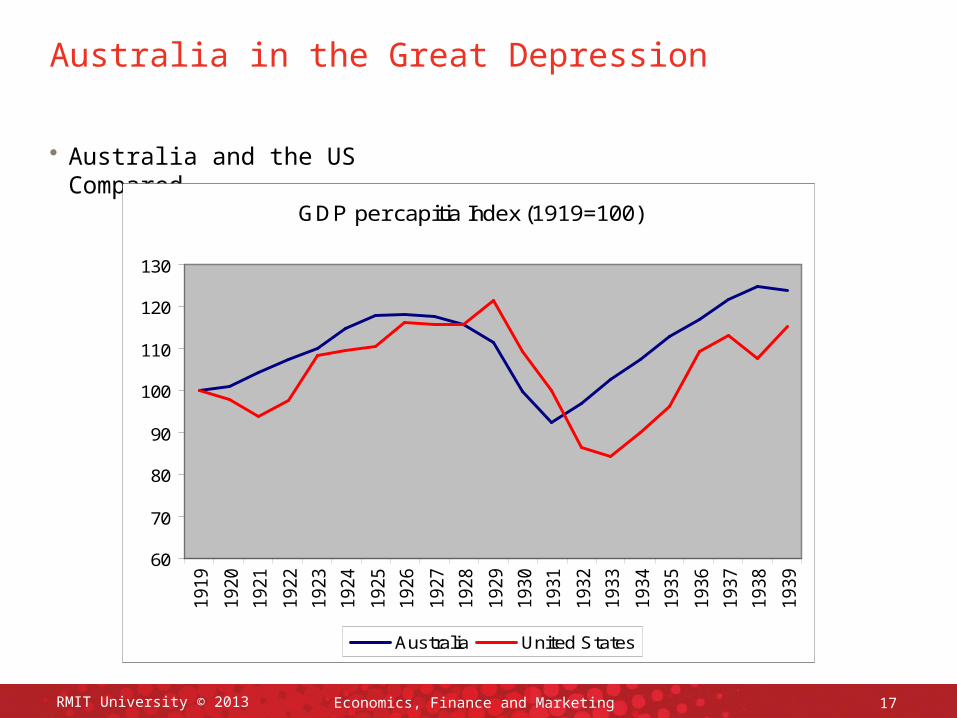

Australia in the Great Depression

• Australia and the US Compared

GDP per capitia Index (1919=100)

60

70

80

90

100

110

120

130

1919

1920

1921

1922

1923

1924

1925

1926

1927

1928

1929

1930

1931

1932

1933

1934

1935

1936

1937

1938

1939

Australia United States

Economics, Finance and Marketing 18RMIT University © 2013

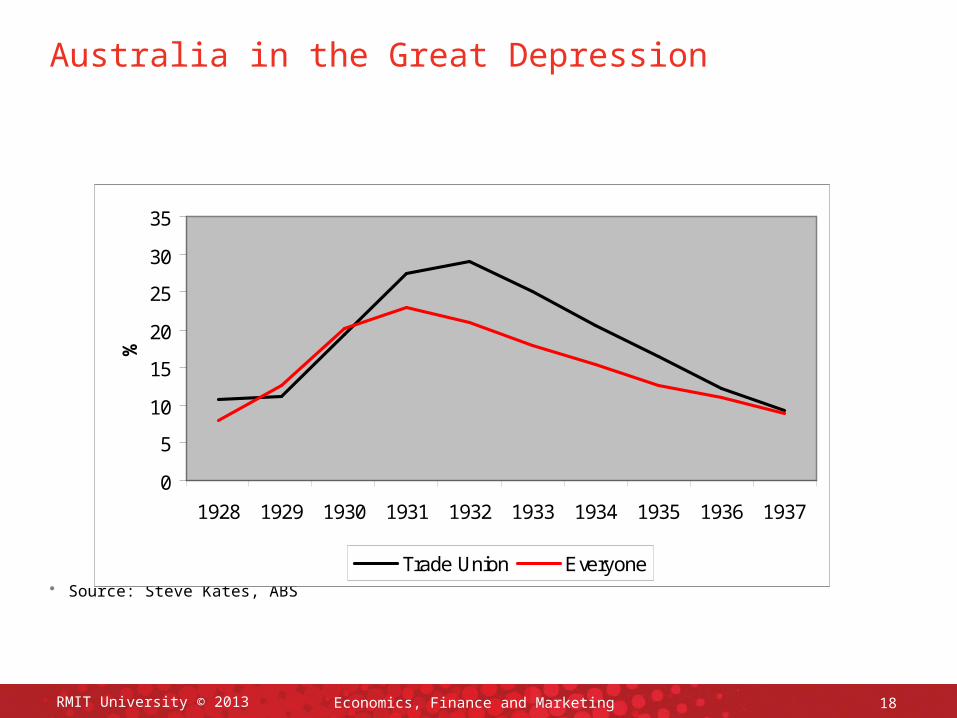

Australia in the Great Depression

• Source: Steve Kates, ABS

0

5

10

15

20

25

30

35

1928 1929 1930 1931 1932 1933 1934 1935 1936 1937

%

Trade Union Everyone

Economics, Finance and Marketing 19RMIT University © 2013

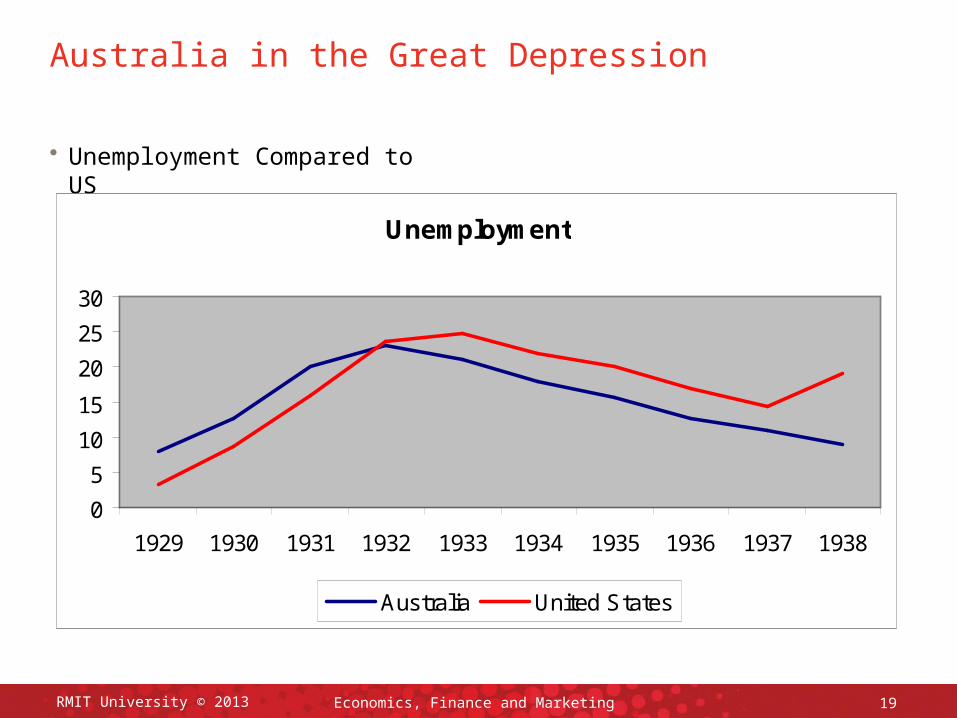

Australia in the Great Depression

• Unemployment Compared to US

Unemployment

0

5

10

15

20

25

30

1929 1930 1931 1932 1933 1934 1935 1936 1937 1938

Australia United States

Economics, Finance and Marketing 20RMIT University © 2013

Australia in the Great Depression

• You’ll notice the Australian turning point is very marked.

• What Happened in 1931?

– Australia went off the Gold Standard.

– Australia adopted the ‘Premiers’ Plan’.

• Kevin Rudd on the Premiers’ Plan

– ‘The alternatives [to the stimulus packages] were to do nothing or, worse, effectively replicate the Premiers' Plan of 1931 when governments cut expenditure, thereby compounding the problems created by a private sector already in retreat. The result, of course, was an economic rout, appalling unemployment and a decade of negligible growth through the 1930s.’

– This statement is completely at odds with Australian economic history but not political history – the ALP government was thrown out of office.

Economics, Finance and Marketing 21RMIT University © 2013

Australia in the Great Depression

• The Premiers’ Plan

– Reduction in government spending of 20 percent.

– Increase in Commonwealth income tax and sales tax.

– Reduction in interest Rates.

– Spending cuts were deeper that tax rises.

– Commonwealth ran a budget surplus from ‘ordinary transactions’ for the period 1931/2 onwards.

Economics, Finance and Marketing 22RMIT University © 2013

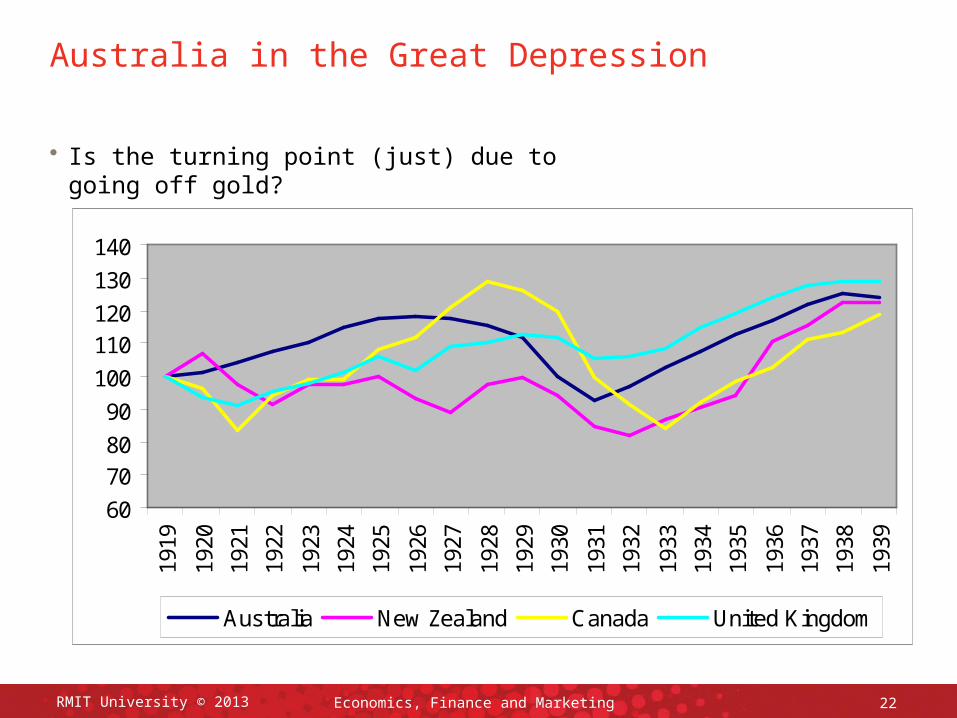

Australia in the Great Depression

• Is the turning point (just) due to going off gold?

60

7080

90

100

110120

130

140

1919

1920

1921

1922

1923

1924

1925

1926

1927

1928

1929

1930

1931

1932

1933

1934

1935

1936

1937

1938

1939

Australia New Zealand Canada United Kingdom

Economics, Finance and Marketing 23

Lessons learned from the Great Depression

• Lesson learned from the Great Depression:

– Keynes’ contribution: Replace the decline in private aggregate demand with increased public spending (and debt).

– Friedman’s contribution: Keep the stock of money in circulation from declining to ensure that monetary liquidity is maintained.

• Are those good lessons to have learned?

• What about these lessons? (Gwartney)

– Avoid these policies:

– Monetary contraction.

– Trade restrictions.

– Tax increases.

– Constant changes in policy; this merely creates uncertainty and delays private sector recovery.

RMIT University © 2013

Economics, Finance and Marketing 24RMIT University © 2013

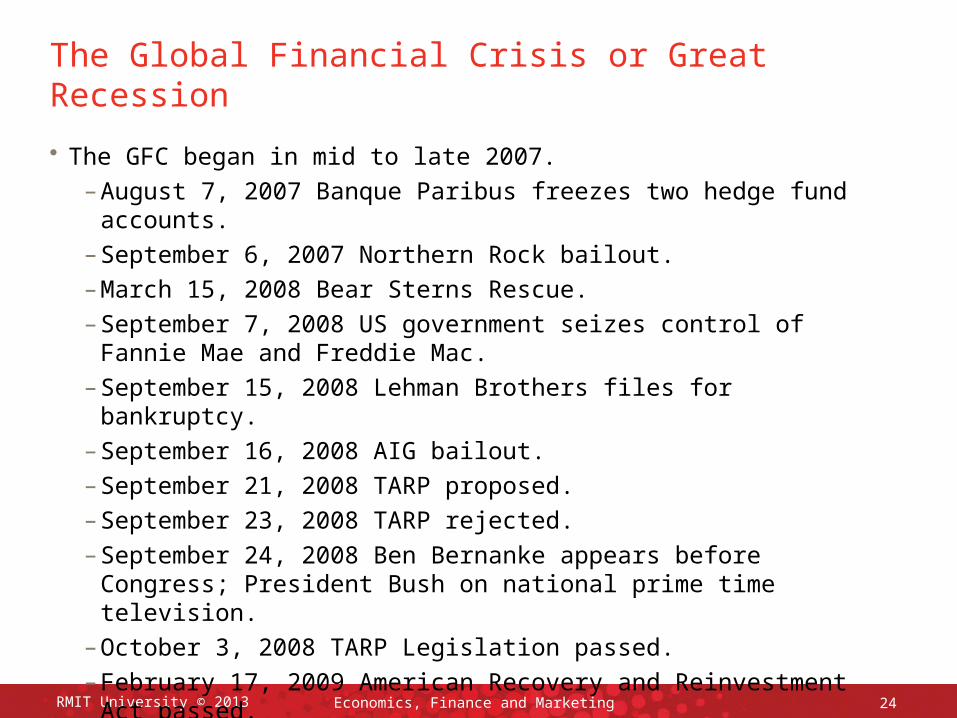

The Global Financial Crisis or Great Recession

• The GFC began in mid to late 2007.

– August 7, 2007 Banque Paribus freezes two hedge fund accounts.

– September 6, 2007 Northern Rock bailout.

– March 15, 2008 Bear Sterns Rescue.

– September 7, 2008 US government seizes control of Fannie Mae and Freddie Mac.

– September 15, 2008 Lehman Brothers files for bankruptcy.

– September 16, 2008 AIG bailout.

– September 21, 2008 TARP proposed.

– September 23, 2008 TARP rejected.

– September 24, 2008 Ben Bernanke appears before Congress; President Bush on national prime time television.

– October 3, 2008 TARP Legislation passed.

– February 17, 2009 American Recovery and Reinvestment Act passed.

Economics, Finance and Marketing 25RMIT University © 2013

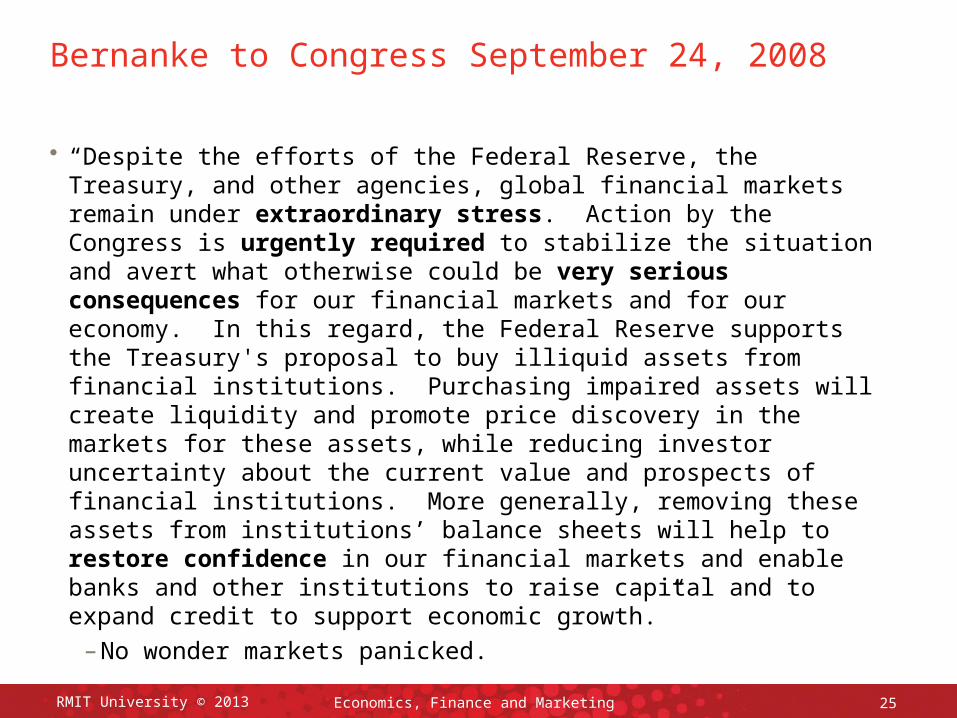

Bernanke to Congress September 24, 2008

• “Despite the efforts of the Federal Reserve, the Treasury, and other agencies, global financial markets remain under extraordinary stress. Action by the Congress is urgently required to stabilize the situation and avert what otherwise could be very serious consequences for our financial markets and for our economy. In this regard, the Federal Reserve supports the Treasury's proposal to buy illiquid assets from financial institutions. Purchasing impaired assets will create liquidity and promote price discovery in the markets for these assets, while reducing investor uncertainty about the current value and prospects of financial institutions. More generally, removing these assets from institutions’ balance sheets will help to restore confidence in our financial markets and enable banks and other institutions to raise capital and to expand credit to support economic growth.”

– No wonder markets panicked.

RMIT University © 2013 Economics, Finance and Marketing 26

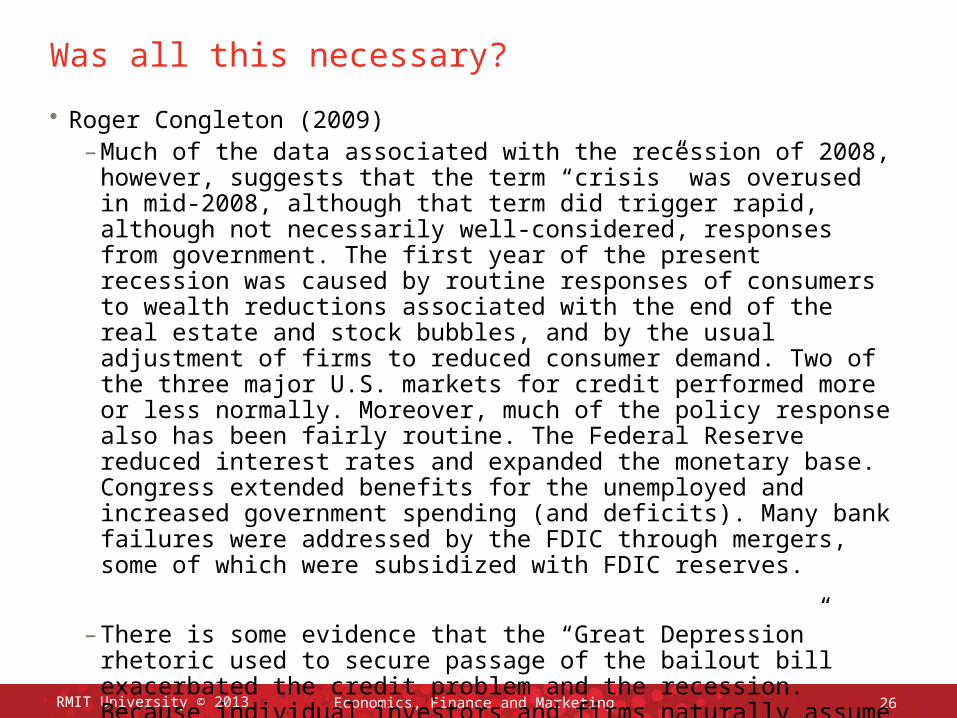

Was all this necessary?

• Roger Congleton (2009)– Much of the data associated with the recession of 2008, however,

suggests that the term “crisis” was overused in mid-2008, although that term did trigger rapid, although not necessarily well-considered, responses from government. The first year of the present recession was caused by routine responses of consumers to wealth reductions associated with the end of the real estate and stock bubbles, and by the usual adjustment of firms to reduced consumer demand. Two of the three major U.S. markets for credit performed more or less normally. Moreover, much of the policy response also has been fairly routine. The Federal Reserve reduced interest rates and expanded the monetary base. Congress extended benefits for the unemployed and increased government spending (and deficits). Many bank failures were addressed by the FDIC through mergers, some of which were subsidized with FDIC reserves.

– There is some evidence that the “Great Depression” rhetoric used to secure passage of the bailout bill exacerbated the credit problem and the recession. Because individual investors and firms naturally assume that Treasury experts have the very best data, the risk of another Great Depression apparently was “new news” to many of them.

Economics, Finance and Marketing 27RMIT University © 2013

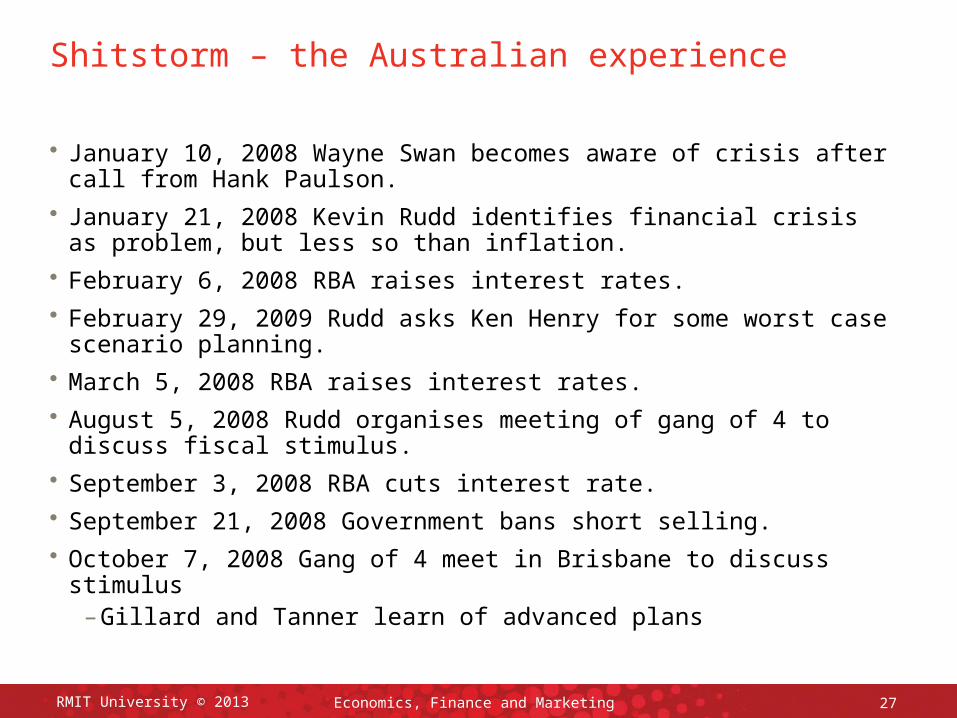

Shitstorm – the Australian experience

• January 10, 2008 Wayne Swan becomes aware of crisis after call from Hank Paulson.

• January 21, 2008 Kevin Rudd identifies financial crisis as problem, but less so than inflation.

• February 6, 2008 RBA raises interest rates.

• February 29, 2009 Rudd asks Ken Henry for some worst case scenario planning.

• March 5, 2008 RBA raises interest rates.

• August 5, 2008 Rudd organises meeting of gang of 4 to discuss fiscal stimulus.

• September 3, 2008 RBA cuts interest rate.

• September 21, 2008 Government bans short selling.

• October 7, 2008 Gang of 4 meet in Brisbane to discuss stimulus– Gillard and Tanner learn of advanced plans

Economics, Finance and Marketing 28RMIT University © 2013

Shitstorm – the Australian experience

• October 8, 2008 RBA drops interest rate by 100 basis points.

• October 9, 2008 Tanner is told stimulus plan will go ahead by his department secretary.

• October 11 – 12, 2008 Gang of 4 and bureaucrats discuss Stimulus I (Swan from US and Tanner from Melbourne).

• October 12, 2008 Government guarantees bank deposits.

• October 14, 2008 $10.4 billion stimulus package announced.

• November 5, 2008 RBA drops interest rate by 75 basis points.

• February 3, 2009 $42 billion stimulus package.

• February 4, 2009 RBA drops interest rate by 100 basis points.

• February 9, 2009 Senate Inquiry into Stimulus package – 3 economists appear for 10 minutes each.

• April 8, 2009 RBA drops interest rate by 25 basis points

• October 7, 2009 RBA raises interest rate by 25 basis points.

Economics, Finance and Marketing 29RMIT University © 2013

Doing the Time Warp

• Richard M. Salsman

– If there is anything more tragic than our current banking crisis, it is that the crisis is being blamed on the wrong group, on the bankers, instead of on the primary culprit, government intervention. The tragedy lies in failing to identify the fundamental cause of the problem, thereby ensuring its continuance. Bankers are not entirely innocent of wrongdoing in the present debacle, but to the extent that bankers have been irresponsible, it has been primarily government intervention that has encouraged them to be so. … Government has created these banking crises – by making it nearly impossible to practice prudent banking. Having done so, government has then pointed to bad banking practices as sufficient cause for still further interventions in the industry.

Economics, Finance and Marketing 30RMIT University © 2013

Doing the Time Warp

• Richard M. Salsman

– If there is anything more tragic than our current banking crisis, it is that the crisis is being blamed on the wrong group, on the bankers, instead of on the primary culprit, government intervention. The tragedy lies in failing to identify the fundamental cause of the problem, thereby ensuring its continuance. Bankers are not entirely innocent of wrongdoing in the present debacle, but to the extent that bankers have been irresponsible, it has been primarily government intervention that has encouraged them to be so. … Government has created these banking crises – by making it nearly impossible to practice prudent banking. Having done so, government has then pointed to bad banking practices as sufficient cause for still further interventions in the industry.

• These words were written in 1991!

• They could have been written to describe the current crisis.

Economics, Finance and Marketing 31RMIT University © 2013

The Global Financial Crisis

• Causes of the Global Financial Crisis

– Bubbles: Very unsatisfactory explanation.

– The Krugman Hypothesis: ‘Alan Greenspan needs to create a housing bubble to replace the Nasdaq bubble.’

– Imbalances: It is true that there are various imbalances in the international economy, many of these are due to various government interventions to prevent prices from fully reflecting economic conditions.

– Financial Deregulation: The idea that the financial system is very deregulated has taken hold. Financial deregulation is a mythical beast.

– Minsky moment:

– The Efficient Market Hypothesis: Very confused explanation.

– Greed: Trivially true, yet what is lacking is an explanation for the sudden outbreak of greed. ‘Greed’ is a constant.

– Government intervention: A perverse incentives argument is likely to be able to explain much of origins of the crisis.

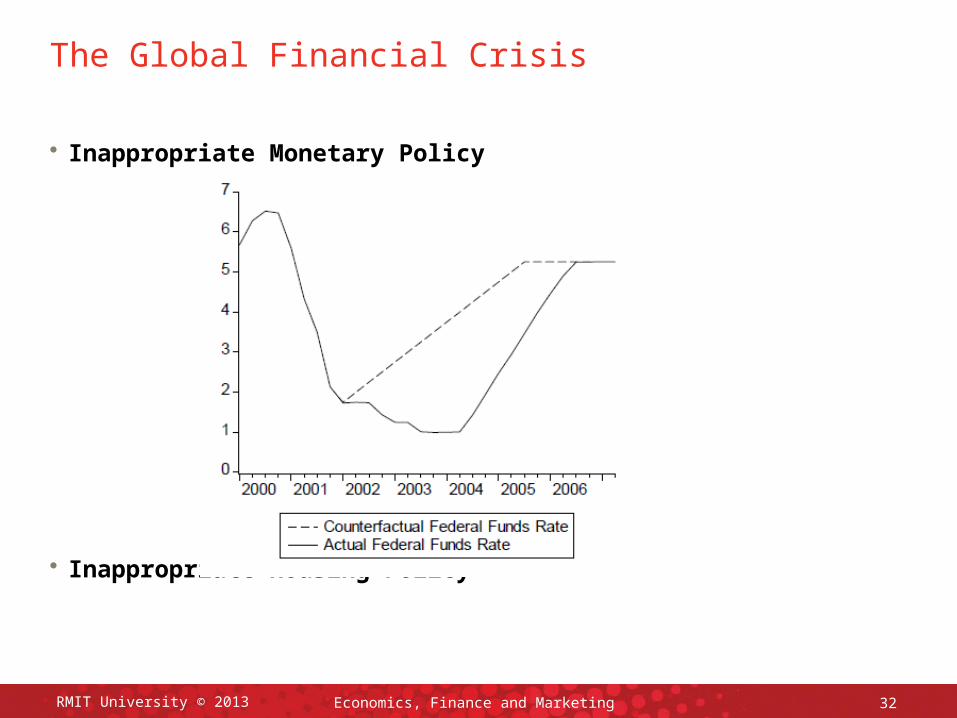

Economics, Finance and Marketing 32RMIT University © 2013

The Global Financial Crisis

• Inappropriate Monetary Policy

• Inappropriate Housing Policy

The deterioration in lending standards

• In the 1970s US social justice activists alleged that banks and other financial institutions were discriminating against minorities – usually African Americans and Hispanics – in a practice known as ‘redlining’.

– The Home Mortgage Disclosure Act (HMDA) required banks and financial institutions to collect and report data on their mortgage applicants.

– The Community Reinvestment Act (CRA) of 1977 required banks and financial institutions to conduct business over the entire geographic region where they operated.

• In 1992, the Boston Federal Reserve produced a working paper, subsequently published in the prestigious peer-reviewed American Economic Review that provided empirical evidence showing that banks were discriminating against minorities.

RMIT University © 2013 Economics, Finance and Marketing 33

The deterioration in lending standards

• Banks were directed by government policy choice to make loans they otherwise would not make and were able to on-sell the loans.

• This type of government action assumes that politicians and bureaucrats can better understand and manage financial institutions than the management of those organisations.

– It also makes the assumption that lenders dislike minorities more than they like making profit.

– Financial markets have historically been very competitive so this form of discrimination would be very unprofitable and would likely not survive long.

– Those individuals making the redlining argument have never explained how and why it survives.

RMIT University © 2013 Economics, Finance and Marketing 34

The deterioration in lending standards

• It subsequently transpired that the data used in the 1992 Boston Fed paper was deeply and fundamentally flawed.

• Unfortunately they never made their entire data set public. There was a series of academic papers that criticised the Fed report.

– One 1994 study looked at a very small sub-sample of the data yet found that more than half the observations contained serious errors.

– The definitive study the Boston Fed report was conducted by Theodore Day and Stan Liebowitz and was published in the 1998 Economic Inquiry – also a peer reviewed journal.

– That study found that after correcting the most severe data errors that no evidence of racial discrimination could be found – banks and other financial institutions had not engaged in redlining.

RMIT University © 2013 Economics, Finance and Marketing 35

The deterioration in lending standards

• The Boston Fed had published a document in 1993 entitled ‘Closing the gap: A guide to equal opportunity lending’; it is still available on their website.

– ‘Even the most determined lending institution will have difficulty cultivating business from minority customers if its underwriting standards contain arbitrary or unreasonable measures of creditworthiness.’

– ‘Policies regarding applicants with no credit history or problem credit history should be reviewed. Lack of credit history should not be seen as a negative factor.’

• Stan Liebowitz

– Those “outdated” standards existed to limit defaults. But bank regulators required the loosened underwriting standards, with approval by politicians and the chattering class. … It also let community activists intervene at yearly bank reviews, shaking the banks down for large pots of money. Banks that got poor reviews were punished; some saw their merger plans frustrated; others faced direct legal challenges by the Justice Department.

RMIT University © 2013 Economics, Finance and Marketing 36

RMIT University © 2013 Economics, Finance and Marketing 37

Partial mea culpa

• Lawrence Lindsey, former member of the Federal Board of Governors

– The regulatory community was placed under intense political pressure to come up with ways of providing access to credit for those populations, and did so, most notably with new rules under the Community Reinvestment Act. I was involved in that process and am proud of what was accomplished. In fact, most of those individuals could be and did turn out to be responsible borrowers and homeowners. But there can also be little doubt that in hindsight the new regulations did contribute to some of the excessive expansion in credit that has occurred. I note this mainly to provide a cautionary tale. Even very well intentioned and largely successful regulations can have unintended consequences.

Economics, Finance and Marketing 38RMIT University © 2013

Round up the usual suspects

• Government Senators’ Minority Report (October 2009)– From the middle of 2007, financial markets began showing signs of

considerable turmoil as the realities of trade in exotic financial derivatives and the explosion in sub-prime lending that had characterised the finance market boom became clear.As subsequent events would reveal, inadequate regulation and greed on the part of financial market players would set in train a sequence of events in the United States, the United Kingdom and Europe that would culminate in the collapse, nationalisation or government bailout of major banks, insurers and credit providers. These included Citigroup, American International Group, Northern Rock, Fannie Mae, Freddie Mac, Bank of America, Goldman Sachs, Morgan Stanley, Royal Bank of Scotland, Lloyds TSB, HBOS and a number of major continental European financial institutions. The list of institutions involved reads like a veritable Who’s Who of those who only months earlier would have considered themselves “masters of the universe”. As we now know, these emperors had no clothes.

Economics, Finance and Marketing 39

Round up the usual suspects

• Peter Wallison in a dissenting report to the US Financial Crisis Inquiry Commission

– Like Congress and the Administration, the Commission’s majority erred in assuming that it knew the causes of the financial crisis. Instead of pursuing a thorough study, the Commission’s majority used its extensive statutory investigative authority to seek only the facts that supported its initial assumptions—that the crisis was caused by “deregulation” or lax regulation, greed and recklessness on Wall Street, predatory lending in the mortgage market, unregulated derivatives and a financial system addicted to excessive risk-taking. The Commission did not seriously investigate any other cause, and did not effectively connect the factors it investigated to the financial crisis. The majority’s report covers in detail many elements of the economy before the financial crisis that the authors did not like, but generally failed to show how practices that had gone on for many years suddenly caused a world-wide financial crisis. In the end, the majority’s report turned out to be a just so story about the financial crisis, rather than a report on what caused the financial crisis.

RMIT University © 2013

Making excuses

• A minority report in the US Financial Crisis Inquiry Commission did argue that contentious regulatory failures in the US could be justified.

• Regulator behaviour

– “The government should not have bailed out _____”.

– For a policymaker, the calculus is simple: if you bail out AIG and you’re wrong, you will have wasted taxpayer money and provoked public outrage. If you don’t bail out AIG and you’re wrong, the global financial system collapses.

– Regulators follow a mini-max rule – they minimize their maximum regret.

RMIT University © 2013 Economics, Finance and Marketing 40

Making excuses

– “Bernanke, Geithner, and Paulson should not have chosen to let Lehman fail”.

– To make this case one must argue:– Bernanke, Geithner, and Paulson had a legal and viable option

available to them other than Lehman filing bankruptcy.– They knew they had this option, considered it, and rejected it.– They were wrong to do so.– They had a reason for choosing to allow Lehman to fail.

– These conditions were not met – unlike many of the other firms there was no credible buyer for Lehman.

– It wasn’t just the failure of Lehman Brothers that intensified the crisis.– In quick succession in September 2008, the failure, near-failure, or

restructuring of ten firms triggered a global financial panic.

RMIT University © 2013 Economics, Finance and Marketing 41

Economics, Finance and Marketing 42RMIT University © 2013

Sensible Commentary I

• Wall Street Journal Asia (November 2009)

– The idea that bankers caused the financial crisis is only credible with politicians and unaccountable bureaucrats. It’s especially seductive in the U.S., where Wall Street firms leveraged up to their necks and then took taxpayer money when they were bailed out. But no such crisis happened in Hong Kong, where banks more prudently managed their balance sheets.

The idea, too, that a public-sector bureaucrat can better align banker incentives than a competitive marketplace is laughable. In its draft proposal the HKMA didn't define what “excessive risk” is because it doesn’t know. Only a private-sector banker competing to hire talent away from a rival can make that judgment.

Economics, Finance and Marketing 43RMIT University © 2013

Sensible Commentary II

• Wall Street Journal Europe (November 2009)

– Whether banks benefit from the explicit guarantees of deposit insurance or the implicit protection of being too-big-to-fail, or both, governments have a right to demand that banks not ride free on the backs of taxpayers.

But whether it's less leverage, more capital, or restrictions on banking activities, no one should be under any illusion that the same people who failed to detect the last bubble and crash will be able to design a system capable of catching the next one in time. The relative risks of being too lax or too restrictive may be hard to gauge, but either way the odds of getting it wrong are substantial if not overwhelming.

This is why putting the risk of failure back into the system should be the sine qua non of any effort at reform. If regulators around the world get nothing else right, the final backstop has to be bankruptcy and/or dissolution for firms that have earned it.

RMIT University © 2013 Economics, Finance and Marketing 44

What do Banks do?

• The business of banking is well-described by Ludwig von Mises (1912, 1981)

– Banks borrow money in order to lend it; the difference between the rate of interest that is paid to them and the rate that they pay, less their working expenses, constitutes their profit on this kind of transaction.

– Imprudent granting of credit is bound to prove just as ruinous to a bank as to any other merchant. That follows from the legal structure of their business; there is no legal connection between their credit transactions and their debit transactions, and their obligation to pay back the money they have borrowed is not affected by the fate of their investments; the obligation continues even if the investments prove dead losses.

Economics, Finance and Marketing 45RMIT University © 2013

The Logic of Stimulus

• David Gruen: Australian Business Economists Conference (December 2008).

– The first, and most obvious, benefit is that involuntary unemployment is lower than it would otherwise be. …

– But there are further benefits to avoiding a recession that would need to be taken into account in a realistic cost-benefit analysis of discretionary fiscal stimulus. Recessions break productive links between firms, and between firms and workers, when firms that would otherwise be viable over the long-term are driven into bankruptcy by a recession. In other words, plenty of the destruction that occurs in a recession is not creative destruction.

Finally, recessions do long-lasting damage, particularly to that cohort of people entering the labour market at the time the recession hits. Thus, for example, university graduates entering the labour market in a recession suffer sizeable initial earnings losses, losses that persist for a period estimated at between eight and fifteen years – that is, long after the recession has ended (Oreopoulos et al., 2006, Kahn 2009).

Economics, Finance and Marketing 46RMIT University © 2013

The Logic of Stimulus

• Robert Reich believes government spending is self-financing

– "The huge debts we're wracking up will cause your taxes to rise!" Wrong again. When it comes to the national debt, as I've said before, the relevant statistic is the ratio of debt to the gross domestic product. The only sure way to bring that debt down and make it manageable in future years is to get the economy growing again -- which requires that, in the short term, the government spend a lot of money (because consumers and businesses won't).

• Lateral Economics

– So for every dollar the government spent, tax revenue to Australia’s governments rose by around 22.5 cents, leaving just 77.5 cents to be repaid. The total windfall to the budget – and to the community – of the additional tax revenue from the cash transfers is around $6.7 billion. This money and the production of all those people and all that capital kept in employment are the riches of good economic management – the only kind of free lunch we know of.

Economics, Finance and Marketing 47RMIT University © 2013

The logic of the stimulusSuppose I walk up to you and forcibly take from your wallet $3636. That is roughly about the amount of the Federal Government's combined stimulus programs per head of population.

I immediately give you back $900 of this for you to spend on anything you want - cigarettes, clothing, computer games, fridges, handbags, mobile phones, tattoos, anything you care to buy. You could even deposit it straight back into your own bank account.

I then spend $2227 of your money on things that take my fancy.

Some lobbyist told me that throwing some of the money I've taken from you (let's call it what it is, a tax) towards housing insulation batts would somehow save the Earth. Someone else whispered in my ear that spending a fraction of the $2227 tax take on school gyms, at inflated rates, would help kids read, write, add and subtract. In fact, so many people are lobbying me to spend your money that I need more cash from elsewhere. I resolve this by borrowing even more currency, on top of your taxes.

I forgot to mention at the outset that 14 cents out of every dollar I spend is on my own administration costs.Julie Novak - The Courier Mail 23rd September, 2009

RMIT University © 2013 Economics, Finance and Marketing 48

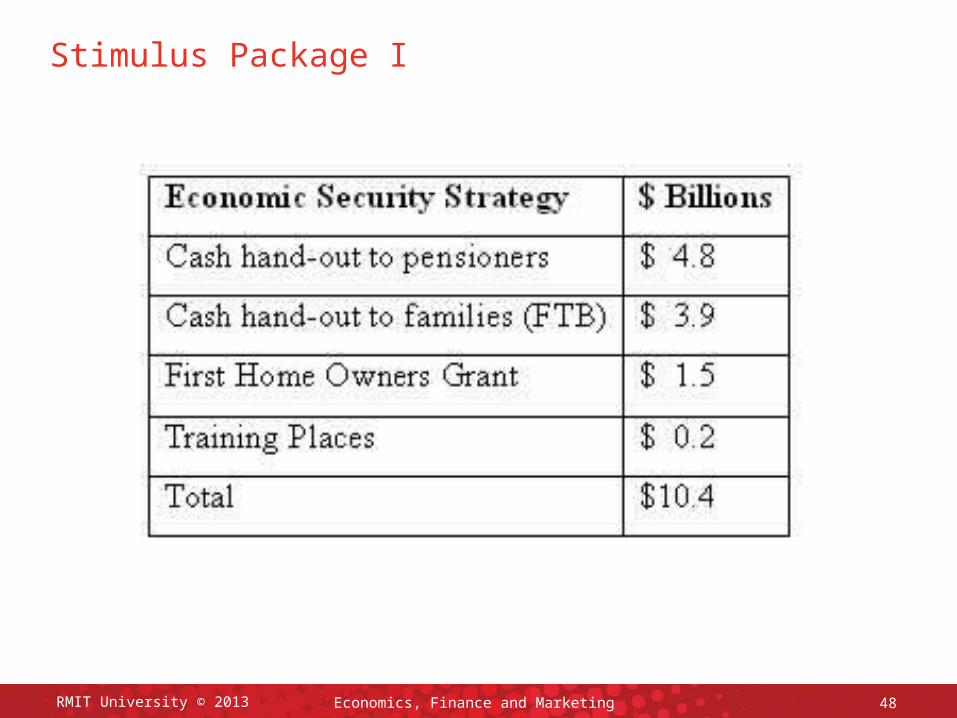

Stimulus Package I

RMIT University © 2013 Economics, Finance and Marketing 49

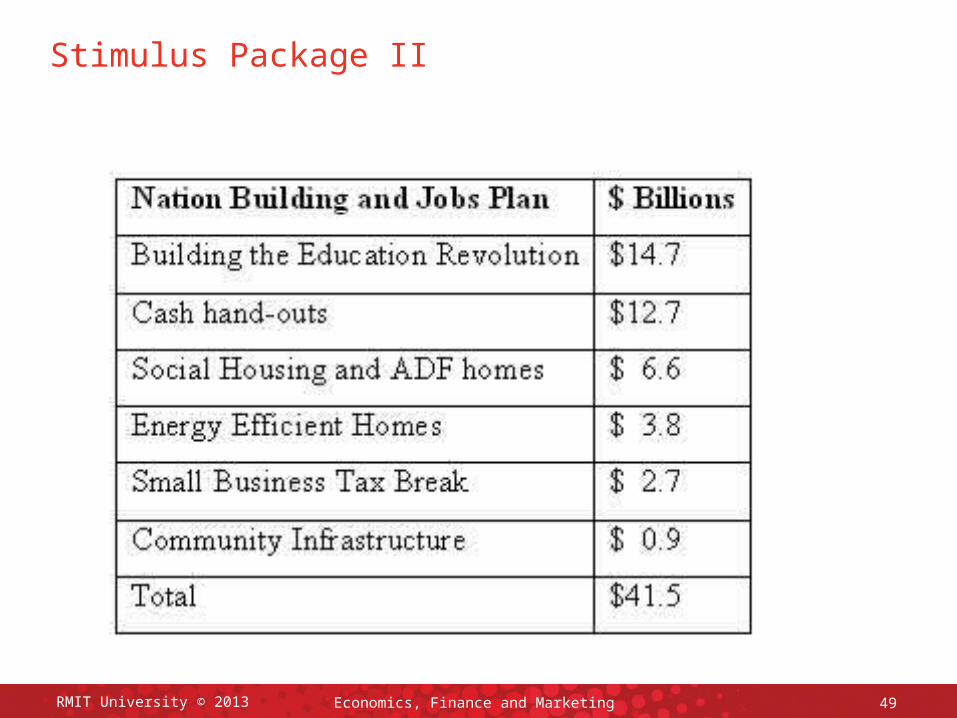

Stimulus Package II

RMIT University © 2013 Economics, Finance and Marketing 50

Other Spending

• December 2008: Nation Building Package $4.7 billion

• May 2009: Nation Building Infrastructure $22.5 billion

• Total: $79.1 billion

– Stimulus I: $10.4 billion

– Stimulus II: $41.5 billion

– Nation Building: $4.7 billion

– Budget: $22.5 billion

Economics, Finance and Marketing 51RMIT University © 2013

What I said in February 2009

In summary, it is my view that the Senate should reject the fiscal stimulus package in its current format.

– The package contains a lot of spending and little actual stimulus.

– The proposed spending is poor quality expenditure of Federal funding.

– Discretionary fiscal policy has a poor track record of success.

– While the government needs to respond to the current economic down turn in a timely manner, there is no immediate urgent need to rush the package. Rather a better quality package should be designed and implemented.

Economics, Finance and Marketing 52RMIT University © 2013

What I said in February 2009

• Government policy should establish conditions whereby living standards can improve.

• Fiscal policy should be prudent and conservative. That implies balanced budgets, and low taxes.

• Public debt should be used sparingly, if at all.

• Government should target Ken Henry’s 3Ps when making policy. Participation, Productivity and Population.

• Government should also consider Glenn Stevens advice – a good project last year is probably still a good project, whereas a bad project last year remains a bad project now. ‘Shovel ready’ is not now, nor has it ever been, an appropriate criteria for public spending.

• To the extent that the federal government wishes to pursue an activist fiscal policy it should target tax cuts. In particular, the federal government should consider payroll tax relief and a GST holiday.

Economics, Finance and Marketing 53RMIT University © 2013

What I said in February 2009

Objections to the Proposed Policy

• Spending multipliers are low.

– “The classic argument for fiscal stimulus presumes that the central cause of our current economic problems is this: We, the people and our government, are not doing nearly enough borrowing and spending on consumer goods. The government must step in force us all to borrow and spend more. This diagnosis is tragically comic once said aloud.” John Cochrane

– “It is easy to ‘Australianise’ this comment, ‘Australians have not been borrowing and spending enough on alcohol, pokies and tobacco and there are not nearly enough plasma televisions around. The government should borrow and spend more to ensure that more consumer spending occurs’. I invite Senators to read that statement out loud and wonder whether it sounds plausible or responsible.”

Economics, Finance and Marketing 54RMIT University © 2013

What I said in February 2009

• When stimuli do work

– Kevin M Murphy - Stimuli are likely to work when the economic value of the output from the stimulus is greater than the costs of the inputs and deadweight losses.

– The economic returns of federal investment in school halls etc. are likely to be low.

– This makes very little, if any, contribution to productivity, participation or population.

– This is primarily expenditure that should occur at the local level. This expenditure rewards State and Territory governments for past neglect of school infrastructure needs and re-enforces perverse incentives.

– It is possible that a properly designed scheme could see federal funding that augments local community and State funding, but this should not be primarily funded at federal level.

Economics, Finance and Marketing 55RMIT University © 2013

What I said in February 2009

– The economic returns of home insulation are likely to be low.

– Are there really under-utilised resources in the home insulation sector?

– Are the skills developed in this sector generic or specific? What will happen to workers after all homes have been insulated?

– How will this policy interact with the Climate Change Policy? – To the extent that this policy is useful and valuable, an open

question, it is better that it be considered as part of the Climate Change policy.

– The economic returns to a $950 hand-out based on having been a taxpayer in 2007-08 likely to be low.

– This is a retrospective tax refund that cannot lead people to change their behaviour – i.e. it has no incentive effects.

– Consequently, this money has no impact on productivity, participation or population.

Economics, Finance and Marketing 56RMIT University © 2013

What I said in February 2009

• While the economic benefits of the Fiscal Package are low, the costs are likely to be high.

– The project choices are rushed and more likely to be less efficient.

– The objective to spend more money faster is likely to lead to poor project choice.

– Public sector spending tends to be less efficient than private spending anyway.

• The Fiscal Stimulus is funded by public debt.

– Public debt is associated with intergenerational burdens.

– Public debt has a history of rising very rapidly to high levels.

– Public debt is associated with irresponsible fiscal behaviour.

– Public debt implies that future taxes will be higher than they otherwise would have been.

Economics, Finance and Marketing 57RMIT University © 2013

What I said in February 2009

• The government is not doing nothing! (sorry about the double negative).

– RBA, an operationally independent arm of government, has lowered rates by 4 per cent over six months.

– The ‘automatic stabilisers’ are operating to put money into the economy already.

• Spending versus saving is a false dichotomy.

• Keynesian strategies are less likely to work in small, open economies.

• Economists tend to over-estimate the benefits of fiscal policy.

Economics, Finance and Marketing 58RMIT University © 2013

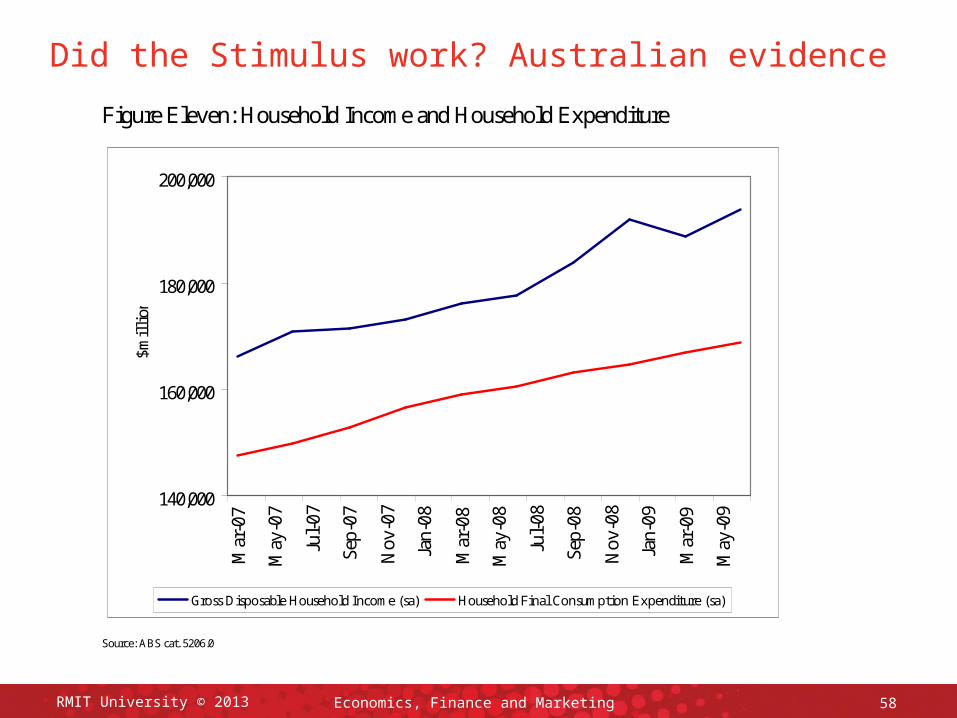

Did the Stimulus work? Australian evidence

Figure Eleven: Household Income and Household Expenditure

140,000

160,000

180,000

200,000

Mar

-07

May

-07

Jul-

07

Sep-

07

Nov

-07

Jan-

08

Mar

-08

May

-08

Jul-

08

Sep-

08

Nov

-08

Jan-

09

Mar

-09

May

-09

$mil

lion

Gross Disposable Household Income (sa) Household Final Consumption Expenditure (sa)

Source: ABS cat. 5206.0

Economics, Finance and Marketing 59RMIT University © 2013

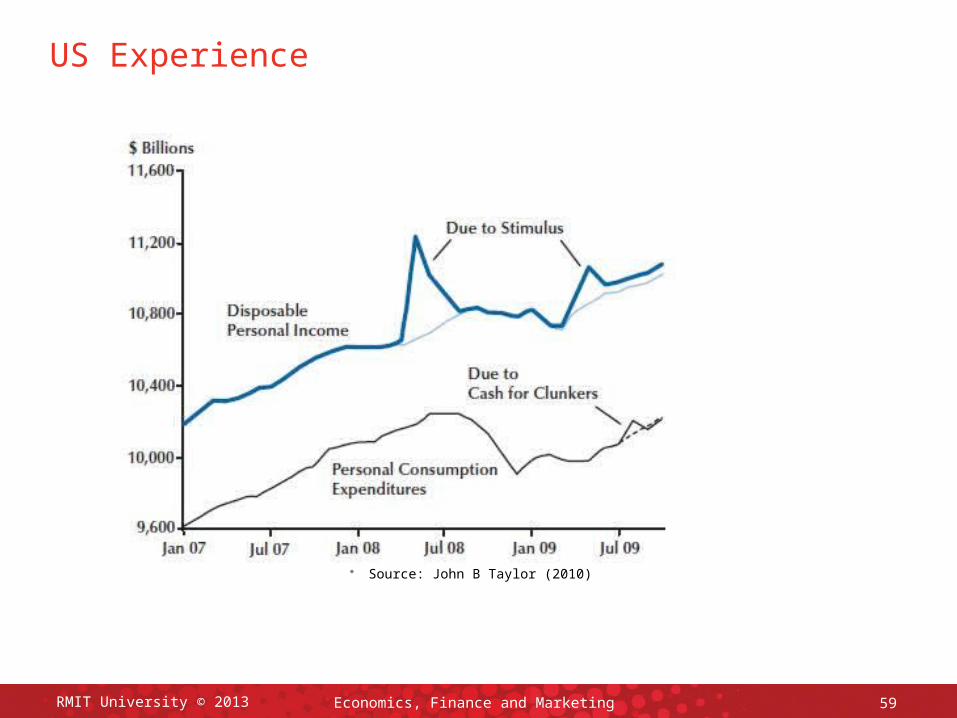

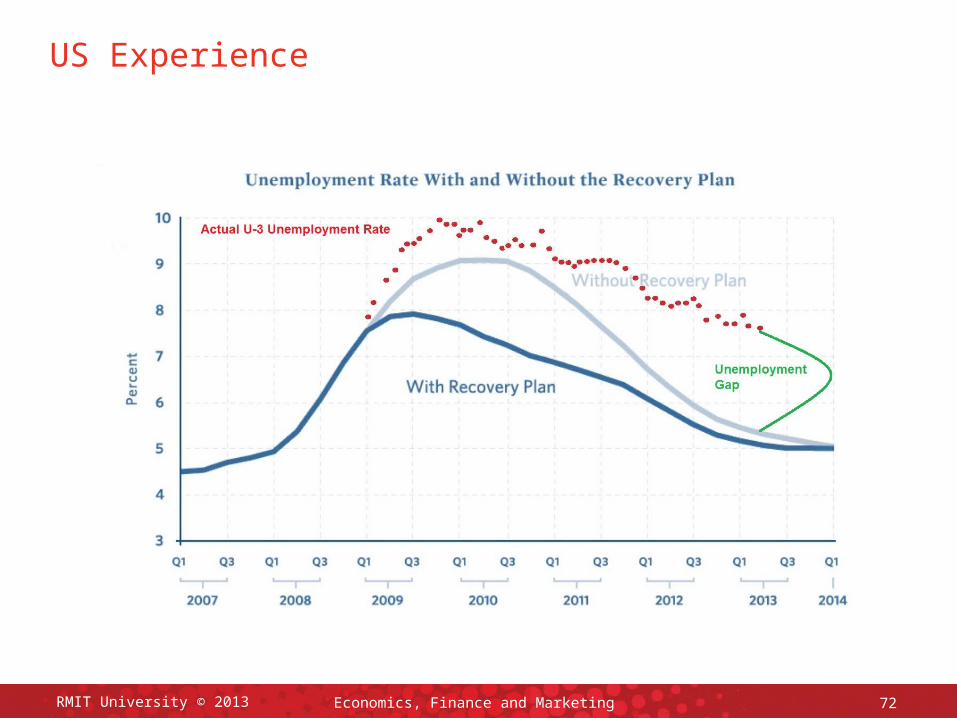

US Experience

• Source: John B Taylor (2010)

Economics, Finance and Marketing 60RMIT University © 2013

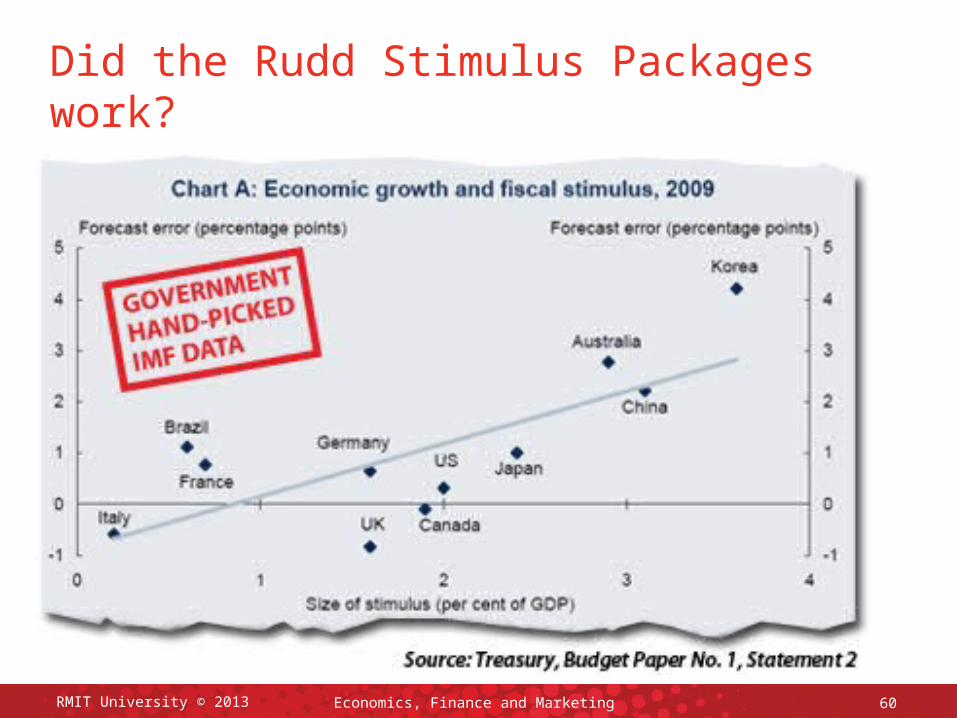

Did the Rudd Stimulus Packages work?

Economics, Finance and Marketing 61RMIT University © 2013

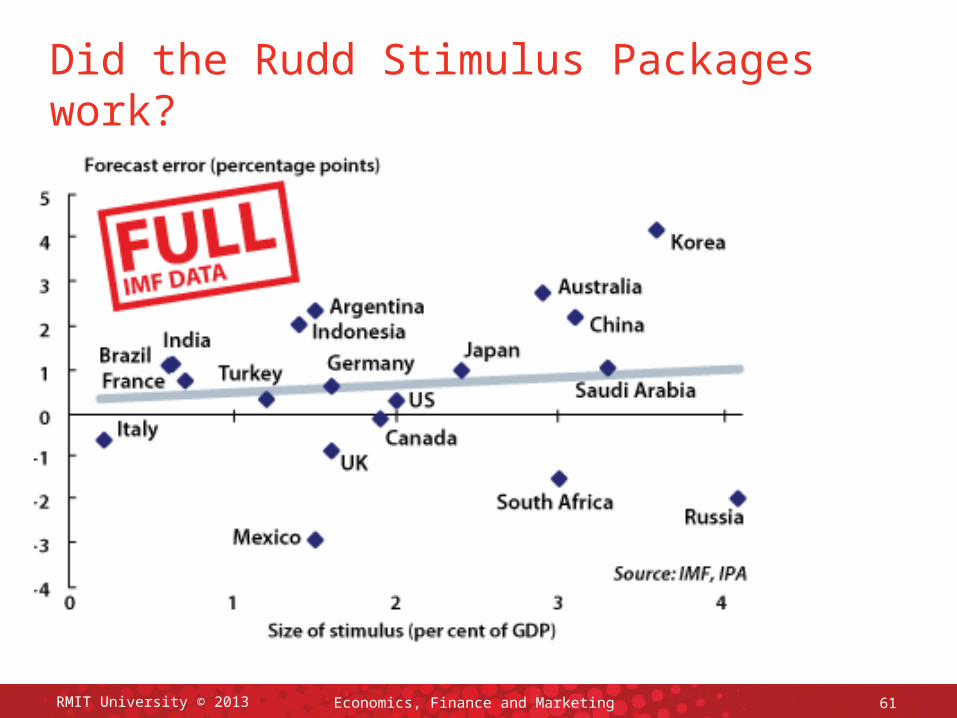

Did the Rudd Stimulus Packages work?

RMIT University © 2013 Economics, Finance and Marketing 62

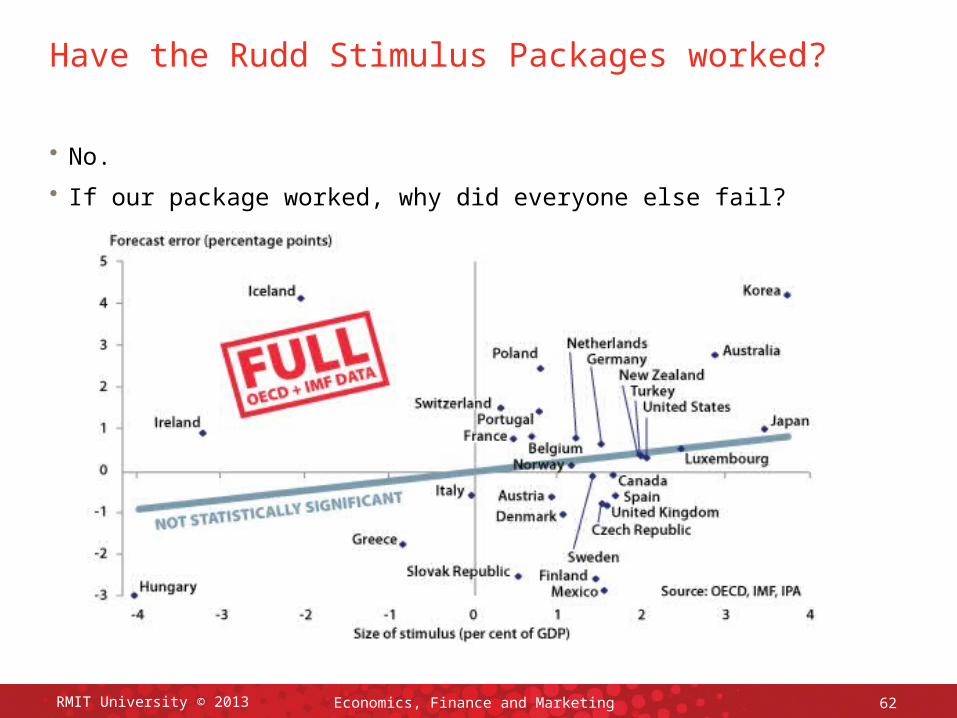

Have the Rudd Stimulus Packages worked?

• No.

• If our package worked, why did everyone else fail?

Economics, Finance and Marketing 63RMIT University © 2013

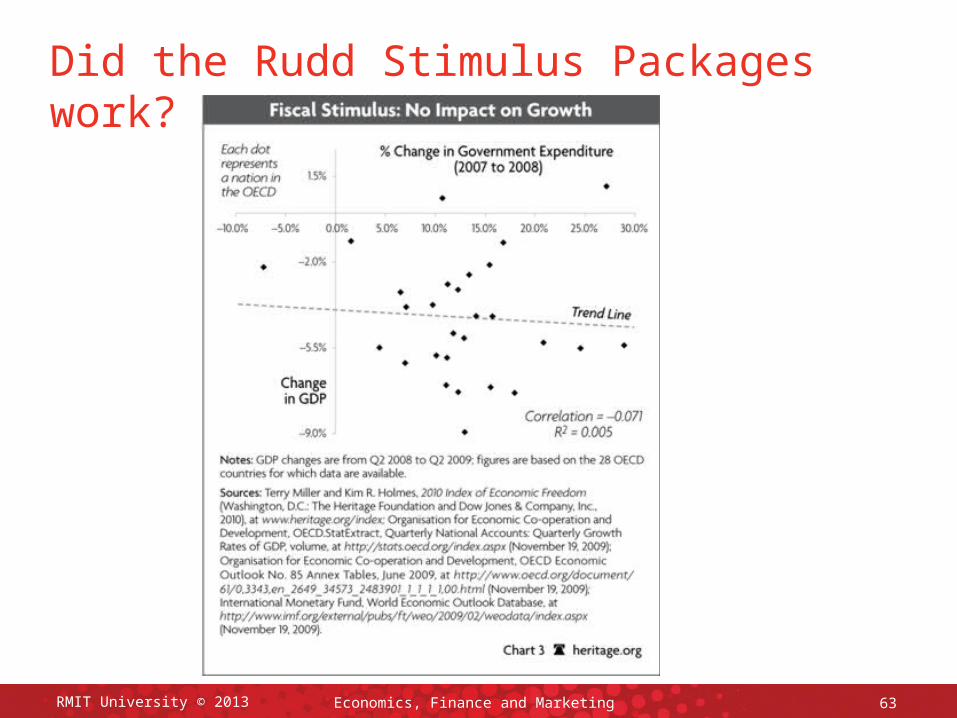

Did the Rudd Stimulus Packages work?

Economics, Finance and Marketing 64RMIT University © 2013

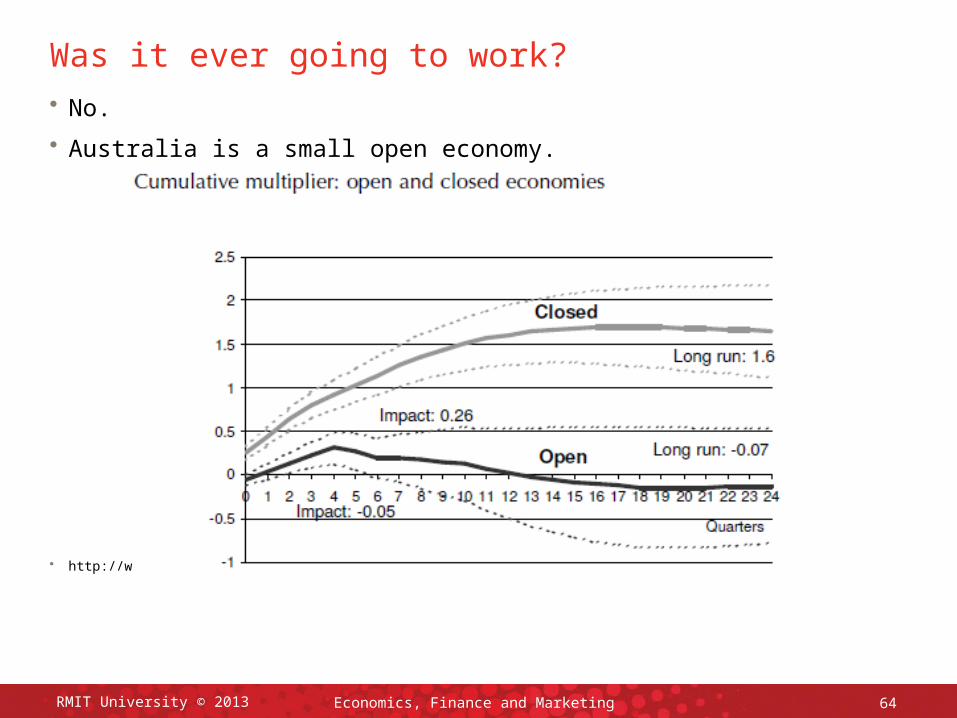

Was it ever going to work?• No.

• Australia is a small open economy.

• http://www.cepr.org/pubs/PolicyInsights/PolicyInsight39.pdf

Economics, Finance and Marketing 65RMIT University © 2013

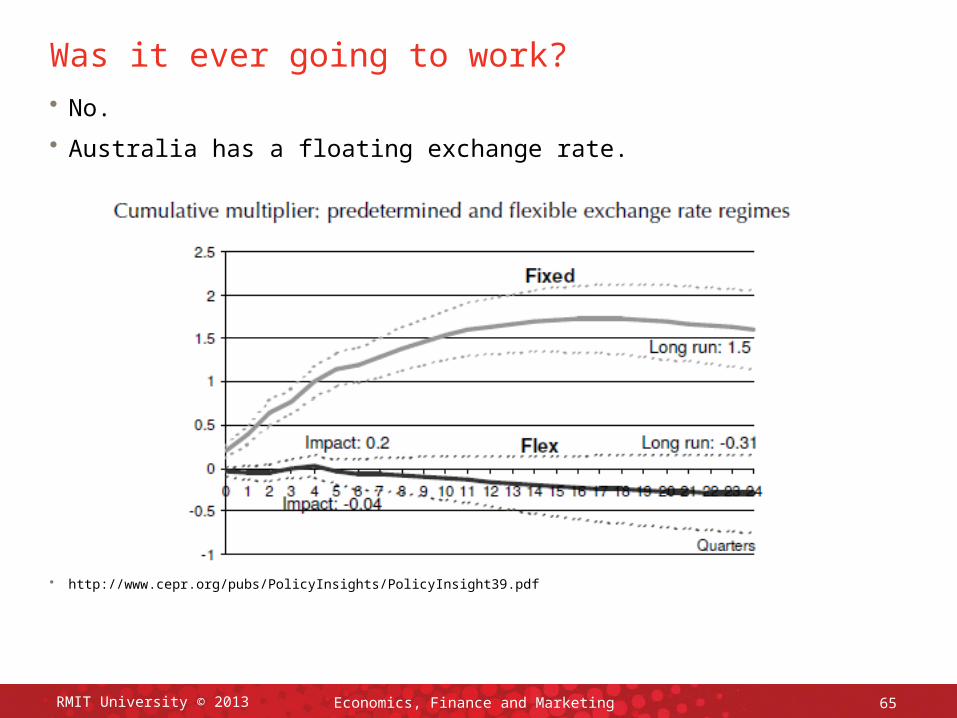

Was it ever going to work?• No.

• Australia has a floating exchange rate.

• http://www.cepr.org/pubs/PolicyInsights/PolicyInsight39.pdf

Economics, Finance and Marketing 66RMIT University © 2013

Waste of Money

• Source: The Cairns Post

Economics, Finance and Marketing 67RMIT University © 2013

Waste of Money

• Gary Banks ‘said that poorly conceived or executed infrastructure projects imposed a double burden on the economy, “with future generations having to service higher debts from incomes that are lower than they would otherwise be”.’ The Australian (November 6)

• ‘A plumber friend of mine has recently tendered for a number of jobs created via the government school hall scheme. Despite having quoted 3 times his normal price he has won 85 percent of the tenders. However, in each of these tenders he has not included the cost of plumbing required to get to the actual hall. So once his job is complete no water will be able to travel to or from the building unless they engage him to do more work. He believes this will add an additional cost of 100 %.’ email communication

Economics, Finance and Marketing 68RMIT University © 2013

Waste of Money

• ‘When the school guttering needed replacing, with about 60m of gutter, Mr Mayne obtained a quote from an independent builder for about $1800 including materials. The bill the school received from the department for the work is $11,000 plus materials. When Mr Mayne queried the disparity in costs, he was told he didn't understand that's the way the system works and it couldn't be changed.’ The Australian (June 16)

• ‘AN undercover playground with concrete floors and no doors costs $1.8 million under the Rudd Government's schools stimulus funding, the State Opposition says.

And it says that's just one example of how schools are being ripped off.

Other documents obtained by The Courier-Mail showed Mulgildie State School west of Bundaberg received $250,000 to build a basic 60sq m shed, after receiving a $29,000 quote from a local shed builder for a similar structure.’ Courier-Mail (June 16)

Economics, Finance and Marketing 69RMIT University © 2013

Waste of Money

• ‘EIGHT tiny schools have been handed $400,000 in taxpayer funds for new fencing, spruced-up classrooms and playground upgrades this year - even though the Queensland government has shortlisted them for closure’. The Australian (August 3)

• ‘The decision to rob high schools of science labs and language centres to help pay for the blowout in the cost of sheds in primary schools has left high school principals furious, and betrayed the Prime Minister's stated priorities of improving science and language education.

The only program in the $16billion Building the Education Revolution to have real educational merit was the smallest, the $1bn - reduced last week to $800million - to build sciences and language centres in high schools.

The remaining $15bn was handed to schools regardless of their existing facilities, their community's resources, or whether they even needed a hall or library.’ The Australian (September 2)

• ‘AN outback school with one student is among nine tiny schools handed $2.25 million in federal grants to build new halls, libraries and classrooms, even though they face closure.’ The Australian (September 3)

Economics, Finance and Marketing 70RMIT University © 2013

Loss of Life and Property Damage

• ‘THE electrocution of a second Queenslander has cast further doubt over the adequacy of training for workers fitting insulation under the Federal Government's controversial rebate scheme.

The 16-year-old youth was electrocuted in a home near Stanwell, southwest of Rockhampton, while installing batts.’ Courier Mail (November 18)

• ‘Mr Wilson was the third insulation installer to die as operators rush to cash in on the Federal Government's rebate scheme.’ Daily Telegraph (November 25)

• ‘DOZENS of NSW homes have been destroyed or damaged by fires which erupted when badly installed ceiling insulation came into contact with downlights.’ Daily Telegraph (September 21)

Economics, Finance and Marketing 71

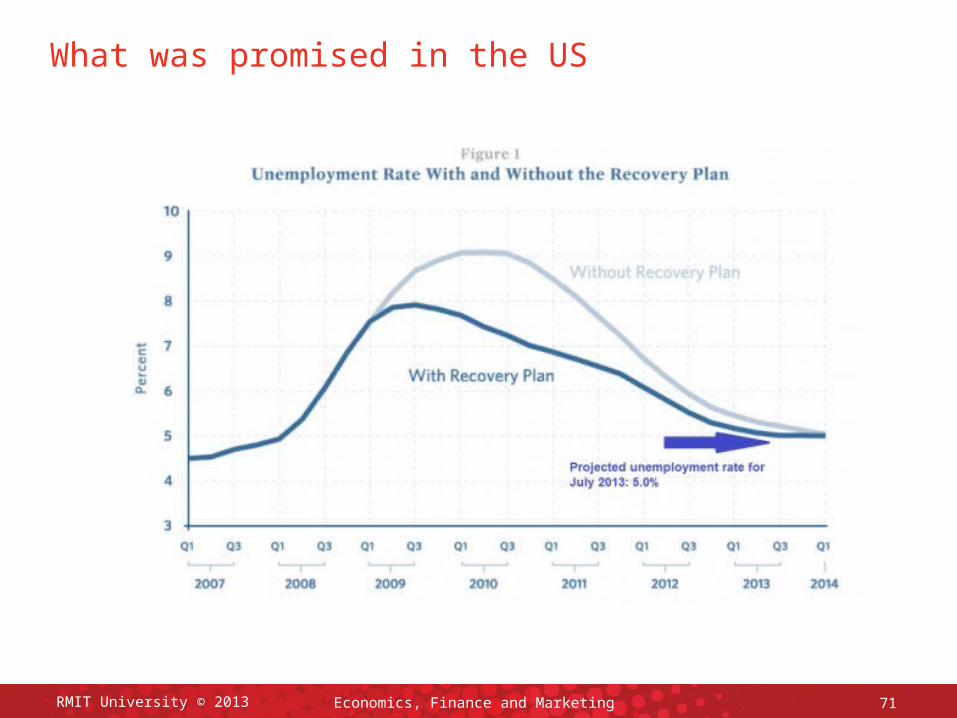

What was promised in the US

RMIT University © 2013

Economics, Finance and Marketing 72RMIT University © 2013

US Experience

RMIT University © 2013 Economics, Finance and Marketing 73

Saved or Spent?

• Treasury relied on a paper by Christian Broda and Jonathan Parker to argue that the stimulus would be spent, not saved.

– US$950 handout

– Consumption higher is households that had received the handout

– Did not test how much was spent

• David Johnson, Jonathan Parker, and Nicholas Souleles. 2006

– 2001 rebate: 2/3 spent over six months

• Sumit Agarwal, Chunlin Liu, and Nicholas Souleles, 2007

– 40 spent spent over six months

• Andrew Leigh – Survey data indicates that Australians spent the money twice as fast as US consumers spent 2001 tax rebate

• David Gruen – Treasury estimate – 2/3 spent in six months (T&U 208)

Economics, Finance and Marketing 74

Saved or Spent?

• Broda and Parker (2012) argue that households increased their spending by ten per cent in the week the cash handout arrived – while that sounds quite large, the US dollar amount was just $14 in that week.

• Over the next seven weeks US consumers in receipt of the cash handout spent an addition US$30 – US$50.

• Aisbett, Brueckner, Steinhauser, and Wilcox (2012)

– Australian replication of Broda and Parker.

– households' consumption of non-durables did not react significantly during or after the one-time, preannounced transfer.

– the average household, which received a payment of $900, spent in the week upon receipt of the payment an additional $1 on non-durables.

RMIT University © 2013

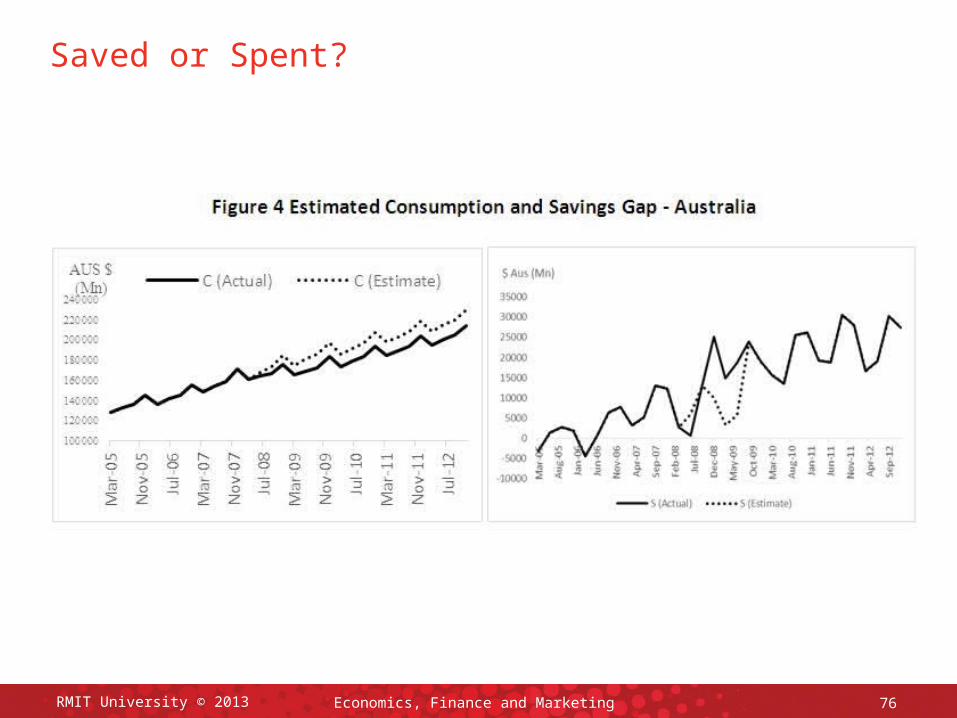

Economics, Finance and Marketing 75

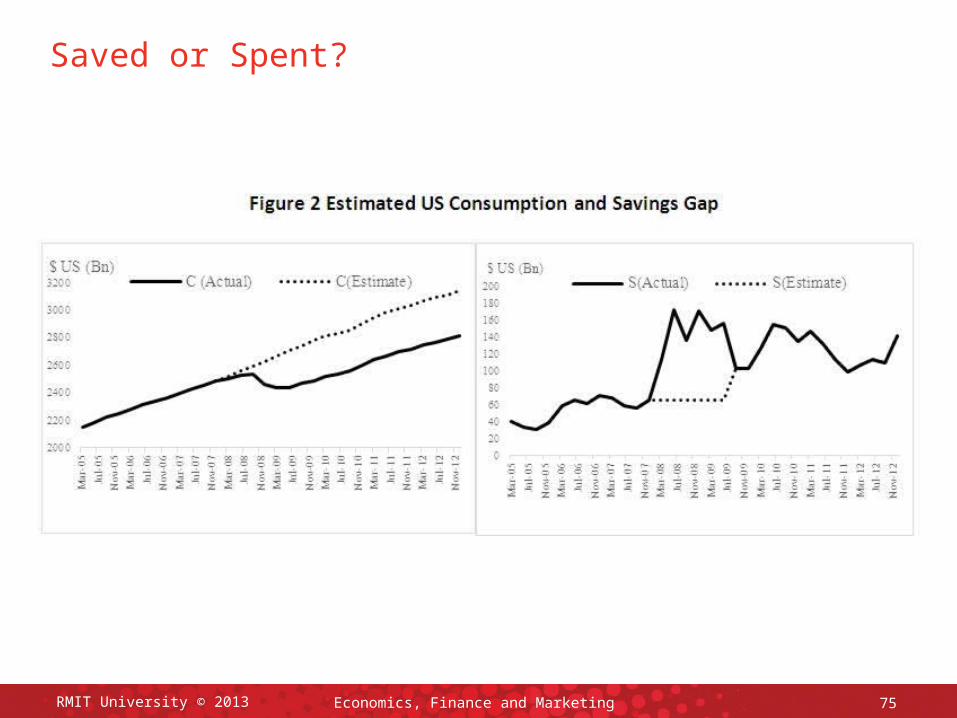

Saved or Spent?

RMIT University © 2013

Economics, Finance and Marketing 76

Saved or Spent?

RMIT University © 2013

RMIT University © 2013 Economics, Finance and Marketing 77

Thoughts on Ricardian Equivalence etc.

• Barro-Ricardo view: Deficits don’t matter because individuals save in order to pay future taxes.

– Large literature – does not hold perfectly.

– Does this mean that deficit spending can stimulate economy?

• Buchanan view: Deficits matter because Ricardian equivalence fails to hold.

– Some people do not save to offset government dissaving.

– Excess consumption occurs and crowds out private investment.

– Future generations inherit a small capital base.

– Deficits expropriate wealth from future generations.

• Just because Ricardian equivalence doesn’t hold doesn’t mean that stimulus can work.

RMIT University © 2013 Economics, Finance and Marketing 78

Was it worth it?But it is hard to resist the conclusion that the government spent more than was needed, no matter how reasonable its actions appeared at the time. The stimulus spending was designed for an economy that was expected to be shrinking at a rate of 1 per cent, not one that was growing at a pretty normal rate of 2.7 percent, which is what happened in 2009.

The government and Treasury had expected collapsing businesses to drag the economy into a long recession, but instead the shock caused by the collapse in world trade and the panic in financial markets passed after a few month, leaving the corporate sector largely intact. The government was left completing large stimulus projects that were no longer really needed.

…

It is the opportunity cost – the things that cannot be accomplished by either this government or the next – that weighs heaviest as a result of the government’s spending more than was needed. Had the economy behaved anything like Treasury’s forecasts for it, no-one would have begrudged the money spent. But now $75 billion has gone, with a negligible addition to Australia’s productive capacity. The debt must be serviced and in due course paid back. In the context of a $1 trillion economy, it is not a crippling burden, but there is depressingly little to show for it.

Taylor and Uren (2010)

Economics, Finance and Marketing 79RMIT University © 2013

Conclusions

• Vulgar Keynesianism failed. Again.

– This theory has been tried again and again and always fails.

• Government spending needs to be restrained.

• Economists have known this for a long time.

• Adam Smith

– Great nations are never impoverished by private, though they sometimes are by publick prodigality and misconduct.

– It is the highest impertinence and presumption, therefore, in kings and ministers, to pretend to watch over the œconomy of private people…. They are themselves always, and without any exception, the greatest spendthrifts in the society. Let them look well after their own expence, and they may safely trust private people with theirs. If their own extravagance does not ruin the state, that of their subjects never will.