Embed Size (px)

Citation preview

Statistics Yearbook

Personal debt

2013

Our objectives

• Creategreaterawarenessof,andaccessto,trulyfree debt advice and debt solutions

• Developextensiverelationshipswithotherorganisations to bring greater help and support to people with problem debt

• Providenewandimprovedproductsandservicesto meet the changing needs of people with problem debt

• Investinourpeople,processesandsystemstoeffectively deliver timely and high quality help and support

• Buildarobust,stableandsustainablecharitythatcan be relied on by all in society

• Championthecauseof peopleinoratriskof problem debt by influencing policymakers and campaigning for change

• Enhancepeoples’financialunderstandingandcapability so they can better manage their money and debts

STEPCHANGE DEBT CHARITY RESEARCH

Main Findings 2013 1

Chief Executive’s Introduction 2

Section 2: Demand 3• Demandforadvice• Debtmap• Reasonsfordebt• Recommendationsflowchart• Demandforadvice–age• Demandforadvicebychannel• Demandforadvice–gender• Demandforadvice–familytype• Demandforadvice–housingtenure• Numberof clientswithbenefits• Clientsonbenefits–averagesurplus• Employment• Ourclientsurvey

Section 3: Debts 15• Averageunsecureddebt• Unsecureddebtlevels• Averageunsecureddebt–age• Averageunsecureddebt–gender• Averageunsecureddebt–housingtenure• Averageunsecureddebt–familytype• Averageunsecureddebt–employment• Typesof unsecureddebt

• Numberof unsecureddebts• Sizeof problembynumberof debtsseen• Multipleunsecureddebts–creditcards• Multipleunsecureddebts–paydayloans• Debttofamilyand/orfriends• Debtcocktails

Section 4: Arrears on essential household bills 25• Arrearsonessentialhouseholdbills• Arrearsnumbers/debts• Arrearsonessentialhouseholdbills–age• Arrearsonessentialhouseholdbills–gender• Arrearsonessentialhouseholdbills–familytype• Arrearsonessentialhouseholdbills–housingtenure

Section 5: Social Policy 29• SocialPolicy–organisations• SocialPolicy–issues• SocialPolicy–biggestconcerns

Appendix 32

ThedataintheStatisticsYearbookisdrawnfromawarehousecontainingthedetailsof morethan16mphonecallsand2.3mclients.The2013dataanalysesaround300,000clientswhoreceivedafulladvicesessionfromStepChangeDebtCharitylastyear.

Table of Contents

You’llnoticeafewchangesinthisyear’sStatisticsYearbook.We’vedecidedtofreshenitupabitbymakingitmorevisuallyexcitingandconcentratingonstatisticsthatbestexplainourclients’stories.Wehopeyouenjoythechanges.

STATISTICS YEARBOOK 2013 1

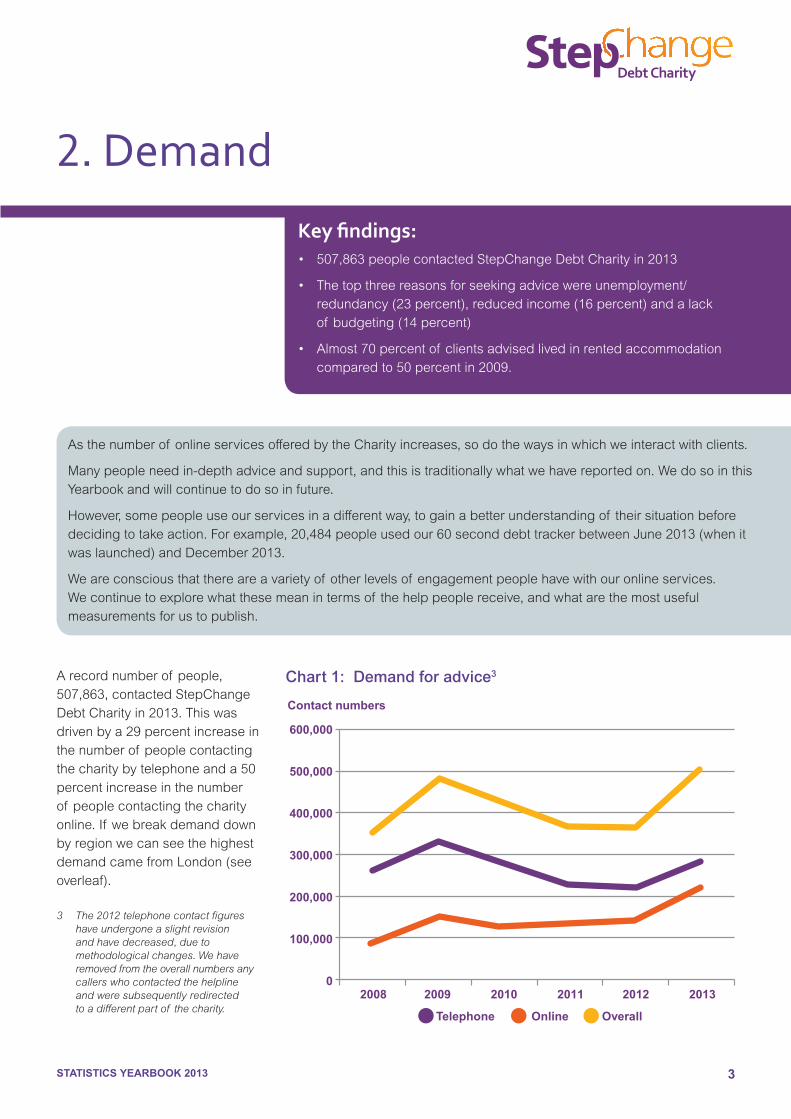

• Arecordnumberof people,507,863,contactedStepChangeDebtCharityin2013.Thiswasdrivenbya29percentincreaseinthenumberof peoplecontactingthecharitybytelephoneanda50percentincreaseinthenumberof peoplecontactingthecharityonline

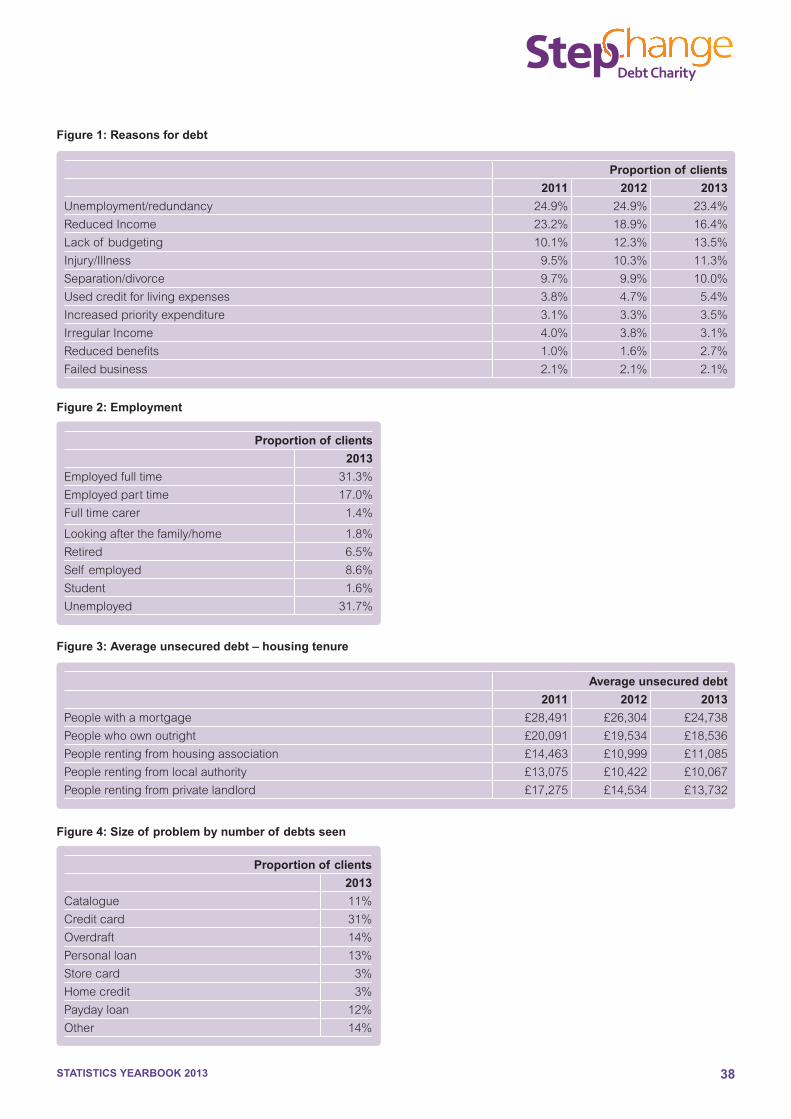

• Asinpreviousyears,demandforadvicewasprimarilyaresultof unemployment(23percent)andreducedincomeresultingfromalossof hoursatwork(16percent)

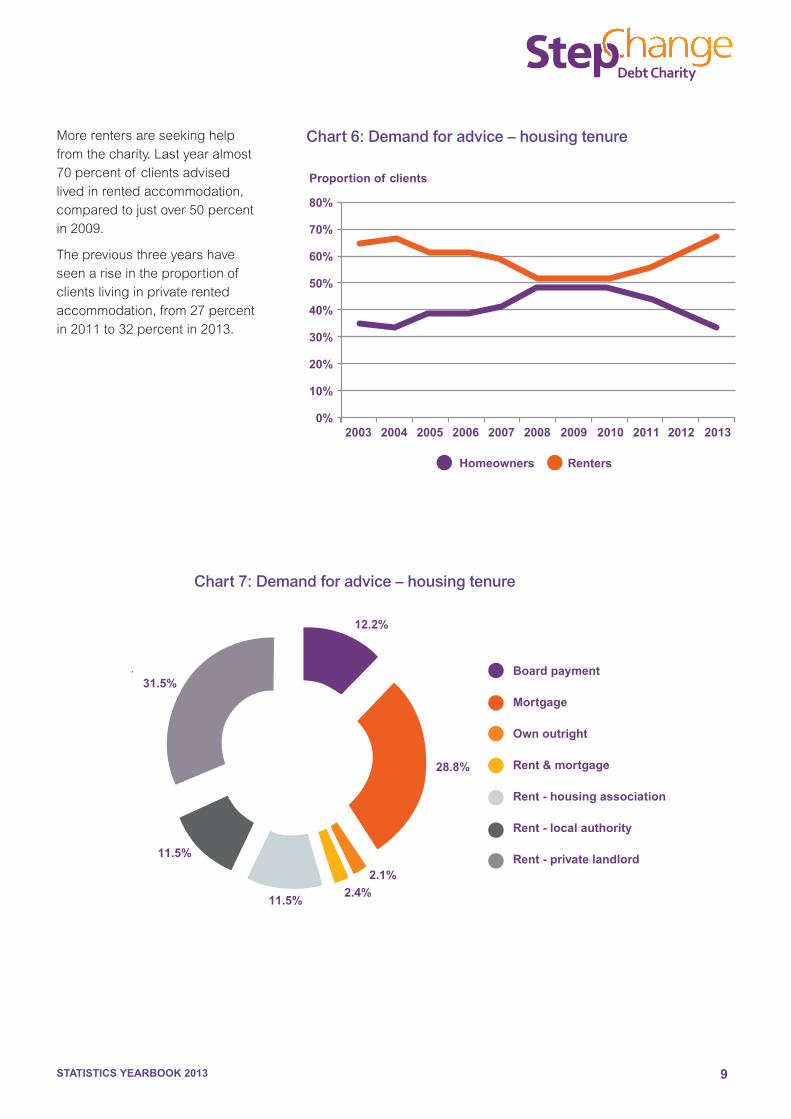

• Theproportionof peoplewholiveinrentedaccommodationseekingadvicefromthecharitycontinuestogrow.Lastyearalmost70percentof clientsadvisedlivedinrentedaccommodation,comparedtojustover50percentin2009

• Beinginworkdoesnotnecessarilyprotectpeoplefromdebtproblems;overhalf of clientsseekinghelpwereinwork,31percentemployedfulltime

• Relyingprimarilyonincomefromjobseeker’sallowancemeansthatpeopledonothaveenoughmoneytomeettheiressentialspend.Clientsreceivingthebenefithave,onaverage,significantlyhigheroutgoingsthanincome

• Theresultsof ourclientsurveyshowedthatindebtedconsumersstillcontinuetowaitalongtimebeforeseekingdebtadvice.Half of thosesurveyedwaitedmorethanayearbetweenrealisingtheirdebtswereaproblemandseekinghelpfromanydebtadviceprovider

• Oursurveyshowedthepsychologicalimpactproblemdebtcanhaveonindividuals.Three-quartersof respondentsexperiencedsleepingproblemsduetotheirdebt,and64percentexperiencedmoodswings.Over50percentalsofoundtheirworkperformancesufferedasaresultof problemdebt

• Paydayloanscontinuetocausehugeproblemsforconsumers.StepChangeDebtCharityclientswithpaydayloanshave,onaverage,three,withtheaveragepaydaydebt(£1,647)outstrippingaverageincome

• Thelastfiveyearshaveseenaworryingriseintheproportionof StepChangeDebtCharityclientswitharrearsonessentialhouseholdbills.ThelargestrisehasbeeninCouncilTaxarrears,wheretheproportionof clientswithmissedpaymentshasincreasedfromlessthan10percentin2009to

over25percentin2013

• Thecharityhasalsoseenbigrisesintheproportionof clientswitharrearsonutilitybills.Around13percentof clientshavearrearson

gasandelectricitybills.

Main Findings 2013

STATISTICS YEARBOOK 2013 2

1 Office of National Statistics: An Examination of Falling Real Wages, 2010 – 20132 ONS Economic Review for November

Since2006ourStatisticsYearbookhasilluminatedthedifficultiesfacedbyhouseholdsstrugglingwithproblemdebtacrosstheUK.Thisyear,myfirstasChief Executiveof theUK’slargestdebtadvicecharity,thedatarevealsacomplexbutconcerningstory.

Althoughthereiswelcomeevidenceof economicgrowth,andaveragedebtisfalling,manypeoplearestilllivinginaverydifficulteconomicenvironment,onethatrequiresarobust,comprehensiveandcoordinatedapproachtohouseholdproblemdebtbygovernment,creditors,serviceprovidersandcharities.

Wehavecontinuedtoseeasharpriseinthenumberof peoplewithhigh-cost,short-termcredit.67,000of thepeopleweadvisedin2013hadpaydayloans,almostdoublethepreviousyear.Over20percentof thoseseekingourhelpwithpaydayloanshadtakenoutmorethanfive,showinganongoingproblemwithirresponsiblelendingpracticeswhichwehopetheFinancialConductAuthoritywilltackle.

Therehasalsobeenasharpincreaseinthenumberof peoplecomingtouswitharrearsonessentialhouseholdbills–thedebtsmanypeoplearestrugglingwitharenottheresultof oneoffextravagances,butastructuralshortfallbetweentheirincomeandessentiallivingexpenses.Theproportionof clientswitharrearsontheirCouncilTaxhasincreasedfrom10percentin2009toover25percentin2013.Theproportionof clientswitharrearsonutilitybills,gasandelectricity,hasdoubledoverthesameperiod.Theneedforinvestmentininfrastructuresuchasenergy,waterandcommunicationswillpassthroughtoconsumers’bills.Interestrateriseswillalsocomesoonerorlaterandbeashockafteralongperiodof staticandlowrates.

Realwagesfellin2013andhavebeenfallingconsistentlysince2010,thelongestperiodof declinefor50years1.Theproportionof averagehouseholddisposableincomeaccountedforbyexpenditureonessentialhouseholdgoodsandserviceshasrisenfrom20percentin2003to27percentin20132.Coupledwithpersistentworriesoverjobsecurity,thismeanspeople’sfinancialhorizonsappeartobereducing.Thelackof people’sfinancialresiliencemeansthatitisverydifficulttocopewithincomecostshocksoverthelongterm,evenovertheshortterm.

Inthisenvironmentthegrowthof thepaydayloanmarketandarrearsisalmostinevitable,anddemandsastronggovernmentresponse.Therapidriseinarrearsonessentialhouseholdbillsinparticularisonethatisunder-reported,andraisesseriousquestionsregardingthepublicsector’sroleasadebtcollectorandthebusinesspracticesof serviceproviders,suchasutilitycompanies.

2014willproveachallengingoneforallorganisationsconcernedwithhelpingfinanciallystressedconsumers,withpeoplefacinghardpersonaleconomiccircumstancesandwelfarechangescontinuingtobite.StepChangeDebtCharitywillcarryonourkeytaskwithvigourandpassion,offeringfree,independentadviceandsupporttoallwhoneedit,nomatterwhattheircircumstances.WewillcontinuetodrivethechangeneededtofurtherhelptheUK’sindebtedpopulation.Wewillcontinuetoadvisepolicymakers,usingevidencefromourclientsandourresearch.Wehaveanexcitingresearchprogrammeplannedfor2014examiningwhatlifeislikeforfamilies“ontheedge”–whoarefalling,orhavefallen,intofinancialdifficulty–andlookingatwhetherthereisanadequatesafetynetinplacetoprotectthem.

Mike O’Connor CBEChief Executive

1. Chief Executive’s Introduction

STATISTICS YEARBOOK 2013 3

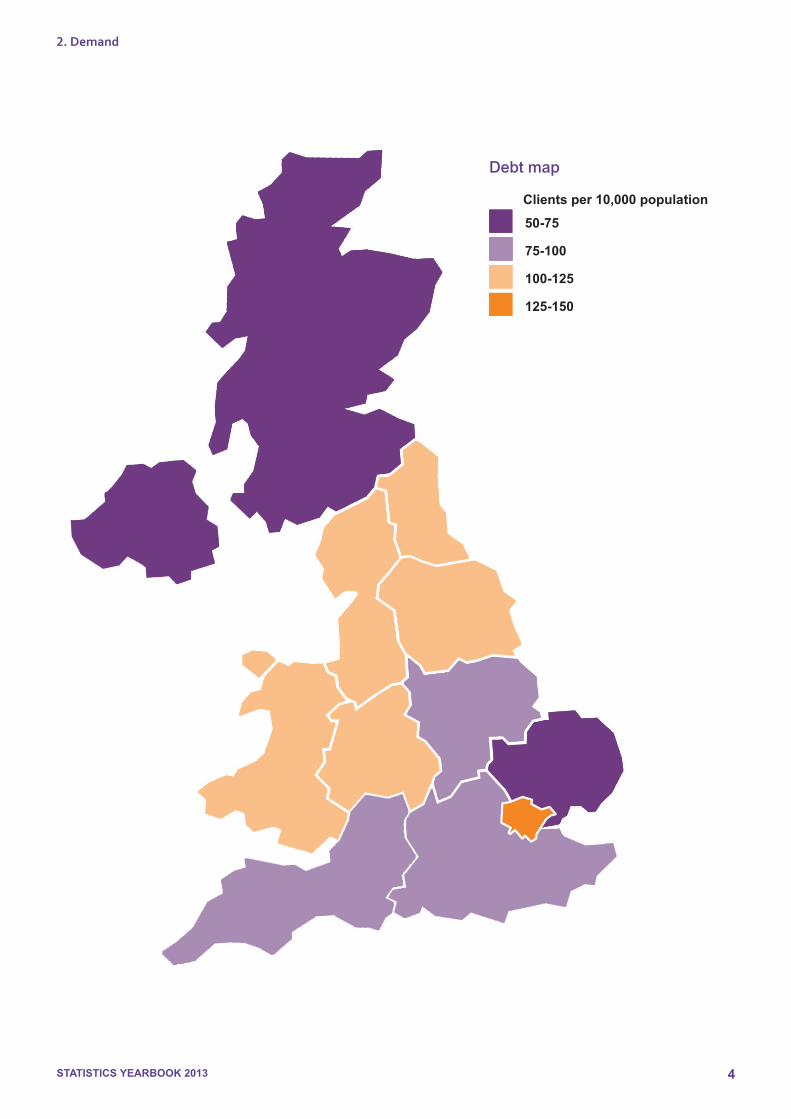

Arecordnumberof people,507,863,contactedStepChangeDebtCharityin2013.Thiswasdrivenbya29percentincreaseinthenumberof peoplecontactingthecharitybytelephoneanda50percentincreaseinthenumberof peoplecontactingthecharityonline.If webreakdemanddownbyregionwecanseethehighestdemandcamefromLondon(seeoverleaf).

3 The 2012 telephone contact figures have undergone a slight revision and have decreased, due to methodological changes. We have removed from the overall numbers any callers who contacted the helpline

and were subsequently redirected to a different part of the charity.

2. Demand

Chart 1: Demand for advice3

600,000

500,000

400,000

300,000

200,000

100,000

02008 2009 2010 2011 2012 2013

Contact numbers

Telephone Online Overall

Key findings:• 507,863peoplecontactedStepChangeDebtCharityin2013

• Thetopthreereasonsforseekingadvicewereunemployment/redundancy(23percent),reducedincome(16percent)andalackof budgeting(14percent)

• Almost70percentof clientsadvisedlivedinrentedaccommodationcomparedto50percentin2009.

Asthenumberof onlineservicesofferedbytheCharityincreases,sodothewaysinwhichweinteractwithclients.

Manypeopleneedin-depthadviceandsupport,andthisistraditionallywhatwehavereportedon.WedosointhisYearbookandwillcontinuetodosoinfuture.

However,somepeopleuseourservicesinadifferentway,togainabetterunderstandingof theirsituationbeforedecidingtotakeaction.Forexample,20,484peopleusedour60seconddebttrackerbetweenJune2013(whenitwaslaunched)andDecember2013.

Weareconsciousthatthereareavarietyof otherlevelsof engagementpeoplehavewithouronlineservices.Wecontinuetoexplorewhatthesemeanintermsof thehelppeoplereceive,andwhatarethemostusefulmeasurementsforustopublish.

STATISTICS YEARBOOK 2013 4

2. Demand

50-75

75-100

100-125

125-150

Debt map

Clients per 10,000 population

STATISTICS YEARBOOK 2013 5

Asinpreviousyears,demandforadvicewasprimarilyaresultof unemployment(23percent)andreducedincomeresultingfromlossof hoursatwork(16percent).

Figure 1: Reasons for debt

STATISTICS YEARBOOK 2013 6

2. Demand

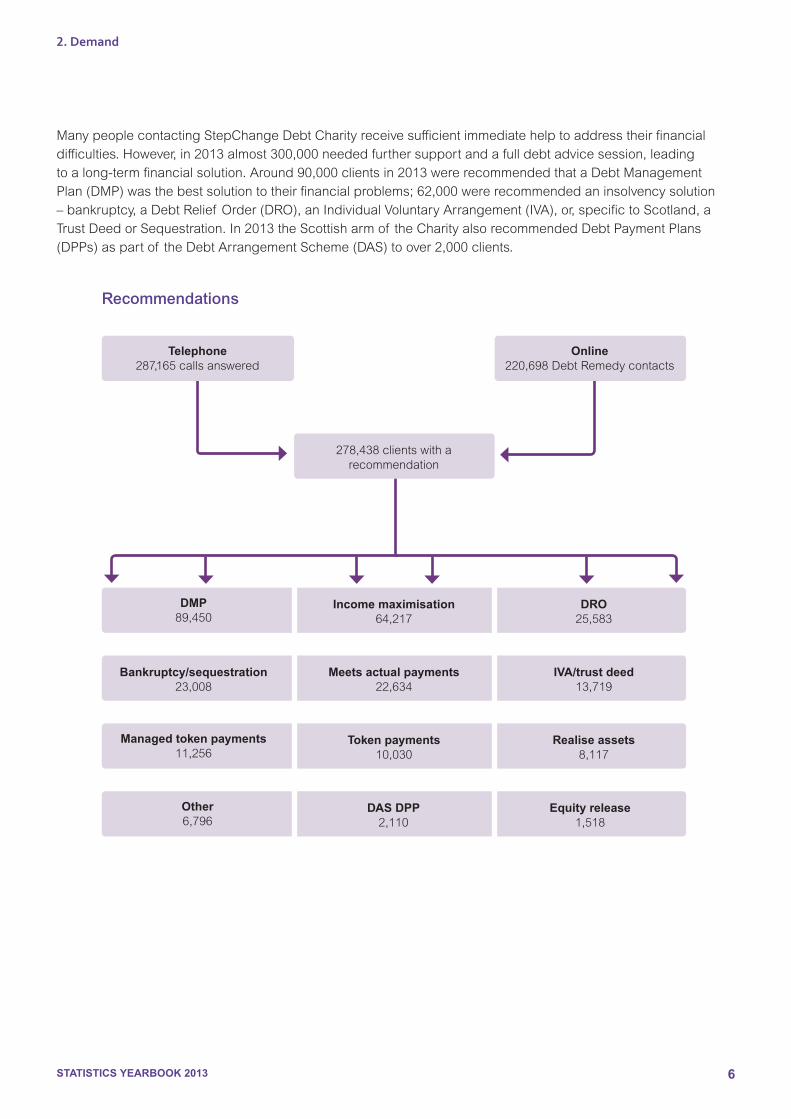

DMP89,450

Income maximisation64,217

DRO25,583

Bankruptcy/sequestration23,008

Meets actual payments22,634

IVA/trust deed13,719

Managed token payments11,256

Token payments10,030

Realise assets8,117

278,438clientswitharecommendation

Other6,796

DAS DPP2,110

Equity release1,518

Telephone287,165callsanswered

Online220,698DebtRemedycontacts

Recommendations

ManypeoplecontactingStepChangeDebtCharityreceivesufficientimmediatehelptoaddresstheirfinancialdifficulties.However,in2013almost300,000neededfurthersupportandafulldebtadvicesession,leadingtoalong-termfinancialsolution.Around90,000clientsin2013wererecommendedthataDebtManagementPlan(DMP)wasthebestsolutiontotheirfinancialproblems;62,000wererecommendedaninsolvencysolution–bankruptcy,aDebtRelief Order(DRO),anIndividualVoluntaryArrangement(IVA),or,specifictoScotland,aTrustDeedorSequestration.In2013theScottisharmof theCharityalsorecommendedDebtPaymentPlans(DPPs)aspartof theDebtArrangementScheme(DAS)toover2,000clients.

STATISTICS YEARBOOK 2013 7

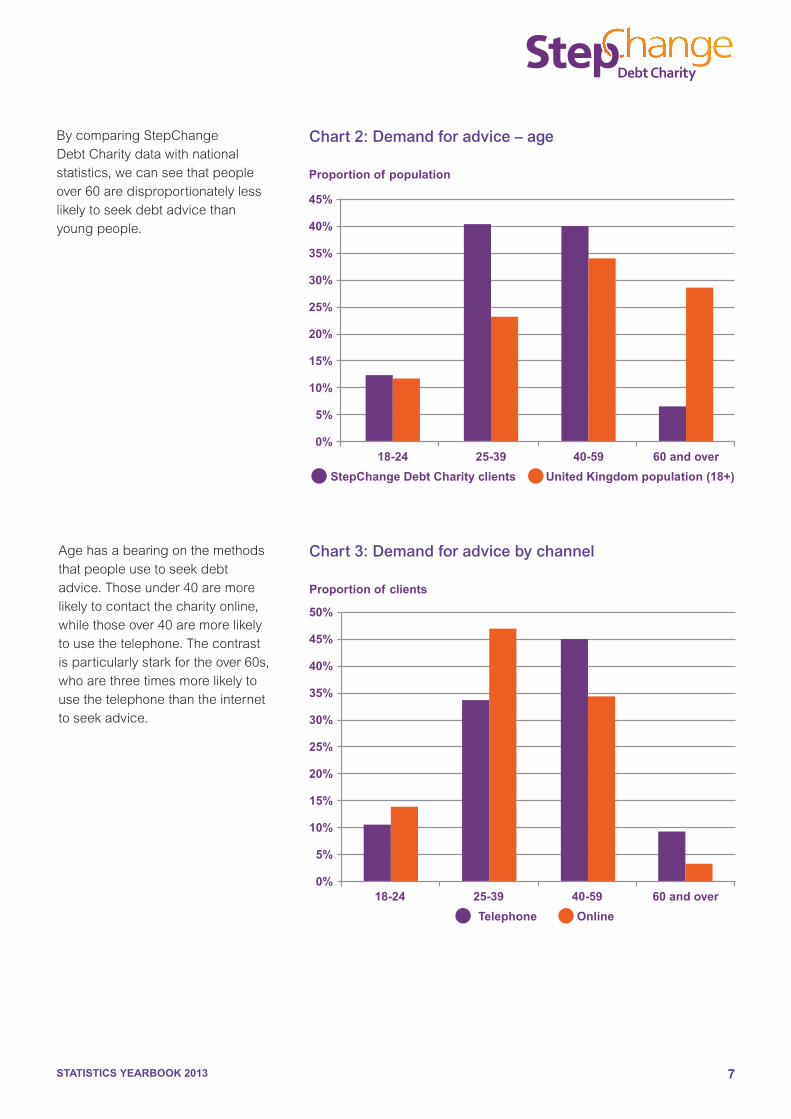

BycomparingStepChangeDebtCharitydatawithnationalstatistics,wecanseethatpeopleover60aredisproportionatelylesslikelytoseekdebtadvicethanyoungpeople.

45%

40%

35%

30%

25%

20%

15%

10%

5%

0%

Proportion of population

18-24 25-39 40-59 60 and over

StepChange Debt Charity clients United Kingdom population (18+)

Chart 2: Demand for advice – age

50%

45%

40%

35%

30%

25%

20%

15%

10%

5%

0%

Proportion of clients

18-24 25-39 40-59 60 and over

Telephone Online

Chart 3: Demand for advice by channelAgehasabearingonthemethodsthatpeopleusetoseekdebtadvice.Thoseunder40aremorelikelytocontactthecharityonline,whilethoseover40aremorelikelytousethetelephone.Thecontrastisparticularlystarkfortheover60s,whoarethreetimesmorelikelytousethetelephonethantheinternettoseekadvice.

STATISTICS YEARBOOK 2013 8

4 ONS Families and Households 2012: lone parent families with dependent children

2. Demand

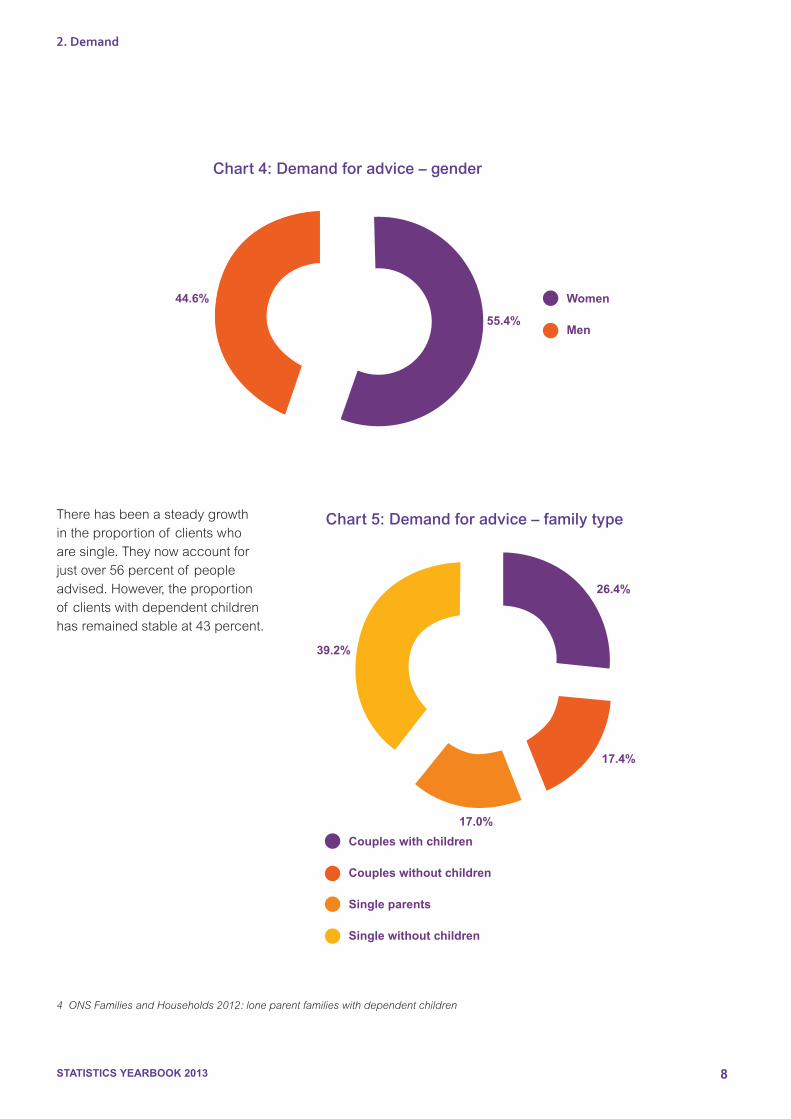

Chart 4: Demand for advice – gender

Women

Men55.4%

44.6%

Therehasbeenasteadygrowthintheproportionof clientswhoaresingle.Theynowaccountforjustover56percentof peopleadvised.However,theproportionof clientswithdependentchildrenhasremainedstableat43percent.

Couples with children

Couples without children

Single parents

Single without children

26.4%

17.4%

39.2%

17.0%

Chart 5: Demand for advice – family type

STATISTICS YEARBOOK 2013 9

80%

70%

60%

50%

40%

30%

20%

10%

0%

Proportion of clients

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Homeowners Renters

Board payment

Mortgage

Own outright

Rent & mortgage

Rent - housing association

Rent - local authority

Rent - private landlord

12.2%

28.8%

2.1%

31.5%

11.5%

11.5%

2.4%

Chart 6: Demand for advice – housing tenure

Chart 7: Demand for advice – housing tenure

Morerentersareseekinghelpfromthecharity.Lastyearalmost70percentof clientsadvisedlivedinrentedaccommodation,comparedtojustover50percentin2009.

Thepreviousthreeyearshaveseenariseintheproportionof clientslivinginprivaterentedaccommodation,from27percentin2011to32percentin2013.

STATISTICS YEARBOOK 2013 10

2. Demand

Claireisalowpaidpart-timeworker.Shehashadherwagesfrozenforfouryearsandhadtoreduceherworkinghoursasshesuffersfromtendonitisandarthritisinherhands.Herhusband,anMOTtester,hasbeenforcedtobecomeself-employedafterhisgaragemadehimredundant.Afterstrugglingforanumberof yearstheirfinancesgotsteadilyworseandtheywerehavingtoincreasinglyrelyonanoverdraftandcreditcardfordaytodayliving.Claireaskedforhelpfromherbankandwasofferedfurthercredit.

ShethenreceivedaletterinJanuary2013fromthecreditcarddepartmentsayingthattheywouldhavetoincreaseherinterestrateuntilherspendingorcreditimproved.ShewasreferredtoStepChangeDebtCharityandwearrangedaDMP.

“[It]isthebestthingwecouldhavedoneandwishIhaddoneitsooner.”

Case study Claire

AfterAdamwasforcedtotakeearlyretirementduetogrowinghealthproblems,hefoundhimself dependentonbenefits.Hehadtakenoutacarloanwhilsthewasstillworking,andhenowstrugglestoliveonhisbenefitsandrepaytheloan.

“Onedayyou’reearningapaycheckandthenextdayyou’renotandyou’reindeeptrouble.”

Thebenefitmoneyisn’tenoughtopayoffhisdebts,orevenliveon,andhehasbeenkeptwaitingayearforallof hisbenefitstobeprocessed.

Adamcontactedthebankfourorfivemonthsafterbeingmedicallyretired.

“Isaid‘lookI’mnotgoingtohaveenoughmoneytopaythesethingsoff,’becauseitsaysontheirbankwebsite,nicely,phoneusandwe’lldoeverythingwecantohelpyouandthefirstthingtheysaidwas‘sorrywecan’thelpyou’so…itwasaveryunpleasantexperienceandquitesouldestroyingactually.”

Hestrugglestoliveonthemoneyhedoeshavecominginandhasnorealwayof earninganymore.

“I’vegotnomoney.Ithinkthethingthat’sgoingtohappenisprobablybankruptcy.”

Case study Adam

STATISTICS YEARBOOK 2013 11

5 Not including housing benefit

Number of clients

180,000

160,000

140,000

120,000

100,000

80,000

60,000

40,000

20,000

0

Child b

enefi

tChild

tax c

redit

Disabilit

y livi

ng allo

wance

Inca

pacity

ben

efit/E

SAIn

com

e support

Jobse

eker

’s all

owance

Work

ing ta

x cre

dit

All clie

nts cl

aimin

g

benefi

ts

2011 2012 2013

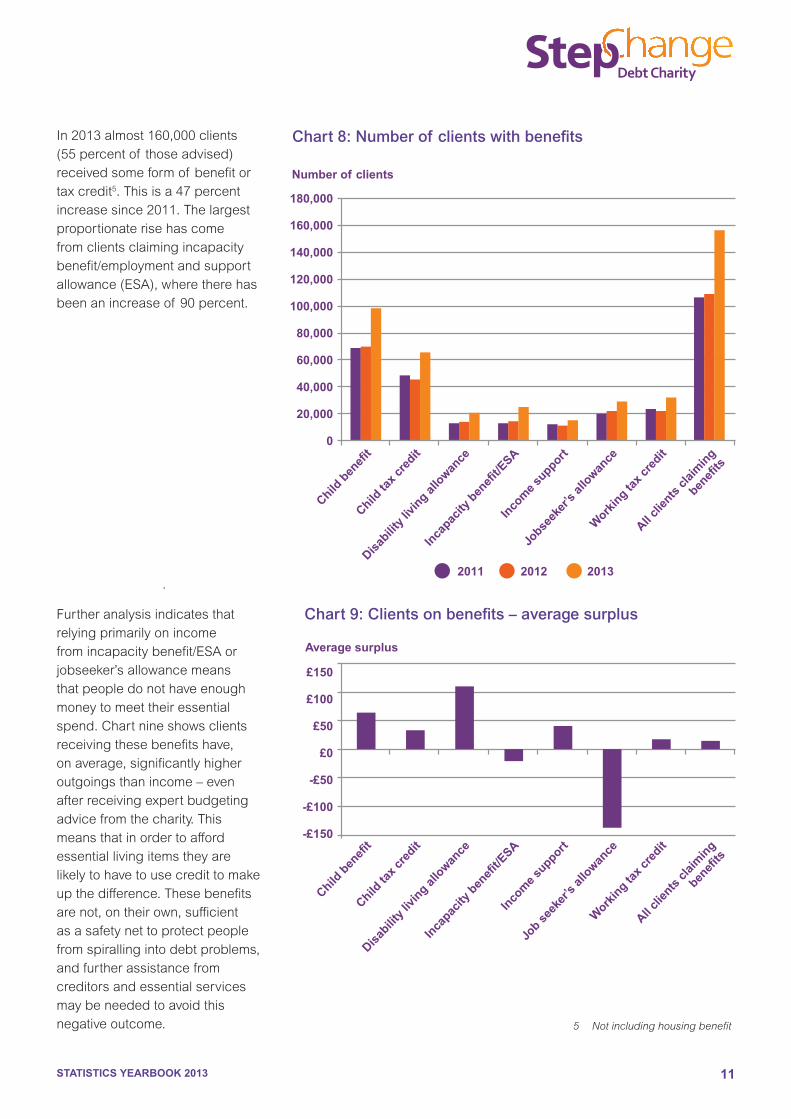

Chart 8: Number of clients with benefitsIn2013almost160,000clients(55percentof thoseadvised)receivedsomeformof benefitortaxcredit5.Thisisa47percentincreasesince2011.Thelargestproportionaterisehascomefromclientsclaimingincapacitybenefit/employmentandsupportallowance(ESA),wheretherehasbeenanincreaseof 90percent.

Chart 9: Clients on benefits – average surplus

Average surplus

£150

£100

£50

£0

-£50

-£100

-£150

Child b

enefi

tChild

tax c

redit

Disabilit

y livi

ng allo

wance

Inca

pacity

ben

efit/E

SAIn

com

e support

Job se

eker

’s all

owance

Work

ing ta

x cre

dit

All clie

nts cl

aimin

g

benefi

ts

Furtheranalysisindicatesthatrelyingprimarilyonincomefromincapacitybenefit/ESAorjobseeker’sallowancemeansthatpeopledonothaveenoughmoneytomeettheiressentialspend.Chartnineshowsclientsreceivingthesebenefitshave,onaverage,significantlyhigheroutgoingsthanincome–evenafterreceivingexpertbudgetingadvicefromthecharity.Thismeansthatinordertoaffordessentiallivingitemstheyarelikelytohavetousecredittomakeupthedifference.Thesebenefitsarenot,ontheirown,sufficientasasafetynettoprotectpeoplefromspirallingintodebtproblems,andfurtherassistancefromcreditorsandessentialservicesmaybeneededtoavoidthisnegativeoutcome.

STATISTICS YEARBOOK 2013 12

2. Demand

6 ONS labour market statistics Sep-Nov 2013

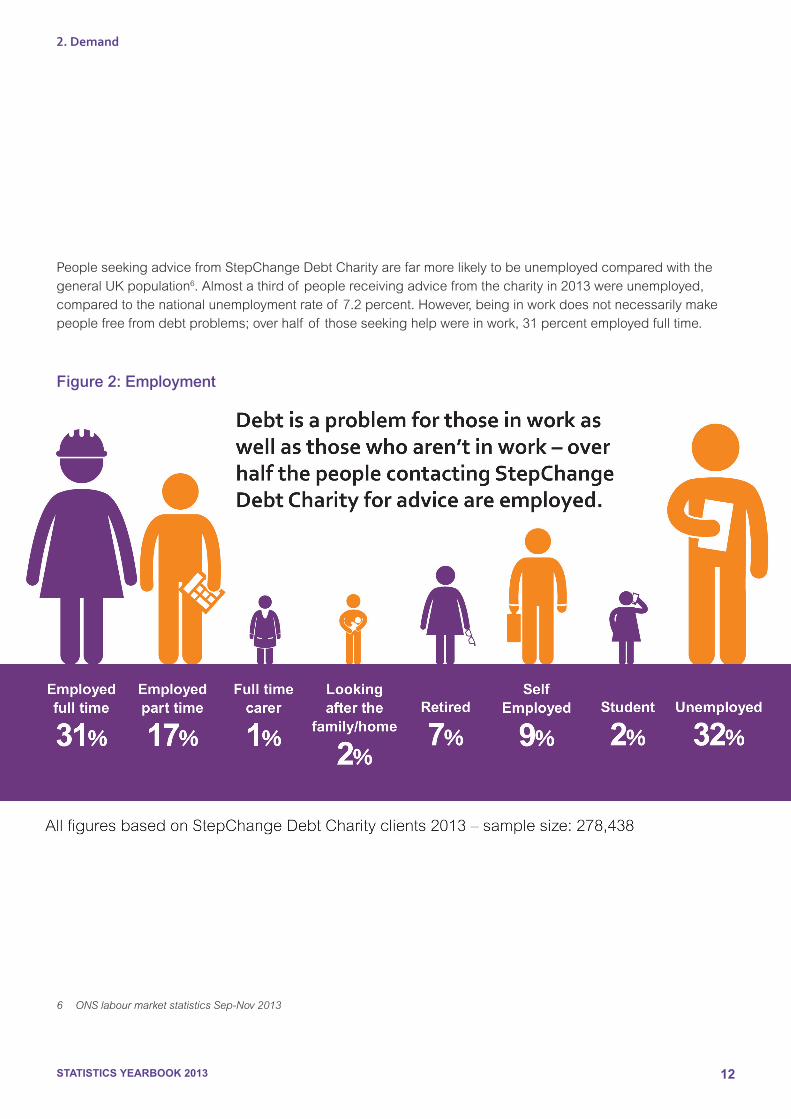

PeopleseekingadvicefromStepChangeDebtCharityarefarmorelikelytobeunemployedcomparedwiththegeneralUKpopulation6.Almostathirdof peoplereceivingadvicefromthecharityin2013wereunemployed,comparedtothenationalunemploymentrateof 7.2percent.However,beinginworkdoesnotnecessarilymakepeoplefreefromdebtproblems;overhalf of thoseseekinghelpwereinwork,31percentemployedfulltime.

Figure 2: Employment

STATISTICS YEARBOOK 2013 13

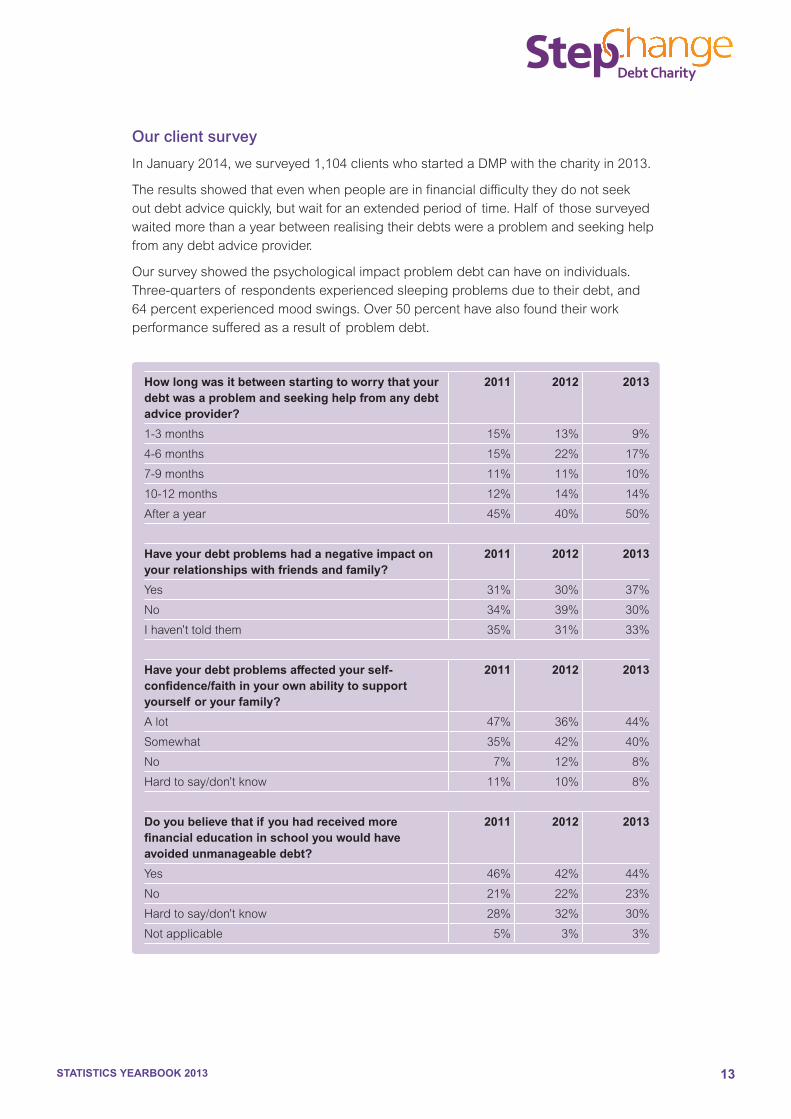

How long was it between starting to worry that your debt was a problem and seeking help from any debt advice provider?

2011 2012 2013

1-3months 15% 13% 9%

4-6months 15% 22% 17%

7-9months 11% 11% 10%

10-12months 12% 14% 14%

Afterayear 45% 40% 50%

Have your debt problems had a negative impact on your relationships with friends and family?

2011 2012 2013

Yes 31% 30% 37%

No 34% 39% 30%

Ihaven’ttoldthem 35% 31% 33%

Have your debt problems affected your self-confidence/faith in your own ability to support yourself or your family?

2011 2012 2013

Alot 47% 36% 44%

Somewhat 35% 42% 40%

No 7% 12% 8%

Hardtosay/don’tknow 11% 10% 8%

Do you believe that if you had received more financial education in school you would have avoided unmanageable debt?

2011 2012 2013

Yes 46% 42% 44%

No 21% 22% 23%

Hardtosay/don’tknow 28% 32% 30%

Notapplicable 5% 3% 3%

Our client survey

InJanuary2014,wesurveyed1,104clientswhostartedaDMPwiththecharityin2013.

Theresultsshowedthatevenwhenpeopleareinfinancialdifficultytheydonotseekoutdebtadvicequickly,butwaitforanextendedperiodof time.Half of thosesurveyedwaitedmorethanayearbetweenrealisingtheirdebtswereaproblemandseekinghelpfromanydebtadviceprovider.

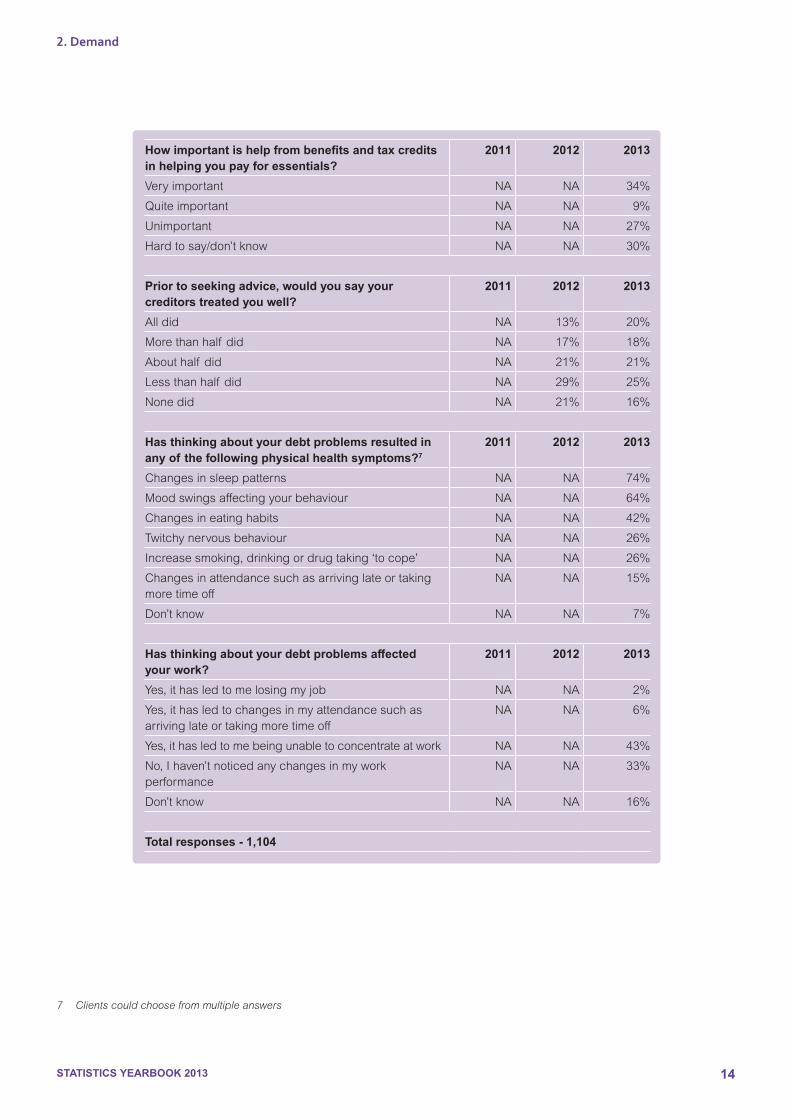

Oursurveyshowedthepsychologicalimpactproblemdebtcanhaveonindividuals.Three-quartersof respondentsexperiencedsleepingproblemsduetotheirdebt,and64percentexperiencedmoodswings.Over50percenthavealsofoundtheirworkperformancesufferedasaresultof problemdebt.

STATISTICS YEARBOOK 2013 14

7 Clients could choose from multiple answers

2. Demand

How important is help from benefits and tax credits in helping you pay for essentials?

2011 2012 2013

Veryimportant NA NA 34%

Quiteimportant NA NA 9%

Unimportant NA NA 27%

Hardtosay/don’tknow NA NA 30%

Prior to seeking advice, would you say your creditors treated you well?

2011 2012 2013

Alldid NA 13% 20%

Morethanhalf did NA 17% 18%

Abouthalf did NA 21% 21%

Lessthanhalf did NA 29% 25%

Nonedid NA 21% 16%

Has thinking about your debt problems resulted in any of the following physical health symptoms?7

2011 2012 2013

Changesinsleeppatterns NA NA 74%

Moodswingsaffectingyourbehaviour NA NA 64%

Changesineatinghabits NA NA 42%

Twitchynervousbehaviour NA NA 26%

Increasesmoking,drinkingordrugtaking‘tocope’ NA NA 26%

Changesinattendancesuchasarrivinglateortakingmoretimeoff

NA NA 15%

Don’tknow NA NA 7%

Has thinking about your debt problems affected your work?

2011 2012 2013

Yes,ithasledtomelosingmyjob NA NA 2%

Yes,ithasledtochangesinmyattendancesuchasarrivinglateortakingmoretimeoff

NA NA 6%

Yes,ithasledtomebeingunabletoconcentrateatwork NA NA 43%

No,Ihaven’tnoticedanychangesinmyworkperformance

NA NA 33%

Don’tknow NA NA 16%

Total responses - 1,104

STATISTICS YEARBOOK 2013 15

3. Debts

Average unsecured debt

£30,000

£25,000

£20,000

£15,000

£10,000

£5,000

£02009 2010 2011 2012 2013

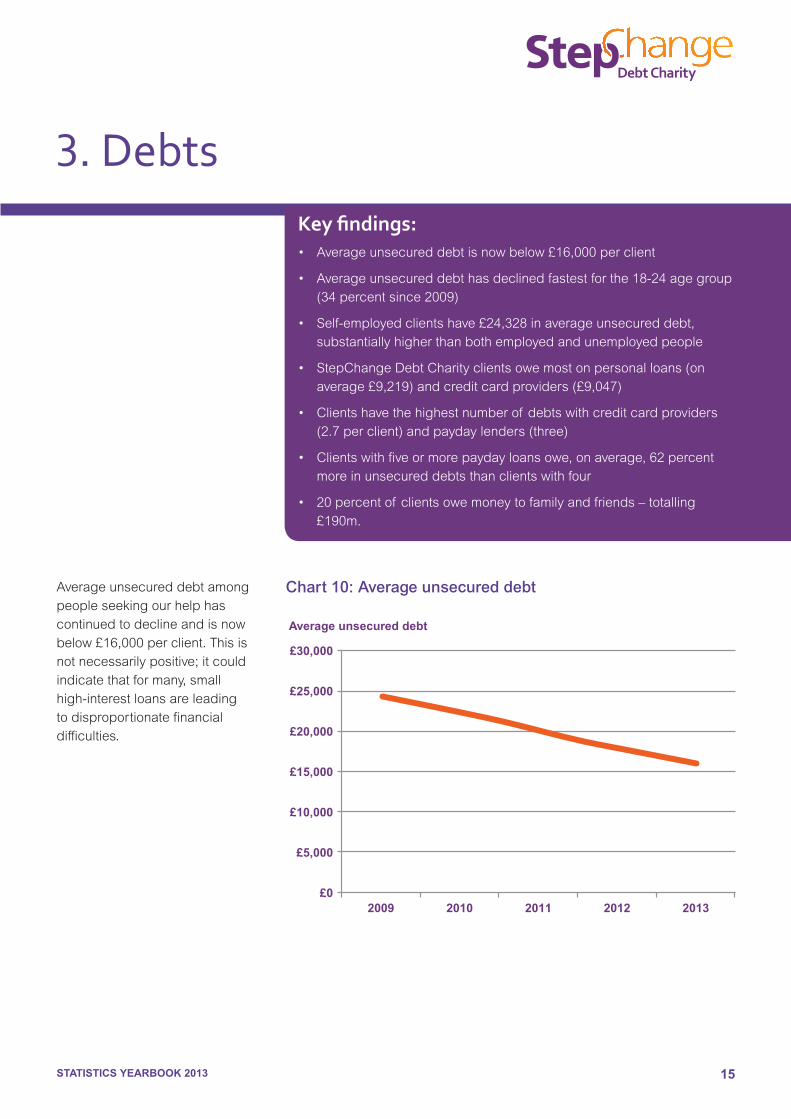

Key findings:• Averageunsecureddebtisnowbelow£16,000perclient

• Averageunsecureddebthasdeclinedfastestforthe18-24agegroup(34percentsince2009)

• Self-employedclientshave£24,328inaverageunsecureddebt,substantiallyhigherthanbothemployedandunemployedpeople

• StepChangeDebtCharityclientsowemostonpersonalloans(onaverage£9,219)andcreditcardproviders(£9,047)

• Clientshavethehighestnumberof debtswithcreditcardproviders(2.7perclient)andpaydaylenders(three)

• Clientswithfiveormorepaydayloansowe,onaverage,62percentmoreinunsecureddebtsthanclientswithfour

• 20percentof clientsowemoneytofamilyandfriends–totalling £190m.

Chart 10: Average unsecured debtAverageunsecureddebtamongpeopleseekingourhelphascontinuedtodeclineandisnowbelow£16,000perclient.Thisisnotnecessarilypositive;itcouldindicatethatformany,smallhigh-interestloansareleadingtodisproportionatefinancialdifficulties.

STATISTICS YEARBOOK 2013 16

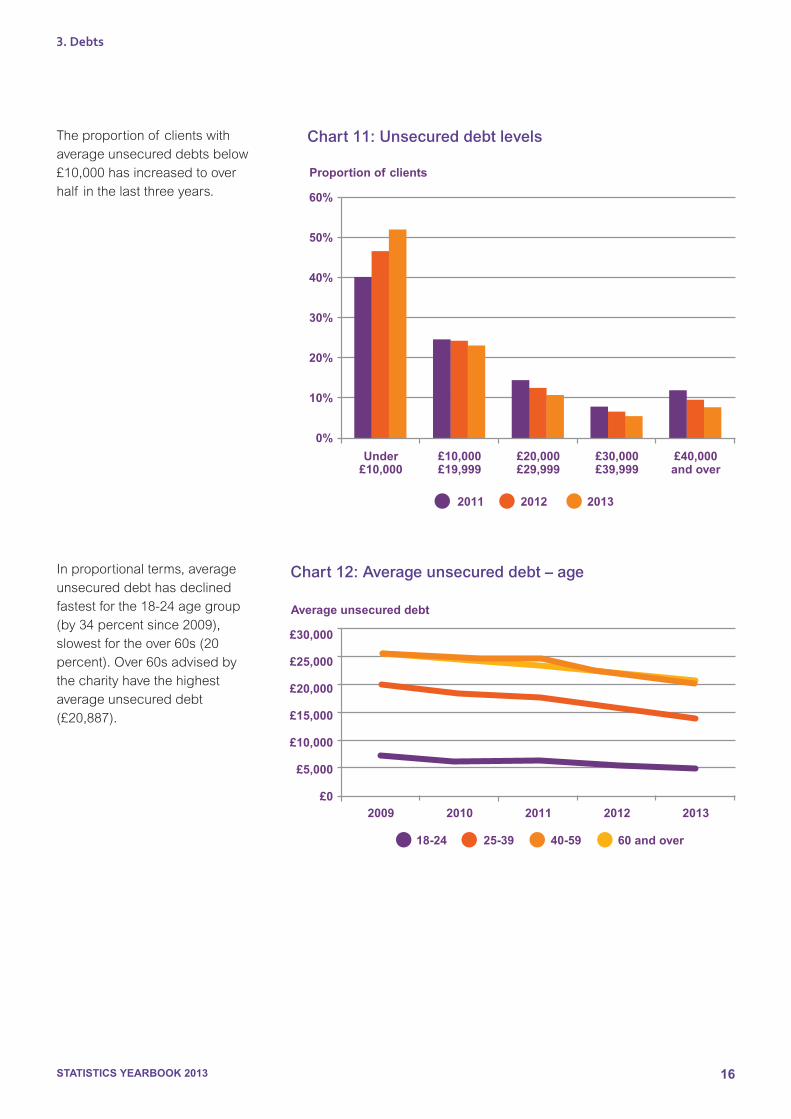

Theproportionof clientswithaverageunsecureddebtsbelow£10,000hasincreasedtooverhalf inthelastthreeyears.

3. Debts

Proportion of clients

60%

50%

40%

30%

20%

10%

0%

2011 2012 2013

Under£10,000

£10,000£19,999

£20,000£29,999

£30,000£39,999

£40,000and over

Chart 11: Unsecured debt levels

Chart 12: Average unsecured debt – ageInproportionalterms,averageunsecureddebthasdeclinedfastestforthe18-24agegroup(by34percentsince2009),slowestfortheover60s(20percent).Over60sadvisedbythecharityhavethehighestaverageunsecureddebt(£20,887).

Average unsecured debt

£30,000

£25,000

£20,000

£15,000

£10,000

£5,000

£0

18-24 25-39 40-59 60 and over

2009 2010 2011 2012 2013

STATISTICS YEARBOOK 2013 17

Cindy,aparttimeworker,andherhusband,alabourer,gotintodebtatthebeginningof 2013asaresultof herhusbandinjuringhisbackandlosinghisjob.Cindy’sincomewasunabletosupportthembothandtheyfellquicklyintodebt.

Cindy’shusbandisnowalotbetterandlookingforworkbutislimitedashecannotgobackintoheavylabouringindustrialjobsbecauseof hisback.TheyhavethreechildrenandCindyhasbeenfeelingintensepressureonherself asthebreadwinner.

“Itisaconstantbattleof worryandpayinglessonagreedpayments.Wehavelostallourcreditratingandthingshavebeenverytough.”

Shehasbeentakinganyextrahoursshecanandhas‘run[herself]intotheground’resultinginheradmissiontohospital.

“Largelyourproblemswouldbehalvedif thebenefitsweremoreinlinewithbasiclivingcosts.”

Case study Cindy

£20,000

£18,000

£16,000

£14,000

£12,000

£10,000

£8,000

£6,000

£4,000

£2,000

£0

Average unsecured debt

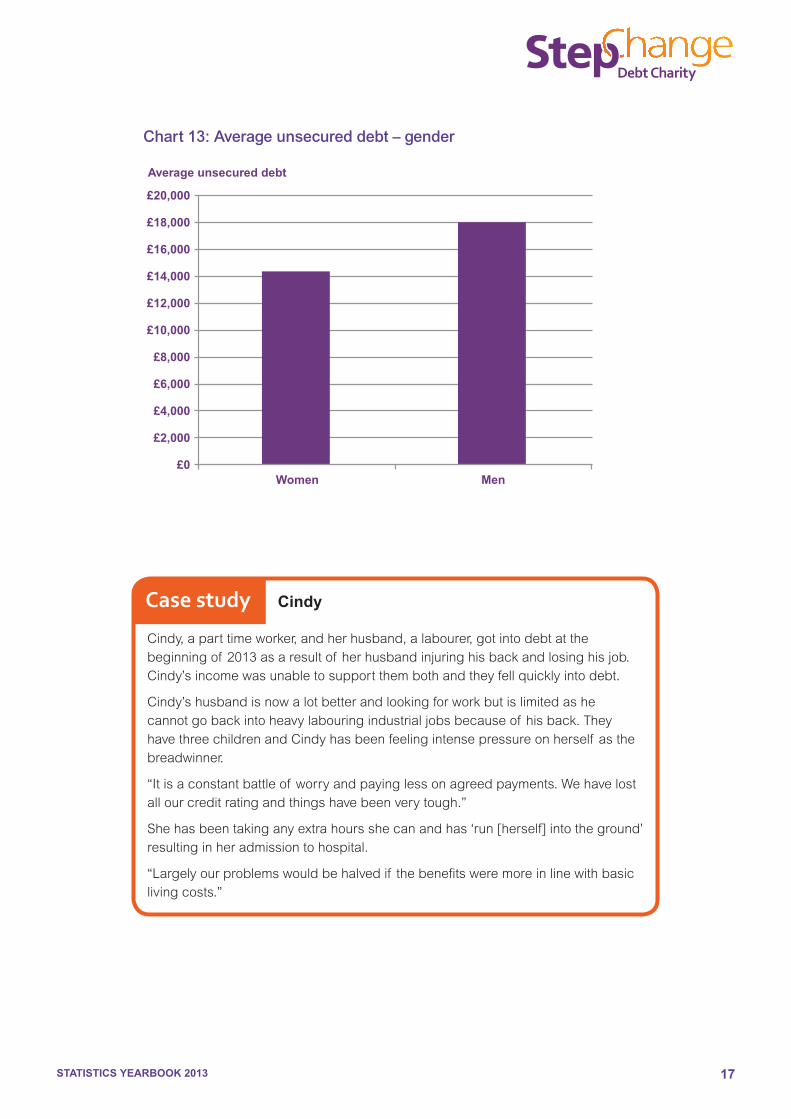

Women Men

Chart 13: Average unsecured debt – gender

STATISTICS YEARBOOK 2013 18

3. Debts

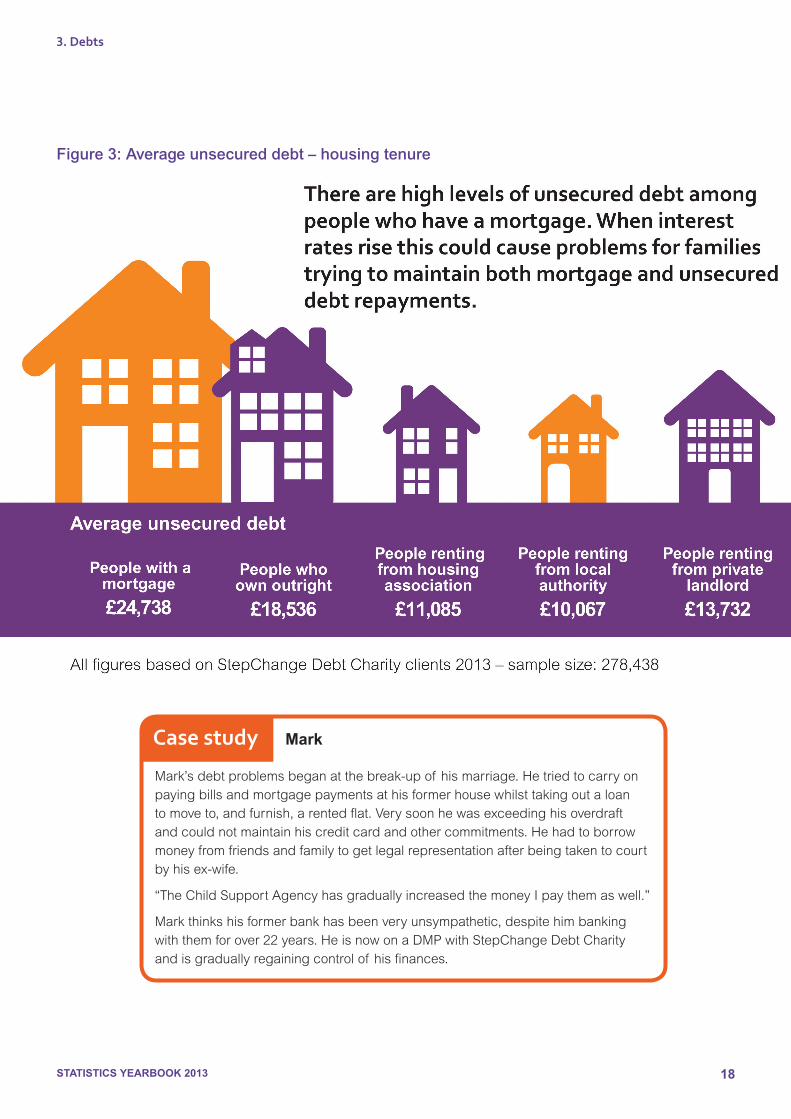

Figure 3: Average unsecured debt – housing tenure

Mark’sdebtproblemsbeganatthebreak-upof hismarriage.Hetriedtocarryonpayingbillsandmortgagepaymentsathisformerhousewhilsttakingoutaloantomoveto,andfurnish,arentedflat.Verysoonhewasexceedinghisoverdraftandcouldnotmaintainhiscreditcardandothercommitments.Hehadtoborrowmoneyfromfriendsandfamilytogetlegalrepresentationafterbeingtakentocourtbyhisex-wife.

“TheChildSupportAgencyhasgraduallyincreasedthemoneyIpaythemaswell.”

Markthinkshisformerbankhasbeenveryunsympathetic,despitehimbankingwiththemforover22years.HeisnowonaDMPwithStepChangeDebtCharityandisgraduallyregainingcontrolof hisfinances.

Case study Mark

STATISTICS YEARBOOK 2013 19

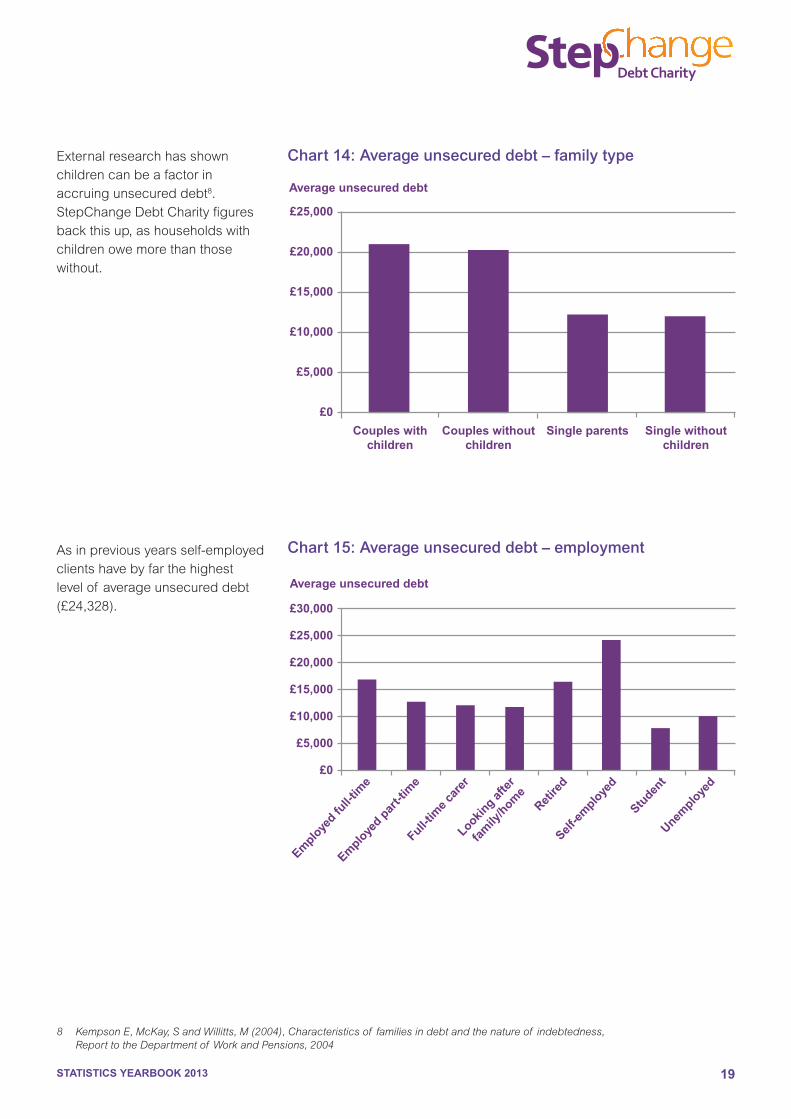

Chart 14: Average unsecured debt – family typeExternalresearchhasshownchildrencanbeafactorinaccruingunsecureddebt8.StepChangeDebtCharityfiguresbackthisup,ashouseholdswithchildrenowemorethanthosewithout.

Average unsecured debt

£25,000

£20,000

£15,000

£10,000

£5,000

£0

Couples with children

Couples without children

Single parents Single without children

Asinpreviousyearsself-employedclientshavebyfarthehighestlevelof averageunsecureddebt(£24,328).

Chart 15: Average unsecured debt – employment

Average unsecured debt

£30,000

£25,000

£20,000

£15,000

£10,000

£5,000

£0

Emplo

yed fu

ll-tim

e

Emplo

yed p

art-t

ime

Full-tim

e car

erLookin

g afte

r

fam

ily/h

ome

Retire

dSelf

-em

ploye

d

Studen

tUnem

ploye

d

8 Kempson E, McKay, S and Willitts, M (2004), Characteristics of families in debt and the nature of indebtedness, Report to the Department of Work and Pensions, 2004

STATISTICS YEARBOOK 2013 20

3. Debts

£10,000

£9,000

£8,000

£7,000

£6,000

£5,000

£4,000

£3,000

£2,000

£1,000

£0

Average unsecured debt

Catalo

gueCre

dit ca

rd

Overd

raft

Perso

nal lo

an

Store

card

Home c

redit

Payday

loan

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0.0

Catalo

gueCre

dit ca

rd

Overd

raft

Perso

nal lo

an

Store

card

Home c

redit

Payday

loan

Chart 16: Types of unsecured debtStepChangeDebtCharityclientsonaverageowemostonpersonalloans(£9,219)andcreditcards(£9,047).

Chart 17: Number of unsecured debtsHowever,ourclientshavethehighestnumberof debtswithcreditcardproviders(2.7)andwithpaydaylenders(three)indicatingproblemsarisingfrommultipledebts.

Number of debts

STATISTICS YEARBOOK 2013 21

WhenMarytookoutaloan,herunclesignedasherguarantor.Afterlosingherjob,shestruggledtokeepupherrepayments.Thecreditorbegantocallherrepeatedly-upto18timesperdayonsomeoccasions-tochasethearrearsonheraccount.Mary’sunclestartedtomakeupthepaymentsuntilhelosthisjob.BothMaryandheruncletriedtocanceltheContinuousPaymentAuthorityontheirdebitcardswiththelenderandtheirbanks;howeverthelenderstillcontinuedtotakepayments,leavingtheminapositionwheretheystruggledtobuyfoodandpayessentialhouseholdbills.Mary’sunclefoundwork,butwasstillunabletomakethefullmonthlypaymentfortheloan.Thelenderkeptcallinghimatwork,despiterepeatedrequestsnotto,whichalmostledtohimreceivingdisciplinaryactionaboutreceivingpersonalcalls.

MaryiscurrentlyonaDMParrangedbyStepChangeDebtCharity,butisconsideringbankruptcy.

Case study Mary

Figure 4: Proportion of unsecured debts

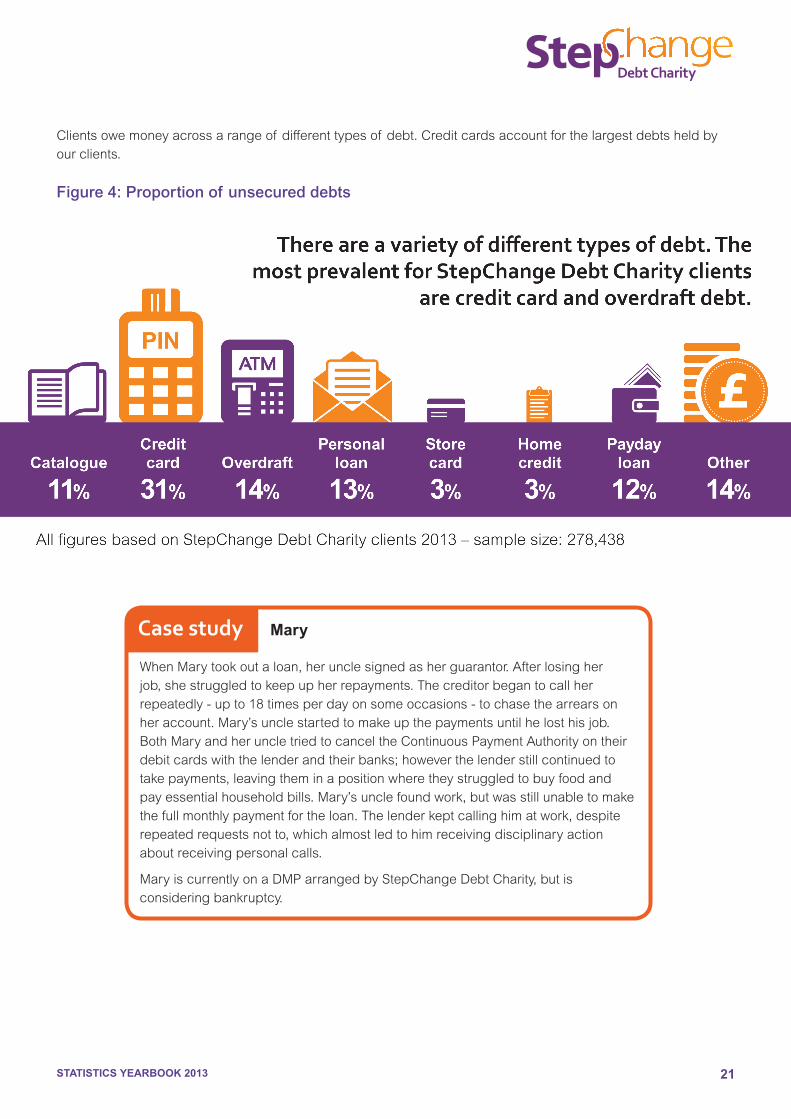

Clientsowemoneyacrossarangeof differenttypesof debt.Creditcardsaccountforthelargestdebtsheldbyourclients.

STATISTICS YEARBOOK 2013 22

3. Debts

35%

30%

25%

20%

15%

10%

5%

0%

£30,000

£25,000

£20,000

£15,000

£10,000

£5,000

£01 2 3 4 5+

Number of credit cards Average credit card debt

Proportion of clients with each number of credit cards

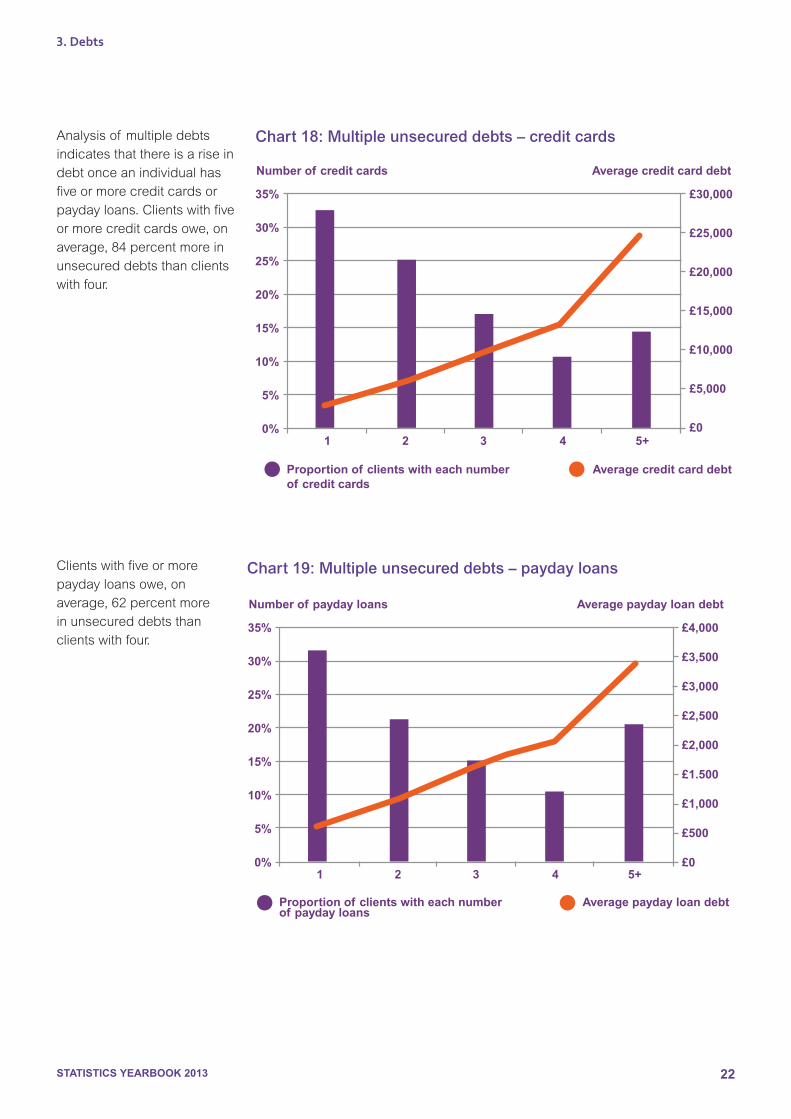

Average credit card debt

Analysisof multipledebtsindicatesthatthereisariseindebtonceanindividualhasfiveormorecreditcardsorpaydayloans.Clientswithfiveormorecreditcardsowe,onaverage,84percentmoreinunsecureddebtsthanclientswithfour.

35%

30%

25%

20%

15%

10%

5%

0%

£4,000

£3,500

£3,000

£2,500

£2,000

£1.500

£1,000

£500

£01 2 3 4 5+

Number of payday loans Average payday loan debt

Proportion of clients with each number of payday loans

Chart 18: Multiple unsecured debts – credit cards

Chart 19: Multiple unsecured debts – payday loansClientswithfiveormorepaydayloansowe,onaverage,62percentmoreinunsecureddebtsthanclientswithfour.

Average payday loan debt

STATISTICS YEARBOOK 2013 23

Average credit card debt

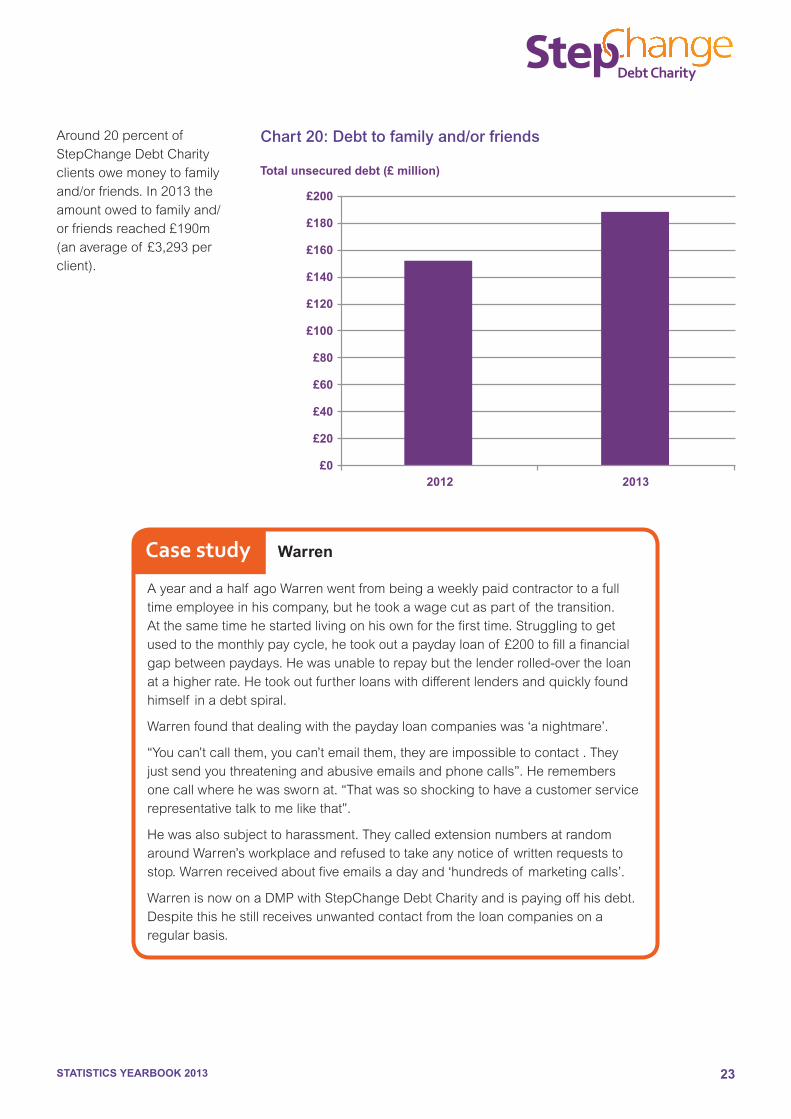

Around20percentof StepChangeDebtCharityclientsowemoneytofamilyand/orfriends.In2013theamountowedtofamilyand/orfriendsreached£190m(anaverageof £3,293perclient).

£200

£180

£160

£140

£120

£100

£80

£60

£40

£20

£02012 2013

Chart 20: Debt to family and/or friends

Ayearandahalf agoWarrenwentfrombeingaweeklypaidcontractortoafulltimeemployeeinhiscompany,buthetookawagecutaspartof thetransition.Atthesametimehestartedlivingonhisownforthefirsttime.Strugglingtogetusedtothemonthlypaycycle,hetookoutapaydayloanof £200tofillafinancialgapbetweenpaydays.Hewasunabletorepaybutthelenderrolled-overtheloanatahigherrate.Hetookoutfurtherloanswithdifferentlendersandquicklyfoundhimself inadebtspiral.

Warrenfoundthatdealingwiththepaydayloancompanieswas‘anightmare’.

“Youcan’tcallthem,youcan’temailthem,theyareimpossibletocontact.Theyjustsendyouthreateningandabusiveemailsandphonecalls”.Heremembersonecallwherehewasswornat.“Thatwassoshockingtohaveacustomerservicerepresentativetalktomelikethat”.

Hewasalsosubjecttoharassment.TheycalledextensionnumbersatrandomaroundWarren’sworkplaceandrefusedtotakeanynoticeof writtenrequeststostop.Warrenreceivedaboutfiveemailsadayand‘hundredsof marketingcalls’.

WarrenisnowonaDMPwithStepChangeDebtCharityandispayingoffhisdebt.Despitethishestillreceivesunwantedcontactfromtheloancompaniesonaregularbasis.

Case study Warren

Total unsecured debt (£ million)

STATISTICS YEARBOOK 2013 24

3. Debts

Debt cocktails

Clients with a catalogue debt Proportion with other debt type Avg no. debts Avg debt balanceCatalogue 1.98 £1,937CreditCard 73.8% 2.72 £6,482Overdraft 64.1% 1.37 £1,617Personalloan 52.3% 1.72 £7,829Storecard 17.1% 1.38 £966Homecredit 17.9% 1.73 £1,398Paydayloan 26.8% 2.88 £1,490

Clients with a credit card debt Proportion with other debt type Avg no. debts Avg debt balanceCatalogue 35.1% 1.98 £1,952CreditCard 2.71 £9,047Overdraft 69.6% 1.37 £2,119Personalloan 56.5% 1.60 £9,750Storecard 14.9% 1.37 £1,120Homecredit 8.8% 1.67 £1,443Paydayloan 19.8% 3.10 £1,739

Clients with an overdraft debt Proportion with other debt type Avg no. debts Avg debt balanceCatalogue 33.8% 1.92 £1,789CreditCard 77.2% 2.81 £9,354Overdraft 1.34 £1,958Personalloan 56.5% 1.60 £9,221Storecard 14.4% 1.36 £1,053Homecredit 9.3% 1.64 £1,315Paydayloan 22.6% 3.00 £1,628

Clients with a personal loan debt Proportion with other debt type Avg no. debts Avg debt balanceCatalogue 34.1% 1.94 £1,758CreditCard 77.4% 2.79 £9,079Overdraft 69.8% 1.38 £1,953Personalloan 1.60 £9,219Storecard 14.1% 1.36 £1,094Homecredit 11.6% 1.74 £1,428Paydayloan 20.5% 3.01 £1,622

Clients with storecard debt Proportion with other debt type Avg no. debts Avg debt balanceCatalogue 46.3% 2.03 £2,108CreditCard 84.6% 3.08 £9,575Overdraft 73.6% 1.39 £1,915Personalloan 58.5% 1.62 £9,603Storecard 1.35 £1,075Homecredit 8.8% 1.59 £1,402Paydayloan 19.0% 2.89 £1,581

Clients with a home credit debt Proportion with other debt type Avg no. debts Avg debt balanceCatalogue 57.2% 2.33 £1,938CreditCard 59.2% 2.24 £3,152Overdraft 56.1% 1.41 £1,233Personalloan 56.8% 2.05 £5,751Storecard 10.4% 1.34 £849Homecredit 1.62 £1,356Paydayloan 41.4% 2.97 £1,441Clients with a payday loan debt Proportion with other debt type Avg no. debts Avg debt balanceCatalogue 38.7% 2.01 £1,730CreditCard 60.2% 2.23 £3,695Overdraft 62.0% 1.37 £1,558Personalloan 45.4% 1.74 £5,768Storecard 10.1% 1.31 £818Homecredit 18.7% 1.55 £1,247Paydayloan 3.04 £1,647

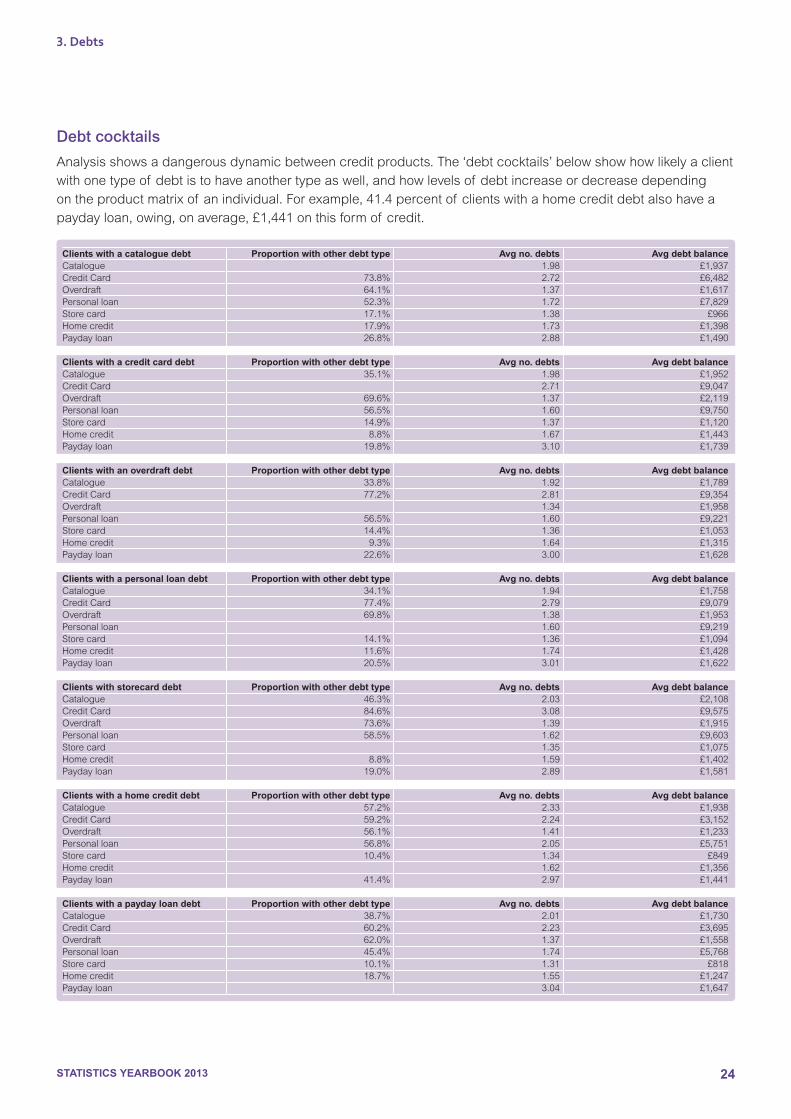

Analysisshowsadangerousdynamicbetweencreditproducts.The‘debtcocktails’belowshowhowlikelyaclientwithonetypeof debtistohaveanothertypeaswell,andhowlevelsof debtincreaseordecreasedependingontheproductmatrixof anindividual.Forexample,41.4percentof clientswithahomecreditdebtalsohaveapaydayloan,owing,onaverage,£1,441onthisformof credit.

STATISTICS YEARBOOK 2013 25

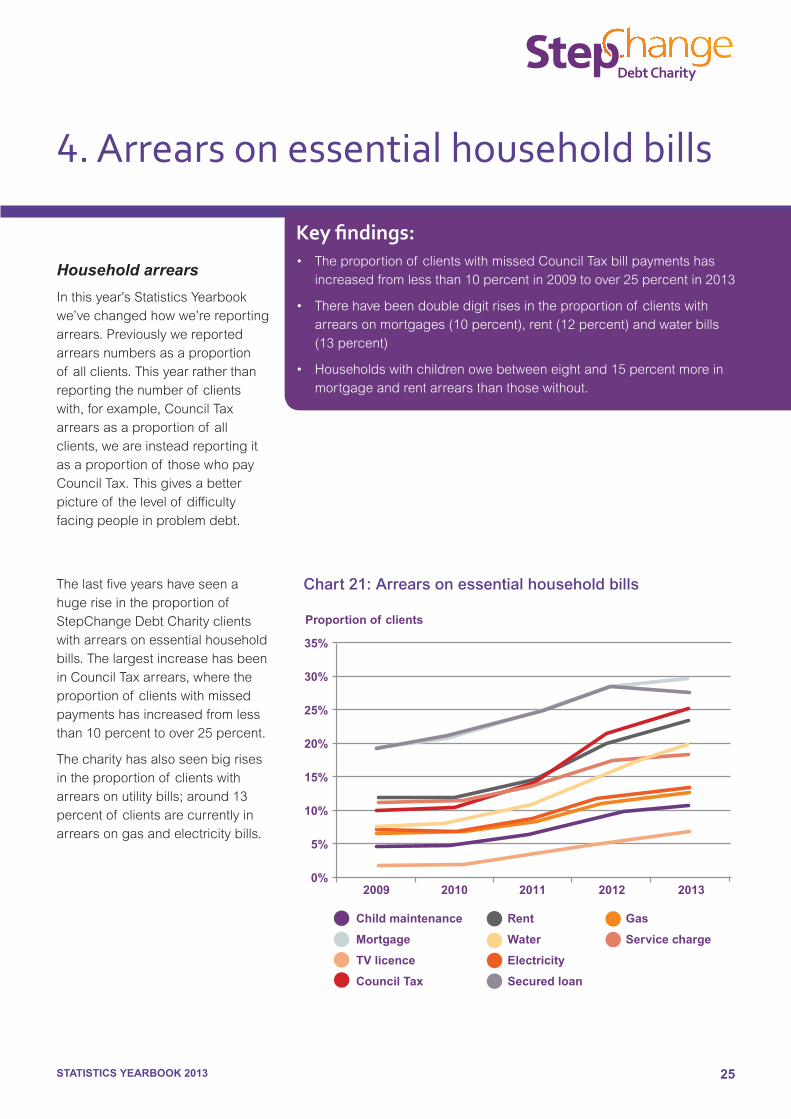

Household arrears

Inthisyear’sStatisticsYearbookwe’vechangedhowwe’rereportingarrears.Previouslywereportedarrearsnumbersasaproportionof allclients.Thisyearratherthanreportingthenumberof clientswith,forexample,CouncilTaxarrearsasaproportionof allclients,weareinsteadreportingitasaproportionof thosewhopayCouncilTax.Thisgivesabetterpictureof thelevelof difficultyfacingpeopleinproblemdebt.

4. Arrears on essential household bills

Key findings:• Theproportionof clientswithmissedCouncilTaxbillpaymentshas

increasedfromlessthan10percentin2009toover25percentin2013

• Therehavebeendoubledigitrisesintheproportionof clientswitharrearsonmortgages(10percent),rent(12percent)andwaterbills(13percent)

• Householdswithchildrenowebetweeneightand15percentmoreinmortgageandrentarrearsthanthosewithout.

Chart 21: Arrears on essential household bills

35%

30%

25%

20%

15%

10%

5%

0%2009 2010 2011 2012 2013

Proportion of clients

Child maintenance

Mortgage

TV licence

Council Tax

Rent

Water

Electricity

Secured loan

Gas

Service charge

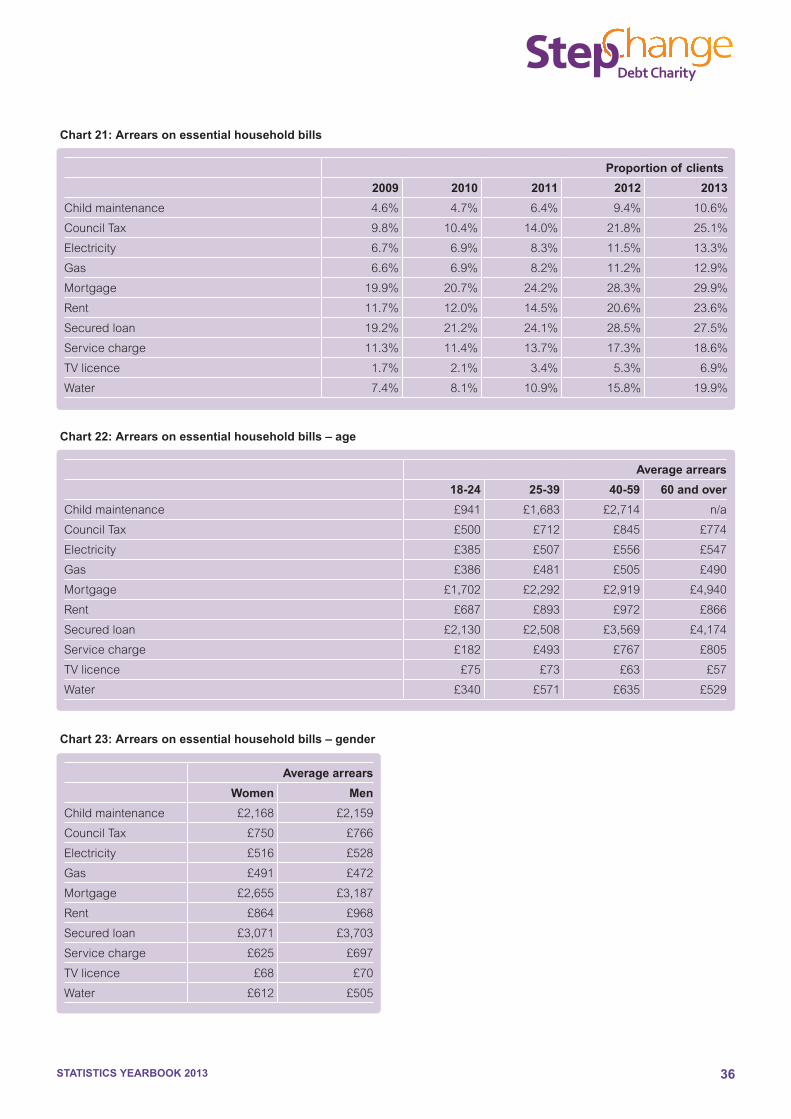

Thelastfiveyearshaveseenahugeriseintheproportionof StepChangeDebtCharityclientswitharrearsonessentialhouseholdbills.ThelargestincreasehasbeeninCouncilTaxarrears,wheretheproportionof clientswithmissedpaymentshasincreasedfromlessthan10percenttoover25percent.

Thecharityhasalsoseenbigrisesintheproportionof clientswitharrearsonutilitybills;around13percentof clientsarecurrentlyinarrearsongasandelectricitybills.

STATISTICS YEARBOOK 2013 26

4. Arrears on household bills

Figure 5: Arrears numbers

STATISTICS YEARBOOK 2013 27

£7,000

£5,000

£4,000

£3,000

£2,000

£1,000

£0

Average arrears

Child m

ainte

nance

Council Ta

xElec

tricit

y

GasMortg

age

Rent

Secure

d loan

Servic

e char

geTV lic

ence

Wat

er

18-24 25-39 40-59 60 and over

£4,000

£3,500

£3,000

£2,500

£2,000

£1,500

£1000

£500

£0

Average arrears

Child m

ainte

nance

Council Ta

xElec

tricit

y

GasMortg

age

Rent

Secure

d loan

Servic

e char

geTV lic

ence

Wat

er

Women Men

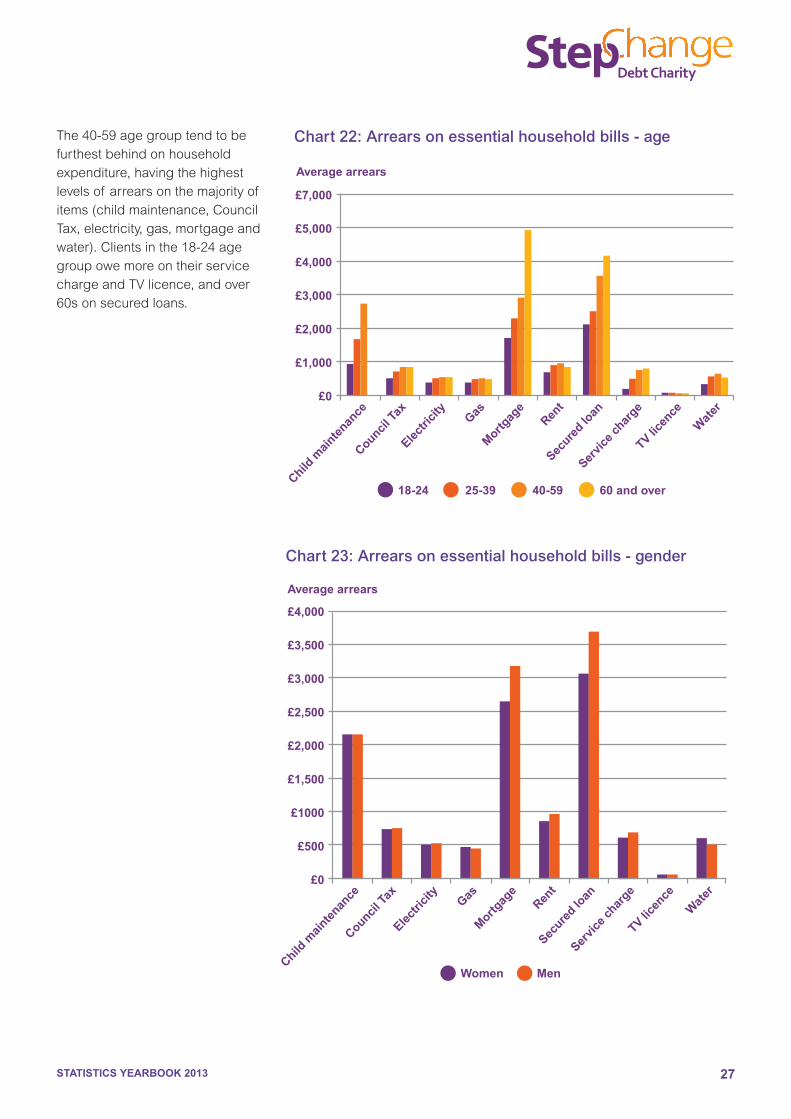

Chart 22: Arrears on essential household bills - age

Chart 23: Arrears on essential household bills - gender

The40-59agegrouptendtobefurthestbehindonhouseholdexpenditure,havingthehighestlevelsof arrearsonthemajorityof items(childmaintenance,CouncilTax,electricity,gas,mortgageandwater).Clientsinthe18-24agegroupowemoreontheirservicechargeandTVlicence,andover60sonsecuredloans.

STATISTICS YEARBOOK 2013 28

4. Arrears on household bills

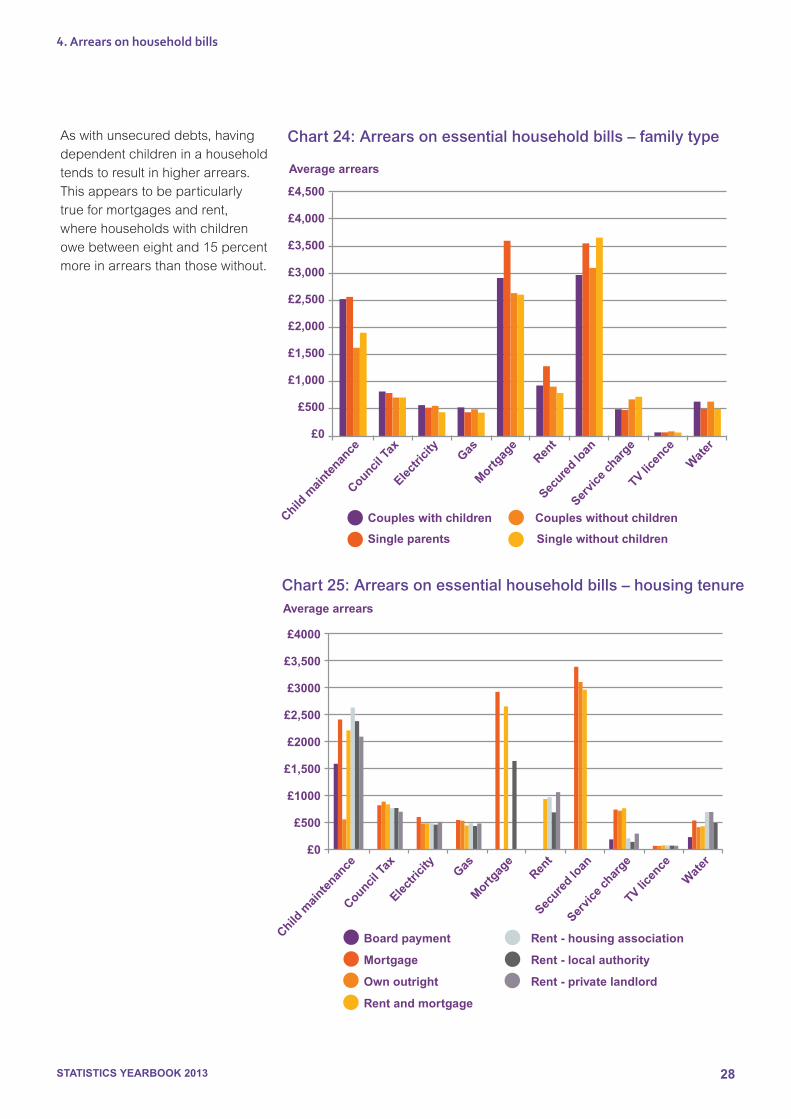

Aswithunsecureddebts,havingdependentchildreninahouseholdtendstoresultinhigherarrears.Thisappearstobeparticularlytrueformortgagesandrent,wherehouseholdswithchildrenowebetweeneightand15percentmoreinarrearsthanthosewithout.

£4,500

£4,000

£3,500

£3,000

£2,500

£2,000

£1,500

£1,000

£500

£0

Average arrears

Child m

ainte

nance

Council Ta

xElec

tricit

y

GasMortg

age

Rent

Secure

d loan

Servic

e char

geTV lic

ence

Wat

er

Couples with children Couples without children

Single parents Single without children

Chart 24: Arrears on essential household bills – family type

Chart 25: Arrears on essential household bills – housing tenure

£4000

£3,500

£3000

£2,500

£2000

£1,500

£1000

£500

£0

Average arrears

Child m

ainte

nance

Council Ta

xElec

tricit

y

GasMortg

age

Rent

Secure

d loan

Servic

e char

geTV lic

ence

Wat

er

Board payment

Mortgage

Own outright

Rent and mortgage

Rent - housing association

Rent - local authority

Rent - private landlord

STATISTICS YEARBOOK 2013 29

5. Social policy

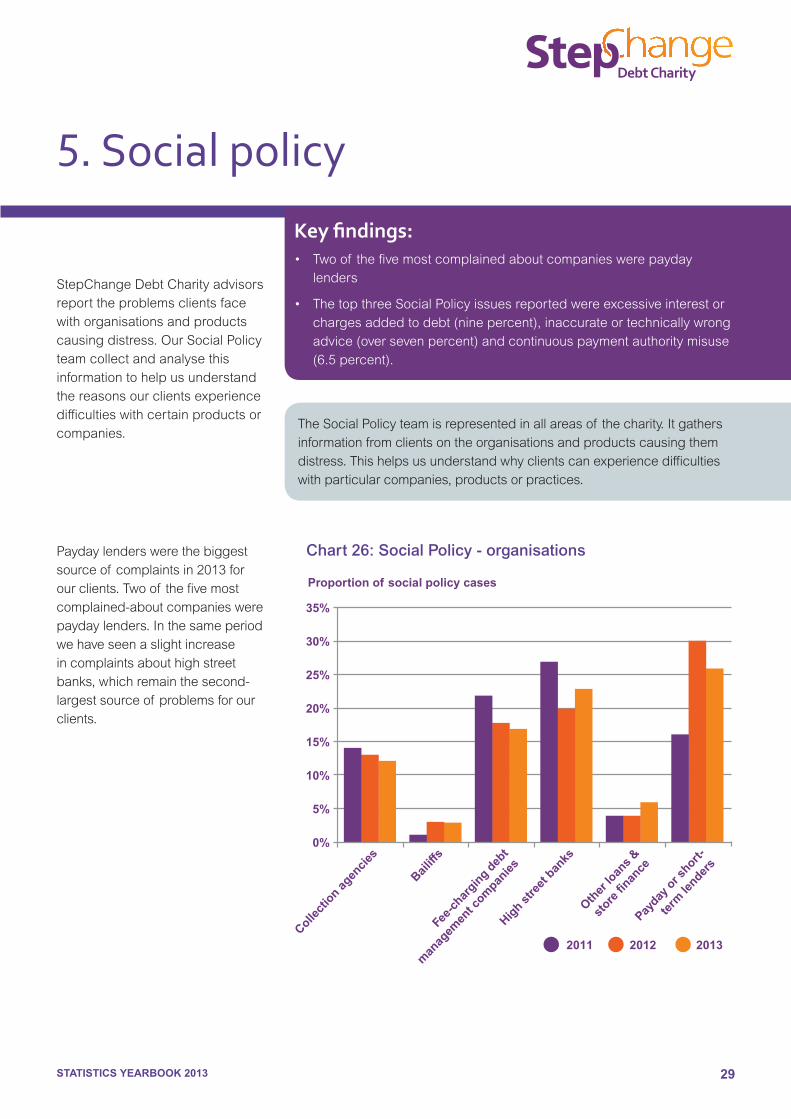

StepChangeDebtCharityadvisorsreporttheproblemsclientsfacewithorganisationsandproductscausingdistress.OurSocialPolicyteamcollectandanalysethisinformationtohelpusunderstandthereasonsourclientsexperiencedifficultieswithcertainproductsorcompanies.

Paydaylenderswerethebiggestsourceof complaintsin2013forourclients.Twoof thefivemostcomplained-aboutcompanieswerepaydaylenders.Inthesameperiodwehaveseenaslightincreaseincomplaintsabouthighstreetbanks,whichremainthesecond-largestsourceof problemsforourclients.

35%

30%

25%

20%

15%

10%

5%

0%

Collect

ion ag

encie

s

Bailiff

sFe

e-ch

argin

g deb

t

man

agem

ent c

ompan

iesHig

h stre

et b

anks

Other

loan

s &

store

finan

cePay

day o

r short-

term

lender

s

2011 2012 2013

Proportion of social policy cases

Key findings:• Twoof thefivemostcomplainedaboutcompanieswerepayday

lenders

• ThetopthreeSocialPolicyissuesreportedwereexcessiveinterestorchargesaddedtodebt(ninepercent),inaccurateortechnicallywrongadvice(oversevenpercent)andcontinuouspaymentauthoritymisuse(6.5percent).

Chart 26: Social Policy - organisations

TheSocialPolicyteamisrepresentedinallareasof thecharity.Itgathersinformationfromclientsontheorganisationsandproductscausingthemdistress.Thishelpsusunderstandwhyclientscanexperiencedifficultieswithparticularcompanies,productsorpractices.

STATISTICS YEARBOOK 2013 30

5. Social policy

10%

9%

8%

7%

6%

5%

4%

3%

2%

1%

0%

Substan

dard

cust

omer

serv

iceMisl

eadin

g advic

eContin

uous pay

men

t

auth

ority m

isuse

Inac

cura

te o

r tec

hnically

wrong ad

vice

Exces

sive i

ntere

st o

r

char

ges ad

ded to

deb

t

Proportion of social policy cases

Chart 27: Social Policy - issues

Dave’sdebtproblemsstartedwiththebreakdownof hismarriagebackin2007.Hehadtoleavethemaritalhomewhilstcontinuingtopayforitandrentatthesametime.Hefinancedalotof thiswithcreditcards.Hetriedtosellthemaritalhomebutputitonthemarketjustasthehousingmarketcollapsed.Heeventuallysolditfora£16,000loss.Ontopof thishehadtochangejobsduetoathreatof redundancyandendedupearningalotlessthanhewasusedto.

“IwaspayingoutmuchmorethanIwasearninguntilitgottoapointwhereIcouldn’tmakepaymentsanymore,whichiswhenIcontactedStepChangeandIwasputontoaDMP.”

Case study Dave

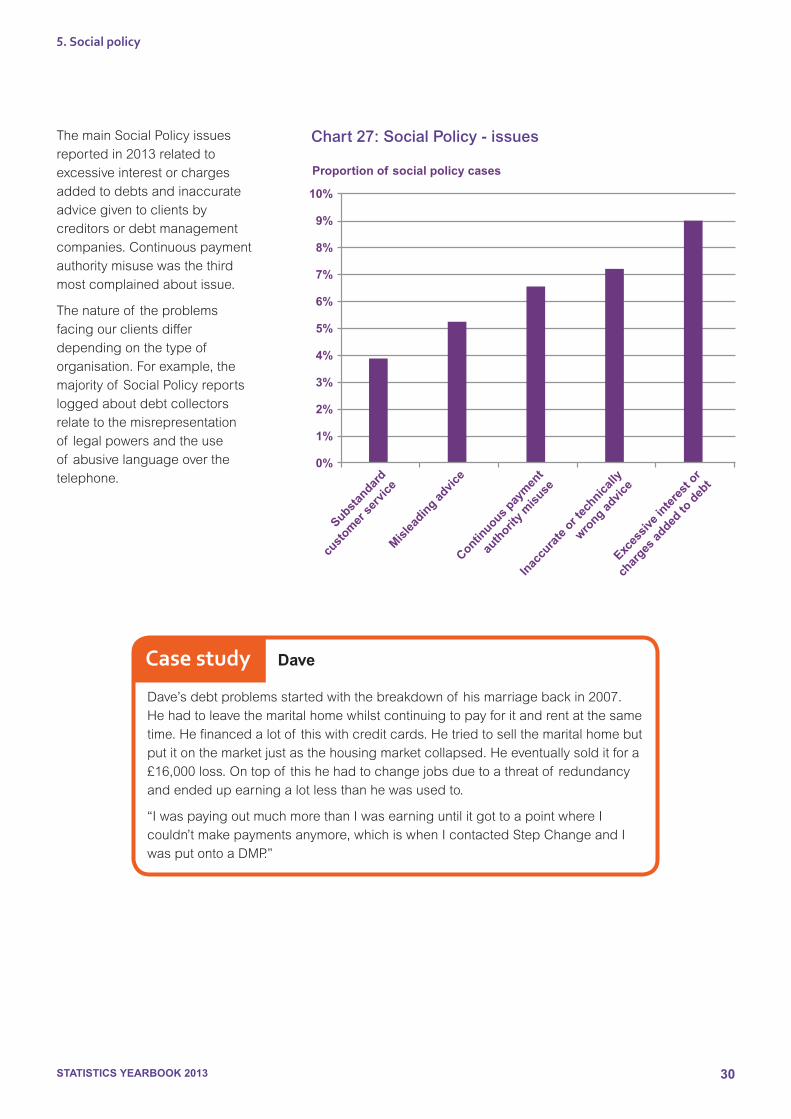

ThemainSocialPolicyissuesreportedin2013relatedtoexcessiveinterestorchargesaddedtodebtsandinaccurateadvicegiventoclientsbycreditorsordebtmanagementcompanies.Continuouspaymentauthoritymisusewasthethirdmostcomplainedaboutissue.

Thenatureof theproblemsfacingourclientsdifferdependingonthetypeof organisation.Forexample,themajorityof SocialPolicyreportsloggedaboutdebtcollectorsrelatetothemisrepresentationof legalpowersandtheuseof abusivelanguageoverthetelephone.

STATISTICS YEARBOOK 2013 31

Figure 6: Social Policy/biggest concerns

STATISTICS YEARBOOK 2013 32

Appendix

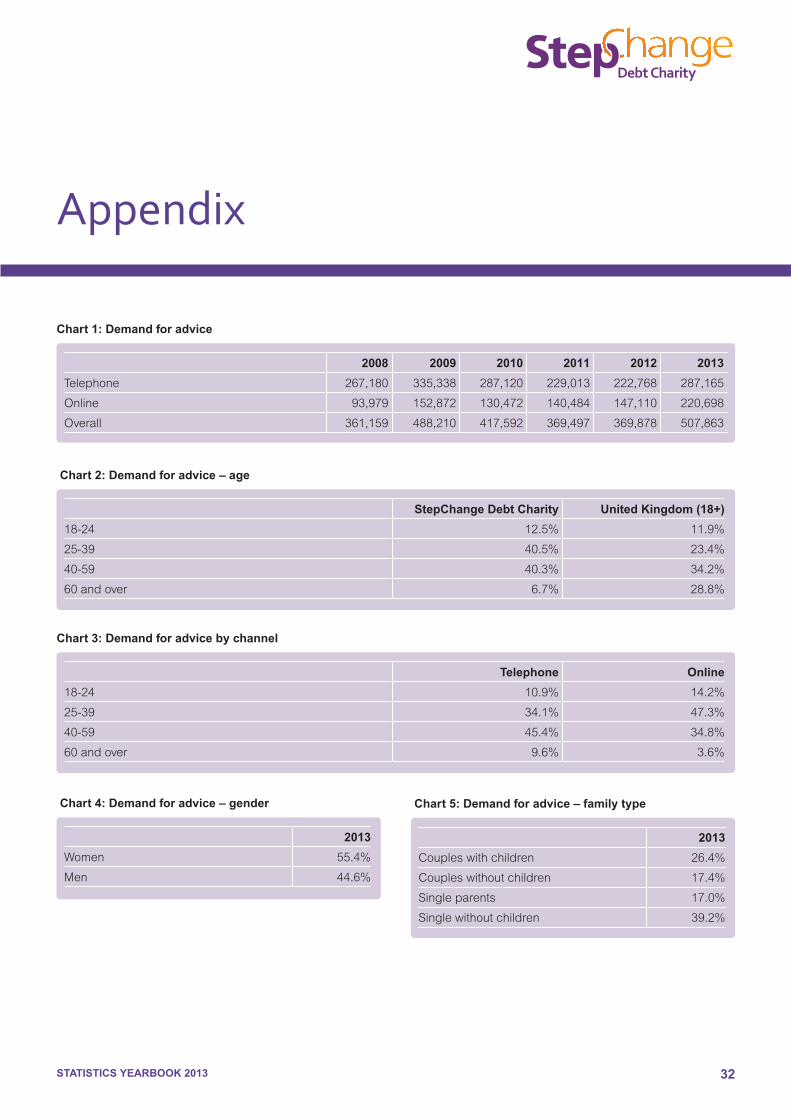

2008 2009 2010 2011 2012 2013

Telephone 267,180 335,338 287,120 229,013 222,768 287,165

Online 93,979 152,872 130,472 140,484 147,110 220,698

Overall 361,159 488,210 417,592 369,497 369,878 507,863

Chart 1: Demand for advice

StepChange Debt Charity United Kingdom (18+)

18-24 12.5% 11.9%

25-39 40.5% 23.4%

40-59 40.3% 34.2%

60andover 6.7% 28.8%

Chart 2: Demand for advice – age

Telephone Online

18-24 10.9% 14.2%

25-39 34.1% 47.3%

40-59 45.4% 34.8%

60andover 9.6% 3.6%

2013

Women 55.4%

Men 44.6%

Chart 4: Demand for advice – gender

2013

Coupleswithchildren 26.4%

Coupleswithoutchildren 17.4%

Singleparents 17.0%

Singlewithoutchildren 39.2%

Chart 5: Demand for advice – family type

Chart 3: Demand for advice by channel

STATISTICS YEARBOOK 2013 33

Appendix

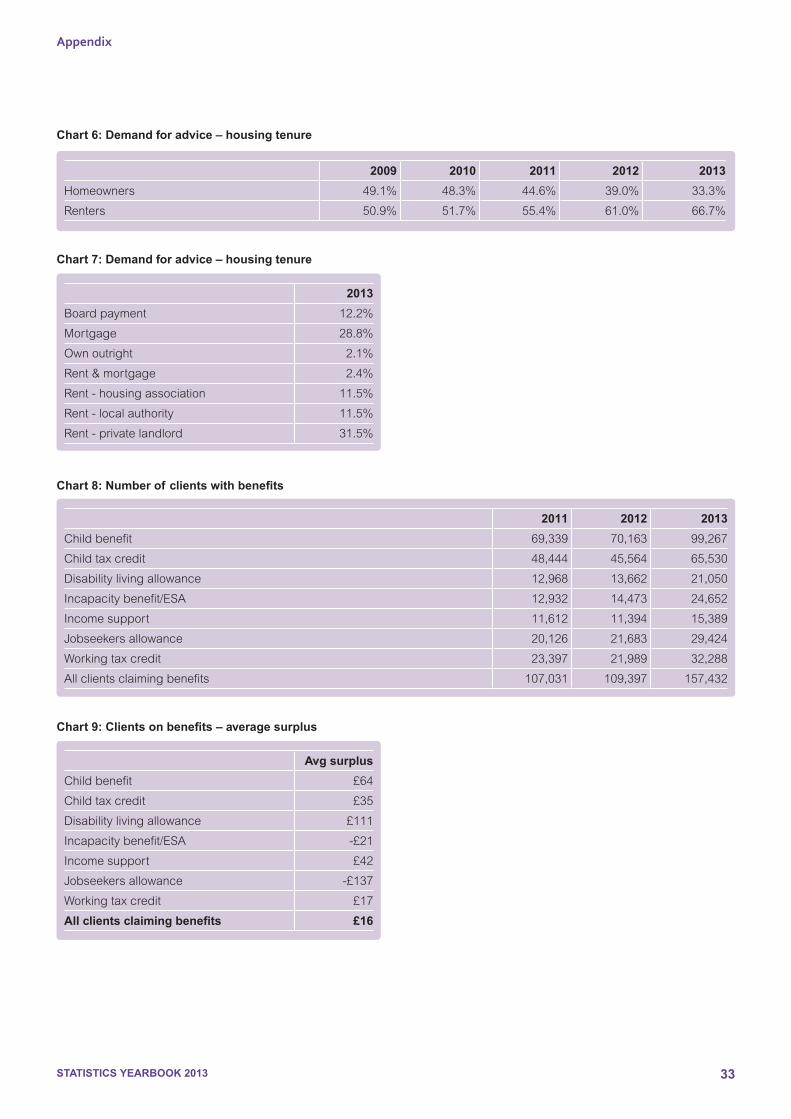

2009 2010 2011 2012 2013

Homeowners 49.1% 48.3% 44.6% 39.0% 33.3%

Renters 50.9% 51.7% 55.4% 61.0% 66.7%

2013

Boardpayment 12.2%

Mortgage 28.8%

Ownoutright 2.1%

Rent&mortgage 2.4%

Rent-housingassociation 11.5%

Rent-localauthority 11.5%

Rent-privatelandlord 31.5%

Chart 6: Demand for advice – housing tenure

2011 2012 2013

Childbenefit 69,339 70,163 99,267

Childtaxcredit 48,444 45,564 65,530

Disabilitylivingallowance 12,968 13,662 21,050

Incapacitybenefit/ESA 12,932 14,473 24,652

Incomesupport 11,612 11,394 15,389

Jobseekersallowance 20,126 21,683 29,424

Workingtaxcredit 23,397 21,989 32,288

Allclientsclaimingbenefits 107,031 109,397 157,432

Avg surplus

Childbenefit £64

Childtaxcredit £35

Disabilitylivingallowance £111

Incapacitybenefit/ESA -£21

Incomesupport £42

Jobseekersallowance -£137

Workingtaxcredit £17

All clients claiming benefits £16

Chart 8: Number of clients with benefits

Chart 7: Demand for advice – housing tenure

Chart 9: Clients on benefits – average surplus

STATISTICS YEARBOOK 2013 34

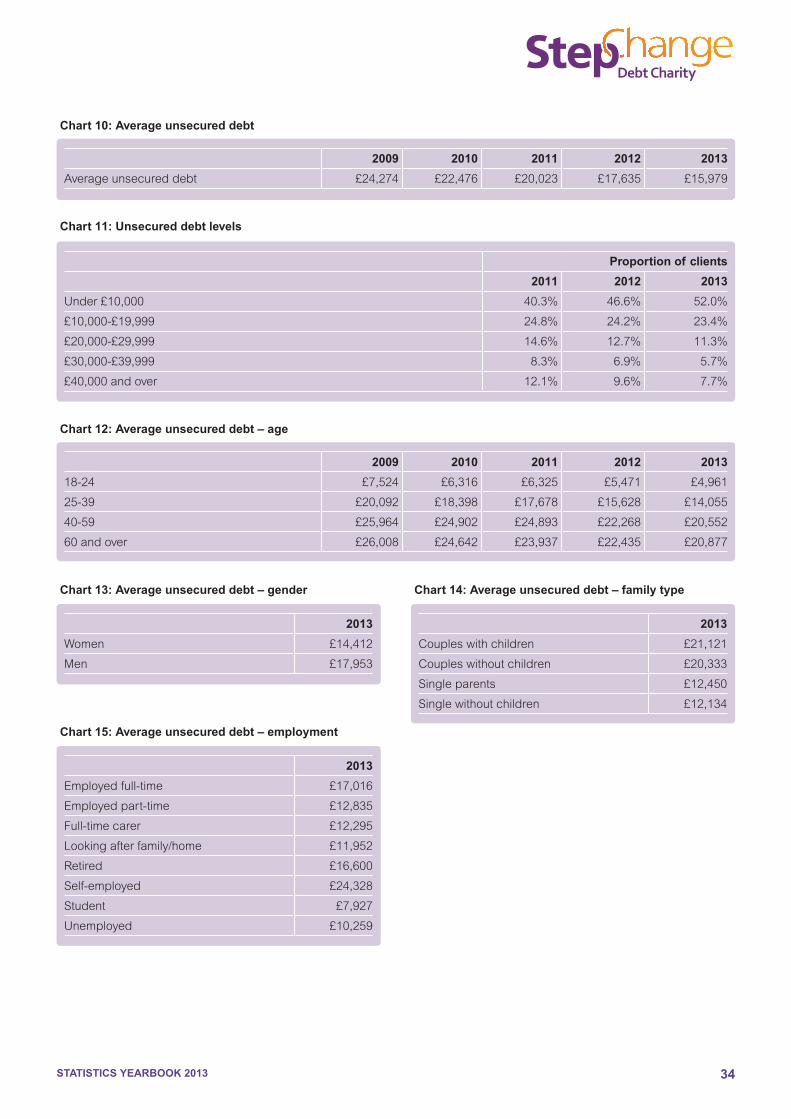

2009 2010 2011 2012 2013

Averageunsecureddebt £24,274 £22,476 £20,023 £17,635 £15,979

Chart 10: Average unsecured debt

Proportion of clients

2011 2012 2013

Under£10,000 40.3% 46.6% 52.0%

£10,000-£19,999 24.8% 24.2% 23.4%

£20,000-£29,999 14.6% 12.7% 11.3%

£30,000-£39,999 8.3% 6.9% 5.7%

£40,000andover 12.1% 9.6% 7.7%

Chart 11: Unsecured debt levels

2009 2010 2011 2012 2013

18-24 £7,524 £6,316 £6,325 £5,471 £4,961

25-39 £20,092 £18,398 £17,678 £15,628 £14,055

40-59 £25,964 £24,902 £24,893 £22,268 £20,552

60andover £26,008 £24,642 £23,937 £22,435 £20,877

Chart 12: Average unsecured debt – age

2013

Women £14,412

Men £17,953

Chart 13: Average unsecured debt – gender

2013

Coupleswithchildren £21,121

Coupleswithoutchildren £20,333

Singleparents £12,450

Singlewithoutchildren £12,134

Chart 14: Average unsecured debt – family type

2013

Employedfull-time £17,016

Employedpart-time £12,835

Full-timecarer £12,295

Lookingafterfamily/home £11,952

Retired £16,600

Self-employed £24,328

Student £7,927

Unemployed £10,259

Chart 15: Average unsecured debt – employment

STATISTICS YEARBOOK 2013 35

Appendix

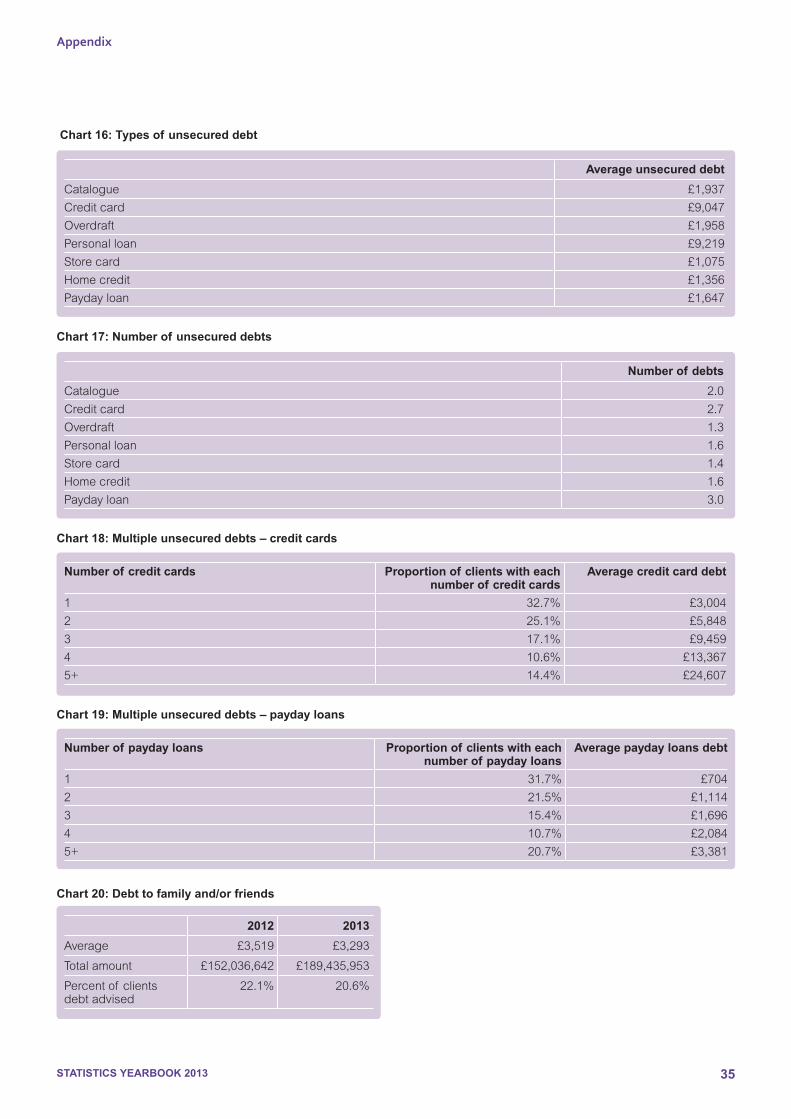

Number of credit cards Proportion of clients with each number of credit cards

Average credit card debt

1 32.7% £3,0042 25.1% £5,8483 17.1% £9,4594 10.6% £13,3675+ 14.4% £24,607

Chart 16: Types of unsecured debt

Average unsecured debt

Catalogue £1,937Creditcard £9,047Overdraft £1,958Personalloan £9,219Storecard £1,075Homecredit £1,356Paydayloan £1,647

Number of payday loans Proportion of clients with each number of payday loans

Average payday loans debt

1 31.7% £7042 21.5% £1,1143 15.4% £1,6964 10.7% £2,0845+ 20.7% £3,381

Chart 18: Multiple unsecured debts – credit cards

Chart 19: Multiple unsecured debts – payday loans

2012 2013

Average £3,519 £3,293

Totalamount £152,036,642 £189,435,953

Percentof clientsdebtadvised

22.1% 20.6%

Chart 20: Debt to family and/or friends

Chart 17: Number of unsecured debts

Number of debts

Catalogue 2.0Creditcard 2.7Overdraft 1.3Personalloan 1.6Storecard 1.4Homecredit 1.6Paydayloan 3.0

STATISTICS YEARBOOK 2013 36

Proportion of clients

2009 2010 2011 2012 2013

Childmaintenance 4.6% 4.7% 6.4% 9.4% 10.6%

CouncilTax 9.8% 10.4% 14.0% 21.8% 25.1%

Electricity 6.7% 6.9% 8.3% 11.5% 13.3%

Gas 6.6% 6.9% 8.2% 11.2% 12.9%

Mortgage 19.9% 20.7% 24.2% 28.3% 29.9%

Rent 11.7% 12.0% 14.5% 20.6% 23.6%

Securedloan 19.2% 21.2% 24.1% 28.5% 27.5%

Servicecharge 11.3% 11.4% 13.7% 17.3% 18.6%

TVlicence 1.7% 2.1% 3.4% 5.3% 6.9%

Water 7.4% 8.1% 10.9% 15.8% 19.9%

Chart 21: Arrears on essential household bills

Average arrears

18-24 25-39 40-59 60 and over

Childmaintenance £941 £1,683 £2,714 n/a

CouncilTax £500 £712 £845 £774

Electricity £385 £507 £556 £547

Gas £386 £481 £505 £490

Mortgage £1,702 £2,292 £2,919 £4,940

Rent £687 £893 £972 £866

Securedloan £2,130 £2,508 £3,569 £4,174

Servicecharge £182 £493 £767 £805

TVlicence £75 £73 £63 £57

Water £340 £571 £635 £529

Chart 22: Arrears on essential household bills – age

Average arrears

Women Men

Childmaintenance £2,168 £2,159

CouncilTax £750 £766

Electricity £516 £528

Gas £491 £472

Mortgage £2,655 £3,187

Rent £864 £968

Securedloan £3,071 £3,703

Servicecharge £625 £697

TVlicence £68 £70

Water £612 £505

Chart 23: Arrears on essential household bills – gender

37STATISTICS YEARBOOK 2013

Appendix

Average arrears

Couples with children

Couples without children

Single parents Single without children

Childmaintenance £2,524 £2,569 £1,621 £1,912

CouncilTax £822 £800 £712 £711

Electricity £571 £518 £558 £447

Gas £523 £445 £519 £431

Mortgage £2,908 £3,591 £2,633 £2,598

Rent £933 £1,279 £911 £780

Securedloan £2,957 £3,530 £3,097 £3986

Servicecharge £498 £487 £682 £738

TVlicence £69 £59 £73 £69

Water £627 £510 £633 £508

Chart 24: Arrears on essential household bills – family type

Average arrears

Board payment

Mortgage Own outright

Rent & mortgage

Rent - housing

association

Rent - local authority

Rent - private

landlord

Childmaintenance £1,584 £2,412 £550 £2,213 £2,632 £2,379 £2,097

CouncilTax £0 £819 £882 £830 £764 £763 £695

Electricity £0 £596 £474 £481 £485 £451 £503

Gas £0 £534 £523 £455 £470 £415 £478

Mortgage £0 £2,928 £0 £2,666 £0 £1,635 N/A

Rent £0 £0 £0 £920 £959 £678 £1,061

Securedloan £0 £3,390 £3,107 £2,967 £0 £0 £0

Servicecharge £174 £731 £724 £763 £195 £134 £289

TVlicence £0 £59 £61 £67 £75 £72 £68

Water £220 £517 £403 £410 £700 £687 £448

Chart 25: Arrears on essential household bills – housing tenure

Proportion of Social Policy cases

2011 2012 2013

Collectionagencies 14% 13% 12%

Bailiffs 1% 3% 3%

Fee-chargingdebtmanagementcompanies

22% 18% 17%

Highstreetbanks 27% 20% 23%

Otherloans&storefinance 4% 4% 6%

Paydayorshort-termlenders

16% 30% 26%

Chart 26: Social Policy – organisations

Proportion of Social Policy issues

2013

Substandardcustomerservice 4%

Misleadingadvice 5%

Continuouspaymentauthoritymisuse 7%

Inaccurateortechnicallywrongadvice 7%

Excessiveinterestorchargesaddedtodebt 9%

Chart 27: Social Policy - issues

Proportion of clients 2011 2012 2013

Unemployment/redundancy 24.9% 24.9% 23.4%ReducedIncome 23.2% 18.9% 16.4%Lackof budgeting 10.1% 12.3% 13.5%Injury/Illness 9.5% 10.3% 11.3%Separation/divorce 9.7% 9.9% 10.0%Usedcreditforlivingexpenses 3.8% 4.7% 5.4%Increasedpriorityexpenditure 3.1% 3.3% 3.5%IrregularIncome 4.0% 3.8% 3.1%Reducedbenefits 1.0% 1.6% 2.7%Failedbusiness 2.1% 2.1% 2.1%

Figure 1: Reasons for debt

Proportion of clients 2013

Employedfulltime 31.3%Employedparttime 17.0%Fulltimecarer 1.4%

Lookingafterthefamily/home 1.8%Retired 6.5%Self employed 8.6%Student 1.6%Unemployed 31.7%

Figure 2: Employment

Average unsecured debt 2011 2012 2013

Peoplewithamortgage £28,491 £26,304 £24,738Peoplewhoownoutright £20,091 £19,534 £18,536Peoplerentingfromhousingassociation £14,463 £10,999 £11,085Peoplerentingfromlocalauthority £13,075 £10,422 £10,067Peoplerentingfromprivatelandlord £17,275 £14,534 £13,732

Figure 3: Average unsecured debt – housing tenure

Proportion of clients 2013

Catalogue 11%Creditcard 31%Overdraft 14%Personalloan 13%Storecard 3%Homecredit 3%Paydayloan 12%Other 14%

Figure 4: Size of problem by number of debts seen

38STATISTICS YEARBOOK 2013

STATISTICS YEARBOOK 2013 39

2009 2010 2011 2012 2013

Number in arrears

Avg arrears amount

Number in arrears

Avg arrears amount

Number in arrears

Avg arrears amount

Number in arrears

Avg arrears amount

Number in arrears

Avg arrears amount

CouncilTax 13,100 £633 13,353 £675 16,956 £717 25,500 £782 45,561 £756

Electricity 10,939 £408 11,081 £452 12,657 £440 17,443 £488 28,925 £521

Gas 8,368 £361 8,457 £403 9,461 £408 12,356 £455 20,270 £484

Mortgage 17,543 £2,702 17,391 £3,049 18,110 £3,086 18,612 £3,338 24,095 £2,911

Rent 8,246 £723 8,517 £736 10,858 £769 16,942 £828 31,449 £901

Securedloan 5,594 £1,589 5,140 £2,428 4,894 £2,572 4,686 £2,969 5,492 £3,364

Water 10,168 £359 11,014 £404 14,186 £545 20,288 £786 36,410 £574

Figure 5: Arrears numbers

Paydaylenders 1 Excessinterestorchargesaddedtodebt

2 Continuouspaymentauthoritymisuse

3 Irresponsiblelending

4 Intimidating,abusive,orinappropriatelanguageonphonecalls

5 Inaccuracyortechnicallywrongadvice

Highstreetbanks 1 Continuouspaymentauthoritymisuse

2 Inaccuracyortechnicallywrongadvice

3 Refusaltoopenbasicbankaccount

4 Substandardcustomerservice

5 Excessinterestorchargesaddedtodebt

Fee-chargingdebtmanagementcompanies 1 ProvidingmisleadinginformationaboutStepChangeDebtCharity

2 Inaccuracyortechnicallywrongadvice

3 Withholdingornotdisbursingclientpayments

4 Misleadingordeceptiveadvice

5 Excessinterestorchargesforservicesprovided

Debtcollectors 1 Misrepresentinglegalpowers

2 Intimidating,abusive,orinappropriatelanguageonphonecalls

3 Excessinterestorchargesaddedtodebt

4 Excessivephonecallsorcallingatinappropriatetimes

5 Statutorydemandusedinappropriately

Figure 6: Social Policy – biggest concerns

Appendix

© 2014 Foundation for Credit Counselling

Registered Office: Wade House, Merrion Centre, Leeds LS2 8NG

Registered in England No 2757055

Registered Charity No 1016630

For more information about this report:Call: 0207 3914598 Monday to Friday 9am to 6pmEmail: [email protected]: www.stepchange.org

Write to StepChange Debt Charity London Office:6th Floor, Lynton House,7-12 Tavistock SquareLondon WC1H 9LT

For help and advice with problem debts:Call: 0800 138 1111 Monday to Friday 8am to 8pm and Saturday 9am to 4pm

Online: www.stepchange.org

![Jambalaya [yearbook] 1920 plus Medical yearbook 1920](https://img.pdfslide.us/doc/110x75/586cd4c31a28ab0b6b8bf18e/jambalaya-yearbook-1920-plus-medical-yearbook-1920.jpg)