Embed Size (px)

Citation preview

STATUTORY BANK BRANCH

AUDIT – STEP BY STEP

APPROACH

PRESENTED BY:

CA. JASMINDER SINGH

INDEX

� Pre Audit Work

� Preliminary for Audit

� Scope of AuditScope of Audit

� Day-Wise Schedule

� Various MOCs

� LFAR & MAIN REPORT

� TAX AUDIT REPORT

� GHOSH & JILANI COMMITTEE

PRE- AUDIT WORK

� Know-How of the Branch

� Deposit Oriented or Advance Oriented

� Composition of Advances� Composition of Advances

� Go in for a Pre-Audit Visit, if possible

� Going through LFAR

� Ghosh & Jilani Committee Recommendations

PRELIMINARY FOR AUDIT

� No. of Team Members

� Well Balanced Team

� Allocation of WorkAllocation of Work

� Time Bound Working

� Confirm from branch whether required set of documents that form part of report are available

SCOPE OF AUDIT

� Scrutiny of Balance Sheet

� Checking of NPA Accounts

� Checking of Large Borrowal Accounts

� FOREX (If Applicable)

LFAR� LFAR

� Ghosh & Jilani Committee

� Statutory Compliances

� Provisioning

� Reconciliation of Other Banks’ Account

� General Checking

� Classification of Advances

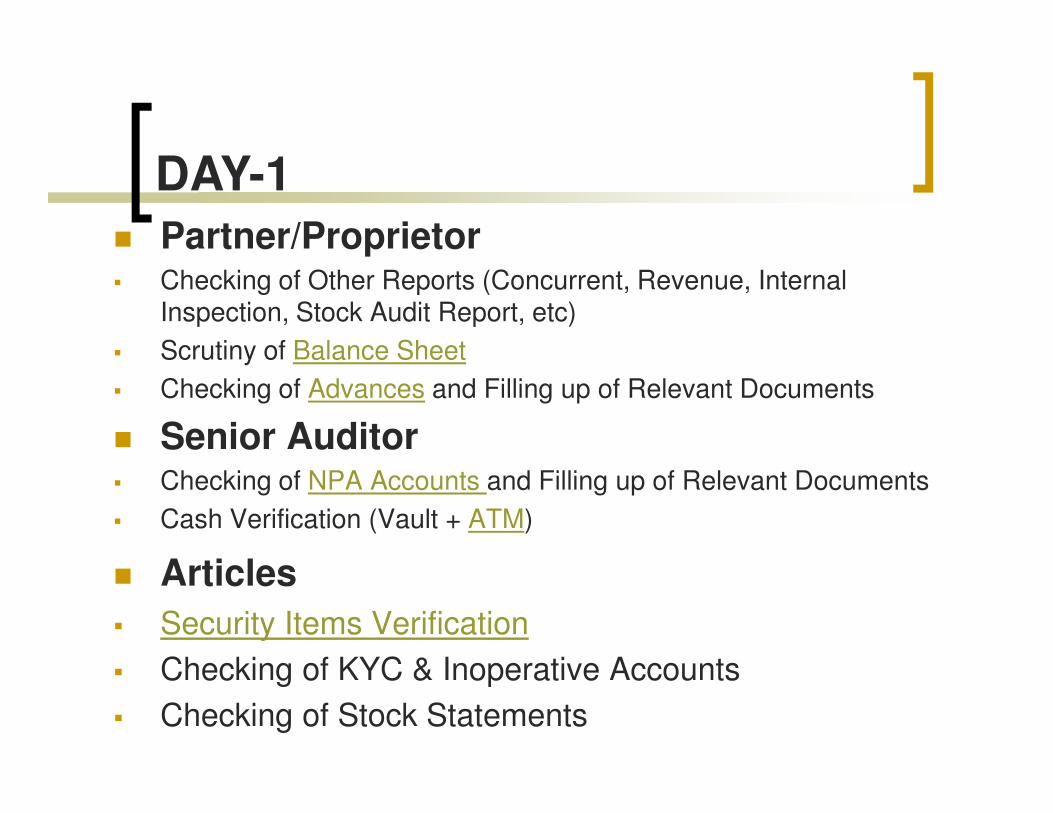

DAY-1

� Partner/Proprietor� Checking of Other Reports (Concurrent, Revenue, Internal

Inspection, Stock Audit Report, etc)

� Scrutiny of Balance Sheet

� Checking of Advances and Filling up of Relevant Documents

� Senior Auditor� Checking of NPA Accounts and Filling up of Relevant Documents

� Cash Verification (Vault + ATM)

� Articles

� Security Items Verification

� Checking of KYC & Inoperative Accounts

� Checking of Stock Statements

DAY-2/3� Partner/Proprietor� Checking of LC/BG & FOREX

� Asset Classification

� Senior Auditor � Checking of Depreciation & Provisions� Checking of Depreciation & Provisions

� Long Outstanding Entries

� Reconciliation of Other Bank’s Accounts

� Articles � Checking of Statutory Compliances & Filling up of Tax Audit

Report in Consultancy with Senior Auditor

� Checking for Revenue Leakage

DAY-3/4

� Deposit Trend checking for Window Dressing

� Further checking based on your Observations

� Filling up of Remaining Documents (LFAR & Ghosh & Jilani Committee Recommendations & Other Annexures)

� Reconciling all Reports

� Checking, Rechecking and nicely arranging the sets

VARIOUS MOCs

� Revenue Leakage� P&L Account :Credit

� Balance Sheet Effect : Advances Increase

� Change in Head (Expense)� Correct Account :Debit

� Wrong Account :Credit

� Balance Sheet Effect : NIL

CONTINUED…

� Depreciation under-charged� Depreciation Account :Debit

� Fixed Asset Account :Credit

� Interest Reversal� P&L Account : Debit

� Balance Sheet Effect: Advance Decrease

MOC - 1

� Processing Charges amounting to Rs. 0.75 Lacs

not charged in XYZ Account (Medium Enterprise).

Outstanding Balance is Rs. 234.00 Lacs

� Rectification :Charges to be recovered in respective

account.

Sr.

No.

No. of

P&L Item

Heading of P&L Item

Additions(Credit)(Rs.)

Deductions(Debit)(Rs.)

Remarks(Give BriefDetail)

Income

MOC Annexure I(PROFIT & LOSS ACCOUNT)

Service 75000 -- Processing 1

Sr.

No.

No. of

P&L

Item

Heading of

P&L Item

Additions

(Debit)

(Rs.)

Deductions

(Credit)

(Rs.)

Remarks

(Give Brief

Detail)

Expenditure

Service

Charges Head75000 -- Processing

Fees Charged1

-- -- -- -- -- --

Sr.

No.

YSA

Code

Heading of

Yearly Extract

Additions(Credit)(Rs.)

Deductions(Debit)(Rs.)

Remarks(Give BriefDetail)

Liabilities

MOC Annexure IIYEARLY ABSTRACT

-- -- --------

Sr. No.

YSACode

Heading of Yearly

Extract

Additions(Debit)

(Rs.)

Deductions(Credit)

(Rs.)

Remarks(Give Brief Detail)

Assets

-- -- --------

1 --75000 Standard

Assets

Standard Assets

increase due to

charges recovered

Sr. No

.

Name of Borrower

Outstanding

Asset Classification

Security wiseClassification

IntReversal on A/C of movemen

t inAssets Classification

Security wise Provision

RestructuringProvision

Total Provision

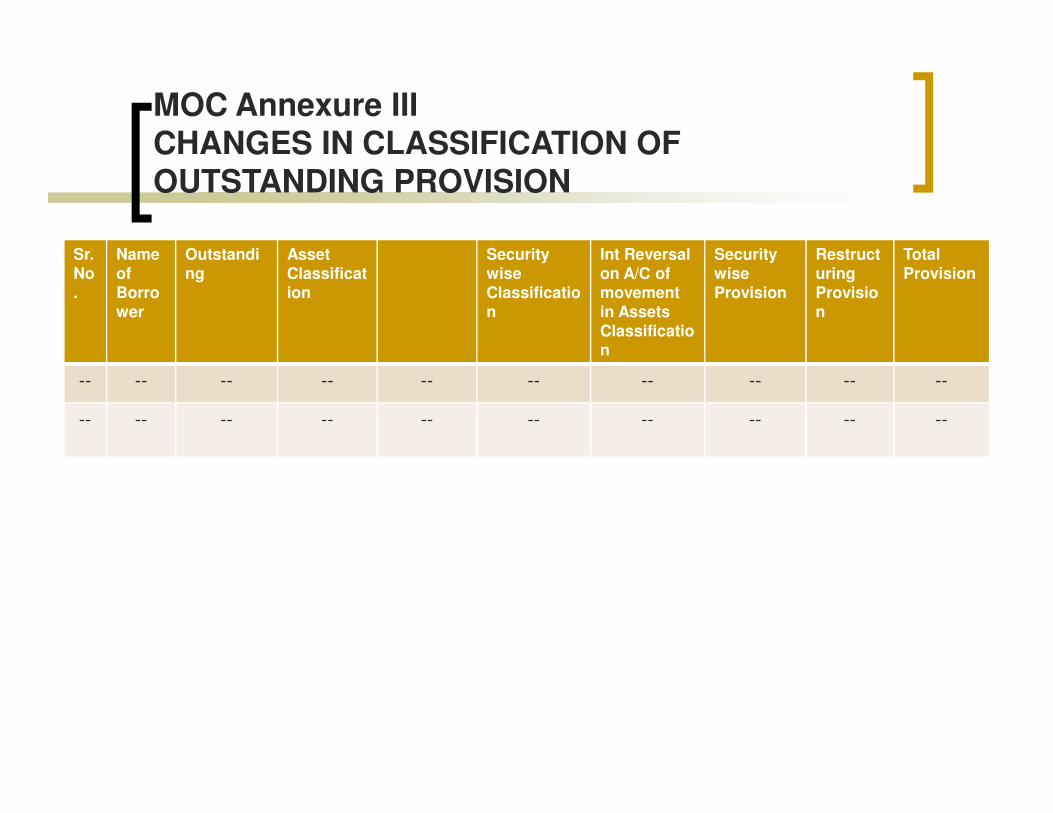

MOC Annexure IIICHANGES IN CLASSIFICATION OF OUTSTANDING PROVISION

XYZ Standard -- 93600 -- 936001 23400000XYZ

XYZ

Standard

Standard

Existing

Proposed

Standard

Standard

--

--

93600

93900 --

-- 93600

93900

1 23400000

23475000

Existing Provision : At 0.40% of 23400000

Proposed Provision : At 0.40% of 23475000

MOC - 2

� XYZ is a loan account (SME) amounting to Rs.

15.00 Lacs. Interest not served since Nov, 2013

amounting to Rs. 0.45 Lacs. The same has not

been declared NPA by the Branch. Outstanding been declared NPA by the Branch. Outstanding

Balance as on 31.03.2013 is Rs. 13.45 Lacs

� Rectification : Account to be declared NPA

Sr.

No.

No. of

P&L Item

Heading of P&L Item

Additions(Credit)(Rs.)

Deductions(Debit)(Rs.)

Remarks(Give Brief Detail)

Income

1 -- 45000 Interest not served Interest

MOC Annexure I(PROFIT & LOSS ACCOUNT)

Sr.

No.

No. of

P&L

Item

Heading of

P&L Item

Additions

(Debit)

(Rs.)

Deductions

(Credit)

(Rs.)

Remarks

(Give Brief

Detail)

Expenditure

1 -- 45000 Interest not served

reversed

-- -------- --

Interest

Income

Sr.

No.

YSA

Code

Heading of

Yearly Extract

Additions(Credit)(Rs.)

Deductions(Debit)(Rs.)

Remarks(Give Brief Detail)

Liabilities

MOC Annexure IIYEARLY ABSTRACT

------------

Sr.

No.

YSA

Code

Heading of

Yearly Extract

Additions

(Debit)(Rs.)

Deductions

(Credit)(Rs.)

Remarks

(Give Brief Detail)

Assets

1

2

3

Loan Account

NPA

Standard

Asset

--

1300000 --

--1300000

45000 Total Assets reduced

NPA increased

Standard Assets

decreased

MOC Annexure IIICHANGES IN CLASSIFICATION OF OUTSTANDING PROVISION

Sr. No

.

Name of Borrower

Outstanding

Asset Classification

Security wiseClassification

IntReversal on A/C of movemen

t inAssets Classification

Security wise Provision

RestructuringProvision

Total Provision

XYZ1 1345000 -- --3363Existing

Proposed

XYZ

XYZ

1 1345000

1300000

Standard

NPA

Standard

NPA

-- --3363

195000

3363

45000 -- 195000

Existing Provision : At 0.25% of 1345000

Proposed Provision : At 15.00% of 1300000

MOC - 3

� Expenses amounting to Rs. 0.50 Lacs wrongly

debited to Sundry Expenses Account instead of

Postage Expenses.

� Rectification :Expenses to be debited to correct

head

Sr.

No.

No. of

P&L Item

Heading of P&L Item

Additions(Credit)(Rs.)

Deductions(Debit)(Rs.)

Remarks(Give Brief Detail)

Income

-- -------- --

MOC Annexure I(PROFIT & LOSS ACCOUNT)

Sr. No.

No. of P&L

Item

Heading of P&L Item

Additions(Debit)

(Rs.)

Deductions(Credit)

(Rs.)

Remarks(Give Brief Detail)

Expenditure

--

--50000

50000Sundry

Expenses

Wrong head credited

Right head debitedPostage

Expense

1

2

Sr.

No.

YSA

Code

Heading of

Yearly Extract

Additions(Credit)(Rs.)

Deductions(Debit)(Rs.)

Remarks(Give BriefDetail)

-- -- -- -- -- --

Liabilities

MOC Annexure IIYEARLY ABSTRACT

-- -- -- -- -- --

Sr.

No.

YSA

Code

Heading of

Yearly

Extract

Additions

(Debit)

(Rs.)

Deductions

(Credit)

(Rs.)

Remarks

(Give Brief

Detail)

-- -- -- -- -- --

Assets

MOC Annexure IIICHANGES IN CLASSIFICATION OF OUTSTANDING PROVISION

Sr. No

.

Name of Borrower

Outstanding

Asset Classification

Security wiseClassification

IntReversal on A/C of movemen

t inAssets Classification

Security wise Provision

RestructuringProvision

Total Provision

-- -- -- -- -- -- -- -- -- --

MOC - 4

� Mr. X has a CC Limit (SME)amounting to Rs. 10.00 Lacs

(Outstanding Balance – 9.45 Lacs) which is regular as on

31.03.2014. He also has a TL (SME) amounting to Rs.

20.00 Lacs (Outstanding Balance – 18.65 Lacs). The TL

was required to be classified as NPA as on 31.03.2014. was required to be classified as NPA as on 31.03.2014.

But the same was omitted to be declared NPA by the

Branch. Interest not served amounts to Rs. 0.55 Lacs

and Principal not repaid amounts to Rs. 1.00 Lacs.

Interest for March,2014 amounting to Rs. 0.10 Lacs has

not been served in CC Account.

� Rectification: Both the accounts are to be declared NPA

Sr.

No.

No. of

P&L Item

Heading of P&L Item

Additions(Credit)(Rs.)

Deductions(Debit)(Rs.)

Remarks(Give Brief Detail)

Income

1 Interest

Account (CC)-- 10000 Interest not served

reversed

MOC Annexure I(PROFIT & LOSS ACCOUNT)

Sr. No.

No. of P&L

Item

Heading of P&L Item

Additions(Debit)

(Rs.)

Deductions(Credit)

(Rs.)

Remarks(Give Brief Detail)

-- -- -- -- -- --

Expenditure

Account (CC) reversed

Interest

Account (TL)-- 55000 Interest not served

reversed

Sr.

No.

YSA

Code

Heading of

Yearly Extract

Additions(Credit)(Rs.)

Deductions(Debit)(Rs.)

Remarks(Give BriefDetail)

-- -- -- -- -- --

Liabilities

MOC Annexure IIYEARLY ABSTRACT

Sr.

No.

YSA

Code

Heading of

Yearly Extract

Additions

(Debit)(Rs.)

Deductions

(Credit)(Rs.)

Remarks

(Give Brief Detail)

Assets

1

2

3

Standard

Assets

Standard

Assets

NPA

--

--

2745000

2745000

65000Standard Assets

reduced

NPA increased

Standard Assets

decreased

--

MOC Annexure IIICHANGES IN CLASSIFICATION OF OUTSTANDING PROVISION

Sr. No

.

Name of Borrower

Outstanding

Asset Classification

Security wiseClassification

Int Reversal on A/C of

movement in Assets Classification

Security wise Provision

RestructuringProvision

Total Provision

X 2810000 Standard Existing Standard -- 7025 -- 70251

2745000 NPA Proposed NPA 65000 411750 -- 411750

X 2810000 Standard Existing Standard -- 7025 -- 70251

Existing Provision : At 0.25% of 2810000

Proposed Provision : At 15.00% of 2745000

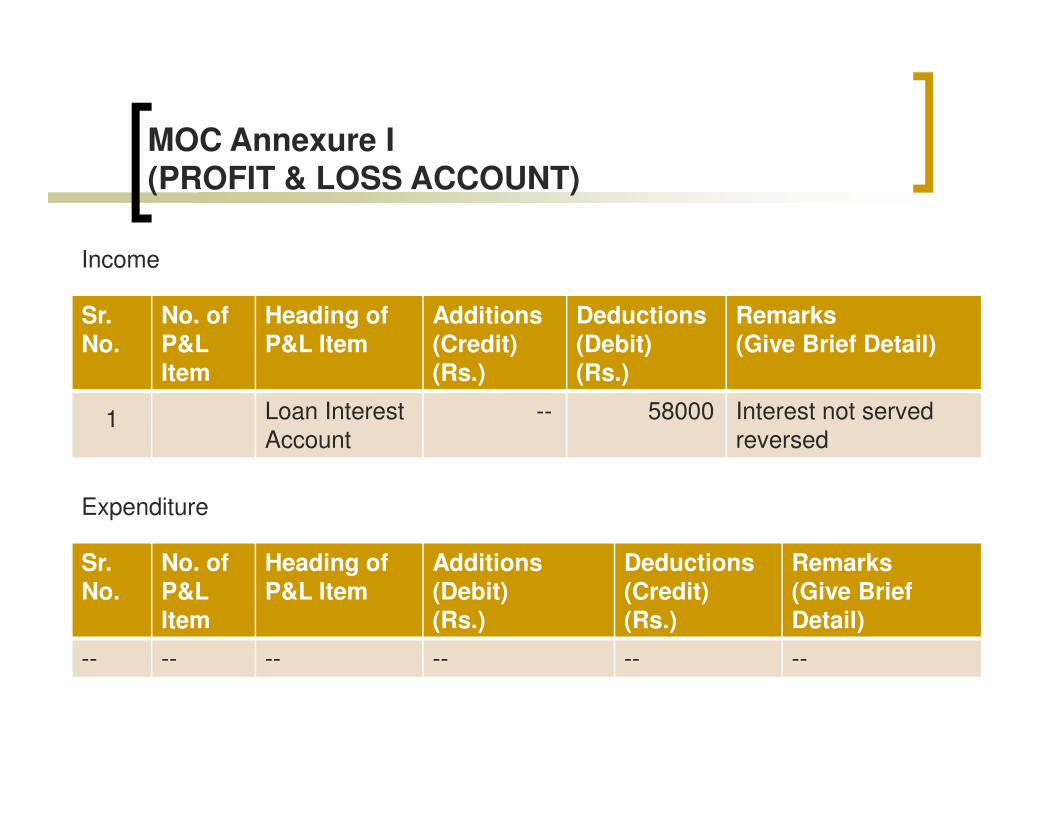

MOC - 5

� ABC has a CC Limit (SME) amounting to Rs. 15.00

Lacs has been declared NPA by the branch as on

31.03.2014. But interest not served amounting to

Rs. 0.58 Lacs not reversed. (Balance Outstanding

is Rs. 15.58 Lacs)is Rs. 15.58 Lacs)

� Rectification: Interest to be reversed

Sr.

No.

No. of

P&L

Item

Heading of P&L Item

Additions

(Credit)

(Rs.)

Deductions(Debit)

(Rs.)

Remarks(Give Brief Detail)

Income

-- 58000 Interest not served Loan Interest 1

MOC Annexure I(PROFIT & LOSS ACCOUNT)

Sr.

No.

No. of

P&L

Item

Heading of

P&L Item

Additions

(Debit)

(Rs.)

Deductions

(Credit)

(Rs.)

Remarks

(Give Brief

Detail)

-- -- -- -- -- --

Expenditure

-- 58000 Interest not served

reversed

Loan Interest

Account1

Sr.

No.

YSA

Code

Heading of

Yearly Extract

Additions(Credit)(Rs.)

Deductions(Debit)(Rs.)

Remarks(Give Brief Detail)

-- -- -- -- -- --

Liabilities

MOC Annexure IIYEARLY ABSTRACT

-- -- -- -- -- --

Sr.

No.

YSA

Code

Heading of

Yearly

Extract

Additions

(Debit)

(Rs.)

Deductions

(Credit)

(Rs.)

Remarks

(Give Brief Detail)

Assets

1 NPA -- 58000 NPA reduced

MOC Annexure IIICHANGES IN CLASSIFICATION OF OUTSTANDING PROVISION

Sr. No

.

Name of Borrower

Outstanding

Asset Classification

Security wiseClassification

Int Reversal on A/C of

movement in Assets Classification

Security wise Provision

RestructuringProvision

Total Provision

1 ABC 1558000

NPA

NPA

1500000ABC Proposed

Existing

NPA

NPA

--

-- 233700

225000 --

--

225000

233700

NPA1500000ABC Proposed NPA -- 225000 -- 225000

MOC - 6

� Mr. A has a CC Limit amounting to Rs. 20.00 Lacs

(Outstanding Balance : 20.10 Lacs)which is regular as on

31.03.2014. He also has a TL amounting to Rs. 30.00 Lacs

(Outstanding Balance is Rs. 28.32 Lacs). The Account

classifies as NPA as on 31.03.2014. TL has been declared classifies as NPA as on 31.03.2014. TL has been declared

NPA & Interest reversed by the Branch but the CC Limit

was omitted to be declared the same by the Branch.

Interest for March,2014 amounting to Rs. 0.10 Lacs has

not been served in CC Account.

� Rectification : CC Limit is to be declared NPA

Sr.

No.

No. of

P&L

Item

Heading of P&L Item

Additions

(Credit)

(Rs.)

Deductions(Debit)

(Rs.)

Remarks(Give Brief Detail)

Income

Loan Interest -- 10000 Interest not served

MOC Annexure I(PROFIT & LOSS ACCOUNT)

Sr.

No.

No. of

P&L

Item

Heading of

P&L Item

Additions

(Debit)

(Rs.)

Deductions

(Credit)

(Rs.)

Remarks

(Give Brief Detail)

-- -- -- -- -- --

Expenditure

Loan Interest

Account-- 10000 Interest not served

reversed1

Sr.

No.

YSA

Code

Heading of

Yearly Extract

Additions(Credit)(Rs.)

Deductions(Debit)(Rs.)

Remarks(Give BriefDetail)

-- -- -- -- -- --

Liabilities

MOC Annexure IIYEARLY ABSTRACT

Sr.

No.

YSA

Code

Heading of

Yearly Extract

Additions

(Debit)(Rs.)

Deductions

(Credit)(Rs.)

Remarks

(Give Brief Detail)

Assets

1

2

3 NPA

Standard

Assets

Standard

Assets

--

--

-- 2000000

2000000

10000 Interest reversed

Standard assets

reduced

NPA Accounts

increased

MOC Annexure IIICHANGES IN CLASSIFICATION OF OUTSTANDING PROVISION

Sr. No

.

Name of Borrower

Outstanding

Asset Classification

Security wiseClassification

Int Reversal on A/C of

movement in Assets Classification

Security wise Provision

RestructuringProvision

Total Provision

Standard Existing Standard -- 5025 -- 50251 A 2010000

NPA Existing NPA 32000 -- 420000A 2800000 420000

A 4800000 NPA NPAProposed 42000 720000 720000--

Existing Provision : At 0.25% of 2010000

Existing Provision : At 15.00% of 2800000

Proposed Provision : At 15.00% of 4800000

MOC - 7

� PQR Loan account has an Outstanding Balance as

on 31.03.2014 of Rs. 8.46 Lacs has been classified

as Sub-Standard Asset. But the same should have

been classified as Doubtful Asset (D1).been classified as Doubtful Asset (D1).

� Rectification: Asset Classification is to be changed.

Sr.

No.

No. of

P&L

Item

Heading of P&L Item

Additions

(Credit)

(Rs.)

Deductions(Debit)

(Rs.)

Remarks(Give Brief

Detail)

-- -- -- -- -- --

Income

MOC Annexure I(PROFIT & LOSS ACCOUNT)

-- -- -- -- -- --

Sr.

No.

No. of

P&L

Item

Heading of

P&L Item

Additions

(Debit)

(Rs.)

Deductions

(Credit)

(Rs.)

Remarks

(Give Brief

Detail)

-- -- -- -- -- --

Expenditure

Sr.

No.

YSA

Code

Heading of

Yearly Extract

Additions(Credit)(Rs.)

Deductions(Debit)(Rs.)

Remarks(Give Brief Detail)

-- -- -- -- -- --

Liabilities

MOC Annexure IIYEARLY ABSTRACT

-- -- -- -- -- --

Sr.

No.

No. of

P&L

Item

Heading of

P&L Item

Additions

(Debit)

(Rs.)

Deductions

(Credit)

(Rs.)

Remarks

(Give Brief Detail)

Assets

Sun Standard

Assets

Doubtful

Assets

--

--846000

846000 Sub-Standard Assets

reduced

Doubtful Assets

increased

1

2

MOC Annexure IIICHANGES IN CLASSIFICATION OF OUTSTANDING PROVISION

Sr. No

.

Name of Borrower

Outstanding

Asset Classification

Security wiseClassification

Int Reversal on A/C of

movement in Assets Classification

Security wise Provision

RestructuringProvision

Total Provision

NPA Existing NPA -- 126900 -- 1269001 PQR 846000

NPA Proposed NPA -- 211500 -- 211500PQR 846000

MOC - 8

� Provision for Rent amounting to Rs. 0.65 Lacs has

not been made

� Rectification :Change in Provisioning� Rectification :Change in Provisioning

Sr.

No.

No. of

P&L

Item

Heading of P&L Item

Additions

(Credit)

(Rs.)

Deductions(Debit)

(Rs.)

Remarks(Give Brief

Detail)

-- -- -- -- -- --

Income

MOC Annexure I(PROFIT & LOSS ACCOUNT)

-- -- -- -- -- --

Sr.

No.

No. of

P&L

Item

Heading of

P&L Item

Additions

(Debit)

(Rs.)

Deductions

(Credit)

(Rs.)

Remarks

(Give Brief

Detail)

Expenditure

1Rent

Expense

65000 --

Sr.

No.

YSA

Code

Heading of

Yearly Extract

Additions(Credit)(Rs.)

Deductions(Debit)(Rs.)

Remarks(Give Brief Detail)

Liabilities

MOC Annexure IIYEARLY ABSTRACT

1Prov. For 65000 --

Sr.

No.

YSA

Code

Heading of

Yearly

Extract

Additions

(Debit)

(Rs.)

Deductions

(Credit)

(Rs.)

Remarks

(Give Brief Detail)

-- -- -- -- -- --

Assets

1Prov. For

Rent

65000 --

MOC Annexure IIICHANGES IN CLASSIFICATION OF OUTSTANDING PROVISION

Sr. No

.

Name of Borrower

Outstanding

Asset Classification

Security wiseClassification

Int Reversal on A/C of

movement in Assets Classification

Security wise Provision

RestructuringProvision

Total Provision

-- -- -- -- -- -- -- -- -- --

-- -- -- -- -- -- -- -- -- --

MOC ANNEXURE IVFIXED ASSET RETURN

Sr. No.

Original Cost

Cumulative Depreciation

Net Book Value

Remarks

A FURNITURE & FITTINGS

i Closing Balance as per

Br. Return as on 31.03.2013

ii Proposed Closing Balanceii Proposed Closing Balance

iii Net Entry to be passed at LHO

B ELECTRICAL FITTINGS

i Closing Balance as per

Br. Return as on 31.03.2013

ii Proposed Closing Balance

iii Net Entry to be passed at LHO

Sr. No.

Original Cost

Cumulative Depreciation

Net Book Value

Remarks

C OTHER PLANT MACHINERY

i Closing Balance as per

Br. Return as on 31.03.2013

CONTINUED…

31.03.2013

ii Proposed Closing Balance

iii Net Entry to be passed at LHO

D Computer Software

i Closing Balance as per

Br. Return as on 31.03.2013

ii Proposed Closing Balance

iii Net Entry to be passed at LHO

Sr. No.

Original Cost

Cumulative Depreciation

Net Book Value

Remarks

E CARS

i Closing Balance as per

Br. Return as on 31.03.2013

ii Proposed Closing Balance

CONTINUED…

ii Proposed Closing Balance

iii Net Entry to be passed at LHO

F COMPUTERS

i Closing Balance as per

Br. Return as on 31.03.2013

ii Proposed Closing Balance

iii Net Entry to be passed at LHO

Sr. No.

Original Cost

Cumulative Depreciation

Net Book Value

Remarks

G GRAND TOTAL

i Closing Balance as per

Br. Return as on 31.03.2013

CONTINUED…

31.03.2013

(Ai+Bi+Ci+Di+Ei+Fi)

Ii Proposed Closing Balance

(Aii+Bii+Cii+Dii+Eii+Fii)

iii Net Entry to be passed at LHO

(Aiii+Biii+Ciii+Diii+Eiii+Fiii)

MOC ANNEXURE VCAPITAL ADEQUACY DATA – CAR B I

Sr.No

Account

Customer Name

Bucket No.

Outstanding

Outstanding After

Basel

Basel Coll. After

Net Exposure

Risk Weig

Risk Weighted

a) Funded Exposures

1 Existing

Proposed

2 Existing2 Existing

Proposed

TOTAL

b) Non- Funded Exposures

1 Existing

Proposed

2 Existing

Proposed

TOTAL

MOC ANNEXURE VI CAPITAL ADEQUACY DATA – CAR B II

Sr.No

Account

Customer Name

Bucket No.

Outstanding

Outstanding After

Basel

Basel Coll. After

Net Exposure

Risk Weig

Risk Weighted

a) Funded Exposures

1 Existing

Proposed

2 Existing2 Existing

Proposed

TOTAL

b) Non- Funded Exposures

1 Existing

Proposed

2 Existing

Proposed

TOTAL

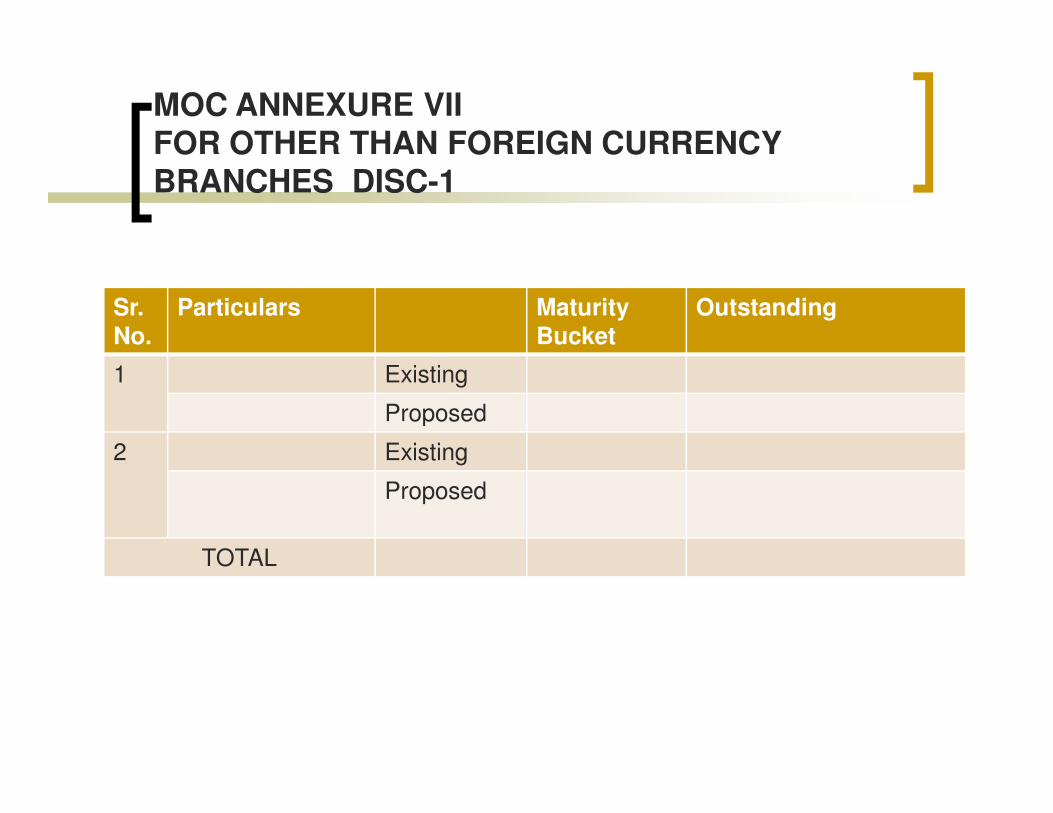

MOC ANNEXURE VII FOR OTHER THAN FOREIGN CURRENCY BRANCHES DISC-1

Sr.No.

Particulars Maturity Bucket

Outstanding

1 Existing

ProposedProposed

2 Existing

Proposed

TOTAL

MOC ANNEXURE VIII FOR FOREIGN CURRENCY BRANCHES DISC-3

Sr.No.

Particulars Maturity Bucket

Outstanding

1 Existing

ProposedProposed

2 Existing

Proposed

TOTAL

VARIOUS FINACLE COMMANDS TO BE USED

� NAME SEARCH

� INTTI

� AINTRPT

� GI� GI

� LIMIT HISTORY

� MSGOIRP

� REPORTS MENU

� CTRL E

LONG FORM AUDIT REPORT

� Does the branch generally carry cash balances, which vary sig-nificantly from the limits fixed by the controlling authorities of the bank? Whether excess balances have been reported to the controlling authorities of the bank?

� Does the branch hold adequate insurance cover for cash-on-hand and cash-in-transit?cash-in-transit?

� Is cash maintained in effective joint custody of two or more officials, as per the instructions of the controlling authorities of the bank?

� Has the Branch kept money-at-call and short notice during the year? If so, whether instructions/guidelines, if any, laid down by the controlling authorities of the bank have been complied with?

� Are there any investments held by branches on behalf of Head Office/other offices of the bank? If so, whether these have been made available for physical verification or evidences have been produced with regard to the same where these are not in possession of the branch?

LONG FORM AUDIT REPORT

� In the cases examined by you, have you come across instances of credit facilities having been sanctioned beyond the delegated authority or limit fixed for the branch? Are such cases promptly reported to higher authorities?

� List of major items of the contingent liabilities (other than constituents’ liabilities such as guarantees, letters of credit, acceptances, liabilities such as guarantees, letters of credit, acceptances, endorsements, etc.) not acknowledged by the Branch?

� In the cases examined by you, have you come across instances of credit facilities released by the branch without execution of all the necessary documents? If so, give details of such cases.

� Are credit card dues recovered promptly?

� Has the branch identified and classified advances into standard /substandard/doubtful/loss assets in line with the norms prescribed by the Reserve Bank of India (The auditor may refer to the relevant H.O. Instructions for identification of NPAs and Classification of Advances).

LONG FORM AUDIT REPORT

� Where the auditor disagrees with the branch classification of advances into standard/substandard/doubtful/loss assets, the details of such advances with reasons should be given. Also indicate whether suitable changes have been incorporated/suggested in the Memorandum of Changes.

Have you come across cases where the relevant Controlling Authority of � Have you come across cases where the relevant Controlling Authority of the bank has authorised legal action for recovery of advances or recalling of advances but no such action was taken by the branch? If so, give details of such cases.

� Have all non-performing advances been promptly reported to the relevant Controlling Authority of the bank? Also state whether any rehabilitation programme in respect of such advances has been undertaken, and if so, the status of such programme.

LONG FORM AUDIT REPORT

� In the cases examined by you has the branch complied with the Recovery Policy prescribed by the controlling authorities of the bank with respect to compromise/ settlement and write-off cases? Details of the cases of compromise/ settlement and write-off cases involving write-offs/ waivers in excess of 50.00 lakh may be given.

Are there any overdue /matured term deposits at the end of the year? If � Are there any overdue /matured term deposits at the end of the year? If so, amounts thereof should be indicated.

� Details of the outstanding amounts of letters of credit and co-acceptances funded by the Branch at the end of the

� Details of outstanding amounts of guarantees invoked and funded by the Branch at the end of the year

(a) Guarantees invoked, paid but not adjusted:

(b) Guarantees invoked but not paid

LONG FORM AUDIT REPORT

� Has the branch complied with the Income Recognition norms prescribed by R.B.I

� Does the bank have a system of estimating and providing interest accrued on overdue/matured term deposits?

� Are there any outstanding debits in the Head Office Account in respect Are there any outstanding debits in the Head Office Account in respect of inter-branch transactions?

� Have you come across items of double responses in the Head Office Account? If so, give details.

� Does the branch forward on a daily basis to a designated cell/Head Office, a statement of debit/credit transactions in relation to other branches?

� Smaller / medium sized branch to rectify irregularities pointed out during inspection / audit within 4 months.

� In order to bring about uniformity of software used by various branches/offices, there should be formal method of incorporating change in standard software and it should be approved by senior management. Such changes to be inspected and monitored

GHOSH & JILANI COMMITTEE RECOMMENDATIONS

management. Such changes to be inspected and monitored continuously.

� Every bank should have a manual of instructions for its inspectors/ auditors And periodically update the same.

� System of exclusive scrutiny of credit portfolio with focus on Larger advances and group exposures.

� Special scrutiny of high value accounts shifted to the bank Along with executives and accounts transferred from other Branches along with officials The observations of RBI inspections Should be promptly/ and affectively followed up by banks.

� Rotation of staff / duties and transfer covering all categories of staff Including dealing room / securities department, staff etc.

� Financial and administrative powers of officials should be laid down

� Precautions in handling cash and valuables- restriction of entry to cash cabin, dual custody of cash / valuables, surprise Verification at regular intervals etc.

GHOSH & JILANI COMMITTEE RECOMMENDATIONS

intervals etc.

� Precautions against shortage in cash reported by cashier.

� Introduction of surprise checking at frequent intervals

� Precautions against misappropriation of cash by member of staff in the guise of customer service. Only authorized personnel should accept cash / issue counterfoils in cash dept.

� Cashiers should not be allowed to make entries in Passbook.

� Proper system should be evolved in respect of cash balances insurance and prompt reporting of inter branch and inter bank remittances of cash.

� Precaution against misusing banking channels for tax evasion POs /TC in excess of Rs.50000 /- should be by way of debit to constituents account and not by cash. Doubtful Cases should be reported to higher authorities.

� Exercise of caution at the time of opening of New Deposit Account of all types.

GHOSH & JILANI COMMITTEE RECOMMENDATIONS

types.

� Customers to be educated about implication of introducing an account without knowing the party.

� Close watch on the operations in the new accounts should Be kept

� Issue of fresh cheques book should be only against requisition slip from previous check book and other precautions to be taken in respect of cheques books.

� Precaution in payment of cheques – verification of signature custody of specimen signatures, custody of bank Cheques books etc.

� Bank guarantees / LCs to be issued in security forms serially Numbered under two signatures above certain cut off point in Triplicate , binding on beneficiary to seek conformation of controlling office (incorporation of suitable condition in the document) etc.

� Safe custody of / access to vouchers through written orders of manager – records to be maintained of those who have accessed such records.

GHOSH & JILANI COMMITTEE RECOMMENDATIONS

– records to be maintained of those who have accessed such records.

� Fraud cases up to Rs.25,000/- having involvement of an Insider should not be reported to police where recovery is not Doubtful.

� Bills discounting facility under L/C, Co-acceptance should be Extended only to customers having regular sanctioned Limits.

� Guarantees above a certain limit be signed by two officials

CERTIFICATES TO BE OBTAINED

� Certificates in respect of H.O. Investments

� Certificates regarding Guarantees Invoked

� Certificates regarding Interest Subventions that are not applicable

LIST OF CIRCULARS

� Master Circular – Know Your Customer (KYC) norms / Anti-Money

Laundering (AML) standards/Combating of Financing of Terrorism

(CFT)/Obligation of banks under PMLA, 2002

� Master Circular - Prudential norms on Income Recognition, Asset

Classification and Provisioning pertaining to Advances Classification and Provisioning pertaining to Advances

� RBI/2012-13/500

DCM (NPD) No.5133/ 09.39.000/2012-13

RESTRUCTURING

� The guidelines issued by the Reserve Bank of India on Restructuring of Advances are divided into 4 Categories :

• Guidelines on restructuring of advances extended to industrial units.

• Guidelines on restructuring of advances extended to industrial units under the Corporate Debt Restructuring (CDR) Mechanism

• Guidelines on restructuring of advances extended to Small and Medium Enterprises (SME)

• Guidelines on restructuring of all other advances.

� Banks may Restructure the Accounts classified under ‘Standard', ‘Sub-Standard' and ‘Doubtful' Categories.

� While a Restructuring Proposal is under consideration, the usual Asset Classification Norms would continue to apply.

� Normally, in restructuring alteration in the Original Loan Agreement are made with the formal consent / application of the debtor.

Eligibility Criteria for Restructuring of Advances

made with the formal consent / application of the debtor.

� Financial Viability is to be established and there is a reasonable certainty of repayment from the Borrower

� Banks may review the reasons for classification of the Borrowers as Wilful Defaulters, and satisfy itself that the Borrower is in a position to rectify the Wilful Default. The restructuring of such cases may be done with Board's Approval. Others require approval of the Core Group only.

� BIFR cases are not eligible for restructuring without their express approval

� The accounts classified as 'standard assets' should be immediately re-classified as 'sub-standard assets' upon restructuring

� The non-performing assets would continue to have the same asset classification as prior to restructuring and slip into further lower asset classification categories as per extant asset classification norms

Asset Classification Norms

� Standard accounts classified as NPA and NPA accounts retained in the same category on restructuring by the bank should be upgraded only when all the outstanding loan/facilities in the account perform satisfactorily during the ‘specified period’ (Annex - 5), i.e. principal and interest on all facilities in the account are serviced as per terms of payment during that period.

� If satisfactory performance after the specified period is not evidenced, the asset classification of the restructured account would be governed by restructuring payment schedule.

� Where the pre-restructuring facilities were classified as 'sub-standard' and 'doubtful', interest income on the additional finance should be

Asset Classification Norms

and 'doubtful', interest income on the additional finance should be recognised only on cash basis.

� If the restructured asset does not qualify for upgradation at the end of the above specified period, the additional finance shall be placed in the same asset classification category as the restructured debt.

Asset classification norms

� FITL / debt or equity instrument created by conversion of unpaid interest will be

classified in the same asset classification category in which the restructured

advance has been classified.

� Further movement in the asset classification of FITL / debt or equity instruments

would also be determined based on the subsequent asset classification of the

Prudential Norms for Conversion of Unpaid Interest into 'Funded Interest Term Loan' (FITL), Debt or Equity Instruments

would also be determined based on the subsequent asset classification of the

restructured advance.

Income recognition norms

� The income, if any, generated by these instruments may be recognised on

accrual basis, if these instruments are classified as 'standard', and on cash

basis in the cases where these have been classified as a non-performing asset.

� The unrealised income represented by FITL / Debt or equity instrument should

have a corresponding credit in an account styled as "Sundry Liabilities Account

(Interest Capitalization)".

Income recognition norms

� In the case of conversion of unrealised interest income into equity, which is quoted, interest income can be recognized after the account is upgraded to standard category at market value of equity, on the date of such upgradation, not exceeding the amount of interest converted into equity.

Prudential Norms for Conversion of Unpaid Interest into 'Funded Interest Term Loan' (FITL), Debt or Equity Instruments

equity.

� Only on repayment in case of FITL or sale / redemption proceeds of the debt / equity instruments, the amount received will be recognized in the P&L Account, while simultaneously reducing the balance in the "Sundry Liabilities Account (Interest Capitalisation)".