Embed Size (px)

Citation preview

Sector: Metals

Sector view: Neutral

Sensex: 19,392

52 Week h/l (Rs): 116 / 73

Market cap (Rscr) : 34,366

6m Avg vol (‘000Nos): 3,047

Bloomberg code: SAIL IB

BSE code: 500113

NSE code: SAIL

FV (Rs): 10

Prices as on 05 Dec, 2012

Company rating grid

Low High

1 2 3 4 5

Earnings Growth

Cash Flow

B/S Strength

Valuation appeal

Risk

Share price trend

50

70

90

110

130

150

Dec‐11 Apr‐12 Aug‐12 Dec‐12

SAIL Sensex

Share holding pattern

75

80

85

90

95

100

Dec‐11 Mar‐12 Jun‐12 Sep‐12

Promoters Institutions Others%

Rating: SELL Target (9‐12 months): Rs70.7

CMP: Rs83.2

Downside: 15%

Company ReportDecember 06, 2012

Research Analyst: Tarang Bhanushali

Nikhil Anand [email protected]

Initiating Coverage

Not yet out of the woods

Steel Authority of India Ltd (SAIL) has underperformed the Sensex by 19.7% over the past one year, on account of concerns over the delays in the company’s expansion projects, lower margins and availability of iron ore. SAIL’s expansion plans have been facing delays in project implementation besides cost escalation. Projects which were earlier expected to be completed by FY12 are now estimated to get over in a phased manner by FY14E. Volume growth over the last five years has remained stagnant due to delay in capacity addition and technical issues at various plants.

We believe these issues would continue over the next one year as benefits of the new capacities would set in only from H2 FY14. We expect sales volume growth to remain flat in FY13 and increase 9% yoy to 12.8mn tons in FY14 as the impact of incremental production from new capacities would be offset by the shutdown of old facilities. The full benefit of new capacities would be witnessed only by FY15, where we expect the company to register a volume growth of 14.6% yoy to 14.7mn tons.

SAIL’s Gua mines have remained closed since June ’11 and its Bolani mines were also shut for a month due to expiry of forest clearance. The company’s margins have been hit over the last two years on the back of high fixed costs, high coking coal costs, increase in consumption of externally purchased coke and degrading product mix. EBIDTA/ton in Q3 FY13 is expected to decline to its lowest level since FY04 as steel prices decline sequentially. Though we expect margins to improve going ahead, we believe it would remain below its 5‐year historical average. Earnings growth would further decline on account of rising interest costs and depreciation.

At the CMP, the stock is trading at 7.2x FY14E EV/EBIDTA, higher than its domestic as well as international peers. We assign no value to the company’s CWIP, given the dismal track record of SAIL’s execution capabilities. We value SAIL at 6.5x FY14E EV/EBIDTA and arrive at a fair value of Rs70.7. At the CMP, the stock is 15% above our fair value; Initiate coverage with a SELL rating.

Financial summary Y/e 31 Mar (Rs m) FY12 FY13E FY14E FY15E

Revenues 466,582 485,804 517,089 623,895

yoy growth (%) 7.5 4.1 6.4 20.7

OPM (%) 13.8 12.3 15.9 19.3

Pre‐exceptional PAT 38,674 27,784 36,768 59,104

Reported PAT 35,931 27,784 36,768 59,104

yoy growth (%) (28.3) (22.7) 32.3 60.7

EPS (Rs) 9.4 6.7 8.9 14.3

P/E (x) 8.9 12.4 9.3 5.8

EV/EBITDA (x) 7.2 9.4 7.1 5.0

Debt/Equity (x) 0.5 0.6 0.6 0.6

RoE (%) 9.9 6.7 8.4 12.5

RoCE (%) 10.5 7.9 9.4 13.0 Source: Company, India Infoline Research

Steel Authority of India Ltd

Steel Authority of India Ltd

2

Expansion projects to start contributing from H2 FY14E SAIL has been investing heavily over the last four years to raise its crude steel capacity from the current 13.4mtpa to 21.4mtpa and to also improve its product mix. However, the company has been facing delays in its project implementation and has also witnessed cost escalation for the same. Capex estimate for the expansion plan has increased from the initial capex target of Rs540bn to Rs618bn. Of this, the company proposes to spend around Rs227.4bn on technology upgradation and modernization of its facilities, while the balance Rs391bn would be utilised for capacity expansions. The company has witnessed significant delays in its capex plans and the projects which were earlier expected to be completed by FY12 are now estimated to get over in a phased manner by FY14. Till Q2 FY13, the company has incurred a capex of Rs459bn and is expected to spend a further 80bn in H2 FY13.

Capex estimate for the expansion plan has increased from the initial capex target of Rs540bn to Rs618bn

Capex of Rs619bn planned for expansion cum upgradation of existing capacities

…of that SAIL has incurred a capex of Rs459bn till date

391.370.4

35.1

121.9 618.7

0

100

200

300

400

500

600

700

1 2 3 4 5

(Rs bn)

Expansion Product Mix improvement

Upgradation/Modernisation De‐bottleneckingTotal Estimated Value

12

22

52

106113 110

44

0

20

40

60

80

100

120

FY07

FY08

FY09

FY10

FY11

FY12

H1FY13

(Rs bn)

Source: Company, India Infoline Research

Product mix in FY12 Product mix after expansion, share of semis to reduce

8%

12%

4%

21%

5%

14%

33%

2%1% HR Coils

Plates

Rly Products

Bars & Rods

Structurals

Semis

PET Products

Galvanized

CR Coils

8%

19%

14%

12%

11%

16%

16%

3%1%

HR Coils

Plates

Rly Products

Bars & Rods

Structurals

Semis

PET Products

Galvanized

CR Coils

Source: Company, India Infoline Research

Steel Authority of India Ltd

3

Capacity expansion

Plants Hot Metal (MTPA) Crude Steel(MTPA) Saleable Steel(MTPA)

FY12 After

Expansion FY12 After

Expansion FY12 After

Expansion

Bhilai Steel Plant (BSP) 5.1 7.5 4.9 7.0 4.3 6.6

Durgapur Steel Plant (DSP) 2.1 2.5 1.9 2.2 1.8 2.1

Rourkela Steel Plant (RSP) 2.3 4.5 2.2 4.2 2.1 4.0

Bokaro Steel Plant (BSL) 4.0 5.8 3.6 4.6 3.3 4.2

IISCO Steel Plant (ISP) 0.5 2.9 0.3 2.5 0.3 2.4

Visvesvaraya Iron & Steel Plant (VISL) 0.1 0.3 0.1 0.2 0.1 0.2

Alloy Steel Plant (ASP) ‐ ‐ 0.2 0.5 0.2 0.4

Salem Steel Plant (SSP) ‐ ‐ 0.1 0.2 0.3 0.3

Total 14.1 23.5 13.4 21.4 12.4 20.2 Source: Company, India Infoline Research

The company expects to commission the plants in a phased manner over the next two years. The updates of the various projects are IISCO Steel Plant, Burnpur: IISCO is the first large expansion project which would be commissioned among other projects. The company is adding incremental saleable steel capacity of 2.1mtpa, while it stated that after commissioning of the new plant, the old capacity of 0.3mt would be phased out. The coke oven battery which was commissioned in Q1 FY13 has developed some technical issues and is expected to ramp up in Q4 FY13. The company will start the sinter plant once the coke oven gases become available, as the gases from the coke oven plant would be used as a feed in the sinter plant. The blast furnace is also ready and will be commissioned as soon as the coke oven battery and the sinter plant become operational. The development of the Steel Melting Shop (SMS) will be completed sometime in the next quarter. The wire rod mill (0.5mtpa) is already commissioned and is also waiting for the feed from the coke over. The rest of the value added capacity of heavy section mill (0.6mtpa) and bar mill (0.75mtpa) is on track and the expansion of the integrated steel plant will be completed by March, FY13. The company would start its trial runs for the integrated plant in Q1 FY14 and hence volume growth from the plant would be witnessed only in H2 FY14. Volumes in FY13 at the IISCO plant are expected to be around the same levels as those of FY12 and a substantial increase will come only by H2 FY14. The expansion plans at ISP have incurred cost overruns to the tune of Rs26bn. The estimated cost is now Rs164bn as compared to the initial cost of Rs138bn. Bokaro Steel Plant: Capacity expansion at Bokaro Steel Plant consists of building a new Cold Rolling Mill (CRM) (1.2mtpa), up‐gradation of SMS and rebuilding of coke oven batteries. These facilities will enhance the hot steel capacity from 4mtpa to 5.8mtpa and that of crude steel from 3.65mtpa to 4.61mtpa. The company has completed re‐building of coke‐oven batteries, while it is upgrading the third blast furnace. Repair of Blast Furnace‐1, Blast Furnace‐2 and Blast Furnace‐5 has been completed while cold trials have begun from the new CRM complex. The company expects the production level at Bokaro Steel Plant to be slightly lower in FY13 than last year due to some shutdowns undertaken for maintenance work since September ’12.

The coke oven battery which was commissioned in Q1 FY13 has developed some technical issues and is expected to ramp up in Q4 FY13

Volumes in FY13 at the IISCO plant are expected to be around the same levels as those of FY12 and a substantial increase will come only by H2 FY14 The new facilities will enhance the hot steel capacity from 4mtpa to 5.8mtpa and that of crude steel from 3.65mtpa to 4.61mtpa

Steel Authority of India Ltd

4

Bhilai Steel Plant (BSP): A total of five projects were part of the modernisation cum expansion plan at Bhilai Steel Plant. A blast furnace with a capacity of 2.8mtpa, a bar rod mill of 0.9mtpa capacity, 1.2mtpa Universal Rail Mill, a SMS of 4mtpa capacity along with a sinter plant are part of the expansion plans. BSP has completed the first part of SMS and the inauguration of the erection activity of furnace shell in February, 2012. The company is phasing out its twin hearth furnace but maintains that there will be no significant impact as the phase‐out will be concurrent with the ramp‐up of new capacity. The blast furnace along with the other projects should be completed by September ‘13. The expansion of BSP got delayed by ~18 months due to inadequate manpower and non‐deployment of modern equipments. We do not expect any incremental volumes from the new plant in FY14 and estimate the benefits to be accrued only by FY15. Rourkela Steel Plant (RSP): The facilities being added at Rourkela Steel Plant include a sinter, a coke oven battery, a new 4.3 meter wide plate mill (0.9mtpa), BOF and a blast furnace, which will enhance the hot metal capacity from 2mtpa to 4.5mtpa. Presently, the construction of the sinter plant is completed and it will start operations with the availability of coke oven gases. Coke oven batteries have been completed with the Blast Furnace already undergoing trial runs and the company expects to start operations by March ‘13. Other units like steel melting shop (SMS), casters and plate mill would start operations by the end of Q4 FY13. The initial cost of modernisation and expansion plans was estimated at ~Rs79bn, but the actual cost incurred stands at Rs118bn. Besides the blast furnace, the remaining facilities are also expected to be completed by this fiscal year. We expect meaningful volume growth from the new capacity to come from H2 FY14. However, overall volume growth from the RSP facility would be restricted with a maintenance shutdown of the old blast furnace. Durgapur Steel Plant (DSP): The expansion plan of DSP includes increasing hot metal capacity from 2.1mtpa to 2.5mtpa, introduction of energy efficient technology and rebuilding of coke oven batteries. However, the major value driver is the expansion of downstream facilities. The company is adding 0.75mtpa of caster and 1mtpa of medium structural mill capacity, which would improve value addition. The expected date of commission has been delayed by three months to March ‘13. Currently, Durgapur steel plant’s sales volume comprises 55‐60% of semis and is expected to reduce significantly once the structural mill is commissioned.

The blast furnace along with the other projects should be completed by September ‘13

We do not expect any incremental volumes from the new plant in FY14 and estimate the benefits to be accrued only by FY15 Coke oven batteries have been completed with the Blast Furnace already undergoing trial runs and the company expects to start operations by March ‘13 Overall volume growth from the RSP facility would be restricted with a maintenance shutdown of the old blast furnace The major value driver is the expansion of downstream facilities. The company is adding 0.75mtpa of caster and 1mtpa of medium structural mill capacity, which would improve value addition

Steel Authority of India Ltd

5

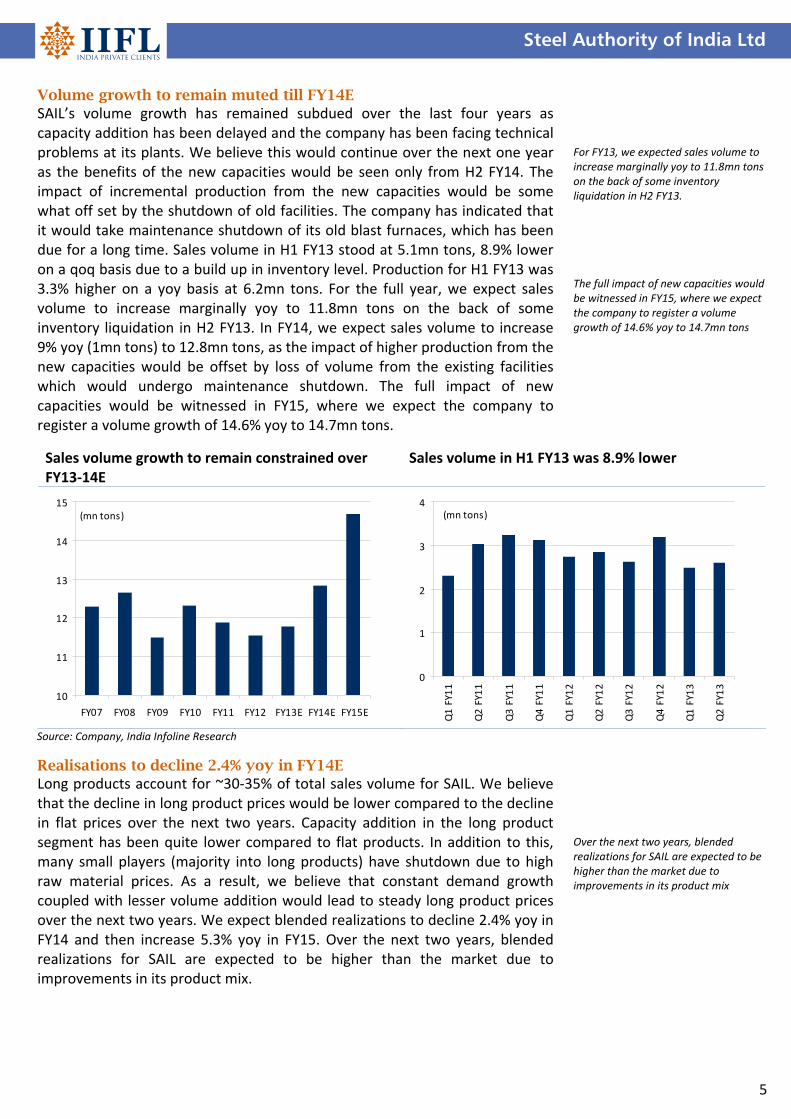

Volume growth to remain muted till FY14E SAIL’s volume growth has remained subdued over the last four years as capacity addition has been delayed and the company has been facing technical problems at its plants. We believe this would continue over the next one year as the benefits of the new capacities would be seen only from H2 FY14. The impact of incremental production from the new capacities would be some what off set by the shutdown of old facilities. The company has indicated that it would take maintenance shutdown of its old blast furnaces, which has been due for a long time. Sales volume in H1 FY13 stood at 5.1mn tons, 8.9% lower on a qoq basis due to a build up in inventory level. Production for H1 FY13 was 3.3% higher on a yoy basis at 6.2mn tons. For the full year, we expect sales volume to increase marginally yoy to 11.8mn tons on the back of some inventory liquidation in H2 FY13. In FY14, we expect sales volume to increase 9% yoy (1mn tons) to 12.8mn tons, as the impact of higher production from the new capacities would be offset by loss of volume from the existing facilities which would undergo maintenance shutdown. The full impact of new capacities would be witnessed in FY15, where we expect the company to register a volume growth of 14.6% yoy to 14.7mn tons.

Realisations to decline 2.4% yoy in FY14E Long products account for ~30‐35% of total sales volume for SAIL. We believe that the decline in long product prices would be lower compared to the decline in flat prices over the next two years. Capacity addition in the long product segment has been quite lower compared to flat products. In addition to this, many small players (majority into long products) have shutdown due to high raw material prices. As a result, we believe that constant demand growth coupled with lesser volume addition would lead to steady long product prices over the next two years. We expect blended realizations to decline 2.4% yoy in FY14 and then increase 5.3% yoy in FY15. Over the next two years, blended realizations for SAIL are expected to be higher than the market due to improvements in its product mix.

For FY13, we expected sales volume to increase marginally yoy to 11.8mn tons on the back of some inventory liquidation in H2 FY13. The full impact of new capacities would be witnessed in FY15, where we expect the company to register a volume growth of 14.6% yoy to 14.7mn tons

Over the next two years, blended realizations for SAIL are expected to be higher than the market due to improvements in its product mix

Sales volume growth to remain constrained over FY13‐14E

Sales volume in H1 FY13 was 8.9% lower

10

11

12

13

14

15

FY07 FY08 FY09 FY10 FY11 FY12 FY13E FY14E FY15E

(mn tons)

0

1

2

3

4

Q1 FY11

Q2 FY11

Q3 FY11

Q4 FY11

Q1 FY12

Q2 FY12

Q3 FY12

Q4 FY12

Q1 FY13

Q2 FY13

(mn tons)

Source: Company, India Infoline Research

Steel Authority of India Ltd

6

Employee costs to swell over the next one year SAIL’s margins over the years have been impacted by high employee costs. Staff cost has accounted for ~20% of total costs for SAIL; the highest amongst the large steel manufacturers. Even though SAIL has managed to reduce its headcount by ~15,000 over the last three years, total staff costs have increased. SAIL’s 5‐year wage agreement for its non‐executive grade employees (50% of total wage bill) expired on December ’11. The company is negotiating with the labour unions and has made provision for 12.5% increase in wages (in addition to the annual inflation linked increase). We believe that the labor union would demand ~25% increase in wages, inline with that of other PSU Coal India. We expect share of employee costs of total costs to increase from 20% in FY12 to 23% in FY14.

Staff cost has accounted for ~20% of total costs for SAIL, the highest amongst the large steel manufacturers SAIL has managed to reduce its head count by ~15,000 over the last three years

Average realizations to stay above Rs40,000/ton Blended realizations hit a peak in Q1 FY13

20,000

25,000

30,000

35,000

40,000

45,000

FY07

FY08

FY09

FY10

FY11

FY12

FY13E

FY14E

FY15E

(Rs/ton)

20,000

25,000

30,000

35,000

40,000

45,000

Q1 FY11

Q2 FY11

Q3 FY11

Q4 FY11

Q1 FY12

Q2 FY12

Q3 FY12

Q4 FY12

Q1 FY13

Q2 FY13

(Rs/ton)

Source: Company, India Infoline Research

Head count has reduced by ~29,000 over the period FY07‐H1 FY13

Employee cost to jump in H2 FY13

80

100

120

140

FY07

FY08

FY09

FY10

FY11

FY12

H1 FY13

(Nos)

0

20

40

60

80

100

120

FY07

FY08

FY09

FY10

FY11

FY12

FY13E

FY14E

FY15E

(Rs bn)

Source: Company, India Infoline Research

Steel Authority of India Ltd

7

EBIDTA/ton to improve marginally in FY14E SAIL’s margins over the last two years have shrunk sharply on account of high coking coal costs, shutdown of its coke oven batteries and inferior product mix. EBIDTA/ton in FY12 declined to Rs5,557/ton, the lowest level since FY06. Rising employee costs have also added to the pressure on margins. Average cost of production has increased sharply from Rs25,317/ton in FY10 to Rs34,853/ton in FY12. In fact in Q2 FY13, this has jumped to Rs37,347/ton as coke oven batteries were shut down and sales volume were lower. This combined with a decline in realizations pushed EBIDTA/ton down to Rs4,267/ton, the lowest since FY04. We expect EBIDTA/ton to decline further in Q3 FY13 as coke oven batteries at IISCO are not ready and the company will have to buy coke from external market. The decline in realizations on a qoq basis would further add to the pressure on margins. However, by Q4 FY13, coke oven batteries are expected to stabilize, which would lead to lower external coke purchase. In addition to this, costs are expected to go down on the back of lower coking coal prices. We expect EBIDTA/ton to increase marginally in FY14 to Rs6,410/ton from Rs5,074/ton in FY13. In FY15, a jump in volumes and estimate of higher steel prices would lead to a jump in EBIDTA/ton to Rs8,179/ton.

FY13E operating profit to fall to FY06 levels

‐

20

40

60

80

100

120

140

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13E FY14E FY15E

(Rs bn)

0

5

10

15

20

25

30(%)

Operating profit OPM

Source: Company, India Infoline Research

Average cost of production has increased sharply from Rs25,317/ton to Rs34,853/ton in FY12

We expect EBIDTA/ton to decline further in Q3 FY13 as coke oven batteries at IISCO are not ready and the company will have to coke from external market

EBIDTA/ton to improve marginally in FY14E … to touch its lowest level since FY04 in Q3 FY13

0

2,000

4,000

6,000

8,000

10,000

FY07

FY08

FY09

FY10

FY11

FY12

FY13E

FY14E

FY15E

(Rs/ton)

0

2,000

4,000

6,000

8,000

10,000

Q1 FY11

Q2 FY11

Q3 FY11

Q4 FY11

Q1 FY12

Q2 FY12

Q3 FY12

Q4 FY12

Q1 FY13

Q2 FY13

Q3 FY13E

(Rs/ton)

Source: Company, India Infoline Research

Steel Authority of India Ltd

8

Availability of long term cheap iron ore at risk SAIL has 100% captive iron ore and currently depends on four mines for its iron ore requirements. The company plans to meet the requirement from the new capacities by raising its mining capacity at the current mines and by starting 4 new mines. The company is currently mining at Kiriburu, Meghataburu and Bolani in Orissa and Gua mines in Jharkhand. Iron ore capacity is expected to rise from ~20mtpa currently to ~58mt as new capacity gets commissioned. Of these, majority of the future requirements will be met from Rowghat (14mtpa) and Chiria (7mtpa).

Iron ore integration

Mine (mtpa) Existing Capacity

After expansion Remarks

Kiriburu 4.3 5.5

Meghataburu 4.3 6.5 Expansion to be completed in line with the commissioning of the new plants

Bolani 4.1 10 Forest clearance has been extended for some time

Gua 2.4 10 Closed for the last 17 months due to absence of environmental clearance

New Pellet Plants New 5 To use existing stock of iron ore fines Barsua, Kalta, Taldih 3.3 6.5

Environmental clearance received from MOEF

Rowghat New 12 All statutory clearances received, but is situated in Naxal belt

Chiria 1.5 7.5 Stage‐I forest clearance received, is situated in naxal belt

Source: Company, India Infoline Research

The Kirburu and the Meghataburu mines are currently the major suppliers of iron ore for the company. The Gua mines have stopped operations since June ‘11 on account of absence of environmental and forest clearance. The Bolani mines too were shut in last month post the expiry of its temporary working permit. However, the management has indicated that it has received the temporary extension and would continue to operate the mines till the time the report is tabled. The state wild life department is expected to submit a wildlife management plan to MOEF, with the latter’s go‐ahead required to re‐start mining.

SAIL plans to outsource the development of the Rowghat mine in Chhattisgarh and Chiria mine in Jharkhand. However, Naxalite activity in the area has long delayed commissioning of the Rowghat mine. The company has asked for extra security from the Government to start mining in the region. The management has indicated that the phased deployment of the forces has already begun. The crucial rail and road infrastructure building work would precede the mine development to move men and machines to the inaccessible deposit areas. While environment clearance for Chiria mine is already in place, the company is awaiting the Stage‐II forest clearance. The mine is also located in the Naxal belt and would take some time to commission. As a result, we believe that the availability of long term iron ore is at risk as some of the existing mines are exhausted, clearance for its premier two mines is pending and starting new mines would take some time and would also lead to higher costs for the company.

The company is currently mining at Kiriburu, Meghataburu and Bolani in Orissa and Gua mines in Jharkhand The Gua mines have stopped operations since June ‘11 on account of absence of environmental and forest clearance SAIL plans to outsource the development of the Rowghat mine in Chhattisgarh and Chiria mine in Jharkhand While environment clearance for Chiria mine is already in place, the company is awaiting the Stage‐II forest clearance

Steel Authority of India Ltd

9

Debt levels to jump 54% over FY12-15E SAIL, over the last three years, has been investing heavily in expanding its capacity. With the huge capex it has incurred, debt levels have doubled over the period FY09‐12. Gross debt increased from 87bn in FY09 to Rs184bn in FY12 which led to the company reducing itself from a net cash company to a net debt company by FY12. We expect debt levels to jump further by 54% over the period FY12‐15 as the company expects to incur a capex of ~Rs250bn over the same period. Net debt/equity is expected to increase from 0.3x in FY12 to 0.5x in FY14.

Return ratios to remain muted A combination of lower profitability and a jump in share of Capital Work In Progress (CWIP) would keep RoE and RoCE in single digits over the next two years. SAIL’s RoE has declined sharply from 36.3% in FY08 to 9.9% in FY12 as the company’s EBIT declined from 29% to 14% over the same period. In addition to this, CWIP as a % of total capital employed increased from 12.2% in FY08 to 46.8% in FY12. We expect this scenario to continue for the next two years as benefits from the new capacities would be felt only in H2 FY14 and margins are expected to remain subdued.

Debt levels to jump further by 54% over the period FY12‐15 as the company expects to incur a capex of ~Rs250bn over the same period

SAIL’s RoE has declined sharply from 36.3% in FY08 to 9.9% in FY12

CWIP as a % of total capital employed increased from 12.2% in FY08 to 46.8% in FY12

Gross debt to spiral 54% over FY12‐15E We estimate SAIL to incur a capex of Rs266bn over FY13‐15E

0

50

100

150

200

250

300

FY07

FY08

FY09

FY10

FY11

FY12

FY13E

FY14E

FY15E

(Rs bn)

0

20

40

60

80

100

120

FY07

FY08

FY09

FY10

FY11

FY12

FY13E

FY14E

FY15E

(Rs bn)

Source: Company, India Infoline Research

CWIP as a % of capital employed would jump to 48.4% in FY13E

RoE and RoCE to remain in single digits over the next two years

0

10

20

30

40

50

60

FY08 FY09 FY10 FY11 FY12 FY13E FY14E FY15E

(%)

0

10

20

30

40

50

FY07 FY08 FY09 FY10 FY11 FY12 FY13E FY14E FY15E

(%)

RoE RoCE

Source: Company, India Infoline Research

Steel Authority of India Ltd

10

Underperformance to continue; Reinitiate with SELL SAIL has underperformed the Sensex by 19.7% and the BSE Metal Index by 1.3% over the past one year, on account of concerns over the delays in the company’s expansion projects, lower margins and availability of iron ore. SAIL’s expansion plan has been facing delays in its project implementation and has also witnessed cost escalation. Projects which were earlier expected to be completed by FY12 are now estimated to get over in a phased manner by FY14E. Volume growth over the last five years has remained stagnant as capacity addition has been delayed and the company has been facing technical issues at various plants. We believe these issues would continue over the next one year as benefits of the new capacities would set in only from H2 FY14. We expect sales volume growth to remain flat in FY13 and increase 9% yoy to 12.8mn tons in FY14 as the impact of incremental production from new capacities would be offset by the shutdown of old facilities. The full benefit of new capacities would be witnessed only by FY15, where we expect the company to register a volume growth of 14.6% yoy to 14.7mn tons. SAIL’s Gua mines have remained closed since June ’11 and its Bolani mines were also shut for a month due to expiry of forest clearance. The company’s margins have been hit over the last two years on the back of high fixed costs, high coking coal costs, increase in consumption of externally purchased coke and degrading product mix. EBIDTA/ton in Q3 FY13 is expected to decline to its lowest level since FY04 as steel prices decline sequentially. Though we expect margins to improve going ahead, we believe it would remain below its 5‐year historical average. Earnings growth would further decline on account of rising interest costs and depreciation. At the CMP, the stock is trading at 7.2x FY14 EV/EBIDTA, higher than its domestic as well as international peers. We assign no value to the company’s CWIP, given the dismal track record of SAIL’s execution capabilities. We value SAIL at 6.5x FY14E EV/EBIDTA and arrive at a fair value of Rs70.7. At the CMP, the stock is 15% above our fair value; Initiate coverage with a SELL rating. Marginally below its 5‐yr average EV/EBIDTA

0

2

4

6

8

10

12

14

16

Oct‐07 Jun‐08 Mar‐09 Dec‐09 Sep‐10 Jun‐11 Mar‐12 Dec‐12

EV/EBIDTA (x) Average EV/EBIDTA (x)

Source: Company, India Infoline Research

SAIL has underperformed the Sensex by 19.7% and the BSE Metal Index by 1.3% over the past one year

In FY14, we expect sales volume to increase 9% yoy (1mn tons) to 12.8mn tons

EBIDTA/ton in Q3 FY13 is expected to decline to its lowest level since FY04 as steel prices decline sequentially

At the CMP, the stock is trading at 7.2x FY14 EV/EBIDTA, higher than its domestic as well as international peers

Steel Authority of India Ltd

11

Financials Income statement Y/e 31 Mar (Rs mn) FY12 FY13E FY14E FY15E

Revenue 466,582 485,804 517,089 623,895

Operating profit 64,163 59,704 82,237 120,236

Depreciation (16,859) (19,504) (23,555) (27,026)

Interest expense (7,782) (11,111) (14,264) (15,971)

Other income 16,046 10,833 8,413 7,687

Profit before tax 55,569 39,921 52,831 84,926

Taxes (16,897) (12,139) (16,064) (25,823)

Minorities and other 1 1 1 1

Adj. profit 38,674 27,784 36,768 59,104

Exceptional items (2,742) 0 0 0

Net profit 35,931 27,784 36,768 59,104

Balance sheet Y/e 31 Mar (Rs mn) FY12 FY13E FY14E FY15E

Equity capital 41,305 41,305 41,305 41,305

Reserves 361,426 382,572 410,587 455,620

Net worth 402,732 423,878 451,892 496,926

Debt 184,513 239,513 279,513 284,513

Deferred tax liab (net) 17,817 18,121 18,121 18,121

Total liabilities 605,061 681,512 749,526 799,560

Fixed assets 470,800 563,139 624,584 667,558

Investments 685 685 685 685

Net working capital 66,954 95,802 86,797 101,216

Inventories 138,989 161,911 158,877 191,693

Sundry debtors 48,478 50,475 53,726 64,823

Other current assets 59,381 61,827 65,809 79,402

Sundry creditors (80,985) (84,322) (89,752) (108,291)

Other current liabilities (98,909) (94,090) (101,862) (126,412)

Cash 66,622 21,886 37,460 30,100

Total assets 605,061 681,512 749,526 799,560

Cash flow statement Y/e 31 Mar (Rs mn) FY12 FY13E FY14E FY15E

Profit before tax 55,569 39,921 52,831 84,926

Depreciation 16,859 19,504 23,555 27,026

Tax paid (16,897) (12,139) (16,064) (25,823)

Working capital ∆ (32,854) (28,848) 9,004 (14,419)

Operating cashflow 22,678 18,439 69,326 71,710

Capital expenditure (95,515) (111,843) (85,000) (70,000)

Free cash flow (72,838) (93,404) (15,674) 1,710

Equity raised 251 (23) 0 (0)

Investments (77) ‐ ‐ ‐

Debt financing/ disposal

(28,089) 55,000 40,000 5,000

Dividends paid (9,600) (6,614) (8,753) (14,071)

Other items (503) 306 1 1

Net ∆ in cash (110,855) (44,737) 15,574 (7,359)

Key ratios Y/e 31 Mar FY12 FY13E FY14E FY15E

Growth matrix (%)

Revenue growth 7.5 4.1 6.4 20.7

Op profit growth (18.2) (7.0) 37.7 46.2

EBIT growth (18.0) (19.4) 31.5 50.4

Net profit growth (19.2) (28.2) 32.3 60.7

Profitability ratios (%)

OPM 13.8 12.3 15.9 19.3

EBIT margin 13.6 10.5 13.0 16.2

Net profit margin 8.3 5.7 7.1 9.5

RoCE 10.5 7.9 9.4 13.0

RoNW 9.9 6.7 8.4 12.5

RoA 4.9 3.4 4.1 6.0

Per share ratios

EPS 9.4 6.7 8.9 14.3

Dividend per share 2.0 1.3 1.8 2.9

Cash EPS 13.4 11.4 14.6 20.9

Book value per share 97.5 102.6 109.4 120.3

Valuation ratios (x)

P/E 8.9 12.4 9.3 5.8

P/CEPS 6.2 7.3 5.7 4.0

P/B 0.9 0.8 0.8 0.7

EV/EBIDTA 7.2 9.4 7.1 5.0

Payout (%)

Dividend payout 24.8 23.8 23.8 23.8

Tax payout 30.4 30.4 30.4 30.4

Liquidity ratios

Debtor days 38 38 38 38

Inventory days 109 122 112 112

Creditor days 63 63 63 63

Leverage ratios

Interest coverage 8.1 4.6 4.7 6.3

Net debt / equity 0.3 0.5 0.5 0.5

Net debt / op. profit 1.8 3.6 2.9 2.1

Du‐Pont Analysis Y/e 31 Mar FY12 FY13E FY14E FY15E

Tax burden (x) 0.70 0.70 0.70 0.70

Interest burden (x) 0.88 0.78 0.79 0.84

EBIT margin (x) 0.14 0.11 0.13 0.16

Asset turnover (x) 0.60 0.59 0.57 0.63

Financial leverage (x) 2.01 1.99 2.06 2.08

RoE (%) 9.9 6.7 8.4 12.5

Recommendation parameters for fundamental reports:

Buy – Absolute return of over +10%

Market Performer – Absolute return between ‐10% to +10%

Sell – Absolute return below ‐10%

Published in 2012. © India Infoline Ltd 2012 This report is for the personal information of the authorised recipient and is not for public distribution and should not be reproduced or redistributed without prior permission. The information provided in the document is from publicly available data and other sources, which we believe, are reliable. Efforts are made to try and ensure accuracy of data however, India Infoline and/or any of its affiliates and/or employees shall not be liable for loss or damage that may arise from use of this document. India Infoline and/or any of its affiliates and/or employees may or may not hold positions in any of the securities mentioned in the document. The report also includes analysis and views expressed by our research team. The report is purely for information purposes and does not construe to be investment recommendation/advice or an offer or solicitation of an offer to buy/sell any securities. The opinions expressed are our current opinions as of the date appearing in the material and may be subject to change from time to time without notice. Investors should not solely rely on the information contained in this document and must make investment decisions based on their own investment objectives, risk profile and financial position. The recipients of this material should take their own professional advice before acting on this information. India Infoline and/or its affiliate companies may deal in the securities mentioned herein as a broker or for any other transaction as a Market Maker, Investment Advisor, etc. to the issuer company or its connected persons. This report is published by IIFL ‘India Private Clients’ research desk. IIFL has other business units with independent research teams separated by 'Chinese walls' catering to different sets of customers having varying objectives, risk profiles, investment horizon, etc and therefore, may at times have, different and contrary views on stocks, sectors and markets. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to local law, regulation or which would subject IIFL and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. IIFL, IIFL Centre, Kamala City, Senapati Bapat Marg, Lower Parel (W), Mumbai 400 013. For Research related queries, write to: Amar Ambani, Head of Research at or [email protected] For Sales and Account related information, write to customer care: [email protected] or call on 91‐22 4007 1000

![IIFL Holdings Ltdcontent.indiainfoline.com/admin/PDF/corporate_presentation_INR_Q3… · IIFL Holdings Ltd [Bloomberg Code: IIFL IN ] Investor Presentation April 2016 . 17.5 19.6](https://img.pdfslide.us/doc/110x75/5edff300ad6a402d666b3977/iifl-holdings-iifl-holdings-ltd-bloomberg-code-iifl-in-investor-presentation.jpg)