Embed Size (px)

Citation preview

Long Products Flat Products News Stainless Steel Scrap Metal Ferro Alloys

ASNVol. 4Issue 9May 2021

Australian Steel News

STEEL MARKET SUMMARY - May

China Rebate Withdrawal To Raise Steel Prices

As if steel pricing and supply line chaos wasn´t enough to drive steel buyers and

consumers around the bend, China has upped the ante by removing its VAT rebate

on 146 exported steel products – effective May 1st. The products from which the

rebate of 13% has been removed include: HRC, hot-rolled sheet, plate, rebar, wire

rod, colour-coated steel and cold-rolled sheet with 0.5-3.00mm and below 0.5mm

thickness. China made no changes to rebates for duties on exported cold-rolled coil

and hot-dip galvanised steel. The rebate cut, which was forecast by Australian Steel

News, is widely expected to put upward pressure on world steel prices and to alter

steel trade flows in the midst of a global boom. The volume of steel enjoying the

now-cancelled rebates was more than 44 million metric tonnes in 2019, according to

Kallanish Commodities. That´s more than two thirds of total steel exports

In a separate announcement, the central government´s Finance Ministry also

entirely removed the import duty on pig iron, crude steel and recycled steel (ferrous

scrap). “The measures will reduce the cost of importing, expand the import of iron

and steel resources and lend downward pressure to domestic crude steel output,

guiding the steel industry towards the reduction of overall energy consumption,

while promoting the transformation and high-quality development of the steel

industry,” the Ministry said.

When the rebate removal was announced last week, many commentators rushed to

predict steel prices would automatically and immediately rise by 13%. However, that

remains to be seen. At least one Beijing-based steel analyst told S&P Global Platts

that he expects the rebate cancellation to have little impact on both China´s steel

export prices and volume in the near term, saying: “Most of the Chinese mills, when

signing export deals recently, had already factored in the possible cancellation.” The

recent price hikes by Chinese exporters would seem to support the notion they were

expecting the rebate to be removed. However, even with a full 13% increment,

Chinese steel exports could remain competitive in a climate where global demand

has been recovering and supply has been limited. Additionally, other market players

are likely to take this opportunity to raise their own export prices. Turning to scrap

prices, our Long Products graph shows the LME steel scrap price for May 3. The

next day it jumped by US$45 to $474 as seen in our Scrap Metal Prices graph.

The spanner in the works created by China´s export rebate decision came two

weeks after the World Steel Association (WSA) released its Short Range Outlook for

2021 and 2022. The WSA forecasts global steel demand will grow by 5.8% in 2021

and by a further 2.7% in 2022 to 1,924.6 million metric tonnes. Specifically, the

report says China´s steel demand is expected to grow by 3.0% in 2021 but that it

will decelerate to 1.0% in 2022 as the effect of the 2020 stimulus subsides. In the

advanced economies, a recovery in demand this year of 8.2% will be followed by

4.2% growth in 2022. However, steel demand in 2022 will still fall short of 2019

levels. The WSA also forecasts global construction will....(Click to continue reading)

“Key Indicators, Pricing and News for the Australian Steel Industry”*

RBA Holds Interest Rates – May 4

The Reserve Bank of Australia has kept interest rates on hold and has flagged the possibility of more stimulus ahead.RBA – Monetary Policy Decision

583600

770

869

608 591

702

764

554563

656643 639

532

632 632650 690

372

423

387

471 460429

300

400

500

600

700

800

900

Dec 1st Jan 1st Feb 1st Mar 1st Apr 1st May 3rd

Long Products – Construction Steels

Wire Rod

Rebar China

Rebar Turkey

Rebar SE Asia

Scrap Turkey

Building Approvals Trend Up - May 5

Dwellings approved rose 17.4% in March, following at 20.1% rise in February. NSW saw a 26.9% rise and Victoria a 24.7% rise.ABS – Building Approvals, Australia

Australian Construction & Economic Data

New Loans At Record Level – May 4

New loan commitments for housing rose 5.5% in March, seasonally adjusted, to a new record high of $30.2 billion.ABS – Lending Indicators

Private Home Starts Rise – April 14

New private sector house starts rose by 26.6% to a 20-year high of 33,761 dwellings in the December quarter.ABS – Building Activity, Australia

Prices are displayed in USD per tonne. See Key to Prices for full product description.

690

797 768 788840

950

830

996 970

1150

1286

1540

591

654 629695

770

568634 608

920

540

645

730

880

346 434 452 458421

454300

500

700

900

1100

1300

1500

Dec 1st Jan 1st Feb 1st Mar 1st Apr 1st May 3rd

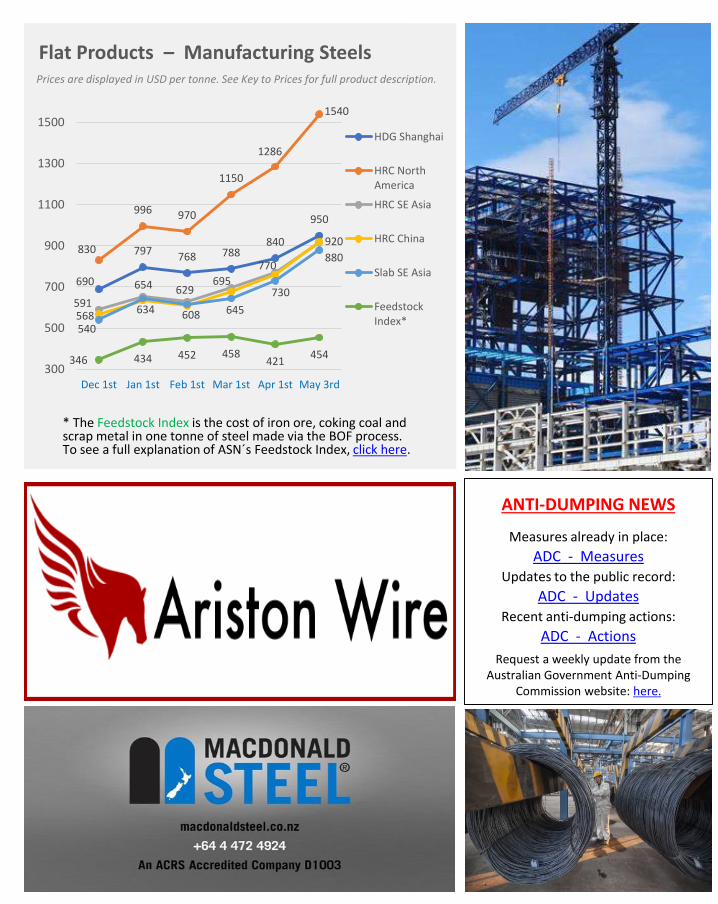

Flat Products – Manufacturing Steels

HDG Shanghai

HRC NorthAmerica

HRC SE Asia

HRC China

Slab SE Asia

FeedstockIndex*

* The Feedstock Index is the cost of iron ore, coking coal and scrap metal in one tonne of steel made via the BOF process. To see a full explanation of ASN´s Feedstock Index, click here.

Prices are displayed in USD per tonne. See Key to Prices for full product description.

ANTI-DUMPING NEWS

Measures already in place:

ADC - MeasuresUpdates to the public record:

ADC - UpdatesRecent anti-dumping actions:

ADC - Actions

Request a weekly update from theAustralian Government Anti-Dumping

Commission website: here.

372

423

387

471 460474

102 102

160

125112 109

124

174

156

172157

183

50

100

150

200

250

300

350

400

450

500

Dec 1st Jan 1st Feb 1st Mar 1st Apr 1st May 4th

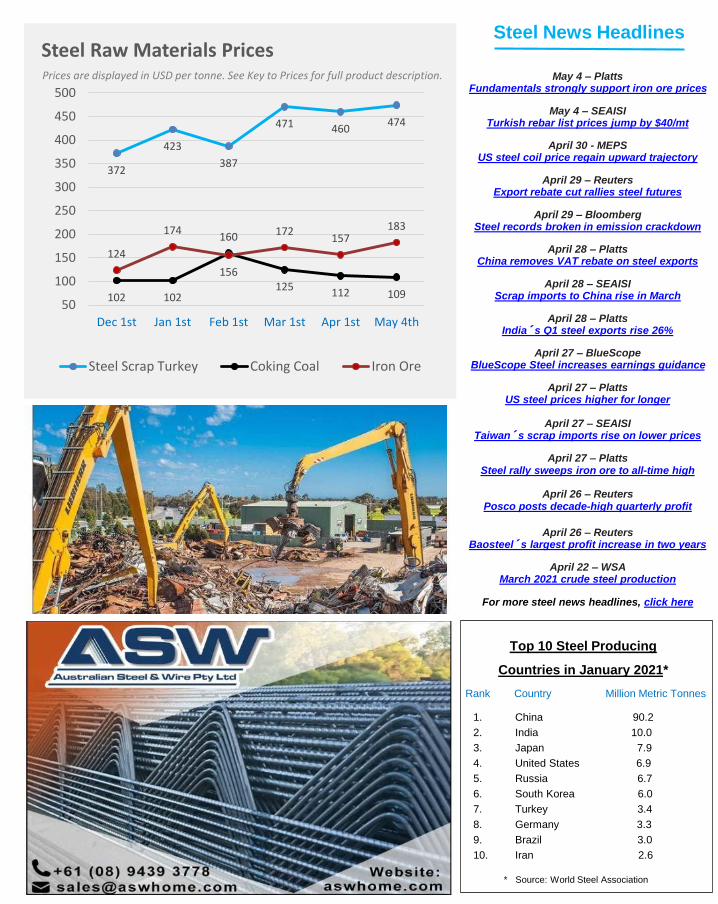

Steel Raw Materials Prices

Steel Scrap Turkey Coking Coal Iron Ore

Steel News Headlines

May 4 – PlattsFundamentals strongly support iron ore prices

May 4 – SEAISITurkish rebar list prices jump by $40/mt

April 30 - MEPSUS steel coil price regain upward trajectory

April 29 – ReutersExport rebate cut rallies steel futures

April 29 – BloombergSteel records broken in emission crackdown

April 28 – PlattsChina removes VAT rebate on steel exports

April 28 – SEAISIScrap imports to China rise in March

April 28 – PlattsIndia´s Q1 steel exports rise 26%

April 27 – BlueScopeBlueScope Steel increases earnings guidance

April 27 – PlattsUS steel prices higher for longer

April 27 – SEAISITaiwan´s scrap imports rise on lower prices

April 27 – PlattsSteel rally sweeps iron ore to all-time high

April 26 – ReutersPosco posts decade-high quarterly profit

April 26 – ReutersBaosteel´s largest profit increase in two years

April 22 – WSAMarch 2021 crude steel production

For more steel news headlines, click here

Prices are displayed in USD per tonne. See Key to Prices for full product description.

* Source: World Steel Association

1. China 90.2

2. India 10.0

3. Japan 7.9

4. United States 6.9

5. Russia 6.7

6. South Korea 6.0

7. Turkey 3.4

8. Germany 3.3

9. Brazil 3.0

10. Iran 2.6

Rank Country Million Metric Tonnes

Top 10 Steel Producing

Countries in January 2021*

Reinforcing Steels / David Roberts / [email protected]

Structural Steel / PC Strand / Mark Horwitz / [email protected]

Special Steels / Tube and Pipe / Matt Gilpin / [email protected]

Stainless Steel / Howard Seligsohn / [email protected]

Flat Products / Stuart Robertson / [email protected]

Rural Products / Liubov Morozova-Sogrine / [email protected]

Wire and Aluminium / Steve Wade / [email protected]

May 3 Apr 1 Mar 1 Feb 1 Jan 1 Dec 1

Copper 9949 8768 9198 7827 7741 7644

Aluminium 2445 2212 2154 1985 1978 2045

Nickel 17477 16001 18655 17807 16540 16102

Zinc 2904 2765 2788 2548 2723 2768

Vanadium 36.50 35.20 33.50 30.50 30.00 27.00

Non-Ferrous Metals PricesPrices are displayed in USD per tonne, except Vanadium in USD/kg. See Key to Prices.

372

423

471

460474

380

475

397

460

442

466

321

447

368

427

401

420

290

340

390

440

490

Dec 1st Jan 1st Feb 1st Mar 1st Apr 1st May 4th

Steel Scrap Turkey East Asia Import CFR

Taiwan Containerized CFR

2667 2638

2874

3072

2830

2982

19662036

2194

2389

2156

2301

1800

2000

2200

2400

2600

2800

3000

3200

Dec 1st Jan 1st Feb 1st Mar 1st Apr 1st May 3rd

Stainless Steel Feedstock Index*- EAF (AUD)

Stainless Steel Feedstock Index*- EAF (USD)

* The Stainless Steel Feedstock Index is the cost of iron ore, chromium and nickel in one tonne of stainless steel created through the EAF process. For a full explanation of ASN´s unique Stainless Steel Feedstock Index, click here.

Prices are displayed in USD per tonne. See Key to Prices.

Stainless Steel Feedstock IndexPrices are in the currency indicated. See Key to Prices.

Scrap Metal Prices - HMS 1/2 80 : 20

Ariston Wire Contacts

Wire and Reinforcing Accessories:

Fran Liebovitz / [email protected]

Galvanised Mesh and Fencing Products:

Ian Jones / [email protected]

Telephone: (02) 93874188

Website: www.aristonwire.com.au

Ferro Alloy Prices

FeCrHC basis 60% Cr 6-8% C ddp NWE

FeMnHC Mn 78% ddp Europe Works

FeSi75% Si fob China

FeMo65-70% Mo dp Rotterdam

22,75023,85024,900

28,925

27,05028,225

Dec 1st Jan 1stFeb 1st Mar 1stApr 1st May 3rd

1973 19732205

2590 2557 2579

Dec 1st Jan 1stFeb 1st Mar 1stApr 1st May 3rd

12251360

1460 1450 1465 1485

Dec 1st Jan 1stFeb 1st Mar 1stApr 1st May 3rd

1062 1116

1345 1320 1287

1560

Dec 1st Jan 1stFeb 1st Mar 1stApr 1st May 3rd

Prices are displayed in USD per tonne.

Top Steel-Producing Companies*(Figures quoted are millions of metric tonnes)

Rank Company HQ 2019

1. ArcelorMittal Luxembourg 97.312. China Baowu China 95.473. Nippon Steel Japan 51.684. HBIS Group China 46.565. POSCO South Korea 43.126. Shagang Group China 41.107. Ansteel Group China 39.208. Jianlong Group China 31.199. Tata Steel India 30.1510. Shougang Group China 29.34

* Source: World Steel Association

0.76 0.77 0.75 0.77

0.63 0.64 0.64 0.64

1.06 1.06 1.08 1.07

0.4

0.6

0.8

1

1.2

1.4

Feb 1st Mar 1st Apr 1st May 3rd

FX Rates – May 3rd, 2021

USD/AUD Euro/AUD NZD/AUD

0.8

1

0.8

0.8

0.8

0.6

3

0.6

5

0.6

4

0.6

5

1.0

8

1.0

5

1.1

1.1

0.4

0.6

0.8

1

1.2

1.4

NAB ANZ W/PAC CBA

Future FX Rates

USD/AUD Euro/AUD NZD/AUD

Movement since April 1st, 2021:

May 3 Apr 1 Mar 1 Feb 1 Jan 1 Dec 1

BHP Group 47.03 45.65 50.09 44.12 42.43 38.56

Bisalloy Steel 1.10 1.05 1.05 1.15 1.40 1.36

BlueScope Steel 21.46 20.02 17.25 16.62 17.48 17.20

Fletcher Building 6.83 6.45 6.14 5.83 5.44 5.48

Rio Tinto 120.09 112.00 127.70 111.27 113.83 102.95

Sims Ltd 15.89 15.08 13.60 12.37 13.45 11.19

Company Share Prices - (ASX end of day quote in AUD) Currency Changes

AUD is up 2.7%

against the USD

AUD is unchanged

against the Euro

…..will reach the 2019 level again in 2022. Additionally, the recovery in the

global automotive industry is expected to be very strong in the United States

where production levels this year will exceed the 2019 level, whereas the world

automotive industry will reach that mark in 2022.

Australia was not detailed in the WSA outlook, however a slew of economic

indicators bode well for steel usage. No such degree of optimism, however, from

the citizens of Whyalla – Sanjeev Gupta´s spiritual home – who remain anxious

observers of the gathering GFG / Greensill crisis. Credit Suisse is seeking the

wind-up of Whyalla´s steelworks to recoup losses on invoices, which Greensill

packaged into bonds purchased by the Swiss bank. A hearing in the NSW

Supreme Court is scheduled for May 6. Meanwhile, prices in Australia continue

to firm as demand remains strong and shortages and delays plague the

domestic supply situation. Whilst scrap has firmed slightly, most import sources

of supply are taking advantage of the seller´s market mind-set to move prices up

beyond their cost recovery. In a market like this one, the domestic players would

typically be taking advantage to widen their spreads and put extra on the bottom

line. However, their formulae based pricing will mean they either retract from

pricing commitments made, or leave plenty of margin on the table. Eventually,

it´s likely the import option may become the only way to get enough steel. But

given the shipping delays and difficulty in committing to such high pricing more

than three to four months in advance, it is likely the market will remain tight and

short of steel for the next quarter at least. (Return to page 1)

Market Summary - Continued

Source: X-rates.com Banks´ estimate of the value of the AUD at the end of Q3 2021.

AustralianSteel.com

Extensive coverage of steel prices, plus details of services and suppliers

in the Australasian steel industry.

Visit the website: here

Steel Industry Services

Baltic Dry Index Fuel Prices Associations

Industry Insider - Comment

By Simon Pepper*Director of Customs and Logistics, SILA Global

The Baltic Dry Index (BDI) is

issued daily by the London-

based Baltic Exchange. It is a

composite of the Capesize,

Panamax and Supramax

Timecharter Averages. The BDI

is a proxy for dry bulk shipping

stocks and a general bellwether

to shipping markets. Here are

two websites with links to it:

Trading Economics

The Business Times

Variations in petroleum and

diesel prices can critically

impact the final transport costs

of moving steel within Australia.

The Australian Institute of

Petroleum (AIP) is the peak

representative body of

Australia´s downstream

petroleum industry. It publishes

a weekly prices report for

petroleum and diesel.

AIP Petroleum & Diesel prices

The steel, metals and related

industry sectors in Australia

and New Zealand are well

served by numerous peak

bodies and associations. The

website AustralianSteel.com

contains a list of the most

prominent associations which

serve the industry. Click below.

AustralianSteel.com Industry

Associations list

Many services and associations exist to assist people and companiesworking in the steel and metals industries. Here is a selection:

Australia’s anti-dumping system can be a daunting subject

to understand and often difficult to navigate. The Anti-

Dumping Commission (ADC) manages Australia´s anti-

dumping and countervailing system, which states its main

aim being to: “.…investigate claims that dumped and

subsidised imports have injured Australian industry.”

In broad terms, anti-dumping claims can be made by

Australian businesses who are capable of producing a

commodity subject to an investigation. By definition,

“Dumping generally occurs when a company exports a

product into Australia at a price that is lower than the price

charged in the country of manufacture.” This could occur in

different circumstances or for different reasons. The

process of investigation into claims can take quite some

time, depending on the commodity involved, and the

suppliers and importers of the investigated product.

The ADC has a Dumping Commodity Register which lists

the goods currently subject to “measures”. At present, the

list contains 27 commodities, more than half of which are

either steel feed materials, or semi-manufactured or fully

finished steel articles. This is quite a wide net and it is

very easy to be caught up in it.

The Register indicates the commodity, the country of

export, their associated tariff classifications, and

statistical codes. Ensuring that origin information is

available and that your goods are classified correctly is

essential to understanding if dumping may apply. From

this foundation and understanding the goods covered by

the case becomes the next essential step because, even

though your goods may have the same origin and

classification as those listed, they may be excluded from

the case based on the specifications of the material.

There are also certain exporters which are listed as

exempt or have tariff concessions that, if applicable to

your goods, can make the shipment excluded from any

dumping being applicable. Importers are encouraged to

self-assess as to….(click here to continue reading)

• In the US, Nucor, Gerdau, CMC and Steel Dynamics have announced

an immediate $40/st increase in their rebar prices, blaming tight

domestic supply and a lack of imported material. (Platts)

• Time is running out for Sanjeev Gupta´s GFG Alliance as applications

in the UK to compel the liquidation of three Liberty Steel Group

companies are due to be heard by a judge in early May. (BBC)

• Belgian authorities have melted down more than 22,000 guns and

turned them down into 60 tonnes of recycled steel. It is the third time

Belgian security forces have cooperated with steel giant ArcelorMittal to

collect and destroy firearms. (Reuters)

• Steel exports from India surged 26% in the first quarter of 2021 to total

around 2.47 million metric tonnes. (Scrap Monster)

Offcuts……Steel Around The World Key to Prices

Prices and figures quoted should be taken as indicative numbers only. While all

care has been taken in compiling this newsletter, readers acting upon the

information herein do so entirely at their own risk. The publisher accepts no

responsibility for any consequences arising from commercial decisions made by

readers. Most of the numeric information in this newsletter is freely available at the

sources quoted. Readers are urged to check figures against the original source. All

comments expressed are the opinion of the publisher, unless otherwise stated.

Copyright is reserved for the full contents of the newsletter.

Australian Steel News particularly acknowledges two of its principal sources of

information: S&P Global Platts (Platts) and South East Asia Iron and Steel Institute

(SEAISI).

Australian Steel News (ASN) is a completely independent, monthly newsletter

which is owned and published by Caletablanca Media. ASN and Caletablanca

Media are not in any way connected to any steel industry association or

company or any other entity in Australia. To suggest information you would like

to see included in ASN, email [email protected]. To add yourself to

ASN´s mailing list, email [email protected] with the word ADD in the

subject line. To remove yourself from the list, email [email protected]

with the word REMOVE in the subject line. The Caletablanca Media website is:

www.caletablanca.com

Subscribe / Contact

* Disclaimer

1. Wire Rod – Shanghai Futures

Exchange (SHFE). Standard

bundle size Chinese wire rod

grade HPB235 in diameters 6.5

and 8.0mm. VIEW

2. Steel Rebar China – SHFE

closing price on day converted

at 7.0 Yuan/USD. VIEW

3. Steel Rebar Southeast Asia

CFR – S&P Global Platts

(Platts) daily rebar.

4. Steel Rebar Turkey – London

Metal Exchange (LME) one

month exports FOB Turkish

port. VIEW

5. Steel Scrap Turkey – LME

closing contract price CFR

Turkish port. VIEW

6. HRC North America – LME

closing contract price ex works

Indiana. Short ton price

converted by 110% to per

tonne. VIEW

7. HDG Shanghai – Platts China

FOB export monthly.

8. HRC Southeast Asia – Platts

daily HRC CFR SS400.

9. HRC China – LME closing

contract price FOB China.

VIEW

10. Slab Southeast Asia – Platts

monthly CFR Southeast Asia.

11. Coking Coal – Platts Australian

premium low volume HCC.

12. Iron Ore – NAB sourced

Bloomberg indicative CFR for

62 Fe shipping to Qingdao.

VIEW

13. Non-Ferrous Metals – LME

official closing day price for:

copper, aluminium, nickel and

zinc. VIEW

14. Vanadium – Ferro vanadium

80% China price in USD/kilo

from Vanadiumprice website.

VIEW

15. Taiwan Containerized Scrap –

Platts weekly Taiwan CFR.

16. East Asia Import Scrap – Platts

weekly East Asia Import CFR.

17. Ferro Alloy Prices – Argus

Metals International mid-point

price of range on date

indicated.

18. FX Rates – Sourced from X-

rates.com. VIEW

19. Company Share Prices –

Australian Stock Exchange end

of day quote in AUD. VIEW