Embed Size (px)

Citation preview

StevenShreve: StochasticCalculusandFinance

PRASAD CHALASANI

CarnegieMellon [email protected]

SOMESH JHA

CarnegieMellon [email protected]

THIS IS A DRAFT: PLEASEDO NOT DISTRIBUTEc

Copyright;StevenE. Shreve,1996

October6, 1997

Contents

1 Intr oduction to Probability Theory 11

1.1 TheBinomialAssetPricingModel . . . . . . . . . . . . . . . . . . . . . . . . . . 11

1.2 FiniteProbabilitySpaces. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

1.3 LebesgueMeasureandtheLebesgueIntegral . . . . . . . . . . . . . . . . . . . . 22

1.4 GeneralProbabilitySpaces. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

1.5 Independence. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

1.5.1 Independenceof sets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

1.5.2 Independenceof -algebras . . . . . . . . . . . . . . . . . . . . . . . . . 41

1.5.3 Independenceof randomvariables. . . . . . . . . . . . . . . . . . . . . . 42

1.5.4 Correlationandindependence. . . . . . . . . . . . . . . . . . . . . . . . 44

1.5.5 Independenceandconditionalexpectation. . . . . . . . . . . . . . . . . . 45

1.5.6 Law of LargeNumbers. . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

1.5.7 CentralLimit Theorem. . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

2 Conditional Expectation 49

2.1 A BinomialModel for StockPriceDynamics . . . . . . . . . . . . . . . . . . . . 49

2.2 Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

2.3 ConditionalExpectation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

2.3.1 An example . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

2.3.2 Definitionof ConditionalExpectation . . . . . . . . . . . . . . . . . . . . 53

2.3.3 Furtherdiscussionof Partial Averaging . . . . . . . . . . . . . . . . . . . 54

2.3.4 Propertiesof ConditionalExpectation . . . . . . . . . . . . . . . . . . . . 55

2.3.5 Examplesfrom theBinomialModel . . . . . . . . . . . . . . . . . . . . . 57

2.4 Martingales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

1

2

3 Arbitrage Pricing 59

3.1 BinomialPricing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

3.2 Generalone-stepAPT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

3.3 Risk-NeutralProbabilityMeasure . . . . . . . . . . . . . . . . . . . . . . . . . . 61

3.3.1 PortfolioProcess. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

3.3.2 Self-financingValueof a PortfolioProcess . . . . . . . . . . . . . . . . 62

3.4 SimpleEuropeanDerivativeSecurities. . . . . . . . . . . . . . . . . . . . . . . . 63

3.5 TheBinomialModel is Complete. . . . . . . . . . . . . . . . . . . . . . . . . . . 64

4 The Mark ov Property 67

4.1 BinomialModelPricingandHedging . . . . . . . . . . . . . . . . . . . . . . . . 67

4.2 ComputationalIssues. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

4.3 Markov Processes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

4.3.1 Differentwaysto write theMarkov property . . . . . . . . . . . . . . . . 70

4.4 Showing thata processis Markov . . . . . . . . . . . . . . . . . . . . . . . . . . 73

4.5 Applicationto ExoticOptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74

5 StoppingTimesand American Options 77

5.1 AmericanPricing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

5.2 Valueof PortfolioHedginganAmericanOption . . . . . . . . . . . . . . . . . . . 79

5.3 Informationup to aStoppingTime . . . . . . . . . . . . . . . . . . . . . . . . . . 81

6 Propertiesof American Derivative Securities 85

6.1 Theproperties. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

6.2 Proofsof theProperties. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

6.3 CompoundEuropeanDerivativeSecurities. . . . . . . . . . . . . . . . . . . . . . 88

6.4 OptimalExerciseof AmericanDerivativeSecurity. . . . . . . . . . . . . . . . . . 89

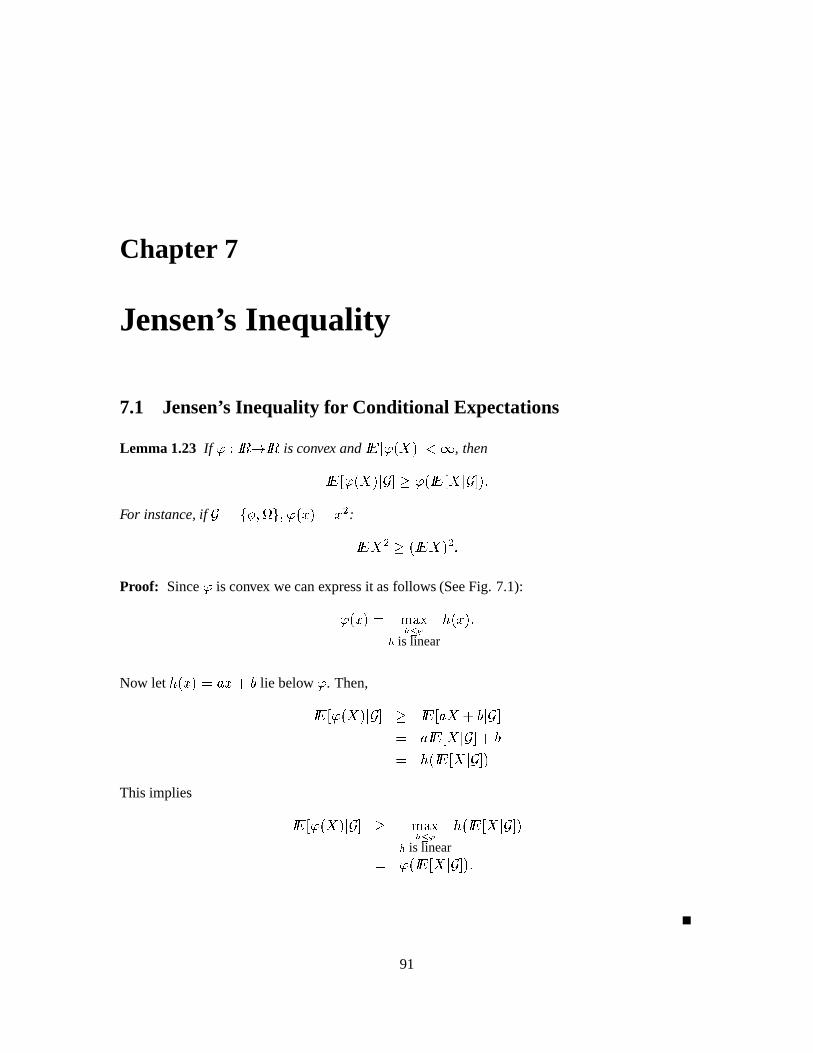

7 Jensen’s Inequality 91

7.1 Jensen’s Inequalityfor ConditionalExpectations. . . . . . . . . . . . . . . . . . . 91

7.2 OptimalExerciseof anAmericanCall . . . . . . . . . . . . . . . . . . . . . . . . 92

7.3 StoppedMartingales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94

8 RandomWalks 97

8.1 FirstPassageTime . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97

3

8.2 is almostsurelyfinite . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97

8.3 Themomentgeneratingfunctionfor . . . . . . . . . . . . . . . . . . . . . . . . 99

8.4 Expectationof . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100

8.5 TheStrongMarkov Property . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

8.6 GeneralFirstPassageTimes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

8.7 Example:PerpetualAmericanPut . . . . . . . . . . . . . . . . . . . . . . . . . . 102

8.8 DifferenceEquation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106

8.9 Distributionof FirstPassageTimes . . . . . . . . . . . . . . . . . . . . . . . . . . 107

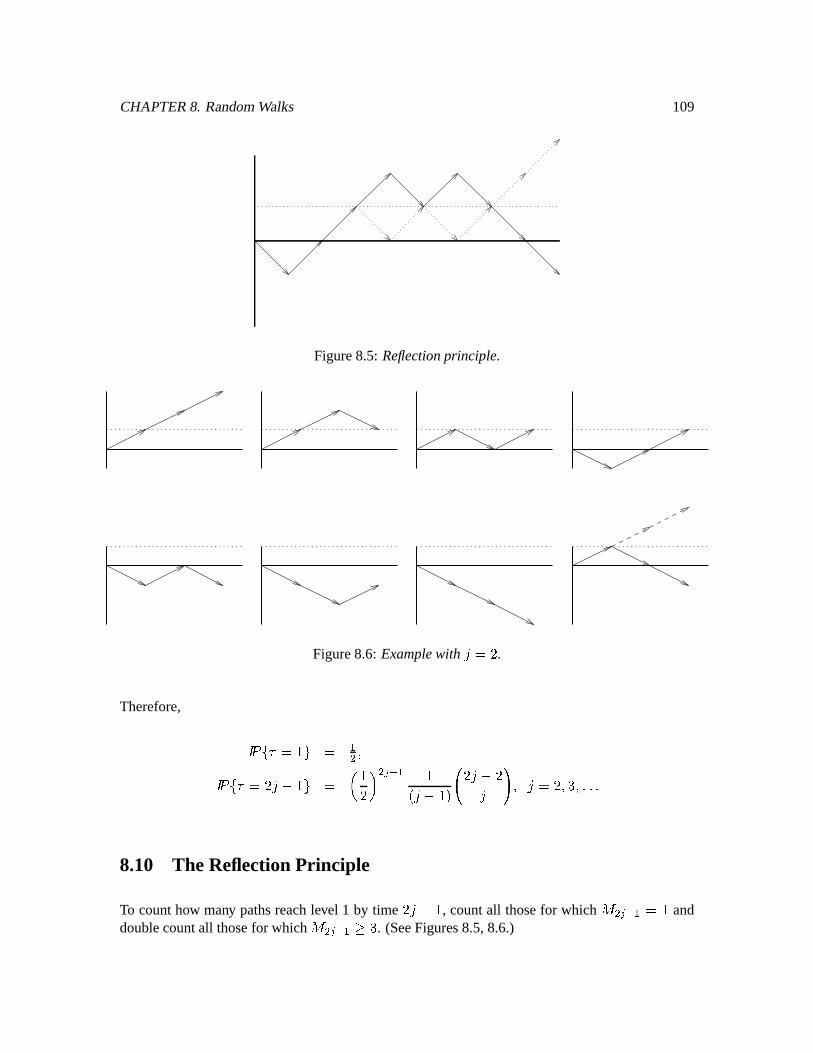

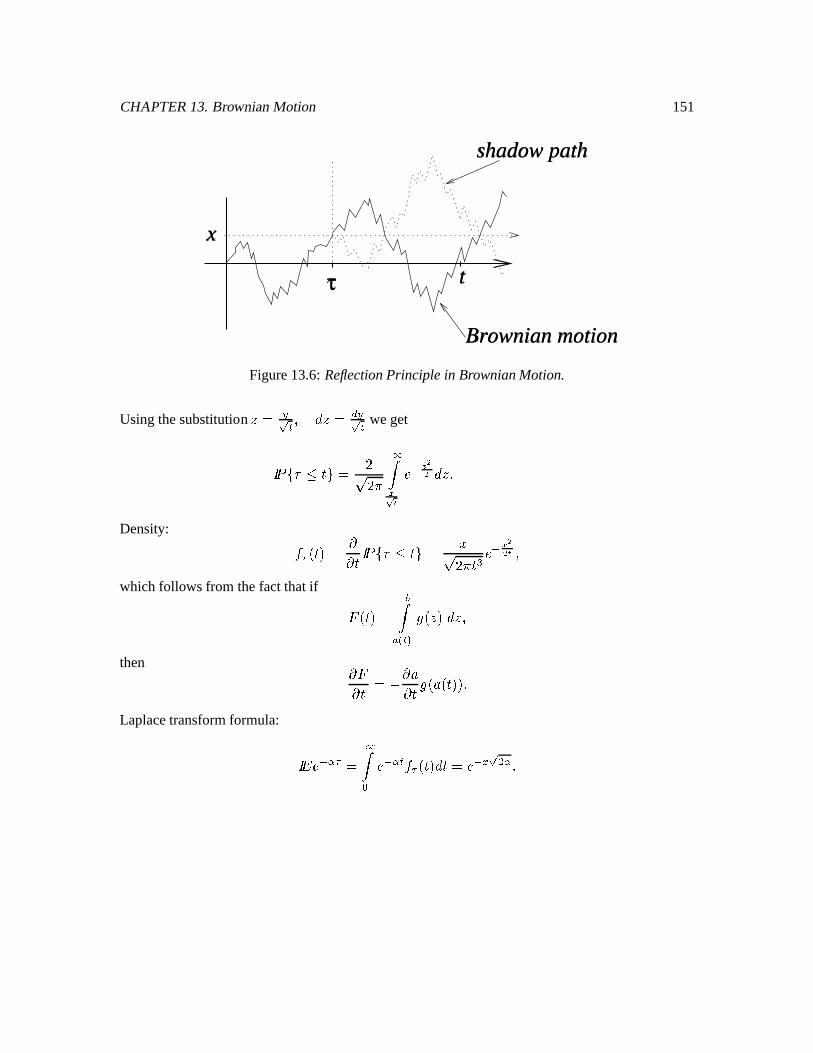

8.10 TheReflectionPrinciple . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 109

9 Pricing in terms of Market Probabilities: The Radon-Nikodym Theorem. 111

9.1 Radon-NikodymTheorem . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111

9.2 Radon-NikodymMartingales. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112

9.3 TheStatePriceDensityProcess . . . . . . . . . . . . . . . . . . . . . . . . . . . 113

9.4 StochasticVolatility BinomialModel . . . . . . . . . . . . . . . . . . . . . . . . . 116

9.5 AnotherApplicatonof theRadon-NikodymTheorem . . . . . . . . . . . . . . . . 118

10 Capital AssetPricing 119

10.1 An OptimizationProblem. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 119

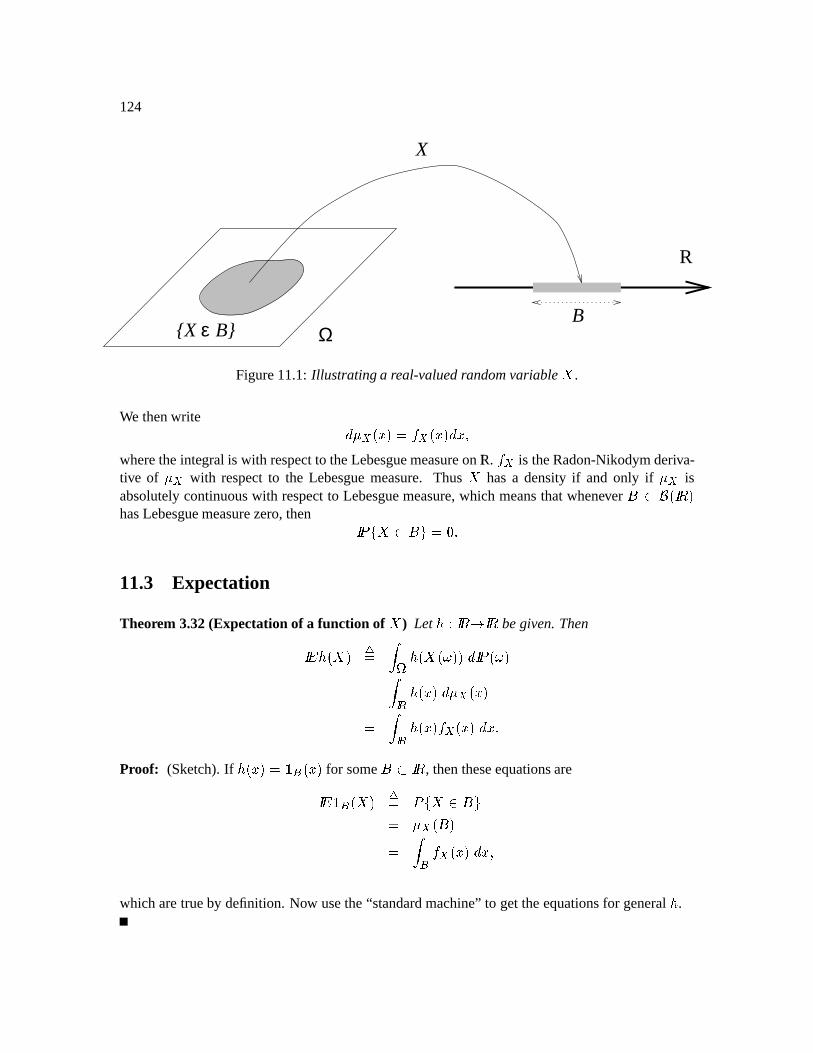

11 GeneralRandomVariables 123

11.1 Law of a RandomVariable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 123

11.2 Densityof aRandomVariable . . . . . . . . . . . . . . . . . . . . . . . . . . . . 123

11.3 Expectation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 124

11.4 Two randomvariables. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125

11.5 Marginal Density . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 126

11.6 ConditionalExpectation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 126

11.7 ConditionalDensity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 127

11.8 MultivariateNormalDistribution . . . . . . . . . . . . . . . . . . . . . . . . . . . 129

11.9 Bivariatenormaldistribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 130

11.10MGF of jointly normalrandomvariables. . . . . . . . . . . . . . . . . . . . . . . 130

12 Semi-ContinuousModels 131

12.1 Discrete-timeBrownianMotion . . . . . . . . . . . . . . . . . . . . . . . . . . . 131

4

12.2 TheStockPriceProcess. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132

12.3 Remainderof theMarket . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 133

12.4 Risk-NeutralMeasure. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 133

12.5 Risk-NeutralPricing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 134

12.6 Arbitrage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 134

12.7 StalkingtheRisk-NeutralMeasure. . . . . . . . . . . . . . . . . . . . . . . . . . 135

12.8 Pricinga EuropeanCall . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138

13 Brownian Motion 139

13.1 SymmetricRandomWalk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 139

13.2 TheLaw of LargeNumbers. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 139

13.3 CentralLimit Theorem . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 140

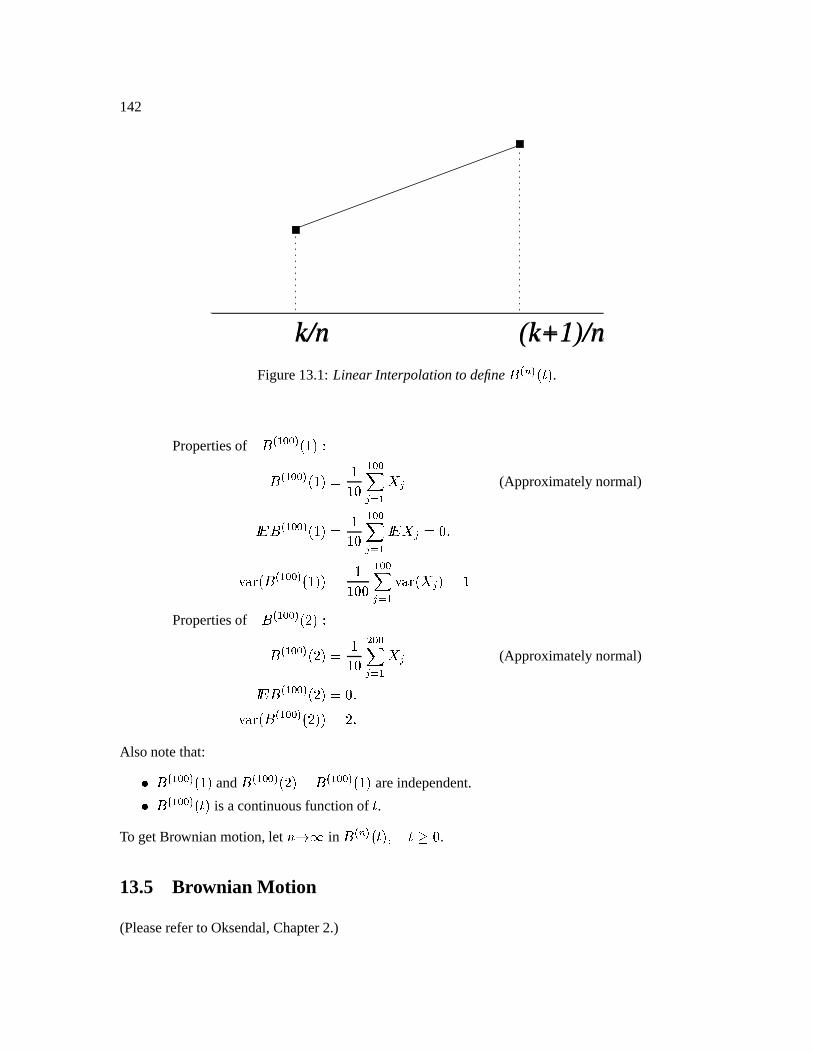

13.4 BrownianMotion asaLimit of RandomWalks . . . . . . . . . . . . . . . . . . . 141

13.5 BrownianMotion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142

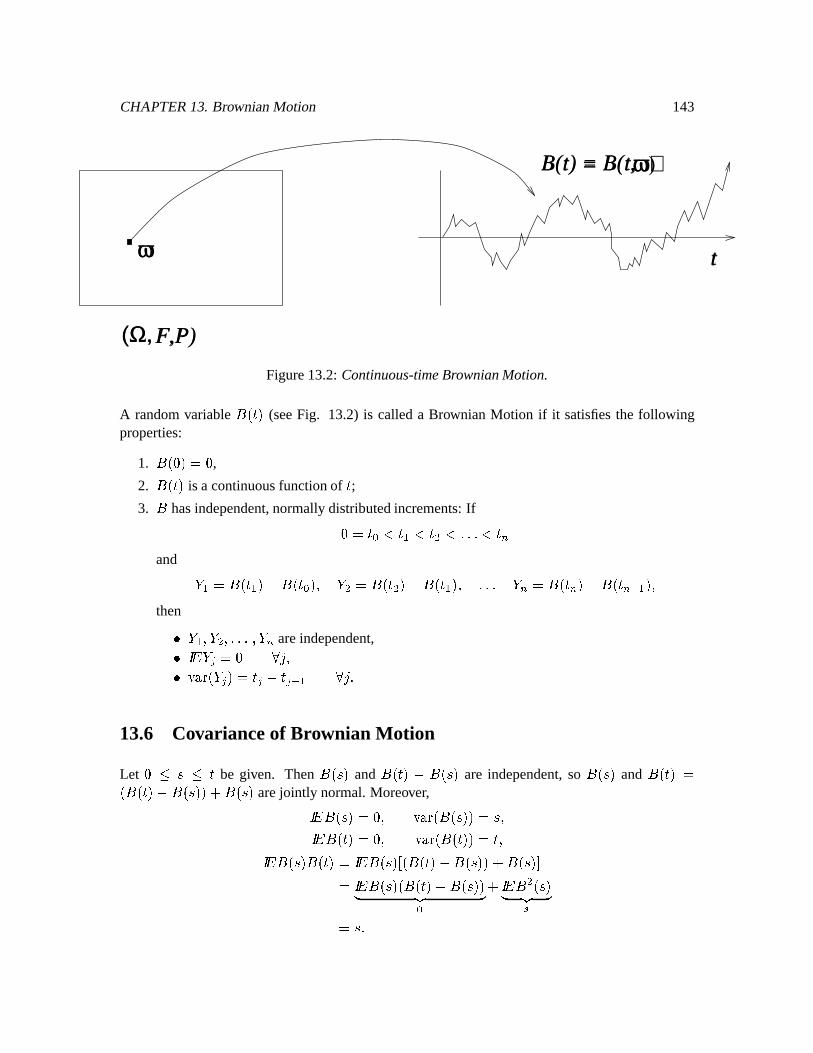

13.6 Covarianceof BrownianMotion . . . . . . . . . . . . . . . . . . . . . . . . . . . 143

13.7 Finite-DimensionalDistributionsof BrownianMotion . . . . . . . . . . . . . . . . 144

13.8 Filtrationgeneratedby a BrownianMotion . . . . . . . . . . . . . . . . . . . . . . 144

13.9 MartingaleProperty. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 145

13.10TheLimit of a BinomialModel . . . . . . . . . . . . . . . . . . . . . . . . . . . . 145

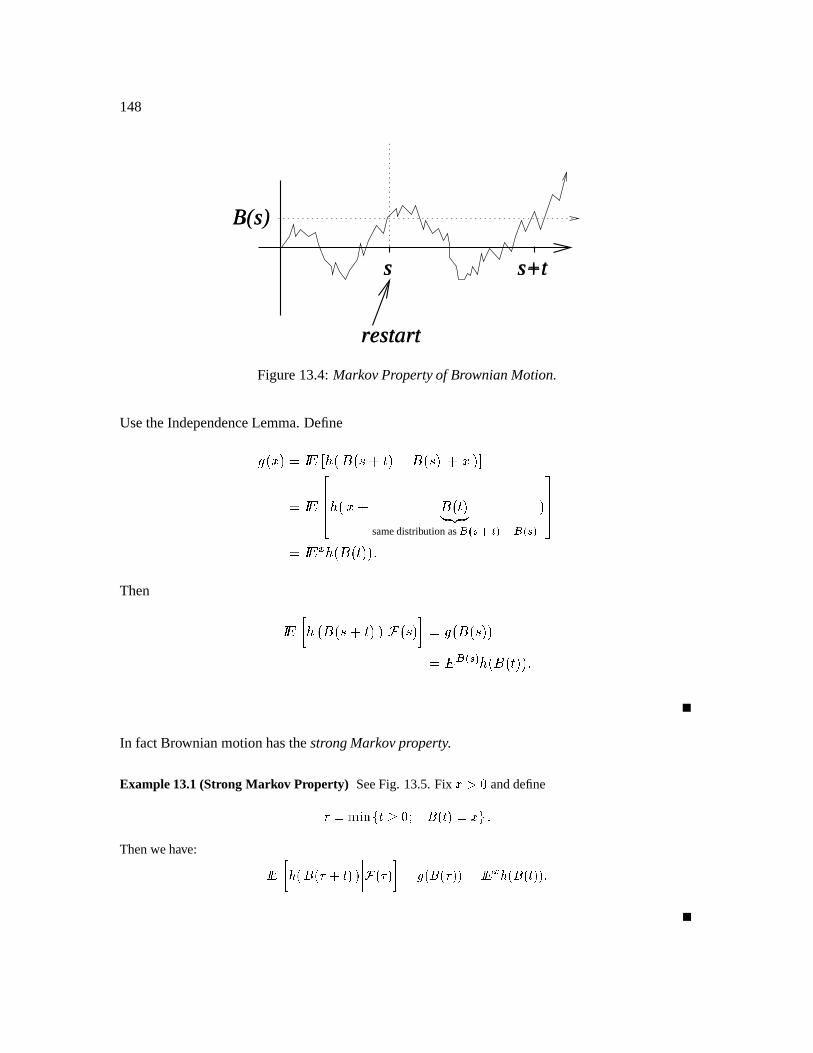

13.11StartingatPointsOtherThan0 . . . . . . . . . . . . . . . . . . . . . . . . . . . . 147

13.12Markov Propertyfor BrownianMotion . . . . . . . . . . . . . . . . . . . . . . . . 147

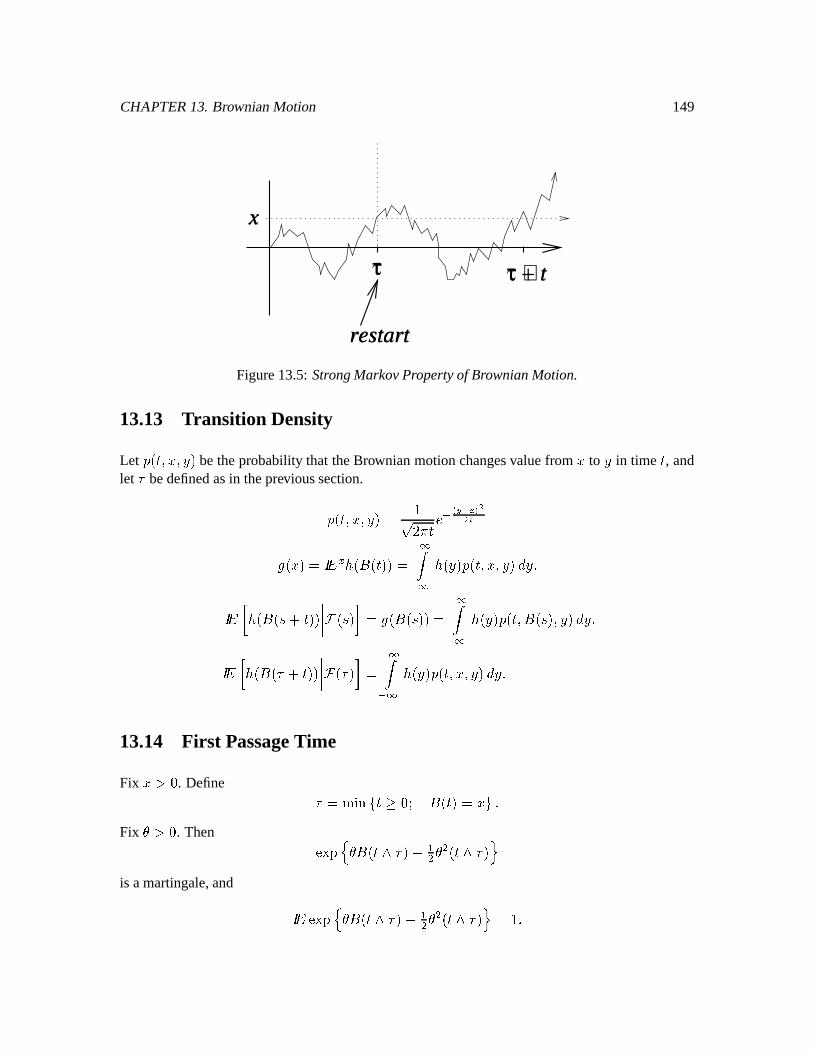

13.13TransitionDensity. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 149

13.14FirstPassageTime . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 149

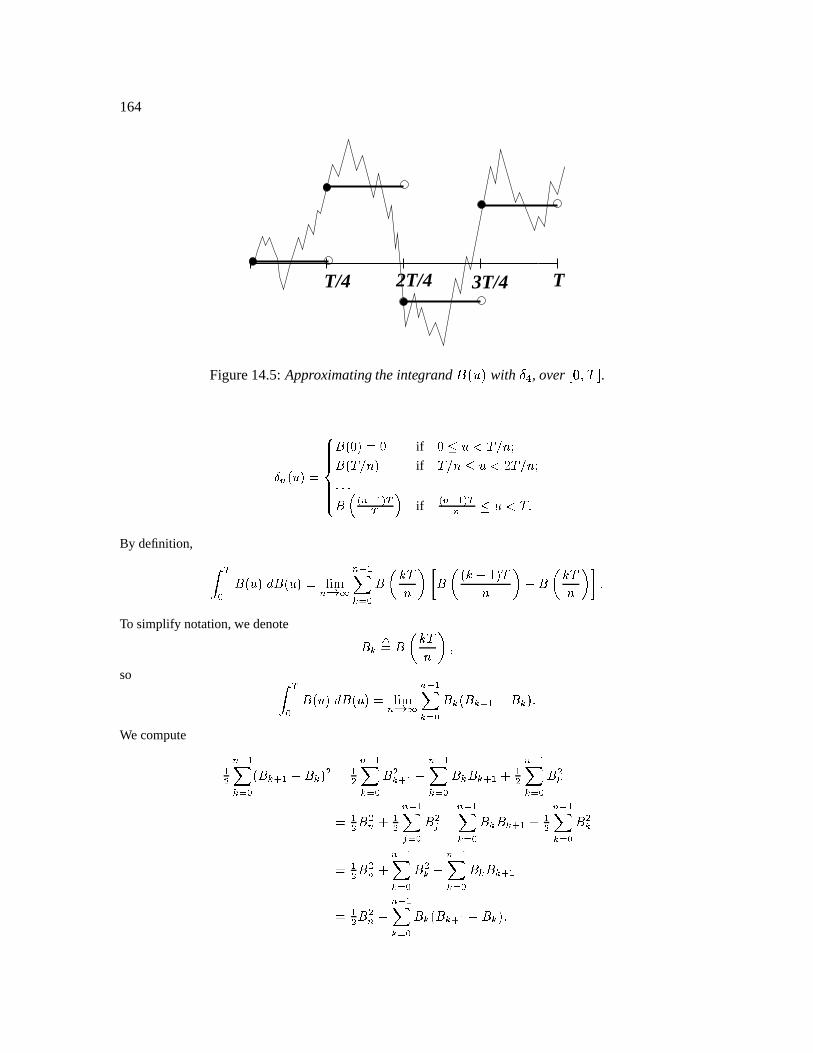

14 The It o Integral 153

14.1 BrownianMotion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153

14.2 FirstVariation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153

14.3 QuadraticVariation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 155

14.4 QuadraticVariationasAbsoluteVolatility . . . . . . . . . . . . . . . . . . . . . . 157

14.5 Constructionof theIto Integral . . . . . . . . . . . . . . . . . . . . . . . . . . . . 158

14.6 Ito integralof anelementaryintegrand . . . . . . . . . . . . . . . . . . . . . . . . 158

14.7 Propertiesof theIto integralof anelementaryprocess. . . . . . . . . . . . . . . . 159

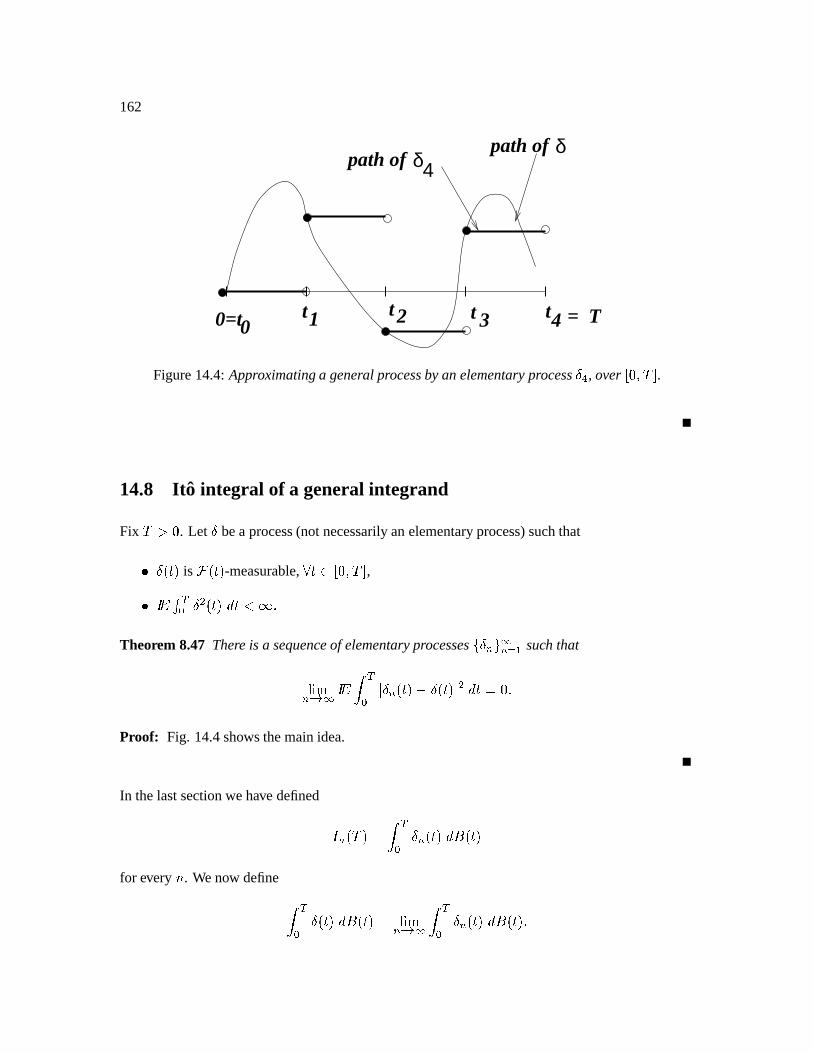

14.8 Ito integralof a generalintegrand. . . . . . . . . . . . . . . . . . . . . . . . . . . 162

5

14.9 Propertiesof the(general)Ito integral . . . . . . . . . . . . . . . . . . . . . . . . 163

14.10Quadraticvariationof anIto integral . . . . . . . . . . . . . . . . . . . . . . . . . 165

15 It o’sFormula 167

15.1 Ito’s formulafor oneBrownianmotion . . . . . . . . . . . . . . . . . . . . . . . . 167

15.2 Derivationof Ito’s formula . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 168

15.3 GeometricBrownianmotion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 169

15.4 Quadraticvariationof geometricBrownianmotion . . . . . . . . . . . . . . . . . 170

15.5 Volatility of GeometricBrownianmotion . . . . . . . . . . . . . . . . . . . . . . 170

15.6 Firstderivationof theBlack-Scholesformula . . . . . . . . . . . . . . . . . . . . 170

15.7 Meanandvarianceof theCox-Ingersoll-Rossprocess. . . . . . . . . . . . . . . . 172

15.8 MultidimensionalBrownianMotion . . . . . . . . . . . . . . . . . . . . . . . . . 173

15.9 Cross-variationsof Brownianmotions . . . . . . . . . . . . . . . . . . . . . . . . 174

15.10Multi-dimensionalIto formula . . . . . . . . . . . . . . . . . . . . . . . . . . . . 175

16 Mark ov processesand the Kolmogorov equations 177

16.1 StochasticDif ferentialEquations. . . . . . . . . . . . . . . . . . . . . . . . . . . 177

16.2 Markov Property . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 178

16.3 Transitiondensity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 179

16.4 TheKolmogorov BackwardEquation . . . . . . . . . . . . . . . . . . . . . . . . 180

16.5 ConnectionbetweenstochasticcalculusandKBE . . . . . . . . . . . . . . . . . . 181

16.6 Black-Scholes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 183

16.7 Black-Scholeswith price-dependentvolatility . . . . . . . . . . . . . . . . . . . . 186

17 Girsanov’s theorem and the risk-neutral measure 189

17.1 Conditionalexpectationsunder . . . . . . . . . . . . . . . . . . . . . . . . . . 191

17.2 Risk-neutralmeasure. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 193

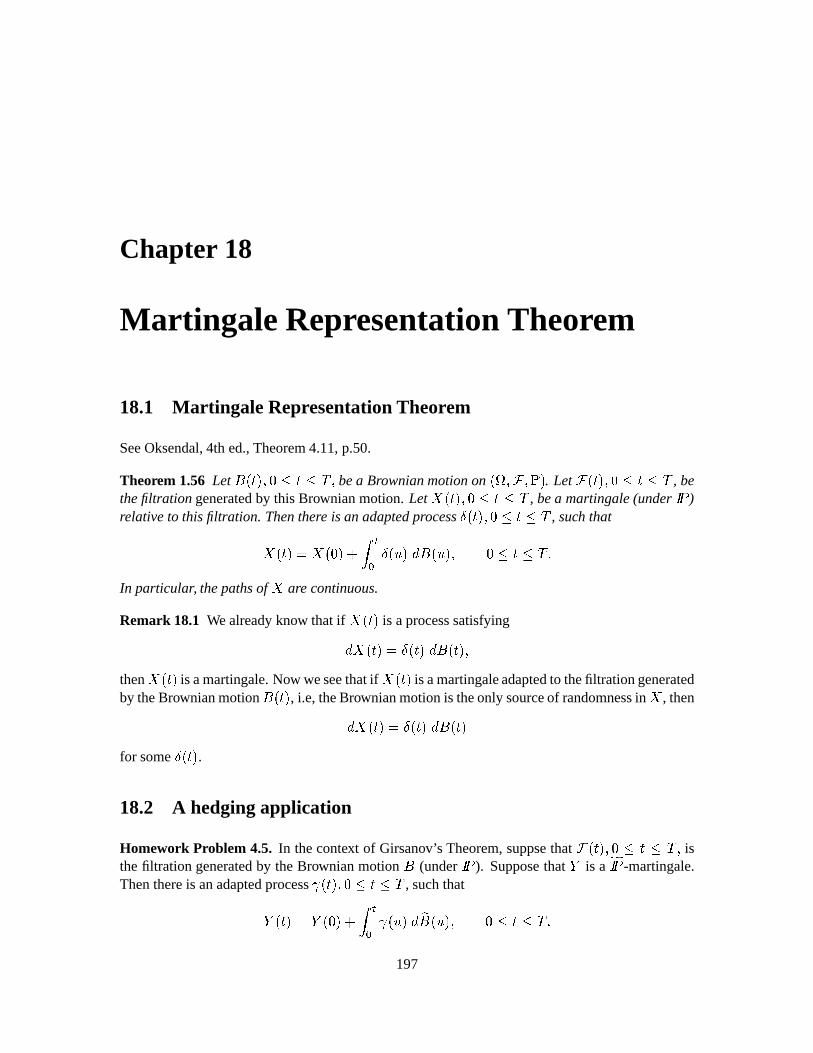

18 Martingale RepresentationTheorem 197

18.1 MartingaleRepresentationTheorem . . . . . . . . . . . . . . . . . . . . . . . . . 197

18.2 A hedgingapplication. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 197

18.3 -dimensionalGirsanov Theorem . . . . . . . . . . . . . . . . . . . . . . . . . . 199

18.4 -dimensionalMartingaleRepresentationTheorem . . . . . . . . . . . . . . . . . 200

18.5 Multi-dimensionalmarketmodel . . . . . . . . . . . . . . . . . . . . . . . . . . . 200

6

19 A two-dimensionalmarket model 203

19.1 Hedgingwhen . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 204

19.2 Hedgingwhen . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 205

20 Pricing Exotic Options 209

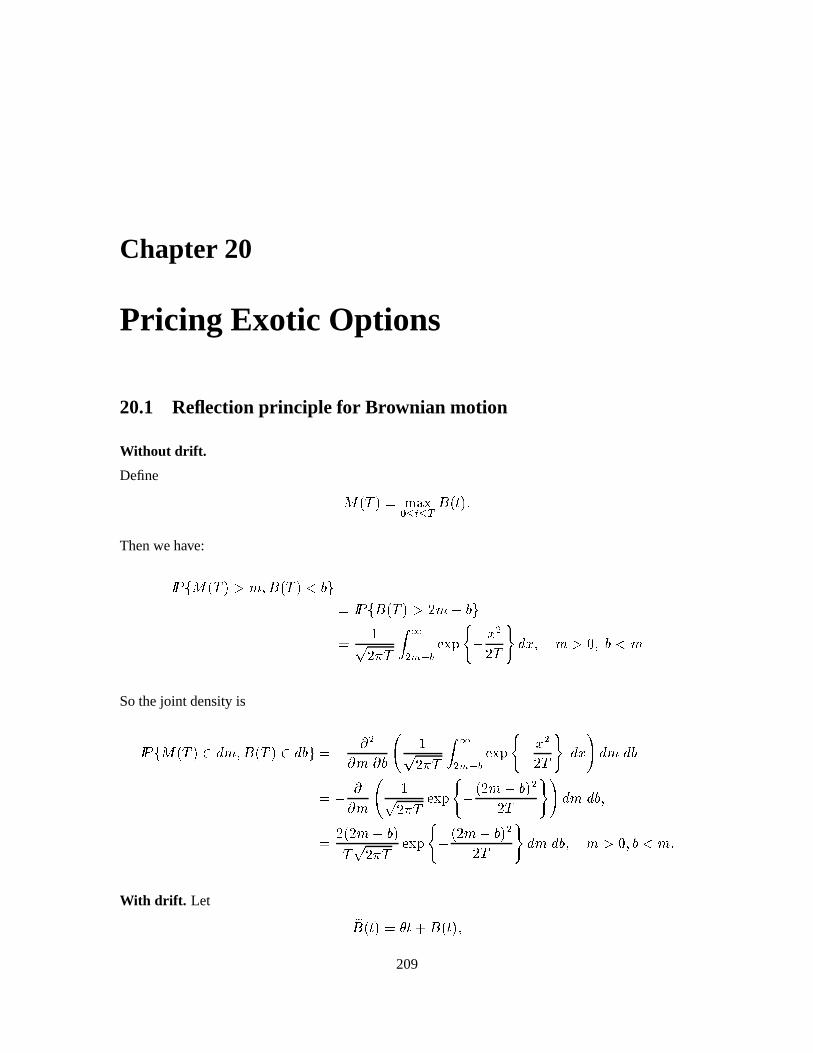

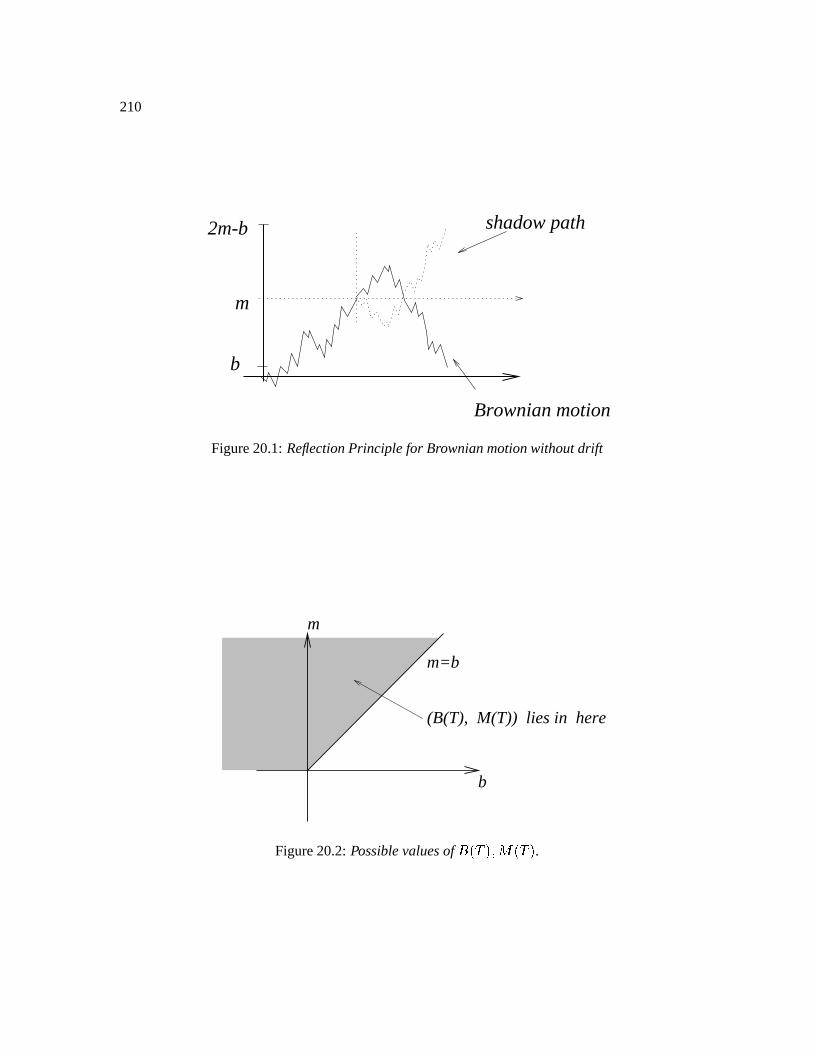

20.1 Reflectionprinciplefor Brownianmotion . . . . . . . . . . . . . . . . . . . . . . 209

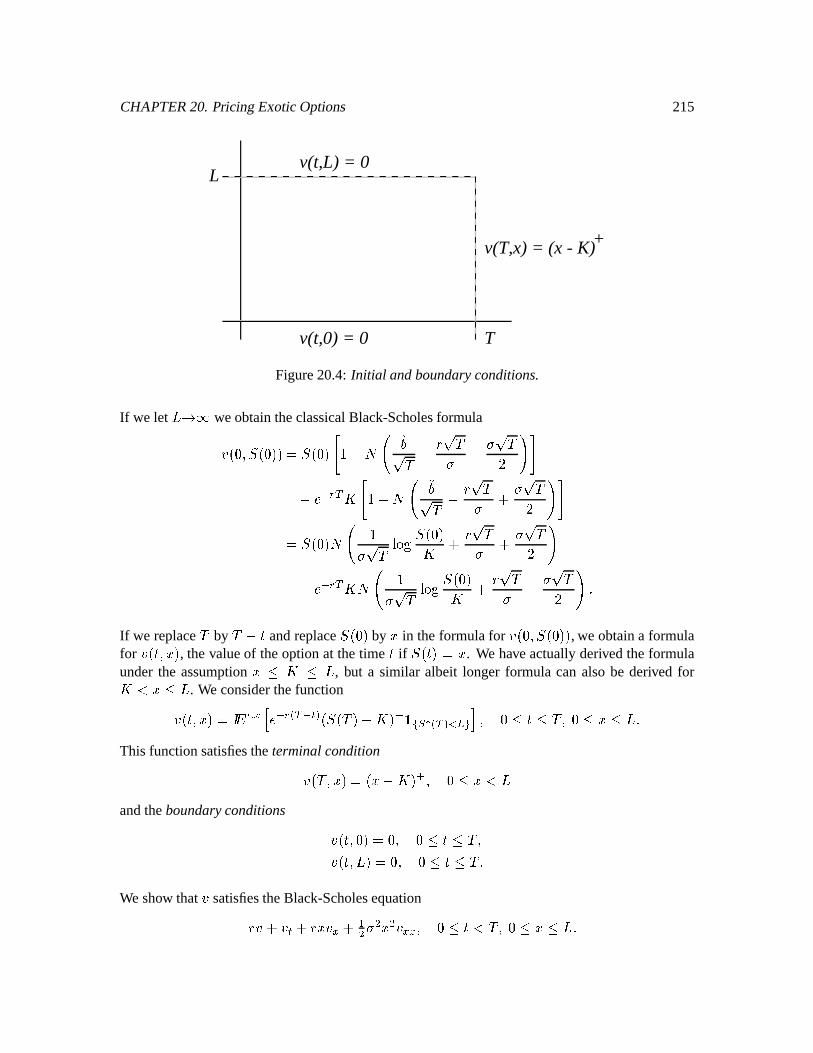

20.2 Up andoutEuropeancall. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 212

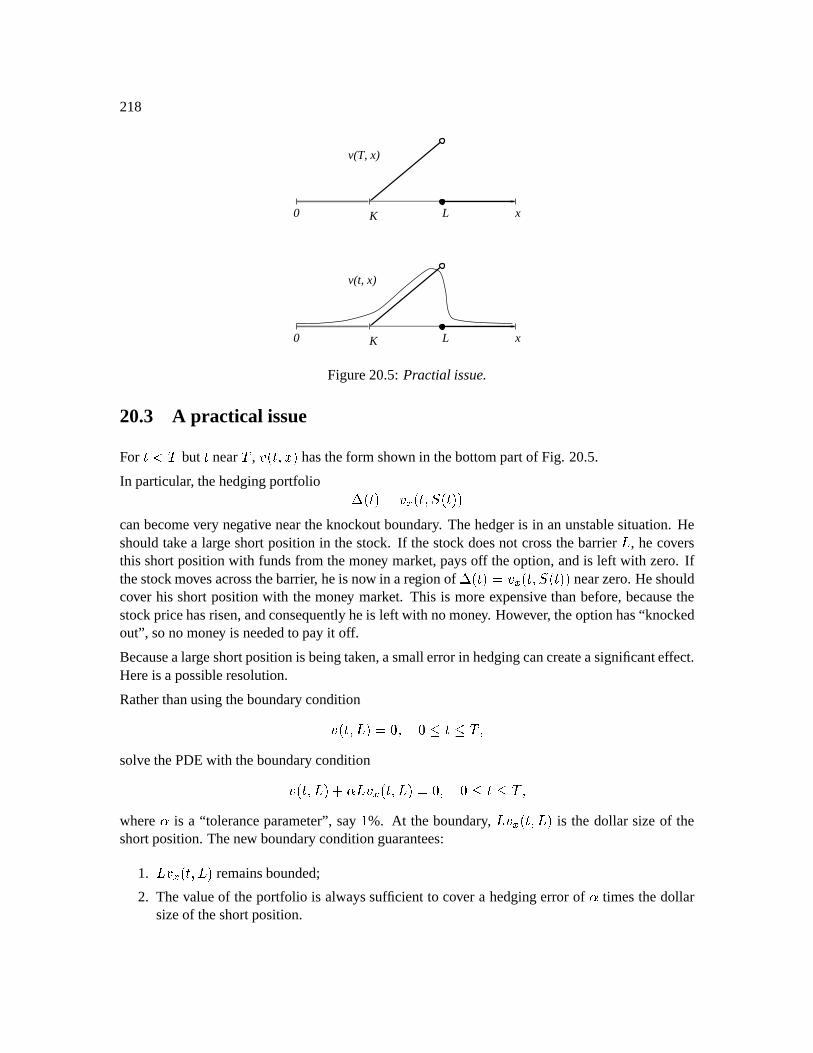

20.3 A practicalissue. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 218

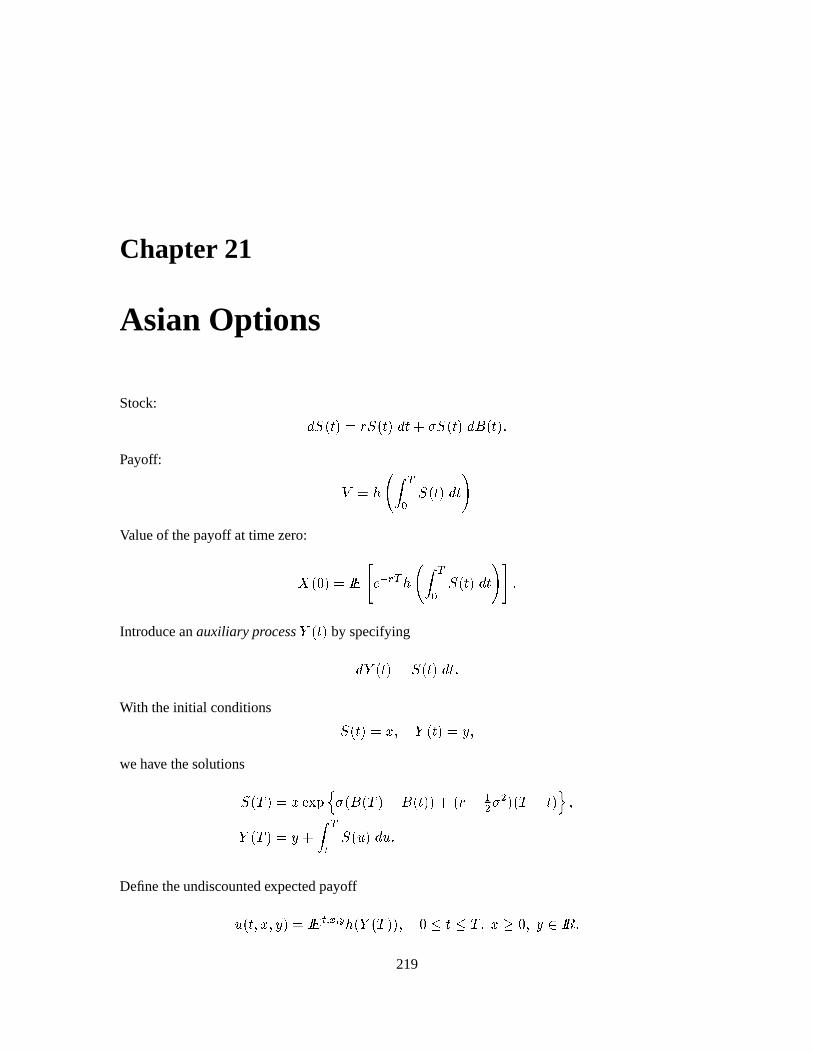

21 Asian Options 219

21.1 Feynman-KacTheorem. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 220

21.2 Constructingthehedge . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 220

21.3 Partial averagepayoff Asianoption . . . . . . . . . . . . . . . . . . . . . . . . . . 221

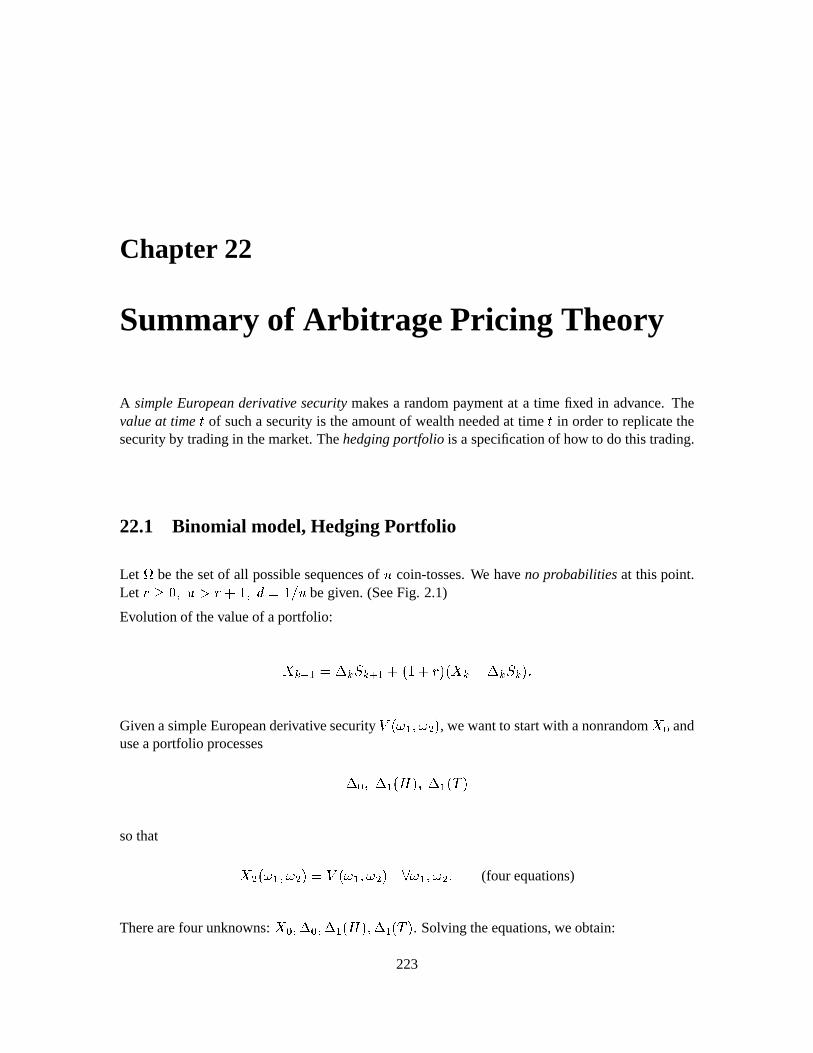

22 Summary of Arbitrage Pricing Theory 223

22.1 Binomialmodel,HedgingPortfolio . . . . . . . . . . . . . . . . . . . . . . . . . 223

22.2 Settingup thecontinuousmodel . . . . . . . . . . . . . . . . . . . . . . . . . . . 225

22.3 Risk-neutralpricingandhedging . . . . . . . . . . . . . . . . . . . . . . . . . . . 227

22.4 Implementationof risk-neutralpricingandhedging . . . . . . . . . . . . . . . . . 229

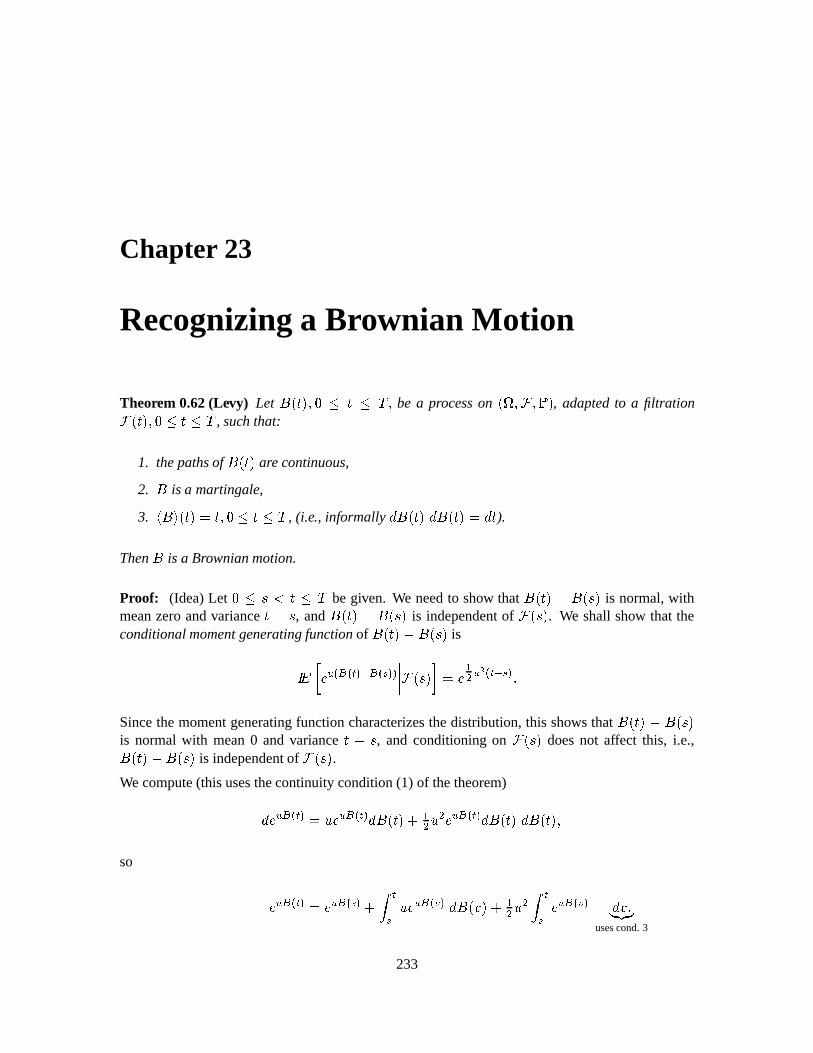

23 Recognizinga Brownian Motion 233

23.1 Identifyingvolatility andcorrelation . . . . . . . . . . . . . . . . . . . . . . . . . 235

23.2 Reversingtheprocess. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 236

24 An outsidebarrier option 239

24.1 Computingtheoptionvalue. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 242

24.2 ThePDEfor theoutsidebarrieroption . . . . . . . . . . . . . . . . . . . . . . . . 243

24.3 Thehedge. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 245

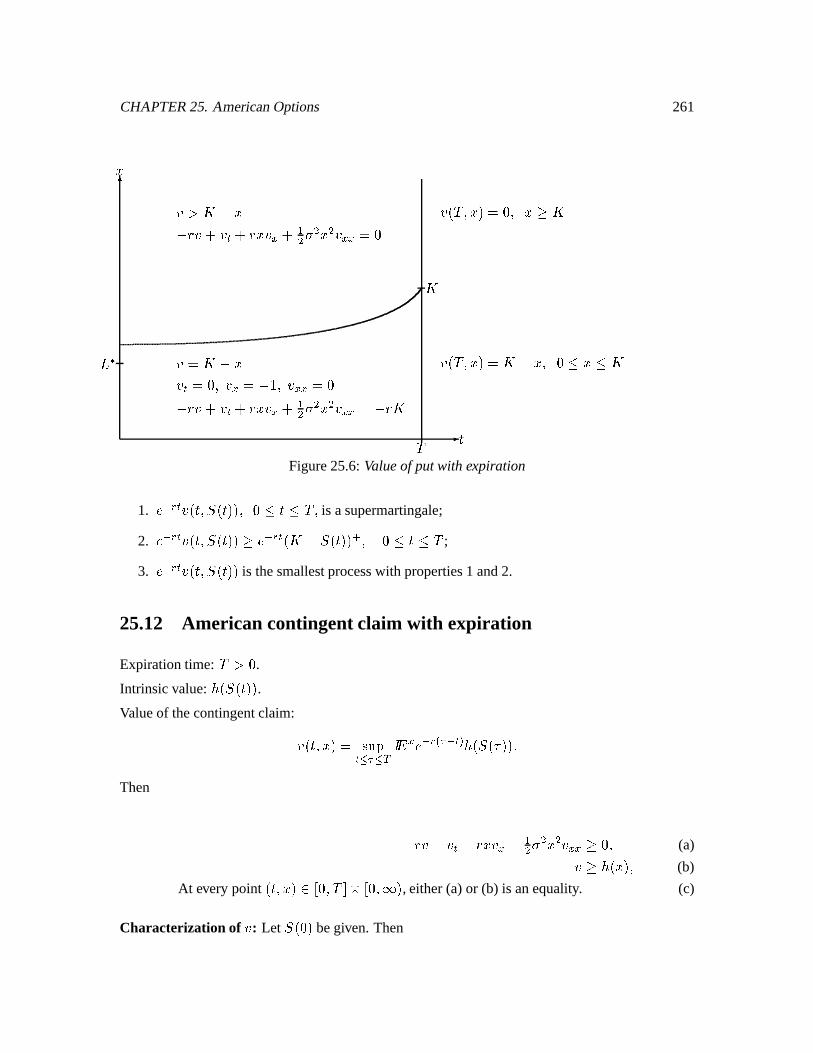

25 American Options 247

25.1 Preview of perpetualAmericanput . . . . . . . . . . . . . . . . . . . . . . . . . . 247

25.2 Firstpassagetimesfor Brownianmotion:first method. . . . . . . . . . . . . . . . 247

25.3 Drift adjustment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 249

25.4 Drift-adjustedLaplacetransform . . . . . . . . . . . . . . . . . . . . . . . . . . . 250

25.5 Firstpassagetimes:Secondmethod . . . . . . . . . . . . . . . . . . . . . . . . . 251

7

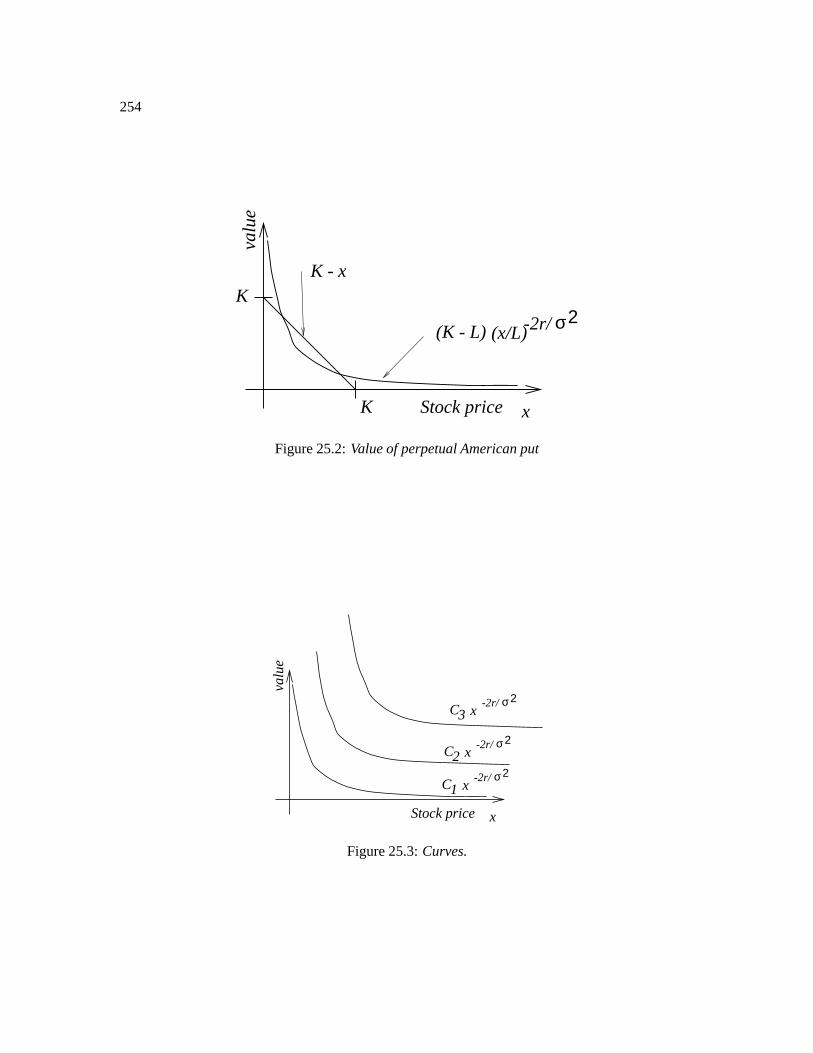

25.6 PerpetualAmericanput . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 252

25.7 Valueof theperpetualAmericanput . . . . . . . . . . . . . . . . . . . . . . . . . 256

25.8 Hedgingtheput . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 257

25.9 PerpetualAmericancontingentclaim . . . . . . . . . . . . . . . . . . . . . . . . . 259

25.10PerpetualAmericancall . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 259

25.11Putwith expiration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 260

25.12Americancontingentclaimwith expiration . . . . . . . . . . . . . . . . . . . . . 261

26 Options on dividend-paying stocks 263

26.1 Americanoptionwith convex payoff function . . . . . . . . . . . . . . . . . . . . 263

26.2 Dividendpayingstock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 264

26.3 Hedgingat time . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 266

27 Bonds,forward contractsand futur es 267

27.1 Forwardcontracts. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 269

27.2 Hedginga forwardcontract. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 269

27.3 Futurecontracts. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 270

27.4 Cashflow from afuturecontract . . . . . . . . . . . . . . . . . . . . . . . . . . . 272

27.5 Forward-futurespread. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 272

27.6 Backwardationandcontango. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 273

28 Term-structure models 275

28.1 Computingarbitrage-freebondprices:first method . . . . . . . . . . . . . . . . . 276

28.2 Someinterest-ratedependentassets . . . . . . . . . . . . . . . . . . . . . . . . . 276

28.3 Terminology. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 277

28.4 Forwardrateagreement. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 277

28.5 Recoveringtheinterest from theforwardrate . . . . . . . . . . . . . . . . . . 278

28.6 Computingarbitrage-freebondprices:Heath-Jarrow-Mortonmethod. . . . . . . . 279

28.7 Checkingfor absenceof arbitrage . . . . . . . . . . . . . . . . . . . . . . . . . . 280

28.8 Implementationof theHeath-Jarrow-Mortonmodel . . . . . . . . . . . . . . . . . 281

29 Gaussianprocesses 285

29.1 An example:BrownianMotion . . . . . . . . . . . . . . . . . . . . . . . . . . . . 286

30 Hull and White model 293

8

30.1 Fiddlingwith theformulas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 295

30.2 Dynamicsof thebondprice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 296

30.3 Calibrationof theHull & Whitemodel . . . . . . . . . . . . . . . . . . . . . . . . 297

30.4 Optionona bond . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 299

31 Cox-Ingersoll-Rossmodel 303

31.1 Equilibriumdistributionof . . . . . . . . . . . . . . . . . . . . . . . . . . . . 306

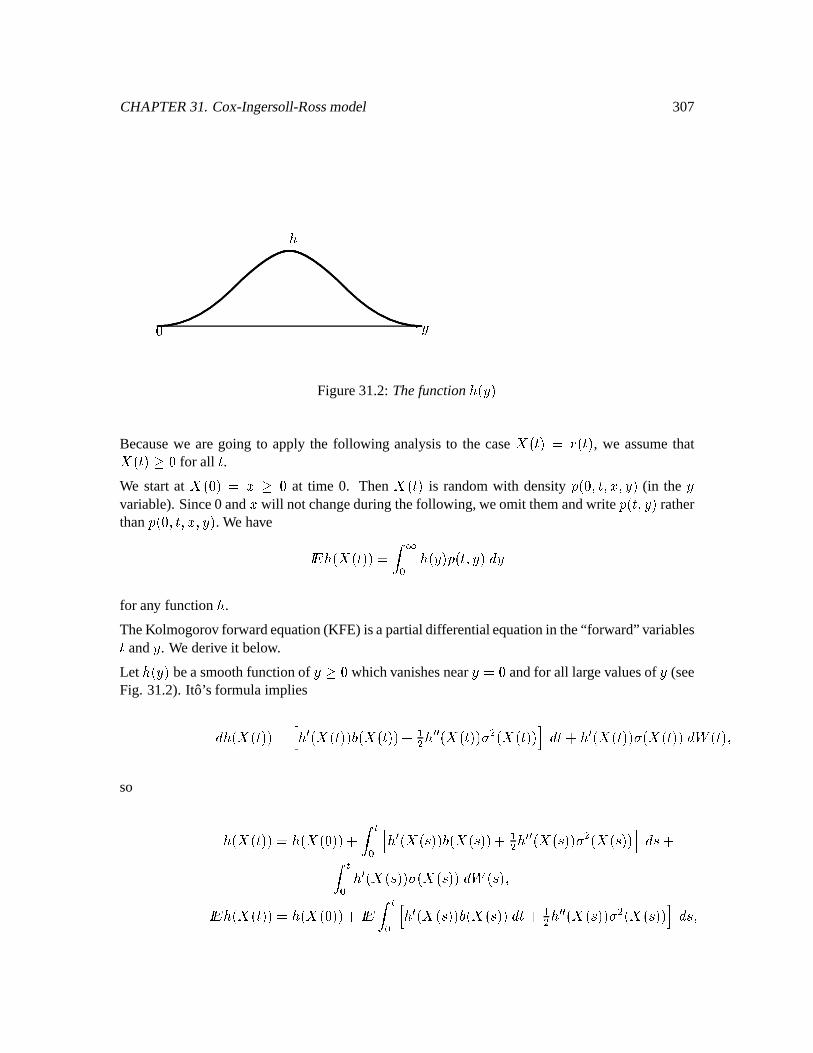

31.2 Kolmogorov forwardequation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 306

31.3 Cox-Ingersoll-Rossequilibriumdensity . . . . . . . . . . . . . . . . . . . . . . . 309

31.4 Bondpricesin theCIR model . . . . . . . . . . . . . . . . . . . . . . . . . . . . 310

31.5 Optionona bond . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 313

31.6 Deterministictimechangeof CIR model . . . . . . . . . . . . . . . . . . . . . . . 313

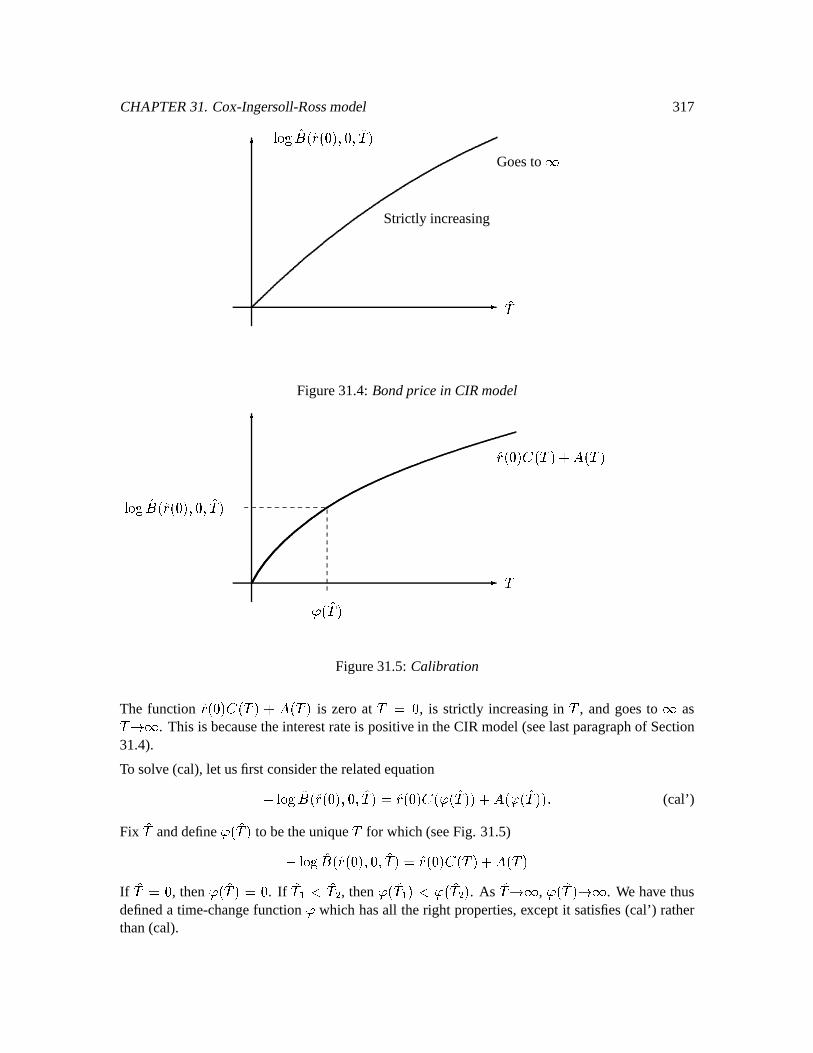

31.7 Calibration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 315

31.8 Trackingdown "!##$% in thetimechangeof theCIR model . . . . . . . . . . . . . 316

32 A two-factor model (Duffie & Kan) 319

32.1 Non-negativity of & . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 320

32.2 Zero-couponbondprices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 321

32.3 Calibration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 323

33 Changeof numeraire 325

33.1 Bondpriceasnumeraire . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 327

33.2 Stockpriceasnumeraire . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 328

33.3 Mertonoptionpricing formula . . . . . . . . . . . . . . . . . . . . . . . . . . . . 329

34 Brace-Gatarek-Musiela model 335

34.1 Review of HJM underrisk-neutral . . . . . . . . . . . . . . . . . . . . . . . . . 335

34.2 Brace-Gatarek-Musielamodel . . . . . . . . . . . . . . . . . . . . . . . . . . . . 336

34.3 LIBOR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 337

34.4 ForwardLIBOR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 338

34.5 Thedynamicsof '(*)* . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 338

34.6 Implementationof BGM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 340

34.7 Bondprices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 342

34.8 ForwardLIBOR undermoreforwardmeasure. . . . . . . . . . . . . . . . . . . . 343

9

34.9 Pricinganinterestratecaplet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 343

34.10Pricinganinterestratecap . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 345

34.11Calibrationof BGM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 345

34.12Longrates. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 346

34.13Pricinga swap. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 346

35 Notesand References 349

35.1 Probabilitytheoryandmartingales.. . . . . . . . . . . . . . . . . . . . . . . . . . 349

35.2 Binomialassetpricingmodel. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 349

35.3 Brownianmotion. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 350

35.4 Stochasticintegrals. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 350

35.5 Stochasticcalculusandfinancialmarkets. . . . . . . . . . . . . . . . . . . . . . . 350

35.6 Markov processes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 351

35.7 Girsanov’stheorem,themartingalerepresentationtheorem,andrisk-neutralmeasures.351

35.8 Exoticoptions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 352

35.9 Americanoptions.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 352

35.10Forwardandfuturescontracts. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 353

35.11Termstructuremodels. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 353

35.12Changeof numeraire. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 353

35.13Foreignexchangemodels. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 353

35.14REFERENCES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 354

10

Chapter 1

Intr oduction to Probability Theory

1.1 The Binomial AssetPricing Model

The binomialassetpricing modelprovidesa powerful tool to understandarbitragepricing theoryandprobabilitytheory. In thiscourse,weshalluseit for boththesepurposes.

In thebinomialassetpricing model,we modelstockpricesin discretetime,assumingthatat eachstep,thestockpricewill changeto oneof two possiblevalues.Let usbegin with aninitial positivestockprice +-, . Therearetwo positivenumbers, and . , with

$/01.2) (1.1)

suchthatat thenext period,thestockpricewill beeither 3+4, or .5+-, . Typically, we take and .to satisfy $676897. , so changeof the stockprice from +-, to :+-, representsa downwardmovement,andchangeof the stockprice from + , to .;+ , representsan upward movement. It iscommonto alsohave < = , andthis will be thecasein many of our examples.However, strictlyspeaking,for whatwe areaboutto doweneedto assumeonly (1.1)and(1.2)below.

Of course,stockpricemovementsaremuchmorecomplicatedthanindicatedby thebinomialassetpricing model.We considerthis simplemodelfor threereasons.First of all, within this modeltheconceptof arbitragepricingandits relationto risk-neutralpricing is clearlyilluminated.Secondly,themodelis usedin practicebecausewith a sufficientnumberof steps,it providesa good,compu-tationally tractableapproximationto continuous-timemodels.Thirdly, within thebinomialmodelwe candevelop the theoryof conditionalexpectationsandmartingaleswhich lies at the heartofcontinuous-timemodels.

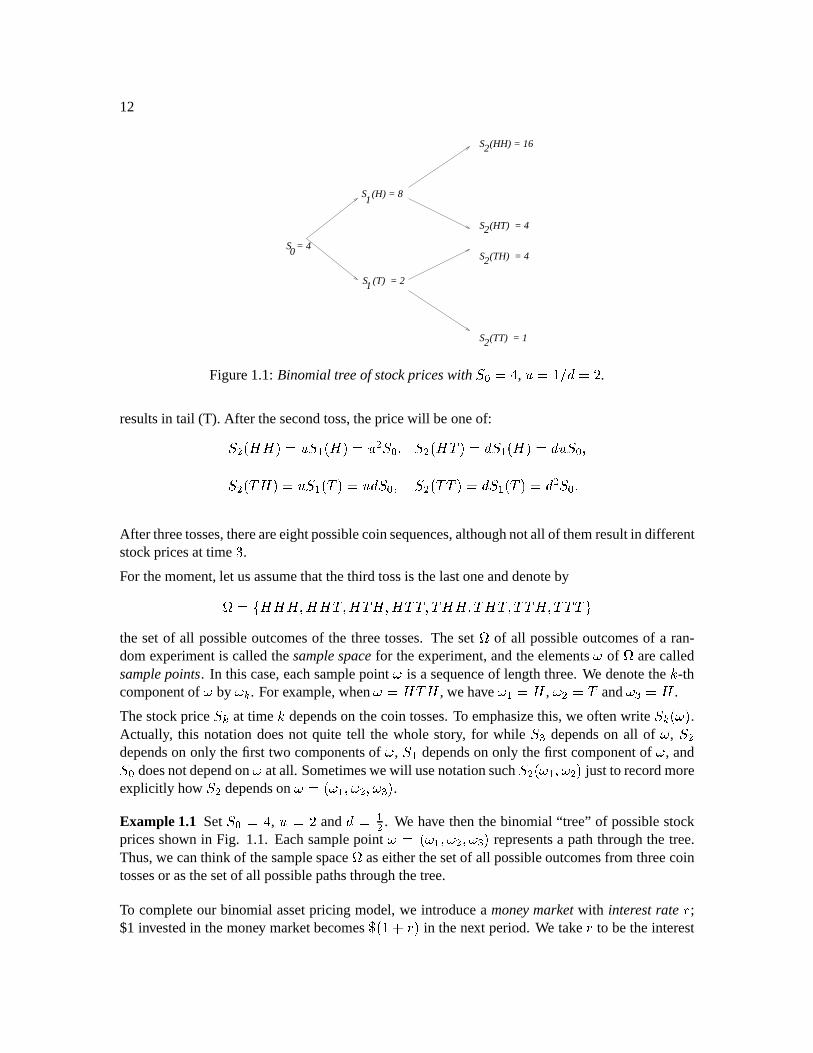

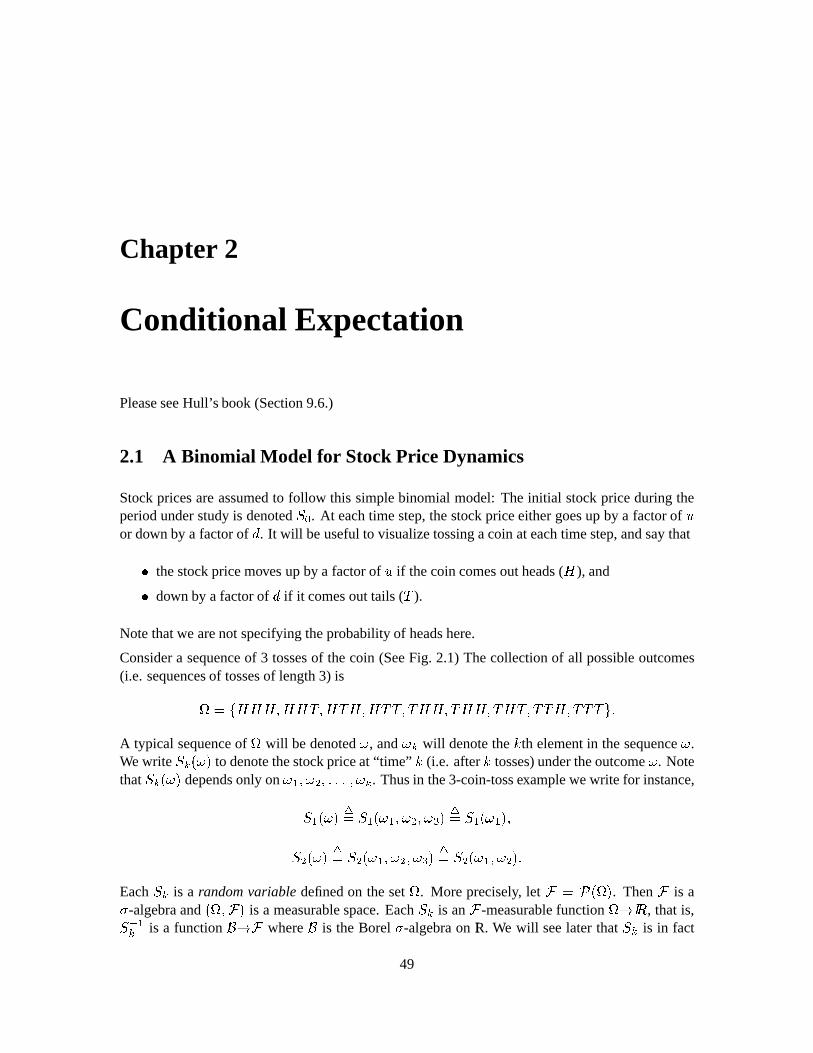

With this third motivation in mind, we develop notationfor the binomial model which is a bitdifferentfrom thatnormallyfoundin practice.Let usimaginethatwe aretossinga coin,andwhenwe geta “Head,” thestockpricemovesup, but whenwe get a “Tail,” thepricemovesdown. Wedenotethepriceat time by +">#?@".5+-, if thetossresultsin head(H), andby +">A(":+-, if it

11

12

S = 40

S (H) = 8

S (T) = 2

S (HH) = 16

S (TT) = 1

S (HT) = 4

S (TH) = 4

1

1

2

2

2

2

Figure1.1: Binomialtreeof stock priceswith +-,(CB , .ED%F .resultsin tail (T). After thesecondtoss,thepricewill beoneof:+2G%#?@?@H.;+"I#?@J. G +-,K)L+2G%#?MA("3+NO#?@J:.5+4,>)+2G%A(?@".5+">A(J.5:+-,K) +2G%APA(JQ3+"IA(JQ G +-,%RAfter threetosses,thereareeightpossiblecoinsequences,althoughnotall of themresultin differentstockpricesat time S .For themoment,let usassumethatthethird tossis thelastoneanddenotebyT VUK?W?@?M)*?@?MAP)?MAX?M)*?YAPA()AP?@?M)A(?MAP)APA(?M)APAPA[Zthe setof all possibleoutcomesof the threetosses.The set

Tof all possibleoutcomesof a ran-

domexperimentis calledthesamplespacefor theexperiment,andtheelements\ ofT

arecalledsamplepoints. In this case,eachsamplepoint \ is a sequenceof lengththree.We denotethe ] -thcomponentof \ by \J^ . For example,when\_?MA(? , wehave \`a? , \NGPbA and \Hc(? .

Thestockprice + ^ at time ] dependson thecoin tosses.To emphasizethis,we oftenwrite + ^ d\a .Actually, this notationdoesnot quite tell the whole story, for while +-c dependson all of \ , +2Gdependson only thefirst two componentsof \ , +N dependson only thefirst componentof \ , and+ , doesnotdependon \ atall. Sometimeswewill usenotationsuch+ G d\ )e\ G just to recordmoreexplicitly how +fG dependson \_gd\hi)e\NGI)e\HcI .Example1.1 Set + , gB , .9LF and j G . We have thenthebinomial “tree” of possiblestockpricesshown in Fig. 1.1. Eachsamplepoint \Qkd\`l)\NGK)e\Hci representsa paththroughthe tree.Thus,we canthink of thesamplespace

Taseitherthesetof all possibleoutcomesfrom threecoin

tossesor asthesetof all possiblepathsthroughthetree.

To completeour binomialassetpricing model,we introducea money marketwith interestrate ;$1 investedin themoney marketbecomesm5hn0K in thenext period.We take to betheinterest

CHAPTER1. Introductionto ProbabilityTheory 13

ratefor bothborrowingandlending. (This is not asridiculousasit first seems,becausein a manyapplicationsof themodel,anagentis eitherborrowing or lending(not both)andknowsin advancewhich shewill bedoing; in suchanapplication,sheshouldtake to betherateof interestfor heractivity.) We assumethat o`n0p0.fR (1.2)

Themodelwouldnotmakesenseif wedid nothave thiscondition.For example,if "nqpr0. , thentherateof returnon themoney marketis alwaysat leastasgreatasandsometimesgreaterthanthereturnon thestock,andnoonewould investin thestock.Theinequality <r`n1 cannothappenunlesseither is negative(whichneverhappens,exceptmaybeonceuponatimein Switzerland)or9rL . In the lattercase,thestockdoesnot really go “down” if we geta tail; it just goesup lessthanif we hadgottena head.Oneshouldborrow money at interestrate andinvestin the stock,sinceevenin theworstcase,thestockpricerisesat leastasfastasthedebtusedto buy it.

With the stock as the underlyingasset,let us considera Europeancall option with strike priceskt $ andexpirationtime . Thisoptionconferstheright to buy thestockat time fors

dollars,andsois worth +"` s at time if +"` s is positiveandis otherwiseworthzero.We denotebyu Id\aJg#+NOd\a" s wv6xQyzKU>+NOd\a| s )*$:Zthevalue(payoff) of this optionat expiration. Of course,

u O\a actuallydependsonly on \h , andwecananddosometimeswrite

u >\`e ratherthanu Id\a . Ourfirst taskis to computethearbitrage

priceof thisoptionat timezero.

Supposeat time zeroyou sell thecall foru , dollars,where

u , is still to bedetermined.You nowhave anobligationto pay off #.;+-,( s v if \`~L? andto payoff #:+-,( s v if \`~A . Atthe time you sell theoption,you don’t yet know which value \` will take. You hedgeyour shortpositionin theoptionby buying , sharesof stock,where , is still to bedetermined.Youcanusetheproceeds

u , of thesaleof theoption for this purpose,andthenborrow if necessaryat interestrate to completethe purchase.If

u , is morethannecessaryto buy the /, sharesof stock,youinvesttheresidualmoney at interestrate . In eithercase,youwill have

u , , + , dollarsinvestedin themoney market,wherethisquantitymight benegative. Youwill alsoown /, sharesof stock.

If thestockgoesup,thevalueof yourportfolio (excludingtheshortpositionin theoption)is , + ?W-nVJn0KI u , 9 , + , l)andyou needto have

u I#?@ . Thus,you wantto chooseu , and , sothatu I#?@J/,l+">#?@-n`n6KI u ,9/,I+-,llR (1.3)

If thestockgoesdown, thevalueof yourportfolio is/,I+">A(-n`n6KI u ,9/,I+-,ll)andyou needto have

u A( . Thus,youwantto chooseu , and , to alsohaveu IA(J/,l+">A[nVJn0KI u ,`/,l+-,IlR (1.4)

14

Thesearetwo equationsin two unknowns,andwesolve thembelow

Subtracting(1.4)from (1.3),weobtainu #?@H u A(J , #+ #?@H9+ A(l) (1.5)

sothat /,P u I#?@" u OA(+ #?@"q+ A( R (1.6)

This is a discrete-timeversionof thefamous“delta-hedging”formulafor derivativesecurities,ac-cordingto which thenumberof sharesof anunderlyingasseta hedgeshouldhold is thederivative(in the senseof calculus)of the valueof the derivative securitywith respectto the price of theunderlyingasset.This formula is sopervasive thewhena practitionersays“delta”, shemeansthederivative (in thesenseof calculus)just described.Note,however, thatmy definitionof /, is thenumberof sharesof stockoneholdsat time zero,and(1.6) is a consequenceof this definition,notthe definition of , itself. Dependingon how uncertaintyentersthe model, therecan be casesin which thenumberof sharesof stocka hedgeshouldhold is not the(calculus)derivative of thederivativesecuritywith respectto thepriceof theunderlyingasset.

To completethesolutionof (1.3) and(1.4), we substitute(1.6) into either(1.3) or (1.4)andsolveforu , . After somesimplification,this leadsto theformulau ,P `n6 `n0[9.9 u O#?@-n .bJn0K.oq u >A(aR (1.7)

This is thearbitrageprice for theEuropeancall optionwith payoffu at time . To simplify this

formula,wedefine x `n0[9.q ) x .0e`n6K.o9 P ) (1.8)

sothat(1.7)becomes u ,P Jn1H u I#?@-n u OA[R (1.9)

Becausewe have taken 9g. , both

and

aredefined,i.e.,thedenominatorin (1.8) is not zero.Becauseof (1.2),both

and

arein the interval $)II , andbecausethey sumto , we canregardthemasprobabilitiesof ? and A , respectively. They arethe risk-neutral probabilites.They ap-pearedwhenwe solvedthe two equations(1.3) and(1.4), andhave nothingto do with the actualprobabilitiesof getting ? or A on thecoin tosses.In fact,at this point, they arenothingmorethana convenienttool for writing (1.7)as(1.9).

We now considera Europeancall which paysoffs

dollarsat time F . At expiration,thepayoff of

this option isu G x8#+ G s v , where

u G and + G dependon \ and \ G , thefirst andsecondcointosses.Wewantto determinethearbitragepricefor thisoptionat timezero.Supposeanagentsellstheoptionat time zerofor

u , dollars,whereu , is still to bedetermined.Shethenbuys , shares

CHAPTER1. Introductionto ProbabilityTheory 15

of stock,investingu ,P/,l+-, dollarsin themoney marketto financethis. At time , theagenthas

a portfolio (excludingtheshortpositionin theoption)valuedat (x/,I+NHn`n6KI u ,9/,I+-,llR (1.10)

Althoughwe do not indicateit in thenotation,+" andtherefore dependon \` , theoutcomeof

thefirst coin toss.Thus,therearereally two equationsimplicit in (1.10): O#?@x /,i+N>#?@ne`n6KI u ,a9,I+-,iO) IA(x /,i+N>A(-nJn6KI u ,9/,I+-,IlRAfter thefirst coin toss,theagenthas

dollarsandcanreadjustherhedge.Supposeshedecidestonow hold sharesof stock,where is allowedto dependon \ becausetheagentknowswhatvalue \` hastaken.Sheinveststheremainderof herwealth,

`6<+" in themoney market.Inthenext period,herwealthwill begivenby theright-handsideof thefollowing equation,andshewantsit to be

u G . Therefore,shewantsto haveu G<*+2GJnhn6>E J9<*+"lR (1.11)

Althoughwedonot indicateit in thenotation,+2G andu G dependon \` and \NG , theoutcomesof the

first two coin tosses.Consideringall four possibleoutcomes,wecanwrite (1.11)asfour equations:u G #?@?@ ?Ww+ G ?W?@;nJn0KI #?@"9 #?@+ #?@l)u G%?A[ <O?Ww+2G>?A[ne`n6KI i?W"<O?Ww+"O?Wwl)u G%A(?@ <OA(+2GKA(?@-n`n6KI OA[H<IA(+"IA(wl)u GKAPA( <OA(+2GKAPA(-nVJn0KI lA(J9<>A(+"iA(lRWe now havesix equations,thetwo representedby (1.10)andthefour representedby (1.11),in thesix unknowns

u , , /, , O#?@ , <>A( , >#?@ , and >A[ .

To solvetheseequations,andtherebydeterminethearbitragepriceu , at timezeroof theoptionand

thehedgingportfolio , , #?@ and A( , webegin with thelasttwou G>A[?W >A(+2GEA(?@-nJn0KI iA("<OA(+"IA(O)u G>APA( >A(+2GEAPA(2ne`n6KI iA(J9<>A[+"IA(lRSubtractingoneof thesefrom theotherandsolvingfor <OA( , we obtainthe“delta-hedgingfor-mula” <IA(J u G%A(?@" u GKAPA[+fG%A(?@"9+2G%APA( ) (1.12)

andsubstituting this into eitherequation,wecansolvefor A(" `n0 u G A(?@-n u G AA(R (1.13)

16

Equation(1.13),givesthevaluethehedgingportfolio shouldhave at time if thestockgoesdownbetweentimes $ and . We definethis quantityto bethearbitragevalueof theoptionat time if\`aCA , andwe denoteit by

u OA[ . We have justshown thatu OA[Px `n6" u G%A(?@5n u GKAPA(R (1.14)

The hedgershouldchooseher portfolio so that her wealth A( if \ A agreeswith

u A(definedby (1.14). This formula is analgousto formula(1.9),but postponedby onestep.Thefirsttwo equationsimplicit in (1.11)leadin a similarway to theformulas<>?W" u G%?W?@f u G>?A[+2G%?W?@fq+2GK#?MA( (1.15)

and I#?@J u O#?@ , where

u O?W is thevalueof theoptionat time if \`aQ? , definedbyu I#?@x `n0f u GK#?@?W-n u G>?A[R (1.16)

Thisisagainanalgousto formula(1.9),postponedbyonestep.Finally, weplugthevalues #?@Ju O?W and

IA(P u OA[ into thetwo equationsimplicit in (1.10). Thesolutionof theseequa-tions for /, and

u , is the sameasthe solutionof (1.3) and(1.4), andresultsagainin (1.6) and(1.9).

Thepatternemerging herepersists,regardlessof thenumberof periods.Ifu ^ denotesthevalueat

time ] of a derivative security, andthis dependson thefirst ] coin tosses\`I)ERIRER)\N^ , thenat time]<b , after thefirst ]< tosses\hI)IRIRER)\J^l- areknown, the portfolio to hedgea shortpositionshouldhold ^O- d\ )IRERIR)e\ ^O sharesof stock,where ^O- d\ )ERIRIRw)\ ^O- J u ^%\`I)IRERIR)e\N^l-I)?Wf u ^3\`i)ERIRER)\N^O-I)A(+2^3\`I)IRERIR)e\N^l-I)?Wfq+2^:d\`I)ERIRIR)e\N^l-I)wA( ) (1.17)

andthevalueat time ]ob of thederivative security, whenthefirst ]b coin tossesresultin theoutcomes\hI)IRIRER)\N^O- , is givenbyu ^l->d\`l)IRERIR)e\N^O*J `n6"

u ^3d\hi)ERIRIRw)\N^O-I)*?@5n u ^:d\`l)IRIRER)\J^l-I)A[(1.18)

1.2 Finite Probability Spaces

LetT

bea setwith finitely many elements.An exampleto keepin mindisT VUK?W?@?M)*?@?MAP)?MAX?M)*?YAPA()AP?@?M)A(?MAP)APA(?M)APAPA[Z (2.1)

of all possibleoutcomesof threecoin tosses.Let bethesetof all subsetsofT

. Somesetsin are , U>?@?@?)?W?MAP)?jA(?M)?MAaAZ , UIAPAPAZ , and

Titself. How many setsaretherein ?

CHAPTER1. Introductionto ProbabilityTheory 17

Definition 1.1 A probability measure is a function mapping into $)E with the followingproperties:

(i) T J ,(ii) If I)*[GI)ERIRIR is asequenceof disjoint setsin , then gY^* f [^l¡b¢^ 2 #[^KlRProbabilitymeasureshave the following interpretation.Let bea subsetof . Imaginethat

Tis

thesetof all possibleoutcomesof somerandomexperiment.Thereis acertainprobability, between$ and , that whenthat experimentis performed,the outcomewill lie in the set . We think of #[ asthisprobability.

Example1.2 Supposea coin hasprobability c for ? and Gc for A . For the individualelementsofTin (2.1),define pU>?@?@?£Z(¤ cK¥ c ) pU>?@?MAZ(¤ cK¥ G ¤ Gc%¥ ) pU>?MA(?£Z(¤ c¦¥ G ¤ Gc%¥ ) pU>?MAPAZ(§¤ c%¥ ¤ Gc>¥ G ) pUIA[?W?£Z(¤ c¦¥ G ¤ c%¥ ) pUIA(?MAZ(§¤ c%¥ ¤ Gc>¥ G ) pUIAA(?£Z~¤ c ¥ ¤ Gc ¥ G ) pUIAPAAZ~¤ Gc ¥ c R

For ¨< , we define #[` ¢©«ª>¬ pUl\PZ3R (2.2)

For example, pU>?@?@?)?@?A[)?jA(?M)?MAAZa8 S-® c n1F S;® G FS-® n7 S-® FS;® G S )which is anotherwayof sayingthattheprobabilityof ? on thefirst tossis c .As in theaboveexample,it is generallythecasethatwespecifyaprobabilitymeasureononly someof thesubsetsof

Tandthenuseproperty(ii) of Definition1.1to determine #[ for theremaining

setsV¨j . In theaboveexample,wespecifiedtheprobabilitymeasureonly for thesetscontainingasingleelement,andthenusedDefinition1.1(ii) in theform (2.2)(seeProblem1.4(ii)) to determine for all theothersetsin .

Definition 1.2 LetT

be a nonemptyset. A -algebrais a collection ¯ of subsetsofT

with thefollowing threeproperties:

(i) /¨M¯ ,

18

(ii) If V¨¯ , thenits complement(°¨M¯ ,

(iii) If i)(GE)*cK)IRIRER is a sequenceof setsin ¯ , then ± ^ 2 (^ is alsoin ¯ .

Herearesomeimportant -algebrasof subsetsof thesetT

in Example1.2: , ²J«) T³ )´ ²J«) T )OU>?@?W?M)?@?jAP)?jA(?M)?MAaAZ3)UIA(?M?)wAX?MAP)APA[?)APAAZ ³ )(Gµ ²J«) T )OU>?@?W?M)?@?jAZ:)U>?jA(?M)?MAAZ3)UIA(?M?)wAP?A[Z3)OUlAPA(?M)APAPAZ3)andall setswhich canbebuilt by takingunionsof these

³ )Pc¶ g Thesetof all subsetsofT R

To simplify notationa bit, let usdefineP·xVU>?@?@?)?W?MAP)?MAP?)?jAPAZ|¸U>? on thefirst tossZ:)P¹qxVUEA(?@?)wA(?MA()APAP?M)AAPAZa¸UIA on thefirst tossZ3)sothat `VU>) T )*·()P¹"Z3)andlet usdefine ··¸xVU>?@?@?M)*?@?jAZVU>?@? on thefirst two tossesZ3) ·¹ xVU>?MA(?M)*?MAPAZ`VU>?MA on thefirst two tossesZ3) ¹5· xVUIA(?@?M)A(?MAZ`VUIA[? on thefirst two tossesZ3) ¹5¹ xVUEAPA(?M)APAPAZaVUIAPA on thefirst two tossesZ3)sothat (Gº U>) T )*·a·[)*·¹H)*¹5·)P¹;¹N) · )* ¹ )* ·a· ±M ¹;· )* ·· ±M ¹;¹ )* ·a¹ ± ¹5· ) ·¹ ± ¹5¹ ) °·· ) °·¹ )* °¹5· )* °¹5¹ Z3RWe interpret -algebrasasarecordof information.Supposethecoin is tossedthreetimes,andyouarenot told theoutcome,but you aretold, for every setin whetheror not theoutcomeis in thatset.For example,you would betold thattheoutcomeis not in andis in

T. Moreover, you might

betold that theoutcomeis not in · but is in ¹ . In effect, you have beentold that thefirst tosswasa A , andnothingmore.The -algebra is saidto containthe“information of thefirst toss”,which is usuallycalledthe“information up to time ”. Similarly, [G containsthe“information of

CHAPTER1. Introductionto ProbabilityTheory 19

thefirst two tosses,” which is the“informationup to time F .” The -algebraPc(Q contains“fullinformation”abouttheoutcomeof all threetosses.Theso-called“tri vial” -algebra , containsnoinformation.Knowing whethertheoutcome\ of thethreetossesis in (it is not)andwhetherit isinT

(it is) tellsyounothingabout\Definition 1.3 Let

Tbeanonemptyfiniteset.A filtrationisasequenceof -algebrasP,%)*)(GE)IRERIR)wP»

suchthateach -algebrain thesequencecontainsall thesetscontainedby theprevious -algebra.

Definition 1.4 LetT

be a nonemptyfinite setandlet be the -algebraof all subsetsofT

. Arandomvariableis a functionmapping

Tinto ¼ .

Example1.3 LetT

begivenby (2.1)andconsiderthebinomialassetpricing Example1.1,where+-,9B , .VF and b G . Then +-, , +" , +2G and +4c areall randomvariables. For example,+2G%#?@?MA(JV. G +-,[LI½ . The“randomvariable” +-, is really not random,since +-,¾\a`VB for all\¿¨ T . Nonetheless,it is a functionmappingT

into ¼ , andthustechnicallya randomvariable,albeita degenerateone.

A randomvariablemapsT

into ¼ , andwe canlook at thepreimageundertherandomvariableofsetsin ¼ . Consider, for example,therandomvariable+2G of Example1.1. Wehave+2GK#?@?@?W"+2GK#?@?MA("I½)+2GK#?MA(?@HQ+2G%#?MAPA("+2G%A[?W?@2Q+2G%A(?MA("bB5)+2GKAPA(?@J+fG>AAPA(J%RLet usconsidertheinterval B5)F%ÀE . Thepreimageunder +2G of this interval is definedto beUO\¨ TÁ +2GKd\a¨ B5)*F%À>ÂZaVUl\0¨ TÁ B/Ã0+2G[Ã0F%À:Z(Q °¹;¹ RThecompletelist of subsetsof

Twe cangetaspreimagesof setsin ¼ is:) T )P··[)*·a¹±j¹5·)P¹;¹H)

andsetswhich canbebuilt by takingunionsof these.This collectionof setsis a -algebra,calledthe -algebra generatedby the randomvariable +2G , andis denotedby `+2G* . The informationcontentof this -algebrais exactly the information learnedby observing+2G . More specifically,supposethecoin is tossedthreetimesandyou do not know theoutcome\ , but someoneis willingto tell you, for eachsetin h#+2G , whether\ is in theset.Youmight betold, for example,that \ isnot in ·· , is in ·¹ ±j ¹5· , andis not in ¹;¹ . Thenyou know thatin thefirst two tosses,therewasa headanda tail, andyou know nothingmore. This informationis thesameyou would havegottenby beingtold thatthevalueof +fG>d\a is B .Note that (G definedearliercontainsall the setswhich arein `#+2G , andevenmore. This meansthattheinformationin thefirst two tossesis greaterthantheinformationin + G . In particular, if youseethefirst two tosses,you candistinguishP·¹ from ¹5· , but you cannotmakethis distinctionfrom knowing thevalueof +2G alone.

20

Definition 1.5 LetT

bea nonemtpyfinite setandlet bethe -algebraof all subsetsofT

. Let

bearandomvariableon T )w . The -algebra h generatedby

is definedto bethecollectionof all setsof theform Ul\b¨ TÁ d\aJ¨@Z , where is a subsetof ¼ . Let ¯ bea sub- -algebraof . Wesaythat

is ¯ -measurableif every setin ` is alsoin ¯ .

Note:We normallywrite simply U ¨Z ratherthan UO\¨ TÁ d\aJ¨MZ .Definition 1.6 Let

Tbea nonempty, finite set,let bethe -algebraof all subsetsof

T, let be

a probabiltymeasureon T )w , andlet

bea randomvariableonT

. Givenany set gÄV ¼ , wedefinethe inducedmeasureof to beÅhÆ ( x pU ¨Z3RIn otherwords,theinducedmeasureof a set tells ustheprobabilitythat

takesa valuein . In

thecaseof +2G abovewith theprobabilitymeasureof Example1.2,somesetsin ¼ andtheir inducedmeasuresare: ÅaÇlÈ %J #¦J$)Å ÇlÈ ¼J T `%)Å ÇlÈ $)*É6" T `%)Å ÇlÈ $)*SE5 pUK+2GKZ~b P¹;¹HJ8 FS ® G RIn fact,theinducedmeasureof + G placesamassof size ¤ c¦¥ G Ê at thenumber I½ , amassof sizeËÊ at the numberB , anda massof size ¤ Gc%¥ G ËÊ at the number . A commonway to recordthis

informationis to give thecumulativedistribution function Ì ÇlÈ #Í; of +2G , definedby

Ì ÇlÈ Í5Px +2GÃ0Í;JÎÏÏÏÐ ÏÏÏÑ$) if ÍM%)ËÊ ) if Ã1Íj6B5)ÒÊ ) if BÃ1ÍjI½)%) if I½/Ã0ÍfR (2.3)

By the distribution of a randomvariable

, we meanany of the several waysof characterizingÅ`Æ

. If

is discrete,asin thecaseof +fG above, we caneithertell wherethemassesareandhowlargethey are,or tell whatthecumulative distribution functionis. (Laterwe will considerrandomvariables

whichhavedensities,in whichcasetheinducedmeasureof aset QÄ0 ¼ is theintegral

of thedensityover theset .)

Important Note. In orderto work throughthe conceptof a risk-neutralmeasure,we setup thedefinitionsto makea cleardistinctionbetweenrandomvariablesandtheir distributions.

A randomvariable is a mappingfromT

to ¼ , nothingmore. It hasanexistencequiteapartfromdiscussionof probabilities. For example,in the discussionabove, +2G%APA(?@k+2G>APAPA(/ ,regardlessof whethertheprobabilityfor ? is c or G .

CHAPTER1. Introductionto ProbabilityTheory 21

Thedistributionof a randomvariableis a measure

Å`Æon ¼ , i.e.,a way of assigningprobabilities

to setsin ¼ . It dependsontherandomvariable

andtheprobabilitymeasure weuseinT

. If wesettheprobabilityof ? to be c , then

Å ÇlÈassignsmassÊ to thenumberI½ . If wesettheprobability

of ? to be G , then

Å ÇlÈassignsmass Ë to thenumber I½ . Thedistributionof +2G haschanged,but

therandomvariablehasnot. It is still definedby+2GK#?@?@?W"+2GK#?@?MA("I½)+2GK#?MA(?@HQ+2G%#?MAPA("+2G%A[?W?@2Q+2G%A(?MA("bB5)+2GKAPA(?@J+fG>AAPA(J%RThus,arandomvariablecanhavemorethanonedistribution(a“market”or “objective” distribution,anda “risk-neutral”distribution).

In a similar vein, two different randomvariablescanhave the samedistribution. Supposein thebinomial modelof Example1.1, the probability of ? andthe probability of A is G . ConsideraEuropeancall with strikeprice lB expiring at time F . Thepayoff of thecall at time F is therandomvariable #+ G 0lB: v , which takesthevalue F if \£Q?W?@? or \_?@?MA , andtakesthevalue $ ineveryothercase.Theprobabilitythepayoff is F is Ë , andtheprobabilityit is zerois cË . Consideralsoa Europeanput with strikeprice S expiring at time F . Thepayoff of theput at time F is #S+2G* v ,which takesthevalue F if \gAA(? or \gAAPA . Like thepayoff of thecall, thepayoff of theput is F with probability Ë and $ with probability cË . Thepayoffs of thecall andtheputaredifferentrandomvariableshaving thesamedistribution.

Definition 1.7 LetT

bea nonempty, finite set,let bethe -algebraof all subsetsofT

, let bea probabiltymeasureon T )w , andlet

bea randomvariableon

T. Theexpectedvalueof

is

definedto be Ó x ¢©ª>Ô \a pUl\PZ3R (2.4)

Noticethattheexpectedvaluein (2.4)is definedto beasumoverthesamplespaceT

. SinceT

is afinite set,

cantakeonly finitely many values,whichwelabel Í-l)IRERIR)Í» . We canpartition

Tinto

thesubsetsU JÍ-lZ:)IRIRER)lU »~QÍ»;Z , andthenrewrite (2.4)as Ó x ¢©ª>Ô d\a pUl\PZ »¢^* f ¢©«ª¾Õ ÆJÖ ;× ÖØ d\a pUO\PZ »¢^* f Í;^ ¢©ª%Õ ÆJÖ ;× ÖØ pUl\PZ »¢^* f Í ^ pU ^ QÍ ^ Z »¢^* f Í;^ ÅhÆ U>Í;^KZ3R

22

Thus,althoughtheexpectedvalueis definedasasumover thesamplespaceT

, wecanalsowrite itasa sumover ¼ .

To maketheabove setof equationsabsolutelyclear, we consider+2G with thedistributiongivenby(2.3). Thedefinitionof Ó/+2G is Ó/+2GÙ +2G%?W?@?@ pUK?W?@?£ZHn6+2G%#?@?MA( pU>?@?AZn+2G%#?MA(?@ pU>?MA(?£ZHn1+2G>?AA( pU>?MAPAZn+ G A(?@?@ pUIA[?W?£ZHn1+ G A(?MA( pUIA[?AZn+2G%APA(?@ pUIAPA(?£ZNn6+fG%APAPA(w pUIAPAPAZ I½ÚI #··(2n6BÚI #P·¹±j¹5·-nPÚl P¹;¹H I½ÚI pU>+2GE½:ZanBÚI pU>+2GbBZanbÚI pU>+2GKZ I½Ú ÅaÇOÈ U3I½:Z`nBÚ ÅÇlÈ UIB«Z|nQÚ ÅaÇOÈ U3KZ I½Ú Û n6BÚ BÛ nB~Ú BÛ B3ÜÛ RDefinition 1.8 Let

Tbeanonempty, finite set,let bethe -algebraof all subsetsof

T, let bea

probabiltymeasureon T )< , andlet

bea randomvariableonT

. Thevarianceof

is definedto betheexpectedvalueof 9 Ó G , i.e.,

Var Px ¢©ªKÔ d\a2 Ó G pUl\PZ3R (2.5)

Oneagain,we canrewrite (2.5)asa sumover ¼ ratherthanoverT

. Indeed,if

takesthevaluesÍ )ERIRER)*Í » , then

Var " »¢^* f #Í5^9 Ó G pU QÍ5^KZ »¢^ 2 #Í5^9 Ó G ÅhÆ #Í;^IlR1.3 LebesgueMeasureand the LebesgueIntegral

In thissection,we considerthesetof realnumbers ¼ , which is uncountablyinfinite. We definetheLebesguemeasureof intervalsin ¼ to betheir length.Thisdefinitionandthepropertiesof measuredeterminethe Lebesguemeasureof many, but not all, subsetsof ¼ . The collectionof subsetsof ¼ we consider, andfor which Lebesguemeasureis defined,is thecollectionof Borel setsdefinedbelow.

We useLebesguemeasureto constructthe Lebesgueintegral, a generalizationof the Riemannintegral. We needthis integral because,unlike theRiemannintegral, it canbedefinedon abstractspaces,suchas the spaceof infinite sequencesof coin tossesor the spaceof pathsof Brownianmotion. This sectionconcernsthe Lebesgueintegral on the space ¼ only; the generalizationtootherspaceswill begivenlater.

CHAPTER1. Introductionto ProbabilityTheory 23

Definition 1.9 TheBorel -algebra, denotedÝ# ¼ , is thesmallest -algebracontainingall openintervalsin ¼ . Thesetsin Ý# ¼ arecalledBorel sets.

Everysetwhichcanbewrittendown andjustabouteverysetimaginableis in Ý# ¼ . Thefollowingdiscussionof this factusesthe -algebrapropertiesdevelopedin Problem1.3.

By definition,everyopeninterval #Þ;)*ßl is in Ý~ ¼ , whereÞ and ß arerealnumbers.SinceÝ~# ¼ isa -algebra,every unionof openintervalsis alsoin Ý# ¼ . For example,for every realnumberÞ ,theopenhalf-line Þ5)É6H »K f #Þ;)*Þn6àis aBorel set,asis PÉb)*Þ:J »K 2 #Þ9à")Þ3lRFor realnumbersÞ and ß , theunion PÉb)*Þ:2±9#ßK)É6is Borel. SinceÝ~ ¼ is a -algebra,every complementof a Borelsetis Borel,so Ý# ¼ contains Þ;)*ßw§¤>PÉb)*Þ:2±9#ßK)É6 ¥ ° RThisshowsthateveryclosedinterval is Borel. In addition,theclosedhalf-lines

Þ;)*É6J »> f Þ;)*ÞPn1à«and ePÉb)*Þ¾ »> f Þp9à")*Þ¾areBorel. Half-openandhalf-closedintervalsarealsoBorel,sincethey canbewritten asintersec-tionsof openhalf-linesandclosedhalf-lines.For example,#Þ;)*ßw5gPÉb)ßw3á9#Þ5)É6lREverysetwhich containsonly onerealnumberis Borel. Indeed,if Þ is a realnumber, thenU>Þ«Z( â»> f 3Þp à )*ÞPn à ® RThis meansthatevery setcontainingfinitely many realnumbersis Borel; if ãU>Þ )Þ G )IRERIR)Þ » Z ,then 0 »^ f U>Þ:^KZ:R

24

In fact,everysetcontainingcountablyinfinitely many numbersis Borel; if bVU>Þ«i)Þ3GE)IRERIRZ , then0 »^ f U>Þ:^KZ:RThis meansthat the set of rational numbersis Borel, as is its complement,the setof irrationalnumbers.

Thereare,however, setswhich arenot Borel. We have just seenthatany non-Borelsetmusthaveuncountablymany points.

Example1.4 (TheCantorset.) Thisexamplegivesa hint of howcomplicateda Borel setcanbe.Weuseit later whenwediscussthesamplespacefor an infinitesequenceof coin tosses.

Considertheunit interval $)E , andremovethemiddlehalf, i.e., removetheopenintervalxä B ) SB2® RTheremainingset å ` $) B ± SB )E hastwo pieces.Fromeach of thesepieces,removethemiddlehalf, i.e., removetheopenset[Gx I½ ) SI½ ® ISI½ ) IæI½ ® RTheremainingset å G $) I½ SI½ ) B SB ) ISI½ IæI½ )EaRhasfour pieces.Continuethis process,soat stage] , theset

å ^ has F ^ pieces,andeach piecehaslength Ë Ö . TheCantorset å x â^ 2 å ^is definedto bethesetof pointsnot removedat anystageof thisnonterminatingprocess.

Notethat thelengthof , thefirst setremoved,isG . The“length” of (G , thesecondsetremoved,

is Ò n Ò Ë . The“length” of thenext setremovedis BÚ cG Ò , andin general, thelengthof the] -th setremovedis F «^ . Thus,thetotal lengthremovedis¢^* f F ^ ¦)andsotheCantorset,thesetof pointsnot removed,haszero “length.”

Despitethefact that theCantorsethasno“length,” thereare lotsof pointsin thisset.In particular,noneof theendpointsof thepiecesof thesets

å ) å G )ERIRIR is ever removed.Thus,thepoints$) B ) SB )E%) E½ ) SI½ ) ISI½ ) IæI½ ) ½KB )IRIRERare all in

å. This is a countablyinfinite setof points. We shall seeeventuallythat theCantorset

hasuncountablymanypoints. ç

CHAPTER1. Introductionto ProbabilityTheory 25

Definition 1.10 Let Ý~# ¼ bethe -algebraof Borel subsetsof ¼ . A measure on # ¼/)wÝ~# ¼ is afunction è mappingÝ into $)É£ with thefollowing properties:

(i) è`#¦J$ ,(ii) If I)*[GI)ERIRIR is asequenceof disjoint setsin Ý~# ¼ , thenè ^* f [^ ¡ ¢^ 2 è`#(^ElRLebesguemeasure is definedto bethemeasureon # ¼/)wÝ~# ¼ which assignsthemeasureof eachinterval to beits length.Following Williams’sbook,wedenoteLebesguemeasureby è , .A measurehasall thepropertiesof aprobabilitymeasuregivenin Problem1.4,exceptthatthetotalmeasureof thespaceis notnecessarily (in fact, è-,3# ¼JÉ ), oneno longerhastheequationè`# ° JP@è`#[in Problem1.4(iii), andproperty(v) in Problem1.4needsto bemodifiedto say:

(v) If I)(GE)IRERIR is a sequenceof setsin Ý~# ¼ with [é0(G[éÚEÚIÚ and è`#*0É , thenè â^* f [^ ¡ ºêìëíy»>î è|P»lRTo seethattheadditionalrequirmentè`#*0É is neededin (v), considera ¦)*É6l)(GJ F)*É6l)Pc` S)*É6O)IRIRERRThen á ^ 2 [^ , so è-,3#á ^ 2 [^KJ$ , but êìëíyo»>î è,3P»3JQÉ .

WespecifythattheLebesguemeasureof eachinterval is its length,andthatdeterminestheLebesguemeasureof all otherBorel sets.For example,theLebesguemeasureof theCantorsetin Example1.4mustbezero,becauseof the“length” computationgivenat theendof thatexample.

TheLebesguemeasureof asetcontainingonly onepointmustbezero.In fact,sinceU>Þ«ZïÄ Þp à )*Þn à ®for every positiveinteger à , we musthave$/Ã6è-,KU>Þ«ZÃ6è-, Þ/ à )*Þ[n à ® Fà RLetting àjðÉ , weobtain è,KUKÞZ($«R

26

The Lebesguemeasureof a setcontainingcountablymany pointsmustalsobe zero. Indeed,ifbVU>Þ )Þ G )IRERIRZ , then è-,3#[J ¢^ f è-,KU>Þ:^KZ~¢^ f $Q$RTheLebesguemeasureof asetcontaininguncountablymany pointscanbeeitherzero,positiveandfinite, or infinite. We maynot computetheLebesguemeasureof anuncountablesetby addingupthe Lebesguemeasureof its individual members,becausethereis no way to addup uncountablymany numbers.Theintegralwasinventedto getaroundthis problem.

In orderto think aboutLebesgueintegrals,wemustfirst considerthefunctionsto beintegrated.

Definition 1.11 Let ñ be a function from ¼ to ¼ . We saythat ñ is Borel-measurable if the setU>Í£¨q ¼ Á ñNÍ5¨Z is in Ý# ¼ whenever L¨9Ý# ¼ . In thelanguageof Section2, we wantthe -algebra generatedby ñ to becontainedin Ý~ ¼ .Definition 3.4 is purely technicalandhasnothingto do with keepingtrack of information. It isdifficult to conceive of a functionwhich is not Borel-measurable,andwe shallpretendsuchfunc-tions don’t exist. Hencefore,“function mapping ¼ to ¼ ” will mean“Borel-measurablefunctionmapping ¼ to ¼ ” and“subsetof ¼ ” will mean“Borel subsetof ¼ ”.

Definition 1.12 An indicator function ò from ¼ to ¼ is a functionwhich takesonly thevalues$and . We call xVU>ÍY¨ ¼ Á òH#Í;H¾Zthesetindicatedby ò . We definetheLebesgueintegral of ò to beó:ô õ òX¦è-, xCè,3(lRA simplefunction ö from ¼ to ¼ is a linearcombinationof indicators,i.e.,a functionof theformö"#Í5J »¢^* f÷ ^iò3^3#Í;l)whereeachò3^ is of theform ò3^3#Í;Jg² %) if ÍM¨[^:)$) if ÍD¨[^:)andeach÷ ^ is a realnumber. WedefinetheLebesgueintegral of ö to beó õ ö[%è-,x »¢^ 2÷ ^ ó ô õ ò3^E%è-,( »¢^ f÷ ^Oè,3(^ElRLet ñ be a nonnegative function definedon ¼ , possiblytaking the value É at somepoints. WedefinetheLebesgueintegral of ñ to beó%ô õ ñ%è-,xbø*ùúpû ó%ô õ ö[¦è, Á ö is simpleand öHÍ5Ã0ñJ#Í; for every ͨM ¼üR

CHAPTER1. Introductionto ProbabilityTheory 27

It is possiblethatthis integral is infinite. If it is finite, we saythat ñ is integrable.

Finally, let ñ bea functiondefinedon ¼ , possiblytakingthevalue É atsomepointsandthevaluePÉ atotherpoints.We definethepositiveandnegativepartsof ñ to beñ v #Í;PxyzKUKñNÍ5l)$:Z3)ñ #Í;PxyzK;U3PñJ#Í5O)*$:Z3)respectively, andwedefinetheLebesgueintegral of ñ to beó ô õ ñ(¦è-,ïx ó ô õ ñ v ¦è,0 ó ô õ ñ %è-,K)providedtheright-handsideis notof theform ÉýMÉ . If both þ ô õ ñ v %è-, and þ ô õ ñ %è-, arefinite(or equivalently, þ ô õÿ ñ ÿ ¦è,[0É , since

ÿ ñ ÿ ñ v n6ñ ), wesaythat ñ is integrable.

Let ñ beafunctiondefinedon ¼ , possiblytakingthevalue É atsomepointsandthevalue PÉ atotherpoints.Let bea subsetof ¼ . Wedefineó ¬ ñ[¦è , x ó ô õ ¬ ñ¦è , )where ¬ Í5Pxg² %) if ÍM¨p)$) if ÍD¨p)is the indicator functionof .

TheLebesgueintegral just definedis relatedto theRiemannintegral in onevery importantway: iftheRiemannintegral þ PñJ#Í5:Í is defined,thentheLebesgueintegral þ ñ[¦è, agreeswith theRiemannintegral. TheLebesgueintegralhastwo importantadvantagesover theRiemannintegral.The first is that the Lebesgueintegral is definedfor morefunctions,aswe show in the followingexamples.

Example1.5 Let bethesetof rationalnumbersin $«)I , andconsiderñWx . Beingacountableset, hasLebesguemeasurezero,andsotheLebesgueintegralof ñ over $)I isó , ñ¦è-,XQ$RTo computethe Riemannintegral þ , ñJ#Í5w3Í , we choosepartition points $8Í,M7Í-8ÚEÚIÚJÍ»b anddivide the interval $)E into subintervals Í,K)*Í4Â) Í4*)*Í;G)ERIRER) Í»¦-I)*Í»E . In eachsubinterval Í5^O-I)*Í5^i thereis a rationalpoint ^ , where ñN ^I[ , andthereis alsoan irrationalpoint ^ , where ñJ# ^ h$ . We approximatetheRiemannintegral from above by theuppersum»¢^* f ñJ ^ IÍ ^ qÍ ^l- h »¢^* f aÚ:#Í ^ qÍ ^O- J%)andwealsoapproximateit from below by the lowersum»¢^* f ñJ#E^IIÍ5^P9Í;^l-*h »¢^* f $(Ú:#Í5^qÍ5^O-*J$R

28

No matterhow fine we takethepartitionof $)I , theuppersumis always andthelower sumisalways $ . Sincethesetwo do not converge to a commonvalueasthepartitionbecomesfiner, theRiemannintegral is notdefined. çExample1.6 ConsiderthefunctionñJ#Í5x ² Éb) if ÍQ$)$) if Í Q$RThis is not a simple function becausesimple function cannottake the value É . Every simplefunctionwhich lies between$ and ñ is of theformö"#Í5[xg² ) if Í<$)$) if Í $)for some ¨ $)*É6 , andthushasLebesgueintegraló ô õ ö[%è-,P è-,KU>$:Z($RIt followstható ô õ ñ%è-,Pbø*ùú û ó ô õ ö[%è-, Á ö is simpleand öH#Í;Ã0ñJ#Í5 for every ͨ ¼ ü $«RNow considerthe Riemannintegral þ ñJ#Í;5:Í , which for this function ñ is the sameas the

Riemannintegral þ - ñJ#Í5;3Í . Whenwepartition ¦)I into subintervals,oneof thesewill contain

the point $ , andwhenwe computethe upperapproximatingsumfor þ - ñJ#Í5;3Í , this point willcontribute É timesthelengthof thesubintervalcontainingit. ThustheupperapproximatingsumisÉ . On theotherhand,thelowerapproximatingsumis $ , andagaintheRiemannintegraldoesnotexist. çTheLebesgueintegralhasall linearity andcomparisonpropertiesonewouldexpectof anintegral.In particular, for any two functions ñ and ò andany realconstant÷ ,ó%ô õ #ñ/n£ò55¦è-,µ ó¦ô õ ñ(¦è-,`n ó%ô õ òP%è-,%)ó ô õ ÷ ñ%è , ÷ ó ô õ ñ%è , )andwhenever ñJ#Í;ÃòfÍ5 for all ͨ ¼ , wehaveó%ô õ ñ¦è-,~à ó%ô õ ò5a¦è-,IRFinally, if and aredisjoint sets,thenó ¬ ñ¦è-,X ó ¬ ñ¦è-,`n ó ñ¦è,%R

CHAPTER1. Introductionto ProbabilityTheory 29

Therearethreeconvergencetheoremssatisfiedby the Lebesgueintegral. In eachof thesethe sit-uationis that thereis a sequenceof functions ñ » )*࣠¦)*F)ERIRlR converging pointwiseto a limitingfunction ñ . Pointwiseconvergencejustmeansthatê ëíy»>î ñ » Í5JñJ#Í; for every ͨM ¼/RThereareno suchtheoremsfor the Riemannintegral, becausethe Riemannintegral of the limit-ing function ñ is too oftennot defined. Beforewe statethe theorems,we giventwo examplesofpointwiseconvergencewhicharisein probabilitytheory.

Example1.7 Considera sequenceof normaldensities,eachwith variance andthe à -th havingmeanà : ñE»#Í;Px F ! #"

ÈÈ RTheseconvergepointwiseto thefunctionñJ#Í5J$ for every ÍM¨ ¼/RWe have þ ô õ ñI»:%è-,( for every à , so ê ëíy<»>î þ ô õ ñE»%è-,P , but þ ô õ ñ(¦è-,($ . çExample1.8 Considerasequenceof normaldensities,eachwith mean$ andthe à -th having vari-ance » : ñ » #Í5Px $ àF

ÈÈ RTheseconvergepointwiseto thefunctionñJ#Í5x² Éb) if ÍQ$)$) if Í Q$RWe have again þ ô õ ñE»%è-,@ for every à , so êìëíyo»>î þ ô õ ñE»%è-, , but þ ô õ ñ¦è,@ý$ . Thefunction ñ is nottheDiracdelta;theLebesgueintegralof this functionwasalreadyseenin Example1.6to bezero. çTheorem 3.1 (Fatou’s Lemma)Let ñE»-)*à@%)*F«)IRIRlR bea sequenceof nonnegativefunctionscon-verging pointwiseto a function ñ . Thenó ô õ ñ%è-,Ã6ê ëíy6ë&%'»>î ó ô õ ñE»a¦è,%RIf ê ë yo»>î þ ô õ ñI»%è-, is defined,thenFatou’sLemmahasthesimplerconclusionó%ô õ ñ%è-,Ãêìëíy»>î ó3ô õ ñE»a¦è-,%RThis is thecasein Examples1.7and1.8,whereê ë y»>î ó%ô õ ñE»a¦è-,P%)

30

while þ ô õ ñ¦è-,ï$ . We couldmodify eitherExample1.7 or 1.8 by setting ò¾»jgñE» if à is even,but ò » F%ñ » if à is odd. Now þ ô õ ò » %è , ä if à is even,but þ ô õ ò » ¦è , 7F if à is odd. ThesequenceU>þ ô õ ò%»a¦è-,KZ »> f hastwo clusterpoints, and F . By definition, the smallerone, , isê ëíy6ë&%'i»Kî þ ô õ ò%»a¦è-, andthelargerone, F , is êìëíyø*ùú »>î þ ô õ ò%»a¦è, . Fatou’sLemmaguaranteesthateventhesmallerclusterpointwill begreaterthanor equalto theintegralof thelimiting function.

Thekey assumptionin Fatou’sLemmais thatall thefunctionstakeonlynonnegativevalues.Fatou’sLemmadoesnotassumemuchbut it is is not verysatisfyingbecauseit doesnotconcludetható ô õ ñ%è-,Pºêìëíy»>î ó ô õ ñE»a¦è-,%RTherearetwo setsof assumptionswhich permitthisstrongerconclusion.

Theorem 3.2 (MonotoneConvergenceTheorem)Let ñE»5)*à@ %)*F)ERIRER bea sequenceof functionsconvergingpointwiseto a function ñ . Assumethat$/Ã1ñ%>Í5Ã0ñKG%#Í;Ã0ñEc3#Í5ÃÚEÚIÚ for every Íj¨ ¼/RThen ó%ô õ ñ%è-,Pºêìëíy»>î ó3ô õ ñE»a¦è-,%)where bothsidesareallowedto be É .

Theorem 3.3 (DominatedConvergenceTheorem)Let ñE»5)àã%)*F)ERIRER bea sequenceof functions,which maytakeeitherpositiveor negativevalues,converging pointwiseto a function ñ . Assumethat there is a nonnegativeintegrablefunction ò (i.e., þ ô õ òP%è-,0É ) such thatÿ ñE»#Í5 ÿ ÃòfÍ5 for every ÍM¨ ¼ for every à"RThen ó%ô õ ñ%è-,Pºêìëíy»>î ó3ô õ ñE»a¦è-,%)andbothsideswill befinite.

1.4 GeneralProbability Spaces

Definition 1.13 A probabilityspace T )) consistsof threeobjects:

(i)T

, a nonemptyset, called the samplespace, which containsall possibleoutcomesof somerandomexperiment;

(ii) , a -algebraof subsetsofT

;

(iii) , aprobabilitymeasureon T )< , i.e.,afunctionwhichassignsto eachset ¨j anumber #[¨ $«)I , which representstheprobabilitythat theoutcomeof therandomexperimentlies in theset .

CHAPTER1. Introductionto ProbabilityTheory 31

Remark 1.1 WerecallfromHomeworkProblem1.4thataprobabilitymeasure hasthefollowingproperties:

(a) #%J$ .(b) (Countableadditivity) If )* G )ERIRER is asequenceof disjoint setsin , then gY^* f [^l¡b¢^ 2 #[^KlR(c) (Finiteadditivity) If à is a positiveintegerand I)IRERIR)P» aredisjoint setsin , then # ±£ÚIÚEÚ*±j » J # -nÚIÚEÚ*n6 » lR(d) If and aresetsin and Ä( , then ) (2n1 )+*P[lR

In particular, )r0 #[lR(d) (Continuityfrom below.) If I)*[GI)ERIRER is asequenceof setsin with PÄ0[G(ÄQÚIÚIÚ , then ^* f [^ ¡ ºêìëíy»>î #»5lR(d) (Continuityfrom above.) If )* G )ERIRER is a sequenceof setsin with é0 G éÚIÚEÚ , then g â^* f [^l¡bºêìëíy»>î #»5lRWe have alreadyseensomeexamplesof finite probabilityspaces.We repeattheseandgive someexamplesof infinite probabilityspacesaswell.

Example1.9 Finitecoin tossspace.Tossa coin à times,so that

Tis the setof all sequencesof ? and A which have à components.

We will usethis spacequitea bit, andsogive it a name:T » . Let bethecollectionof all subsets

ofT » . Supposetheprobabilityof ? on eachtossis , a numberbetweenzeroandone. Thenthe

probabilityof A is xãa . For each\£d\`I)\JGI)ERIRIRw)\H»3 inT » , wedefine pUl\PZïx -, =/. )0)13254 ·6 » © Ú 7, =/. )0)18294 ¹6 » © R

For eachV¨j , wedefine #[ x ¢©«ª>¬ pUl\PZ3R (4.1)

Wecandefine #[ thiswaybecause hasonly finitely many elements,andsoonly finitely manytermsappearin thesumontheright-handsideof (4.1). ç

32

Example1.10 Infinite coin tossspace.Tossa coin repeatedlywithout stopping,sothat

Tis thesetof all nonterminatingsequencesof ?

and A . We call thisspaceT . This is anuncountablyinfinite space,andwe needto exercisesome

carein theconstructionof the -algebrawewill usehere.

For eachpositive integer à , we defineP» to bethe -algebradeterminedby thefirst à tosses.Forexample,[G containsfour basicsets,·a· x Ul\qg\`i)e\NGK)\"c>)ERIRIR Á \`J?M)\NG?£Z Thesetof all sequenceswhich begin with ?W?M)·¹ x Ul\qg\`i)e\NGK)\"c>)ERIRIR Á \`J?M)\NGbAZ Thesetof all sequenceswhich begin with ?A[)¹5· x Ul\qg\`i)e\NGK)\"c>)ERIRIR Á \`JbA()e\NG`Q?9Z Thesetof all sequenceswhich begin with A(?)P¹;¹ x Ul\qg\`i)e\NGK)\"c>)ERIRIR Á \`JbA()e\NG`CAZ Thesetof all sequenceswhich begin with APA(RBecause(G is a -algebra,we mustalsoput into it thesets , T , andall unionsof the four basicsets.

In the -algebra , we put every set in every -algebra » , where à rangesover the positiveintegers.We alsoput in every othersetwhich is requiredto make bea -algebra.For example,thesetcontainingthesinglesequenceUK?W?@?@?@?VÚIÚIÚeZ~VU>? onevery tossZis not in any of the » -algebras,becauseit dependson all thecomponentsof thesequenceandnot just thefirst à components.However, for eachpositiveinteger à , thesetU>? on thefirst à tossesZis in P» andhencein . Therefore,U>? onevery tossZ â»> f UK? onthefirst à tossesZis alsoin .

We next constructthe probability measure on T )< which correspondsto probability ¨ $)E for ? andprobability ( for A . Let L¨9 begiven. If thereis a positive integer àsuchthat Q¨jP» , thenthedescriptionof dependsononly thefirst à tosses,andit is clearhow todefine #[ . For example,supposeb ·· ±/ ¹;· , wherethesesetsweredefinedearlier. Then is in (G . We set #·a·` G and #¹5·J , andthenwehave (h #P··6±¹5·(J G n g n RIn otherwords,theprobabilityof a ? on thesecondtossis .

CHAPTER1. Introductionto ProbabilityTheory 33

Let usnow considera set ¨q for which thereis no positive integer à suchthat L¨ . Suchis thecasefor theset UK? onevery tossZ . To determinetheprobabilityof thesesets,we write themin termsof setswhich arein P» for positive integers à , andthenusethepropertiesof probabilitymeasureslistedin Remark1.1. For example,UK? on thefirst tossZ é U>? on thefirst two tossesZé U>? on thefirst threetossesZé ÚIÚIÚ;)and â»K f U>? on thefirst à tossesZVU>? onevery tossZ3RAccordingto Remark1.1(d)(continuityfrom above), pUK? onevery tossZ(ê ëíy»Kî pUK? on thefirst à tossesZ(ºê ëíy»>î » RIf , then pU>? onevery tossZ( ; otherwise, pU>? onevery tossZ($ .A similarargumentshowsthatif $/ sothat $/ , theneverysetin

T whichcontainsonly oneelement(nonterminatingsequenceof ? and A ) hasprobabilityzero,andhencevery setwhich containscountablymany elementsalsohasprobabiliyzero.We arein a casevery similar toLebesguemeasure:every point hasmeasurezero,but setscanhave positive measure.Of course,theonly setswhich canhave positiveprobabiltyin

T arethosewhich containuncountablymanyelements.

In theinfinite coin tossspace,wedefineasequenceof randomvariables&2I)w&GE)IRIRER by&-^3d\ax² if \ ^ ?)$ if \N^[bA()andwealsodefinetherandomvariable d\a" »¢^ 2 &^:d\aF ^ RSinceeach&-^ is eitherzeroor one,

takesvaluesin theinterval $)Ii . Indeed,

APAPAPA@ÚIÚEÚJ$ , #?@?@?W?QÚIÚEÚ@º and the other valuesof

lie in between. We definea “dyadic rationalnumber”to bea numberof the form

.G Ö , where ] and : areintegers. For example, cË is a dyadicrational.Every dyadicrationalin (0,1)correspondsto two sequences\¨ T . For example, #?@?AAPAPAPAÚEÚIÚJ #?MA(?@?@?W?M?ÚEÚIÚJ SB RThenumbersin (0,1)whicharenotdyadicrationalscorrespondto asingle \0¨ T ; thesenumbershave auniquebinaryexpansion.

34

Wheneverweplacea probabilitymeasure on T ) , wehaveacorrespondinginducedmeasureÅ Æ

on $«)I . For example,if weset G in theconstructionof thisexample,thenwe haveÅhÆ $«) F ïQ pU First tossis AZ( F )ÅhÆ F )I~Q pU First tossis ?9Z( F )ÅhÆ $«) B ïQ pU First two tossesare AAZ( B )ÅhÆ B ) F Q pU First two tossesare A[?9Z( B )Å Æ F ) SB Q pU First two tossesare ?MAZ( B )ÅhÆ SB )I~Q pU First two tossesare ?@?£Z( B RContinuingthisprocess,wecanverify thatfor any positiveintegers] and : satisfying$/à :L0F ^ :F ^ æ)wehave Å`Æ :L1F ^ ) :F ^ F ^ RIn otherwords,the

Å`Æ-measureof all intervalsin $)E whoseendpointsaredyadicrationalsis the

sameastheLebesguemeasureof theseintervals.Theonly waythiscanbeis for

ÅhÆto beLebesgue

measure.

It is interesingto considerwhat

Å Æwould look like if we takea valueof otherthan G whenwe

constructtheprobabilitymeasure onT

.

We concludethis examplewith anotherlook at theCantorsetof Example3.2. LetT<; 6 1>= be the

subsetofT

in which every even-numberedtossis thesameastheodd-numberedtossimmediatelyprecedingit. For example,?W?MAPAAPA(?@? is thebeginningof asequencein

T?; 6 1>= , but ?MA is not.Considernow thesetof realnumberså ! xVU \a Á \q¨ T?; 6 1>= Z3RThe numbersbetween Ë ) G canbewritten as

d\a , but the sequence\ mustbegin with eitherA(? or ?MA . Therefore,noneof thesenumbersis in

å ! . Similarly, thenumbersbetween A@ ) cA@ canbewritten as

d\a , but thesequence\ mustbegin with APAPA[? or APA(?MA , sononeof thesenumbersis in

å ! . Continuingthisprocess,weseethat

å ! will notcontainany of thenumberswhichwereremoved in the constructionof the Cantorset

åin Example3.2. In otherwords,

å ! Ä å .With a bit morework, onecanconvinceonselfthat in fact

å ! å , i.e., by requiringconsecutivecoin tossesto bepaired,we areremoving exactly thosepointsin $«)I which wereremovedin theCantorsetconstructionof Example3.2. ç

CHAPTER1. Introductionto ProbabilityTheory 35

In additionto tossinga coin, anothercommonrandomexperimentis to pick a number, perhapsusinga randomnumbergenerator. Herearesomeprobabilityspaceswhich correspondto differentwaysof pickinga numberat random.

Example1.11Supposewe choosea numberfrom ¼ in sucha way that we are sureto get either , B or I½ .Furthermore,weconstructtheexperimentsothattheprobabilityof getting is

ËÊ , theprobabilityofgetting B is

ËÊ andtheprobabilityof getting I½ is Ê . We describethis randomexperimentby takingTto be ¼ , to be Ý# ¼ , andsettingup theprobabilitymeasuresothat pU3KZ B Û )( pUIB«Z( B Û )P pU3E½:Z~ Û R

This determines #[ for every set ¨@Ý~ ¼ . For example,theprobabilityof theinterval #$)*æ>isÒÊ , becausethis interval containsthenumbers and B , but not thenumberI½ .

Theprobabilitymeasuredescribedin this exampleis

Å ÇOÈ, themeasureinducedby thestockprice+2G , whentheinitial stockprice +4,XCB andtheprobabilityof ? is c . Thisdistributionwasdiscussed

immediatelyfollowing Definition2.8. çExample1.12 Uniform distributionon $)E .Let

T $)I andlet §Ý~ $)Ii , thecollectionof all Borel subsetscontaininedin $)Ii . ForeachBorelset VÄ $«)I ,wedefine (hbè-,#[ tobetheLebesguemeasureof theset.Becauseè , $)E«ã , thisgivesusa probabilitymeasure.

This probabilityspacecorrespondsto therandomexperimentof choosinga numberfrom $)E sothateverynumberis “equallylikely” to bechosen.Sincethereareinfinitely meannumbersin $«)I ,thisrequiresthateverynumberhaveprobabiltyzeroof beingchosen.Nonetheless,wecanspeakoftheprobabilitythat thenumberchosenlies in a particularset,andif thesethasuncountablymanypoints,thenthis probabilitycanbepositive. çI know of no way to designa physicalexperimentwhich correspondsto choosinga numberatrandomfrom $«)I so thateachnumberis equallylikely to bechosen,just asI know of no way totossa coin infinitely many times. Nonetheless,bothExamples1.10and1.12provide probabilityspaceswhichareoftenusefulapproximationsto reality.

Example1.13 Standardnormaldistribution.Definethestandardnormaldensity

P#Í5x FB Í GF RLet

T ¼ , gCÝ~# ¼ andfor everyBorel set VÄ0 ¼ , define ([x ó ¬ o%è-,KR (4.2)

36

If in (4.2)is aninterval Þ;)*ßw , thenwecanwrite (4.2)asthelessmysteriousRiemannintegral:

Þ;)*ßwNx ó F Í GF 3ÍfRThiscorrespondsto choosingapointat randomontherealline,andeverysinglepointhasprobabil-ity zeroof beingchosen,but if a set is given,thentheprobabilitythepoint is in thatsetis givenby (4.2). çThe constructionof the integral in a generalprobabilityspacefollows the samestepsasthe con-structionof Lebesgueintegral. We repeatthisconstructionbelow.

Definition 1.14 Let T )) beaprobabilityspace,andlet

bearandomvariableonthisspace,i.e.,a mappingfrom

Tto ¼ , possiblyalsotakingthevaluesCÉ .D If

is an indicator, i.e, d\a" ¬ d\aJ ² if \ ¨M)$ if \ ¨M(°)

for someset V¨j , wedefine ó Ô : gx #(ORD If

is asimplefunction, i.e, \aJ »¢^* f ÷ ^ ¬ Ö \al)whereeach÷ ^ is a realnumberandeach[^ is a setin , we defineó Ô : Lx »¢^* f ÷ ^ ó Ô ¬ Ö 3 »¢^ 2 ÷ ^I (^KlRD If

is nonnegativebut otherwisegeneral,we defineó Ô 3 x ø*ùú û ó Ô &6: Á & is simpleand &d\aà \a for every \0¨ T ü RIn fact,we canalwaysconstructasequenceof simplefunctions&5»5)àj%)*F«)IRIRlR suchthat$oÃ6&2>d\aÃ&G%d\aÃ6&;c3d\aÃRERIR for every \ ¨ T )and &jd\aJbê ëíy»Kî &;»4d\a for every \ ¨ T . With thissequence,wecandefineó Ô : x êìëíy»>î ó Ô &5»3 R

CHAPTER1. Introductionto ProbabilityTheory 37D If

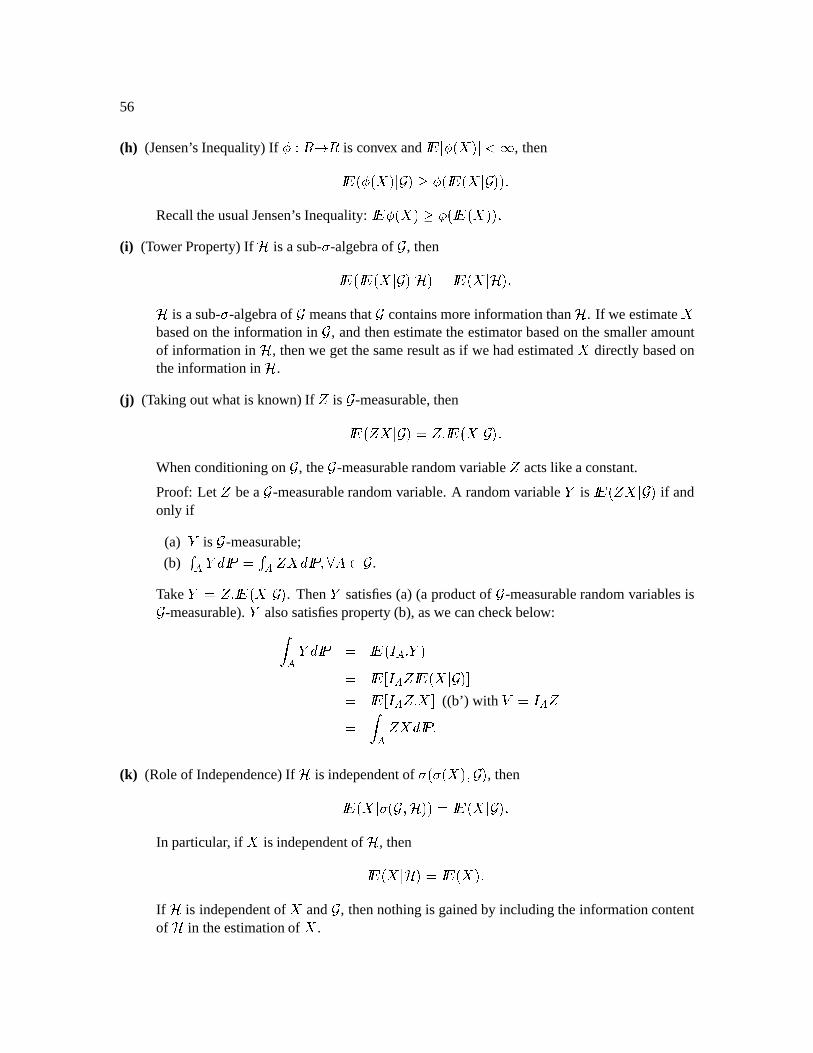

is integrable, i.e, ó Ô v 3 ã0Éb) ó Ô : 0Éb)where v d\aPxyozKU d\al)$:Z3) \aPxyzK;U3 d\al)$:Z3)thenwe define ó Ô 3 x ó Ô v 3 b1 ó Ô : R

If is asetin and

is a randomvariable,we defineó ¬ 3 x ó Ô ¬ Ú 3 RTheexpectationof a randomvariable

is definedto be Ó x ó Ô 3 R

Theabove integral hasall thelinearity andcomparisonpropertiesonewould expect. In particular,if

and & arerandomvariablesand ÷ is a realconstant,thenó Ô n&;3 ó Ô : 6n ó Ô &_: )ó Ô ÷ : ÷ ó Ô :)If d\a`Ã&d\a for every \0¨ T , thenó Ô : Ã ó Ô &_: R

In fact,wedon’t needto have d\a`Ã&d\a for every \¨ T in orderto reachthisconclusion;it is

enoughif thesetof \ for which d\aPÃQ&d\a hasprobabilityone.Whena conditionholdswith

probabilityone,we sayit holdsalmostsurely. Finally, if and aredisjoint subsetsofT

and

is a randomvariable,then ó ¬E : ó ¬ 3 1n ó 3 RWe restatetheLebesgueintegral convergencetheoremin this moregeneralcontext. We acknowl-edgein thesestatementsthatconditionsdon’t needto hold for every \ ; almostsurelyis enough.

Theorem 4.4 (Fatou’s Lemma)Let »5)àW%)F)IRERlR bea sequenceof almostsurely nonnegative

randomvariablesconvergingalmostsurelyto a randomvariable

. Thenó Ô 3 Ã6ê ëíy6ë&%'»>î ó Ô » : )or equivalently, Ó Ã6ê ë yë&%'»>î Ó »5R

38

Theorem 4.5 (MonotoneConvergenceTheorem)Let »;)*à ¦)*F)ERIRlR bea sequenceof random

variablesconvergingalmostsurely to a randomvariable

. Assumethat$/à Xà G[à cÃÚIÚEÚ almostsurelyRThen ó Ô 3 ºê ëíy»Kî ó Ô »:3 )or equivalently, Ó êìëíy»>î Ó »5RTheorem 4.6 (DominatedConvergenceTheorem)Let

»;)*à@L%)*F«)IRIRlR bea sequenceof randomvariables,converging almostsurely to a randomvariable

. Assumethat there existsa random

variable & such that ÿ » ÿ Ã6& almostsurelyfor every à"RThen ó Ô 3 Qµê ëíy»>î ó Ô »`: )or equivalently, Ó êìëíy»>î Ó »5RIn Example1.13,we constructeda probabilitymeasureon # ¼/)Ý~ ¼ by integratingthestandardnormaldensity. In fact,whenever isanonnegativefunctiondefinedon ¼ satisfyingþ ô õ ¦è,P ,wecall a densityandwe candefineanassociatedprobabilitymeasureby #[[x ó ¬ ¦è-, for every Q¨jÝ~# ¼lR (4.3)

We shalloftenhave a situationin which two measurearerelatedby anequationlike (4.3). In fact,themarketmeasureandtherisk-neutralmeasuresin financialmarketsarerelatedthisway. We saythat in (4.3) is theRadon-Nikodymderivativeof : with respectto è-, , andwewrite 9 : ¦è-, R (4.4)

Theprobabilitymeasure weightsdifferentpartsof therealline accordingto thedensity . Nowsupposeñ is a functionon #¼/)Ý# ¼l) . Definition1.14givesusa valuefor theabstractintegraló%ô õ ñ: RWe canalsoevaluate ó ô õ ñ o%è-,K)which is anintegralwith respecto Lebesguemeasureover therealline. We wantto show tható%ô õ ñ: ó¦ô õ ñ- %è-,K) (4.5)

CHAPTER1. Introductionto ProbabilityTheory 39

anequationwhich is suggestedby thenotationintroducedin (4.4)(substituteF ô GF>HI for in (4.5)and“cancel” the ¦è , ). We includea proof of this becauseit allows us to illustratethe conceptof thestandard machineexplainedin Williams’sbookin Section5.12,page5.

Thestandardmachineargumentproceedsin four steps.

Step1. Assumethat ñ is an indicator function, i.e., ñNÍ5P ¬ Í5 for someBorel set Ä ¼ . Inthatcase,(4.5)becomes #[` ó ¬ ¦è-,>RThis is truebecauseit is thedefinitionof #[ .

Step2. Now that we know that (4.5) holdswhen ñ is an indicator function, assumethat ñ is asimplefunction, i.e.,a linearcombinationof indicatorfunctions.In otherwords,ñJ#Í5J »¢^* f ÷ ^Eö5^#Í;l)whereeach÷ ^ is a realnumberandeachö;^ is anindicatorfunction.Thenó ô õ ñ3 ó ô õKJ »¢^ 2÷ ^Iö;^LW: »¢^ 2 ÷ ^ ó%ô õ ö;^H: »¢^ 2 ÷ ^ ó ô õ ö;^K %è-, ó ô õ J »¢^ 2÷ ^Iö;^ L ¦è, ó ô õ ñ- ¦è-,>R

Step3. Now that we know that (4.5) holdswhen ñ is a simple function, we considera generalnonnegativefunction ñ . Wecanalwaysconstructasequenceof nonnegativesimplefunctionsñ » )*à<%)*F«)IRIRER suchthat$Ã6ñ¦>#Í5Ã1ñ>G%Í5Ã0ñEc3#Í;ÃRIRER for every ͨ ¼/)and ñJ#Í;Jbê ëíy»Kî ñI»2#Í; for every Íj¨M ¼ . We havealreadyprovedtható:ô õ ñE»3 V ó%ô õ ñE» %è-, for every à"RWelet àjðÉ andusetheMonotoneConvergenceTheoremonbothsidesof thisequalitytoget ó¦ô õ ñ: ó%ô õ ñ- ¦è,KR

40

Step4. In the last step,we consideran integrable function ñ , which cantakeboth positive andnegativevalues.By integrable, we meantható%ô õ ñ v 3 ã0Éb) ó%ô õ ñ : 0ÉbR¿FromStep3, we have ó ô õ ñ v 3 ó ô õ ñ v ¦è,K)ó ô õ ñ 3 ó ô õ ñ ¦è,KRSubtractingthesetwo equations,we obtainthedesiredresult:ó ô õ ñ: ó ô õ ñ-v3 b ó ô õ ñ : ó%ô õ ñ v %è-, ó%ô õ ñ ¦è-, óKõ ñ- ¦è-,%R

1.5 Independence

In this section,we defineanddiscussthe notion of independencein a generalprobability space T )w)* , althoughmostof theexampleswegivewill befor coin tossspace.

1.5.1 Independenceof sets

Definition 1.15 Wesaythattwo sets¨j and g¨Y areindependentif 6áMh #[ NlRSupposea randomexperimentis conducted,and \ is theoutcome.Theprobability that \¸¨6 is #[ . Supposeyou arenot told \ , but you aretold that \¨O . Conditionalon this information,theprobabilitythat \ ¨ is # ÿ [x #6áBp )p RThesets and areindependentif andonly if this conditionalprobability is theuncondidtionalprobability #[ , i.e.,knowing that \C¨ doesnot changetheprobabilityyou assignto . Thisdiscussionis symmetricwith respectto and ; if and areindependentandyou know that\ ¨j , theconditionalprobabilityyou assignto is still theunconditionalprobability ) .Whethertwo setsareindependentdependsontheprobabilitymeasure . For example,supposewetossa coin twice, with probability for ? andprobability LP for A on eachtoss.To avoidtrivialities,weassumethat $/ . Then pU>?@?£Z( G )P pU>?MAZ( pUIA[?9Z 5 )P pUIAAZ~ G R (5.1)

CHAPTER1. Introductionto ProbabilityTheory 41

Let bVUK?W?M)*?MAZ and VUK?A[)A(?£Z . In words, is theset“ ? on thefirst toss”and is theset“one ? andone A .” Then áMVVU>?MAZ . We compute #(h G n 5 ) )F ; ) #(w )F G ) #6áBh 5 RThesesetsareindependentif andonly if F G 5 , which is thecaseif andonly if G .If G , then ) , theprobabilityof oneheadandonetail, is G . If you aretold that the cointossesresultedin a headon thefirst toss,theprobabilityof , which is now theprobabilityof a Aon thesecondtoss,is still G .Supposehowever that $«R $ . By far themostlikely outcomeof thetwo coin tossesis APA , andtheprobabilityof oneheadandonetail is quitesmall; in fact, )pL$R $ Û Ü . However, if youaretold thatthefirst tossresultedin ? , it becomesvery likely thatthetwo tossesresultin oneheadandonetail. In fact,conditionedon gettinga ? on thefirst toss,theprobabilityof one ? andoneA is theprobabilityof a A on thesecondtoss,which is $R Û%Û .1.5.2 Independenceof P -algebras

Definition 1.16 Let ¯ andQ besub- -algebrasof . Wesaythat ¯ andQ areindependentif everysetin ¯ is independentof every setin Q , i.e, #6áRh #[ )p for every V¨BQM)S¨¯RExample1.14 Tossa coin twice, and let be given by (5.1). Let ¯ be the -algebradeterminedby thefirst toss: ¯ containsthesets) T )OU>?@?)?MA[Z3)UIA[?)APAZ3RLet Q bethe -albegradeterminedby thesecondtoss: Q containsthesets) T )OU>?@?)A[?@Z3)U>?MAP)APAZ3RThesetwo -algebrasareindependent.For example,if we choosetheset U>?@?M)*?MAZ from ¯ andtheset U>?@?)wA(?£Z from Q , thenwe have pU>?@?M)*?MAZ> pUK?W?M)A[?9Z`g G n 5 I G n 5 J G ) ¤ UK?W?M)*?MAZHá U>?@?)wA(?£Z ¥ pU>?@?£Z( G RNo matterwhichsetwechoosein ¯ andwhichsetwechoosein Q , wewill find thattheproductoftheprobabiltiesis theprobabilityof theintersection.

42