Embed Size (px)

Citation preview

Status of Research in SAFA Member Bodies

1

Executive Summary Recognizing the importance of research as one of the core elements for the

development of any profession, South Asian Federation of Accountants (SAFA) had

commissioned a study to find out the status of Research in its member bodies. The

Institute of Cost and Management Accountants of Pakistan was assigned this task in

the SAFA Assembly held in January, 2004.

India

The Institute of Chartered Accountants of India has been a torch bearer in the area of

research. Its Standards Board, Research Committee and Auditing and Assurance

Standards Board and other Committees have issued a large number of publications

most of which are research based, in different spheres of the profession. A good

number of research studies are in hand.

The Institute of Cost and Works Accountants of India has also carried out extensive

research mainly in industrial sector. It has immensely contributed in the development

of accounting literature by framing Cost Accounting Records and Cost Audit Rules for

47 Industries in India. It has also issued a number of research publications in other

areas. A number of research projects are in process.

Pakistan

The Institute of Chartered Accountants of Pakistan (ICAP) has set up different

Committees to carry out research. It has undertaken and accomplished several research

projects. The Institute has also identified several areas to undertake research for future.

Institute of Cost and Management Accountants of Pakistan (ICMAP) has set up a

Research Department, which has undertaken and completed a number of research

studies in professional areas. ICMAP has also developed Cost Accounting Record

Status of Research in SAFA Member Bodies

2

Rules for various industries. The Institute has also identified several research projects

for future.

Bangladesh

The research work in the Institute of Chartered Accountants of Bangladesh is in its

initial phase. A number of research projects are under way in it, mainly directed

towards setting of Standards on Accounting (BSA) and on Auditing (BAS).

The Institute of Cost and Management Accountants of Bangladesh, has carried out

research work and has developed Cost Accounting Record Rules for few industries. It

has also issued research based publications. A number of research projects which are

in hand are in different stages of completion.

Sri Lanka

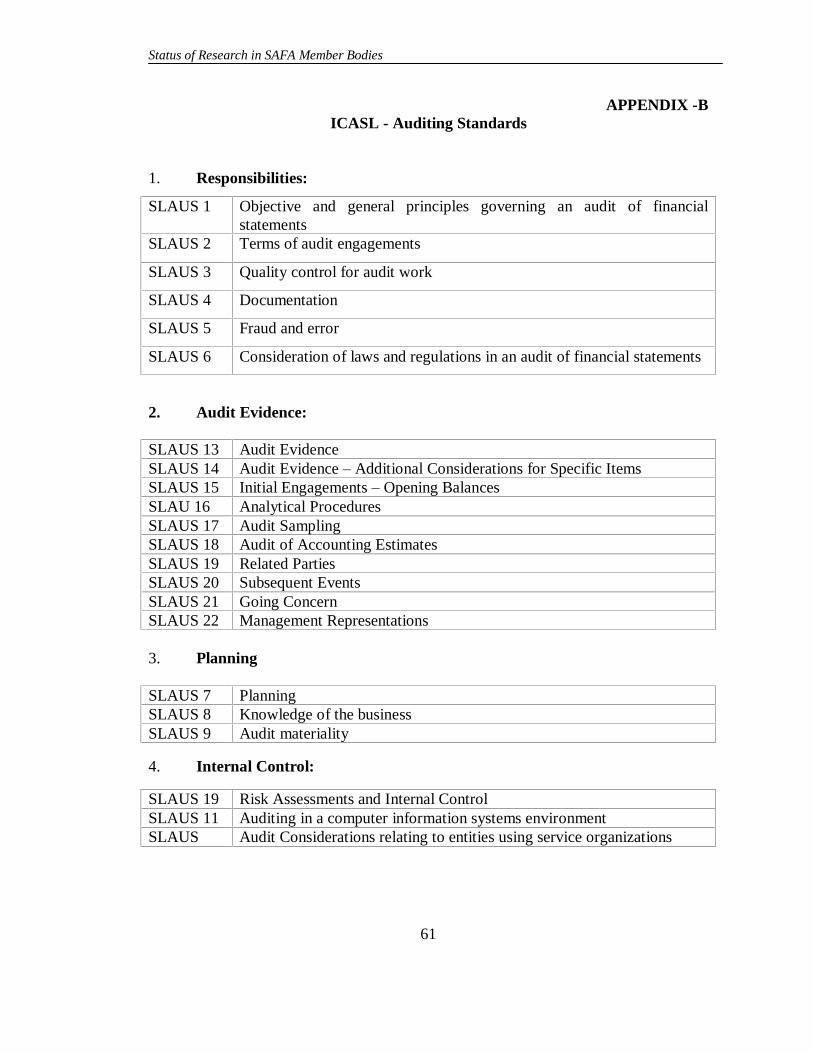

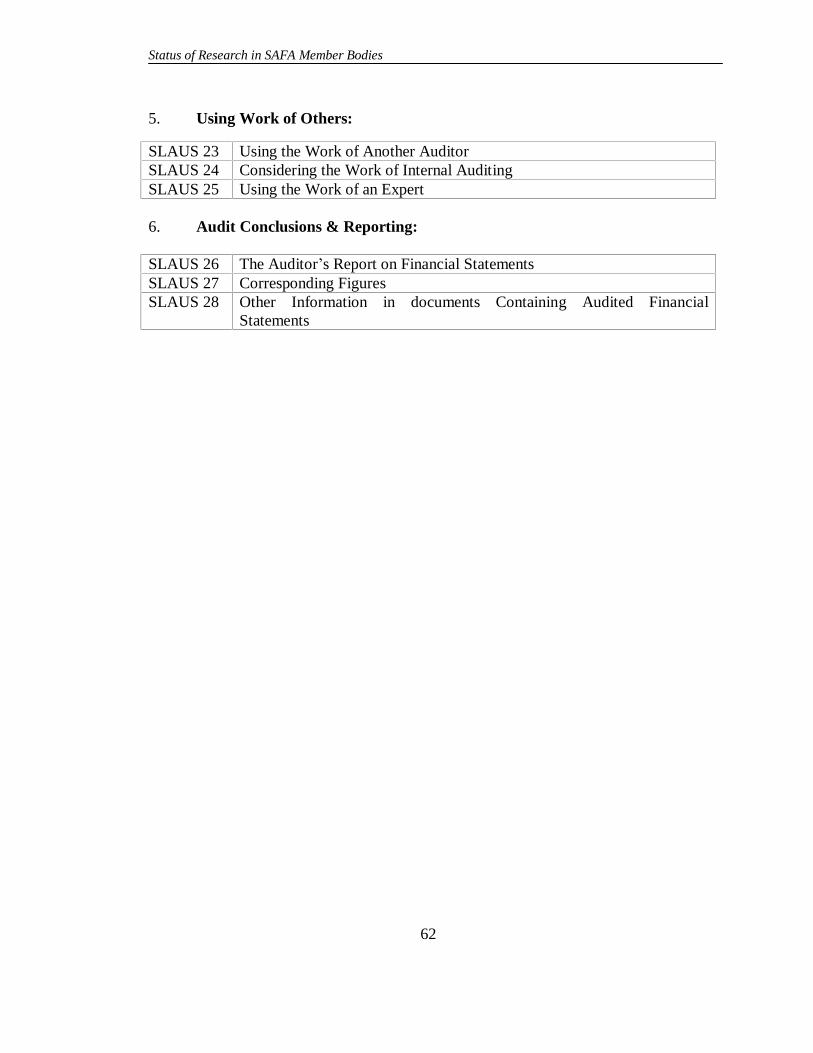

The Institute of Chartered Accountants of Sri Lanka (ICASL), has set up a Technical

Division which has developed Sri Lanka Auditing Standards. It also has launched a

new faculty on Professional Reporting. The Technical Division is also developing

statement of recommended practice for Insurance Contracts.

Nepal

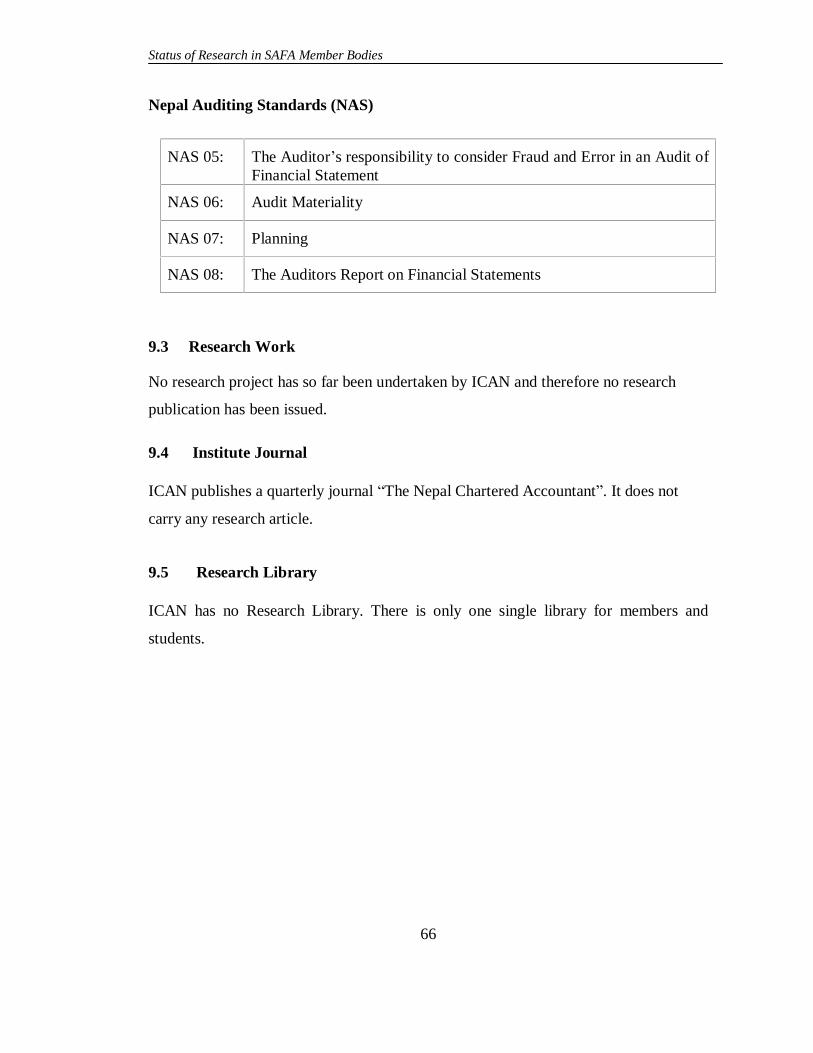

The Institute of Chartered Accountants of Nepal (ICAN) does not have an independent

research department. It has, however, issued few publications on Nepal Accounting and

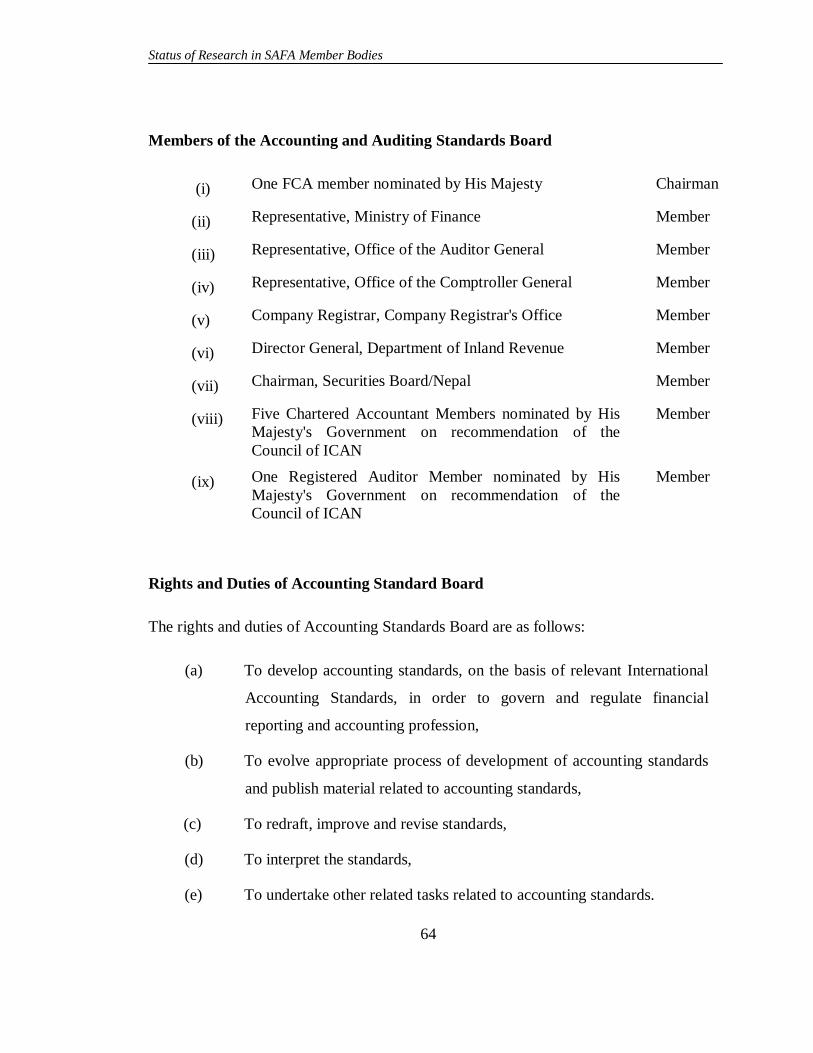

Auditing Standards. The Accounting & Auditing Standards Boards of the Institute

have been assigned to develop further Accounting and Auditing standards for Nepal.

Status of Research in SAFA Member Bodies

3

1 Introduction

1.1 Background of the Study

The accounting profession is undergoing a rapid transition. The catalystic factors to

this transition are:

(i) international financial operation and cross border investments

(ii) free-trade regime

(iii) unabated forces of globalization.

The above developments demand an international perspective of accounting profession

and pose a threat to the national as well as regional accounting perspective. The

thought of national or regional accounting information and its compatibility with

international accounting standards, demands that critical review is made to strike a

balance in controversies of national, regional and international perspective and other

issues.

To gain insight into the issues and controversies, the SAFA member bodies in their

52nd SAFA Assembly held on January 17, 2004 at Lahore, commissioned a study to

find out the status of research activities in the SAFA member bodies and to facilitate

and supplement each other research projects wherever possible.

1.2 Role of SAFA

Research is stated to be the backbone of any professional advancement. The present

scenario involves fast developments in the field of technology world over. The

accounting disciplines necessitate updating the tools and techniques in practice. To

Status of Research in SAFA Member Bodies

4

meet the future challenges in the accounting profession, the professional accounting

bodies throughout the world are engaged in research work on continuous basis.

For the development of accounting profession in South Asian region, proper

understanding and cooperation among member bodies of the region was a dire need

of the time. The process was formalized with the formation of South Asian

Federation in 1984, by joint efforts of the Accounting Bodies of India, Pakistan,

Bangladesh and Sri Lanka. The Institute of Chartered Accountants of Nepal, joined

the Federation later in 1997.

Presently the Federation, a body of eight accounting institutions, is playing a vital

role in developing and strengthening the research and other professional activities of

its Member Bodies.

1.3 Objective of the Study

The SAFA has assigned the task to study the present research activities of its member

bodies, namely the Institutes of Chartered Accountants Bangladesh, India, Nepal,

Pakistan and Sri Lanka, the Institute of Cost and Management Accountants

Bangladesh, Institute of Cost and Management Accountants of Pakistan and the

Institute of Cost and Works Accountants of India to Institute of Cost & Management

Accountants of Pakistan (ICMAP) and compile a report to review the developments

made in research areas by each member body. The report is to provide an insight to

accelerate the pace of research to achieve greater harmonization of accounting

profession in the South Asian Region. The Professional Accountants of SAARC

countries can make best use of the research conducted in different areas by the

member bodies.

1.4 Scope of the Study

To describe and compile the activities undertaken by SAFA member institutions, and

to evaluate the operational mechanism established to augment such activities.

Status of Research in SAFA Member Bodies

5

1.5 Information Source

The study has been compiled on the basis of information collected from the following

sources:

Charter of each Institute.

Websites of the Institutes.

Information provided by each Institute.

Journals and other published materials of the member bodies available in the

library of ICMAP.

Status of Research in SAFA Member Bodies

6

2 The Institute of Chartered

Accountants of India (ICAI)

2.1 Management of the Institute

The Institute of Chartered Accountants of India, was established on July 1, 1949 by an

Act of Parliament, The Chartered Accountants Act, 1949 for the purpose of regulating

the profession of Chartered Accountants in India. It completed 50 years of service to

the nation on July 1, 1999. Affairs of the Institute are managed and controlled by a

Council comprising 30 members. Out of these, 24 are elected by the members of the

Institute from all over the country and 6 are nominated by the Central Government.

Besides the Central Council, there are 5 Regional Councils located at Mumbai,

Chennai, Kolkata, Kanpur and New Delhi. The Headquarter of the Institute is at New

Delhi. Duration of the Central Council constituted under the Act is three years. The

Institute has several departments for ensuring its efficient functioning.

The Executive Committee, one of the three Standing Committees of the Institute,

administers the affairs of the Institute.

Activities of the Institute are divided into four divisions:

Technical Directorate;

Board of Studies;

Continuing Professional Education Directorate;amd

The Administration.

The above divisions are headed by a Director who reports to ICAI Secretary.

The Technical Director is assisted by a Deputy Director, an Assistant Director and two

Status of Research in SAFA Member Bodies

7

Technical Officers. Technical Directorate assists the following Technical Committees

of the Council in the matter of development of the profession:

Accounting Standards Board

Research Committee

Expert Advisory Committee

Professional Development Committee

Board of Studies Committee

Information Technology Committee

Continuing Professional Education Committee.

The ICAI is a member of International Federation of Accountants (IFAC),

International Accounting Standards Board (IASB), Confederation of Asian & Pacific

Accountants (CAPA) and South Asian Federation of Accountants (SAFA).

2.2 Research Setup

The Institute has formed various standing and non-standing committees, which perform

functions as mandated by the Council. Primarily the research activities are undertaken

by the Technical Directorate, which supports Institute�s various committees like the

Accounting Standards Board, Research Committee, Expert Advisory Committee, etc.

The activities of other committees involve considerable research initiatives. Primary

function of the Accounting Standards Board is to evolve Accounting Standards and

provide guidance on issues arising there from. The Research Committee prepares

recommendations on generally accepted accounting principles and practices, and

undertakes research projects in the areas not covered by the functions of Institute�s

other Committees. The other Technical Committees including the Auditing and

Assurance Standards Board, Corporate and Allied Laws Committee, Fiscal Laws

Committee, Committee on Financial Markets and Investors� Protection, etc, have been

set up and doing research pursuits over years. The relatively nascent committees, also

engaged in research include the Committee on Insurance, Committee on Trade Laws

Status of Research in SAFA Member Bodies

8

and World Trade Organisation, Committee on Information Technology, Committee on

Internal Audit, etc. Thus they also augment the research initiatives of the Institute in

respective areas.

Each of the Committee reports to the Council on its activities. The authoritative

documents prepared by the Committees, unless the power of issuance thereof is

delegated, are issued upon approbation and under authority of the Council.

All Committees are supported by officials of different cadres. The management of the

Institute has the authority to determine the composition of the official strength of such

designation as may be considered expedient from time to time. The Research and

Technical Committees are supported by high-level officials say Directors, Additional

Directors, etc over the years. The departments are supported by Chartered Accountants

working at various levels.

2.3 Research Foundation

The Institute also promotes the ICAI-Accounting Research Foundation, incorporated

with the main objective of imparting and promoting knowledge, learning, education

and understanding and basic applied research in the areas of accounting, auditing,

capital markets, fiscal policies, etc. The ICAI- Accounting Research Foundation is a

core research body. In addition to engaging in the reputed projects on conversion of

accounts of the Municipal Corporation of Delhi (MCD) to accrual basis, the Research

Foundation is currently rendering and supporting the projects on the following

subjects:

Corporate Financial Communications: Trends and Practices of Business Groups

in India Issues in Accounting � Valuation of Intangibles Developing a Code for Governance of Non-Governmental Organisations (NGOs)

Status of Research in SAFA Member Bodies

9

Electronic Communication and Direct Taxation

The Foundation also proposes undertaking the following research projects: Paradigm Shift in Accounting Practices of Local Bodies and Panchayats - A

Move Towards Modern Accounting and Financial Reporting Fiscal laws Administration � Concept of Accountability Taxation of E-Commerce Business Framework for National Income Accounting Convergence of Information Technology with Corporate Governance Framework of Government Accounting System for Better Accounting,

Accountability and Disclosure Practices The Structure of Accounting Profession in India � Its future in WTO Regime Ethical Standards for Professional Accountants/Auditors � A Study of Global

Standards including Indian Standards Considerations in Deciding Accounting Policies by Listed Companies Effect of Accounting Information in Published Annual Reports on Movement in

Share Prices Extent of Compliance with Accounting Standards � A Study Issues on Accounting from Small and Medium Enterprises� Perspective Investment Decision Models of Retail and Institutional Investors � Use of

Accounting Information Current Risk Management Practices by Indian Companies Current Risk Management Practices by Banking Companies and Financial

Institutions Accounting Standards � Expectation Gap

Status of Research in SAFA Member Bodies

10

The ICAI- Accounting Research Foundation has the acquiescence of the Guru Gobind

Singh Indraprastha Vishwa Vidyalaya to enroll Research Fellows, which are awarded

doctoral degree (Ph.D.) by the said University.

The ICAI- Accounting Research Foundation is governed by a Board of Directors in

accordance with the Foundation�s Articles of Association. The Board of Directors of

the ICAI- Accounting Research Foundation comprises:

President and Vice President of the Institute

Secretary of the Institute

Six members of the Institute�s Central Council

Dean of the ICAI- Accounting Research Foundation

Five eminent personalities in Government, industry, academics and the

profession of accountancy, law or other related professions

2.4 Journal of the Institute

The Institute brings out a monthly Journal christened �The Chartered Accountant

Journal�, which is distributed to its members free of cost. The chartered accountancy

students and others may subscribe to the Journal.

The Chartered Accountant Journal contains technical and research articles, relevant in

professional context.

2.5 Research Projects

The list of publications including research projects issued by Accounting Standards

Board, Research Committee and Auditing & Assurance Standards Board of the

Institute is given in Appendix-A.

Status of Research in SAFA Member Bodies

11

2.6 Research Library

The Institute�s Central Council Library situated at the Institute�s head office at New

Delhi, is a �Nucleus Library�. It is equipped with technical and useful resources

(publications and CDs) on varied topics of professional usage and value. The Central

Council Library presently has around 50000 books. The Central Council Library itself

and the libraries of the Regional Councils are quite comprehensive in terms of the

high-value basic and advanced-level resources. These publications are useful reservoir

of knowledge for research initiatives.

Moreover, the Committees possess resources required to perform their functions and

are equipped with adequate research literature on respective subjects.

Status of Research in SAFA Member Bodies

12

APPENDIX-A

(A.) ICAI - List of Projects Completed and Effective at present Accounting Standards Board

1. Accounting Standards (ASs)

Sl. No. Accounting Standard (AS) Title of the Accounting Standard

1. AS 1 (issued 1979) Disclosure of Accounting Policies 2. AS 2 (Revised 1999) Valuation of Inventories 3. AS 3 (Revised 1997) Cash Flow Statements 4. AS 4 (Revised 1995) Contingencies and Events Occurring After the

Balance Sheet Date 5. AS 5 (Revised 1997) Net Profit or Loss for the Period, Prior Period Items

and Changes in Accounting Policies 6. AS 6 (Revised 1994) Depreciation Accounting 7. AS 7 (Revised 2002)) Construction Contracts 8. AS 8 (issued 1985) (withdrawn

pursuant to AS 26 becoming mandatory)

Accounting for Research and Development

9. AS 9 (issued 1985) Revenue Recognition 10. AS 10 (issued 1985) Accounting for Fixed Assets 11. AS 11 (Revised 2003) The Effects of Changes in Foreign Exchange Rates 12. AS 12 (issued 1991) Accounting for Government Grants 13. AS 13 (issued 1993) Accounting for Investments 14. AS 14 (issued 1994) Accounting for Amalgamations 15. AS 15 (issued 1995) Accounting for Retirement Benefits in the Financial

Statements of Employers 16. AS 16 (issued 2000) Borrowing Costs 17. AS 17 (issued 2000) Segment Reporting 18. AS 18 (issued 2000) Related Party Disclosures 19. AS 19 (issued 2001) Leases 20. AS 20 (issued 2001) Earnings Per Share 21. AS 21 (issued 2001) Consolidated Financial Statements 22. AS 22 (issued 2001) Accounting for Taxes on Income 23. AS 23 (issued 2001) Accounting for Investments in Associates in

Consolidated Financial Statements 24. AS 24 (issued 2002) Discontinuing Operations 25. AS 25 (issued 2002) Interim Financial Reporting 26. AS 26 (issued 2002) Intangible Assets 27. AS 27 (issued 2002) Financial Reporting of Interests in Joint Ventures 28. AS 28 (issued 2002) Impairment of Assets 29. AS 29 (issued 2003) Provisions, Contingent Liabilities and Contingent

Assets

Status of Research in SAFA Member Bodies

13

2. The following is the list of Accounting Standards Interpretations (ASIs) issued

till date. All are effective at present:

i. ASI 1, Substantial Period of Time (Re.: AS 16)

ii. ASI 2, Accounting for Machinery Spares (Re.: AS 2 and AS 10)

iii. ASI 3, Accounting for Taxes on Income in the situations of Tax Holiday under Sections 80-IA and 80-IB of the Income-tax Act, 1961 (Re.: AS 22)

iv. ASI 4, Losses under the head Capital Gains (Re.: AS 22)

v. ASI 5, Accounting for Taxes on Income in the situation of Tax Holiday under Sections 10A and 10B of the Income-tax Act, 1961 (Re.: AS 22)

vi. ASI 6, Accounting for Taxes on Income in the context of Section 115JB of the Income-tax Act, 1961 (Re.: AS 22)

vii. ASI 7, Disclosure of deferred tax assets and deferred tax liabilities in the balance sheet of a company (Re.: AS 22)

viii. ASI 8, Interpretation of the term �Near Future� (Re.: AS 21, AS 23 and AS 27)

ix. ASI 9, Virtual certainty supported by convincing evidence (Re.: AS 22)

x. ASI 10, Interpretation of paragraph 4(e) of AS 16 (Re.: AS 16)

xi. ASI 11, Accounting for Taxes on Income in case of an Amalgamation (Re.: AS 22)

xii. ASI 12, Applicability of AS 20 (Re.: AS 20)

xiii. ASI 13, Interpretation of paragraphs 26 and 27 of AS 18 (Re.: AS 18)

xiv. ASI 14, Disclosure of Revenue from Sales Transactions (Re.: AS 9)

xv. ASI 15, Notes to the Consolidated Financial Statements (Re.: AS 21)

xvi. ASI 16, Treatment of Proposed Dividend under AS 23 (Re.: AS 23)

xvii. ASI 17, Adjustments to the Carrying Amount of Investment arising from Changes in Equity not Included in the Statement of Profit and Loss of the Associate (Re.: AS 23)

Status of Research in SAFA Member Bodies

14

xviii. ASI 18, Consideration of Potential Equity Shares for Determining whether an Investee is an Associate under AS 23 (Re.: AS 23)

xix. ASI 19, Interpretation of the term �intermediaries� (Re.: AS 18)

xx. ASI 20, Disclosure of Segment Information (Re.: AS 17)

xxi. ASI 21, Non-Executive Directors on the Board � whether related parties (Re.: AS 18)

xxii. ASI 22, Treatment of Interest for determining Segment Expense (Re.: AS 17)

xxiii. ASI 23, Remuneration paid to key management personnel � whether a related party transaction (Re.: AS 18)

xxiv. ASI 24, Definition of �Control� (Re.: AS 21)

xxv. ASI 25, Exclusion of a subsidiary from consolidation (Re.: AS 21)

xxvi. ASI 26, Accounting for taxes on income in the consolidated financial statements (Re.: AS 21)

xxvii. ASI 27, Applicability of AS 25 to Interim Financial Results (Re.: AS 25)

xxviii. ASI 28, Disclosure of parent�s/venturer�s shares in post-acquisition reserves of a subsidiary/jointly controlled entity (Re.: AS 21 and AS 27)

3. Others

i. Preface to the Statements of Accounting Standards (revised 2004)

ii. Framework for the Preparation and Presentation of Financial Statements (issued 2000)

iii. Guidance Note on Terms Used in Financial Statements (issued 1983)

iv. Technical Guide on Accounting and Financial Reporting by Urban Local Bodies

(issued 2000)

v. Background Material for Seminars on AS 16, Borrowing Costs (issued 2004)

vi. Background Material for Seminars on AS 17, Segment Reporting (issued 2003)

vii. Background Material for Seminars on AS 18, Related Party Disclosures (issued 2002)

viii. Background Material for Seminars on AS 19, Leases (issued 2003)

ix. Background Material for Seminars on AS 20, Earnings Per Share (issued 2002)

Status of Research in SAFA Member Bodies

15

x. Background Material for Seminars on AS 21, Consolidated Financial Statements (issued 2002)

xi. Background Material for Seminars AS 22, Accounting for Taxes on Income (issued 2003)

xii. Background Material for Seminars on AS 23, Accounting for Investments in Associates in Consolidated Financial Statements (issued 2002)

Status of Research in SAFA Member Bodies

16

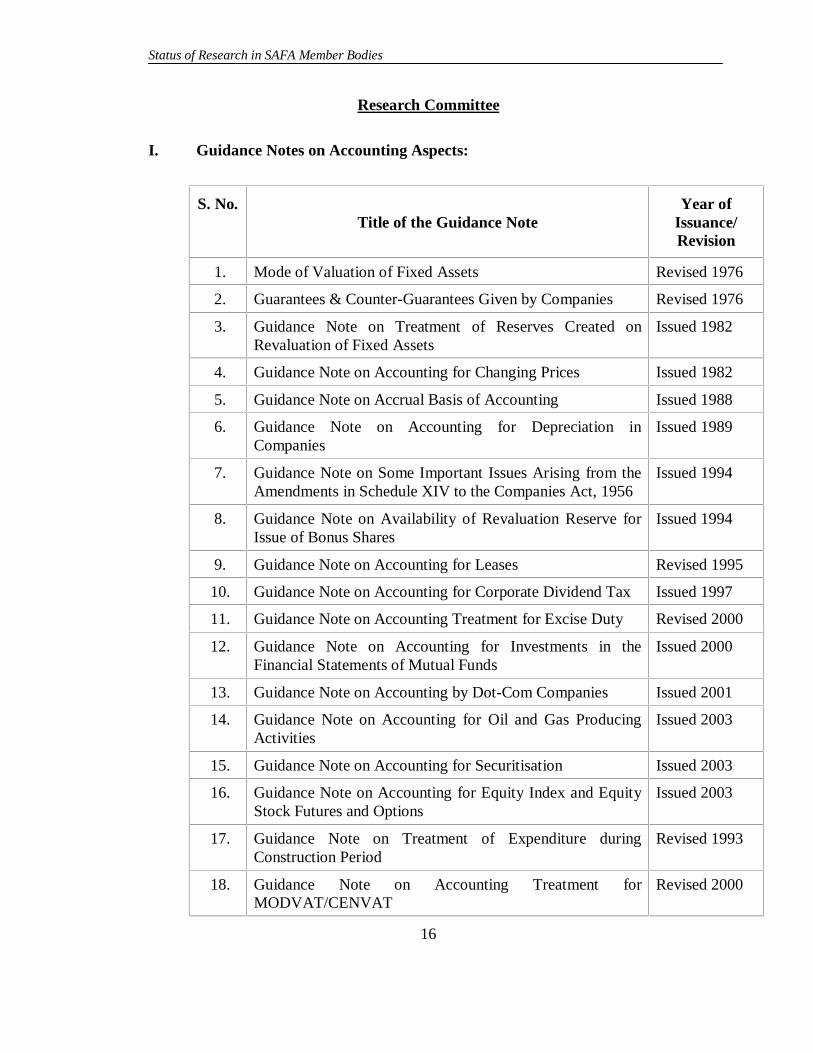

Research Committee

I. Guidance Notes on Accounting Aspects:

S. No. Title of the Guidance Note

Year of Issuance/ Revision

1. Mode of Valuation of Fixed Assets Revised 1976

2. Guarantees & Counter-Guarantees Given by Companies Revised 1976

3. Guidance Note on Treatment of Reserves Created on Revaluation of Fixed Assets

Issued 1982

4. Guidance Note on Accounting for Changing Prices Issued 1982

5. Guidance Note on Accrual Basis of Accounting Issued 1988

6. Guidance Note on Accounting for Depreciation in Companies

Issued 1989

7. Guidance Note on Some Important Issues Arising from the Amendments in Schedule XIV to the Companies Act, 1956

Issued 1994

8. Guidance Note on Availability of Revaluation Reserve for Issue of Bonus Shares

Issued 1994

9. Guidance Note on Accounting for Leases Revised 1995

10. Guidance Note on Accounting for Corporate Dividend Tax Issued 1997

11. Guidance Note on Accounting Treatment for Excise Duty Revised 2000

12. Guidance Note on Accounting for Investments in the Financial Statements of Mutual Funds

Issued 2000

13. Guidance Note on Accounting by Dot-Com Companies Issued 2001

14. Guidance Note on Accounting for Oil and Gas Producing Activities

Issued 2003

15. Guidance Note on Accounting for Securitisation Issued 2003

16. Guidance Note on Accounting for Equity Index and Equity Stock Futures and Options

Issued 2003

17. Guidance Note on Treatment of Expenditure during Construction Period

Revised 1993

18. Guidance Note on Accounting Treatment for MODVAT/CENVAT

Revised 2000

Status of Research in SAFA Member Bodies

17

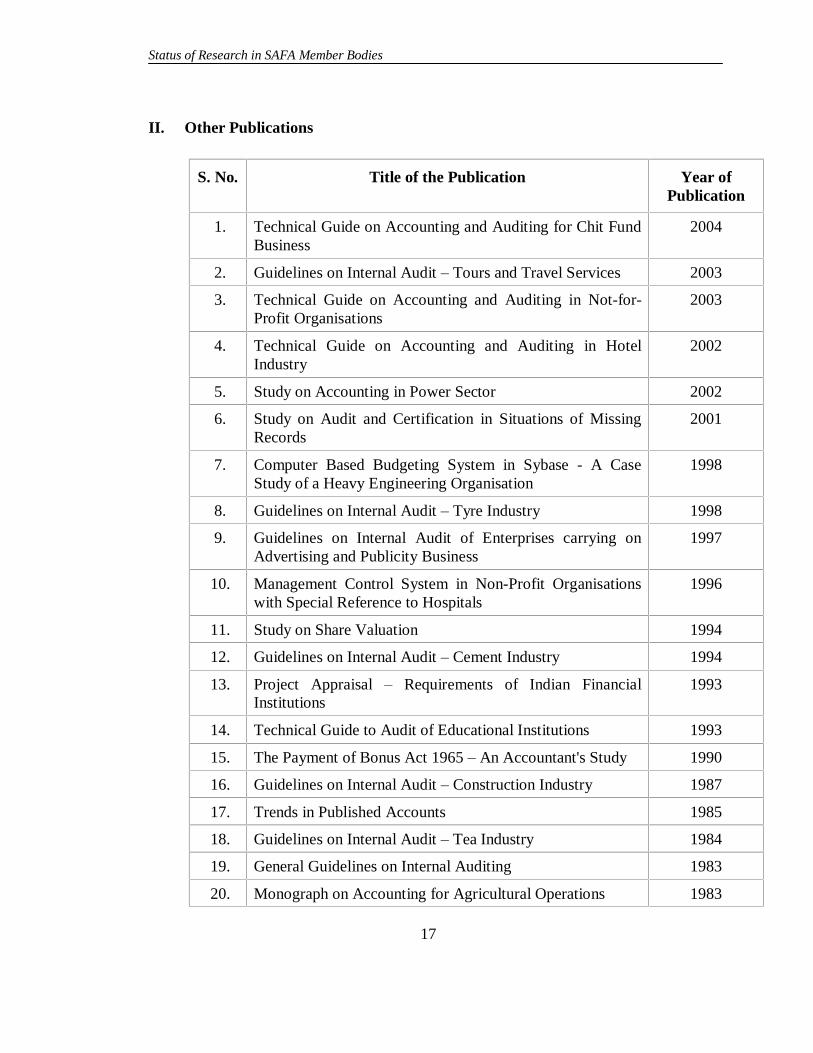

II. Other Publications

S. No. Title of the Publication Year of Publication

1. Technical Guide on Accounting and Auditing for Chit Fund Business

2004

2. Guidelines on Internal Audit � Tours and Travel Services 2003

3. Technical Guide on Accounting and Auditing in Not-for-Profit Organisations

2003

4. Technical Guide on Accounting and Auditing in Hotel Industry

2002

5. Study on Accounting in Power Sector 2002

6. Study on Audit and Certification in Situations of Missing Records

2001

7. Computer Based Budgeting System in Sybase - A Case Study of a Heavy Engineering Organisation

1998

8. Guidelines on Internal Audit � Tyre Industry 1998

9. Guidelines on Internal Audit of Enterprises carrying on Advertising and Publicity Business

1997

10. Management Control System in Non-Profit Organisations with Special Reference to Hospitals

1996

11. Study on Share Valuation 1994

12. Guidelines on Internal Audit � Cement Industry 1994

13. Project Appraisal � Requirements of Indian Financial Institutions

1993

14. Technical Guide to Audit of Educational Institutions 1993

15. The Payment of Bonus Act 1965 � An Accountant's Study 1990

16. Guidelines on Internal Audit � Construction Industry 1987

17. Trends in Published Accounts 1985

18. Guidelines on Internal Audit � Tea Industry 1984

19. General Guidelines on Internal Auditing 1983

20. Monograph on Accounting for Agricultural Operations 1983

Status of Research in SAFA Member Bodies

18

21. Monograph on Accounting for Livestock 1983

22. Monograph on Accounting for Rubber Plantation 1983

23. Guidelines on Internal Audit � Jute Industry 1982

24. Accounting and Auditing Technical Guide on Textile Industry

1982

25. Accounting and Control Systems in a Shipping Company 1982

26. An Approach to Social Cost-Benefit Analysis under Indian Conditions

1981

27. Monograph on Accounting for Poultry Farming 1980

28. Technical Guide for Audit of Co-operative Societies 1979

29. Management Control Systems 1977

30. Internal Control Questionnaire 1976

31. Technical Guide for Audit � Sugar Industry 1975

32. Integrated System of Cost and Financial Accounts 1973

Status of Research in SAFA Member Bodies

19

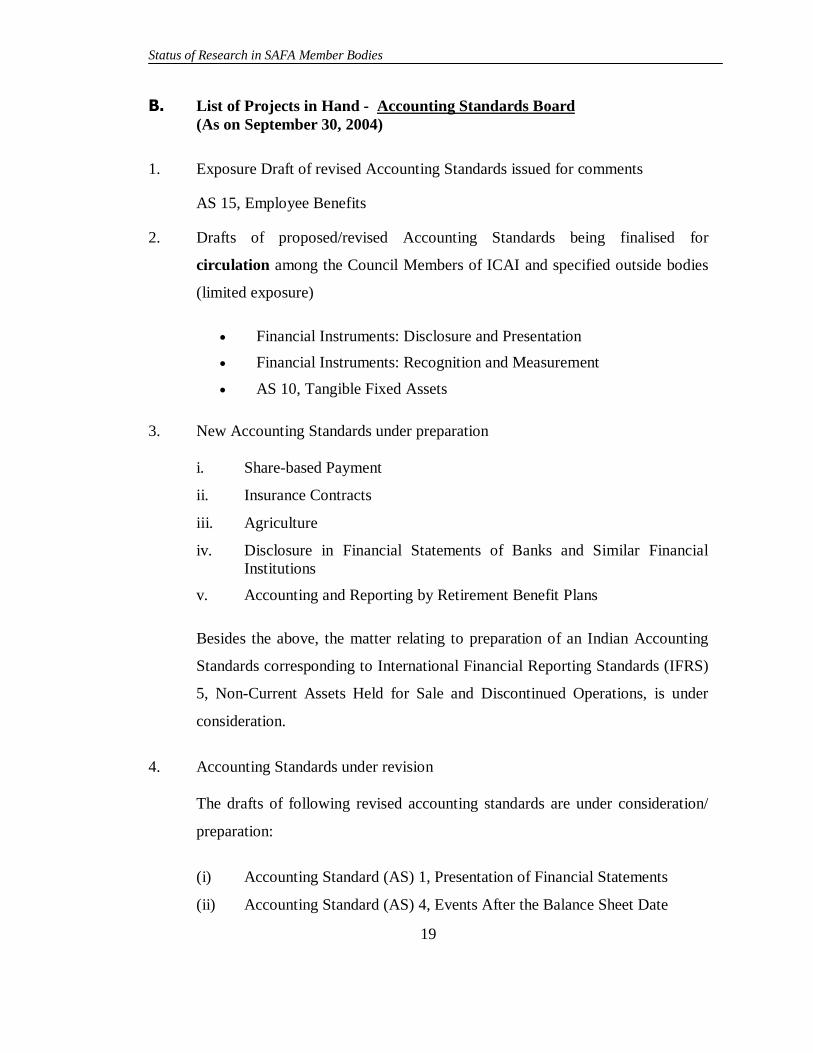

B. List of Projects in Hand - Accounting Standards Board (As on September 30, 2004)

1. Exposure Draft of revised Accounting Standards issued for comments

AS 15, Employee Benefits

2. Drafts of proposed/revised Accounting Standards being finalised for

circulation among the Council Members of ICAI and specified outside bodies

(limited exposure)

Financial Instruments: Disclosure and Presentation

Financial Instruments: Recognition and Measurement

AS 10, Tangible Fixed Assets

3. New Accounting Standards under preparation

i. Share-based Payment

ii. Insurance Contracts

iii. Agriculture

iv. Disclosure in Financial Statements of Banks and Similar Financial Institutions

v. Accounting and Reporting by Retirement Benefit Plans

Besides the above, the matter relating to preparation of an Indian Accounting

Standards corresponding to International Financial Reporting Standards (IFRS)

5, Non-Current Assets Held for Sale and Discontinued Operations, is under

consideration.

4. Accounting Standards under revision

The drafts of following revised accounting standards are under consideration/

preparation:

(i) Accounting Standard (AS) 1, Presentation of Financial Statements

(ii) Accounting Standard (AS) 4, Events After the Balance Sheet Date

Status of Research in SAFA Member Bodies

20

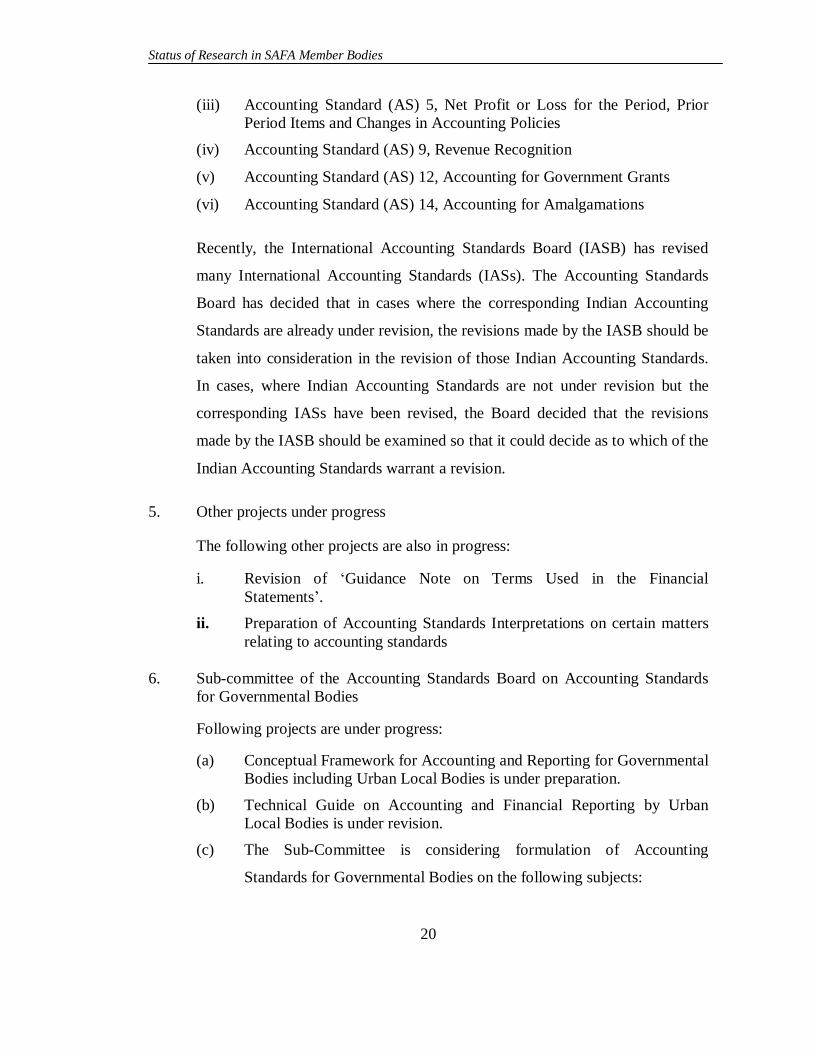

(iii) Accounting Standard (AS) 5, Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies

(iv) Accounting Standard (AS) 9, Revenue Recognition

(v) Accounting Standard (AS) 12, Accounting for Government Grants

(vi) Accounting Standard (AS) 14, Accounting for Amalgamations

Recently, the International Accounting Standards Board (IASB) has revised

many International Accounting Standards (IASs). The Accounting Standards

Board has decided that in cases where the corresponding Indian Accounting

Standards are already under revision, the revisions made by the IASB should be

taken into consideration in the revision of those Indian Accounting Standards.

In cases, where Indian Accounting Standards are not under revision but the

corresponding IASs have been revised, the Board decided that the revisions

made by the IASB should be examined so that it could decide as to which of the

Indian Accounting Standards warrant a revision.

5. Other projects under progress

The following other projects are also in progress:

i. Revision of �Guidance Note on Terms Used in the Financial Statements�.

ii. Preparation of Accounting Standards Interpretations on certain matters relating to accounting standards

6. Sub-committee of the Accounting Standards Board on Accounting Standards

for Governmental Bodies

Following projects are under progress:

(a) Conceptual Framework for Accounting and Reporting for Governmental Bodies including Urban Local Bodies is under preparation.

(b) Technical Guide on Accounting and Financial Reporting by Urban Local Bodies is under revision.

(c) The Sub-Committee is considering formulation of Accounting

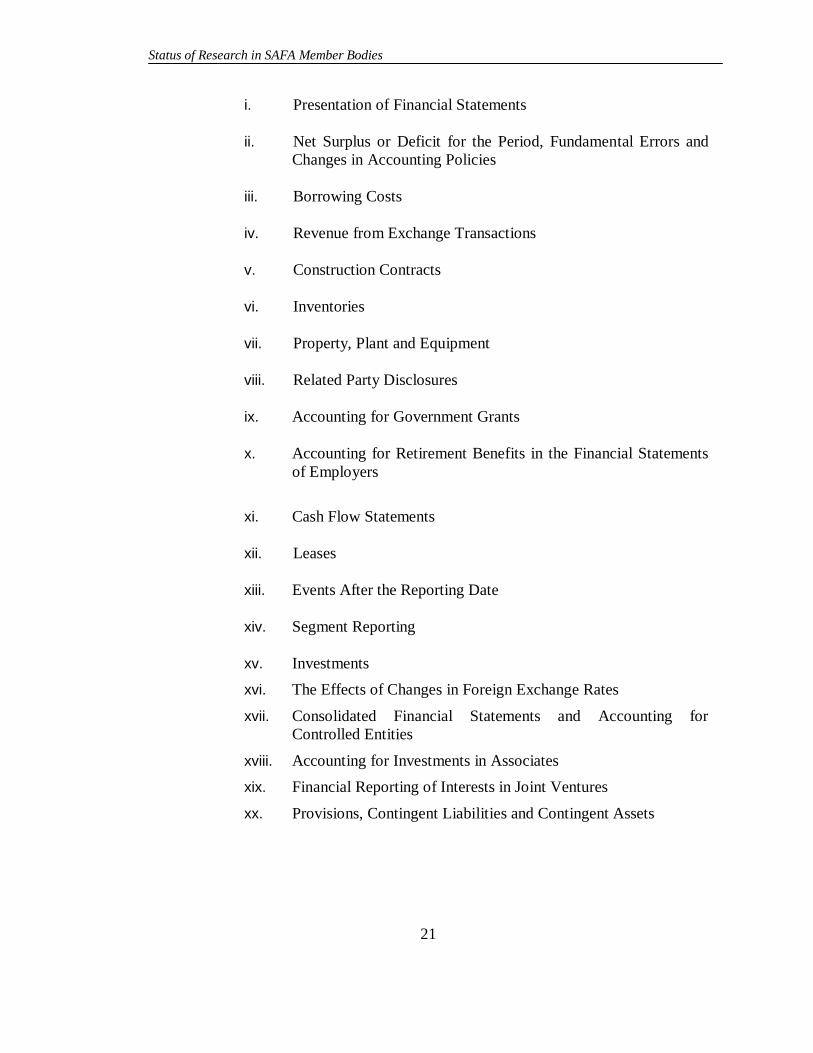

Standards for Governmental Bodies on the following subjects:

Status of Research in SAFA Member Bodies

21

i. Presentation of Financial Statements ii. Net Surplus or Deficit for the Period, Fundamental Errors and

Changes in Accounting Policies iii. Borrowing Costs iv. Revenue from Exchange Transactions v. Construction Contracts vi. Inventories vii. Property, Plant and Equipment viii. Related Party Disclosures ix. Accounting for Government Grants x. Accounting for Retirement Benefits in the Financial Statements

of Employers

xi. Cash Flow Statements xii. Leases xiii. Events After the Reporting Date xiv. Segment Reporting xv. Investments

xvi. The Effects of Changes in Foreign Exchange Rates

xvii. Consolidated Financial Statements and Accounting for Controlled Entities

xviii. Accounting for Investments in Associates

xix. Financial Reporting of Interests in Joint Ventures

xx. Provisions, Contingent Liabilities and Contingent Assets

Status of Research in SAFA Member Bodies

22

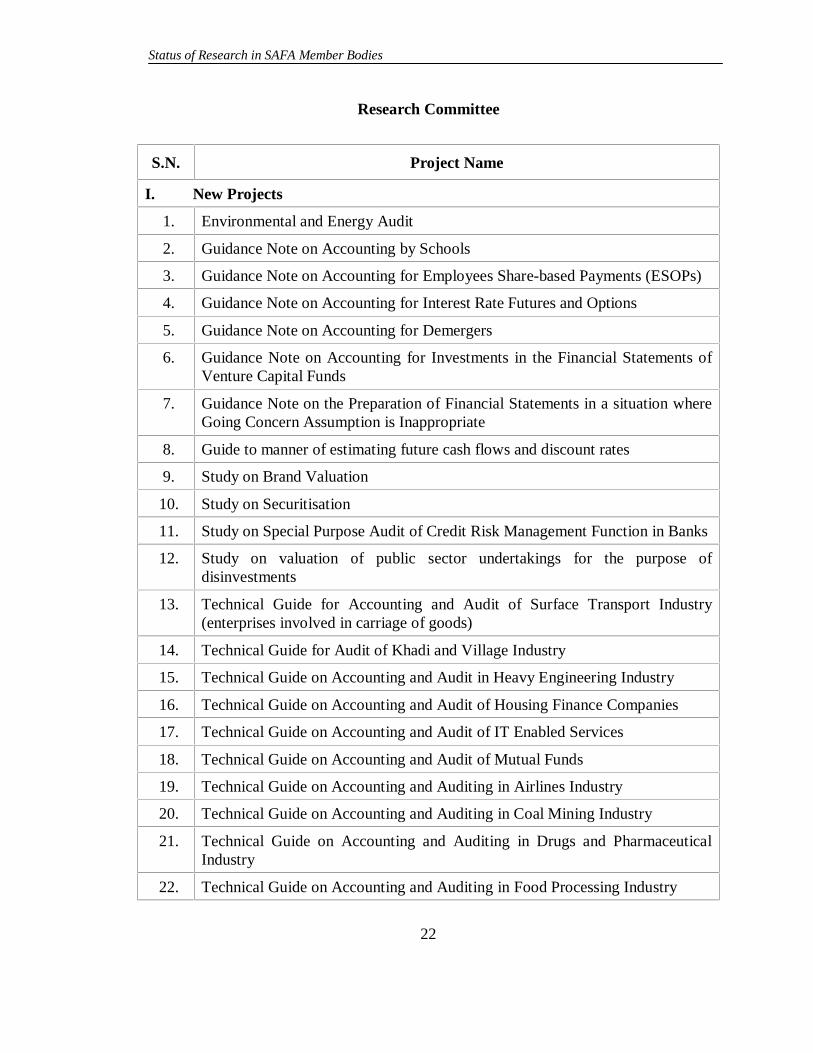

Research Committee

S.N. Project Name

I. New Projects

1. Environmental and Energy Audit

2. Guidance Note on Accounting by Schools

3. Guidance Note on Accounting for Employees Share-based Payments (ESOPs)

4. Guidance Note on Accounting for Interest Rate Futures and Options

5. Guidance Note on Accounting for Demergers

6. Guidance Note on Accounting for Investments in the Financial Statements of Venture Capital Funds

7. Guidance Note on the Preparation of Financial Statements in a situation where Going Concern Assumption is Inappropriate

8. Guide to manner of estimating future cash flows and discount rates

9. Study on Brand Valuation

10. Study on Securitisation

11. Study on Special Purpose Audit of Credit Risk Management Function in Banks

12. Study on valuation of public sector undertakings for the purpose of disinvestments

13. Technical Guide for Accounting and Audit of Surface Transport Industry (enterprises involved in carriage of goods)

14. Technical Guide for Audit of Khadi and Village Industry

15. Technical Guide on Accounting and Audit in Heavy Engineering Industry

16. Technical Guide on Accounting and Audit of Housing Finance Companies

17. Technical Guide on Accounting and Audit of IT Enabled Services

18. Technical Guide on Accounting and Audit of Mutual Funds

19. Technical Guide on Accounting and Auditing in Airlines Industry

20. Technical Guide on Accounting and Auditing in Coal Mining Industry

21. Technical Guide on Accounting and Auditing in Drugs and Pharmaceutical Industry

22. Technical Guide on Accounting and Auditing in Food Processing Industry

Status of Research in SAFA Member Bodies

23

23. Technical Guide on Accounting and Auditing in NBFCs

24. Technical Guide on Employees Stock Option Plans (ESOPs)

25. Frequently Asked Questions (FAQs) in respect of accounting in Not-for-Profit Organisations

26. Guidance Note on Treatment of Expenditure during Construction Period

27. Guidelines on Internal Audit � Tea Industry

28. Study on Share Valuation

29. Guidance Note on Accounting Treatment for MODVAT/CENVAT

30. The Payment of Bonus Act 1965 � An Accountant's Study

Status of Research in SAFA Member Bodies

24

C. Research projects planned to be undertaken in future

Research Committee

S.N. Project Name

I. New Projects

1. Guidance Note on Accounting for Loyalty Programmes

2. Guidance Note on Accounting for Value Added Tax

3. Preparation of formats of financial statements of Panchayati Raj Institutions

4. Study on Derivatives

5. Study on Insurance Survey Work

6. Technical Guide for Accounting and Audit of Courier Companies

7. Technical Guide for Accounting and Audit of Surface Transport Industry (enterprises involved in carriage of passengers)

8. Technical Guide on Accounting and Audit in Edible Oil Industry

9. Technical Guide on Accounting and Audit in Plastic Industry

10. Technical Guide on Accounting and Audit in Roads, Toll Bridges and Other Infrastructure Projects

11. Technical Guide on Accounting and Audit of Aqua Farming (including Marine Products)

12. Technical Guide on Accounting and Audit of Producers and Distributors of Films and Television Serials

13. Technical Guide on Accounting and Auditing in Automobile Industry

14. Technical Guide on Accounting and Auditing in Fertiliser Industry

15. Technical Guide to Accounting and Auditing in Newspaper Publishing Industry

16. Technical Guide on Accounting and Auditing in Paper Industry

17. Technical Guide on Accounting and Auditing in Tele-communications Industry

18. Technical Guide on Accounting and Auditing in Zinc Industry

19. Technical Guide on Accounting for Bio-tech Industry

II. Revision of the Existing Publications of the Committee

1. Accounting and Control Systems in a Shipping Company

2. An Approach to Social Cost-Benefit Analysis under Indian Conditions

Status of Research in SAFA Member Bodies

25

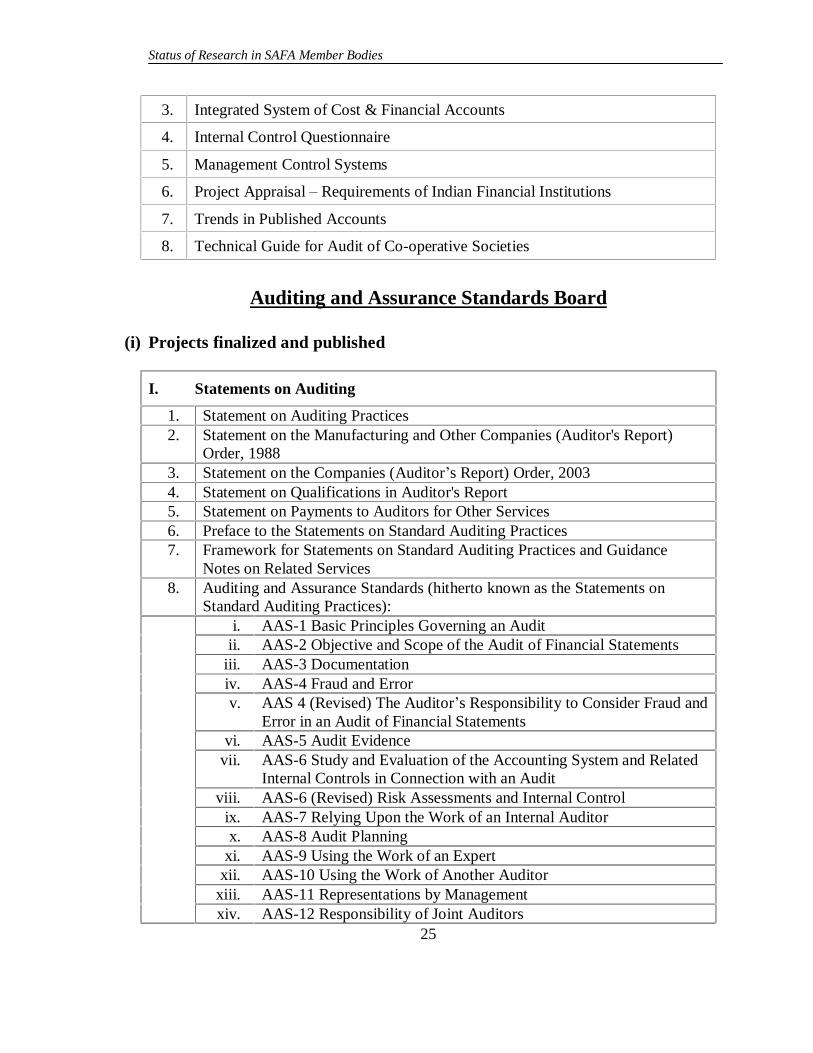

3. Integrated System of Cost & Financial Accounts

4. Internal Control Questionnaire

5. Management Control Systems

6. Project Appraisal � Requirements of Indian Financial Institutions

7. Trends in Published Accounts

8. Technical Guide for Audit of Co-operative Societies

Auditing and Assurance Standards Board

(i) Projects finalized and published

I. Statements on Auditing

1. Statement on Auditing Practices 2. Statement on the Manufacturing and Other Companies (Auditor's Report)

Order, 1988 3. Statement on the Companies (Auditor�s Report) Order, 2003 4. Statement on Qualifications in Auditor's Report 5. Statement on Payments to Auditors for Other Services 6. Preface to the Statements on Standard Auditing Practices 7. Framework for Statements on Standard Auditing Practices and Guidance

Notes on Related Services 8. Auditing and Assurance Standards (hitherto known as the Statements on

Standard Auditing Practices): i. AAS-1 Basic Principles Governing an Audit

ii. AAS-2 Objective and Scope of the Audit of Financial Statements iii. AAS-3 Documentation iv. AAS-4 Fraud and Error v. AAS 4 (Revised) The Auditor�s Responsibility to Consider Fraud and

Error in an Audit of Financial Statements vi. AAS-5 Audit Evidence

vii. AAS-6 Study and Evaluation of the Accounting System and Related Internal Controls in Connection with an Audit

viii. AAS-6 (Revised) Risk Assessments and Internal Control ix. AAS-7 Relying Upon the Work of an Internal Auditor x. AAS-8 Audit Planning

xi. AAS-9 Using the Work of an Expert xii. AAS-10 Using the Work of Another Auditor

xiii. AAS-11 Representations by Management

xiv. AAS-12 Responsibility of Joint Auditors

Status of Research in SAFA Member Bodies

26

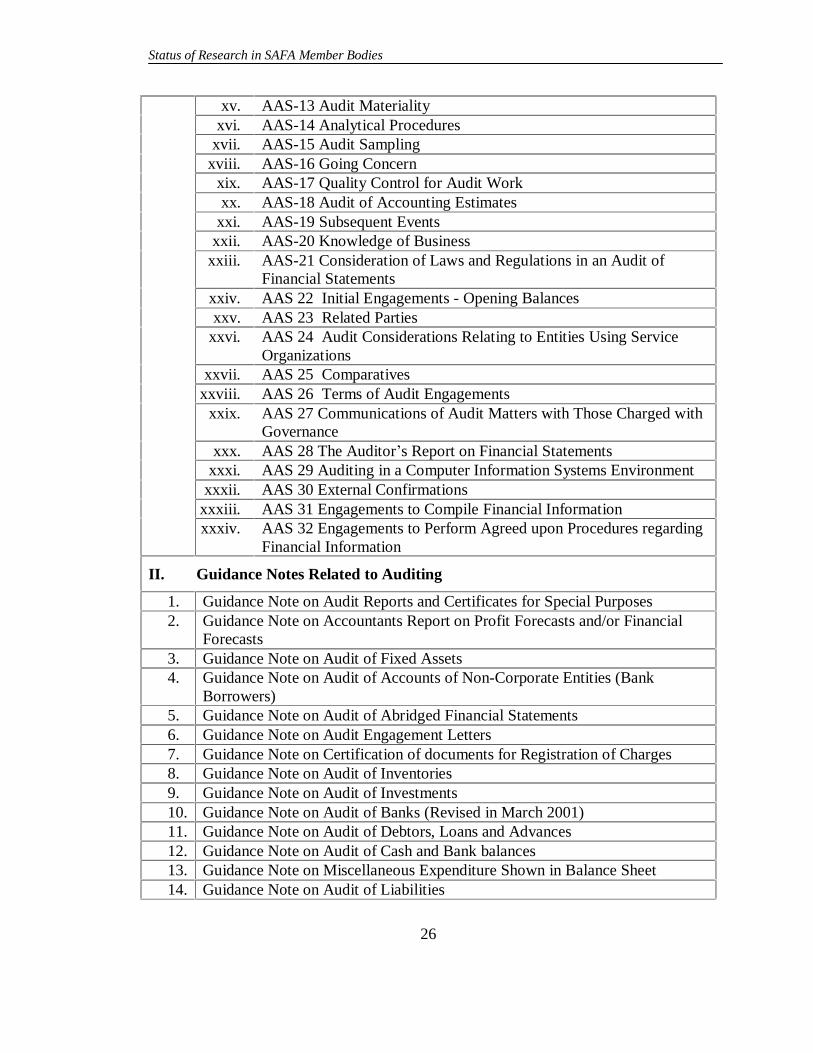

xv. AAS-13 Audit Materiality xvi. AAS-14 Analytical Procedures

xvii. AAS-15 Audit Sampling xviii. AAS-16 Going Concern

xix. AAS-17 Quality Control for Audit Work xx. AAS-18 Audit of Accounting Estimates

xxi. AAS-19 Subsequent Events xxii. AAS-20 Knowledge of Business

xxiii. AAS-21 Consideration of Laws and Regulations in an Audit of Financial Statements

xxiv. AAS 22 Initial Engagements - Opening Balances xxv. AAS 23 Related Parties

xxvi. AAS 24 Audit Considerations Relating to Entities Using Service Organizations

xxvii. AAS 25 Comparatives xxviii. AAS 26 Terms of Audit Engagements

xxix. AAS 27 Communications of Audit Matters with Those Charged with Governance

xxx. AAS 28 The Auditor�s Report on Financial Statements xxxi. AAS 29 Auditing in a Computer Information Systems Environment

xxxii. AAS 30 External Confirmations xxxiii. AAS 31 Engagements to Compile Financial Information

xxxiv. AAS 32 Engagements to Perform Agreed upon Procedures regarding Financial Information

II. Guidance Notes Related to Auditing

1. Guidance Note on Audit Reports and Certificates for Special Purposes 2. Guidance Note on Accountants Report on Profit Forecasts and/or Financial

Forecasts 3. Guidance Note on Audit of Fixed Assets 4. Guidance Note on Audit of Accounts of Non-Corporate Entities (Bank

Borrowers) 5. Guidance Note on Audit of Abridged Financial Statements 6. Guidance Note on Audit Engagement Letters 7. Guidance Note on Certification of documents for Registration of Charges 8. Guidance Note on Audit of Inventories 9. Guidance Note on Audit of Investments 10. Guidance Note on Audit of Banks (Revised in March 2001) 11. Guidance Note on Audit of Debtors, Loans and Advances 12. Guidance Note on Audit of Cash and Bank balances 13. Guidance Note on Miscellaneous Expenditure Shown in Balance Sheet 14. Guidance Note on Audit of Liabilities

Status of Research in SAFA Member Bodies

27

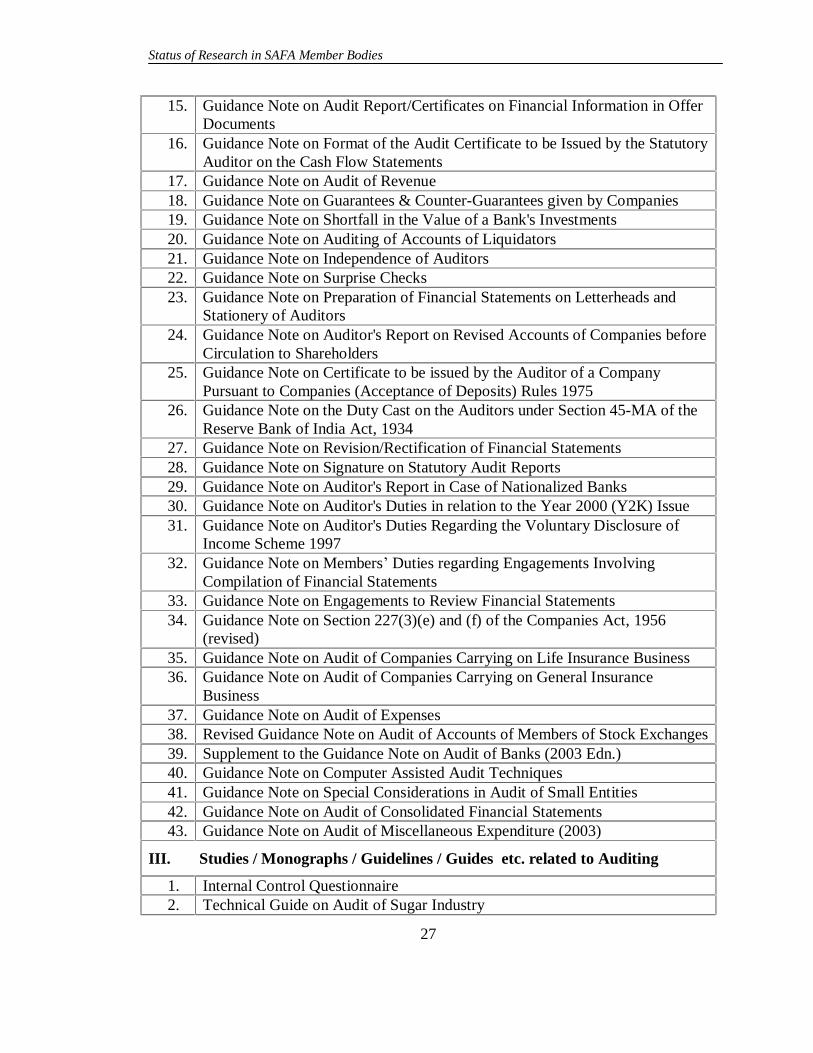

15. Guidance Note on Audit Report/Certificates on Financial Information in Offer Documents

16. Guidance Note on Format of the Audit Certificate to be Issued by the Statutory Auditor on the Cash Flow Statements

17. Guidance Note on Audit of Revenue 18. Guidance Note on Guarantees & Counter-Guarantees given by Companies 19. Guidance Note on Shortfall in the Value of a Bank's Investments 20. Guidance Note on Auditing of Accounts of Liquidators 21. Guidance Note on Independence of Auditors 22. Guidance Note on Surprise Checks 23. Guidance Note on Preparation of Financial Statements on Letterheads and

Stationery of Auditors 24. Guidance Note on Auditor's Report on Revised Accounts of Companies before

Circulation to Shareholders 25. Guidance Note on Certificate to be issued by the Auditor of a Company

Pursuant to Companies (Acceptance of Deposits) Rules 1975 26. Guidance Note on the Duty Cast on the Auditors under Section 45-MA of the

Reserve Bank of India Act, 1934 27. Guidance Note on Revision/Rectification of Financial Statements 28. Guidance Note on Signature on Statutory Audit Reports 29. Guidance Note on Auditor's Report in Case of Nationalized Banks 30. Guidance Note on Auditor's Duties in relation to the Year 2000 (Y2K) Issue 31. Guidance Note on Auditor's Duties Regarding the Voluntary Disclosure of

Income Scheme 1997 32. Guidance Note on Members� Duties regarding Engagements Involving

Compilation of Financial Statements 33. Guidance Note on Engagements to Review Financial Statements 34. Guidance Note on Section 227(3)(e) and (f) of the Companies Act, 1956

(revised) 35. Guidance Note on Audit of Companies Carrying on Life Insurance Business 36. Guidance Note on Audit of Companies Carrying on General Insurance

Business 37. Guidance Note on Audit of Expenses 38. Revised Guidance Note on Audit of Accounts of Members of Stock Exchanges 39. Supplement to the Guidance Note on Audit of Banks (2003 Edn.) 40. Guidance Note on Computer Assisted Audit Techniques 41. Guidance Note on Special Considerations in Audit of Small Entities 42. Guidance Note on Audit of Consolidated Financial Statements 43. Guidance Note on Audit of Miscellaneous Expenditure (2003)

III. Studies / Monographs / Guidelines / Guides etc. related to Auditing

1. Internal Control Questionnaire 2. Technical Guide on Audit of Sugar Industry

Status of Research in SAFA Member Bodies

28

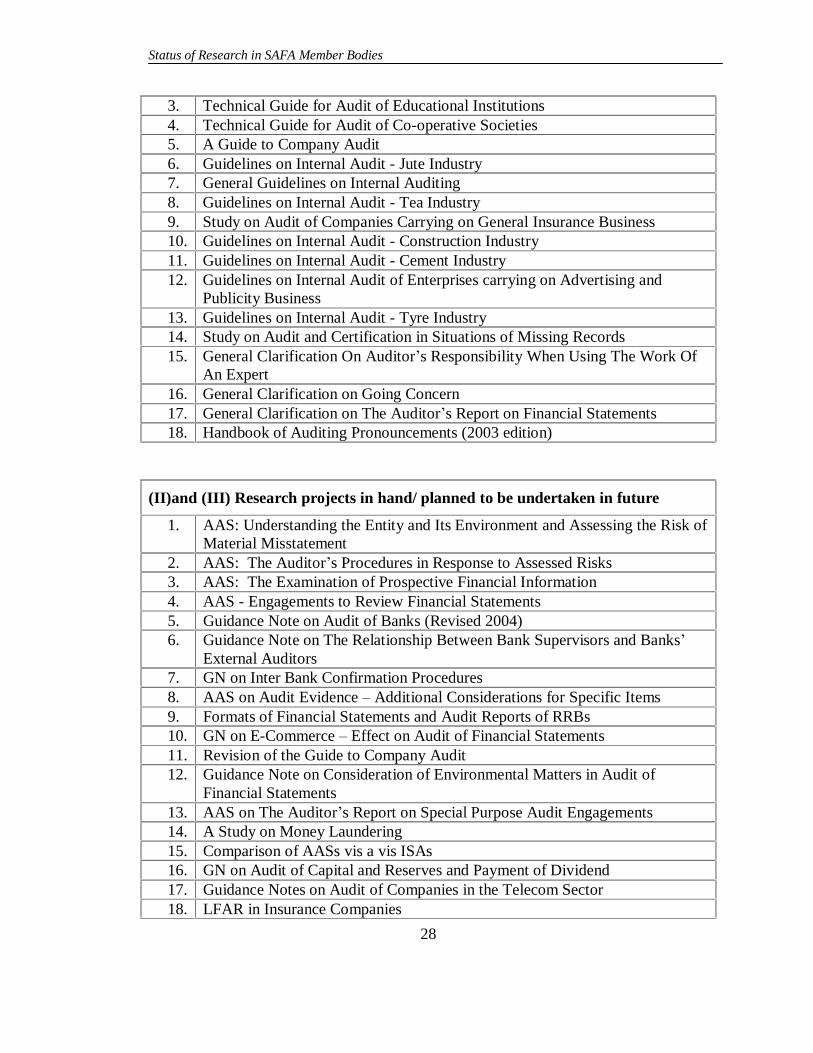

3. Technical Guide for Audit of Educational Institutions 4. Technical Guide for Audit of Co-operative Societies 5. A Guide to Company Audit 6. Guidelines on Internal Audit - Jute Industry 7. General Guidelines on Internal Auditing 8. Guidelines on Internal Audit - Tea Industry 9. Study on Audit of Companies Carrying on General Insurance Business 10. Guidelines on Internal Audit - Construction Industry 11. Guidelines on Internal Audit - Cement Industry 12. Guidelines on Internal Audit of Enterprises carrying on Advertising and

Publicity Business 13. Guidelines on Internal Audit - Tyre Industry 14. Study on Audit and Certification in Situations of Missing Records 15. General Clarification On Auditor�s Responsibility When Using The Work Of

An Expert 16. General Clarification on Going Concern 17. General Clarification on The Auditor�s Report on Financial Statements 18. Handbook of Auditing Pronouncements (2003 edition)

(II)and (III) Research projects in hand/ planned to be undertaken in future

1. AAS: Understanding the Entity and Its Environment and Assessing the Risk of Material Misstatement

2. AAS: The Auditor�s Procedures in Response to Assessed Risks 3. AAS: The Examination of Prospective Financial Information 4. AAS - Engagements to Review Financial Statements 5. Guidance Note on Audit of Banks (Revised 2004) 6. Guidance Note on The Relationship Between Bank Supervisors and Banks�

External Auditors 7. GN on Inter Bank Confirmation Procedures 8. AAS on Audit Evidence � Additional Considerations for Specific Items 9. Formats of Financial Statements and Audit Reports of RRBs 10. GN on E-Commerce � Effect on Audit of Financial Statements 11. Revision of the Guide to Company Audit 12. Guidance Note on Consideration of Environmental Matters in Audit of

Financial Statements 13. AAS on The Auditor�s Report on Special Purpose Audit Engagements 14. A Study on Money Laundering 15. Comparison of AASs vis a vis ISAs 16. GN on Audit of Capital and Reserves and Payment of Dividend 17. Guidance Notes on Audit of Companies in the Telecom Sector 18. LFAR in Insurance Companies

Status of Research in SAFA Member Bodies

29

19. Guidance Notes on IT Environments � Stand Alone Computers 20. Guidance Notes on IT Environments � Online Computer Systems 21. Guidance Notes on IT Environments � Database Systems 22. Guidance Note on Audit of Payment of Dividends 23. Guidance Note on Audit of Mutual Funds 24. Guidance Note on Audit of Payments of Dividends 25. Glossary of Terms 26. Guidance Note on Concurrent Audit in Banks

Status of Research in SAFA Member Bodies

30

3 The Institute of Cost and Works

Accountants of India (ICWAI)

3.1 Management of the Institute

The profession of Cost Accounting in India was first introduced to the Indian sub-

continent in 1944. A company under the Companies Act was registered with the

objectives of promoting, regulating, and developing the profession of Cost

Accountancy. It was reconstituted by a special Act of Parliament namely the Cost and

Works Accountants Act 1959. The Institute of Cost And Works Accountants of India

(ICWA) was then established by The Cost & Works Accountants Act 1959.

The ICWAI is managed by a Council constituted under the Act .The Council is

composed of 12 Fellow members elected by members and 4 persons nominated by the

Central Government. Duration of the Council constituted under the Act is three years

from the date of its first meeting. After election of members the Council at its first

meeting elects President and Vice President from amongst the Council members.

The ICWAI is a member of International Federation of Accountants (IFAC),

International Accounting Standards Board (IASB), Confederation of Asian & Pacific

Accountants (CAPA) and South Asian Federation of Accountants (SAFA).

3.2 Research Facility

Research Departments of the Institute assist the following technical committees doing research:

Training and Educational Facilities Committee

Professional Development Committee

Research and Publication Committee

Journal Committee

Status of Research in SAFA Member Bodies

31

3.3 Objectives of the Technical Committees

To carry out research and publication work covering various economic spheres

and the publishing of books and booklets for the information of members in

industrial, education and commercial sectors in India and abroad.

To promote and develop the adoption of scientific methods in cost and

management accounting.

To develop the professional body of members and equip them fully to discharge

their functions and fulfill the objectives of the Institute in the context of the

developing economy.

To keep abreast of the latest developments in the Cost and Management

Accounting Principles and Practices, to incorporate such changes which are

essential for sustained vitality of the industry and other economic activities.

To organize seminars and conferences on subjects of professional interest in

different parts of the country for cross-fertilization of ideas for professional

growth.

3.4 Research Setup

A Committee of ICWAI Council namely, Research and Publications Committee

(renamed: Research & Journal Committee) looks after the Research activities. The

members of the Institute�s Council elect members of the committee. One of them is

elected Chairman, while the Director of Research (a paid executive of the Institute) is

the Secretary of the Committee. The Institute has a full-fledged Research Directorate

with all facilities.

The Committee mainly formulates the policy. The Research Directorate under the

headship of Director Research carries out research activities.

Status of Research in SAFA Member Bodies

32

3.5 Functions of Research and Publications Committee

The Research & Publication Committee undertakes the following functions:

Carrying out research work on costing and allied subjects and giving guidance and encouragement to the members in various areas of research activities.

Publication of research pamphlets and other literature on behalf of the Institute, subject to approval of the Council.

Making recommendations to the Council on any or all matters relating to research and publications.

Engaging research personnel on remuneration basis, subject to the approval of the Council.

Incurring expenses within the limits sanctioned by the Council for the performance of the above functions.

Carrying out any other functions as may be assigned from time to time by the Council.

3.6 Research Studies

Research studies are undertaken according to the research policies. Members of the

Institute and other experts are invited and encouraged to undertake research studies.

The Research Project proposals are considered and approved by the Committee. The

Committee (or experts engaged by the Committee) monitors the research findings. The

final reports after approval are published as Institute�s publication. The Institute also

undertakes Applied Research Projects funded by various bodies of national importance.

3.7 Institute�s Publications

Besides the research findings of various Research Projects undertaken by the Institute

or by the experts engaged for the purpose ICWAI, also publish a bi-annual Research

Bulletin containing valuable research articles on relevant topics.

Status of Research in SAFA Member Bodies

33

3.8 Research Work

A very significant development in the area of research in ICWAI is the development of

Cost Accounting Standards and Cost Accounting Records and Cost Audit Rules.

Projects undertaken and completed are shown in Appendix-A.

3.9 Journal of the Institute

The Institute publishes a monthly Journal �The Management Accountant�, based on

research and technical articles. It is one of the most valued professional journals on

Cost and Management Accounting, Cost Management, Economics, Finance,

Management, Corporate Laws and other relevant subjects. The Journal has an active

circulation among the students and members of the Institute.

3.10 Research Library

A large number of books, periodicals and newspapers, clippings relating to the

profession and other disciplines are available in the library.

Status of Research in SAFA Member Bodies

34

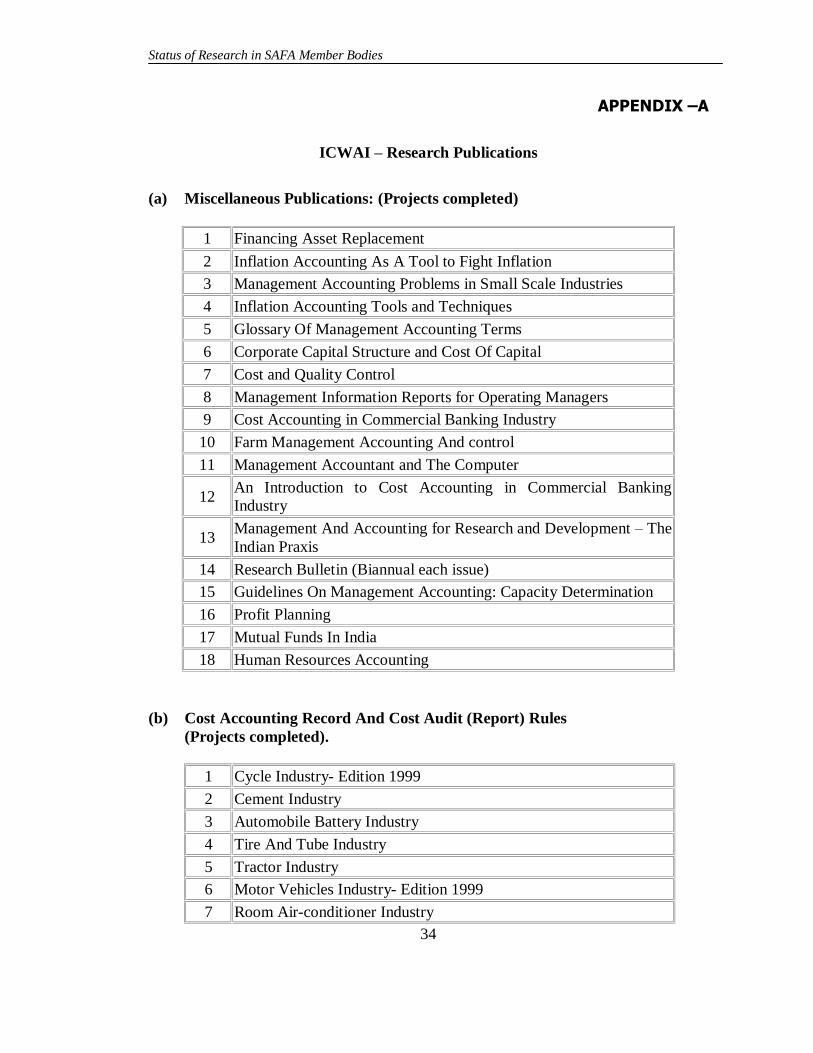

APPENDIX �A

ICWAI � Research Publications

(a) Miscellaneous Publications: (Projects completed)

1 Financing Asset Replacement

2 Inflation Accounting As A Tool to Fight Inflation

3 Management Accounting Problems in Small Scale Industries

4 Inflation Accounting Tools and Techniques

5 Glossary Of Management Accounting Terms

6 Corporate Capital Structure and Cost Of Capital

7 Cost and Quality Control

8 Management Information Reports for Operating Managers

9 Cost Accounting in Commercial Banking Industry

10 Farm Management Accounting And control

11 Management Accountant and The Computer

12 An Introduction to Cost Accounting in Commercial Banking Industry

13 Management And Accounting for Research and Development � The Indian Praxis

14 Research Bulletin (Biannual each issue)

15 Guidelines On Management Accounting: Capacity Determination

16 Profit Planning

17 Mutual Funds In India

18 Human Resources Accounting (b) Cost Accounting Record And Cost Audit (Report) Rules (Projects completed).

1 Cycle Industry- Edition 1999

2 Cement Industry

3 Automobile Battery Industry

4 Tire And Tube Industry

5 Tractor Industry

6 Motor Vehicles Industry- Edition 1999

7 Room Air-conditioner Industry

Status of Research in SAFA Member Bodies

35

8 Refrigerator Industry

9 Electric Fan Industry

10 Caustic Soda Industry

11 Electric Motors Industry

12 Aluminum Industry

13 Vanaspati Industry

14 Industrial Alcohol Industry- Edition 1999

15 Sugar Industry- Edition 1999

16 Paper Industry

17 Textile Industry- Edition 2001

18 Soda Ash Industry

19 Dyes Industry

20 Jute Industry

21 Rayon Industry- Edition 2001

22 Dry Cell Battery Industry Dry Cell Battery Industry

23 Power Driven Pump Industry

24 Cables and Conductors Industry

25 Milk Food Industry

26 Sulphuric Acid Industry

27 Steel Tubes & Pipes Industry

28 Fertilizer Industry

29 Insecticides- Tech. Grade Industry

30 Cosmetics & Toiletries Industry-Edition 2001

31 Shaving Systems Industries -Edition 2001

32 Polyester Industries �Edition 2001

33 Footwear Industries -Edition 2001

34 Soaps & Detergent Industries -Edition 2001

35 Industrial Gases Industries -Edition 2001

36 Nylon Industry- Edition-2001

Status of Research in SAFA Member Bodies

36

4 The Institute of Chartered

Accountants of Pakistan (ICAP) 4.1 Management of the Institute

The Institute of Chartered Accountants of Pakistan (ICAP) was established on July 1,

1961 to regulate the profession of accountancy in the Country. It is a statutory

autonomous body under the Chartered Accountants Ordinance 1961. Necessitated by

significant growth in the profession, the Chartered Accountants Ordinance and Bye-

Laws were revised in 1983.

Head office of the Institute is in Karachi. The Institute also has regional offices at

Lahore and Islamabad. The ICAP is a member of International Federation of

Accountants (IFAC), International Accounting Standards Board (IASB), Confederation

of Asian & Pacific Accountants (CAPA) and South Asian Federation of Accountants

(SAFA).

Affairs of the Institute are managed by a Council which discharges the functions

assigned to it under the Ordinance. The Council is elected for a term of four years. It is

composed of 16 members. Twelve members are elected by the members of the

Institute. Four members are nominated by the Federal Government. The Council also

elects two Vice Presidents every year, one each from Northern and Southern Region.

4.2 Research Setup

The Institute has formed various Committees for research and other technical work.

Functions of these committees are as under:

Professional Standards & Technical Advisory Services

The Professional Standards & Technical Advisory Committee (PS&TAC) is the apex

Committee of the ICAP in all matters relating to:

Status of Research in SAFA Member Bodies

37

Accounting Standards,

Auditing Standards,

Code of Ethics,

Corporate Laws, and

Technical queries from members.

It is supported by two Accounting & Auditing Standards Committees (AASC) and two

Technical Advisory Committees (TAC), in South and North Region.

Accounting and Auditing Standards Committees (South) & (North)

The above Committees:

Examine and offer comments on the Exposure Drafts of the International Accounting Standards (IAS) & IFRS issued by the International Accounting Standards Board (IASB)

Consider and give recommendation regarding adoption of IAS/IFRS issued by the IASB to the Council of the Institute.

Examine and offer comments on the Exposure Drafts of the International Standards on Auditing (ISAs) issued by the International Federation of Accountants (IFAC)

Consider and give recommendation regarding adoption of ISAs issued by IFAC to the Council of the Institute

Develop disclosure checklist based on the requirements of IASs and Fourth Schedule to the Companies Ordinance, 1984

Research the current trends in financial reporting and suggest appropriate changes in the local regulations

Technical Advisory Committees (South) & (North)

Technical Advisory Committees (South) and (North):

Conduct research and issue Technical Releases on accounting and auditing matters namely TRs and ATRs

Issue circulars to the members of the Institute on upcoming issues to keep them updated

Examine queries on technical matters from members and send appropriate

Status of Research in SAFA Member Bodies

38

reply

Publish (finalized) selected opinions

Joint Committee of ICAP/State Bank of Pakistan

Joint Committee of ICAP and SBP has been constituted to expeditiously resolve the

issues relating to accounting and auditing of banks. The key focus areas are as under:

Conduct research and develop guidelines for external auditors to assist SBP in its supervisory role.

Examine applicability of IAS 39 and IAS 40 on banks and devise a modus operandi to smoothly implement these IASs.

Accounting and Auditing Standards for Interest Free Modes of Financing and Investments

The above Committee:

Conducts research particularly on accounting aspects of Islamic modes of financing

Develops and issues standards on the identified products of Islamic modes of financing and investments

Consults Shariah experts for clarification on various issues which come across during development of the Standards mentioned above.

Deals with queries relating to application of interest free modes of financing and investments

Committee on Taxation and Economic Policies

This Committee:

Considers queries relating to taxation and economic policies

Develops detailed proposals for incorporation in the Federal Budget

Offers comments on the drafts of rules and regulations relating to Income Tax, Sales Tax, Customs and Excise Duty etc.

Suggests necessary amendments in the rules and regulations with a view to

Status of Research in SAFA Member Bodies

39

simplify the process and facilitate the taxpayers

Committee on Banking

The Committee on Banking:

Considers various accounting and auditing matters relating to banks, DFIs and NBFCs

Examines and offers comments on regulations and guidelines issued by the State Bank of Pakistan and Securities and Exchange Commission of Pakistan, relating to DFIs and NBFCs

ICAP Committees are composed of Chartered Accountants in public practice and

industry and also learned persons from outside the profession.

The Director Technical Department along with his staff is mainly responsible for

providing support to the above committees.

The Technical Department also coordinates with international professional bodies such

as IASC, IFAC, SAFA, CAPA and Accounting & Auditing Organization for Islamic

Financial Institutions.

4.3 Research Work

Projects undertaken and finished are shown in Appendix-A.

4.4 Journal of the Institute

The Institute brings out a bi-monthly Journal �The Pakistan Accountant�. It contains

research and technical articles.

4.5 Research Library

The Technical Department has a Research Library. A large number of books and

journals on different subjects are available in the library.

Status of Research in SAFA Member Bodies

40

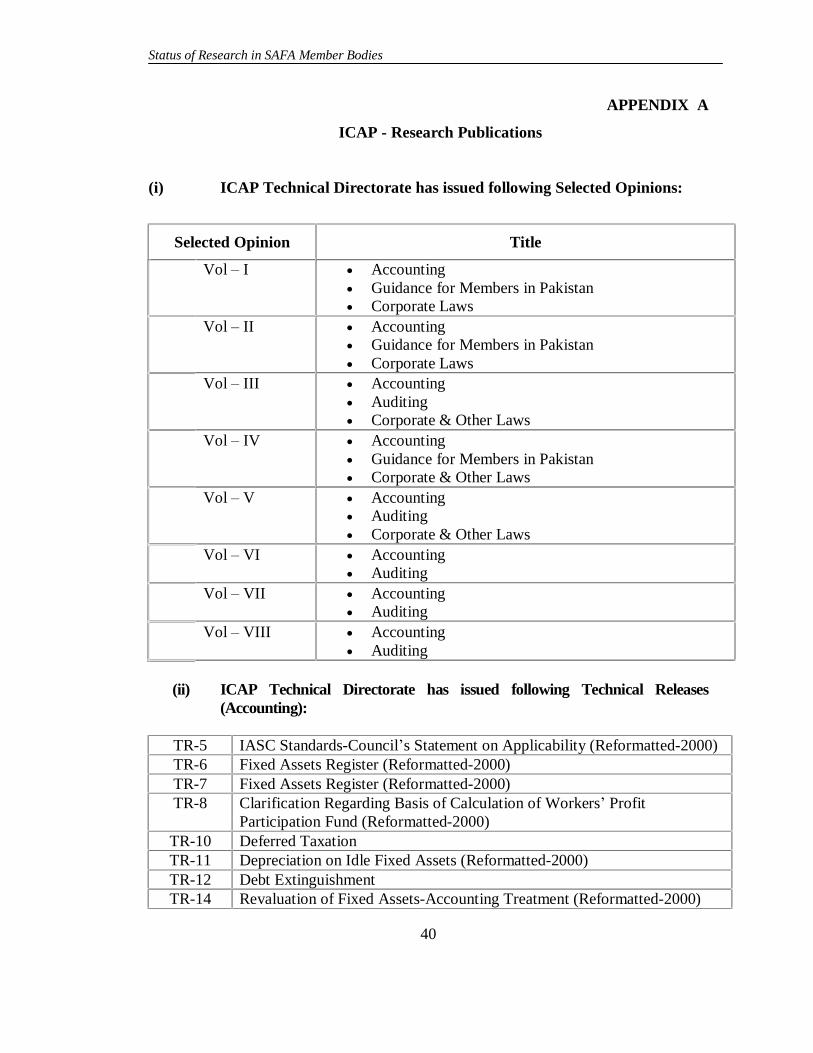

APPENDIX A

ICAP - Research Publications

(i) ICAP Technical Directorate has issued following Selected Opinions:

Selected Opinion Title

Vol � I Accounting Guidance for Members in Pakistan Corporate Laws

Vol � II Accounting Guidance for Members in Pakistan Corporate Laws

Vol � III Accounting Auditing Corporate & Other Laws

Vol � IV Accounting Guidance for Members in Pakistan Corporate & Other Laws

Vol � V Accounting Auditing Corporate & Other Laws

Vol � VI Accounting Auditing

Vol � VII Accounting Auditing

Vol � VIII Accounting Auditing

(ii) ICAP Technical Directorate has issued following Technical Releases

(Accounting):

TR-5 IASC Standards-Council�s Statement on Applicability (Reformatted-2000) TR-6 Fixed Assets Register (Reformatted-2000) TR-7 Fixed Assets Register (Reformatted-2000) TR-8 Clarification Regarding Basis of Calculation of Workers� Profit

Participation Fund (Reformatted-2000) TR-10 Deferred Taxation TR-11 Depreciation on Idle Fixed Assets (Reformatted-2000) TR-12 Debt Extinguishment TR-14 Revaluation of Fixed Assets-Accounting Treatment (Reformatted-2000)

Status of Research in SAFA Member Bodies

41

TR-15 Bonus Shares-Accounting Treatment (Reformatted-2000) TR-19 Excise Duty-Accounting Treatment (Reformatted-2000) TR-20 Accounting for Expenditure During Construction Period (Reformatted-

2000) TR-21 Date of Commencement of Commercial Production (Reformatted-2000) TR-22 Book Value Per Share (Revised-2002) TR-23 Accounting for Investments (Revised-1998) TR-24 Exchange Risk Free-Accounting Treatment (Reformatted-2000) TR-25 Prudential Regulations for Banks (Reformatted-2000) TR-27 IAS 12, Accounting for Taxes on Income TR-28 Golden Handshake �Accounting TR-29 Carry-Over-Transaction (COT)

(iii) Auditing Technical Releases of ICAP

ATR-1 Only members to sign audit documents ATR-6 Audit by ex-employees (Reformatted 2002) ATR-8 Preparation of accounts from incomplete records and report thereon as

auditor (Reformatted 2002) ATR-9 Signing of correspondence and financial statements by members

ATR-11 Appointment of auditors �I (Reformatted 2002) ATR-12 Appointment of auditors-II ATR-13 Lien on books of accounts due to non-payment of professional dues ATR-14 Minimum hourly charge out rates for audit work by practicing members

(Revised) ATR-16 Acceptance of Audit Assignments by New Auditors by New Auditor(s)

when Audit Fee of Existing Auditor(s) is Outstanding ATR-17

Auditors� Report to the Trustees/Board of Governors/Management Committee

Status of Research in SAFA Member Bodies

42

5 Institute of Cost and Management Accountants of Pakistan (ICMAP)

5.1 Management of the Institute

The Institute was established in the year 1951 as a company limited by guarantee under

the name and style of Pakistan Institute of Industrial Accountants. Its founder members

included persons like late Mohammad Shoaib, Ex-Finance Minister of Pakistan and

Executive Vice President of World Bank. Mr. Mohammad Shaoib was the first

President of ICMAP.

The Institute was reconstituted under an Act of Parliament in 1966 and

rechristened Institute of Cost and Management Accountants of Pakistan.

Head Office of the Institute is located at Karachi. The Institute also has regional offices

at Lahore and Islamabad where it has own spacious campus also. The ICMAP is a

member of International Federation of Accountants (IFAC), International Accounting

Standards Board (IASB), Confederation of Asian & Pacific Accountants (CAPA) and

South Asian Federation of Accountants (SAFA).

The Council is the governing body of the Institute. It is constituted under the Cost and

Management Accountants Act 1966, to look after the affairs of the Institute. The

Council has 12 members of which 8 are elected. Four members are nominated by the

Federal Government. The Council is required to discharge its statutory functions as

provided under the Act & Regulations.

The Council is elected for a term of three years. Office bearers are elected from

amongst 12 Council members.

Status of Research in SAFA Member Bodies

43

5.2 Research Setup

A full-fledged Research Department exists in the Institute. The Research Department

which is headed by a Director who functionally reports to the Research Committee.

Outside researchers are also hired by the Institute for specific research projects. This

Department was established in 1989 with the following objectives:

To identify potential areas of research and make strategic plans for pursuing research projects.

To promote and encourage a congenial research environment for the members and students.

To draft Cost Accounting Record Orders for major industries and take steps for upgrading existing rules in the light of experience and feedback.

To update members on current issues of topical interest, particularly for practicing members.

To review and recommend revision in Cost Accounting Record Orders to the Securities & Exchange Commission of Pakistan (SECP).

To provide help and assistance to members in practice.

To provide information to members on professional issues.

To liaise with IASB bodies on professional pronouncements and to offer comments and make recommendations.

To seek enforcement and pronouncements by international and regional bodies.

To liaise with the regional Advisory Committees for research.

The Research Department carries out its functions under a Research Committee,

members whereof are named by the Council. Members of the Research Committee

consist of members of ICMAP Council, Members of the Institute and people from

outside the Institute. Subject specialists and academicians are invited to attend

meetings of the Research Committee.

Status of Research in SAFA Member Bodies

44

5.3 Research Work

The Research Department since its establishment has carried out the following research

studies. The studies, duly approved by the Research Committee and the National

Council, have been published:

Cost & Management Accounting Techniques � Employed in the Cotton Textile (Ring).

Sugar Industry in Pakistan � Problems and Potentials (2000)

Input Costs and Corporate Tax Structure � An Analysis of Trends in SAARC

Region (2001)

Role of Small & Medium Enterprises in GDP and Macro Economic Development of Pakistan (2001)

Cost Audit Handbook (2001)

Cost Accounting Records Rules enforced in Pakistan: Cost Accounting Record

Order - Cement Industry

Cost Accounting Record Order

- Vegetable Ghee/Cooking Oil Industry

Cost Accounting Record Order

- Sugar Industry � 2000

Draft Cost Accounting Record Rules submitted to Securities and Exchange Commission of Pakistan (SECP) for enforcement:

Cost Accounting Record Order

- Pharmaceutical Industry � 2000

Cost Accounting Record Order

- Chemical Fertilizer Industry � 2000

Cost Accounting Record Order

- Cotton Textile Industry � 2000

Cost Accounting Record Order

- Thermal Power Generating Cos. 2001

Cost Accounting Record Order

- Engineering Industry � 2002

Status of Research in SAFA Member Bodies

45

Cost Accounting Record Order

- Motor Vehicle Industry 2002

Cost Accounting Record Order

- Synthetic & Rayon Industry 2002

Cost Accounting Record Order

- Electric Cables & Conductors Industry � 2003

Cost Accounting Record Order

Cycle Industry 2003

Cost Accounting Record Order

Steel Tubes and Pipe Industry 2003

Studies are in the process of review: History of Profession of Management Accounting Profession in

Pakistan Housing Industry as a catalyst for Pakistan�s economy

Industries identified for future research studies and development of Cost Accounting Record Rules:

1. Automobile Battery Industry

2. Caustic Soda Industry

3. Dyes Industry

4. Steel Tubes and Pipes Industry

5. Paper Industry

6. Refrigerator Industry

7. Soda Ash Industry

8. Tractor Industry

9. Tires & Tubes Industry

10. Gas Industry

11. Room Air Conditioner Industry

12. Aluminum Industry

13. Commercial Banks

14. Petroleum Industry

15. Telecommunications Industry

16. Electric Fan Industry

Status of Research in SAFA Member Bodies

46

17. Electric Lamp Industry

18. Electric Motor Industry

5.4 Journal of the Institute

The Institute publishes monthly Journal �Management Accountant� which carries

research and technical articles. When invited Research Department assists the Journal

Committee also in its publications.

5.5 Research Library

The Institute has a research library equipped with technical books, Journals, IFAC,

IASB, CAPA and SAFA publications, newspapers clippings on related subjects and

commerce, trade and finance. Research sections exist in ICMAP�s libraries at Lahore,

Islamabad and Multan also.

5.6 ICMAP Publications List of publications of the Institute appears at Appendix A.

Status of Research in SAFA Member Bodies

47

APPENDIX A ICMAP � PUBLICATIONS

Title 1. The Interpretations of Financial Statements and Operating Reports

2. Economic Reforms Order, 1972 3. Effective Management Reporting System 4. Tax Planning 5. International Accounting Standards 6. Effective Cash Management 7. Corporate Laws, Companies Ordinance, 1984 8. Investment Strategy for Industrial and Economic Development 1988-89 9. Cost Audit Practical Guidelines

10. Cost Accounting � A Tool for Performance Evaluation 11. Privatization � An Overview 12. Future Challenges for Audit 13. Contemporary Issues of Today�s Economy 14. Role of Management Accountants in Developing Countries 15. Modern Trends and Techniques of Management 16. Challenges of 21st Century and the Role of Management Accountants 17. Synergetic Dimension of Management 18. Modern Economic Trends and International Challenges to Industries in Pakistan 19. Responsibility of Management Accountants in Developing Countries 20. Management Accountants in Changing Global Perspective 21. The Edge of Management Accountants 22. Management Accounting - Challenges and Prospects 23. Legal Requirement for Listing of Companies - need for Restructuring of Corporate

Laws 24. Adding Value to Business 25. Inflation Accounting 26. Management Audit 27. Time Management 28. The Use of Financial Information by the Chief Engineers for Management of Large

Scale Projects 29. Divine Accounting 30. Exploring the New Frontiers of Management Accounting 31. Management Accounting for Optimal Utilization of Resources 32. Interest Free Economy and the Management Accountants 33. Management Accountants Role in Market Economy 34 Debt Management in Developing Countries 35 Education and Training of Industrial Accountants 36 Profitable Inventory Management 37 Productivity and Cost Control

Status of Research in SAFA Member Bodies

48

38 The Nature and Purpose of Organization 39 Accounting Education in Pakistan 40 Waste in Project Planning, Investment Decisions and Project Implementation in

Public Enterprises in Developing Countries 41 Excellence in Manufacturing Innovative Role of Management Accountants in

Strengthening Quality Management Systems 42 Information Technology (Electronic Commerce) 43 How to Install a Cost System 44 International Accounting Standards 45 Managerial Effectiveness

46 The Future of Management Accounting in Developing Countries 47 The Integration of Managerial and Financial Accounting 48 New Accountancy 49 Internationalization of Accounting Profession 50 Capital Structure of Public Enterprises 51 Management Accounting in Government 52 Constraints to the Acceptance and Achievement of the Need for Accounting and

Accountability 53 The Application of Internal Auditing to Managerial Accounting 54 Wither Management Accounting 55 Performance and Financial Management in Public Sector Institutions 56 Control Accountability and the Management Accountants 57 The Convergence of Management Accountancy and Information Technology 58 Managing Accounting in the 21st Century 59 The Management Accountants in the Information Age 60 From Management Accounting to Executive Management and the Boardroom 61 The Challenge and Management of Change 62 Sugar Industry in Pakistan � Problems, Potentials 63 Cost and Management Accounting Techniques Employed in the Cotton Textile

(Ring) Spinning Industry of Pakistan 64 Cost Audit Handbook 65 Report on the Role of Small and Medium Enterprises in GDP and Macro Economic

Development of Pakistan 66 Input Costs and Corporate Tax Structure - an Analysis of Trends in SAARC

Region 67 SAFA Computer Education of Accountants in South Asia Approved by the SAFA

Assembly prepared and printed by ICMAP 68 Income Tax Ordinance 1979 - Critical Appraisal 69 Match Unmatch/Revenue Record Unit 70 Issues in Contemporary Manufacturing Management 71 The Role of Management Accounting in Creating Value 72 Cost and Management Audits for Banks

Status of Research in SAFA Member Bodies

49

6 The Institute of Chartered

Accountants of Bangladesh (ICAB)

6.1 Management of the Institute

The Institute of Chartered Accountants of Bangladesh (ICAB) is the National

Professional Accounting Body of Bangladesh, established under the Bangladesh

Chartered Accountants Order 1973 (Presidential Order No. 2 of 1973).

The Ministry of Commerce, Bangladesh is the regulating body of ICAB, which is an

autonomous professional body.

The Council of ICAB is responsible for the administration and management of the

Institute. The Council is composed of 20 members elected after every three years by

the members of the Institute from its two regional constituencies at Dhaka and

Chittagong in Bangladesh. The Council is headed by an elected President who is the

Chief Executive of the Institute. The President and the Vice-President of the Institute

are elected by the Council to manage the affairs of the Institute. The Council is

assisted by its various standing and non-standing committees. For the purpose of

assisting the Council in matters concerning its functions, the Council is empowered to

constitute Regional Committees. Presently there are two Regional Committees, one in

Dhaka and other in Chittagong. The Council has also formed two chapters one at

London, UK and other in Canada at Toronto.

The Institute of Chartered Accountants of Bangladesh is member of International

Federation of Accountants (IFAC), the Confederation of Asian & Pacific Accountants

(CAPA), International Accounting Standards Board (IASB) and South Asian

Federation of Accountants (SAFA).

Status of Research in SAFA Member Bodies

50

6.2 Research Setup

The Council, besides other standing committees, has established a Technical &

Research Committee, which undertakes research work. The Committee functions

under a Chairman who is assisted by the Institute�s secretariat.

At present, there is no independent Research Department. The Director of Studies

looks after research work also. He is assisted by an Assistant Director (Technical &

Research). There are two supporting staff to look after various technical & research

related activities of ICAB.

6.3 Research Projects

Research Projects Finalized:

1st Phase of review and adoption of Bangladesh Accounting Standards (BAS)

and Bangladesh Standards on Auditing (BSA) has been completed.

Research Projects in Hand:

2nd phase of review and adopting Bangladesh Accounting Standards (BAS)

and Bangladesh Standards on Auditing (BSA) is in hand.

Research Projects Planned To Be Undertaken in Future:

As per recent negotiations between World Bank and Govt. of Bangladesh,

ICAB is expecting to obtain US$1.37 million as grant from World Bank to

strengthen the capacity of ICAB. Management of ICAB is preparing the

project profile in this regard. The proposed project is likely to start from July

2005.

6.4 Research Library

ICAB maintains a central library in Dhaka for the use of its members & students and

other research-oriented activities. There are 10,680 books and journals in the library.

Collection in the library has a good number of research related books and other

material.

Status of Research in SAFA Member Bodies

51

6.5 Research Publications

Research publications of ICAB are shown in Appendix-A

6.6 Journal of the Institute

The Institute publishes a quarterly journal titled "The Bangladesh Accountant" and a

monthly "News Bulletin". The journal provides an opportunity to publish research

and review articles by the faculty of the Institute and fellow academicians elsewhere.

The journal includes articles on different topics of interest for readers.

Status of Research in SAFA Member Bodies

52

APPENDIX-A

ICAB-Research Publications

Publications jointly published by ICAB & UNDP under the project "Training of Chartered Accountants" (No: BGD/85/014) in December 1994:

i. National Economic Management: Project Training of Chartered Accountants;

ii. Technical Guide on Audit of Non-Government Educational Institutions;

iii. Technical Guide on Audit of Development Financial Institutions; iv. Technical Guide on Audit of Textile Industries; v. Technical Guide for Audit of Chemical Industries;

vi. Technical Guide on Audit of Sugar Industry; vii. Technical Guide on Audit of Public Utility Organizations;

viii. Management and Organization Structure: Diploma in Corporate Management;

ix. Advanced Management Accounting: Diploma in Advanced Financial Management;

x. Human Factor in Management: Diploma in Corporate Management; xi. Production and Productivity Management: Diploma in Corporate

Management; xii. Marketing Management: Diploma in Corporate Management;

xiii. Organization & Management Development: Diploma in Corporate Management;

xiv. Compendium of the Income Tax in Bangladesh: As Amended up to 30 June 1994; Bank Audit Guide;

xv. Economic Accounting and Finance; xvi. Management Control: Diploma in Corporate Management;

xvii. Tax Management: Diploma in Corporate Management; xviii. Management Audit Including Case Study: Diploma in Advanced

Financial Management; and xix. Management Accounting: Diploma in Advanced Financial

Management; Publications published by ICAB in March 2003 under The World Bank financed project "Development of Accounting and Auditing Standards in Bangladesh":

i. Strategic Plan for the Institute of Chartered Accountants of Bangladesh for 2003-2017;

Status of Research in SAFA Member Bodies

53

ii. Checklist for Standard Disclosures and Compliance; iii. Ethical Standards and Independence of Chartered Accountancy Profession in

Bangladesh; iv. Corporate Governance in Bangladesh; v. Education and Training System for Accountancy Profession in Bangladesh;

vi. Survey of Published Annual Reports of Listed Companies (Financial); and vii. Survey of Published Annual Reports of Listed Companies (Non-Financial);

OTHER PUBLICATIONS:

(a) Evaluation of Financial Statement as a Communication Device in Bangladesh

(Research study) written by Mr. Mahbub Ahmed, Associate Professor, Department of Accounting, University of Dhaka - First Edition, December 1982.

(b) Bangladesh Accounting Standards (BAS), Volume I & II, published by the

Institute of Chartered Accountants of Bangladesh, in April, 2004. (c) Bangladesh Standards on Auditing (BSA), published by the Institute of

Chartered Accountants of Bangladesh, in August 2004.

Status of Research in SAFA Member Bodies

54

7 The Institute of Cost and Management

Accountants of Bangladesh (ICMAB)

7.1 Management of the Institute

The Institute of Cost and Management Accountants of Bangladesh, an autonomous

professional body under the Ministry of Commerce, Government of People's Republic

of Bangladesh, is dedicated to Cost and Management Accounting education and

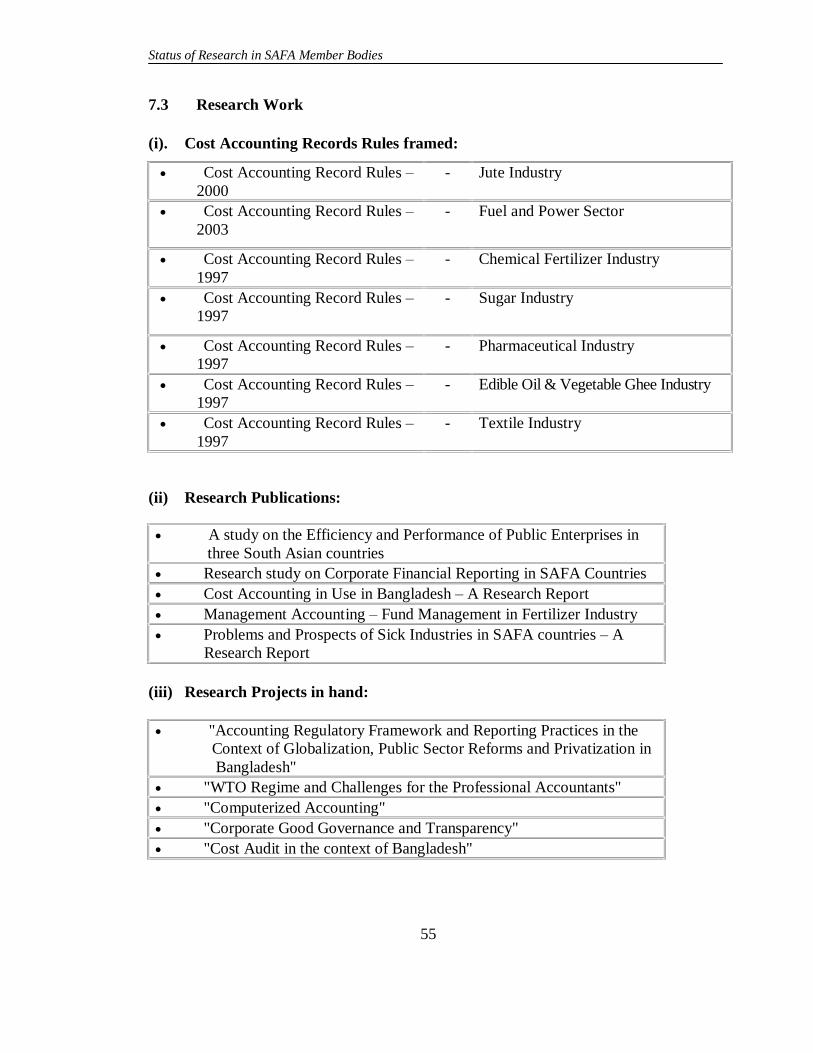

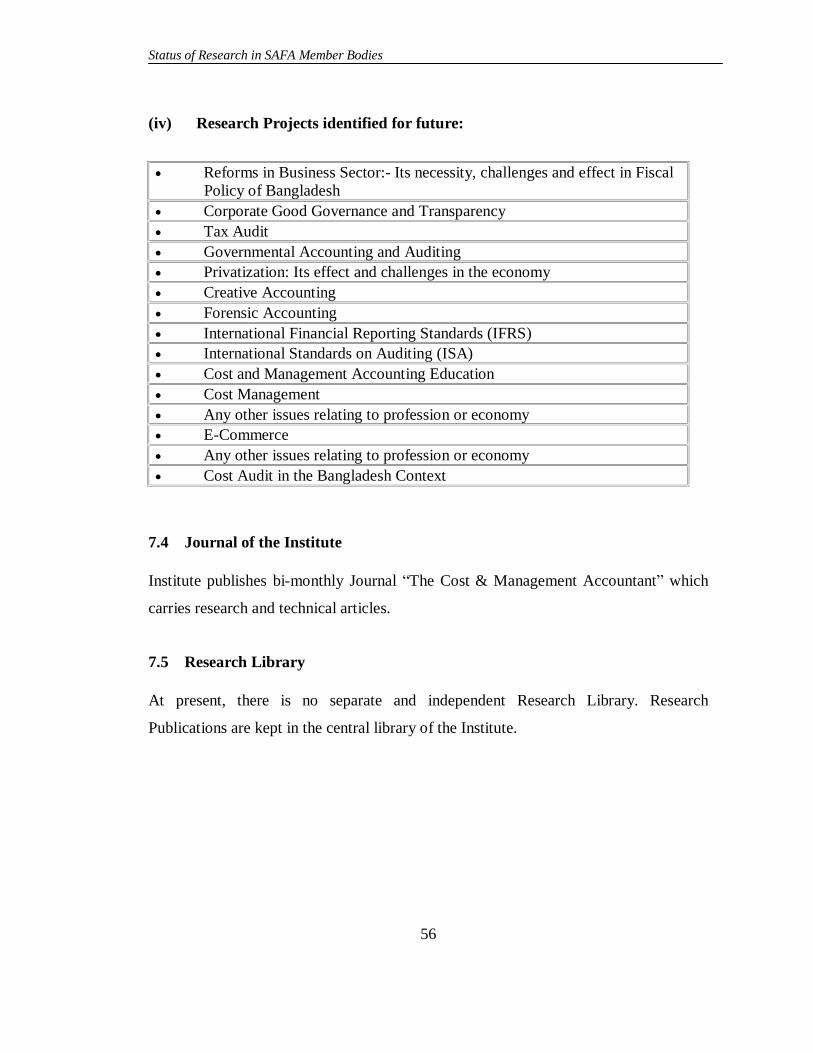

research.